Embed Size (px)

Citation preview

December 2015Felix Poh, Max Magni, Rohit Razdan

Seizing the CPG Opportunity in China: Online and Out Ahead

Seizing the CPG Opportunity in China: Online and Out Ahead2

3Seizing the CPG Opportunity in China: Online and Out Ahead

INTRODUCTIONChina’s CPG companies must deal with a situation that will undergo dramatic shifts over the next few years. First, as the economy has re-balanced overall growth has slowed, dropping to just below 7% after multiple years of double-digit expansion. Physical channels are also projected to lose share despite continued increases; online, by contrast, is positioned for explosive gains (with a projected CAGR of 21% from 2014 to 2019). CPG organizations need to adjust to this ‘new normal’ as well as shifting channel dynamics.

e-Commerce will demand agility and new capabilities from China’s CPG companies. They must partner with retailers who are expanding their footprints and targeting new segments and occasions. CPG winners will also develop new, multi-channel strategies that encompass both online and offline platforms and integrate an omni-channel approach (including, in some cases, CPG companies that are going direct to consumers).

This report provides a detailed picture on how some of China’s most successful CPG companies are navigating today’s market. We highlight what differentiates them through a proprietary Customer and Channel Management (CCM) survey developed in collaboration with Nielsen that was conducted for the first time in China. It covered five modules: Channel Strategy, Online Strategy, Route-to-Market, Pricing, as well as Trade and Promotions. Using Nielsen’s retail measurement of in-market performance the report also contrasts the practices of winners and non-winners (or “others”). Winners are companies that achieved higher sales growth than their categories, and outperformed others on one or more customer- or channel-management metrics.

Excelling in CCM is difficult. While 14 of the 23 companies surveyed ‘won’ in at least one module, only six ‘won’ in more than one, and only one company ‘won’ in all five.

Seizing the CPG Opportunity in China: Online and Out Ahead4

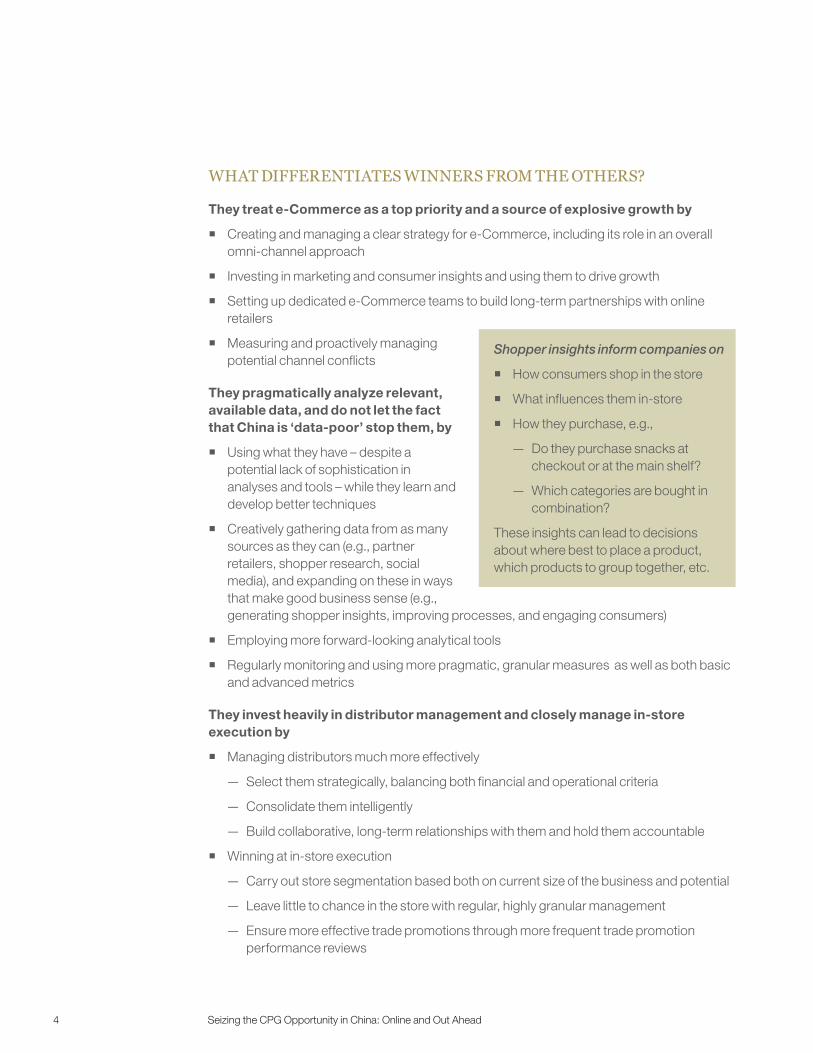

WHAT DIFFERENTIATES WINNERS FROM THE OTHERS?

They treat e-Commerce as a top priority and a source of explosive growth by

� Creating and managing a clear strategy for e-Commerce, including its role in an overall omni-channel approach

� Investing in marketing and consumer insights and using them to drive growth

� Setting up dedicated e-Commerce teams to build long-term partnerships with online retailers

� Measuring and proactively managing potential channel conflicts

They pragmatically analyze relevant, available data, and do not let the fact that China is ‘data-poor’ stop them, by

� Using what they have – despite a potential lack of sophistication in analyses and tools – while they learn and develop better techniques

� Creatively gathering data from as many sources as they can (e.g., partner retailers, shopper research, social media), and expanding on these in ways that make good business sense (e.g., generating shopper insights, improving processes, and engaging consumers)

� Employing more forward-looking analytical tools

� Regularly monitoring and using more pragmatic, granular measures as well as both basic and advanced metrics

They invest heavily in distributor management and closely manage in-store execution by

� Managing distributors much more effectively

— Select them strategically, balancing both financial and operational criteria

— Consolidate them intelligently

— Build collaborative, long-term relationships with them and hold them accountable

� Winning at in-store execution

— Carry out store segmentation based both on current size of the business and potential

— Leave little to chance in the store with regular, highly granular management

— Ensure more effective trade promotions through more frequent trade promotion performance reviews

Shopper insights inform companies on

� How consumers shop in the store

� What influences them in-store

� How they purchase, e.g.,

— Do they purchase snacks at checkout or at the main shelf?

— Which categories are bought in combination?

These insights can lead to decisions about where best to place a product, which products to group together, etc.

5Seizing the CPG Opportunity in China: Online and Out Ahead

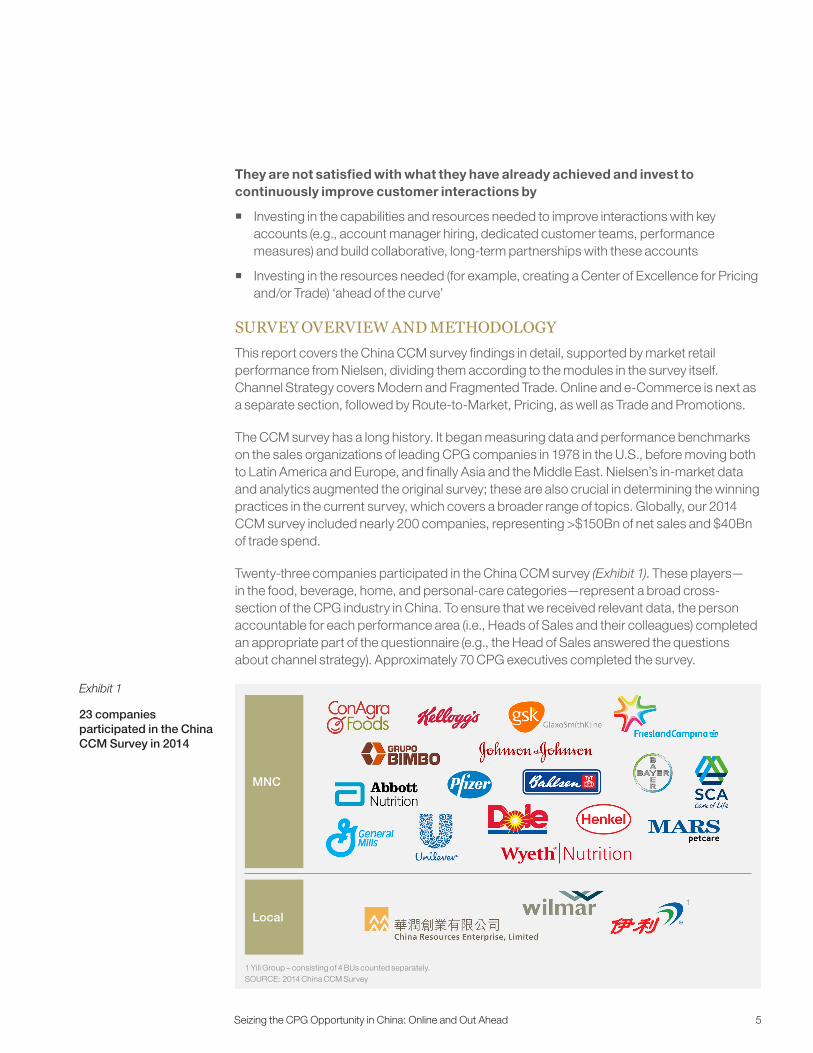

They are not satisfied with what they have already achieved and invest to continuously improve customer interactions by

� Investing in the capabilities and resources needed to improve interactions with key accounts (e.g., account manager hiring, dedicated customer teams, performance measures) and build collaborative, long-term partnerships with these accounts

� Investing in the resources needed (for example, creating a Center of Excellence for Pricing and/or Trade) ‘ahead of the curve’

SURVEY OVERVIEW AND METHODOLOGYThis report covers the China CCM survey findings in detail, supported by market retail performance from Nielsen, dividing them according to the modules in the survey itself. Channel Strategy covers Modern and Fragmented Trade. Online and e-Commerce is next as a separate section, followed by Route-to-Market, Pricing, as well as Trade and Promotions.

The CCM survey has a long history. It began measuring data and performance benchmarks on the sales organizations of leading CPG companies in 1978 in the U.S., before moving both to Latin America and Europe, and finally Asia and the Middle East. Nielsen’s in-market data and analytics augmented the original survey; these are also crucial in determining the winning practices in the current survey, which covers a broader range of topics. Globally, our 2014 CCM survey included nearly 200 companies, representing >$150Bn of net sales and $40Bn of trade spend.

Twenty-three companies participated in the China CCM survey (Exhibit 1). These players—in the food, beverage, home, and personal-care categories—represent a broad cross-section of the CPG industry in China. To ensure that we received relevant data, the person accountable for each performance area (i.e., Heads of Sales and their colleagues) completed an appropriate part of the questionnaire (e.g., the Head of Sales answered the questions about channel strategy). Approximately 70 CPG executives completed the survey.

Exhibit 1

23 companies participated in the China CCM Survey in 2014

MNC

Local

SOURCE: 2014 China CCM Survey1 Yili Group – consisting of 4 BUs counted separately.

1

Seizing the CPG Opportunity in China: Online and Out Ahead6

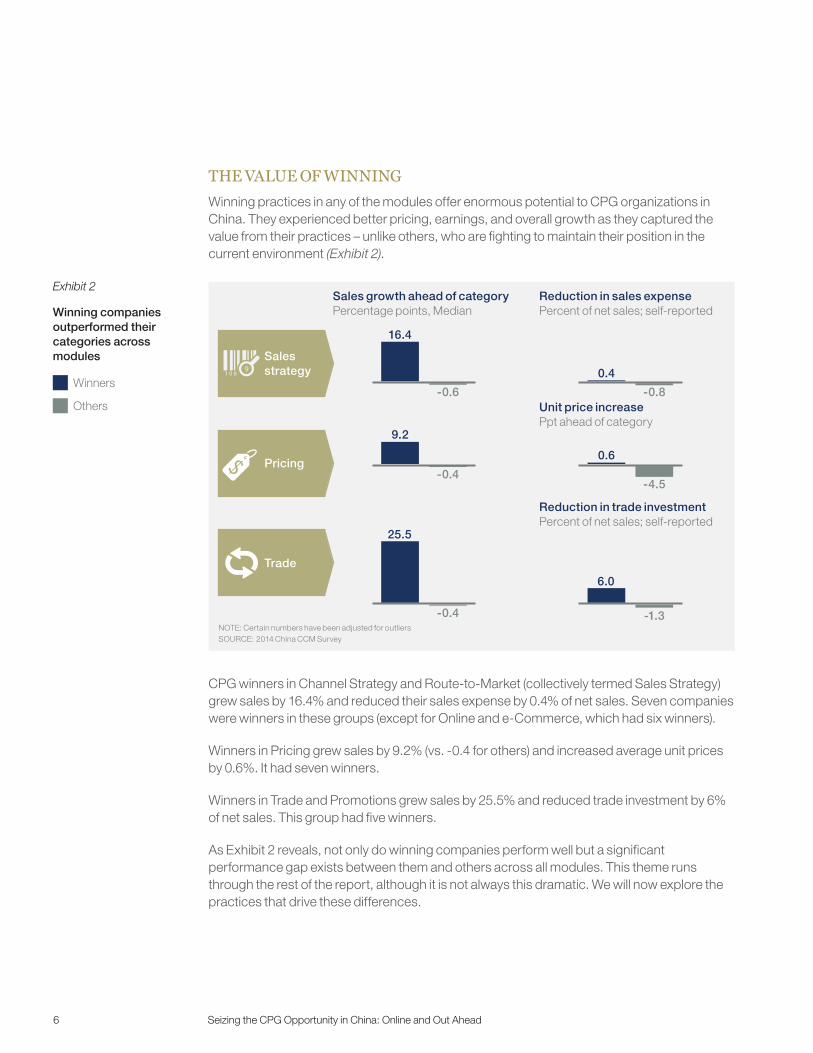

THE VALUE OF WINNING Winning practices in any of the modules offer enormous potential to CPG organizations in China. They experienced better pricing, earnings, and overall growth as they captured the value from their practices – unlike others, who are fighting to maintain their position in the current environment (Exhibit 2).

CPG winners in Channel Strategy and Route-to-Market (collectively termed Sales Strategy) grew sales by 16.4% and reduced their sales expense by 0.4% of net sales. Seven companies were winners in these groups (except for Online and e-Commerce, which had six winners).

Winners in Pricing grew sales by 9.2% (vs. -0.4 for others) and increased average unit prices by 0.6%. It had seven winners.

Winners in Trade and Promotions grew sales by 25.5% and reduced trade investment by 6% of net sales. This group had five winners.

As Exhibit 2 reveals, not only do winning companies perform well but a significant performance gap exists between them and others across all modules. This theme runs through the rest of the report, although it is not always this dramatic. We will now explore the practices that drive these differences.

Exhibit 2

Winning companies outperformed their categories across modules

Winners

Others

SOURCE: 2014 China CCM SurveyNOTE: Certain numbers have been adjusted for outliers

Sales growth ahead of categoryPercentage points, Median

Reduction in sales expensePercent of net sales; self-reported

Unit price increasePpt ahead of category

Reduction in trade investmentPercent of net sales; self-reported

16.4

-0.6

0.4

-0.8

9.2

-0.4

0.6

-4.5

25.5

-0.4

6.0

-1.3

Pricing

Trade

Sales strategy

7Seizing the CPG Opportunity in China: Online and Out Ahead

DETAILED FINDINGS FOR EACH SURVEY MODULE

Modern Trade

Build collaborative, long-term partnerships with key accounts (such as hyper / super chains). Over 1.5 times as many winners as others use “willingness to collaborate” as a core metric when segmenting and prioritizing their key accounts, in addition to current sales value and future growth potential. Once segmented and prioritized, joint setting of the account strategy and plan with the most important key accounts is a top priority for winners, as is the alignment of account targets.

Use cost-to-serve to optimize performance at key accounts. Around two-thirds of all participants measure the cost-to-serve of their key accounts, but more winners actually act on these results, making meaningful changes in their strategy (e.g., product mix, delivery size, or distribution model).

Invest in the capabilities and resources needed to improve the customer-facing functions for key accounts (e.g., customer marketing, shopper insights). All winners believe that a few critical capabilities – key account management, shopper insights, better access to retailer data, and rapid innovation – will drive key account growth. Most are investing heavily in building these capabilities. Over 85% of winners increased account managers at both the national and regional levels, assigned dedicated customer teams to their key accounts, and conducted rigorous performance evaluations. Almost 60% increased revenue management resources.

Fragmented Trade

Use a basic product portfolio to reduce overlap with other channels. Eighty-six percent of winners minimize the overlap between modern and fragmented trade by offering traditional retailers 25% or less of their total product portfolio, thereby reducing channel conflict and driving cost efficiencies. No winners provided their entire portfolio.

Use granular, growth-oriented data to segment and manage fragmented trade. Over half of winners segment their traditional retailers based on the store’s overall growth potential and type, in addition to its size. Growth potential measures include the store owners’ willingness to collaborate, the socioeconomic level of the store’s neighborhood, as well as the traffic levels directly next to the store. Over twice as many winners (43%) as others (17%) also manage execution at a granular level (i.e., channel and sub-channel) based on detailed data and shopper insights, in order to realize the development priorities of each outlet segment.

Actively measure channel conflict and implement containment strategies (e.g., coordinated promotional calendars, different packaging for different channels). Almost half of winners (43%) accomplish this with good results, versus 25% of others.

Different types of focus for smaller vs. larger players

Smaller players (net sales revenue < 1Bn RMB) are more likely to focus on regional hyper / super accounts because they do not have the scale and negotiating power needed to deal effectively with national key accounts.

Seizing the CPG Opportunity in China: Online and Out Ahead8

Online/e-Commerce

Six companies were winners in e-Commerce, with sales growth at an incredible 241% ahead of their categories. While online could be seen as “just another channel,” 63% of the participants in China believe its continued growth will create the biggest opportunities for them in the next five years. It is their absolute priority for growth. Most winners also believe that e-Commerce is and will be more profitable than brick-and-mortar stores (Exhibit 3).

Invest in marketing and consumer insights to drive growth. All winners invest more in online marketing and advertising spend (and also tend to have a better idea as to who they are actually reaching through these efforts), as well as online trade promotions and shopper marketing that gathers consumer insights. Over 2.5 times as many winners as others also invest in mobile initiatives (e.g., mobile coupons, and apps that drive consumer engagement).

1 Winners are defined as those in the top 25% of e-Commerce sales growth, with minimum sales of 25 million RMB

e-Commerce: a tremendous growth engine

~70% of participants see e-Commerce as their greatest growth opportunity, although the growth priorities will differ for relatively mature and emerging online categories. For instance, online players will increasingly focus on food (including home delivery) which may well be the next wave of growth.

At the same time participants will be concerned about increased pricing pressure from key online retailers, which may hinder their profitability. Almost 70% see increased pricing pressure within categories and online retailers’ stronger push for greater trade spend as issues.

Exhibit 3

Winners1 believe that online sales tend to be more profitable than brick-and-mortar

Winners

Others

SOURCE: 2014 China CCM SurveyHow profitable are your online sales compared to off-line/traditional sales? [1.21]

Profitability of online sales versus brick-and-mortarPercent of respondents who say online is more profitable

Two years ago

Achieved even though winners already invest more in marketing, trade promotion and mobile initiatives to drive online growth

Current

Tmall

JD

Yihaodian

Other online retailers

(e.g., Amazon, Jumei, Lefeng)

18

50

36

50

27

67

36

83

27

67

36

83

18

67

27

67

9Seizing the CPG Opportunity in China: Online and Out Ahead

Have a clear strategy for flagship stores on Tmall as well as their own Chinese ‘brand.com’. Winning companies rely more heavily on retailers such as Tmall rather than on their own brand.com. They typically perform only basic tasks on their own websites (e.g., general information about the company and its offerings) because Tmall has built up so much trust with consumers in China and has a leading position in the country’s B2C market. This poses a marked contrast to other markets. As a result, 80% of winners plan to increase their investments in their flagship stores on Tmall. All winners plan to collect better data on shopper insights and behaviors through their Tmall stores, and to enhance brand strength and potentially test new products and promotions.

Proactively manage any potential conflicts or pressure. Most winners view channel conflicts as a major barrier to online growth, but have already designed strategies to resolve them. They employ different SKUs, bundles, and unique online promotions. Taobao is a notorious pain point, but winners report increased success in collaborating with Taobao to better manage re-seller issues such as under-cutting prices and providing poor customer service. Taobao is now tracking consumer complaints more effectively, and most winners use this data to act against offending re-sellers. A smaller number of winners also use rewards and accountability to strengthen their relationships with the best-performing third-party re-sellers.

Build long-term partnerships with online retailers. Winners provide retailers with additional support across multiple dimensions. Online retailers receive more non-price support from winners, and winners have dedicated e-Commerce teams that create and sustain long-term partnerships with these retailers. A significant majority of winners also plan to invest heavily in their e-Commerce priorities over the next few years (Exhibit 4).

Exhibit 4

Winners invest much more in dedicated e-Commerce capabilities

Winners

Others

Key Account / HQ Selling

Sales Planning

Trade / Customer Marketing

Shopper Marketing

Shopper Insights

Marketing

73 73

45 27

45 27

18 27

45 9

18 9

100 67

100 67

83 50

83 83

67 67

50 67

SOURCE: 2014 China CCM Survey

1 Additional response options not shown.Do you have dedicated resources for different types of roles within your e-Commerce team? [2.3]Where are you planning on increasing headcount over the next two years? (All that apply) [2.5]

Share of dedicated resources within e-Commerce team by roles1

Percent of respondents who have dedicated resources

Where headcounts will be increasing over the next two years1

Percent of respondents who are expanding resources

Seizing the CPG Opportunity in China: Online and Out Ahead10

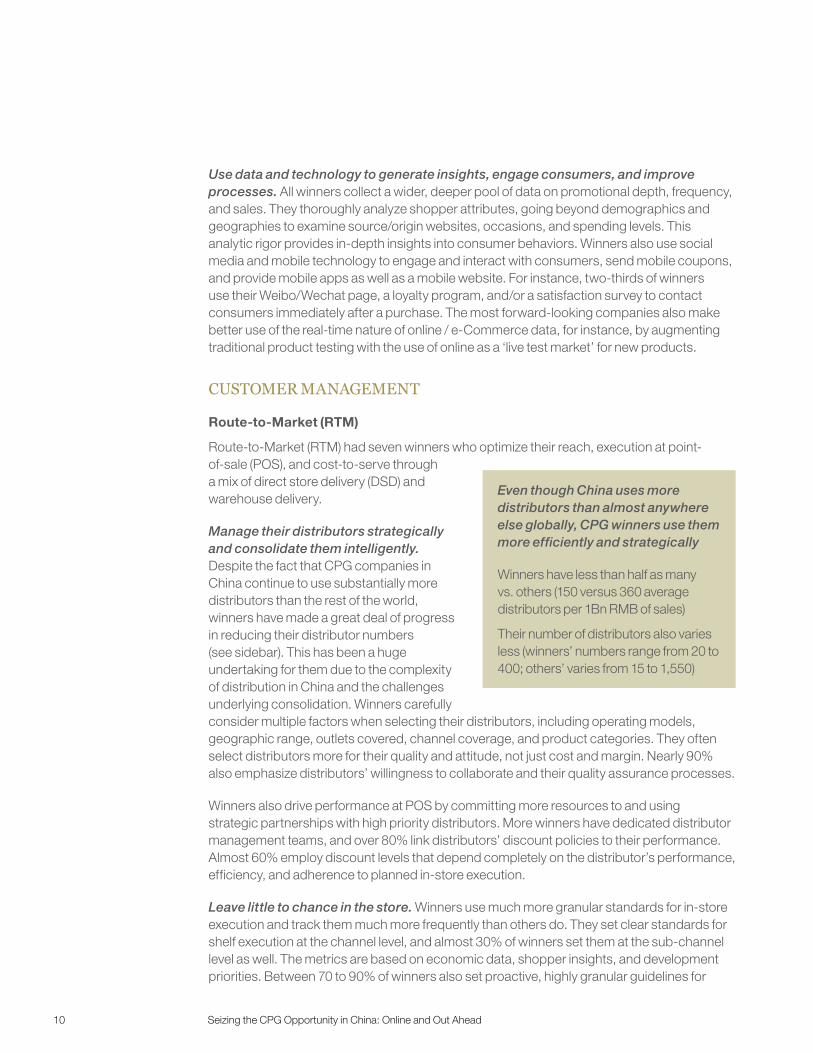

Use data and technology to generate insights, engage consumers, and improve processes. All winners collect a wider, deeper pool of data on promotional depth, frequency, and sales. They thoroughly analyze shopper attributes, going beyond demographics and geographies to examine source/origin websites, occasions, and spending levels. This analytic rigor provides in-depth insights into consumer behaviors. Winners also use social media and mobile technology to engage and interact with consumers, send mobile coupons, and provide mobile apps as well as a mobile website. For instance, two-thirds of winners use their Weibo/Wechat page, a loyalty program, and/or a satisfaction survey to contact consumers immediately after a purchase. The most forward-looking companies also make better use of the real-time nature of online / e-Commerce data, for instance, by augmenting traditional product testing with the use of online as a ‘live test market’ for new products.

CUSTOMER MANAGEMENT

Route-to-Market (RTM)

Route-to-Market (RTM) had seven winners who optimize their reach, execution at point-of-sale (POS), and cost-to-serve through a mix of direct store delivery (DSD) and warehouse delivery.

Manage their distributors strategically and consolidate them intelligently. Despite the fact that CPG companies in China continue to use substantially more distributors than the rest of the world, winners have made a great deal of progress in reducing their distributor numbers (see sidebar). This has been a huge undertaking for them due to the complexity of distribution in China and the challenges underlying consolidation. Winners carefully consider multiple factors when selecting their distributors, including operating models, geographic range, outlets covered, channel coverage, and product categories. They often select distributors more for their quality and attitude, not just cost and margin. Nearly 90% also emphasize distributors’ willingness to collaborate and their quality assurance processes.

Winners also drive performance at POS by committing more resources to and using strategic partnerships with high priority distributors. More winners have dedicated distributor management teams, and over 80% link distributors’ discount policies to their performance. Almost 60% employ discount levels that depend completely on the distributor’s performance, efficiency, and adherence to planned in-store execution.

Leave little to chance in the store. Winners use much more granular standards for in-store execution and track them much more frequently than others do. They set clear standards for shelf execution at the channel level, and almost 30% of winners set them at the sub-channel level as well. The metrics are based on economic data, shopper insights, and development priorities. Between 70 to 90% of winners also set proactive, highly granular guidelines for

Even though China uses more distributors than almost anywhere else globally, CPG winners use them more efficiently and strategically

Winners have less than half as many vs. others (150 versus 360 average distributors per 1Bn RMB of sales)

Their number of distributors also varies less (winners’ numbers range from 20 to 400; others’ varies from 15 to 1,550)

11Seizing the CPG Opportunity in China: Online and Out Ahead

field teams, including ones for specific store activities, promotions, and SKUs that should be listed and in stock. They also track performance more frequently, including sales representatives’ in-store performance and order/delivery efficiency. For instance, all winners tracked the number of outlet visits per day and speed to shelf on a weekly basis. Over 80% also monitored total sales to customers, promotion compliance, and store visit compliance/call completion rates every week.

Use systems and data more effectively to optimize customer management. Winners invest in mobile technologies and systems that will enhance in-store execution and help them act on consumer and shopper insights. For instance, low-cost smartphones equipped with the right apps can help winners’ field teams capture relevant data and carry out route planning as well. In addition, most winners employ a customer relationship management system of some type, whether to track the sales pipeline and conversion, or for account planning.

Pricing

CPG companies in China must set their suggested prices thoughtfully in various categories, as different degrees of freedom may exist across different product categories. After carefully considering each category, organizations should select the strategic and tactical levers that would help them set the most appropriate suggested price for that category. Many of the winning practices below can help them as they go through this process.

Focus employees on driving revenue, not just volume. The majority of winners (83%) maintained price increases on their Tier 1 and Tier 2 brands over the past two years, while all winners grew sales during this period. Winners did so by tending to focus more on revenue than volume or any other variable when evaluating key employees, in order to better cultivate a value-driven mindset versus a purely volume-driven mindset.

Seizing the CPG Opportunity in China: Online and Out Ahead12

Regularly monitor and use granular measures. More granular metrics help winners take more precise, targeted actions (Exhibit 5). These companies consider consumer price elasticity more than 1.5 times as often as others do when setting suggested list prices. They also measure price elasticity and price gaps at a much more granular level (e.g., SKU, pack size, customer, and brand).

Improve suggested price compliance by frequently tracking and adjusting prices for Tier 1 and Tier 2 products. Around 70% of winners track pricing metrics at least monthly (including net revenue per unit, price gap to competition, net profit per unit, and velocity). They also review and adjust suggested list prices for Tier 1 and Tier 2 products more frequently. For instance, all winners review Tier 1 suggested list prices semi-annually or more often, while ~ 70% do so for Tier 2 suggested list prices as well. This process helps winners achieve better compliance at POS, where 70% achieve 80% compliance with suggested prices while others only capture 50% to 80% compliance.

Establish a Center of Excellence for Pricing, possibly combined with Trade. Almost 90% of winners establish a Center of Excellence (COE) for Pricing, and a little over 80% create a single COE for Pricing and Trade. This ensures that institutional muscle is built up over time as a focused set of resources becomes increasingly comfortable and adept at carrying out pricing and trade analyses.

Winners

Others

Exhibit 5

Winners also monitor price at a much more granular level

SKU

Customer

Pack Size

Category

Channel

Brand

27

18

18

36

45

55

71

57

57

57

43

43

55

27

36

64

55

73

71

71

43

71

43

71

SOURCE: 2014 China CCM Survey

1 Additional response options not shown.At what levels do you regularly (i.e., at least every 12 months) measure and track price elasticity? (All that apply) [2.5]At what levels do you regularly (i.e., at least every 12 months) measure and track price gaps? (All that apply) [2.6]

Level at which price elasticity is measured1

Percent of respondentsLevel of granularity

Level at which price gaps are measured1

Percent of respondentsHigh

Low

13Seizing the CPG Opportunity in China: Online and Out Ahead

Trade and promotions

Employ more forward-looking analytical approaches when setting trade rates. The majority of winners combine an integrated ATL/BTL media mix model with other methods when they set trade levels between Trade and Marketing. While over half (60%) employ basic metrics, even more (80%) use more forward-looking measures such as trade ROI and retailer/distributor category growth.

Ensure more effective trade promotions by reviewing trade promotion performance more frequently. All winners conduct important analyses monthly or even more frequently, including event-level post promotion analyses and trade performance reviews. Most (80% to 100%) use both basic and advanced metrics (such as cannibalization impact and incremental customer ROI). In addition, 80% of winners conduct formal reviews of price-related trade spend (e.g., TPRs or EDLP), while 60% conduct formal reviews of non-price trade spend (e.g., merchandising). All winners also take immediate action based on these reviews, re-planning the remaining events in the year to improve performance without changing the level of funding.

Invest in the resources needed to achieve trade promotion excellence. Winners dedicate resources to build the integrated revenue management capabilities they need to increase net selling price over time (through a combination of price and mix effects). Although ~80% of participants have a Trade or Trade and Pricing COE, more winners created dedicated trade teams and invested in trade tools to carry out increasingly more advanced analytics over time.

* * *

CPG companies in China have an incredible opportunity if they are willing to commit themselves and develop a truly seamless, omni-channel approach. By developing the capabilities and systems they need to capitalize on e-Commerce’s explosive growth, while continuing to manage their physical channels effectively, they can significantly strengthen their competitive advantage both now and in the future. However, they will need to adopt forward-looking practices, integrate different market views, and hone their underlying analytical skills. This road will be long and challenging, but those who succeed will not only achieve their individual targets but position themselves as true leaders in one of the world’s largest markets.

Trade: Building the tools winners need to capture and analyze the data for decision-making

Over 1.5 times as many winners are creating and using Trade Promotion Optimization (TPO) tools

80% to 100% of winners capture data through multiple sources, including syndicated scans, their partner retailers, and proprietary shopper research

Seizing the CPG Opportunity in China: Online and Out Ahead14

AUTHORSFelix Poh is a principal in McKinsey’s Shanghai office, Max Magni is a director in the New Jersey office and Rohit Razdan is a principal in the Singapore office.

CONTACTS

McKinsey & Company

Nielsen

Yi Jin Kiki Fan, Managing Director – Nielsen China; [email protected]

Christopher Kong, Senior Director; [email protected]

About McKinsey & Company

McKinsey & Company is a global management consulting firm, deeply committed to helping institutions in the private, public, and social sectors achieve lasting success. For over eight decades, our primary objective has been to serve as our clients’ most trusted external advisor. With consultants in more than 100 offices in 60 countries, we bring unparalleled expertise to clients across all industries and functions, anywhere in the world. We work closely with teams at all levels of an organization to shape winning strategies, mobilize for change, build capabilities, and drive successful execution.

About Nielsen

Nielsen Holdings N.V. (NYSE: NLSN) is a global information and measurement company with leading market positions in marketing and consumer information, television and other media measurement, online intelligence, mobile measurement, trade shows, and related properties. Nielsen has a presence in approximately 100 countries, with headquarters in New York, United States, and Diemen, the Netherlands. For more information, visit nielsen.com.

Acknowledgements

The authors are grateful to the executives who offered valuable insights for this publication.

The authors would like to thank the following McKinsey colleagues for their contribution and support: Alex Sawaya, Amrita Dhar Sen, Tina Shen and Xiaodong Zhang.

15Seizing the CPG Opportunity in China: Online and Out Ahead

2/F, East Ocean Centre (Phase II) 618 Yanan East Road Huang Pu District Shanghai 200001 People’s Republic of China

+86 (21) 2326 9200

www.nielsen.com

17/F Platinum Building 233 Tai Cang Road Shanghai 200020 People’s Republic of China

Phone: +86 (21) 6385 8888 Fax: +86 (21) 6386 2000

www.mckinsey.com