Embed Size (px)

Citation preview

2009 - 2010

Supply

demand

pRICe

oCCupanCy

1 RaI = 1,600 Sq m

1 heCtaRe = 6.25 RaI

1 aCRe = 2.53 RaI

1 RaI = 400 Sq wah

IndustrIal EstatE MarkEt rEPOrt

thaIland

www.colliers.co.th

Industrial Estate MarketexeCutIve SummaRythe year 2010 heralded the biggest increase in supply of serviced Industrial land Plots (sIlPs) for thirteen years reflecting the underlying long term confidence in the manufacturing sector despite ongoing political unrest over the past four years.

the Eastern seaboard is the dominant player in the industrial estate market with around 63% of total supply of land in sIlPs.

the Map ta Phut situation has been largely resolved but question marks remain as to thailand’s future for heavy industry.

year end 2010 | industrial

maRket IndICatoRS

ConveRSIon table

thailand industrial estate Market rePOrt | 2H 2010

COLLIERS INTERNATIONAL | P. 2

InduStRIal ZonIng Colliers International thailand has divided the industrial estate market into five main zones in thailand. these are as follows.

Eastern seaboard area – this represents the industrial powerhouse due to its location surrounding the main container port in thailand, laem Chabang and its proximity to the Bangkok metropolis. Further growth has come about due to suppliers clustering around large manufacturers.

north Eastern area – the remoteness of this area and poor transportation means that the area is a bit player in the industrial scene. the border with Cambodia and laos (leading to Vietnam) could provide limited potential for the future.

northern area – limited industrial activity takes place here due to its remote location and is predominantly an agricultural area with a difficult

topography for industrial development. the proximity to China could show greater promise with the ever increasing trade between the two countries.

Central area – another key industrial area due to its proximity to Bangkok.

southern seaboard area – an under developed industrial area catering mainly to the Malaysian market with halal produce as well as heavy industrial projects based on oil.this report is concerned predominantly with sIlPs but it must be stated that a considerable number of stand alone factories exist outside of the industrial estates.

the total supply of sIlPs increased from 118,500 to about 119,600 rais in H2 2010. this increase occurred in the Central area, and the dominant Eastern seaboard area. the year 1996 heralded the highest increase of sIlPs, but the asian Financial Crisis put an end to this surge and growth

in supply was limited until 2009 with a robust increase despite the global economic downturn. Growth for the first half of 2010 even outstripped the whole of 2009.

source: Colliers International thailand research

hIStoRICal Supply SIlpS

Supply

COLLIERS INTERNATIONAL | P. 3

thailand industrial estate Market rePOrt | 2H 2010

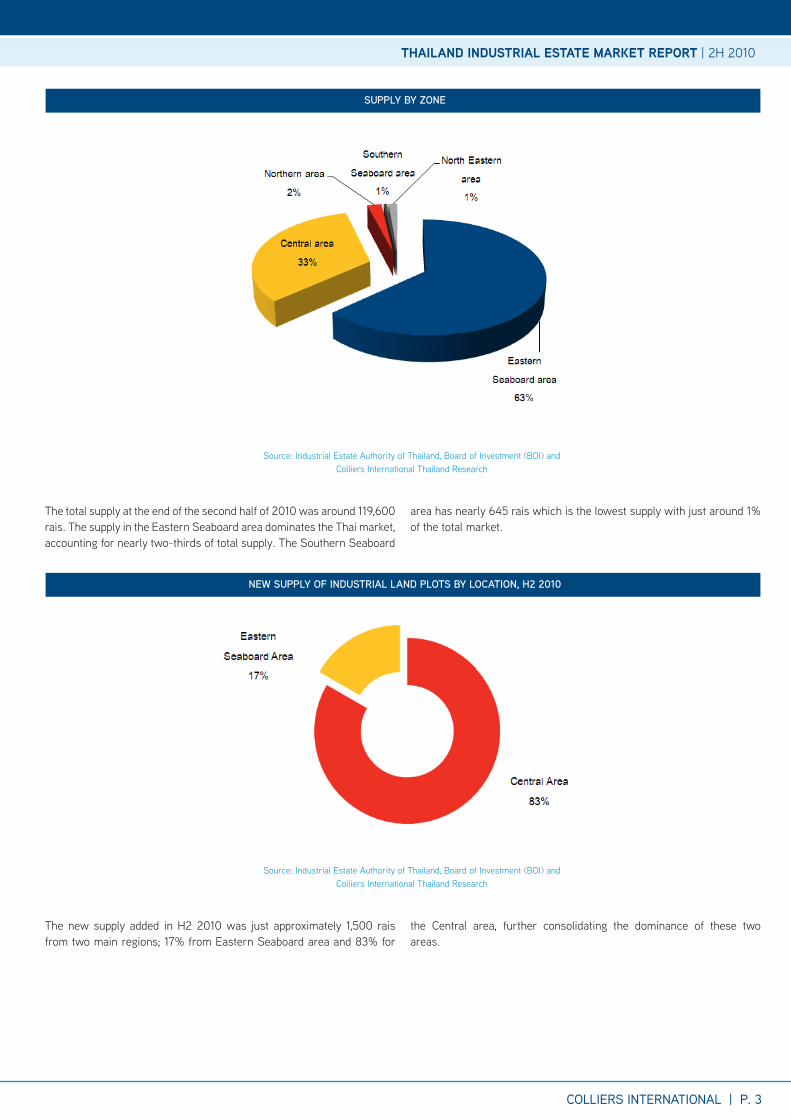

Supply by Zone

new Supply of InduStRIal land plotS by loCatIon, h2 2010

source: Industrial Estate authority of thailand, Board of Investment (BOI) and Colliers International thailand research

source: Industrial Estate authority of thailand, Board of Investment (BOI) and Colliers International thailand research

the total supply at the end of the second half of 2010 was around 119,600 rais. the supply in the Eastern seaboard area dominates the thai market, accounting for nearly two-thirds of total supply. the southern seaboard

area has nearly 645 rais which is the lowest supply with just around 1% of the total market.

the new supply added in H2 2010 was just approximately 1,500 rais from two main regions; 17% from Eastern seaboard area and 83% for

the Central area, further consolidating the dominance of these two areas.

COLLIERS INTERNATIONAL | P. 4

thailand industrial estate Market rePOrt | 2H 2010

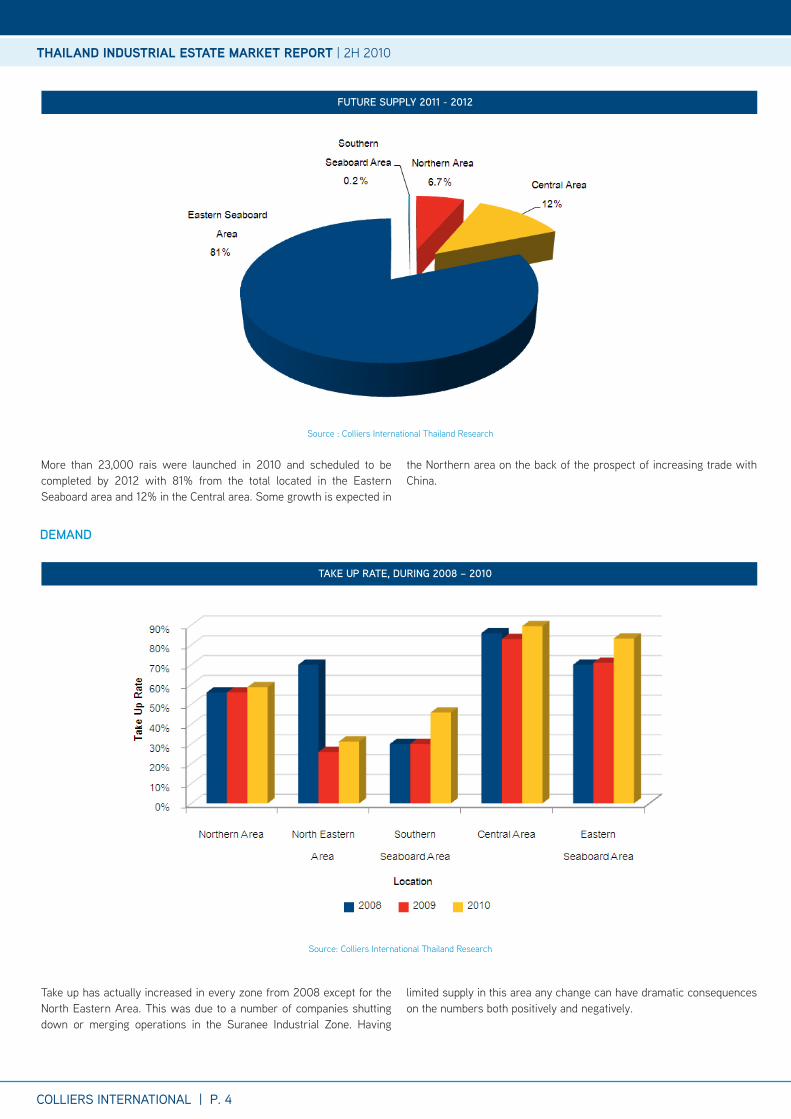

More than 23,000 rais were launched in 2010 and scheduled to be completed by 2012 with 81% from the total located in the Eastern seaboard area and 12% in the Central area. some growth is expected in

the northern area on the back of the prospect of increasing trade with China.

source : Colliers International thailand research

futuRe Supply 2011 - 2012

take up has actually increased in every zone from 2008 except for the north Eastern area. this was due to a number of companies shutting down or merging operations in the suranee Industrial Zone. Having

limited supply in this area any change can have dramatic consequences on the numbers both positively and negatively.

source: Colliers International thailand research

take up Rate, duRIng 2008 – 2010

demand

foReIgn dIReCt InveStment peR half yeaR

manufaCtuRIng expoRtS mInuS gold

COLLIERS INTERNATIONAL | P. 5

source : Board of Investment (BOI) and Colliers International thailand research

Colliers International thailand researchsource: Bank of thailand and Customs department

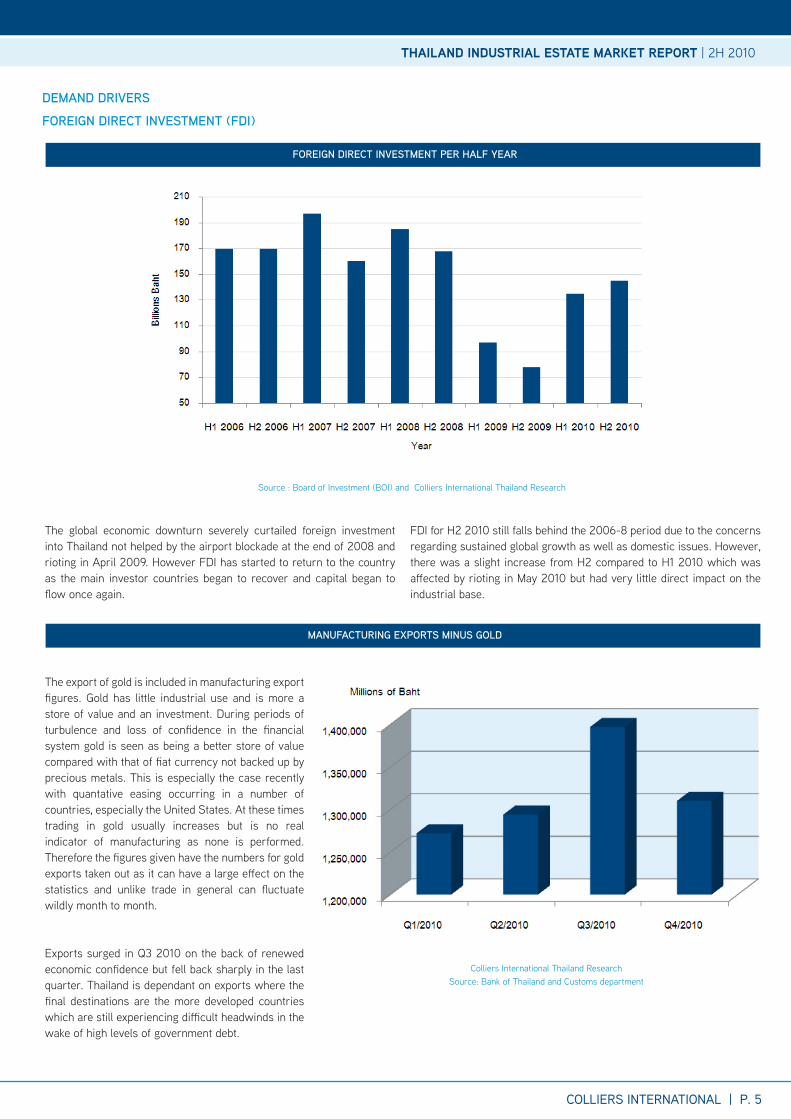

the global economic downturn severely curtailed foreign investment into thailand not helped by the airport blockade at the end of 2008 and rioting in april 2009. However FdI has started to return to the country as the main investor countries began to recover and capital began to flow once again.

FdI for H2 2010 still falls behind the 2006-8 period due to the concerns regarding sustained global growth as well as domestic issues. However, there was a slight increase from H2 compared to H1 2010 which was affected by rioting in May 2010 but had very little direct impact on the industrial base.

the export of gold is included in manufacturing export figures. Gold has little industrial use and is more a store of value and an investment. during periods of turbulence and loss of confidence in the financial system gold is seen as being a better store of value compared with that of fiat currency not backed up by precious metals. this is especially the case recently with quantative easing occurring in a number of countries, especially the united states. at these times trading in gold usually increases but is no real indicator of manufacturing as none is performed. therefore the figures given have the numbers for gold exports taken out as it can have a large effect on the statistics and unlike trade in general can fluctuate wildly month to month.

Exports surged in Q3 2010 on the back of renewed economic confidence but fell back sharply in the last quarter. thailand is dependant on exports where the final destinations are the more developed countries which are still experiencing difficult headwinds in the wake of high levels of government debt.

thailand industrial estate Market rePOrt | 2H 2010

demand dRIveRS

foReIgn dIReCt InveStment (fdI)

COLLIERS INTERNATIONAL | P. 6

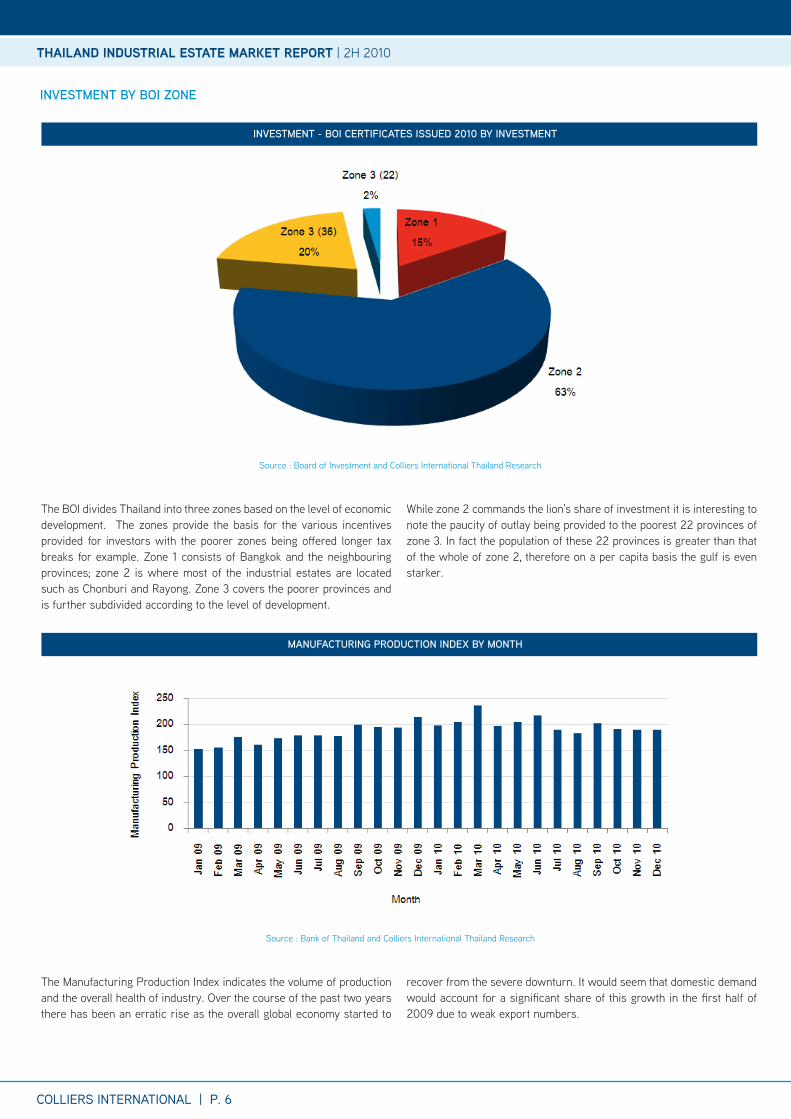

the BOI divides thailand into three zones based on the level of economic development. the zones provide the basis for the various incentives provided for investors with the poorer zones being offered longer tax breaks for example. Zone 1 consists of Bangkok and the neighbouring provinces; zone 2 is where most of the industrial estates are located such as Chonburi and rayong. Zone 3 covers the poorer provinces and is further subdivided according to the level of development.

While zone 2 commands the lion’s share of investment it is interesting to note the paucity of outlay being provided to the poorest 22 provinces of zone 3. In fact the population of these 22 provinces is greater than that of the whole of zone 2, therefore on a per capita basis the gulf is even starker.

the Manufacturing Production Index indicates the volume of production and the overall health of industry. Over the course of the past two years there has been an erratic rise as the overall global economy started to

recover from the severe downturn. It would seem that domestic demand would account for a significant share of this growth in the first half of 2009 due to weak export numbers.

source : Board of Investment and Colliers International thailand research

source : Bank of thailand and Colliers International thailand research

InveStment - boI CeRtIfICateS ISSued 2010 by InveStment

manufaCtuRIng pRoduCtIon Index by month

InveStment by boI Zone

thailand industrial estate Market rePOrt | 2H 2010

COLLIERS INTERNATIONAL | P. 7

source : department of Industrial Works and Colliers International thailand research

source : department of Industrial Works and Colliers International thailand research

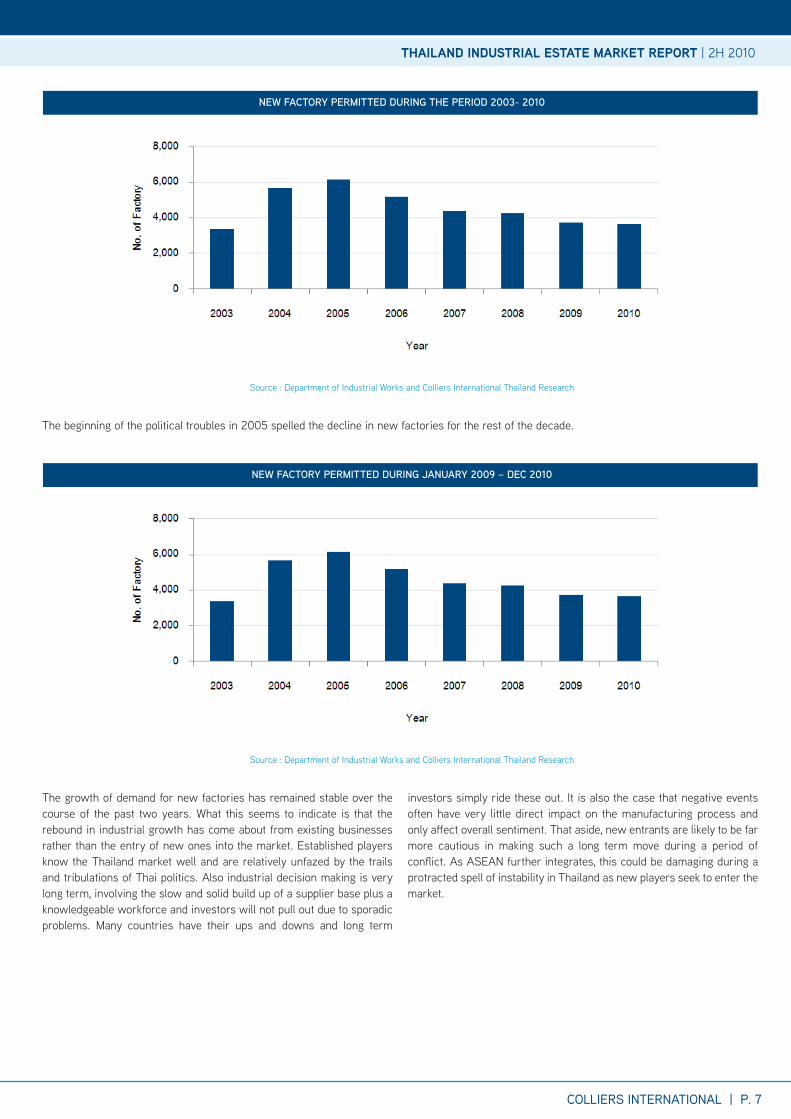

new faCtoRy peRmItted duRIng the peRIod 2003- 2010

new faCtoRy peRmItted duRIng JanuaRy 2009 – deC 2010

the beginning of the political troubles in 2005 spelled the decline in new factories for the rest of the decade.

the growth of demand for new factories has remained stable over the course of the past two years. What this seems to indicate is that the rebound in industrial growth has come about from existing businesses rather than the entry of new ones into the market. Established players know the thailand market well and are relatively unfazed by the trails and tribulations of thai politics. also industrial decision making is very long term, involving the slow and solid build up of a supplier base plus a knowledgeable workforce and investors will not pull out due to sporadic problems. Many countries have their ups and downs and long term

investors simply ride these out. It is also the case that negative events often have very little direct impact on the manufacturing process and only affect overall sentiment. that aside, new entrants are likely to be far more cautious in making such a long term move during a period of conflict. as asEan further integrates, this could be damaging during a protracted spell of instability in thailand as new players seek to enter the market.

thailand industrial estate Market rePOrt | 2H 2010

COLLIERS INTERNATIONAL | P. 8

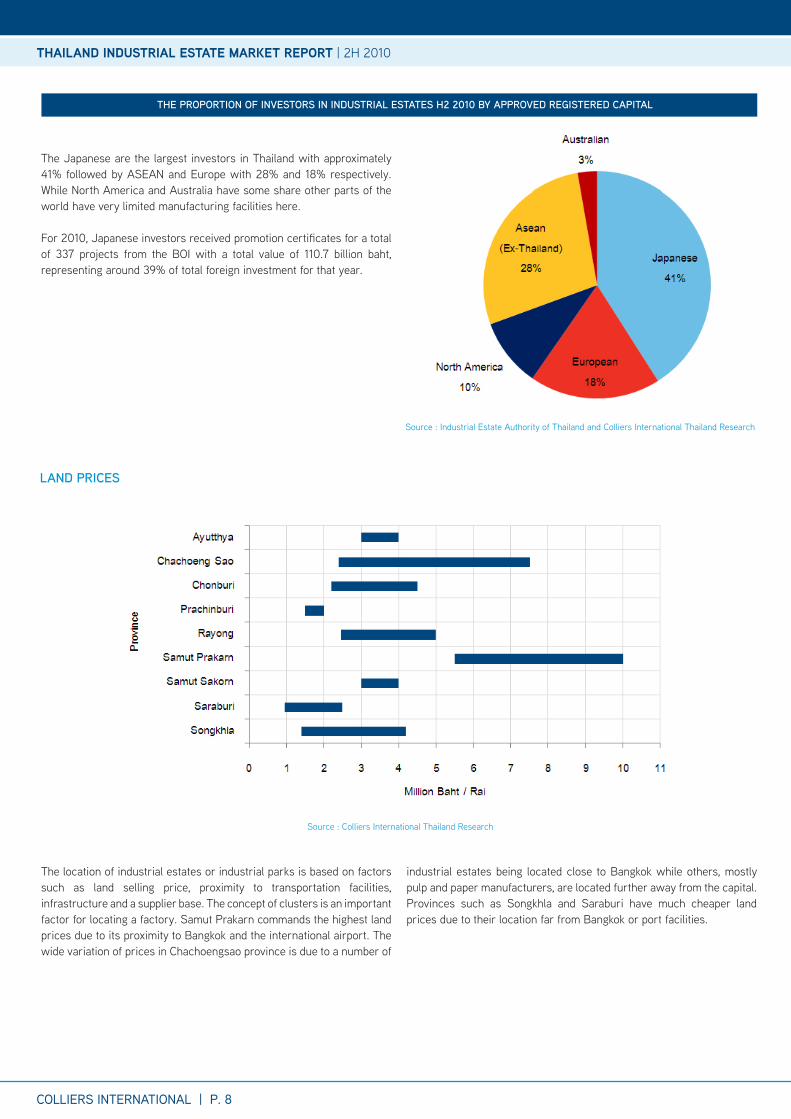

the Japanese are the largest investors in thailand with approximately 41% followed by asEan and Europe with 28% and 18% respectively. While north america and australia have some share other parts of the world have very limited manufacturing facilities here.

For 2010, Japanese investors received promotion certificates for a total of 337 projects from the BOI with a total value of 110.7 billion baht, representing around 39% of total foreign investment for that year.

source : Industrial Estate authority of thailand and Colliers International thailand research

the pRopoRtIon of InveStoRS In InduStRIal eStateS h2 2010 by appRoved RegISteRed CapItal

thailand industrial estate Market rePOrt | 2H 2010

the location of industrial estates or industrial parks is based on factors such as land selling price, proximity to transportation facilities, infrastructure and a supplier base. the concept of clusters is an important factor for locating a factory. samut Prakarn commands the highest land prices due to its proximity to Bangkok and the international airport. the wide variation of prices in Chachoengsao province is due to a number of

industrial estates being located close to Bangkok while others, mostly pulp and paper manufacturers, are located further away from the capital. Provinces such as songkhla and saraburi have much cheaper land prices due to their location far from Bangkok or port facilities.

source : Colliers International thailand research

land pRICeS

COLLIERS INTERNATIONAL | P. 9

thailand industrial estate Market rePOrt | 2H 2010

the developer of rBFs buys land usually in the area of an industrial estate or industrial park and builds factory buildings for lease or sale. areas range from 1,000 – 6,000 sq m and are built to international standards. tICOn is the biggest developer in this business; they have many factories and warehouses in thailand. Other developers include tFd and industrial estate developers such as amata, Pinthong and Hemaraj, although this group develops factories only in their own industrial estates.

all of the ready built factories are located in large industrial estates and industrial parks in the Central area and Eastern seaboard area, such as Hi – tech, rojana, Bangpa – In, Bangpoo, amata nakorn, amata City, laem Chabang, Pinthong.

a large number of tenants in the ready built factories are for Japanese with nearly 63% followed by Europe and Canada with 12.2% and 7.8% respectively. Most of the industrial factories are for the electronic / electrical industries with just over half and about 20% are for the auto parts industry.

waRehouSeS

Warehouses are in locations that support distribution such as Bangna – trad road, laem Chabang, ayutthaya province and saraburi province.

Europeans rent the most warehouse space with 30% of the total followed by Japanese and australians with 24% and 17% respectively. 48% of

tenants rent warehouse space for logistics as opposed to pure storage. the European strength in this field can be partly explained by the number of European dominated retailers such as tesco and Big C.

although the occupancy rate in rBFs and warehouses decreased approximately 9% from 2009 in both types, thailand is still a strong location for manufacturing, so tICOn continues to develop ready built factories and logistics warehouses for rent and sale in the long term.

heavy InduStRy

While the Map ta Phut situation has largely been resolved with the vast majority of projects given the green light there are still long term concerns regarding the future of heavy industry projects such as steel, refining and petrochemicals. the Map ta Phut zone is fast filling up and there is limited space for further development. there are currently no firm plans for opening up any other zone to heavy industry despite the southern seaboard being mooted. Currently interest in further development is outside of the country with interest in both Myanmar and Cambodia as alternative locations. the new dawei deep water seaport and industrial zone in Myanmar has attracted considerable interest from thai companies including a contract given to Italian-thai development to develop the area.

launCheS wIth hIgh take up RateS In q4 2010

CollIeRS InteRnatIonal thaIland management team

OFFICE & IndustrIal sErVICEsnarumon rodsiravoraphat | senior Manager PrOJECt salEs & MarkEtInGMonchai Orawongpaisan | senior Manager rEsIdEntIal salEs & lEasInGsupatra Buranatham | Consultant rEtaIl sErVICEsasharawan Wachananont | senior Manager adVIsOrY sErVICEsnapatr tienchutima | associate director

rEal EstatE ManaGEMEnt sErVICEsBandid Chayintu | associate director

adVIsOrY sErVICEs | HOsPItalItY Jean Marc Garret | director

InVEstMEnt sErVICEsnukarn suwatikul | associate director Wasan rattanakijjanukul | senior Manager

rEsEarCHantony Picon | associate directorsurachet kongcheep | senior Manager

ValuatIOn & adVIsOrY sErVICEsnicholas Brown | associate directorPhachsanun Phormthananunta | associate director santipong kreemaha | senior Manager Wanida suksuwan | Manager PattaYa OFFICEMark Bowling | senior sales Managersupannee starojitski | senior Business development Manager / Office Manager

COlliers internatiOnal thailand:

Bangkok Office 17/F Ploenchit Center, 2 sukhumvit road, klongtoey,Bangkok 10110 thailandtel +662 656 7000fax +662 656 7111 emaIl [email protected] Pattaya Office 519/4-5, Pattaya second road (Opposite Central Festival Pattaya Beach), nongprue, Banglamung, Chonburi 20150tel +6638 427 771fax +6638 427 772 emaIl [email protected]

ReSeaRCheR:

thailandantony Piconassociate director | researchemaIl [email protected]

ReSeaRCheR:

thailandsurachet kongcheepsenior Manager | researchemaIl [email protected]

480 offices in 61 countries on 6 continents

• the third largest commercial real estate services company in the world

• the second most recognised commercial real estate brand globally

• us$2 billion in annual revenue• Over 2 billion square feet under management

• Over 15,000 professionals

this report and other research materials may be found on our website at www.colliers.co.th. Questions related to information herein should be directed to the research department at the number indicated above. this document has been prepared by Colliers International for advertising and general information only. Colliers International makes no guarantees, representations or warranties of any kind, expressed or implied, regarding the information including, but not limited to, warranties of content, accuracy and reliability. any interested party should undertake their own inquiries as to the accuracy of the information. Colliers International excludes unequivocally all inferred or implied terms, conditions and warranties arising out of this document and excludes all liability for loss and damages arising there from. Colliers International is a worldwide affiliation of independently owned and operated companies.

www.colliers.co.th

accelerating success.

thailand industrial estate Market rePOrt | 2H 2010

united states: 135Canada: 39latin america: 17asia Pacific: 194EMEa: 95