Embed Size (px)

Citation preview

UNAUDITED ABRIDGED RESULTS

Half Year Ended 30 June 2015

Centenary Room, Royal Harare Gold Club26 August 2015

PresentersCaleb Musodza, Managing DirectorKenias Horonga, Finance Director

Operations OverviewOperations OverviewCaleb MusodzaCaleb Musodza

Financial OverviewFinancial OverviewKenias HorongaKenias Horonga

Strategic Issues and Strategic Issues and OutlookOutlook

Caleb MusodzaCaleb Musodza

Question and AnswerQuestion and AnswerTurnall ExecutivesTurnall Executives

Presentation OutlinePresentation Outline

33

Company Overview

Company HistoryTurnall Holdings Limited, formerly the Building and Construction division of TH Zimbabwe Limited, operates through two divisions: Turnall Building Products – 1943 Turnall Piping Products– 1972

Sole shareholder of four dormant companies namely:

• Acacia Holdings Limited• Hastt Corporation Limited• Hastt Discs [Private] Limited• Tractor and Equipment

Turnroof Africa [Pty ] Limited

Directorate

• R Likukuma - Non Executive Chairperson• J. Mushayavanhu - Non Executive Deputy Chairman• C. Musodza - Executive• K. Horonga - Executive• C. E. Dhlembeu - Non Executive• L. Sasikwa - Non Executive• P. C. C. Moyo - Non Executive• C. M. Gadzikwa - Non Executive• K. Naik - Non Executive• J. P Mutizwa - Non Executive• P. Chingoka - Non Executive• P. Marufu - Non Executive

Executive Management

• Caleb Musodza - Managing Director

• Kenias Horonga - Finance Director

• Francis Chigwedere - Technical Director

• Roselyn Chisveto -Sales & Marketing Executive

• Tendayi Mhiribidi -Human Resources Executive

Management

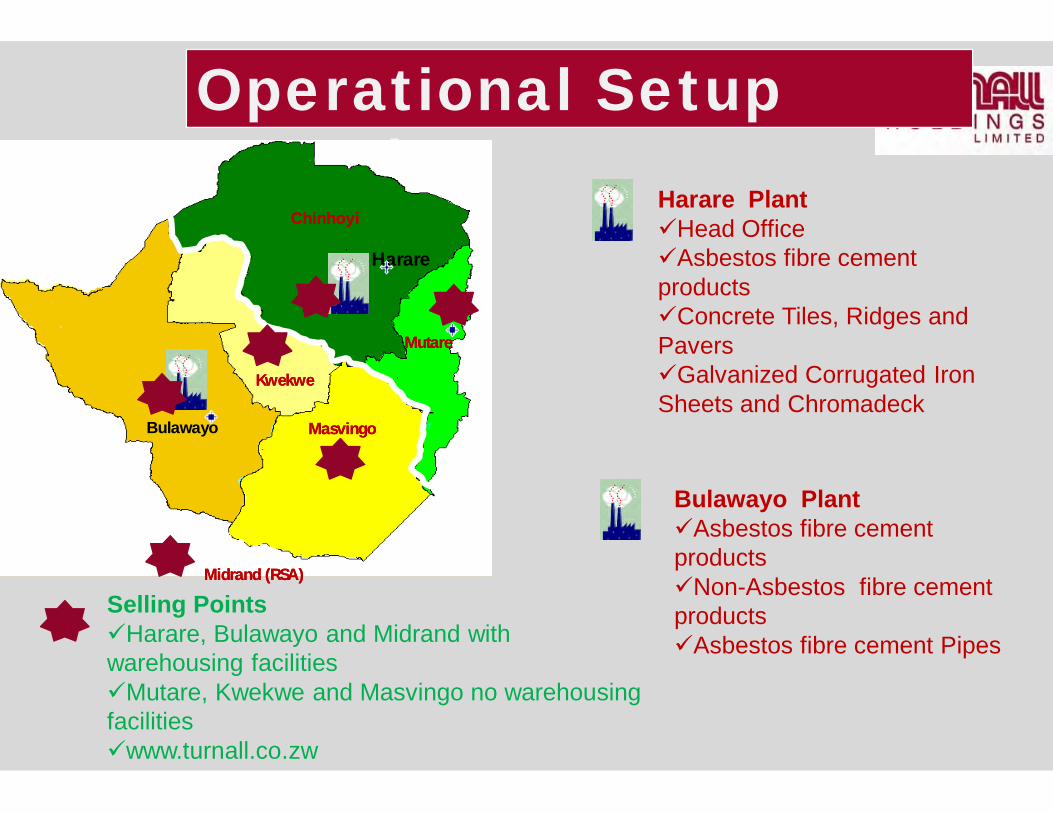

Operational Setup Overview

Harare

MutareMutare

Bulawayo MasvingoMasvingo

KwekweKwekwe

ChinhoyiChinhoyi

Midrand (RSA)Midrand (RSA)

Harare PlantHead OfficeAsbestos fibre cement products Concrete Tiles, Ridges and PaversGalvanized Corrugated Iron Sheets and Chromadeck

Bulawayo PlantAsbestos fibre cement productsNon-Asbestos fibre cement productsAsbestos fibre cement Pipes

Selling PointsHarare, Bulawayo and Midrand with warehousing facilitiesMutare, Kwekwe and Masvingo no warehousing facilitieswww.turnall.co.zw

Products : Building Products

Available in Asbestos and Non-asbestos options

Slates Pantiles Endurite Trafford Tile Ceiling Boards/Flat Sheets Fascia & Barge Boards

Products : Turnallware

Office/Home market

Available in Asbestos and Non-asbestos options

Products : Concrete Products

Tiles

Ridges

Pavers

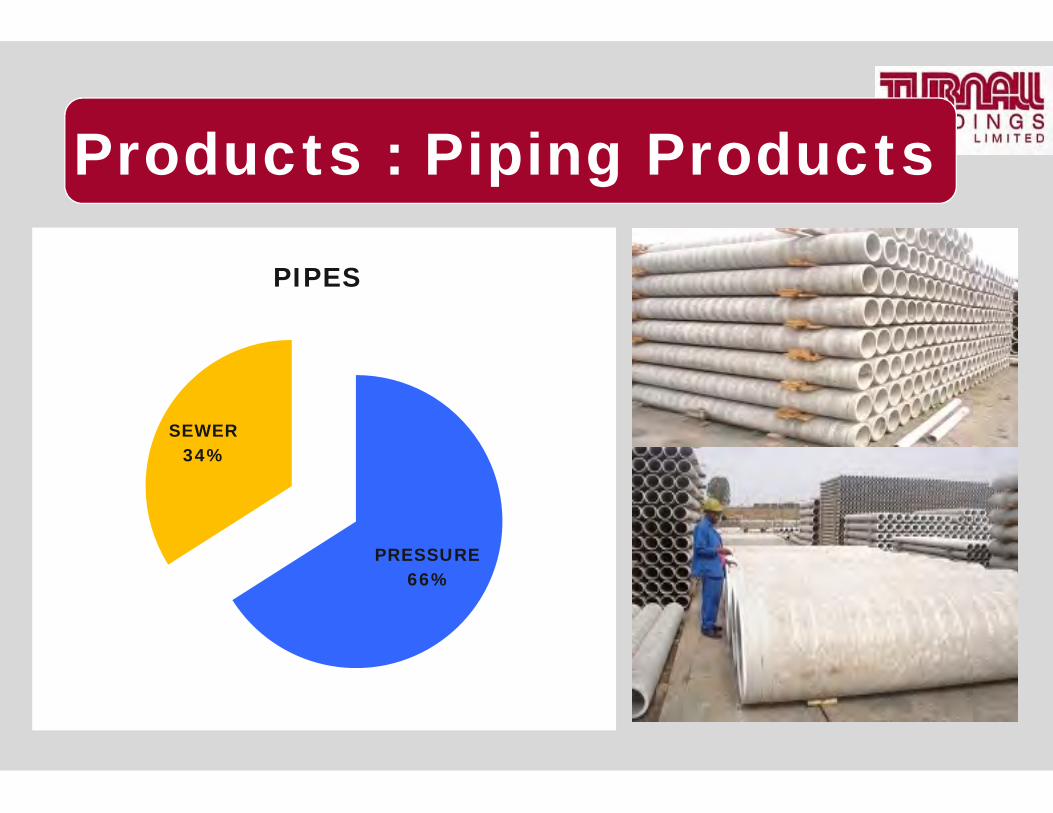

Products : Piping Products

PRESSURE66%

SEWER34%

PIPES

Our MarketsOur Markets

GeographyZimbabweSouth AfricaZambiaMalawiBotswanaNamibiaDRC

UsageRoof coveringBeatificationWater reticulationSewer reticulationPaving solutionsAlternative uses

Target CustomersIndividual projectsCommercial and Industrial projectsGovernment/NGO/Social projects

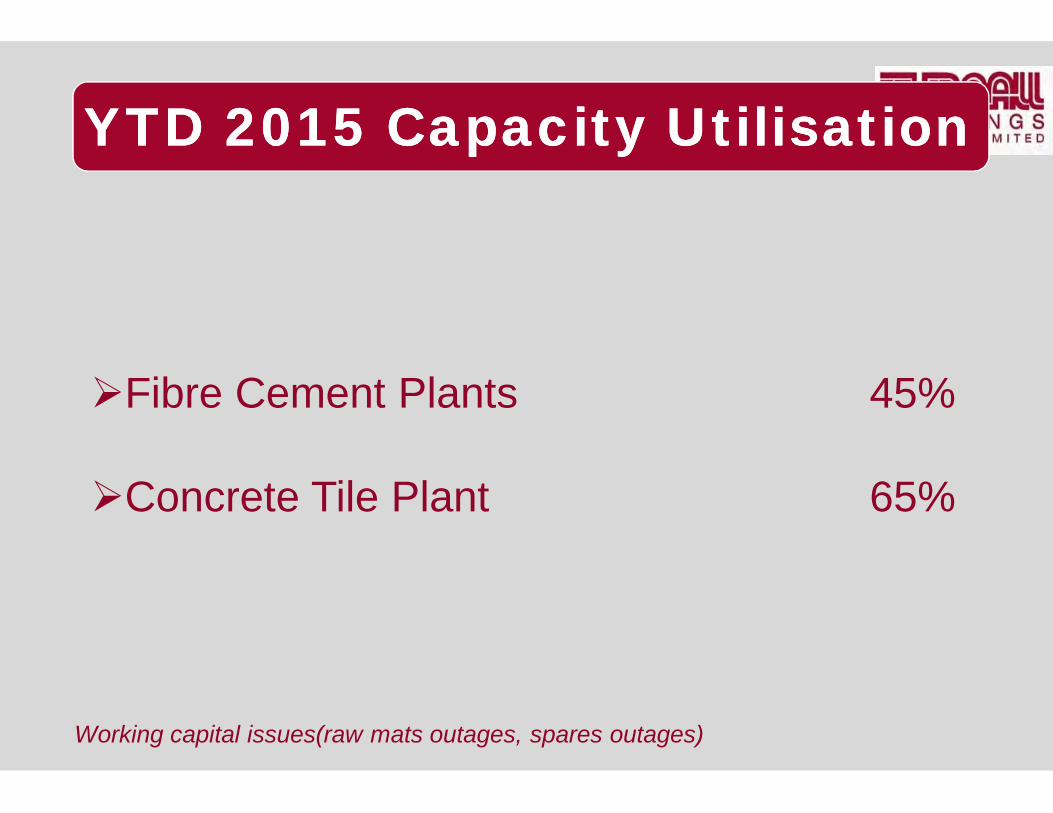

YTD 2015 Capacity UtilisationYTD 2015 Capacity Utilisation

Fibre Cement Plants 45%

Concrete Tile Plant 65%

Working capital issues(raw mats outages, spares outages)

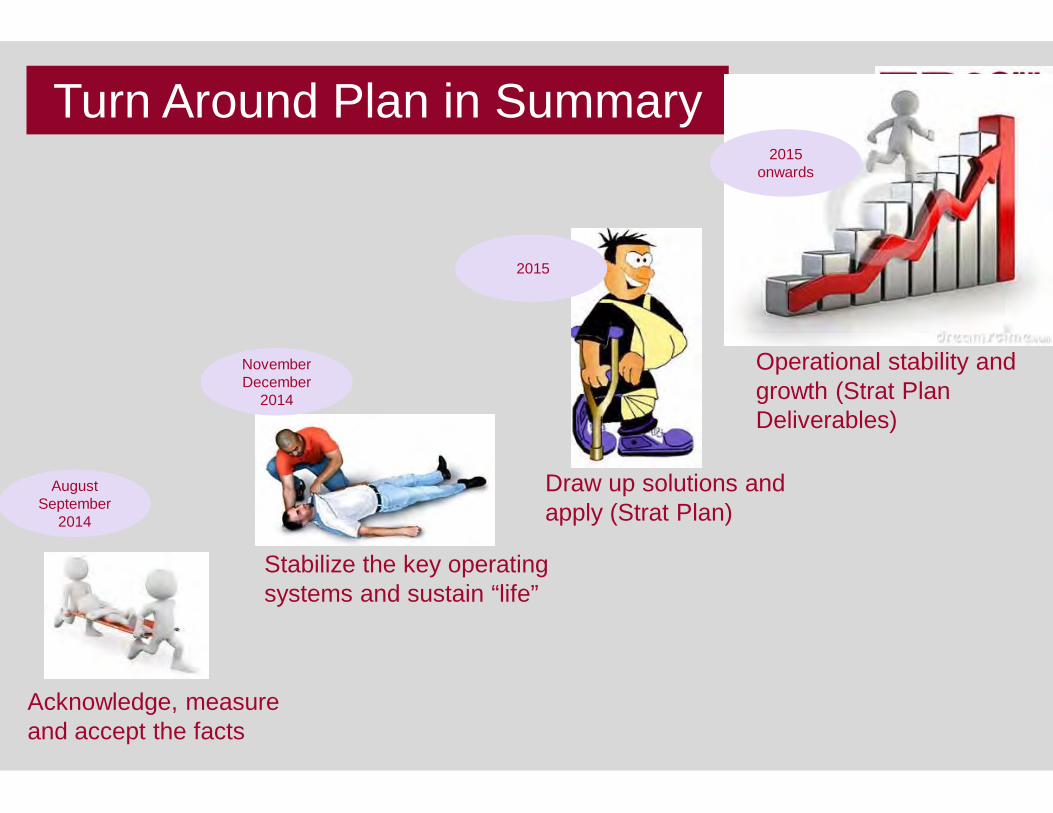

August September

2014

Turn Around Plan in Summary

Acknowledge, measure and accept the facts

Stabilize the key operating systems and sustain “life”

Draw up solutions and apply (Strat Plan)

Operational stability and growth (Strat Plan Deliverables)

November December

2014

2015

2015 onwards

The 3 Year Strategic Plan…Rebirth with integrity

To be the dominant manufacturer and distributor of construction materials for the African continent.

“We enrich African lives and build stakeholder value by providing high quality, affordable and environmentally-friendly construction materials using the talent and passion of our people in the safest, ethical and most professional manner.”

Results through Superior Customer ServiceIntegrity & TransparencyTeamwork & CommitmentExcellence & Innovation

ACRONYM – “RITE”

Vision

Mission Statement

Core Values

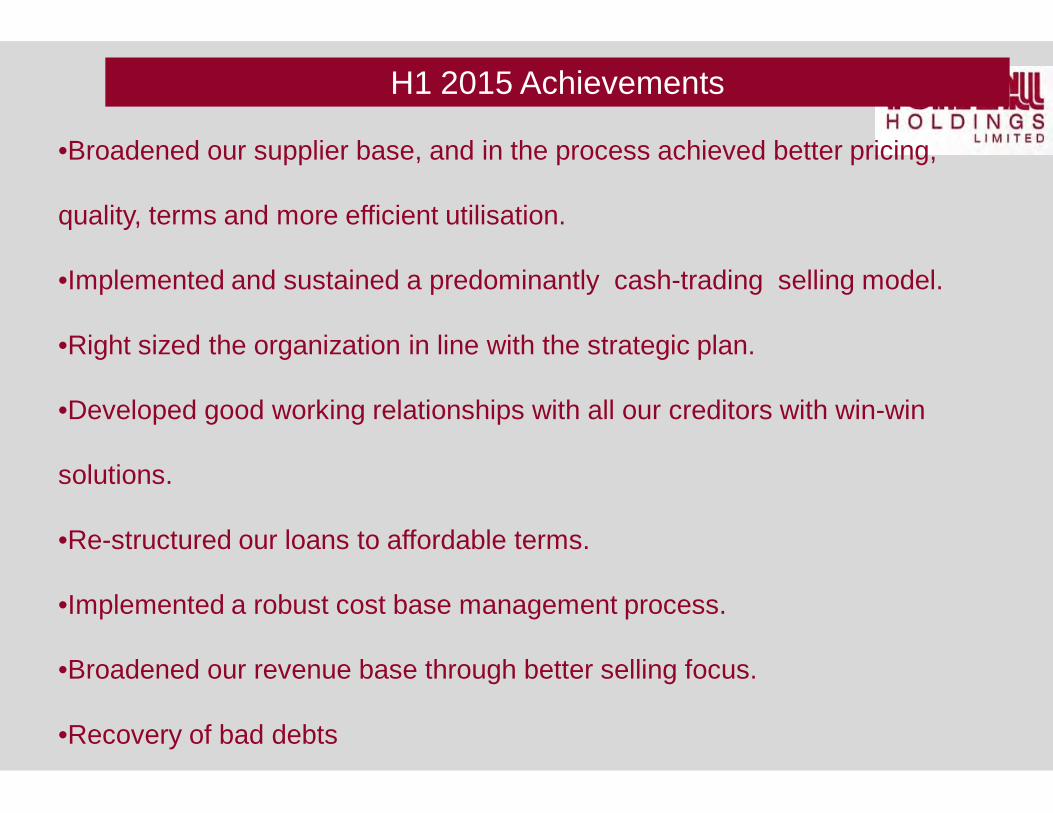

H1 2015 Achievements

•Broadened our supplier base, and in the process achieved better pricing,

quality, terms and more efficient utilisation.

•Implemented and sustained a predominantly cash-trading selling model.

•Right sized the organization in line with the strategic plan.

•Developed good working relationships with all our creditors with win-win

solutions.

•Re-structured our loans to affordable terms.

•Implemented a robust cost base management process.

•Broadened our revenue base through better selling focus.

•Recovery of bad debts

1717

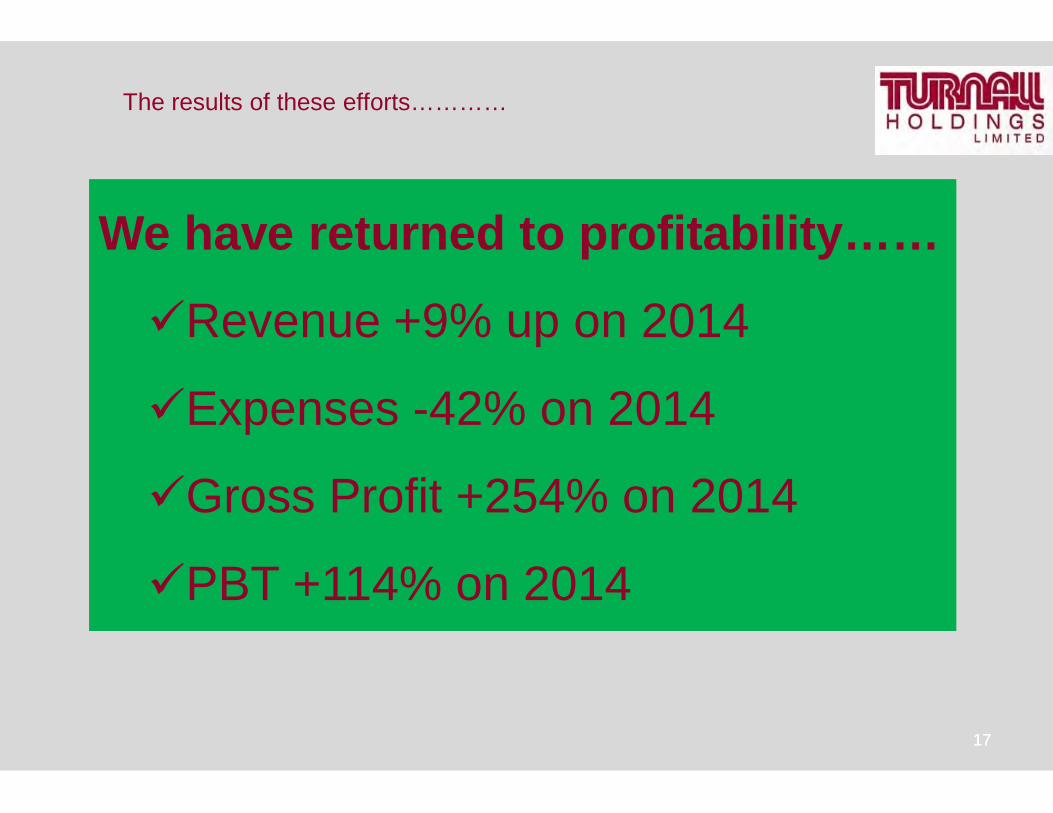

The results of these efforts…………

We have returned to profitability……

Revenue +9% up on 2014

Expenses -42% on 2014

Gross Profit +254% on 2014

PBT +114% on 2014

Financials

Basis of preparation

•Principal accounting policies of the Group have been consistently followed.•Financial statements were approved for issue by the Board of Directors on 20August 2015.

Statement of compliance•Finstats prepared in accordance with accounting policies consistent withInternational Financial Reporting Standards (IFRS) and in the manner requiredby the Zimbabwe Companies Act (Chapter 24:03).•Finstats on statutory records and have been prepared on the historical costbasis•Except for property, plant and equipment that is carried at revalued amounts.•Finstats are presented in United States dollars, which is the Group’s functionaland presentation currency.

Basis of preparation and Statement of compliance

Consolidated Statement of Profit or Loss and Other Comprehensive Income

2020

Note Unaudited UnauditedSix months Six months Audited year

ended ended ended30.06.2015 30.06.2014 31.12.2014

Revenue 1 14 014 935 12 878 086 33 834 344Cost of sales (10 928 832) (12 005 661) (32 367 915)Gross profit 3 086 103 872 425 1 466 429

Other income 79 526 18 195 65 223Selling and distribution expenses (699 638) (775 999) (1 839 248)Administration expense (1 289 729) (2 738 383) (13 046 329)Profit/(loss) from operating activities 1 176 262 (2 623 762) (13 353 925)Finance costs 2 (686 524) (892 261) (1 542 206)Profit/(loss) before tax 489 738 (3 516 023) (14 896 131)Tax (charge)/credit (89 984) 874 834 2 971 606Profit/(loss) for the year 399 754 (2 641 189) (11 924 525)Other comprehensive income/(loss) net of taxRevaluation of property, plant and equipment - - (3 496 112)Foreign currency translation differences 1 009 - 1 667Total comprehensive income/(loss) for the year 400 763 (2 641 189) (15 418 970)

Statement of Profit or loss and other comprehensive income

Unaudited UnauditedSix months Six months Audited year

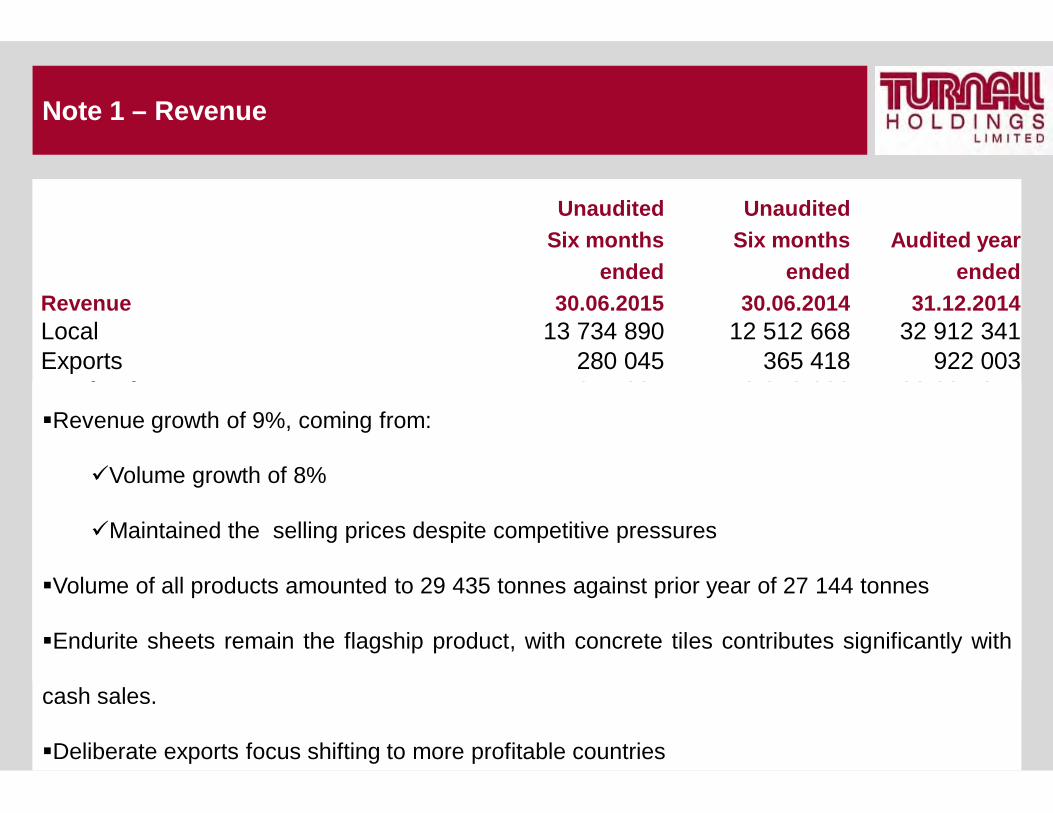

ended ended endedRevenue 30.06.2015 30.06.2014 31.12.2014Local 13 734 890 12 512 668 32 912 341Exports 280 045 365 418 922 003Total sales 14 014 935 12 878 086 33 834 344

Note 1 – Revenue

Revenue growth of 9%, coming from:

Volume growth of 8%

Maintained the selling prices despite competitive pressures

Volume of all products amounted to 29 435 tonnes against prior year of 27 144 tonnes

Endurite sheets remain the flagship product, with concrete tiles contributes significantly with

cash sales.

Deliberate exports focus shifting to more profitable countries

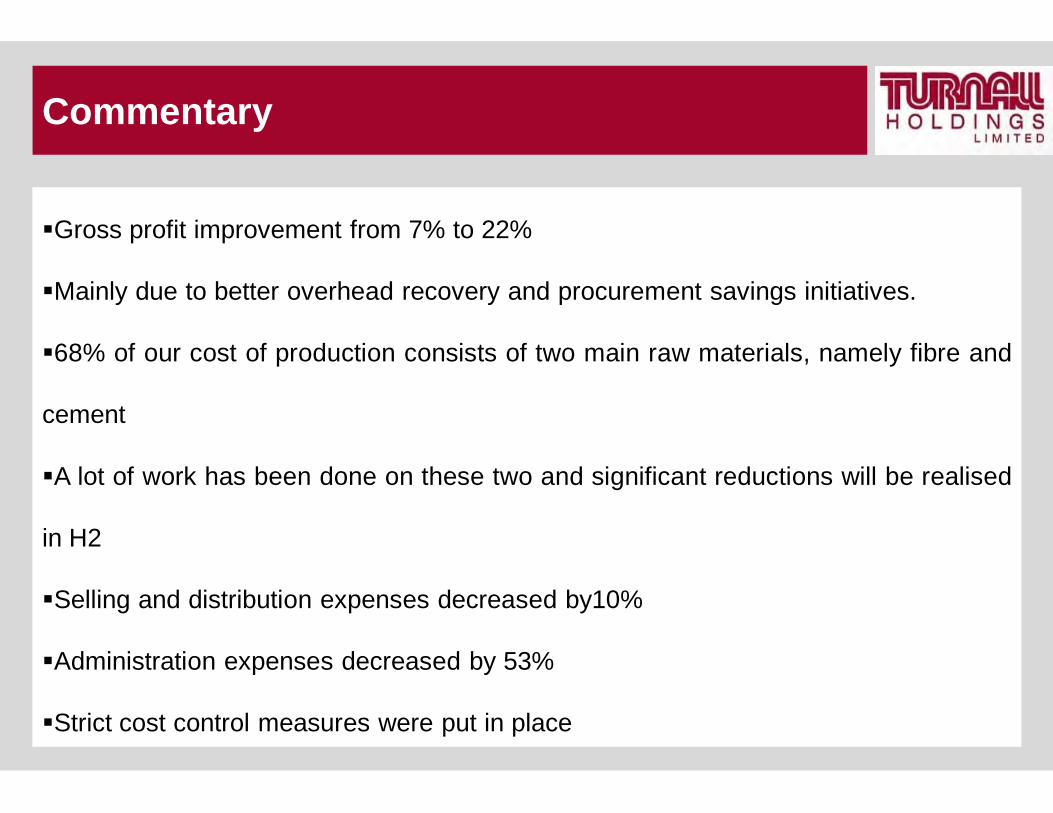

Gross profit improvement from 7% to 22%

Mainly due to better overhead recovery and procurement savings initiatives.

68% of our cost of production consists of two main raw materials, namely fibre and

cement

A lot of work has been done on these two and significant reductions will be realised

in H2

Selling and distribution expenses decreased by10%

Administration expenses decreased by 53%

Strict cost control measures were put in place

Commentary

Unaudited UnauditedSix months Six months Audited year

ended ended ended30.06.2015 30.06.2014 31.12.2014

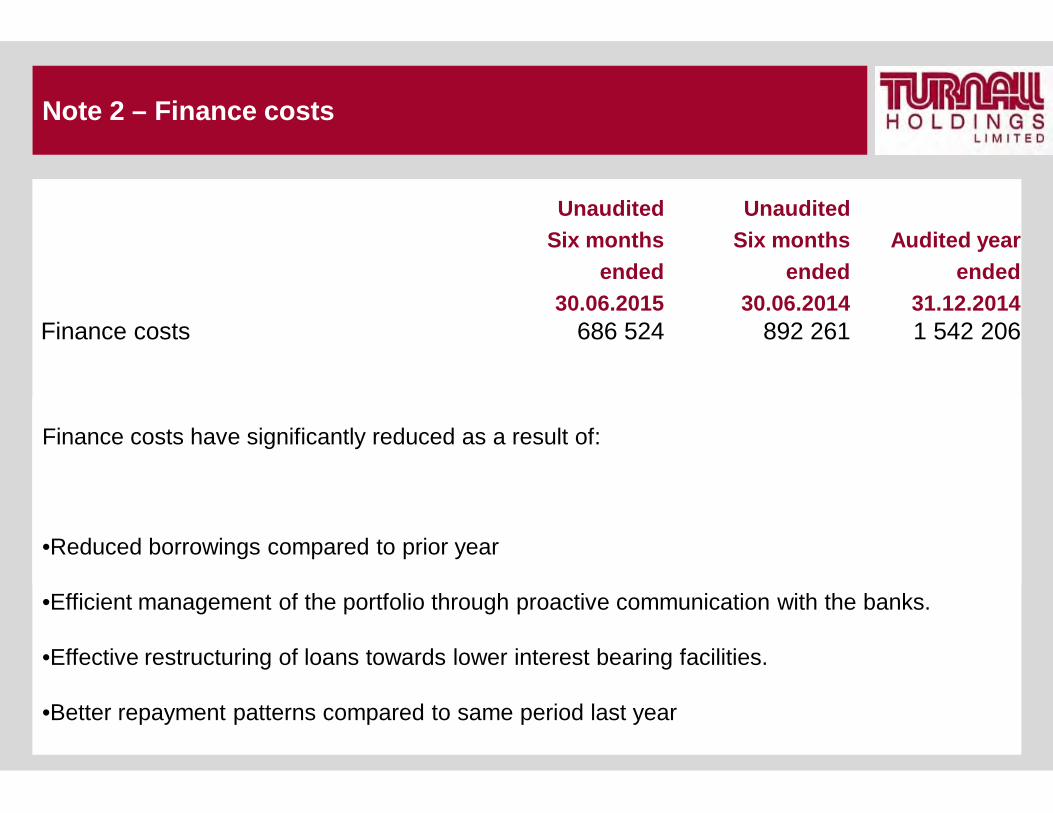

Finance costs 686 524 892 261 1 542 206

Note 2 – Finance costs

Finance costs have significantly reduced as a result of:

•Reduced borrowings compared to prior year

•Efficient management of the portfolio through proactive communication with the banks.

•Effective restructuring of loans towards lower interest bearing facilities.

•Better repayment patterns compared to same period last year

Consolidated Statement of Financial Position

2525

Consolidated Statement of Financial Position

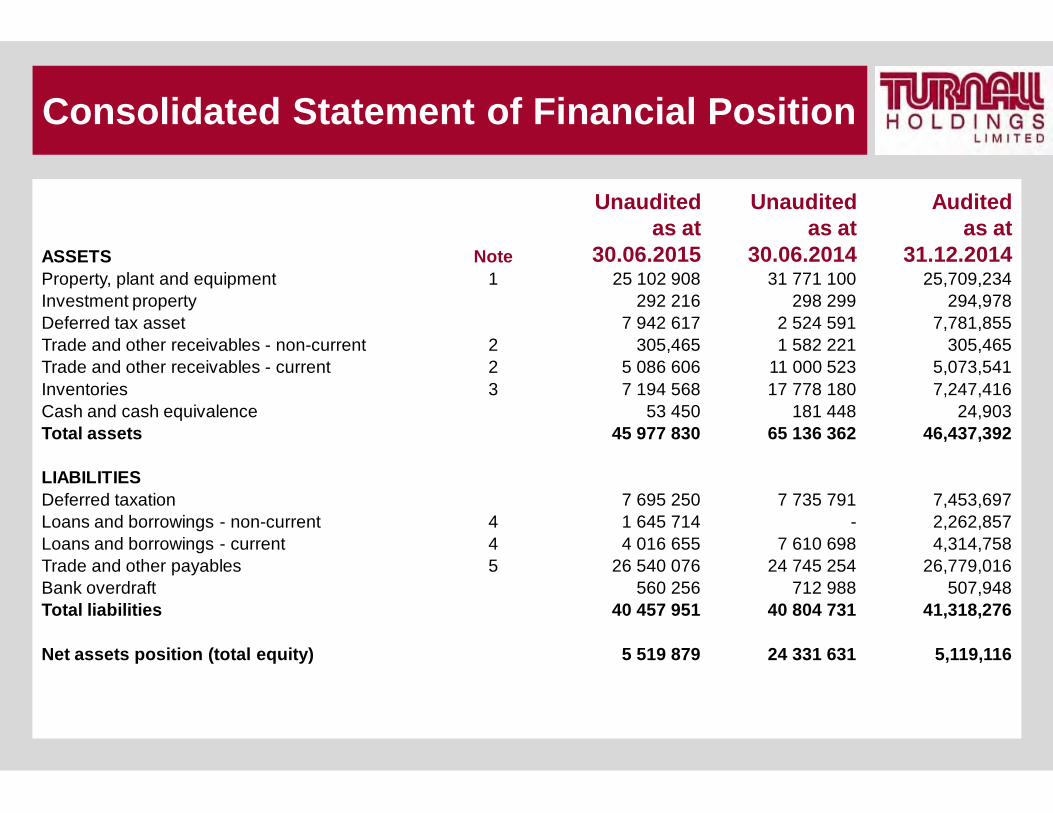

Unaudited Unaudited Auditedas at as at as at

ASSETS Note 30.06.2015 30.06.2014 31.12.2014Property, plant and equipment 1 25 102 908 31 771 100 25,709,234 Investment property 292 216 298 299 294,978 Deferred tax asset 7 942 617 2 524 591 7,781,855 Trade and other receivables - non-current 2 305,465 1 582 221 305,465 Trade and other receivables - current 2 5 086 606 11 000 523 5,073,541 Inventories 3 7 194 568 17 778 180 7,247,416 Cash and cash equivalence 53 450 181 448 24,903 Total assets 45 977 830 65 136 362 46,437,392

LIABILITIESDeferred taxation 7 695 250 7 735 791 7,453,697 Loans and borrowings - non-current 4 1 645 714 - 2,262,857 Loans and borrowings - current 4 4 016 655 7 610 698 4,314,758 Trade and other payables 5 26 540 076 24 745 254 26,779,016 Bank overdraft 560 256 712 988 507,948 Total liabilities 40 457 951 40 804 731 41,318,276

Net assets position (total equity) 5 519 879 24 331 631 5,119,116

Additions-Additions amounted to US$192 625(2014: US$334 845).

-All the additions were for the maintenance of the current capacity

Assets pledged as securityThe Harare and Bulawayo properties are pledged as security for the FBC and BancABCloans.

Note 1 - Property, plant and equipment

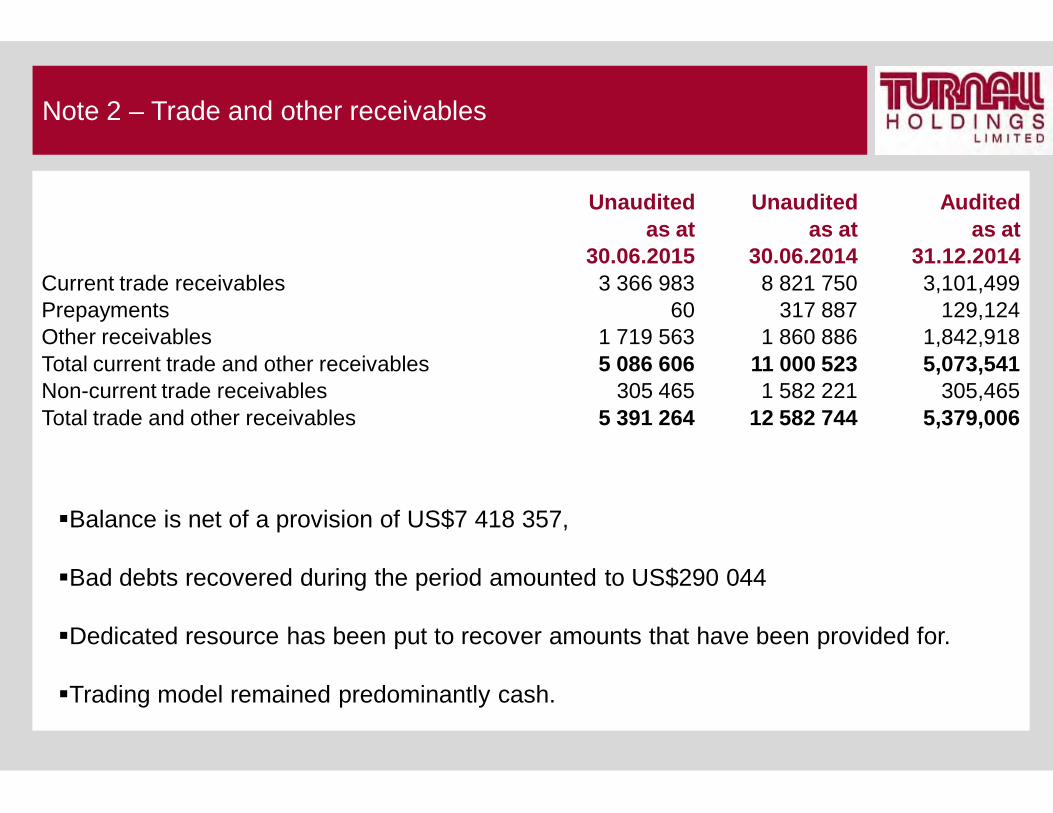

Note 2 – Trade and other receivables

Balance is net of a provision of US$7 418 357,

Bad debts recovered during the period amounted to US$290 044

Dedicated resource has been put to recover amounts that have been provided for.

Trading model remained predominantly cash.

Unaudited Unaudited Auditedas at as at as at

30.06.2015 30.06.2014 31.12.2014Current trade receivables 3 366 983 8 821 750 3,101,499 Prepayments 60 317 887 129,124 Other receivables 1 719 563 1 860 886 1,842,918 Total current trade and other receivables 5 086 606 11 000 523 5,073,541 Non-current trade receivables 305 465 1 582 221 305,465 Total trade and other receivables 5 391 264 12 582 744 5,379,006

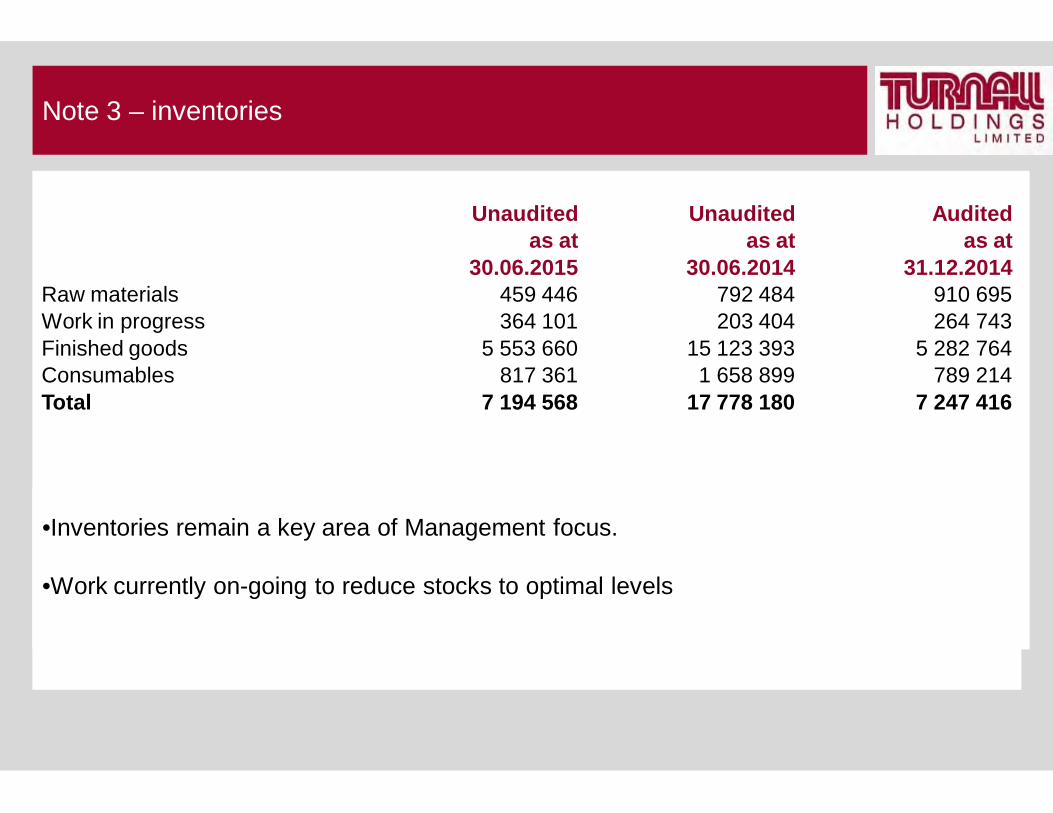

Note 3 – inventories

•Inventories remain a key area of Management focus.

•Work currently on-going to reduce stocks to optimal levels

Unaudited Unaudited Auditedas at as at as at

30.06.2015 30.06.2014 31.12.2014Raw materials 459 446 792 484 910 695 Work in progress 364 101 203 404 264 743 Finished goods 5 553 660 15 123 393 5 282 764 Consumables 817 361 1 658 899 789 214 Total 7 194 568 17 778 180 7 247 416

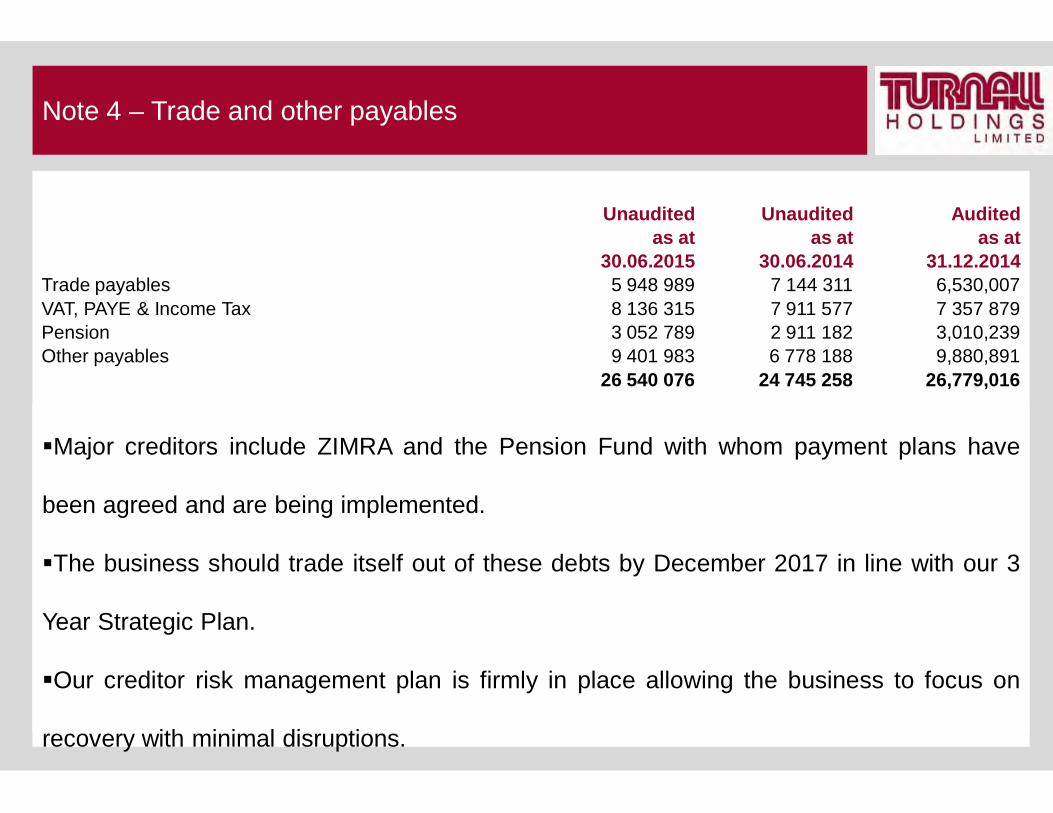

Note 4 – Trade and other payables

Major creditors include ZIMRA and the Pension Fund with whom payment plans have

been agreed and are being implemented.

The business should trade itself out of these debts by December 2017 in line with our 3

Year Strategic Plan.

Our creditor risk management plan is firmly in place allowing the business to focus on

recovery with minimal disruptions.

Unaudited Unaudited Auditedas at as at as at

30.06.2015 30.06.2014 31.12.2014Trade payables 5 948 989 7 144 311 6,530,007 VAT, PAYE & Income Tax 8 136 315 7 911 577 7 357 879 Pension 3 052 789 2 911 182 3,010,239 Other payables 9 401 983 6 778 188 9,880,891

26 540 076 24 745 258 26,779,016

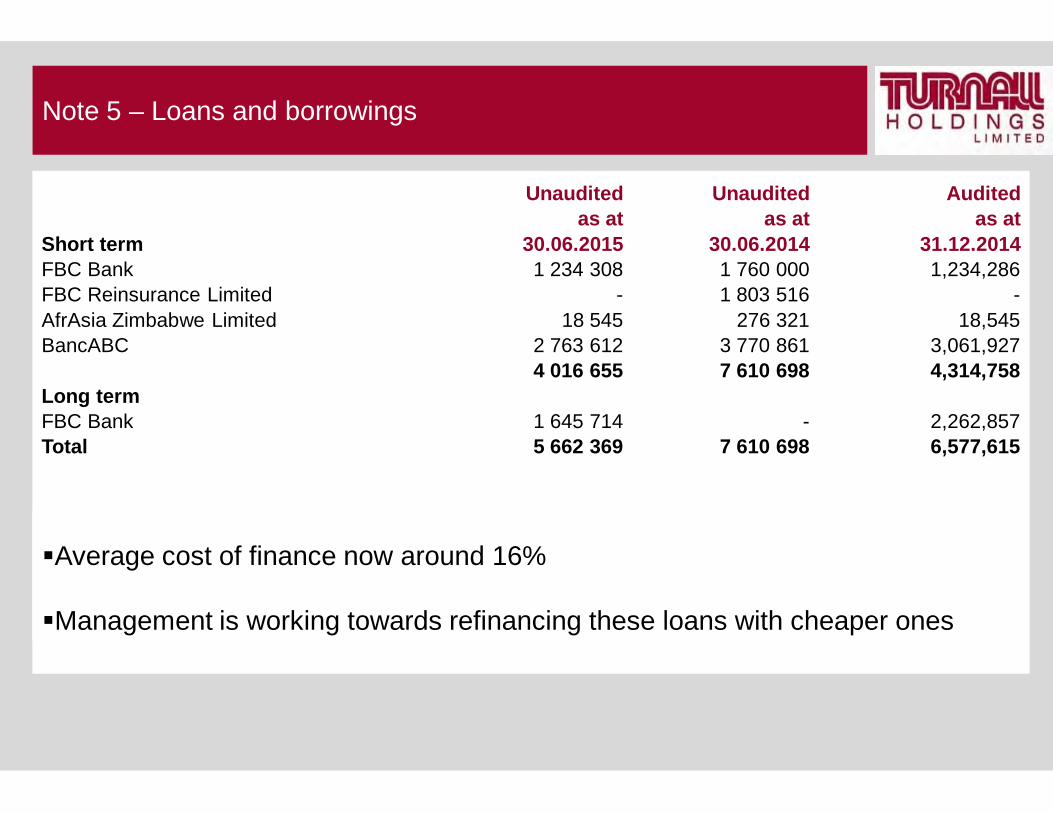

Note 5 – Loans and borrowings

Average cost of finance now around 16%

Management is working towards refinancing these loans with cheaper ones

Unaudited Unaudited Auditedas at as at as at

Short term 30.06.2015 30.06.2014 31.12.2014FBC Bank 1 234 308 1 760 000 1,234,286 FBC Reinsurance Limited - 1 803 516 -AfrAsia Zimbabwe Limited 18 545 276 321 18,545 BancABC 2 763 612 3 770 861 3,061,927

4 016 655 7 610 698 4,314,758 Long term FBC Bank 1 645 714 - 2,262,857 Total 5 662 369 7 610 698 6,577,615

Statement of cash flows

3232

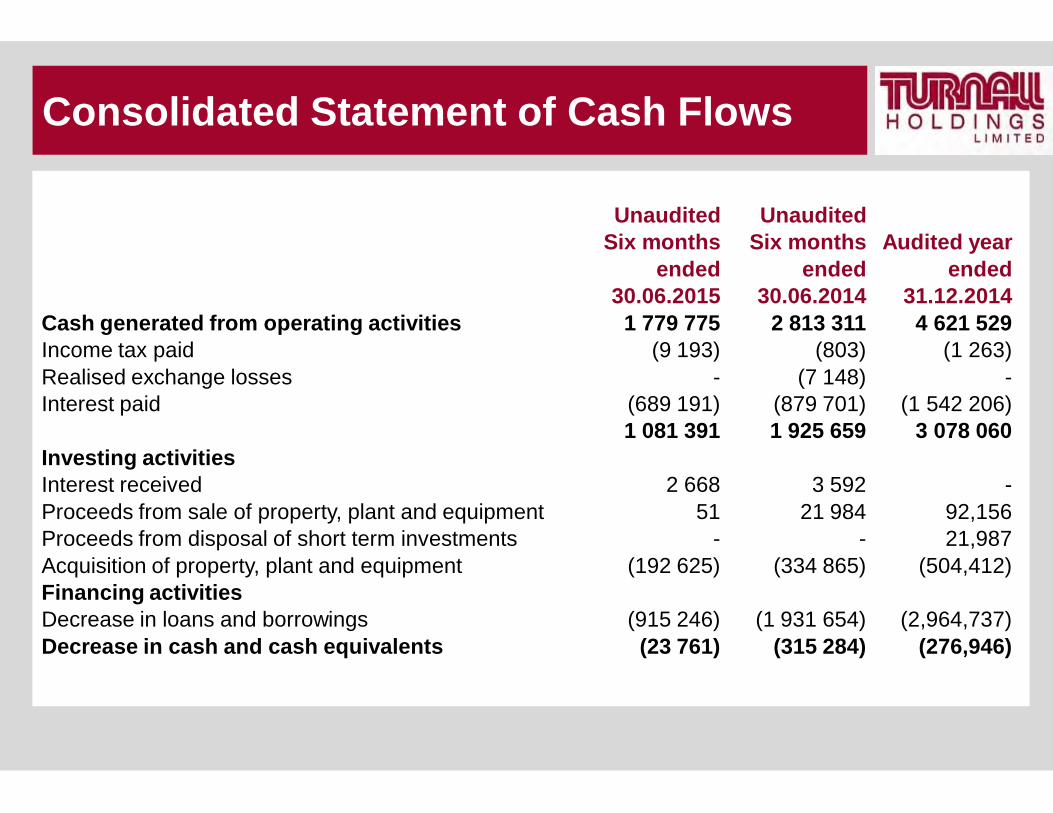

Consolidated Statement of Cash Flows

Unaudited UnauditedSix months Six months Audited year

ended ended ended30.06.2015 30.06.2014 31.12.2014

Cash generated from operating activities 1 779 775 2 813 311 4 621 529 Income tax paid (9 193) (803) (1 263)Realised exchange losses - (7 148) -Interest paid (689 191) (879 701) (1 542 206)

1 081 391 1 925 659 3 078 060 Investing activitiesInterest received 2 668 3 592 -Proceeds from sale of property, plant and equipment 51 21 984 92,156 Proceeds from disposal of short term investments - - 21,987 Acquisition of property, plant and equipment (192 625) (334 865) (504,412)Financing activitiesDecrease in loans and borrowings (915 246) (1 931 654) (2,964,737)Decrease in cash and cash equivalents (23 761) (315 284) (276,946)

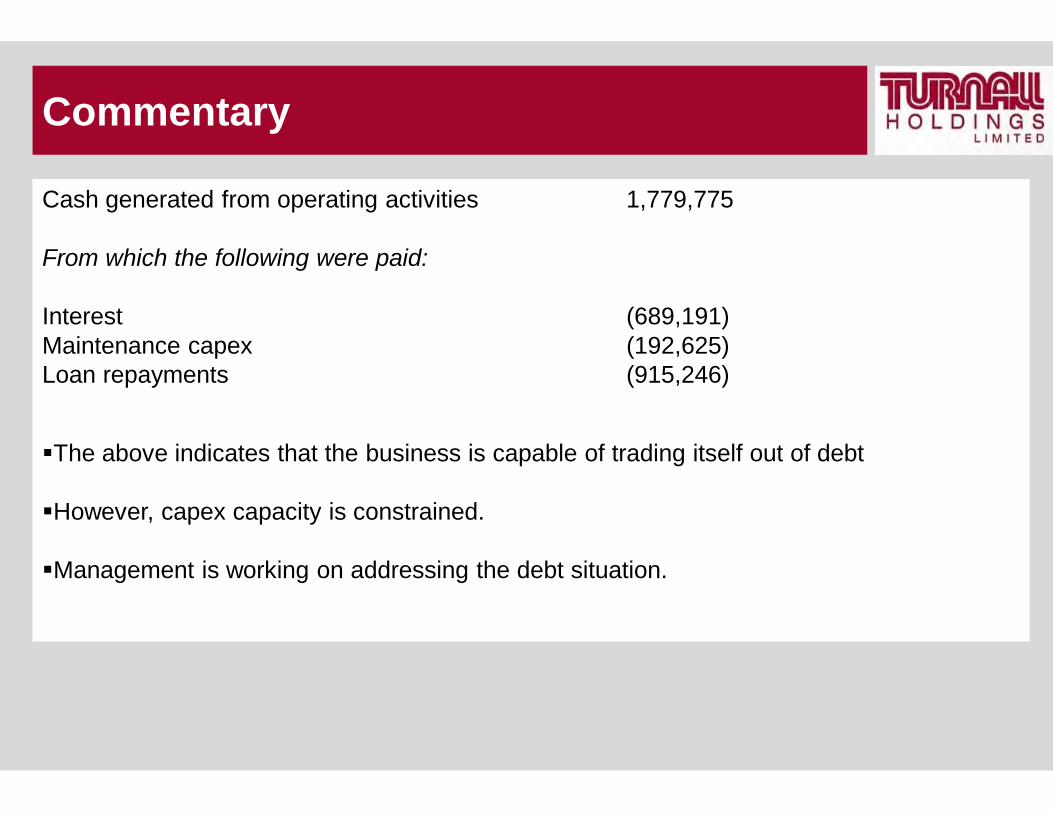

Cash generated from operating activities 1,779,775

From which the following were paid:

Interest (689,191)Maintenance capex (192,625)Loan repayments (915,246)

The above indicates that the business is capable of trading itself out of debt

However, capex capacity is constrained.

Management is working on addressing the debt situation.

Commentary

The future outlook

•H2 2015 and full year 2015 will be profitable, driven by full actualization of the

benefits of our initiatives, in particular on raw materials. We are well placed to

sustain profitability into the future.

•We have made good progress on working capital funding solutions, with the

actual funding imminent.

•The work on getting our balance sheet right is continuing, this is a “must win

battle” for us.

• Our new vision has opened new business scopes for us, which we are

pursuing……we are more than just asbestos!!!

Challenges for Developing CountriesChallenges for Developing Countries

Opportunities for Turnall

Affordable Housing – safe shelter

Access to Safe Drinking Water – about 30% of developing nations population do not have access

Effective Sanitation – less than 50% of developing nations population have access

All key elements in ZimAsset

We see the potential….and we will achieve it!

3838

Thank youTinotendaSiyabonga

Questions &

Answers