Embed Size (px)

Citation preview

第三期 NO.3 2016

離岸人民幣快報

Offshore RMB

Express

目錄 市場數據 Chart Book 3

清算行資訊 Information on RMB Clearing 7

政策追蹤 Policy Watch 9

市場動態 Market Updates 11

RMB 專題研究 RMB Offshore Market Insights 12

編者 Editors: 張文晶 (Annie Cheung) 譚愛瑋(Celine Tam) 孔玲(Kera Kong)

Co

nte

nts

在人民幣兌美元匯率繼續承受貶值壓力的情況下,人民幣國際化之路能否和如何走下去便是一個全新的課題。如果市場環境嚴峻到必需在人民幣匯率穩定和國際化之間作出一個選擇,而不能同時兼顧時,可能的政策選擇會是以匯率穩定爲主、國際化為輔。 Given the persistent depreciation pressure on the RMB against the USD, whether the RMB will continue on its internationalization journey and how the RMB can progress further will be a brand new topic. If the market condition changes drastically and there is an imminent need to make a decision between the stability of the RMB exchange rate and the progress of internationalization, given that both cannot be achieved at the same time, it is highly probable that exchange rate stability will be the primary focus and internationalization will be secondary.

發展規劃部經濟研究處

中國銀行(香港)Bank of China (Hong Kong) Limited

2016/03/09

2

人民幣存款(圖1)

2016年1月底香港人民幣存款爲8,521億元,環比微升0.1%,同比減少13.2%。

人民幣跨境結算(圖2)

2016年1月份跨境貿易結算的人民幣匯款總額為 4,801億元,環比下降28.1%。

市場數據

Chart Book

1. 人民幣資金池狀況 RMB Capital Pool

RMB Deposits (Chart. 1)

RMB deposits in Hong Kong edged up by 0.1% MoM to RMB 852.1bn in January 2016. The outstanding amount decreased by 13.2% from a year ago.

RMB Cross-border Trade Settlement (Chart. 2) The amount of RMB cross-border trade settlement decreased by 28.1% MoM to RMB 480.1bn in January 2016.

3

資料來源:Bloomberg, BOCHK 資料來源:Bloomberg, BOCHK

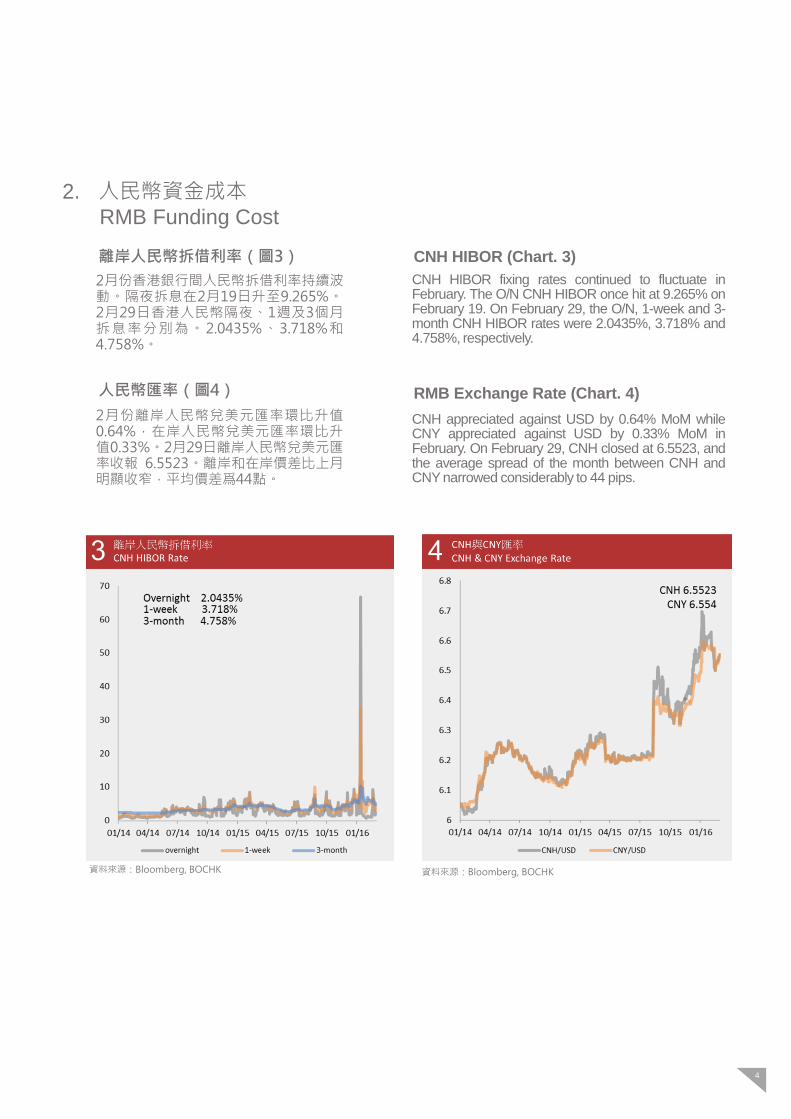

離岸人民幣拆借利率(圖3)

2月份香港銀行間人民幣拆借利率持續波動。隔夜拆息在2月19日升至9.265%。 2月29日香港人民幣隔夜、1週及3個月拆息率分別為。2.0435%、3.718%和4.758%。

人民幣匯率(圖4)

2月份離岸人民幣兌美元匯率環比升值0.64%,在岸人民幣兌美元匯率環比升值0.33%。2月29日離岸人民幣兌美元匯率收報 6.5523。離岸和在岸價差比上月明顯收窄,平均價差爲44點。

2. 人民幣資金成本 RMB Funding Cost

CNH HIBOR (Chart. 3)

CNH HIBOR fixing rates continued to fluctuate in February. The O/N CNH HIBOR once hit at 9.265% on February 19. On February 29, the O/N, 1-week and 3-month CNH HIBOR rates were 2.0435%, 3.718% and 4.758%, respectively.

RMB Exchange Rate (Chart. 4)

CNH appreciated against USD by 0.64% MoM while CNY appreciated against USD by 0.33% MoM in February. On February 29, CNH closed at 6.5523, and the average spread of the month between CNH and CNY narrowed considerably to 44 pips.

4

資料來源:Bloomberg, BOCHK 資料來源:Bloomberg, BOCHK

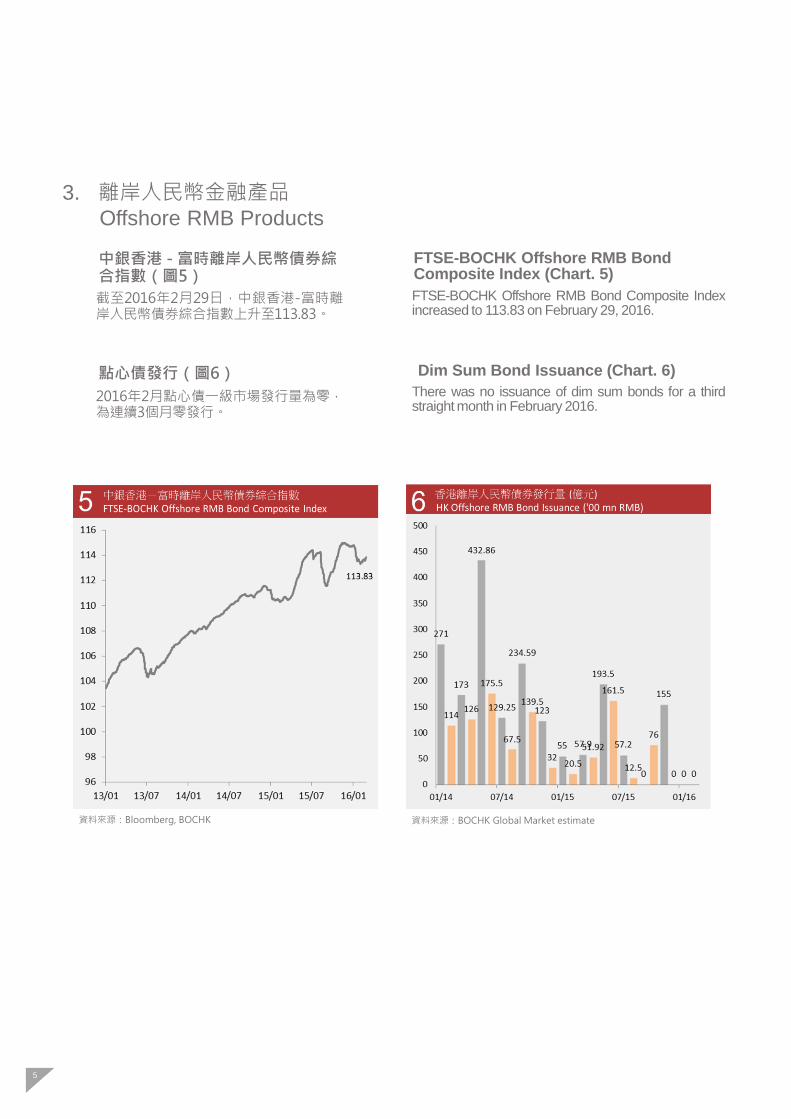

中銀香港 - 富時離岸人民幣債券綜合指數(圖5)

截至2016年2月29日,中銀香港-富時離岸人民幣債券綜合指數上升至113.83。

點心債發行(圖6)

2016年2月點心債一級市場發行量為零,為連續3個月零發行。

3. 離岸人民幣金融產品 Offshore RMB Products

FTSE-BOCHK Offshore RMB Bond Composite Index (Chart. 5)

FTSE-BOCHK Offshore RMB Bond Composite Index increased to 113.83 on February 29, 2016.

Dim Sum Bond Issuance (Chart. 6)

There was no issuance of dim sum bonds for a third straight month in February 2016.

5

資料來源:Bloomberg, BOCHK 資料來源:BOCHK Global Market estimate

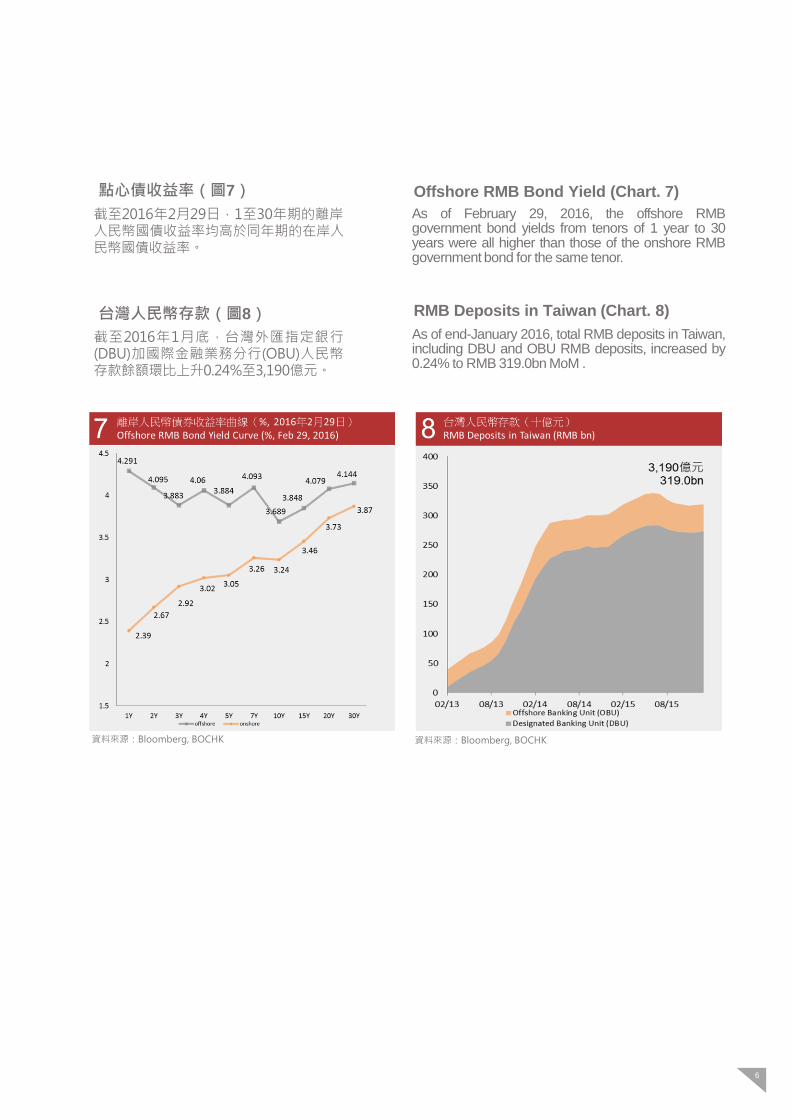

點心債收益率(圖7)

截至2016年2月29日,1至30年期的離岸人民幣國債收益率均高於同年期的在岸人民幣國債收益率。

台灣人民幣存款(圖8)

截至2016年1月底,台灣外匯指定銀行(DBU)加國際金融業務分行(OBU)人民幣存款餘額環比上升0.24%至3,190億元。

Offshore RMB Bond Yield (Chart. 7)

As of February 29, 2016, the offshore RMB government bond yields from tenors of 1 year to 30 years were all higher than those of the onshore RMB government bond for the same tenor.

RMB Deposits in Taiwan (Chart. 8)

As of end-January 2016, total RMB deposits in Taiwan, including DBU and OBU RMB deposits, increased by 0.24% to RMB 319.0bn MoM .

6

資料來源:Bloomberg, BOCHK 資料來源:Bloomberg, BOCHK

清算行資訊

Information on RMB Clearing

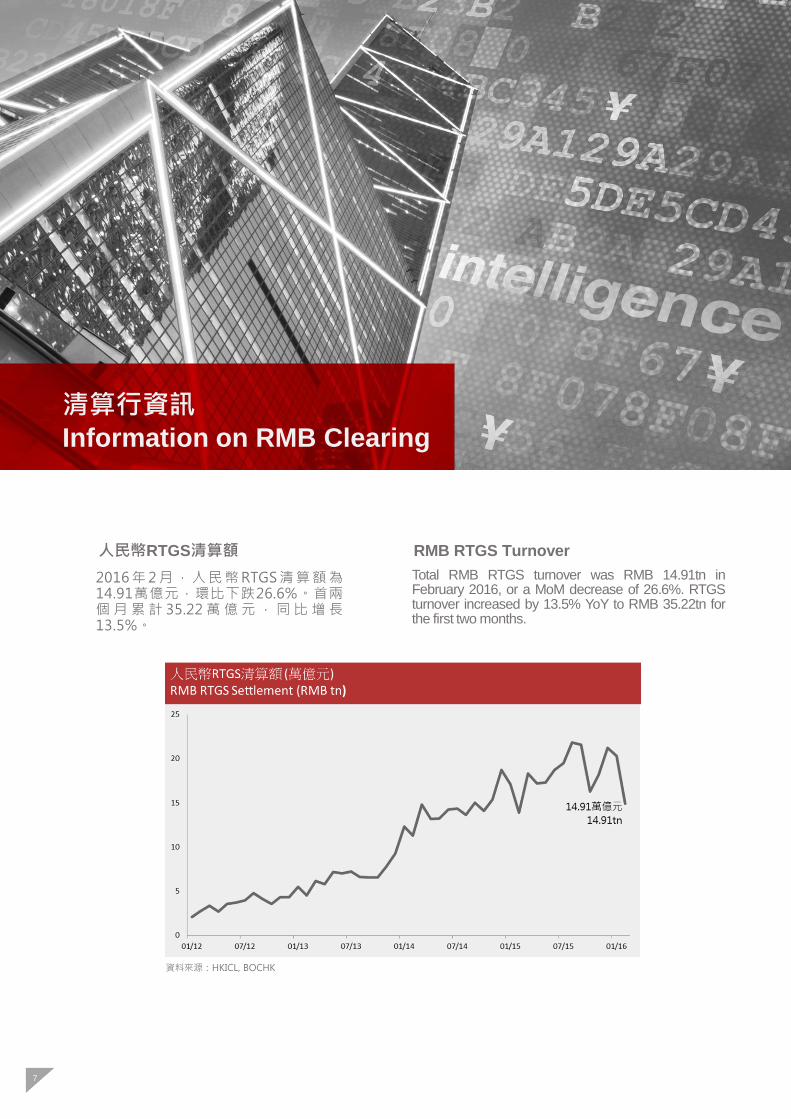

人民幣RTGS清算額

2016年2月,人民幣RTGS清算額為14.91萬億元,環比下跌26.6%。首兩個月累計 35.22 萬億元,同比增長13.5%。

RMB RTGS Turnover

Total RMB RTGS turnover was RMB 14.91tn in February 2016, or a MoM decrease of 26.6%. RTGS turnover increased by 13.5% YoY to RMB 35.22tn for the first two months.

7

資料來源:HKICL, BOCHK

8

Mainland RMB Cross-border Settlement

According to the People’s Bank of China (PBOC), RMB cross-border trade settlement reached RMB 564.3bn in January 2016, amongst which RMB cross-border trade settlement for goods amounted to RMB 492.2bn and settlement for services and other current accounts amounted to RMB 72.1bn. Meanwhile, the amount of RMB direct investment reached RMB 317.8bn, amongst which outward and inward direct investments were RMB 152.2bn and RMB 165.6bn, respectively. BOC Cross-border RMB Index (CRI) Increased by 15 points from the previous month and 20 points from the beginning of 2015 to 276 points in December 2015. CRI climbed for the first 8 months of 2015, and reached the peak at 321 points in August. CRI then retreated as a result of volatile RMB exchange rates in the onshore and offshore markets, interest rate fluctuation, the Fed’s rate hike and increasing economic headwinds. Overall, CRI gained slightly in 2015.

中國人民幣跨境結算業務

根據中國人民銀行公佈數據,2016年1月份跨境貿易人民幣結算業務發生5,643億元。其中貨物貿易4,922億元、服務貿易及其他經常項目721億元。另外,直接投資人民幣結算業務發生3,178億元,其中對外直接投資1,522億元、外商直接投資1,656億元。

2015年12月中國銀行跨境人民幣指數為276點,當月上升15點,全年上升20點。本月人民幣淨流出1,390億元。從全年情況看,1-8月CRI指數震盪走高,8月達到321點全年高點。之後受境內外市場人民幣匯率、利率波動,美聯儲加息,經濟下行壓力加大等多重因素的影響出現較大回落,但全年仍實現小幅提升。

資料來源:BOC, BOCHK

SWIFT 人民幣追蹤

2016年1月份,人民幣維持全球付款第五最活躍貨幣的地位, 佔全球支付2.45%。

SWIFT’s RMB Tracker

In January 2016, RMB held its position as the fifth most active currency used for global payments by value, accounting for 2.45% of global payments.

資料來源:SWIFT

外管局放寬QFII投資額度

2月4日,國家外匯管理局發佈《合格境外機構投資者境內證券投資外匯管理規定》。主要內容包括: 1) 不再對QFII機構設統一的投資額度上限,而是根據機構資產規模或管理的資產規模的一定比例作為其獲取投資額度的依據;2) 對QFII機構基礎額度內的額度申請採取備案管理;超過基礎額度的,才需外管局審批;3) 允許QFII機構開放式基金按日申購、贖回;4) QFII機構資金匯出的鎖定期從1年縮短為3個月,但保留資金分批、分期匯出要求。

政策追蹤

Policy Watch

SAFE Relaxed QFII Investment Quota

On February 4, State Administration of Foreign

Exchange (SAFE) released “the Provisions on Foreign

Exchange Administration of Domestic Securities

Investment by Qualified Foreign Institutional Investors

(QFII)”. It mainly included: 1) The unified investment

quota ceiling set on individual QFII would be revoked.

Instead, a certain percentage of the asset size or asset

size managed by the QFII would be used as the base

for calculating the investment quota. 2) Application for

investment quota by the QFII within the base quota

would be subject to management by record filing.

Approval by SAFE would only be required when

investment quota exceeds the base quota. 3) The QFII

would be allowed to subscribe or redeem open-ended

funds on a daily basis. 4) The lock-up period of the

outward remittance of capital by the QFII would be

shortened from 1 year to 3 months. However,

requirements for outward remittance of capital in

batches and by installments remain.

9

10

人行進一步放開銀行間債券市場

2月24日,中國人民銀行宣佈在中國境外依法註冊成立的商業銀行、保險公司、證券公司、基金管理公司及其他資產管理機構等金融機構,以及養老基金、慈善基金、捐贈基金等人行認可的其他中長期機構投資者,均可投資銀行間債券市場,且沒有額度限制。符合條件的境外機構投資者通過銀行間市場結算代理人完成備案、開戶等手續後,即可成為銀行間債券市場的參與者。

PBOC Further Liberalized Interbank Bond Market

The People’s Bank of China (PBOC) announced on

February 24 that commercial banks, insurance firms,

security firms, fund management companies and other

asset management companies that registered outside

of China, as well as other medium-to-long term

institutional investors that were approved by the PBOC,

such as pension funds, charity funds and endowment

funds, would be authorized to invest in onshore

interbank bond market without quota limitation. Eligible

offshore institutional investors can become market

participants after completing the filing and account

opening procedure with the interbank market

settlement agents.

人行下調存款準備金率

人行宣佈自3月1日起,普遍下調金融機構存款準備金率0.5個百分點。降準後,大型金融機構及中小型金融機構的存款準備金率分別是17%和15%。

PBOC Cut RRR

The PBOC cut the reserve requirement ratio (RRR) by

50 bps for all financial institutions with effect from March

1. The RRR for large and medium to small financial

institutions would be 17% and 15%, respectively

following the PBOC’s announcement.

中行與中國遠洋海運集團簽署1,500億元合作協議

2月18日,中國銀行與中國遠洋海運集團在滬簽署《全球戰略合作協定》。根據協定,中行在全球範圍內向中國遠洋海運集團提供意向性總額不超過1,500億元的授信服務。雙方合作範圍將覆蓋信貸、直接融資、現金管理、企業年金、財務顧問、投資銀行、保險等領域。

市場動態

Market Updates

BOC Signed RMB 150bn Cooperative Agreement with China COSCO Shipping Co. Ltd.

On February 18, Bank of China (BOC) signed a

cooperative agreement with China COSCO Shipping

Corporation Limited. Under the agreement, China

COSCO Shipping Corporation Limited would be

expected to receive credit lines of no more than RMB

150bn on a global basis from BOC. The bilateral

cooperation will cover credit facility, direct financing,

cash management, company annuity, financial

consulting, investment banking, insurance, etc.

11

RMB 專題研究

RMB Offshore Market Insights

專題一: 貶值壓力下的人民幣國際化

RMB Internationalization under the Depreciation Pressure

高級經濟研究員 戴道華 Daohua Dai, Senior Economist

2015年底,IMF決定在其SDR貨幣籃子當中納入人民幣,是人民幣國際化的重要里程碑。該決定既是對人民幣國際化已有進程的一種追認,因爲其量度指標要求人民幣無論在貿易還是金融領域的國際使用都要達到一定規模,也是對人民幣未來進一步國際化的一種推動,因爲它會帶來對人民幣資產更多的需求。然而,之後緊接著發生了人民幣匯率的攻防戰。在人民幣兌美元匯率繼續承受貶值壓力的情況下,人民幣國際化之路能否和如何走下去便是一個全新的課題。

As of end-2015, the IMF decided to include the RMB in

the SDR currency basket, which is an important

milestone for the internationalization of the RMB. As the

quantitative indicators require RMB to achieve certain

scale in the international usage in both trade and

financial sector, this decision is not only an

acknowledgement of the progress of the RMB

internationalization, but also motivation for further RMB’s

internationalization progress in the future, as this will

trigger more demand for RMB assets. However, this was

swiftly followed by the high-stake battles of the RMB

exchange rate. Given the persistent depreciation

pressure on the RMB against the USD, whether the

RMB will continue on its internationalization journey and

how the RMB can progress further will be a brand new

topic.

人民幣在國際儲備貨幣家庭當中剛剛入門,對其的要求可能會更高。另外,人民幣匯率是有管理的浮動匯率,市場參與者對有管理還是有一定的期望,人民幣的持份者因爲其利益所在當然希望通過管理,人民幣匯率能夠只升不跌,或是不會給其投資造成匯兌損失。這種期望未必合理,但就很現實,遂對人民幣在貶值壓力下的國際化帶來挑戰。

As the RMB had just joined the league of international

reserve currencies, the expectations towards RMB may

be higher. In addition, the RMB’s exchange rate is

managed-float, therefore market participants will

generally form certain expectation towards the managed

regime. RMB stakeholders with personal interests will

definitely hope that RMB exchange rate will only

appreciate or at least not to incur exchange rate losses in

their investment through the managed regime. This

expectation may not be reasonable but it is very realistic,

which brings challenges to the RMB internationalization

under depreciation pressure.

12

15

Within the six years’ period between 2010 and 2015, the

USD had experienced a strong rally up to 38%.

According to the statistics in the SDR’s preliminary

assessment report by the IMF in August 2015, the

changes in the positions of USD and EUR were evident,

as the international reserve currency status of the USD

had risen on almost every aspect while that of EUR had

plummeted. It is worth noting that the dollar’s share had

only declined in terms of trade finance utilization, and that

of EUR had also declined. Within the same period, the

use of the RMB as a trade finance currency had

increased by 2%, while the absolute advantage enjoyed

by the USD remained unchanged. On the other hand,

the exchange rate of GBP and JPY also depreciated

against the USD within the same period, amongst which

GBP was relatively stronger while JPY weaker than

EUR. Their share generally declined. However as their

shares are not big to begin with, the impact and

significance of increment or decline in their proportions

are relatively limited.

在2010年至2015年這6年期間,美元錄得一輪升浪,高低升幅曾達到38%。根據IMF 2015年8月SDR初步檢討報告當中的數據,美元和歐元榮辱互見,美元的國際儲備貨幣地位幾乎全方位提升,歐元則下降。值得指出的是,美元僅在貿易融資方面使用的佔比下降,同時歐元佔比也在下降,期間是人民幣作爲貿易融資貨幣取得兩個百分點的佔比提升,但美元的絕對優勢不變。另外,期間英鎊和日圓兌美元也錄得貶值,其中英鎊相對稍強,日圓就比歐元更弱,其各個佔比降多於升,惟其比重本來就不大,故升跌的影響和意義也相對有限。

13

According to the IMF, the RMB fulfilled the criteria of

joining the SDR currency basket with one of the

supporting factors coming from exports, and the other

from the progress achieved by the RMB in a series of

international financial indicators in the past 5 years. With

reference to the changes of other major international

reserve currencies within the same period, it can be

deduced that changes in exchange rate will directly

influence the status of an international reserve currency.

IMF認爲人民幣符合加入SDR貨幣籃子的標準,其中一半來自中國出口所提供的支持,另外一半則是來自人民幣在過去5年内在一系列國際金融領域指標當中取得的進展所提供的支持。參考其他主要國際儲備貨幣同期地位的沉浮,就可以看出匯率的變化對一隻國際儲備貨幣的地位的影響是相當直接的。

15

Based on the above, the most important measuring

indicators of the internationalization progress of a

currency in the financial sector are the stock indicators,

such as the size of official foreign reserves, size of

international banking liabilities, size of international debt

securities, etc. They are complemented by the flow

indicators such as the issuance of international debt

securities, cross-border payments, trade finance, FX

market transactions, etc. The RMB has already

successfully placed itself among the top five currencies

globally in these areas. Currently, the shares taken up by

the RMB are still considerably small, with the highest

recorded in trade finance at 3.4% while others are still at

low single-digit numbers. In the future, if the RMB

continuously faces depreciation pressure, the impact on

its flow indicators may be considerably small. This is

because the volatility of the RMB exchange rate under

the depreciation expectation will be higher, therefore

RMB-related trading and payment transactions may not

necessarily decline. However, the impact on the most

important stock indicators may be larger.

從上所見,量度一隻貨幣在金融領域國際化程度的指標最主要的是存量指標,如官方外匯儲備持有的規模、國際銀行業負債規模、國際債券市場規模等,輔以流量指標如國際債券發行量、跨境支付、貿易融資和外匯市場交投等。人民幣在這些領域多已躋身全球前五大貨幣之列,但佔比則較小,最高為貿易融資的3.4%,其他佔比為更低的單位數字。未來人民幣如果持續承受貶值壓力,對流量指標的影響可能相對較小,因爲貶值預期下匯率波幅會擴大,人民幣相關的交易性和支付性的往來未必會減少,但對最重要的存量指標的影響就可能較大。

14

人民幣得以成功納入SDR,新的貨幣籃子將在今年10月份開始生效,而非以往在新一年的第一天開始生效,IMF的考慮是讓有興趣配置人民幣的央行和貨幣當局有充足的時間作出組合調整。但如果人民幣在今年連續第3年兌美元貶值,同時爲了順應SDR收窄離岸和在岸價差的要求而令CNH大幅波動、CNH Hibor大幅抽高,那麽有興趣配置人民幣資產(主要是債券)的央行就要面對三大挑戰:其取得人民幣資金的成本會增加;配置人民幣資產後要面對的匯率風險會增加;其最主要的投資標的人民幣主權類債券因爲是避險首選,其收益率偏低。其投資決定困難,有可能先觀望爲主。如果這些央行從分散投資的角度依然想配置人民幣資產,它們很可能需要對沖人民幣匯率風險,就意味著在買入人民幣債券的同時要沽售遠期人民幣,以鎖定匯率,規避匯率風險,但這會增加人民幣的貶值壓力和預期,對人民幣匯率穩定的影響複雜化。對投資者而言是一個難題,對監管者而言也是一個難題。

The RMB is successfully added to the SDR and the new

currency basket will be effective from October this year.

This is different from previous practice where changes

will be effective from the first day of a new calendar year.

The major consideration of the IMF is to allow central

banks and monetary authorities with interest in asset

allocations into the RMB to have sufficient time to

conduct portfolio adjustments. However if the RMB

depreciates against the USD this year for the third year

consecutively, and at the same time, to fulfill SDR’s

requirement by narrowing the spread between offshore

and onshore exchange rates which may cause CNH to

exhibit higher volatilities and CNH Hibor to increase

dramatically, then central banks with interests in RMB

assets (mainly in bonds) will face three major challenges:

the increasing cost to obtain RMB funding; the increasing

exchange rate risks following asset allocation into the

RMB; RMB sovereign bonds, a major underlying

investment asset primarily for safety reasons, have lower

yields. Therefore, central banks may face difficulties in

making investment decisions and may possibly adopt a

“wait and see” approach. If from the perspective of risk

diversification, those central banks who are still

interested to increase allocations in the RMB assets will

have to sell RMB forwards at the same time while

purchasing RMB bonds, in order to lock-in the exchange

rate and mitigate exchange rate risk. But this will

increase the pressure and expectation of depreciation on

the RMB, which will further complicate the RMB

exchange rate stabilization. This is a challenge for both

the investors and also the regulators.

15

As such, if the market condition changes drastically and

there is an imminent need to make a decision between

the stability of the RMB exchange rate and the progress

of internationalization, given that both cannot be

achieved at the same time, it is highly probable that

exchange rate stability will be the primary focus and

internationalization will be secondary.

據此,如果市場環境嚴峻到必需在人民幣匯率穩定和國際化之間作出一個選擇,而不能同時兼顧時,可能的政策選擇會是以匯率穩定爲主、國際化為輔。

在匯率穩定的目標之下,如果需求減弱,就要減少供應,那麽離岸人民幣資金池就會收縮,流動性偏緊,資金成本上升,才能有效穩住CNH匯率,但這樣一來,人民幣國際銀行業負債將難以擴展,甚至可能收縮。而在人民幣國際債券市場方面,同樣的因素會影響點心債的發行,如2015年香港地區點心債累計發行841億元人民幣,較2014年的2138億元減少六成。不過,熊貓債發行就有明顯進展,2015年共計65億元人民幣熊貓債的發行量創下新高。兩者皆是人民幣國際債券,而且不無替代效應,惟熊貓債的發行量迄今小於點心債,如果不能完全補充的話,整個人民幣國際債券市場的相關指標也將承受壓力。

Under the target of exchange rate stability, if demand

weakens, the corresponding supply will also have to be

reduced. As a result, the offshore RMB liquidity pool will

shrink, which will cause the liquidity to tighten and

funding cost to increase, only then can the CNH

exchange rate be effectively stabilized. However, under

this scenario, it will be difficult for the RMB international

banking liabilities to further expand. Instead they may

even shrink. With regard to the RMB international debt

securities market, the same factor will affect the issuance

of Dim Sum bonds. For example, the total cumulative

issuance of Dim Sum bonds in Hong Kong in 2015 was

RMB 84.1bn, down by 60% compared to the RMB

213.8bn in 2014. On the other hand, the issuance of

Panda bonds made impressive progress. In 2015, the

total issuance of Panda bonds hit a historical high of

RMB 6.5bn. Both are considered RMB international debt

securities, and are not mutually exclusive. However, the

issuance of Panda bonds is still smaller than the Dim

Sum bonds. If they could not complement for each

other’s shortfall, the relevant indicator of the overall RMB

international debt securities market will also be under

pressure.

RMB 專題研究

RMB Offshore Market Insights

專題二: 境外機構持有人民幣資產分析及對離岸市場影響

Analysis of RMB Asset Holdings of Foreign Institutions and the Impacts

on Offshore Market

經濟研究員 巴晴 Qing Ba, Economist

“811”匯改以來,離岸人民幣CNH匯率出現波動,境外人民幣資產規模亦出現收縮。美聯儲啟動加息週期,中國經濟下行壓力持續,外匯儲備、外匯佔款出現連續數月下降加劇了市場對人民幣未來走勢的擔憂。離岸人民幣CNH匯率反應相對敏感,兩地匯率價差不時拉闊,數次出現了匯差擴大至1,600基點以上的情況。另外,在岸市場上出現了一定規模境外機構減持人民幣資產情況。截至2015年11月,境外機構持有的人民幣資產規模較2015年高峰時期下降了7,200億元人民幣,而離岸市場上人民幣資產規模也收縮了近一成半。

Since the exchange rate reform on August 11, the

offshore RMB exchange rate (CNH) has been volatile

and the total size of offshore RMB assets has also

dwindled. The initiation of rate-hike cycle by the Fed, the

considerable downward pressure on China’s economy

and the decline in foreign exchange reserves and funds

outstanding for foreign exchange for consecutive months

has heightened the markets’ worries of the RMB’s future.

The CNH is quite sensitive, as the exchange rates of

both onshore and offshore diverged from time to time,

and there were multiple times where the spread peaked

at 1,600 pips and above. On the other hand, there were

also sizable reductions in RMB assets held by foreign

institutions in the onshore market. As of end-November

2015, the amount of RMB assets held by foreign

institutions declined by RMB 720bn from the historical

high. The size of RMB assets in the offshore market has

also shrunk by almost 15%.

在近期跨境監管政策頻出的背景下,兩地匯差時而擴大,在一定程度上反映出市場未能完全出清,人民幣貶值陰影揮之不去,難免對境外投資者持有人民幣資產信心產生一定影響。如何穩定境外投資者持有人民幣資產信心,避免更多境外投資者賣出人民幣資產,對CNH造成較大的貶值壓力,可能是近期離岸市場面臨的挑戰之一。

Against the backdrop of frequent announcements of

cross-border regulatory policies recently, the spread

between the onshore and offshore exchange rates

sometimes widens. At a certain level, it reflects that the

market conditions are not clear and the gloom of RMB

depreciation pressure persists, which influences the

confidence of investors towards holdings of RMB assets.

The most imminent challenge is how to regain the

confidence of foreign institutions in RMB assets, to

prevent more foreign investors from selling RMB assets

which may cause further depreciation pressure on the

CNH.

16

15

Secondly, there are also foreign institutions to hold RMB

assets in each offshore center. As of end-2015, the

assets mainly included RMB deposits and certificate of

deposits which aggregately amounted to approximately

RMB 1,010bn in Hong Kong, RMB deposits of

approximately RMB 310bn in Taiwan and also other

RMB assets in other offshore centers, with the total

amount of appropriately RMB 1.5tn.

第二,各離岸中心也有境外機構持有的人民幣資產。截至2015年底,主要包括香港離岸市場人民幣存款及存款證共約10,100億元,台灣人民幣存款約3,100億元,再加上其他離岸中心的人民幣資產,大約1.5萬億元。

17

Currently, the onshore RMB financial assets owned by

foreign institutions amounted to approximately RMB

3,609bn (as of end-November 2015), including RMB

assets in equities held by foreign institutions, bonds held

by non-residents onshore, RMB deposits held by non-

residents in onshore banks, and loans from offshore

institutions to onshore institutions.

目前境外機構持有的境內人民幣金融資產大約有36,090億元(截至2015年11月底),其中包括:境外機構持有的股票類人民幣資產;非居民在境內持有的債券;非居民在境內銀行的人民幣存款;以及境外機構對境內機構的貸款。

Thirdly, foreign institutions (such as central banks etc.)

can also obtain RMB assets through bilateral currency

swap agreements. Some market participants worry that

the bilateral currency swap agreements signed between

China and other countries may induce foreign institutions

who hold a huge amount of RMB assets to liquidate

under the expectation of RMB depreciation, exerting

depreciation pressure in the offshore market. In fact, as

the bilateral currency swap agreements are merely

liquidity commitments by the People’s Bank of China

(PBOC) to other central banks, and not the actual

amount of RMB lent to or actual balance held by foreign

institutions. According to statistics by the PBOC, as of

end of September 2015, the actual balance of RMB

drawn by offshore monetary authorities amounted to

only RMB 23bn, a very small portion of the total size of

RMB funds overseas.

第三,境外機構(如央行等)也可以通過互換協定獲取一定人民幣資產。市場上有人擔心中國簽訂的人民幣貨幣互換會導致境外機構持有大量人民幣資產,在人民幣貶值預期下出現拋售,對離岸市場形成貶值壓力。實際上,由於互換協議僅僅是中國央行對其他央行的借款承諾,而非實際借出人民幣或境外機構實際持有量。央行數據顯示,截至2015年9月末,境外貨幣當局實際動用人民幣餘額僅為230億元,佔海外人民幣資金量的很小一部分。

15

By rough estimation, the RMB assets held by foreign

institutions is between RMB 2tn - 2.5tn, which is limited.

So even if there are considerably large liquidations in

RMB assets in the offshore market, China will be able to

handle it through its forex reserve. However, it is worth

noting that when there is huge selling pressure in the

offshore market, the spread between the CNH and CNY

exchange rates may also widen, which may in turn

affects the onshore market. Therefore, to narrow the

spread between the CNH and CNY, it is especially

important to manage the expectations of the RMB

exchange rate.

初步估算,境外機構持有的人民幣資產大約為2-2.5萬億元人民幣,整體規模有限,即使在離岸市場出現較大規模人民幣資產減持的現象,中國外儲也有能力消化。當然需要注意的是,當離岸市場上出現拋售壓力時,CNH與CNY之間有可能持續出現價差,差價越大,會反過來影響在岸市場。所以,收斂CNH與CNY的匯率差價,對管理人民幣匯率預期尤為重要。

18

目前央行主要通過加強資本帳戶宏觀審慎管理,收緊境外流動性等操作,穩定CNH匯率。短期內政策效果明顯,兩地匯差明顯收窄,人民幣匯率成功企穩。長遠而言,近期CNH匯率波動是對離岸市場一次有益考驗,有利於人民幣國際化的長遠發展。人民幣靠“單邊升值”去支撐國際化加速發展,是不可持續的。穩步的國際化,必須建基於海外對人民幣資產的真正信心和需求,以及離岸市場的多樣化發展。加快推動匯率市場化改革,從軟盯住美元轉向參考一籃子貨幣,以實際行動不斷推進國內金融體系的完善、開放和市場主導改革,人民幣國際化將會繼續前進。

At the moment, the major measures undertaken by the

PBOC to stabilize the RMB exchange rate are through

the strengthening of macro-prudential management of

capital account and the tightening of offshore liquidity. In

the short term, these policies are seen to bring significant

results, with the narrowing spread between the two

exchange rates and the successful stabilization of the

RMB exchange rate. In the long term, the recent volatility

in the RMB exchange rate is a fruitful experience for the

offshore market and is beneficial to the long term

development of RMB internationalization. The

dependence on “one-way appreciation” of the RMB to

accelerate the internationalization progress is

unsustainable. The stable development of the RMB

internationalization must be built on the real confidence

and demand from overseas towards RMB assets and

the diversified development of the offshore market. In

order to accelerate the reform of exchange rate, it can

start from the transition of purely focusing on USD to

referring to a basket of currencies, and through the

continuous facilitation of the enhancement, liberalization

and market-oriented reforms of the onshore financial

system. The RMB internationalization will continue on its

journey.

聲明:本報告僅供參考之用,不反映中銀香港意見,不構成任何投資建議。 Disclaimer: This report is for reference and information purposes only. It does not reflect the views of Bank of China (Hong Kong) or constitute any investment advice.