Embed Size (px)

Citation preview

11/5/2012 1

November 2012

Revenge of the men in grey suits…

And some reasons to be cheerful…

Stuart Hicks BSc (Hons) MRICS IRRV (Hons)

Director, Dunlop HeywoodEmail: [email protected]

Tel: 0161 817 4844

Member 1992 : Royal Institution of Chartered SurveyorsMember : Rating Surveyors Association & Town Panel ChairmanFormer Chairman : British Retail Consortium Rating Panel (NW)

Recognised as a leading rating advisor across the UK in respect of various categories of specialist property and in empty rates liability.

www.dunlopheywood.com

Who am I ?

11/5/2012 2

Agenda

1. Business Rates – what are they?

2. Rateable Value – what is it?

3. The Valuation Date – controversy!

4. The Economy – over supply & empty property.

5. Empty Property Rates & Mitigation – Evasion or Avoidance?

And finally...

7. Postponement of the 2015 Revaluation

Business Rates – What Are They?

1. Business Rates are a charge on the occupation of commercial

property; a tax. But from the 1960’s the owner became liable if certain

classes of property were left vacant.

2. The ratepayer is either the occupier or the owner of the property.

3. Central Government collects all business rates from Local Authorities.

4. Local Authorities fund services from Council Tax, Fees & Charges and

a Central Government Grant.

5. The Central Government Grant includes redistributed Business Rates.

6. Central Government determines how much Local Authorities can

spend and distributes taking account of the level of need and resource.

11/5/2012 3

Business Rates – The Times, They Are A Changing!

1. A new retention scheme is being delivered through the Local Government

Finance Bill and will be implemented from April 2013.

2. The retention scheme allows Local Authorities to retain a proportion of Business

Rates as well as any growth in same.

3. There are 24 new Enterprise Zones in England;

• Rate Relief will be funded by Central Government (£275k over 5

years).

• 100% business rates retention.

4. Will Local Authorities become more aggressive in the collection of business

rates and in their relationship with the Valuation Office Agency?

5. Business rates deferral scheme for 2012/13 similar to 2009/10 scheme.

Rateable Value – What Is It?

1. The measure or yardstick for business rates liability is rateable value.

The definition is prescribed in Schedule 6 paragraph 2(1) before

amendment by the Rating (Valuation) Act 1999:

‘The rateable value of a non-domestic hereditament shall be taken to be

an amount equal to the rent at which it is estimated the hereditament

might reasonably be expected to let from year to year if the tenant

undertook to pay all usual tenant’s rates and taxes and to bear the costs

of the repairs and insurance and other expenses (if any) necessary to

maintain the hereditament in a state to command that rent’

11/5/2012 4

2010 Rating List – Valuation Date 1 April 2008

11/5/2012 5

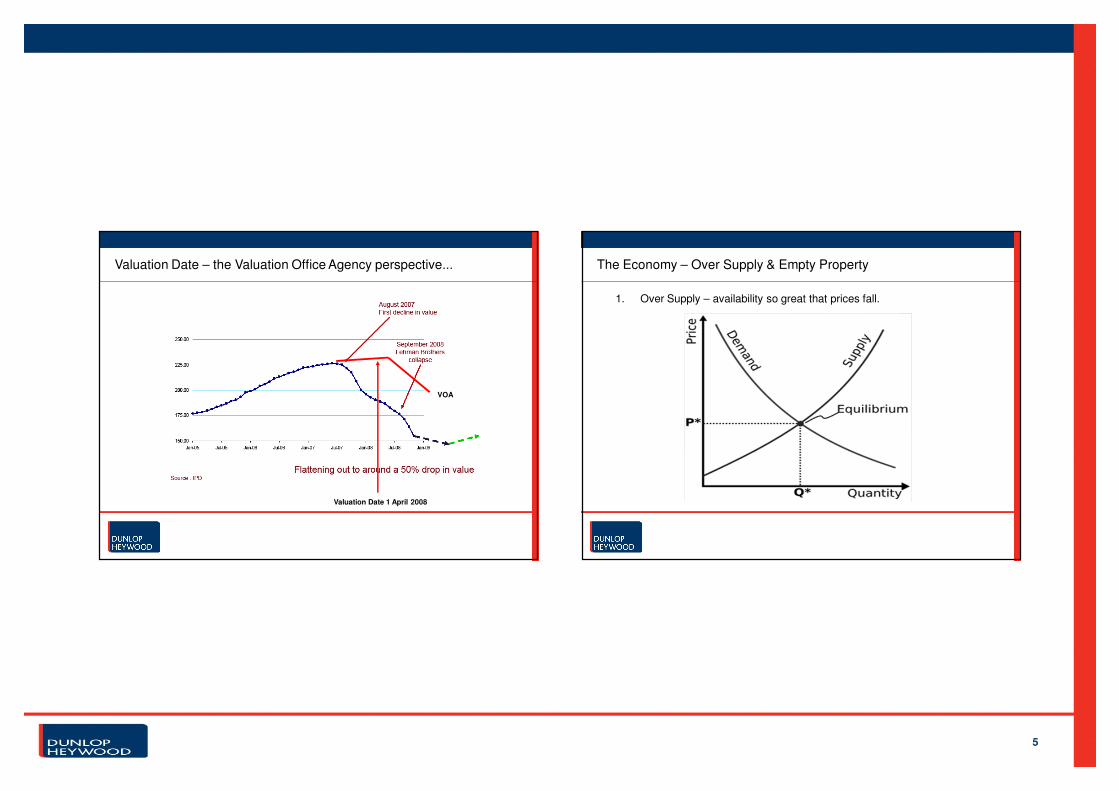

Valuation Date – the Valuation Office Agency perspective...

Valuation Date 1 April 2008

VOA

The Economy – Over Supply & Empty Property

1. Over Supply – availability so great that prices fall.

11/5/2012 6

The Economy – Over Supply & Empty Property

1. Appeals - remember the Valuation Date!

2. All rating valuations need to be framed within the economic context of 1

April 2008.

3. The economic context will differ by sector and by location; e.g. financial

services.

4. To appeal we need to identify a change in the physical state or use and

occupation at the relevant date.

5. Vacancy rather than availability.

• Change in the level of occupancy.

• Building or availability of new space.

Empty Property Rates & Mitigation – Evasion or Avoidance?

1. Up to April 2008 50% business rates payable on empty shops and

offices; 0% payable on industrials and warehousing.

2. In 2008 compulsory 100% exemptions changed.

3. After initial 3 months (commercial property) or 6 months (industrial

property) 100% relief full business rates are payable unless the

rateable value is less than £2,600.

4. Is it about revenue or encouraging use?

5. What effect will the new retention scheme have?

11/5/2012 7

Empty Property Rates & Mitigation – Evasion or Avoidance?

1. Inland Revenue Commissioners v Duke of Westminster 1936

• Lord Tomlin “Every man is entitled if he can to organise his

affairs so as the tax attaching under the appropriate Acts is

less than it otherwise would be”

• Lord Atkin “the subject...has the legal right to dispose of his

capital and income as to attract...the least amount of tax”

2. WT Ramsey Ltd v Inland Revenue Commissioners 1982

• Where a transaction has pre-arranged artificial steps which

serve no commercial purpose other than to save tax, then the

proper approach is to tax the transaction as a whole.

Empty Property Rates & Mitigation – Evasion or Avoidance?

1. Furniss (Inspector of Taxes) v Dawson D.E.R. Furniss v Dawson G.E.

Murdoch v Dawson R.S. 1984

• Steps inserted in a preordained series of transactions with no

commercial purpose other than tax avoidance should be

disregarded for tax purposes; notwithstanding that the inserted

step has a business effect.

2. Extension to the Ramsey Principle.

3. The Westminster Principle establishes the right to minimise tax and the

Ramsey Principle allows for artificial financial transactions to be

ignored.

11/5/2012 8

Empty Property Rates & Mitigation – Evasion or Avoidance?

1. The law is dynamic and in this area the law is evolving.

2. Most mitigation schemes rely on a 6 week period of occupation

(following which the relevant period of rates relief applies) or

exemption.

3. Case law exists on what constitutes occupation. There are four

elements:

• There must be ACTUAL occupation.

• It must be EXCLUSIVE to the occupier.

• It must be BENEFICIAL to the occupier.

• It must not be for too TRANSIENT a period.

Empty Property Rates & Mitigation – Occupation

1. There is nothing in the Regulations that prevents a ratepayer from repeatedly

occupying fro 6 week periods to claim repeated periods of relief.

2. Makro Properties Ltd and Makro Self Service Wholesalers Ltd v Nuneaton and

Bedworth BC 2012

• Storing 16 pallets of documents.

• Occupied 0.2% of 140,000 sqft

3. Judge Jarman said “It has been recognised for a considerable amount of time

that ratepayers...can and do organise their affairs to avoid paying rates. In

Gage, Alverstone CJ dealt with this question and stated that if the ratepayer

thought that she would not be within the charging act by going out of

possession, she was quite entitled to do so. In my judgement the same applies

to going in and out of occupation.

11/5/2012 9

Empty Property Rates & Mitigation – Blue Tooth

1. The installation of a small electronic box broadcasting messages on blue tooth.

2. Various Magistrates Court Decisions including Chester and West Cheshire

Council v Public Safety Charitable Trust 2012

• District Judge NPM Sanders held that PSCT was in occupation.

3. As PSCT are a registered charity and the messages broadcast were of a

charitable nature; it was further determined that the ratepayer was entitled to

80% mandatory rate relief.

4. Local Authority to appeal along with two other similar cases.

Empty Property Rates & Mitigation – Charity

1. Charities benefit from a mandatory 80% relief and the remaining 20% liability

can be cancelled by a Local Authority on a discretionary basis.

2. Further the Local Government Finance Act 1988 S.45a(2) provides that empty

properties are zero rated where;

• The ratepayer is a charity and;

• It appears that when next in use the hereditament will wholly or mainly

be used for charitable purposes.

3. In Preston City Council v Oyston Angel Charity 2012 relief was confirmed and

further that the intention to occupy did not have to be by the ratepayer charity.

11/5/2012 10

Empty Property Rates & Mitigation – Liquidation

1. If your property falls into one of the following you will be exempt from paying

business rates:

• A property where the owner is bankrupt.

• A property where the owner is entitled to possession as a liquidator.

• A property whose owner is a company in administration.

• A property whose owner is a company subject to a winding up order.

2. Some of the more ambitious mitigation schemes push the boundaries of the

law.

3. In such cases the Insolvency Service may consider taking action against

Company Directors.

4. How will the new retention scheme change things?

Empty Property Rates & Mitigation – Liquidation

1. Method:

1. Company set up with share capital of £100.

2. Signs leases for property at £1 rent.

3. Makes a declaration of solvency.

4. This enables the company to enter a Members Voluntary Liquidation.

5. Liability for rates remains with the company in liquidation i.e. exempt.

2. Because there are no creditors to press for winding up exemption remains.

3. The Insolvency Service recently wound up 13 companies in the public interest.

Commenting on the case Investigation Supervisor, Alex Deane said;

“In making the decision to wind up these companies, the court is sending a clear

message that schemes which abuse the insolvency regime to avoid paying

business rates liabilities are not acceptable.”

11/5/2012 11

Postponement of the 2015 Revaluation

1. The Government has announced its intention to postpone the next business

rates revaluation in England to 2017.

2. Since the last Revaluation based upon 2008 rents, the economy and property

market has been subject to exceptional changes.

3. If the Revaluation went ahead the valuation date would be 1 April 2013.

4. For the 2015 Rating List to be put in place a draft List would have to be

published in October 2014.

5. The General Election date is fixed as 15 May 2015. So postponing removes a

very contentious element from campaigning; rateable value shifts.

6. How would your rateable value change? How would rateable values change in

the North East, North West, Yorkshire and the Midlands?

Postponement of the 2015 Revaluation

7. Most Conservative seats are in the South which would see the biggest

increases in rateable value along with a likely increase in the UBR.

8. Similar ‘chickening out’ by Labour when they cancelled the Council Tax

revaluation due in 2007; another political ‘hot potato’.

9. Business Rates Information Letter (9/2012)

“The Government is committed to maintaining up to date rate bills through

regular five yearly revaluations in England which will resume after 2017, once

the economy has had a chance to recover fully from the financial and fiscal crisi

this Government inherited from the last Administration”

11/5/2012 12

‘Complex problems often have quick,

easy to understand, wrong answers’