Embed Size (px)

Citation preview

TRID Rule Overview TILA-RESPA Integrated Disclosure Rule

Introduction

For more than 30 years, Federal law has required lenders to provide two different disclosure forms to consumers applying for a mortgage. The law also has generally required two different forms at or shortly before closing on the loan. Two different Federal agencies developed these forms separately, under two different Federal statutes; The Truth-in-Lending Act and the Real Estate Settlement Procedures Act of 1974. The information on these forms is overlapping and the language is inconsistent. Consumers often find the forms confusing, and lenders and settlement agents find the forms burdensome to provide and explain.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 2

Overview

Dodd-Frank Wall Street Reform and Consumer Protection Act: – Created the Consumer Financial Protection Bureau (“CFPB”);– Mandated that the CFPB integrate mortgage disclosures; Truth-in-Lending Act (“TILA”); Real Estate Settlement Procedures Act of 1974 (“RESPA”).

– Currently there are four different disclosure forms; Two forms when a customer applies for a mortgage; Two forms when closing a loan.

– As of October 3, 2015, there will be two integrated disclosure forms; Loan Estimate; Closing Disclosure.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 3

Overview (cont.)

TILA-RESPA Integrated Disclosure (“TRID”) Rule is far more than a new set of disclosures.

TRID ushers in new responsibilities for lenders, title companies, and other settlement service providers that might also bring new liability and enforcement risks.

Challenges CCM faces:– Major system changes;– Business process changes;– Training; and– Monitoring.

New forms must be embedded into technology and business systems.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 4

New Forms

Loan Estimate (“LE”)– Integrates Initial TILA disclosure and RESPA Good Faith Estimate

(“GFE”).– Generally contains:

First page: 1) identifying information describing the borrower and the loan; 2) loan terms, amount, payments, and rate; 3) particular loan features such as prepayment penalties and balloon payments; 4) projected payments showing any increases; and 5) estimated cash to close and closing costs.

Second page breaks down closing costs and includes details on pre-paid and escrowed amounts and cash to close.

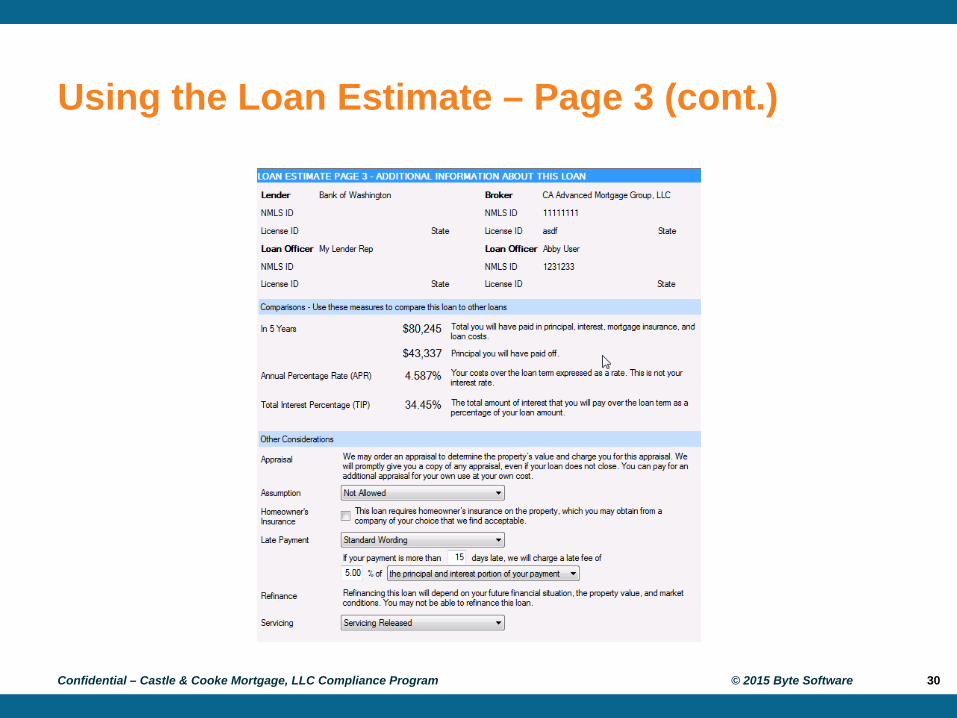

Third page contains a series of additional disclosures regarding: total payments of five years; APR; Total Interest Payment (“TIP”); appraisal availability to borrower; whether assumable, requirement for homeowners insurance; late payment policies; refinancing not guaranteed; and the possibility of servicing transfer.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 5

New Forms

Closing Disclosure (“CD”)– Merges and replaces the final Truth-in-Lending (“TIL”) statement and

the HUD-1 settlement statement.– Generally contains:

First page: Essentially the same as the first page of the LE and contains: 1) identifying information describing borrower and loan ; 2) loan terms, amount, payments and rate; 3) particular loan features such as prepayment penalties and balloon payments; 4) projected payments showing any increases; and 5) estimated cash to close and closing costs.

Second and third pages: Include closing cost details and a calculation of cash to close and a summary of the real estate transaction.

Fourth and fifth pages: Provide several disclosures, including whether loan is assumable; whether loan has demand feature; late payment policies; refinancing can’t be guaranteed; potential for servicing transfer; appraisal availability to borrower; APR; finance charge; amount financed; and Total Interest Percentage.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 6

Applicability

Effective for all loans with an application date on or after October 3, 2015.

Covers most closed-end consumer credit transactions secured by real estate.

Includes certain loans that are currently subject to TILA but not RESPA (construction-only loans, loans secured by vacant land or by 25 or more acres, and credit extended to certain trusts for tax or estate planning purposes).

No small creditor exemption under this rule. Higher priced mortgages are covered (with other

additional HPM rules).

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 7

Applicability (cont.)

Does not apply to:– Home Equity Lines of Credit (“HELOCs”);– Reverse Mortgages;– Mortgages secured by a mobile home, or a dwelling not attached

to land (e.g. house boat);– Commercial / business loans;– Loans made by a person or entity making five or fewer mortgages

in a calendar year and thus is not a creditor; and– Partial exemption for certain transactions associated with housing

assistance loan programs for low- to moderate-income borrowers. Exempt from the requirement to provide the RESPA Settlement Cost

Booklet, RESPA GFE, RESPA settlement statement, application servicing disclosure statement, the LE, the CD and the Special Information Booklet.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 8

Applicability (cont.)

The integrated disclosure forms may not be used prior to October 3, 2015.

The old forms must be used for all applications received prior to October 3, 2015.

The old law is in effect until October 3, 2015.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 9

Loan Estimate

Good faith estimate of credit costs and loan terms. Must follow 12 C.F.R. §1026.37 and use standard form H-24. Provides consumer with a good faith estimate of credit costs

and transaction items. Must be in writing. Satisfy timing and delivery requirements:

– Delivered or placed into the mail no later than three general business days after the loan application;

– It is considered to be received three business days after being placed in the mail;

– Must be delivered or placed into the mail no later than seven general business days before “consummation;” and

– Delivery can be hand delivered, mailed or sent electronically.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 10

Waivers

No waiver of the three-day delivery requirement. Waiver of the seven-day requirement:

– Must have a bona-fide personal financial emergency;– Must have a written statement from the consumer that describes

the bona-fide financial emergency; and– The lender may not provide a pre-printed form defining the

“emergency.”

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 11

Definitions

“Application” is considered to be made when the consumer submits all of the following:– Name;– Income;– Social security number (for requesting a credit report);– Property address;– Property value estimate; and– Requested mortgage loan amount.

An application can be written or electronic and can include a written record of an oral application.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 12

Definitions (cont.)

“Business day” for delivering the Loan Estimate, a day on which the creditor’s offices are open to the public for carrying out substantially all of its business functions.

“Business day” for other purposes, including delivery of the Closing Disclosure, is all calendar days except Sundays and legal public holidays.

As defined in Regulation Z, “consummation” is when a consumer becomes contractually obligated on a credit transaction.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 13

Loan Estimate: “Good Faith” Requirement

Must estimate in good faith consistent with the best information reasonably available to the creditor at the time disclosed.

General rule to determine “good faith:” – Look at difference between actual charges and charges in the

Loan Estimate;– If actual charges exceed charges listed in the Loan Estimate: Not

in good faith; – If actual charges are equal to or less than charges listed in the

Loan Estimate: In good faith; and– Good faith depends on the sum of all the charges in a particular

category.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 14

Revisions and Corrections to Loan Estimates

Creditors are bound by the LE and may not issue revisions because they discover technical errors, miscalculations, or underestimations of charges.

Revised LEs only permitted in certain circumstances:– Changed circumstances that exceeds tolerance;– Changed circumstances that affects eligibility;– Consumer-requested revisions;– Interest rate locked and points of lender credits change;– Consumer delay of more than 10 days to proceed; and– New construction loan and settlement is delayed.

When there is a changed circumstance after the LE has been provided, the creditor can revise the LE within three business days.

The revised LE generally can be provided NO LATER than seven business days before consummation.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 15

Definitions

“Changed Circumstances” means:– An extraordinary event;– Information relied on turns out to be inaccurate, or it changed after

disclosures provided; or– New information that creditor did not rely on.

Examples:– Natural disaster;– New title insurer; and– New and/or changed information discovered.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 16

Loan Estimate - Timing

Must be provided to the borrower within three business days of receiving the application:– In person;– Electronically (via E-Sign Rules); and– Placed in the mail in accordance with the “Mailbox Rule.”

If the consumer withdraws within the three-day period, then you do not have to provide the LE.

If the creditor can’t approve the loan based on the terms requested by the consumer, you don’t have to provide a LE.

If the consumer amends the application, then you must provide the LE within three days of receiving the amended application.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 17

Loan Estimate – Timing (cont.)

If the consumer withdraws the application or the creditor determines that it cannot be approved on the terms requested by the consumer within the three-business day period, the creditor does not have to provide the LE.– However, if the LE is not provided the creditor will not have

complied with the LE requirements under Regulation Z if it later consummates the transaction on the terms originally applied for by the consumer.

The creditor must ensure that the consumer receives the revised LE no later than four business days prior to consummation.

Cannot provide a revised LE in conjunction with or after you provide the CD.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 18

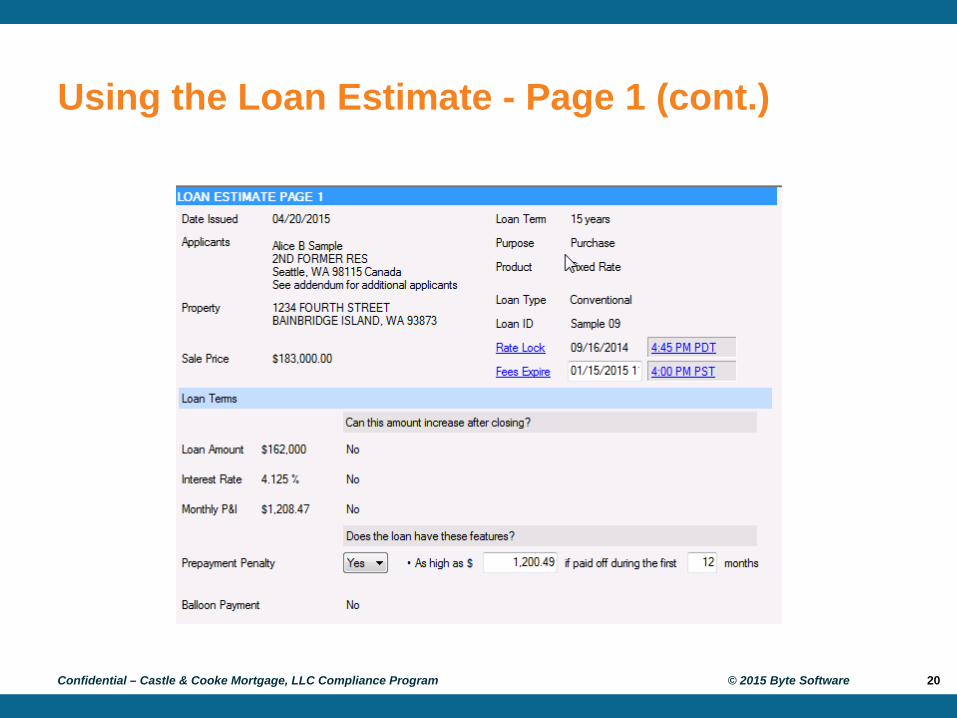

Using the Loan Estimate – Page 1

Page 1 – General information– Application data – property, loan, and rate lock status– Loan terms– Projected payments during the term of the loan– Costs at closing including the total estimated closing costs and the

estimated cash to close

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 19

Using the Loan Estimate - Page 1 (cont.)

Confidential – Castle & Cooke Mortgage, LLC Compliance Program © 2015 Byte Software 20

Using the Loan Estimate - Page 1 (cont.)

Confidential – Castle & Cooke Mortgage, LLC Compliance Program © 2015 Byte Software 21

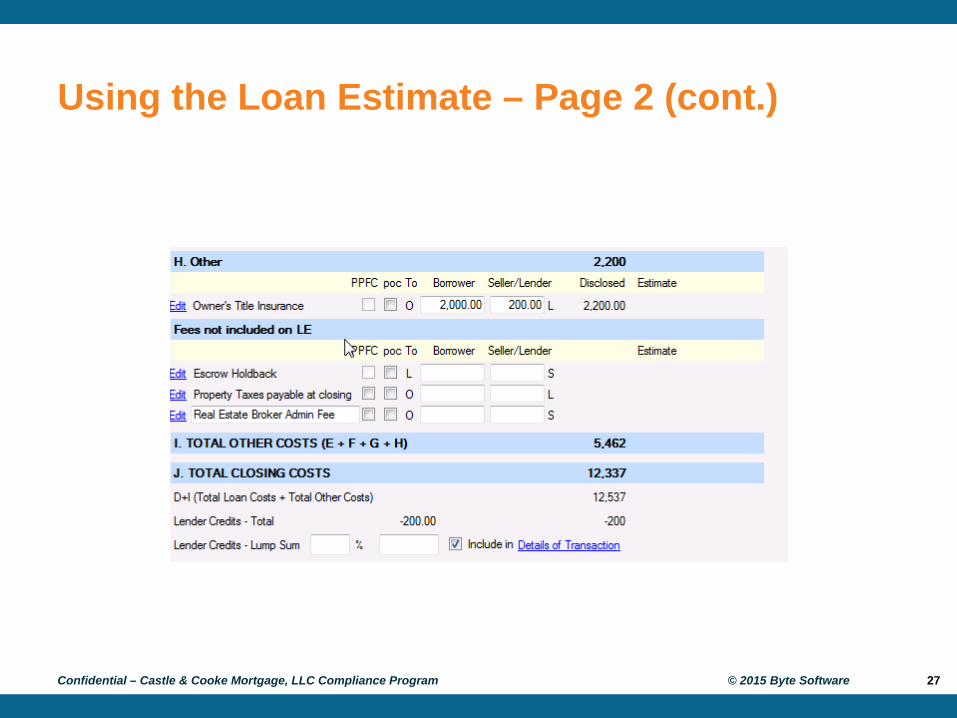

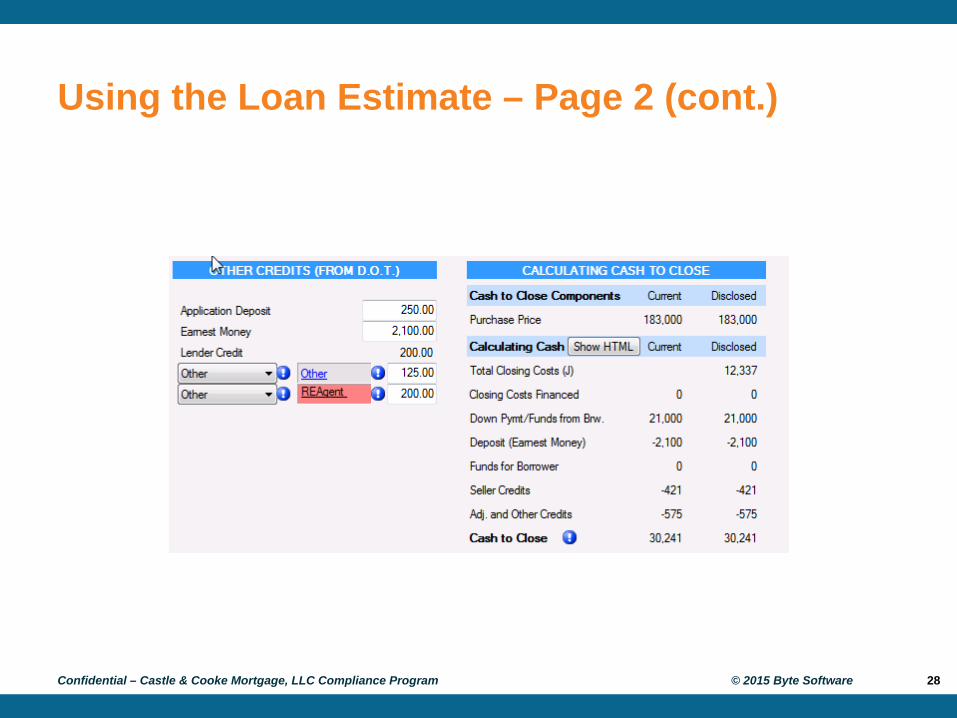

Using the Loan Estimate - Page 2

Page 2 – Costs– A good-faith itemization of the loan costs and other costs

associated with the loan. Loan costs - paid by the consumer to the creditor or third-party

provider. Other costs – taxes, governmental recording fees and certain other

payments involved in the closing process.– A calculating cash to close table.– Adjustable payment table.– Adjustable interest rate table.– Consumer must pay during the origination of the loan.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 22

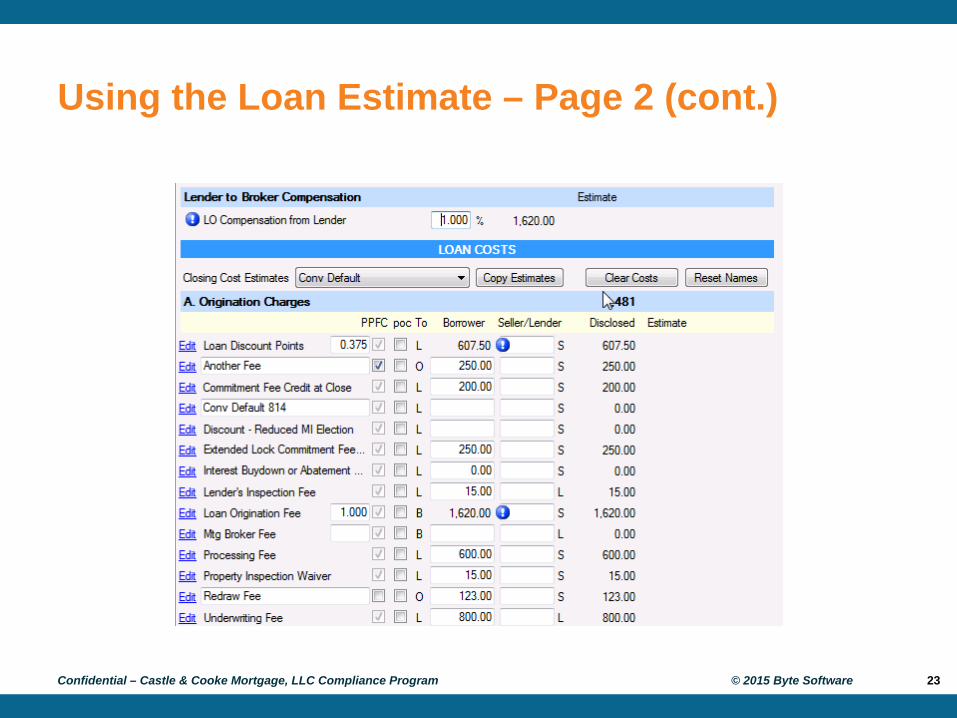

Using the Loan Estimate – Page 2 (cont.)

Confidential – Castle & Cooke Mortgage, LLC Compliance Program © 2015 Byte Software 23

Using the Loan Estimate – Page 2 (cont.)

Confidential – Castle & Cooke Mortgage, LLC Compliance Program © 2015 Byte Software 24

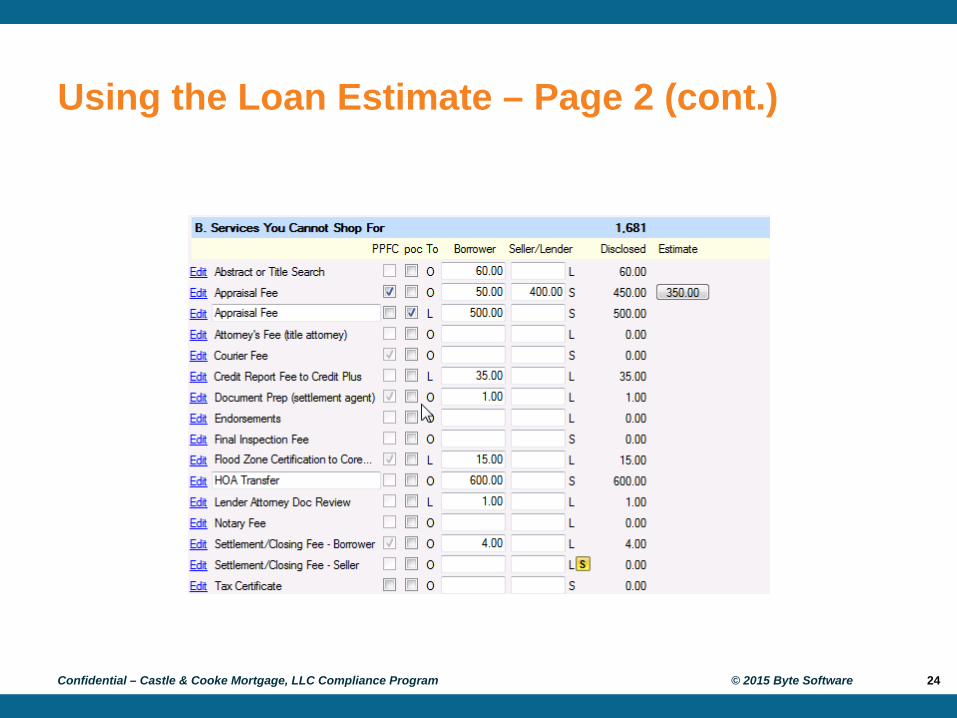

Using the Loan Estimate – Page 2 (cont.)

Confidential – Castle & Cooke Mortgage, LLC Compliance Program © 2015 Byte Software 25

Using the Loan Estimate – Page 2 (cont.)

Confidential – Castle & Cooke Mortgage, LLC Compliance Program © 2015 Byte Software 26

Using the Loan Estimate – Page 2 (cont.)

Confidential – Castle & Cooke Mortgage, LLC Compliance Program © 2015 Byte Software 27

Using the Loan Estimate – Page 2 (cont.)

Confidential – Castle & Cooke Mortgage, LLC Compliance Program © 2015 Byte Software 28

Using the Loan Estimate – Page 3

Page 3 – Additional information about the loan.– Contact information– Comparisons table– Other considerations table– Signature statement

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 29

Using the Loan Estimate – Page 3 (cont.)

Confidential – Castle & Cooke Mortgage, LLC Compliance Program © 2015 Byte Software 30

Tolerance and Variance Guidelines

Creditor may charge the consumer more than the amount disclosed in the LE in specific circumstances.

What can change:– Certain amounts can change under the rule;– Others may change with certain tolerance thresholds; and– Changed circumstances.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 31

Zero Tolerance Fees

Fees paid to creditor, mortgage broker, or an affiliate of either.

Fees paid to an unaffiliated third-party if the creditor did not permit the consumer to shop.

Transfer taxes. For charges subject to zero tolerance, any amount

charged beyond the amount disclosed on the LE must be refunded to the consumer.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 32

Definitions

Affiliate – any company that controls, is controlled by, or is under common control with another company, as set forth in the Bank Holding Company Act of 1956.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 33

10% Tolerance Fees

Charges for third-party services and recording fees paid by or imposed on the consumer are grouped together and subject to a 10% cumulative tolerance.

The creditor may charge the consumer more than the amount disclosed on the LE for any of these charges so long as the total sum of the charges added together does not exceed the sum of all such charges disclosed on the LE by more than 10%. If it does, the difference must be refunded to the consumer.

These charges are:– Recording fees; and– Charges for third-party services:

Not paid to the creditor or an affiliate of the creditor; and Consumer is permitted by the creditor to shop, and selects a service

provider from the creditor’s written list of service providers.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 34

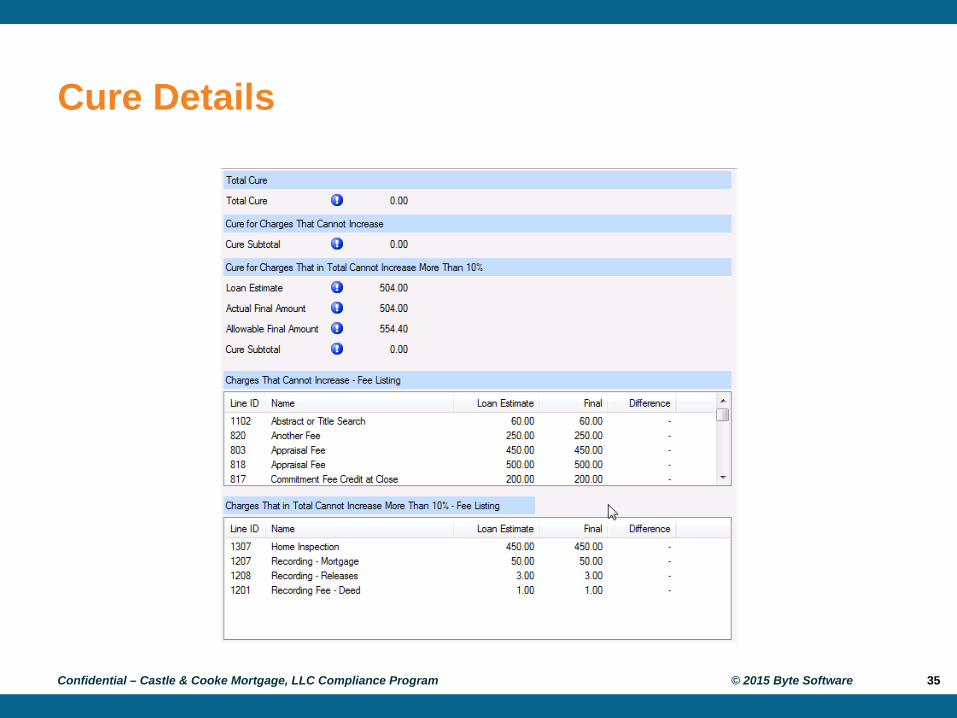

Cure Details

Confidential – Castle & Cooke Mortgage, LLC Compliance Program © 2015 Byte Software 35

No Tolerance Fees

Prepaid interest. Property insurance premiums. Amounts placed into escrow, impound, reserve, etc. For services required by the creditor if the creditor

permits the consumer to shop: charges paid to third-party service providers not included on creditor’s written list.

Charges paid to third-party service providers for services not required by the creditor.

Change circumstance applies.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 36

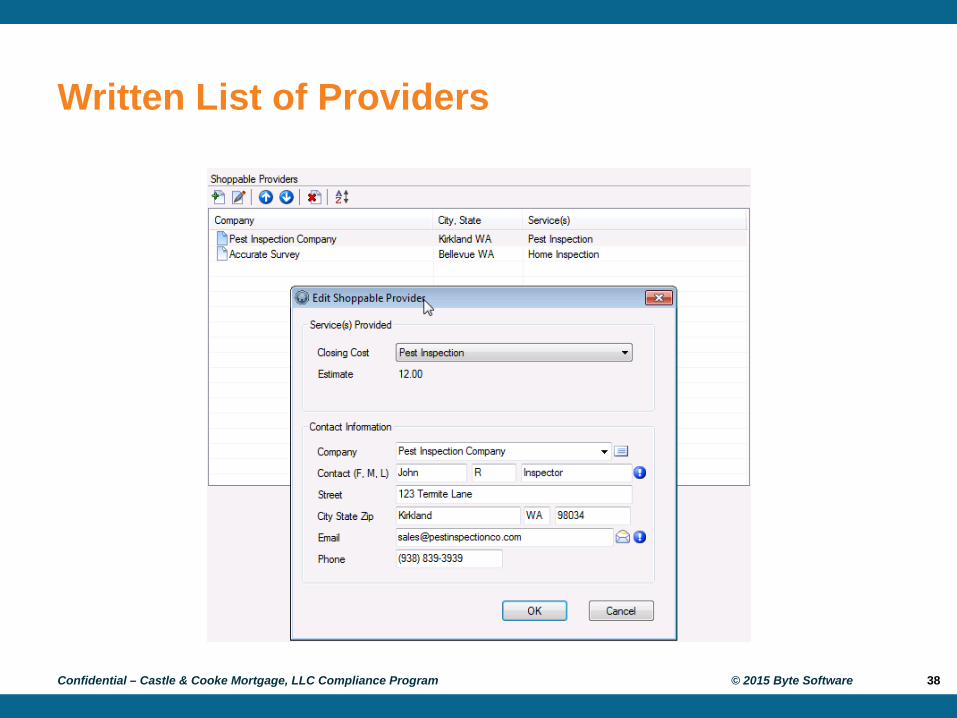

Loan Estimate – When is a Consumer Permitted to Shop for a Service?

If the consumer is permitted to shop for a settlement service, the creditor must provide the consumer with a written list of services for which the consumer can shop.

The written list is separate from the LE, but must be provided within the same time frame – no later than three-business days after the creditor receives the application.

The list must identify at least one available settlement service provider for each service.

State that the consumer may choose a different provider of that service.

The service providers identified on the written list must correspond to the settlement services for which the consumer can shop as disclosed on the LE.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 37

Written List of Providers

Confidential – Castle & Cooke Mortgage, LLC Compliance Program © 2015 Byte Software 38

Loan Estimate: Exceptions

When a creditor may charge the consumer more than the amount disclosed in the LE:– When certain variations are expressly permitted by the TILA –

RESPA Rule;– The amount charged falls within explicit tolerance thresholds and

the estimate is not for a zero tolerance charge where variations are never permitted; and

– Certain changed circumstances permit a revised LE or a CD that permits the charge to be changed.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 39

Closing Disclosures

This form integrates and replaces the existing HUD-1 and the Final TIL disclosure.

For federally related mortgage loans form H-25 must be used.

The creditor is required to ensure the consumer receives the CD no later than three-business days before consummation.

The CD generally must contain the actual terms and costs of the transaction.

Creditors provide the CD for to the consumer. Creditors may use settlement agents to provide the CD

as long as the creditor ensures compliance.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 40

Closing Disclosure (cont.)

In rescindable transactions, the CD must be given separately to each consumer who has the right to rescind under TILA.

In transactions that are not rescindable, the CD may be provided to any consumer with primary liability on the obligation.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 41

Closing Disclosure - Timing

The CD must be received by the consumer at least three-business days before consummation.

The CD must be delivered or placed in the mail no later than seven-business days before consummation.– May be delivered “in person.”– May be delivered via electronic delivery methods subject to

compliance with the consumer consent and other applicable provisions of the Electronic Signatures in Global and National Commerce Act (15 U.S.C.) [(§ 1026.19)(f)(1)(ii)(A)].

Note: “Business day” for CD delivery purposes is all calendar days except Sundays and legal public holidays.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 42

Closing Disclosure – Timing (cont.)

Consumers may waive or modify the three-business day waiting period when:– The extension of credit is needed to meet a “bona fide personal

financial emergency.”– The consumer has received the CD, and– The consumer give the creditor a dated written statement that : Describes the emergency; Specifically modifies or waives the waiting period; Bears the signature of all consumers who are primarily liable on the

legal obligation; and Note: the creditor is prohibited from providing the consumer with a

pre-printed waiver form.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 43

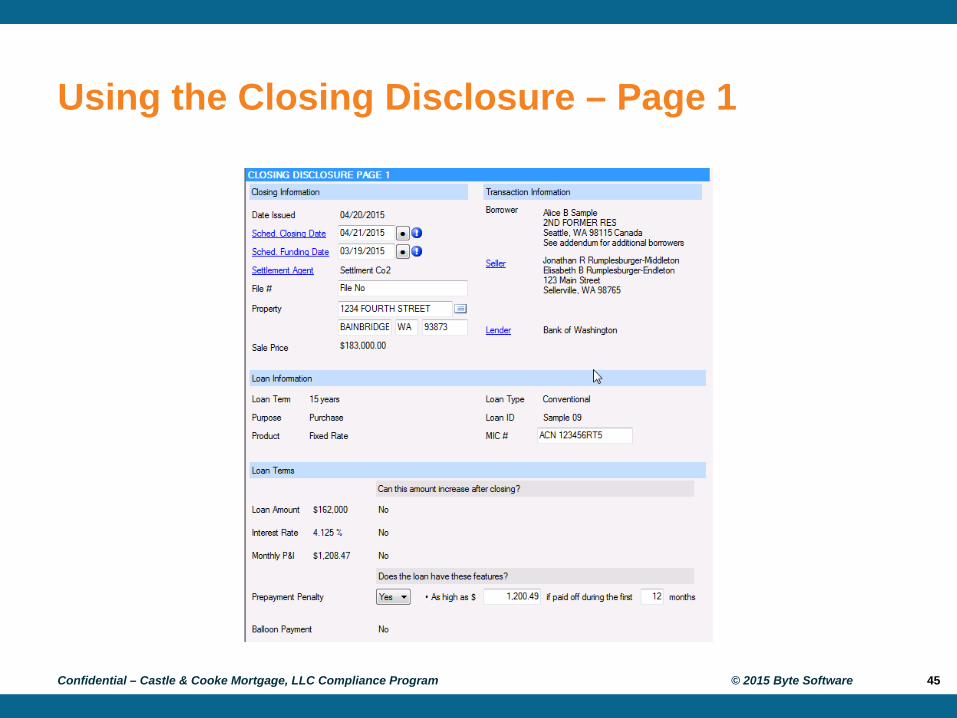

Using the Closing Disclosure

Page 1 – General information (mirrors the LE)– loan terms– projected payments – costs at closing

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 44

Using the Closing Disclosure – Page 1

Confidential – Castle & Cooke Mortgage, LLC Compliance Program © 2015 Byte Software 45

Using the Closing Disclosure – Page 1 (cont.)

Confidential – Castle & Cooke Mortgage, LLC Compliance Program © 2015 Byte Software 46

Using the Closing Disclosure – Page 2

Page 2 – Loan costs and other costs

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 47

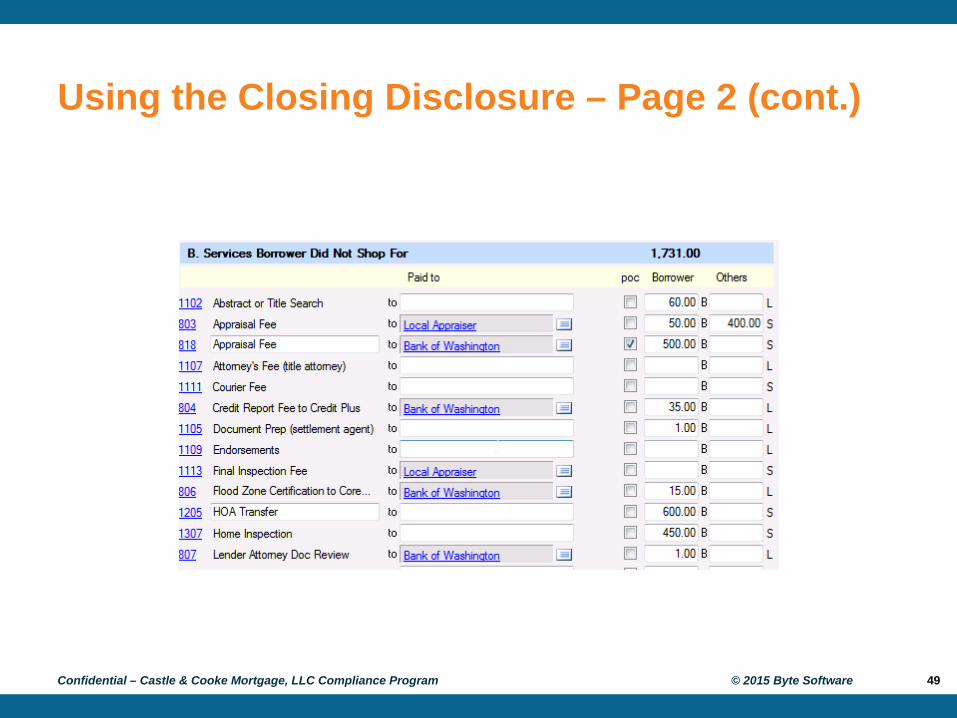

Using the Closing Disclosure – Page 2 (cont.)

Confidential – Castle & Cooke Mortgage, LLC Compliance Program © 2015 Byte Software 48

Using the Closing Disclosure – Page 2 (cont.)

Confidential – Castle & Cooke Mortgage, LLC Compliance Program © 2015 Byte Software 49

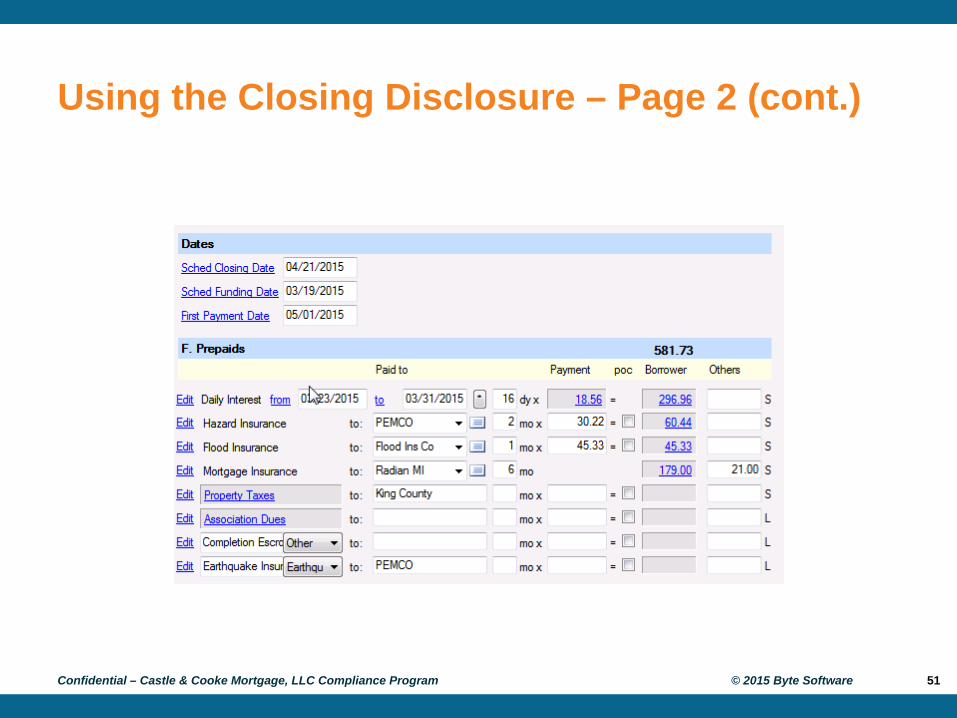

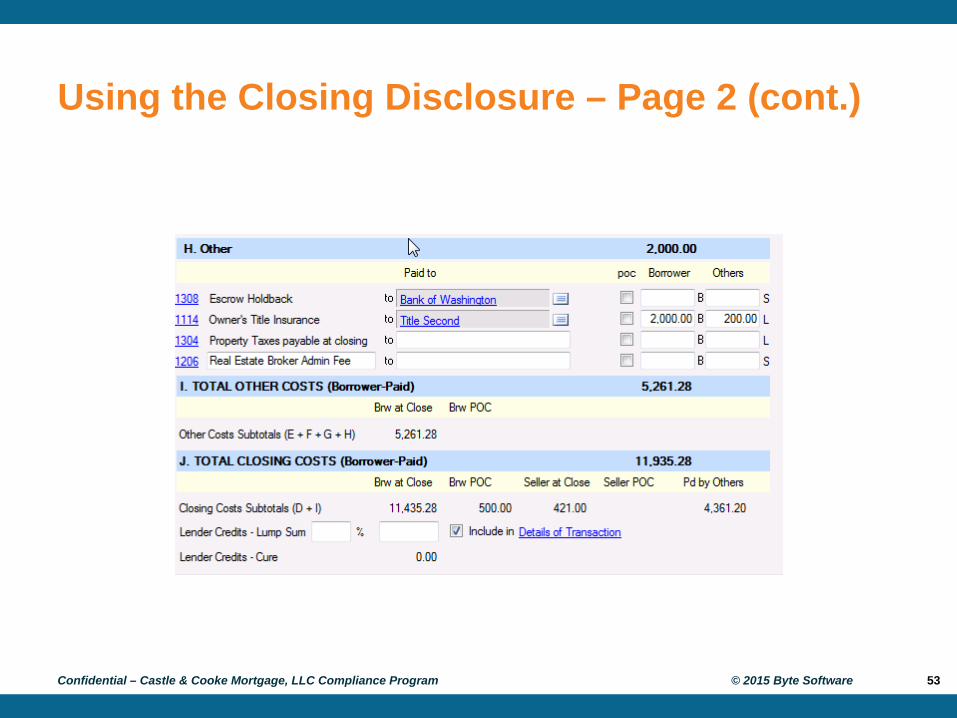

Using the Closing Disclosure – Page 2 (cont.)

Confidential – Castle & Cooke Mortgage, LLC Compliance Program © 2015 Byte Software 50

Using the Closing Disclosure – Page 2 (cont.)

Confidential – Castle & Cooke Mortgage, LLC Compliance Program © 2015 Byte Software 51

Using the Closing Disclosure – Page 2 (cont.)

Confidential – Castle & Cooke Mortgage, LLC Compliance Program © 2015 Byte Software 52

Using the Closing Disclosure – Page 2 (cont.)

Confidential – Castle & Cooke Mortgage, LLC Compliance Program © 2015 Byte Software 53

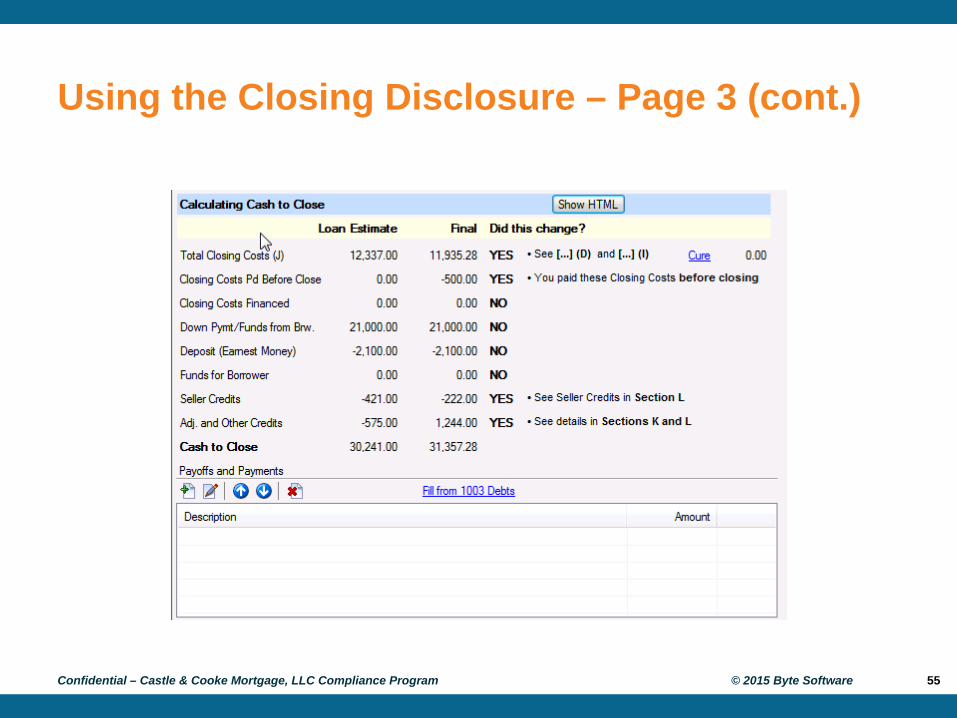

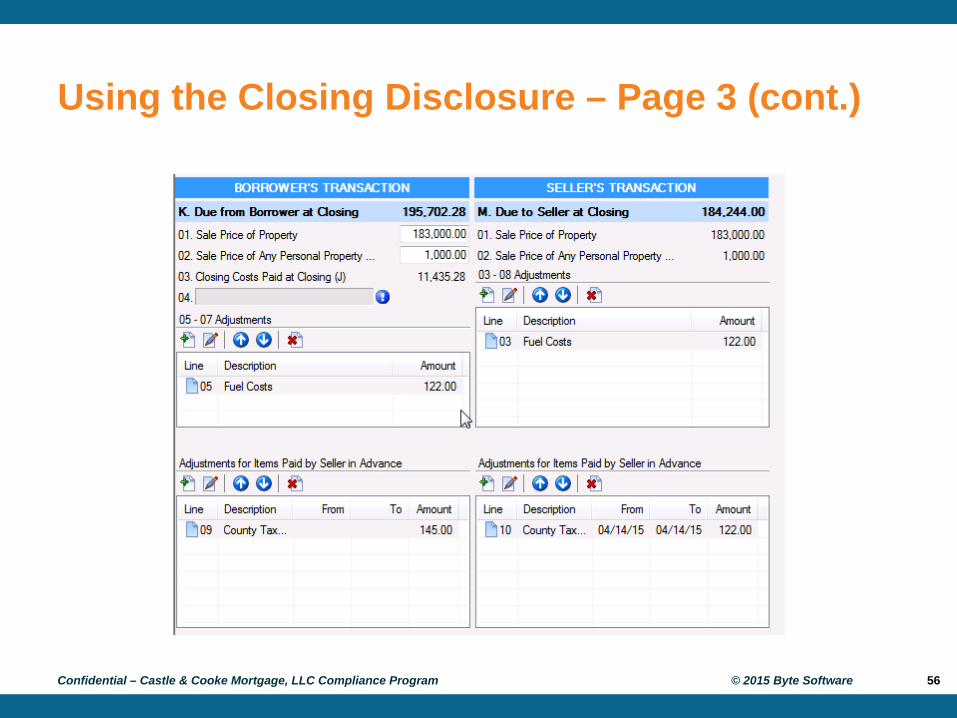

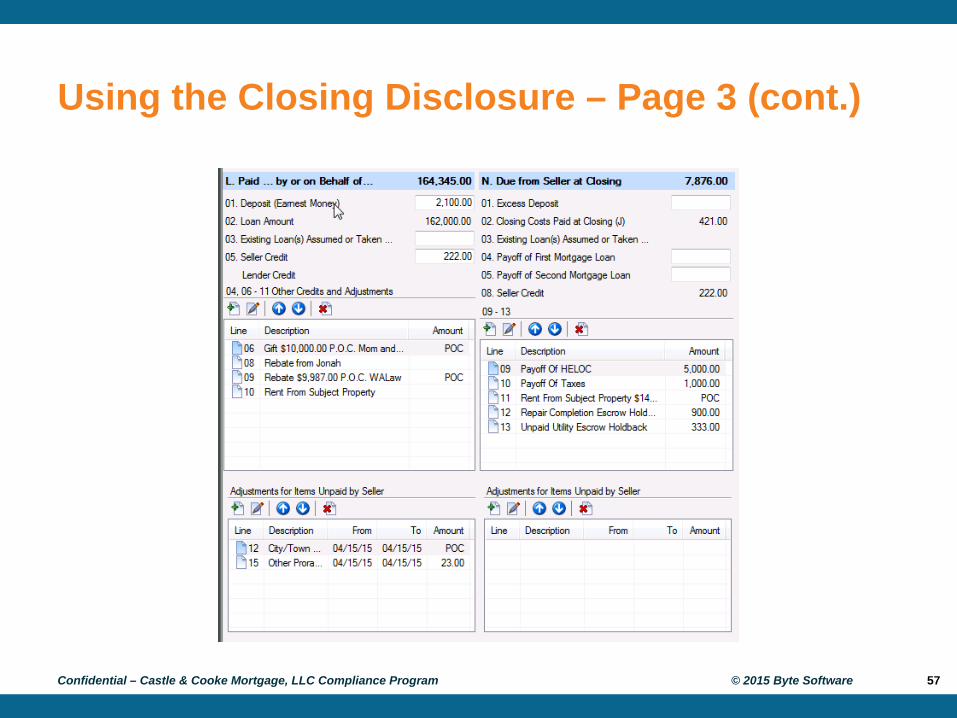

Using the Closing Disclosure – Page 3

Page 3 – Calculating Cash to Close, Summaries of Transactions

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 54

Using the Closing Disclosure – Page 3 (cont.)

Confidential – Castle & Cooke Mortgage, LLC Compliance Program © 2015 Byte Software 55

Using the Closing Disclosure – Page 3 (cont.)

Confidential – Castle & Cooke Mortgage, LLC Compliance Program © 2015 Byte Software 56

Using the Closing Disclosure – Page 3 (cont.)

Confidential – Castle & Cooke Mortgage, LLC Compliance Program © 2015 Byte Software 57

Using the Closing Disclosure – Page 3 (cont.)

Confidential – Castle & Cooke Mortgage, LLC Compliance Program © 2015 Byte Software 58

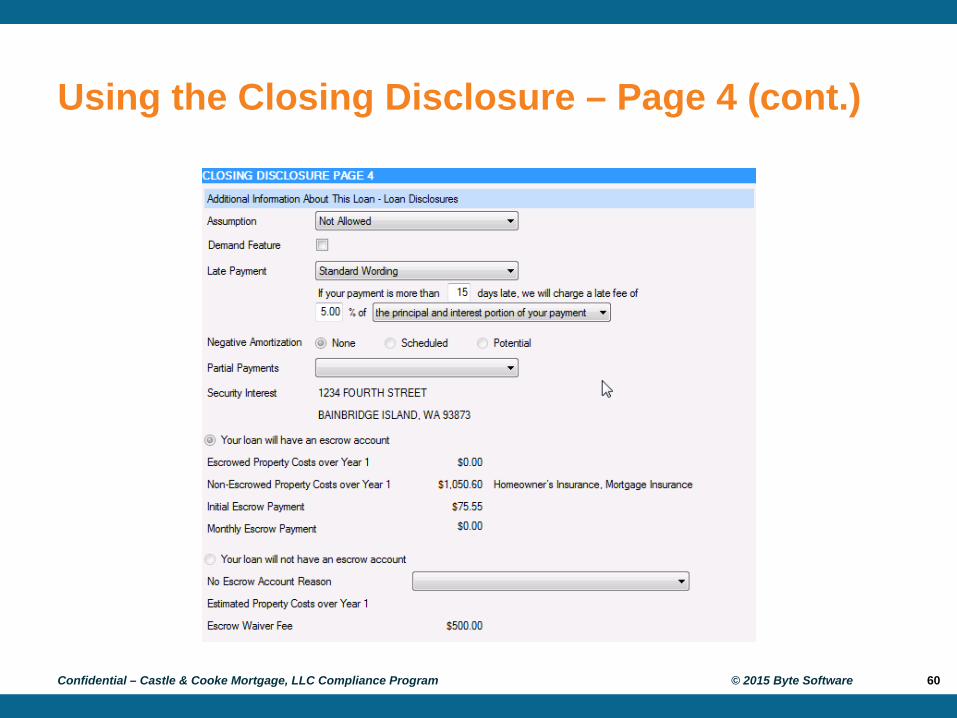

Using the Closing Disclosure – Page 4

Page 4 – Additional information about this loan– Loan Disclosures Table– Adjustable Payment Table– Adjustable Interest Rate Table

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 59

Using the Closing Disclosure – Page 4 (cont.)

Confidential – Castle & Cooke Mortgage, LLC Compliance Program © 2015 Byte Software 60

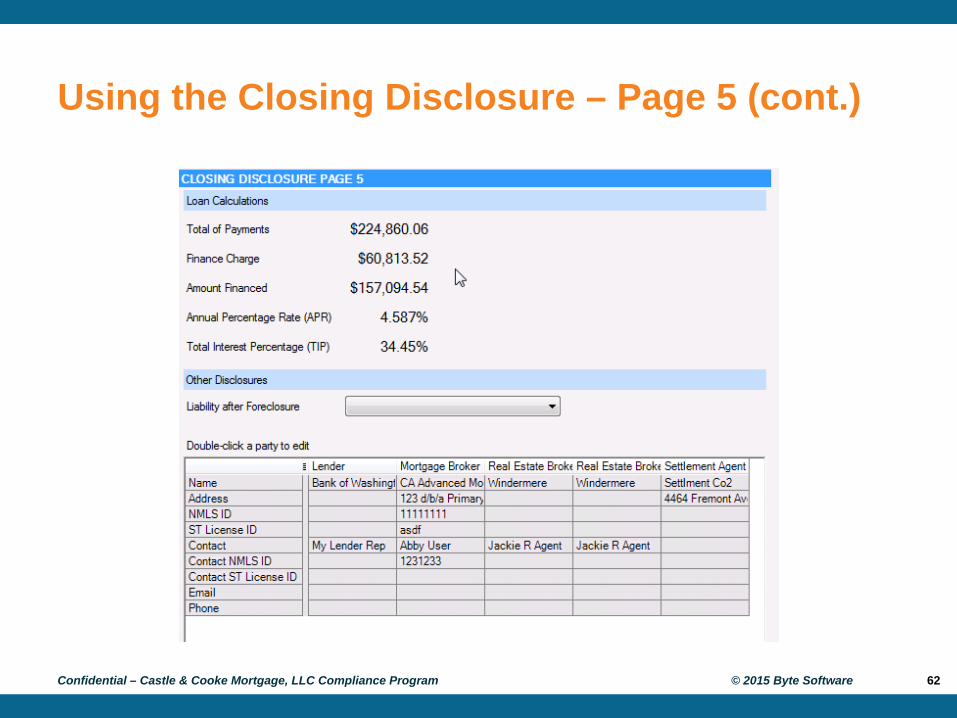

Using the Closing Disclosure – Page 5

Page 5 - “other” tables– Loan calculations– Other disclosures– Questions notice– Contact information– Confirm receipt

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 61

Using the Closing Disclosure – Page 5 (cont.)

Confidential – Castle & Cooke Mortgage, LLC Compliance Program © 2015 Byte Software 62

Closing Disclosure Revisions and Corrections

General rule – Creditors must re-disclose terms or costs on a CD if certain changes occur to the transaction after the CD was first provided making it inaccurate.

Three types of changes:– Changes before consummation requiring a new three-business

day waiting period;– Changes before consummation that do not require a new waiting

period; and – Changes occurring after consummation.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 63

Revisions and Corrections (cont.)

Changes requiring new forms and waiting period:– Disclosed APR becomes inaccurate;– Changes in the loan product; and– Adding a prepayment penalty.

Changes requiring new forms but NO waiting period:– Changes that do not affect the following: APR; Loan product; and Adding a prepayment penalty.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 64

Closing Disclosure Tolerance Violations

General rule – if a consumer paid more than disclosed on his/her LE beyond the applicable tolerance:– Creditor must refund the excess within 60 days; and– Provide a corrected CD reflecting refund within 60 days.

10% cumulative tolerance:– If the total sum of charges exceeds the sum disclosed by more

than 10%, the difference must be refunded to the consumer; and– A corrected CD would be needed.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 65

Changes After Consummation

A corrected CD is needed:– When an event with settlement has made the disclosure

inaccurate and results in a change to the amount paid by the consumer or seller within 30 days of consummation;

– To document refunds for tolerance violations; and– To correct non-numerical clerical errors (errors that don’t effect

numbers or timing or other requirements).

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 66

Record Retention Requirements

Creditor– CD and related documents – five years.– Post-consummation escrow cancellation notice and post-

consummation partial payment notice – two years.– LE and all evidence of compliance with the integrated disclosure

requirements – three years.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 67

RESPA – TILA Civil Liability

RESPA Liability– No private right of action for integrated disclosures under RESPA.– Administrative enforcement only.

TILA Liability– Unlike RESPA, potential civil liability/private right of action (i.e.

borrower lawsuits).– Potential assignee liability for investors.– Rule relies heavily on TILA statutory authority.– Does not state which statutory liability applies to different parts of

the rule (or the forms).– Preamble includes description of the statutory authority used for

each provision, which provides sufficient guidance for industry, consumers, and courts regarding liability.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 68

CFPB Civil & Administrative Liability

CFPB may bring two type of actions:– Administrative enforcement proceedings; or – Civil actions in Federal district court.

No criminal enforcement authority. Can obtain legal or equitable relief in the form of:

– Rescission or reformation of contracts;– Refund of money, return of real property, or restitution;– Disgorgement of compensation for unjust enrichment;– Payment notification regarding the violation;– Limits on the activities or function of the person against whom the action is

brought; and– Civil money penalties:

Tier 1: Up to $5,000 / day. Tier 2: Reckless violations – up to $25,000 / day. Tier 3: Knowing violations – up to $1,000,000 / day.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 69

CFPB Resources

Webinars provided by the CFPB Archives with recordings are available at:

– http://www.consumerfinance.gov/regulatory-implementation/tilarespa/CFPB Rule overview: 06/17/2014 FAQ: 08/26/2014 Loan Estimate contents: 10/02/2014 Closing disclosure contents: 11/18/2014

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 70

CFPB Resources (cont.)

CFPB Regulatory Implementation Website:– http://www.consumerfinance.gov/regulatory-

implementation/tilarespa/ Small Entity Compliance Guide Guide to Forms Sample and Annotated Forms Links to Webinars Disclosure Timeline Illustration Additional Guidance Materials eRegulations Tool: http;//www.consumerfinance.gov/eregulations

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 71

Quiz

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 72

Test Your TRID Knowledge

The Loan Estimate disclosure form replaces which two forms currently in use?A. HUD-1 and GFEB. TIP and Initial TILAC. CD and GFED. Initial TILA and GFE

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 73

Test Your TRID Knowledge

Can you use the new Closing Disclosure form on an application taken July 15, 2015?A. TrueB. False

The lender must provide the borrower a Loan Estimate within three-business days of receiving the borrower’s application…:A. In personB. Electronically (via E-Sign Rules)C. By placing it in the mail D. Any of the above

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 74

Test Your TRID Knowledge

Does the TRID Rule apply to HELOCs?A. TrueB. False

The TRID Rule does not apply to Reverse Mortgages.A. TrueB. False

The Loan Estimate can be hand delivered, mailed or emailed.A. TrueB. False

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 75

Test Your TRID Knowledge

In order to have a waiver of the seven-day requirement:A. Must have a bona-fide personal financial emergency.B. Must have a written statement from the consumer that describes

the bona-fide financial emergency.C. The lender may not provide a pre-printed form defining the

“emergency.”D. All of the above.

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 76

Test Your TRID Knowledge

An application is considered to be made when the consumer submits all of the following:– Name– Income– Social Security Number– Mother’s maiden name– Property Address– Requested mortgage loan amountA. TrueB. False

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 77

Test Your TRID Knowledge

What is the correct definition of “business day” relative to the delivery of Loan Estimates?A. A day on which the creditor’s offices are open to the public for

carrying out substantially all of its business functions.B. All calendar days except Sundays and legal public holidays.

If the consumer withdraws his/her loan application within the three-day period, the lender must still provide a Loan Estimate.A. TrueB. False

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 78

Test Your TRID Knowledge

What is the general rule to determine “good faith?”A. If actual charges exceed charges listed in the Loan Estimate.B. If actual charges are equal to or less than charges listed in the

Loan Estimate.

Creditors may not issue revisions to the Loan Estimate solely because they discover technical errors, miscalculations, or underestimations of charges.A. TrueB. False

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 79

Test Your TRID Knowledge

When there is a changed circumstance after the Loan Estimate has been provided, the creditor can revise the Loan Estimate within three-business days.A. TrueB. False

Which of the following are “changed circumstances?”A. An extraordinary eventB. Information relied on turns out to be inaccurateC. New information the creditor did not rely onD. All of the above

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 80

Test Your TRID Knowledge

If the consumer withdraws his/her application within the three-day period, you do not have to provide the Loan Estimate.A. TrueB. False

As defined in Regulation Z, “consummation” is when a consumer becomes contractually obligated on a credit transaction.A. TrueB. False

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 81

Test Your TRID Knowledge

If amounts paid by the consumer at closing exceed the amounts disclosed on the Loan Estimate beyond the applicable tolerance threshold, the creditor must refund the excess to the consumer no later than 60 calendar days after consummation.A. TrueB. False

Which of the examples listed below are “zero tolerance fees?”A. Fees paid to a creditor, mortgage broker, or an affiliate of eitherB. Fees paid to the County Assessor’s OfficeC. Fees paid to the home owners association

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 82

Test Your TRID Knowledge

When can a creditor charge the consumer more than the amount disclosed in the Loan Estimate?A. When certain variations are expressly permitted by the TILA-

RESPA Rule.B. The amount charged falls within explicit tolerance thresholds

and the estimate is not for a zero tolerance charge where variations are never permitted.

C. Changed circumstances permit a revised Loan Estimate or a Closing Disclosure that permits the charge to be changed.

D. A and CE. A, B, and C

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 83

Test Your TRID Knowledge

The Closing Disclosure integrates and replaces which of the following?A. Form H-25 and the GFEB. Initial TILA and the GFEC. HUD-1 and the final TILAD. None of the above

The creditor is required to ensure the consumer receives the Closing Disclosure not later than three-business days before consummation.A. TrueB. False

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 84

Test Your TRID Knowledge

A corrected Closing Disclosure is needed when an event with settlement has made the disclosure inaccurate and results in a change to the amount paid by the consumer or seller within 30 days of consummation.A. TrueB. False

A corrected Closing Disclosure is needed to document refunds for tolerance violations.A. TrueB. False

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 85

Test Your TRID Knowledge

A creditor must retain a Closing Disclosure and related documents for:A. Three yearsB. Five yearsC. Two yearsD. Seven years from the date of consummation

Confidential – Castle & Cooke Mortgage, LLC Compliance Program 86