Embed Size (px)

Citation preview

Brazilian Scenario - Trends and Challenges to keep IT investments

Jayme Faria - ICT Consulting Manager Latin America

Frost & Sullivan

February - 2016

xxx

Presented to:

2

2009 2013 2014 2015

Macroeconomic “rollercoaster” in the past 7 years

High Expectations Path errors Weak political

leadership to change Issues Foreseen

• Commodities Boom helps exports • Strong R$ X USD • Decreasing inflation/interest rates (Selic and Public

Banks) • Increasing middle class and consumption • World Cup + Olympics to boost GDP • Petrobras pre-salt investments (Oil US$110/barrell in

2011) • Respect for investors • Fiscal superavit

• Commodities Low Prices (China < demand) • Weak R$ X USD • Increasing inflation/interest rates • Consumption reduces significantly • World Cup as explanation for lower GDP • Petrobras corruption scandals and reduced investments (Oil US$40/barrel in 2015) • Downgrade of Brazilian debt to junk status from Fitch and Standard & Poor’s (end of 2015) • Optimistic forecasts indicate a 2.5% shrinkage for Brazilian economy in 2016 • The finance minister quit in despair after less than a year in the job (end of 2015) • High inflation rates and unemployment rates tending to get even worse during 2016

Source: The Economist, Frost & Sullivan

2016

Policy and economy at the edge of the

precipice

3

Brazil’s perspective is not so encouraging...

•Consumers are indebted

•Consumers confidence index decrease

•Social conditions deterioration

•Exports reduction

•Drop on investments grade

•Commodities price decrease

•Shortage of credit

•Petrobras crisis

•Fall in president’s popularity

•Lack of Government actions

•Difficulty on comply the budget

•Unemployment rates – 6.8% in 2015

•Higher inflation rate – 10.7% in 2015

•Currency devaluation – 1USD = 4BRL

•Increase in interest rates – SELIC 14.25%

•GDP shrinkage: 3.8% in 2015

Economy Politics

Consumption Trade

Source: Frost & Sullivan

4

Diversify the agenda is the solution for exports and to the overall economy in Brazil

Source: Frost & Sullivan and OECD-FAO Agricultural Outlook 2015

• Growth rate expected is ‘just’ 7% for 2015

• Stock market crash of values

• Lower commodities prices globally

China’s lower growth

path • China accounts for 27,2% of total Agriculture sector exportation of Brazil

• 35% of Brazil’s total oilseed production exported to China

Brazil’s exports dependency on China

• Directly through bilateral trade

• Indirectly through changing world prices

• 33% of decrease on exportations in first semester of 2015

Brazilian agriculture affected

• Brazil has stimulated the consumption, but forgot about the production capacity

• Commodities vs manufactured products

Recent years brief overview

5

Productivity is what sustained the growth of the agriculture business in Brazil, and is the necessary diversification to overcome the current situation

Source: Frost & Sullivan and cepea.esalq.usp.br

2010 2011 2012 2013 2014

Total (excluding Agribusiness) 7.5% 2.0% 2.2% 2.1% -0.3%

Agribusiness 7.5% 5.4% -2.8% 3.9% 1.6%

-4.0%-2.0%0.0%2.0%4.0%6.0%8.0%

10.0%

GDP growth comparison

Technology leveraged the grains productivity

• Harverters and Irrigation techniques boosted the growth –

6.4% from 2014 to 2015 More productivity with no area increase (just 1.7% of growth)

• The acreage grew from 57 million to 58 million hectares from 2014 to 2015

IOT could take Agriculture to the next level

• Predictive data analytics , Sensors, Smart meters, Precision seeding,

Fertility and disease management and weather accurate forecasts

2012 was a bad year due to the

unfavorable weather conditions which

affected mainly corn and soybean crops

6

Budget pressures generate important incentives for increased productivity in different sectors

On-demand instead of peak capacity

Opex instead of Capex

Don't just invest your budget, optimize it Source: Frost & Sullivan

7

Digital transformation will take place in this context

Big Data Cloud

Mobile

Social

IOE

The Brazilian Big Data

market was expected to

end on US$400

million in 2015

The Brazilian Cloud market was expected

to end on US$668

million in 2015

The Brazilian users of

smartphones with a mobile

broadband have surpassed

70 million during the

1H2015

The Brazilian WhatsApp

active users were more

than 50 million in 2015

The Brazilian M2M market was expected

to end on US$190

million in 2015

Source: Frost & Sullivan

8

Industry executives recognize that change is here and see new challenges in IT

New, disruptive

competitors Digitalisation New Business

Models

Servitisation

Forces Driving Change

36% 27% 18% 12%

Perceived Rate of Industry Change

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

2010

Now

Not changing at all

Changing only slowly

Changing at a moderate pace

Changing fast

Changing very fast

Source: Frost & Sullivan survey of 1,500 executives, 2014

Source: Frost & Sullivan

9

And need to transform the business with strategic and tactical initiatives

Strategic Focal Points Tactical Focal Points

Business Model

Cost

Customer Experience

Partnership

Innovation Supply Chain Management

Operational Excellence

Risk Management

Workforce Empowerment

Reducing Cost

Service Excellence

Digital Products and Services

Source: Frost & Sullivan

10

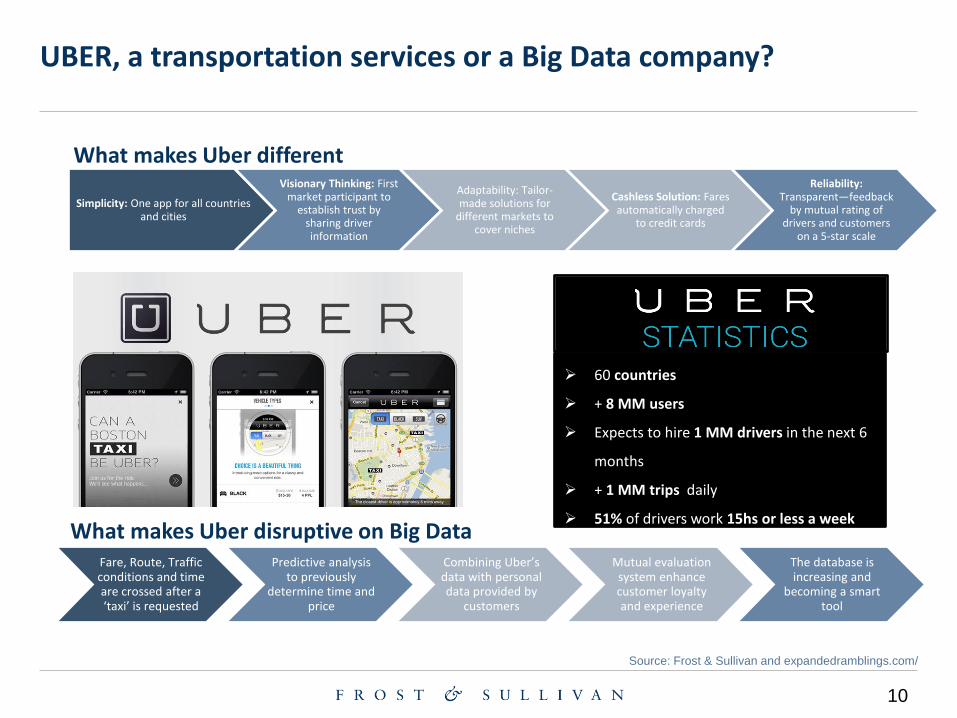

UBER, a transportation services or a Big Data company?

Source: Frost & Sullivan and expandedramblings.com/

Fare, Route, Traffic conditions and time are crossed after a ‘taxi’ is requested

Predictive analysis to previously

determine time and price

Combining Uber’s data with personal data provided by

customers

Mutual evaluation system enhance customer loyalty and experience

The database is increasing and

becoming a smart tool

Simplicity: One app for all countries and cities

Visionary Thinking: First market participant to

establish trust by sharing driver information

Adaptability: Tailor-made solutions for

different markets to cover niches

Cashless Solution: Fares automatically charged

to credit cards

Reliability: Transparent—feedback

by mutual rating of drivers and customers

on a 5-star scale

What makes Uber different

What makes Uber disruptive on Big Data

60 countries

+ 8 MM users

Expects to hire 1 MM drivers in the next 6

months

+ 1 MM trips daily

51% of drivers work 15hs or less a week

11

Source: Frost & Sullivan

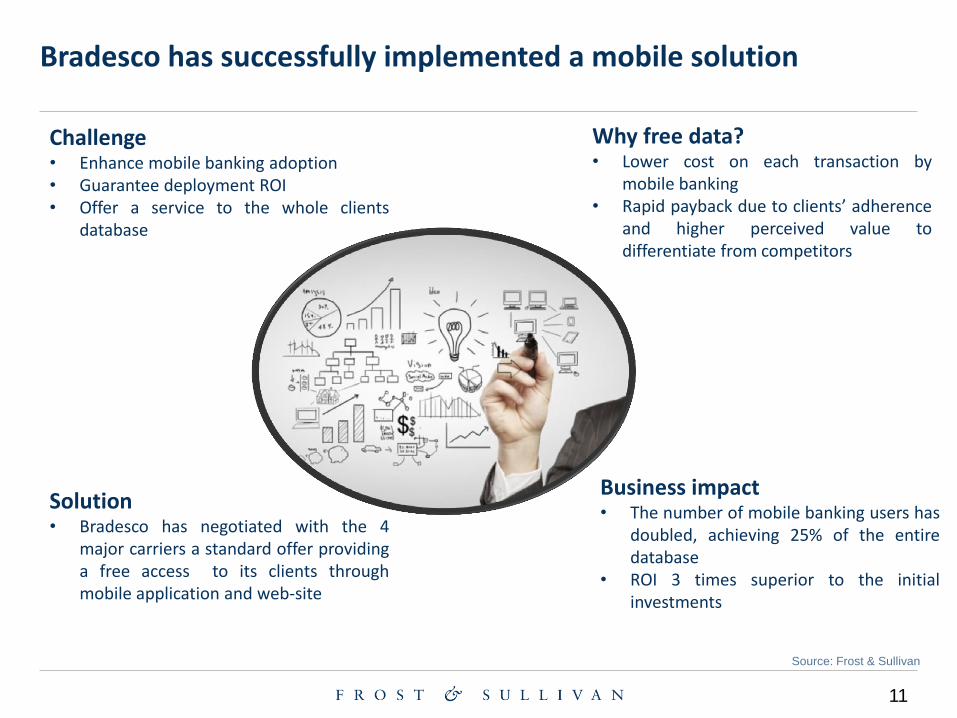

Bradesco has successfully implemented a mobile solution

Solution

• Bradesco has negotiated with the 4 major carriers a standard offer providing a free access to its clients through mobile application and web-site

Business impact

• The number of mobile banking users has doubled, achieving 25% of the entire database

• ROI 3 times superior to the initial investments

Challenge

• Enhance mobile banking adoption • Guarantee deployment ROI • Offer a service to the whole clients

database

Why free data?

• Lower cost on each transaction by mobile banking

• Rapid payback due to clients’ adherence and higher perceived value to differentiate from competitors

12

Market Demand

• Sao Paulo is the financial center of Brazil

• High consumption

• Proof of concept to future rollout in the whole state

Opportunity for Innovation

• Create an environment of continuous innovation

• Evaluation of new concepts and solutions

Effectiveness of Investments

• Customers interaction

• Alternative supply

• Loss reduction

Productivity

• Smart Meters

• Process Automation

Source: Frost & Sullivan and Cisco

Cisco and Eletropaulo are partners on a Smart Grid project in Barueri

Reduce technical and commercial losses

(fraud)

Improve the service quality

Reduce operational costs

Improve planning of grid expansion

Improve assets management

Promote energy efficiency

Grid suitable to connect micro-

generation (Eolic and solar)

Customers manage their own

consumption using Client Portal

Main Benefits

Main Motivations

13

Source: Frost & Sullivan

Lessons that Brazil could take from European countries which retook growth path after the financial collapse: Spain

How the crisis started?

- Spain also saw the boom and bust that accompany a housing bubble

- During the economic boom, 800 thousand apartments were built in the country every year

- Too many projects were financed on credit, and as result, private debt was twice as high as the entire Spanish GDP in 2008

How Spain faced the

crisis?

- In 2012, Spain also received billions of dollars from the European Union to rescue the banking system

- The Spanish government undertook a tough policy of fiscal austerity prompting protests among ordinary citizens

How is Spain nowadays?

- The government expects economic growth of 3 percent in 2015

- The situation is much better than some years ago, but the main problems still remain unresolved

- Almost one in five people in Spain remain unemployed, lower rate than the highest of 27% which were seen during the worst crisis’ period

14

Source: Frost & Sullivan

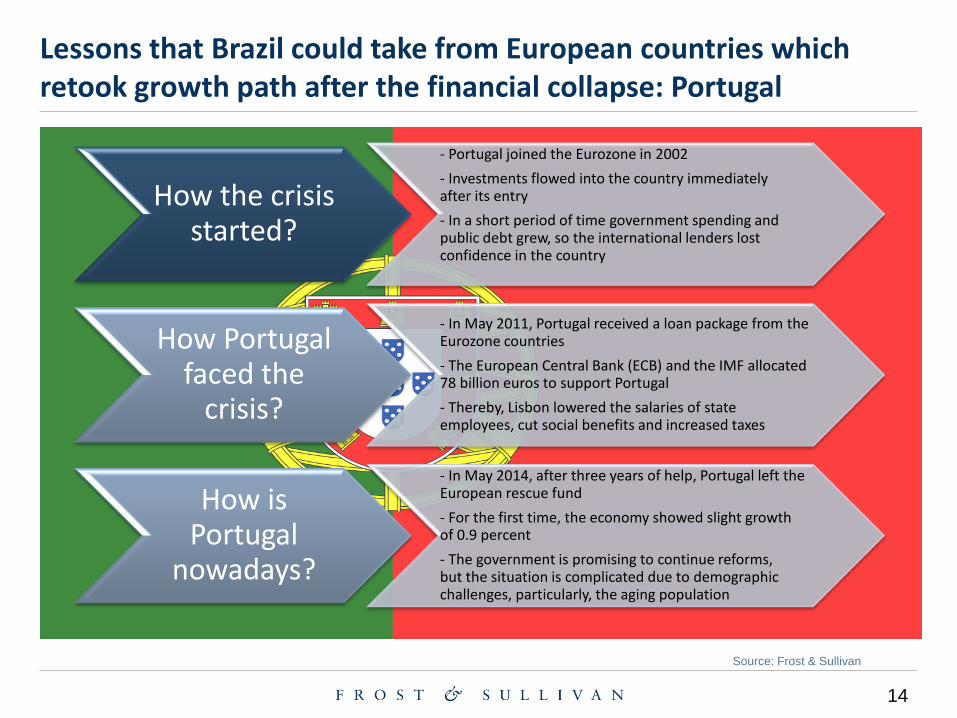

Lessons that Brazil could take from European countries which retook growth path after the financial collapse: Portugal

How the crisis started?

- Portugal joined the Eurozone in 2002

- Investments flowed into the country immediately after its entry

- In a short period of time government spending and public debt grew, so the international lenders lost confidence in the country

How Portugal faced the

crisis?

- In May 2011, Portugal received a loan package from the Eurozone countries

- The European Central Bank (ECB) and the IMF allocated 78 billion euros to support Portugal

- Thereby, Lisbon lowered the salaries of state employees, cut social benefits and increased taxes

How is Portugal

nowadays?

- In May 2014, after three years of help, Portugal left the European rescue fund

- For the first time, the economy showed slight growth of 0.9 percent

- The government is promising to continue reforms, but the situation is complicated due to demographic challenges, particularly, the aging population

15

The opportunity is here…

0

1

2

3

4

5

6

7

2013 2018

Glo

bal

Rev

enu

es (

US$

Tn) Smart Grids

Smart Manufacturing

Healthcare

Smart Cities

Smart Buildings

Connected Car

Traditional

$3.8 Tn

$6.3 Tn

2014 2018

• There is a need to evaluate the strategies and options towards a focus on business needs, innovation and transformation.

The need for change is now

Smart and connected industries

Cloud and enterprise application

Orchestration, Collaboration,

Enablers

Programmable Infrastructure

Programmable Network

SDN, SDS, SD-WAN & NFV: Data centers orchestration and automation, mobile network virtualization

SaaS, BAaaS, PaaS, IaaS, ERP, CRM, SCM, HCM, mobile apps

BPM, BRM, Big Data Analytics, IoT

Smart: cities, homes, health, transport, etc

Digitally-Enabled Business Services

Source: Frost & Sullivan

16

Conclusions

In an increasingly competitive scenario, and restrained by economic crisis, companies should assess co-operation relationships, alliances

and acquisitions to effectively monetize emerging opportunities.

Integrate disruptive and emerging technologies. Be Proactive, new ideas create new businesses and generate more revenue sources.

Source: Frost & Sullivan