Embed Size (px)

Citation preview

Growing Your Offshore RMB Business

Ricky Li

Strategic Planner

Economics and Strategic Planning Department

Bank of China (Hong Kong) Limited

July 2015

SWIFT Business Forum Vietnam 2015

2

A. RMB the Next International Currency?

B. Policy Initiatives and Offshore Market Development

C. Implications of Offshore RMB Business to Enterprises

Growing Your Offshore RMB Business

3

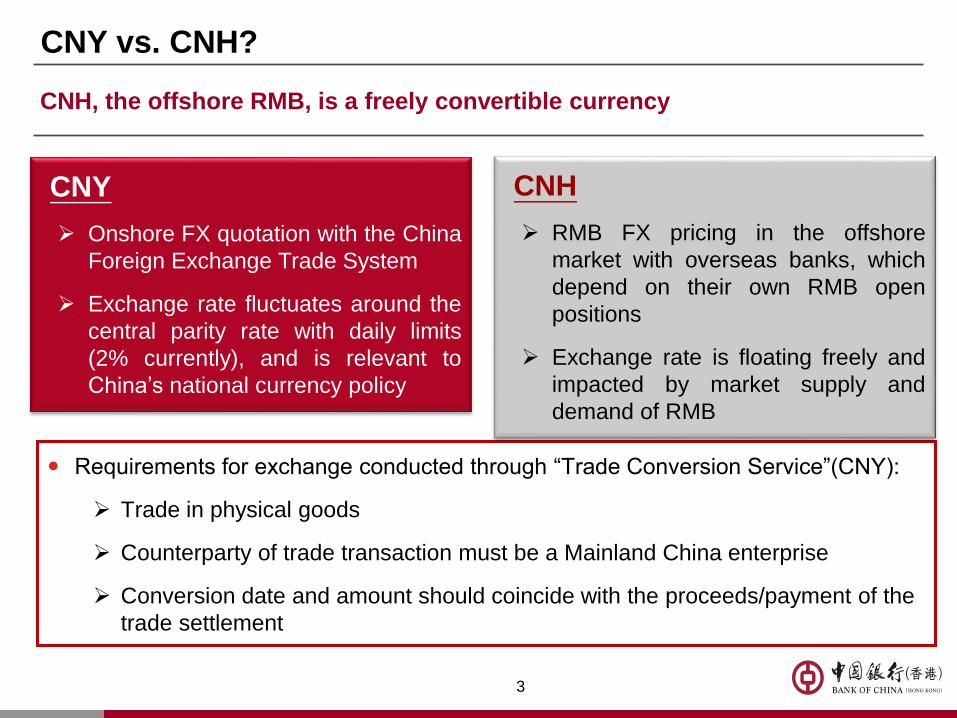

CNY vs. CNH?

Requirements for exchange conducted through “Trade Conversion Service”(CNY):

Trade in physical goods

Counterparty of trade transaction must be a Mainland China enterprise

Conversion date and amount should coincide with the proceeds/payment of the

trade settlement

CNH

RMB FX pricing in the offshore

market with overseas banks, which

depend on their own RMB open

positions

Exchange rate is floating freely and

impacted by market supply and

demand of RMB

CNY

Onshore FX quotation with the China

Foreign Exchange Trade System

Exchange rate fluctuates around the

central parity rate with daily limits

(2% currently), and is relevant to

China’s national currency policy

CNH, the offshore RMB, is a freely convertible currency

4

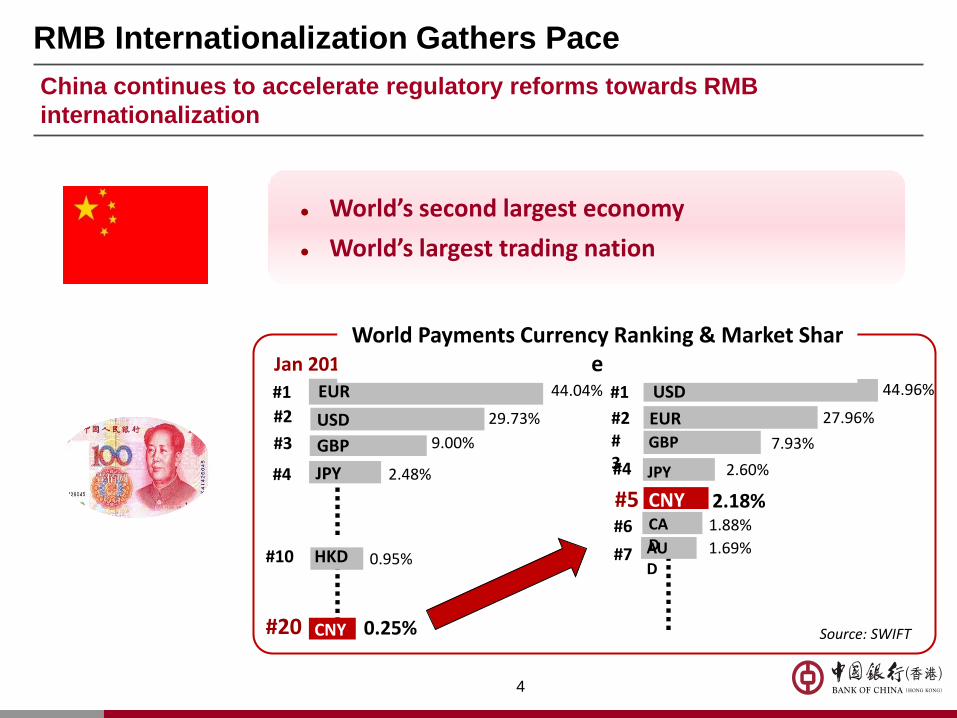

World’s second largest economy

World’s largest trading nation

China continues to accelerate regulatory reforms towards RMB

internationalization

RMB Internationalization Gathers Pace

0.25% Source: SWIFT

Jan 2012 May 2015 44.04%

USD

EUR

GBP

JPY

HKD

CNY

9.00%

2.48%

0.95%

29.73%

#1

#2

#3

#4

#10

#20

1.69%

44.96%

EUR

USD

GBP

JPY

AUD

7.93%

2.60%

27.96%

#1

#2 #3 #4

#5

#7

World Payments Currency Ranking & Market Share

2.18% CNY 1.88% CA

D #6

5

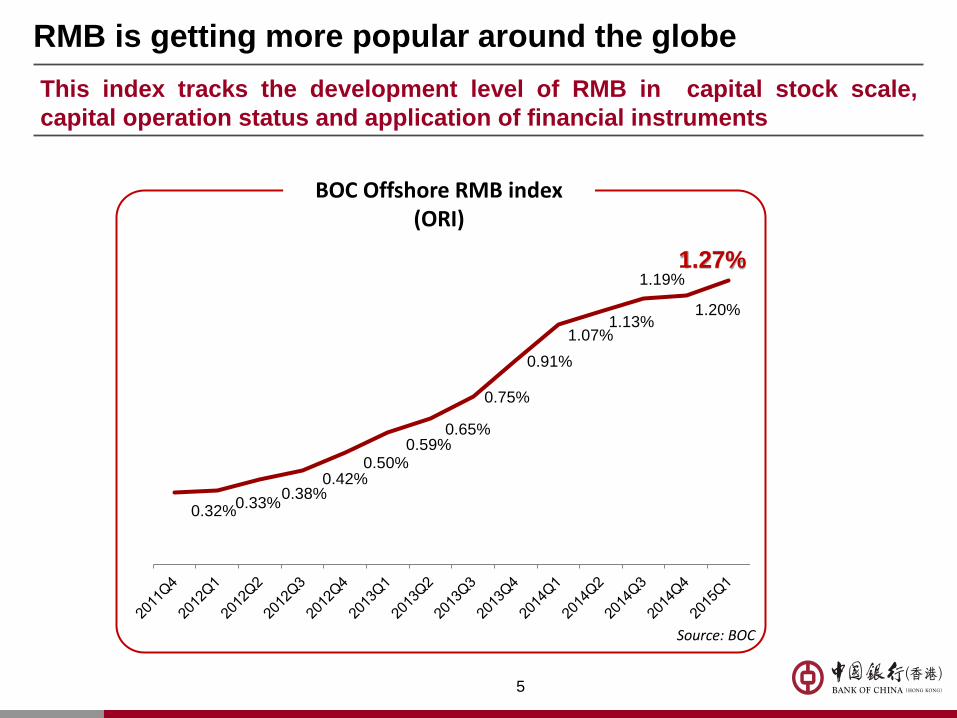

RMB is getting more popular around the globe

BOC Offshore RMB index (ORI)

Source: BOC

0.32% 0.33%

0.38% 0.42%

0.50% 0.59%

0.65%

0.75%

0.91%

1.07% 1.13%

1.19%

1.20%

1.27%

This index tracks the development level of RMB in capital stock scale,

capital operation status and application of financial instruments

6

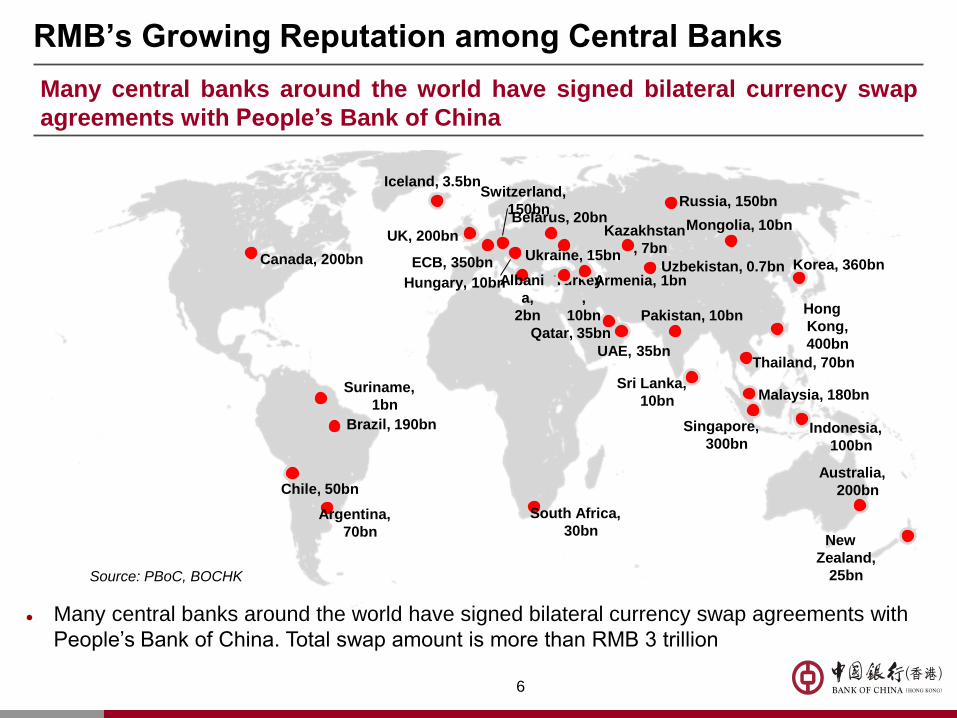

RMB’s Growing Reputation among Central Banks

Many central banks around the world have signed bilateral currency swap agreements with

People’s Bank of China. Total swap amount is more than RMB 3 trillion

Many central banks around the world have signed bilateral currency swap

agreements with People’s Bank of China

UAE, 35bn

Korea, 360bn

Pakistan, 10bn

Iceland, 3.5bn

Belarus, 20bn

Hong

Kong,

400bn

Thailand, 70bn

Malaysia, 180bn

Indonesia,

100bn

Singapore,

300bn

Mongolia, 10bn Kazakhstan

, 7bn

Uzbekistan, 0.7bn Turkey

,

10bn

Australia,

200bn

Argentina,

70bn

Brazil, 190bn

UK, 200bn

Ukraine, 15bn

New

Zealand,

25bn

Hungary, 10bn Albani

a,

2bn

ECB, 350bn

Source: PBoC, BOCHK

Switzerland,

150bn

Qatar, 35bn

Russia, 150bn

Sri Lanka,

10bn

Canada, 200bn

Armenia, 1bn

Suriname,

1bn

South Africa,

30bn

Chile, 50bn

7

More RMB clearing banks were designated by PBoC Countries/Regions Clearing Banks appointed by PBoC Key Competencies

Hong Kong BOC Hong Kong (Dec 2003) First-mover advantage / largest liquidity pool

Efficient financial infrastructure

Macau BOC Macau (Sep 2004) Proximity to China

Taiwan BOC Taipei (Feb 2013) Trade surplus / Easy acceptance

Singapore ICBC Singapore (May 2013) An established commodity and FX trading center

UK CCB London (Jun 2014) Traditional FX trading center / Europe financial center

Germany BOC Frankfurt (Jun 2014) Strong trade relationship

France BOC Paris (Jun 2014) Breakthrough to Africa

South Korea BOCOM Seoul (Jul 2014) Close economic and political tie

Luxembourg ICBC Luxembourg (Sep 2014) Largest fund centre in Europe

Qatar ICBC Doha (Nov 2014) First RMB clearing bank in Middle East

Canada ICBC Canada (Nov 2014) First RMB clearing bank in North America

Australia BOC Sydney (Nov 2014) Growing trade and financial linkages with China

Malaysia BOC Malaysia (Jan 2015) Strong trade relationship

Thailand ICBC Thailand (Jan 2015) 3rd largest ASEAN trading partner of China

Chile CCB Chile (May 2015) First RMB clearing bank in South America

Hungary BOC Hungary (Jun 2015) One of the largest trading partner of China in Mid/East

Europe

South Africa BOC Johannesburg (Jun 2015) First RMB clearing bank in Africa

8

A. RMB the Next International Currency?

B. Policy Initiatives and Offshore Market Development

C. Implications of Offshore RMB Business to Enterprises

Growing Your Offshore RMB Business

9

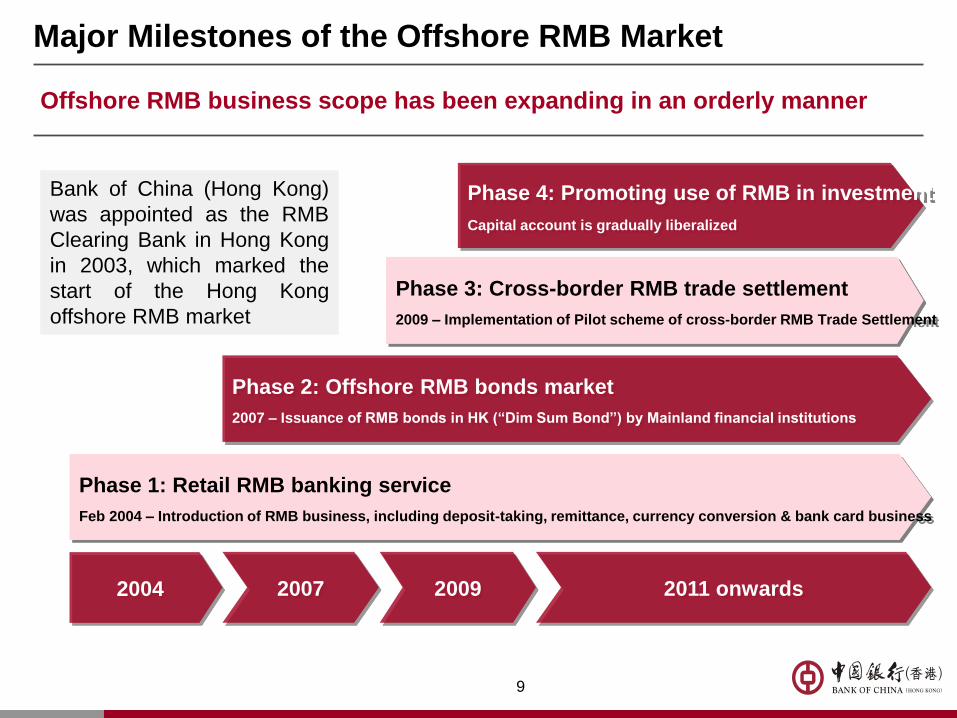

2007 2004 2009 2011 onwards

Phase 1: Retail RMB banking service

Feb 2004 – Introduction of RMB business, including deposit-taking, remittance, currency conversion & bank card business

Phase 2: Offshore RMB bonds market

2007 – Issuance of RMB bonds in HK (“Dim Sum Bond”) by Mainland financial institutions

Phase 3: Cross-border RMB trade settlement

2009 – Implementation of Pilot scheme of cross-border RMB Trade Settlement

Phase 4: Promoting use of RMB in investment

Capital account is gradually liberalized

Bank of China (Hong Kong)

was appointed as the RMB

Clearing Bank in Hong Kong

in 2003, which marked the

start of the Hong Kong

offshore RMB market

Major Milestones of the Offshore RMB Market

Offshore RMB business scope has been expanding in an orderly manner

10

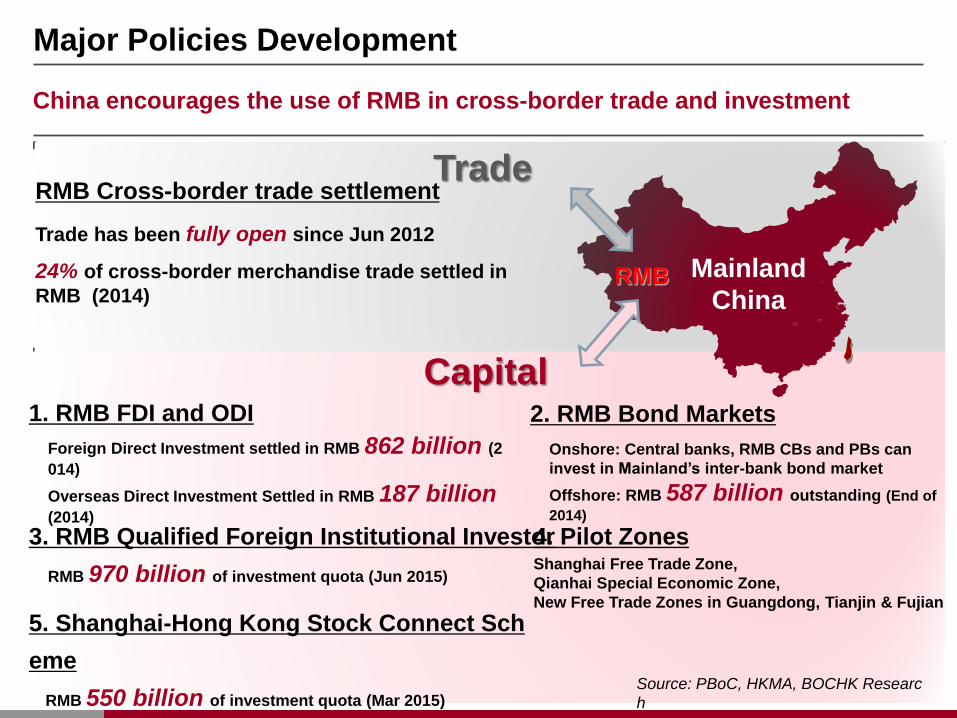

1. RMB FDI and ODI

Foreign Direct Investment settled in RMB 862 billion (2014)

Overseas Direct Investment Settled in RMB 187 billion

(2014)

Mainland

China RMB

Major Policies Development

Capital

China encourages the use of RMB in cross-border trade and investment

Source: PBoC, HKMA, BOCHK Researc

h

Trade RMB Cross-border trade settlement

Trade has been fully open since Jun 2012

24% of cross-border merchandise trade settled in

RMB (2014)

2. RMB Bond Markets

Onshore: Central banks, RMB CBs and PBs can

invest in Mainland’s inter-bank bond market

Offshore: RMB 587 billion outstanding (End of

2014)

3. RMB Qualified Foreign Institutional Investor

RMB 970 billion of investment quota (Jun 2015)

4. Pilot Zones Shanghai Free Trade Zone,

Qianhai Special Economic Zone,

New Free Trade Zones in Guangdong, Tianjin & Fujian

5. Shanghai-Hong Kong Stock Connect Sch

eme

RMB 550 billion of investment quota (Mar 2015)

11

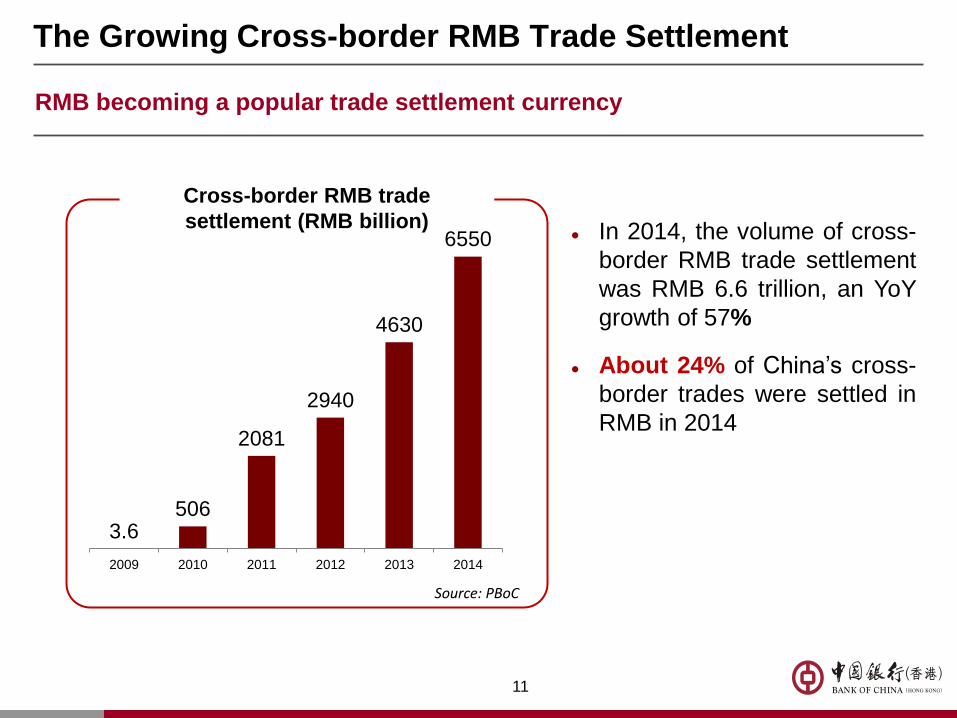

The Growing Cross-border RMB Trade Settlement

In 2014, the volume of cross-

border RMB trade settlement

was RMB 6.6 trillion, an YoY

growth of 57%

About 24% of China’s cross-

border trades were settled in

RMB in 2014

Source: PBoC

Cross-border RMB trade

settlement (RMB billion)

3.6 506

2081

2940

4630

6550

2009 2010 2011 2012 2013 2014

RMB becoming a popular trade settlement currency

12

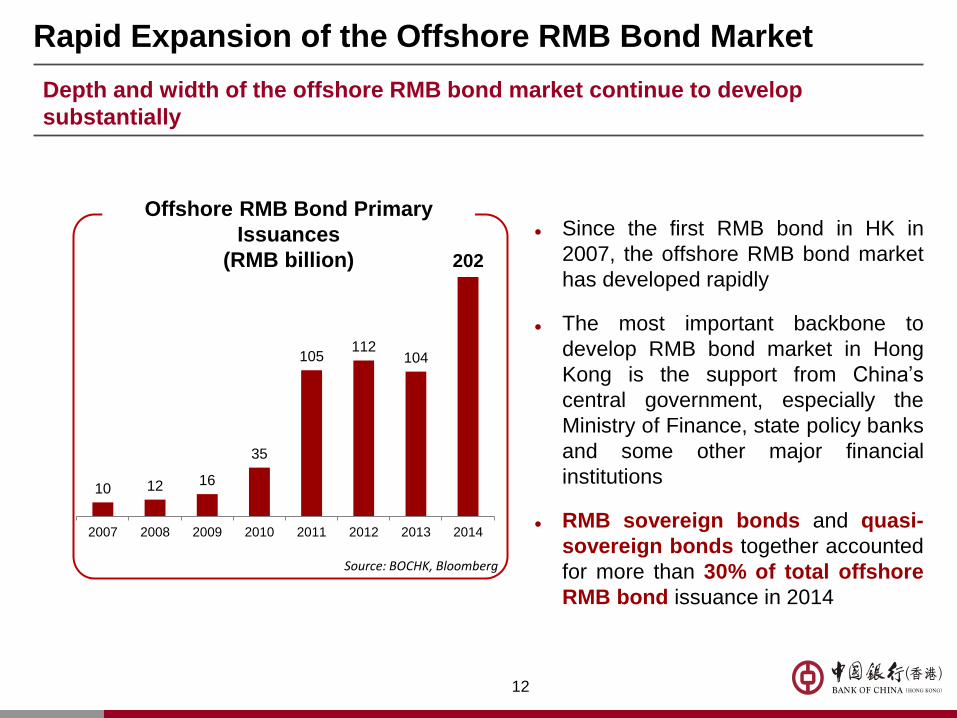

Rapid Expansion of the Offshore RMB Bond Market

Since the first RMB bond in HK in

2007, the offshore RMB bond market

has developed rapidly

The most important backbone to

develop RMB bond market in Hong

Kong is the support from China’s

central government, especially the

Ministry of Finance, state policy banks

and some other major financial

institutions

RMB sovereign bonds and quasi-

sovereign bonds together accounted

for more than 30% of total offshore

RMB bond issuance in 2014

Source: BOCHK, Bloomberg

Offshore RMB Bond Primary

Issuances

(RMB billion)

10 12 16

35

105 112

104

202

2007 2008 2009 2010 2011 2012 2013 2014(Sep)

Depth and width of the offshore RMB bond market continue to develop

substantially

13

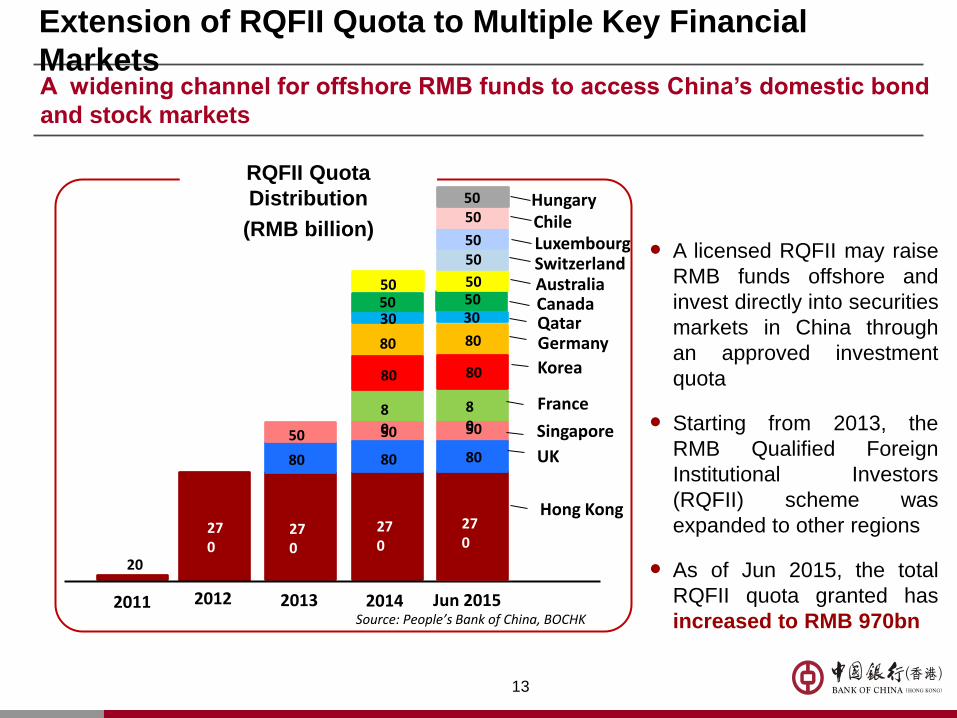

Extension of RQFII Quota to Multiple Key Financial

Markets

A licensed RQFII may raise

RMB funds offshore and

invest directly into securities

markets in China through

an approved investment

quota

Starting from 2013, the

RMB Qualified Foreign

Institutional Investors

(RQFII) scheme was

expanded to other regions

As of Jun 2015, the total

RQFII quota granted has

increased to RMB 970bn

A widening channel for offshore RMB funds to access China’s domestic bond

and stock markets

RQFII Quota Distribution

(RMB billion)

RQFII Quota

Distribution

(RMB billion)

Source: People’s Bank of China, BOCHK

80

80

80

80

50

80

50

270

270

270

20

2011 2012 2013 2014

30 50 50

Jun 2015

80

80

80

80

50

270

Canada 50 50

Switzerland 50

30

Luxembourg Chile

50

50 Hungary 50

Qatar

Hong Kong

UK

Singapore

France

Korea

Germany

Australia

14

“Gradual relaxation on the first line with efficient control mechanisms at the back”

Promote financial reform from four aspects:

1. Cross-border use of RMB, 2. Capital account convertibility,

3. Interest rate liberalization, 4. Foreign exchange management

Innovative arrangement in cross-border use of RMB:

Cross-border two-way RMB cash pooling: Corporates in FTZ can set up special

RMB deposit accounts for handing intra-group two-way cross-border RMB cash

pooling

Cross-border RMB loan: Allowing non-bank FIs and corporates in FTZ to borrow

RMB fund from the offshore market, subject to “Macro Prudential Policy Parameter”

or quota management framework

Accelerating Capital Account Liberalization in Test Zones Recently introduced policies aiming to promote financial market

liberalization will have considerable influence on promoting offshore RMB

centre development

New Free Trade Zones announced for Tianjin, Fujian and Guangdong

(includes Qianhai Special Economic Zone)

• Shanghai Free Trade Zone

15

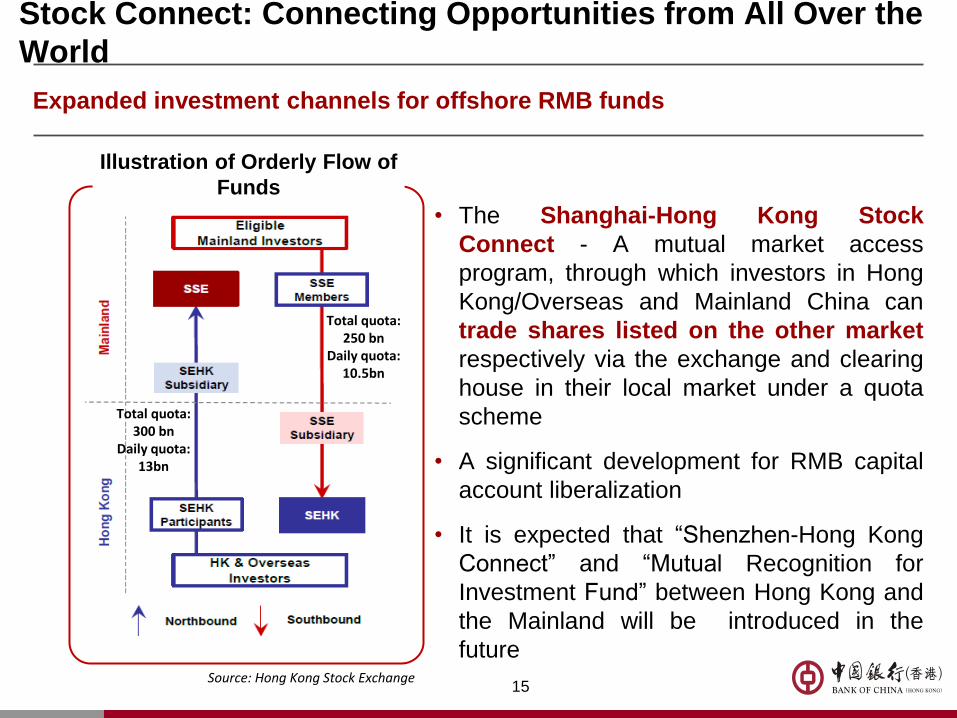

Stock Connect: Connecting Opportunities from All Over the

World

• The Shanghai-Hong Kong Stock

Connect - A mutual market access

program, through which investors in Hong

Kong/Overseas and Mainland China can

trade shares listed on the other market

respectively via the exchange and clearing

house in their local market under a quota

scheme

• A significant development for RMB capital

account liberalization

• It is expected that “Shenzhen-Hong Kong

Connect” and “Mutual Recognition for

Investment Fund” between Hong Kong and

the Mainland will be introduced in the

future Source: Hong Kong Stock Exchange

Illustration of Orderly Flow of

Funds

Total quota: 300 bn

Daily quota: 13bn

Total quota: 250 bn

Daily quota: 10.5bn

Expanded investment channels for offshore RMB funds

16

Outlook of RMB Internationalization

Global use of RMB gathers pace

Apart from the strong position in Asia-pacific countries,

western developed countries have also gained

momentum to participate in RMB community

Capital account liberalization will be the next policy

focus

Foreign investors are gaining more access to China’s

capital market

On track to be a global reserve currency:

• Potential Inclusion of RMB in the IMF’s Special Drawing

Rights (SDR) Currency Basket by end-2015

• RMB is now in transition from a trading currency to an

investment currency; the international reserve currency

status will establish eventually

17

A. RMB the Next International Currency?

B. Policy Initiatives and Offshore Market Development

C. Implications of Offshore RMB Business to Enterprises

Growing Your Offshore RMB Business

18

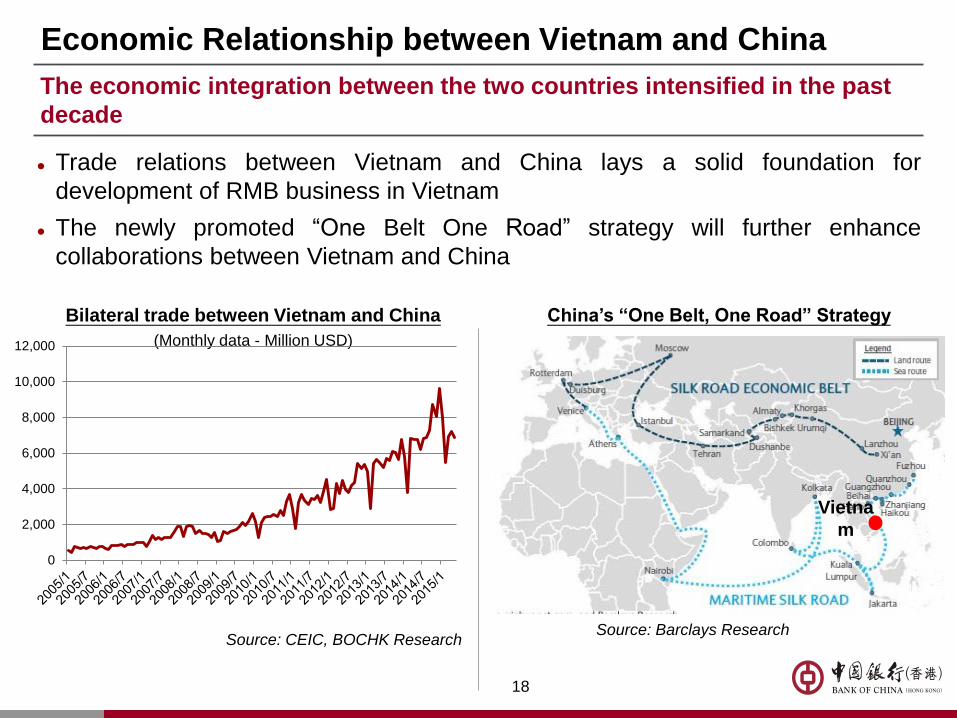

Economic Relationship between Vietnam and China

Trade relations between Vietnam and China lays a solid foundation for

development of RMB business in Vietnam

The newly promoted “One Belt One Road” strategy will further enhance

collaborations between Vietnam and China

The economic integration between the two countries intensified in the past

decade

Bilateral trade between Vietnam and China

(Monthly data - Million USD)

Source: CEIC, BOCHK Research

China’s “One Belt, One Road” Strategy

Source: Barclays Research

Vietna

m

0

2,000

4,000

6,000

8,000

10,000

12,000

19

Implications of Offshore RMB Business to Enterprises

Firms set to benefit from the use of RMB in settlements

For a company that exports to China

Conducting trade settlements in RMB means receiving payments in a stable currency

with lower volatility and opportunities for diversified investments in RMB assets

For a company that imports from China

Making payments in RMB may increase its bargaining power and negotiate for better

pricing terms

For companies with strong trade relationships in China and with revenue

and expenses in RMB

Using RMB in trade settlements create a natural hedge to currency risk with the benefits

of avoiding conversion costs

For multi-national companies with investment in China

Using RMB as settling currency will facilitate smooth implementation of their projects and

eliminate foreign exchange exposure

20

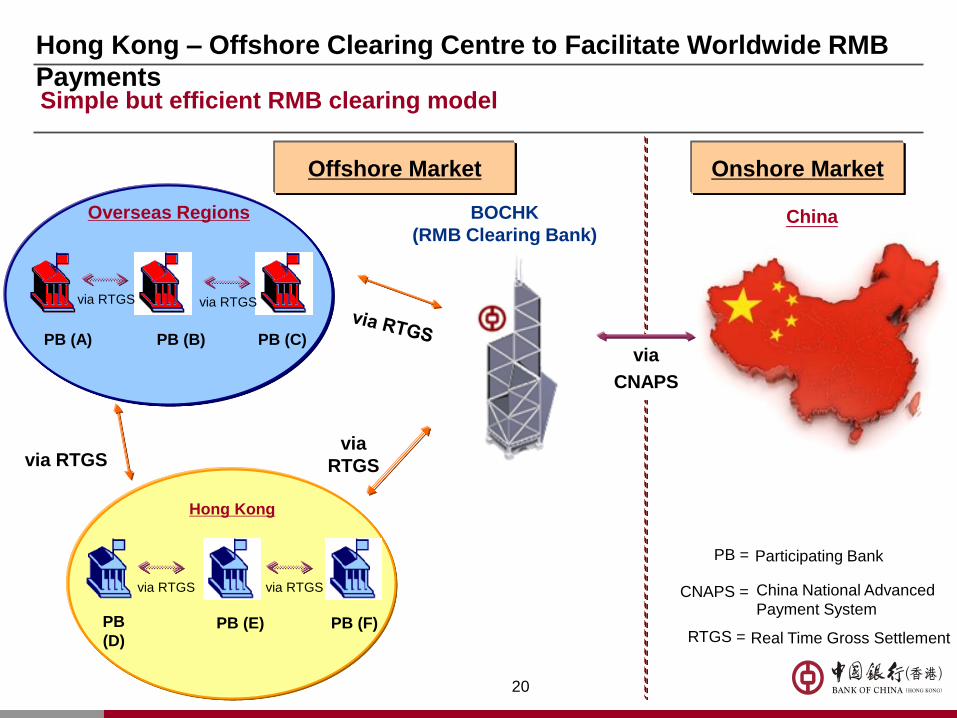

Hong Kong – Offshore Clearing Centre to Facilitate Worldwide RMB

Payments

China

via

RTGS via RTGS

Hong Kong

PB

(D) PB (E) PB (F)

via RTGS via RTGS

Overseas Regions

PB (A) PB (B) PB (C)

via RTGS via RTGS

China National Advanced

Payment System

via

CNAPS

Offshore Market Onshore Market

CNAPS =

PB = Participating Bank

Simple but efficient RMB clearing model

BOCHK

(RMB Clearing Bank)

RTGS = Real Time Gross Settlement

21

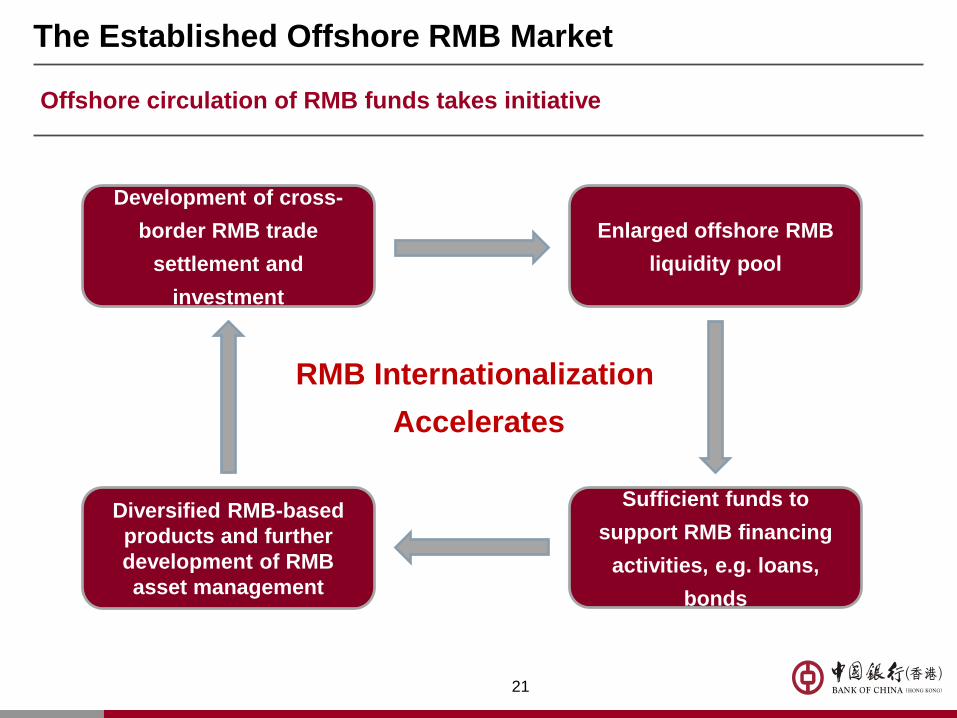

Offshore circulation of RMB funds takes initiative

Development of cross-

border RMB trade

settlement and

investment

Enlarged offshore RMB

liquidity pool

Diversified RMB-based

products and further

development of RMB

asset management

Sufficient funds to

support RMB financing

activities, e.g. loans,

bonds

RMB Internationalization

Accelerates

The Established Offshore RMB Market

22

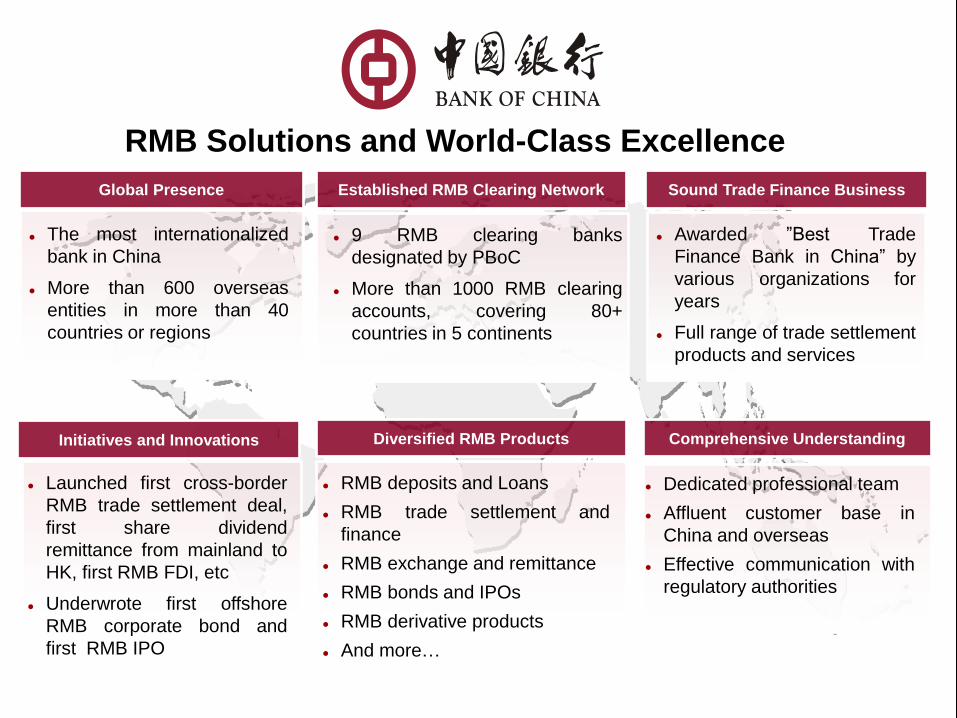

RMB Solutions and World-Class Excellence

Global Presence

The most internationalized

bank in China

More than 600 overseas

entities in more than 40

countries or regions

Established RMB Clearing Network

9 RMB clearing banks

designated by PBoC

More than 1000 RMB clearing

accounts, covering 80+

countries in 5 continents

Initiatives and Innovations

Launched first cross-border

RMB trade settlement deal,

first share dividend

remittance from mainland to

HK, first RMB FDI, etc

Underwrote first offshore

RMB corporate bond and

first RMB IPO

Diversified RMB Products

RMB deposits and Loans

RMB trade settlement and

finance

RMB exchange and remittance

RMB bonds and IPOs

RMB derivative products

And more…

Sound Trade Finance Business

Awarded ”Best Trade

Finance Bank in China” by

various organizations for

years

Full range of trade settlement

products and services

Comprehensive Understanding

Dedicated professional team

Affluent customer base in

China and overseas

Effective communication with

regulatory authorities

23

Disclaimer

Products and services described in this presentation and any associated material (collectively, the “Materials”) provided by Bank of China (Hong Kong)

Limited, its subsidiaries, affiliates or group companies (collectively, “BOCHK Group”), may not be suitable for persons in all jurisdictions.

The information contained in the Materials is for your general reference only and is provided without warranty of any kind and may be changed at any

time without prior notice. Persons in receipt of the Materials should consult their own professional advisers before making any investment decision to

purchase any securities or financial products. It is not possible for the Materials to disclose all risks and significant aspects associated with the products

and services described herein. No person should deal in any such securities or financial products or avail themselves to BOCHK Group’s investment

services unless he understands the nature of the relevant transactions and the extent of his exposure to potential loss.

Each prospective investor should consider carefully whether the products and investments are suitable for him in light of his circumstances and financial

position.

None of the Materials constitutes an offer of any securities for sale or solicitation of an offer to sell any securities in the United States or any other

jurisdiction in which such offer or sale is prohibited. The financial products and services referred to in the Materials, have not been and will not be

registered under the U.S. Securities Act of 1933, as amended (the "Securities Act”), and no such securities may be offered or sold in the United States

unless registered under the Securities Act or pursuant to an exemption from such registration. The products may not be at any time offered, sold,

transferred, delivered, exchanged, exercised or redeemed within the United States or to, or for the account or benefit of, any U.S. person (as defined in

the Securities Act or the U.S. Internal Revenue Code of 1986, as amended).

No invitation is made in the Materials or the information contained herein to enter into, or offer to enter into, any agreement to purchase, acquire,

dispose of, subscribe for any securities, and no offer is made of any shares in or debentures of a company for purchase or subscription, except as

permitted under the laws of Hong Kong.

You should note that information in the Materials is reflective of data as of the specified date and is based on current assumptions and market conditions.

All estimates and opinions, if any, included in the Materials may be subject to change without notice and past performance is not indicative of future

results.

Although information in the Materials has been prepared in good faith from sources believed to be reliable, BOCHK Group does not represent or warrant

its accuracy, truthfulness and completeness. None of BOCHK Group or its representatives shall have any responsibility or liability whatsoever (for

negligence or otherwise) for any loss howsoever arising from any use of the Materials or its contents or otherwise arising in connection with the

Materials.

To the extent that the financial products described in the Materials are listed in Hong Kong, they are neither endorsed, issued, sold nor promoted by The

Stock Exchange of Hong Kong Limited. The Stock Exchange of Hong Kong Limited expressly disclaims any liability for any loss howsoever arising from

or in reliance upon the whole or any part of the contents of the Materials.

24

Disclaimer

From time to time, and in the ordinary course of business, members of the BOCHK Group may provide advisory and investment or commercial

banking services, and enter into other commercial transactions related to products described in the Materials, for which customary compensation has

been received. Prospective investors should make enquiries with their respective brokers as to the terms and/or existence of any such commission

arrangements. For example, at any time, member(s) of the BOCHK Group may act as a distributor or market-maker or otherwise be long or short of or

have financial interests in services/products described in the Materials.

In making an investment decision or availing yourself of the services described in the Materials, you are deemed to represent that you have made your

investment and trading decisions (including decisions with regard to the suitability of the products) based upon your own judgment and not in reliance

upon any view expressed by us and that you fully understand all the risks involved and are capable of assuming and willing to assume such risks.

BOCHK Group does not make any representation regarding the legality of investments described in the Materials under any applicable laws.

The Materials are protected by copyright. No part of it may be modified, reproduced, transmitted and distributed in any form for use without BOCHK

Group’s prior written consent.

If the presentation materials fall within the definition of “investment research” under Paragraph 16.2 (f) of the Code of Conduct for Persons Licensed by

or Registered with the Securities and Futures Commission, we shall make disclosure in the form set out in “Disclosure for Research Report and

Presentation”.

“Investment research” includes documentation containing any one of the following:-

(i) result of investment analysis of securities;

(ii) investment analysis of factors likely to influence the future performance of securities, not including any analysis on macro economic or strategic

issue; or

(iii) advice or recommendation based on any of the foregoing result or investment analysis.

25

Thank You!