Embed Size (px)

Citation preview

38 Volume 1, Number 1, July - December 2007

..........................................................................................GH Bank Housing Journal

T hailand Real Estate Market Cycles:Case Study of 1997 Economic Crisis

by Asst Prof Sonthya Vanichvatana, Ph D

Vice President of the Thai Real Estate AssociationChairperson of the Department of Real Estate, Assumption University of Thailand

xecutive Summary

This paper describes the fundamentalelements of real estate cycles, including types,characteristics and important influencing fac-tors. It also discusses the crucial 1997 economiccrisis which is an important Thailand realestate cycle illustration. The paper aims to iden-tify important factors and their characteristicsso that we can visualize a real estate cycle’sfundamentals and share our findings with thereal estate community and other related aca-demic researchers.

ntroduction

The real estate industry is viewed withinterest from many perspectives: from thedemand side, supply side, financial institutions,policy makers, and related professionals. Thisindustry is a critical element of any economy.

I

ESize and Stakeholders

The real estate industry in Thailandconstituted about 6.5% of gross domestic pro-duct (GDP) in 2006. Although a home is oneof life’s four essentials, the real estate industryinvolves many stakeholders: design-relatedprofessionals, construction companies, buildingmaterials producers and suppliers, advertisingand sales, etc. Any real estate boom-and-bustcycle tremendously impacts a country. There-fore, it is important that all stakehol-ders gaina comprehensive understanding of these recur-ring cycles.

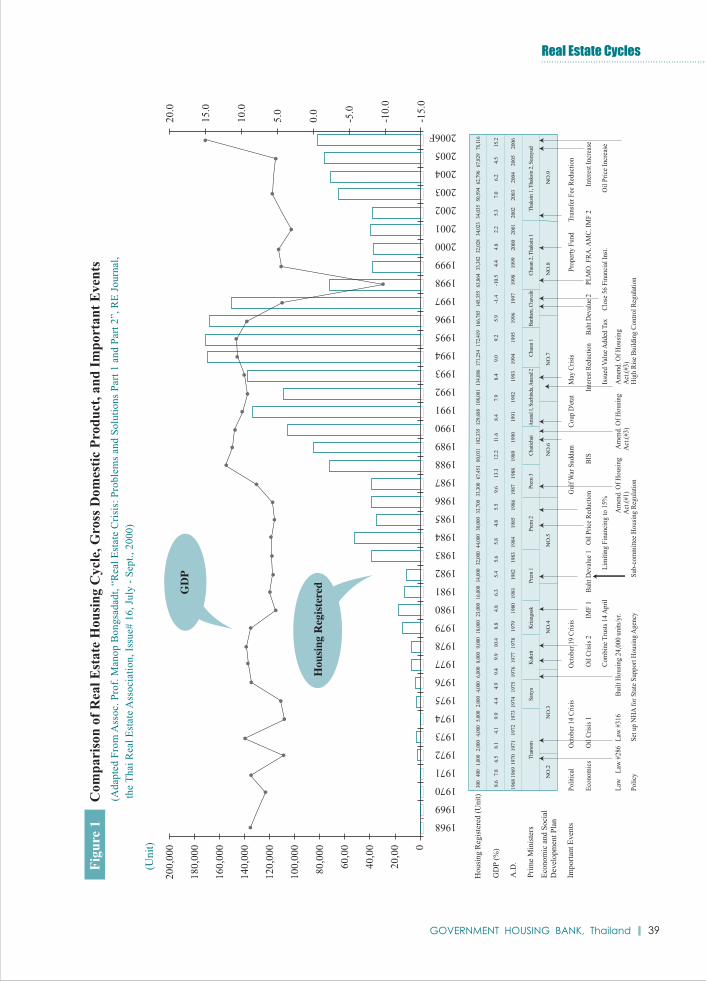

Modified from Bongsadadt (Bongsadadt,2000), Figure 1 compares new housing regis-tered and GDP (period includes many Thaigovernment changes and other major political,economic and real estate related events).During the past 40 years the two factorsfluctuated cyclically and asymmetrically. Allreal estate industry observers would like toknow where the real market is heading so thatthey can develop more accurate business plans.

................................................................Real Estate Cycles

39GOVERNMENT HOUSING BANK, Thailand

40 Volume 1, Number 1, July - December 2007

..........................................................................................GH Bank Housing Journal

undamental Elements of Real EstateCycles

According to macro-economic theory,real estate cycles are similar to economic orother business cycles. The interaction betweendemand and supply causes vacancy rates, rentsand housing inventories to rise and fall over andover again, like a bouncing a tennis ball thathas dropped to the floor.

lements of a Real Estate Cycle

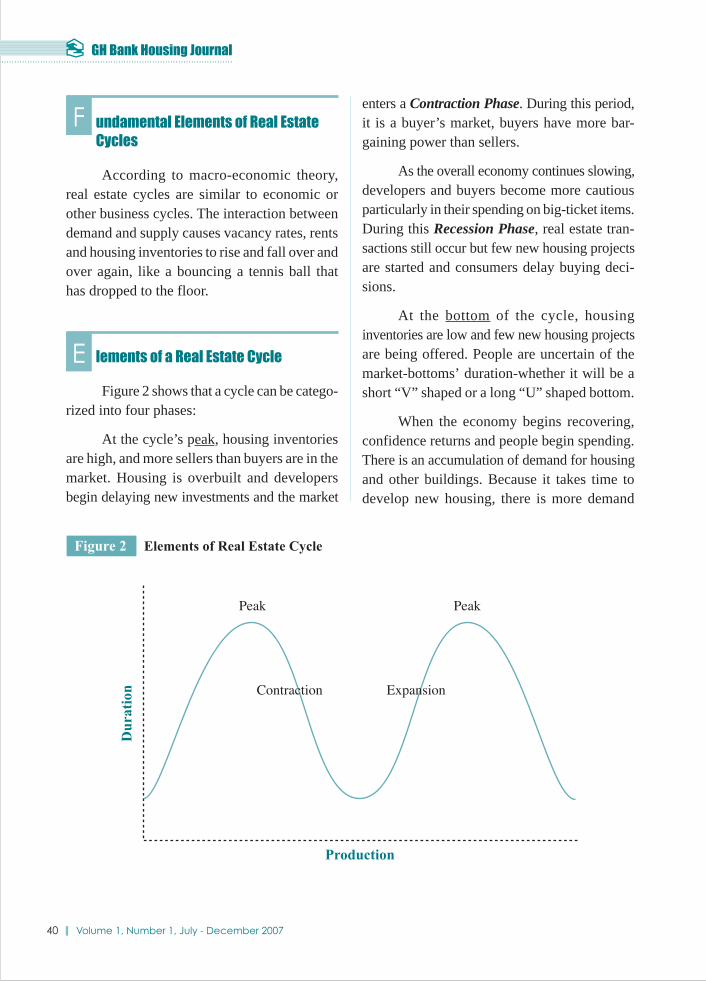

Figure 2 shows that a cycle can be catego-rized into four phases:

At the cycle’s peak, housing inventoriesare high, and more sellers than buyers are in themarket. Housing is overbuilt and developersbegin delaying new investments and the market

enters a Contraction Phase. During this period,it is a buyer’s market, buyers have more bar-gaining power than sellers.

As the overall economy continues slowing,developers and buyers become more cautiousparticularly in their spending on big-ticket items.During this Recession Phase, real estate tran-sactions still occur but few new housing projectsare started and consumers delay buying deci-sions.

At the bottom of the cycle, housinginventories are low and few new housing projectsare being offered. People are uncertain of themarket-bottoms’ duration-whether it will be ashort “V” shaped or a long “U” shaped bottom.

When the economy begins recovering,confidence returns and people begin spending.There is an accumulation of demand for housingand other buildings. Because it takes time todevelop new housing, there is more demand

F

E

................................................................Real Estate Cycles

41GOVERNMENT HOUSING BANK, Thailand

than supply during this phase. This phase iscalled the Recovery Phase. During this period,it is a seller’s market where sellers have morebargaining buyer.

As the economy’s momentum trendsupward, housing markets follow and enter anExpansion Phase. New and existing developersgain confidence and produce new projects forthe market. This phase will end when thedemand is absorbed and excess supply beginsoccurring until the market peaks again. Themarket moves cyclically up and down but withdifferent durations and amplitudes.

ypes of Real Estate Cycles

After World War II, many US and UKresearchers identified property cycles andclassified them into three types based onduration and time as follows (Lee, 1999):

1. Short Cycle: three to five years.This type of cycle is based on housing andbuilding demand. The cycle fluctuates similarto other business cycles.

2. Major Cycle: nine to 10 years. Thistype of cycle is based on a supply-side produc-tion lag. It occurs because real estate productsrequire lengthy periods to develop when theyrespond to boom business-cycle demands.This cycle type affects many property typesincluding office buildings and industrial deve-lopment.

3. Long Swing: 20 to 30 years. Thistype of cycle reflects waves of urbanization.Populations expand away from the nation’scapital during periods of economic growth.

ycles of Different Property Sectors

The real estate industry encompassesmany product sectors including residential,low-rise and high-rise developments includingcondominiums, offices, retail outlets, andindustrial developments. Each sector mayexperience market fluctuations at differenttimes. For example, during the economic crisis(1997-2000), mega-stores expanded rapidlywhile other property sectors were at the bot-tom. Residential properties, including detachedhomes, town houses, or condominiums allhave different market cycles.

actors Influencing Real Estate Cycles

Similar to other businesses, the realestate industry is influenced by macro-economicfactors and specific business micro-economicfactors. Many researchers have identifieddifferent important factors and their levels ofinfluence and relationship to business cycles.

Macro economic factors can be categorizedas follows:

1. Gross domestic product and employ-ment rates

2. Financial factors including interestrates and foreign currency exchange rate

3. Capital factors for example the stockexchange index, and

4. Geographic factors such as nationalincome and population - grouping by age.

T

C

F

42 Volume 1, Number 1, July - December 2007

..........................................................................................GH Bank Housing Journal

Micro-economic factors include real estatespecific variables. A widely-used variable is“Housing Starts” , which is the number ofapprovals for housing development applica-tions at related government agencies. This is aleading indicator that identifies housing num-bers before construction permits are issued andbefore title-deeds are transferred .The latternumbers come at a much later date.

Three Stages of Indicators

These indicators can also be classifiedinto three different stages (Dachavas & Lert-bunnapong, 1999):

1. Leading Indicators are factors thatoccur before the other phases and can be usedto determine market supply - i.e. housing starts.

2. Coincident Indicators are factorsthat occur at similar times during the phase.

3. Lagging Indicators are factors thatoccur after other factors have occurred.

During the past several decades, re-searchers from many parts of the world havebuilt related statistical and mathematicalmodels. These studies used data and specificcases to explain country and city-scope realestate cycles. Many of these studies have showninteresting relationships between these impor-tant factors. However, these results cannot beapplied to or used to explain phenomenonoccurring at different locations.

997 Thailand Economic Crisis

Any real estate cycle impacts an economyin many ways. Thailand’s real estate industry

by-and-large has learned its lesson fromprevious cycles. The country’s most recent 1997economic crisis drastically impacted everyonein the country including the real estate industry.

The following findings are from researchby Vanichvatana (Vanichvatana, 2004). Thisstudy explored the 1997 economic crisis thatwas partly triggered by an oversupply of realestate. The real cause can be linked back to theThai government’s 1992 financial liberalizationmeasures. The study outlined the factors frommany perspectives: the international environ-ment, national environment in terms of finan-cial and other governmental policies, realestate development companies, and consumerbehavior. The paper then describes variousGovernment remedies and supporting policiesand regulations. It also describes the Govern-ment’s remedies for ensuring more accuratereal estate industry demand and supply sideinformation and measures implemented toprevent the reoccurrence of massively exces-sive housing inventories.

992 - 2000 Real Estate CycleCharacteristics

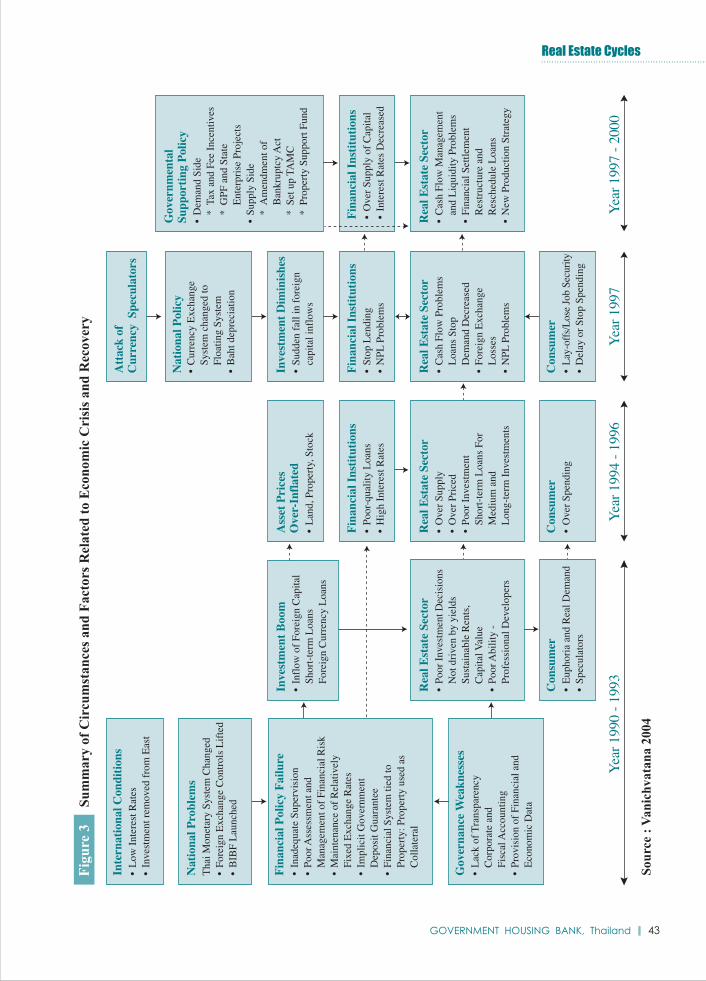

The following section describes theenvironment just prior to and after the 1997economic crisis wide, from 1992 - 2000. Thisparticular cycle can be divided into four phases:(1) 1990 - 1993 the beginning of financialliberalization, (2) 1994 - 1996 the boom years,(3) 1997 the crisis year, and (4) after the crisis,1997 - 2000 the recovery years, as shown inFigure 3.

1

1

................................................................Real Estate Cycles

43GOVERNMENT HOUSING BANK, Thailand

44 Volume 1, Number 1, July - December 2007

..........................................................................................GH Bank Housing Journal

1990 - 1993 : The Beginning of FinancialLiberalization

Two important milestones can be usedto describe financial liberalization in Thailand(Siamwalla 2000). During this period monetarypolicies were rapidly changing with liberaliza-tion, deregulation and financial innovations.

1. In 1990, the acceptance of the obli-gations under Article VIII of the InternationalMonetary Fund which required the lifting of allcontrols on foreign-exchange transactions incurrent accounts. An immediate result was alarge influx of offshore loans. Everyone wantedto benefit from the low-offshore interest rates.

2. In 1993, the gradual opening of capi-tal accounts with the launching of the BangkokInternational Banking Facility (BIBF)1. Throughthis policy, all financial institutions, both localand offshore, could freely transfer and exchangeforeign currencies. Institutions receiving BIBFapproval could accept deposits and lend inforeign currencies. Deposits and loans couldbe done offshore or in Thailand. Borrowedfunds could be invested onshore or offshore.However, the new policies increased the amountof foreign debt. (Chunhawan & Mahutanobol,2006).

Not Ready for the Liberalization!

Thailand was not ready for financialliberalization and this led to the financial crisisof 1997. The causes included: inadequatesupervision, poor assessment and management,maintenance of a relatively fixed-exchange rate,

implicit government deposit guarantees, andpolicies that primarily used property as colla-teral for loans.

Not Ready as Real Estate Professionals!

In addition to real estate loans, the newpolicies resulted in a high inflow of foreigncapital for businesses. However, most of themedium and short term loans were used to fundlong-term real estate projects. With relativelyeasy project-funding, numerous poor investmentdecisions were made. Many of these investmentswere not driven by yields, sustainable rents, orcapital value. Moreover, during this period,almost anyone with little or no experience orability could enter the real estate industry.

1994 - 1997 : The Boom Years

During this phase, all asset prices, inclu-ding land, property and securities were appre-ciating. Everyone wanted to get into the realestate business because everyone seemed tobe making money. However, before long mostreal estate sectors peaked and quickly becameoversupplied. Many purchasers had overpaidand had bought long-term real estate invest-ments with medium and long term loans. Thefollowing segments were most severely hit:office buildings, low-rise housing, condominiumsand industrial estates.

Consumers and speculators were alsocaught up in the euphoria. By 1995, the officemarket and lower quality condominium marketsover-supply became noticeable.

1 Bangkok International Banking Facilities (BIBF) was established in 1993 to grant significant tax advantages fromobtaining deposits or loans in foreign exchange from abroad. Banks (Thai commercial and foreign banks) that hadbeen granted BIBF license by 1996 could significantly increase the magnitude of short-term capital inflows byreducing borrowing costs and easy access to foreign capital markets.

................................................................Real Estate Cycles

45GOVERNMENT HOUSING BANK, Thailand

1997 : The Crisis Year

The Thai baht was attacked by currencyspeculators in 1997. The government mistak-enly tried to fight off the attack by lifting thefixed currency exchange system and allowingthe baht to float. The baht suddenly depreciated.Foreign capital inflows diminished and finan-cial institutions stopped lending to many busi-nesses including real estate developers. Mostreal estate companies began to experiencecash flow problems as bank lending stoppedand housing demand dropped precipitously.Moreover, the companies with foreign loansall suffered massive foreign exchange losses.Consumer demand also dropped as many peoplestopped spending and sentiment dropped asmany employers laid-off employees.

1997 - 2000 : The Recovery Years

After the crisis, the number of housingdevelopers dropped drastically, from about2,000 to only 200 companies. Research studies(Vanichvatana, 2004) indicated that survivingcompanies found ways to manage their cashflows and their liquidity problems. Many wereable to restructure their loans. Some turned theirlenders into partners and completed partially-finished housing projects. After the crisis, de-velopers began paying much more attention tobuilding design and product strategy, includingusing energy saving solutions.

Government Support - Policies

The Thai government realized that thereal estate industry was a significant driver ofthe country’s GDP and developed policies to

use the industry to jumpstart the Thai economy.It developed supply and demand side remediesand issued the requisite policies and regulations.

It’s main supporting strategy was deve-loping remedies that would create demandand supply equilibrium (Jatusripitak 2002).Government policies were issued to promotedemand and to strengthen the operations ofreal estate developers and those in relatedareas. Such policies could be categorized intotwo following groups.

Supporting Demand-Side Policies

The government developed demand-sidepolicies to encourage homebuyers to makequicker buying decisions. The policies includedownership cost reductions such as tax incentivesand reduced transfer fees.

1. Taxation Privileges and Transfer FeeReductions:

The following incentives were of-fered during 2001 and 2003

• Reduced Special Business Tax rate

• Reduced Personal Income Tax bydeducting expenses of buying ahouse and deducting loan interestexpense

• Reduced real estate title transferfees

• Reduce registration fees whenreal estate used as loan collateral

2. Encouraging home purchases byusing independent state agencies

The Government used two majorapproaches to support the demand side: (1)

46 Volume 1, Number 1, July - December 2007

..........................................................................................GH Bank Housing Journal

Incentives for Government Pension Funds (GPF)and State Enterprises officials (GPF 2003),and (2) Providing special low-price housing fornon-stable-income population (NHA 2003).

Supporting Supply Side Policy

The Government also issued supply sidepolicies to support real estate developers asfollows:

1. Amendments to the Bankruptcy Act

In 1999, the Bankruptcy Act wasamended. These amendments added a newsection on Company Rehabilitation. This gavebusinesses more time and opportunities tocompromise with lenders before filing forbankruptcy. These new rules permitted debtorsand lenders to set up teams to continue opera-ting a business while rescheduling and restruc-turing debts (Ministry of Justice 2003)

2. Resolve Non-Performing Loan Pro-blems by establishing TAMC

Thai Assets Management Corpora-tion (TAMC) was set up in 2001 to furtherresolve financial institution non-performingloans problems resulting from the 1997 crisis.TAMC is an organization established underthe Emergency Decree of the Thai AssetManagement Corporation B.E.2544.

TAMC received non-performingassets from commercial banks and other finan-cial companies. Because of loan paymentconditions, much of the decline in the non-per-forming loans (NPLs) was due to reschedulingrather than tangible restructuring (BizAsia2001).

3. Increase Investment Capital throughProperty Funds

Since 1997, the Ministry of Financeand the Securities Exchange Commissionhave approved the establishment five typesof property funds2. Property Funds are a majorsource of capital for properties and provideequity financing for properties.

ustainable Development of Real EstateIndustry

From the above analysis, all stakeholders,both public agencies and private organizations,need to be more responsible for the industry’ssustainable long-term development. On thepublic side, new policies, laws and regulationsmust be continuously updated. A clear exampleis the recent cooperation between the Bank ofThailand and the Ministry of Finance to guardagainst past monetary and financial controlsmistakes: (1) Tighter controls against currencyattacks, and (2) limiting mortgage loan amounts.

2 Property Funds have been under the care of the Securities Exchange Commission (SEC). The four (out of five)types of Property Fund directly related to solving real estate issue are: Property Fund for Public Offering, Type IFund- Property Fund, Type II Fund - Property Fund for Resolving Financial Institution Problems, Type Fund IV -Property and Loan Fund. The other type is Type III Fund - Mutual Fund for Resolving Financial InstitutionsProblems (SEC 2003) (SEC 2000).

S

................................................................Real Estate Cycles

47GOVERNMENT HOUSING BANK, Thailand

eferences

Bongsadadt, Manop (2000). “Real Estate Crisis: Problem and Solutions Part 1 and Part 2”,RE Journal, the Thai Real Estate Association, No. 16, July - September

Dechavas, Kanok & Lertbunnapong, Bunna (1999). “The Study of Real Estate Business TrendAnalyzed by Economic Indicators”, RE Journal, the Thai Real Estate Association, No. 13,November - December.

Government Pension Fund (GPF) website (2003). http://www.gpf.or.th

Jatusripitak, Somkid (2003), Key Note Speaker Speech, Real Estate Economic Index for theYear 2003, 2003 Annual Seminar of the Three related Thailand Real Estate Associations,Public Relation, Office of Minister, Ministry of Finance

Lee, Saipin (1999). “Understanding of THE PROPERTY MARKET CYCLE?”, RE Journal, theThai Real Estate Association, No. 11, July - August.

Ministry of Justice website (2003). http://moj.go.th

National Housing Authority (NHA) web site (2003). http://www.nhanet.or.th

Siamwalla, Ammar (2000). Anatomy of the Thai Economic Crisis, Thai Economy Watch, websitehttp://ThaiEconWatch.com

Thai Asset Management Corporation (TAMC) website (2003). http://www.tamc.or.th

Vanichvatana, Sonthya (2004). THAILAND 2004 UP TREND REAL ESTATE CYCLE:FUNDAMENTAL AND CHARACTERISTICS. Proceedings of the Tenth Pacific RimReal Estate Society (PRRES) Conference, Bangkok, Thailand, January.

To prevent the market from overheating,homes priced at Bt10 million and more will belimited to mortgages of 70 per cent of marketvalue.

R

Developers and investors have also beenencouraged to further their education and re-ceive professional accreditations. Real estate isnot a hobby; it is a real business.