Embed Size (px)

Citation preview

MANAGING RISK IN A DIGITAL WORLDSuccessfully enabling the quest for new revenues

FINANCE & RISK EXECUTIVES IN BANKS ARE INCREASINGLY COMING TOGETHER TO HELP ADDRESS MANY CHALLENGES

How do we make our BUSINESS AND OPERATING MODELS AGILE, FLEXIBLE and suited for LONG TERM PROFITABLE GROWTH?

How do we reduce the DUPLICATION & COMPLEXITY in our business operations?

How do we manage the sudden increase in VOLUME & INTENT OF REGULATIONS in a cost-effective manner?

How do we make our FINANCE & RISK FUNCTIONS more efficient & effective to drive better BUSINESS INSIGHTS?

KEY QUESTIONS

FACING EXECUTIVES

2Copyright © 2014 Accenture All rights reserved.

3

WHILE BUDGETS ARE BEING RAPIDLY CONSUMED ON REGULATORY, INFRASTRUCUTRE AND TACTICAL ISSUES

2014 Compliance Risk

Study: Respondents

expect spend to grow by

10 to 20 percent or more

over the next two years.

Copyright © 2014 Accenture All rights reserved.

FUNDING TODAY’S

PRIORITIES 1

BUILDING FOR

THE FUTURE

SOLVING FOR

THE PAST

4

WHILE THE DIGITAL REVOLUTION IS RADICALLY RE-SHAPING EVERY ASPECT OF THE BANKING INDUSTRY

Digital banking

transactions are now

worth c. £1bn a day,

with c. 40 million mobile

and internet banking

transactions every week

(Source: BBA)

Copyright © 2014 Accenture All rights reserved.

VALUE AGGREGATOR

ADVICE PROVIDER

ACCESS FACILITATOR

Source: Accenture, The Everyday Bank, 2013

DIGITAL REVOLUTION DRIVERS: CHANGE WILL BE DRIVEN BY EMERGING CUSTOMER BEHAVIOURS

While also answering to Regulators and Shareholders

Regulatory

Compliance

New digital

competition

Deteriorating

industry

boundaries

Pressure on

profitability

DIGITAL INTENSIFIES CUSTOMER POWER

DIGITAL CREATES NEW COMPETITORS

Copyright © 2014 Accenture All rights reserved. 5

Technology

innovation

6

NEW ENTRANTS AND BUSINESS MODELS ARE EMERGING ACROSS THE INDUSTRY AS DISRUPTORS

LARGE DIGITAL PLAYERS & FINTECH STARTUPS

FS

P2P lending

Virtual & direct banking

Self service banks & kiosks

Mobile insurance

Mobile banking

Mobile points-of-sale

Mobile payments & e-wallets

Real-time dynamic pricing

Data-driven credit-rating

Personal financial

management tools

P2P payments

Copyright © 2014 Accenture All rights reserved.

NEW ENTRANTS & MODELS

7

WHILE FINTECH COMPANIES ARE CONTINUING TO EMERGE BRINGING NEW INNOVATIONS AT PACE, WORKING WITH ESTABLISHED MARKET LEADERS

UBS

Bank of America

Merrill Lynch

Credit Suisse

Santander

HSBC

RBS

Barclays

Lloyds Bank

VocaLink

JPMorgan Chase

Deutsche Bank

Morgan Stanley

Citibank

Goldman Sachs

Nationwide

PixelPin

Logical Glue

uTrade Solutions

FinGenius

PhotoPay

Waratek

BehavioSec

Digital Shadows

Open Bank Project

Erudine

Squirro

Kiboo

Growth Intelligence

OP3Nvoice

Copyright © 2014 Accenture All rights reserved.

8

OLD APPROACHES WILL NOT DELIVER NEW RESULTS AND THE TIMING FOR ACTION IS NOW

Time

Mark

et P

enet

rati

on

Traditional strategy

Digital Enabling Strategy

“A new form of market creation is emerging, radically impacting timelines”

Accenture Institute of High Performance (Nov, 2013)

Copyright © 2014 Accenture All rights reserved.

Today

8Copyright © 2014 Accenture All rights reserved.

WINDOW FOR DECISION

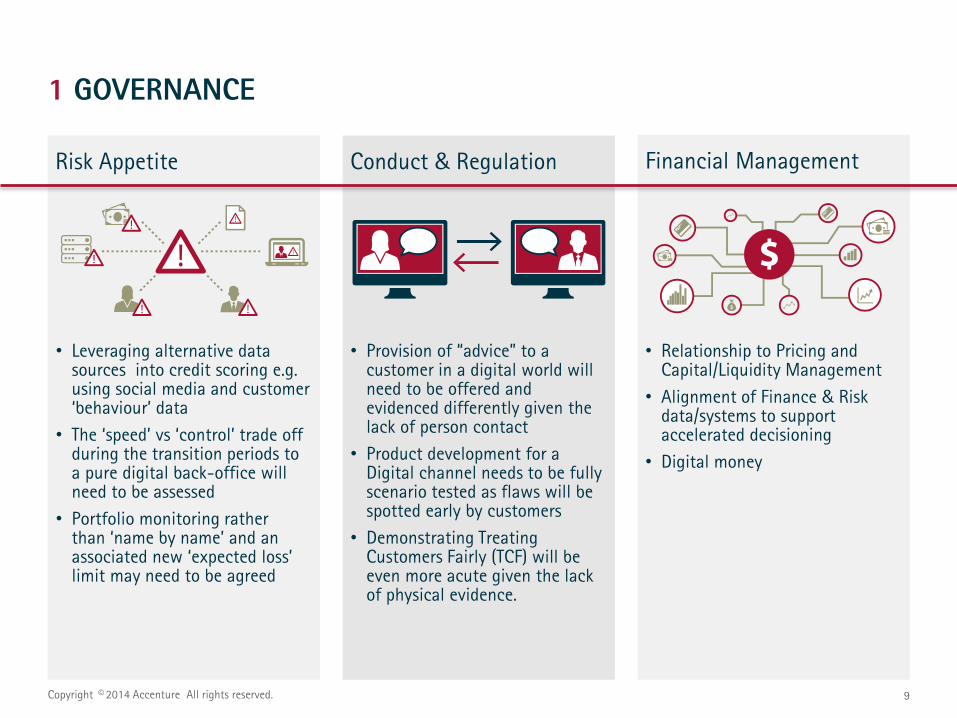

1 GOVERNANCE

Risk Appetite Financial Management

9Copyright © 2014 Accenture All rights reserved.

Conduct & Regulation

• Leveraging alternative data sources into credit scoring e.g. using social media and customer ‘behaviour’ data

• The ‘speed’ vs ‘control’ trade off during the transition periods to a pure digital back-office will need to be assessed

• Portfolio monitoring rather than ‘name by name’ and an associated new ‘expected loss’ limit may need to be agreed

• Provision of “advice” to a customer in a digital world will need to be offered and evidenced differently given the lack of person contact

• Product development for a Digital channel needs to be fully scenario tested as flaws will be spotted early by customers

• Demonstrating Treating Customers Fairly (TCF) will be even more acute given the lack of physical evidence.

• Relationship to Pricing and Capital/Liquidity Management

• Alignment of Finance & Risk data/systems to support accelerated decisioning

• Digital money

IT Resilience & Business Continuity

Talent & CultureCredit Risk Decisions

Operational Risk (incl. 3rd Parties)

2 PROCESS

10Copyright © 2014 Accenture All rights reserved.

• Increased speed to decision will be important in order to capture / retain highest credit quality customers

• Hand-offs to third parties (e.g. under-writers) can’t be the manual ‘weak link’ in the chain

• Better devices and better connectivity will improve user experience, but be an entry point for business risks. IT supply chain has specific assurance challenges

• Cloud computing will transform the way businesses rely on IT. This will increase information stewardship control testing

• As customers demand ‘contextual’ services or links and bundled products, the management of 3rd party suppliers to the same standard as the bank’s internal targets is equally important

• Linkage from Mobile apps at the front end to core accounting platforms & payments systems

• Digital support may challenge the traditional positioning of the three lines of defence. Real time operation will require risk and finance professionals to be more closely aligned

• Senior Managers Regime accountability heightened

Cyber Security & Financial Crime

Digital Data Sourcing

Analytics & Insight Data Privacy

3 DATA & TECHNOLOGY

11Copyright © 2014 Accenture All rights reserved.

• Using more data from disparate sources will require enhanced control, ‘big data’ management strategies, and ‘data conflict’ testing in order to build a more comprehensive view of the customer

• Digital data monitoring can trigger early warning (customers searching for credit card deals, unsecured loans, payday lending)

• Customers will have to become more savvy in terms of sharing data to avoid the burden falling on the Bank

• Banks may need to ‘entice’ or compensate customers for using their data

• Digital channels may attract customers who posses a higher tendency to ‘stress the boundaries of the truth’ due to the anonymity that the channel affords

• Data and information (both customer/client and the banks) have a currency, but the reputation cost of breaches often eclipses the value of the underlying data

• Capturing additional data sources and data points both from internal ‘silos’ and external ‘new media’ will build a more representative profile of the customer and validate historic assumptions

12

Learn more about Accenture Finance and Risk

www.accenture.com/financeandrisk

Copyright © 2014 Accenture All rights reserved.

![Research Article - JCIM (Journal16... · Psorinum therapy[12,13,17,18] is believed to treat several forms of cancer successfully, enabling the patients to survive for several years](https://img.pdfslide.us/doc/110x75/5c78fae609d3f2cb498c5a59/research-article-jcim-16-psorinum-therapy12131718-is-believed-to.jpg)