Embed Size (px)

Citation preview

3D Printing – Opportunities, Risks and Path Forward

2015

2

Agenda

• Market Trends – Current and Emerging State

• Adoption Considerations

• Path Forward

3

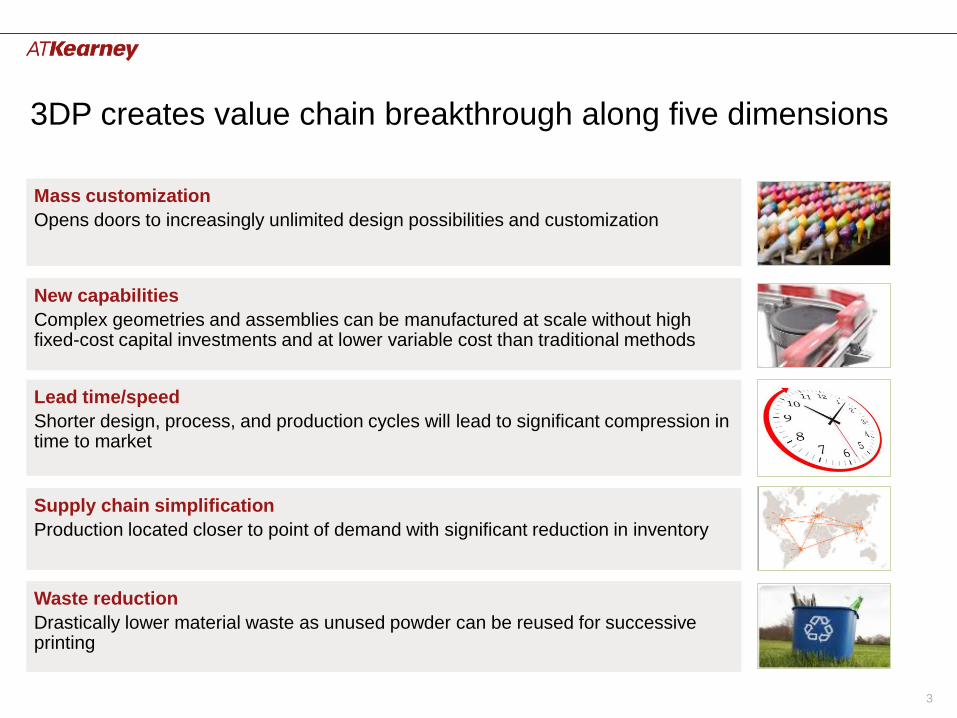

3DP creates value chain breakthrough along five dimensions

Mass customization

Opens doors to increasingly unlimited design possibilities and customization

New capabilities

Complex geometries and assemblies can be manufactured at scale without high fixed-cost capital investments and at lower variable cost than traditional methods

Supply chain simplification

Production located closer to point of demand with significant reduction in inventory

Waste reduction

Drastically lower material waste as unused powder can be reused for successive printing

Lead time/speed

Shorter design, process, and production cycles will lead to significant compression in time to market

4

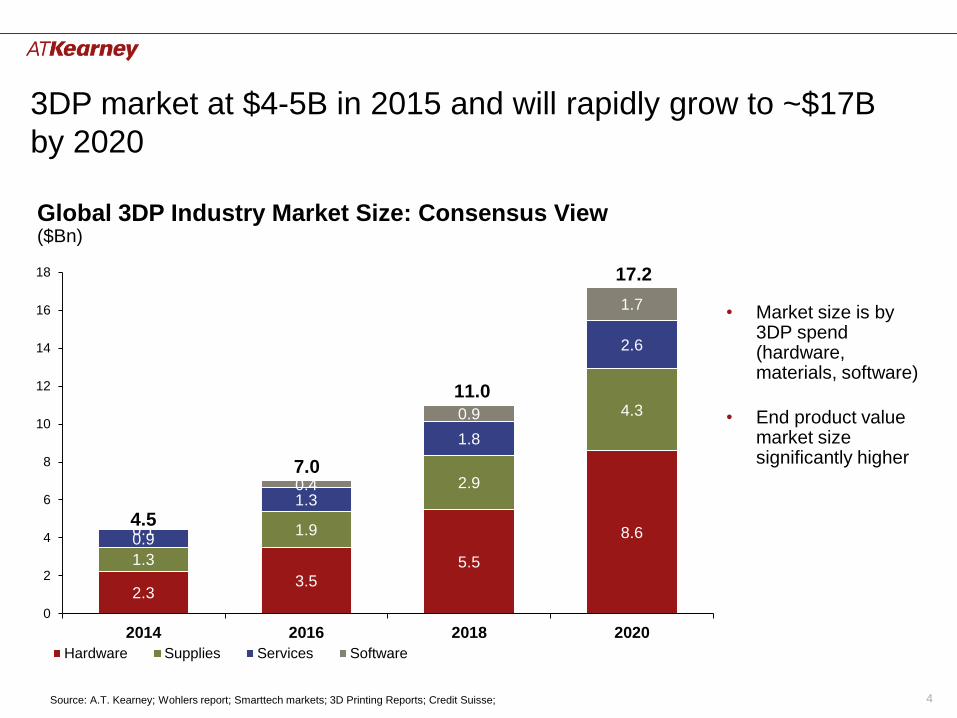

3DP market at $4-5B in 2015 and will rapidly grow to ~$17B

by 2020

Global 3DP Industry Market Size: Consensus View($Bn)

Source: A.T. Kearney; Wohlers report; Smarttech markets; 3D Printing Reports; Credit Suisse;

2.33.5

5.5

8.6

1.3

1.9

2.9

4.3

0.9

1.3

1.8

2.6

0.1

0.4

0.9

1.7

0

2

4

6

8

10

12

14

16

18

2014 2016 2018 2020

Hardware Supplies Services Software

4.5

7.0

11.0

17.2

• Market size is by 3DP spend (hardware, materials, software)

• End product value market size significantly higher

5

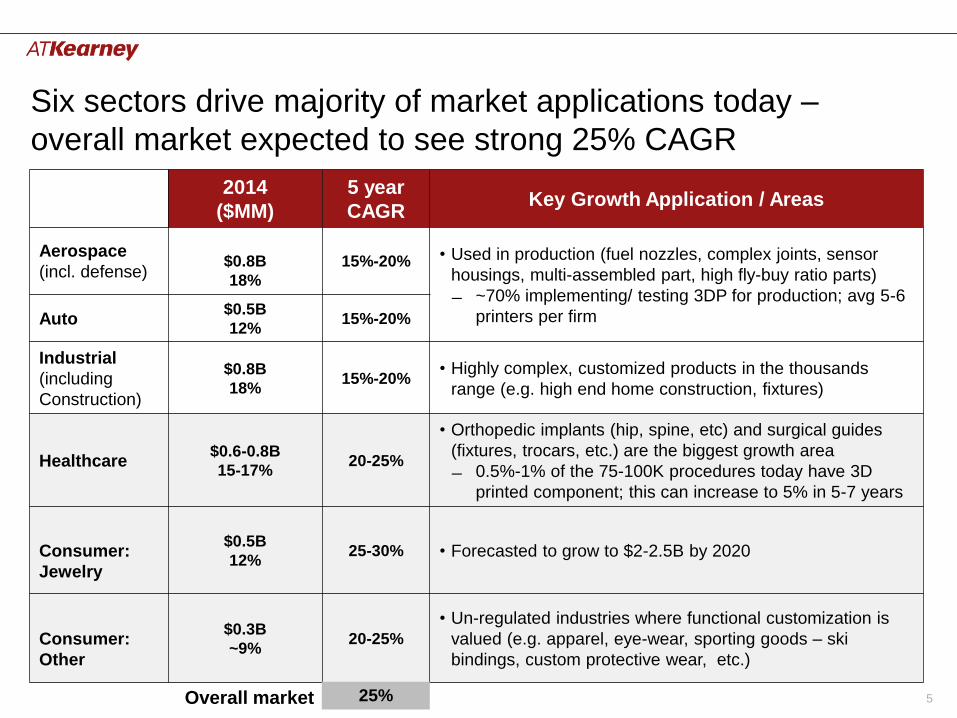

Six sectors drive majority of market applications today –

overall market expected to see strong 25% CAGR

2014

($MM)

5 year

CAGRKey Growth Application / Areas

Aerospace

(incl. defense)$0.8B

18%

15%-20% • Used in production (fuel nozzles, complex joints, sensor

housings, multi-assembled part, high fly-buy ratio parts)

~70% implementing/ testing 3DP for production; avg 5-6

printers per firmAuto$0.5B

12%15%-20%

Industrial

(including

Construction)

$0.8B

18%15%-20%

• Highly complex, customized products in the thousands

range (e.g. high end home construction, fixtures)

Healthcare$0.6-0.8B

15-17%20-25%

• Orthopedic implants (hip, spine, etc) and surgical guides

(fixtures, trocars, etc.) are the biggest growth area

0.5%-1% of the 75-100K procedures today have 3D

printed component; this can increase to 5% in 5-7 years

Consumer:

Jewelry

$0.5B

12%25-30% • Forecasted to grow to $2-2.5B by 2020

Consumer:

Other

$0.3B

~9%20-25%

• Un-regulated industries where functional customization is

valued (e.g. apparel, eye-wear, sporting goods – ski

bindings, custom protective wear, etc.)

Overall market 25%

6

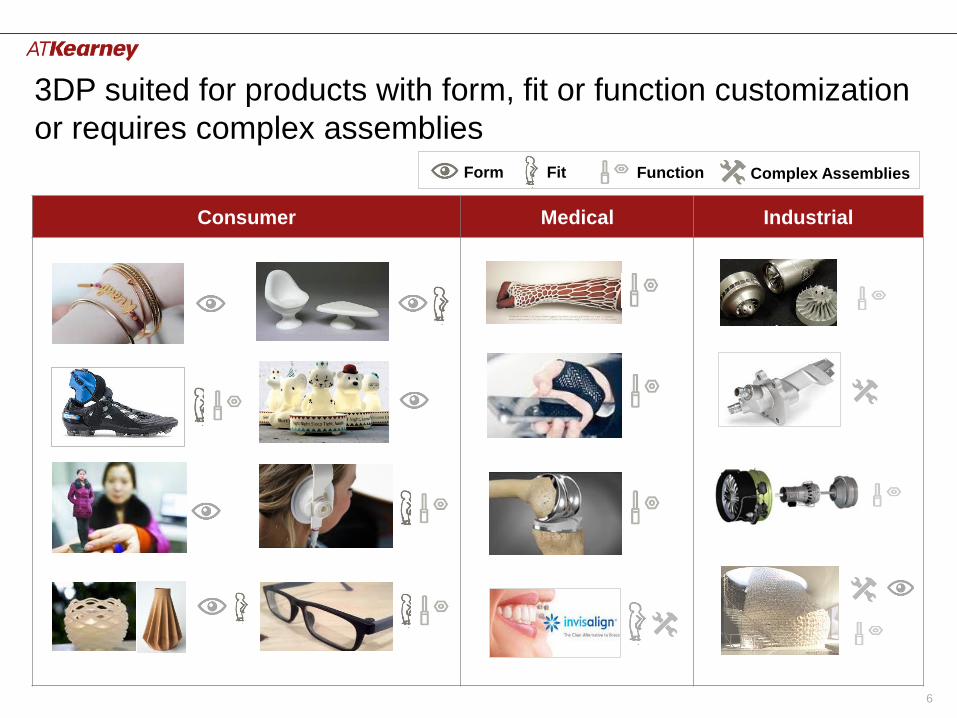

3DP suited for products with form, fit or function customization

or requires complex assemblies

Consumer Medical Industrial

Form Fit Function Complex Assemblies

7

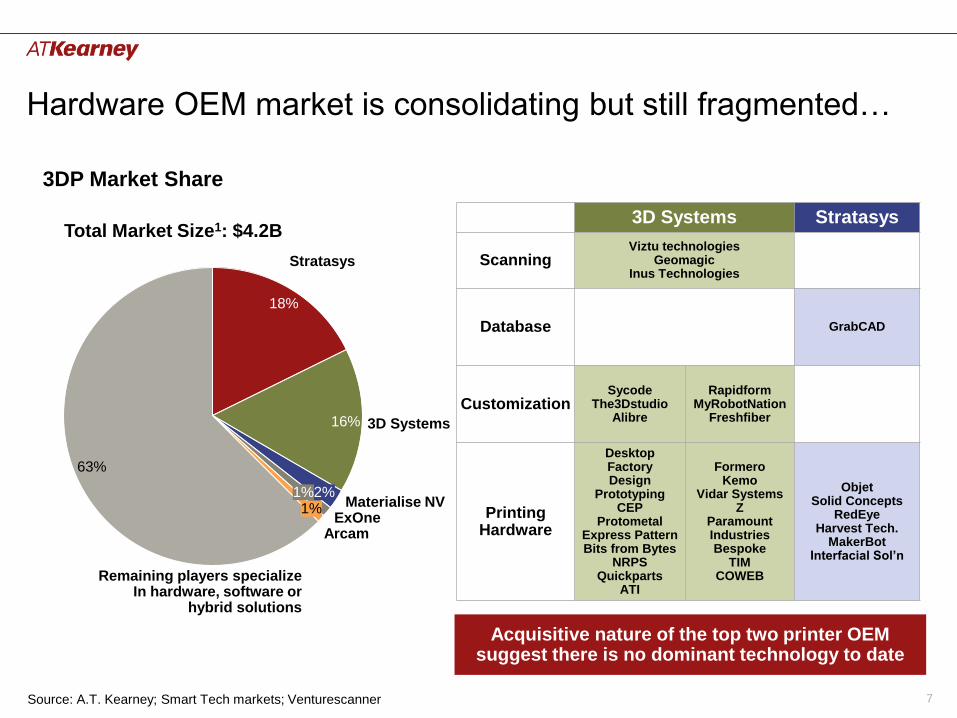

Hardware OEM market is consolidating but still fragmented…

Source: A.T. Kearney; Smart Tech markets; Venturescanner

3DP Market Share

Remaining players specializeIn hardware, software or

hybrid solutions

ExOne1%

Stratasys

Arcam

18%

63%

2%

3D Systems

1%

16%

Materialise NV

Total Market Size1: $4.2B3D Systems Stratasys

ScanningViztu technologies

GeomagicInus Technologies

Database GrabCAD

CustomizationSycode

The3DstudioAlibre

RapidformMyRobotNation

Freshfiber

Printing Hardware

DesktopFactoryDesign

Prototyping CEP

ProtometalExpress PatternBits from Bytes

NRPSQuickparts

ATI

FormeroKemo

Vidar SystemsZ

Paramount IndustriesBespoke

TIM COWEB

ObjetSolid Concepts

RedEyeHarvest Tech.

MakerBotInterfacial Sol’n

Acquisitive nature of the top two printer OEM suggest there is no dominant technology to date

8

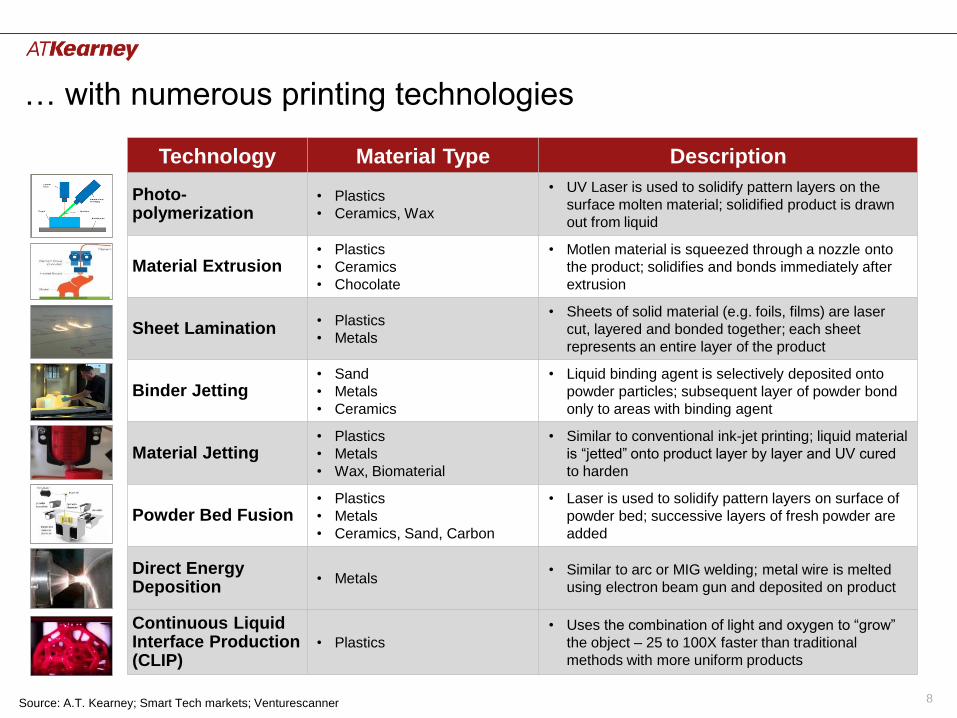

… with numerous printing technologies

Source: A.T. Kearney; Smart Tech markets; Venturescanner

Technology Material Type Description

Photo-polymerization

• Plastics

• Ceramics, Wax

• UV Laser is used to solidify pattern layers on the

surface molten material; solidified product is drawn

out from liquid

Material Extrusion• Plastics

• Ceramics

• Chocolate

• Motlen material is squeezed through a nozzle onto

the product; solidifies and bonds immediately after

extrusion

Sheet Lamination• Plastics

• Metals

• Sheets of solid material (e.g. foils, films) are laser

cut, layered and bonded together; each sheet

represents an entire layer of the product

Binder Jetting• Sand

• Metals

• Ceramics

• Liquid binding agent is selectively deposited onto

powder particles; subsequent layer of powder bond

only to areas with binding agent

Material Jetting• Plastics

• Metals

• Wax, Biomaterial

• Similar to conventional ink-jet printing; liquid material

is “jetted” onto product layer by layer and UV cured

to harden

Powder Bed Fusion• Plastics

• Metals

• Ceramics, Sand, Carbon

• Laser is used to solidify pattern layers on surface of

powder bed; successive layers of fresh powder are

added

Direct Energy Deposition

• Metals• Similar to arc or MIG welding; metal wire is melted

using electron beam gun and deposited on product

Continuous Liquid Interface Production (CLIP)

• Plastics

• Uses the combination of light and oxygen to “grow”

the object – 25 to 100X faster than traditional

methods with more uniform products

9

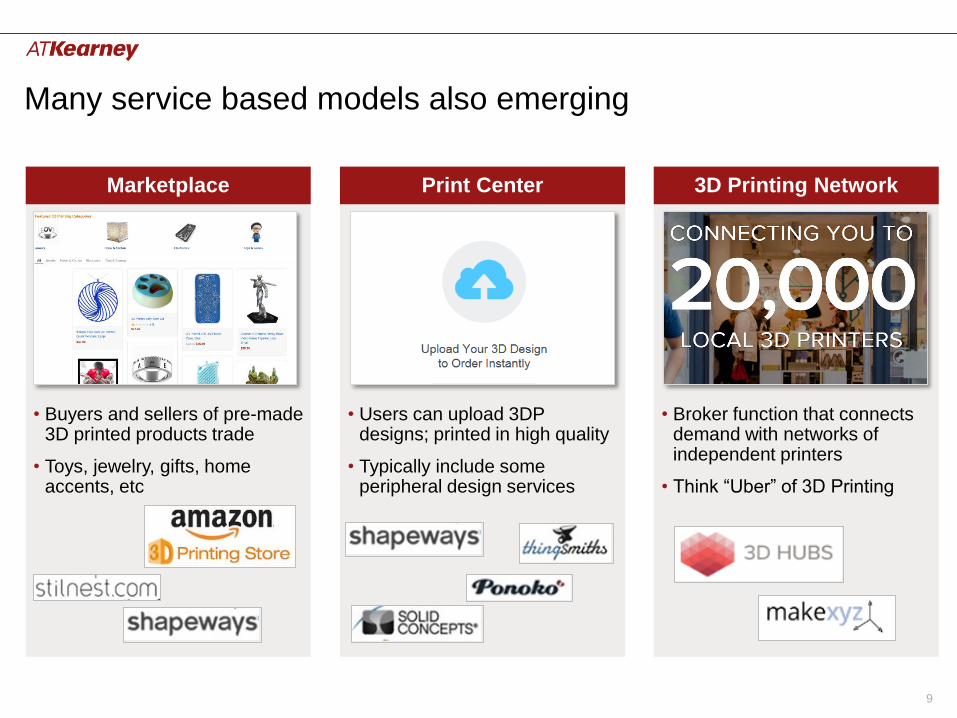

Many service based models also emerging

• Buyers and sellers of pre-made 3D printed products trade

• Toys, jewelry, gifts, home accents, etc

• Users can upload 3DP designs; printed in high quality

• Typically include some peripheral design services

• Broker function that connects demand with networks of independent printers

• Think “Uber” of 3D Printing

Marketplace Print Center 3D Printing Network

10

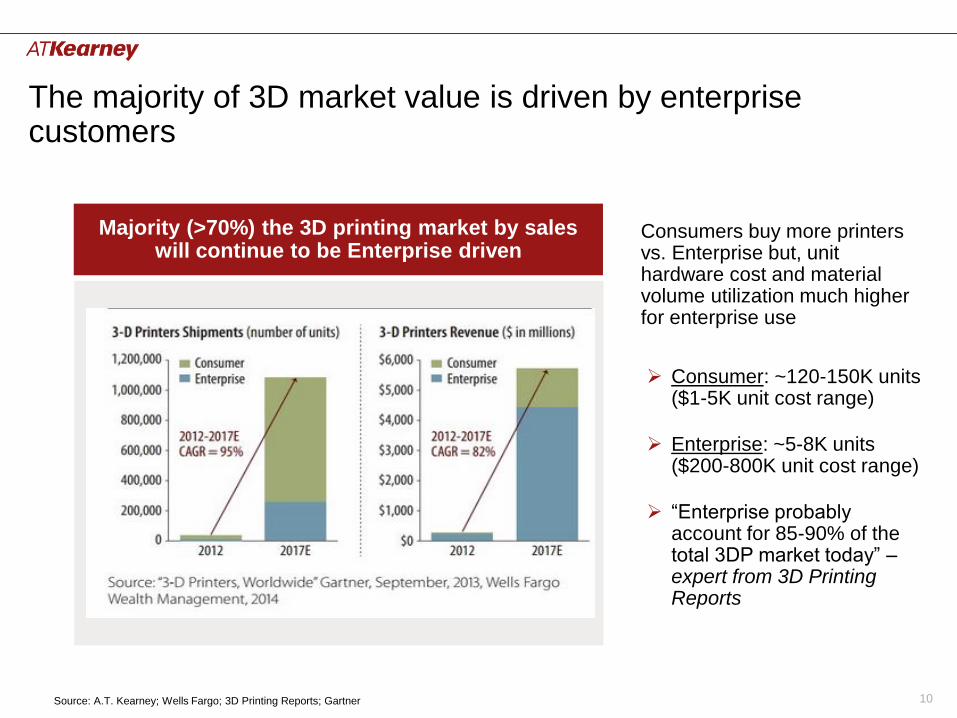

The majority of 3D market value is driven by enterprise customers

Source: A.T. Kearney; Wells Fargo; 3D Printing Reports; Gartner

Majority (>70%) the 3D printing market by sales will continue to be Enterprise driven

Consumers buy more printers vs. Enterprise but, unit hardware cost and material volume utilization much higher for enterprise use

Consumer: ~120-150K units ($1-5K unit cost range)

Enterprise: ~5-8K units ($200-800K unit cost range)

“Enterprise probably account for 85-90% of the total 3DP market today” –expert from 3D Printing Reports

11

Agenda

• Market Trends – Current and Emerging State

• Adoption Considerations

• Path Forward

12

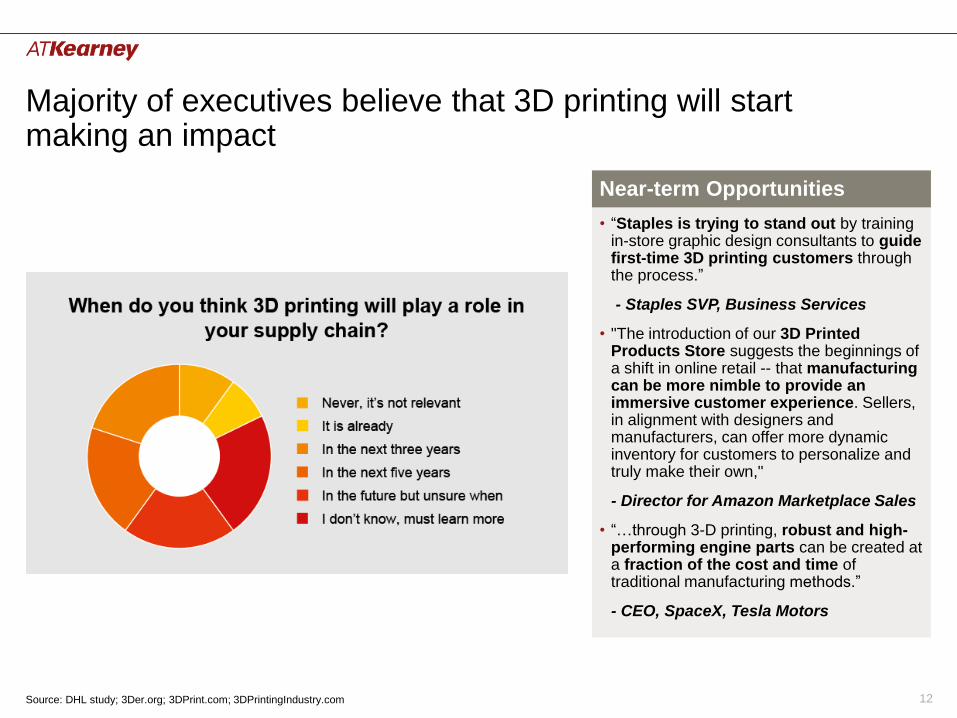

Majority of executives believe that 3D printing will start making an impact

Near-term Opportunities

• “Staples is trying to stand out by training in-store graphic design consultants to guide first-time 3D printing customers through the process.”

- Staples SVP, Business Services

• "The introduction of our 3D Printed Products Store suggests the beginnings of a shift in online retail -- that manufacturing can be more nimble to provide an immersive customer experience. Sellers, in alignment with designers and manufacturers, can offer more dynamic inventory for customers to personalize and truly make their own,"

- Director for Amazon Marketplace Sales

• “…through 3-D printing, robust and high-performing engine parts can be created at a fraction of the cost and time of traditional manufacturing methods.”

- CEO, SpaceX, Tesla Motors

Source: DHL study; 3Der.org; 3DPrint.com; 3DPrintingIndustry.com

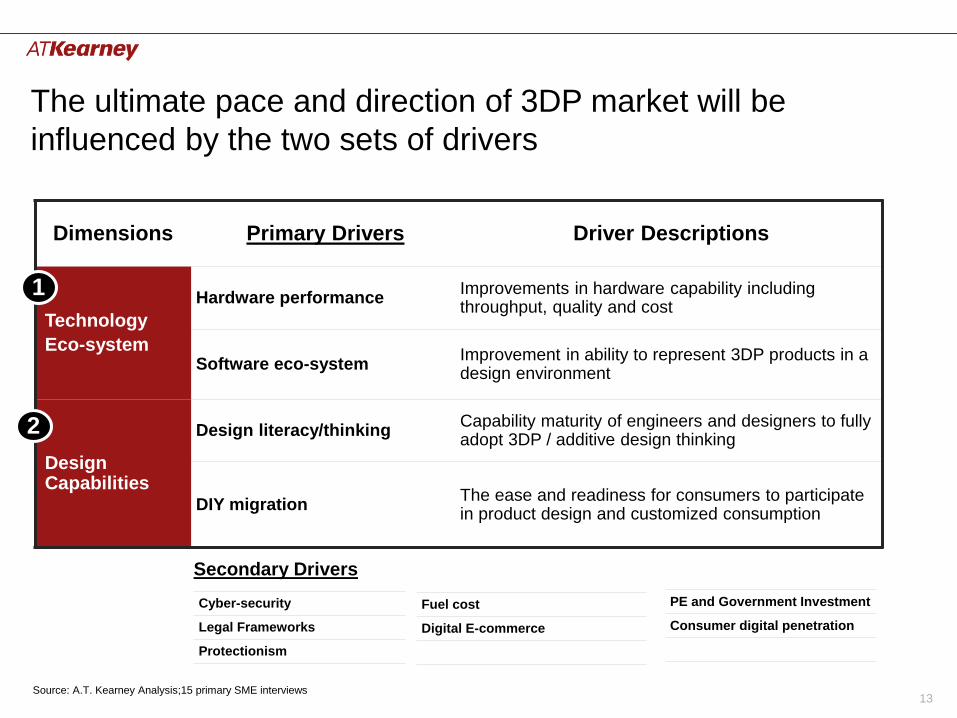

13

Dimensions Primary Drivers Driver Descriptions

Technology

Eco-system

Hardware performanceImprovements in hardware capability including throughput, quality and cost

Software eco-system Improvement in ability to represent 3DP products in a design environment

Design Capabilities

Design literacy/thinkingCapability maturity of engineers and designers to fully adopt 3DP / additive design thinking

DIY migrationThe ease and readiness for consumers to participate in product design and customized consumption

Source: A.T. Kearney Analysis;15 primary SME interviews

The ultimate pace and direction of 3DP market will be

influenced by the two sets of drivers

Cyber-security

Legal Frameworks

Protectionism

Fuel cost

Digital E-commerce

PE and Government Investment

Consumer digital penetration

Secondary Drivers

1

2

14

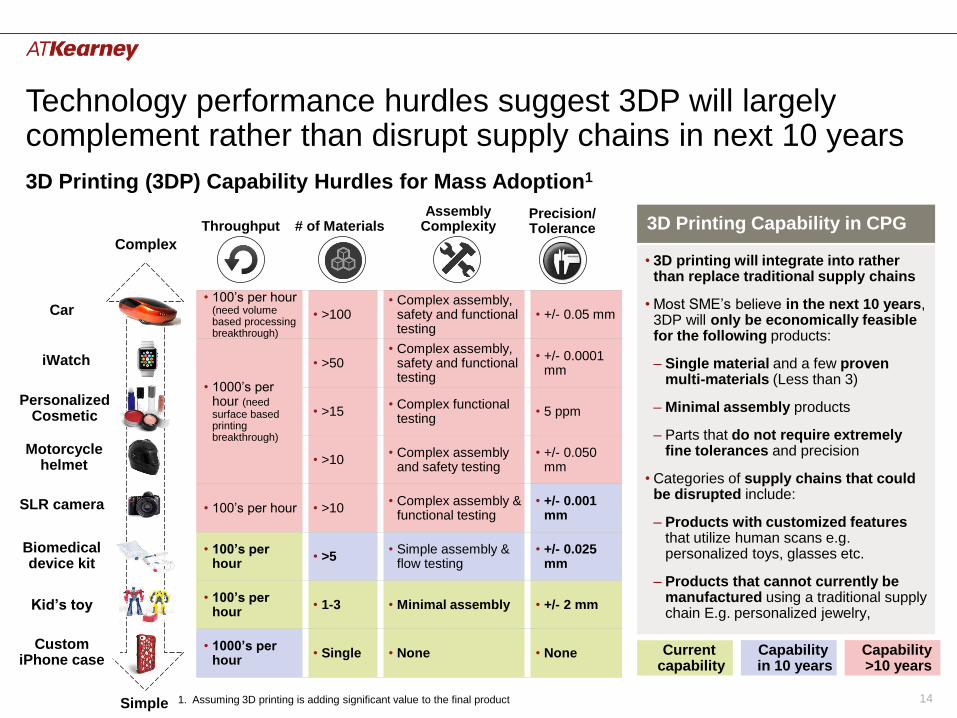

Technology performance hurdles suggest 3DP will largely complement rather than disrupt supply chains in next 10 years

• 100’s per hour (need volume based processing breakthrough)

• >100• Complex assembly,

safety and functional testing

• +/- 0.05 mm

• 1000’s per hour (need surface based printing breakthrough)

• >50• Complex assembly,

safety and functional testing

• +/- 0.0001 mm

• >15• Complex functional

testing• 5 ppm

• >10• Complex assembly

and safety testing• +/- 0.050

mm

• 100’s per hour • >10• Complex assembly &

functional testing• +/- 0.001

mm

• 100’s per hour

• >5• Simple assembly &

flow testing• +/- 0.025

mm

• 100’s per hour

• 1-3 • Minimal assembly • +/- 2 mm

• 1000’s per hour

• Single • None • None

Complex

Simple

3D Printing (3DP) Capability Hurdles for Mass Adoption1

Kid’s toy

Custom iPhone case

Biomedical device kit

SLR camera

Motorcycle helmet

Personalized Cosmetic

Car

iWatch

3D Printing Capability in CPGThroughput # of MaterialsAssembly

ComplexityPrecision/Tolerance

• 3D printing will integrate into rather than replace traditional supply chains

• Most SME’s believe in the next 10 years, 3DP will only be economically feasible for the following products:

– Single material and a few proven multi-materials (Less than 3)

– Minimal assembly products

– Parts that do not require extremely fine tolerances and precision

• Categories of supply chains that could be disrupted include:

– Products with customized features that utilize human scans e.g. personalized toys, glasses etc.

– Products that cannot currently be manufactured using a traditional supply chain E.g. personalized jewelry,

1. Assuming 3D printing is adding significant value to the final product

Capability in 10 years

Current capability

Capability >10 years

15

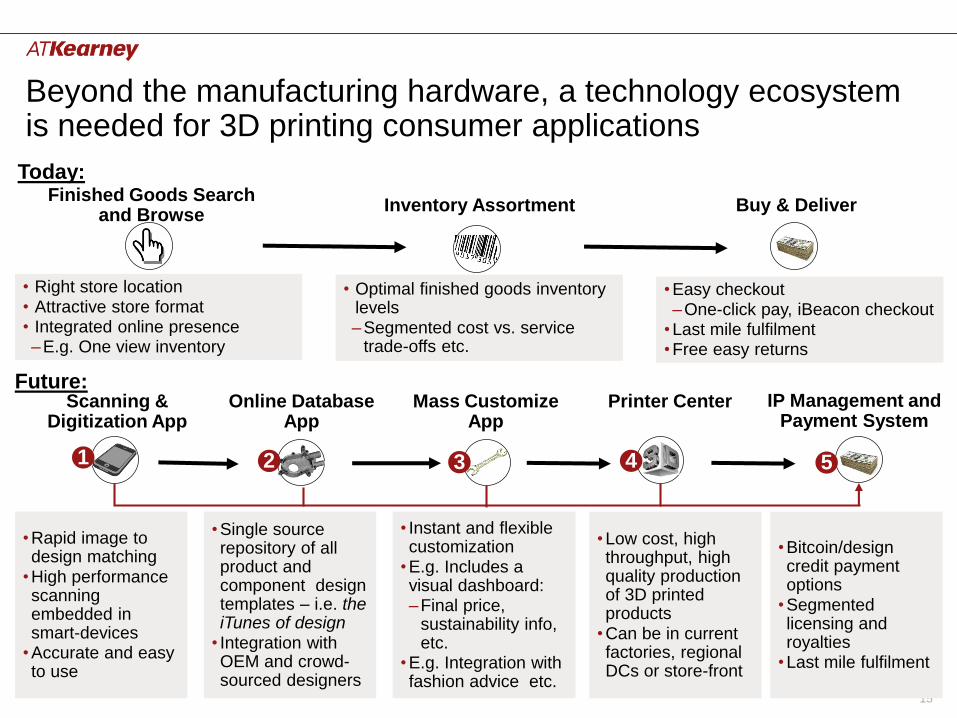

Beyond the manufacturing hardware, a technology ecosystem is needed for 3D printing consumer applications

Inventory AssortmentFinished Goods Search

and BrowseBuy & Deliver

Today:

• Rapid image to design matching

• High performance scanning embedded in smart-devices

• Accurate and easy to use

• Single source repository of all product and component design templates – i.e. the iTunes of design

• Integration with OEM and crowd-sourced designers

• Instant and flexible customization

• E.g. Includes a visual dashboard:–Final price,

sustainability info, etc.

• E.g. Integration with fashion advice etc.

• Low cost, high throughput, high quality production of 3D printed products

• Can be in current factories, regional DCs or store-front

• Bitcoin/design credit payment options

• Segmented licensing and royalties

• Last mile fulfilment

Online Database App

Scanning & Digitization App

Mass Customize App

Printer Center

2 3 41

Future:IP Management and

Payment System

• Right store location• Attractive store format• Integrated online presence–E.g. One view inventory

• Easy checkout–One-click pay, iBeacon checkout

• Last mile fulfilment• Free easy returns

• Optimal finished goods inventory levels–Segmented cost vs. service

trade-offs etc.

5

16

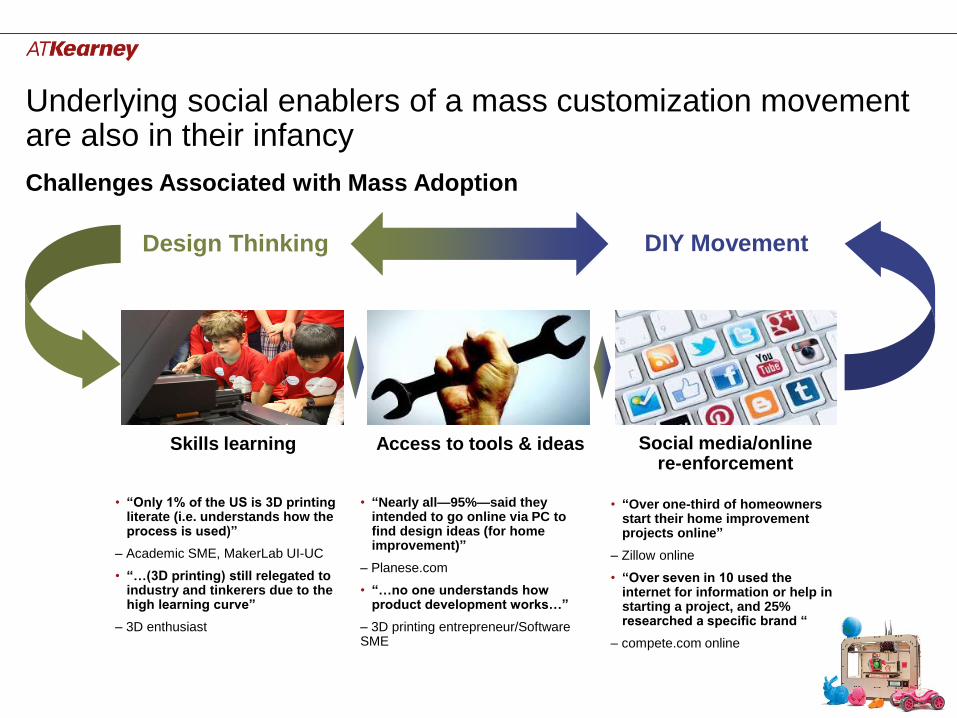

Underlying social enablers of a mass customization movement are also in their infancy

Challenges Associated with Mass Adoption

Design Thinking DIY Movement

Skills learning Access to tools & ideas Social media/online re-enforcement

• “Nearly all—95%—said they intended to go online via PC to find design ideas (for home improvement)”

– Planese.com

• “…no one understands how product development works…”

– 3D printing entrepreneur/Software SME

• “Over one-third of homeowners start their home improvement projects online”

– Zillow online

• “Over seven in 10 used the internet for information or help in starting a project, and 25% researched a specific brand “

– compete.com online

• “Only 1% of the US is 3D printing literate (i.e. understands how the process is used)”

– Academic SME, MakerLab UI-UC

• “…(3D printing) still relegated to industry and tinkerers due to the high learning curve”

– 3D enthusiast

17

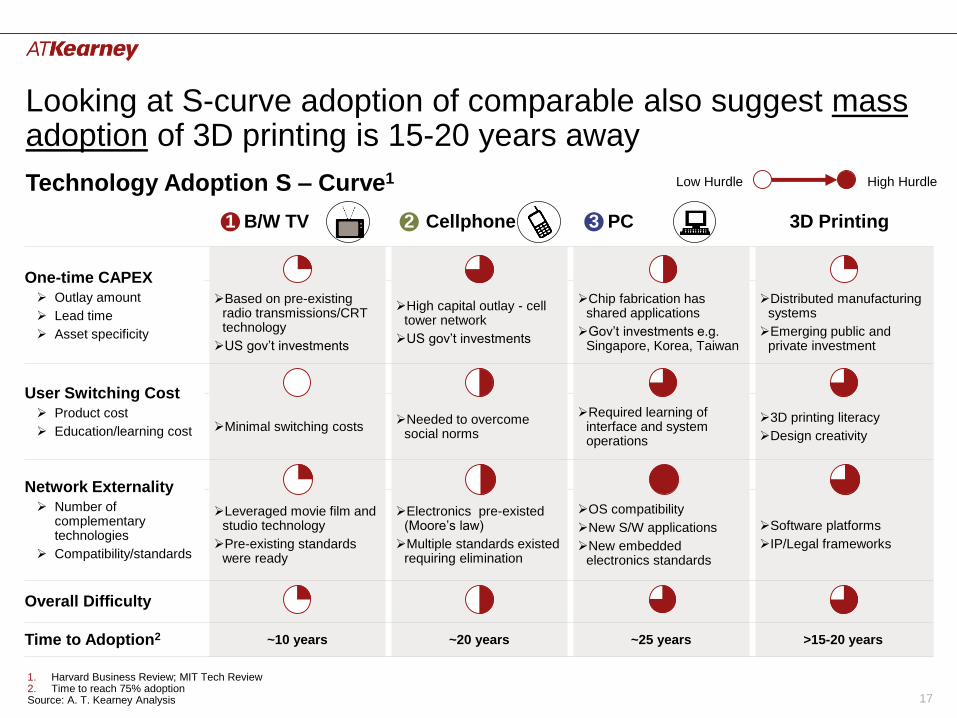

Looking at S-curve adoption of comparable also suggest mass adoption of 3D printing is 15-20 years away

B/W TV Cellphone PC 3D Printing

One-time CAPEX

Outlay amount

Lead time

Asset specificity

Based on pre-existingradio transmissions/CRT technology

US gov’t investments

High capital outlay - cell tower network

US gov’t investments

Chip fabrication has shared applications

Gov’t investments e.g. Singapore, Korea, Taiwan

Distributed manufacturing systems

Emerging public and private investment

User Switching Cost

Product cost

Education/learning cost Minimal switching costsNeeded to overcome

social norms

Required learning of interface and system operations

3D printing literacy

Design creativity

Network Externality

Number of complementarytechnologies

Compatibility/standards

Leveraged movie film andstudio technology

Pre-existing standards were ready

Electronics pre-existed (Moore’s law)

Multiple standards existed requiring elimination

OS compatibility

New S/W applications

New embedded electronics standards

Software platforms

IP/Legal frameworks

Overall Difficulty

Time to Adoption2 ~10 years ~20 years ~25 years >15-20 years

High HurdleLow HurdleTechnology Adoption S – Curve1

1. Harvard Business Review; MIT Tech Review2. Time to reach 75% adoptionSource: A. T. Kearney Analysis

1 2 3

18

Agenda

• Market Trends – Current and Emerging State

• Adoption Considerations

• Path Forward

19

Understand

How 3DP

Scenarios

Impact

Strategy

Conduct

Category

Hackathons

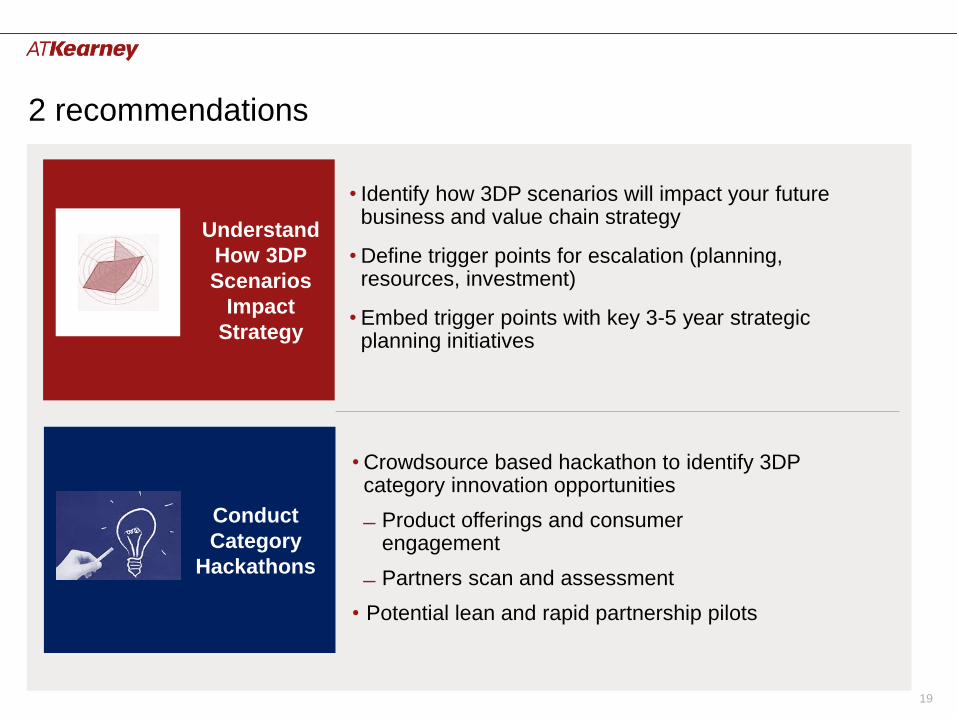

• Identify how 3DP scenarios will impact your future business and value chain strategy

• Define trigger points for escalation (planning, resources, investment)

• Embed trigger points with key 3-5 year strategic planning initiatives

• Crowdsource based hackathon to identify 3DP category innovation opportunities

Product offerings and consumer engagement

Partners scan and assessment

• Potential lean and rapid partnership pilots

2 recommendations

20

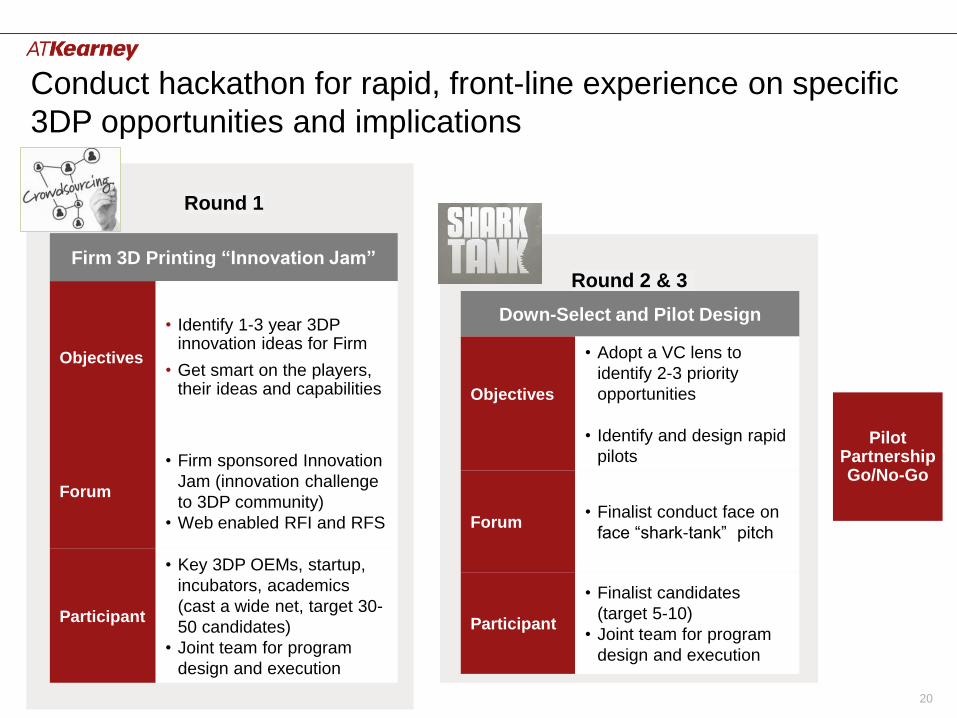

Conduct hackathon for rapid, front-line experience on specific

3DP opportunities and implications

Round 1

Round 2 & 3

Pilot Partnership Go/No-Go

Firm 3D Printing “Innovation Jam”

Objectives

• Identify 1-3 year 3DP innovation ideas for Firm

• Get smart on the players, their ideas and capabilities

Forum

• Firm sponsored Innovation

Jam (innovation challenge

to 3DP community)

• Web enabled RFI and RFS

Participant

• Key 3DP OEMs, startup,

incubators, academics

(cast a wide net, target 30-

50 candidates)

• Joint team for program

design and execution

Down-Select and Pilot Design

Objectives

• Adopt a VC lens to

identify 2-3 priority

opportunities

• Identify and design rapid

pilots

Forum• Finalist conduct face on

face “shark-tank” pitch

Participant

• Finalist candidates

(target 5-10)

• Joint team for program

design and execution

21

Check out the companion article

Read full article here

22

Americas Atlanta

Bogotá

Calgary

Chicago

Dallas

Detroit

Houston

Mexico City

New York

Palo Alto

San Francisco

São Paulo

Toronto

Washington, D.C.

Asia Pacific Bangkok

Beijing

Hong Kong

Jakarta

Kuala Lumpur

Melbourne

Mumbai

New Delhi

Seoul

Shanghai

Singapore

Sydney

Tokyo

Europe Amsterdam

Berlin

Brussels

Bucharest

Budapest

Copenhagen

Düsseldorf

Frankfurt

Helsinki

Istanbul

Kiev

Lisbon

Ljubljana

London

Madrid

Milan

Moscow

Munich

Oslo

Paris

Prague

Rome

Stockholm

Stuttgart

Vienna

Warsaw

Zurich

Middle East

and Africa

Abu Dhabi

Doha

Dubai

JohannesburgManama

Riyadh

A.T. Kearney is a leading global management consulting firm with offices in more than 40 countries. Since

1926, we have been trusted advisors to the world's foremost organizations. A.T. Kearney is a partner-owned

firm, committed to helping clients achieve immediate impact and growing advantage on their most mission-

critical issues. For more information, visit www.atkearney.com.