Embed Size (px)

Citation preview

The SaaS Revolution from India

A Joint Study by Google India & Accel Partners

Objective: Identify key opportunity areas, business models and challenges for Indian SaaS companies in the global market

Methodology: ● Primary Interviews with Indian SaaS companies across segments (Oct-Dec 2015)

● Primary Interactions with investors active in this space, SIs, educational institutes (Oct-Dec 2015)

● Google India primary research for SMB consumers targeted to the US (n=200x4, Jan-Feb 2016)

● Secondary Research by Zinnov conducted in India

● Benchmark business metrics from Accel India SaaS portfolio

● Google search trends data for the calendar years 2013, 2014 and 2015

# 1

Executive Summary

Global SaaS Industry

● Global SaaS to be a $132B revenue industry by 2020 driven by SMB demand

● Purpose-built high quality SaaS products will replace generic B2B “single software providers” of today

● Online discovery and adoption will increasingly reduce dependence on Feet-on-Street (FOS) sales

● New and innovative monetization methods are emerging beyond basic software subscription models, driven by verticalization

SaaS business from India

● India will likely grow to be a $10B revenue industry by 2025 (8% of Global SMB SaaS)

● Categories such as CRM, Data Visualization, HR, Marketing, Healthcare & Education are ripe for big SaaS companies to emerge out of India

● As SaaS shifts to mobile, SaaS companies in India will have an edge - India being a mobile first country

● Cost advantage on engineering, inside sales, onboarding and support will allow Indian SaaS firms to aggressively enter and scale the SMB market

● High growth SaaS companies from India need to build world-class products, size the market accurately, focus on competitive pricing and have a high CAC budget to fuel initial growth

● India & other emerging markets’ enterprises starting to adopt Indian SaaS products

Source: Based on analyses by Zinnov and Accel

# 2

A. The hyper-growing SaaS Industry

B. India’s place in the SaaS hyper-growth

C. SaaS for Emerging Markets

D. Key takeaways for the SaaS Industry & Entrepreneurs from India

Contents

# 3

A1. Fast growing Global Public Cloud Computing Market

Approximate figures for ease of computation

Key drivers for Public Cloud growth

● 2x growth in US SMB Cloud adoption by 20201,2

● Strong demand for Cloud Services in Europe &

Asia

● Strong demand for vertical specific solutions

Global Public Cloud Computing Market1,2

Revenue in USD Billion

56

76

175

2020 2013 2015

# 4

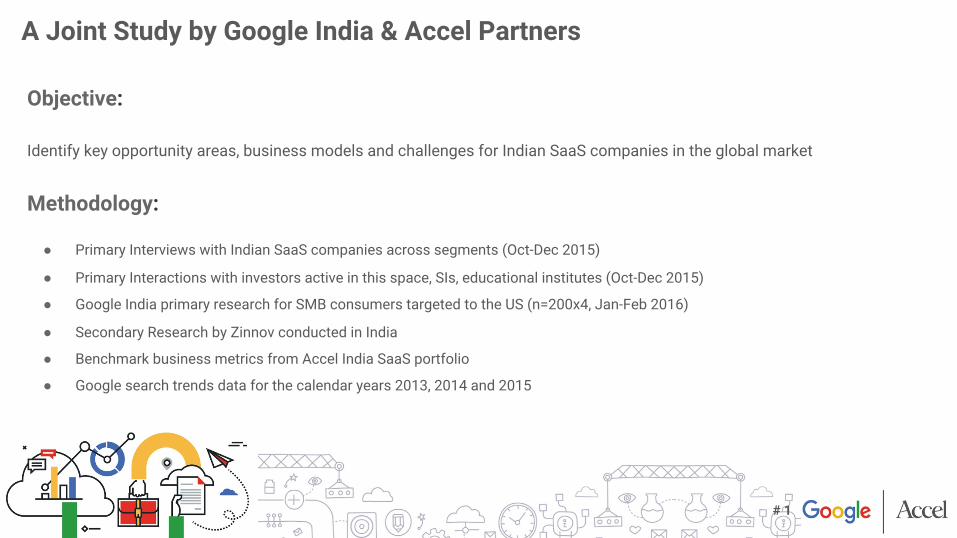

A2. SaaS will be a key driver for total Public Cloud adoption

a:: Others include IaaS, PaaS and BPaaS

51

68

5 8

43

2015 2013 2020

132

Othersa

SaaS

Public Cloud revenue split by sub segments1,2 Key drivers of SaaS adoption

Revenue in USD Billion

● Increasing availability of higher quality SaaS

products

● Faster time to market

● Rapid growth in SaaS Cloud adoption by US and

Europe SMBs

● Increased visibility of business metrics leading to

control over profitability and costs

● Shift of IT from Capex to Opex model

>75% of Public Cloud revenues from SaaS1,2

# 5

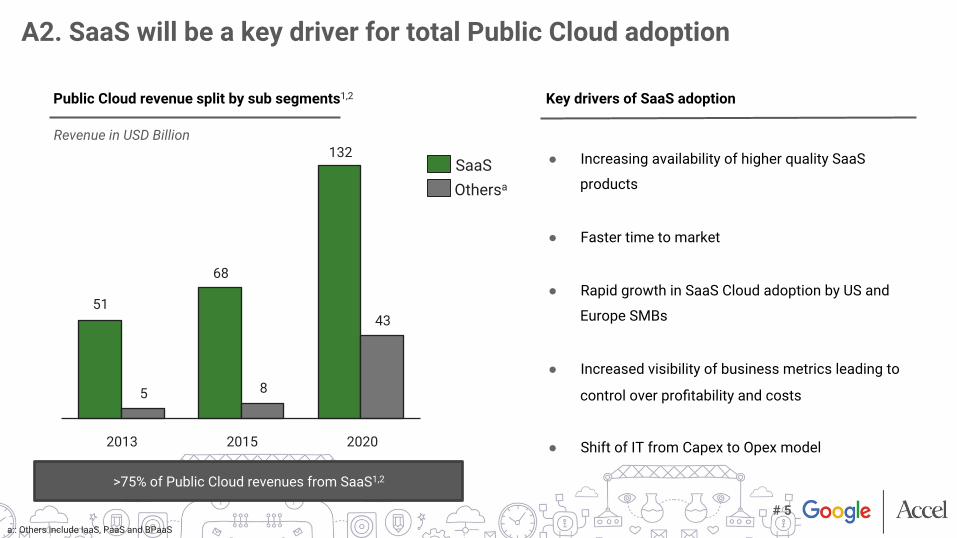

● Instant Collaboration for SMBs on the go: 40% US SMBs currently use instant collaboration software

● Mobile SMBs to increasingly adopt file sharing: 37% US SMBs currently use SaaS file sharing on the go

● Cloud based accounting to optimize cash flows: 31% US SMBs currently use SaaS Accounting

A3. Highly underpenetrated SMB markets for SaaS

10% SMB SaaS

90% Non-SaaS

(Opportunity)

Strong initial traction among SMBs1,2

Underpenetrated SMB software markets – 2015 1,2

Revenue in USD B

SMB will overtake Enterprise SaaS Market before 20201,2

Revenue in USD B

2020

132

76

2015

24

44

68

56

SMB SaaS Enterprise SaaS

$200B

$24B

#6

4.3

2.1 1.9 1.9

1.3 1.2 1.1 1.0 0.9 0.9 0.5 0.4 0.4 0.3 0.3 0.3

0.1 0.1 0.0

A4. Purpose-built SaaS products gaining traction

Advertising

BPM Marketing Finance Sales BI/ Analytics

Developers Collaboration

Identity HR Web Design

Education IT (Mgmt, Automation)

Vertical Specific

SaaS (Travel,

Retail, etc.)

Health care

File Sharing

and Backup

ERP Services and

Support

Productivity

Opportunity for many specialized SaaS companies

Global SaaS funding between 2011 and 20142,5

Funding in USD Billion

# 7

A5. Online product discovery is critical for growth

100 120

180

2011 2013 2015

Online search interest growth for SaaS products4

3% 5%

9%

2011 2013 2015

Brand comparison searches4

5 7

9

2011 2013 2015

Time spent by users on review sites & marketplaces (mins)10

95%

5%

Yes No

Do you prefer to "silently" try before buying a product?6

More information seekers More comparisons of products

Free trial and Freemium is a must More focus on features and user reviews than on FOS sales

Customer behavior is changing

Online is becoming the key driver

# 8

A6. New monetization models to emerge

Per User Most common and easy for enterprises to understand; pricing trends

moving from annual to quarterly to monthly

Aligning to usage, direct outcome or value-based: e.g. percentage of

payments processed (Stripe), unit price X number of key interactions,

percentage of savings realized

Free for enterprises, revenue from suppliers to the enterprises e.g.

Zenefits

Free for enterprises, revenue from services and premium products e.g.

Cloudera, mongoDB

Model Highlights

Will amplify the growth of

verticalized SaaS

Source: Models are publicly abvailable on their respective websites

Usage / Value / Outcome Based

Monetizing Network Effects

Freemium / Open Source

# 9

A. The hyper-growing SaaS Industry

B. India’s place in the SaaS hyper-growth

C. SaaS for Emerging Markets

D. Key takeaways for the SaaS Industry & Entrepreneurs from India

Contents

# 10

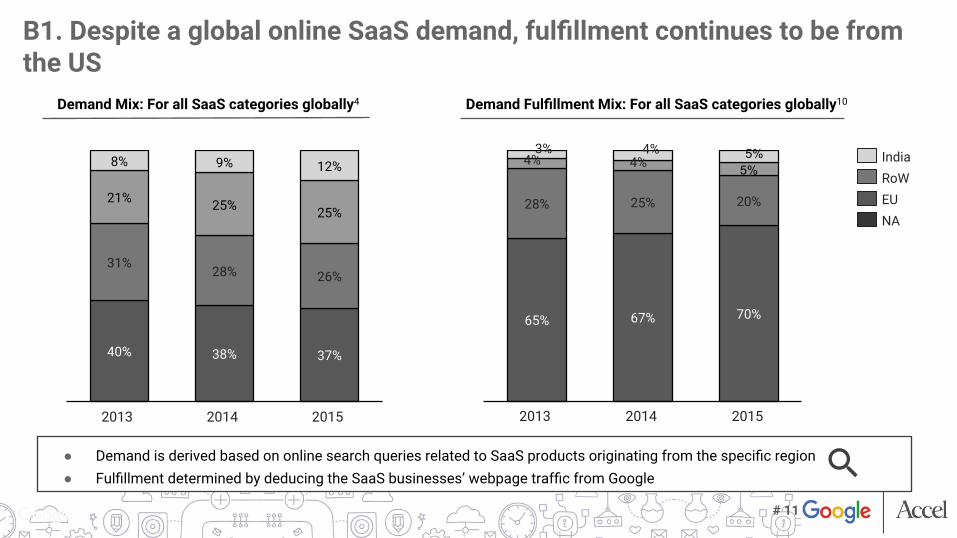

● Demand is derived based on online search queries related to SaaS products originating from the specific region ● Fulfillment determined by deducing the SaaS businesses’ webpage traffic from Google

B1. Despite a global online SaaS demand, fulfillment continues to be from the US

40% 38% 37%

31% 28% 26%

21% 25% 25%

8% 9% 12%

2014 2015 2013

NA EU RoW India

65% 67% 70%

28% 25% 20%

5% 5%

2014 2015

4% 4%

2013

4% 3%

Demand Fulfillment Mix: For all SaaS categories globally10 Demand Mix: For all SaaS categories globally4

# 11

● Demand is derived based on online search queries related to SaaS products originating from the specific region ● Fulfillment determined by deducing the SaaS businesses’ webpage traffic from Google

B2. However, in select categories, India has changed the global fulfillment landscape

39% 37% 37%

28% 27% 25%

23% 24% 25%

10% 12% 13%

2015 2014 2013

NA EU RoW India

77% 62%

52%

17% 33%

42%

2015

4%

2014

4%

2013

5%

Demand Mix: For a category with strong Indian SaaS service providers4

Demand Fulfillment Mix: For a category with strong Indian SaaS service providers10

# 12

a:: A product manager may be from multiple backgrounds (eg. With US experience from the IT sector or consumer sector)

● Enough skilled PMs from IT(MNCs) and consumer companies transitioning to entrepreneurship - over 500 SaaS startups in India currently3

● Institutionalization of product community is starting to show

● MNC product managers skilled in operational aspects starting to move to business / P&L management ● High quality product thinking from consumer/mobile companies influencing SaaS industry

● Product learnings and insights from the US are seeing quick adoption among current SaaS companies

B3. Indian ecosystem ready for product driven SaaS founders Product managers by Country2

Thousands

Indian product managers’ background and experiencea; 2,3,4,7

Thousands

Indicators of ecosystem readiness

2020 2015 2010

IT

Consumer US

365

32

174

US UK Israel India

17 36

68

# 13

B4. India has the necessary developer horsepower to build SaaS

4x cost difference between India and the US By 2020, most of current UX developers will enhance skillsets to move towards UX design & aesthetics DevOps skills is on the critical path

India

130

25

Israel

5

UK

28

US

120

Cloud oriented software developers2,3,7,8

Skill Ready

SaaS Ready

Thousands

5

India

40

6

Israel

1

UK US

22

Skill Ready

SaaS Ready

UI/UX designers2,3,7,8

Thousands

SaaS Ready: Workforce that has working knowledge of / worked on cloud platforms for SaaS product development Skill Ready: Workforce that is ready to acquire an incremental skill with minimal effort and move to a new role/product

# 14

B5. India poised to gain from a shift to mobile in SaaS

Use of mobile/tablets for accessing SaaS6

Desktop SaaS users planning to use mobile/tablet to access SaaS6

2014 2016

40%

10% 80%

70% 40%

Primary Device

No

20%

80%

Yes

Mobile App/UX developers2

121

29 6

39

70

15

120

US UK Israel India

2015 2020

Thousands

Strong Indian talent pool for mobile applications owing to the fast growth in consumer internet industry

210

# 15

Sales closure rates from qualified leads (%)3 Preferred mode of product walkthrough before online SaaS purchase6

Over the phone or internet chat with

agent

Can understand it online myself

12%

In-person visit by salesman

71%

18%

High quality products with inbound sales has a

3x potential of growth than DIY

B6. Inside Sales is critical for business

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

DIY With Inside Sales support

15%

6% 10%

40%

100% of interviewed companies indicated the need for

inbound sales support for serious / non-free customers2

# 16

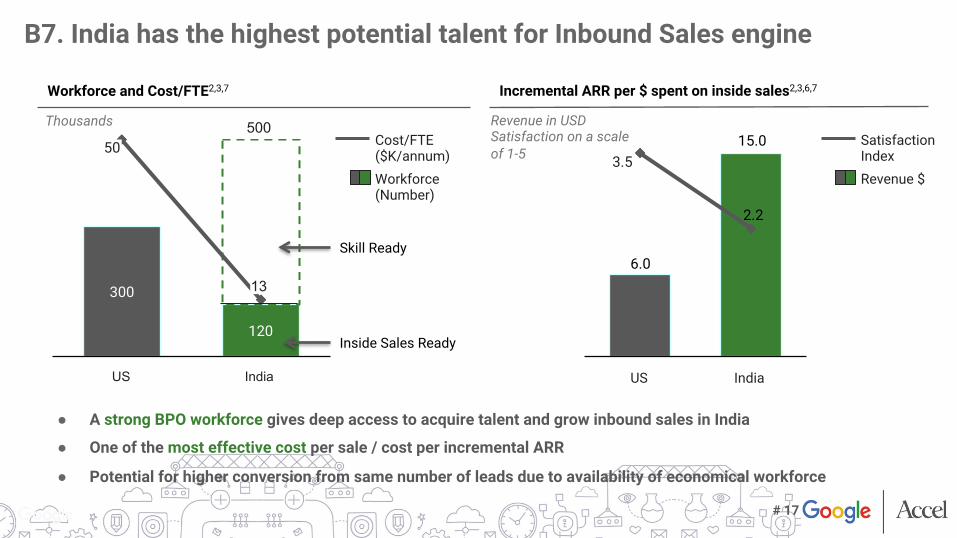

● A strong BPO workforce gives deep access to acquire talent and grow inbound sales in India

● One of the most effective cost per sale / cost per incremental ARR

● Potential for higher conversion from same number of leads due to availability of economical workforce

300

120

India

13

US

Skill Ready

Inside Sales Ready

Workforce �(Number)

Cost/FTE �($K/annum)

6.0

15.0

2.2

India US

Revenue $

Satisfaction �Index

Workforce and Cost/FTE2,3,7 Incremental ARR per $ spent on inside sales2,3,6,7

B7. India has the highest potential talent for Inbound Sales engine

Thousands Revenue in USD Satisfaction on a scale of 1-5 50

3.5

500

# 17

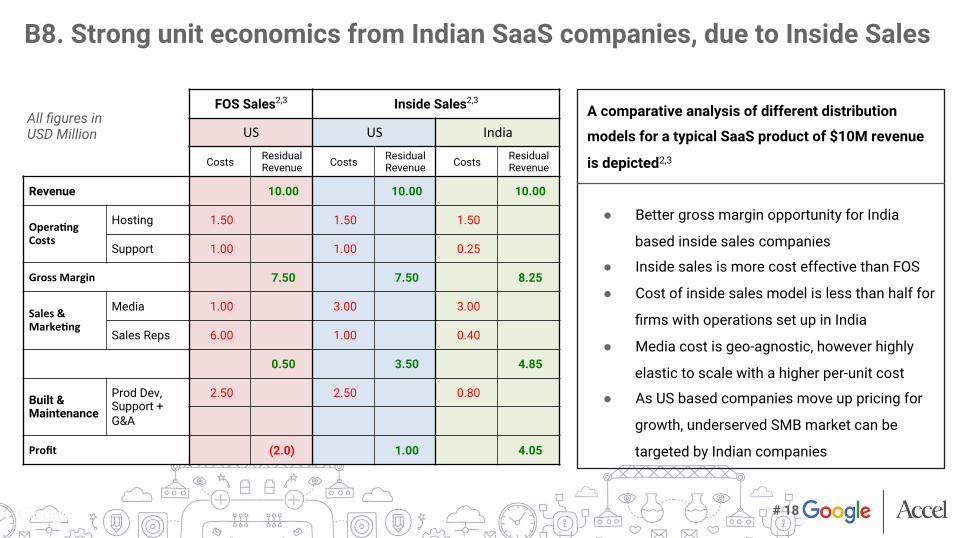

A comparative analysis of different distribution

models for a typical SaaS product of $10M revenue

is depicted2,3

● Better gross margin opportunity for India

based inside sales companies

● Inside sales is more cost effective than FOS

● Cost of inside sales model is less than half for

firms with operations set up in India

● Media cost is geo-agnostic, however highly

elastic to scale with a higher per-unit cost

● As US based companies move up pricing for

growth, underserved SMB market can be

targeted by Indian companies

FOS Sales2,3 Inside Sales2,3

US US India

Costs Residual Revenue Costs Residual

Revenue Costs Residual Revenue

Revenue 10.00 10.00 10.00

Opera&ngCosts

Hosting 1.50 1.50 1.50

Support 1.00 1.00 0.25

GrossMargin 7.50 7.50 8.25

Sales&Marke&ng

Media 1.00 3.00 3.00

Sales Reps 6.00 1.00 0.40

0.50 3.50 4.85

Built & Maintenance

Prod Dev, Support + G&A

2.50 2.50 0.80

Profit (2.0) 1.00 4.05

B8. Strong unit economics from Indian SaaS companies, due to Inside Sales

All figures in USD Million

# 18

B9. Focus on CAC during $1M - $5M ARR critical for hyper-growth

800 1,050

750 600

400

325

150 200

150

150

150 150

5-15M 1-5M

1,350

< 1M > 15M

1,050

1,525

950 1,000

Support cost

CAC Employee cost

Evolution of normalized costs with business size2,3

Costs per million dollars revenue (USD k)

Revenue mix (New/Existing customers)

80/20 70/30 50/50 40/60

Revenue churn2,3

● Cash negative initially with high churn and most cash outflow on CAC

● CAC highest between $1M to $5M ARR range

● Post $15M, recurring revenue from existing customers takes over

40%

25% 20%

15%

25%

15%

5%

-5% -10%

-5% 0% 5%

10% 15% 20% 25% 30% 35% 40% 45%

< 1M 1-5M 5-15M > 15M

Evolution of SaaS business metrics

Revenue

Revenue

# 19

Segments with high demand fulfillment from the US and a higher cost arbitrage for India present big opportunities for Indian SaaS companies to be built

Education

Web / App UX Design

HR / Identity Management

Sales / CRM

Data Management / Visualization

Web Hosting

Healthcare Software

Marketing & Ecom Enablement

Accounting, Billing & Collections

IT Security/ Antivirus

File Sharing & Backup

Productivity & Collaboration

BPM

Online Survey

Photo & Video Editing Events & Mtg Mgmt

Services, Support & Helpdesk

ERP

Finance, Payroll & Expenses

Retail

Developer Softwares

Logistics/Fleet/GPS

BI Analytics

Restaurant/ Hotel Mgmt.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%

1 1.5 2 2.5 3 3.5 4 4.5 5

Dem

and

Fulfi

llmen

t by

US

Cost Arbitrage for Businesses in India (Low to High)

Chart Legend: • Size of the bubble: Online interest

(search volumes) for the category in 20154

• X axis: Cost arbitrage for businesses in India for the segment3

• Y axis represents the traffic to SaaS businesses’ webpage10

B10. Market categories where big SaaS startups can emerge from India

# 20

0.6

2.5

10

2.6%

3.3%

8.0%

-

2.0

4.0

6.0

8.0

10.0

12.0

2015 2020 2025

Global SMB SaaS Fulfilment from India

Global Share of India

● Currently, a few horizontal segments where big SaaS companies catering to a Global market have emerged out of India

● Maturity and scale of most startups starting to happen

now

● By 2020, a good number of Indian companies will be targeting most opportunity areas

● By 2025, many of them would have scaled and captured

sizeable market share

B11. Indian SaaS industry can touch $10Bn by 2025

Indian SMB SaaS industry projection2,3 Highlights

Revenue in USD Billion

A perfect storm of a) changing customer behavior, b) market accessibility & growth, c) talent availability and d) cost advantage has created an incredible setting for massive global SaaS companies to be built out of India

# 21

A. The hyper-growing SaaS Industry

B. India’s place in the SaaS hyper-growth

C. SaaS for Emerging Markets

D. Key takeaways for the SaaS Industry & Entrepreneurs from India

Contents

# 22

Lack of legacy software • Many large enterprises in EMs have adopted only basic software and are now open to new software that improves productivity and

increases revenue making it much easier to adopt Cloud

Product fit • Products are being built to meet the unique needs in emerging markets (e.g. mobile-first) and at EM price points

Costs & profitability for customer • Cloud models for technology adoption are being accepted given low upfront costs • Increasing cost of skilled labor driving productivity needs across enterprises • Fastest adoption of SaaS in revenue generating functions

Sales model • Enterprises still need a “high-touch” selling model, however, the cost of in-market sales teams much lower in EMs

Opportunities across verticals • New age companies in EMs (e.g. ecommerce) are becoming the first to embrace SaaS products. Other verticals quickly catching up

Source: Based on analyses by Zinnov and Accel

C1. Emerging Markets could become large Enterprise SaaS markets over the next decade

# 23

Source: Based on analyses by Zinnov and Accel

Customize for local languages • Local languages are the primary business language for most of the SMBs in EMs

Mobile-first • Be mobile first rather than mobile-enabled

Offer value & innovate on pricing • Use network effects to offer value based verticalized SaaS offerings - scaling quickly, becomes all the more important • Align pricing to business objectives / outcome of the clients instead on purely relying on subscription based pricing

Online-offline integration • Build products that are able to work offline (cost of data still high) • Build low data consuming products (connectivity unreliable)

C2. Great SaaS products for EMs can learn from consumer products

# 24

A. The hyper-growing SaaS Industry

B. India’s place in the SaaS hyper-growth

C. SaaS for Emerging Markets

D. Key takeaways for the SaaS Industry & Entrepreneurs from India

Contents

# 25

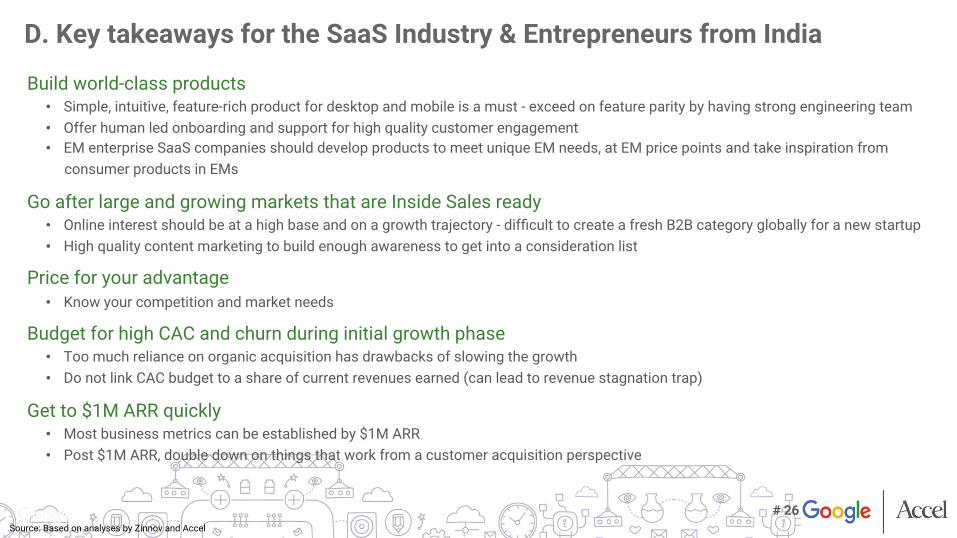

Build world-class products • Simple, intuitive, feature-rich product for desktop and mobile is a must - exceed on feature parity by having strong engineering team • Offer human led onboarding and support for high quality customer engagement • EM enterprise SaaS companies should develop products to meet unique EM needs, at EM price points and take inspiration from

consumer products in EMs

Go after large and growing markets that are Inside Sales ready • Online interest should be at a high base and on a growth trajectory - difficult to create a fresh B2B category globally for a new startup • High quality content marketing to build enough awareness to get into a consideration list

Price for your advantage • Know your competition and market needs

Budget for high CAC and churn during initial growth phase • Too much reliance on organic acquisition has drawbacks of slowing the growth • Do not link CAC budget to a share of current revenues earned (can lead to revenue stagnation trap)

Get to $1M ARR quickly • Most business metrics can be established by $1M ARR • Post $1M ARR, double down on things that work from a customer acquisition perspective

Source: Based on analyses by Zinnov and Accel

D. Key takeaways for the SaaS Industry & Entrepreneurs from India

# 26

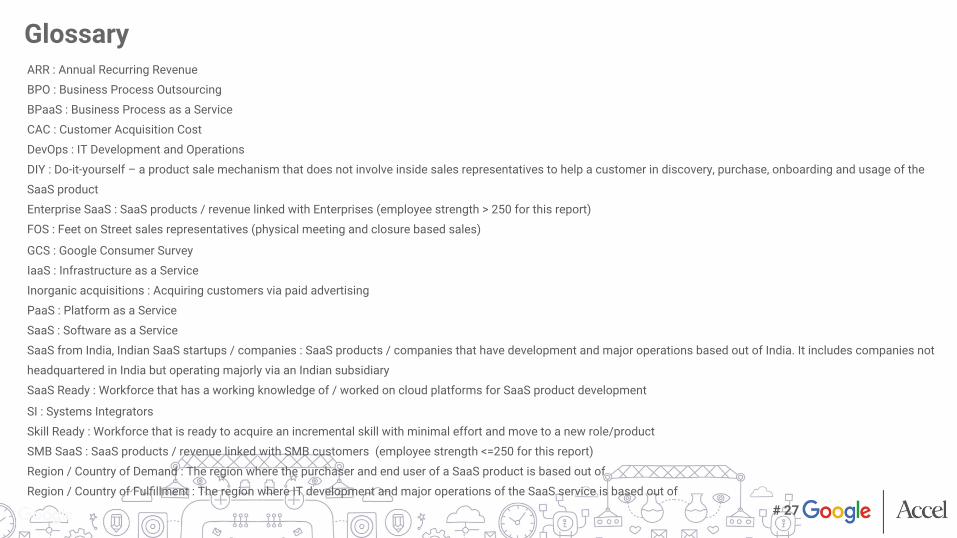

ARR : Annual Recurring Revenue

BPO : Business Process Outsourcing

BPaaS : Business Process as a Service

CAC : Customer Acquisition Cost

DevOps : IT Development and Operations

DIY : Do-it-yourself – a product sale mechanism that does not involve inside sales representatives to help a customer in discovery, purchase, onboarding and usage of the

SaaS product

Enterprise SaaS : SaaS products / revenue linked with Enterprises (employee strength > 250 for this report)

FOS : Feet on Street sales representatives (physical meeting and closure based sales)

GCS : Google Consumer Survey

IaaS : Infrastructure as a Service

Inorganic acquisitions : Acquiring customers via paid advertising

PaaS : Platform as a Service

SaaS : Software as a Service

SaaS from India, Indian SaaS startups / companies : SaaS products / companies that have development and major operations based out of India. It includes companies not

headquartered in India but operating majorly via an Indian subsidiary

SaaS Ready : Workforce that has a working knowledge of / worked on cloud platforms for SaaS product development

SI : Systems Integrators

Skill Ready : Workforce that is ready to acquire an incremental skill with minimal effort and move to a new role/product

SMB SaaS : SaaS products / revenue linked with SMB customers (employee strength <=250 for this report)

Region / Country of Demand : The region where the purchaser and end user of a SaaS product is based out of

Region / Country of Fulfillment : The region where IT development and major operations of the SaaS service is based out of

Glossary

# 27

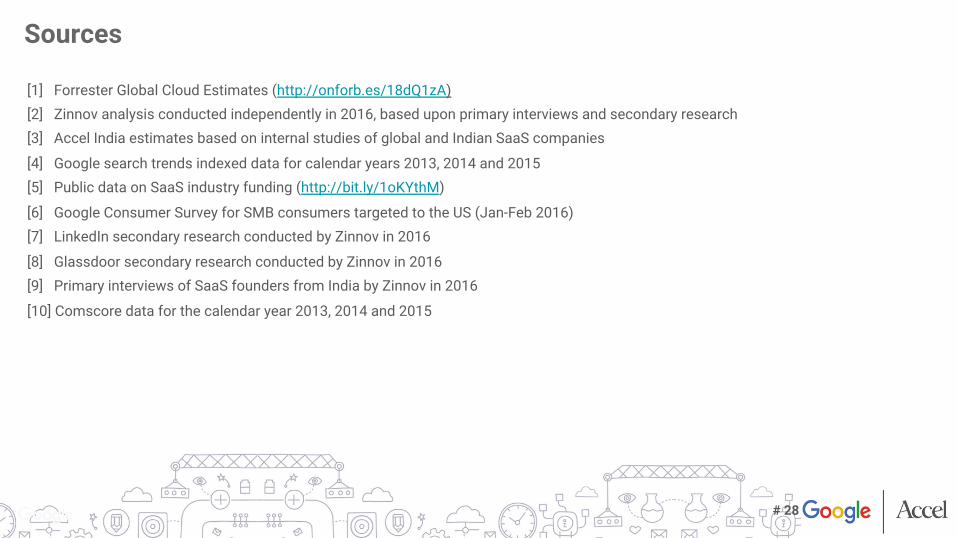

[1] Forrester Global Cloud Estimates (http://onforb.es/18dQ1zA) [2] Zinnov analysis conducted independently in 2016, based upon primary interviews and secondary research [3] Accel India estimates based on internal studies of global and Indian SaaS companies

[4] Google search trends indexed data for calendar years 2013, 2014 and 2015 [5] Public data on SaaS industry funding (http://bit.ly/1oKYthM)

[6] Google Consumer Survey for SMB consumers targeted to the US (Jan-Feb 2016) [7] LinkedIn secondary research conducted by Zinnov in 2016

[8] Glassdoor secondary research conducted by Zinnov in 2016 [9] Primary interviews of SaaS founders from India by Zinnov in 2016

[10] Comscore data for the calendar year 2013, 2014 and 2015

Sources

# 28

Rajan Anandan MD & VP, Google India & South-East Asia Shekhar Kirani Partner, Accel India

Amiya Adwitiya Accel India [email protected] Arpit Jaiswal Industry Manager - Software as a Service, Google India [email protected] Jayank Srivastava Analytical Lead, Google India Karan Gambhir Industry Head - Technology, Google India Nitin Bawankule Director – Google India & South Asia Frontier

Contact

# 29

The information and opinions in this Report have been prepared or compiled by ACCEL PARTNERS and are subject to change/modification without any notice. The information contained in this Report is believed to be accurate at the time of date of issue of this Report, but no representation or warranty is given (express or implied) as to its accuracy, completeness or correctness. ACCEL PARTNERS accepts no liability whatsoever for any direct, indirect or consequential loss or damage arising in any way from any use of or reliance placed on this material for any purpose. The contents of this Report are the copyright of ACCEL PARTNERS. Nothing on this Report constitutes advice, nor creates any contractual relationship. Google does not take any responsibility on the findings of the research or any data/methods used by third parties in compilation of the report.

Disclaimer

# 30