Embed Size (px)

Citation preview

CHENNAIRESIDENTIAL & OFFICEJULY TO DECEMBER 2017

2

RESIDENTIAL RECAP H1 2017

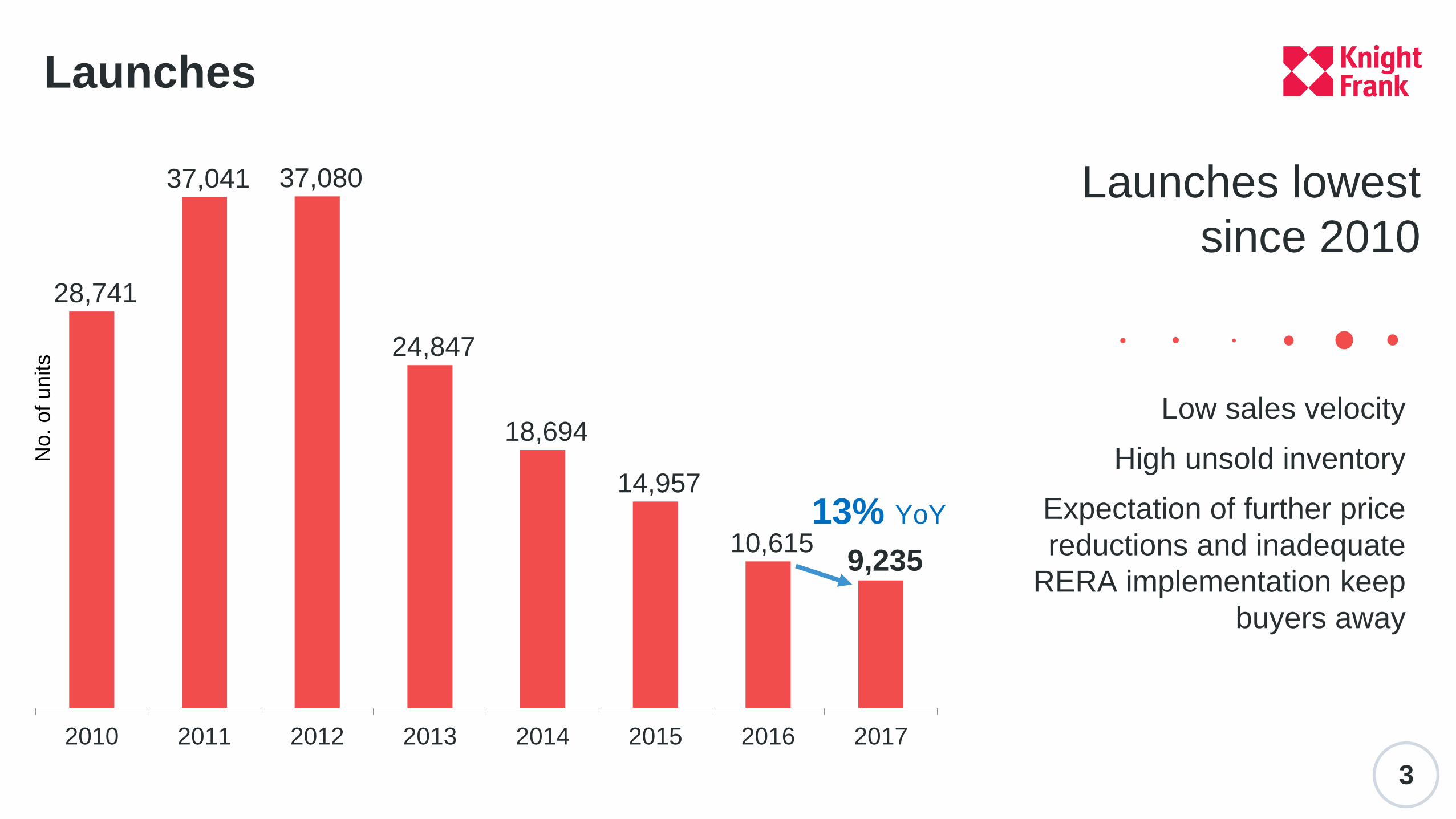

Low sales velocity

High unsold inventory

Expectation of further price

reductions and inadequate

RERA implementation keep

buyers away

3

28,741

37,041 37,080

24,847

18,694

14,957

10,615 9,235

2010 2011 2012 2013 2014 2015 2016 2017

13% YoY

Launches

Launches lowest

since 2010

No. o

f units

4

11,377

7,317

9,102

5,855 5,815

4,800

6,035

3,200

H1 2014 H2 2014 H1 2015 H2 2015 H1 2016 H2 2016 H1 2017 H2 2017

33% YoY

Lacklustre demand

discouraged additional

supply; 33% drop YoY

Half-yearly launches

Developers focus on liquidating

current inventory load

No. o

f units

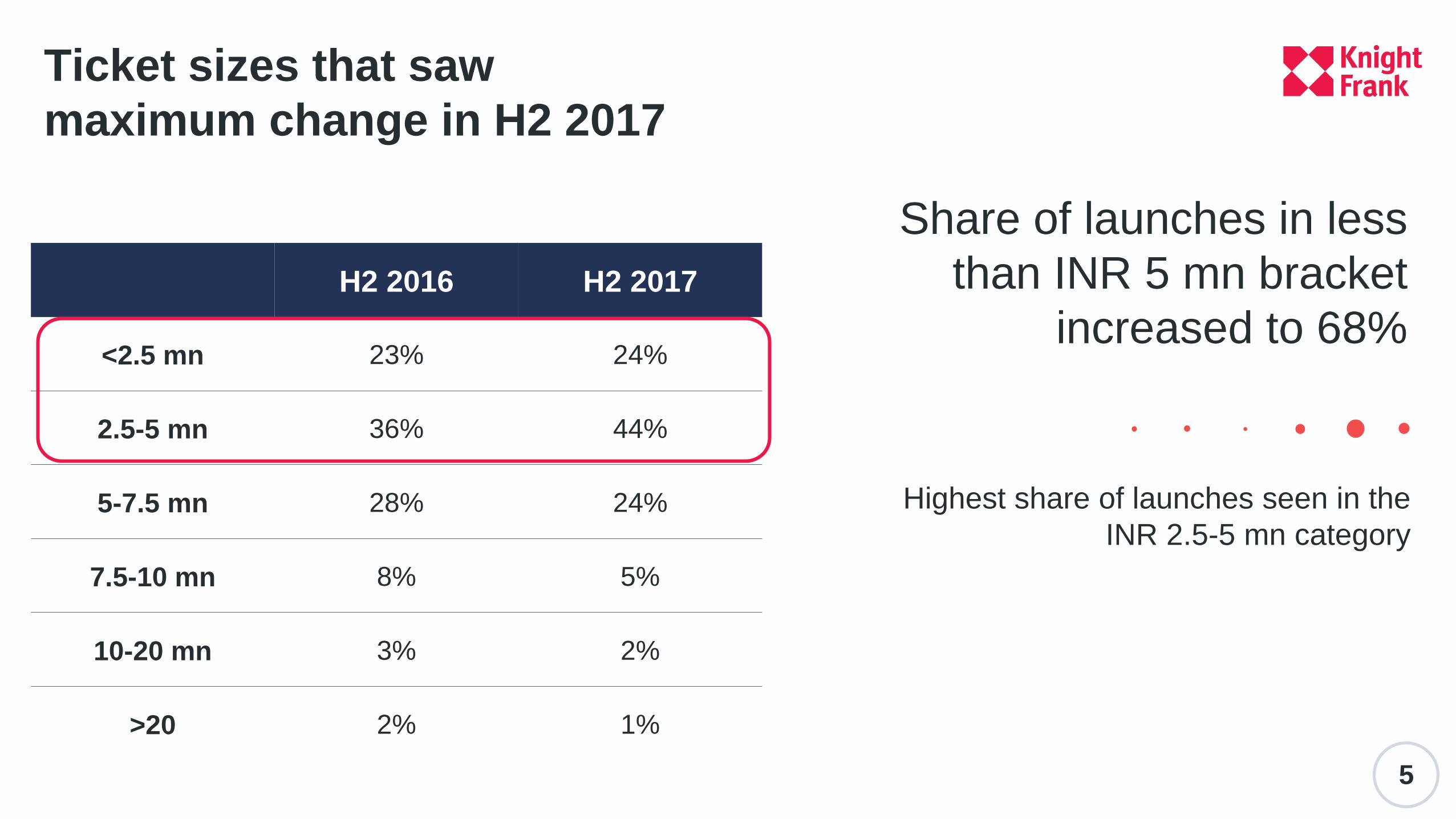

Highest share of launches seen in the

INR 2.5-5 mn category

5

H2 2016 H2 2017

<2.5 mn 23% 24%

2.5-5 mn 36% 44%

5-7.5 mn 28% 24%

7.5-10 mn 8% 5%

10-20 mn 3% 2%

>20 2% 1%

Ticket sizes that saw

maximum change in H2 2017

Share of launches in less

than INR 5 mn bracket

increased to 68%

Demand weak as buyers

continue to wait and watch

RERA still to be applied in

letter and spirit

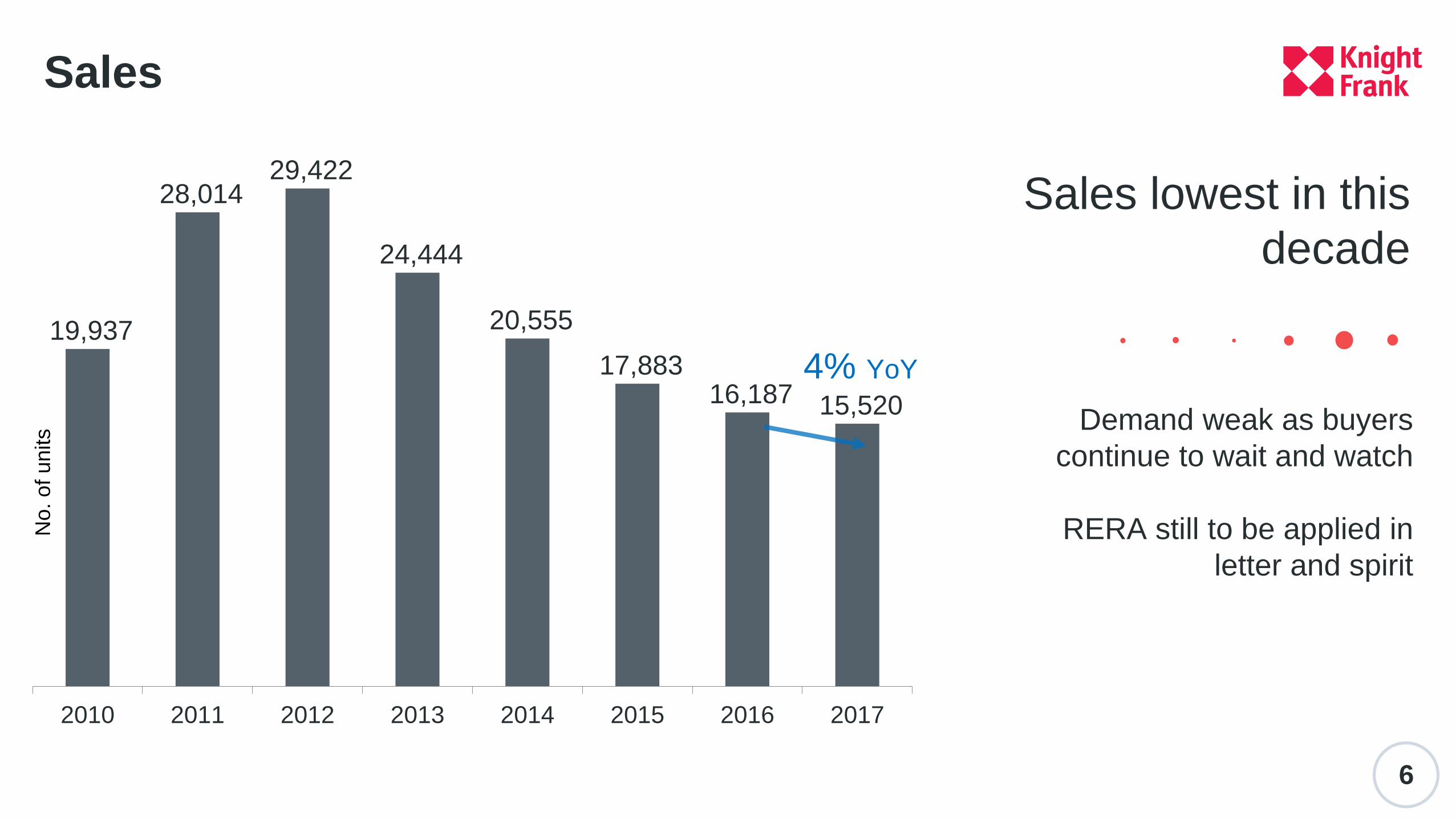

6

19,937

28,014 29,422

24,444

20,555

17,883 16,187 15,520

2010 2011 2012 2013 2014 2015 2016 2017

4% YoY

Sales

Sales lowest in this

decade

No. o

f units

H2 2017 shows similar trend

as demand fell 14% YoY

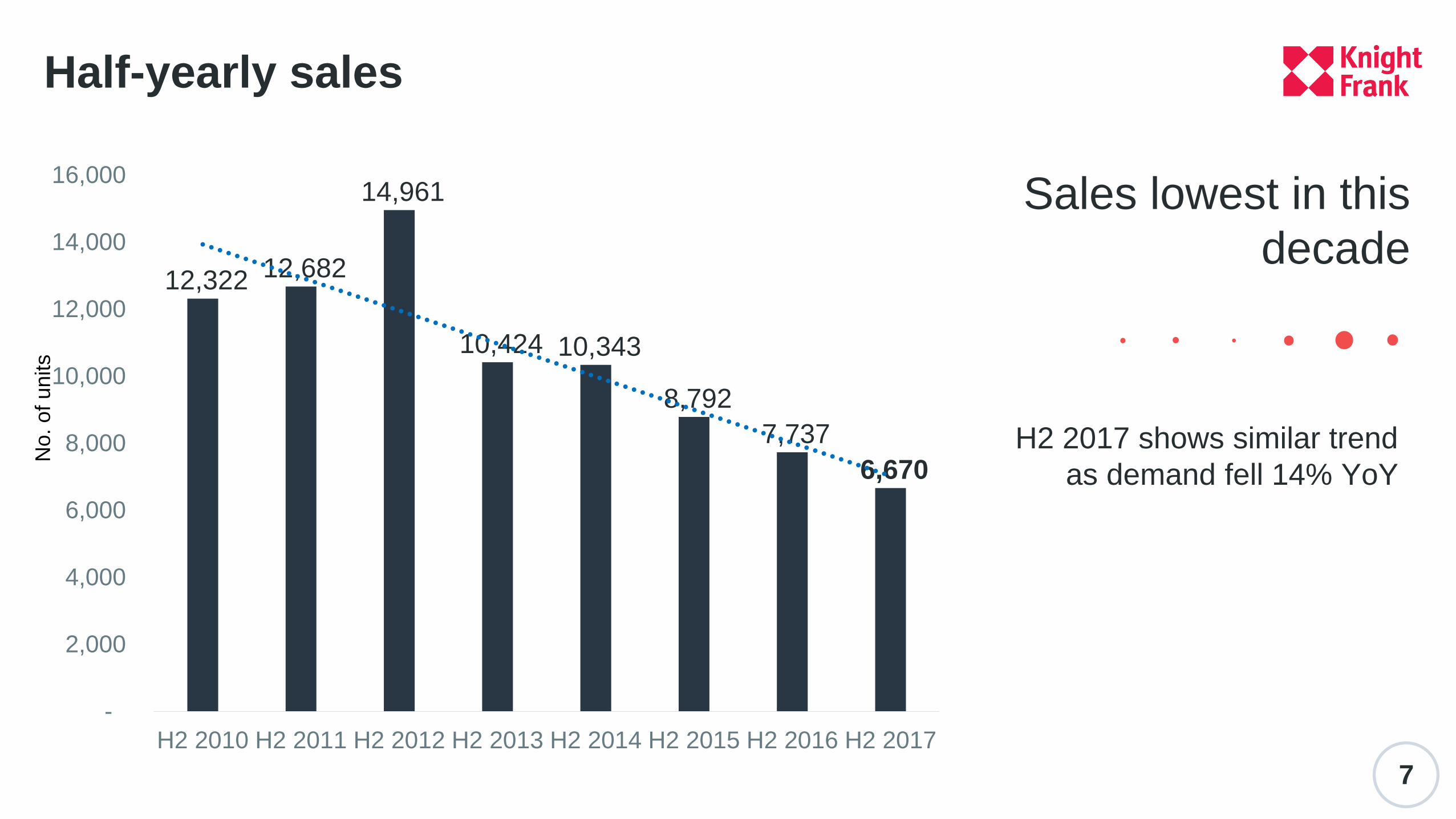

7

Half-yearly sales

Sales lowest in this

decade12,322 12,682

14,961

10,424 10,343

8,792

7,737

6,670

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

H2 2010 H2 2011 H2 2012 H2 2013 H2 2014 H2 2015 H2 2016 H2 2017

No. o

f units

3% decline YoY

in prices

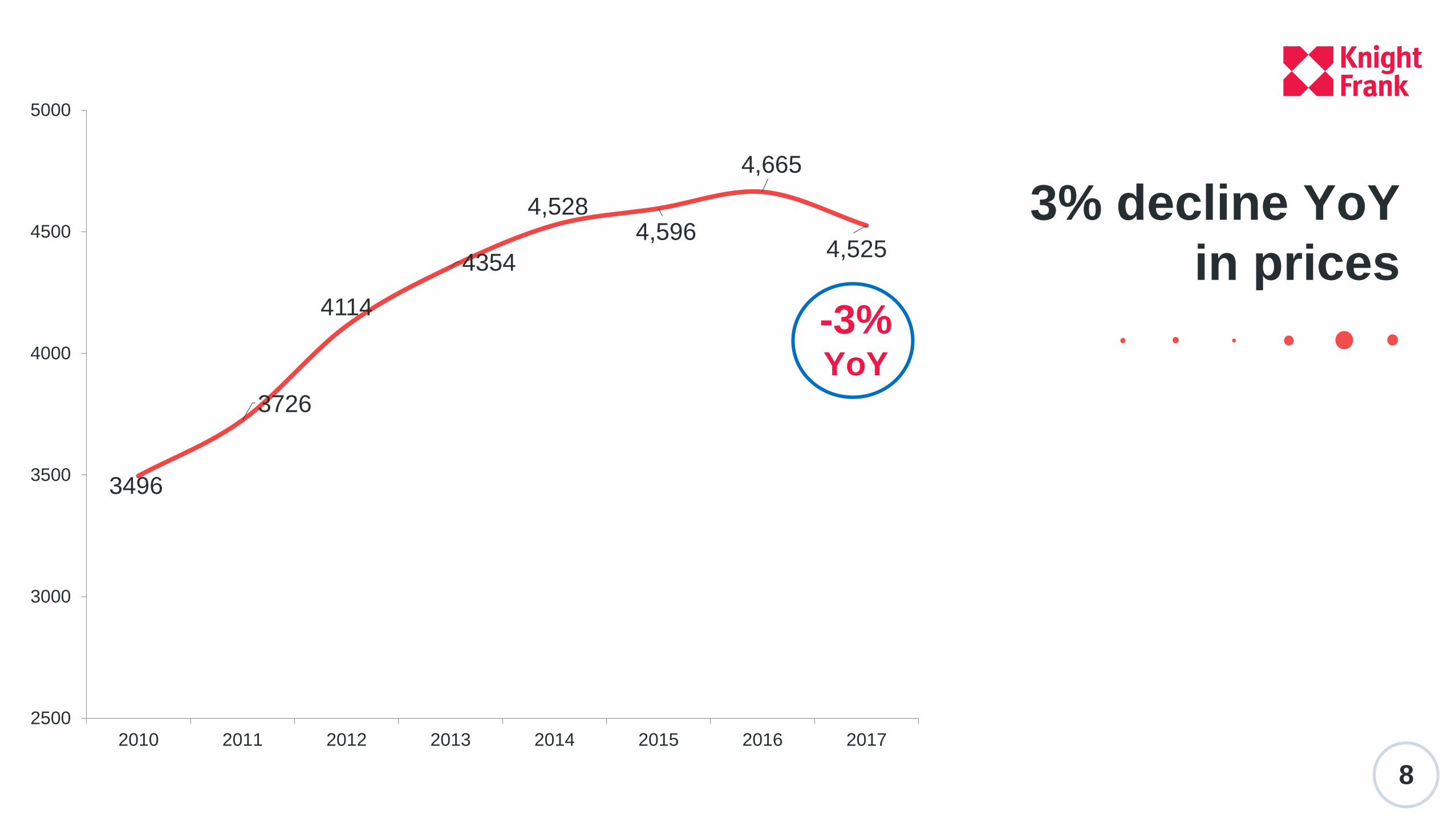

8

3496

3726

4114

4354

4,528 4,596

4,665

4,525

2500

3000

3500

4000

4500

5000

2010 2011 2012 2013 2014 2015 2016 2017

-3%YoY

70

80

90

100

110

120

130

140

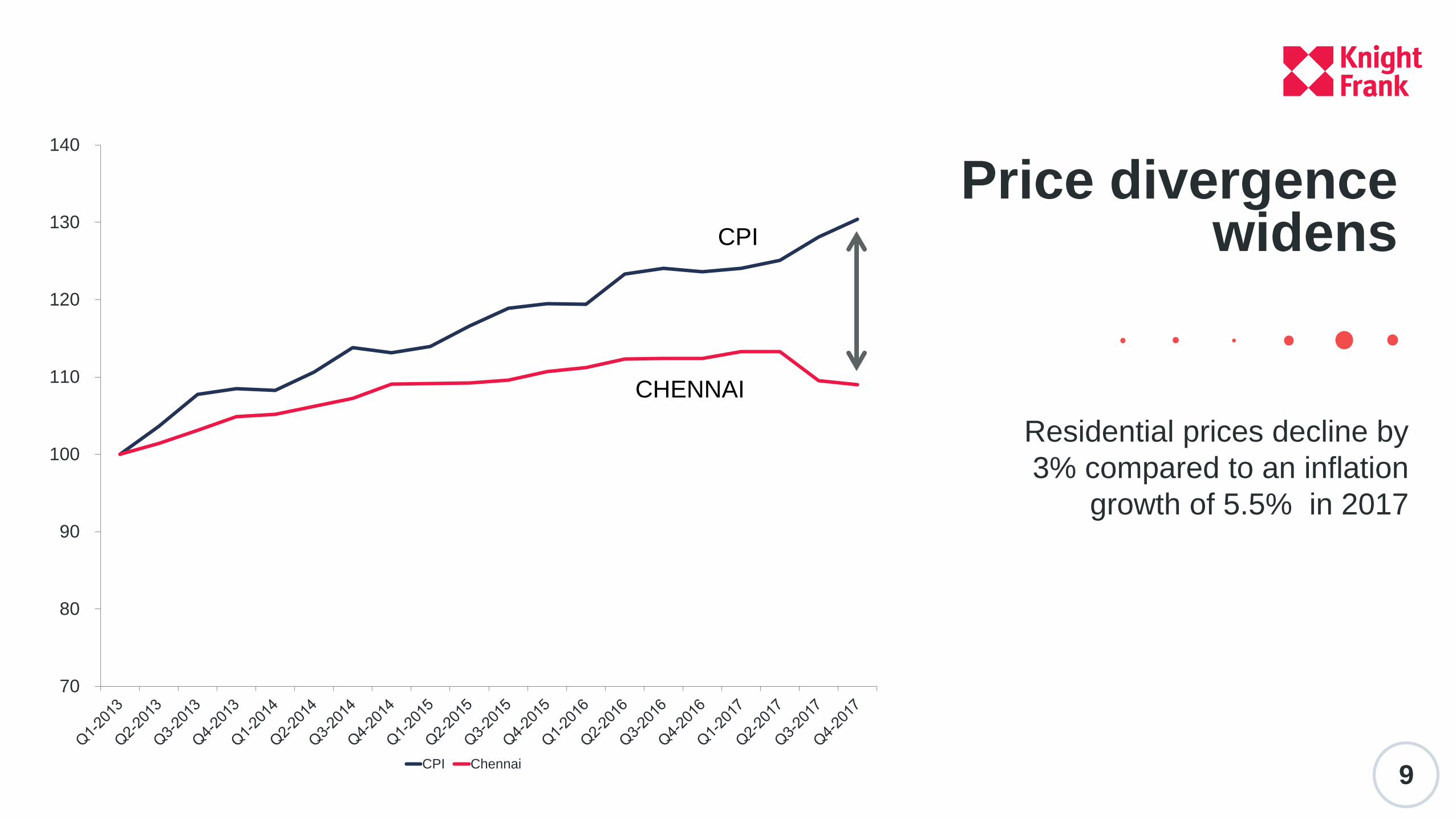

CPI Chennai

Residential prices decline by

3% compared to an inflation

growth of 5.5% in 2017

Price divergence widens

9

CPI

CHENNAI

10

Chennai is nearly touching the

Knight Frank Affordability

Benchmark* of

4.5

(*house price to income ratio)

2017

4.72010

5.4

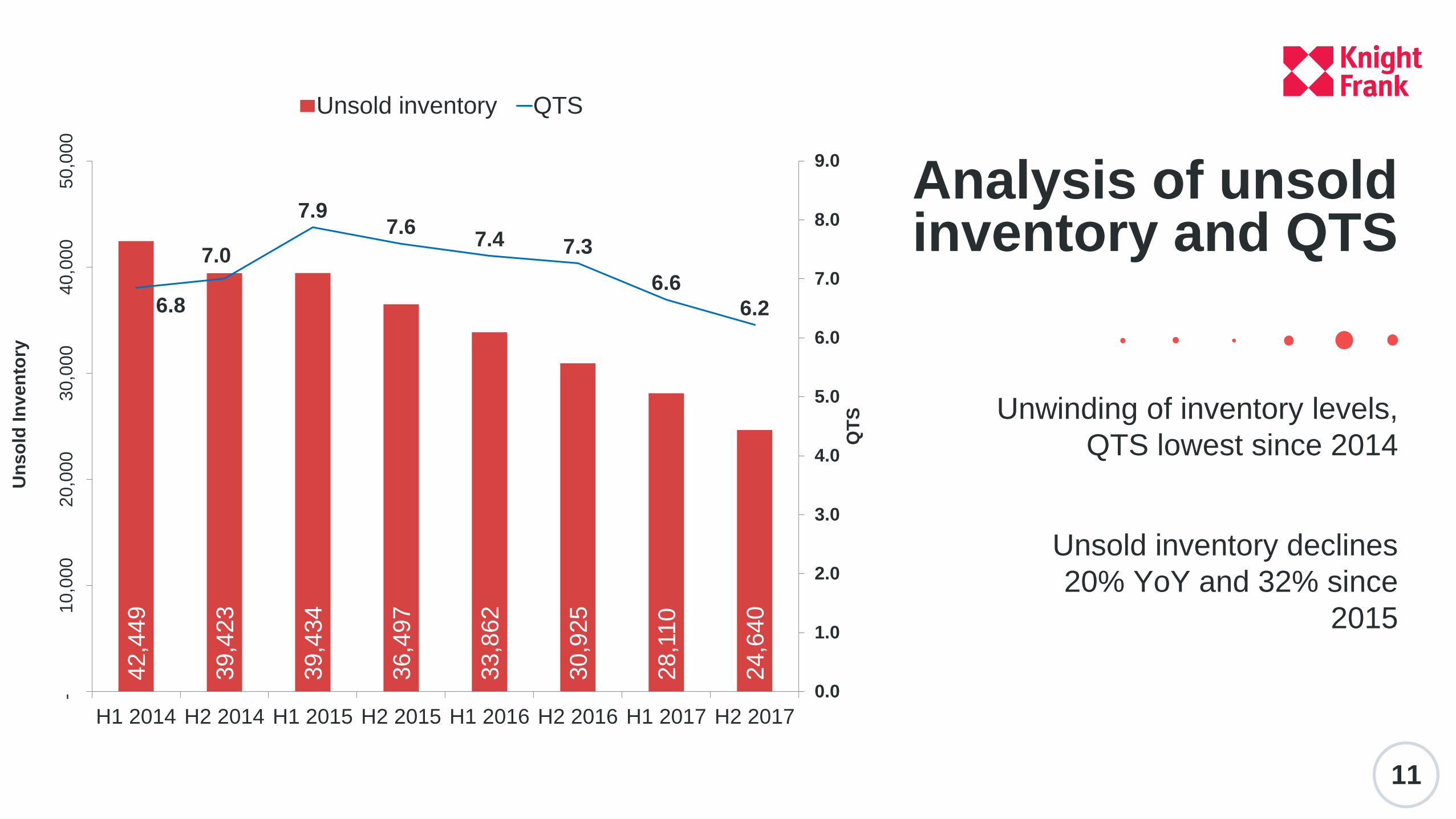

Unwinding of inventory levels,

QTS lowest since 2014

Unsold inventory declines

20% YoY and 32% since

2015

Analysis of unsold inventory and QTS

11

42,4

49

39,4

23

39,4

34

36,4

97

33,8

62

30,9

25

28,1

10

24,6

40

6.8

7.0

7.97.6

7.4 7.3

6.6

6.2

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

- 1

0,0

00

20,0

00

30,0

00

40,0

00

50,0

00

H1 2014 H2 2014 H1 2015 H2 2015 H1 2016 H2 2016 H1 2017 H2 2017

QT

S

Un

so

ld In

ven

tory

Unsold inventory QTS

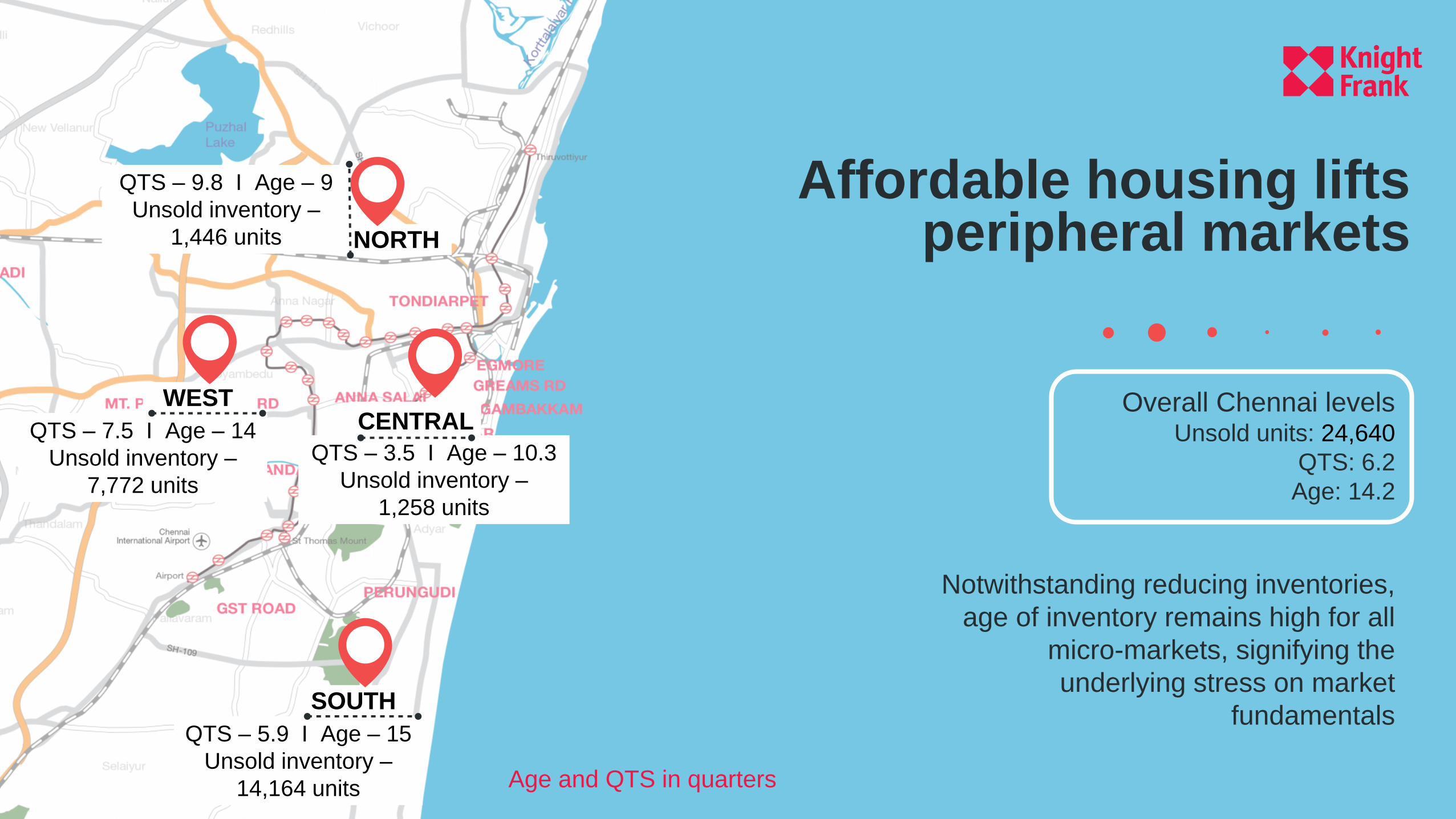

Affordable housing lifts peripheral markets

QTS – 9.8 I Age – 9

Unsold inventory –

1,446 units NORTH

QTS – 7.5 I Age – 14

Unsold inventory –

7,772 units

WEST

QTS – 5.9 I Age – 15

Unsold inventory –

14,164 units

SOUTH

QTS – 3.5 I Age – 10.3

Unsold inventory –

1,258 units

CENTRALOverall Chennai levels

Unsold units: 24,640

QTS: 6.2

Age: 14.2

Notwithstanding reducing inventories,

age of inventory remains high for all

micro-markets, signifying the

underlying stress on market

fundamentals

Age and QTS in quarters

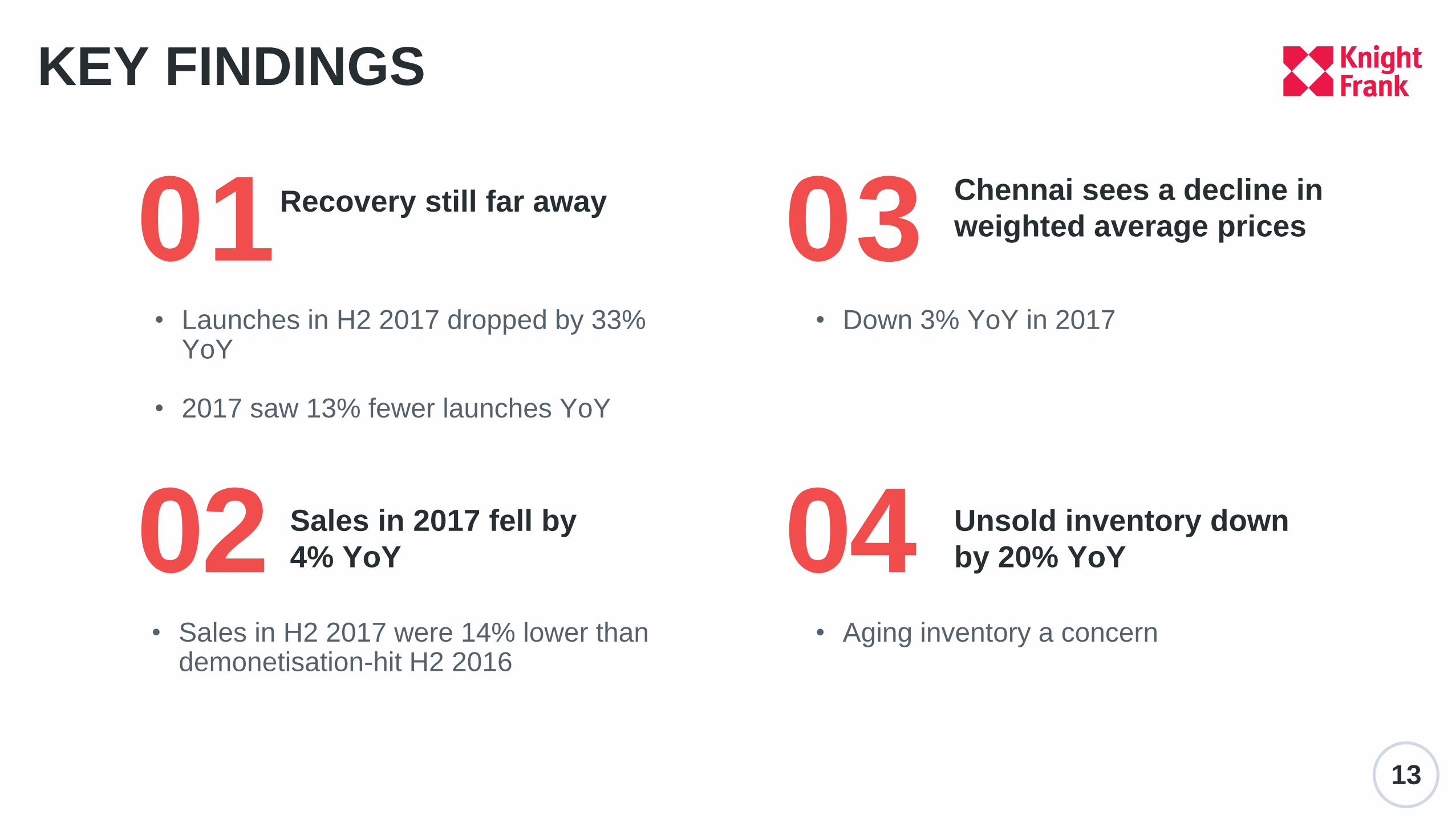

KEY FINDINGS

13

01 03

02 04

Recovery still far away Chennai sees a decline in

weighted average prices

• Down 3% YoY in 2017

Unsold inventory down

by 20% YoY

• Aging inventory a concern

Sales in 2017 fell by

4% YoY

• Sales in H2 2017 were 14% lower than demonetisation-hit H2 2016

• Launches in H2 2017 dropped by 33% YoY

• 2017 saw 13% fewer launches YoY

14

Supply crunch made office

vacancies plummet

IT/ITeS and manufacturing

share narrowed

OFFICE RECAP H1 2017

Vacancy continues

downtrend

15

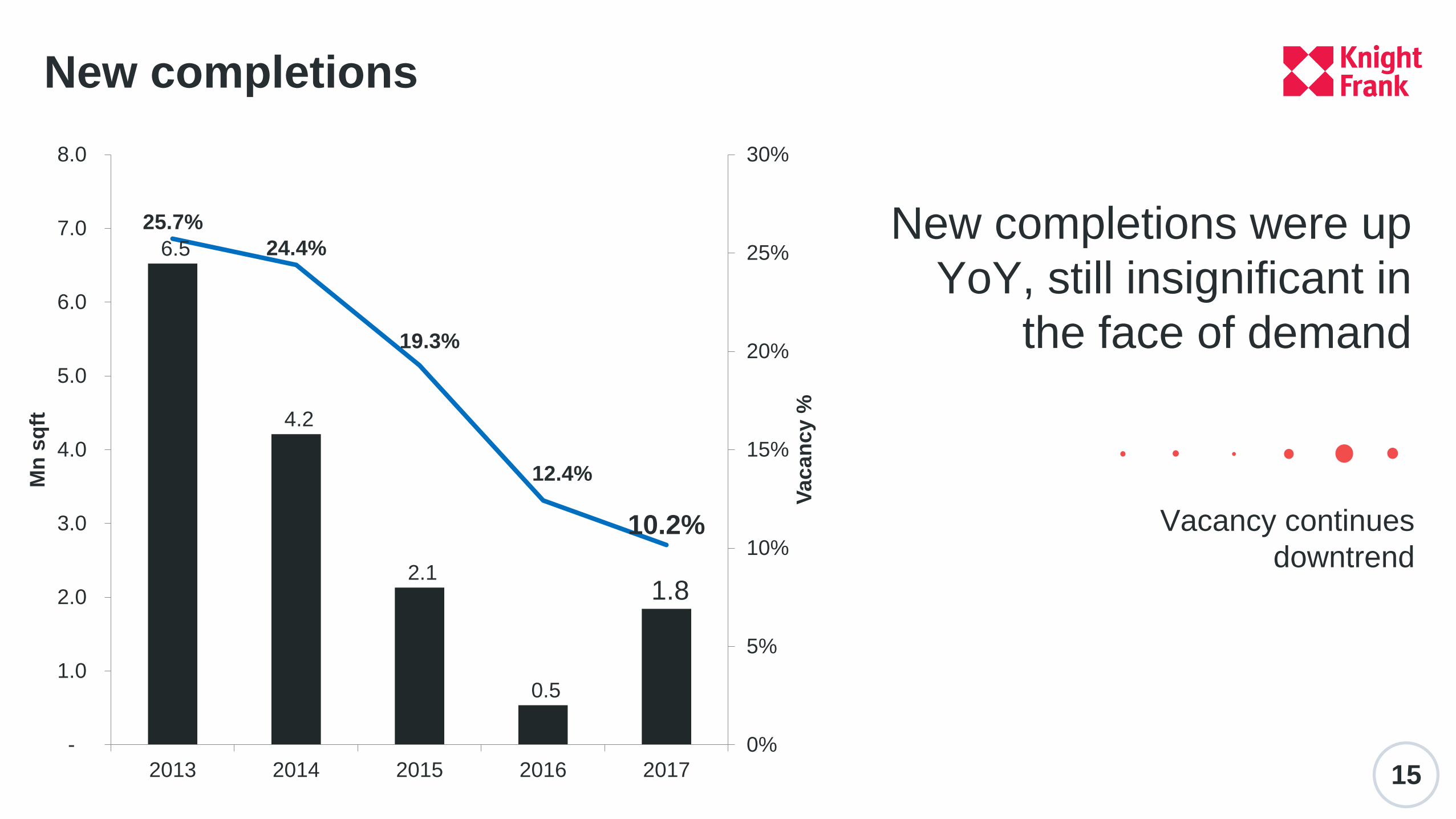

6.5

4.2

2.1

0.5

1.8

25.7%

24.4%

19.3%

12.4%

10.2%

0%

5%

10%

15%

20%

25%

30%

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

2013 2014 2015 2016 2017

Vac

an

cy %

Mn

sq

ft

New completions

New completions were up

YoY, still insignificant in

the face of demand

16

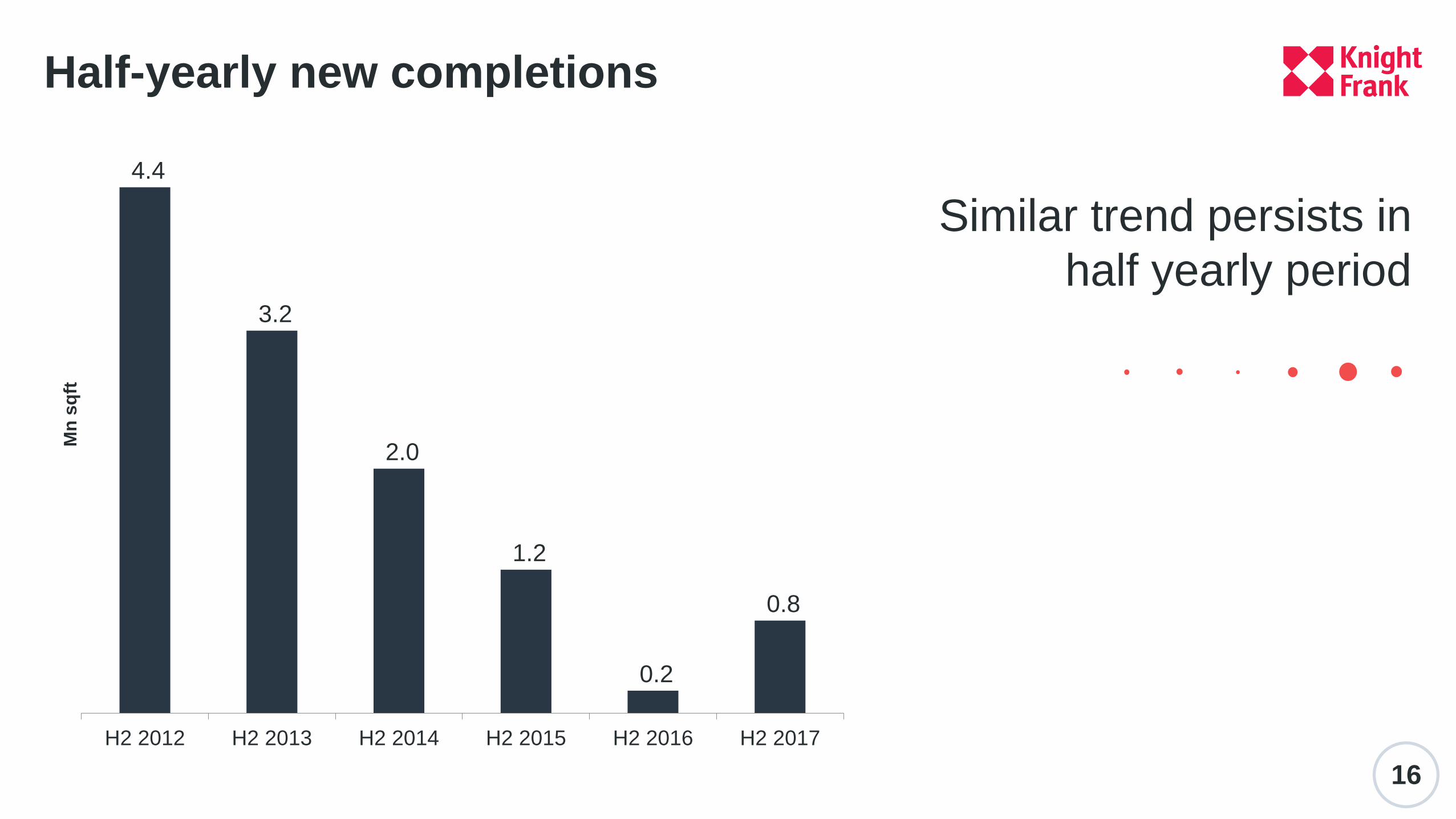

4.4

3.2

2.0

1.2

0.2

0.8

H2 2012 H2 2013 H2 2014 H2 2015 H2 2016 H2 2017

Mn

sq

ftHalf-yearly new completions

Similar trend persists in

half yearly period

17

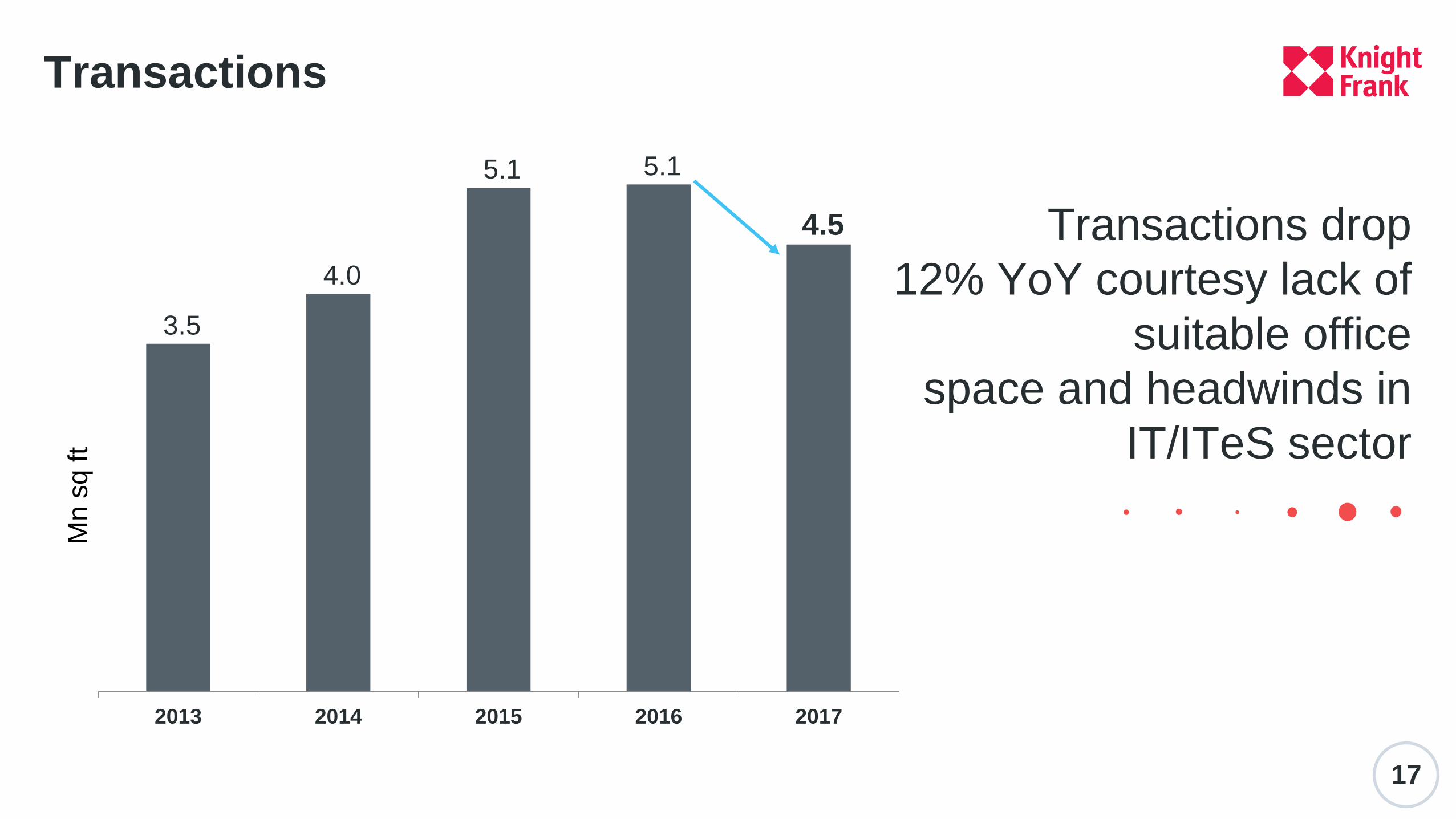

3.5

4.0

5.1 5.1

4.5

2013 2014 2015 2016 2017

Transactions

Transactions drop

12% YoY courtesy lack of

suitable office

space and headwinds in

IT/ITeS sector

Mn

sq

ft

18

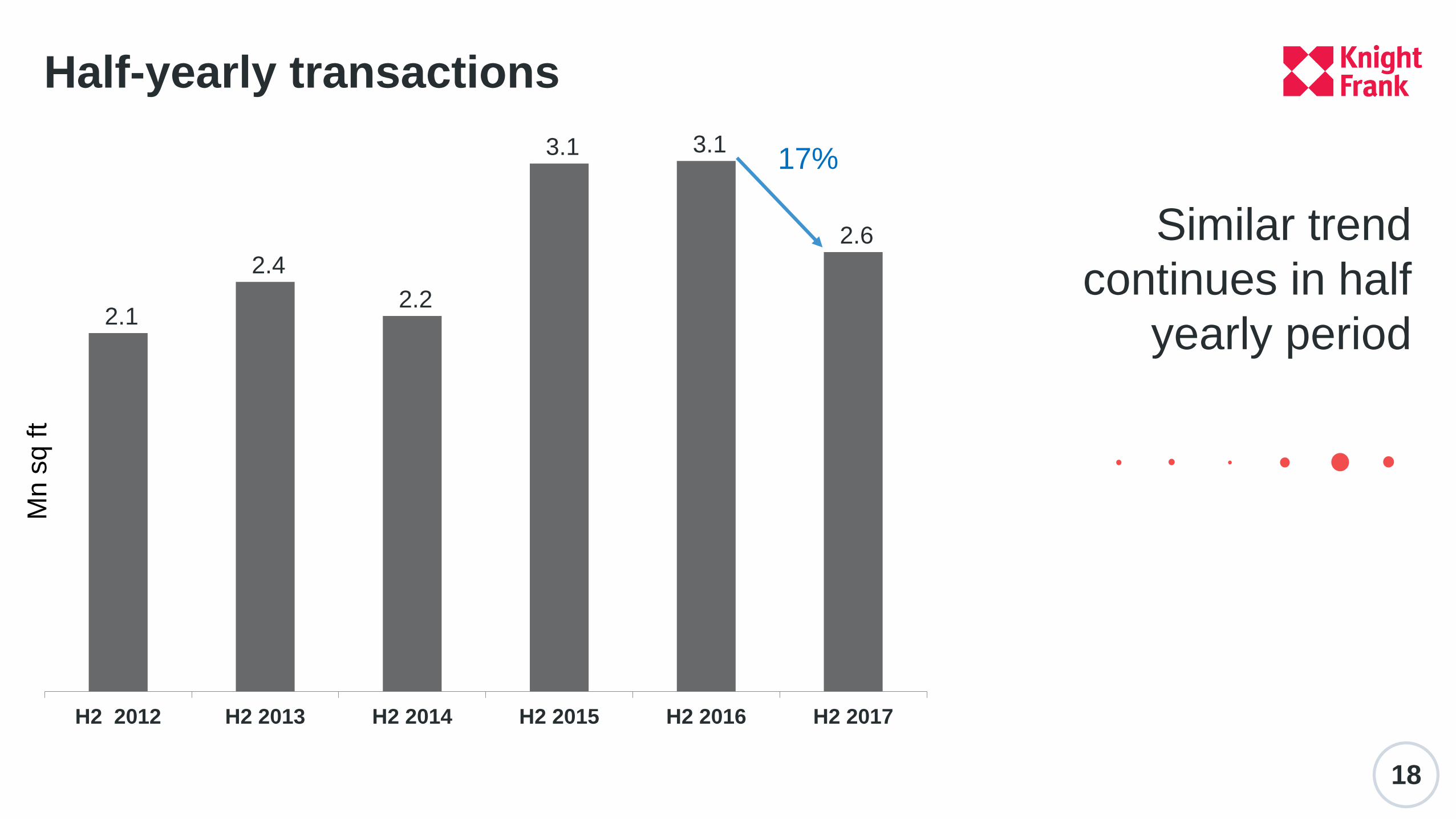

2.1

2.4

2.2

3.1 3.1

2.6

H2 2012 H2 2013 H2 2014 H2 2015 H2 2016 H2 2017

Half-yearly transactions

Similar trend

continues in half

yearly period

Mn

sq

ft

17%

19

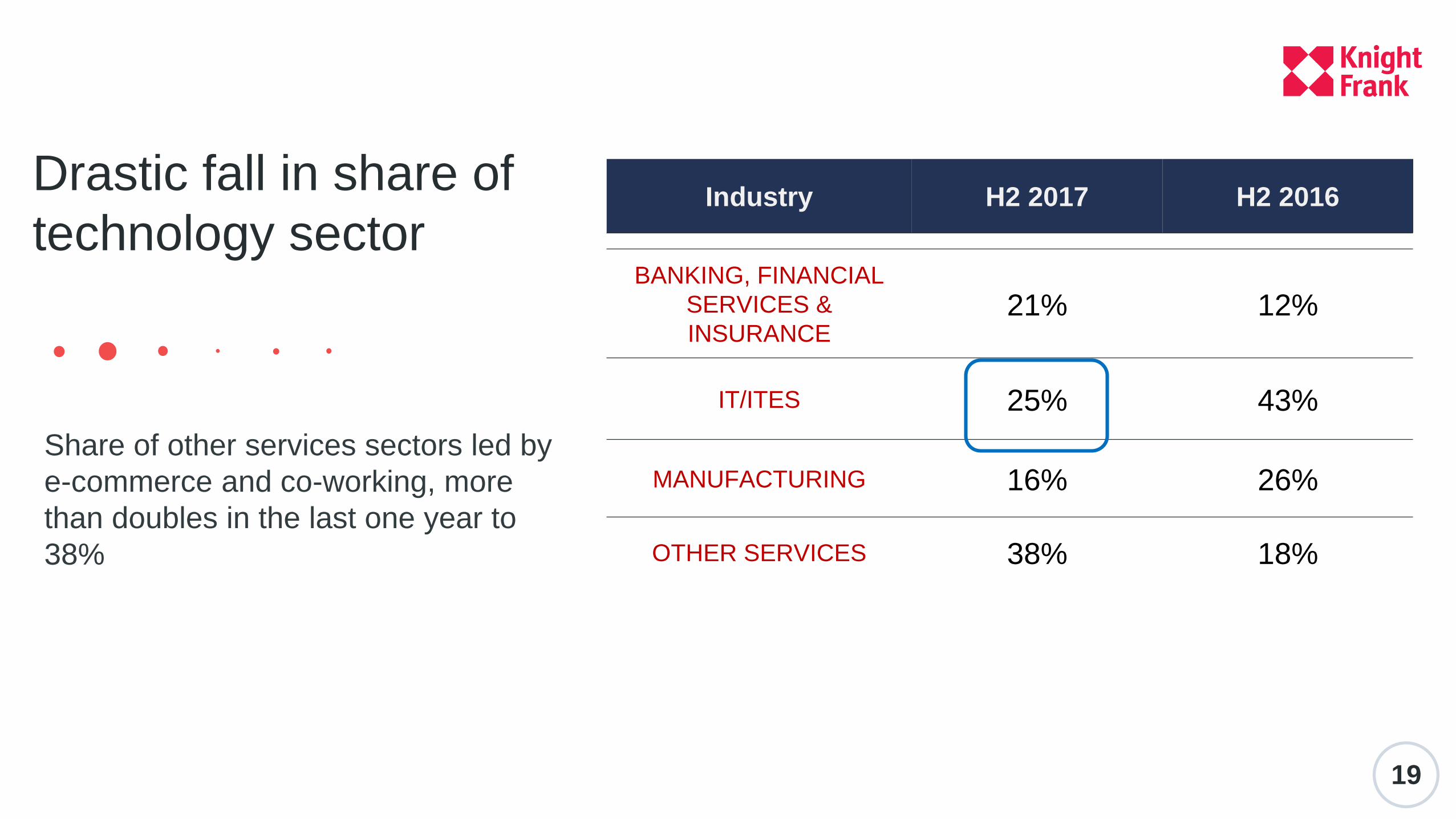

Industry H2 2017 H2 2016

BANKING, FINANCIAL

SERVICES &

INSURANCE21% 12%

IT/ITES 25% 43%

MANUFACTURING 16% 26%

OTHER SERVICES 38% 18%

Share of other services sectors led by

e-commerce and co-working, more

than doubles in the last one year to

38%

Drastic fall in share of

technology sector

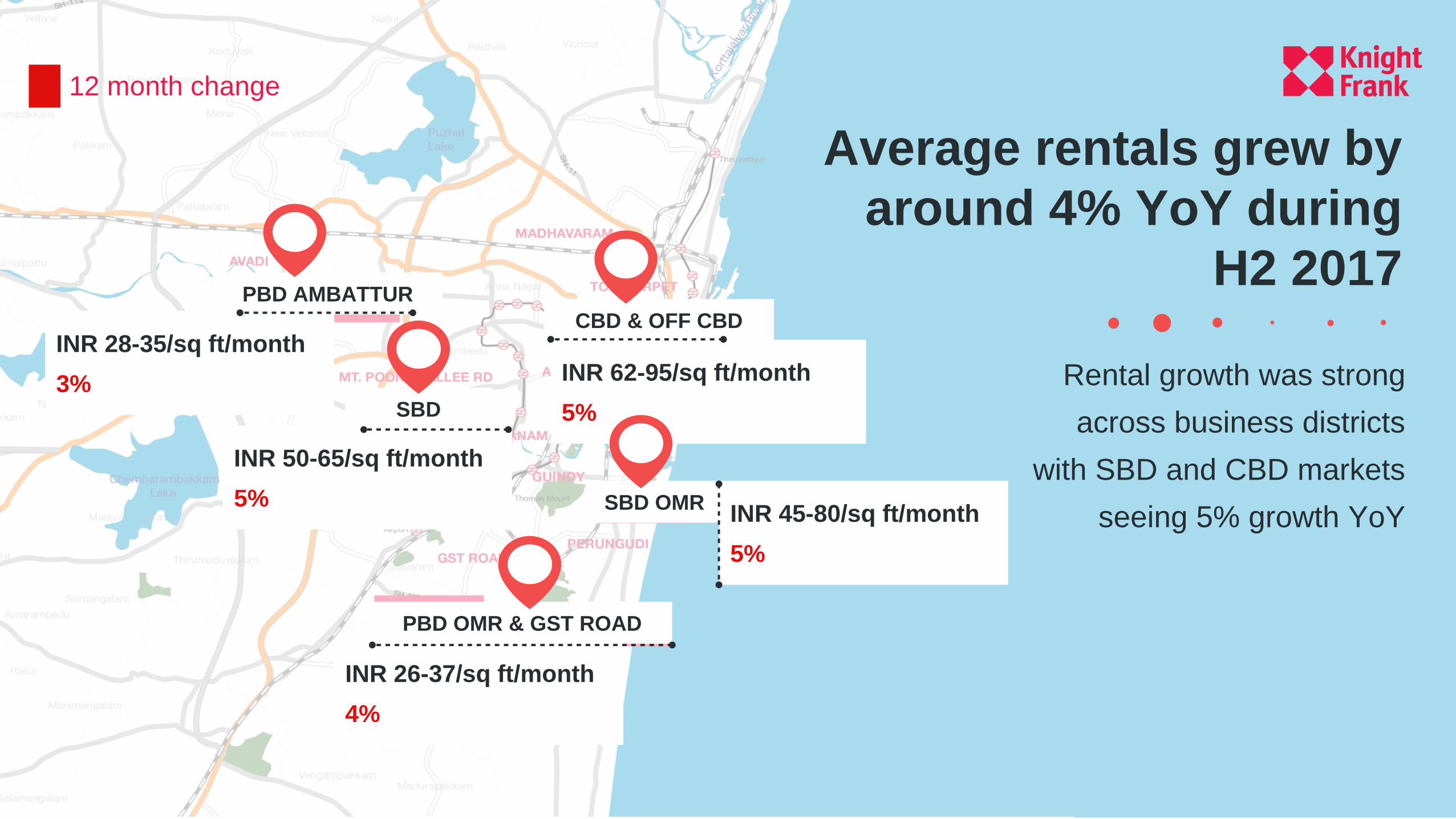

Average rentals grew by

around 4% YoY during

H2 2017

Rental growth was strong

across business districts

with SBD and CBD markets

seeing 5% growth YoY

12 month change

CBD & OFF CBD

INR 62-95/sq ft/month

5%

PBD AMBATTUR

INR 28-35/sq ft/month

3%SBD

INR 50-65/sq ft/month

5%

PBD OMR & GST ROAD

INR 26-37/sq ft/month

4%

SBD OMRINR 45-80/sq ft/month

5%

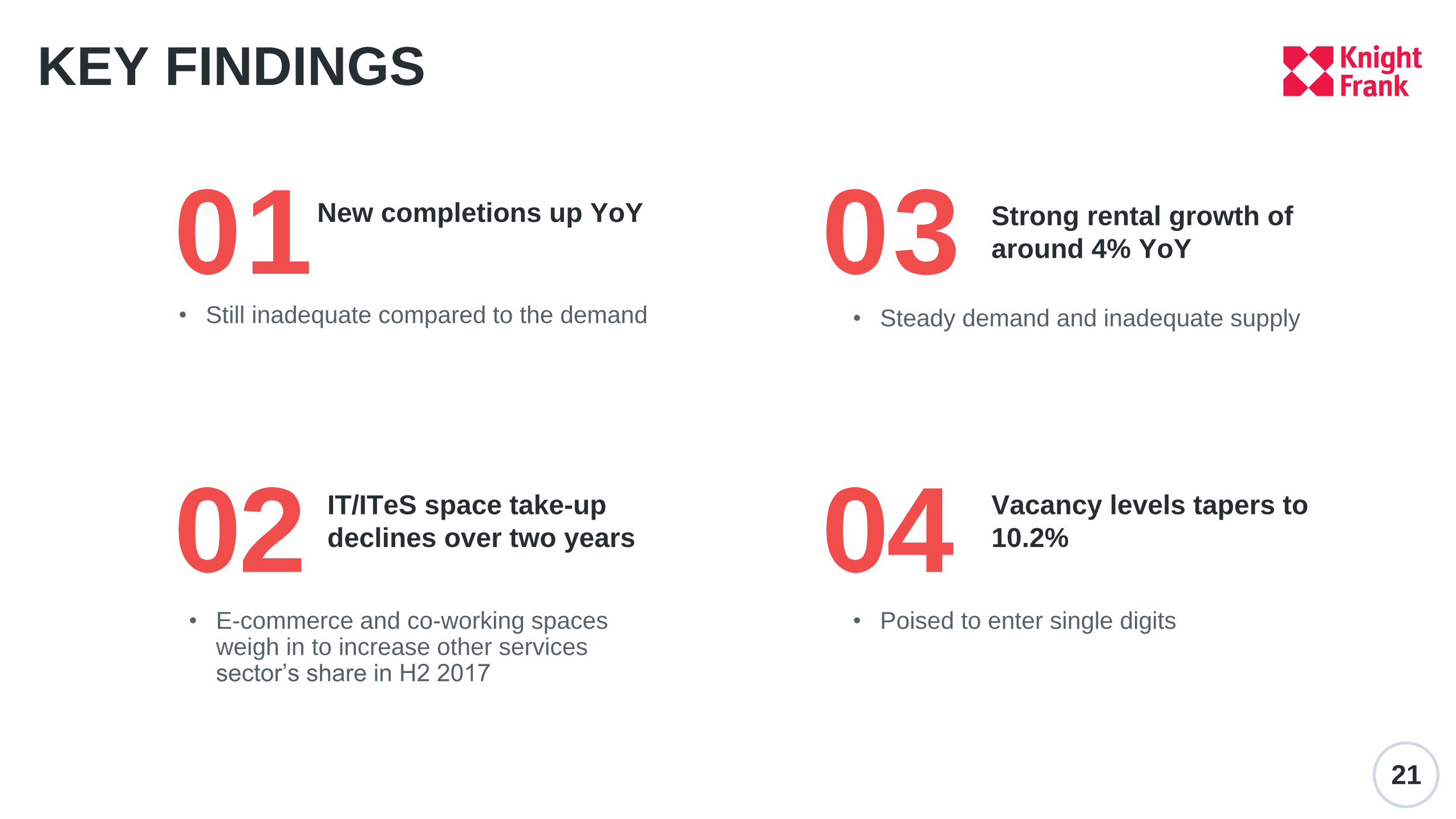

KEY FINDINGS

01 03

02 04

21

New completions up YoY

• Still inadequate compared to the demand

Strong rental growth of

around 4% YoY

• Steady demand and inadequate supply

Vacancy levels tapers to

10.2%

• Poised to enter single digits

IT/ITeS space take-up

declines over two years

• E-commerce and co-working spaces weigh in to increase other services sector’s share in H2 2017

CHENNAIRESIDENTIAL & OFFICE

In residential segment, recovery still far away

Supply crunch continues to hamstring the

Chennai office market