Embed Size (px)

Citation preview

–

–

–

–

–

–

Source: OFCOM 2014

Majority under 45 favoursconnected devices

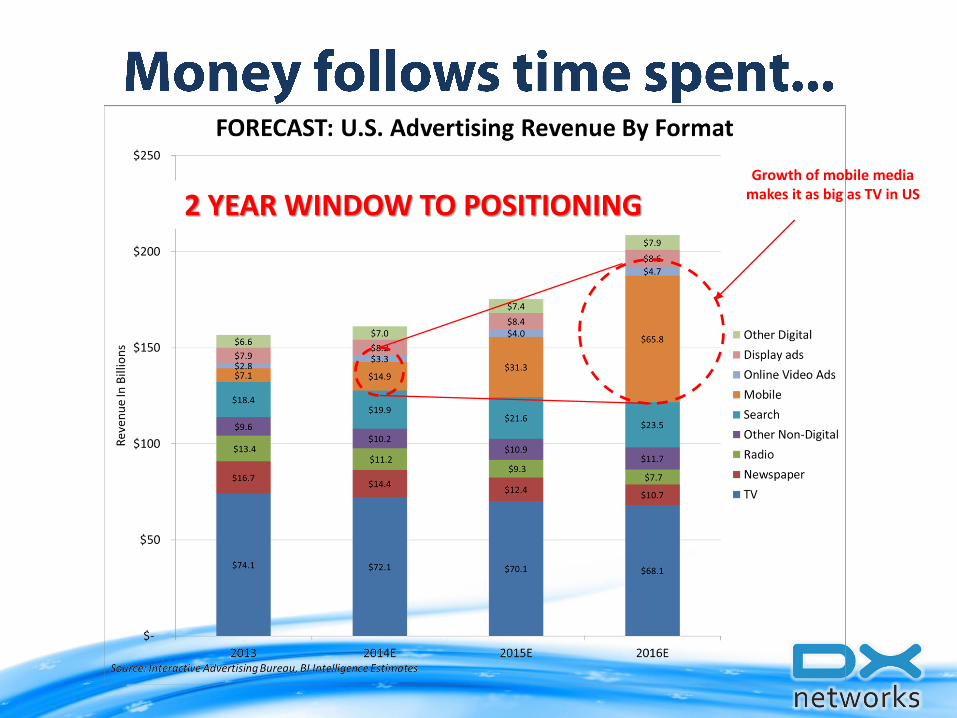

Growth of mobile media makes it as big as TV in US

2 YEAR WINDOW TO POSITIONING

SERVIÇOS MÓVEIS PESSOAIS - Acessos Móveis por Tecnologia

Tecnologia Total Part. (%)

CDMA 14,594 0.01

GSM (2G) 138,104,023 50.09

WCDMA (3G) 118,474,236 42.97

LTE (4G) 3,270,375 1.19

Terminais de Dados M2M 9,100,913 3.30

Terminais de Dados Banda Larga 6,742,772 2.45

Total 275,706,913 100

BANDA LARGA FIXA POR FAIXA MÉDIA DE VELOCIDADE VENDIDA

Faixa 2014-01 2014-02 2014-03 2014-04 2014-05 2014-06

0Kbps a 512Kbps 1,462,650 1,474,217 1,486,245 1,478,647 1,473,130 1,505,989

512kbps a 2Mbps 9,192,365 9,156,889 9,096,443 8,999,479 8,906,775 8,822,626

2Mbps a 12Mbps 9,094,480 9,221,242 9,365,328 9,482,451 9,641,659 9,701,412

12Mbps a 34Mbps 2,265,127 2,345,625 2,421,023 2,508,093 2,586,409 2,646,628

> 34Mbps 357,613 389,231 426,456 464,926 508,419 548,079

> 128 Million

> 21 Million

Mobile is >6x bigger

Dominant

Aggregator

Retail

Boutique

Tertiary

Closed circuit

Individuals

Reach

100% of population

0% of population

COMPANIES SEEK GREATER REACH FOR THEIR PRODUCTS (AND BRANDS), EVEN CLOSED CIRCUIT DISTRIBUTION

WITH CONTENT PARTNERS WE BUILD ON EXISTING

DISTRIBUTIONS TO INCREASE REACH

RECENT DEVELOPMENTS HAVE MADEVIDEO CONTENT PRODUCTION FEASIBLE

Them

atic

Mag

azin

e

Arc

hiv

e

Live

Hour/Day

Inexpensive

Constant updates

Eventful

Dynamic

Day/Week

Betterproduction

Weeklyupdates

Semi-dynamic

Month/Quarter

Themes

Calendar

Production value

Niched

No time frame

Collections

Films

Edited material

Licensing

Sen

seo

fu

rge

ncy

/ P

erc

eiv

edti

me

val

ue

Production value / cost

Advance to these with timewith curated content and live eventsMore suitable for engagement

Web Video offeringse.g.: Netflix, YouTubeare focused on these

VIDEO PRODUCTION OR VIDEO FEEDS ARE NOW EASIER, MORE AFFORDABLE AND OF GREATER QUALITY THAN

BEFORE

PROGRAMMATIC CONTENT / USER GENERATED

aggregator &distributor

content providers

productlicensingNational sponsors,

advertisersLocal sponsors,advertisers

consumers &subscribers

$$$$$

$$$$

$

ACCESS AND COST OF ACQUISITION

$

A BALANCED MONETIZATION AND GO-TO-MARKET STRATEGY ARE AT THE HEART OF BUILDING AN IPTV DESTINATION

Create Distribute Monetize

Old School

Digital

Majors

Digital

Indies

•

•

–

–

•

•

•

•

–

•

Presence

Impact

Reach

Contact

UseAudienceAudience

NORMAL RANGE SUBS: 1.8% to 10.5%NORMAL RANGE FREE: 3.7% to 22.1%

FAN BASE = engaged audience / community

We work with manufacturers(gatekeepers), internet sites, social media and physical retail to form a destination

Total n. devices in distribution

Total devices within target

Devices reached by campaign

Store or landing page accessed

Consumers that accessed application

Recurrent users

In DX Mobile IPTV average watch time isclose to 1 hour per session, and recurrenceis 3x/week

sDX

PRODUCTION DISTRIBUTION

ADVERTISING

MOBILE E-COMMERCE

CORPORATE

MOBILE ACTIVATION

LOCAL MONITORING

BIG DATA

MARKET RESEARCH

Content

Influence

Solutions

Analysis

Manymonetization

strategiescreate revenue

hedge andimproves

reach

PlanBusiness models

Content

Product Architecture

Contingencies

Go-to-Market

BuildIntegration

Product and processes

Implementation

Licensing

Production

Design and Production

Third-party integration

OperateSoftware product

Infrastrutcure

Content management

Post-production

Client acquisition

Customer Support

Monitoring

Analysis

What we do: we

mobile video destinations.

![[Infográfico] Mobile Video](https://img.pdfslide.us/doc/110x75/555ec753d8b42a74708b53dd/infografico-mobile-video.jpg)