Embed Size (px)

Citation preview

Page 1 Page 1

Iron Ore Production Costs

Michael Dixon

AME Group

March 2014

Page 2 Page 2

Outlook for Iron Ore Production Costs

Agenda

• Introducing AME

• Market outlook and what this means for production costs

• Impact of iron ore demand changes for costs

• Medium term cost influences & the

Outlook for production costs

Page 3 Page 3

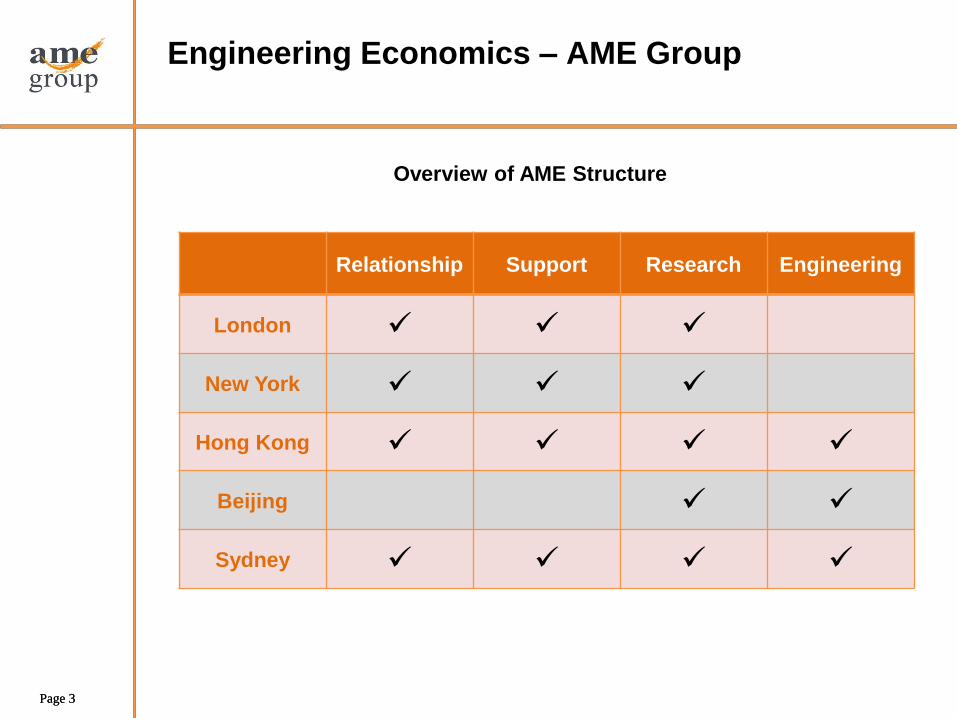

Relationship Support Research Engineering

London

New York

Hong Kong

Beijing

Sydney

Engineering Economics – AME Group

Overview of AME Structure

Page 4 Page 4

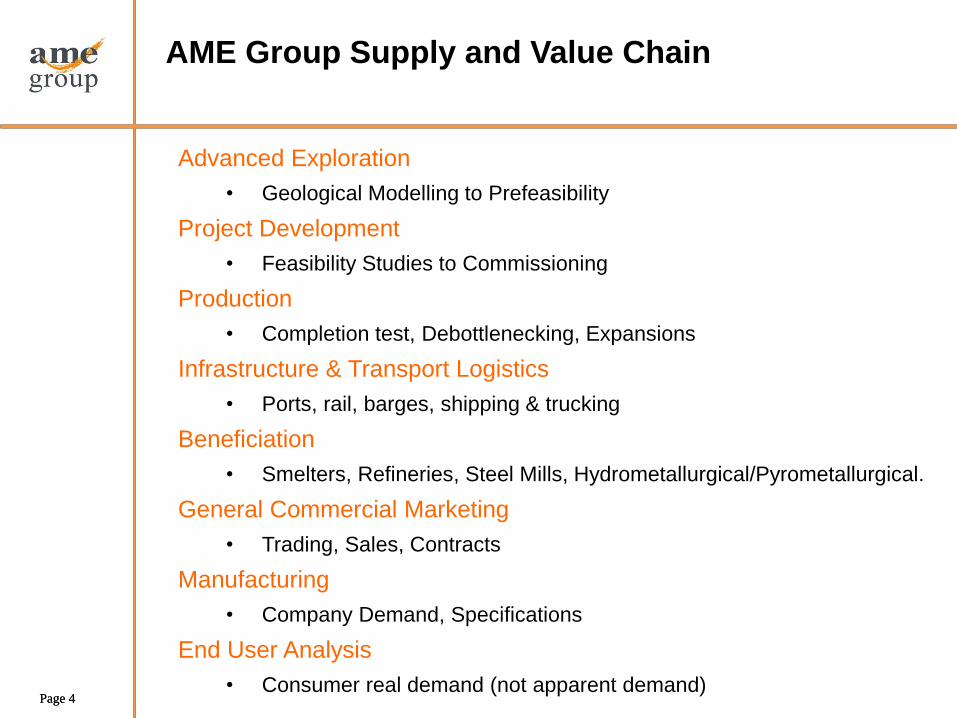

Advanced Exploration

• Geological Modelling to Prefeasibility

Project Development

• Feasibility Studies to Commissioning

Production

• Completion test, Debottlenecking, Expansions

Infrastructure & Transport Logistics

• Ports, rail, barges, shipping & trucking

Beneficiation

• Smelters, Refineries, Steel Mills, Hydrometallurgical/Pyrometallurgical.

General Commercial Marketing

• Trading, Sales, Contracts

Manufacturing

• Company Demand, Specifications

End User Analysis

• Consumer real demand (not apparent demand)

AME Group Supply and Value Chain

Page 5 Page 5

Outlook for Iron Ore Production costs

Agenda

• Introducing AME

• Market outlook and what this means for production costs

• Impact of iron ore demand changes for costs

• Medium term cost influences & the

Outlook for production costs

Page 6 Page 6

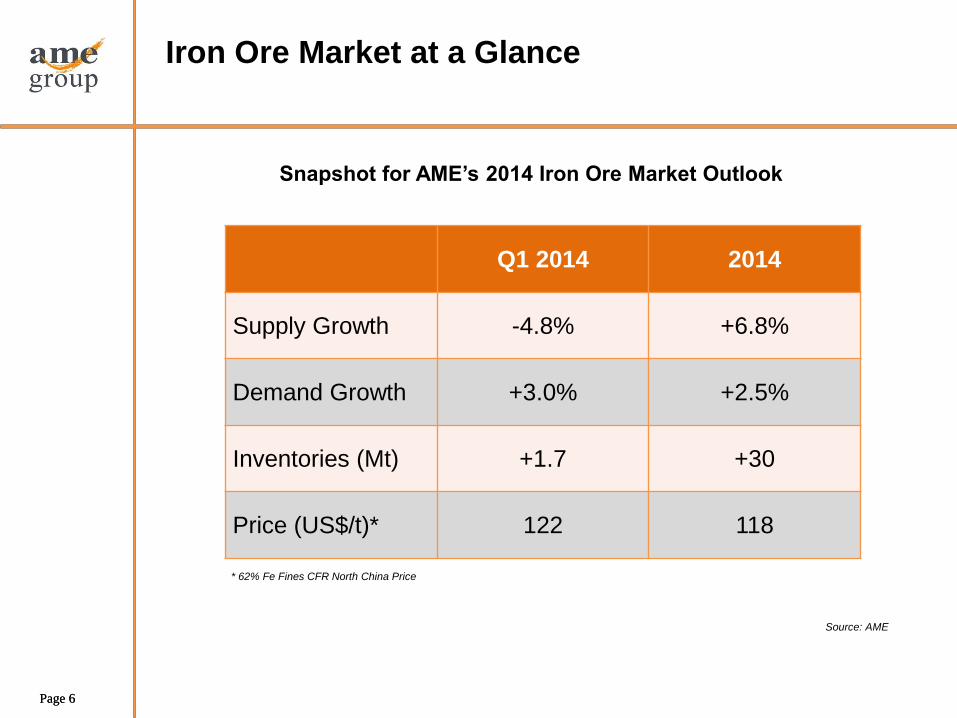

Iron Ore Market at a Glance

Q1 2014 2014

Supply Growth -4.8% +6.8%

Demand Growth +3.0% +2.5%

Inventories (Mt) +1.7 +30

Price (US$/t)* 122 118

Snapshot for AME’s 2014 Iron Ore Market Outlook

Source: AME

* 62% Fe Fines CFR North China Price

Page 7 Page 7

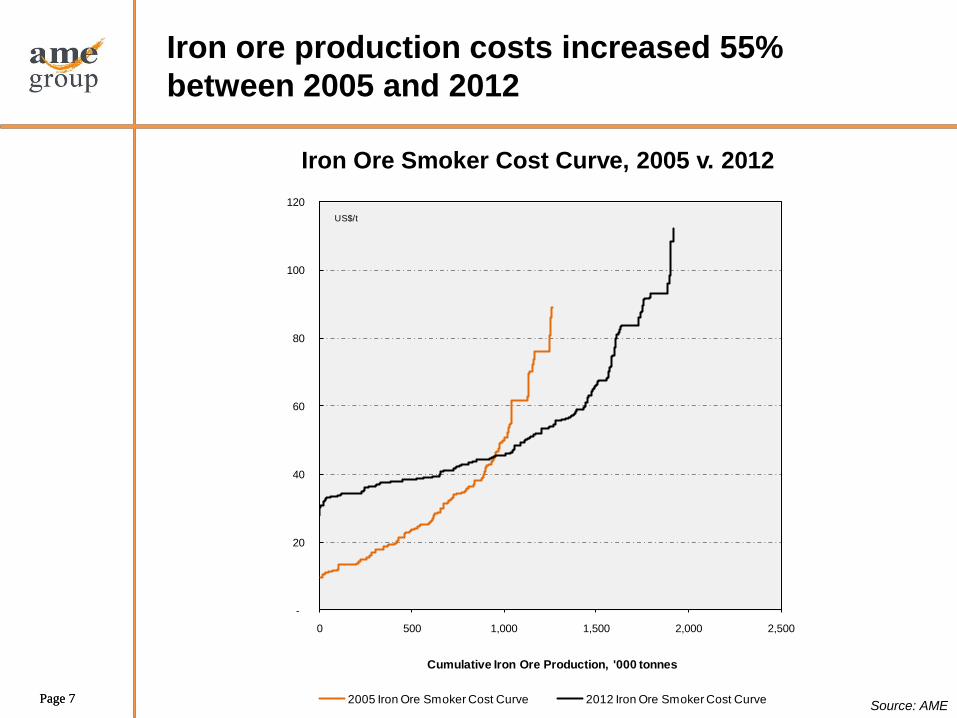

Iron ore production costs increased 55%

between 2005 and 2012

Iron Ore Smoker Cost Curve, 2005 v. 2012

Source: AME

-

20

40

60

80

100

120

0 500 1,000 1,500 2,000 2,500

Cumulative Iron Ore Production, '000 tonnes

2005 Iron Ore Smoker Cost Curve 2012 Iron Ore Smoker Cost Curve

US$/t

Page 8 Page 8

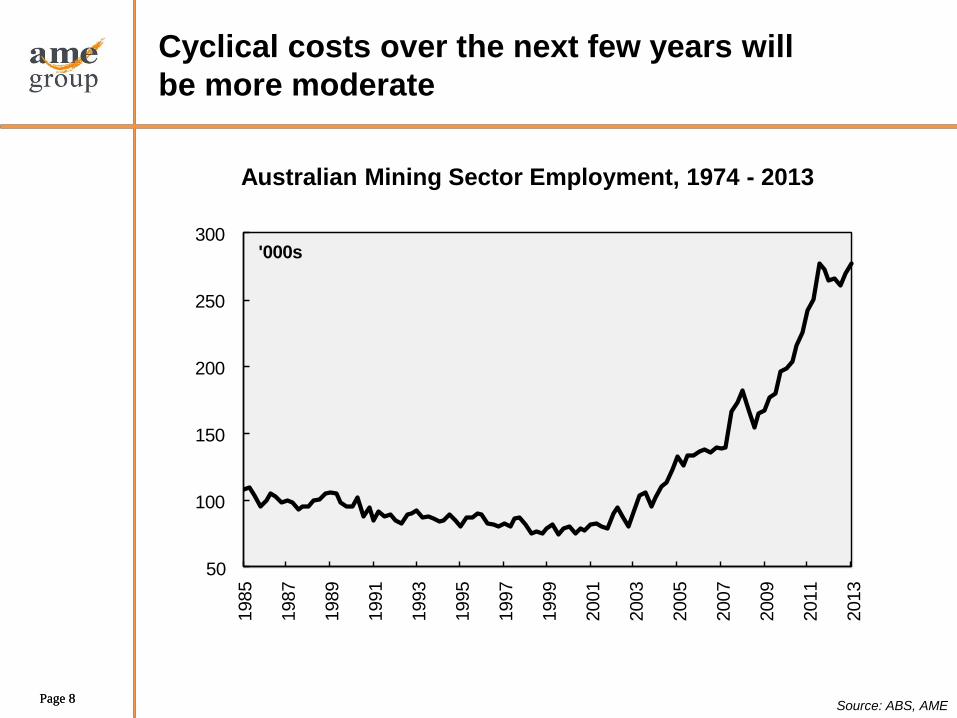

Cyclical costs over the next few years will

be more moderate

Australian Mining Sector Employment, 1974 - 2013

Source: ABS, AME

50

100

150

200

250

3001985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

'000s

Page 9 Page 9

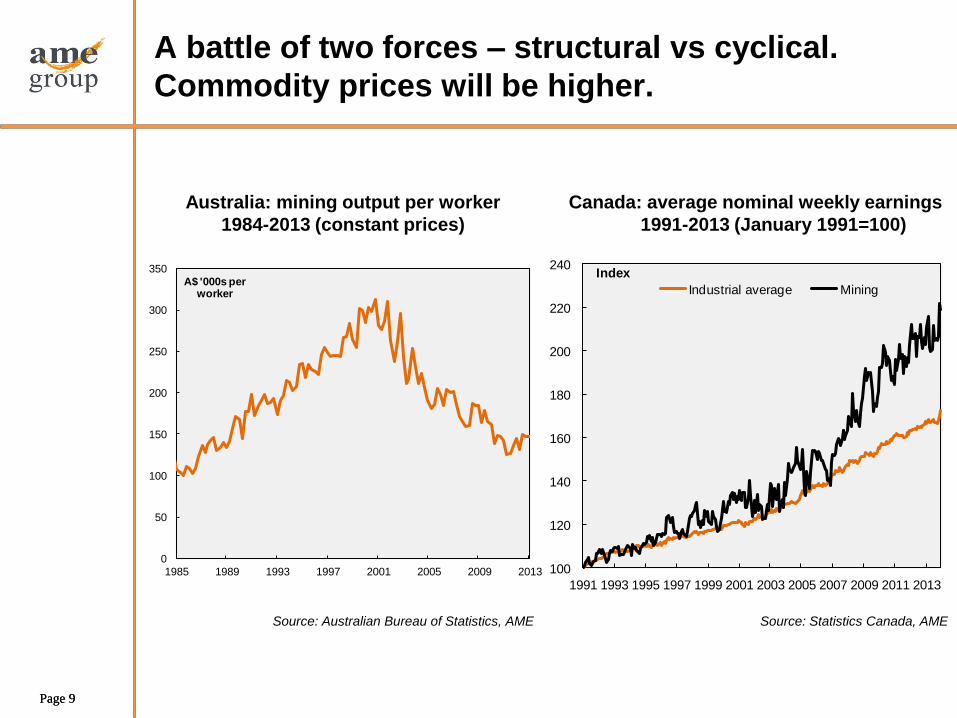

A battle of two forces – structural vs cyclical.

Commodity prices will be higher.

Canada: average nominal weekly earnings

1991-2013 (January 1991=100)

Source: Australian Bureau of Statistics, AME

Australia: mining output per worker

1984-2013 (constant prices)

Source: Statistics Canada, AME

0

50

100

150

200

250

300

350

1985 1989 1993 1997 2001 2005 2009 2013

A$ '000s per worker

100

120

140

160

180

200

220

240

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Index

Industrial average Mining

Page 10 Page 10

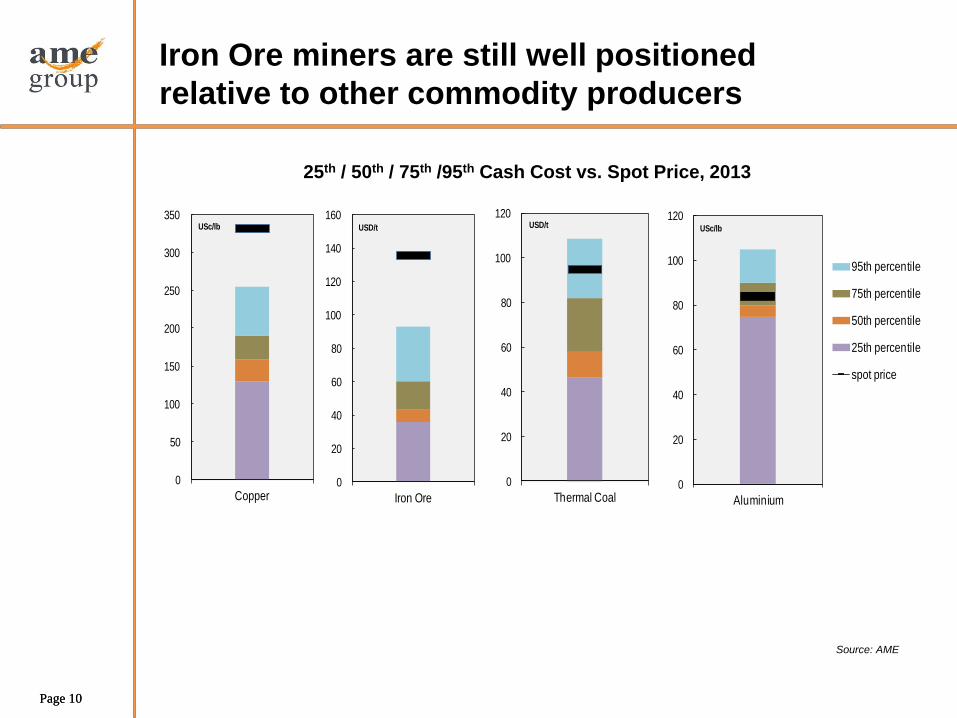

Iron Ore miners are still well positioned

relative to other commodity producers

25th / 50th / 75th /95th Cash Cost vs. Spot Price, 2013

Source: AME

0

50

100

150

200

250

300

350

Copper

USc/lb

0

20

40

60

80

100

120

140

160

Iron Ore

USD/t

0

20

40

60

80

100

120

Thermal Coal

USD/t

0

20

40

60

80

100

120

Aluminium

USc/lb

95th percentile

75th percentile

50th percentile

25th percentile

spot price

Page 11 Page 11

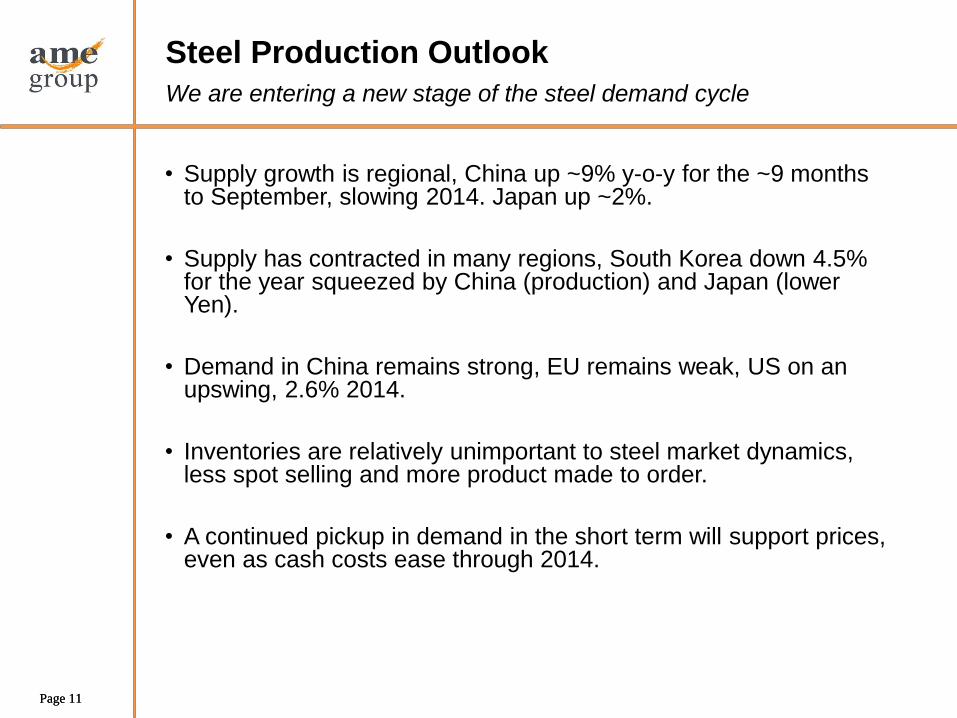

• Supply growth is regional, China up ~9% y-o-y for the ~9 months to September, slowing 2014. Japan up ~2%.

• Supply has contracted in many regions, South Korea down 4.5% for the year squeezed by China (production) and Japan (lower Yen).

• Demand in China remains strong, EU remains weak, US on an upswing, 2.6% 2014.

• Inventories are relatively unimportant to steel market dynamics, less spot selling and more product made to order.

• A continued pickup in demand in the short term will support prices, even as cash costs ease through 2014.

Steel Production Outlook

We are entering a new stage of the steel demand cycle

Page 12 Page 12

Outlook for Iron Ore Production costs

Agenda

• Introducing AME

• Market outlook and what this means for production costs

• Impact of iron ore demand changes for costs

• Medium term cost influences & the

Outlook for production costs

Page 13 Page 13

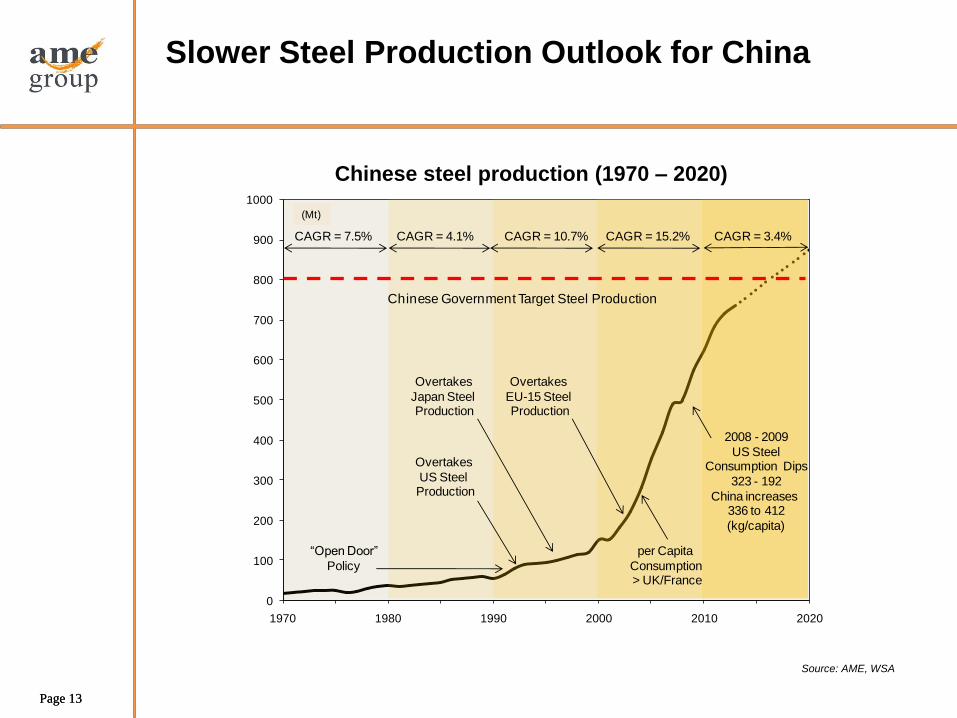

Source: AME, WSA

0

100

200

300

400

500

600

700

800

900

1000

1970 1980 1990 2000 2010 2020

Overtakes

US Steel Production

Overtakes

Japan Steel Production

Overtakes

EU-15 Steel Production

per Capita

Consumption > UK/France

2008 - 2009

US SteelConsumption Dips

323 - 192

China increases 336 to 412

(kg/capita)

Chinese Government Target Steel Production

CAGR = 7.5% CAGR = 4.1% CAGR = 10.7% CAGR = 15.2% CAGR = 3.4%

(Mt)

“Open Door”

Policy

Chinese steel production (1970 – 2020)

Slower Steel Production Outlook for China

Page 14 Page 14

• Historically, EAF production in China averaged around 30% of production until the early 1990’s.

• When steel production boomed from the early 90’s until the present the share of EAF production declined to less than 10%.

• The current share of scrap utilisation will be maintained over the next two decades.

• Dominance of BOF steelmaking route over EAF means Chinese steel producers can only use a limited portion of scrap in their feed.

• Chinese steelmaking will remain mainly blast furnace as there is a structural shift towards higher quality steels, by Government policy.

Will scrap displace Coal and Iron Ore?

Mini-mills do not pose a threat to demand over the next 20 years

Page 15 Page 15

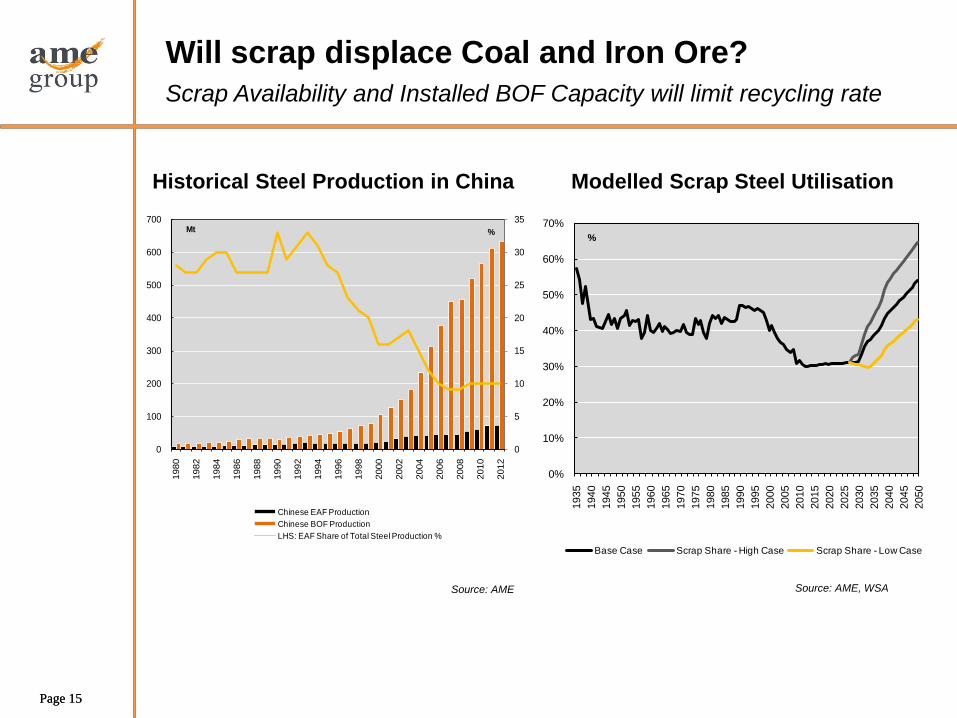

Historical Steel Production in China

0%

10%

20%

30%

40%

50%

60%

70%

1935

1940

1945

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

Base Case Scrap Share - High Case Scrap Share - Low Case

%

Modelled Scrap Steel Utilisation

Source: AME, WSA

(Mt) (%)

0

5

10

15

20

25

30

35

0

100

200

300

400

500

600

700

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

Chinese EAF Production

Chinese BOF Production

LHS: EAF Share of Total Steel Production %

Mt %

Will scrap displace Coal and Iron Ore?

Scrap Availability and Installed BOF Capacity will limit recycling rate

Source: AME

Page 16 Page 16

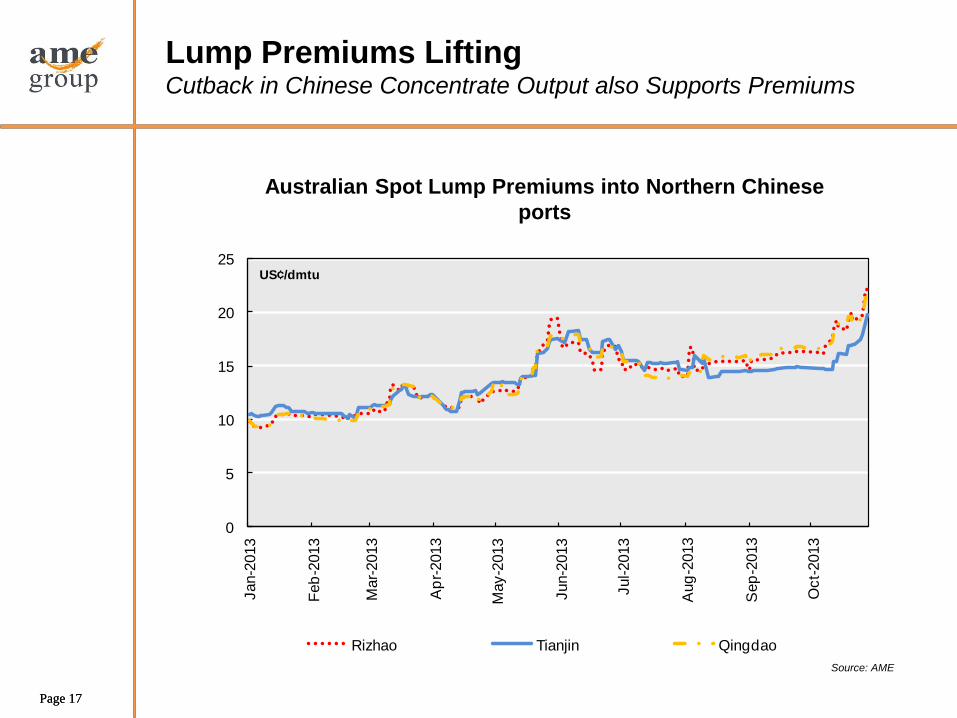

• Rio and BHP agreed on lump premiums with Chinese steelmakers for Q4 at 18- 19¢/dmtu – higher than 3Q premiums of 13- 14¢/dmtu.

• Japanese steelmakers negotiated lump premiums at 16¢/dmtu with one miner and 19¢/dmtu with another for the December quarter.

• North Asian mills were offered higher premiums in previous quarters with miners citing different demand conditions from China.

• Spot premiums have lifted above 20¢/dmtu as conc. output in China’s NE mines dropped, operating at 70% capacity due to colder weather.

• Higher concentrate prices, driven by lower supply, have prompted stronger lump demand.

Lump Premiums Lifting Shortage of Cargoes and Strengthening Demand as Sinter Plants Stop

Page 17 Page 17

0

5

10

15

20

25Jan-2

013

Feb

-2013

Mar-

2013

Ap

r-2013

May-2

013

Jun-2

013

Jul-2013

Aug

-2013

Sep

-2013

Oct-

2013

Rizhao Tianjin Qingdao

US¢/dmtu

Australian Spot Lump Premiums into Northern Chinese

ports

Source: AME

Lump Premiums Lifting Cutback in Chinese Concentrate Output also Supports Premiums

Page 18 Page 18

Outlook for Iron Ore Production costs

Agenda

• Introducing AME

• Market outlook and what this means for production costs

• Impact of iron ore demand changes for costs

• Medium term cost influences & the

Outlook for production costs

Page 19 Page 19

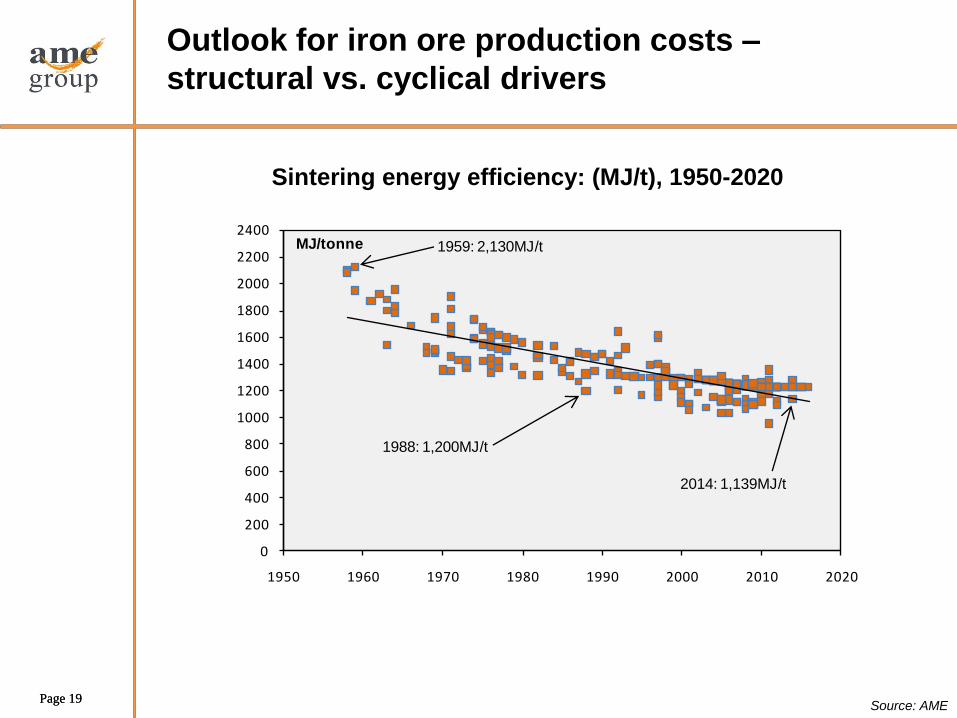

Outlook for iron ore production costs –

structural vs. cyclical drivers

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2200

2400

1950 1960 1970 1980 1990 2000 2010 2020

MJ/tonne 1959: 2,130MJ/t

1988: 1,200MJ/t

2014: 1,139MJ/t

Sintering energy efficiency: (MJ/t), 1950-2020

Source: AME

Page 20 Page 20

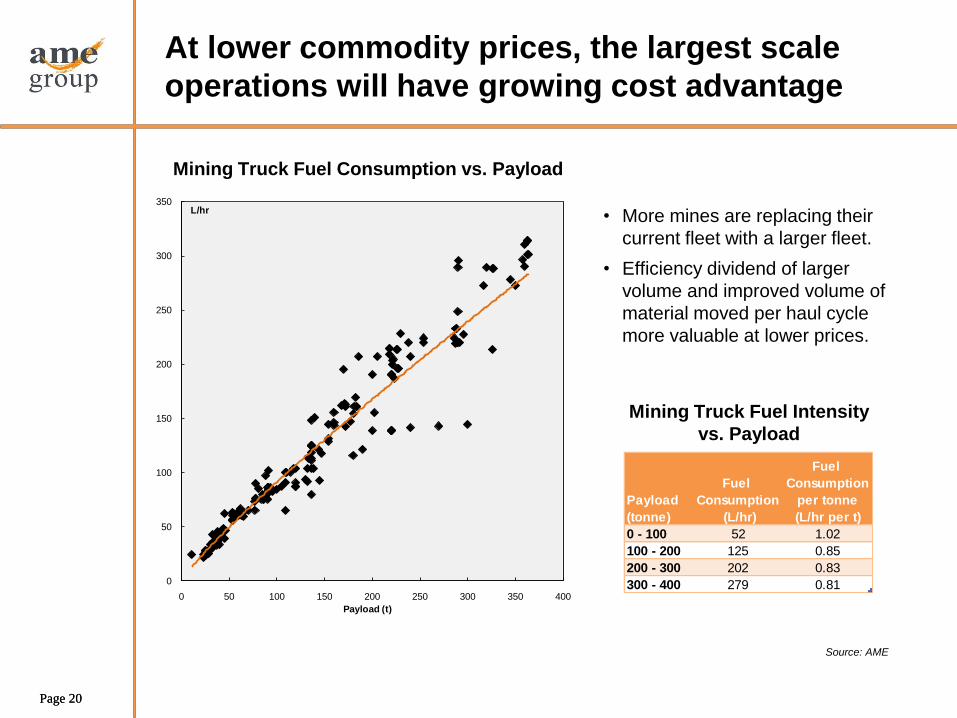

At lower commodity prices, the largest scale

operations will have growing cost advantage

Mining Truck Fuel Consumption vs. Payload

• More mines are replacing their

current fleet with a larger fleet.

• Efficiency dividend of larger

volume and improved volume of

material moved per haul cycle

more valuable at lower prices.

Source: AME

Mining Truck Fuel Intensity

vs. Payload

0

50

100

150

200

250

300

350

0 50 100 150 200 250 300 350 400

L/hr

Payload (t)

Payload

(tonne)

Fuel

Consumption

(L/hr)

Fuel

Consumption

per tonne

(L/hr per t)

0 - 100 52 1.02

100 - 200 125 0.85

200 - 300 202 0.83

300 - 400 279 0.81

Page 21 Page 21

A large proportion of Chinese Iron Ore mines are

uncompetitive

• Increasing strip ratios are forcing many Chinese iron ore mines to

go underground

• The majority of Chinese supply sits in the fourth quartile of the

cash cost curve.

• In 2013, 10-15% of Chinese capacity operating at $110/t-$140/t.

• Higher cost Chinese production will be displaced by additional

tonnes from Brazil, Australia and India

Page 22 Page 22

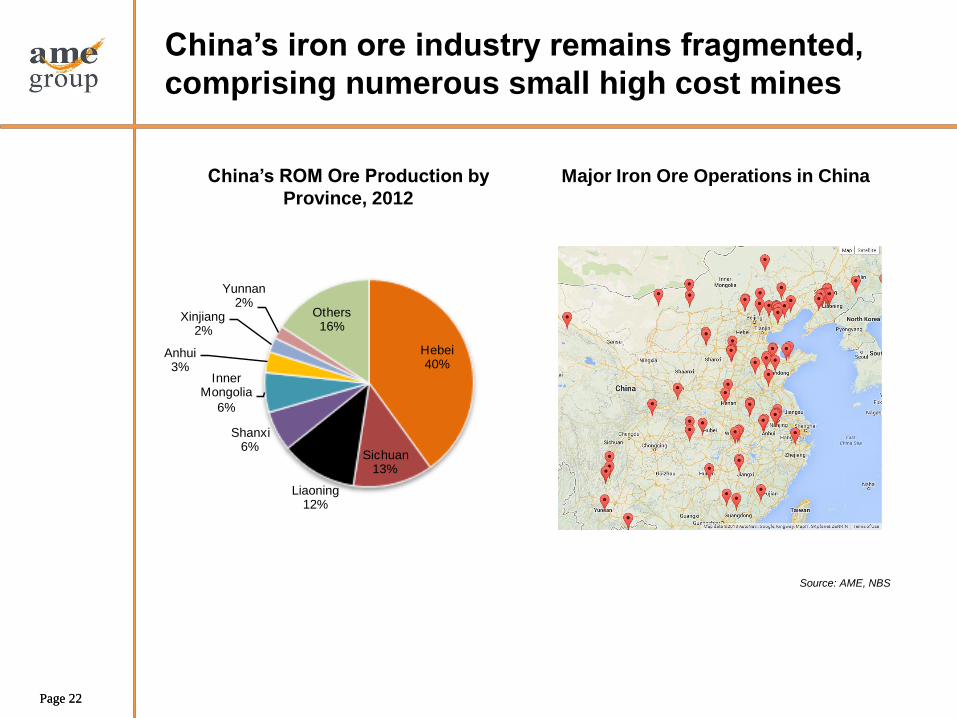

China’s iron ore industry remains fragmented,

comprising numerous small high cost mines

Hebei40%

Sichuan13%

Liaoning12%

Shanxi6%

Inner Mongolia

6%

Anhui3%

Xinjiang2%

Yunnan2%

Others16%

China’s ROM Ore Production by

Province, 2012

Source: AME, NBS

Major Iron Ore Operations in China

Page 23 Page 23

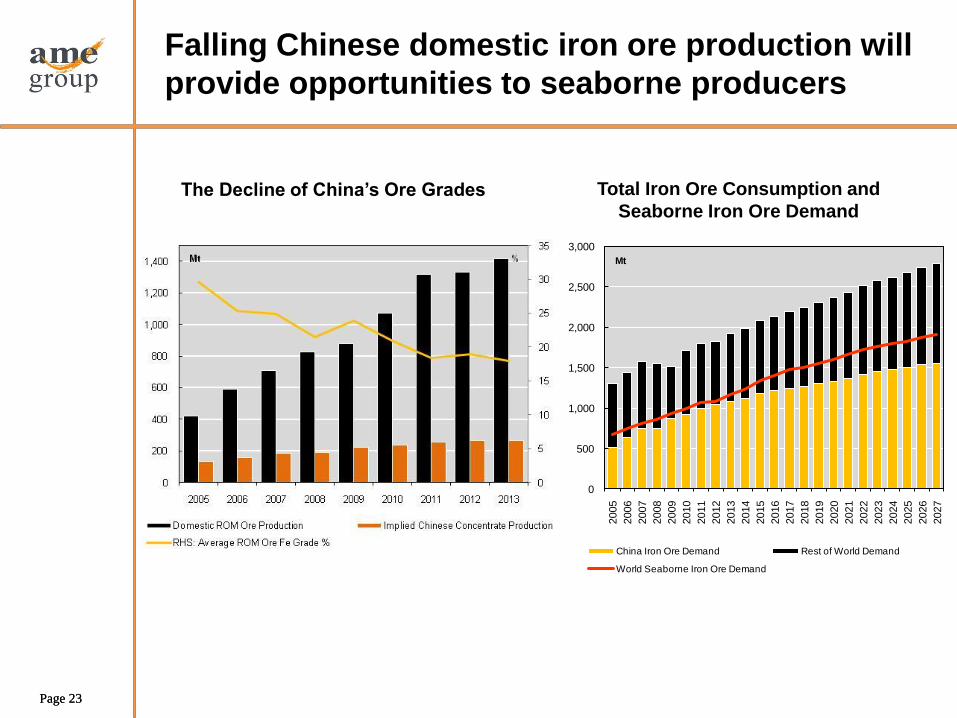

Falling Chinese domestic iron ore production will

provide opportunities to seaborne producers

The Decline of China’s Ore Grades Total Iron Ore Consumption and

Seaborne Iron Ore Demand

0

500

1,000

1,500

2,000

2,500

3,000

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

China Iron Ore Demand Rest of World Demand

World Seaborne Iron Ore Demand

Mt

Page 24 Page 24

Declining grade necessitates higher processing

cost for production

• Low ore grade in China necessitates additional beneficiation such

as multiple stage grinding and screening and magnetic separation,

which drives production costs higher.

• Iron ore deposits in China are generally low grade deposits with

high impurities, with deposit grade of as low as 5-15% Fe being

mined.

• The aggressive decline of China’s domestic ore grades will mean

Chinese seaborne demand will outpace China’s total consumption

over the short term.

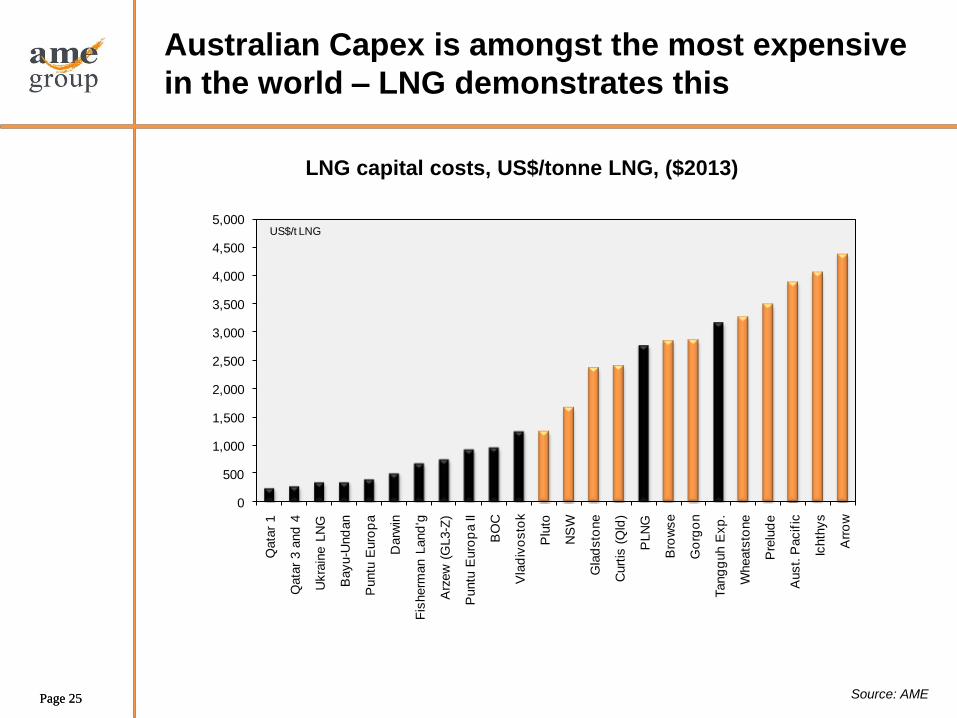

Page 25 Page 25

Australian Capex is amongst the most expensive

in the world – LNG demonstrates this

Source: AME

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Qata

r 1

Qata

r 3 a

nd

4

Ukra

ine L

NG

Bayu-U

nd

an

Puntu

Euro

pa

Darw

in

Fis

herm

an L

and

'g

Arz

ew

(G

L3-Z

)

Puntu

Euro

pa II

BO

C

Vla

div

osto

k

Plu

to

NS

W

Gla

dsto

ne

Curt

is (

Qld

)

PLN

G

Bro

wse

Go

rgo

n

Tang

guh E

xp

.

Wheats

tone

Pre

lud

e

Aust.

Pacif

ic

Ichth

ys

Arr

ow

US$/t LNG

LNG capital costs, US$/tonne LNG, ($2013)

Page 26 Page 26

Forward looking information Certain statements and graphics contained in this presentation may contain forward-looking information within the meaning of various securities laws. Such forward-looking

information are identified by words such as "estimates", "intends", "expects", "believes", "may", "will" and included, without limitation, statements regarding the company's plan of

business operations, production levels and costs, potential contractual arrangements and the delivery of equipment, receipt of working capital, anticipated revenues, mineral reserve and

mineral resource estimates, and projected expenditures. There can be no assurance that such statements will prove to be accurate; actual results and future events could differ

materially from such statements. Factors that could cause actual results to differ materially include, among others, metal prices, risks inherent in the mining industry, financing risks,

labour risks, uncertainty of mineral reserve and resource estimates, equipment and supply risks, regulatory risks and environmental concerns. Most of these factors are outside the

control of the company. Investors are cautioned not to put undue reliance on forward-looking information. Except as otherwise required by applicable securities statutes or regulation,

the company expressly disclaims any intent or obligation to update publicly forward-looking information, whether as a result of new information, future events or otherwise.

Copyright @ AME Group 2014

Contact Details and Important Information

For further details, please visit our website at www.amegroup.com

Hong Kong Sydney London New York

4/F Lucky Building

39 Wellington Street

Central, Hong Kong

AME House

342 Kent Street

Sydney NSW 2000

32 Hanover Square

London W1S 1JB

United Kingdom

Level 16, 733 3rd Avenue

New York NY 10017

United States

T: +852 2846 8220

F: +852 2801 5337

T: +61 2 9262 2264

F: +61 2 9262 2587

T: +44 203 714 8725

T: +1 646 790 5770