Embed Size (px)

Citation preview

Verina Ingram, Madeleen Husselman

African forest

apiculture market

chains:

Win-wins for

livelihoods &

conservation?

Bush/wild mango Irvingia spp.

THINKING beyond the canopy

Aims

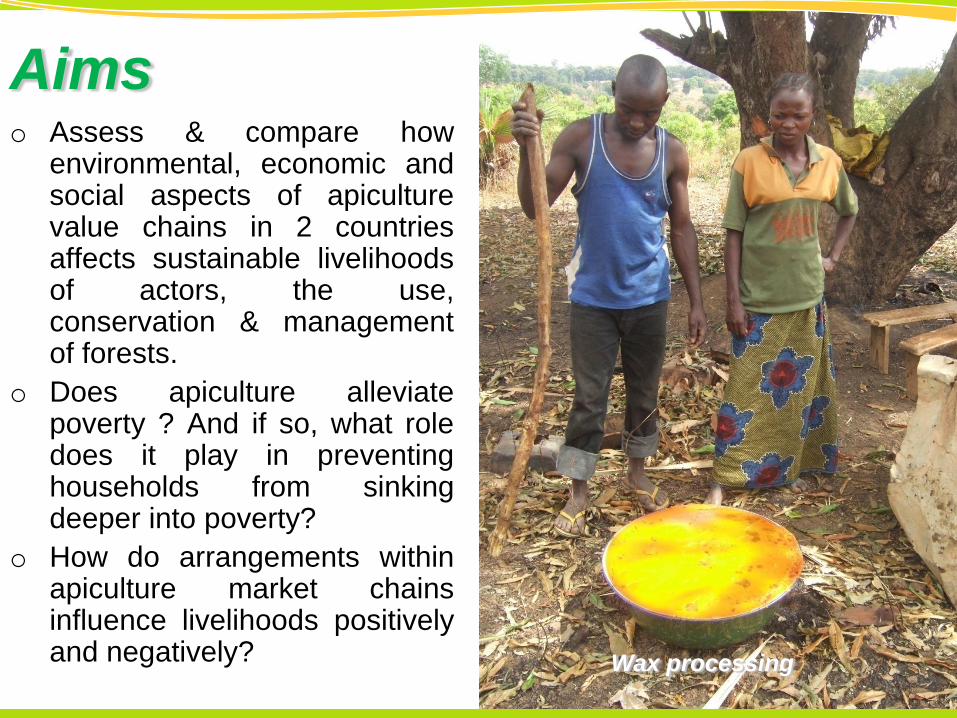

Wax processing

o Assess & compare howenvironmental, economic andsocial aspects of apiculturevalue chains in 2 countriesaffects sustainable livelihoodsof actors, the use,conservation & managementof forests.

o Does apiculture alleviatepoverty ? And if so, what roledoes it play in preventinghouseholds from sinkingdeeper into poverty?

o How do arrangements withinapiculture market chainsinfluence livelihoods positivelyand negatively?

Me

tho

do

log

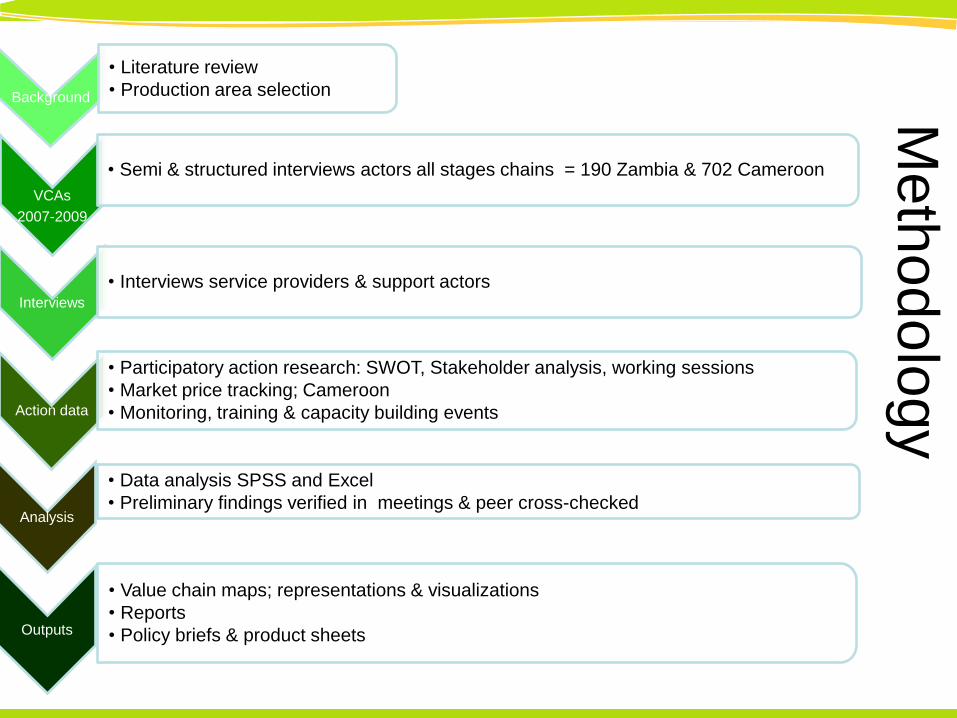

yBackground

• Literature review

• Production area selection

Interviews

• Interviews service providers & support actors

VCAs

2007-2009

• Semi & structured interviews actors all stages chains = 190 Zambia & 702 Cameroon

Action data

• Participatory action research: SWOT, Stakeholder analysis, working sessions

• Market price tracking; Cameroon

• Monitoring, training & capacity building events

Analysis

• Data analysis SPSS and Excel

• Preliminary findings verified in meetings & peer cross-checked

Outputs

• Value chain maps; representations & visualizations

• Reports

• Policy briefs & product sheets

Ngoundal

North West

Adamaoua

Cameroon

Zambia

Europe, USA

Results: Cameroon

• History : Traditional (NW 88%, Ad 97%), project ‘push’ 80s, market focus >5 years

• Production technologies: Basic & traditional, large volume, low quality, new

technologies now emerging for wax processing & propolis collection

• Economic: Ad 68% household beekeepers, 55% primary activity

• Llivelihoods: Contributes to 48% incomes Ad, 30-60% in NW

• Ecological conditions: rapid deforestation of montane forest, slower degrading

savanna forest, forest protection/controls in NW, competing forest uses

• Institutional context: High level collective organization (NW n=284) Ad n=98), bio &

ethical schemes at enterprise level, Geographical Indication scheme emerging

• Regulatory context: Unregulated national production & market, no standards, exports

to Europe regulated since 2009, no interaction forestry & livestock authorities,

customary rules exist but often overridden and degrading concerning forest use in

NW, but good in Adamaoua

• Governance: high corruption levels re transport, business set up, taxes and exports,

poor ‘doing business’ and ‘corruption perception’ indexes

• Regions: Adamaoua 41% & NW 30% est. national production,

high & increasing population density 70-99 inhabitants km² NW

and 8/km² Adamaoua

• Regions: Mwinilunga 82%, Kapiri 5% est. national production,

low population density 6 to 11.2 inhabitants km2

• History: Traditional, 150 years of trade, colonial support,

government post –independence, donor push since 1970s &

community owned, organic 1990s & fair trade since 2003,

change to private enterprises

Results: Zambia

• Production technologies: 90% traditional bark hives, low level hive

management, low volume 2nd processing except for beer

• Economic: Mw 48% & K 29% households are beekeepers, 20-25% income

• Livelihood: Mw 50% households beekeepers, av.73 hives, av. yield 7.4 – 20

kg, male dominated

• Ecological conditions: Miombo woodlands, secondary clearings preferred for

diversity, Kapiri degraded forest more regulated,

• Institutional context: Source foreign exchange, beekeeping Division ‘65-‘91,

high level NGO/development involvement, numerous SMEs vertically active in

chain, support marketing

• Regulatory context: Govt support, national beekeeping policy developed 2008.

good customary regulation for forest use

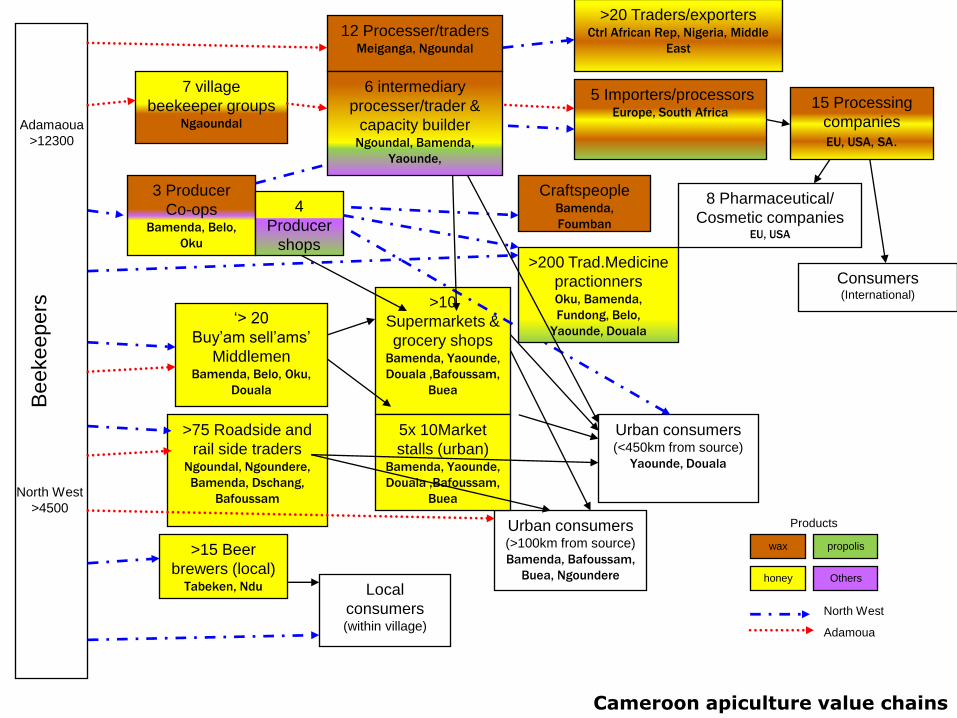

Beekeepers

7 village

beekeeper groupsNgaoundal

>15 Beer

brewers (local)Tabeken, Ndu

15 Processing

companies

EU, USA, SA.

Urban consumers (>100km from source)

Bamenda, Bafoussam,

Buea, Ngoundere

Urban consumers (<450km from source)

Yaounde, Douala

Local

consumers (within village)

‘> 20

Buy’am sell’ams’

Middlemen Bamenda, Belo, Oku,

Douala

>10

Supermarkets &

grocery shops Bamenda, Yaounde,

Douala ,Bafoussam,

Buea

5x 10Market

stalls (urban)Bamenda, Yaounde,

Douala ,Bafoussam,

Buea

>75 Roadside and

rail side tradersNgoundal, Ngoundere,

Bamenda, Dschang,

Bafoussam

3 Producer

Co-opsBamenda, Belo,

Oku

North West

Adamoua

Cameroon apiculture value chains

4

Producer

shops

CraftspeopleBamenda,

Foumban

>200 Trad.Medicine

practionnersOku, Bamenda,

Fundong, Belo,

Yaounde, Douala

12 Processer/tradersMeiganga, Ngoundal

>20 Traders/exporters Ctrl African Rep, Nigeria, Middle

East

honey

wax propolis

Others

Consumers(International)

5 Importers/processors Europe, South Africa

8 Pharmaceutical/

Cosmetic companiesEU, USA

Products

6 intermediary

processer/trader &

capacity builderNgoundal, Bamenda,

Yaounde,

Adamaoua

>12300

North West

>4500

B

E

E

K

E

E

P

E

R

S

♀

Importing

companies in

Eastern and

Southern Africa

Urban consumers

(>150km from

source)

Urban consumers

(<150km from

source)

Local consumers

(within village)

Supermarkets and grocery shops

Roadside traders

Medium-small

registered companies

Pc=K3555/kg

BK=70%

Q=65%

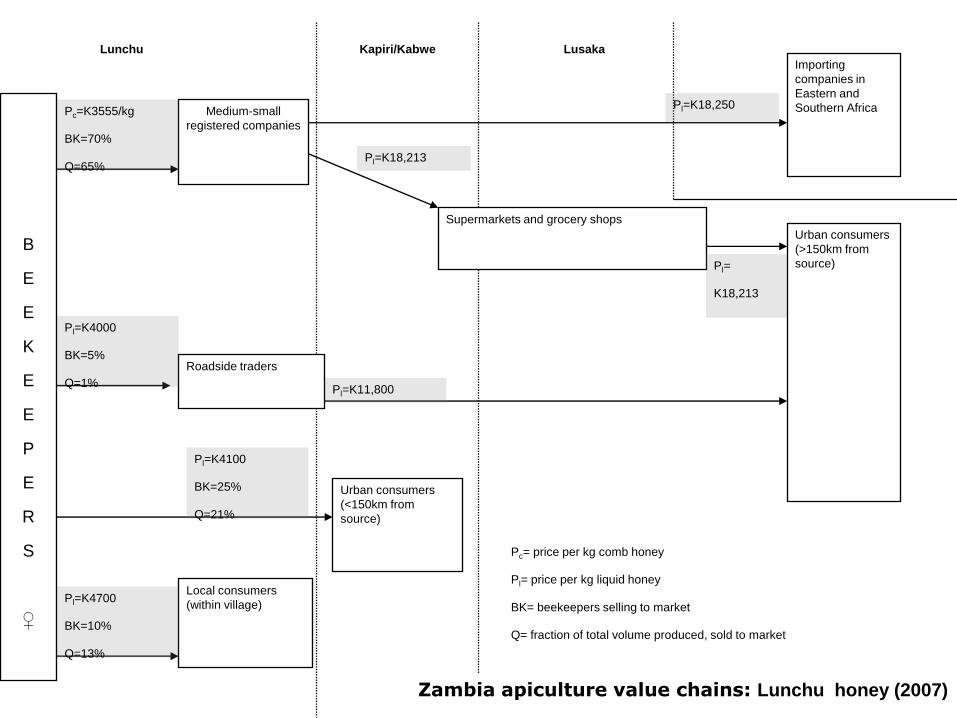

Lunchu Kapiri/Kabwe Lusaka

Pl=K18,213

Pl=K18,250

Pl=K4000

BK=5%

Q=1%Pl=K11,800

Pl=K4100

BK=25%

Q=21%

Pl=K4700

BK=10%

Q=13%

Pl=

K18,213

Pc= price per kg comb honey

Pl= price per kg liquid honey

BK= beekeepers selling to market

Q= fraction of total volume produced, sold to market

Zambia apiculture value chains: Lunchu honey (2007)

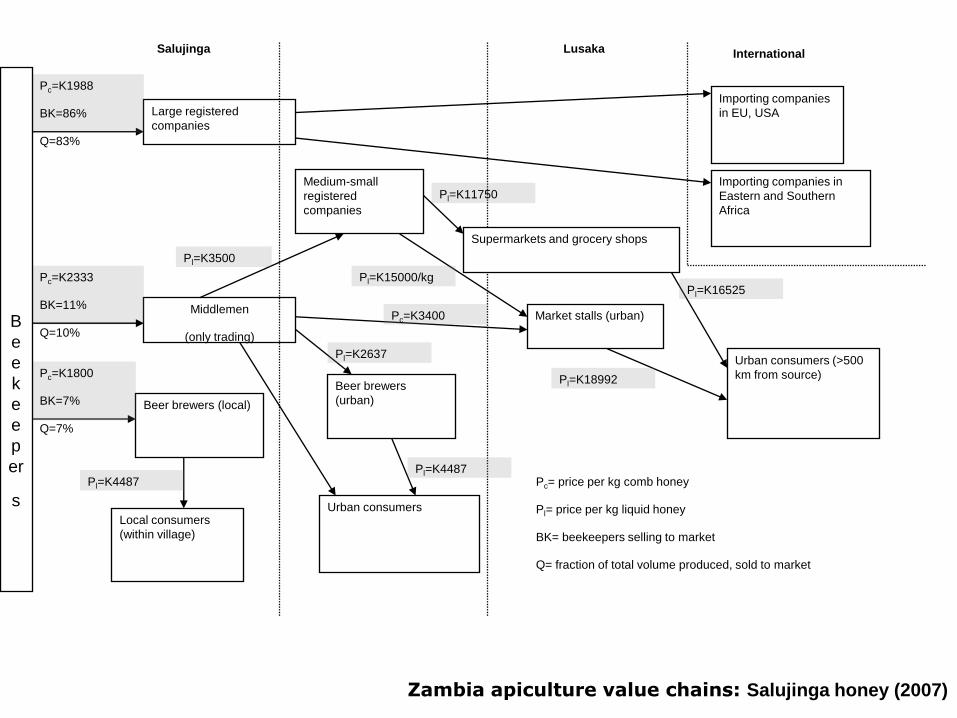

Large registered

companies

Beer brewers (local)

Importing companies

in EU, USA

Importing companies in

Eastern and Southern

Africa

Urban consumers (>500

km from source)

Urban consumersLocal consumers

(within village)

Middlemen

(only trading)

Market stalls (urban)

Beer brewers

(urban)

Supermarkets and grocery shops

Pc=K1988

BK=86%

Q=83%

Pc=K2333

BK=11%

Q=10%

Medium-small

registered

companies

Pc=K1800

BK=7%

Q=7%

B

e

e

k

e

e

p

er

s

Pl=K3500

Pc=K3400

Pl=K15000/kgPl=K16525

Pl=K18992

Pl=K11750

Pl=K4487

Pl=K2637

Pl=K4487

Salujinga Lusaka

Pc= price per kg comb honey

Pl= price per kg liquid honey

BK= beekeepers selling to market

Q= fraction of total volume produced, sold to market

International

Zambia apiculture value chains: Salujinga honey (2007)

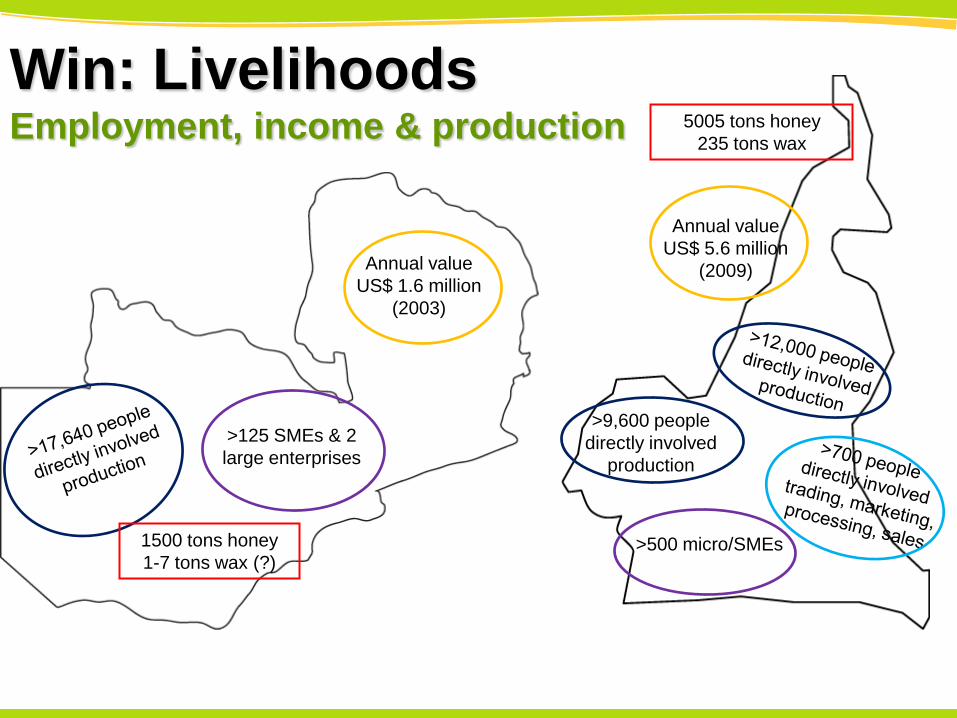

Win: LivelihoodsEmployment, income & production

Annual value

US$ 5.6 million

(2009)

>9,600 people

directly involved

production

>500 micro/SMEs

>125 SMEs & 2

large enterprises

Annual value

US$ 1.6 million

(2003)

1500 tons honey

1-7 tons wax (?)

5005 tons honey

235 tons wax

• Inherently unsustainable practices: bark hives (Zam), water &

charcoal use in wax production (Cam), smoking techniques

•Little positive evidence despite conservation rhetoric

• Once projects finish protection levels decrease & degradation

from other sources continues (Cam)

• Hive trials show secondary forest just as productive (Zam)

• Loss of honey type due to decreasing forest : white montane

honey (Cam)- major marketing and quality indicator Geog

Indicator

• Link between forest health and honey production needs to be

explicit before local beekeepers act to conserve e.g. hive resources

• Apiculture needs to be sufficiently valuable + high livelihood

priority to outweigh other beekeeper & conflicting external

interests

Win?: ConservationForest management & protection

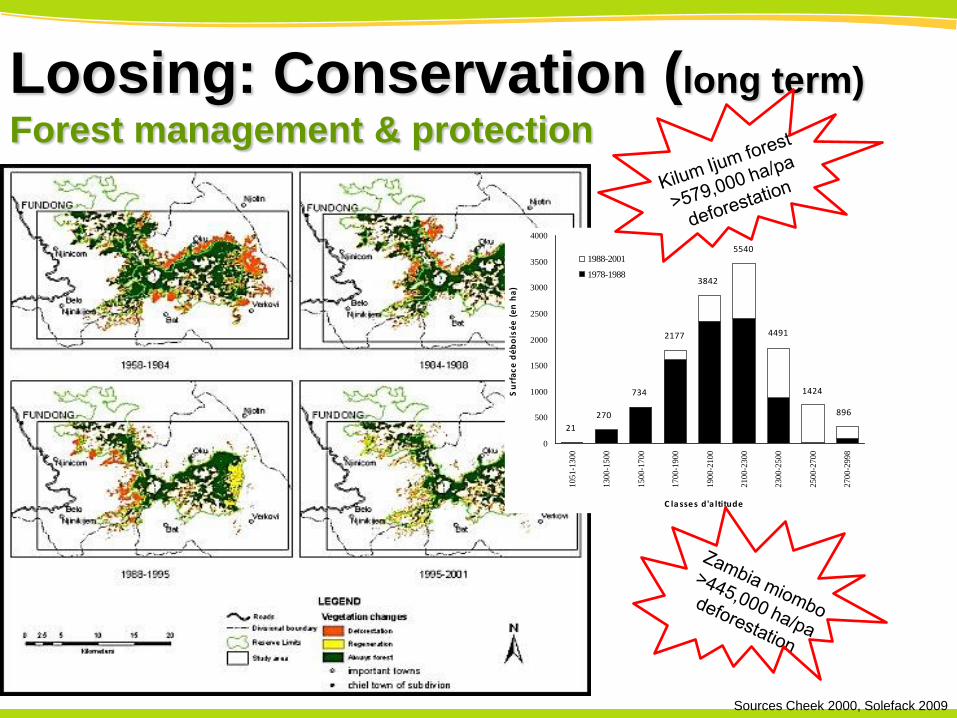

Loosing: Conservation (long term)

Forest management & protection

0

500

1000

1500

2000

2500

3000

3500

4000

1051-1

300

1300-1

500

1500-1

700

1700-1

900

1900-2

100

2100-2

300

2300-2

500

2500-2

700

2700-2

998

C la sses d'a ltitudeS

urf

ac

e d

éb

ois

ée

(e

n h

a)

1988-2001

1978-1988

21

270

734

2177

3842

5540

4491

1424

896

Sources Cheek 2000, Solefack 2009

Cameroon: Beeswax

ArrangementsNegative impact value chain arrangements- Unclear/usufruct land tenure = conservation disincentive- Open access to forest = tragedy of commons- Conservation focus ignored livelihoods aspects & forest useconflicts – dual approach needed for long term sustainability- Production focus and not markets discourages beekeepers- Entering specialty & export markets = high cost for small, local,remote organizations with unsure and marginal profits- Importers have hands in both honey pots- restrictive marketcontrol or bonus?- Collective action without ‘good’ governance rules leads = over-organized, high cost, inefficient organizations and ultimately ‘death’- Dependency on export markets raises cash & can increase scale &quality but creates credit access problems-Remoteness is a cost and market barrier-Many small, unconnected organizations and actors = inefficiency,lack of exchange on technology and market information.

Positive impact value chain arrangements+ new market chains and new markets+ deregulation opens up competition+ external actors ‘brokers’ promote information/sector exchanges+ remote forests = naturally organic, pest free, highly resilientenvironment+ successful income & high value = incentive for forestmanagement

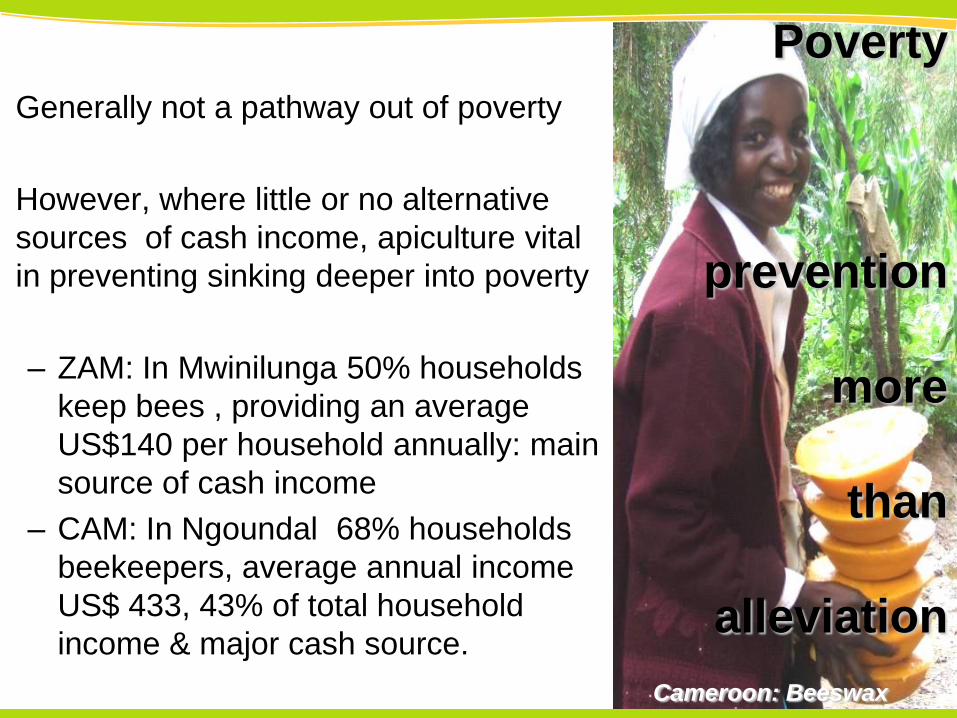

• Generally not a pathway out of poverty

• However, where little or no alternative

sources of cash income, apiculture vital

in preventing sinking deeper into poverty

– ZAM: In Mwinilunga 50% households

keep bees , providing an average

US$140 per household annually: main

source of cash income

– CAM: In Ngoundal 68% households

beekeepers, average annual income

US$ 433, 43% of total household

income & major cash source.

Cameroon: Beeswax

Poverty

prevention

more

than

alleviation

Opportunities & challenges

• Introduction of modern technologies allows more women to

get involved in production

• Women already active in adding value –especially in Zambia

• Low entry barriers: both poor & and wealthy households keep

bees (low costs, ease of entry & potentially high returns

• Lost opportunity: Low level value-adding in both countries

despite wide range of options available (low tech & cost): e.g.

candles, creams, wines, beers

• National and African regional markets highly promising and

easy to reach

• Export & specialty markets increasingly open (propolis,

organic, ethical & fair trade, community trade etc.)

• Need strong, financed national institutions coordinating sector

support, with clear roles and responsibilities and supporting

legal frameworks to enforce and protect.

• Increased coordination and networking facilities (stakeholder

platforms, trade fairs, etc.) to avoid duplication & improve

collaboration

The balance....Livelihoods win and conservation looses, unless......

• Apiculture is more highly valued (economic, social &legal aspects and values)

• The value is sustained over a long term

• Can compete favorably with other forest uses &population pressure

• Unlikely that apiculture alone can achieve MDG goalsof poverty alleviation & environmental sustainability.

• ……instead consider apiculture as one activity indiversified livelihood portfolio

• External factors also have a major impact (agriculture,industry, infrastructure, market access politicalculture….)

• Value chain approach taken with business focusedsupport and capacity building for associations,cooperatives and service providers

• Coordinated and inter-sectoral policies and institutionscreated.

T’ank you plenty na!

On

mange

quoi?

La

forêt....