Embed Size (px)

Citation preview

PRIVATE EQUITY REAL ESTATE: fundraising and structuring Baltic Real Estate Investments Forum, 2015, Vilnius Benas Poderis, Head of Investment Funds Center, ORION ASSET MANAGEMENT

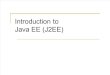

Access to Private Equity investors: what do all these have in common?

People having

money:

High Net Worth

Individuals,

corporations etc.

People (?)

money: lawyers,

tax advisers,

evaluators, other

service providers

etc.

People making money

(having RE projects /

target investments): developers, project

managers etc.

People managing

money : family

offices, asset

managers, pension

funds, insurance

companies banks etc.

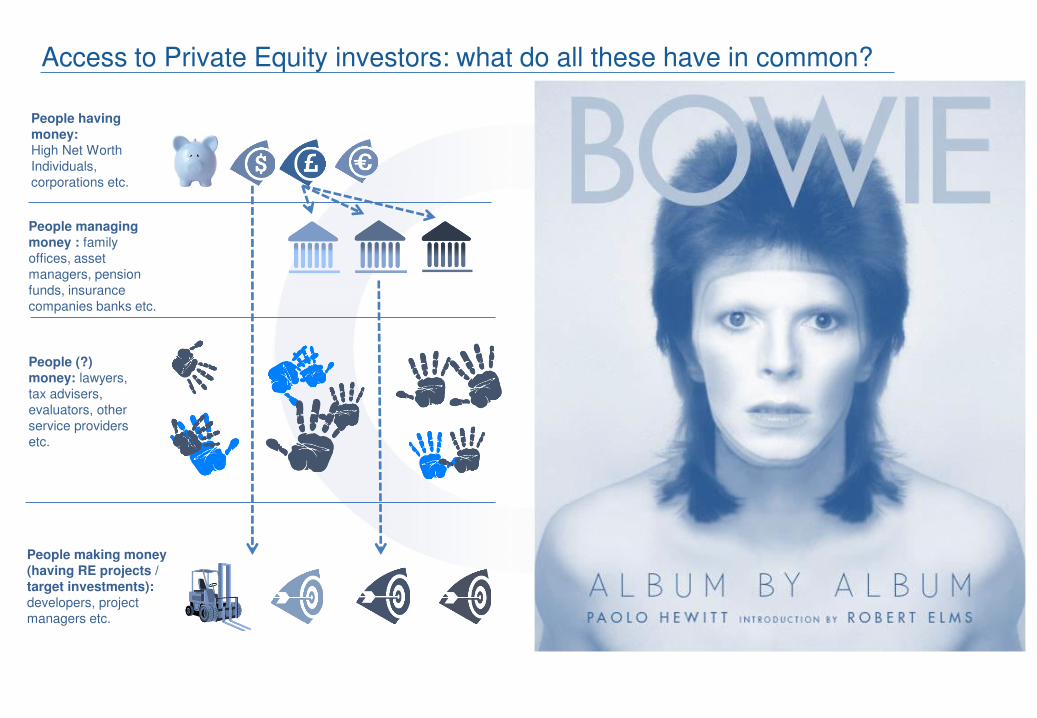

Access to Private Equity investors: securitization way to attract all

People having money: High Net Worth Individuals, corporations etc.

People making money (having RE projects / target investments):

developers, project managers etc.

People managing money : family offices, asset managers, pension funds,

insurance companies, banks etc.

IPO/SPO (listing) BONDS /

CONVERTIBLES

COLLECTIVE

INVESTMENT

SCHEMES

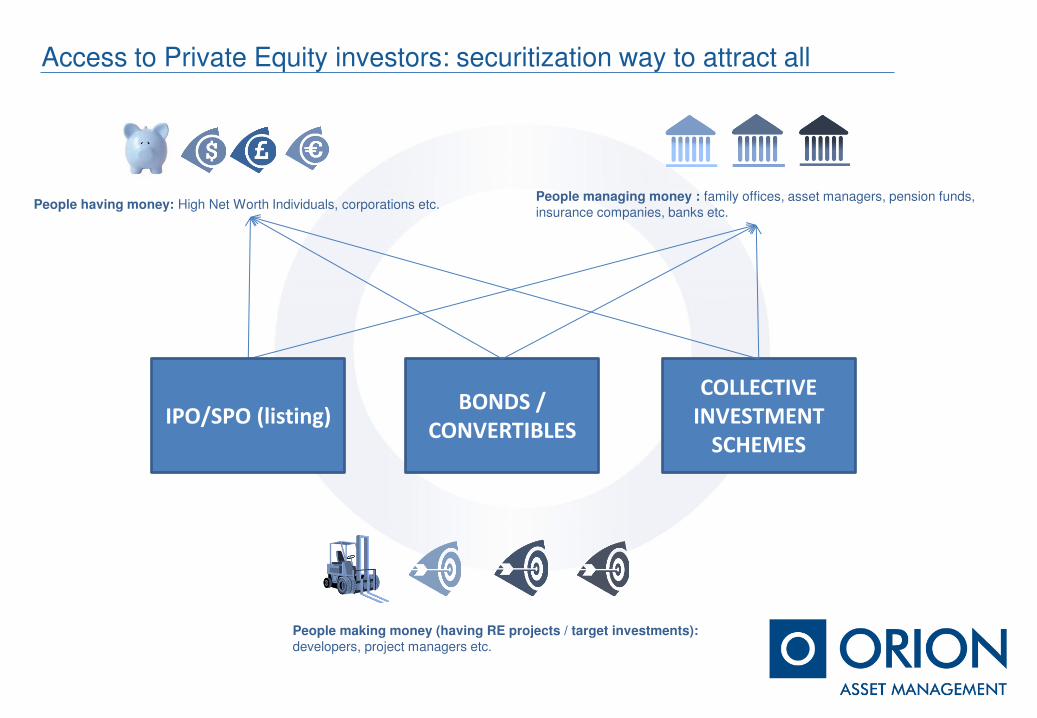

Access to Private Equity investors: simple math (Lithuania)

1 2

6 7 7

12

18

2 2 2 2 2 3 3

1 0 0 0 0 0 0

0

5

10

15

20

2009 2010 2011 2012 2013 2014 2015*

Number of financial instruments

RE Investment Funds (licensed in LT)

Listed instruments

RE private BONDS

5 5 11

23 25 28

130

0

50

100

150

2009 2010 2011 2012 2013 2014 2015*

RE Investment Funds (licensed in LT)

Listed instruments

RE BONDS

New capital raised

200 m. EUR

*expected, due to the data about funds currently raising capital or funds currently being

established

0 m. EUR 37,5 m. EUR

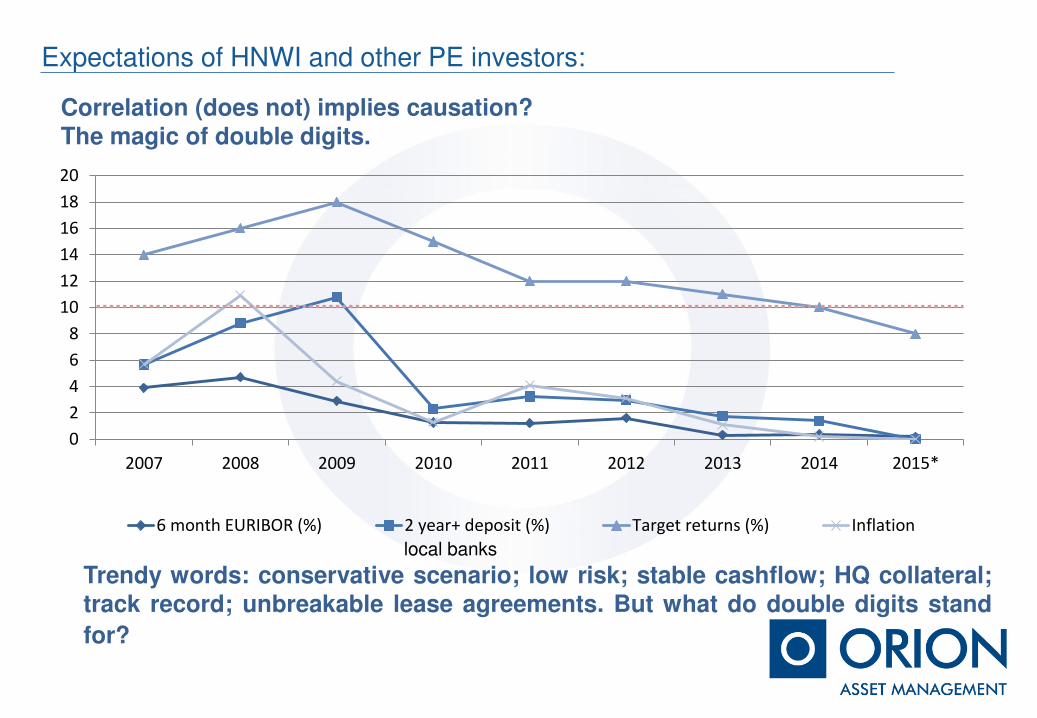

Expectations of HNWI and other PE investors:

0

2

4

6

8

10

12

14

16

18

20

2007 2008 2009 2010 2011 2012 2013 2014 2015*

6 month EURIBOR (%) 2 year+ deposit (%) Target returns (%) Inflation

Correlation (does not) implies causation? The magic of double digits.

Trendy words: conservative scenario; low risk; stable cashflow; HQ collateral; track record; unbreakable lease agreements. But what do double digits stand

for?

local banks

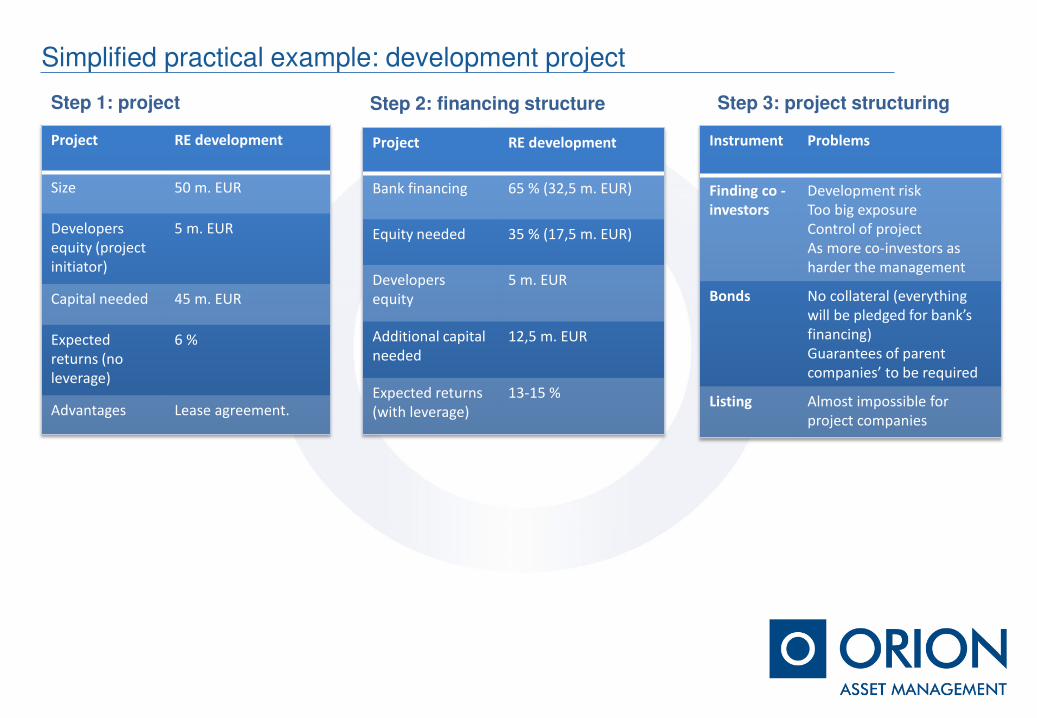

Simplified practical example: development project

Project RE development

Size 50 m. EUR

Developers

equity (project

initiator)

5 m. EUR

Capital needed 45 m. EUR

Expected

returns (no

leverage)

6 %

Advantages Lease agreement.

Step 1: project

Project RE development

Bank financing 65 % (32,5 m. EUR)

Equity needed 35 % (17,5 m. EUR)

Developers

equity

5 m. EUR

Additional capital

needed

12,5 m. EUR

Expected returns

(with leverage)

13-15 %

Step 2: financing structure Step 3: project structuring

Instrument Problems

Finding co -

investors

Development risk

Too big exposure

Control of project

As more co-investors as

harder the management

Bonds No collateral (everything

will e pledged fo a k’s financing)

Guarantees of parent

o pa ies’ to e e ui ed

Listing Almost impossible for

project companies

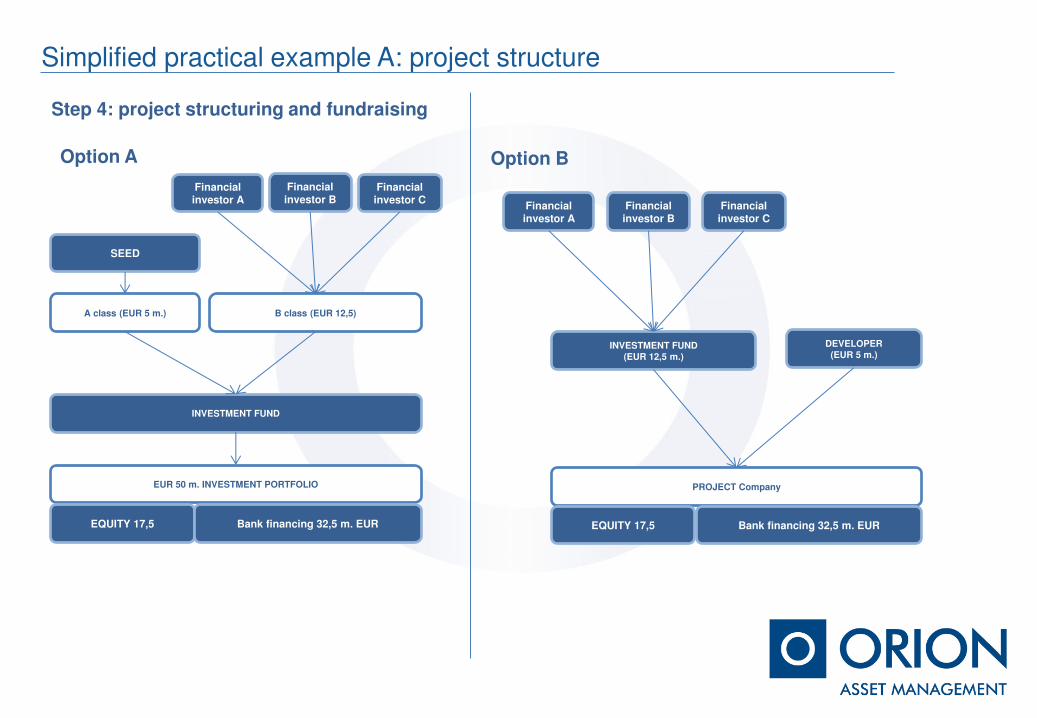

SEED

EUR 50 m. INVESTMENT PORTFOLIO

A class (EUR 5 m.) B class (EUR 12,5)

INVESTMENT FUND

EQUITY 17,5 Bank financing 32,5 m. EUR

Simplified practical example A: project structure

Financial investor B

PROJECT Company

INVESTMENT FUND

(EUR 12,5 m.)

EQUITY 17,5 Bank financing 32,5 m. EUR

DEVELOPER

(EUR 5 m.)

Financial investor C

Financial investor A

Financial investor B

Financial investor C

Financial investor A

Step 4: project structuring and fundraising

Option A Option B

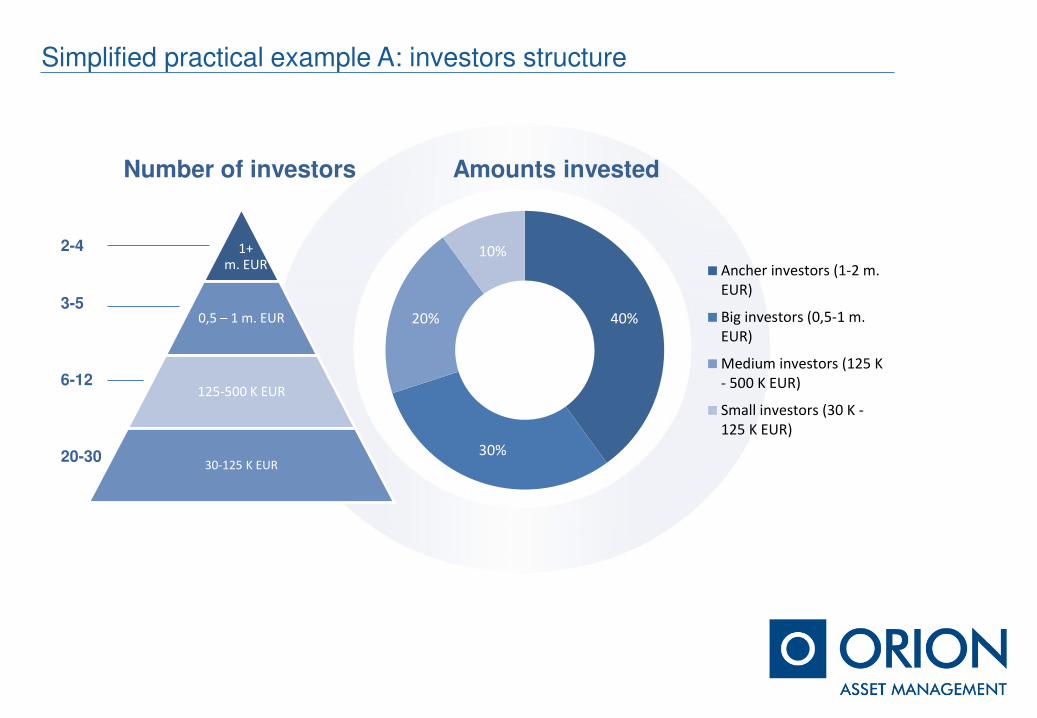

1+ m. EUR

0,5 – 1 m. EUR

125-500 K EUR

30-125 K EUR

40%

30%

20%

10%

Ancher investors (1-2 m.

EUR)

Big investors (0,5-1 m.

EUR)

Medium investors (125 K

- 500 K EUR)

Small investors (30 K -

125 K EUR)

Simplified practical example A: investors structure

Number of investors Amounts invested

2-4 3-5 6-12 20-30

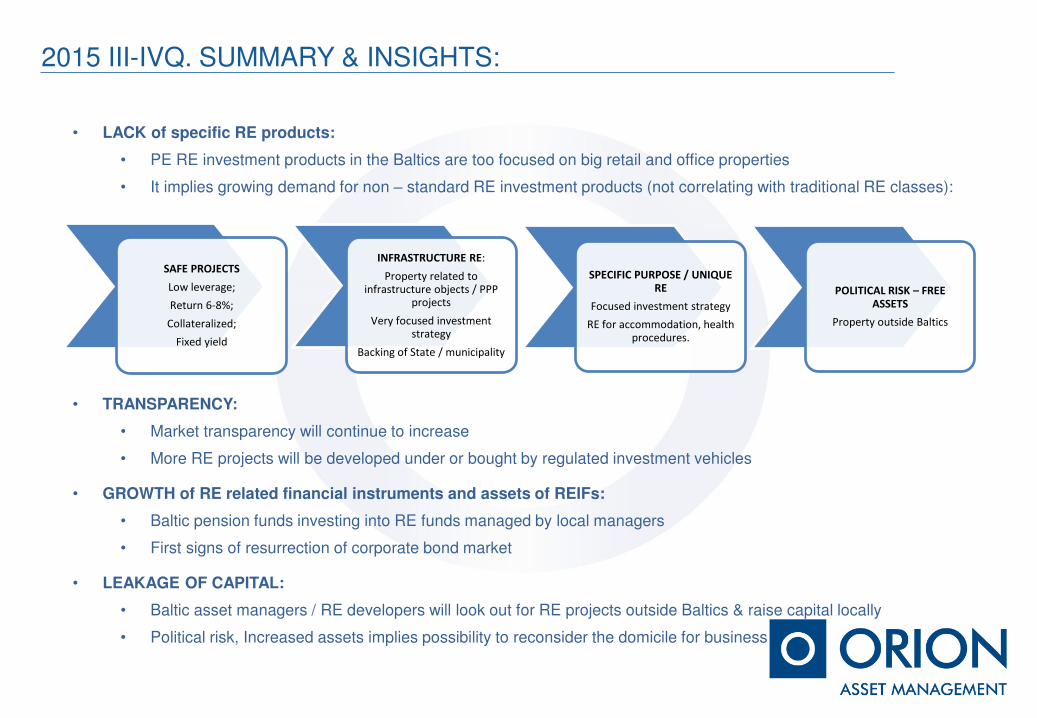

2015 III-IVQ. SUMMARY & INSIGHTS:

• LACK of specific RE products:

• PE RE investment products in the Baltics are too focused on big retail and office properties

• It implies growing demand for non – standard RE investment products (not correlating with traditional RE classes):

SAFE PROJECTS

Low leverage;

Return 6-8%;

Collateralized;

Fixed yield

INFRASTRUCTURE RE:

Property related to infrastructure objects / PPP

projects

Very focused investment strategy

Backing of State / municipality

SPECIFIC PURPOSE / UNIQUE RE

Focused investment strategy

RE for accommodation, health procedures.

POLITICAL RISK – FREE ASSETS

Property outside Baltics

• TRANSPARENCY:

• Market transparency will continue to increase

• More RE projects will be developed under or bought by regulated investment vehicles

• GROWTH of RE related financial instruments and assets of REIFs:

• Baltic pension funds investing into RE funds managed by local managers

• First signs of resurrection of corporate bond market

• LEAKAGE OF CAPITAL:

• Baltic asset managers / RE developers will look out for RE projects outside Baltics & raise capital locally

• Political risk, Increased assets implies possibility to reconsider the domicile for business

THANK YOU FOR YOUR ATTENTION

Benas Poderis

Head of Investment Funds Center

A.Tumeno str. 4, Vilnius, Lithuania

www.orion.lt