Embed Size (px)

Citation preview

1© GfK May 1, 2023 | E-Fashion 2016

GfK | Gino Thuij | E-Fashion – September 8 2016

The clash of the generations

(Online) Fashion overview

2© GfK May 1, 2023 | E-Fashion 2016

3© GfK May 1, 2023 | E-Fashion 2016

Industry Lead Fashion & Lifestyle

GfK

Gino Thuij

4© GfK May 1, 2023 | E-Fashion 2016

We have more than 13,000 experts in more than 100 countries

5© GfK May 1, 2023 | E-Fashion 2016

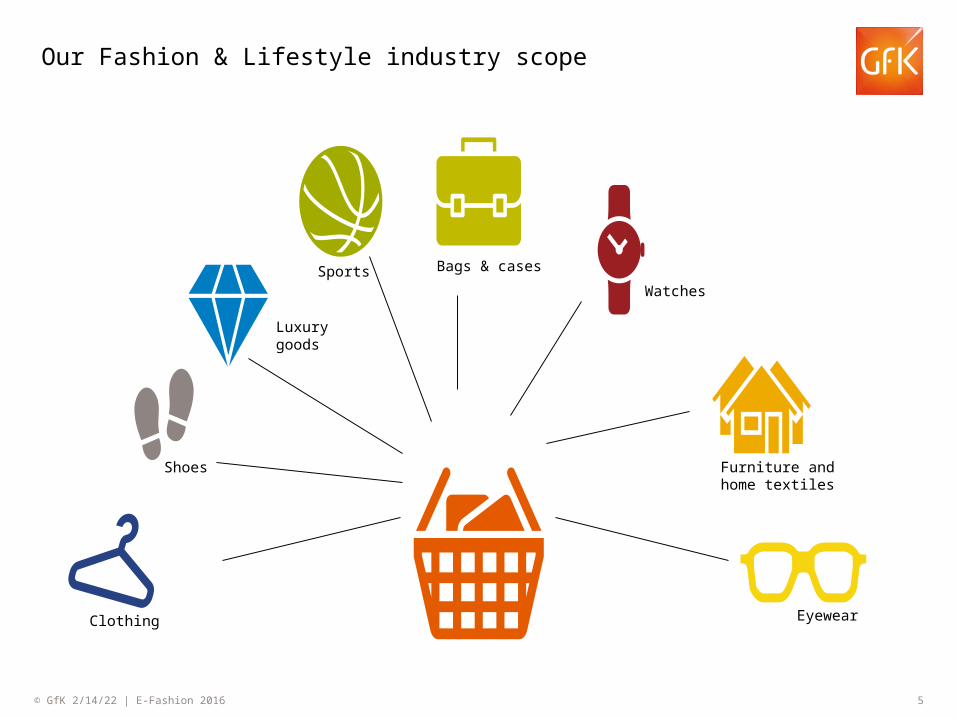

Our Fashion & Lifestyle industry scope

Bags & casesSports

Luxurygoods

Clothing

Watches

Eyewear

Furniture andhome textiles

Shoes

6© GfK May 1, 2023 | E-Fashion 2016

Clash of the generationsThe difference between generations regarding shopping for fashion

An international overviewHow is fashion shopping developing in Europe?

What’s going on in The Netherlands?Long term developments of (online) fashion in NL

Content

123

7© GfK May 1, 2023 | E-Fashion 2016

An international overview

8© GfK May 1, 2023 | E-Fashion 2016

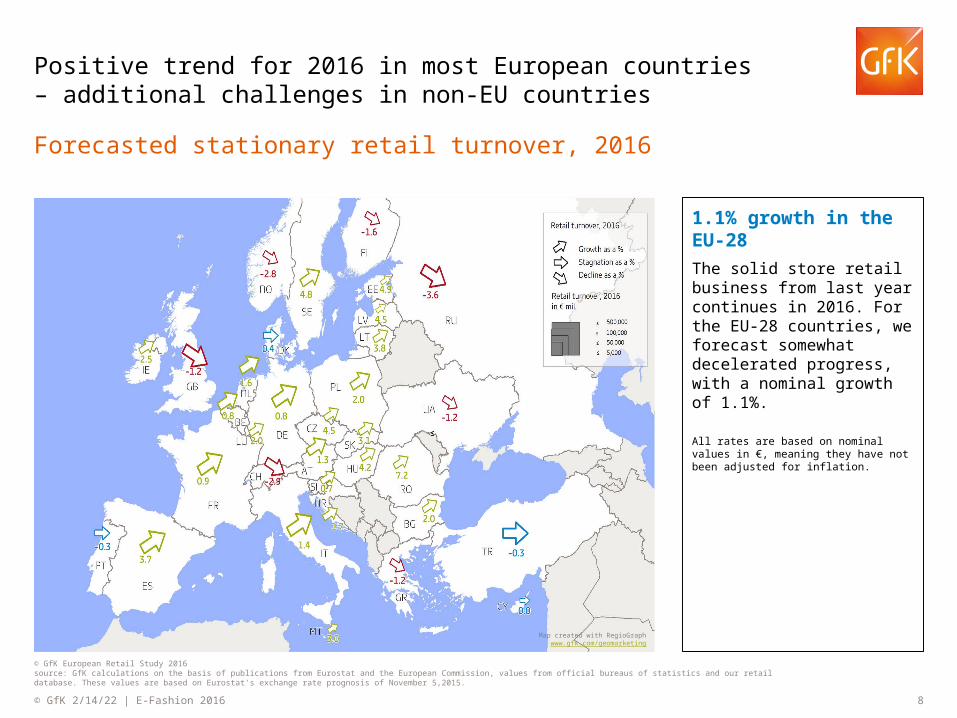

Positive trend for 2016 in most European countries – additional challenges in non-EU countries

Forecasted stationary retail turnover, 2016

© GfK European Retail Study 2016source: GfK calculations on the basis of publications from Eurostat and the European Commission, values from official bureaus of statistics and our retail database. These values are based on Eurostat‘s exchange rate prognosis of November 5,2015.

1.1% growth in the EU-28The solid store retail business from last year continues in 2016. For the EU-28 countries, we forecast somewhat decelerated progress, with a nominal growth of 1.1%.

All rates are based on nominal values in €, meaning they have not been adjusted for inflation.

Map created with RegioGraph www.gfk.com/geomarketing

9© GfK May 1, 2023 | E-Fashion 2016

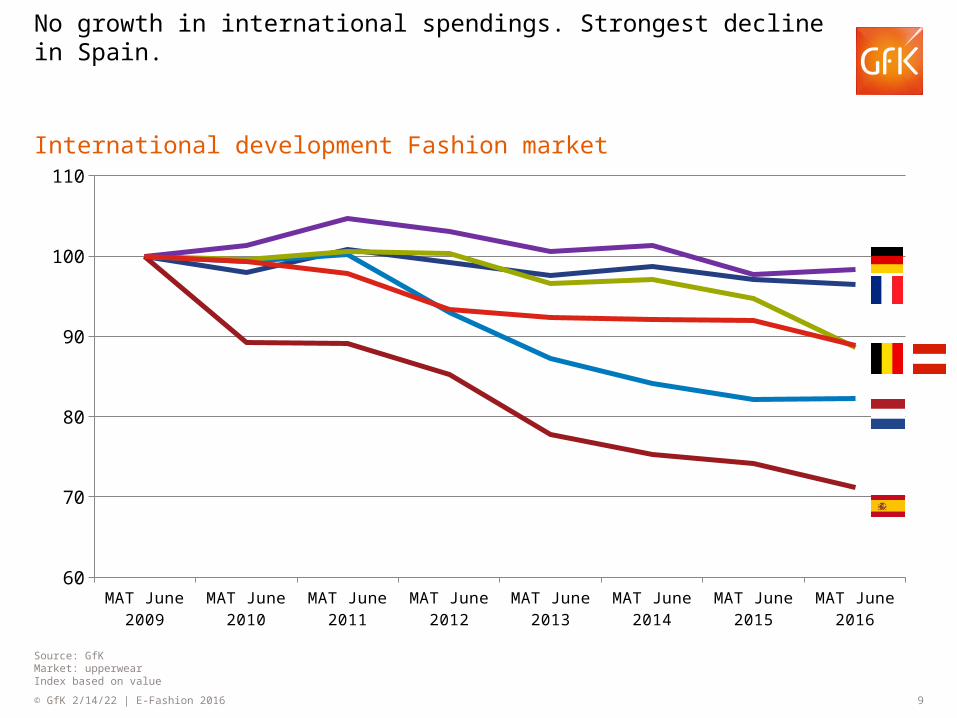

No growth in international spendings. Strongest decline in Spain.

MAT June 2009

MAT June 2010

MAT June 2011

MAT June 2012

MAT June 2013

MAT June 2014

MAT June 2015

MAT June 2016

60

70

80

90

100

110

Source: GfKMarket: upperwear Index based on value

International development Fashion market

10© GfK May 1, 2023 | E-Fashion 2016

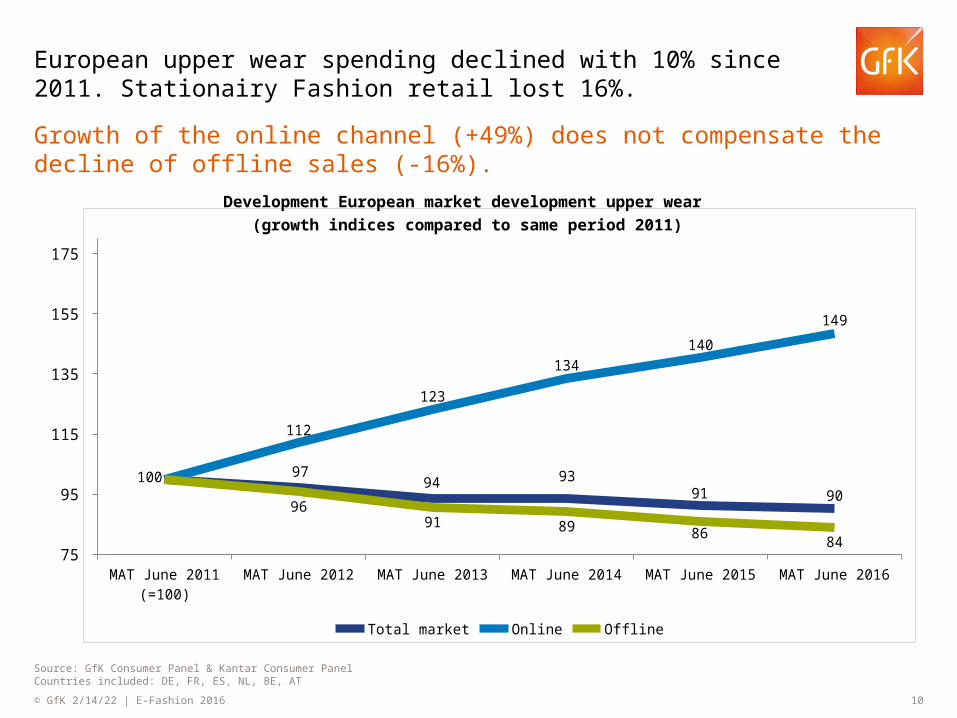

Growth of the online channel (+49%) does not compensate the decline of offline sales (-16%).

Source: GfK Consumer Panel & Kantar Consumer PanelCountries included: DE, FR, ES, NL, BE, AT

European upper wear spending declined with 10% since 2011. Stationairy Fashion retail lost 16%.

MAT June 2011 (=100)

MAT June 2012 MAT June 2013 MAT June 2014 MAT June 2015 MAT June 2016 75

95

115

135

155

175

97 94 93

91 90

112

123

134 140

149

100

96 91 89 86 84

Total market Online Offline

Development European market development upper wear (growth indices compared to same period 2011)

11© GfK May 1, 2023 | E-Fashion 2016

Source: GfK Consumer Panel & Kantar Consumer Panel, MAT June 2016Countries included: DE, FR, ES, NL, BE, AT

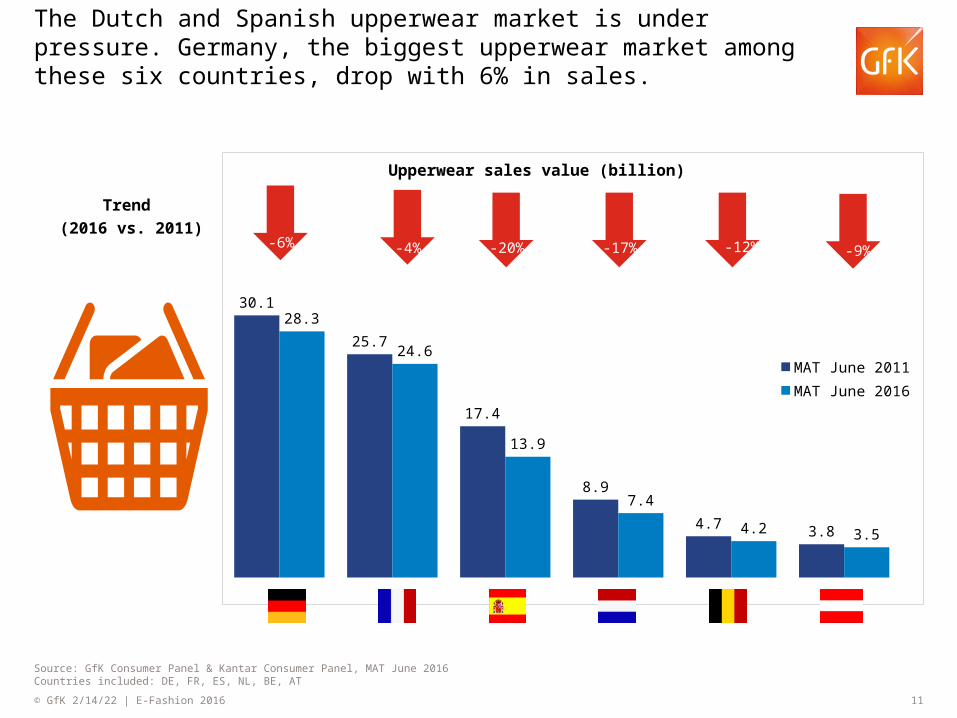

The Dutch and Spanish upperwear market is under pressure. Germany, the biggest upperwear market among these six countries, drop with 6% in sales.

30.1

25.7

17.4

8.9

4.7 3.8

28.3

24.6

13.9

7.4

4.2 3.5

MAT June 2011MAT June 2016

Upperwear sales value (billion)

-6% -20% -17% -12% -9%

Trend (2016 vs. 2011)

-4%

12© GfK May 1, 2023 | E-Fashion 2016

Source: GfK Consumer Panel & Kantar Consumer Panel, MAT JuneCountries included: DE, FR, ES, NL, BE, AT

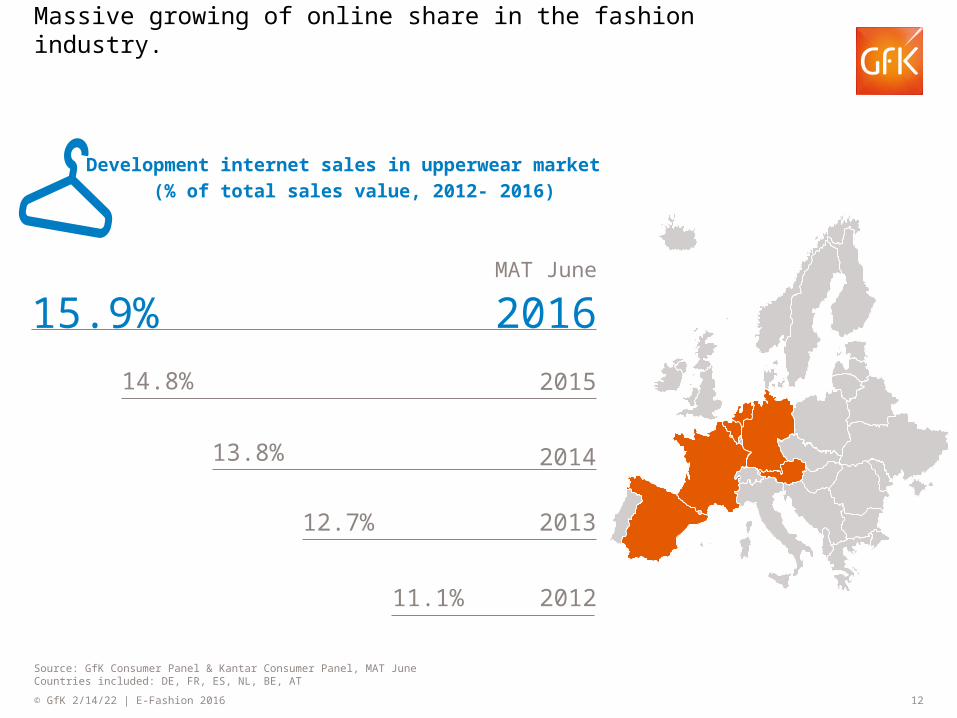

Massive growing of online share in the fashion industry.

201312.7%

201413.8%

201514.8%

15.9%MAT June

2016

Development internet sales in upperwear market (% of total sales value, 2012- 2016)

201211.1%

13© GfK May 1, 2023 | E-Fashion 2016

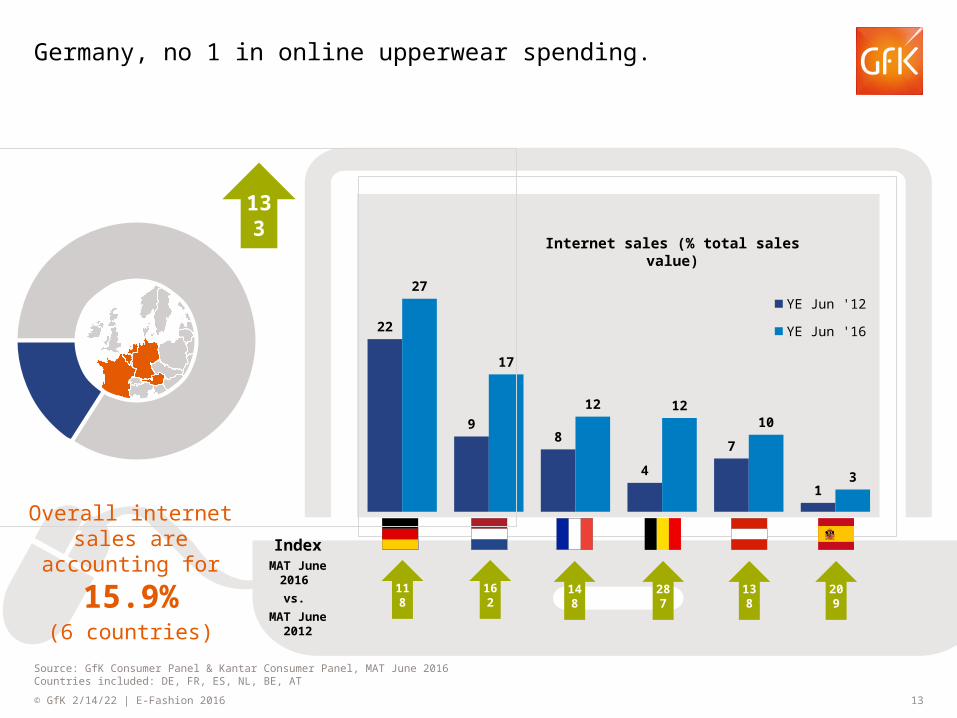

Germany, no 1 in online upperwear spending.

22

98

4

7

1

27

17

12 1210

3

YE Jun '12

YE Jun '16

Internet sales (% total sales value)

IndexMAT June 2016

vs. MAT June 2012

Source: GfK Consumer Panel & Kantar Consumer Panel, MAT June 2016Countries included: DE, FR, ES, NL, BE, AT

Overall internet sales are

accounting for 15.9%(6 countries)

118 162 148 287 138 209

133

14© GfK May 1, 2023 | E-Fashion 2016

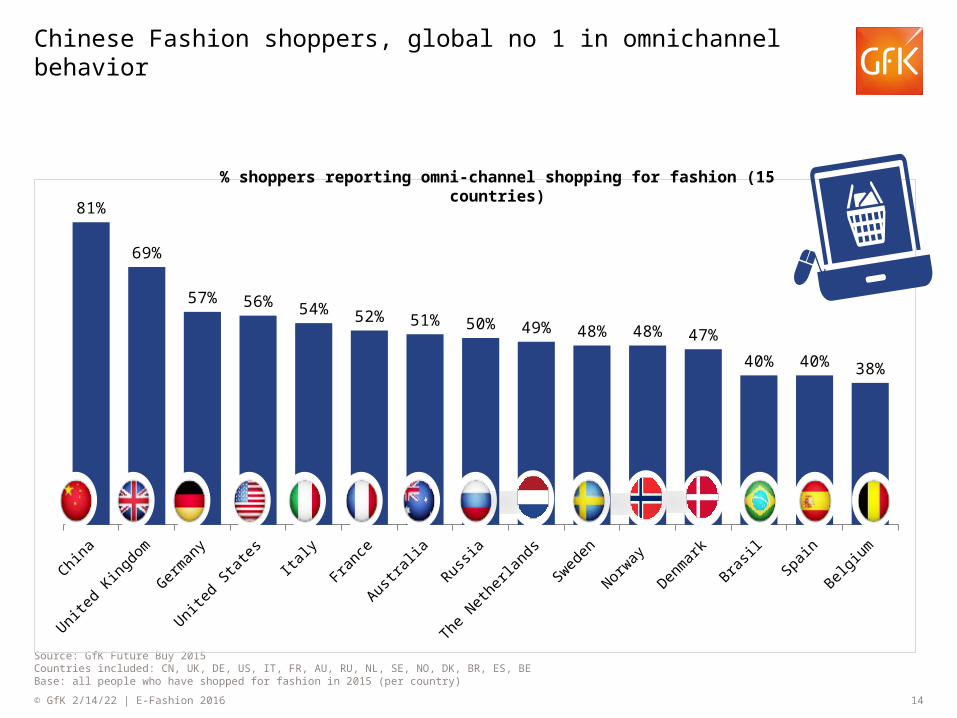

Chinese Fashion shoppers, global no 1 in omnichannel behavior

Source: GfK Future Buy 2015Countries included: CN, UK, DE, US, IT, FR, AU, RU, NL, SE, NO, DK, BR, ES, BEBase: all people who have shopped for fashion in 2015 (per country)

China

United

King

dom

German

y

United

Stat

es Italy

France

Austra

lia

Russia

The N

etherl

ands

Sweden

Norway

Denmark

Brasil

Spain

Belgium

81%

69%

57% 56% 54% 52% 51% 50% 49% 48% 48% 47%

40% 40% 38%

% shoppers reporting omni-channel shopping for fashion (15 countries)

15© GfK May 1, 2023 | E-Fashion 2016

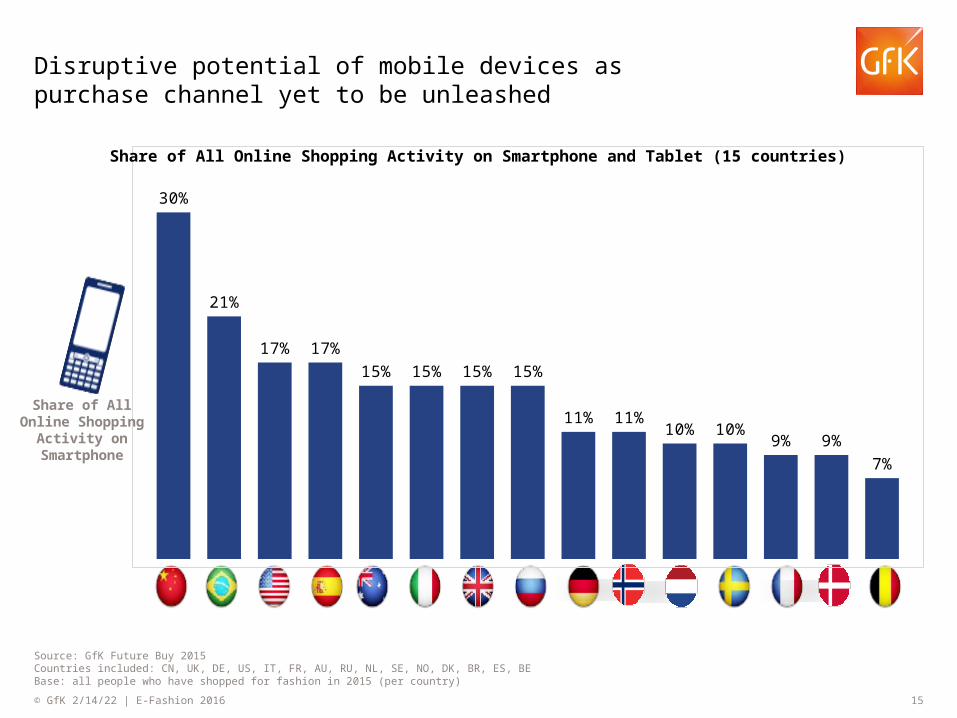

Disruptive potential of mobile devices as purchase channel yet to be unleashed

Source: GfK Future Buy 2015Countries included: CN, UK, DE, US, IT, FR, AU, RU, NL, SE, NO, DK, BR, ES, BEBase: all people who have shopped for fashion in 2015 (per country)

30%

21%

17% 17%15% 15% 15% 15%

11% 11%10% 10%

9% 9%7%

Share of All Online Shopping Activity on Smartphone and Tablet (15 countries)

Share of All Online Shopping Activity

on Smartphone

16© GfK May 1, 2023 | E-Fashion 2016

2015 reported levels of showrooming

Source: GfK Future Buy 2015Countries included: CN, UK, DE, US, IT, FR, AU, RU, NL, SE, NO, DK, BR, ES, BEBase: all people who have shopped for fashion in 2015 (per country)

Don’t over estimate the impact of showrooming in NL

32%31%

26%

23%

20% 20%19%

17% 17%15%

13% 13% 13%12%

7%

Saw product in store then

purchased on phone elsewhere

18© GfK May 1, 2023 | E-Fashion 2016

What’s going on in The Netherlands?

19© GfK May 1, 2023 | E-Fashion 2016

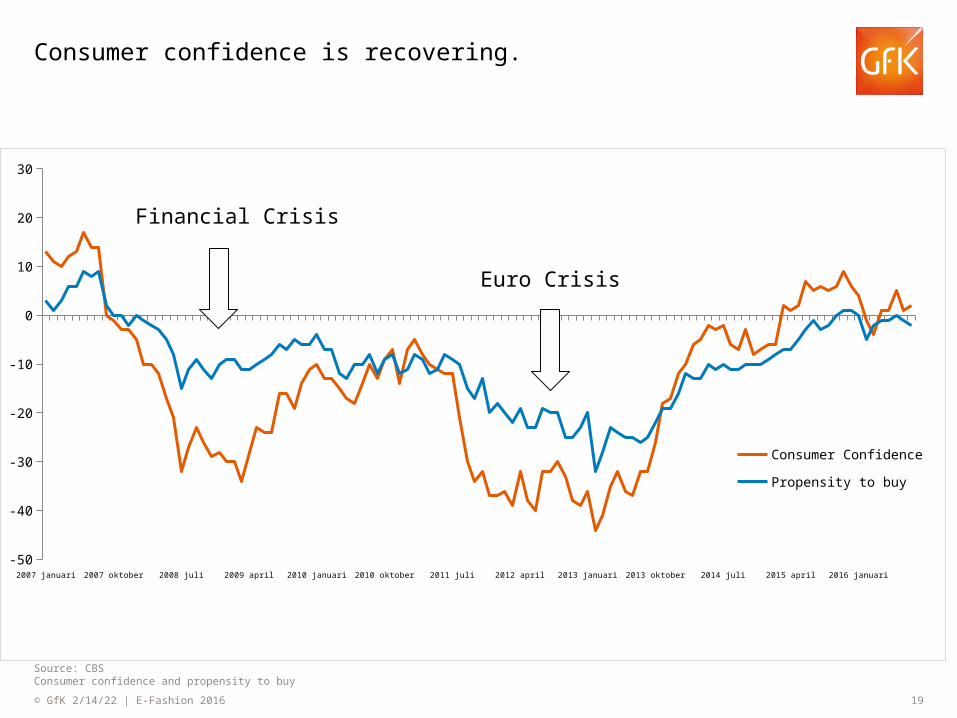

Source: CBSConsumer confidence and propensity to buy

Consumer confidence is recovering.

2007 januari 2007 juli 2008 januari 2008 juli 2009 januari 2009 juli 2010 januari 2010 juli 2011 januari 2011 juli 2012 januari 2012 juli 2013 januari 2013 juli 2014 januari 2014 juli 2015 januari 2015 juli 2016 januari 2016 juli-50

-40

-30

-20

-10

0

10

20

30

Consumer Confidence

Propensity to buy

Financial Crisis

Euro Crisis

21© GfK May 1, 2023 | E-Fashion 2016

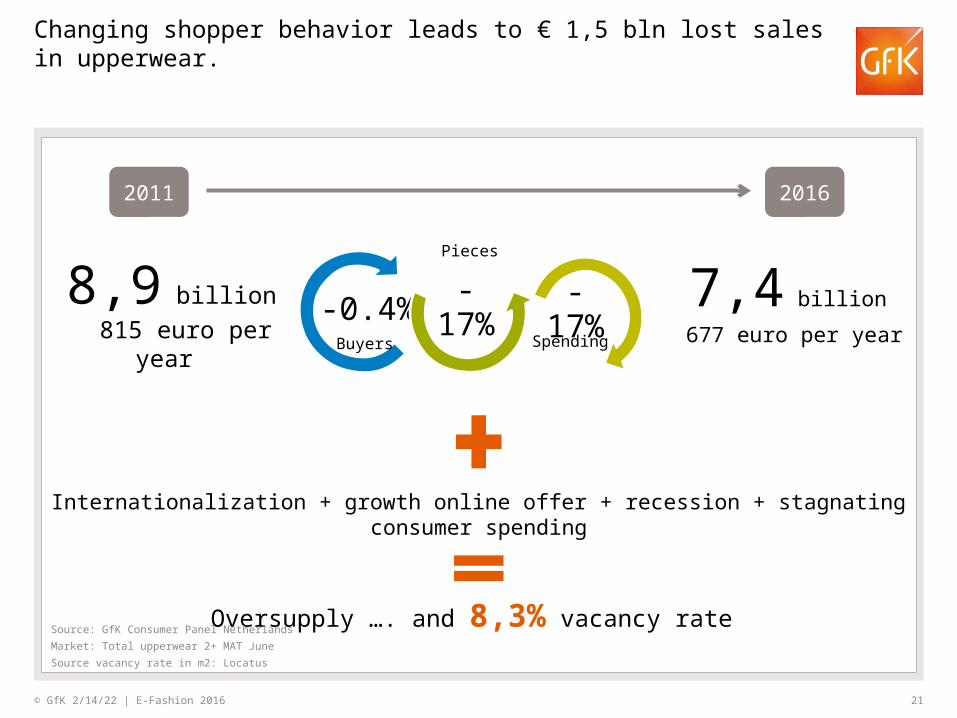

7,4 billion

677 euro per year

8,9 billion 815 euro per year

2014

-0.4% -17%Buyers

Pieces

-17%Spending

Internationalization + growth online offer + recession + stagnating consumer spending

Oversupply …. and 8,3% vacancy rate

2011 2016

Changing shopper behavior leads to € 1,5 bln lost sales in upperwear.

Source: GfK Consumer Panel NetherlandsMarket: Total upperwear 2+ MAT JuneSource vacancy rate in m2: Locatus

22© GfK May 1, 2023 | E-Fashion 2016

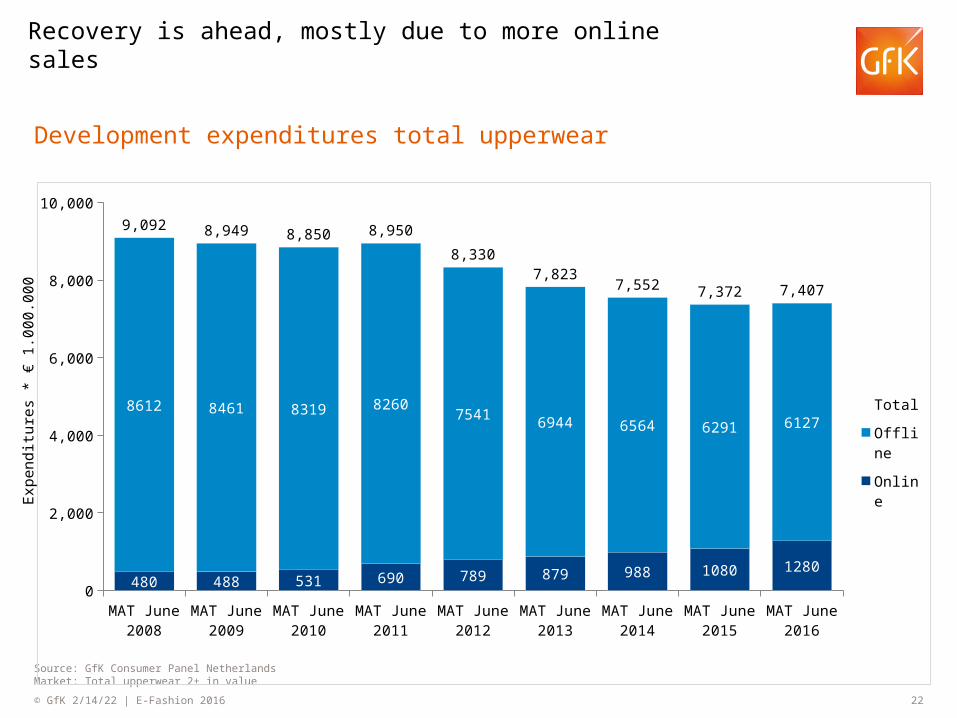

Development expenditures total upperwear

Source: GfK Consumer Panel NetherlandsMarket: Total upperwear 2+ in value

Recovery is ahead, mostly due to more online salesE

xpen

ditu

res

* €

1.00

0.00

0

MAT June 2008

MAT June 2009

MAT June 2010

MAT June 2011

MAT June 2012

MAT June 2013

MAT June 2014

MAT June 2015

MAT June 2016

0

2,000

4,000

6,000

8,000

10,000

480 488 531 690 789 879 988 1080 1280

8612 8461 8319 82607541 6944 6564 6291 6127

9,092 8,949 8,850 8,950

8,330 7,823

7,552 7,372 7,407

Total

Offline

Online

23© GfK May 1, 2023 | E-Fashion 2016

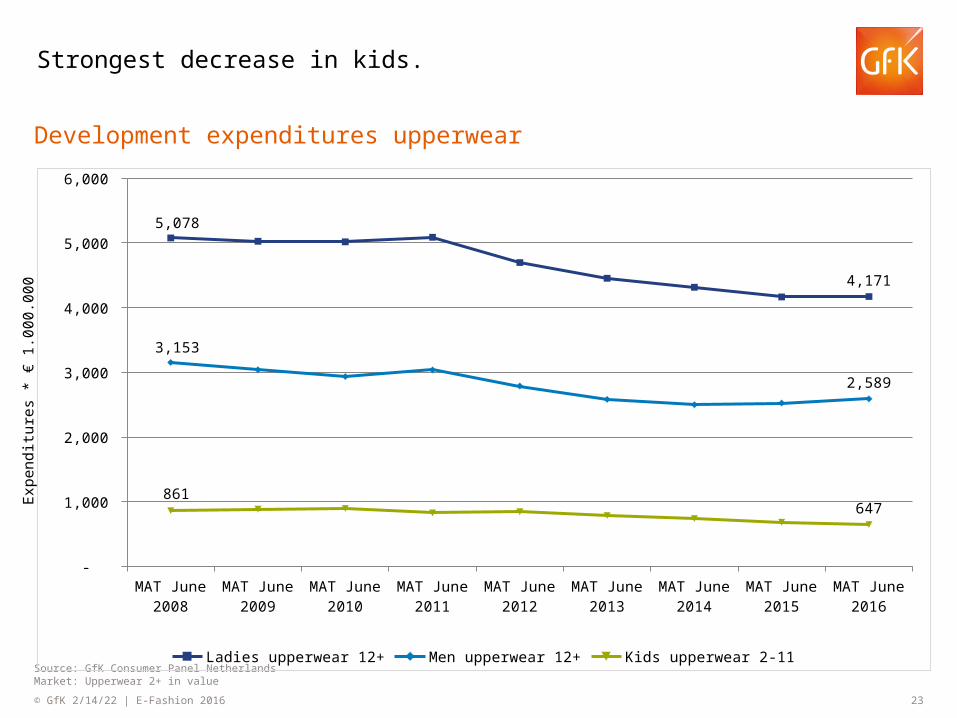

Development expenditures upperwear

Source: GfK Consumer Panel NetherlandsMarket: Upperwear 2+ in value

Strongest decrease in kids.

MAT June 2008

MAT June 2009

MAT June 2010

MAT June 2011

MAT June 2012

MAT June 2013

MAT June 2014

MAT June 2015

MAT June 2016

-

1,000

2,000

3,000

4,000

5,000

6,000

5,078

4,171

3,153

2,589

861 647

Ladies upperwear 12+ Men upperwear 12+ Kids upperwear 2-11

Exp

endi

ture

s *

€ 1.

000.

000

24© GfK May 1, 2023 | E-Fashion 2016

Dutch fashion retailers are expanding.

Reasons to be optimistic.

25© GfK May 1, 2023 | E-Fashion 2016

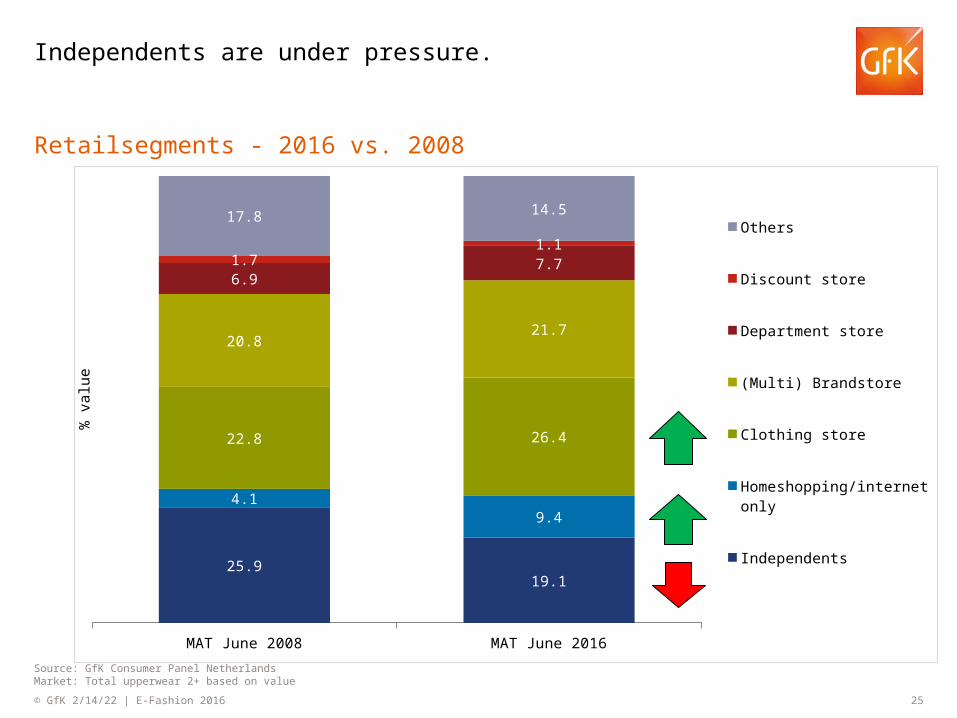

Independents are under pressure.

Retailsegments - 2016 vs. 2008

Source: GfK Consumer Panel NetherlandsMarket: Total upperwear 2+ based on value

MAT June 2008 MAT June 2016

25.919.1

4.19.4

22.8 26.4

20.821.7

6.97.71.71.1

17.8 14.5Others

Discount store

Department store

(Multi) Brandstore

Clothing store

Homeshopping/internet only

Independents

% v

alue

26© GfK May 1, 2023 | E-Fashion 2016

Three new retailers in the top 14.

Retail - 2016 vs. 2008

Source: GfK Consumer Panel NetherlandsMarket: Total upperwear 2+ based on value, MAT June 2008 – MAT June 2016

OUT

STABLE IN

27© GfK May 1, 2023 | E-Fashion 2016

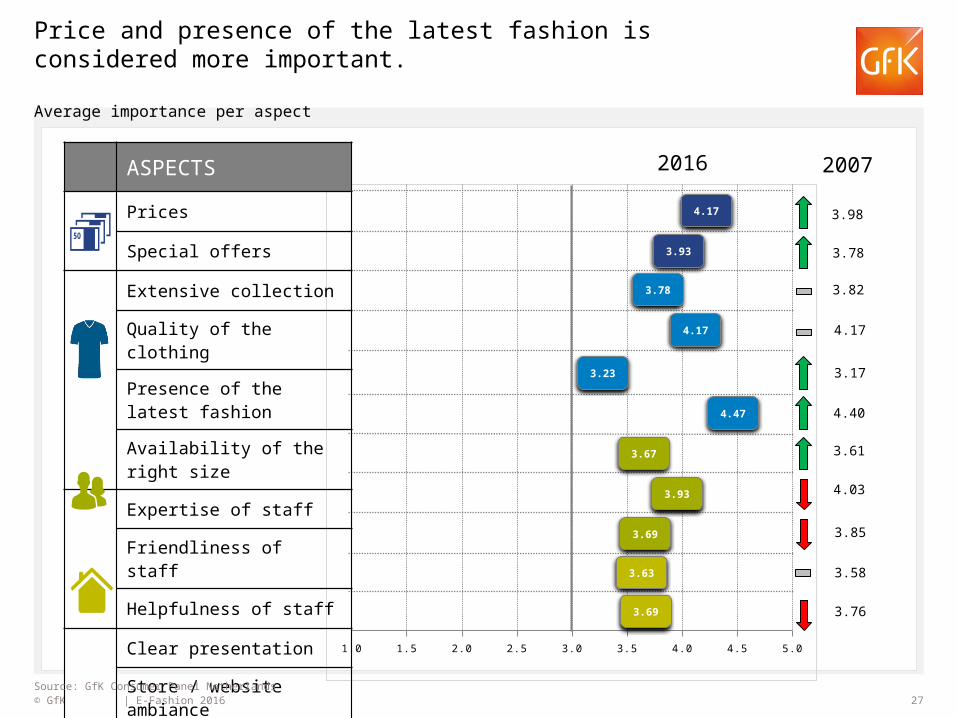

1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0

Price and presence of the latest fashion is considered more important.

Average importance per aspect

4.17

4.47

3.69

3.63

3.69

3.93

3.78

4.17

3.67

3.93

3.23

ASPECTS

Prices

Special offers

Extensive collection

Quality of the clothing

Presence of the latest fashion

Availability of the right size

Expertise of staff

Friendliness of staff

Helpfulness of staff

Clear presentation

Store / website ambiance

2016 2007

3.98

3.78

3.82

4.17

3.17

4.40

3.61

4.03

3.85

3.58

3.76

Source: GfK Consumer Panel Netherlands

28© GfK May 1, 2023 | E-Fashion 2016

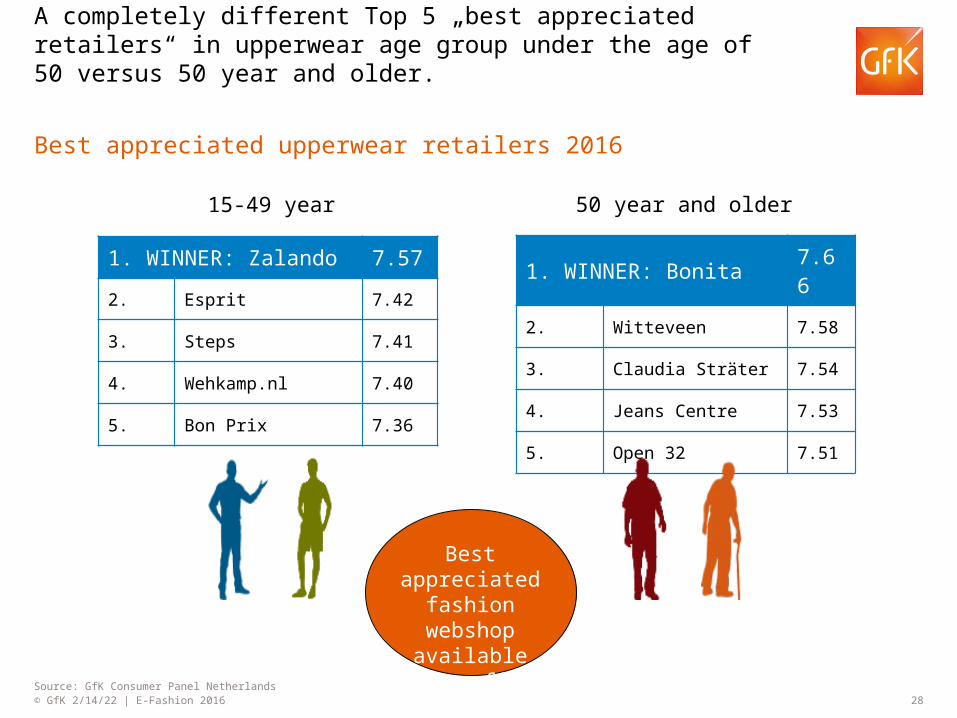

A completely different Top 5 „best appreciated retailers“ in upperwear age group under the age of 50 versus 50 year and older.

Best appreciated upperwear retailers 2016

Source: GfK Consumer Panel Netherlands

1. WINNER: Bonita 7.66

2. Witteveen 7.58

3. Claudia Sträter 7.54

4. Jeans Centre 7.53

5. Open 32 7.51

1. WINNER: Zalando 7.57

2. Esprit 7.42

3. Steps 7.41

4. Wehkamp.nl 7.40

5. Bon Prix 7.36

15-49 year 50 year and older

Best appreciated fashion webshop available October

first!

29© GfK May 1, 2023 | E-Fashion 2016

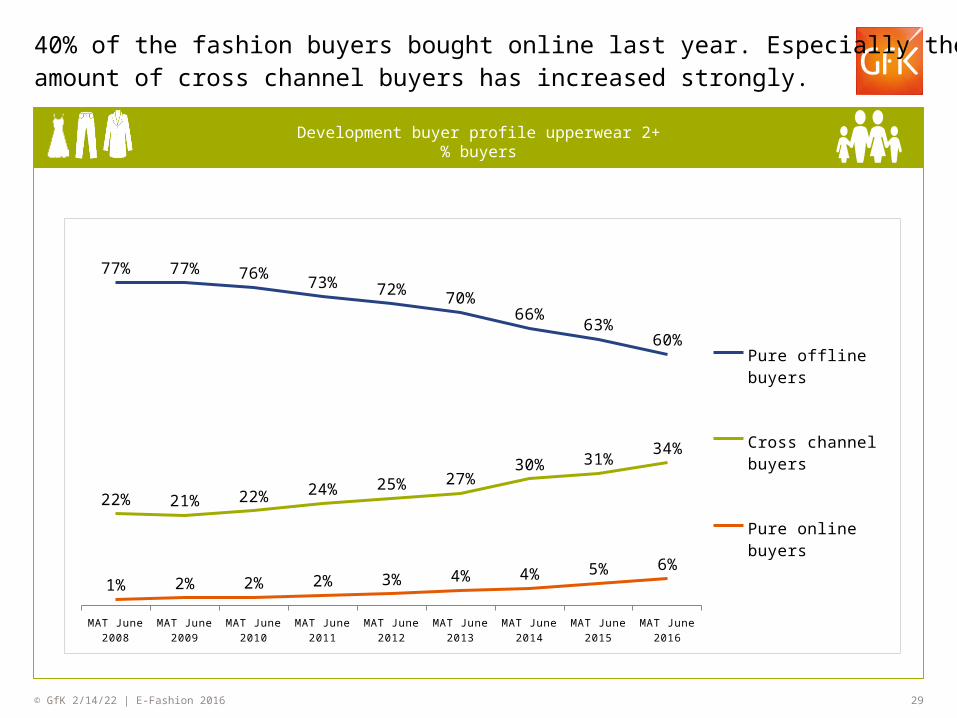

MAT June 2008

MAT June 2009

MAT June 2010

MAT June 2011

MAT June 2012

MAT June 2013

MAT June 2014

MAT June 2015

MAT June 2016

77% 77% 76% 73% 72% 70%66%

63%60%

22% 21% 22% 24% 25% 27%30% 31%

34%

1% 2% 2% 2% 3% 4% 4% 5% 6%

Pure offline buyers

Cross channel buyers

Pure online buyers

Development buyer profile upperwear 2+% buyers

40% of the fashion buyers bought online last year. Especially the amount of cross channel buyers has increased strongly.

30© GfK May 1, 2023 | E-Fashion 2016

MAT June 2008

MAT June 2009

MAT June 2010

MAT June 2011

MAT June 2012

MAT June 2013

MAT June 2014

MAT June 2015

MAT June 2016

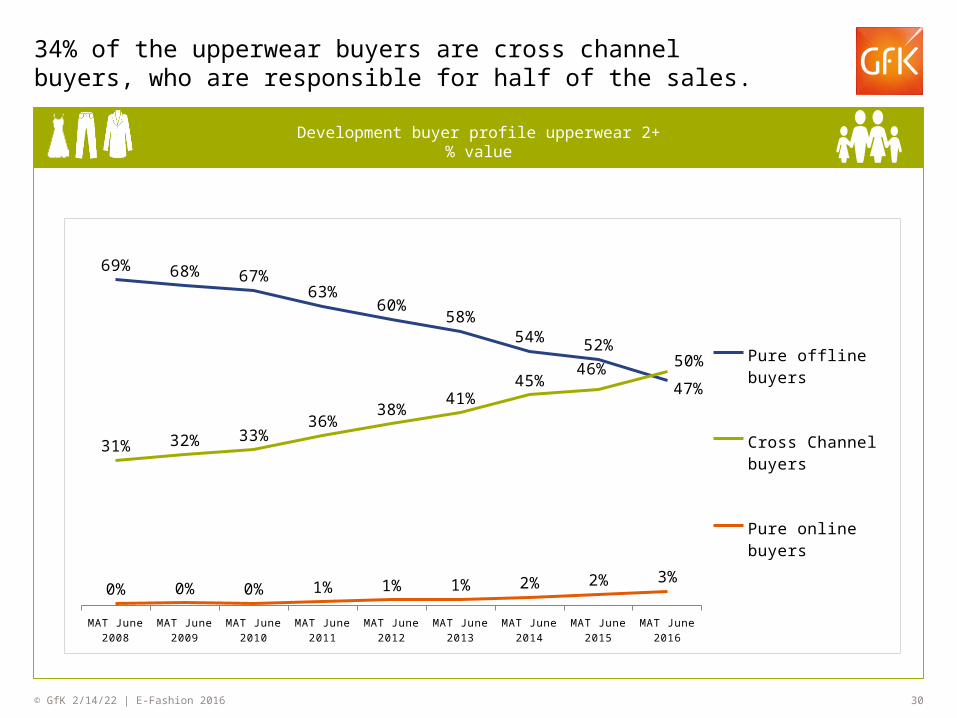

69% 68% 67%63%

60%58%

54% 52%

47%

31% 32% 33%36%

38%41%

45%46% 50%

0% 0% 0% 1% 1% 1% 2% 2% 3%

Pure offline buyers

Cross Channel buyers

Pure online buyers

Development buyer profile upperwear 2+% value

34% of the upperwear buyers are cross channel buyers, who are responsible for half of the sales.

31© GfK May 1, 2023 | E-Fashion 2016

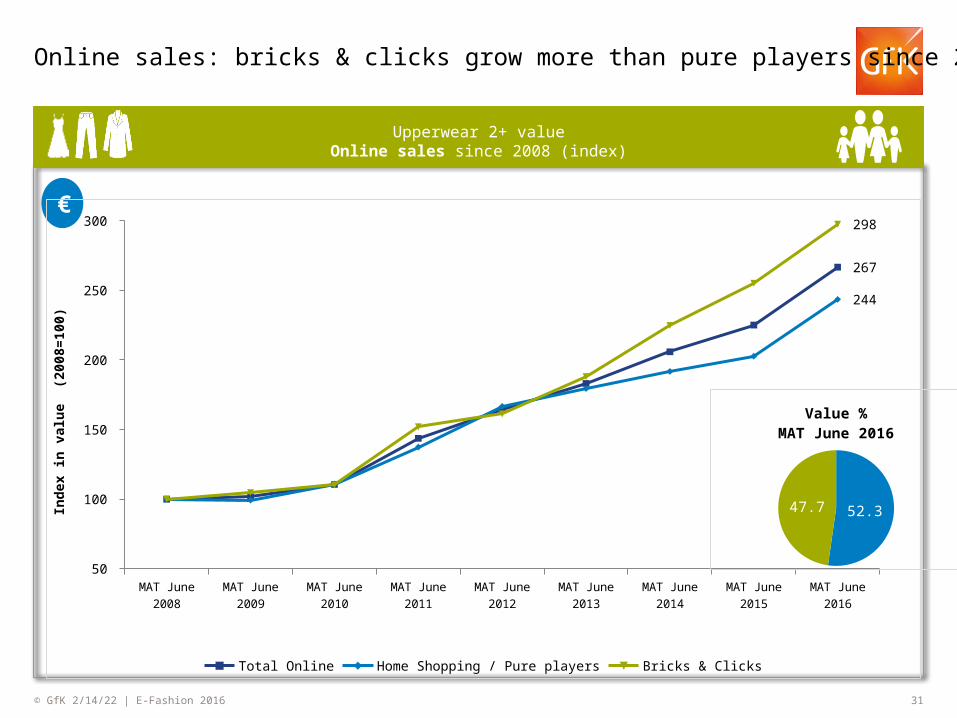

Upperwear 2+ valueOnline sales since 2008 (index)

Online sales: bricks & clicks grow more than pure players since 2013.

€

MAT June 2008

MAT June 2009

MAT June 2010

MAT June 2011

MAT June 2012

MAT June 2013

MAT June 2014

MAT June 2015

MAT June 2016

50

100

150

200

250

300

267

244

298

Total Online Home Shopping / Pure players Bricks & Clicks

Inde

x in

val

ue (

2008

=100

)

52.347.7

Value %MAT June 2016

32© GfK May 1, 2023 | E-Fashion 2016

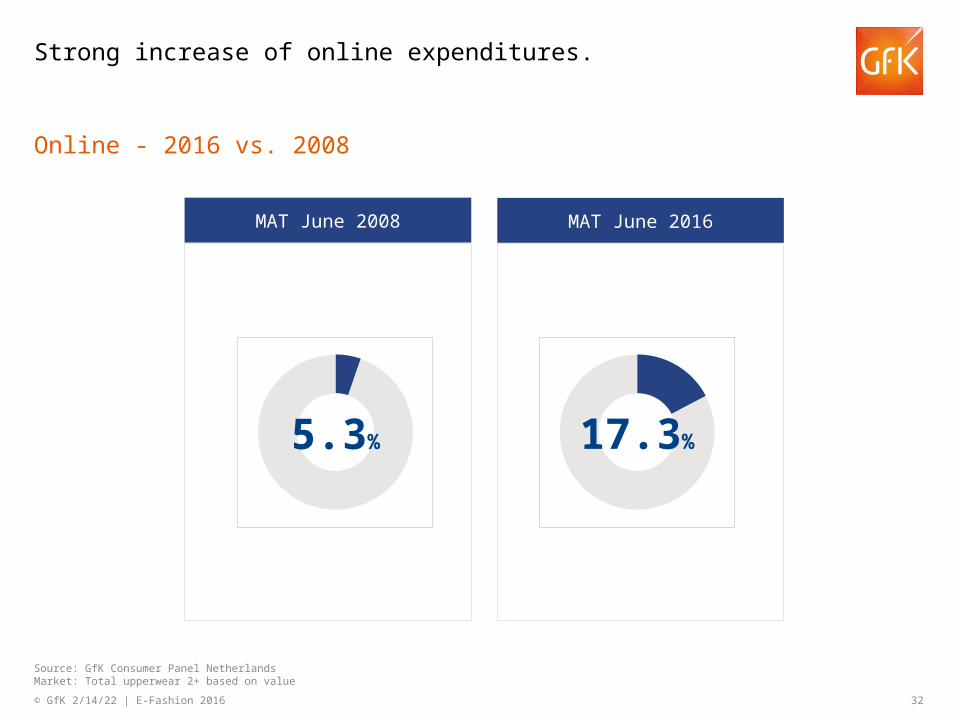

Strong increase of online expenditures.

Online - 2016 vs. 2008

Source: GfK Consumer Panel NetherlandsMarket: Total upperwear 2+ based on value

MAT June 2008

MAT June 2016

5.3% 17.3%

33© GfK May 1, 2023 | E-Fashion 2016

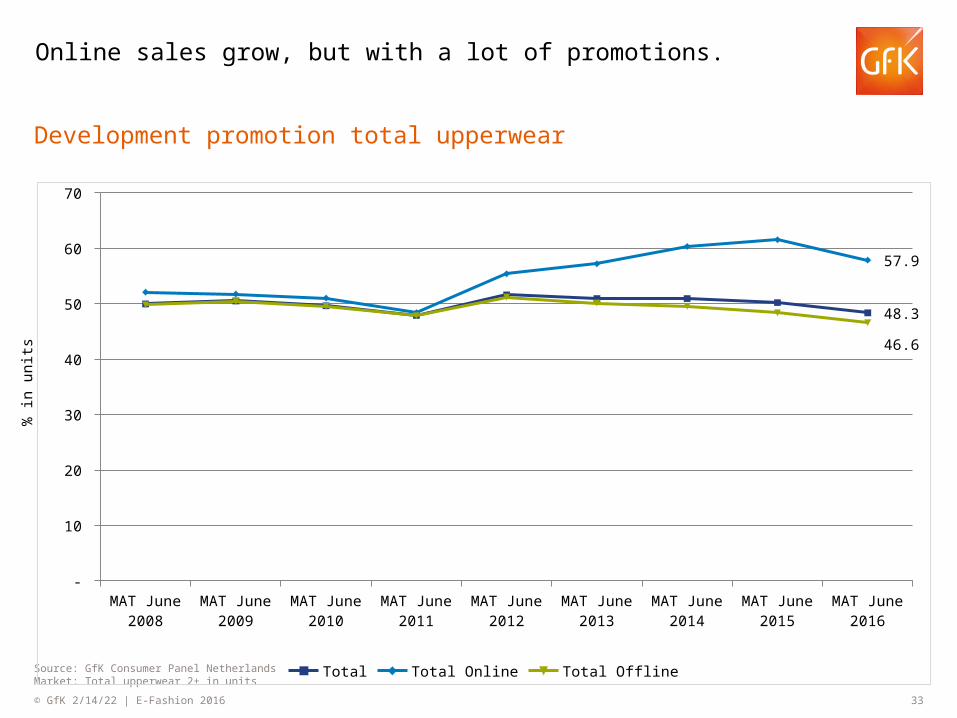

Development promotion total upperwear

Source: GfK Consumer Panel NetherlandsMarket: Total upperwear 2+ in units

Online sales grow, but with a lot of promotions.%

in u

nits

MAT June 2008

MAT June 2009

MAT June 2010

MAT June 2011

MAT June 2012

MAT June 2013

MAT June 2014

MAT June 2015

MAT June 2016

-

10

20

30

40

50

60

70

48.3

57.9

46.6

Total Total Online Total Offline

34© GfK May 1, 2023 | E-Fashion 2016

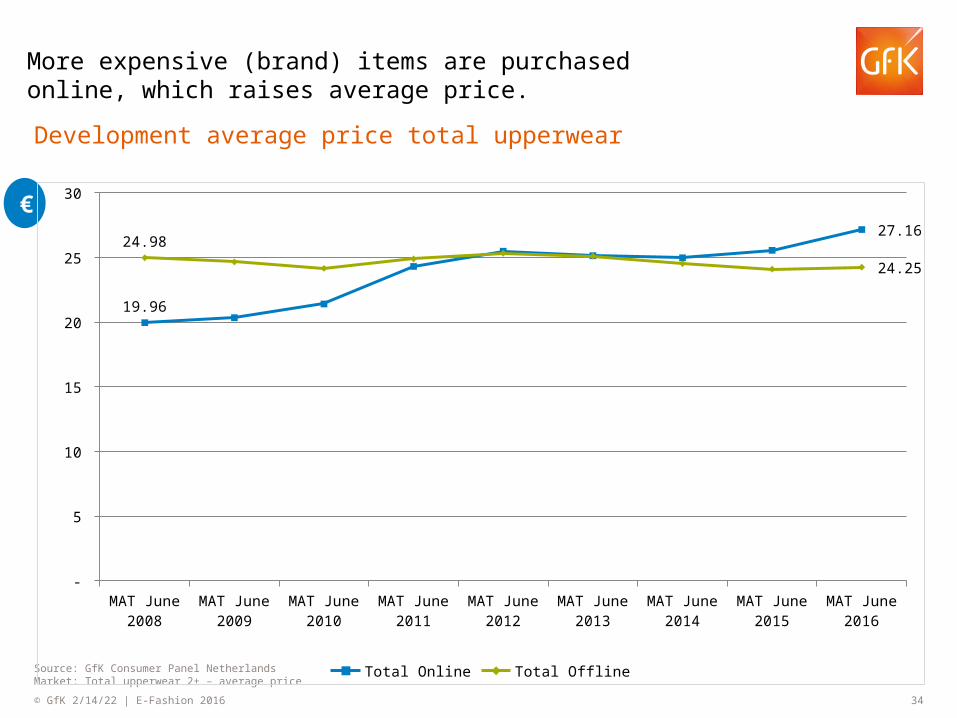

Development average price total upperwear

Source: GfK Consumer Panel NetherlandsMarket: Total upperwear 2+ – average price

More expensive (brand) items are purchased online, which raises average price.

€

MAT June 2008

MAT June 2009

MAT June 2010

MAT June 2011

MAT June 2012

MAT June 2013

MAT June 2014

MAT June 2015

MAT June 2016

-

5

10

15

20

25

30

19.96

27.16 24.98

24.25

Total Online Total Offline

35© GfK May 1, 2023 | E-Fashion 2016

Wehkamp, H&M and Esprit stable online. Two new entries.

Top 5 online retail - 2016 vs. 2008

Source: GfK Consumer Panel NetherlandsMarket: Total upperwear 2+ based on value

MAT June 2008

MAT June 2016

36© GfK May 1, 2023 | E-Fashion 2016

Clash of the generations

37© GfK May 1, 2023 | E-Fashion 2016

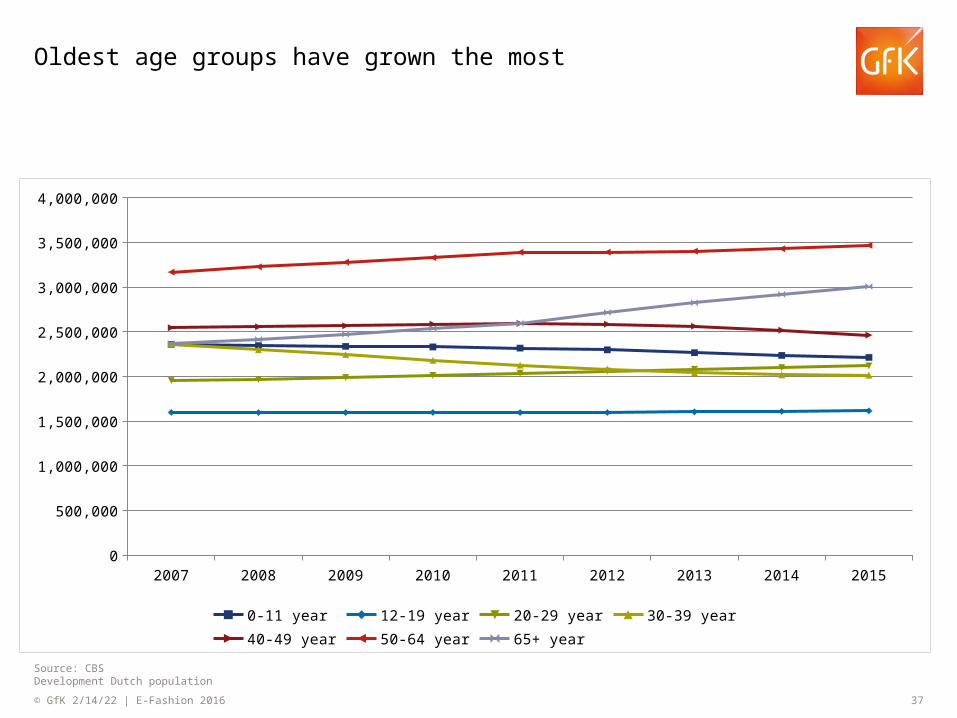

Source: CBSDevelopment Dutch population

Oldest age groups have grown the most

2007 2008 2009 2010 2011 2012 2013 2014 20150

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

0-11 year 12-19 year 20-29 year 30-39 year 40-49 year 50-64 year 65+ year

38© GfK May 1, 2023 | E-Fashion 2016

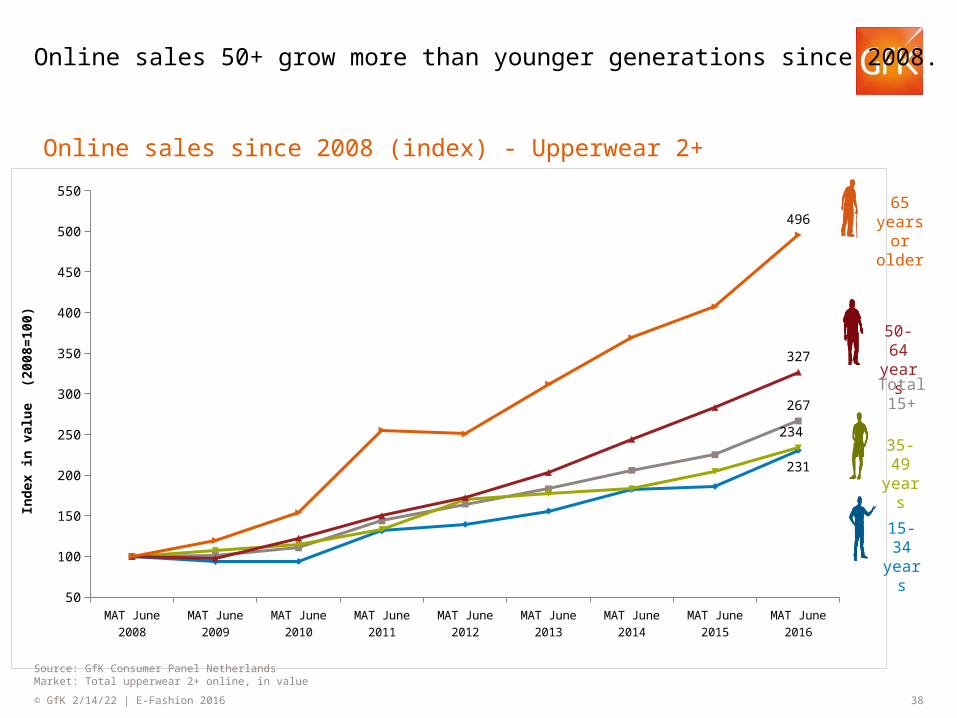

Online sales 50+ grow more than younger generations since 2008.

MAT June 2008

MAT June 2009

MAT June 2010

MAT June 2011

MAT June 2012

MAT June 2013

MAT June 2014

MAT June 2015

MAT June 2016

50

100

150

200

250

300

350

400

450

500

550

267

231

234

327

496

Inde

x in

val

ue (

2008

=100

)

Source: GfK Consumer Panel NetherlandsMarket: Total upperwear 2+ online, in value

Online sales since 2008 (index) - Upperwear 2+

50-64 years

65 years or older

35-49 years

15-34 years

Total 15+

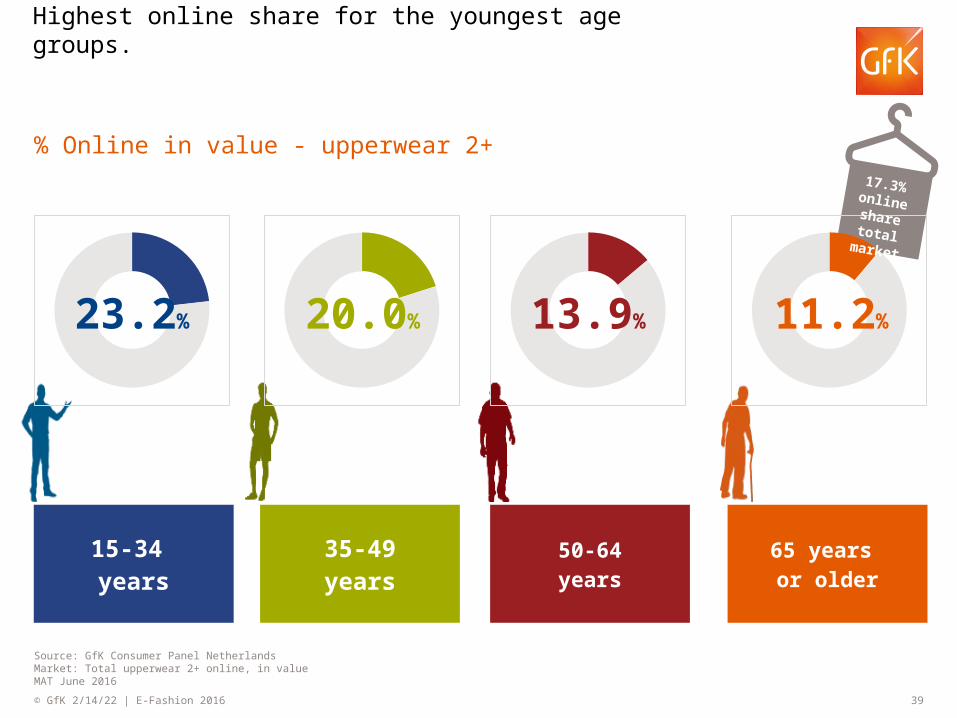

39© GfK May 1, 2023 | E-Fashion 2016

65 years or older

50-64years

35-49years

% Online in value - upperwear 2+

Highest online share for the youngest age groups.

Source: GfK Consumer Panel NetherlandsMarket: Total upperwear 2+ online, in valueMAT June 2016

15-34 years

23.2% 20.0% 13.9% 11.2%

17.3% online share total market

40© GfK May 1, 2023 | E-Fashion 2016

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

55.0

64.4

55.9

47.2

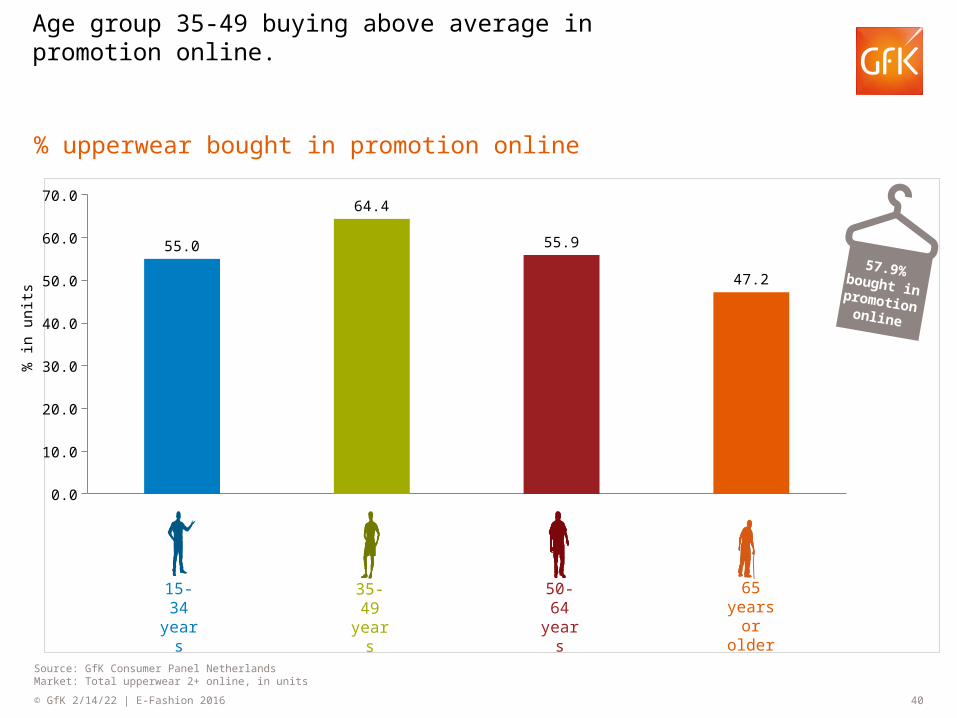

% upperwear bought in promotion online

Age group 35-49 buying above average in promotion online.

15-34 years

50-64 years

35-49 years

65 years or older

Source: GfK Consumer Panel NetherlandsMarket: Total upperwear 2+ online, in units

% in

uni

ts

57.9% bought in promotion online

41© GfK May 1, 2023 | E-Fashion 2016

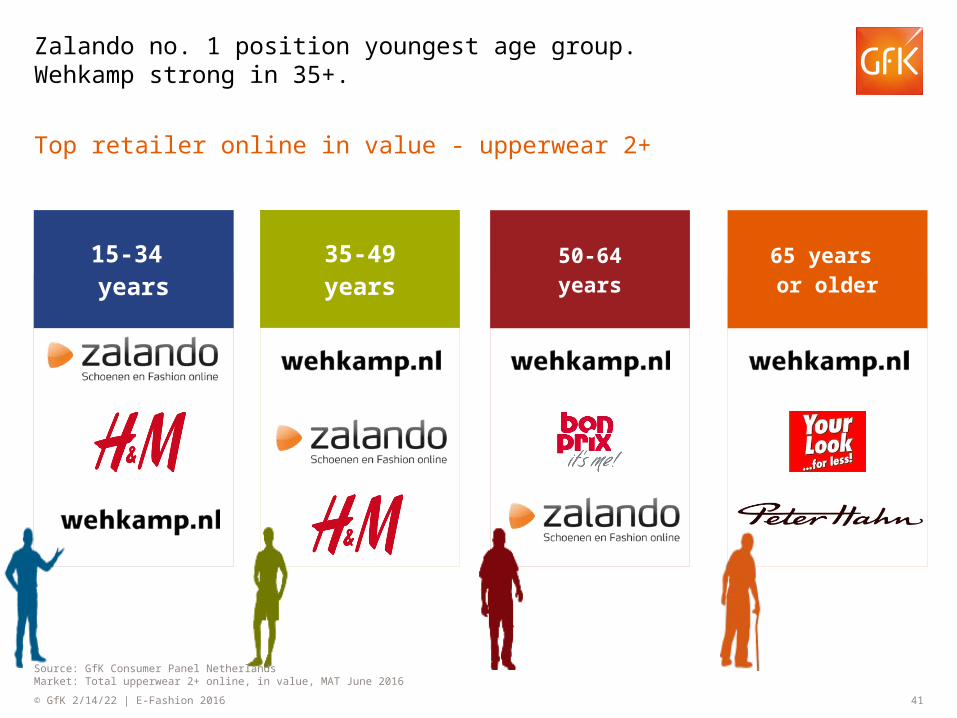

65 years or older

50-64years

35-49years

Top retailer online in value - upperwear 2+

Zalando no. 1 position youngest age group. Wehkamp strong in 35+.

Source: GfK Consumer Panel NetherlandsMarket: Total upperwear 2+ online, in value, MAT June 2016

15-34 years

42© GfK May 1, 2023 | E-Fashion 2016

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

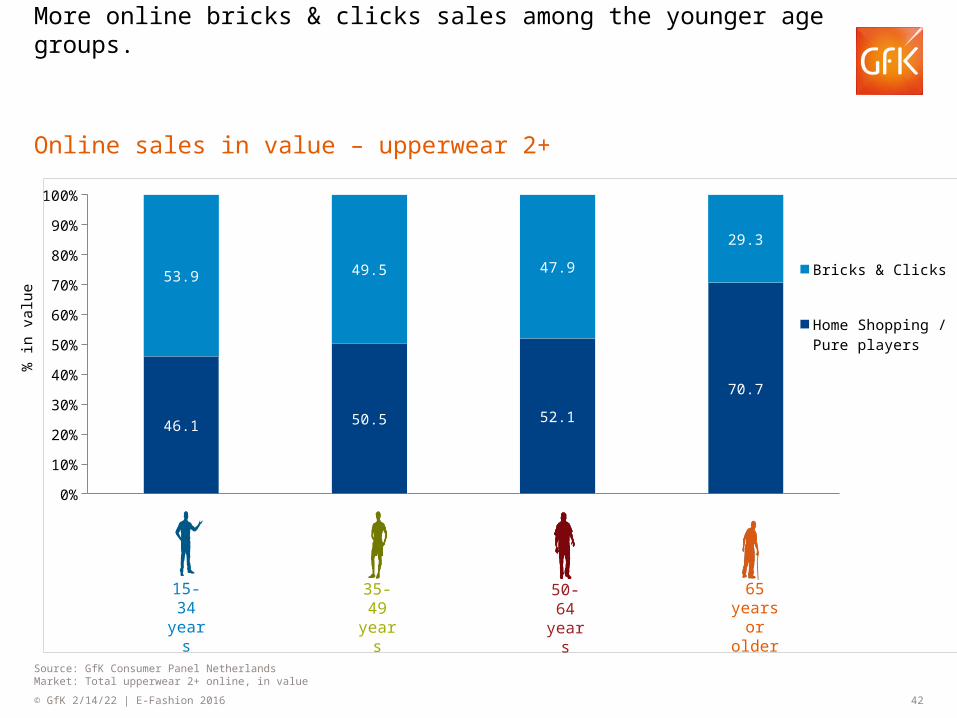

46.1 50.5 52.1

70.7

53.9 49.5 47.9

29.3

Bricks & Clicks

Home Shopping / Pure players

Online sales in value – upperwear 2+

More online bricks & clicks sales among the younger age groups.

15-34 years

50-64 years

35-49 years

65 years or older

Source: GfK Consumer Panel NetherlandsMarket: Total upperwear 2+ online, in value

% in

val

ue

43© GfK May 1, 2023 | E-Fashion 2016

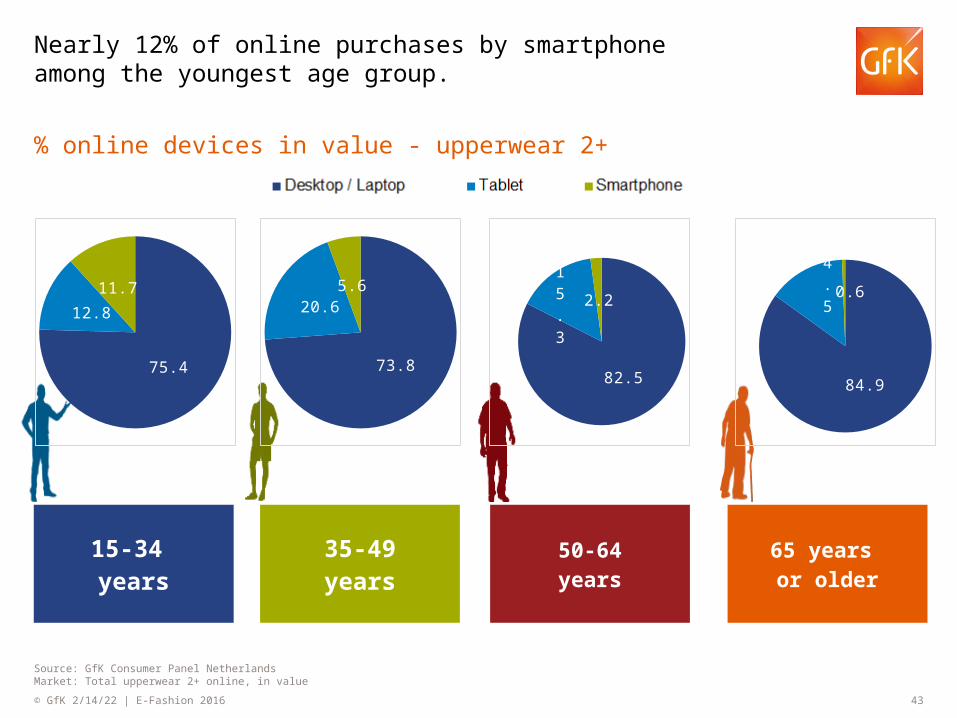

65 years or older

50-64years

35-49years

% online devices in value - upperwear 2+

Nearly 12% of online purchases by smartphone among the youngest age group.

Source: GfK Consumer Panel NetherlandsMarket: Total upperwear 2+ online, in value

15-34 years

75.4

12.811.7

73.8

20.65.6

82.5

15.3

2.2

84.9

14.50.6

44© GfK May 1, 2023 | E-Fashion 2016

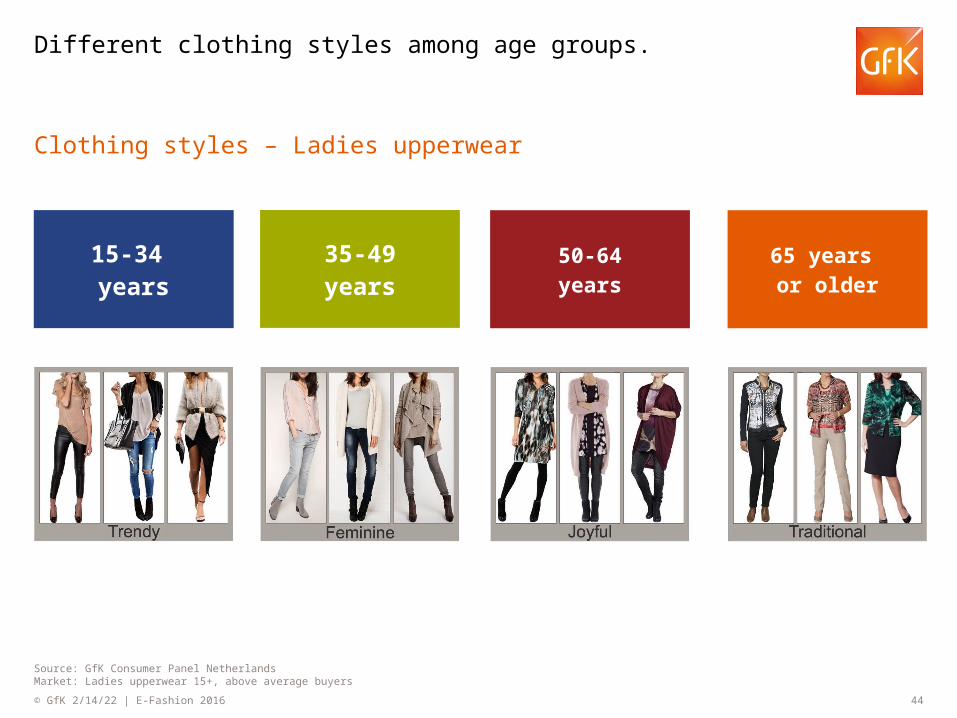

65 years or older

50-64years

35-49years

Clothing styles – Ladies upperwear

Different clothing styles among age groups.

Source: GfK Consumer Panel NetherlandsMarket: Ladies upperwear 15+, above average buyers

15-34 years

45© GfK May 1, 2023 | E-Fashion 2016

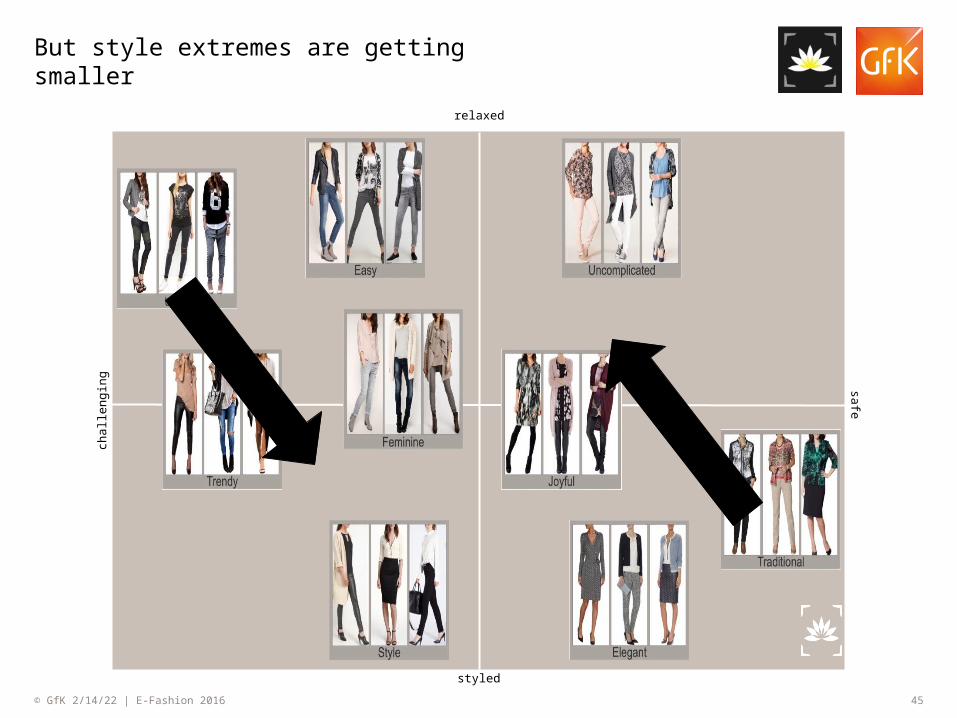

But style extremes are getting smaller

relaxed

styled

chal

leng

ing safe

48© GfK May 1, 2023 | E-Fashion 2016© GfK 2016 | Emerce Live

Keytakeaways

Age groups differ in shopping

behavior, but clothing

styles become more ageless

Mass digitization and changing consumers have upturned

fashion retail in the last years

The oldest age groups are the

fasters growers in online fashion

Increasing importance of both price

and assortment No compromise!

49© GfK May 1, 2023 | E-Fashion 2016

Thank youAny questions?

Presentation (extract) will be shared after personal request with business card.

Gino Thuij | GfK | [email protected] | M: 06-22200411