Embed Size (px)

Citation preview

Investment Patterns in the Healthcare Industry - An Analysis

Janani Sankaran, Industry Analyst

Business and Financial Services, Healthcare

October 13, 2009

N68F-F1 2

Detailed Table of Contents

Significant Developments in the Healthcare Industry Significant Developments in the Healthcare Industry

Significant Developments in the Healthcare Industry

Equity Markets- An OverviewEquity Markets- An Overview

Stock Markets- An Overview

Analysis of Equity Investments by Time Period

Analysis of Equity Investments by Type of Equity

Analysis of Equity Investments by Deal Volume

Investment Analysis- IntroductionInvestment Analysis- Introduction

Number of Deals Analyzed

Analysis of Various Investments by Time

Analysis of Various Investments by Proceeds

Analysis of Various Investments by Type of Funding

N68F-F1 3

Loan Markets- An OverviewLoan Markets- An Overview

Contact Information and About Frost & SullivanContact Information and About Frost & Sullivan

Analysis of Loans by Time

Analysis of Loans by Pricing

Analysis of Loans by Proceeds

Analysis of Loans by extent of Leverage

Concluding ThoughtsConcluding Thoughts

Debt Markets- An OverviewDebt Markets- An Overview

Analysis of Debt Investments by Time

Analysis of Debt Investments by Geographies

Analysis of Debt Investments by Volume and Proceeds

Detailed Table of Contents

N68F-F1 4

Focus Points

Significant Developments in the Healthcare Industry Significant Developments in the Healthcare Industry

Equity Markets- An OverviewEquity Markets- An Overview

Investment Analysis- IntroductionInvestment Analysis- Introduction

Number of Deals Analyzed

Analysis of Various Investments by Time

Analysis of Various Investments by Proceeds

Analysis of Various Investments by Type of Funding

Stock Markets- An Overview

Debt Markets- An OverviewDebt Markets- An Overview Analysis of Debt Investments by Time

Loan Markets- An OverviewLoan Markets- An Overview Analysis of Loans by Time

Conclusion Conclusion

N68F-F1 5

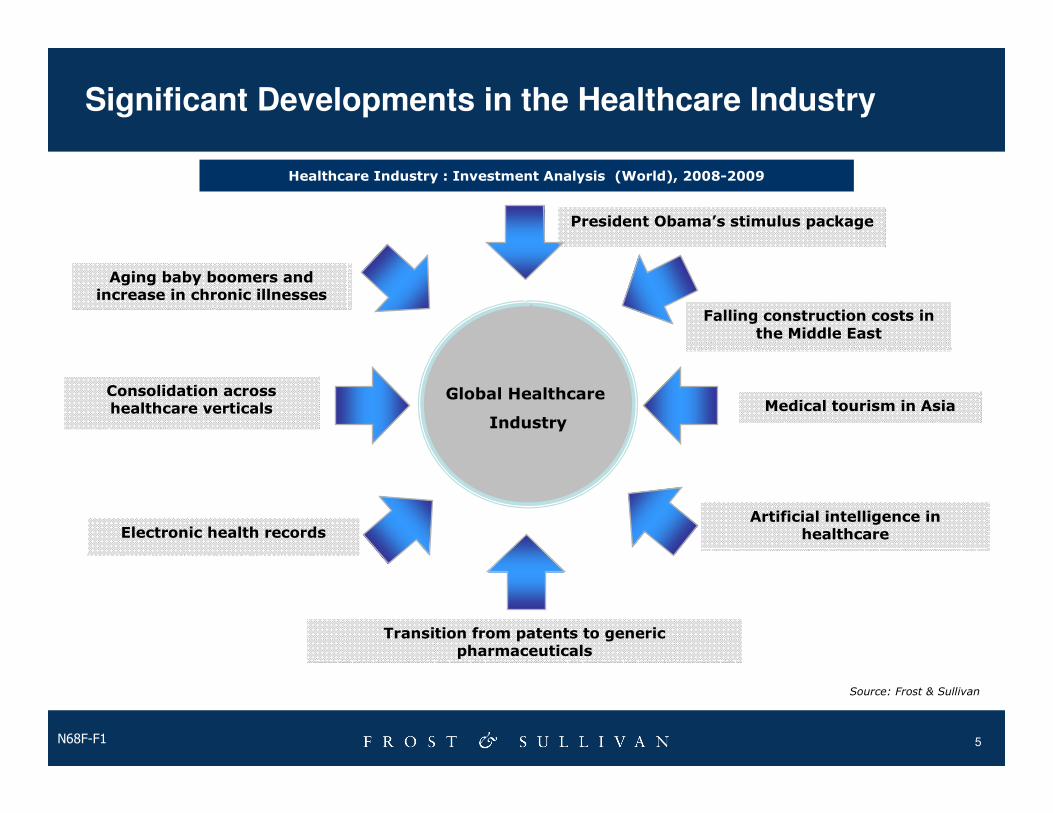

Significant Developments in the Healthcare Industry

Healthcare Industry : Investment Analysis (World), 2008-2009

Global Healthcare

Industry

Aging baby boomers and increase in chronic illnesses

President Obama’s stimulus package

Falling construction costs in the Middle East

Medical tourism in Asia

Transition from patents to generic pharmaceuticals

Artificial intelligence in healthcareElectronic health records

Consolidation across healthcare verticals

Source: Frost & Sullivan

N68F-F1 6

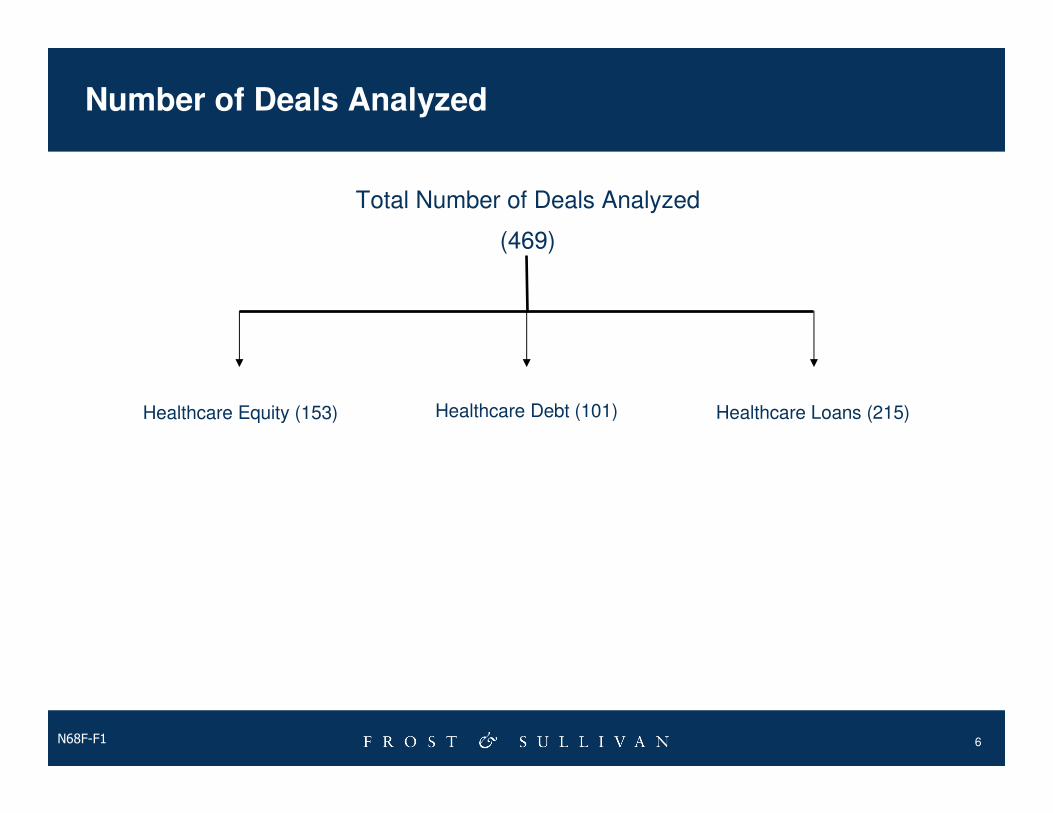

Number of Deals Analyzed

Total Number of Deals Analyzed

(469)

Healthcare Equity (153) Healthcare Loans (215)Healthcare Debt (101)

N68F-F1 7Note: All figures are rounded; the base year is 2008.

Source: Frost & Sullivan

Healthcare Investments - Analysis by Time (World) 2008-2009

Healthcare Industry : Investment Analysis by time and by Volume (World), 2008-2009

Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009Biotechnology 14 10 1 12 8Healthcare equipment 22 34 10 25 17Other Healthcare Providers 12 24 21 16 8Hospitals 17 18 17 8 7Pharmaceuticals 30 37 19 46 36Total Deals 95 123 68 107 76

SegmentNumber of Deals over quarters (x)

8.1 11.2

27.6

14.7

23.4

19.5

30.9

15.0

14.625.0

7.5

30.1 27.943.0

1.5

10.514.7

22.423.2

10.512.6

9.2

17.9

47.4

31.6

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009

Quarter

Dea

l V

olu

me

(%

)

Biotechnology Healthcare Equipment Other Healthcare Providers Hospitals Pharmaceuticals

N68F-F1 8

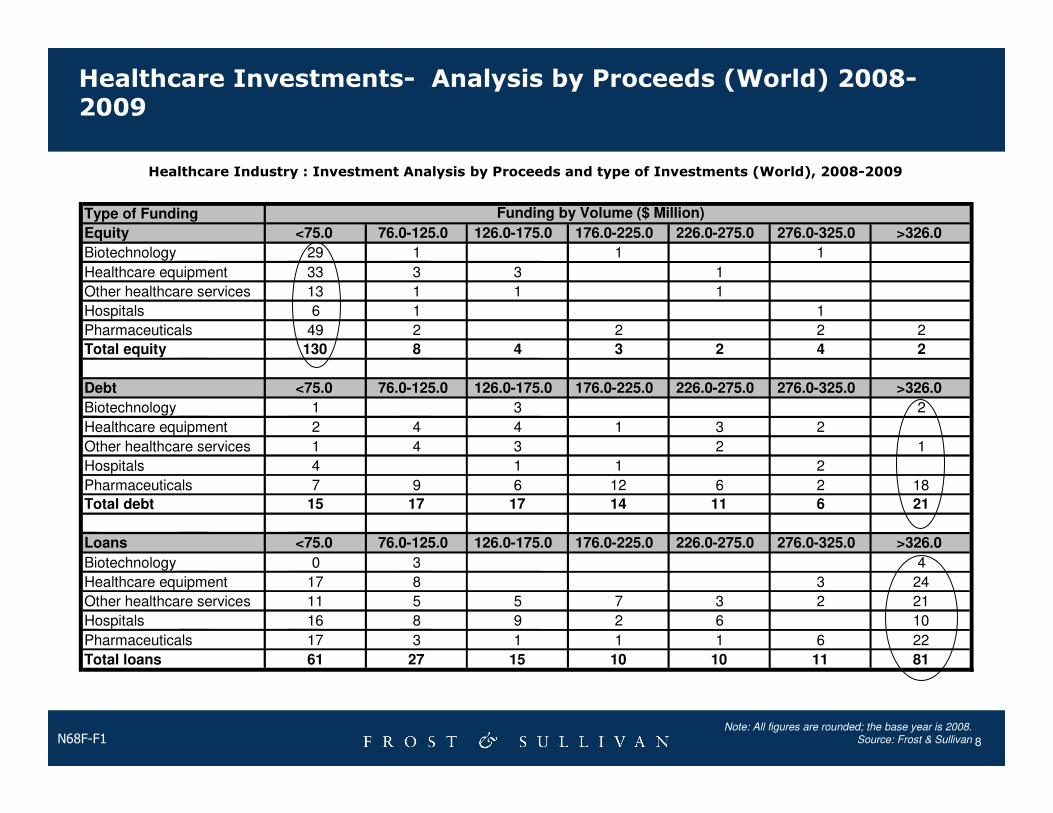

Healthcare Investments- Analysis by Proceeds (World) 2008-2009

Type of Funding

Equity <75.0 76.0-125.0 126.0-175.0 176.0-225.0 226.0-275.0 276.0-325.0 >326.0

Biotechnology 29 1 1 1

Healthcare equipment 33 3 3 1

Other healthcare services 13 1 1 1

Hospitals 6 1 1

Pharmaceuticals 49 2 2 2 2

Total equity 130 8 4 3 2 4 2

Debt <75.0 76.0-125.0 126.0-175.0 176.0-225.0 226.0-275.0 276.0-325.0 >326.0

Biotechnology 1 3 2

Healthcare equipment 2 4 4 1 3 2

Other healthcare services 1 4 3 2 1

Hospitals 4 1 1 2

Pharmaceuticals 7 9 6 12 6 2 18

Total debt 15 17 17 14 11 6 21

Loans <75.0 76.0-125.0 126.0-175.0 176.0-225.0 226.0-275.0 276.0-325.0 >326.0

Biotechnology 0 3 4

Healthcare equipment 17 8 3 24

Other healthcare services 11 5 5 7 3 2 21

Hospitals 16 8 9 2 6 10

Pharmaceuticals 17 3 1 1 1 6 22

Total loans 61 27 15 10 10 11 81

Funding by Volume ($ Million)

Note: All figures are rounded; the base year is 2008. Source: Frost & Sullivan

Healthcare Industry : Investment Analysis by Proceeds and type of Investments (World), 2008-2009

N68F-F1 9

0

10

20

30

40

50

60

70

Biotechnology Healthcare

equipment

Other healthcare

services

Hospitals Pharmaceuticals

Segments

Vo

lum

e (

x)

0.0

10,000.0

20,000.0

30,000.0

40,000.0

50,000.0

60,000.0

Valu

e (

$ M

illio

n)

Equity volume Debt volume Loans volumeEquity amount Debt amount Loans amount

15%

26%

23%

3%

13%6%

14%

22%

44%

34%

Biotechnology Healthcare equipment Other healthcare servicesHospitals Pharmaceuticals

Deals by Volume

Deals by Value

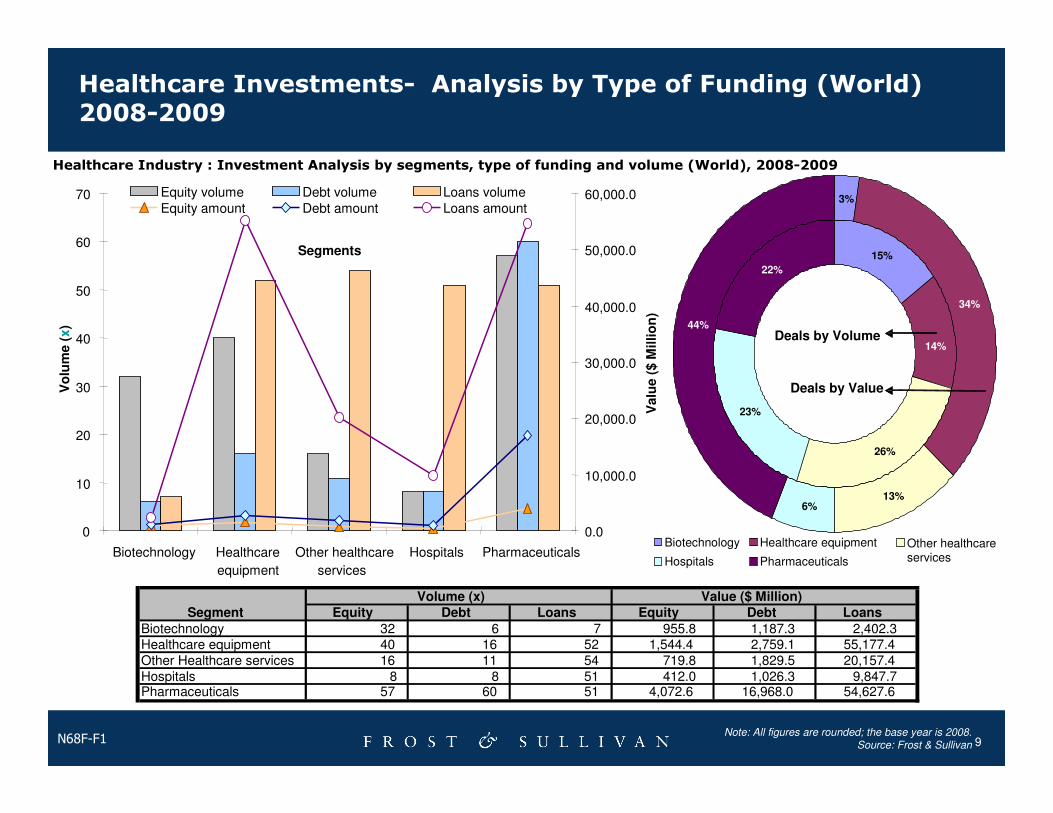

Healthcare Investments- Analysis by Type of Funding (World) 2008-2009

Equity Debt Loans Equity Debt Loans

Biotechnology 32 6 7 955.8 1,187.3 2,402.3Healthcare equipment 40 16 52 1,544.4 2,759.1 55,177.4Other Healthcare services 16 11 54 719.8 1,829.5 20,157.4Hospitals 8 8 51 412.0 1,026.3 9,847.7Pharmaceuticals 57 60 51 4,072.6 16,968.0 54,627.6

Volume (x)Segment

Value ($ Million)

Note: All figures are rounded; the base year is 2008. Source: Frost & Sullivan

Healthcare Industry : Investment Analysis by segments, type of funding and volume (World), 2008-2009

N68F-F1 10

Equity Deals

N68F-F1 11

Stock Markets - An Overview

60.0

70.0

80.0

90.0

100.0

110.0

120.0

130.0

140.0

Jan 0

5

Mar

05

Ma

y 05

Jul 05

Sep 0

5

No

v 05

Jan 0

6

Mar

06

Ma

y 06

Jul 06

Sep 0

6

No

v 06

Jan 0

7

Mar

07

Ma

y 07

Jul 07

Sep 0

7

No

v 07

Jan 0

8

Mar

08

Ma

y 08

Jul 08

Sep 0

8

No

v 08

Jan 0

9

Mar

09

Ma

y 09

Jul 09

Months

Ind

exed

to

100

NASDAQ Biotechnology Index

S&P Healthcare Index

Amex Pharmaceutical Index

Dow Jones Industrial Average

S&P 500

Especially in the recessionary times,

the healthcare index is outperforming

the benchmark S&P 500 and the Dow

Jones Industrial Average handsomely.

NASDAQ Biotech S&P HC Amex Pharma DJ Industrial Average S&P 5001 year 0.1 (0.3) (0.5) (0.1) (0.1)2 year 0.1 (0.4) (0.7) (0.1) (0.0)3 year 0.1 (0.4) (1.0) 0.0 0.04 year 0.1 (0.5) (1.1) (0.0) 0.05 year 0.0 (0.8) (1.7) (0.2) (0.2)6 year 0.2 (2.5) (3.8) (1.5) (1.4)

Investment Horizon

Sharpe's Ratio (%) for Various Indices from August 2002

NASDAQ Biotech S&P HC Amex Pharma DJ Industrial Average S&P 5001 year (0.2) (0.5) (0.7) (0.3) (0.4)2 year (0.4) (0.6) (1.0) (0.4) (0.5)3 year (0.6) (1.6) (2.6) (0.9) (1.1)4 year (2.8) (5.7) (5.2) (4.3) (5.0)

Investment Horizon

Sharpe's Ratio for Various Indices from Jan 2005

Biotech the standout industry

performer in terms of Sharpe's Ratio

Note: All figures are rounded; the base year is 2008. Source: Frost & Sullivan

Healthcare Industry : Stock Markets- An Overview (World), 2005-2009

N68F-F1 12

Debt Deals

N68F-F1 13

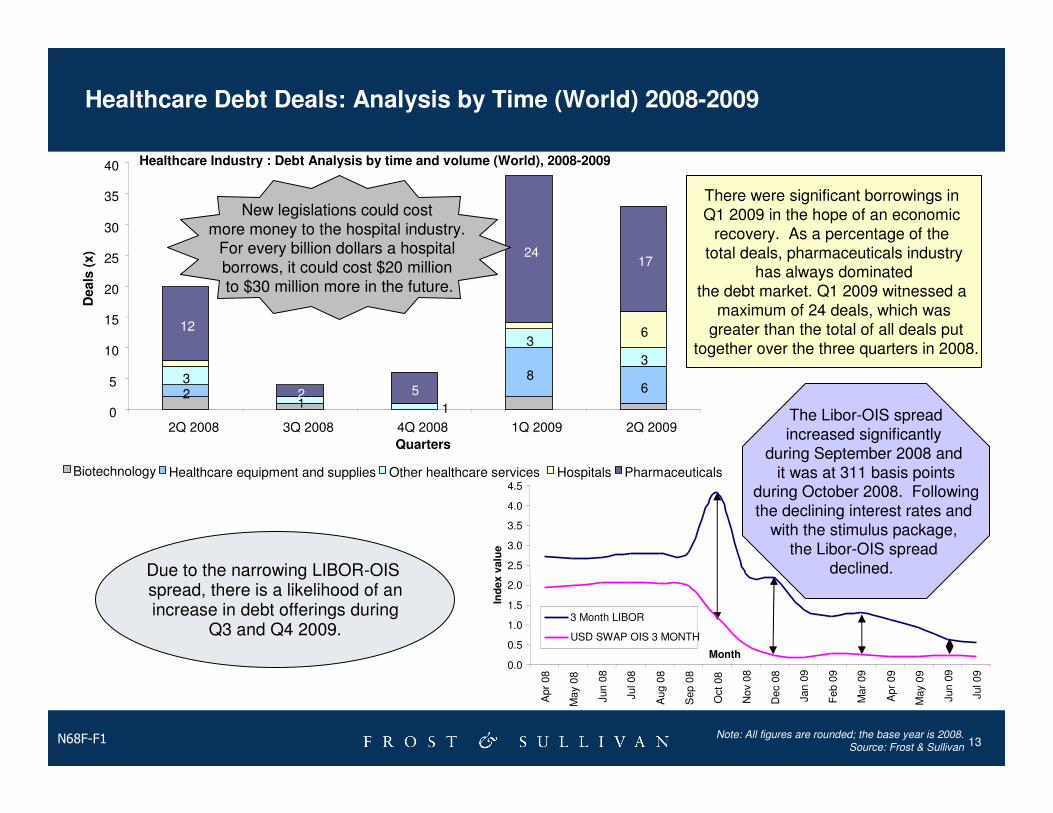

3

1

3

3

12

2 5

2417

2 68

1

6

0

5

10

15

20

25

30

35

40

2Q 2008 3Q 2008 4Q 2008 1Q 2009 2Q 2009

Quarters

Deals

(x)

Biotechnology Healthcare equipment and supplies Other healthcare services Hospitals Pharmaceuticals

There were significant borrowings in Q1 2009 in the hope of an economic

recovery. As a percentage of the total deals, pharmaceuticals industry

has always dominated the debt market. Q1 2009 witnessed a

maximum of 24 deals, which wasgreater than the total of all deals put

together over the three quarters in 2008.

New legislations could cost more money to the hospital industry.

For every billion dollars a hospital borrows, it could cost $20 million to $30 million more in the future.

The Libor-OIS spreadincreased significantly

during September 2008 and it was at 311 basis points

during October 2008. Following the declining interest rates and

with the stimulus package, the Libor-OIS spread

declined. Due to the narrowing LIBOR-OIS spread, there is a likelihood of anincrease in debt offerings during

Q3 and Q4 2009.

Healthcare Debt Deals: Analysis by Time (World) 2008-2009

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Apr

08

May

08

Jun 0

8

Jul 08

Aug 0

8

Sep 0

8

Oct

08

Nov

08

Dec 0

8

Jan 0

9

Feb 0

9

Mar

09

Apr

09

May

09

Jun 0

9

Jul 09

Month

Ind

ex v

alu

e

3 Month LIBOR

USD SWAP OIS 3 MONTH

Note: All figures are rounded; the base year is 2008. Source: Frost & Sullivan

Healthcare Industry : Debt Analysis by time and volume (World), 2008-2009

N68F-F1 14

Loan Deals

N68F-F1 15

4

23

9

5

8

8

8

12

3

7

17

13

1

6

2

1

14

2

1

28

16

7

11

7

2

0 10 20 30 40 50 60

<50

50-200

200-500

500-1000

>1000

Levered Loans North America

Levered Loans Europe

Levered Loans APAC

Unlevered Loans North America

Unlevered Loans Europe

Unlevered Loans APAC

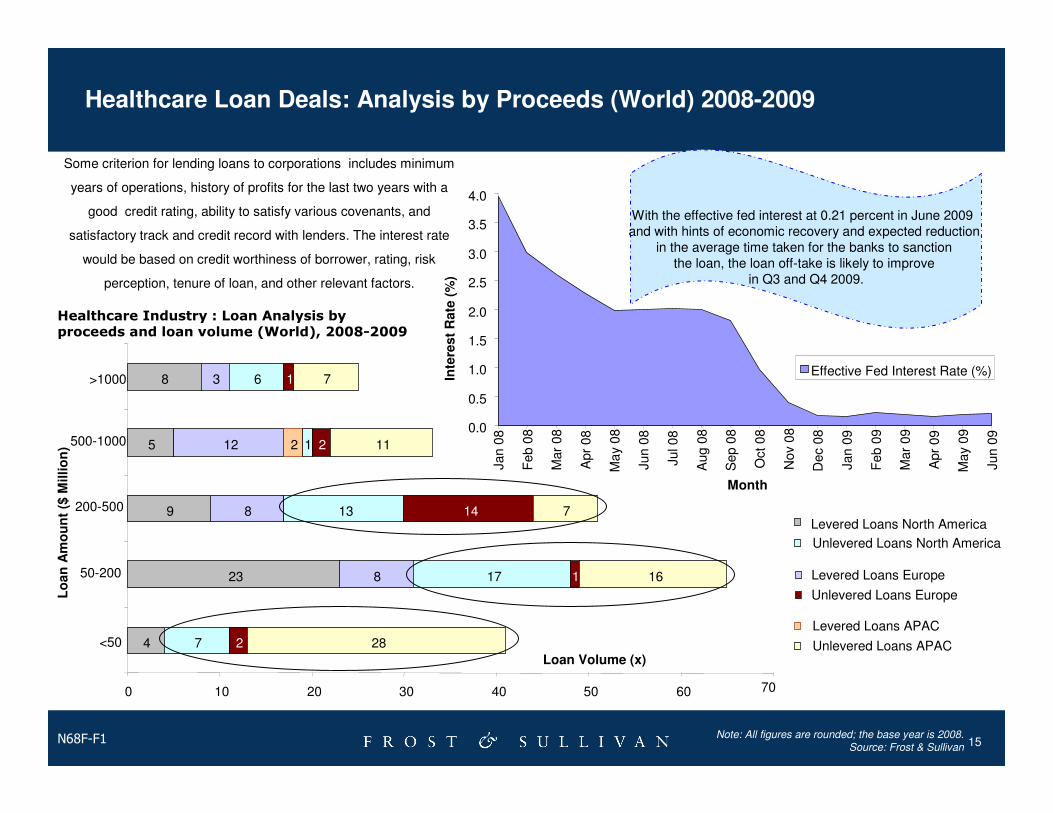

Some criterion for lending loans to corporations includes minimum

years of operations, history of profits for the last two years with a

good credit rating, ability to satisfy various covenants, and

satisfactory track and credit record with lenders. The interest rate

would be based on credit worthiness of borrower, rating, risk

perception, tenure of loan, and other relevant factors.

With the effective fed interest at 0.21 percent in June 2009 and with hints of economic recovery and expected reduction

in the average time taken for the banks to sanction the loan, the loan off-take is likely to improve

in Q3 and Q4 2009.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Jan 0

8

Feb 0

8

Mar

08

Apr

08

Ma

y 08

Jun 0

8

Jul 0

8

Aug 0

8

Sep 0

8

Oct 08

Nov

08

Dec 0

8

Jan 0

9

Feb 0

9

Mar

09

Apr

09

Ma

y 09

Jun 0

9

Month

Inte

rest

Rate

(%

)

Effective Fed Interest Rate (%)

70

Lo

an

Am

ou

nt

($ M

illio

n)

Loan Volume (x)

Healthcare Loan Deals: Analysis by Proceeds (World) 2008-2009

Note: All figures are rounded; the base year is 2008. Source: Frost & Sullivan

Healthcare Industry : Loan Analysis by proceeds and loan volume (World), 2008-2009

N68F-F1 16

Concluding Thoughts

N68F-F1 17

Some Interesting Facts

• A recent study by Harvard University researchers found that the average out-of-pocket medical debt for those who filed

for bankruptcy was $12,000. The study noted that 68 percent of those who filed for bankruptcy had health insurance. In

addition, the study found that 50 percent of all bankruptcy filings were partly the result of medical expenses. In every 30

seconds in the U.S. someone files for bankruptcy in the aftermath of a serious health problem.

• A new survey shows that more than 25 percent of Americans said that housing problems resulted from medical debt,

including the inability to make rent or mortgage payments and the development of bad credit ratings.

• About 1.5 million American families lose their homes to foreclosure every year due to unaffordable medical costs.

Concluding Thoughts

• Pharmaceutical, drug development, medical technologies, and other life sciences are considered to be attractive sectors

for investment from 2010 to 2015. Historical high growth rates due to increases in health expenditure, growth in the

ageing population coupled with greater incidence in chronic illness, and developments in technology are considered to

be the driving factors behind the attractive investment options.

• Niche areas such as percutaneous valve replacement, bioprosthetics with stem cell seeding on a matrix, and robotics

are expected to be the future in the medical devices industry.

• Policies toward Medicare and Medicaid are expected to have a significant impact on the general ‘health’ of the

healthcare industry.

Conclusion

N68F-F1 18

Next Steps

� Register for the next Chairman’s Series on Growth:

The Growth Excellence Model: Competitive Benchmarking & Growth

Investing (November 3, 2009) (http://www.frost.com/growth)

� Register for Frost & Sullivan’s Growth Opportunity Newsletter and

keep abreast of innovative growth opportunities

(www.frost.com/news)

N68F-F1 19

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by taking our survey.

What would you like to see from Frost & Sullivan?

N68F-F1 20

For Additional Information

Johanna Haynes

Corporate Communications

(210) 247-3870

Lori Salazar-Malone

Sales Manager

Business & Financial Services

(210) 247-2448

Jennifer O’Grady

Research Manager

Business & Financial Services

(214) 887-1818