Embed Size (px)

Citation preview

Advance Payment Systems:

Paying Too Much Today and

Being Satisfied Tomorrow

Forthcoming in International Journal of Research in

Marketing, 2015, Vol. 32, Issue 3, 238-250

Fabian Schulz Goethe University Frankfurt

Christian Schlereth WHU – Otto Beisheim School of Management

Nina MazarUniversity of Toronto

Bernd Skiera Goethe University Frankfurt

AdvancePpayment Systems (also referred to as equal billing)

RefundExtra

payment

Usage predic-

tion for billing

cycle

Calculation of

advance pay-

ment rates

Determina-

tion of actual

usage in

billing cycle

Determination

of last billing

rate

1

Advance Payment Systems (APS) are best known for utility services

billing and taxes

e.g., electricity, water, gas… taxes

But APS are applicable to ANY recurring service where consumption and

payments are separated in time

Credit cards balances Cloud computing services Pay-as-you-drive car insurances

2

Also outside of Germany, APS are increasingly advertised by

electricity service providers

Company

Advance

payment

system

offered

Optional or

mandatory

France

EDF Yes Optional

ENI Yes Optional

GDF Suez Yes Optional

Poweo Direct Energy Yes Optional

Germany

EnBW Yes Mandatory

Eon Yes Mandatory

EWE Yes Mandatory

RWE Yes Mandatory

Vattenfall Europe Yes Mandatory

Italy

Acqua Gas Azienda

Municipale No -

Aem No -

Edison SpA No -

Enel No -

Hera Group No -

Spain

EDP Renováveis No -

Endesa Yes Optional

Eon Spain No -

Gas Natural Yes Optional

Iberdrola Yes Optional

UK

EDF Energy Yes Optional

Eon UK Yes Optional

National Grid Yes Optional

RWE npower Yes Optional

Scottish and Southern nergy Yes Optional

Europe US

3

Service providers can choose between three payment systems;

our focus: advance payments

Pros

Small non-

payment

risk

Earlier

cash flow

Low oper-

ational

costs

Customer

loyalty

High Low

Payment

timing

Advance payment

(Predicted usage

paid upfront)

Prepaid

(Usage allowance

bought)

Ex ante

Ex post

Focus of this study

4

Do you remember the feeling you had when filing your last tax return?

Refund Extra payment

Most people have one of the following two reactions:

5

Inconsistent research findings on payment sequence preferences

Pre-pay for

hedonic goods

Payment sequence

preferences for goods

Payment sequence

preferences for taxes

Income sequence preferences

Present

value120.8 118.7

Choice 17% 83%

e.g., Loewenstein & Sicherman (1991)

Guyse et al. (2002)

Read & Powell (2002)

Pos-tpay for

utilitarian goodsTax-payers prefer to pre-pay

Consumers prefer to

• Preference to prepay for hedonic

goods to enjoy consumption as if

it was for free

• Lack of self-control

• Asymmetric penalties

• Alignment with productivity

• Convenience

e.g., Ayers, et al. (1999)

Jones (2012)

Highfill, Thorson and Weber (1998)

e.g., Prelec and Loewenstein (1998)

Patrick and Park (2006)

Re

as

on

Dir

ec

tio

n

Workers prefer rising income

streams

• Different results with regards to direction of payment sequence preferences

• Mainly small experiments in lab (with exception of taxes)

• Consequences on payment sequence preferences in the consumption sphere is unknown

6

Δ: refund (+) or extra payment (-)

b: total yearly bill according to actual consumption

Prospect Theory (e.g., Silverlining principle) is not able to explain

preference for a refund

, 0(b, ) ( (b ))

, 0( )

ifv

if

, 0

(b, ) 1 ( (b )), 0( )

ifv

if

( b) ;

(b, ) max , 0( (b ))

, 0( )

v if

if

7

Research goals: Analyze payment sequence preferences, as well as

causes and consequences

Question 1 Question 2 Question 3

Question

Managerial

implications

Support decision for payment system (sdvance vs. pre-payment vs. post-

payment)

Support decision for advance payment system design

Provide insights into causes for preferences to support offer design and

communication

First paper to examine „irrational behaviour“ in advance payment

sequences and whether customers’ preferences shift with relative

magnitude of last bill

First paper to examine behavioral and attitudinal consequences

First paper to use survey data and billing data

Scientific

contribution

Do preferences for

payment sequences

exist?

Do payment

sequences have

attitudinal

consequences?

Do payment

sequences have

behavioral

consequences?

8

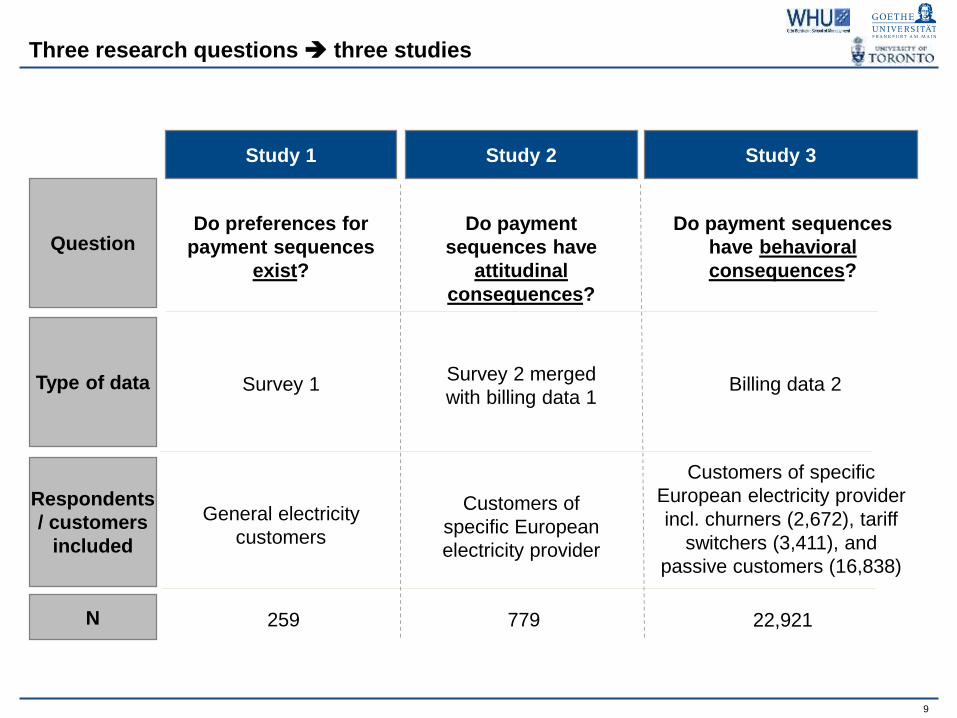

Three research questions three studies

Study 1 Study 2 Study 3

QuestionDo preferences for

payment sequences

exist?

Do payment

sequences have

attitudinal

consequences?

Do payment sequences

have behavioral

consequences?

Type of data

Respondents

/ customers

included

N

Survey 1Survey 2 merged

with billing data 1Billing data 2

General electricity

customers

Customers of

specific European

electricity provider

Customers of specific

European electricity provider

incl. churners (2,672), tariff

switchers (3,411), and

passive customers (16,838)

259 779 22,921

9

Three research questions = three studies

Study 1 Study 2 Study 3

QuestionDo preferences for

payment sequences

exist?

Do payment

sequences have

attitudinal

consequences?

Do payment sequences

have behavioural

consequences?

Type of data

Respondents

/ customers

included

N

Survey 1Survey 2 merged

with billing data 1Billing data 2

General electricity

customers

Customers of

specific European

electricity provider

Customers of specific

European electricity

provider

259 779 22,921

10

Test for preference of payment sequence preference: Survey 1

Methodology: Survey Versions 1 + 2

Alternative 1:

Extra payment

sequence

Alternative 2:

Refund sequence

Monthly

advance

payment

rate

Predicted

extra

payment at

end of year

Monthly

advance

payment

rate

Predicted

refund at end

of year

Version 1:

Equal total

payments

Choice-set 1 (low, low) 45€ 60€ 55€ 60€

Choice-set 2 (high, high) 40€ 120€ 60€ 120€

Choice-set 3 (low, high) 45€ 60€ 60€ 120€

Choice-set 4 (high, low) 40€ 120€ 55€ 60€

Choice experiment set-up:

Which sequence would you prefer for expected yearly electricity bill of 600€?

Version 2:

Higher total

payments

for refund

sequence

Choice-set 1 (low, low) 45€ 60€ 55€ 57.50€

Choice-set 2 (high, high) 40€ 120€ 60€ 115€

Choice-set 3 (low, high) 45€ 60€ 60€ 115€

Choice-set 4 (high, low) 40€ 120€ 55€ 57.50€

Version 3: Low

uncertainty

Version 4: High

uncertainty

11

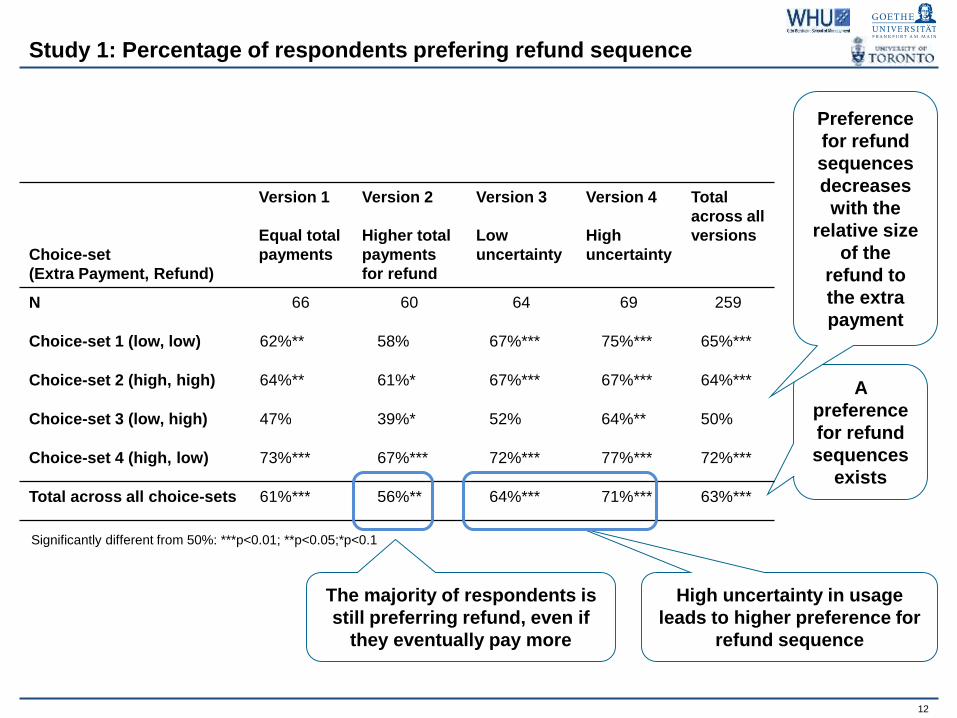

Study 1: Percentage of respondents prefering refund sequence

Significantly different from 50%: ***p<0.01; **p<0.05;*p<0.1

A

preference

for refund

sequences

exists

Preference

for refund

sequences

decreases

with the

relative size

of the

refund to

the extra

payment

The majority of respondents is

still preferring refund, even if

they eventually pay more

Choice-set

(Extra Payment, Refund)

Version 1

Equal total

payments

Version 2

Higher total

payments

for refund

Version 3

Low

uncertainty

Version 4

High

uncertainty

Total

across all

versions

N 66 60 64 69 259

Choice-set 1 (low, low) 62%** 58% 67%*** 75%*** 65%***

Choice-set 2 (high, high) 64%** 61%* 67%*** 67%*** 64%***

Choice-set 3 (low, high) 47% 39%* 52% 64%** 50%

Choice-set 4 (high, low) 73%*** 67%*** 72%*** 77%*** 72%***

Total across all choice-sets 61%*** 56%** 64%*** 71%*** 63%***

High uncertainty in usage

leads to higher preference for

refund sequence

12

Three research questions = three studies

Study 1 Study 2 Study 3

QuestionDo preferences for

payment sequences

exist?

Do payment

sequences have

attitudinal

consequences?

Do payment sequences

have behavioral

consequences?

Type of data

Respondents

/ customers

included

N

Survey 1Survey 2 merged

with billing data 1Billing data 2

General electricity

customers

Customers of

specific European

electricity provider

Customers of specific

European electricity provider

259 779 22,921

13

Impact of payment sequence on attitudes: billing + survey data

Survey data: n=779 (customers of

European electricity provider)Billing data: n=782 (customers of

European electricity provider)

Dependent

variables

+

Price awareness

Likelihood to recommend

provider

Price awareness

-Independent

variable

Refund or extra payment

Relative last billing rate (in % of

total yearly rate)

Control

variables

Timing Customers received last bill at 16th of

a random month in 2011January 2012

Gender

Age

Income

Education

Total electricity spending

Type of contract

Avg. Price / kWh

14

Simple 2 sample comparison already shows impact of payment

sequences on attitudes …

Refund receivers are half as accurate in

their price estimate …

… and more likely to recommend their

provider

% of customers (difference significant at 1% leve)lPrice awareness: Refund receivers vs.

extra payment makers

Average probability to recommend

provider on 10 point scale

38.81%

20.00%

Refund receivers Extra paymentmakers

.

Reading example: People

who received a refund with

their last billing rate over-/

underestimate their monthly

advance payments on

average by 38%

6.446.13

Refund receivers Extra paymentmakers

Note: Extra payment makers: N= 384; Refund receivers: N=398; mean difference significant at 5% / 10% confidence level

45,70%

74,25%

Advance

payments

Yearly

bill

Advance

payments

Yearly

bill

15

… which is confirmed by linearly regressing relative last billing rate

with attitude measures

Model 1: Refund Sequence Dummy

Model

Model 2: Asymmetric Magnitude

Model

Advance

payment

awareness:

Absolute

percentage

error

Yearly bill

awareness:

Absolute

percentage

error

Likelihood of

recom-

mending

provider on

10-point

scale

Advance

payment

awareness:

Absolute

percentage

error

Yearly bill

awareness:

Absolute

percentage

error

Likelihood

of recom-

mending

provider on

10-point

scale

Payment sequence

information

Refund sequence dummy .26*** .28** .31* - - -

Relative magnitude of

refund - - - .74** 3.61*** 2.64***

Relative magnitude of

extra payment sequence- - - -.09 2.23*** .93

Model fitR-square .15 .07 .03 .15 .14 .05

F-Value 13.29*** 5.23*** 2.60*** 11.85*** 10.85*** 3.41***

Number of observations 779 779 779 779 770 779

***p<0.01; **p<0.05;*p<0.1

Note: Control variables not reported due to lack of space Refund sequences

reduce price con-

sciousness

Refund sequences have a

positive influence on likelihood

to recommend the provider

( )

Results of linear regression models

16

Three research questions = three studies

Study 1 Study 2 Study 3

QuestionDo preferences for

payment sequences

exist?

Do payment

sequences have

attitudinal

consequences?

Do payment

sequences have

behavioral

consequences?

Type of data

Respondents

/ customers

included

N

Survey 1Survey 2 merged

with billing data 1Billing data 2

General electricity

customers

Customers of

specific European

electricity provider

Customers of specific

European electricity provider

259 779 22,921

17

Methodology – Question 3: Behavioral consequences

We created a sample of churners, tariff

switchers, and passive customers …

… to calculate impact of payment sequence

How does type of payment sequence affect

odds of churning and tariff switching?

What is effect of magnitude of last billing rate

on odds of churning and tariff switching?

Questions:

Methodology:

Multinomial logit model: Basis=staying passive

Model 1: Dummy for refund sequence

Model 2: Assymetric magnitude model

(absolute of last billing rate/total yearly bill)

All tariff switchers of European

electricity company in 2011:

N= 3,411

Random sample of passive

customers (did not churn, or

switch tariffs) in 2011:

N= 16,838

All churners of European

electricity provider in 2011:

N= 2,672

N= 22,921

18

Payment sequences have significant impact on behavior

More than 50% of churners‘ and tariff

switchers had to make extra payments …

… leading to a significant difference in mean

relative last billing rate

37 4453

63 5647

Churners Tariffswitchers

Passivecustomers

Extrapayment made

Refundreceived

% of customers (difference

significant at 1% level)

% of customers with refunds and extra

payment in last billing rateMean last billing rate in % of total yearly rate

-5.1%

-2.3%

+0.7%Churners

Reading example:

People who churned are those

that had to make an extra

payment of 5% of their total

yearly billing rate to complete

their last billing cycle.

Note: all differences to passive customer sample significant at 1%

Analysis excluding outliers with last billing rate >100% or <-100% of total amount

Tariff

switchers

Passive

customers

19

Results hold if we control for other variables, but high refunds can

also have negative effects

Model 1: Refund

sequence dummy model

Model 2: Asymmetric

magnitude model

Odds-

ratios:

Churn

Odds-

ratios: Tariff

switch

Odds-

ratios:

Churn

Odds-

ratios: Tariff

switch

Payment

sequence

information

Refund sequence dummy 0.627*** 0.788*** - -

Magnitude of refund sequence - - 1.530* 1.708***

Magnitude of extra payment sequence - - 8.489*** 4.187***

Customer

information

Length of customer relationship (in month) 0.878*** 0.883*** 0.879*** 0.883***

Average price per kWh paid (in €) 0.615*** 1.010 0.576*** 0.995

Total usage (in kWh/yr.) 1.076*** 1.060*** 1.075*** 1.060***

Model fit

Nagelkerke's R-Square 0.326 0.328

-2Loglikelihood 28,025 28,076

Chi-Square 6,731 6,777

N 22,921 22,921

H4a/b: Refund sequences

have a negative influence

on churn / tariff switching

probability

Refund sequences have a

negative influence on

churn / tariff switching

probability

High refunds may also

have negative effects,

but effect of high extra

payment 4 x as large

Results of multinomial logit model: three variables (stay passive (basis), churn, switch)

***p<0.01; **p<0.05;*p<0.1

20

Findings & implications

Question 1: Question 2: Question 3:

Question

Preference for

refund sequences

exist and people

are willing to pay

more just to

experience refund.

Preference for

refund sequences

decreases with the

relative size of the

refund to the extra

payment

Findings

Do preferences for

payment sequences

exist?

Do payment sequences

have attitudinal

consequences?

Do payment sequences

have behavioral

consequences?

Refund sequences …

… decrease price

consciousness

… (increase

likelihood to

recommend

provider)

Refund sequences …

… decrease churn

and tariff switching

probability …

… but refunds

should not be too

high

21

Advance payment systems could be a viable

alternative to post-payment or pre-payment

systems

Advance payment rates should be set such

that chance of receiving a refund is increased

However, there is a limit to how much

providers should overcharge

Implications of our research

Managerial implications Theoretical implications

Advance payment systems may be subject to

further research to identify preferences

between different payment systems

Commonly accepted finding that customers

show more "rational" payment timing

preferences for utilitarian goods (Prelec &

Loewenstein, 1998; Patrick & Park, 2006)

does not hold in advance payment systems

22

Managerial Implication: Purposely aim for refunds!

Last billing rate in % of total amount due**

* Note: Change = Refund / 11 such that 11*monthly advance payment equals total billing rate for 1 year

** Source: Customer sample from survey 2 (cut-off at +/- 100%): N=840

… mostly leading to a zero-centered

distribution of last billing rate

Single customer

example

Last billing rate in

2011-€190

Change of

monthly advance

payment for 2012*

-€18

Advance payments are adjusted

every year….

Increase in advance payment rate 5% (i.e., 3.45€ per month on average)

Share of customers receiving a refund 70%

Decrease in churn 7.7%

23

![WHO | World Health Organization - IRAQ · satisfied' or 'Very satisfied' at question '5 [q111]' (Are you satisfied with the frequency of cluster meetings?) Answered: 51 Skipped: 1](https://img.pdfslide.us/doc/110x75/5f616a76e5f1367b116a92fc/who-world-health-organization-iraq-satisfied-or-very-satisfied-at-question.jpg)