Embed Size (px)

Citation preview

Howcanenvironmentalpoliciesbedesignedtobecompatiblewith(green)economicgrowth?Evidencefromfirms

andindustries

AntoineDechezleprêtre

OECDGlobalForumonEnvironment2016

Overplayedcompetitivenessconcernsinfluencepolicydesign

• Environmentalpoliciescanleadtosmallnegativeeffectsontrade,employment,plantlocationandproductivity– Inpollution- &energy-intensive,trade-exposedsectors

• Theseimpactsaresmallcomparedtootherdeterminantsoftradeandinvestmentlocation– Impactsoverplayed,butfirmslegitimatelyvoicetheirconcerns

• Infearofpotentialadversecompetitivenesseffects,recentclimatepoliciesshieldindustrialsectorsfromfullregulatorycosts

TheperverseeffectsofEUETSfreeallocationrule:thecementindustry

Observed cement installationsby activity level

Theoretical distribution

0

10

20

30

40

50

Num

bero

finstalla

tions

2012- LDCountries

0

10

20

30

40

50

Num

bero

fInstalla

tions

2012CF- LDCountries

Ø5.8Mtexcessclinkerproductionin2012(=5.2MtCO2emissions)

Activity level thresholds: free allocation reduced by 50% (resp. 75%) if production falls by 50% (resp. 75%)

Worryingconsequences

• CO2intensityoftheEuropeancementsector+5% 2011-2014!– EU2050objective:-80%CO2emissions

• Cumulativesurplus:450Mcredits(=tonnesCO2)forthecementsector

• Freeallocationsarereceivedbylarge,carbon-intensiveincumbentfirms

• SMEswhohavedevelopedcommerciallyviablelow-carboncements(e.g.Ecocem,EMC,CarbonCure,BanahCEM)getnothing

Designingpoliciescompatiblewitheconomicperformance

• WorryingaboutlosersislegitimateØLeveltheplayingfieldattheconsumptionlevel(eg consumptiontax),withoutcreatingperverseincentivesthatdiscourageefficiencyandareincompatiblewithlongtermobjectives

• Growth-compatibleenvironmentalpoliciesneedtoencourageinnovationØSupportnewtechdevelopment,includingbynewentrants,throughinnovationpolicies

ØProvidestablepollutionpricingmechanisms

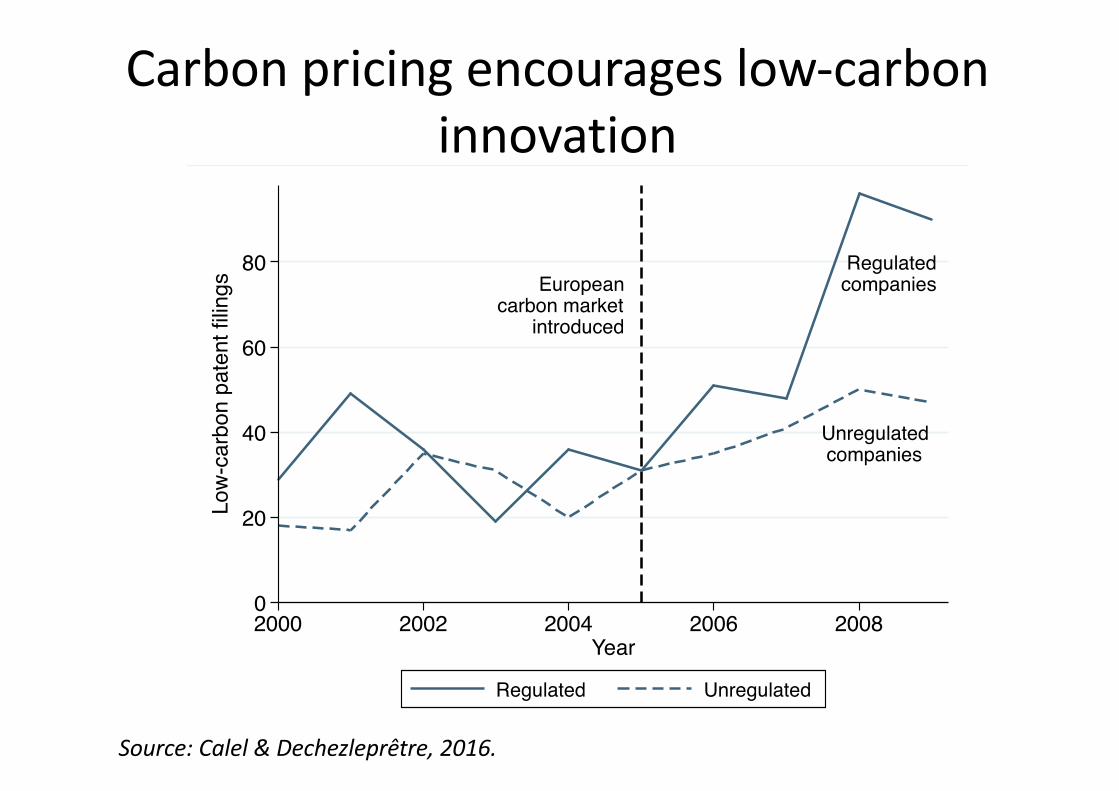

Europeancarbon market

introduced

Regulatedcompanies

Unregulatedcompanies

0

20

40

60

80

Low

-car

bon

pate

nt fi

lings

2000 2002 2004 2006 2008Year

Regulated Unregulated

Source:Calel &Dechezleprêtre,2016.

Carbonpricingencourageslow-carboninnovation

!0.3%

!0.2%

!0.1%

0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

Electricity%%dirty%

Car%%dirty%

Biotechs%

Electricity%clean%

Car%clean% Robot%

IT%Nano% 3D%

Baseline=averagetechnology

Source:author’scalculationsfromEPO’sPATSTATdatabase

Reversing thedangerous decline ingloballow-carbon innovation

20

40

60

80

100

Oil p

rice

(201

5 $)

3%

4%

5%

6%

Shar

e of

clim

ate-

rela

ted

inve

ntio

ns

1985 1990 1995 2000 2005 2010 2015Year

Low-carbon innovation Crude oil price

20

40

60

80

100

Oil p

rice

(201

5 $)

3%

4%

5%

6%

Shar

e of

clim

ate-

rela

ted

inve

ntio

ns

1985 1990 1995 2000 2005 2010 2015Year

Low-carbon innovation Crude oil price