Embed Size (px)

Citation preview

OUTLOOK 13

1

INTRODUCTION 2

THE CONSUMER 4

TELEVISION 6

NEWS MEDIA 8

ONLINE 10

RADIO 12

OUT OF HOME 14

CINEMA 16

SPONSORSHIP 18

DIRECT MARKETING 20CONTENTS

INTRODUCTION

2013 is the year we expect to see a return to growth in the advertising economy in theRepublic of Ireland. After five consecutive years of decline, we believe the market will nowbegin to reflect the stability and delicate growth that we are seeing elsewhere in theeconomy. Overall we forecast 0.7% growth to a total of €698m but this is being driven bythe digital sector, which we expect to increase by almost 11% in the Republic. Excludingdigital, the underlying position is less favorable, showing a decline of 2%.

In Northern Ireland, we anticipate a rise in digital spending of circa 8% this year, but thiswill be the only sector to see any growth, and overall we are forecasting a fall in total spendof 2.1% to €159m, due to weak demand again this year.

When we look at advertising spend on a per capita basis, the difference between the twomarkets becomes very clear. The level of advertising spend in ROI per capita is €156,compared with only €89 in NI. This is an indicator of the underlying weakness in theregion, despite growing business and consumer confidence.

Reflecting on the last five years, it occurs to us that one of the key factors contributing tothe fall in spend across the island is the lack of evidence within marketing departmentsregarding how effective their investment was and the implications of cutting back.

Every marketer should be able to answer the following question “what percentage of yourtotal sales is exclusively attributable to your marketing activities?” The reality is very fewhave this knowledge. However, it is likely that most would know what their brandawareness is from their latest brand tracker, but how useful is that? How does that helpyou to prepare a marketing plan, present a budget proposal, or allocate your marketingresources effectively?

ADVERTISING INVESTMENT PER CAPITAIN THE REPUBLIC OF IRELAND IS 75%GREATER THAN NORTHERN IRELAND

2

3

Surely, knowing precisely what marketing contributes to your business is essential and itcan be established by investing in market mix modeling. However, analysis of this kind isstill demoted in favour of softer, blunter research into brand awareness and brand equity,which does little to quantify the impact of marketing on sales or enable marketers tooptimise the mix of their investments.

Ask yourself, which would help you to convince your Finance Director more….a) beingable to show that 20% of your total sales revenue relies on marketing and that cutting thebudget will result in sales decline of 10%, or b) showing him/her your top-of-mindawareness trend and what the consumer thinks of your brand? There’s only one answer,really, isn’t there?

In our opinion, too much money and time is invested in brand tracking and too little inmodeling and other forms of marketing analytics.

In Ireland less than €500,000 is spent per annum on market mix modeling. That is a dismal0.06% of the total media spend (North & South). In the UK it is 0.69%, eleven and a halftimes greater than the Irish figure! In the US the investment level is greater again and arecent survey of marketing directors found companies expect to increase the analyticsportion of their marketing budgets by 60% in the next three years.

We are not saying that you shouldn’t invest in brand tracking. It can be genuinely useful inhelping a company monitor its brand equity over time and identify potential problems. Itcan also provide useful intelligence on key competitors in terms of brand preference andwhere your brand sits on the consideration set. However, we believe it is given too muchemphasis and carried out too often. When is the last time you ever came out of a brandtracking presentation feeling inspired?

Investment in marketing analytics will give you immediate guidance on how to grow yourprofit. When used in conjunction with all the data that is washing around our companies,it will help to properly evaluate marketing performance, gain insight into purchasing habits,and make evidence-based marketing decisions.

The use of this so-called ‘Big Data’ is helping organisations of all kinds anticipate the future.Police departments internationally are increasingly using historic data to predict where andwhen crimes may happen and Barack Obama used it to win a second term by assigningevery voter in the country a pair of scores based on the probability that they would a) casta ballot and b) support Obama.

So is this the Holy Grail? No, it’s just one part of it, so is brand tracking but overrelianceon it will slow you down. Remember, if you do what you’ve always done, you’ll get whatyou’ve always gotten.

Ok, now that we have that off our chest…the following pages provide a snapshot of thekey developments we expect to see this year across the main industry sectors. We hopeyou find the document useful. If you wish to discuss any of the issues, please feel free tocall me on +353 1 649 6458.

In the meantime, best wishes for 2013.

Alan Cox

726.4 693.0 697.8

168.2

2011 2012 2013

162.0 158.7

ROI NI

UK INVESTMENT IN MARKET MIX MODELLING IS 11.5 TIMESGREATER THAN IRELAND

Total Advertising Spend (€m)

Source: Core Media Estimates

THE

CONSUMER

Something pivotal happened in 2012; or rather something pivotal didn’t happen. Our worstfears were not realised; it was certainly a mixed year, but it’s worth noting that “mixed” is animprovement on previous years.

There is a sense of a fundamental shift in the air. 2013 is being heralded as the first year we canstart to look forward again, as opposed to the years of backward glances and naval gazing.

In the Republic of Ireland, away from the sound bites and politicking, Budget 2013 was one ofpain, certainly, but also progress. It was our fifth ‘recessionary’ budget, but it’s worth notingthat as defined in pure economic terms, neither the Republic nor Northern Ireland are inrecession. Although growth is admittedly weak both sides of the border, sentiment surveys areshowing some signs of recovery, albeit from a low base.

Sentiment indices for 2012 have been the strongest in four years in ROI and are on the rise inNI. Figures for January this year in the Republic continued the recent upward trend and receiveda considerable ‘bounce’ after the predictable fall off in December.

The budget also prioritised business, in terms of the Foreign Direct Investment and SME sectors,rather than domestic spending, which seems a prudent medium-term strategy. As a result, therewill be no huge change in consumer spending in 2013, rather a more measured approach.However, high street retail sales in ROI have begun to turn a corner in the last few months of2012, with December seeing a volume increase of 0.8%. More encouragingly, the value of thesesales was up by 1.1%.

Two of the key factors affecting sentiment in 2013 will be the Irish presidency of the EU, andthe G8 summit in Northern Ireland; both of which are leading to considerable international focus.

It was timely that our presidency corresponded with the final crunch talks on the promissorynotes debacle, and perhaps it was of some help in securing the landmark agreement. Whilethe Government’s success will have little impact on our individual pockets, the new deal shouldsignal a significant increase in consumer confidence and faith in the future.

As a central bank source said recently in the press, “It’s not that paradise starts tomorrow. It’snot heaven on earth all of a sudden. It’s a good first step”

So, what are the key trends in addressing consumers in 2013?

“IT’S NOT THAT PARADISE STARTS TOMORROWIT’S NOT HEAVEN ON EARTH ALL OF A SUDDEN IT’S A GOOD FIRST STEP”

4

5

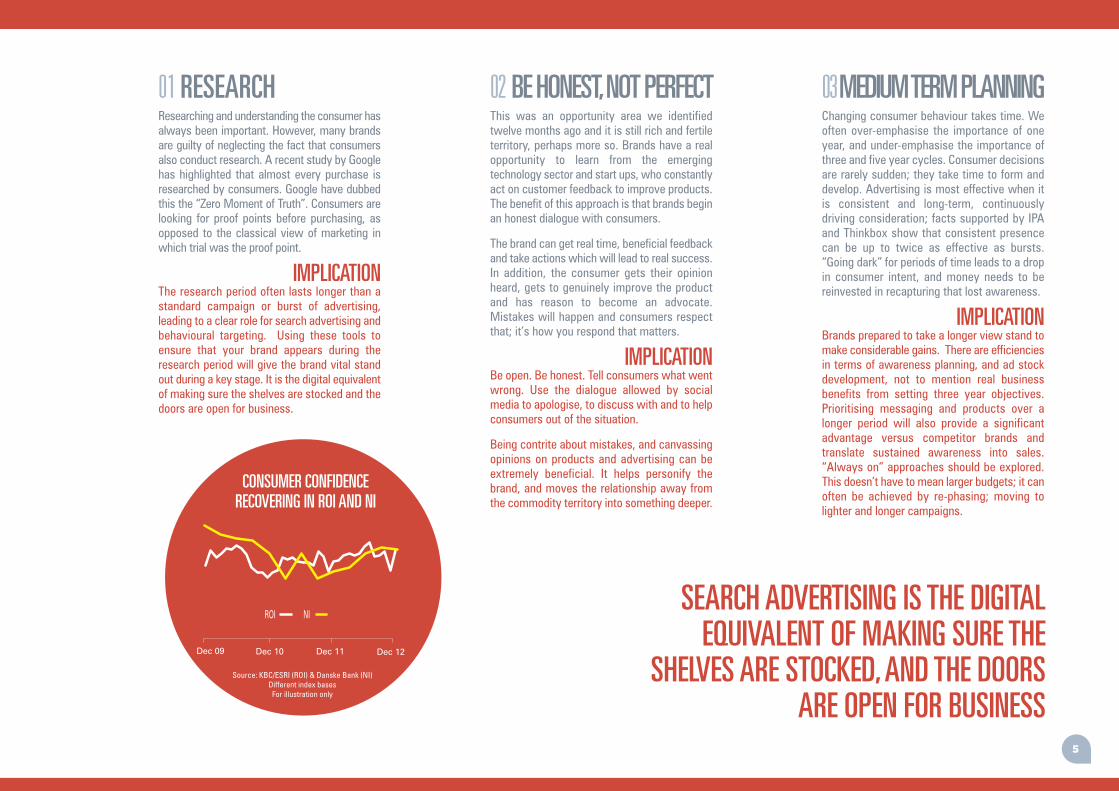

01 RESEARCH Researching and understanding the consumer hasalways been important. However, many brandsare guilty of neglecting the fact that consumersalso conduct research. A recent study by Googlehas highlighted that almost every purchase isresearched by consumers. Google have dubbedthis the “Zero Moment of Truth”. Consumers arelooking for proof points before purchasing, asopposed to the classical view of marketing inwhich trial was the proof point.

IMPLICATIONThe research period often lasts longer than astandard campaign or burst of advertising,leading to a clear role for search advertising andbehavioural targeting. Using these tools toensure that your brand appears during theresearch period will give the brand vital standout during a key stage. It is the digital equivalentof making sure the shelves are stocked and thedoors are open for business.

This was an opportunity area we identifiedtwelve months ago and it is still rich and fertileterritory, perhaps more so. Brands have a realopportunity to learn from the emergingtechnology sector and start ups, who constantlyact on customer feedback to improve products.The benefit of this approach is that brands beginan honest dialogue with consumers.

The brand can get real time, beneficial feedbackand take actions which will lead to real success.In addition, the consumer gets their opinionheard, gets to genuinely improve the productand has reason to become an advocate.Mistakes will happen and consumers respectthat; it’s how you respond that matters.

IMPLICATIONBe open. Be honest. Tell consumers what wentwrong. Use the dialogue allowed by socialmedia to apologise, to discuss with and to helpconsumers out of the situation.

Being contrite about mistakes, and canvassingopinions on products and advertising can beextremely beneficial. It helps personify thebrand, and moves the relationship away fromthe commodity territory into something deeper.

Changing consumer behaviour takes time. Weoften over-emphasise the importance of oneyear, and under-emphasise the importance ofthree and five year cycles. Consumer decisionsare rarely sudden; they take time to form anddevelop. Advertising is most effective when itis consistent and long-term, continuouslydriving consideration; facts supported by IPAand Thinkbox show that consistent presencecan be up to twice as effective as bursts.“Going dark” for periods of time leads to a dropin consumer intent, and money needs to bereinvested in recapturing that lost awareness.

IMPLICATIONBrands prepared to take a longer view stand tomake considerable gains. There are efficienciesin terms of awareness planning, and ad stockdevelopment, not to mention real businessbenefits from setting three year objectives.Prioritising messaging and products over alonger period will also provide a significantadvantage versus competitor brands andtranslate sustained awareness into sales.“Always on” approaches should be explored.This doesn’t have to mean larger budgets; it canoften be achieved by re-phasing; moving tolighter and longer campaigns.

02 BE HONEST, NOT PERFECT 03 MEDIUM TERM PLANNING

CONSUMER CONFIDENCE RECOVERING IN ROI AND NI

Dec 09 Dec 11Dec 10 Dec 12

NIROISEARCH ADVERTISING IS THE DIGITAL

EQUIVALENT OF MAKING SURE THESHELVES ARE STOCKED, AND THE DOORS

ARE OPEN FOR BUSINESS Source: KBC/ESRI (ROI) & Danske Bank (NI)

Different index bases For illustration only

TELEVISION

Smart TVs, tablets, video-on-demand, catch-up, SKY Go, 3-D, Ultra HD, Netflix and Apple TVare just a few of the technological advances that have revolutionised how we watch ‘television’content. 2013 will be the year that we understand how this is affecting consumers.

However, before predicting the future it is important to comment on the present. Television viewingin Ireland is higher than ever before. The average adult watched 3 hours and 35 minutes of TV in2012, an increase of 19% on 2000. Even young adults under 34, who are generally early adoptersof technology, are watching 4% more TV than 2000. In Northern Ireland, viewing is up 29% in thelast five years for adults. The faster rate of growth in NI is due to infrastructure upgrades, whichincreased the number of homes with multi-channel television.

So, why is television performing this well despite the challenges of a digital world? The mainreason has been the growth of Digital Video Recorders (DVRs) which are now in 53% of allhomes in the Republic and 44% in the North; the easy access they provide to content meansthere is always something to watch. In fact, homes with DVRs watch 16% more TV content.

Although TV viewing is on the up, viewing to commercial breaks is not. One consequence ofthe TV revolution has been the ability to “ad-skip”. In the US where the DVR market is mature,55% of commercials are skipped when time-shifted. This compares to only 30% in less maturemarkets such as the UK & Ireland.

It is important to note that the above figures are for time-shifted viewing only. Despite all thehype surrounding DVRs the vast majority of our viewing is still watched “live”. In Ireland only8.4% of viewing is time-shifted; therefore, only 3% of all TV commercials seen in a day areskipped. Not in my household, you may reply, but remember you are not a typical viewer.

It is naive to suggest that things will always be this way; skipping will inevitably increase andbecome a major issue in years to come as consumers become more used to time-shifting.However, this is taking longer than expected and in 2013 commercial impacts are only likely todecline by 1% due to this technology. Other factors relating to falling programming budgets mayresult in an additional 2% fall in commercial impacts.

In terms of spend, TV will see a return to growth this year of 1% in the Republic, but we expecta 2% decline in Northern Ireland due to lower demand in the region.

ONLY 3% OF ALL TV COMMERCIALS ARE FASTFORWARDED

6

7

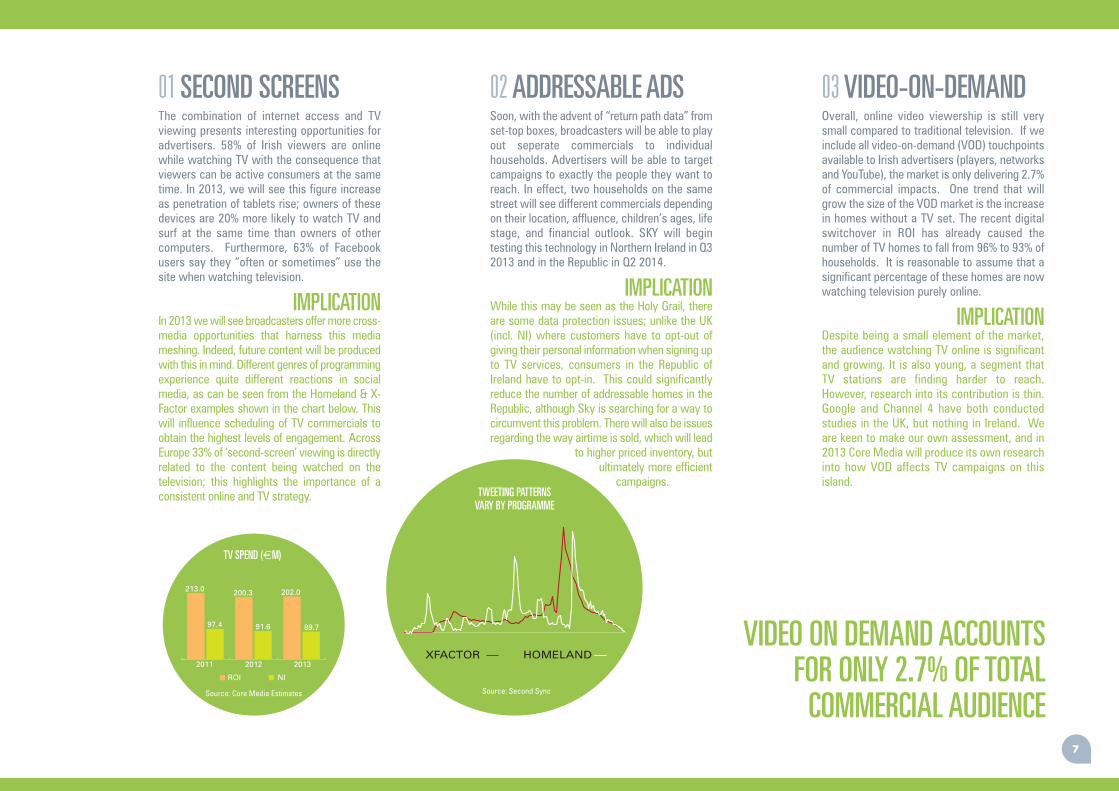

01 SECOND SCREENSThe combination of internet access and TVviewing presents interesting opportunities foradvertisers. 58% of Irish viewers are onlinewhile watching TV with the consequence thatviewers can be active consumers at the sametime. In 2013, we will see this figure increaseas penetration of tablets rise; owners of thesedevices are 20% more likely to watch TV andsurf at the same time than owners of othercomputers. Furthermore, 63% of Facebookusers say they “often or sometimes” use thesite when watching television.

IMPLICATIONIn 2013 we will see broadcasters offer more cross-media opportunities that harness this mediameshing. Indeed, future content will be producedwith this in mind. Different genres of programmingexperience quite different reactions in socialmedia, as can be seen from the Homeland & X-Factor examples shown in the chart below. Thiswill influence scheduling of TV commercials toobtain the highest levels of engagement. AcrossEurope 33% of ‘second-screen’ viewing is directlyrelated to the content being watched on thetelevision; this highlights the importance of aconsistent online and TV strategy.

Soon, with the advent of “return path data” fromset-top boxes, broadcasters will be able to playout seperate commercials to individualhouseholds. Advertisers will be able to targetcampaigns to exactly the people they want toreach. In effect, two households on the samestreet will see different commercials dependingon their location, affluence, children’s ages, lifestage, and financial outlook. SKY will begintesting this technology in Northern Ireland in Q32013 and in the Republic in Q2 2014.

IMPLICATIONWhile this may be seen as the Holy Grail, thereare some data protection issues; unlike the UK(incl. NI) where customers have to opt-out ofgiving their personal information when signing upto TV services, consumers in the Republic ofIreland have to opt-in. This could significantlyreduce the number of addressable homes in theRepublic, although Sky is searching for a way tocircumvent this problem. There will also be issuesregarding the way airtime is sold, which will lead

to higher priced inventory, butultimately more efficient

campaigns.

Overall, online video viewership is still verysmall compared to traditional television. If weinclude all video-on-demand (VOD) touchpointsavailable to Irish advertisers (players, networksand YouTube), the market is only delivering 2.7%of commercial impacts. One trend that willgrow the size of the VOD market is the increasein homes without a TV set. The recent digitalswitchover in ROI has already caused thenumber of TV homes to fall from 96% to 93% ofhouseholds. It is reasonable to assume that asignificant percentage of these homes are nowwatching television purely online.

IMPLICATIONDespite being a small element of the market,the audience watching TV online is significantand growing. It is also young, a segment thatTV stations are finding harder to reach.However, research into its contribution is thin.Google and Channel 4 have both conductedstudies in the UK, but nothing in Ireland. Weare keen to make our own assessment, and in2013 Core Media will produce its own researchinto how VOD affects TV campaigns on thisisland.

02 ADDRESSABLE ADS 03 VIDEO-ON-DEMAND

TV SPEND (€M)

213.0 200.3 202.0

97.4

2011 2012 2013

91.6 89.7

ROI NI

VIDEO ON DEMAND ACCOUNTSFOR ONLY 2.7% OF TOTAL

COMMERCIAL AUDIENCESource: Core Media Estimates Source: Second Sync

TWEETING PATTERNSVARY BY PROGRAMME

XFACTOR HOMELAND

NEWS

MEDIA

As stated in last year’s outlook, the “news” part of newspapers is doing fine. It’s the “paper”part that’s the issue. In the intervening time, most of the industry have accepted this. Lastsummer, the Newspaper Marketing Agency, the body that seeks to raise awareness of the valueof newspapers in the UK, was rebranded as Newsworks. This new name, removing the word"newspaper" from the title, is indicative of the changed landscape of the industry. Similarly, itsmembers are now referred to as “newsbrands”.

This change is symbolic of the new reality in the national press industry, which now needs tooperate across a range of different platforms – desktop computers, laptops, tablets andsmartphones - as well as print.

While this might appear cosmetic, there is no doubting the importance of branding. A product’sbrand is a statement of intent. Not only does it inform its users what to expect and what itstands for, it also helps the company stay focused and inspired. 2012 was a tough year andanother lean year is predicted. An industry-wide reframing and renaming of the newspaperbusiness will show how the sector is embracing the changing way news is being consumed.

Removing words like “paper”, “print” and the related iconography from the industry’s awardsceremonies, representative bodies etc. will bring more integration and will encourage agenciesto incorporate the full scope of what each publisher has to offer.

INTEREST IN NEWS IS SOLIDREADERS ARE MERELY CHOOSING DIFFERENTMETHODS OF CONSUMPTION

8

9

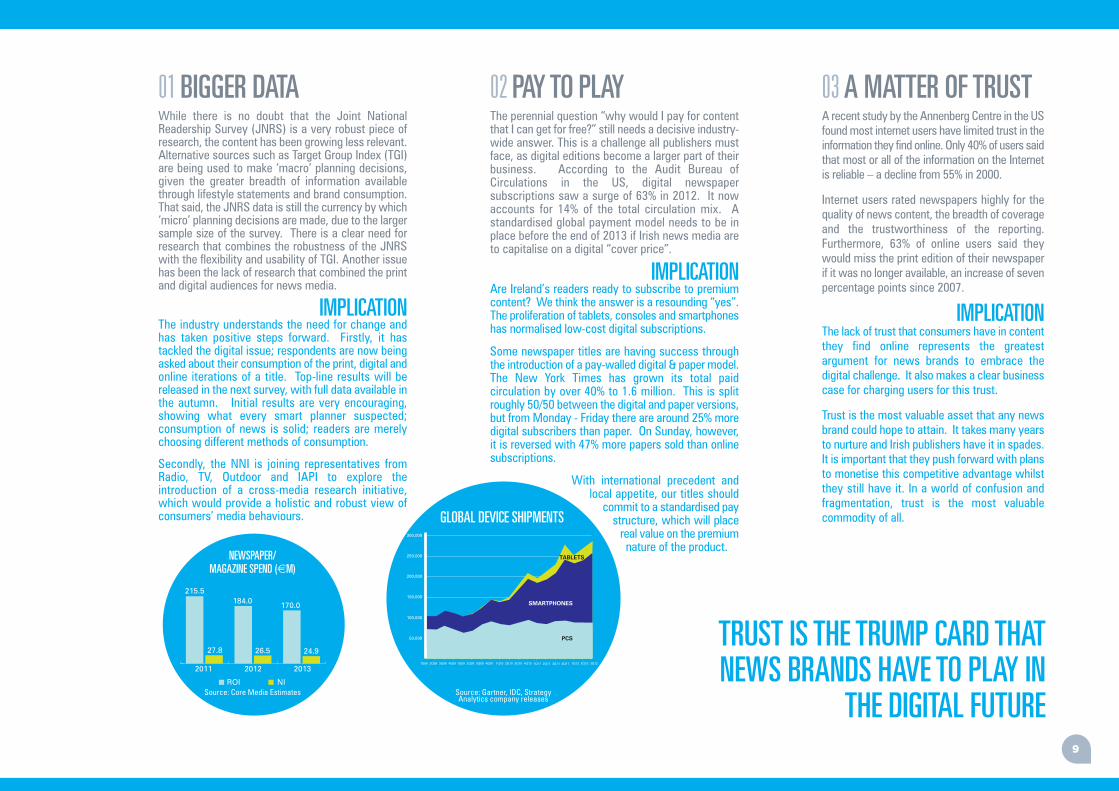

01 BIGGER DATAWhile there is no doubt that the Joint NationalReadership Survey (JNRS) is a very robust piece ofresearch, the content has been growing less relevant.Alternative sources such as Target Group Index (TGI)are being used to make ‘macro’ planning decisions,given the greater breadth of information availablethrough lifestyle statements and brand consumption.That said, the JNRS data is still the currency by which‘micro’ planning decisions are made, due to the largersample size of the survey. There is a clear need forresearch that combines the robustness of the JNRSwith the flexibility and usability of TGI. Another issuehas been the lack of research that combined the printand digital audiences for news media.

IMPLICATIONThe industry understands the need for change andhas taken positive steps forward. Firstly, it hastackled the digital issue; respondents are now beingasked about their consumption of the print, digital andonline iterations of a title. Top-line results will bereleased in the next survey, with full data available inthe autumn. Initial results are very encouraging,showing what every smart planner suspected;consumption of news is solid; readers are merelychoosing different methods of consumption.

Secondly, the NNI is joining representatives fromRadio, TV, Outdoor and IAPI to explore theintroduction of a cross-media research initiative,which would provide a holistic and robust view ofconsumers’ media behaviours.

The perennial question “why would I pay for contentthat I can get for free?” still needs a decisive industry-wide answer. This is a challenge all publishers mustface, as digital editions become a larger part of theirbusiness. According to the Audit Bureau ofCirculations in the US, digital newspapersubscriptions saw a surge of 63% in 2012. It nowaccounts for 14% of the total circulation mix. Astandardised global payment model needs to be inplace before the end of 2013 if Irish news media areto capitalise on a digital “cover price”.

IMPLICATIONAre Ireland’s readers ready to subscribe to premiumcontent? We think the answer is a resounding “yes”.The proliferation of tablets, consoles and smartphoneshas normalised low-cost digital subscriptions.

Some newspaper titles are having success throughthe introduction of a pay-walled digital & paper model.The New York Times has grown its total paidcirculation by over 40% to 1.6 million. This is splitroughly 50/50 between the digital and paper versions,but from Monday - Friday there are around 25% moredigital subscribers than paper. On Sunday, however,it is reversed with 47% more papers sold than onlinesubscriptions.

With international precedent andlocal appetite, our titles shouldcommit to a standardised paystructure, which will placereal value on the premiumnature of the product.

A recent study by the Annenberg Centre in the USfound most internet users have limited trust in theinformation they find online. Only 40% of users saidthat most or all of the information on the Internetis reliable – a decline from 55% in 2000.

Internet users rated newspapers highly for thequality of news content, the breadth of coverageand the trustworthiness of the reporting.Furthermore, 63% of online users said theywould miss the print edition of their newspaperif it was no longer available, an increase of sevenpercentage points since 2007.

IMPLICATIONThe lack of trust that consumers have in contentthey find online represents the greatestargument for news brands to embrace thedigital challenge. It also makes a clear businesscase for charging users for this trust.

Trust is the most valuable asset that any newsbrand could hope to attain. It takes many yearsto nurture and Irish publishers have it in spades.It is important that they push forward with plansto monetise this competitive advantage whilstthey still have it. In a world of confusion andfragmentation, trust is the most valuablecommodity of all.

02 PAY TO PLAY 03 A MATTER OF TRUST

GLOBAL DEVICE SHIPMENTS

1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12

50,000

100,000

150,000

200,000

250,000

300,000

TABLETS

SMARTPHONES

PCS

NEWSPAPER/MAGAZINE SPEND (€M)

215.5184.0 170.0

27.8

2011 2012 2013

26.5 24.9

ROI NI

TRUST IS THE TRUMP CARD THATNEWS BRANDS HAVE TO PLAY IN

THE DIGITAL FUTURESource: Core Media Estimates Source: Gartner, IDC, Strategy

Analytics company releases

ONLINE

In 2012 investment in online media increased by 14% on an all-Ireland basis, taking 22% shareof total media investment in the Republic, but only 10% in Northern Ireland. The key drivers ofgrowth have been ‘richer’ ad formats (e.g. home page takeovers), video-on-demand and mobile.This growth is set to continue and by 2015 we expect online will be the largest media sector inthe Irish market, commanding 28% share of spend.

The advent of programmatic media buying will gain momentum this year as more Real-TimeBuying (RTB) solutions become available. This will open up new options for direct responseadvertisers to derive stronger return on investment, as these platforms allow for greater targetingand use of campaign data.

Search is still dominated by Google, which accounts for 95% of revenue. Bing has failed to makean impact so far, which is unfortunate because the market needs an injection of competition.

Mobile spend is growing and is likely to reach €4m in ROI this year. The NI market is at anearlier stage of development and investment is likely to remain under €500k in 2013. However,this is just the beginning; by 2016 mobile spend will treble to almost €15m across the island.

2013 will see further growth in the tablet space with increased choice and possibilities. By theend of this year there could be 1.25 million devices in NI & ROI combined.

The growth in social media penetration is leveling off, with over 3 million people on the islandusing at least one of the social networks. However, usage continues to rise as smartphonesopen up the ‘always-on’ culture. Facebook, YouTube and Twitter continue to be pervasive, butwe see discreet audiences building across other networks such as Tumblr, Pinterest andInstagram. For the B2B market Linkedin is still the only game in town, with over 800,000 monthlyusers across the island.

We shouldn’t write off Google+, because the company is determined to position it as the gluethat brings together its interfaces across search, mobile and software. As social contentbecomes more search-friendly expect to see Google+ being used as part of more effective SEOstrategies in 2013.

BY 2015 ONLINE WILL BE THE LARGEST MEDIUM INIRELAND WITH 28% MARKET SHARE

10

11

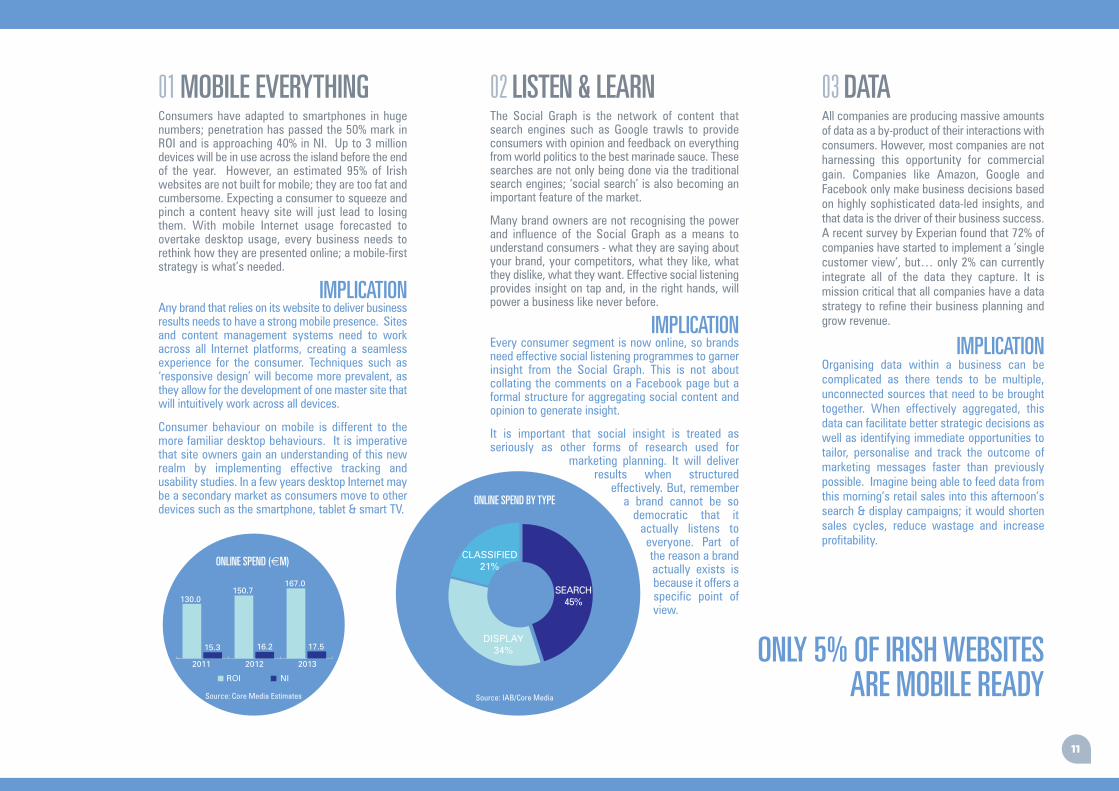

01 MOBILE EVERYTHINGConsumers have adapted to smartphones in hugenumbers; penetration has passed the 50% mark inROI and is approaching 40% in NI. Up to 3 milliondevices will be in use across the island before the endof the year. However, an estimated 95% of Irishwebsites are not built for mobile; they are too fat andcumbersome. Expecting a consumer to squeeze andpinch a content heavy site will just lead to losingthem. With mobile Internet usage forecasted toovertake desktop usage, every business needs torethink how they are presented online; a mobile-firststrategy is what’s needed.

IMPLICATIONAny brand that relies on its website to deliver businessresults needs to have a strong mobile presence. Sitesand content management systems need to workacross all Internet platforms, creating a seamlessexperience for the consumer. Techniques such as‘responsive design’ will become more prevalent, asthey allow for the development of one master site thatwill intuitively work across all devices.

Consumer behaviour on mobile is different to themore familiar desktop behaviours. It is imperativethat site owners gain an understanding of this newrealm by implementing effective tracking andusability studies. In a few years desktop Internet maybe a secondary market as consumers move to otherdevices such as the smartphone, tablet & smart TV.

The Social Graph is the network of content thatsearch engines such as Google trawls to provideconsumers with opinion and feedback on everythingfrom world politics to the best marinade sauce. Thesesearches are not only being done via the traditionalsearch engines; ‘social search’ is also becoming animportant feature of the market.

Many brand owners are not recognising the powerand influence of the Social Graph as a means tounderstand consumers - what they are saying aboutyour brand, your competitors, what they like, whatthey dislike, what they want. Effective social listeningprovides insight on tap and, in the right hands, willpower a business like never before.

IMPLICATIONEvery consumer segment is now online, so brandsneed effective social listening programmes to garnerinsight from the Social Graph. This is not aboutcollating the comments on a Facebook page but aformal structure for aggregating social content andopinion to generate insight.

It is important that social insight is treated asseriously as other forms of research used for

marketing planning. It will deliverresults when structured

effectively. But, remembera brand cannot be sodemocratic that itactually listens toeveryone. Part ofthe reason a brandactually exists isbecause it offers aspecific point ofview.

All companies are producing massive amountsof data as a by-product of their interactions withconsumers. However, most companies are notharnessing this opportunity for commercialgain. Companies like Amazon, Google andFacebook only make business decisions basedon highly sophisticated data-led insights, andthat data is the driver of their business success.A recent survey by Experian found that 72% ofcompanies have started to implement a ‘singlecustomer view’, but… only 2% can currentlyintegrate all of the data they capture. It ismission critical that all companies have a datastrategy to refine their business planning andgrow revenue.

IMPLICATIONOrganising data within a business can becomplicated as there tends to be multiple,unconnected sources that need to be broughttogether. When effectively aggregated, thisdata can facilitate better strategic decisions aswell as identifying immediate opportunities totailor, personalise and track the outcome ofmarketing messages faster than previouslypossible. Imagine being able to feed data fromthis morning’s retail sales into this afternoon’ssearch & display campaigns; it would shortensales cycles, reduce wastage and increaseprofitability.

02 LISTEN & LEARN 03 DATA

ONLINE SPEND BY TYPE

SEARCH45%

DISPLAY34%

CLASSIFIED21%ONLINE SPEND (€M)

130.0150.7

167.0

15.3

2011 2012 2013

16.2 17.5

ROI NI

ONLY 5% OF IRISH WEBSITESARE MOBILE READYSource: Core Media Estimates Source: IAB/Core Media

RADIO

We expect radio to fare better than most media in the Republic of Ireland with 1.5% growth inspend this year, due to its ability to attract revenue from local advertisers, who will becomemore active in 2013. The Northern Ireland market will be less fortunate with spend levels likelyto fall back by 2%.

Despite the small growth in spend in ROI, many stations will continue to struggle financially;we estimate that less than 50% of stations are profitable in the current climate. Thankfully, theBAI has relaxed its 20% rule in relation to news and current affairs content on music-driven/nichestations. Broadcasters such as Phantom and Nova have received approval to reduce theircurrent affairs output to 12% and 10% respectively, whereas Beat’s requirement has fallen to15%. These changes will reduce the overhead burden and improve the flow of programmingacross the day on these stations.

Radio broadcasters in the Republic feel they have been put at a disadvantage since televisioncommercial codes were relaxed in 2011 with the introduction of product placement. They willcontinue to lobby the Broadcasting Authority to permit commercial references to be integratedwithin programming, as is the case in Northern Ireland. We expect the BAI to take theseconcerns on board and make the appropriate changes.

The development of digital broadcasting has stalled in the Republic. Digital, in one guise oranother, will inevitably take over from analogue in the future, but it will be interesting to see ifit’s DAB or internet radio that wins in the long run.

The emergence of internet ‘pure-play’ streaming services is an exciting development that posesa serious threat to the domestic radio sector in the medium term. Traditional radio will endurebecause people want the two-way relationship, but according to research we carried out inJanuary, 18% of regular listeners listen to radio for music, and for no other reason. This is asubstantial minority who are likely to convert to the online option gradually over the next fewyears.

18% OF REGULAR RADIO LISTENERS LISTEN TORADIO FOR MUSIC, AND FOR NO OTHER REASON

12

13

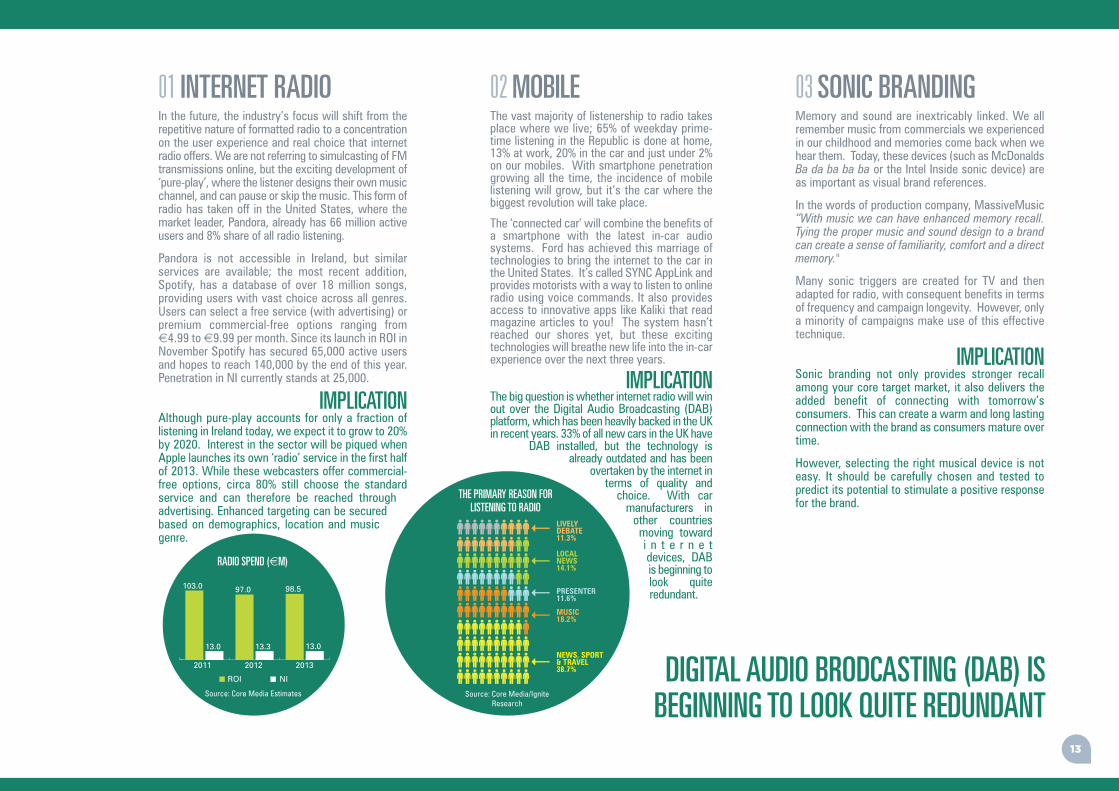

01 INTERNET RADIOIn the future, the industry’s focus will shift from therepetitive nature of formatted radio to a concentrationon the user experience and real choice that internetradio offers. We are not referring to simulcasting of FMtransmissions online, but the exciting development of‘pure-play’, where the listener designs their own musicchannel, and can pause or skip the music. This form ofradio has taken off in the United States, where themarket leader, Pandora, already has 66 million activeusers and 8% share of all radio listening.

Pandora is not accessible in Ireland, but similarservices are available; the most recent addition,Spotify, has a database of over 18 million songs,providing users with vast choice across all genres.Users can select a free service (with advertising) orpremium commercial-free options ranging from€4.99 to €9.99 per month. Since its launch in ROI inNovember Spotify has secured 65,000 active usersand hopes to reach 140,000 by the end of this year.Penetration in NI currently stands at 25,000.

IMPLICATIONAlthough pure-play accounts for only a fraction oflistening in Ireland today, we expect it to grow to 20%by 2020. Interest in the sector will be piqued whenApple launches its own ‘radio’ service in the first halfof 2013. While these webcasters offer commercial-free options, circa 80% still choose the standardservice and can therefore be reached throughadvertising. Enhanced targeting can be securedbased on demographics, location and musicgenre.

The vast majority of listenership to radio takesplace where we live; 65% of weekday prime-time listening in the Republic is done at home,13% at work, 20% in the car and just under 2%on our mobiles. With smartphone penetrationgrowing all the time, the incidence of mobilelistening will grow, but it’s the car where thebiggest revolution will take place.

The ‘connected car’ will combine the benefits ofa smartphone with the latest in-car audiosystems. Ford has achieved this marriage oftechnologies to bring the internet to the car inthe United States. It’s called SYNC AppLink andprovides motorists with a way to listen to onlineradio using voice commands. It also providesaccess to innovative apps like Kaliki that readmagazine articles to you! The system hasn’treached our shores yet, but these excitingtechnologies will breathe new life into the in-carexperience over the next three years.

IMPLICATIONThe big question is whether internet radio will winout over the Digital Audio Broadcasting (DAB)platform, which has been heavily backed in the UKin recent years. 33% of all new cars in the UK have

DAB installed, but the technology isalready outdated and has been

overtaken by the internet interms of quality andchoice. With carmanufacturers inother countriesmoving towardi n t e r n e tdevices, DABis beginning tolook quiteredundant.

Memory and sound are inextricably linked. We allremember music from commercials we experiencedin our childhood and memories come back when wehear them. Today, these devices (such as McDonaldsBa da ba ba ba or the Intel Inside sonic device) areas important as visual brand references.

In the words of production company, MassiveMusic“With music we can have enhanced memory recall.Tying the proper music and sound design to a brandcan create a sense of familiarity, comfort and a directmemory."

Many sonic triggers are created for TV and thenadapted for radio, with consequent benefits in termsof frequency and campaign longevity. However, onlya minority of campaigns make use of this effectivetechnique.

IMPLICATIONSonic branding not only provides stronger recallamong your core target market, it also delivers theadded benefit of connecting with tomorrow’sconsumers. This can create a warm and long lastingconnection with the brand as consumers mature overtime.

However, selecting the right musical device is noteasy. It should be carefully chosen and tested topredict its potential to stimulate a positive responsefor the brand.

02 MOBILE 03 SONIC BRANDING

THE PRIMARY REASON FORLISTENING TO RADIO

LIVELY DEBATE11.3%

LOCAL NEWS14.1%

PRESENTER11.6%

MUSIC18.2%

NEWS, SPORT & TRAVEL38.7%

RADIO SPEND (€M)

103.0 97.0 98.5

13.0

2011 2012 2013

13.3 13.0

ROI NI DIGITAL AUDIO BRODCASTING (DAB) ISBEGINNING TO LOOK QUITE REDUNDANT

Source: Core Media Estimates Source: Core Media/IgniteResearch

OUT OF

HOME

2013 will be another difficult year for out-of-home media. We are forecasting a further declinein revenue of 2% in the Republic and 5% in Northern Ireland.

Significant price reductions are being achieved due to the decline in demand, and while agencieswill continue to put pressure on improvement, we expect media owners to seek yield protectionin 2013. However, the focus will not just be on price; we will keep applying pressure in relationto the quality of plant and no low grade panels will be tolerated. This will result in the industrycontinuing to cull less desirable sites. Billboard inventory decreased by over 6% in 2012 andwe expect a further 4% decrease this year in tandem with an improvement in the presentationand quality of large format panels.

2012 saw the release of the new Dublin Travel Survey, which drives the coverage & frequencymodel for outdoor campaigns. The survey’s new methodology has led to a re-calibration ofcoverage norms for the medium, enabling planners to deliver desired coverage levels whilepurchasing fewer sites. It will be interesting to see the results from the planned Cork TravelSurvey when released later this year.

In addition to delivering improved value and accountability, the OOH sector will have to continueto innovate in order to reverse revenue declines. Alcohol advertising currently accounts forcirca 15% of outdoor revenues, but the imposition of restrictions by the Government may seethis fall further in 2013, potentially leading to an outright ban during 2014. The medium hasfaced challenges like this in the past; the answer is to reinvent and invest in order to make themedium more attractive, flexible and effective.

THE NUMBER OF DIGITAL SCREENS IN ROI WILL GROW TO 1,400 IN 2013

14

15

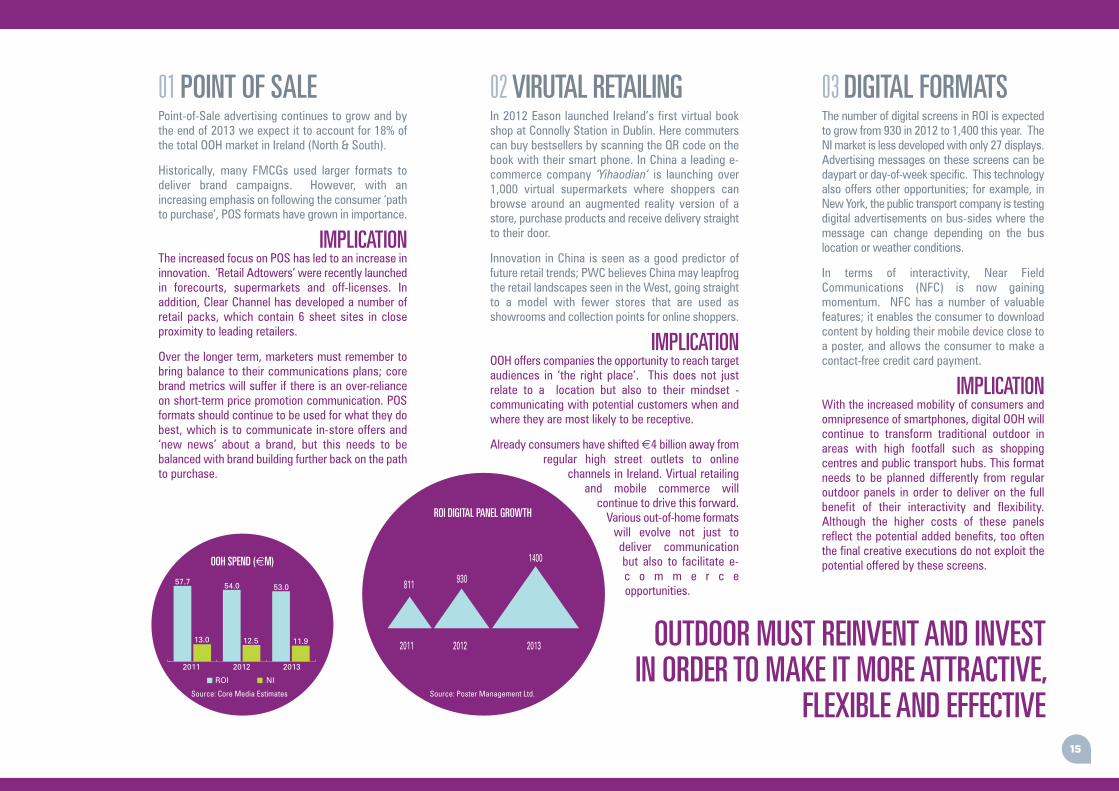

01 POINT OF SALEPoint-of-Sale advertising continues to grow and bythe end of 2013 we expect it to account for 18% ofthe total OOH market in Ireland (North & South).

Historically, many FMCGs used larger formats todeliver brand campaigns. However, with anincreasing emphasis on following the consumer ‘pathto purchase’, POS formats have grown in importance.

IMPLICATIONThe increased focus on POS has led to an increase ininnovation. ‘Retail Adtowers’ were recently launchedin forecourts, supermarkets and off-licenses. Inaddition, Clear Channel has developed a number ofretail packs, which contain 6 sheet sites in closeproximity to leading retailers.

Over the longer term, marketers must remember tobring balance to their communications plans; corebrand metrics will suffer if there is an over-relianceon short-term price promotion communication. POSformats should continue to be used for what they dobest, which is to communicate in-store offers and‘new news’ about a brand, but this needs to bebalanced with brand building further back on the pathto purchase.

In 2012 Eason launched Ireland’s first virtual bookshop at Connolly Station in Dublin. Here commuterscan buy bestsellers by scanning the QR code on thebook with their smart phone. In China a leading e-commerce company ‘Yihaodian’ is launching over1,000 virtual supermarkets where shoppers canbrowse around an augmented reality version of astore, purchase products and receive delivery straightto their door.

Innovation in China is seen as a good predictor offuture retail trends; PWC believes China may leapfrogthe retail landscapes seen in the West, going straightto a model with fewer stores that are used asshowrooms and collection points for online shoppers.

IMPLICATIONOOH offers companies the opportunity to reach targetaudiences in ‘the right place’. This does not justrelate to a location but also to their mindset -communicating with potential customers when andwhere they are most likely to be receptive.

Already consumers have shifted €4 billion away fromregular high street outlets to online

channels in Ireland. Virtual retailingand mobile commerce willcontinue to drive this forward.Various out-of-home formatswill evolve not just todeliver communicationbut also to facilitate e-c o m m e r c eopportunities.

The number of digital screens in ROI is expectedto grow from 930 in 2012 to 1,400 this year. TheNI market is less developed with only 27 displays.Advertising messages on these screens can bedaypart or day-of-week specific. This technologyalso offers other opportunities; for example, inNew York, the public transport company is testingdigital advertisements on bus-sides where themessage can change depending on the buslocation or weather conditions.

In terms of interactivity, Near FieldCommunications (NFC) is now gainingmomentum. NFC has a number of valuablefeatures; it enables the consumer to downloadcontent by holding their mobile device close toa poster, and allows the consumer to make acontact-free credit card payment.

IMPLICATIONWith the increased mobility of consumers andomnipresence of smartphones, digital OOH willcontinue to transform traditional outdoor inareas with high footfall such as shoppingcentres and public transport hubs. This formatneeds to be planned differently from regularoutdoor panels in order to deliver on the fullbenefit of their interactivity and flexibility.Although the higher costs of these panelsreflect the potential added benefits, too oftenthe final creative executions do not exploit thepotential offered by these screens.

02 VIRUTAL RETAILING 03 DIGITAL FORMATS

ROI DIGITAL PANEL GROWTH

OOH SPEND (€M)

57.7 54.0 53.0

13.0

2011 2012 2013

12.5 11.9

ROI NI

OUTDOOR MUST REINVENT AND INVESTIN ORDER TO MAKE IT MORE ATTRACTIVE,

FLEXIBLE AND EFFECTIVE

2011 20132012

811 930

1400

Source: Core Media Estimates Source: Poster Management Ltd.

CINEMA

Much like the latest Twilight instalment, 2012 could be described as a solid sequel to 2011, notbreaking any records but performing respectably. In a year where many media struggled forconsumers and revenue, cinema fared better than most. Overall admissions were down 4% onthe island, with box office receipts down by 3%. Less disposable income and emigration wereblamed by industry insiders. An examination of the figures shows that geographic areasexperiencing higher emigration have suffered more as cinema’s core audience of 18-34 fledthese shores. It is estimated that this age segment shrank by 40,000 in the last year.

In sharp contrast to the audience declines, advertising investment actually increased by 1% inROI, due mainly to significant year-round activity by P&G. Northern Ireland spend was up byalmost 16% because of a major lift in cinema investment across the UK due to the success ofSkyfall. However, this growth will be reversed in both regions in 2013.

Once again the Irish box office charts looked like a Halloween party with superheroes, vampires,hobbits, a sabre toothed tiger and even a teddy bear dominating. Battling it out for top spotwere Christian Bale as Batman and Daniel Craig back as 007; suit and tie won out over capeand cowl as James Bond in Skyfall proved a big a hit with Irish cinema goers, narrowly edgingThe Dark Knight into second place.

The march towards digital continued in 2012. 70% of all screens in the Republic and 90% inNorthern Ireland are now digitally enabled. It is expected that all cinemas will be fully convertedto digital by the end of the first quarter. This is a major step forward considering that only 47%of screens were digital this time last year in ROI and 25% in NI.

ALL CINEMAS WILL BE FULLY CONVERTED TODIGITAL BY THE END OF Q1

16

17

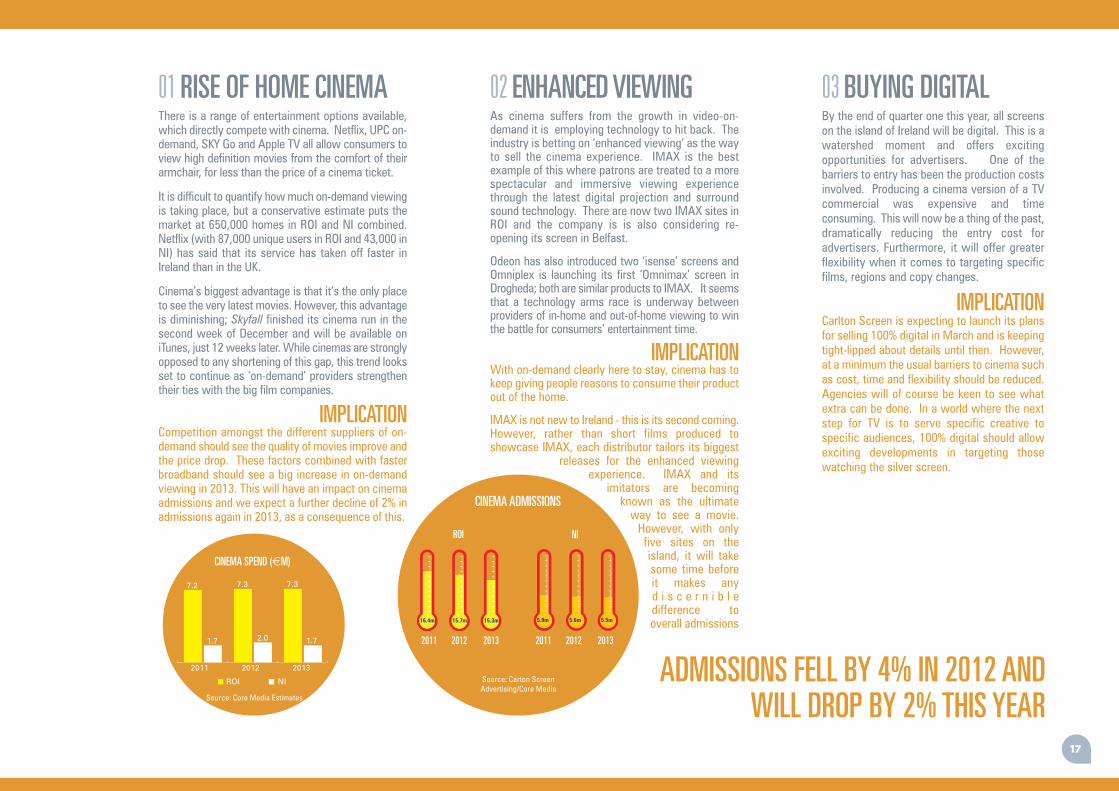

01 RISE OF HOME CINEMAThere is a range of entertainment options available,which directly compete with cinema. Netflix, UPC on-demand, SKY Go and Apple TV all allow consumers toview high definition movies from the comfort of theirarmchair, for less than the price of a cinema ticket.

It is difficult to quantify how much on-demand viewingis taking place, but a conservative estimate puts themarket at 650,000 homes in ROI and NI combined.Netflix (with 87,000 unique users in ROI and 43,000 inNI) has said that its service has taken off faster inIreland than in the UK.

Cinema’s biggest advantage is that it’s the only placeto see the very latest movies. However, this advantageis diminishing; Skyfall finished its cinema run in thesecond week of December and will be available oniTunes, just 12 weeks later. While cinemas are stronglyopposed to any shortening of this gap, this trend looksset to continue as ‘on-demand’ providers strengthentheir ties with the big film companies.

IMPLICATIONCompetition amongst the different suppliers of on-demand should see the quality of movies improve andthe price drop. These factors combined with fasterbroadband should see a big increase in on-demandviewing in 2013. This will have an impact on cinemaadmissions and we expect a further decline of 2% inadmissions again in 2013, as a consequence of this.

As cinema suffers from the growth in video-on-demand it is employing technology to hit back. Theindustry is betting on ‘enhanced viewing’ as the wayto sell the cinema experience. IMAX is the bestexample of this where patrons are treated to a morespectacular and immersive viewing experiencethrough the latest digital projection and surroundsound technology. There are now two IMAX sites inROI and the company is is also considering re-opening its screen in Belfast.

Odeon has also introduced two ‘isense’ screens andOmniplex is launching its first ‘Omnimax’ screen inDrogheda; both are similar products to IMAX. It seemsthat a technology arms race is underway betweenproviders of in-home and out-of-home viewing to winthe battle for consumers’ entertainment time.

IMPLICATIONWith on-demand clearly here to stay, cinema has tokeep giving people reasons to consume their productout of the home.

IMAX is not new to Ireland - this is its second coming.However, rather than short films produced toshowcase IMAX, each distributor tailors its biggest

releases for the enhanced viewingexperience. IMAX and its

imitators are becomingknown as the ultimateway to see a movie.However, with onlyfive sites on theisland, it will takesome time beforeit makes anyd i s c e r n i b l edifference tooverall admissions

By the end of quarter one this year, all screenson the island of Ireland will be digital. This is awatershed moment and offers excitingopportunities for advertisers. One of thebarriers to entry has been the production costsinvolved. Producing a cinema version of a TVcommercial was expensive and timeconsuming. This will now be a thing of the past,dramatically reducing the entry cost foradvertisers. Furthermore, it will offer greaterflexibility when it comes to targeting specificfilms, regions and copy changes.

IMPLICATIONCarlton Screen is expecting to launch its plansfor selling 100% digital in March and is keepingtight-lipped about details until then. However,at a minimum the usual barriers to cinema suchas cost, time and flexibility should be reduced.Agencies will of course be keen to see whatextra can be done. In a world where the nextstep for TV is to serve specific creative tospecific audiences, 100% digital should allowexciting developments in targeting thosewatching the silver screen.

02 ENHANCED VIEWING 03 BUYING DIGITAL

ROI NI

16.4m 15.7m 15.3m

CINEMA SPEND (€M)

7.2 7.3 7.3

1.7

2011 2012 2013

2.0 1.7

ROI NI ADMISSIONS FELL BY 4% IN 2012 ANDWILL DROP BY 2% THIS YEAR

2011 2012 20132011 2012 2013

Source: Core Media Estimates

Source: Carton ScreenAdvertising/Core Media

CINEMA ADMISSIONS

5.9m 5.6m 5.5m

SPONSORSHIP

Last year was a showcase year for Sponsorship with the Olympics and Euro 2012 grabbing theheadlines. P&G’s sponsorship of the Olympics clearly demonstrated the ability of a well-executedplatform to deliver a return at the checkout; its Olympic campaign covered 34 brands and fourmillion stores worldwide and is estimated to have yielded $500m in incremental sales for thecompany.

The key to successful sponsorship is identifying properties that consumers are passionate aboutand showcasing this involvement through the activation of the sponsorship, by providing richexperiences and valuable content. Sponsorship in all its forms (product placement, event, venueand broadcast) is evolving in this direction and the P&G campaign exemplifies this.

Consumer involvement in sponsored events is a major factor in their success. Research byProfessor Tony Meenaghan has shown that increased fan involvement in a sponsored activityevokes a positive emotional response towards the sponsor, but this attribute has not beenuniversally embraced in sponsorship activation; this needs to change.

Naming rights have become popular in recent years; this form of sponsorship can catapult abrand to the top of a consideration table for many consumers. Some major deals have beenstruck including The O2, The Aviva Stadium and Bord Gáis Energy Theatre, all of which areplaying a significant role in customer retention and loyalty programmes for these companies.

However, sponsorship has not been immune to the decline in marketing investment over thepast few years; in 2012 spend fell by 8% to €130m in Ireland (North & South) and we onlyexpect a marginal increase in 2013.

Looking further ahead, spending in this sector will grow substantially as viewers becomeincreasingly able to avoid exposure to TV commercials through the use of Digital Video Recorders(DVRs). In response we will increasingly use sponsorship and product placement to compensatefor the lost commercial impressions.

P&G’S OLYMPIC CAMPAIGN YIELDED $500M ININCREMENTAL SALES FOR THE COMPANY.

18

19

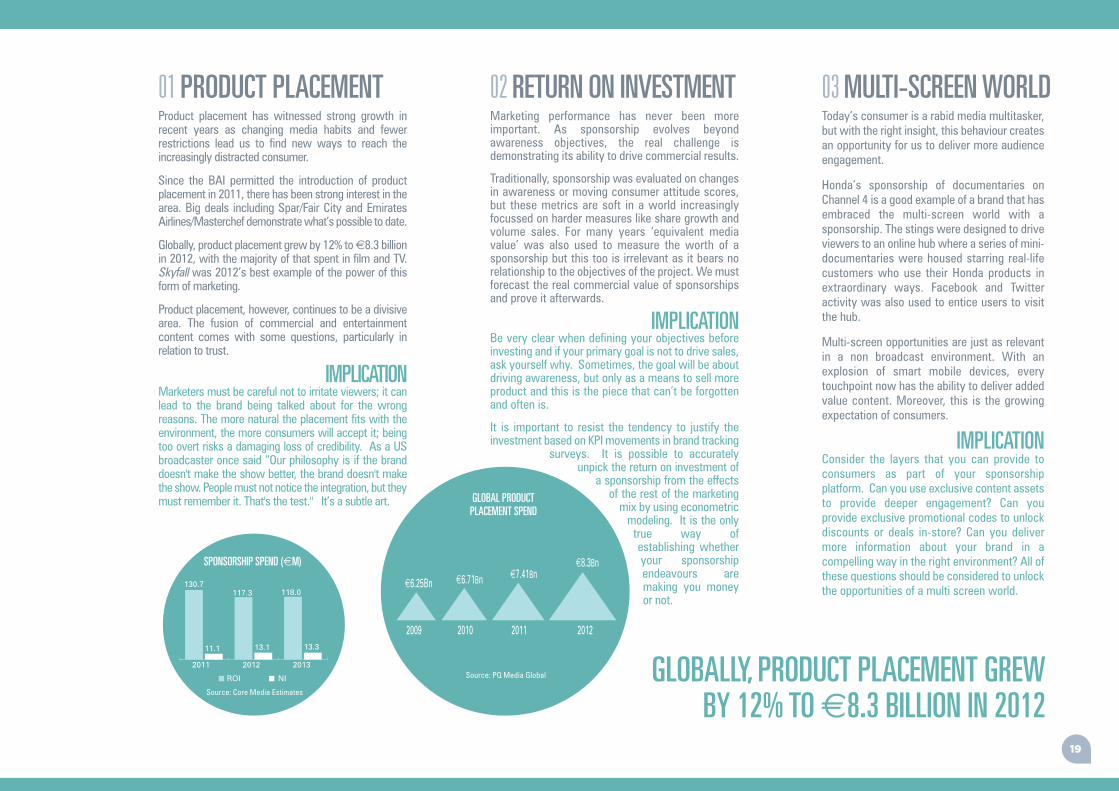

01 PRODUCT PLACEMENTProduct placement has witnessed strong growth inrecent years as changing media habits and fewerrestrictions lead us to find new ways to reach theincreasingly distracted consumer.

Since the BAI permitted the introduction of productplacement in 2011, there has been strong interest in thearea. Big deals including Spar/Fair City and EmiratesAirlines/Masterchef demonstrate what’s possible to date.

Globally, product placement grew by 12% to €8.3 billionin 2012, with the majority of that spent in film and TV.Skyfall was 2012’s best example of the power of thisform of marketing.

Product placement, however, continues to be a divisivearea. The fusion of commercial and entertainmentcontent comes with some questions, particularly inrelation to trust.

IMPLICATIONMarketers must be careful not to irritate viewers; it canlead to the brand being talked about for the wrongreasons. The more natural the placement fits with theenvironment, the more consumers will accept it; beingtoo overt risks a damaging loss of credibility. As a USbroadcaster once said “Our philosophy is if the branddoesn't make the show better, the brand doesn't makethe show. People must not notice the integration, but theymust remember it. That's the test." It’s a subtle art.

Marketing performance has never been moreimportant. As sponsorship evolves beyondawareness objectives, the real challenge isdemonstrating its ability to drive commercial results.

Traditionally, sponsorship was evaluated on changesin awareness or moving consumer attitude scores,but these metrics are soft in a world increasinglyfocussed on harder measures like share growth andvolume sales. For many years ‘equivalent mediavalue’ was also used to measure the worth of asponsorship but this too is irrelevant as it bears norelationship to the objectives of the project. We mustforecast the real commercial value of sponsorshipsand prove it afterwards.

IMPLICATIONBe very clear when defining your objectives beforeinvesting and if your primary goal is not to drive sales,ask yourself why. Sometimes, the goal will be aboutdriving awareness, but only as a means to sell moreproduct and this is the piece that can’t be forgottenand often is.

It is important to resist the tendency to justify theinvestment based on KPI movements in brand tracking

surveys. It is possible to accuratelyunpick the return on investment of

a sponsorship from the effectsof the rest of the marketingmix by using econometricmodeling. It is the onlytrue way ofestablishing whetheryour sponsorshipendeavours aremaking you moneyor not.

Today’s consumer is a rabid media multitasker,but with the right insight, this behaviour createsan opportunity for us to deliver more audienceengagement.

Honda’s sponsorship of documentaries onChannel 4 is a good example of a brand that hasembraced the multi-screen world with asponsorship. The stings were designed to driveviewers to an online hub where a series of mini-documentaries were housed starring real-lifecustomers who use their Honda products inextraordinary ways. Facebook and Twitteractivity was also used to entice users to visitthe hub.

Multi-screen opportunities are just as relevantin a non broadcast environment. With anexplosion of smart mobile devices, everytouchpoint now has the ability to deliver addedvalue content. Moreover, this is the growingexpectation of consumers.

IMPLICATIONConsider the layers that you can provide toconsumers as part of your sponsorshipplatform. Can you use exclusive content assetsto provide deeper engagement? Can youprovide exclusive promotional codes to unlockdiscounts or deals in-store? Can you delivermore information about your brand in acompelling way in the right environment? All ofthese questions should be considered to unlockthe opportunities of a multi screen world.

02 RETURN ON INVESTMENT 03 MULTI-SCREEN WORLD

GLOBAL PRODUCT PLACEMENT SPEND

2009

€6.25Bn €6.71Bn €7.41Bn€8.3Bn

2011 20122010

SPONSORSHIP SPEND (€M)

130.7117.3 118.0

11.1

2011 2012 2013

13.1 13.3

ROI NI GLOBALLY, PRODUCT PLACEMENT GREWBY 12% TO €8.3 BILLION IN 2012

Source: Core Media Estimates

Source: PQ Media Global

DIRECT

MARKETING

In an age where return on investment plays the key role in marketing decision making, knowingwith certainty that you are reaching your intended audience has never been more important.

As a result, the direct marketing industry is faring well with all sectors showing positive growth.Direct marketing now accounts for a third of marketing budgets (up from 28% in 2010), despitethe lack of a post-code system in the Republic of Ireland. Successive governments have madecommitments to introduce national postcodes, but this has met with delay after delay, leavingIreland as the only country in Western Europe without one. In our view the introduction of thissystem will take place in the next 12 months and its arrival will further stimulate the marketthrough the availability of a wider range of targeted services. Knowing exactly who’s receivingyour communications will help reduce wastage for brands and further improve on the relevanceof communications for consumers, leading to a more effective communications channel for all.

In the meantime, there are still a number of strong products available to tailor communicationsto a targeted audience, and the importance of these products will continue to grow. In fact, theability to target a specific audience remains a primary strength of direct mail versus othercommunication channels, including email. Businesses that collect additional information abouttheir customers can develop very personal campaigns through the use of variable data printing.

In recent years the direct marketing sector has seen a shift into digital forms of communicationat the expense of mail, primarily to reduce costs. However, the high volumes of untargeted e-mail and spam have created some antipathy towards e-mail. This has resulted in areassessment of the strength of direct mail and a growth in understanding of how to match themedium with the message. Consumers talk of the need for in-depth, important information tobe sent by post, rather than e-mail. As one USPS customer puts it “E-mail may be the base ofyour communications with me, but I’m getting too much junk. If it’s really important, send it tome by post.”

In 2013, the consumer will increasingly expect direct mail that is relevant to them, specific tothem, and focused on giving them added value.

DIRECT MARKETING NOW ACCOUNTS FOR ATHIRD OF MARKETING BUDGETS

20

21

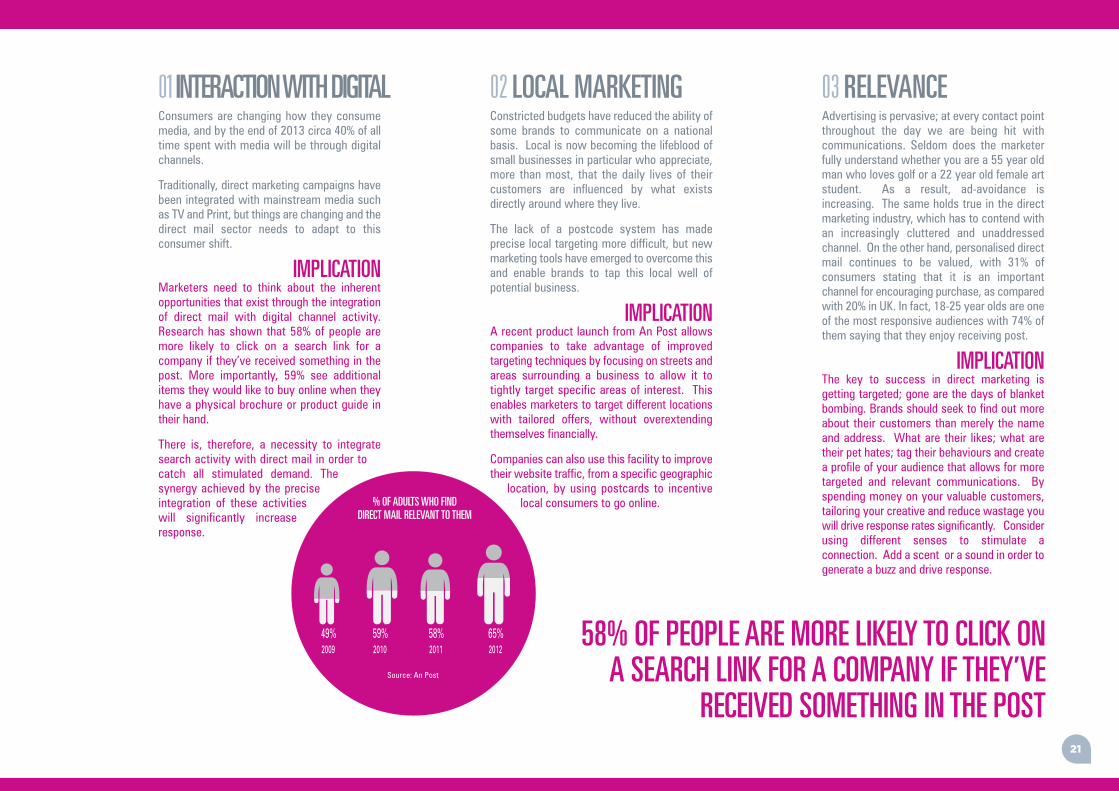

01 INTERACTION WITH DIGITALConsumers are changing how they consumemedia, and by the end of 2013 circa 40% of alltime spent with media will be through digitalchannels.

Traditionally, direct marketing campaigns havebeen integrated with mainstream media suchas TV and Print, but things are changing and thedirect mail sector needs to adapt to thisconsumer shift.

IMPLICATIONMarketers need to think about the inherentopportunities that exist through the integrationof direct mail with digital channel activity.Research has shown that 58% of people aremore likely to click on a search link for acompany if they’ve received something in thepost. More importantly, 59% see additionalitems they would like to buy online when theyhave a physical brochure or product guide intheir hand.

There is, therefore, a necessity to integratesearch activity with direct mail in order tocatch all stimulated demand. Thesynergy achieved by the preciseintegration of these activitieswill significantly increaseresponse.

Constricted budgets have reduced the ability ofsome brands to communicate on a nationalbasis. Local is now becoming the lifeblood ofsmall businesses in particular who appreciate,more than most, that the daily lives of theircustomers are influenced by what existsdirectly around where they live.

The lack of a postcode system has madeprecise local targeting more difficult, but newmarketing tools have emerged to overcome thisand enable brands to tap this local well ofpotential business.

IMPLICATIONA recent product launch from An Post allowscompanies to take advantage of improvedtargeting techniques by focusing on streets andareas surrounding a business to allow it totightly target specific areas of interest. Thisenables marketers to target different locationswith tailored offers, without overextendingthemselves financially.

Companies can also use this facility to improvetheir website traffic, from a specific geographic

location, by using postcards to incentivelocal consumers to go online.

Advertising is pervasive; at every contact pointthroughout the day we are being hit withcommunications. Seldom does the marketerfully understand whether you are a 55 year oldman who loves golf or a 22 year old female artstudent. As a result, ad-avoidance isincreasing. The same holds true in the directmarketing industry, which has to contend withan increasingly cluttered and unaddressedchannel. On the other hand, personalised directmail continues to be valued, with 31% ofconsumers stating that it is an importantchannel for encouraging purchase, as comparedwith 20% in UK. In fact, 18-25 year olds are oneof the most responsive audiences with 74% ofthem saying that they enjoy receiving post.

IMPLICATIONThe key to success in direct marketing isgetting targeted; gone are the days of blanketbombing. Brands should seek to find out moreabout their customers than merely the nameand address. What are their likes; what aretheir pet hates; tag their behaviours and createa profile of your audience that allows for moretargeted and relevant communications. Byspending money on your valuable customers,tailoring your creative and reduce wastage youwill drive response rates significantly. Considerusing different senses to stimulate aconnection. Add a scent or a sound in order togenerate a buzz and drive response.

02 LOCAL MARKETING 03 RELEVANCE

% OF ADULTS WHO FIND DIRECT MAIL RELEVANT TO THEM

49%2009

59%2010

58%2011

65%2012

58% OF PEOPLE ARE MORE LIKELY TO CLICK ONA SEARCH LINK FOR A COMPANY IF THEY’VE

RECEIVED SOMETHING IN THE POSTSource: An Post

FOR MORE INFORMATION PLEASE CONTACT:

ALAN COXTEL: +353 1 649 6458WEB: WWW.COREMEDIA.IEEMAIL: [email protected]

![[2016 Outlook] Media Advertisement](https://img.pdfslide.us/doc/110x75/5881699e1a28ab80508b79b9/2016-outlook-media-advertisement.jpg)