Embed Size (px)

Citation preview

TheBusinessCaseforDigitally-EnabledSmallholderFinance

NairobiWorkshop

9 September2016

Disclaimer:ThecontentsofthisdocumentwerepresentedduringaworkshopofkeystakeholdersintheLab’sthen-ongoingstudyontheBusinessCaseforDigitally-EnabledSmallholderFinance.Theyweredesignatedpreliminaryfindings,andpresentedforvalidation.Thispresentationisprovidedforinformationalpurposesonly.Forfurtherquestionsregardingthisstudy,pleasecontactus at:www.raflearning.org

2

Workshopoverview

• OnSept9,2016,theMasterCardFoundation(MCF)andtheRuralAgricultureFinanceLearningLaborganizedahalf-dayworkshopforanaudienceof~30MCFpartners,sub-grantees,digitalserviceproviders,andothersectordonors

• TheworkshopfeaturedapresentationofthefindingsofinitialMCF/LearningLabresearch,supportedbyDalberg,ontheroleofdigitalizationincost-effectivelyprovidingsmallholderfinance,withafocusontheimpactofdigitalizationofSHFcreditproductsandprocessesonfinancialserviceprovider(FSP)profitability,basedonextensivedeskresearch,sectorinterviews,andasurveyofasignificantsampleofMCFgranteesandsub-granteeswhoaretodayinvolvedinatleastpartlydigitalizeddeliveryoffinancialservicestosmallholders

• Theobjectivesoftheensuingdiscussionduringtheworkshopwereon(i)validatingemergingfindingswithkeysectorstakeholders,(ii)sharingexperiencetodateandmorefullyexploringthechallengesforbroaderdigitalizationofsmallholderfinance,(iii)exploringtheinvestmentprioritiesofdifferenttypesofsectorplayerswheredigitalizationisconcerned,and(iv)collectingfeedbackonthesupportrequiredbythesectortostrengthenthebusinesscasefordigitalizationandrelieveotherbottleneckstosmallholderfinancedigitalization

• Thediscussionvalidatedthebroadfindingsofthestudy,suggestedthatadditionalinvestmentintounderstandingtheROIfordigitalizationcouldbenefittheSHFfinancingcommunity,andviaarichdiscussionsurfacedanumberofadditionalchallengesandopportunitiesfordigitalization.

• Thisdocumentincludedtheworkshoppresentationandcapturesthekeypointsandlearningsfromtheworkshopdiscussions.

• PleasecontacttheLabformoreinformationat:www.raflearning.org oronTwitter@raflearning

Source:Workshopfeedback;Dalberganalysis

3

Workshopobjectivesandpresentationcontents

Objectives• Sharestudyfindings• Facilitatesharingoflessonslearnedamongkeyplayersindigitally-enabledsmallholderfinance• Identifyfurtherdigitalizationbarriersandfostercollectiveproblem-solvingtosurmountthem• IdentifyfurtherresearchneededandnextstepstobuildarobustbusinesscasebothforservingSHFandforinvestingindigitalizationtodoso

Contents(Sectionsofthisdocument)• Readoutofpreliminaryfindings• Q&Aandopendiscussionoffindings• Breakoutsessionswithdiscussionsummary– Session1:Sharingexperiences/lessonslearnedondigitalization(35min)– Session2:Groupexerciseondigitalizationinvestment(30min)– Plenaryonpathforwardandwrapup(25min)

• Annex:AdditionalData

Readoutofpreliminaryfindings

5

• Laythegroundworktodeterminehowdigitalizationcanenableproviderstomoreprofitablyandsustainablyservesmallholderfarmers(SHFs)

Goal

Objectives

• BuildaninitialknowledgebaseofthecurrentandprojecteduseofdigitaltoolsbyFSPsservingSHFs

• BegintoexploretheimpactofdigitalizationonthefinancialperformanceofFSPs

• Identifykeyconstraintstodigitalizationandareasofopportunitytoacceleratedigitalintegration

• Identifyrequirementsforbuildingoutamorerobustbusinesscasefordigitalizationoverthecomingyears

ThestudyobjectivesweretounderstandhowFSPsusedigitaltoolstoserveSHFandexplorehowdigitalizationimpactstheirperformance

6

Wehavesurveyed23financialserviceproviders,asasampleofbroaderecosystem,tobuildoninsightsfromdeskresearchandDSP,funder,andexpertconsultations

Surveyed23FinancialServiceProviders

InterviewedSHFExpertsandDigitalServiceProviders

SpokewithmultipleMCFPartners1 2

3

• 4commercialbanks• 4bankmicrofinanceinstitutions• 7non-bankmicrofinanceinstitutions• 4agribusinesses• 3nichenon-bankfinancialinstitutions• 1mobilenetworkoperator

Thankyoutothoseofyouwhoparticipated!

7

ThestudyexamineshowdifferenttypesofFSPsareintegratingdigitalalongthevaluechainandstartstomakethebusinesscasefordigitalization

KeyresearchquestionsStudysections

Who

What

How

Businesscase

Challenges

WhatdifferenttypesofFSPsservingSHFareintegratingdigitaltools?

Whatfunctionsalongthevaluechainhavetheydigitalized?HowdoesdigitalizationcompareacrossdifferentFSPtypes?

HowdoFSPsfacilitatethedigitalizationprocess?

Towhatextentandhowdoesdigitalizationimprovefinancialperformance?

Goingforward,whatchallengesdoFSPsfaceinintegratingdigitaltools?

Opportunities Whatdothesefindingsimplyaboutpotentialopportunitiesforkeyactorstocatalyzeprogressinthisspace?

8

Surveyrespondentscanbemappedinto4different“digitalizationprofiles”basedonnumberofdifferentproductstheyofferandtheirlevelofintegrationofdigitaltools

Lessthan1,000farmersserved

1,000– 10,000Farmersserved

10,000– 25,000farmersserved

25,000– 100,000farmersserved

Over100,000farmersserved

Legend

Creditonly

Producto

fferin

g

Digitalintegrationalonglendingvaluechain

Low High

End-to-Endfinancialsolution1

TraditionalMFIs.TraditionalMFIsleveragingdigitalforloananalysis

Agribusinesses.Agribusinessesleveragingdigitalpaymentsanddigitalizingdatacollectionandloananalysistoevaluatefarmerrisk

HighTechBanks/NicheNBFIs.HightechcommercialbanksandnicheNBFIsofferingfullydigitalfinancialservices.

CommercialBanks/InnovativeMFIs.InnovativeMFIsandcommercialbanksequippingfieldagentswithmobiledevicesandpartneringwithB2Bdigitalservicesproviderstoofferpaperlessandcashlessendtoendsolutions

Who

What

How

Busin

essc

ase

Challenges

Opp

ortunitie

s

9

HighTechBanks/NicheNBFIsandCommercialBanks/InnovativeMFIshavefullydigitalizedvaluechains,whileotherprofileshaveprimarilydigitalizedloananalysis

HighTechBa

nks/

Niche

NBFIs

CommercialBanks/

Inno

vativ

eMFIs

Tradition

alMFIs

Agrib

usinesses

CustomerRelationshipManagement1

CustomerRegistration

LoanAnalysis CashFlows Delivery ofSupportServices

Organization 1Organization 2Organization 3Organization 4Organization 5Organization 6Organization 7Organization 8 N/A

Organization 9Organization 10Organization 11Organization 12Organization 13 N/A

Organization 14Organization 15Organization 16Organization 17Organization 18Organization 19Organization 20Organization 21Organization 22Organization 23

FullydigitalizedLessdigitalized

Notdigitalized

N/A Nosupportservicesoffered

1. CustomerRelationshipManagementincludesSales&MarketingSource:RAFLLBusinessCaseSurvey&Dalberganalysis

Who

What

How

Busin

essc

ase

Challenges

Opp

ortunitie

s

10

OverathirdofrespondentspartnerwithDSPstofacilitatedigitalizationoftheiroperations,75%ofthosewhopartnerwithDSPsuse“integrators”

23

2

2

2

2

2

7

2

1

UsingseparateDSPstodigitalizeeachfunction

1

Usinganintegratorto

digitalizemultiplestepsatonce

Total#respondents

6

Developingtheirownproprietary

systems

4

1

Usingpre-existingappsandsoftware

1

11

Digitalizefunctionsinternally Utilizeexternalpartnerstodigitalize

Source:RAFLLBusinessCaseSurvey&Dalberganalysis

Numberofsurveyrespondentsbymethodofdigitalization

CommercialBanks/InnovativeMFIs

HighTechBanks/NicheNBFIs

AgribusinessesTraditionalMFIs

Who

What

How

Busin

essc

ase

Challenges

Opp

ortunitie

s

11

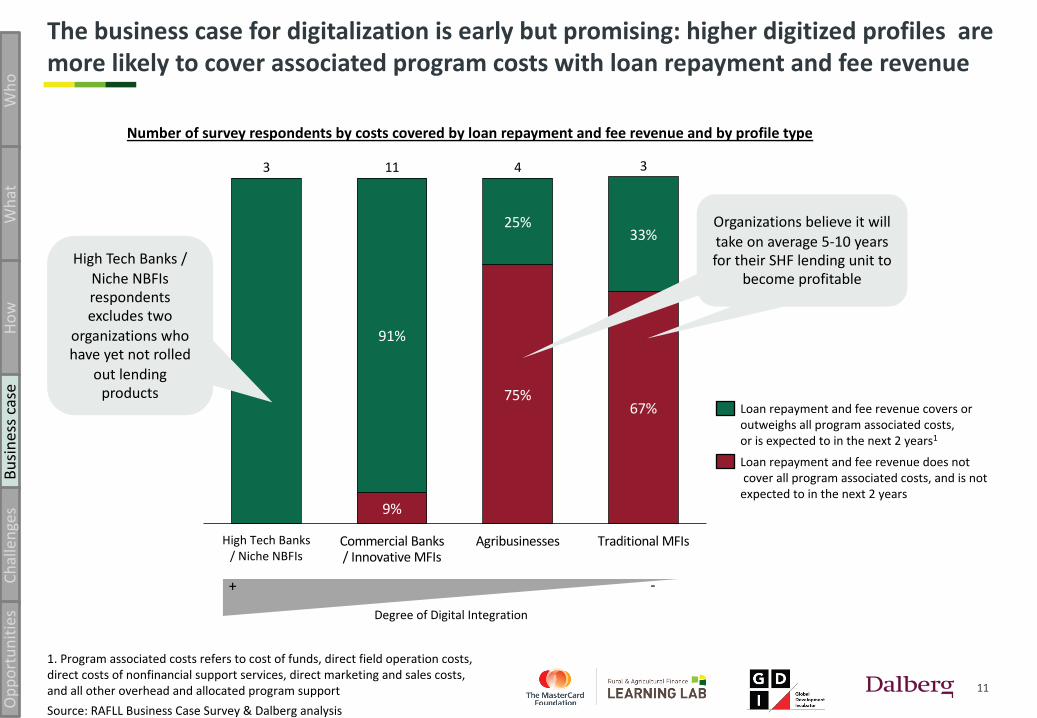

Thebusinesscasefordigitalizationisearlybutpromising:higherdigitizedprofilesaremorelikelytocoverassociatedprogramcostswithloanrepaymentandfeerevenue

Numberofsurveyrespondentsbycostscoveredbyloanrepaymentandfeerevenueandbyprofiletype

9%

67%

91%

33%

75%

25%

3 11

HighTechBanks/NicheNBFIs

CommercialBanks/InnovativeMFIs

TraditionalMFIs

34

Agribusinesses

Loanrepaymentandfeerevenuecoversoroutweighsallprogramassociatedcosts,orisexpectedtointhenext2years1

Loanrepaymentandfeerevenuedoesnotcoverallprogramassociatedcosts,andisnotexpectedtointhenext2years

DegreeofDigitalIntegration

+ -

1.Programassociatedcostsreferstocostoffunds,directfieldoperationcosts,directcostsofnonfinancialsupportservices,directmarketingandsalescosts,andallotheroverheadandallocatedprogramsupportSource:RAFLLBusinessCaseSurvey&Dalberganalysis

HighTechBanks/NicheNBFIsrespondentsexcludestwo

organizationswhohaveyetnotrolled

outlendingproducts

Organizationsbelieveitwilltakeonaverage5-10yearsfortheirSHFlendingunitto

becomeprofitable

Who

What

How

Busin

essc

ase

Challenges

Opp

ortunitie

s

12

Thereisaconsensusamongorganizationsthatintegratingdigitaltoolswillincreaseprofitability

Organizationsbelieveincreasingdigitalizationwillimproveprofitability...

DegreeofDigitalIntegration

+ -

1.RespondentwhoalreadyhasafullydigitalizedlendingvaluechainSource:RAFLLBusinessCaseSurvey&Dalberganalysis

20%

30%

67%

60%70%

33%

50%

50%

TraditionalMFIs

3

CommercialBanks/InnovativeMFIs

11

HighTechBanks/NicheNBFIs

20%1

5

Agribusinesses

4

NeitherAgreenorDisaggreeStronglyAgree Agree

• 83%ofallrespondentsclaimeddigitalizationwillreducethecosttoserveand/orincreaseportfolioquality

• Only17%mentionedrevenuebenefits

“Digitaltoolscanhelpusidentify,classify,andassessfarmersbetterpriortolending.Thiswillreduceour

creditrisk”-Commercialbank

“Digitaltoolswillreducetransportationcosts,recoveryfees,inputcosts,analysiscosts,andreduce

riskslinkedtocreditanalysis”-BankMFI

…primarilybydecreasingcostsand/orreducingrisk

Who

What

How

Busin

essc

ase

Challenges

Opp

ortunitie

s

13

Surprisingly,FSPswhohavemeasuredtheimpactofintegratingdigitaltoolsseemorevaluefromincreasingtheaddressablemarketthanfromreducingthecosttoserve

Numberofsurveyrespondentsbyimpactofintegratingdigitaltoolsandbyprofile

Source:RAFLLBusinessCaseSurvey&Dalberganalysis

1 1

1

3

1

1

11

IncreaseportfolioqualityIncreaseinloanofficercaseload

2

Decreaseloandisbursalcost

2

Increaseincustomerportfolio

4

Decreasecustomeracquisitioncost

AgribusinessesCommercialBanks/InnovativeMFIs

TraditionalMFIsHighTechBanks/NicheNBFIs

Increasedrevenue Decreasedcost Reducedrisk

• 6/7sawanincreaseinrevenue

• Customerportfoliogrewbetween25-50%

• Loanofficercaseloadincreasedbetween30-60%

• 3/7sawadecreaseinthecosttoserve

• Customeracquisitioncostdroppedby25-40%

• Costofdisbursingloansdroppedbyupto80%

Who

What

How

Busin

essc

ase

Challenges

Opp

ortunitie

s

14

ThisisconsistentwithwhatexpertsandDSPshaveexperienced(1/2)

Digitalizationseentodrive

valuethroughportfoliogrowth

Dataisthekeylevertoincreasing

FSPs’addressablemarketcostefficiently

Source:DalberginterviewswithexpertsandDSPs

Keylearnings

• Earlyevidencesuggestsportfoliogrowthisthekeyvaluedriverbehinddigitalinvestments

• PortfoliogrowthisparticularlyimportantforcommercialbanksandMNOswhichhavetighterinvestmenthorizons

• Alternativedataopensupnewmarketsbyunlockinginformationonborrowerspreviouslyconsideredtoorisky/expensivetoserve• However,thetypeofdatausedtodaycontinuestobelimitedandnotasrelevantforSHFlending

• Modelsthatown(oreffectivelyaccess)thedataneededtomakeSHFcreditsolutionsviablewillcapturethemostvalue

“Mostofthebenefitscomefromincreasingcustomerdeposits…foraleadingfinancialinstitutionwehavebeenabletoincreaseactivecustomerbasedfrom

12K-53Koveraperiodof18months…Volumeiskeytorecoupingthedigitalinvestment”-DSP

“CommercialbanksandMNOstargetprimarilyportfoliogrowth”–DSP

“Dataopensnewmarkets..Weexpect[anMFI]toincreaseitsSHFportfoliofrom2%to8%byusingour

digitalcreditscoringservices”-DSP

“Currently,[airtime]dataisownedbyMNOsandthatiswhytheyhavetheabilitytoextendcredit

cheaply…howevertheyareyettohavetherightdatatoproperlyunderstandthecreditriskoflendingto

smallholderfarmers”-Digitalfinanceexpert

“Data.Data.Data.Themoredataweareabletocapturethefurtherdownwecanget”–DSP

Summary

Who

What

How

Busin

essc

ase

Challenges

Opp

ortunitie

s

15

ThisisconsistentwithwhatexpertsandDSPshaveexperienced(2/2)

Digitaltoolsdeliver

additionalrevenue

benefitsbyenablingcustomer-centricproducts

Costsavingsandportfolioqualityare

moresignificantfor

highertouch/smallerorganizations

Source:DalberginterviewswithexpertsandDSPs

• DigitaltoolsallowFSPstomeetcustomerneedseffectivelyandimprovethecustomerexperience

• Customercentricproductsincreaseuserengagementandproduct“stickiness”,drivingloanrepaymentrates,repeatborrowing,upselling/cross-sellingandultimatelycustomerlifetimevalue

• Hookingcustomersiskey:SHFswhoborrowtheirfirstloanwithanFSParehighlylikelytocontinuetoborrowwiththesameFSP

• Highestcostsavingscomefromreducedcustomeracquisitioncosts

• Reducingcostsandfarmerrisksisparticularlysignificantforhighertouchinstitutionsoperatingintightmarginsandservinghigherriskfarmers

“Financialservices,ifdoneright,canbeextremelysticky.Youhavetolookatthefirstfinancialproduct

asmarketing,and thinkintermsofcustomerlifetimevalue.Ifyoustarttherelationshipoffright,the

customersaremorelikelytorepayandcomeback.”-DSP

“Juhudi hadpreviouslytriedSMSrepaymentremindersthatdidn’twork.Usingourplatformtoadd

targetedinformationalcontentincreasedcustomerengagement.Webuildaffinityforthecompany

whichactuallydrivesusageandrepayment.”-DSP

“Wehadacustomerwhohadan11dayidentityverificationprocess;wetookitdownto22secondswithouthavingtosendpeopleouttothevillage”

-DSP“MFIsaremoreopentousingourtechnologybecausetheyarebeingpushedforprofitabilityandwantto

reducecostsandhaveabiggerimpact.”-DSP

SummaryKeylearnings

Who

What

How

Busin

essc

ase

Challenges

Opp

ortunitie

s

16

Goingforward,playersintendtoincreasedigitalusesacrossthelendingvaluechain,withaslightpreferencefordigitalizationofcashflowsandloananalysis

Numberofsurveyrespondentsbyintendeddigitaltoolimplementationandbydigitalizationprofile

1.DigitalcustomerrelationshipmanagementincludesSales &MarketingSource:RAFLLBusinessCaseSurvey&Dalberganalysis

42 2 2

3

3 2 3

1

10

11

1010

9

44

4 3

3

1Digitalcashflows

14

Digitalloananalysis Digitaldeliveryofsupportservices

Digitalcustomerregistration

Digitalcustomerrelationshipmanagement1

18

20

18

21

AgribusinessesTraditionalMFIs

HighTechBanks/NicheNBFIsCommercialBanks/InnovativeMFIs

Who

What

How

Busin

essc

ase

Challenges

Opp

ortunitie

s

17

Respondents’perceivedobstaclestoincorporatingdigitalrelatetohighupfrontcostsandlackofinternalcapabilities

Source:RAFLLBusinessCaseSurvey&Dalberganalysis

Numberofsurveyrespondentsbyperceivedobstaclestodigitalimplementationandbyprofile

2 13 2

21

1

21

11

6

7

8 7 6 4

2

13

11

1

8

Lackofcustomermobilephone

access

Highinitialinvestment

17

Lackofinternalcapabilities

11

Toodrasticofaprocesschange

11

Lackofknowledgeonbesttools

98

Lackofproofofvalue

Transactionfeestoohigh

9

HighTechBanks/NicheNBFIsCommercialBanks/InnovativeMFIs

AgribusinessesTraditionalMFIs

Cost-related InternalCapabilities CustomerEcosystem

Who

What

How

Busin

essc

ase

Challenges

Opp

ortunitie

s

18

Organizations’obstaclesmirrorchallengesencounteredbyDSPstoclosepartnershipswithFinancialServiceProviders(1/2)

Highupfrontcosts

Source:DalberginterviewswithexpertsandDSPs

“Wearefacingacostproblem.It’squiteexpensivetogetabanktosetuptheplatform.Itcosts$16k-$70k

tosetup,and$300monthlyperbranch”-DSP

“Therelativecostofdigitalvariessubstantiallyfordifferentactors.MNO-ledmodelsalreadyhavethe

infrastructureinplacewhilebankshavetopaytosetupthisinfrastructure.”–Digitalfinanceexpert

Summary

Lackofinternal

capabilities

“MFIsareopentousingtechnologybecausetheywanttoreducecostsbuttheylackthecapabilities.”-DSP

“Outtechnologyistheunderwritingbuttouseityouneedthewholedigitallendingstackinplace.The

smallerplayersneedintegratedofferings…youreallyneedtoworkhand-in-handwiththem.That’saconstrainingfactor,wejustcan’taffordit”-DSP

• TraditionalMFIsandlesstech-savvyorganizationslacktheinternalcapabilitiesandcapacitytoimplement,integrateandmanagedigitaltools• Theseorganizationsrequireintegratorswhocanworkcloselywiththemtodigitalizetheircorebankingsystemsbeforedigitalizingotherfunctionsalongthelendingvaluechain

• ThehighupfrontcostchallengestheDSPs’abilitytoselltheirproductstoFSPs

• Thiscostburdenishighestforlowervolumeplayers/thosethatdonotalreadyhavedigitalprocessesinplaceasitrequiresorganizationstocreateentirelynewinfrastructureandprocessestoadoptnewtools

Keybarriers

Who

What

How

Busin

essc

ase

Challenges

Opp

ortunitie

s

19

Organizations’obstaclesmirrorchallengesencounteredbyDSPstoclosepartnershipswithFinancialServiceProviders(2/2)

Lackofdigitalliteracy

Source:DalberginterviewswithexpertsandDSPs

• Risk-aversecommercialbanksrequireproofofimpact onprofitability/portfolioqualitybeforeinvesting

• Provingthebusinesscaseisparticularlychallenginginanascentfieldwhereprofitabilitydatahasyettobecollected

• Valueofdigitaltoolsislikelycorrelatedwithdigitalliteracyoftheendcustomer

• Goingcashlessisparticularlyexpensiveinunderdevelopedmobilemoneyecosystems;customereducationiskey

• Digitalizationofsupportservicesisparticularlychallengingwithlesstechsavvycustomersandwillcontinuetorequirehumaninteraction

“Customersaremuchmorecomfortablegivingcashtoagentsthanusingmobilemoney.We’veinvestedalot

inchangingcustomerbehaviorbutdigitalrepaymentsarenotgrowingasmuchaswe

expected.Customertrainingisexpensiveandtakesalotoftime.”-DSP

“Forfinancialliteracytraining,therehastobeahumancomponentsomewhere.Digitalizing

everythingisunrealisticgivenourtargetcustomer.”-DSP

Summary

Moreproofofvaluerequired

“CommercialBanksendupsaying‘let’sseemorenumbers,let’sseeatrackrecord.’Theywanttoseea

testedmodel.Thechallengeisbuildingthatmodelcantakeyears.”-DSP

“Understandingtheimpactonprofitabilityisvital.BankswhattheROIis,weneedtomakethebusiness

caseforthem”-DSP

“Therearealotofearlystageinterventionsthatarestillinthedatacapturestage.FSPsmightnottrustthedatayetorknowwhattodowithit.”-Digital

financeexpert

Keybarriers

Who

What

How

Busin

essc

ase

Challenges

Opp

ortunitie

s

20

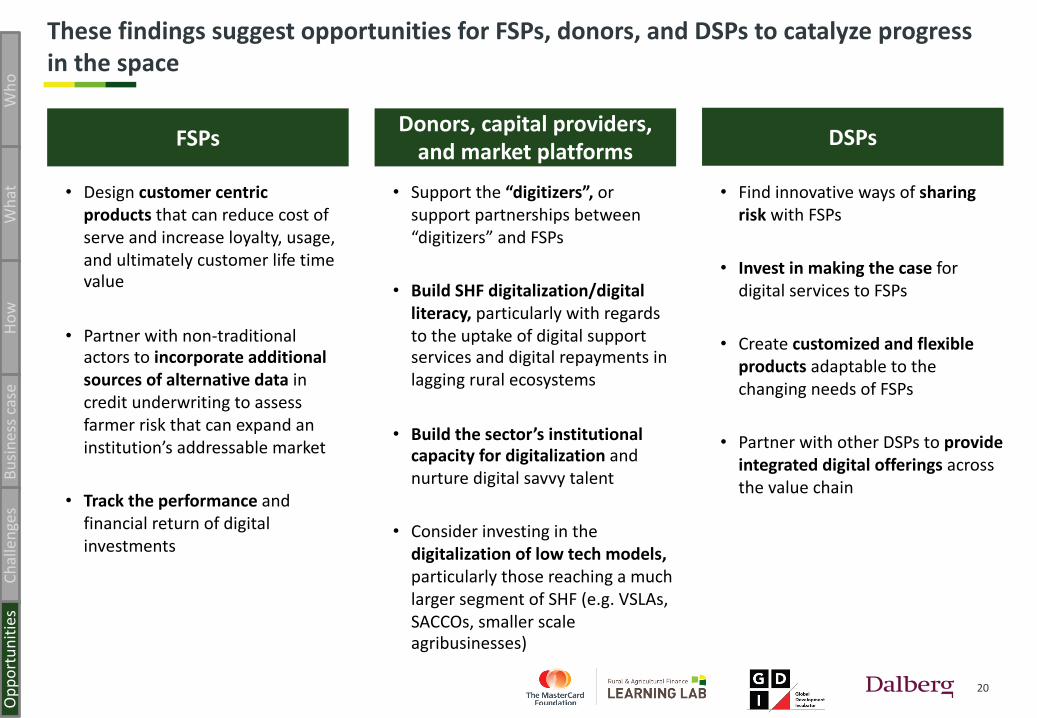

ThesefindingssuggestopportunitiesforFSPs,donors,andDSPstocatalyzeprogressinthespace

• Designcustomercentricproducts thatcanreducecostofserveandincreaseloyalty,usage,andultimatelycustomerlifetimevalue

• Partnerwithnon-traditionalactorstoincorporateadditionalsourcesofalternativedataincreditunderwritingtoassessfarmerriskthatcanexpandaninstitution’saddressablemarket

• Tracktheperformanceandfinancialreturnofdigitalinvestments

Who

What

How

Busin

essc

ase

Challenges

Opp

ortunitie

s

FSPs Donors,capitalproviders,andmarketplatforms DSPs

• Supportthe“digitizers”,orsupportpartnershipsbetween“digitizers”andFSPs

• BuildSHFdigitalization/digitalliteracy,particularlywithregardstotheuptakeofdigitalsupportservicesanddigitalrepaymentsinlaggingruralecosystems

• Buildthesector’sinstitutionalcapacityfordigitalizationandnurturedigitalsavvytalent

• Considerinvestinginthedigitalizationoflowtechmodels,particularlythosereachingamuchlargersegmentofSHF(e.g.VSLAs,SACCOs,smallerscaleagribusinesses)

• FindinnovativewaysofsharingriskwithFSPs

• InvestinmakingthecasefordigitalservicestoFSPs

• CreatecustomizedandflexibleproductsadaptabletothechangingneedsofFSPs

• PartnerwithotherDSPstoprovideintegrateddigitalofferings acrossthevaluechain

Q&Aandopendiscussionoffindings

22

Fordiscussion

• Whatoverallquestions,reactions,orfeedbackdoyouhaveonourpreliminaryfindings?

• IstheemergingtypologyofdigitalsmallholderFSPmodelsuseful?

• HavewecorrectlycapturedthemajortrendsinsectordigitalizationandhowtheydifferbyFSPtype?

• Doourearlyconclusionsre:profitabilityfromdigitalizationresonate(i.e.,positivecorrelationandperhapscausation,marketexpansionbeinggreaterpathwaythancostreduction)?

• Whatdothesefindingsimplyaboutpotentialopportunitiesforkeyactorstocatalyzeprogressinthisspace?

Contactus: raflearning.org |@RAFlearning

Breakoutsessionswithdiscussionsummary

24

Summaryofbreakoutdiscussionsandgrouprecommendationsondigitalization

FSPs,withDSPsupport,wanttoinvestindigitalization.Immediatepriorities:• Dataanalytics:toimprovecredit-scoring,

increasereach,improveoperationalefficiency,etc.

• Broaderanddeeperuseofalternativedata

• Integrationofinternalandvendorsystems

• Usingdataanddigitalsolutionstoincreaseunderstandingoffarmerneeds,andtoboostcustomerenrolmentandretention

• Improvedproductdesign:betterandnewdigitalsolutionsforendusers,moreflexiblesystemsforFSPs,simplerinterfacesacrosstheboard

Providerswanttoinvest… Sector-levelsolutions…but facethesechallenges:

• ROIoninvestmentindigitalizationisnotclear,especiallygiventhehighupfrontcosts,whichhitssmallerorgsparticularlyhard

• FSPsfaceinternalchallengestoadoptingnewtechnologies,fromthecostoftrainingandonboarding (whichmayincludetrainingendusers)tooutrightresistancebystaffinsomecases

• Regulatoryandenablingenvironment(mobileecosystem)hurdleslimitthepotentialofsomedigitalsolutions

• Difficultyaccessingorintegratingdatafromexternalsourceslimitsinnovation;reluctancetosharedatastemsfromuncertaintyabout:intellectualpropertyrights,thevalueofdata,anddataprivacybestpractices

Source:Workshopfeedback;Dalberganalysis

Belowisaone-slidesummaryoftheresultsofthefacilitateddiscussionsthatfollowedpresentationoftheabovefindings.Participantfeedbacksometimeechoedstudyfindings,butalsohighlightednewissuesandprovidedgreaternuance.Followingthisslidearefullernotesfromthediscussions,organizedaccordingthe3successivebreakoutsessions.

FSPsandDSPsseeaneedfor:• Anunbiasedviewofwhatdigitalcanand

cannotdo,thelandscapeoftechnologyvendorsinkeygeographies,andpricingbenchmarksonthecostofinvestment

• KnowledgeandtoolstounderstandROI,includingaquantitativecase/evidencebaseonwheredigitizationhasthebiggestbangforbuck,modelsformeasuringROI,andcasestudiesofsuccess/failure

• DonorsupportforFSP,DSPandpolicy-makercapabilitybuildingarounddigital-ization,andfundingforinnovationsandtechnologyinvestments

• Industry-levelguidelinesonIPandnormsfordataprivacy;gaugesofvalueofdata,facilitatedbyspecialistDSPsthatcandevelopsustainabledatasharingmodels

Breakout1:Sharinglessonslearnedonpathtodigitalization– earlyresults,obstacles,opportunities

35min

• Whatimpactonfinancialperformancehaveyouseenfromdigitalization– quantifiedordirectional?

• Whatarethebarriersthatyourhavefacedindigitalizingthecreditvaluechain?

• Whathashelpedormighthelptomitigatethesebarriers?

• Whatkindsofpartnershipsorvendorshavehelpedyouonyourpathtodigitalization?

• Howdoyouthinkaboutdigitalizationsystemintegratorsvs.buildingdigitalplatformsinternally?I.e.,whereisgoingtothirdpartiesforsupportvaluableand/oressential?

26

ThediscussionconfirmedseveralwidelynotedchallengesforFSPstodigitalizationincludingROI,costs,internalcapabilities,staffincentives,andenablingenvironment

Source:Workshopfeedback;Dalberganalysis

Keylearnings Summary

Staffresistancetodigitalization

Digitalizationbringsinefficiencyandtransparency,exposingFSPstafftoadditionaloperationalscrutinyand,insomecases,restrainingpoorcompliance,unsanctionedactivity,oroutrightfraud.Asaresult,somestaffhavestrongincentivestoresistanyefforttodigitalize;othersareafraidofchangeduetoperceivedthreatstotheirjobs.

Upfrontcosts

HighupfrontcostsofsettingandintegratingdigitalplatformsactasanimportantbarrierforFSPs.Initialshifttodigitalizationlowersoperatingcosts.However,itraisesthecapexsignificantly(throughacquisitionofdigitalequipment,training,etc.).Overall,digitalizationbecomesanexpensiveundertakingandsometimesprohibitivelyexpensiveforsmallerFSPs.

Internalcapabilities

Trainingandtechnologyon-boarding(forbothstaffandendusers)isdoneinperson– thisiscostlyandtime-inefficient.Seniorandmiddlemanagementlackfamiliaritywithwhatdigitalizationentails,howtodigitalize(e.g.,vendors?),andlackoftechnicalstaffthatcaninterfaceeffectivelywithDSPs

ClarityonROIfordigitaliz-

ation

Thebusinesscasefordigitalizingsmallholderfinanceprocessesandproductsistodayweaklydefined;everyoneinthissectorunderstandsthatdigitalizationisthefuture,butmostplayersareuncertainonhowtoprioritizedigitalizationrelativetootherinvestmentsinaresourceconstrainedenvironment,and– critically– whatresultstoexpectwithinwhattimeframe(i.e.,ROIondigitalization?)

Enablingenvironment

Lackofrobustruralmobileecosystemspreventsuccessfuldigitalization(e.g.,limitedaccessbySHFstoreliablemobileconnectivity,insufficientcoverageofmobilemoneyagentnetworks,lowinteroperability,andlowdigitalliteracy).Underdevelopedoroverlyrestrictiveregulatoryenvironments(e.g.,digitalsolutionsvs.KYC)delaythedigitalizationprocesswhilemakingitcostlier.

27

Therearealsoanumberofchallengesspecifictoaccessingorintegratingnewdatasourcesintothesmallholderfinancevaluechainaspartofthedigitalizationprocess

Intellectualproperty rights

Keylearnings

Lackofclarityonintellectualpropertyrightstofarmerdata,particularlybetweenFSPs,whicharethedatabeneficiaries,andDSPswhoaredatagenerators/gatekeepers/curators/orcustodians.

Datasharing

Serviceproviderswhoownvaluabledata(e.g.,telcos)areoftenresistanttodatasharingacrosstheecosystem,wherespecializedintermediaries(e.g.,realtimedataanalyticsfirms)arenotpresent,therebylimitinginnovationandthespeedofdigitalization.Serviceproviderserronsideofcautionwithrespecttotheirdata,thinkingthatitisvaluablewithoutknowingwhatthevalueactuallyis.Overall,thisslowsinnovationinthesector.

Source:Workshopfeedback;Dalberganalysis

Summary

Natureofdigitalservices

Technologyis80-20;DSPslaunchimperfectproductsanditeratealongthewayasmoredatacomesthrough.However,manyFSPsareunwillingtoaccepthalf-completeproductsandareskepticalofsharingtheirdatatoassistintheimprovementofthedigitalservice.Thismakessellingdigitalservicesmuchmoredifficult

Dataprivacy

Thereareconcernsovertheprivacyofcustomers– DSPsareallowedaccesstocustomersofdifferentFSPsandcanaggregatetheseuserdatabasestoimprovetheiralgorithm.Thesectordoesn’tcurrentlyknowhowtonavigatearounddataprivacybecausethetechisstillnewanddataprivacyregulationsareweakorunderspecifiedinmostcountries.Manyinstitutionstakeamorecautiousapproachtodataprivacyanddonotcapturefullvalueoftheir(orDSP)dataassets.

Breakout2:Groupexerciseondigitalizationinvestment

• 5min.Individuallythinkaboutthishypotheticalsituation:Ifyouhad$500ktoinvestindigitalizationtobettersupportyourclients/partners/grantees,whatwouldyouspenditonandwhy?

• 20min:Individualsshareouttheindividualopinionswiththerestofthegroupwithparticularonfollowingquestions:

─ Whattypesofdigitalizationinvestments(andwhere)willgeneratethebiggest“bangforthebuck”?(e.g.,bringinginalternativedata,buildingoutdigitalcustomeracquisitionchannels,digitalmarketing,digitalVASdeliveredinparalleltofinproduct?)

─ WhatarethemaindifferencesintermsofprioritiesbetweenFunders-DSPs-FSPs?

29

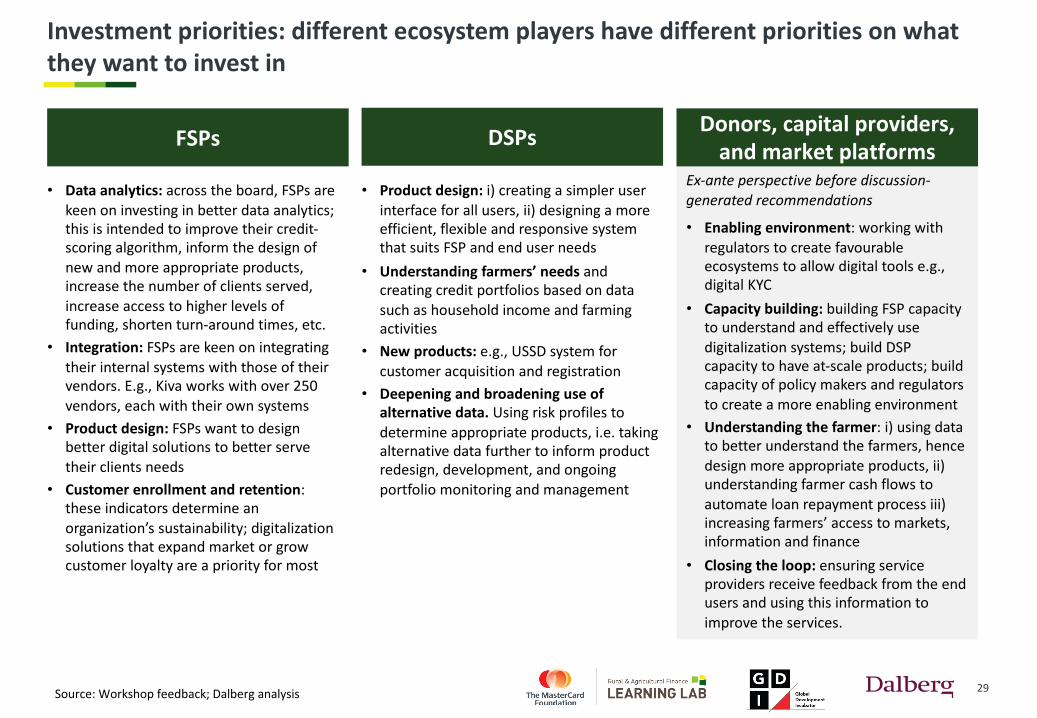

Ex-anteperspectivebeforediscussion-generatedrecommendations

Investmentpriorities:differentecosystemplayershavedifferentprioritiesonwhattheywanttoinvestin

• Dataanalytics:acrosstheboard,FSPsarekeenoninvestinginbetterdataanalytics;thisisintendedtoimprovetheircredit-scoringalgorithm,informthedesignofnewandmoreappropriateproducts,increasethenumberofclientsserved,increaseaccesstohigherlevelsoffunding,shortenturn-aroundtimes,etc.

• Integration:FSPsarekeenonintegratingtheirinternalsystemswiththoseoftheirvendors.E.g.,Kivaworkswithover250vendors,eachwiththeirownsystems

• Productdesign:FSPswanttodesignbetterdigitalsolutionstobetterservetheirclients needs

• Customerenrollment andretention:theseindicatorsdetermineanorganization’ssustainability;digitalizationsolutionsthatexpandmarketorgrowcustomerloyaltyareapriorityformost

FSPs Donors,capitalproviders,andmarketplatformsDSPs

• Enablingenvironment:workingwithregulatorstocreatefavourableecosystemstoallowdigitaltoolse.g.,digitalKYC

• Capacitybuilding:buildingFSPcapacitytounderstandandeffectivelyusedigitalizationsystems;buildDSPcapacitytohaveat-scaleproducts;buildcapacityofpolicymakersandregulatorstocreateamoreenablingenvironment

• Understandingthefarmer:i)usingdatatobetterunderstandthefarmers,hencedesignmoreappropriateproducts,ii)understandingfarmercashflowstoautomateloanrepaymentprocessiii)increasingfarmers’accesstomarkets,informationandfinance

• Closingtheloop:ensuringserviceprovidersreceivefeedbackfromtheendusersandusingthisinformationtoimprovetheservices.

• Productdesign:i)creatingasimpleruserinterfaceforallusers,ii)designingamoreefficient,flexibleandresponsivesystemthatsuitsFSPandenduserneeds

• Understandingfarmers’needs andcreatingcreditportfoliosbasedondatasuchashouseholdincomeandfarmingactivities

• Newproducts:e.g.,USSDsystemforcustomeracquisitionandregistration

• Deepeningandbroadeninguseofalternativedata.Usingriskprofilestodetermineappropriateproducts,i.e.takingalternativedatafurthertoinformproductredesign,development,andongoingportfoliomonitoringandmanagement

Source:Workshopfeedback;Dalberganalysis

Breakout3:Whatdoweneedtomoveforward

Identifytopanswersasagroup,forsharingback:

─ Wherearethegreatestoutstandingquestionsandknowledgegapsformakingdigitalizationinvestments?

─ Whattoolsareneeded/usefulforFSPsadoptingdigital─ Businessmodeltoolkit─ guidesforDSPvendoroptions,─ toolkit/modelformeasuringimpactofdigitalizationonprofitability/ROI

─ Whatadditionalsupportdoesthesectorneedfromintermediaries,investors,andfunderstomovethedigitalizationagendaforward?

31

Movingforward:recommendationsforadvancingdigitalization(1/2)

• FSPsneedDSP/vendorlandscapingandbenchmarkingtohelpthemidentifypotentialdigitalizationvendorsandunderstandtheirrelativestrengths/weaknessesforspecificusecases

• FSPshavevaryingexpectationsofwhatdigitalcan/cannotdo.Inordertomanagetheirexpectations,theyneedaclarificationonwhatdigitalcan/can’tdo.

• DSPswouldliketobenchmarkpricinganddeveloppricingmodelsfordifferentFSPsbasedontheirbusinessmodelsandabilitytopay

• Strongneedsforamorequantitativeandrobustbusinesscasefordigitalization,withbetterindicationofwhereandhowdigitalizationcreatesbenefits;clarityonwhatimpacttoexpectandwithinwhattimeline

• CreatecomprehensiveROIstogaugeimpactofdigitalizatione.g.,benchmarkingcapex;buildingatoolkit/modelformeasuringsuchimpact

• Buildanevidencebaseoncostandimpactofdigitizingdifferentstepsofthevaluechain,includingassessmentofimpactontheenduser

• GranularmappingofKPIsfordigitalizationinordertostandardizeimpactassessment

• Alongsidebuildingabusinesscase,thereisaneedtodevelopcasestudiesoffailuresindigitalization

SectorneedsOpportunities

ClarityonROIfor

digitalization

Technologyvendor

landscapingand

benchmarking

Source:Workshopfeedback;Dalberganalysis

32

Movingforward:recommendationsforadvancingdigitalization(2/2)

• CapacitybuildingforFSPstoenableusageofdigitaltools

• CapacitybuildingforDSPstocreateat-scaleproducts

• Capacitybuildingforpolicymakerstocreateamoreenablingecosystem,e.g.,adaptingKYCrequirementstothedigitalfinanceopportunity

• Fundingsupportforstart-upDSPstobringmoreinnovationtothemarket

• FundingsupportforFSPswhendigitalizationbecomesprohibitivelyexpensive

• ConveningforumsforconnectingDSPsandFSPs

• AmoreopenedsharingenvironmentwillgiveDSPsthedatatheyneedtoinnovateandimprovetheirofferings

• ClarityonIPrightsfordigitaldatausefulforsmallholderfinance

• RobustdataprivacynormsandrulestohelpguideFSPandDSPbehavior,withouterringonsideofexcessivedataprivacyprotectionthatwouldstymieinnovation

• InvestmentintodataanalyticsspecialistDSPsthatcanhelpalternativedataholdersandFSPsbetterexploreandrealizethevalueofdatawithsustainable,marketdrivendatasharingmodels

Datasharing

Supportforinstitutions/orgsinthe

digitalizationprocess

Source:Workshopfeedback;Dalberganalysis

SectorneedsOpportunities

Annex:Additionaldata

34

Whilealmostallorganizationshavedigitalizedloananalysis,themajoritystilluselimitedsourcesofnon-traditionaldataorrelyonairtimedata

4

4

23

3

3

3

Digitalloananalysisusingonesourceofalternativedata

1

1

7

Digitalloananalysisusingtraditionaldatasources

9

Digitalloananalysisusing

multiplesourcesofalternativedata

5

Total#respondentsHavenotdigitalizedloananalysis1

21

1

1

1

1.Respondentcollectstraditionaldatamanually/onpaperSource:RAFLLBusinessCaseSurvey&Dalberganalysis

81%useairtimedata

Numberoftotalsurveyrespondentsbydigitalizationofloananalysisandprofile

HighTechBanks/NicheNBFIs

TraditionalMFIs

CommercialBanks/InnovativeMFIs

AgribusinessesUtilizefarmer

profilescollecteddigitallyandcredit

history

67%ofthosewhousealternativedata

sourcespartnerwithanexternalanalytics

provider

35

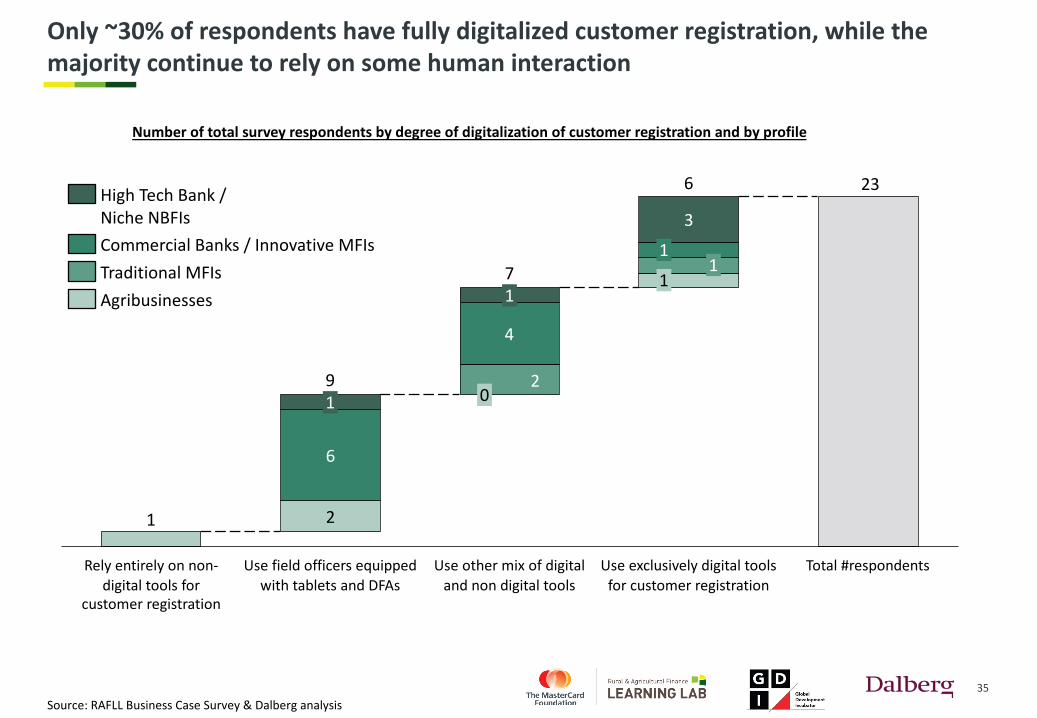

Only~30%ofrespondentshavefullydigitalizedcustomerregistration,whilethemajoritycontinuetorelyonsomehumaninteraction

Source:RAFLLBusinessCaseSurvey&Dalberganalysis

23

1 2

6

2

4

3

Relyentirelyonnon-digitaltoolsfor

customerregistration

6

Useothermixofdigitalandnondigitaltools

71

UsefieldofficersequippedwithtabletsandDFAs

91

1

Total#respondentsUseexclusivelydigitaltoolsforcustomerregistration

0

11

Numberoftotalsurveyrespondentsbydegreeofdigitalizationofcustomerregistrationandbyprofile

HighTechBank/NicheNBFIs

Agribusinesses

CommercialBanks/InnovativeMFIsTraditionalMFIs

36

Digitalizationofcashflows islargelydeterminedbythemobilemoneyecosystem1:mostoftheplayersrelyingoncashoperateinlessfavorableecosystems

1.Penetrationofmobilemoneyinruralareasisusedasaproxyforecosystemmaturity,withcountrieswith>25%penetration(CoteD’Ivoire,Tanzania,Uganda,andKenya)rankedasmoremature(lessmature:Ethiopia,Ghana,Rwanda,Nigeria).2.IncludesrespondentswhousemobilemoneyordigitalpaymentsSource:RAFLLBusinessCaseSurvey&Dalberganalysis

44%43%

56%

7%

50%

MoreFavorableMobileMoneyEcosystem

14 9

LessFavorableMobileMoneyEcosystem

Numberofsurveyrespondentsbydegreeofdigitalizationoffundsdisbursalandrepayment

FullyDigitalTransitioningtoDigitalFullyCash

50%ofthosetransitioningtocashlessfundsdisbursalandcollectionsusealternativedigitalpaymentplatforms

37

Supportservicesappeartobethehardesttodigitalize:only~17%useexclusivelye-learningplatformsanddosoprimarilyforinformationservices

Numberofsurveyrespondentsbydegreeofdigitalizationofsupportservicesoffered

Source:RAFLLBusinessCaseSurvey&Dalberganalysis

88%ofthosewhohavenot

digitalizedsupportservicesoffer

primarilyfinancialliteracytraining

21

3

4

3

4

3

3

OnlydigitaltoolsOthermixofdigitalandnondigitaltools

Total#respondents

Non-digitalizedsupportservices

Fieldofficerwithtablet

10

14

Agribusinesses

Hightechbanks/NicheNBFIs

TraditionalMFIs

Commercialbanks/InnovativeMFIs