Embed Size (px)

Citation preview

Flevum Roundtable

2 november 2011

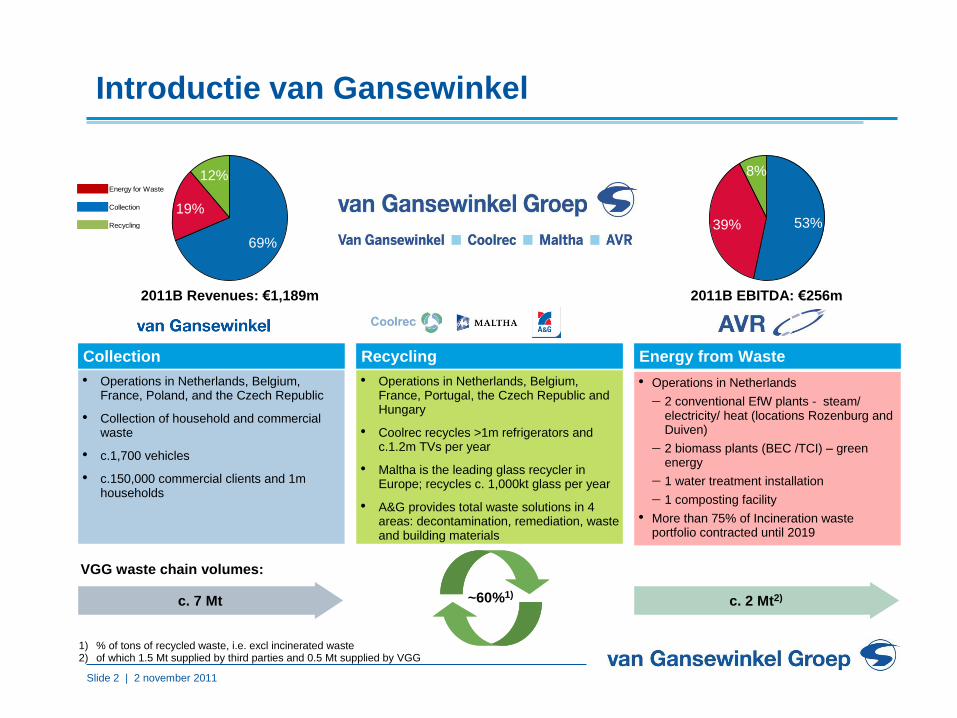

Slide 2 | 2 november 2011

c. 2 Mt2)

Collection Recycling Energy from Waste

• Operations in Netherlands, Belgium, France, Poland, and the Czech Republic

• Collection of household and commercial waste

• c.1,700 vehicles

• c.150,000 commercial clients and 1m households

• Operations in Netherlands, Belgium, France, Portugal, the Czech Republic and Hungary

• Coolrec recycles >1m refrigerators and c.1.2m TVs per year

• Maltha is the leading glass recycler in Europe; recycles c. 1,000kt glass per year

• A&G provides total waste solutions in 4 areas: decontamination, remediation, waste and building materials

• Operations in Netherlands

2 conventional EfW plants - steam/ electricity/ heat (locations Rozenburg and Duiven)

2 biomass plants (BEC /TCI) – green energy

1 water treatment installation

1 composting facility

• More than 75% of Incineration waste portfolio contracted until 2019

c. 7 Mt ~60%1)

2011B Revenues: €1,189m 2011B EBITDA: €256m

VGG waste chain volumes:

Energy for Waste

Collection

Recycling 53%39%

8%

69%

19%

12%

1) % of tons of recycled waste, i.e. excl incinerated waste2) of which 1.5 Mt supplied by third parties and 0.5 Mt supplied by VGG

Introductie van Gansewinkel

Grondstoffen?

Het kan niet op!!

Afvalstoffen in

perspectief

Slide 4 | 2 november 2011

19e eeuw: hygiëne

Slide 5 | 2 november 2011

Ander afval bestond niet

Slide 6 | 2 november 2011

20e eeuw: welvaart maakt afval

Slide 7 | 2 november 2011

20e eeuw: afval moet weg

Slide 8 | 2 november 2011

20e eeuw: milieu

Slide 9 | 2 november 2011

20e eeuw: De vervuiler betaalt

Slide 10 | 2 november 2011

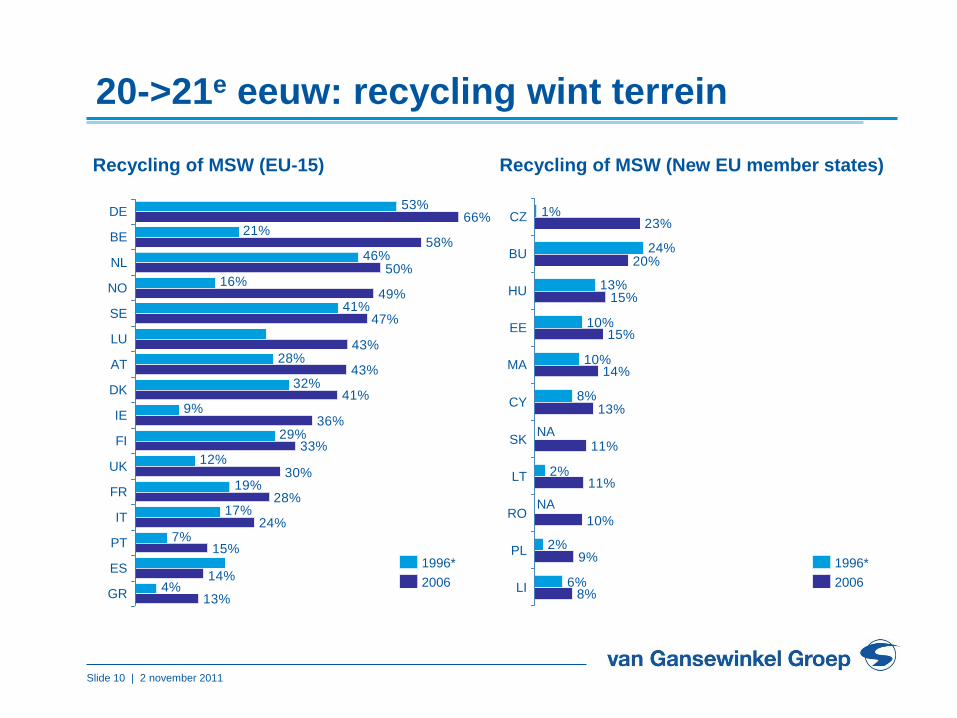

20->21e eeuw: recycling wint terrein

Recycling of MSW (EU-15) Recycling of MSW (New EU member states)

4%

7%

17%

19%

12%

29%

9%

32%

28%

41%

16%

46%

21%

53%

13%

14%

15%

24%

28%

30%

33%

36%

41%

43%

43%

47%

49%

50%

58%

66%

NL

BE

DE

DK

GR

ES

PT

IT

FR

UK

FI

IE

AT

LU

SE

NO

2006

1996*

6%

2%

2%

8%

10%

10%

13%

24%

1%

8%

9%

10%

11%

11%

13%

14%

15%

15%

20%

23%

LI

PL

RO

LT

SK

CY

CZ

MA

EE

HU

BU

2006

1996*

NA

NA

Slide 11 | 2 november 2011

Afval in Nederland (2008, miljoen ton)

0

5

10

15

20

25

30

Bouw

- en s

loopsecto

r

Industr

ie

Huis

houdens

Handel,

die

nste

n e

n

overh

eid

Landbouw

, bosbouw

en v

isserij

Energ

ievoorz

ienin

g

Rio

olw

ate

rzuiv

ering

Verk

eer

en v

erv

oer

Drinkw

ate

rvoorz

ienin

g

Storten + lozen

Verbranden

Nuttige toepassing

20->21e eeuw: recycling wint terrein

Slide 12 | 2 november 2011

20->21e eeuw: recycling wint terrein

Reused Disposal

Zinc 70% 30% 8%

Lead 65% 35% 35%

Phosphate 99%

Rubber 47% 53% 23%

Virgin

65% 35% 19%

Plastic 92% 8% 33%

Paper 35% 65% 25%

Steel 60% 40% 13%

Glass

Recycling

rate*

Production (total 100%)

Waste collected

EU raw materials market (2008)

76%

72%

21%

65%

82%

50%

Recycling share is unlikely to reach 100% as certain percentage of virgin material will

always be required due to quality requirements and growth of materials in the market

223

111

80

37

5

3

Total

(Mton)

80%2

N/A3N/A

Slide 13 | 2 november 2011

Downcycling

21e eeuw: nuttige toepassing, maar….

Slide 14 | 2 november 2011

Energetisch

hergebruik

21e eeuw: nuttige toepassing, maar….

Slide 15 | 2 november 2011

21e eeuw: nuttige toepassing, maar….

CN, US, IN Self-regenerating and will not run out

CN, RU, CA Large recycling share

CN, US, IN Very large supply but often difficult to mine

CN, US, MA Current scarcity specific for Europe

CN, AU, BR Large recycling shares, polluted by non-ferros

US, RU, CA Large in VGG’s home market

CL, US, PE Demand kept rising during crisis

SA, RU, US Energy substitutes already available

CN, BO, SA Main reliance on Chinese production

PE, MX, CN Mined globally

CN, JP, KO Recovery from other base metals possible

CN, US, IN Self-regenerating and will not run out

CN, RU, CA Large recycling share

CN, US, IN Very large supply but often difficult to mine

CN, US, MA Current scarcity specific for Europe

CN, AU, BR Large recycling shares, polluted by non-ferros

US, RU, CA Large in VGG’s home market

CL, US, PE Demand kept rising during crisis

SA, RU, US Energy substitutes already available

CN, BO, SA Main reliance on Chinese production

PE, MX, CN Mined globally

CN, JP, KO Recovery from other base metals possible

Raw Material Markets

Oil 43 yrs

Copper 44 yrs

Gas 61 yrs

Iron ore 64 yrs

Phosphate 75 yrs

Coal 148 yrs

Aluminium* 161 yrs

Soda ∞

Antimony 30 yrs

Silver 29 yrs

Indium 13 yrs

NM

55%

69%

75%

50%

42%

47%

41%

Years to depletion Top 3

producers

Share of

top 3

Comments

95%

44%

78%Rare metals

Slide 16 | 2 november 2011

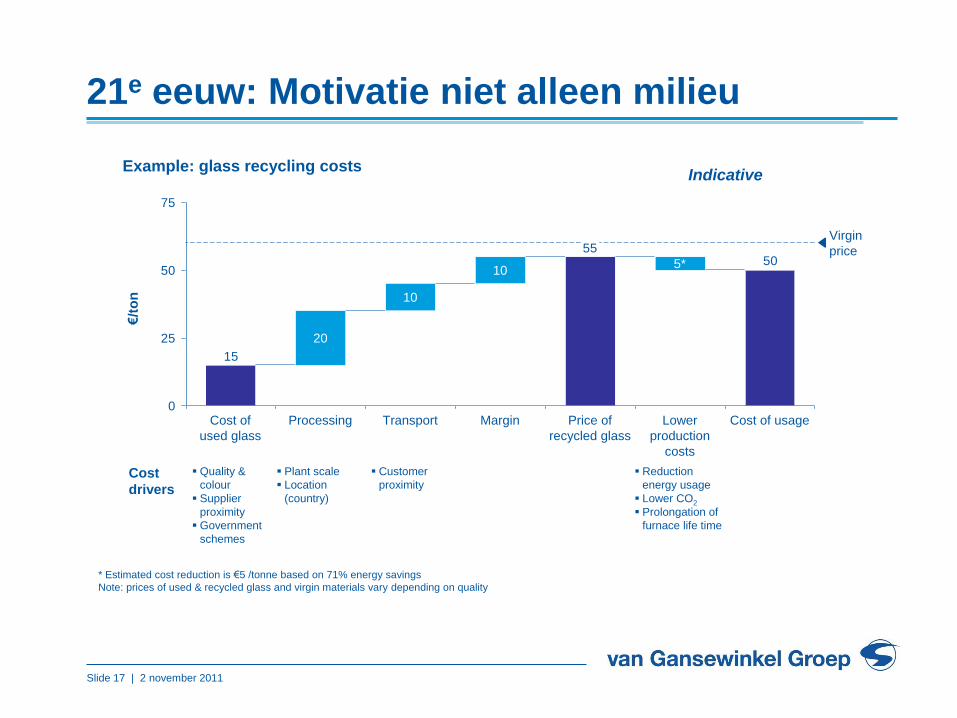

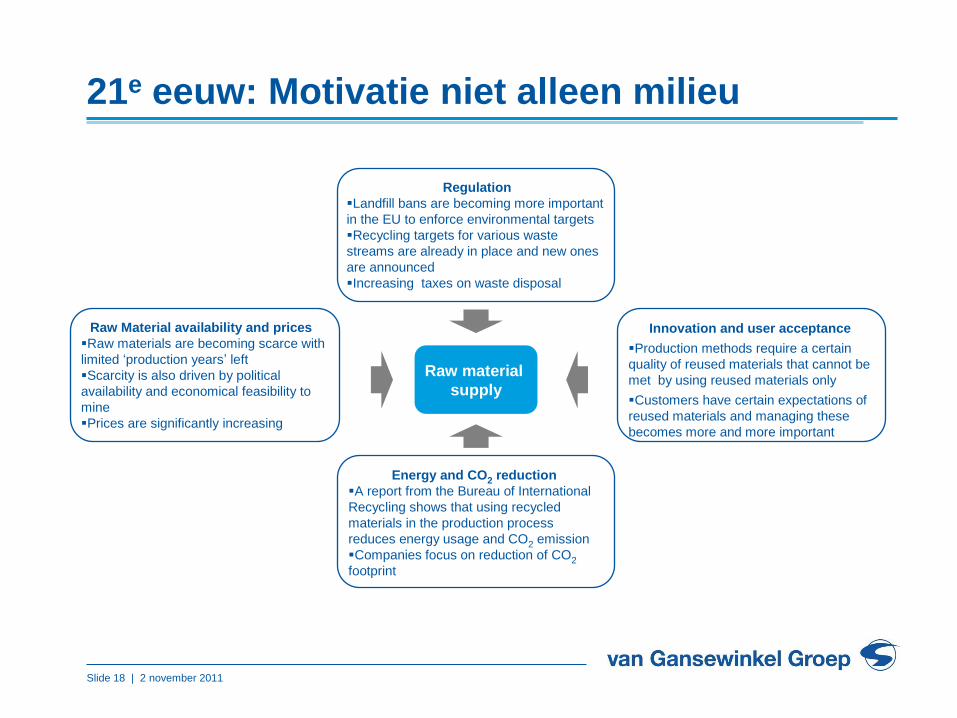

21e eeuw: Motivatie niet alleen milieu

Price developments Virgin materials(Index 2000=100)

0

50

100

150

200

250

300

350

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Tungsten

Tin

Antimony

Soda

Phosphate

NaturalGas

Crude oil

Coal

WoodChips

Rubber

Aluminium ore

Copper ore

Ironore

Economic crisisInflation

2009

239

238

225

205

189

187

172

154

150

145

141

137

130

Inflation 123

2009

239

238

225

205

189

187

172

154

150

145

141

137

130

Inflation 123

Slide 17 | 2 november 2011

21e eeuw: Motivatie niet alleen milieu

5055

15

0

25

50

75

Virgin

price

Cost of usageLower

production

costs

5*

Price of

recycled glass

Margin

10

Transport

10

Processing

20

Cost of

used glass

Example: glass recycling costs

€/t

on

Cost

drivers

Quality &

colour

Supplier

proximity

Government

schemes

Plant scale

Location

(country)

Customer

proximity

Reduction

energy usage

Lower CO2

Prolongation of

furnace life time

* Estimated cost reduction is €5 /tonne based on 71% energy savings

Note: prices of used & recycled glass and virgin materials vary depending on quality

Indicative

Slide 18 | 2 november 2011

21e eeuw: Motivatie niet alleen milieu

Raw material

supply

Raw Material availability and prices .

Raw materials are becoming scarce with

limited ‘production years’ left

Scarcity is also driven by political

availability and economical feasibility to

mine

Prices are significantly increasing

Innovation and user acceptance

Production methods require a certain

quality of reused materials that cannot be

met by using reused materials only

Customers have certain expectations of

reused materials and managing these

becomes more and more important

Energy and CO2 reduction

A report from the Bureau of International

Recycling shows that using recycled

materials in the production process

reduces energy usage and CO2 emission

Companies focus on reduction of CO2

footprint

Regulation

Landfill bans are becoming more important

in the EU to enforce environmental targets

Recycling targets for various waste

streams are already in place and new ones

are announced

Increasing taxes on waste disposal

Slide 19 | 2 november 2011

21e eeuw: conclusie: Afval bestaat niet

Grondstoffen en Energie:

• Schaars

• Duur

Afval

• bevat grondstoffen

• bevat energie

Slide 20 | 2 november 2011

21e eeuw: Afval bestaat niet

Voorbeeld:

Grote bank in Nederland

• > 500 kantoren

• alle afval

• 3 jaar

Slide 21 | 2 november 2011

21e eeuw: Afval bestaat niet

Voorbeeld:

Grote bank in Nederland

• > 500 kantoren

• alle afval

• 3 jaar

Afvalomzet ????????

Slide 22 | 2 november 2011

Afval bestaat niet: stellingen

• De schillenboer/lompenkar komt terug in ons straatbeeld

• Groei van recycling is 100% afhankelijk van grondstofprijzen

• Regelgeving moet niet recycling van gebruikte producten

afdwingen, maar gebruik van gerecyclede grondstoffen.

• Een ‘closed loop’ is te creëren met de ondernemingen vandaag

aanwezig

• De volgende wereldoorlog wordt gevoerd om grondstoffen

(buiten olie)

• Think global, act local dient adagium te zijn voor EU, (&NL,

provincie, gemeente) op gebied van productie en consumptie

Slide 23 | 2 november 2011

Slide 24 | 2 november 2011

Potential savings (reused vs. virgin)*

76%

18%

99%

11%

58%

40%

65%

92%

Zinc 60%

Paper 65%

Lead 65%

Glass 71%

Steel 74%

Plastic 80%

Copper 85%

Aluminium 95%

Energy CO2

Energy and CO2 reduction have been

compared for the entire production

process of the end product

Using recycled material often reduces

the required energy in production as raw

materials are more comparable to the

end product (e.g. scrap vs. bauxite ore

for aluminium production)

CO2 is saved not only in production but

also in transportation

Raw ores are transported in large

quantities from elsewhere in the world to

be prepared for production locally

Not only is the production process for

glass and paper much simpler but these

are found closer to home which results

in more possible reduction of CO2

Slide 25 | 2 november 2011

Trade volume in reused material EU-27

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

0 10.000 20.000 30.000 40.000 50.000 60.000 70.000 80.000

Volume (Mton)

WoodRubber

Plastic

Paper and pulp

Non-Ferrous

Nickel

Glass

Ferrous

Copper

Aluminium

CA

GR

’00-’

09

Ø = 3.5%

Slide 26 | 2 november 2011

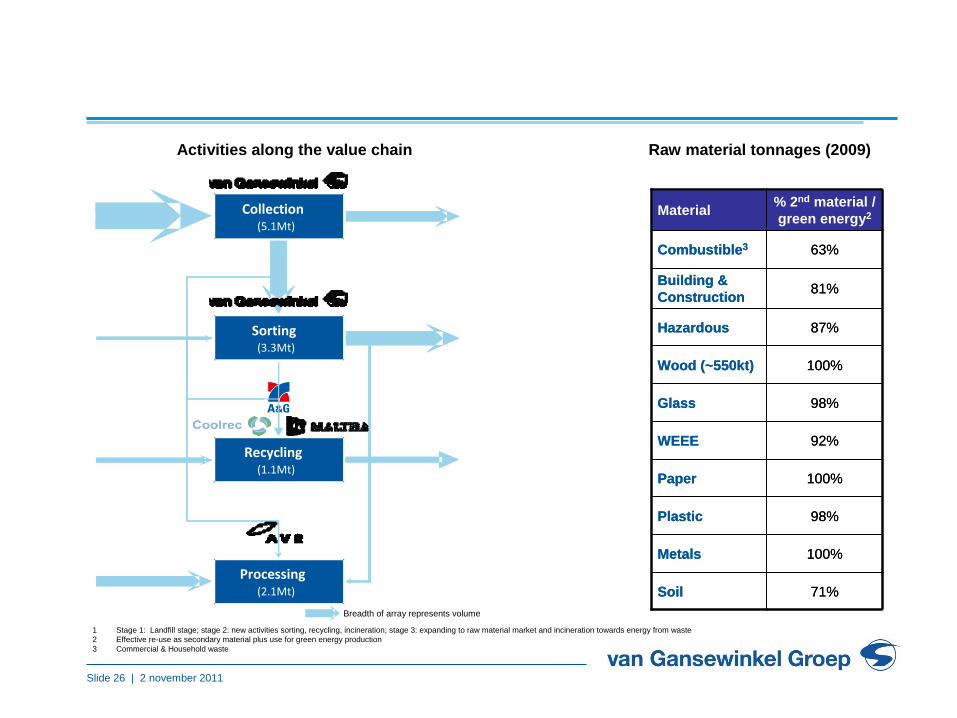

Treatment

Recycling

Incineration

CollectionServicesCollection

(5.1Mt)

Sorting(3.3Mt)

Recycling(1.1Mt)

Processing(2.1Mt)

Treatment

Recycling

Incineration

CollectionServicesCollection

(5.1Mt)

Sorting(3.3Mt)

Recycling(1.1Mt)

Processing(2.1Mt)

Breadth of array represents volume

1 Stage 1: Landfill stage; stage 2: new activities sorting, recycling, incineration; stage 3: expanding to raw material market and incineration towards energy from waste

2 Effective re-use as secondary material plus use for green energy production

3 Commercial & Household waste

81%Building &

Construction

87%Hazardous

63%Combustible3

71%Soil

100%Metals

98%Plastic

100%Paper

92%WEEE

98%Glass

100%Wood (~550kt)

% 2nd material /

green energy2Material

81%Building &

Construction

87%Hazardous

63%Combustible3

71%Soil

100%Metals

98%Plastic

100%Paper

92%WEEE

98%Glass

100%Wood (~550kt)

% 2nd material /

green energy2Material

Raw material tonnages (2009)Activities along the value chain

Slide 27 | 2 november 2011

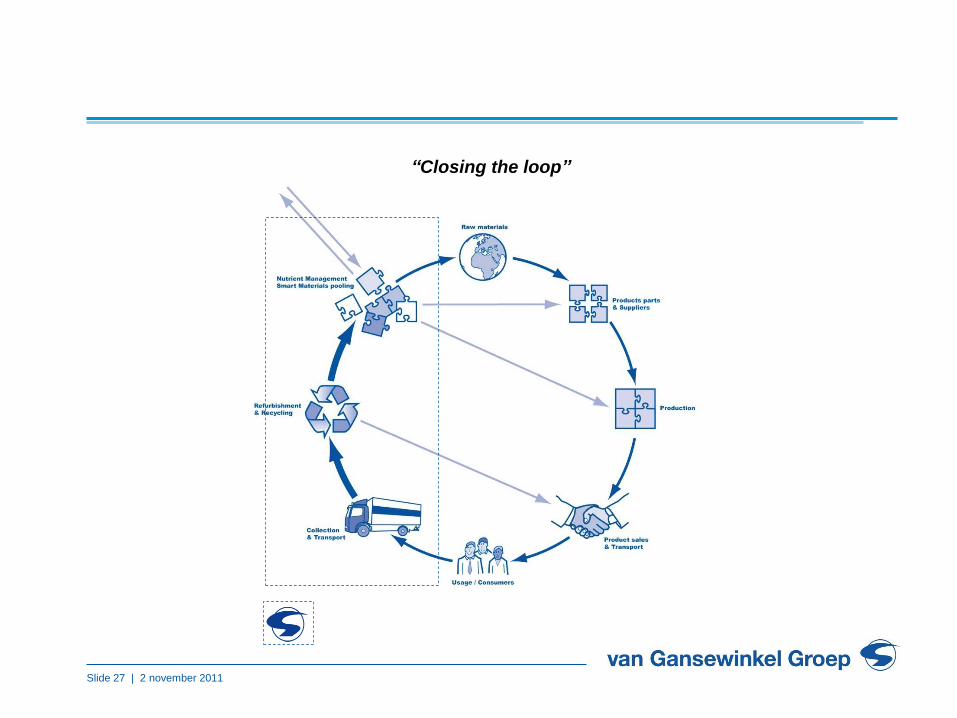

“Closing the loop”

![[HANDBUCH] "Geld verdienen im Internet mit Affiliate Marketing"](https://img.pdfslide.us/doc/110x75/5461fb1fb1af9fbc4d8b4f41/handbuch-geld-verdienen-im-internet-mit-affiliate-marketing.jpg)