Embed Size (px)

Citation preview

Houston Economy in 2016:Another Slow Year as Oil Prices

Find New LowsRobert W. Gilmer, Ph.D.

C.T. Bauer College of BusinessFebruary 2015

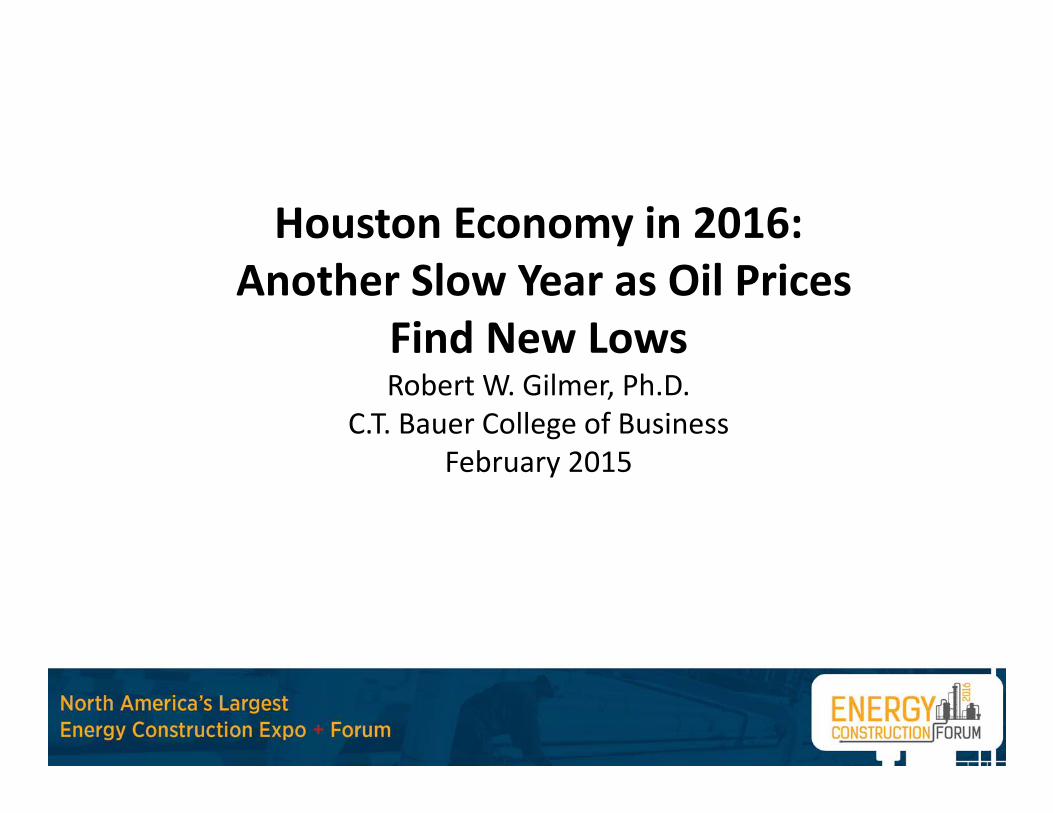

It Is All About Oil in Houston! Price Is Now Down By Over Half

$104

$59$51 $54

$60

43 4637

32 30

$20$30$40$50$60$70$80$90

$100$110$120

Spot Price of WTI in $/barrel

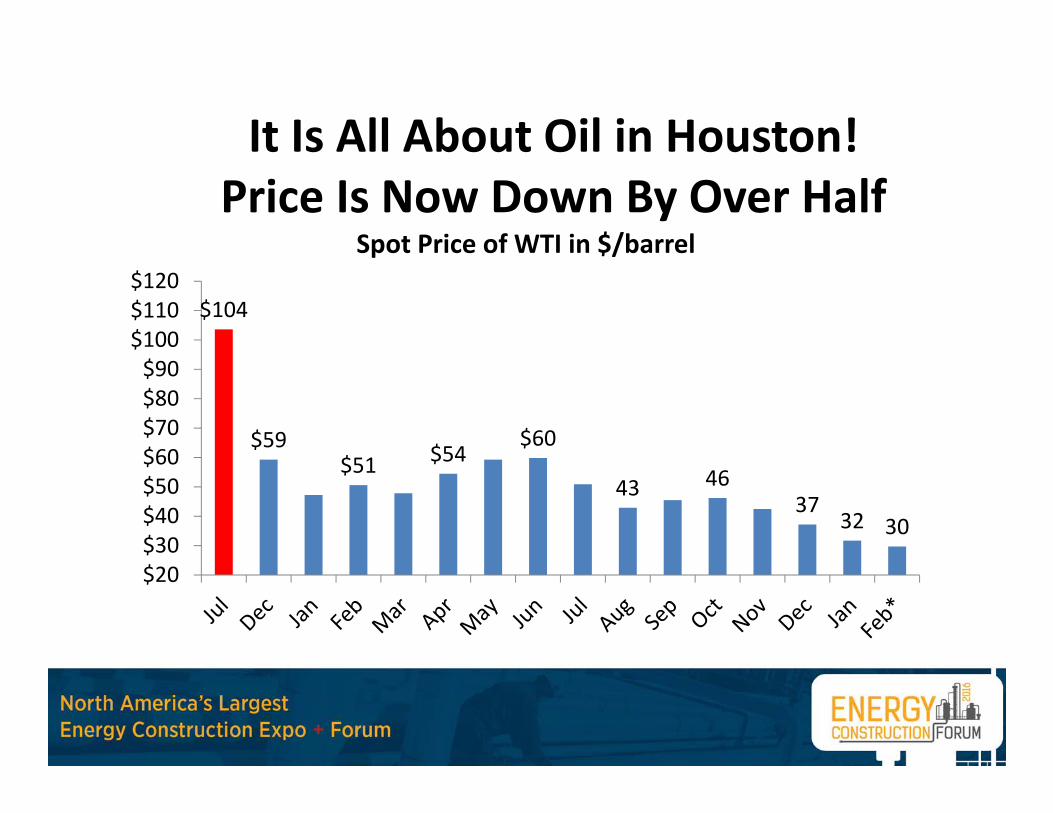

We Are Out of Good Options: Five Past and Present Scenarios

• Fracking Forever! ‐‐ Summer 2014• Maybe It Won’t Be So Bad? ‐‐ Early 2015• V‐Shaped Recovery – Summer 2015 & now off the table• U‐Shaped Recovery – 2016• Check‐Mark Recovery – Current favorite of big investment

houses• Fracking Defeated – Slow and partial recovery of rig count

from current levels of drilling

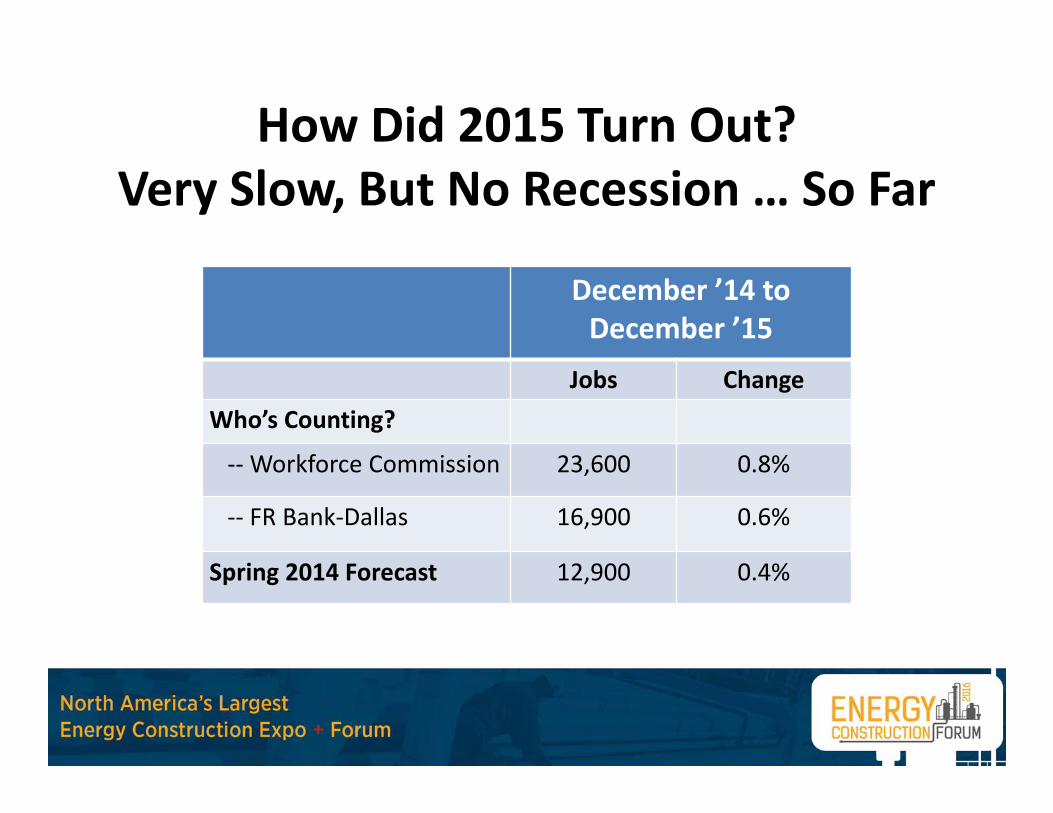

How Did 2015 Turn Out? Very Slow, But No Recession … So Far

December ’14 to December ’15

Jobs ChangeWho’s Counting?

‐‐Workforce Commission 23,600 0.8%

‐‐ FR Bank‐Dallas 16,900 0.6%

Spring 2014 Forecast 12,900 0.4%

Job Losses Or Gains By Sector: December 2014 to December 2015

Sector Number of New Jobs 2015 Percent ChangeTotal Payroll 16,900 0.6%Mining ‐17,700 ‐15.8Construction 11,900 15.6Manufacturing ‐23,000 ‐9.6Wholesale Trade ‐2,800 ‐1.6Transportation and Utilities 400 1.2Information ‐1,200 ‐3.6Banking, Finance, and Real Estate 3,200 2.3Professional and Business Services ‐5,300 ‐1.2Education and Health 19,500 5.9Leisure 16,400 6.2Other Services 200 0.2Government 8,300 2.4

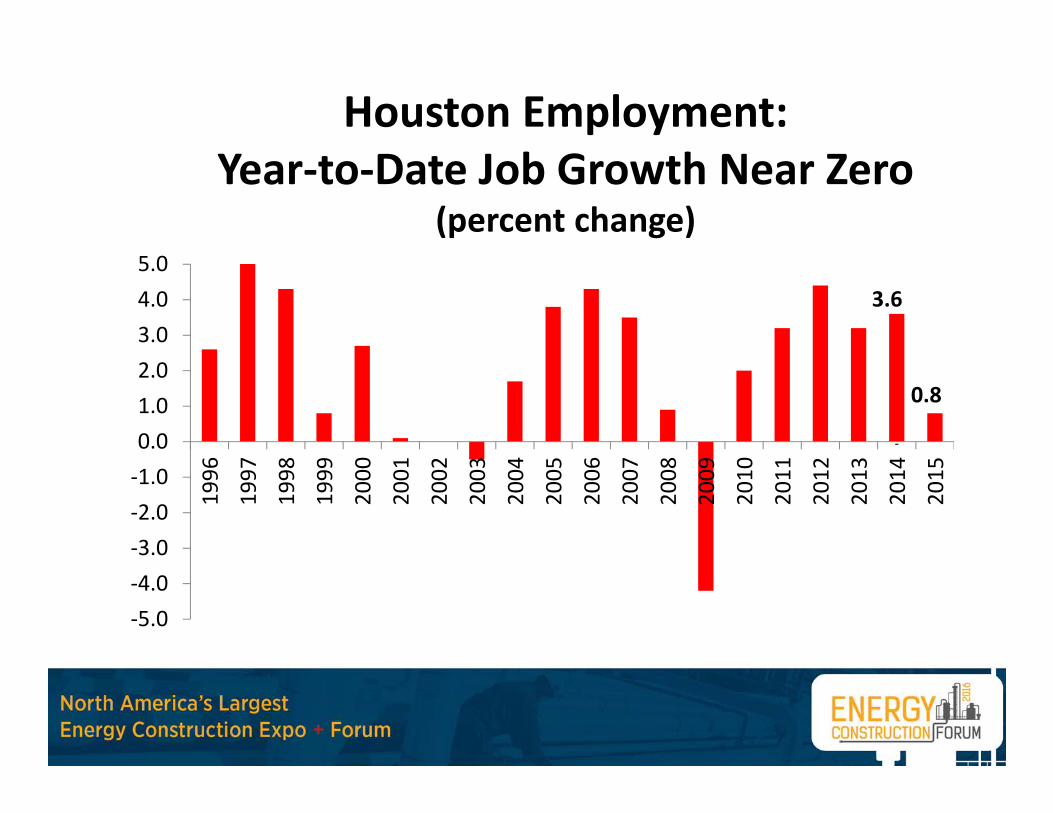

Houston Employment:Year‐to‐Date Job Growth Near Zero

(percent change)

‐5.0‐4.0‐3.0‐2.0‐1.00.01.02.03.04.05.0

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

3.6

0.8

‐

How Are You Feeling? • Many sectors of Houston have not felt much pain from this downturn

yet. What oil bust? • How can this be?

– Maybe they sell into strong national markets: United Airlines, Sysco, AIG, HP, …

– Maybe they live in East Houston– Maybe they are living off of past momentum. Houston Added 680,000 jobs

from 2004‐2024– Population stays strong for usually stays strong for several quarters after

job growth slows– Most damage has been confined to oil producers, oil services, and

manufacturing so far• BUT another slow year in Houston gives time for the slowdown to

spread to many sectors that have felt immune so far – healthcare, retail, restaurants, real estate, leisure, and government

Oil Markets and Oil Price

$30 Oil? Where Are We? How Did We Get Here?

• The Commodity Super Cycle Comes to an End– Oil, metals, food, agricultural raw materials see price soar after 2004 and stay

high for a decade– Primarily driven by a surge in growth by emerging markets, especially China– $100 oil was the market signal to expand capacity, and as the SuperCycle

ended we returned to long‐run price near $60 last spring and early summer• Overshoot $60, and wind up below $30 per barrel?

– In July, the Iran Nuclear Agreement is signed and promises a return of quick 1.2 million bbl/d to export markets

– The August devaluation of the Chinese Yuan distills concerns about China into fear about how bad things might be

• Unless China is much worse than we think, this is NOT 1987, when OPEC dumped 10 million barrels of excess capacity on the market – a decade of demand growth

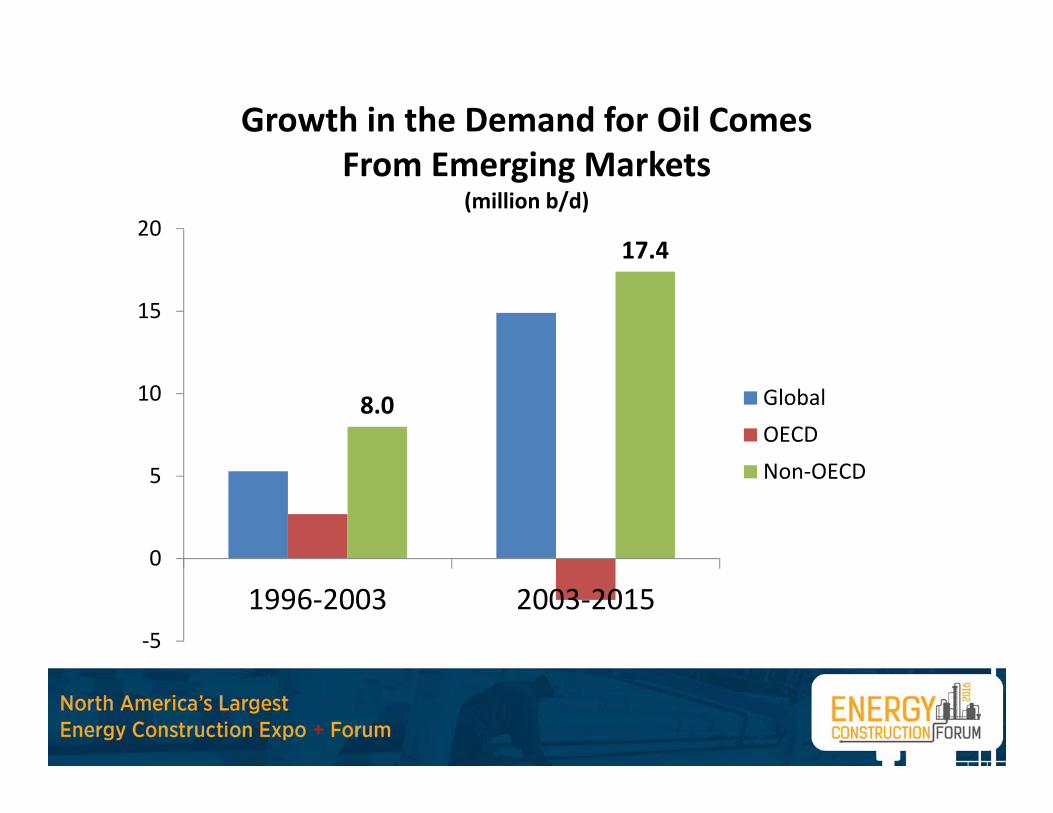

Growth in the Demand for Oil Comes From Emerging Markets

(million b/d)

8.0

17.4

‐5

0

5

10

15

20

1996‐2003 2003‐2015

GlobalOECDNon‐OECD

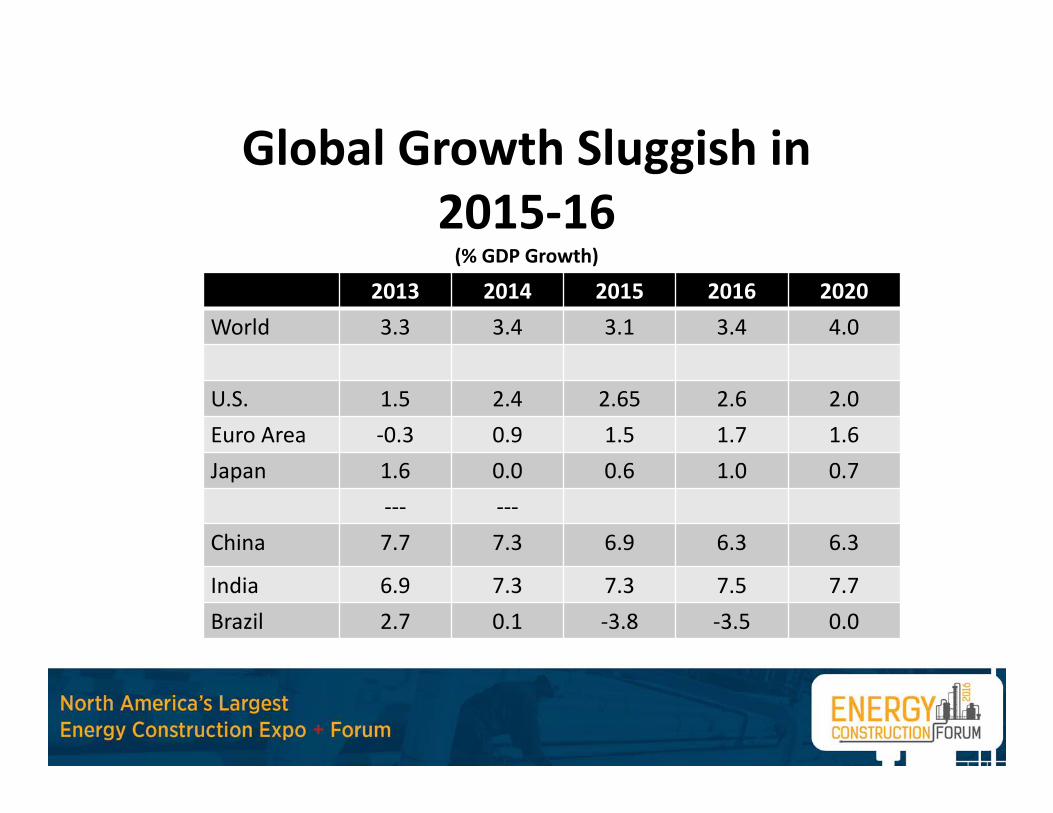

Global Growth Sluggish in 2015‐16(% GDP Growth)

2013 2014 2015 2016 2020World 3.3 3.4 3.1 3.4 4.0

U.S. 1.5 2.4 2.65 2.6 2.0Euro Area ‐0.3 0.9 1.5 1.7 1.6Japan 1.6 0.0 0.6 1.0 0.7

‐‐‐ ‐‐‐China 7.7 7.3 6.9 6.3 6.3

India 6.9 7.3 7.3 7.5 7.7Brazil 2.7 0.1 ‐3.8 ‐3.5 0.0

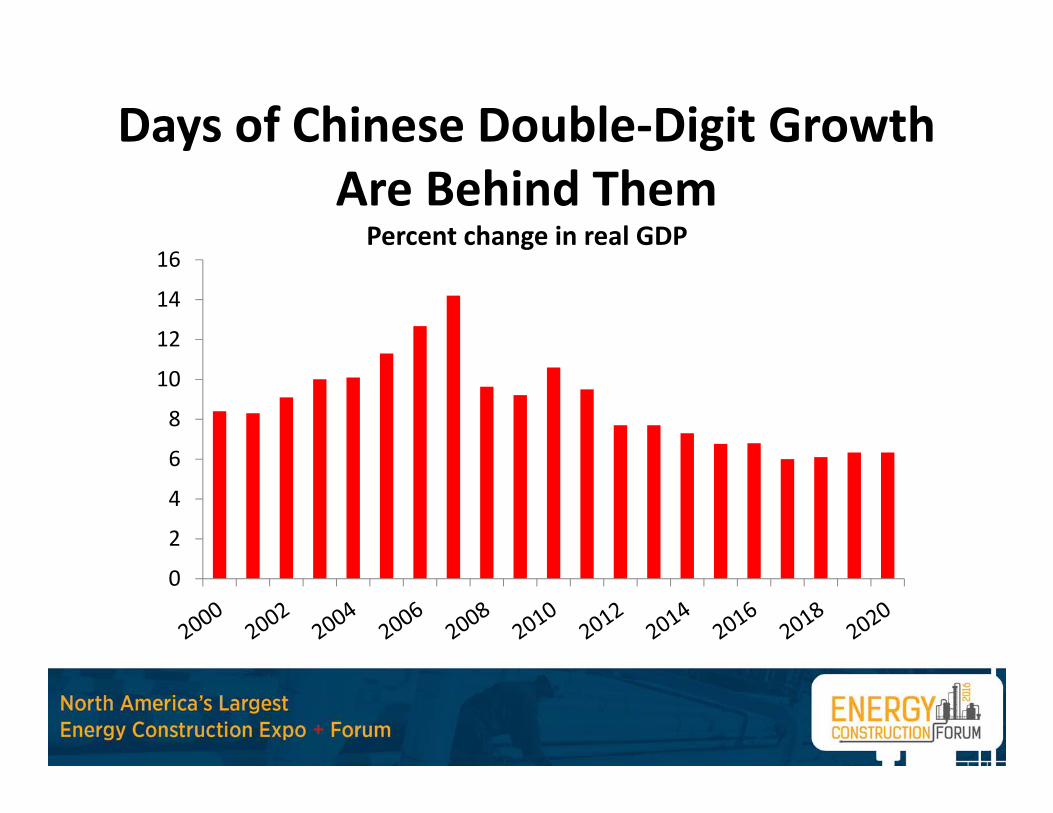

Days of Chinese Double‐Digit Growth Are Behind Them

0

2

4

6

8

10

12

14

16Percent change in real GDP

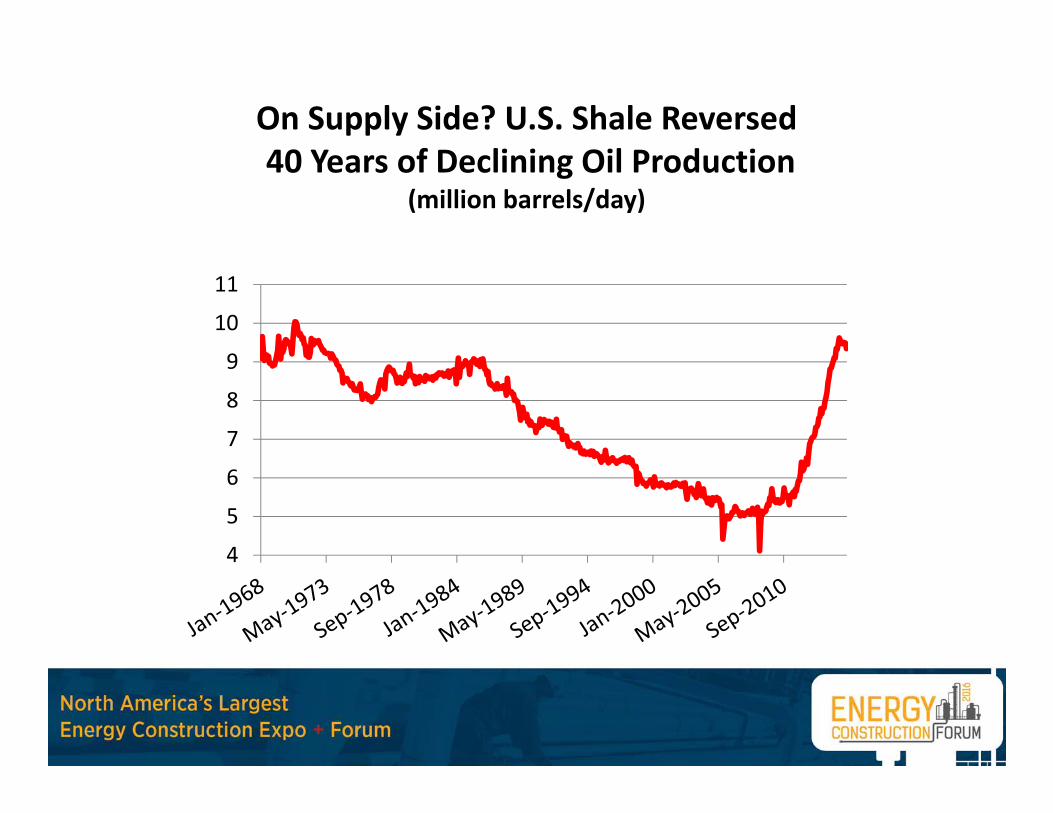

On Supply Side? U.S. Shale Reversed40 Years of Declining Oil Production

(million barrels/day)

4

5

6

7

8

9

10

11

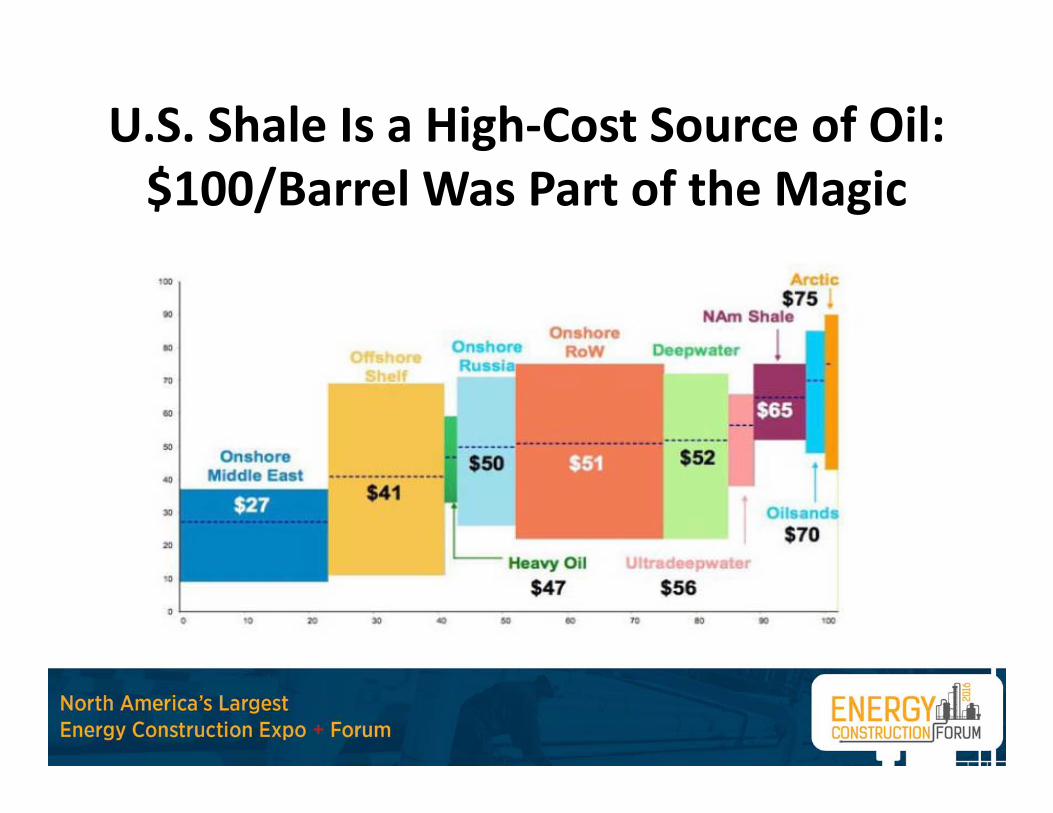

U.S. Shale Is a High‐Cost Source of Oil: $100/Barrel Was Part of the Magic

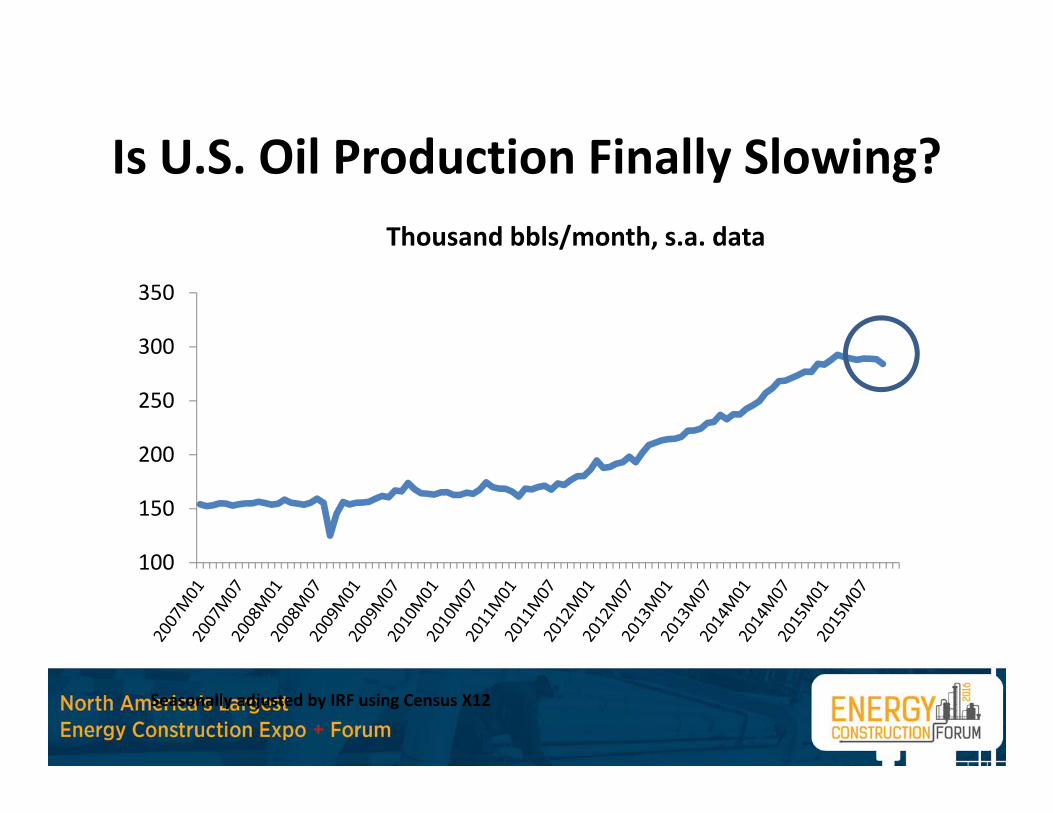

Is U.S. Oil Production Finally Slowing?

100

150

200

250

300

350

Thousand bbls/month, s.a. data

Seasonally adjusted by IRF using Census X12

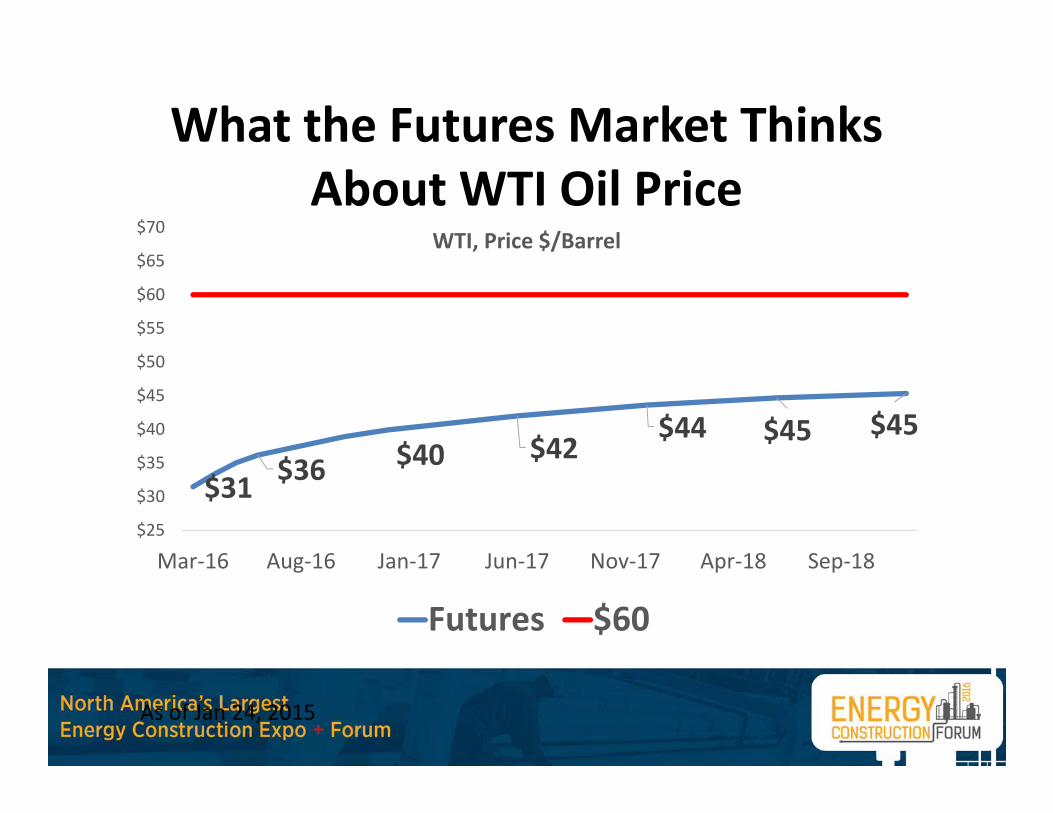

What the Futures Market Thinks About WTI Oil Price

$31 $36 $40 $42$44 $45 $45

$25

$30

$35

$40

$45

$50

$55

$60

$65

$70

Mar‐16 Aug‐16 Jan‐17 Jun‐17 Nov‐17 Apr‐18 Sep‐18

WTI, Price $/Barrel

Futures $60

As of Jan 24, 2015

The Greatest Oil BoomIs Over for Now

Drilling capital expenditures($2014 billion at annual rates)

0

50

100

150

200

250

300

350Baker Hughes rig count

(working rigs)

500700900110013001500170019002100

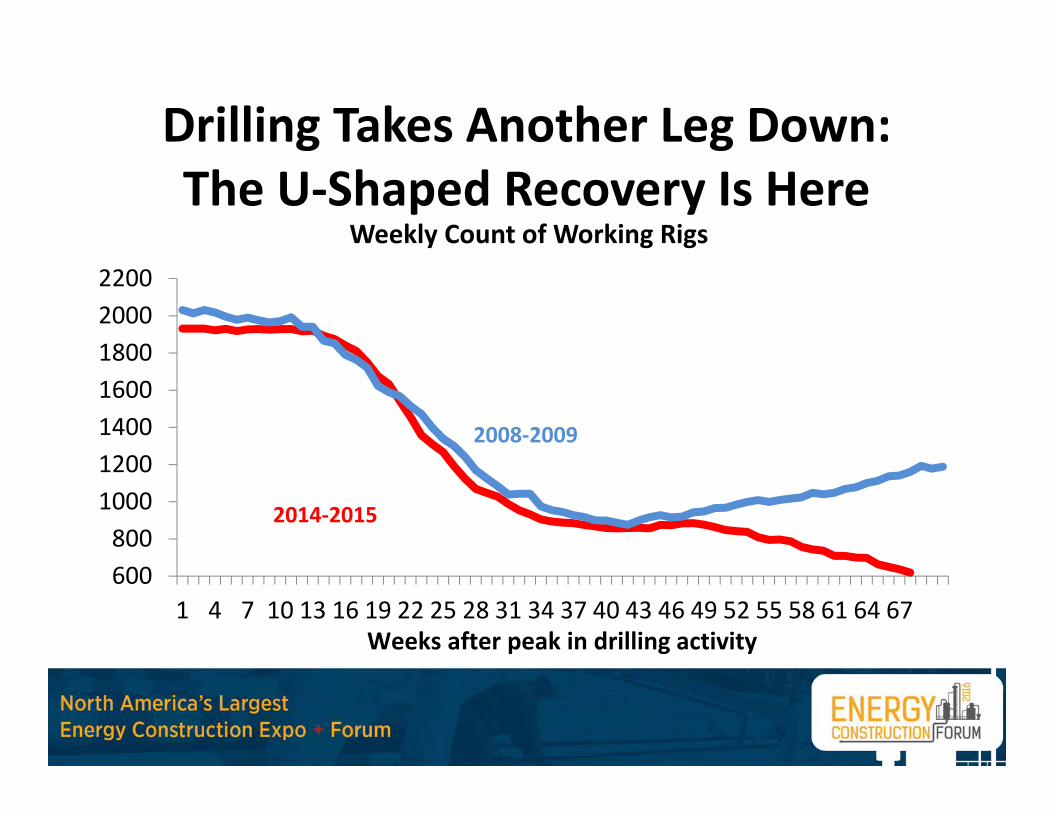

Drilling Takes Another Leg Down:The U‐Shaped Recovery Is Here

600800

1000120014001600180020002200

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52 55 58 61 64 67

Weekly Count of Working Rigs

Weeks after peak in drilling activity

2008‐2009

2014‐2015

Local Job Losses Will Spread If Drilling Does Not Turn Up

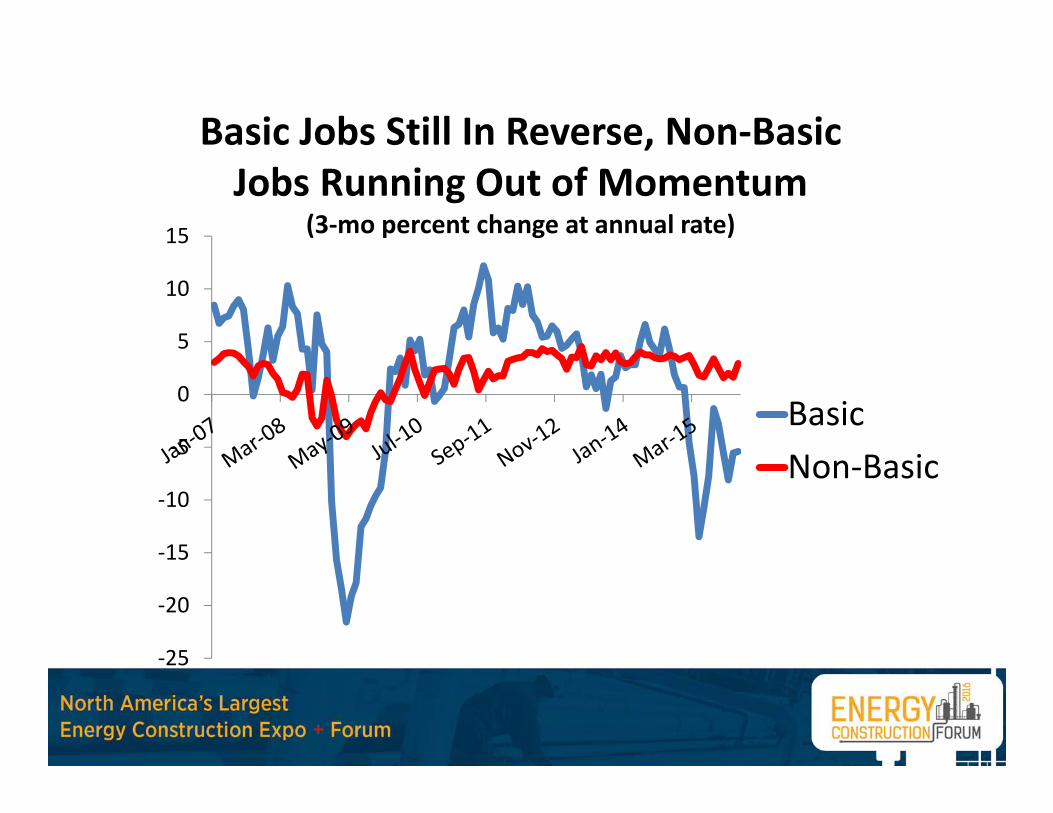

Basic Jobs Still In Reverse, Non‐Basic Jobs Running Out of Momentum

(3‐mo percent change at annual rate)

‐25

‐20

‐15

‐10

‐5

0

5

10

15

BasicNon‐Basic

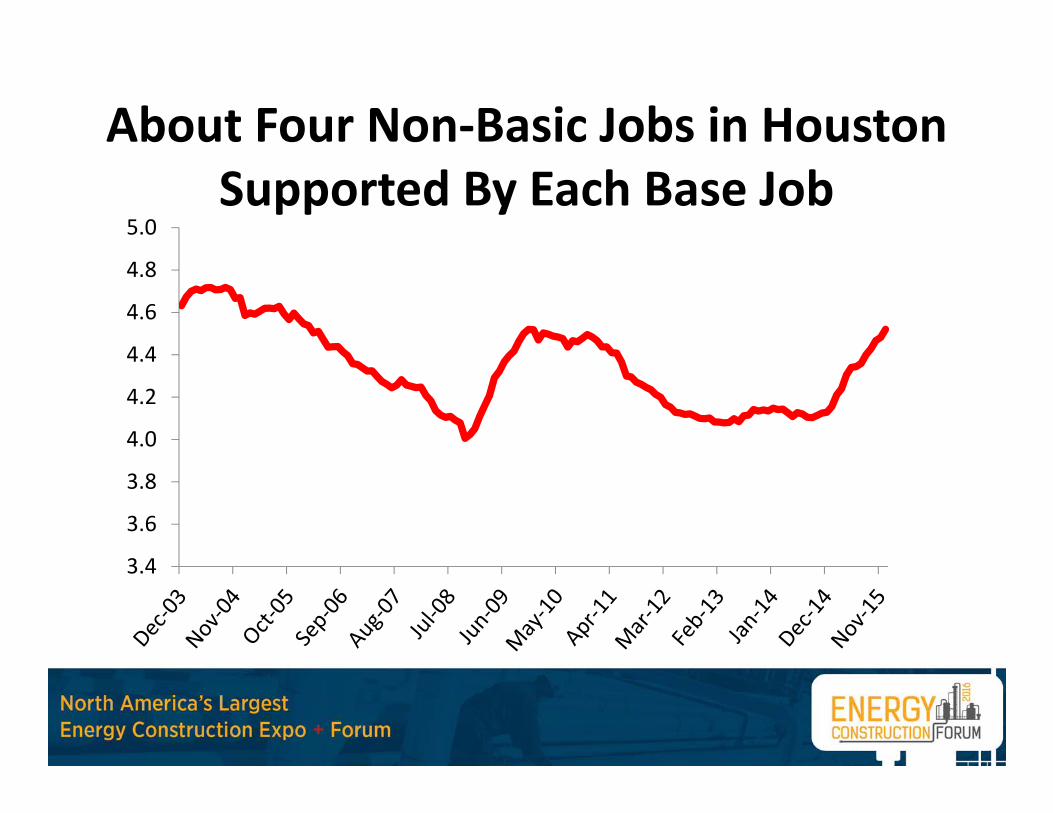

About Four Non‐Basic Jobs in HoustonSupported By Each Base Job

3.4

3.6

3.8

4.0

4.2

4.4

4.6

4.8

5.0

Four Scenarios

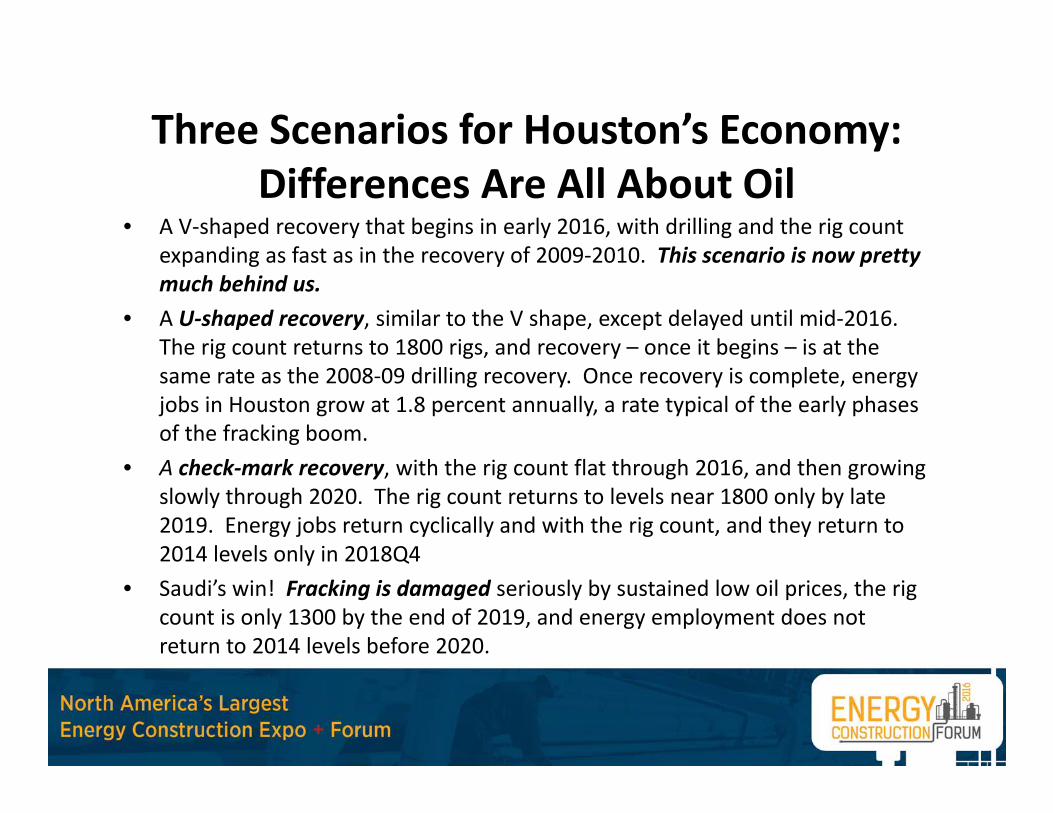

Three Scenarios for Houston’s Economy: Differences Are All About Oil

• A V‐shaped recovery that begins in early 2016, with drilling and the rig count expanding as fast as in the recovery of 2009‐2010. This scenario is now pretty much behind us.

• A U‐shaped recovery, similar to the V shape, except delayed until mid‐2016. The rig count returns to 1800 rigs, and recovery – once it begins – is at the same rate as the 2008‐09 drilling recovery. Once recovery is complete, energy jobs in Houston grow at 1.8 percent annually, a rate typical of the early phases of the fracking boom.

• A check‐mark recovery, with the rig count flat through 2016, and then growing slowly through 2020. The rig count returns to levels near 1800 only by late 2019. Energy jobs return cyclically and with the rig count, and they return to 2014 levels only in 2018Q4

• Saudi’s win! Fracking is damaged seriously by sustained low oil prices, the rig count is only 1300 by the end of 2019, and energy employment does not return to 2014 levels before 2020.

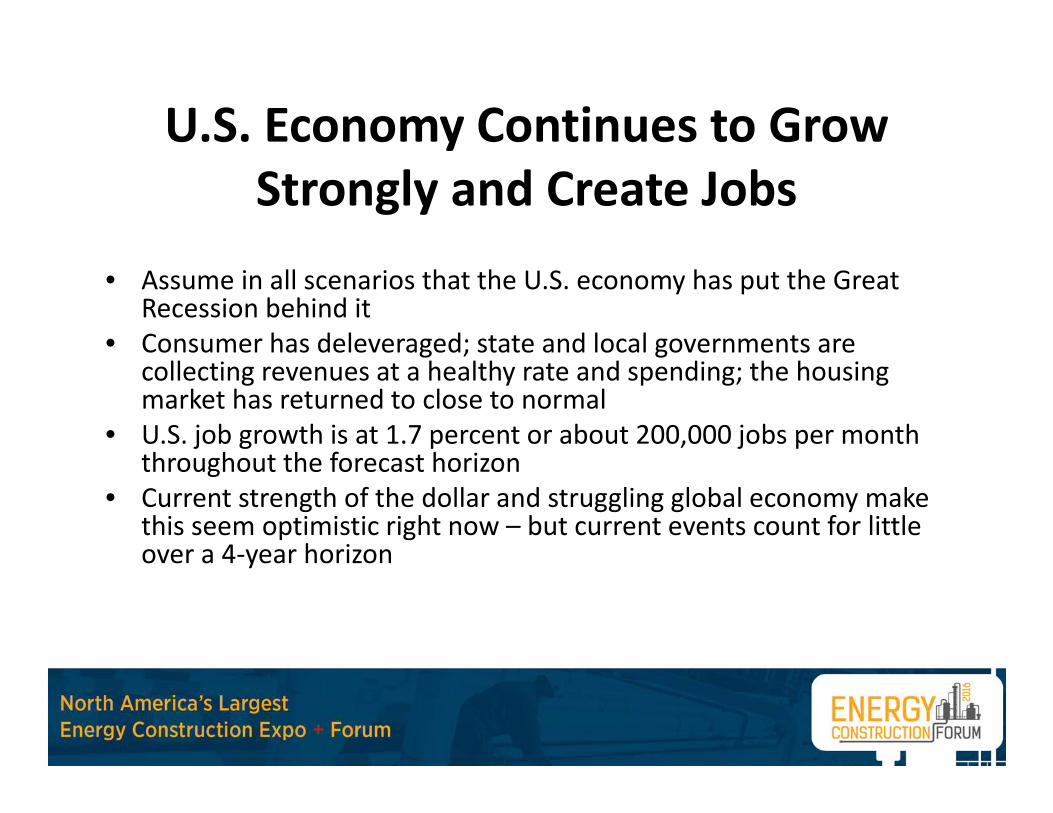

U.S. Economy Continues to Grow Strongly and Create Jobs

• Assume in all scenarios that the U.S. economy has put the Great Recession behind it

• Consumer has deleveraged; state and local governments are collecting revenues at a healthy rate and spending; the housing market has returned to close to normal

• U.S. job growth is at 1.7 percent or about 200,000 jobs per month throughout the forecast horizon

• Current strength of the dollar and struggling global economy make this seem optimistic right now – but current events count for little over a 4‐year horizon

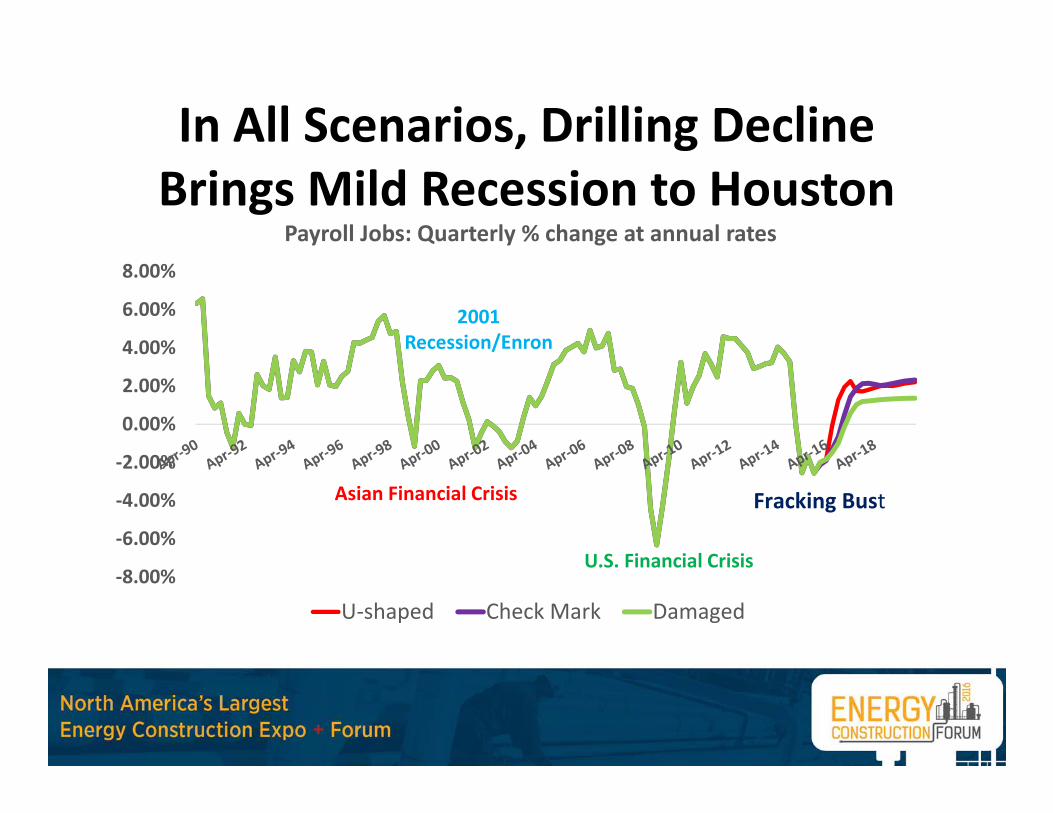

In All Scenarios, Drilling Decline Brings Mild Recession to Houston

‐8.00%

‐6.00%

‐4.00%

‐2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

Payroll Jobs: Quarterly % change at annual rates

U‐shaped Check Mark Damaged

Asian Financial Crisis Fracking Bust

2001 Recession/Enron

U.S. Financial Crisis

Downstream Boom Built on Cheap Energy

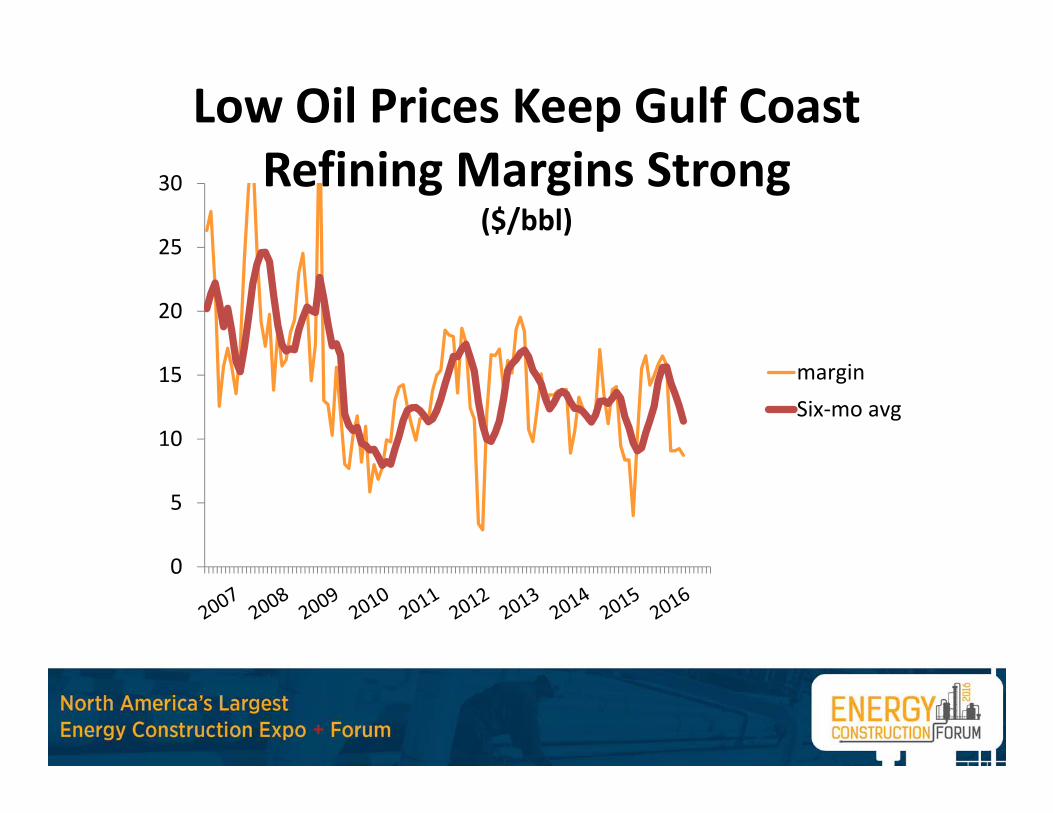

Low Oil Prices Keep Gulf Coast Refining Margins Strong

($/bbl)

0

5

10

15

20

25

30

marginSix‐mo avg

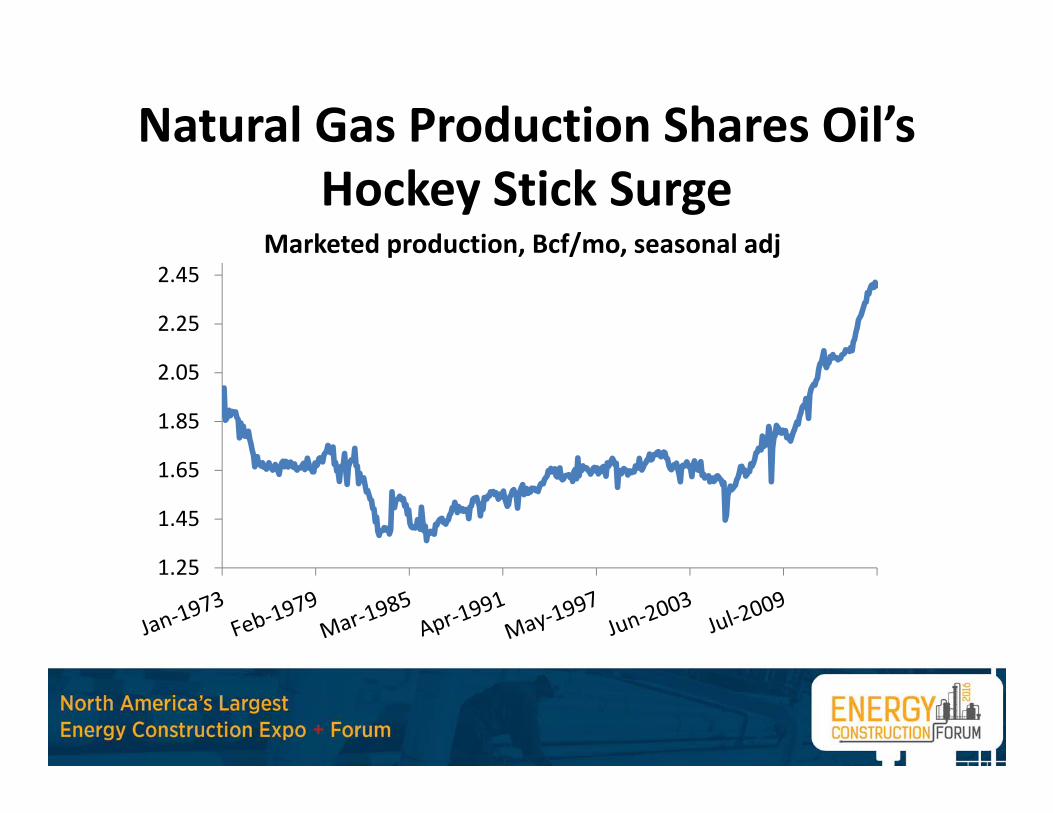

Natural Gas Production Shares Oil’s Hockey Stick Surge

1.25

1.45

1.65

1.85

2.05

2.25

2.45Marketed production, Bcf/mo, seasonal adj

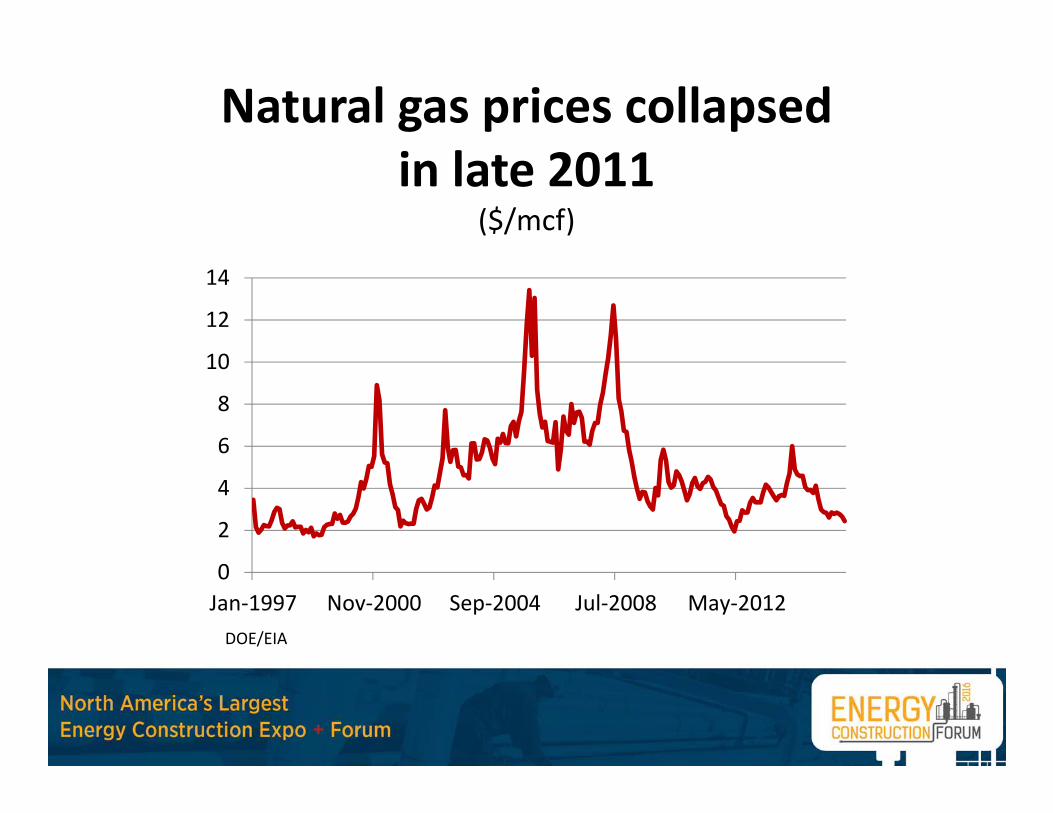

Natural gas prices collapsed in late 2011

($/mcf)

0

2

4

6

8

10

12

14

Jan‐1997 Nov‐2000 Sep‐2004 Jul‐2008 May‐2012DOE/EIA

$153 Billion U.S. Construction Boom is Based on Cheap Energy and Exports

• This $153 total includes many industries and all of the U.S.

• New ethylene crackers, more ethylene‐related expansion in PE, PVC and other derivative plants

• LNG export terminals to sell surplus natural gas into global markets

• Refiners have joined in with additional expansions

Note: The $153 billion figure is based on all shale‐related expansion, estimatedby the American Chemistry Council in October, 2015

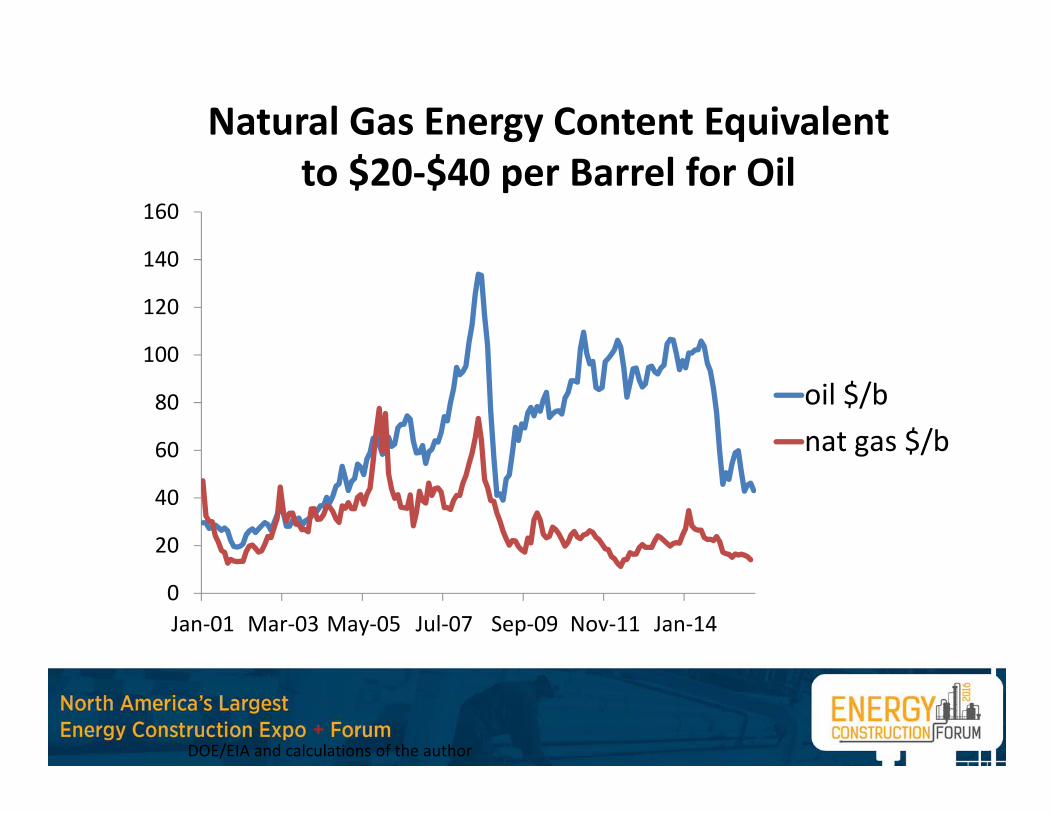

Natural Gas Energy Content Equivalent to $20‐$40 per Barrel for Oil

0

20

40

60

80

100

120

140

160

Jan‐01 Mar‐03 May‐05 Jul‐07 Sep‐09 Nov‐11 Jan‐14

oil $/bnat gas $/b

DOE/EIA and calculations of the author

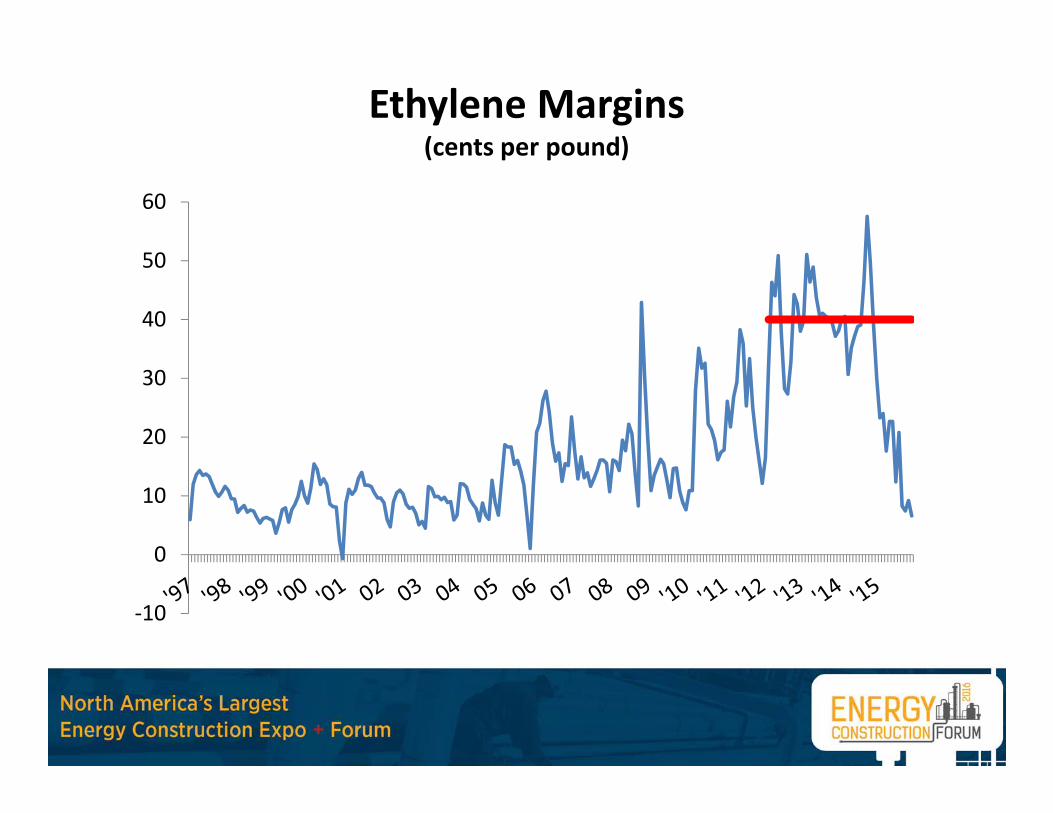

Ethylene Margins(cents per pound)

‐10

0

10

20

30

40

50

60

Large Projects Headline Over $50 Billion in East Houston Construction

Company Location Project Completion Value ($ mil)

Exxon Baytown Ethylene 2017 $5,000

Chevron Freeport Ethylene 2017 $4,000

Dow Baytown Ethylene 2017 $3,500

BASF Freeport Ethylene 2017 $3,000

Freeport LNG Freeport LNG Export 2019 $3,000

Freeport LNG Freeport LNG Export 2020 $3,000

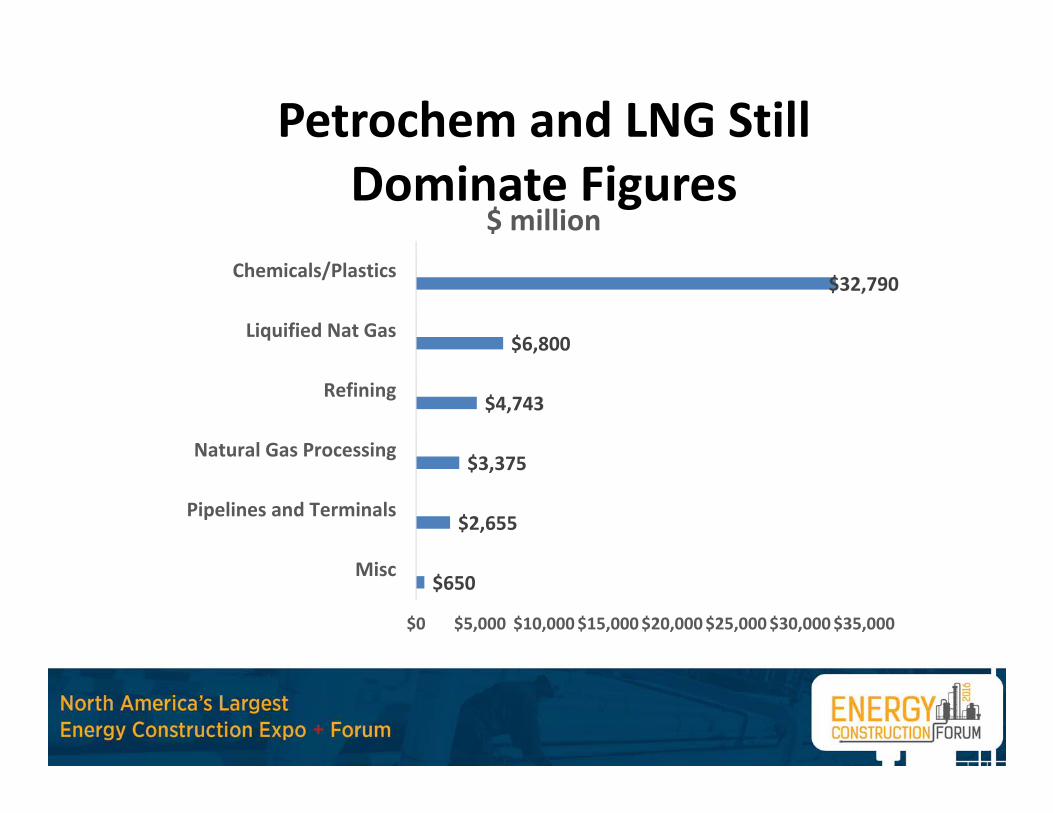

Petrochem and LNG Still Dominate Figures

$650

$2,655

$3,375

$4,743

$6,800

$32,790

$0 $5,000 $10,000$15,000$20,000$25,000$30,000$35,000

Misc

Pipelines and Terminals

Natural Gas Processing

Refining

Liquified Nat Gas

Chemicals/Plastics

$ million

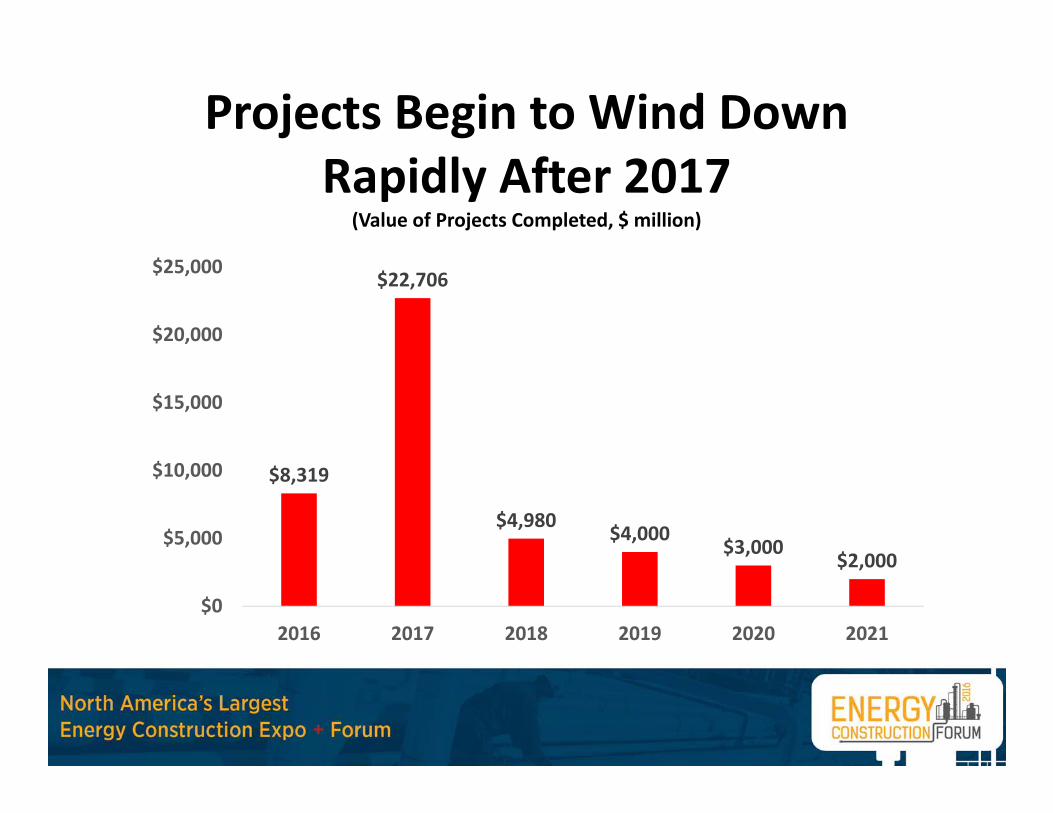

Projects Begin to Wind Down Rapidly After 2017

(Value of Projects Completed, $ million)

$8,319

$22,706

$4,980 $4,000$3,000

$2,000

$0

$5,000

$10,000

$15,000

$20,000

$25,000

2016 2017 2018 2019 2020 2021

A Counterweight to Upstream Damage From Low Oil Prices

• Jobs adds up quickly given the number and scale of proposed construction projects in 2015‐2017

• These are temporary jobs, disappearing as projects end and capital expenditures wind down

• Normally, downstream capital expenditures are small compared to the upstream, move in a narrow range, and create relatively few jobs

• The construction projects just described means the downstream can’t be ignored right now. Can this spending substitute for losses upstream?

Temporary Jobs, Temporary Workers• Does one construction job equal one lost in drilling? In professional and

business services? Compensation is good for the skilled, unionized jobs • BUT we are replacing long‐term employment with temporary construction

jobs – These jobs will be important in keeping machine shops and industrial

base for machinery and fabricated metal busy– But they won’t need high‐end apartments, luxury retail, office space,

or other amenities?• Industrial east side booms while the air could be sucked out of the white‐

collar west side. There is plenty of scope for economic disruption, even if overall job numbers stay healthy

• Assume multipliers for the construction workers are half of the white‐collar jobs they replace

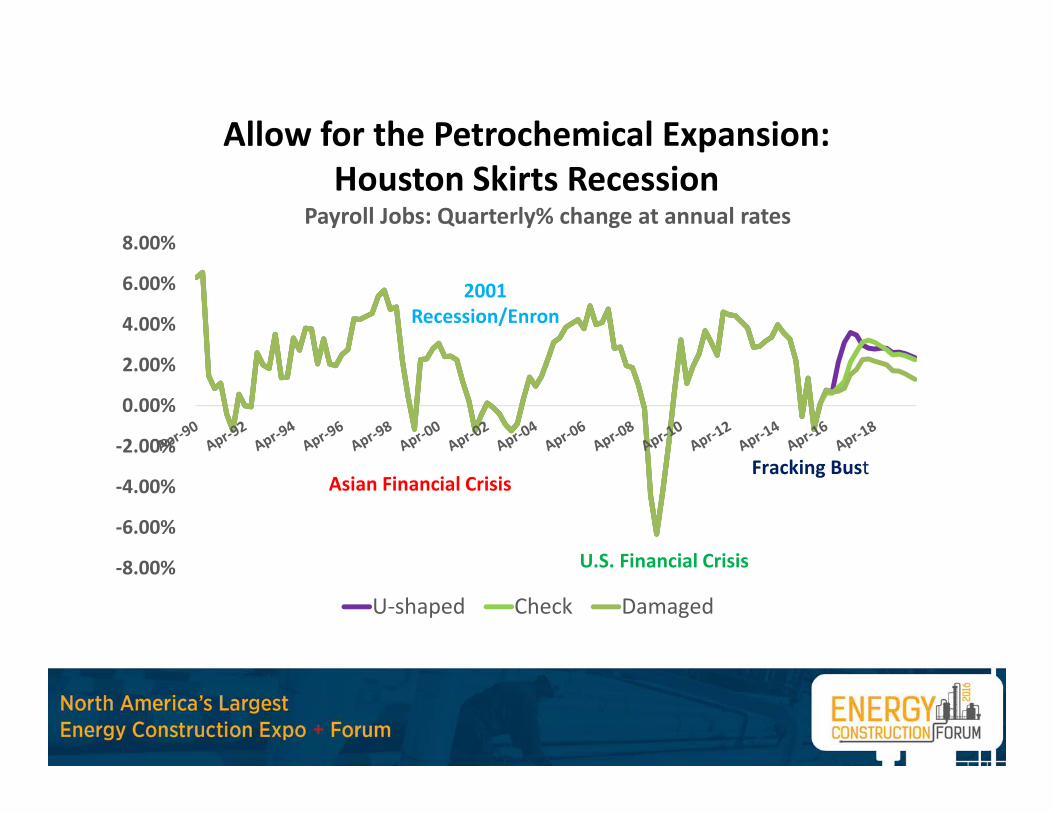

Allow for the Petrochemical Expansion:Houston Skirts Recession

‐8.00%

‐6.00%

‐4.00%

‐2.00%

0.00%

2.00%

4.00%

6.00%

8.00%Payroll Jobs: Quarterly% change at annual rates

U‐shaped Check Damaged

Asian Financial CrisisFracking Bust

2001 Recession/Enron

U.S. Financial Crisis

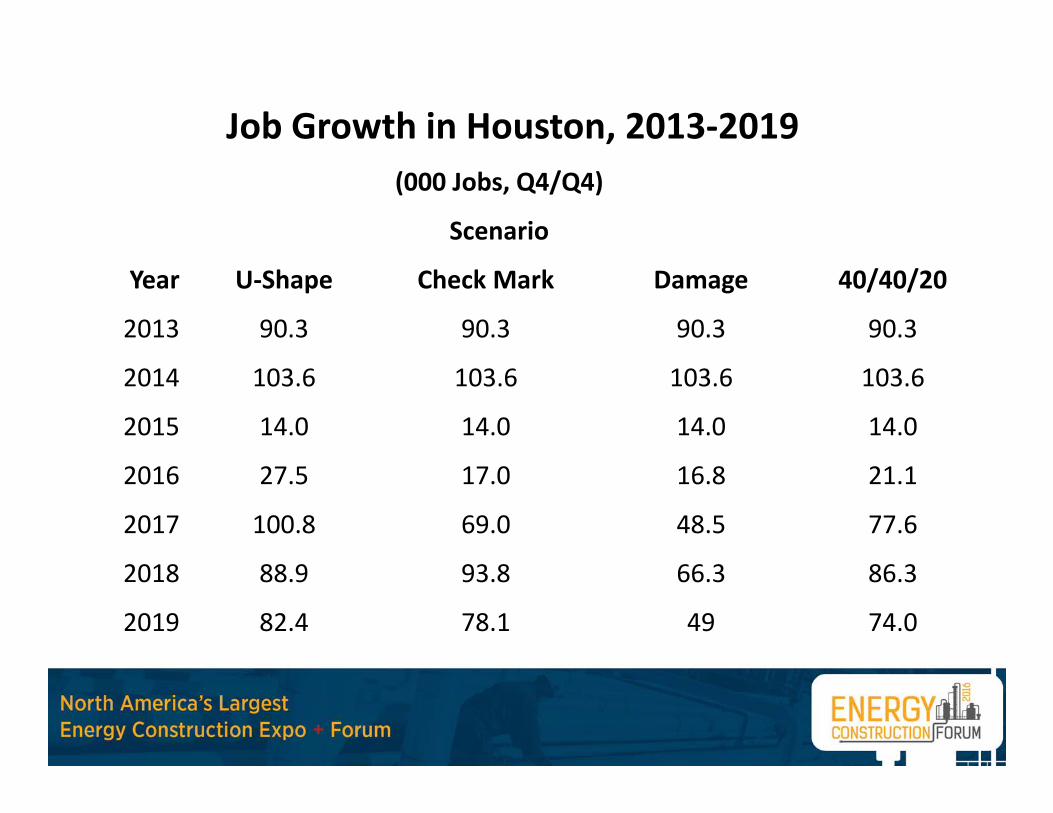

Job Growth in Houston, 2013‐2019(000 Jobs, Q4/Q4)

Scenario

Year U‐Shape Check Mark Damage 40/40/20

2013 90.3 90.3 90.3 90.3

2014 103.6 103.6 103.6 103.6

2015 14.0 14.0 14.0 14.0

2016 27.5 17.0 16.8 21.1

2017 100.8 69.0 48.5 77.6

2018 88.9 93.8 66.3 86.3

2019 82.4 78.1 49 74.0

In Closing …• This is a serious downturn in oil markets, that has run faster and

deeper than 2008‐09, and it has serious implications for Houston• The options for a quick and easy way out of this downturn have

disappeared, and slow job growth will likely stretch through 2016• With limited job growth in 2016, many sectors that seemed

immune to the slowdown in 2015 will begin to feel it. Health care, leisure, retail, single‐family, and multi‐family will be on this list

• That said, it is just one more oil downturn in Houston. It is not 1982 or 1987 in oil markets – and certainly not the Houston economy

Houston Economy in 2016:Another Slow Year as Oil Prices

Find New LowsRobert W. Gilmer, Ph.D.

C.T. Bauer College of BusinessFebruary 2015