Embed Size (px)

Citation preview

CANADIAN HOUSING HEALTH CHECK

Risks contained despite some local overheating concerns

Nation-wide indicators continued to suggest that there is a low probability of a wide-

spread and steep downturn in Canada’s housing market in the next 12 months.

At the local level, indicators paint distinct risk profiles with overheating concerns

topping the list in Vancouver and Toronto, and weak economy posing the main threat

in Calgary.

Escalating prices in Vancouver and Toronto: Affordability-related risks continued

to increase significantly in Vancouver and Toronto this year, as prices accelerated

further, especially for single-detached homes. Vancouver, in particular, showed

strong signs of overheating, although recent declines in sales brought some cooling.

New BC tax on foreign buyers: The surprise introduction by the BC government of

a new 15% tax on home purchased by foreign nationals in Metro Vancouver added a

new layer of risk for the Vancouver market. The tax is without precedents in Canada

and substantially raises uncertainty in the short term.

Energy sector downturn: Modest increases in oil prices this year have been a posi-

tive development; yet, oil-producing provincial economies continue to face difficult

challenges, which maintains material negative risks for housing demand and prices in

Alberta and other oil industry sensitive markets in the near term.

Unemployment: Labour market-related risks eased at the national level in recent

months; however, they remain elevated in Alberta and Saskatchewan where the job-

less rate continued to rise to decades-high levels.

Condo construction boom: The risk of over-building has diminished considerably

this year. While condo units under construction remain historically elevated, complet-

ed but unsold inventories have come down in most markets. High levels of construc-

tion are part of the solution to ease resale market tightness in Vancouver and Toronto.

Housing policy: Ongoing concerns about housing affordability, government exposure

to housing and stability of hot housing markets and the financial system keep the odds

of policy intervention elevated.

Interest rates: The probability of an imminent interest rate hike is low and therefore

poses minimal short-term risks at this stage.

September 2016

Largest four housing markets

Toronto — Record-high resale activity

has been sustained so far in 2016.

Prices continue to accelerate, with

stronger gains registered in single-

detached segments—which remain in

short supply. Healthy condo absorption

has significantly mitigated earlier risks

posed by a spike in condo completions

in early 2015. Rapidly eroding afforda-

bility is a growing source of concern.

Montreal — The market took a pause

this spring after a solid start to the

year. A positive development recently

has been a notable decline in invento-

ries (both existing and newly built),

which firmed up market conditions.

Montreal’s overall vulnerability profile

is improving.

Vancouver — Extremely poor—and still

rapidly deteriorating—affordability is a

significant vulnerability. Home prices

have escalated at mind-boggling rates

(more than 30% y/y); however, resales

have begun to come down since reach-

ing an all-time high this winter. The

new BC tax on foreign buyers in Metro

Vancouver may lead to further sales

decline in the near term.

Calgary — Still under the weight of the

provincial recession. Weakening de-

mographics, surging unemployment

and rising inventories are growing

sources of concerns. Home resales

have recovered somewhat since hitting

a multi-year low at the start of 2016;

however, the scope for further gains is

limited in the near-term. Downward

pressure on prices is likely to persist.

Canada Vancouver Calgary Toronto Montreal

Affordability

Resale market balance

Rental market balance

Interest rates

Labour market

Demographics

New home inventory - singles

New home inventory - multiples

Homes under construction - singles

Homes under construction - multiples

Significantly outside historical norms and posing much higher risk than usual

Modestly outside historical norms and posing moderately higher risk than usual

Within historical norms or not posing any immediate threat

Monitoring dashboard

Craig Wright

Chief Economist

(416) 974-7457

Robert Hogue

Senior Economist

416-974-6192

CANADIAN HOUSING HEALTH CHECK | SEPTEMBER 2016

2

Background

Canadian Housing Health Check provides RBC Economics’ assessment of key indicators of Canada’s housing market that are

deemed to offer early warning of potential imbalances. This monitoring exercise is one of the tools used regularly by RBC Econom-

ics to follow developments in this important sector of the Canadian economy. The report focuses on indicators that have been closely

correlated (leading or coincident) with housing downturns and significant home price declines during housing cycles in the past three

decades or so. While we believe that housing affordability and the sales-to-new listings ratio (and months’ inventory) are the best

indicators of market stress and price pressure, respectively, no single indicator provides perfect and accurate early warning signals of

impending trouble. Accordingly, Canadian Housing Health Check emphasizes a ‘dashboard’ approach to convey the point that trou-

ble in the housing market can arise from many directions and that it is imperative to monitor the situation broadly. This approach is

complemented by a detailed review of individual indicators that includes a graphical depiction of the current situation within a his-

torical context and a brief discussion of the rationale of our assessment.

About the graphics and risk ‘zone’ system The dashboard graphics display the current values of the indicators (dark blue bar) within zones that we consider safe (green), con-

cerning (yellow) or dangerous (red). The width of each graphics represents the range of values posted by the indicator during the past

30 years (or period of time available). The far left corresponds to the safest measure ever recorded and the far right, to the most ex-

treme imbalance reached historically. For most indicators, the left corresponds to low values but for some (sales-to-new listings ratio

and net immigration) to high values.

The yellow and red zones appearing in dashboard graphics and individual indicator charts generally were determined by analyzing

past housing downturns and constitute our estimations of thresholds above (or, in some cases, below) which market imbalances and

significant home price declines occurred at the national level in Canada. The yellow zone comprises a range of values that, histori-

cally, have been mostly associated with imbalances but not always with housing downturns (i.e. sustained price declines). In other

words, these values give somewhat ambiguous and sometimes ‘false’ signals. The red zone, however, comprises values that repre-

sent imbalances much more clearly and of larger magnitude. An indicator in the red zone should be considered a source of worry.

The farther to the right in the red zone in the dashboard graphics are the values, the more extreme is the imbalance, the more intense

is the stress exerted on the market and, ultimately, the more severe the potential correction.

The specific rules at the national level are as follows:

RBC Affordability Measure for the aggregate of all housing types: yellow threshold = 45.7% (0.3 standard deviations above

the long-term mean); and red at 49.8% (1.0 standard deviations above the mean).

Sales-to-new listings ratio: yellow threshold = 0.40; and red = 0.35.

Months of inventory: yellow threshold = 7.0; red = 8.5.

Rental vacancy rate: yellow threshold = 3.0% (long-term mean); and red = 3.5% (0.5 standard deviations above the mean).

Real 5-year bond yield relative to trailing 12-month average: yellow threshold = 1.0 percentage point (1 standard deviation

above the mean); red = 2.0 percentage points (2 standard deviations).

Unemployment rate relative to trailing 12-month average: yellow threshold = 0.41 percentage points (0.6 standard deviation

above the mean); red = 1.0 percentage point (1.5 standard deviations).

Net immigration per 1,000 population: yellow threshold = 6.5 (0.5 standard deviations above the mean); red = 5.0 (0.4 stand-

ard deviations below the mean).

Completed and unoccupied units per 1,000 population, singles and semis: yellow threshold = 0.27 (0.3 standard deviations

above the mean); red = 0.34 (1.3 standard deviation above the mean).

Completed and unoccupied units per 1,000 population, multiples: yellow threshold = 0.36 (the mean); red = 0.43 (0.9 stand-

ard deviation above the mean).

Housing under construction per 1,000 population, singles: yellow threshold = 2.12 (0.5 standard deviations from the mean);

red = 2.34 (1 standard deviation from the mean).

Housing under construction per 1,000 population, multiples: yellow threshold = 3.86 (0.5 standard deviations from the

mean); red = 4.49 (1 standard deviation from the mean).

The areas shaded in grey in the indicator charts correspond to housing downturns – i.e., periods during which home prices (as de-

fined as average prices of homes sold on the MLS system) fell by more than 5% from monthly peak to trough. It is important to note

that the precise timing of these downturns can vary depending on the home price measure used. The grey shaded areas, therefore,

should be seen as broad guidelines.

CANADIAN HOUSING HEALTH CHECK | SEPTEMBER 2016

3

CANADA

Affordability

Deteriorating

Existing home market balance

Tightening

Declining

Rising slightly

Demand fundamentals

Fairly stable

Declining modestly

Rising sharply

Supply fundamentals

Stable

Declining

Declining slightly

Rising

Six-month trend

RBC affordability measure- aggregate

Low High

Sales-to-new listings ratio

LowHigh

Months of inventory

Low High

Change in real 5-Year bond yields

Low High

Low High

Housing under construction per capita - singles

Low High

YellowHousing under construction per capita - multiples

Low High

Yellow

Rental vacancy rate

Change in the unemployment rate

Low High

Yellow

LowHigh

Yellow

Net immigration rate

Low High

YellowCompleted and unsold units per capita - singles and semis

Low High

YellowCompleted and unosold units

per capita - multiples

CANADIAN HOUSING HEALTH CHECK | SEPTEMBER 2016

4

Affordability

CANADA

Existing home market balance

20

25

30

35

40

45

50

55

60

65

70

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

RBC affordability measure - aggregate

Source: RBC Economics Research, Brookfield RPS, Statistics Canada, Bank of Canada, Royal LePage

Ownership costs as % of household income, Canada

In our view, affordability is the most meaningful indicator of underlying

market stress. Other traditional metrics such price-to-income and price-to-rent ratios can be useful guides of market imbalance under many circumstances;

however at this juncture, affordability is a superior gauge because it explicitly

takes into account interest rates (the other measures don’t), which have been—and, in the near term, expected to remain—abnormally low in Canada.

The most recent reading of RBC’s aggregate housing affordability meas-

ure (42.8% in Q2 2016) suggests the presence of greater-than-average

market stress for buyers in Canada with the situation steadily deteriorat-

ing since the spring of 2015. Affordability is most stretched for single-

detached home in Canada’s largest markets. Condo affordability (34.4%)

is generally quite close to historical norms, which implies little in the way

of undue stress in this category.

We estimate the ‘danger zone’ for the aggregate measure to be above 45.0%

nationally.

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Monthly, S.A.

Sales-to-new listings ratio

Source: RBC Economics Research, Canadian Real Estate Association

Monthly, S.A., Canada

Sales-to-new listings ratio

Buyer's market

Balanced market

Seller's market

The sales-to-new listings ratio is a reliable gauge of the degree of slack or

tightness in the resale market. When the ratio approaches, or is above 0.60, the market favours sellers and prices typically rise rapidly. When the ratio

approaches, or is below 0.40, the market favours buyers and prices come

under intense downward pressure. Anything in between is considered a bal-anced market and prices tend to rise modestly.

Canada-wide, the sales-to-new listings ratio climbed into seller’s market

territory this year and was 0.62 in July 2016, just slightly below the six-

year high of 0.65 reached in April and May. In recent months, home

resales in Canada have come off this spring’s all-time highs, while new

listings have partially rebounded following steady declines during the

first half of 2016. The majority of markets are considered balanced with

Toronto and Vancouver (both sellers’ market) bucking the trend.

Historically, the largest price declines occurred when the ratio fell below

0.35.

0

1

2

3

4

5

6

7

8

9

10

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Long-term average

Monthly, S.A., Canada

Months of inventory

Source: RBC Economics Research, Canadian Real Estate Association

The total number of homes for sale expressed as the number of months it

would take to sell them at the current pace of sales is another resale market balance indicator. Historical correlation with prices is difficult to establish

with precision, however, because the Canadian Real Estate Association has

been publishing this indicator only since 2004.

Nonetheless, based on what track record is available, we estimate that down-

ward pressure on prices start to build at levels between 7.0 and 8.5 months,

and that severe pressure emerges at levels exceeding 8.5.

The slowdown in listings during the first half of 2016 amid strong resales

reduced the number of months’ inventory in Canada to the lowest level

(4.6) in more than six years. This level is consistent with continued price

increases.

Demand-supply balance indicators for the existing home market, there-

fore, continue to suggest little in the way of any imminent threat to the

stability of the national market.

0

1

2

3

4

5

6

1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

Long-term average

Rental vacancy rate

Annual:1988-2010; Semi-annual: 2011-currentSource: RBC Economics Research, CMHC

%, total CMAs, purpose-built apartment buildings of three units or more, Canada The rental vacancy rate has not correlated very closely with prices historical-

ly. However, we believe that the Canadian housing story will be very sensi-

tive to the supply of new units into the marketplace, much of which (almost

entirely condos) will be directed toward the rental market. Therefore, this

gauge of market absorption in the rental segment should be monitored close-ly.

A main drawback of the vacancy rate as a monitoring tool is that it is pub-

lished only once a year (in October) by CMHC.

The latest data for October 2015 shows further increase from 2.8% in

October 2014 to 3.3% at the national level, which slightly exceeds the

long-term average (2.9%). The rise primarily reflected large increases in

Alberta and Saskatchewan.

We would consider a vacancy rate above 3.5% as a sign of oversupply in the

rental space.

CANADIAN HOUSING HEALTH CHECK | SEPTEMBER 2016

5

Demand fundamentals

CANADA

Supply fundamentals

-4

-3

-2

-1

0

1

2

3

4

5

6

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Percentage points, Canada

Real 5-year bond yields relative to trailing 12-month average

Source: RBC Economics Research, Bank of Canada, Statistics Canada

Surges in interest rates have been strongly associated with market downturns

and price declines in several housing cycles in the past 30 years in Canada.

A 100 basis-point rise relative to the trailing 12-month average would apply

intense downward pressure on the market and a 200 basis point surge would likely destabilize it and potentially cause a significant price decline.

The yield on the five-year Government of Canada bond continued to

trend lower this year and is currently near historical lows. The real yield

was slightly below its 12-month trailing average since March after mov-

ing briefly above it late last year and early this year. Interest rates re-

main a very supportive influence on housing demand in Canada.

RBC’s base case interest rate forecast calls for the overnight rate to

remain unchanged through the end of 2017, and for longer-term rates to

increase before then. This scenario would pose limited risks to the hous-

ing market in the near term.

-2

-1

1

2

3

4

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Percentage points, Canada

Unemployment rate relative to trailing 12-month average

Source: RBC Economics Research, Statistics Canada

Similarly, spikes of unemployment have been associated with housing down-

turns in the past 30 years, although they have tended to lag price declines rather than lead them.

We estimate that a 0.25 percentage point increase in Canada’s unemployment

rate relative to the trailing 12-month average would stress the market moder-

ately, but that a full percentage-point surge would threaten the stability of the market.

The unemployment rate has eased since spring after rising modestly

during the course of 2015. It dipped below the trailing 12-month average

since May.

Labour market conditions pose little risk nationally at this point. Such is

not the case everywhere across the country, however. Labour market-

related risks are prominent in markets in oil-producing provinces.

1

2

3

4

5

6

7

8

9

10

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

Trailing 4-quarter sum, Canada, per 1,000 population

Net immigration rate

Source: RBC Economics Research, Statistics Canada

Net immigration into Canada is another indicator that has not correlated

closely with housing downturns or price declines historically; however, given

the boom in condo construction in major Canadian cities, any sign that the

strong inflow of immigrants is slowing would be concerning.

The rate of net immigration in Canada (measured per 1,000 population)

recently picked up significantly after falling between Q4/14 and Q2/15.

The latest rate for Q1/16 rose to 7.7 from a 16-year low of 5.1 in Q3/15. This

is now comfortably above the 6.5 threshold signalling some degree of vulner-ability.

Further increase in the rate is likely to occur in light of the federal gov-

ernment this year increasing its target for new permanent residents by

more than 10%.

0.0

0.1

0.2

0.3

0.4

0.5

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

Units per 1,000 population, Canada, n.s.a.

Completed and unsold units - singles and semis

Source: RBC Economics Research, Statistics Canada, Canada Mortgage and Housing Corporation

A telltale of an overbuilt market is the number of units recently completed but

remaining unsold.

We segment the Canadian market into singles and multiples to identify poten-

tial sources of trouble.

On the single-family homes side, the stock of unsold units has remained

quite stable at 0.22-0.24 units per 1,000 population since mid-2014.

There continues to be no signs of any excess supply of new single-

detached units in Canada at this stage. If fact, the opposite is the case in

several markets where single-detached are in short supply.

We would consider the situation concerning at 0.29 units and dangerous at

0.36 units.

CANADIAN HOUSING HEALTH CHECK | SEPTEMBER 2016

6

Supply fundamentals

CANADA

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

Units per 1,000 population, Canada, n.s.a.

Completed and unsold units - multiples

Source: RBC Economics Research, Statistics Canada, Canada Mortgage and Housing Corporation

On the multi-unit dwellings side, market absorption has been quite solid

this year at a time when completions moderated from last year’s strong

pace. This helped to draw down the inventory of unsold units in Canada.

The rate of unsold units eased to 0.32 units per 1,000 population in July

2016, down from a 19-year high of 0.41 units in May 2015.

The unsold inventory surged in the early months of 2015 due to a wave in

condo completions in the Toronto area.

The latest read of this indicator was slightly below the long-term average

(0.36) and well below the 0.48 threshold that would signal a high degree

of excess.

Overall, the inventory of completed but unsold condos evolved construc-

tively in the past year in Canada, thereby lessening oversupply risks.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

Units per 1,000 population, Canada, n.s.a.

Housing under construction - singles

Source: RBC Economics Research, Statistics Canada, Canada Mortgage and Housing Corporation

The object of much concern in recent past has been the number of housing

units under construction in Canada.

We continue to find that little concern of overbuilding is warranted in the

single family home segment, where levels remain well below historical

averages (when measured on a per 1,000 population basis) with the trend

even declining slightly in the past several years, including so far in 2016.

In some of Canada’s largest markets, demand for single family homes

significantly outstrips supply.

0.0

1.0

2.0

3.0

4.0

5.0

6.0

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

Units per 1,000 population, Canada, n.s.a.

Housing under construction - multiples

Source: RBC Economics Research, Statistics Canada, Canada Mortgage and Housing Corporation

On the multiples side, however, there continues to be historically-high

levels of condo units under construction in Canada.

There were 5.8 multi-unit dwellings per 1,000 population under construc-

tion in Canada in Q2/16, matching the decades-high reached in 2014.

Strictly speaking, this level is well into the ‘high risk zone’ (4.5 units or

higher); however, in the context of tight demand-supply balances in mar-

kets such as Vancouver and Toronto, strong construction should be seen

as being part of the solution to bring about some kind of cooling.

Most of the units being built are in the Toronto (34% of total) and Van-

couver (17%) areas.

Strong condo construction in large part reflects structural changes that

arose from policy (e.g. rules limiting urban sprawl) and affordability

(condo apartments are the more affordable housing type) considerations,

and therefore, represents a market share gain over single-family homes.

Nonetheless, the prospects for high levels of condo completions in the

period ahead entail a fair degree of absorption risks.

CANADIAN HOUSING HEALTH CHECK | SEPTEMBER 2016

7

GREATER TORONTO AREA

Affordability

Deteriorating rapidly

Existing home market balance

Tightening

Declining

Stable

Demand fundamentals

Fairly stable

Declining

Rising slightly

Supply fundamentals

Stable

Declining

Stable

Rising

Six-month trend

Change in real 5-Year bond yields

Low High

RBC affordability measure- aggregate

Low High

Sales-to-new listings ratio

LowHigh

Months of inventory

- OntarioLow High

Low High

Yellow

Rental vacancy rate

Change in the unemployment rate

Low High

Yellow

LowHigh

Yellow

Population growth

Low High

YellowCompleted and unsold units per capita - singles and semis

Low High

YellowCompleted and unsold units per

capita - multiples

Low High

Housing under construction per capita - singles

Low High

YellowHousing under construction per capita - multiples

CANADIAN HOUSING HEALTH CHECK | SEPTEMBER 2016

8

Affordability in the GTA has been on a deteriorating trend since 2012

with the pace of deterioration accelerating in the past year. RBC’s meas-

ure is now in a zone that historically has been associated with high risks.

Most of the affordability pressure is concentrated in the single-family

home side of the market. Condo affordability, on the other hand, is much

less strained, as the level remains reasonably close to its long-term aver-

age.

Stretched affordability does not appear to be a primary consideration for

GTA homebuyers at this stage. Home resales reached record levels in the

first half of 2016, although they have retreated somewhat since hitting a

peak in May.

The Toronto-area market would be more sensitive to a substantial rise in

interest rates than most markets in Canada due to its high prices.

Demand-supply conditions remain very tight in the GTA. This is a

sellers’ market. The sales-to-new listings ratio reached a seven-year high

of 0.76 in May 2016, well above the 0.60 threshold marking conditions

favouring sellers. The ratio has eased back a little since then (it was 0.71

in July). Tight market conditions fuel strong—and still accelerating—

price increases, particularly for detached homes (more than 19% y/y),

far exceeding household income growth.

At this stage, the sales-to-new listings ratio suggests little in the way of

any imminent price declines in the region.

On the contrary, current conditions point toward further acceleration in

price gains in the coming months, thereby further exacerbating the

GTA’s affordability challenges.

Affordability

GREATER TORONTO AREA

Existing home market balance

0

1

2

3

4

5

6

7

8

9

10

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Long-term average

Monthly, S.A., Ontario

Months of inventory

Source: RBC Economics Research, Canadian Real Estate Association

Demand-supply tightness is corroborated by very low inventory of homes

for sales (active listings).

Although data is available only at the provincial level, the number of

months’ inventory in Ontario is at its lowest point (2.1 months in July

2016) since records have been published by the Canadian Real Estate

Association (2003).

Concerns that Toronto’s condo boom would flood the rental market and

cause vacancies to rise have not materialized to date.

The rental vacancy rate in the GTA has remained stable and low in re-

cent years. It was 1.6% in October 2015 (the most recent read from

CMHC).

According to the Toronto Real Estate Board, condo rental activity

paused in the second quarter, following very strong growth in recent

years. The Board attributed the recent pause to a declining in condo

rental listings, which limited choice for renters. Average rent continued

to rise at a brisk pace (by more than 6% y/y for a one-bedroom apart-

ment).

So far, there is little evidence that condo investors who rent their units

have overestimated rental demand.

20

30

40

50

60

70

80

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

RBC affordability measure - aggregate

Source: RBC Economics Research, Brookfield RPS, Statistics Canada, Bank of Canada, Royal LePage

Ownership costs as % of household income, Toronto

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Monthly, S.A.

Sales-to-new listings ratio

Source: RBC Economics Research, Canadian Real Estate Association

Monthly, S.A., Toronto

Sales-to-new listings ratio

Buyer's market

Balanced market

Seller's market

0

1

2

3

4

5

6

1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

Long-term average

Rental vacancy rate

Source: RBC Economics Research, CMHC

%, purpose-built apartment buildings of three units or more, Toronto

CANADIAN HOUSING HEALTH CHECK | SEPTEMBER 2016

9

Labour market conditions in the GTA continue to be generally support-

ive for the area’s housing market.

Toronto’s unemployment rate recently fell to its lowest level (6.4% in

July 2016) since the middle of 2008.

Labour market-related risks are low at this point.

Demand fundamentals

GREATER TORONTO AREA

Supply fundamentals

-2

-1

1

2

3

4

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Percentage points, Toronto

Unemployment rate relative to trailing 12-month average

Source: RBC Economics Research, Statistics Canada

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

Y/Y % change in the 15+ population, Toronto

Adult population growth

Source: RBC Economics Research, Statistics Canada

Solid demographic fundamentals have long supported GTA’s housing

market.

Those fundamentals improved this year, following a period of softening

in 2014-2015.

The rate of growth in adult population picked up from 1.6% in mid-2015

to 1.8% most recently, thereby inching closer to GTA’s long-term aver-

age of 1.9%.

A rate below 1.5% would be a source of concern.

GTA home builders are responding to the dearth of single-family homes

in the area, with starts rising 25% y/y so far in 2016 (from historically

low levels in 2015).

This is as a positive development that will help address the tightness issue

in this housing category.

Inventories of newly completed and unsold the single-family continue to

be historically low despite trending slightly higher in the past four years.

There is no indication of overbuilding of single-family homes in the area

at present.

The inventory of recently completed and unsold condo units is no longer

a source of concern in the Toronto area.

Absorption of newly built condos has been brisk in the GTA in the past

year and stocks of unsold units have come down considerably.

The unabsorbed inventory fell from a 22-year peak of 0.58 units per

1,000 population in May 2015 to 0.25 units in July 2016, which is within

the ‘safe zone’—i.e., below the 0.27 threshold signalling the potential for

mild excess supply.

A surge in condo completions (reflecting several large condo projects

reportedly reaching the ‘completed’ stage) led to a sharp increase in the

number of unsold units in early 2015. Completions returned to more

normal levels subsequently.

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

Units per 1,000 population, Toronto, n.s.a.

Completed and unsold units - singles and semis

Source: RBC Economics Research, Statistics Canada, Canada Mortgage and Housing Corporation

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

Units per 1,000 population, Toronto, n.s.a.

Completed and unsold units - multiples

Source: RBC Economics Research, Statistics Canada, Canada Mortgage and Housing Corporation

CANADIAN HOUSING HEALTH CHECK | SEPTEMBER 2016

10

Supply fundamentals

GREATER TORONTO AREA

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

Units per 1,000 population, Toronto, n.s.a.

Housing under construction - singles

Source: RBC Economics Research, Statistics Canada, Canada Mortgage and Housing Corporation

Single-detached starts picked up this year and boosted the number of

such units currently under construction; however, this level remains

below the long-term average for the area when measured in per 1,000

population terms.

Recent levels of construction therefore do not signal any impending wave

of single-unit supply that might cause trouble for the market.

Policy to reduce urban sprawl and favour higher density urban develop-

ment contributed to a significant slowdown in single-detached home

construction since the mid-2000s.

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

Units per 1,000 population, Toronto, n.s.a.

Housing under construction - multiples

Source: RBC Economics Research, Statistics Canada, Canada Mortgage and Housing Corporation

The number of multi-unit dwellings under construction has rebounded

since mid-2015 although it is still down noticeably from the all-time highs

reached in 2014.

The recent rise was attributed to a sharp increase in multi-unit starts in

2015 following two years of decline, although the pace has moderated so

far this year.

Expressed on a per 1,000 population basis, multi-unit construction re-

mains in a high risk zone; however, the potential threat to the market is

tempered by the healthier unsold condo inventory.

The main risk of high levels of construction is that many units could

reach the completed stage at once, thereby flooding the condo resale and/

or rental markets. So far, both of these markets have absorbed the in-

creased supply quite handily.

CANADIAN HOUSING HEALTH CHECK | SEPTEMBER 2016

11

GREATER MONTREAL AREA

Affordability

Deteriorating slightly

Existing home market balance

Tightening

Declining

Rising

Demand fundamentals

Fairly stable

Declining

Rising

Supply fundamentals

Stable

Declining

Stable

Declining

Six-month trend

Change in real 5-Year bond yields

Low High

RBC affordability measure- aggregate

Low High

Sales-to-new listings ratio

LowHigh

Months of inventory -

QuebecLow High

Low High

Yellow

Rental vacancy rate

Change in the unemployment rate

Low High

Yellow

LowHigh

Yellow

Population growth

Low High

YellowCompleted and unsold units per capita - singles and semis

Low High

YellowCompleted and unsold units per capita - multiples

Low High

Housing under construction per capita - singles

Low High

YellowHousing under construction per capita - multiples

CANADIAN HOUSING HEALTH CHECK | SEPTEMBER 2016

12

Affordability

GREATER MONTREAL AREA

Existing home market balance

Existing home supply expressed as number of months’ inventory shows a

steady declining trend in Quebec since early 2015, although it remains

historically high at the juncture.

This is consistent with the modest firming in marked conditions in Mon-

treal.

The wave of condo completions in 2014 increased competition for pur-

pose-built apartment buildings, which over time has translated into high-

er rental vacancy rates.

The vacancy rate in the Montreal area rose from 3.4% in October 2014

to 4.0% in October 2015, thereby signalling some mild degree of oversup-

ply in the rental market.

20

25

30

35

40

45

50

55

60

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

RBC affordability measure - aggregate

Source: RBC Economics Research, Brookfield RPS, Statistics Canada, Bank of Canada, Royal LePage

Ownership costs as % of household income, Montreal

Affordability deteriorated slightly in the Montreal area this year after

showing an improving trend in the previous six years. Despite the recent

erosion, affordability does not pose any unusual risks at this point.

RBC’s aggregate measure was 39.4% in Q2/16, up 1.6 percentage points

from a year ago but still within the safe range.

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Monthly, S.A.

Sales-to-new listings ratio

Source: RBC Economics Research, Canadian Real Estate Association

Monthly, S.A., Montreal

Sales-to-new listings ratio

Buyer's market

Balanced market

Seller's market

Demand-supply conditions in the Montreal area have been on a gradual-

ly tightening trend since last year. The sales-to-new listings ratio contin-

ued to drift higher this year to 0.54 by July, near the highest point in

more than three years.

After rising by 6.0% last year, home resales started 2016 on a solid note

but then stalled in the spring. Meanwhile, the inventory of homes for sale

has been drawn successively, including for condos (which had been a

significant issue earlier). New listings have dropped steadily below year-

ago levels.

The upward trend in the sales-to-new listings ratio suggests that the rate

of price increases may strengthen in the period ahead, and do not point

to any imminent risk of a downward price spiral.

0

2

4

6

8

10

12

14

16

18

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Long-term average

Monthly, S.A., Quebec

Months of inventory

Source: RBC Economics Research, Canadian Real Estate Association

0

1

2

3

4

5

6

7

8

1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

long-term average

Rental vacancy rate

Source: RBC Economics Research, Statistics Canada

%, purpose-built apartment buildings of three units or more, Montreal

CANADIAN HOUSING HEALTH CHECK | SEPTEMBER 2016

13

Montreal’s job market showed notable improvement this year. The un-

employment fell by almost a full percentage point since the beginning of

2016. It currently stands at 7.8%, its second-lowest level in three years.

The drop offered further support for the housing market and therefore

was a positive development from a risk point of view.

Demand fundamentals

GREATER MONTREAL AREA

Supply fundamentals

Following a two year-long period of easing growth, Montreal’s adult

population has grown a little faster since mid-2015 and returned to the

long-term average of 1.0% this spring.

Overall demographics currently pose little risks for the market.

-2

-1

1

2

3

4

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Percentage points, Montreal

Unemployment rate relative to trailing 12-month average

Source: RBC Economics Research, Statistics Canada

0.0

0.4

0.8

1.2

1.6

2.0

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

Y/Y % change in the 15+ population, Montreal

Adult population growth

Source: RBC Economics Research, Statistics Canada

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

Units per 1,000 population, Montreal, n.s.a.

Completed and unsold units - singles and semis

Source: RBC Economics Research, Statistics Canada, Canada Mortgage and Housing Corporation

There continues to be very few newly completed single-family homes that

are unsold in the Montreal area.

We see no evidence of an overbuild in this market segment.

0.0

0.4

0.8

1.2

1.6

2.0

2.4

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

Units per 1,000 population, Montreal, n.s.a.

Completed and unsold units - multiples

Source: RBC Economics Research, Statistics Canada, Canada Mortgage and Housing Corporation

On the multi-unit dwelling side, conditions improved noticeably in the

past year with the stock of unabsorbed units declining markedly. The

stock fell from 0.91 units per 1,000 population in August 2015 to 0.75

units by July 2016.

Nonetheless, despite this improvement, the stock remains somewhat

elevated from a historical perspective. It is still above the long-term aver-

age of 0.69 units in the area.

This suggests that some degree of surplus persists in the multi-unit seg-

ment of the market in Montreal.

CANADIAN HOUSING HEALTH CHECK | SEPTEMBER 2016

14

Supply fundamentals

GREATER MONTREAL AREA

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

Units per 1,000 population, Montreal, n.s.a.

Housing under construction - singles

Source: RBC Economics Research, Statistics Canada, Canada Mortgage and Housing Corporation

The risk of any overbuilding of single-family homes in the short term is

extremely remote.

Current levels of units under construction are significantly below long-

run averages, well within the ‘safe zone’.

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

Units per 1,000 population, Montreal, n.s.a.

Housing under construction - multiples

Source: RBC Economics Research, Statistics Canada, Canada Mortgage and Housing Corporation

A sharp increase in completed units in purpose-built apartment buildings

this year significantly reduced the number multi-unit dwellings under

construction in Montreal.

In per 1,000 population terms, that number fell from an all-time high of

5.8 units in January 2016 to 4.9 units in July. While the level remains

historically elevated, it no longer sends a strong signal for a potential risk

of overbuilding.

Strong condo construction activity in the past decade partly reflected a

structural shift toward multiples supported by urban development policy

and affordability advantage relative to single-family homes.

CANADIAN HOUSING HEALTH CHECK | SEPTEMBER 2016

15

GREATER VANCOUVER AREA

Affordability

Deteriorating sharply

Existing home market balance

Easing rapidly

Stable

Declining

Demand fundamentals

Fairly stable

Declining

Easing slightly

Supply fundamentals

Declining

Declining

Rising

Rising rapidly

Six-month trend

Change in real 5-Year bond yields

Low High

RBC affordability measure- aggregate

Low High

Sales-to-new listings ratio

LowHigh

Months of inventory - BC

Low High

Low High

Yellow

Rental vacancy rate

Change in the unemployment rate

Low High

Yellow

LowHigh

Yellow

Population growth

Low High

YellowCompleted and unsold units per capita - singles and semis

Low High

Completed and unsold units per

capita - multiples

Low High

Housing under construction per capita - singles

Low High

Housing under construction per capita - multiples

CANADIAN HOUSING HEALTH CHECK | SEPTEMBER 2016

16

Affordability

GREATER VANCOUVER AREA

Existing home market balance

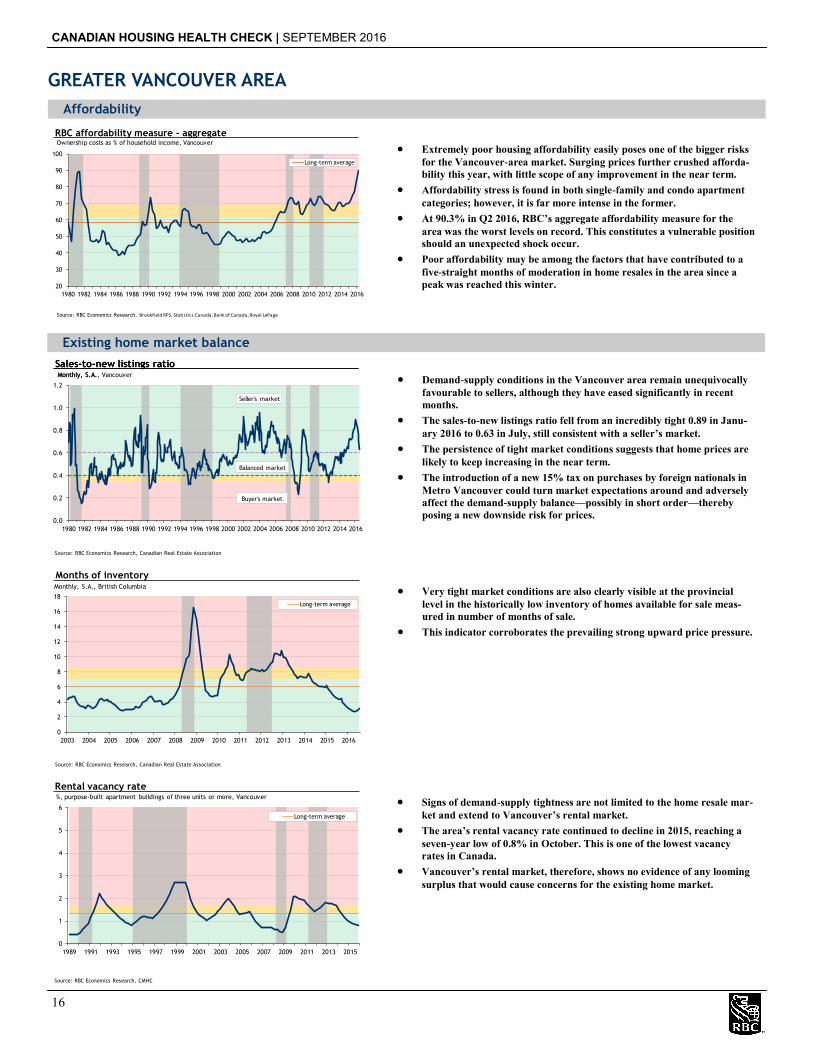

Very tight market conditions are also clearly visible at the provincial

level in the historically low inventory of homes available for sale meas-

ured in number of months of sale.

This indicator corroborates the prevailing strong upward price pressure.

Signs of demand-supply tightness are not limited to the home resale mar-

ket and extend to Vancouver’s rental market.

The area’s rental vacancy rate continued to decline in 2015, reaching a

seven-year low of 0.8% in October. This is one of the lowest vacancy

rates in Canada.

Vancouver’s rental market, therefore, shows no evidence of any looming

surplus that would cause concerns for the existing home market.

20

30

40

50

60

70

80

90

100

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

RBC affordability measure - aggregate

Source: RBC Economics Research, Brookfield RPS, Statistics Canada, Bank of Canada, Royal LePage

Ownership costs as % of household income, Vancouver

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Monthly, S.A.

Sales-to-new listings ratio

Source: RBC Economics Research, Canadian Real Estate Association

Monthly, S.A., Vancouver

Sales-to-new listings ratio

Buyer's market

Balanced market

Seller's market

Extremely poor housing affordability easily poses one of the bigger risks

for the Vancouver-area market. Surging prices further crushed afforda-

bility this year, with little scope of any improvement in the near term.

Affordability stress is found in both single-family and condo apartment

categories; however, it is far more intense in the former.

At 90.3% in Q2 2016, RBC’s aggregate affordability measure for the

area was the worst levels on record. This constitutes a vulnerable position

should an unexpected shock occur.

Poor affordability may be among the factors that have contributed to a

five-straight months of moderation in home resales in the area since a

peak was reached this winter.

Demand-supply conditions in the Vancouver area remain unequivocally

favourable to sellers, although they have eased significantly in recent

months.

The sales-to-new listings ratio fell from an incredibly tight 0.89 in Janu-

ary 2016 to 0.63 in July, still consistent with a seller’s market.

The persistence of tight market conditions suggests that home prices are

likely to keep increasing in the near term.

The introduction of a new 15% tax on purchases by foreign nationals in

Metro Vancouver could turn market expectations around and adversely

affect the demand-supply balance—possibly in short order—thereby

posing a new downside risk for prices.

0

2

4

6

8

10

12

14

16

18

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Long-term average

Monthly, S.A., British Columbia

Months of inventory

Source: RBC Economics Research, Canadian Real Estate Association

0

1

2

3

4

5

6

1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

Long-term average

Rental vacancy rate

Source: RBC Economics Research, CMHC

%, purpose-built apartment buildings of three units or more, Vancouver

CANADIAN HOUSING HEALTH CHECK | SEPTEMBER 2016

17

The job situation in Vancouver has been very positive this past year with

employment up by an impressive 6.6% y/y in July and the jobless rate

falling to its lowest point (5.4% in June) in seven years.

Labour market developments do not pose any immediate threat to the

housing market. On the contrary, they offer substantial support current-

ly.

Demand fundamentals

GREATER VANCOUVER AREA

Supply fundamentals

Adult population growth (1.7% y/y in July 2016) remained slightly weak-

er than the long-term average (2.2%) for the area.

At this stage, demographic factors represent an ambiguous risk factor

for the market.

-2

-1

1

2

3

4

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Percentage points, Vancouver

Unemployment rate relative to trailing 12-month average

Source: RBC Economics Research, Statistics Canada

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

Y/Y % change in the 15+ population, Vancouver

Adult population growth

Source: RBC Economics Research, Statistics Canada

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

Units per 1,000 population, Vancouver, n.s.a.

Completed and unsold units - singles and semis

Source: RBC Economics Research, Statistics Canada, Canada Mortgage and Housing Corporation

Absorption of single-detached and semi-detached has been quite vigorous

since early 2014 and this continued to be the case in 2016. As a result, the

number of recently completed and unsold units has fallen steadily, reach-

ing 0.34 units per 1,000 population in July 2016— well into the ‘safe

zone’.

With singles and semi-detached completions continuing to rise only mod-

estly this year, the Vancouver-area market does not show any signs of

being overbuilt at this point. On the contrary, very tight market condi-

tions for existing homes suggest that supply is short.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

Units per 1,000 population, Vancouver, n.s.a.

Completed and unsold units - multiples

Source: RBC Economics Research, Statistics Canada, Canada Mortgage and Housing Corporation

Similarly, the situation on the multi-unit dwelling side of the market

remains safe.

The number of completed and unsold units has trended lower since early

2014, reaching a nine-year low in July 2016.

Moderate levels of apartment completions in 2014 and 2015 limited the

flow of new supply into the market, and this continued to be the case in

2016 despite a slight increase in completions.

The Vancouver condo market does not appear to be overbuilt at this

point.

CANADIAN HOUSING HEALTH CHECK | SEPTEMBER 2016

18

Supply fundamentals

GREATER VANCOUVER AREA

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

Units per 1,000 population, Vancouver, n.s.a.

Housing under construction - singles

Source: RBC Economics Research, Statistics Canada, Canada Mortgage and Housing Corporation

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

Units per 1,000 population, Vancouver, n.s.a.

Housing under construction - multiples

Source: RBC Economics Research, Statistics Canada, Canada Mortgage and Housing Corporation

Builders’ response to the shortage of single-family homes in the Vancou-

ver area has become more vigorous in 2016 with starts rising by 17%

year to date, and the number of single units under construction reaching

its highest level in nearly 22 years.

On its own, the rising number of single-family homes under construction

suggest increasing risks; however, very low inventories of single-detached

homes for sale in the market implies that absorption is likely to remain

strong.

Fueled by very strong housing starts this year, the number of multi-

family units under construction (on a per 1000 population basis) rose to a

new record level in recent months, thereby signaling greater-than-usual

risks for the future balance of the market.

Such risks are tempered by the very tight market conditions in the resale

market and low inventories of newly built and unsold units.

CANADIAN HOUSING HEALTH CHECK | SEPTEMBER 2016

19

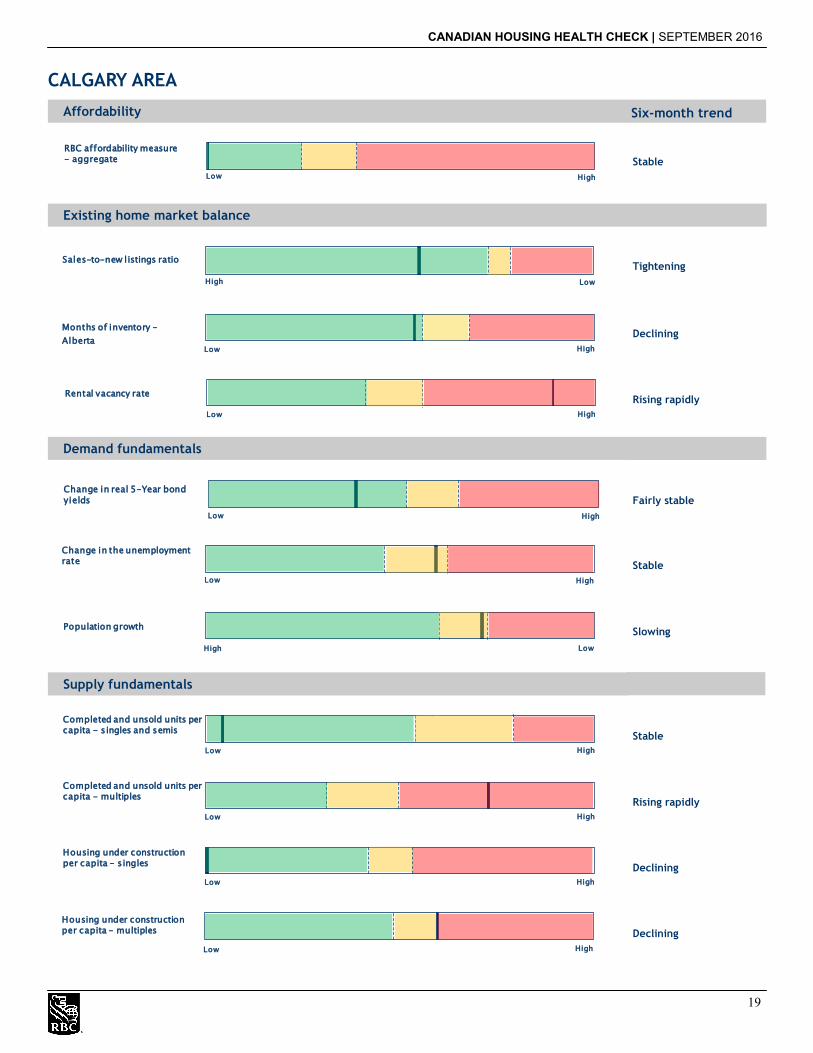

CALGARY AREA

Affordability

Stable

Existing home market balance

Tightening

Declining

Rising rapidly

Demand fundamentals

Fairly stable

Stable

Slowing

Supply fundamentals

Stable

Rising rapidly

Declining

Declining

Six-month trend

Change in real 5-Year bond yields

Low High

RBC affordability measure- aggregate

Low High

Sales-to-new listings ratio

LowHigh

Months of inventory -

AlbertaLow High

Low High

Yellow

Rental vacancy rate

Change in the unemployment rate

Low High

Yellow

LowHigh

Yellow

Population growth

Low High

YellowCompleted and unsold units per capita - singles and semis

Low High

Completed and unsold units per capita - multiples

Low High

Housing under construction per capita - singles

Low High

YellowHousing under construction per capita - multiples

CANADIAN HOUSING HEALTH CHECK | SEPTEMBER 2016

20

Affordability

CALGARY AREA

Existing home market balance

The picture for the overall inventory of homes for sale in Alberta also

improved in recent months, although it continues to show plentiful op-

tions for buyers. The number of months’ inventory was 5.8 in July, down

from cyclical high of 7.0 in February but still well above the 4.6 that

prevailed a year ago.

Calgary Real Estate Board reported that active listings in the area were

up by more than 11% in July relative to a year ago, which is consistent

with the provincial picture of ample options for buyers.

It is also consistent with downward pressure on prices persisting in the

short term, albeit at a diminishing intensity.

The recent drawdown in active inventory has eased downside risks for

prices in the area.

Calgary’s rental market shows signs of increasingly being over-supplied.

The rental vacancy rate surged to a six-year high of 5.3% in October

2015. It was 1.4% a year earlier.

Such high vacancy rate raises significant downside risks for rent values

in the area and revenue prospects for condo investors.

20

30

40

50

60

70

80

90

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

RBC affordability measure - aggregate

Source: RBC Economics Research, Brookfield RPS, Statistics Canada, Bank of Canada, Royal LePage

Ownership costs as % of household income, Calgary

Housing affordability is a generally constructive factor for the Calgary-

area market, remaining quite stable in past year (in the range of 34%-

35% for RBC’s aggregate measure).

In the current difficult context—with historically low oil prices and surg-

ing unemployment sapping the confidence of both buyers and sellers—

the good affordability standing reduces the risk of a significant price

decline.

Calgary faces many tough issues; however, there is no evidence to suggest

that affordability is one of them.

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Monthly, S.A.

Sales-to-new listings ratio

Source: RBC Economics Research, Canadian Real Estate Association

Monthly, S.A., Calgary

Sales-to-new listings ratio

Buyer's market

Balanced market

Seller's market

After weakening considerably in 2015, demand-supply conditions im-

proved so far this year on the back of a slight recovery in home resales

(from a historically low base) and significant reduction in new listings.

The sales-to-new listings ratio—which rose from 0.41 in December 2015

to 0.56 in July—would suggest that the Calgary market is balanced;

however, there continues to be a hefty inventory of active listings.

Despite showing signs of stabilizing recently, housing demand remains

soft in Calgary. Home resales plummeted by 29% in 2015 and are still

down almost 11% year-to-date in 2016.

0

2

4

6

8

10

12

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Long-term average

Monthly, S.A., Alberta

Months of inventory

Source: RBC Economics Research, Canadian Real Estate Association

0

1

2

3

4

5

6

7

8

1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

Long-term average

Rental vacancy rate

Source: RBC Economics Research, Statistics Canada

%, purpose-built apartment buildings of three units or more, Calgary

CANADIAN HOUSING HEALTH CHECK | SEPTEMBER 2016

21

Calgary’s labour market continues to be significantly challenged. The

area’s jobless rate was at a decades-high of 8.6% in July amid a loss of

nearly 32,000 jobs in the past 14 months.

The speed with which labour market conditions have deteriorated still

poses significant risks for the housing market; however, it has eased

somewhat in recent months.

Demand fundamentals

CALGARY AREA

Supply fundamentals

Deteriorating job prospects contributed significantly to a slowdown in

Calgary’s adult population growth—from a recent cyclical high of 4.0%

in early 2014 to a five-year low of 2.0% in July 2016.

Calgary’s 2016 Civic Census showed a net migration loss in the 12

months ending April 2016 for only the second time in the past quarter

century. Given the area’s current economic predicament, further losses

can be expected in the near term.

Demographics-related risks are rising rapidly in the Calgary area.

-2

-1

1

2

3

4

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Percentage points, Calgary

Unemployment rate relative to trailing 12-month average

Source: RBC Economics Research, Statistics Canada

0.0

1.0

2.0

3.0

4.0

5.0

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

Y/Y % change in the 15+ population, Calgary

Adult population growth

Source: RBC Economics Research, Statistics Canada

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

Units per 1,000 population, Calgary, n.s.a.

Completed and unsold units - singles and semis

Source: RBC Economics Research, Statistics Canada, Canada Mortgage and Housing Corporation

There are few signs of overbuilding of single-detached homes in Calgary.

The number of unsold single-detached and semi-detached has trended

lower after 2000 and stabilized at historically low levels since early 2015

(on a per 1000 population basis).

Despite the turbulence in the resale market, stability of the unsold inven-

tory is being achieved by drastic curtailment of new single-family home

construction. Single-family home starts plummeted by 36% last year

and were down 27% y/y in the first seven months of 2016.

Such builder restraint substantially minimizes overbuilding risks in this

category.

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

Units per 1,000 population, Calgary, n.s.a.

Completed and unsold units - multiples

Source: RBC Economics Research, Statistics Canada, Canada Mortgage and Housing Corporation

The number of unabsorbed multi-unit dwellings has surged since the

spring of 2015, albeit from extremely low levels (when Calgary arguably

had a supply shortage).

The stock of unsold units was driven higher by sharp increases in condo

apartment completions (up by 39% in 2015 and 19% year-to-date in

2016) at a time when demand turned cold.

The completed and unsold inventory recently rocketed passed the long-

term average (on a per 1000 population basis) for the area and into the

high risk zone. There is growing evidence of surplus in this segment of

the market in Calgary, which may threaten the stability of the market.

CANADIAN HOUSING HEALTH CHECK | SEPTEMBER 2016

22

Supply fundamentals

CALGARY AREA

0

1

2

3

4

5

6

7

8

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

Units per 1,000 population, Calgary, n.s.a.

Housing under construction - singles

Source: RBC Economics Research, Statistics Canada, Canada Mortgage and Housing Corporation

The dramatic scaling back of single-detached home starts contributed to

a steady decline in the number of units under construction in the past

year to historically low levels in recent months.

Such subdued levels of construction pose minimal risks of destabilizing

the market.

0

2

4

6

8

10

12

14

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Long-term average

Units per 1,000 population, Calgary, n.s.a.

Housing under construction - multiples

Source: RBC Economics Research, Statistics Canada, Canada Mortgage and Housing Corporation

There has been some moderation on the multi-unit side as well this year;

however, the level of construction remains historically elevated due to a

wave in condo starts in 2014 that continues to proceed through the con-

struction ‘pipeline’.

Current levels pose significant—albeit diminishing—risks for the market

especially in light of soft demand and high unsold inventories.

Sharp drops in condo apartment starts in 2015 (down 26%) and so far in

2016 (down 32%) suggest that further moderation is likely ahead.

The material contained in this report is the property of Royal Bank of Canada and may not be reproduced in any way, in whole or in part, without express authoriza-tion of the copyright holder in writing. The statements and statistics contained herein have been prepared by RBC Economics Research based on information from

sources considered to be reliable. We make no representation or warranty, express or implied, as to its accuracy or completeness. This publication is for the infor-

mation of investors and business persons and does not constitute an offer to sell or a solicitation to buy securities.

®Registered trademark of Royal Bank of Canada.

©Royal Bank of Canada.