Embed Size (px)

Citation preview

Business services

Made by-vibhu goel

Banking services

Bank Draft

Bankers Cheque

Real Time Gross Settlement (RTGS)

National Electronic Fund Transfer (NEFT)

Cash Credits

Bank overdraft

E-BANKING

What is E-banking?

In a broad sense, it is the use of electronic means to transfer funds

directly from one account to another, rather than by cheque or cash.

The term online banking was first started in 80’s

E-banking is a delivery of banking services and products through

the internet, the cell phone, etc.

E-banking is an upshot of Globalization.

E-banking vis-A-vis Traditional banking

Speed

Accessibility

Electronic documentation

Time saving

Satisfaction to the customer

Complimentary to traditional banking

Geographical boundaries surpassed

Why E-banking?

From the banking point of view;

Differentiation of products from the others.

A combination of regulatory and competitive reasons.

Stress on branchless banking.

Increasing volumes of banking transactions.

Providing customers with cost effective services

From customer point of view;

Convenience

Low cost banking

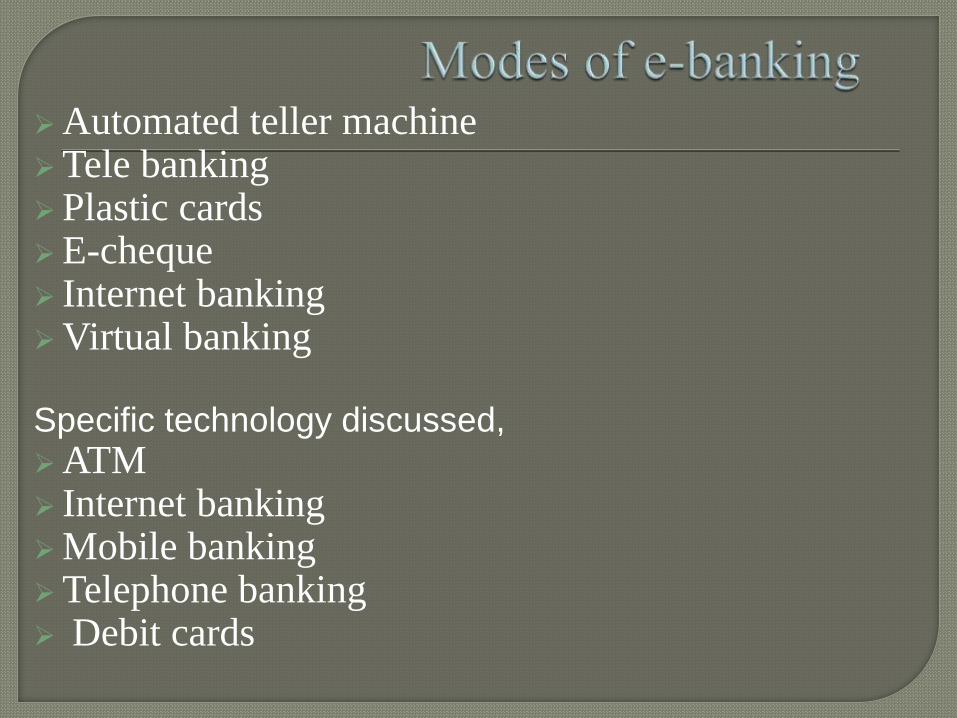

Automated teller machineTele bankingPlastic cardsE-cheque Internet bankingVirtual banking

Specific technology discussed,

ATM Internet bankingMobile bankingTelephone banking Debit cards

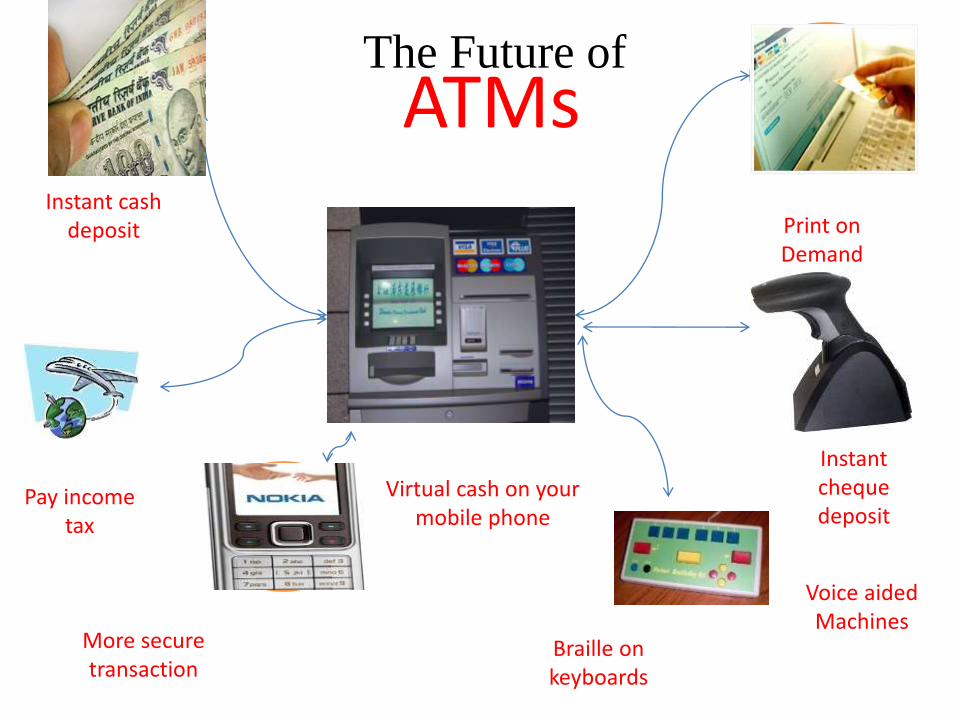

The Future of

ATMsInstant cash

deposit

Pay income tax

Virtual cash on your mobile phone

Braille on keyboards

Print on Demand

Instant cheque deposit

Voice aided Machines

More secure transaction

Internet banking

Plastic cards

Advantages of E-banking Transparency and disclosure practices

Facilitate the offering of more services

Increase customer satisfaction and loyalty

Competitive advantage for banks

Reduce customer attrition

Reduces the time, cost and effort in the interaction

Risk factors

Transaction and security risk

Technology risk

Strategic risk

Legal risk

Cross border risk

Issues

Legal issues

Regulatory issues

Supervisory issues

risks and issues

involved in

e-banking

Insurane:concept

and

principle

DEFINITION

In financial sense

• It is a social device in which

a group of individuals (insured)

transfer risk to another party (insurer)

in order to combine loss experienced,

which

o permits statistical prediction of losses and

o provides for payment of losses from funds

contributed (premium) by all members

who transferred risk

21

Definition (Contd.)

In legal sense

It is a contract by which

one party (Insurer)

in consideration of price paid to him

proportionate to risk provides security to

the other party (Insured) that

o he shall not suffer loss, damage or prejudice

by the happening of certain specified events.

Insurance is meant to protect insured

against uncertain events which may cause

disadvantage to him

22

FUNDAMENTAL ADVANTAGES23

Transfer of risk from one person (Insured) to

another (Insurer)

Sharing (Pooling) of losses on some

equitable basis such that

fortuitous (random) losses will be indemnified

(paid)

Reduction in tension and fear

Credit multiplication

Revenue for investment

Principle of Uberrimae Fides (Utmost Good Faith) –

A positive duty voluntarily to disclose, accurately and fully, all facts material to the risk being proposed, whether requested or not.

Non-disclosure of any fact may be unintentional on the part of the insured.

Even so such a contract is rendered voidable at the insurer’s option and it can refuse any compensation.

Any concealment of material facts is considered intentional.

FUNDAMENTAL PRINCIPLES OF INSURANCE

24

Fundamental Principles Of Insurance (Contd.)

Principle of Indemnity

• On the happening of insured event for which insurance policy is taken up insured should be replenished the amount of loss

• Insured should not derive any unwarranted benefit from a loss

• Made in following ways

Cash payment

Repair

Replacement

Reinstatement

Fundamental Principles Of Insurance (Contd.)

Principle of Subrogation

• Restitution of rights of an assured in favour of Insurer against third party for any damages caused by him in place of assured after Insurer has indemnified him for the loss

• Objectives of the principle:

i. Prevents insured from profiting from damage.

ii. Enforces rule of law that guilty is brought to

book and made to pay for the loss.

iii.Helps Insurer to partially or fully recover

amount paid for loss.

iv. Helps to lower insurance rates.

26

Principle of Contribution

It means indemnity provided for loss occurring on asset, which is insured with several insurers has to be shared pro rata

Corollary of doctrine of Indemnity and hence is applicable in case of GI.

Requisites

Insured asset/Person (in case of hospitalization insurance) must be common to all policies

Risk insured against must be common to all policies

All policies must be in force during the occurrence of loss

Fundamental Principles Of Insurance (Contd.)

Fundamental Principles Of Insurance (Contd.)

28Principle of Proximate Cause

Literally means nearest cause or direct cause.

Immediate cause of mishap, which resulted

in the loss.

While determining ‘proximate cause’

sequence of events according to their time of

occurrence is irrelevant.

Many court judgments act as precedents in

arriving at decisions while making

settlements.

The insurance company is liable to indemnify

only against the insured perils.

CLASSIFICATION OF INSURANCE

LIFEGENERAL (NON-LIFE)

PURE TERM FIRE MARINE MOTOR

ENGINEERING

AVIATION AGRICULTURAL

CONSEQUENTIAL (LOSS)

FIRE

LIABILITY

Type of insurance

Home InsuranceLife Insurance

Property Insurance

Health Insurance

Auto Insurance

Life insurance provides a monetary benefit to a descendant's family or otherdesignated beneficiary, and may specifically provide for income to an insuredperson's family, burial, funeral and other final expenses. Life insurance policiesoften allow the option of having the proceeds paid to the beneficiary either in alump sum cash payment or an annuity.

Annuities provide a stream of payments and are generally classified asinsurance because they are issued by insurance companies, are regulated asinsurance, and require the same kinds of actuarial and investmentmanagement expertise that life insurance requires.

Life Insurance

Health Insurance

Health insurance policies issued by publicly-funded health programs, such as cost of medical treatments.

Dental insurance, like medical insurance, is protects policyholders for dental costs. In the U.S. and Canada, dental insurance is often part of an employer's benefits package, along with health insurance.

Fire insurance

Fire insurance is a insurance that cover property, such as home shop or other fixed asset protection against fire, burn Etc..

It also cover distraction of property due to fire

Marine insurance

Marine insurance and marine cargo insurance cover the loss or damage of vessels at sea or on inland waterways, and of cargo in transit, regardless of the method of transit but excludes losses that can be recovered from the carrier or the carrier's insurance. Many marine insurance underwriters will include "time element" coverage in such policies, which extends the indemnity to cover loss of profit and other business expenses attributable to the delay caused by a covered loss.

All-risk insurance

Bloodstock insurance

Business interruption insurance

Collateral protection insurance.

Legal expenses insurance

Locked funds insurance

Livestock

Nuclear incident insurance

Pet insurance.

Pollution insurance

Travel insurance

Other types

Postal servicesAnd scheme

Speed Post-

The very high speed express service for letters and documents. Speed Post links more than 1200 towns in India, with 290 Speed Post Centres in the national network and around 1000 Speed Post Centres in the state network. For regular users, Speed Post provides delivery ‘anywhere in India’ under contractual service. Speed Post offers a money-back guarantee, under which the Speed Post fee will be refunded if the consignment is not delivered within the published delivery norms..

Instant Money Order Service (iMO)- The instant domestic money is available in 717 post offices. However no International

Money Order facility is available

international Money Transfer- As a result of the collaboration of the Department of Posts with the Western Union

Financial Services, state of the art international money transfer service is now available through post offices in India. This enables instantaneous remittance of money from 185 countries to India. The recipients can in fact collect the money in minutes after the sender has made the remittance.

services

schemes Non-postal services-

The post office has also traditionally served as a financial institution for millions of people in rural India. Currently these are some of the activities being supported:

Public Provident Fund

National Savings Certificate

Kisan Vikas Patra

Savings Bank Account

Monthly Income Scheme

Recurring Deposit Account

National Savings Scheme 1992 - discontinued from 01.11.2002

Post Office Time Deposit

TELECOM SERVICES

Services Cable services

Cellular mobile services

Radio paging services

Fixed line services

VSAT services

DTH services