Embed Size (px)

Citation preview

your state-wide property research guide suburb by suburb

REIQ

QU

EENS

LAN

D M

AR

KET

MO

NIT

OR

ISS

UE 28

SEP QTR 2015

>p2

QMM STATE-WIDE COMMENTARY

Proudly supported by REIQ member

Linda DeBello

STEADY GROWTH CONTINUES IN SEQ The Brisbane local government area (LGA) median house price has pushed to a new high of $615,000 as consistent steady growth continues.

While predictions have been prolific that the slowing conditions in Sydney would flow through to Brisbane, the Queensland capital city has clearly defied predictions, helped by southern investors eyeing off bargains in the sunshine state.

According to data from the Australian Bureau of Statistics, investor activity increased 1.4 per cent in Queensland over the month of September.

Regional centres once reliant on the mining industry are still stabilising, with the bottom of the market likely having now been met in most areas.

Ongoing employment issues are the largest hindrance on these regions entering a recovery phase.

In light of this, a number of local councils are implementing initiatives that will diversify their region’s economy in an effort to create new industries and new jobs.

2 QUEENSLAND MARKET MONITOR

REIQ RESEARCH EXPLANATORY NOTESSALES MARKET DATA

All figures for the most recent quarterly and yearly periods are preliminary only and subject to further revision as additional sales records become available (see Research Methodology online at reiq.com).

As of the June quarter 2013, all sales data includes "Recent Sales" as advised by real estate agents as well as official records as advised by DNRM. As such comparisons with figures published prior to the June quarter 2013 should be done with caution.

A median sale price is derived by arranging a set of sale prices from lowest to highest and then selecting the middle value within this set (ie the 50th percentile, where half of recorded sales were less and half were higher than the median). Only suburbs and regions to record sufficient sales numbers

at the time of reporting are published.

N/ADue to insufficient sales numbers (as at the time of data extraction) no median sale price has been calculated

(LGA) Local Government Area

Brisbane (SD)

Brisbane Statistical Division comprising the LGA’s of Brisbane City, Ipswich City, Logan City, Moreton Bay Regional and Redland City

Sunshine Coast (SD)

Sunshine Coast Region comprising the LGA's of Sunshine Coast Regional and Noosa.

# Figures based upon the new council boundaries

^Indicates acreage sales only (with land size greater than 2400m2). All other data is based upon sales with a land size of less than 2400 m2

~Median price changes influenced by varying quality of stock sold

*Median price changes influenced by varying quantities of new properties sold

fMedian price changes influenced by varying quantities of waterfront properties sold

tMedians affected by varying quantities of townhouses sold

Y Median affected by high yielding property sales

1

Median price changes influenced by the varying volumes of sales between the Mainland and Bay Islands areas

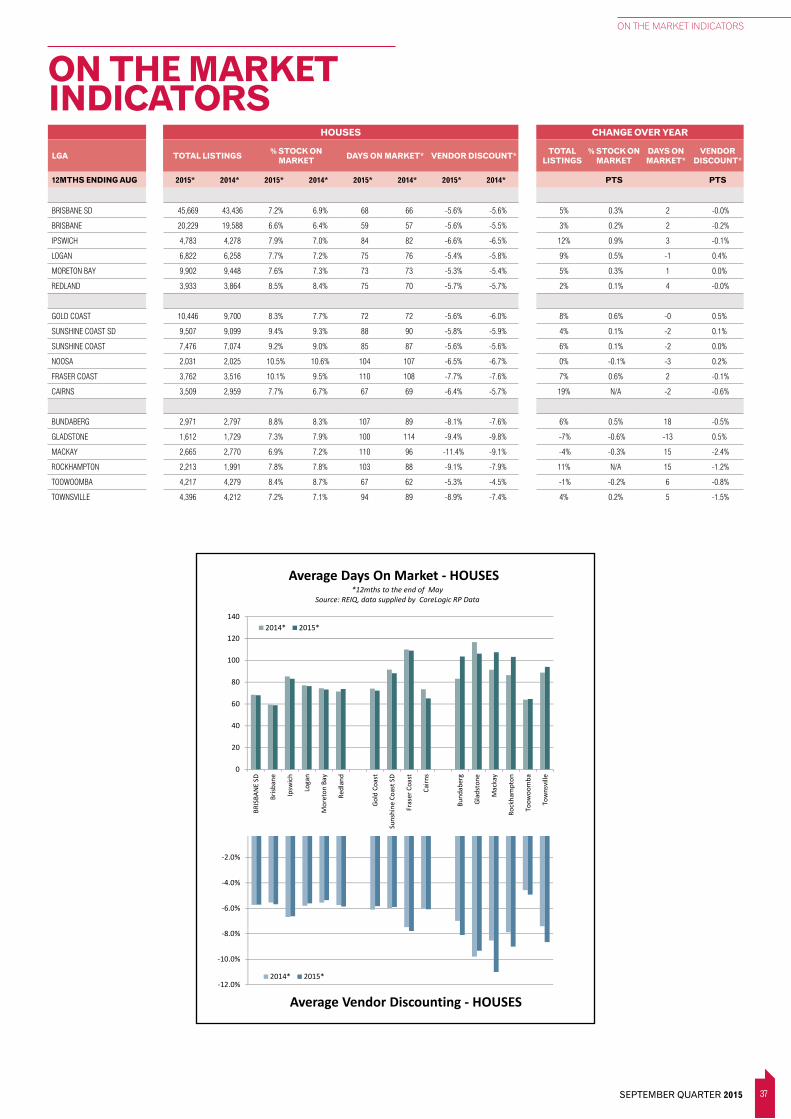

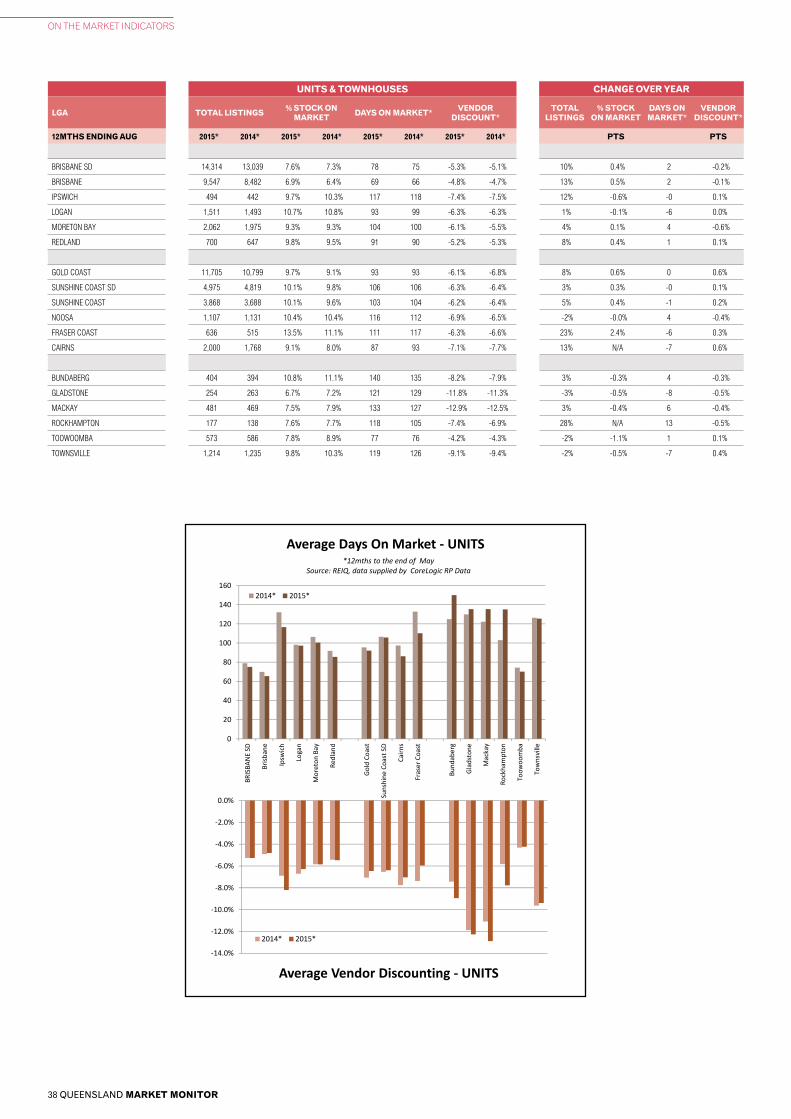

ON THE MARKET INDICATORS

At the time of publication, latest information available was for the 12 months ending the month prior to the current period.

"Days on Market" is calculated as the average number of days it has taken to sell those properties sold by private treaty sale during the 12 month period. The calculation excludes auction listings and listings where an asking price is not advertised. The days on market calculation uses the contract date on the property compared with the first advertised date.

"Vendor Discount" is the average difference between the contract price on a property and the first advertised price. The figure is expressed as a percentage and is an average of all private treaty sales which sold for less than their initial asking price during the last 12 months. Auction listings, listings without an advertised asking price and properties sold at or above list price are excluded from the calculation.

"Total Listings" is the total unique number of properties that have been advertised for sale and captured by RP Data over the 12 month period. To be included in the count, the listings have to be matched to an actual address.

"% Stock on Market" is the percentage of dwellings within the suburb or local government area that have been listed for sale over the past year.

Source: REIQ, data supplied by CoreLogic RP Data (www.corelogic.com.au)

PRICE POINT GRAPHS

All data contained within these graphs represent preliminary sales numbers and are subject to revision as additional sales records become available.

The data excludes any recent sales transactions where the contract sale price was not disclosed.

The intention of these graphs is to gauge trends in sales activity between periods in lieu of actual final sales results.Source: REIQ, data obtained from CoreLogic RPData

Data report date: 11 Nov 2015 Published date: 14 Dec 2015

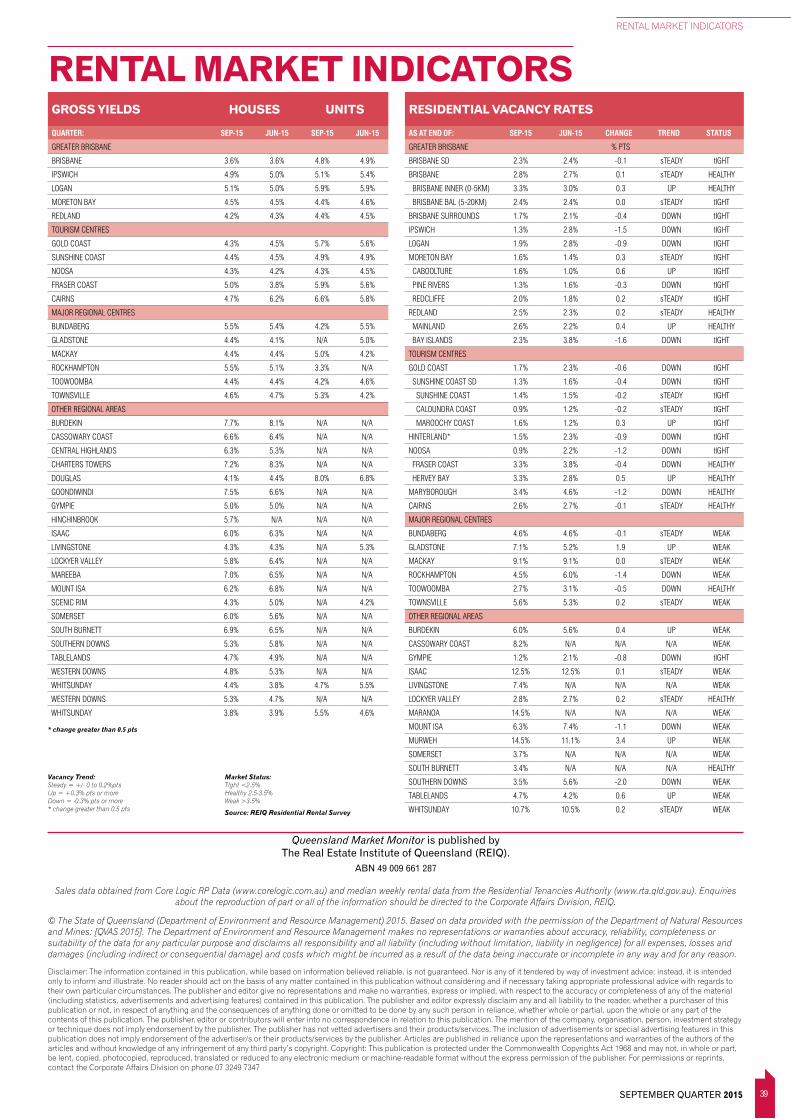

GROSS RENTAL YIELDS

House yields are based upon REIQ median house prices and RTA median weekly rent for three bedroom houses.

Unit yields are based upon REIQ median unit & townhouse sale prices and RTA median weekly rent for two bedroom units and townhouses.

VACANCY RATES

All figures are based upon all residential rentals as at the end of each quarterly period, as submitted by REIQ accredited agents.

Only LGAs with a minimum sample size of 10 per cent (based upon number of bonds held by the RTA) are reported on.

N/ADue to insufficient information received no vacancy rate has been calculated

Source: REIQ Residential Rental Survey

RENTAL MARKET DATA

All median weekly rents are published on a postcode basis, as calculated by the Residential Tenancies Authority, where sufficient data is available.

Caution should be exercised when interpreting any median rental price data based upon a relatively small number of new bond lodgements.

Figures for the new LGA's available for the current quarter only.

LListed localities (or suburbs) represent one of potentially several that fall within that postcode.

N.A.Due to insufficient new bond lodgements, no median rental price has been calculated

Source: Residential Tenancies Authority, Rental Bond lodgements (www.rta.qld.gov.au)

3

STATE-WIDE SUMMARY

SEPTEMBER QUARTER 2015

FALLING

STABILISINGRECOVERING

RISING

BRISBANE HOUSE MARKETSSeptember Quarter 2015

Source: REIQ

Brisbane↑ Moreton Bay

↑ LoganRedlandIpswich

FALLING

STABILISINGRECOVERING

RISING

QUEENSLAND HOUSE MARKETSSeptember Quarter 2015

Source: REIQ

Brisbane SDCairns

Gold CoastSunsine Coast

Fraser Coast

MackayBundaberg Gladstone

Rockhampton Townsville

↑ Toowoomba

The Real Estate Institute of Queensland Ltd. Copyright 2014 21 Turbo Drive, Coorparoo, PO Box 1555, Coorparoo DC Q 4151Ph: (07) 3249 7347 Fax: (07) 3249 6211 Email: [email protected]

3 QUEENSLAND MARKET MONITOR

Queensland market update 1

REIQ Explanatory notes 2

Brisbane market updates

Brisbane City 6

Greater Brisbane 11

Regional market updates

Gold Coast 16

Toowoomba 19

Sunshine Coast 21

Fraser Coast 23

Bundaberg 25

Gladstone 27

Rockhampton 28

Mackay 30

Townsville 32

Cairns 34

Other Regional 36

On The Market Indicators 37

Total Listings

% Stock on Market

Average Vendor Discount

Average Days on Market

Rental Market Indicators 39

Gross rental yields

Residential vacancy rates

TABLE OF CONTENTS

REIQ

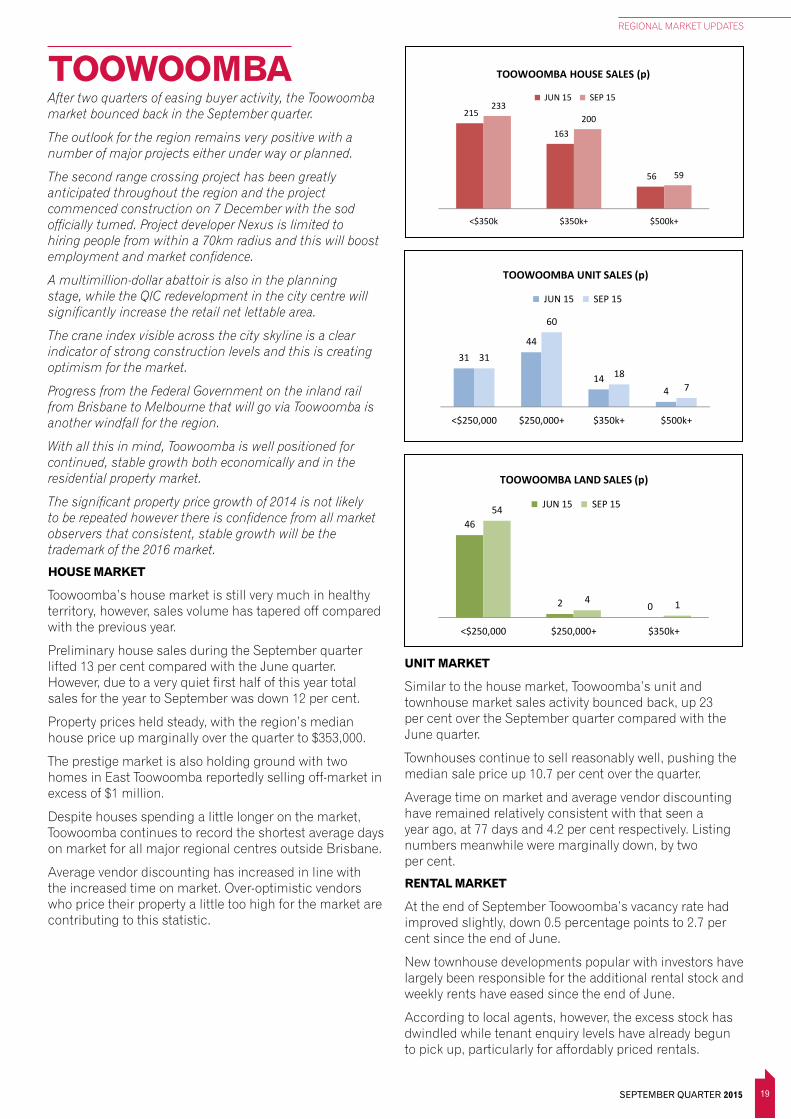

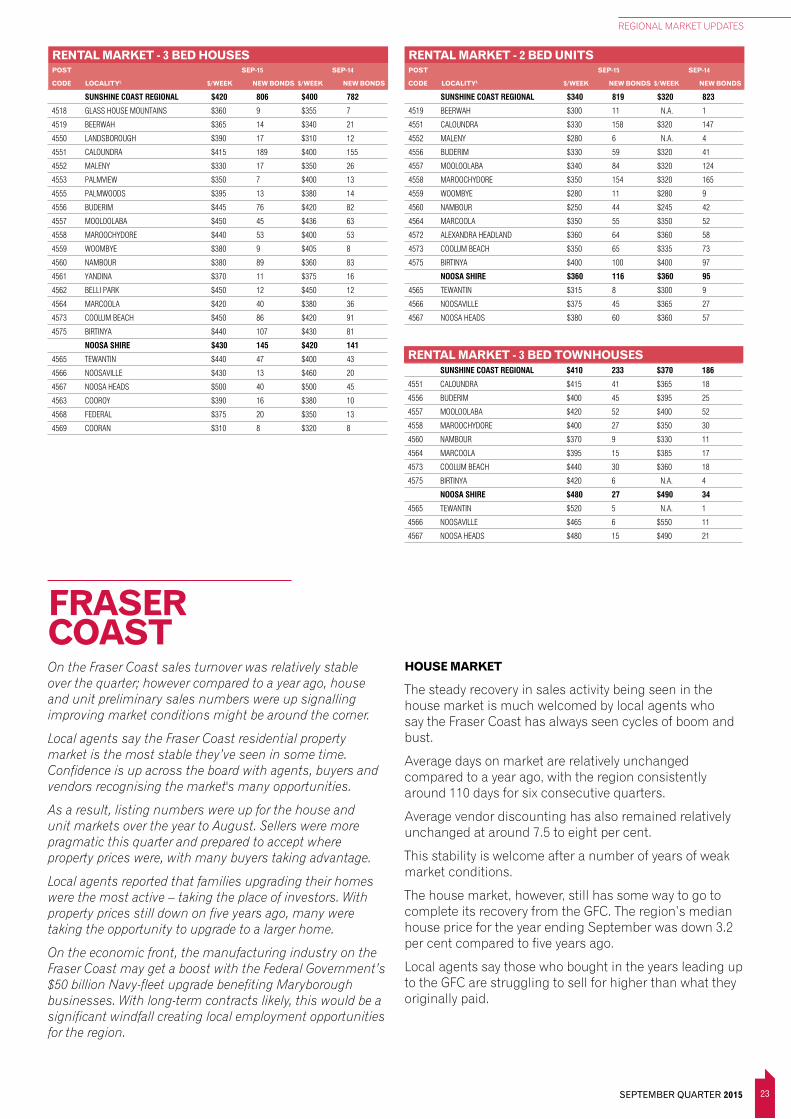

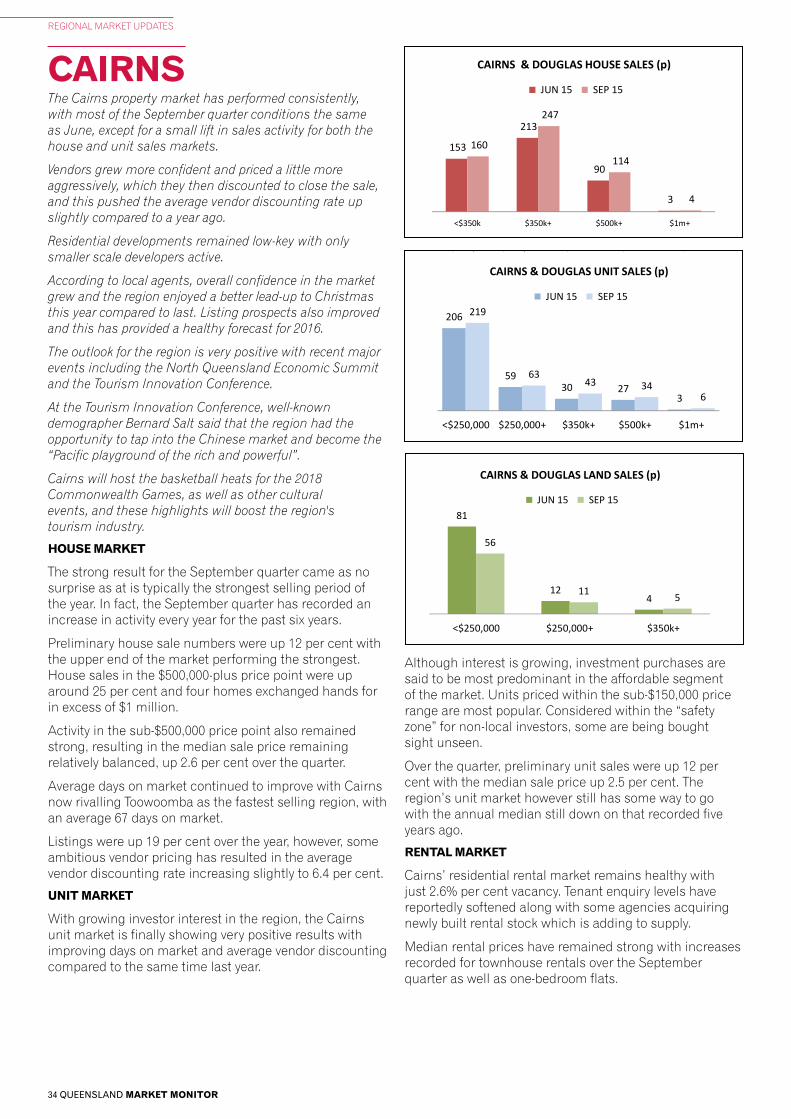

The tourism centres showed significant improvement to house sales markets

STATE-WIDE SUMMARY CONTINUED

HOUSE MARKET

Over the September quarter, the Brisbane house market led the way, with preliminary house sales reaching levels not seen in more than five years. New listings helped the market maintain equilibrium, fostering sustainable property price growth.

Sales activity was also up across the southeast and the tourism centres, with Ipswich the stand-out performer. Ipswich also recorded the highest quarterly increase for the Greater Brisbane region with the median house price lifting 1.6 per cent to $320,000.

The tourism centres also continued to improve, with the Gold Coast's median house price recording the highest quarterly increase of all the major centres.

Cairns performed well over the quarter, recording a new median house price of $400,000, up 2.6 per cent. With house sales activity and listings up, the state’s far north tourism destination moved into stronger market conditions.

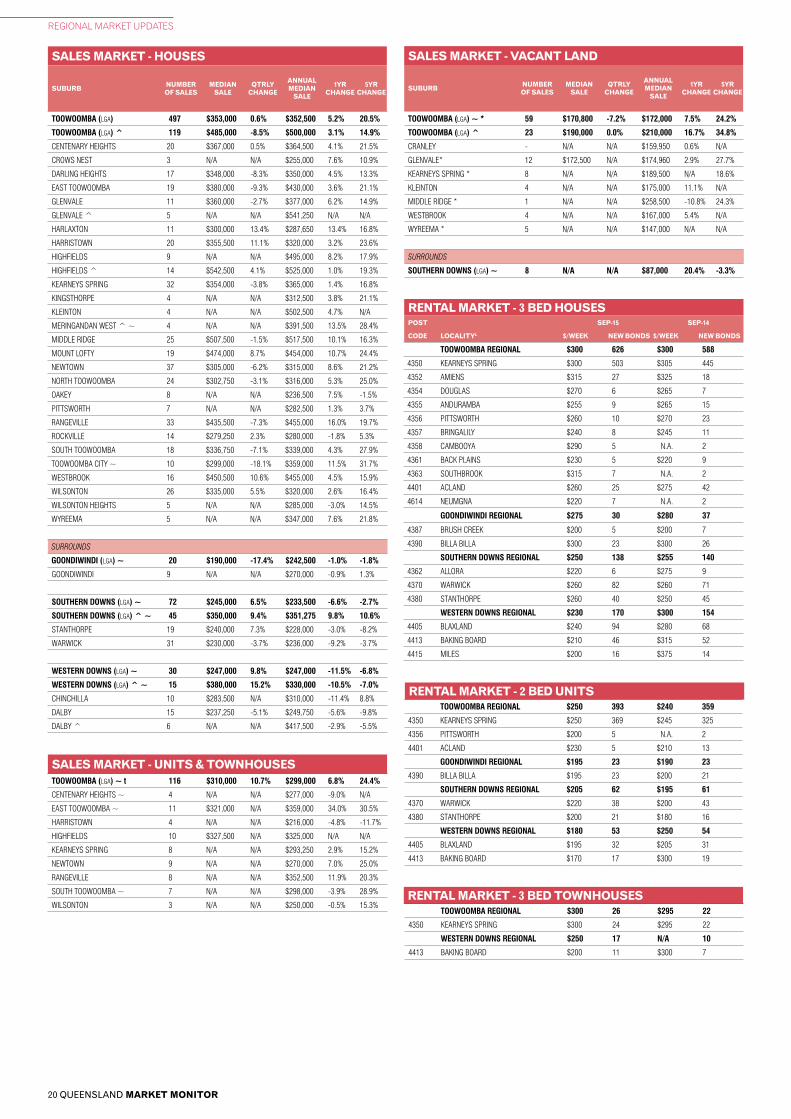

After easing sales activity over the first half of 2015, Toowoomba house sales activity bounced back, up 13 per cent over the quarter. Following a strong 2014, local agents say Toowoomba is likely to stick to the established long-term trend of conservative yet consistent property price growth.

On the Fraser Coast, sales market conditions remained steady with little change.

Average days on market and average vendor discounting remained relatively unchanged, while listings increased slightly heading into spring.

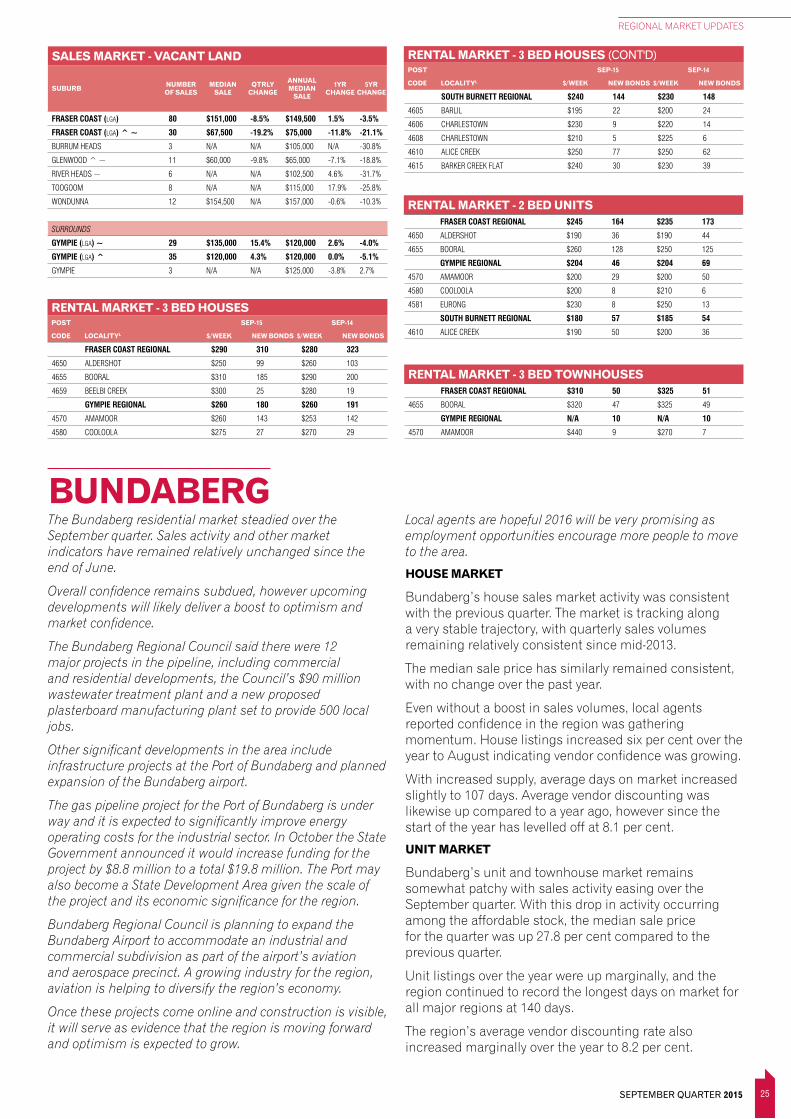

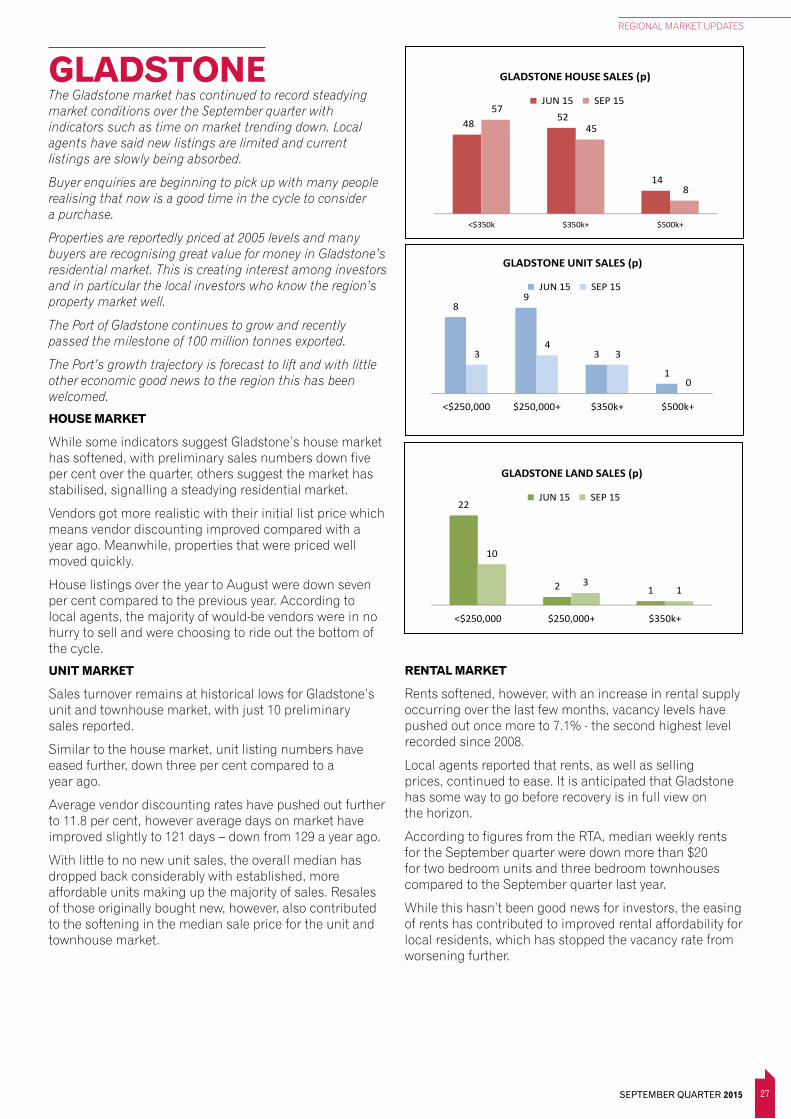

In other regional centres, market conditions remained weak, although, September quarter data shows Gladstone may be turning a corner.

The major east coast cities of Rockhampton and Townsville, along with Bundaberg also recorded relatively stable house sales activity over the quarter, however improvements in days on market and vendor discounting have yet to be seen.

4 QUEENSLAND MARKET MONITOR

STATE-WIDE SUMMARY

HOUSES (<2400) UNITS & TOWNHOUSES VACANT LAND (<2400)

LGA MEDIAN SALE PRICE

QTRLY CHANGE

SALES ACTIVITY CHANGE

MEDIAN SALE PRICE

QTRLY CHANGE

SALES ACTIVITY CHANGE

MEDIAN SALE PRICE

QTRLY CHANGE

SALES ACTIVITY CHANGE

GREATER BRISBANE

BRISBANE SD $480,000 0.2% 5% $397,500 1.9% 7% $207,750 -3.3% 4%

BRISBANE $615,000 0.8% 5% $430,000 1.2% 13% $342,500 0.4% 25%

IPSWICH $320,000 1.6% 12% $258,000 3.2% 15% $176,250 0.2% 18%

LOGAN $359,000 0.4% 5% $238,000 3.9% -15% $179,870 -0.8% -18%

MORETON BAY $406,000 1.2% 3% $330,000 3.9% -6% $240,000 1.9% -8%

REDLAND $485,000 1.0% 2% $390,000 6.1% ~ t -1% $28,000 -88.8% * b 16%

TOURISM CENTRES

GOLD COAST $545,000 3.8% 6% $345,000 -1.4% 27% $240,000 0.0% 9%

SUNSHINE COAST SD $496,500 0.3% 5% $366,500 -0.9% 2% $257,000 3.8% 4%

SUNSHINE COAST $492,500 0.5% 6% $358,000 -0.6% -3% $257,000 4.7% ~ -1%

NOOSA $520,000 -3.7% ~ -5% $434,000 3.2% 23% $310,000 N/A * f 67%"

FRASER COAST $300,000 0.2% 0% $216,250 -15.9% ~ f -13% $151,000 -8.5% ~ 36%"

CAIRNS $400,000 2.6% 12% $225,000 2.5% 10% $192,500 -3.5% ~ -22%

REGIONAL CENTRES

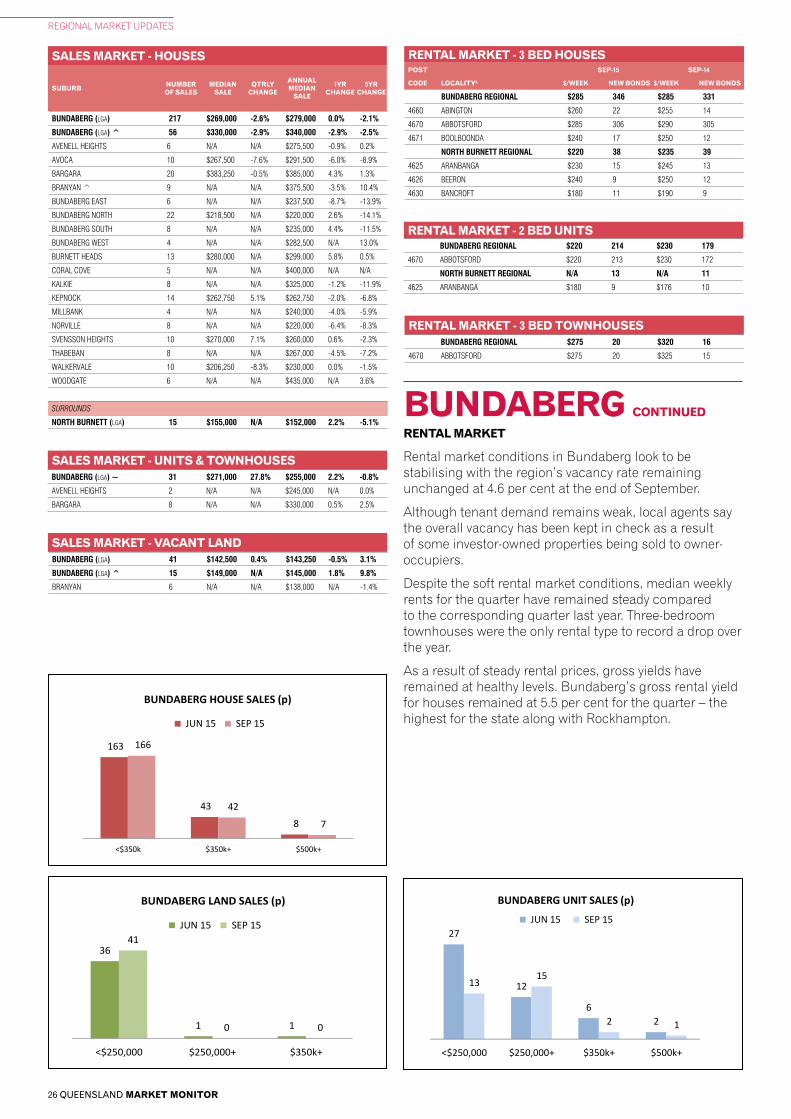

BUNDABERG $269,000 -2.6% 0% $271,000 27.8% ~ -35%" $142,500 0.4% 8%

GLADSTONE $342,000 -9.4% ~ -5% N/A N/A -52%" N/A N/A -44%"

MACKAY $345,000 -2.8% 9% $227,500 -18.8% ~ -29%" $156,000 -25.0% ~ 9%

ROCKHAMPTON $275,000 -7.4% ~ -5% $347,500 N/A 14%" $154,500 -2.8% 21%"

TOOWOOMBA $353,000 0.6% 13% $310,000 10.7% * t 23% $170,800 -7.2% ~ * 23%

TOWNSVILLE $342,000 0.3% -1% $250,000 -19.5% ~ -3% $150,000 -8.5% 57%

ON THE MARKET" HOUSES (ALL) UNITS (ALL)

LGASTOCK

ON MARKET

DAYS ON MARKET

VENDOR DISCOUNT

STOCK ON

MARKET

DAYS ON MARKET

VENDOR DISCOUNT

GREATER BRISBANE

BRISBANE SD 7.2% 68 -5.6% 7.6% 78 -5.3%

BRISBANE 6.6% 59 -5.6% 6.9% 69 -4.8%

IPSWICH 7.9% 84 -6.6% 9.7% 117 -7.4%LOGAN 7.7% 75 -5.4% 10.7% 93 -6.3%MORETON BAY 7.6% 73 -5.3% 9.3% 104 -6.1%REDLAND 8.5% 75 -5.7% 9.8% 91 -5.2%TOURISM CENTRESGOLD COAST 8.3% 72 -5.6% 9.7% 93 -6.1%SUNSHINE COAST SD 9.4% 88 -5.8% 10.1% 106 -6.3%SUNSHINE COAST 9.2% 85 -5.6% 10.1% 103 -6.2%NOOSA 10.5% 104 -6.5% 10.4% 116 -6.9%FRASER COAST 10.1% 110 -7.7% 13.5% 111 -6.3%CAIRNS 7.7% 67 -6.4% 9.1% 87 -7.1%REGIONAL QLDBUNDABERG 8.8% 107 -8.1% 10.8% 140 -8.2%GLADSTONE 7.3% 100 -9.4% 6.7% 121 -11.8%MACKAY 6.9% 110 -11.4% 7.5% 133 -12.9%ROCKHAMPTON 7.8% 103 -9.1% 7.6% 118 -7.4%TOOWOOMBA 8.4% 67 -5.3% 7.8% 77 -4.2%TOWNSVILLE 7.2% 94 -8.9% 9.8% 119 -9.1%

"All figures are for the 12months ending August 2015

SD - Statistical Division: Brisbane SD (Brisbane, Ipswich, Logan, Moreton Bay & Redland); Sunshine Coast SD (Sunshine Coast & Noosa)

"Due to low volume of sales, % changes should be used with caution.N/A - not available due to insufficient sales numbersb The median sale price for vacant land in the Redland City LGA is significantly impacted by shifts in the number of property sales on the bay islands versus the number on the mainland in high quality subdivisions.

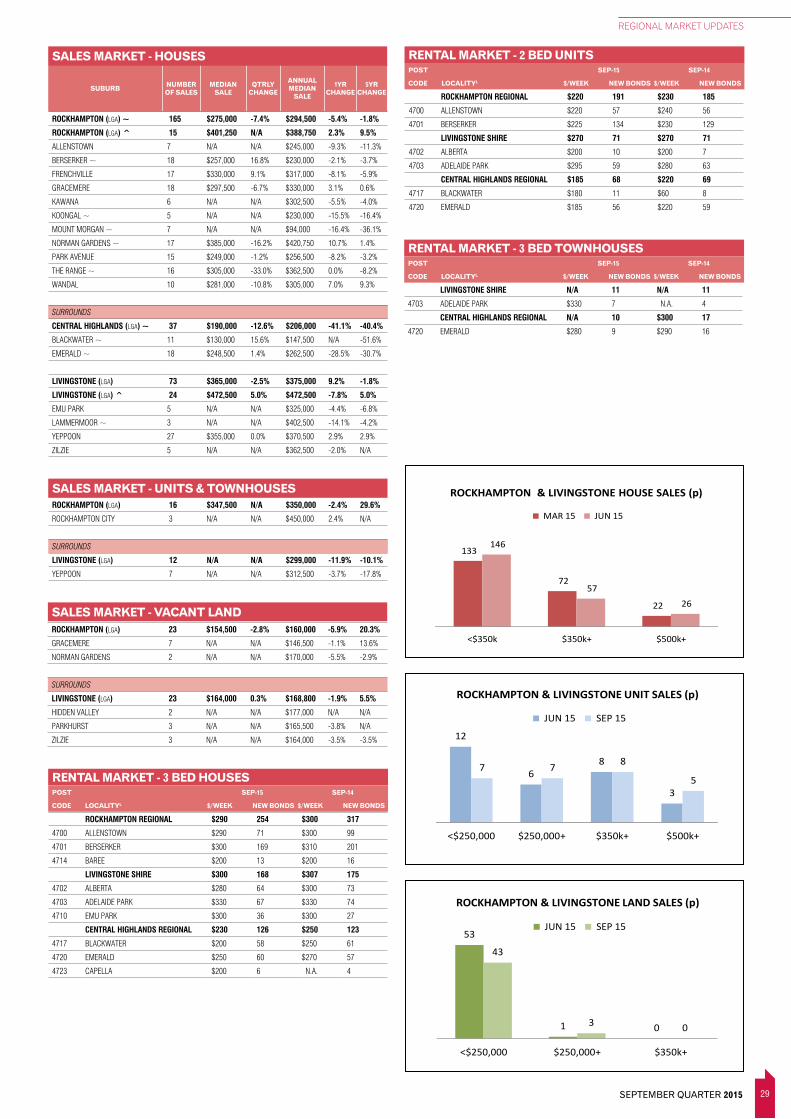

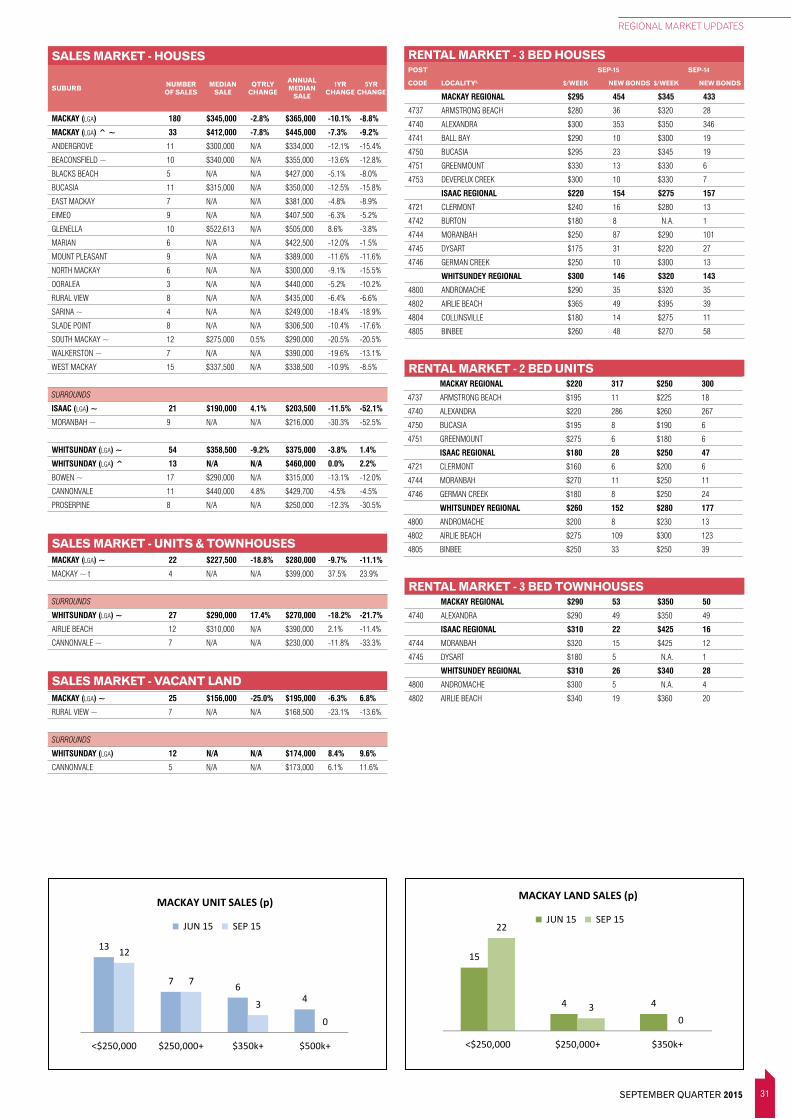

Mackay’s house market was patchy, with some market indicators in decline despite sales numbers increasing nine per cent over the quarter. The region’s median house price softened 2.8 per cent to $345,000 over the September quarter.

UNIT MARKET

Broadly speaking, the unit and townhouse markets across the state followed the sales trends set by the housing markets.

Greater Brisbane and the tourism centres were the standout performers with the Gold Coast recording the highest lift in preliminary sales activity.

Median sale prices in Greater Brisbane were up across all council areas, while the tourism centres recorded relatively steady results on the back of strong sales at the affordable end of the market.

Data reveals that investor interest is picking up with Gold Coast agents saying interstate investors are beginning to turn their attention to the sunshine state.

Toowoomba’s unit and townhouse market rebounded over the quarter, with sales up 23 per cent. News of major infrastructure projects proceeding is keeping the momentum in the market.

In other regional centres, sales turnover in the unit market eased. Investor interest outside the southeast corner is extremely limited and there is little or no new development activity on the cards, softening local economies.

5

STATE-WIDE SUMMARY

SEPTEMBER QUARTER 2015

FOR FULL ON THE MARKET AND RENTAL MARKET STATISTICS BY LOCAL GOVERNMENT AREA, SEE PAGE 37-39

VACANCY RATES

LGA/REGION SEP-15 TRENDGREATER BRISBANEBRISBANE SD 2.3% STEADYBRISBANE 2.8% STEADYIPSWICH 1.3% DOWNLOGAN 1.9% DOWNMORETON BAY 1.6% STEADYREDLAND 2.5% STEADYTOURISM CENTRESGOLD COAST 1.7% DOWNSUNSHINE COAST SD 1.3% DOWNSUNSHINE COAST 1.4% STEADYNOOSA 0.9% DOWNFRASER COAST 3.3% DOWNCAIRNS 2.6% STEADYREGIONAL QLDBUNDABERG 4.6% STEADYGLADSTONE 7.1% UPMACKAY 9.1% STEADYROCKHAMPTON 4.5% DOWNTOOWOOMBA 2.7% DOWNTOWNSVILLE 5.6% STEADY

See page 39 for full vacancy rate data

* change greater than $20 (rents) or 0.5 pts (yields)

RENTAL TRENDS^ MEDIAN WEEKLY RENT GROSS RENTAL YIELDS

LGA 3-BED HOUSE 2-BED FLAT 3-BED TOWNHOUSE HOUSES UNITS

GREATER BRISBANEBRISBANE $420 STEADY $400 STEADY $415 STEADY 3.6% STEADY 4.8% STEADYIPSWICH $300 STEADY $255 STEADY $315 STEADY 4.9% STEADY 5.1% DOWNLOGAN $350 STEADY $270 UP $340 STEADY 5.1% STEADY 5.9% STEADYMORETON BAY $350 STEADY $280 STEADY $340 STEADY 4.5% STEADY 4.4% STEADYREDLAND $390 STEADY $330 UP $395 STEADY 4.2% STEADY 4.4% STEADYTOURISM CENTRESGOLD COAST $450 STEADY $380 STEADY $400 STEADY 4.3% STEADY 5.7% STEADYSUNSHINE COAST $420 STEADY $340 STEADY $410 UP 4.4% STEADY 4.9% STEADYNOOSA $430 DOWN $360 STEADY $480 STEADY 4.3% STEADY 4.3% STEADYFRASER COAST $360 STEADY $285 STEADY $375 UP* 5.0% UP* 5.9% UPCAIRNS $290 STEADY $245 UP $310 DOWN 4.7% DOWN* 6.6% UP*REGIONAL QLDBUNDABERG $285 STEADY $220 STEADY $275 DOWN 5.5% STEADY 4.2% DOWN*GLADSTONE $290 DOWN $220 DOWN* $300 DOWN* 4.4% UP N/A N/AMACKAY $295 STEADY $220 STEADY $290 DOWN 4.4% STEADY 5.0% UP*ROCKHAMPTON $290 STEADY $220 DOWN N.A. UP* 5.5% UP 3.3% N/ATOOWOOMBA $300 STEADY $250 STEADY $300 DOWN* 4.4% STEADY 4.2% DOWNTOWNSVILLE $305 STEADY $255 STEADY $330 STEADY 4.6% STEADY 5.3% UP*

RENTAL MARKET

Vacancy levels in the southeast corner are healthy to tight, with many suburbs either tightening slightly over the quarter or remaining in the healthy range.

However, as the sales market improves local agents anticipate that the rental market will ease over the coming quarters. Ongoing low interest rates mean that for many renters - especially those in the inner city - the cost of living is actually cheaper with a mortgage than in a rental property. This will impact on rental vacancy rates as renters move into home ownership.

In regional areas vacancy rates remained relatively unchanged with weak rental market conditions prevailing.

Gladstone’s vacancy rate was the exception as it returned to above seven per cent with more ex-mining company owned properties coming into the private rental pool.

Subscribe to REIQ's research report & media releases: Keep up to date with the latest market information from the best source for real estate news in

Queensland, the REIQ. Email Yvette Burton to subscribe: [email protected].

6 QUEENSLAND MARKET MONITOR

BRISBANE MARKET UPDATES

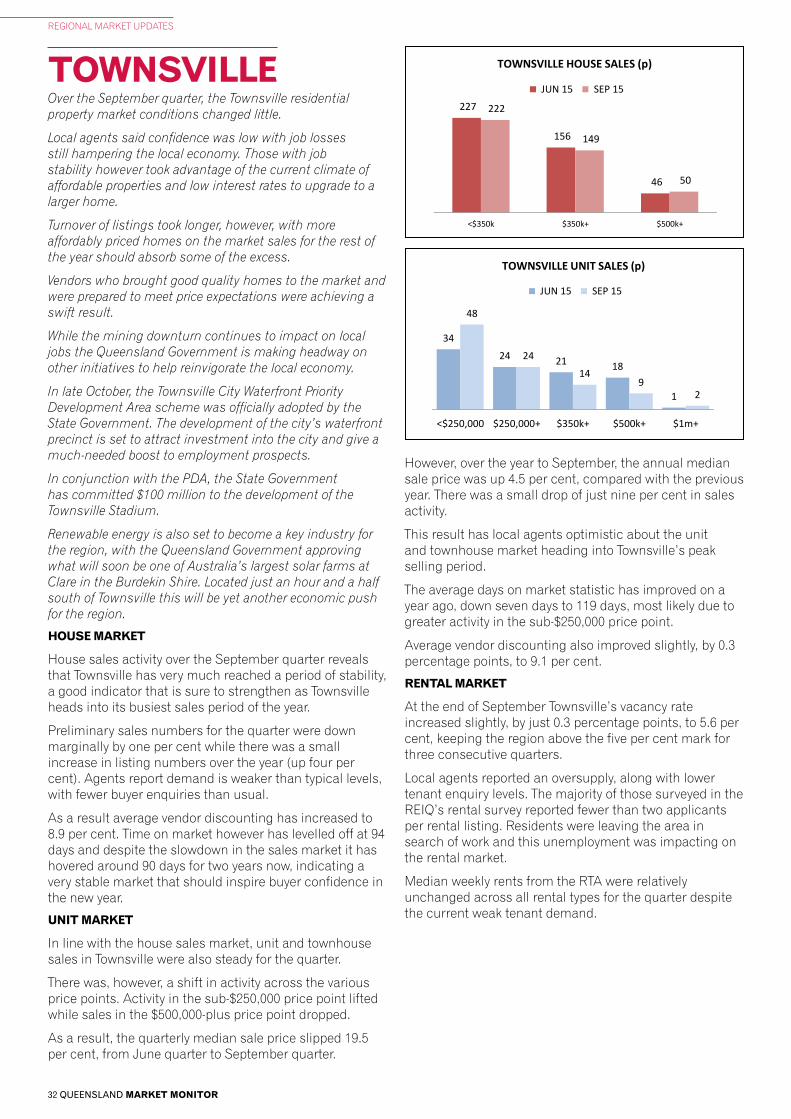

BRISBANE CITYIn line with historical September quarters, Brisbane’s house market recorded a healthy rise in residential sales activity for the 2015 September quarter.

While predictions have been prolific that the slowing conditions in Sydney would flow through to other major capital cities, Brisbane has clearly defied expectations.

On the market indicators of average days on market and average vendor discounting have remained relatively unchanged since the end of June, proving that the Brisbane property market is growing at a healthy and sustainable level.

Listing numbers continue to increase with more vendors recognising the good selling conditions. This trend in listings is encouraging and will ensure there is enough supply to meet the growing demand. With more listings coming onto the market to meet the growth in buyer numbers, conditions are ripe for property prices to grow at a steady rate.

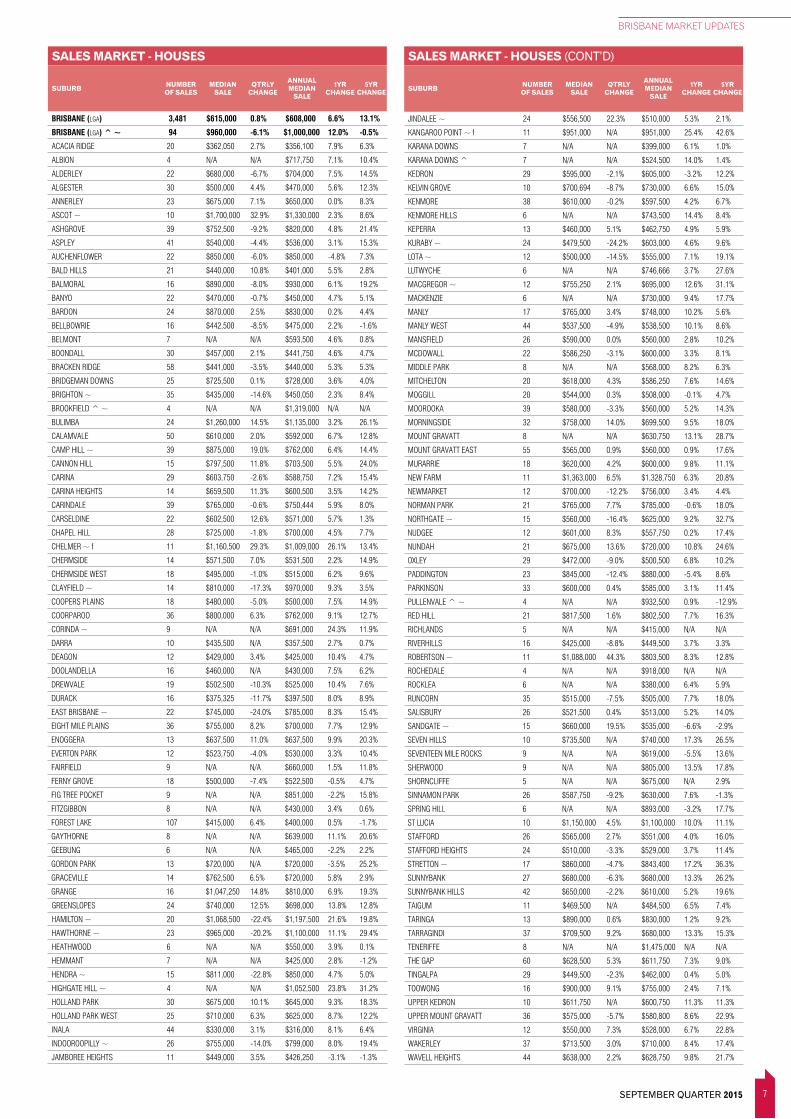

HOUSE MARKET

Over the September quarter, Brisbane preliminary house sales were up five per cent on the June quarter, taking the city’s sales turnover to a level not seen in more than five years.

With growing confidence and activity across all price points, the overall median was up marginally, by 0.8 per cent, to $615,000 – setting yet another record median sale price.

Demand for houses in the $500 000-plus bracket grew significantly, with 129 more sales this quarter compared with the previous quarter.

The growth in listings across all price points is meeting growing buyer demand with average days on market and average vendor discounting rates at levels consistent since the start of the year.

Standout suburbs over the quarter were typically middle to outer-ring suburbs with Eight Mile Plains, Mount Gravatt East and Manly West recording some of the strongest increases in preliminary sales numbers.

The prestige market performed well this quarter. Two new suburbs entered the million-dollar median price group, with Grange and Robertson joining blue-chip suburbs such as Bulimba, Chelmer, Hamilton, New Farm, Teneriffe and St Lucia.

UNIT MARKET

Brisbane’s unit and townhouse market also performed strongly with preliminary unit and townhouse sales up 13 per cent compared with the June quarter.

Increased activity was not confined to any one area with the top increases in activity occurring in inner, middle and outer ring suburbs.

Activity also increased across all price points with the $350,000-plus price point recording the largest increase.

Sales in the prestige unit market lifted, with 14 more sales in the million-dollar-plus category compared with the June quarter.

Brisbane's median unit sale price was up 1.2 per cent to $430,000 this quarter.

The median has hovered around this level since the September quarter last year, indicating that real price growth is yet to occur in this section of Brisbane’s residential market.

With new apartments coming onto the market, listing numbers were up 13 per cent on the previous year. As a result, average days on market increased to 69 days while average vendor discounting remained relatively stable, up just 0.1 percentage points to 4.8 per cent over the year to August.

RENTAL MARKET

Brisbane City vacancy rates increased marginally by 0.1 percentage points to 2.8 per cent, largely due to easing conditions for the city’s inner ring.

Increased supply levels are starting to impact on the inner city, with the vacancy rate easing to 3.3 per cent at the end of September.

Local agents reported that asking rents were easing and rental incentives were being used to help secure tenants. Easing tenant demand was also reported.

However, even though demand is easing, generally speaking median rents have not yet softened, with the exception of the inner-north where rents dropped slightly by $10 over the quarter.

In the middle to outer ring local agents reported that despite low vacancy levels, listings were taking longer to rent. Increased investor activity was also adding to current supply levels.

Listing numbers continue to increase with more vendors recognising the good selling conditions.

7 SEPTEMBER QUARTER 2015

BRISBANE MARKET UPDATES

SALES MARKET - HOUSES

SUBURB NUMBER OF SALES

MEDIAN SALE

QTRLY CHANGE

ANNUAL MEDIAN

SALE

1YR CHANGE

5YR CHANGE

SALES MARKET - HOUSES (CONT’D)

SUBURB NUMBER OF SALES

MEDIAN SALE

QTRLY CHANGE

ANNUAL MEDIAN

SALE

1YR CHANGE

5YR CHANGE

BRISBANE (LGA) 3,481 $615,000 0.8% $608,000 6.6% 13.1%

BRISBANE (LGA) ^ ~ 94 $960,000 -6.1% $1,000,000 12.0% -0.5%

ACACIA RIDGE 20 $362,050 2.7% $356,100 7.9% 6.3%

ALBION 4 N/A N/A $717,750 7.1% 10.4%

ALDERLEY 22 $680,000 -6.7% $704,000 7.5% 14.5%

ALGESTER 30 $500,000 4.4% $470,000 5.6% 12.3%

ANNERLEY 23 $675,000 7.1% $650,000 0.0% 8.3%

ASCOT ~ 10 $1,700,000 32.9% $1,330,000 2.3% 8.6%

ASHGROVE 39 $752,500 -9.2% $820,000 4.8% 21.4%

ASPLEY 41 $540,000 -4.4% $536,000 3.1% 15.3%

AUCHENFLOWER 22 $850,000 -6.0% $850,000 -4.8% 7.3%

BALD HILLS 21 $440,000 10.8% $401,000 5.5% 2.8%

BALMORAL 16 $890,000 -8.0% $930,000 6.1% 19.2%

BANYO 22 $470,000 -0.7% $450,000 4.7% 5.1%

BARDON 24 $870,000 2.5% $830,000 0.2% 4.4%

BELLBOWRIE 16 $442,500 -8.5% $475,000 2.2% -1.6%

BELMONT 7 N/A N/A $593,500 4.6% 0.8%

BOONDALL 30 $457,000 2.1% $441,750 4.6% 4.7%

BRACKEN RIDGE 58 $441,000 -3.5% $440,000 5.3% 5.3%

BRIDGEMAN DOWNS 25 $725,500 0.1% $728,000 3.6% 4.0%

BRIGHTON ~ 35 $435,000 -14.6% $450,050 2.3% 8.4%

BROOKFIELD ^ ~ 4 N/A N/A $1,319,000 N/A N/A

BULIMBA 24 $1,260,000 14.5% $1,135,000 3.2% 26.1%

CALAMVALE 50 $610,000 2.0% $592,000 6.7% 12.8%

CAMP HILL ~ 39 $875,000 19.0% $762,000 6.4% 14.4%

CANNON HILL 15 $797,500 11.8% $703,500 5.5% 24.0%

CARINA 29 $603,750 -2.6% $588,750 7.2% 15.4%

CARINA HEIGHTS 14 $659,500 11.3% $600,500 3.5% 14.2%

CARINDALE 39 $765,000 -0.6% $750,444 5.9% 8.0%

CARSELDINE 22 $602,500 12.6% $571,000 5.7% 1.3%

CHAPEL HILL 28 $725,000 -1.8% $700,000 4.5% 7.7%

CHELMER ~ f 11 $1,160,500 29.3% $1,009,000 26.1% 13.4%

CHERMSIDE 14 $571,500 7.0% $531,500 2.2% 14.9%

CHERMSIDE WEST 18 $495,000 -1.0% $515,000 6.2% 9.6%

CLAYFIELD ~ 14 $810,000 -17.3% $970,000 9.3% 3.5%

COOPERS PLAINS 18 $480,000 -5.0% $500,000 7.5% 14.9%

COORPAROO 36 $800,000 6.3% $762,000 9.1% 12.7%

CORINDA ~ 9 N/A N/A $691,000 24.3% 11.9%

DARRA 10 $435,500 N/A $357,500 2.7% 0.7%

DEAGON 12 $429,000 3.4% $425,000 10.4% 4.7%

DOOLANDELLA 16 $460,000 N/A $430,000 7.5% 6.2%

DREWVALE 19 $502,500 -10.3% $525,000 10.4% 7.6%

DURACK 16 $375,325 -11.7% $397,500 8.0% 8.9%

EAST BRISBANE ~ 22 $745,000 -24.0% $785,000 8.3% 15.4%

EIGHT MILE PLAINS 36 $755,000 8.2% $700,000 7.7% 12.9%

ENOGGERA 13 $637,500 11.0% $637,500 9.9% 20.3%

EVERTON PARK 12 $523,750 -4.0% $530,000 3.3% 10.4%

FAIRFIELD 9 N/A N/A $660,000 1.5% 11.8%

FERNY GROVE 18 $500,000 -7.4% $522,500 -0.5% 4.7%

FIG TREE POCKET 9 N/A N/A $851,000 -2.2% 15.8%

FITZGIBBON 8 N/A N/A $430,000 3.4% 0.6%

FOREST LAKE 107 $415,000 6.4% $400,000 0.5% -1.7%

GAYTHORNE 8 N/A N/A $639,000 11.1% 20.6%

GEEBUNG 6 N/A N/A $465,000 -2.2% 2.2%

GORDON PARK 13 $720,000 N/A $720,000 -3.5% 25.2%

GRACEVILLE 14 $762,500 6.5% $720,000 5.8% 2.9%

GRANGE 16 $1,047,250 14.8% $810,000 6.9% 19.3%

GREENSLOPES 24 $740,000 12.5% $698,000 13.8% 12.8%

HAMILTON ~ 20 $1,068,500 -22.4% $1,197,500 21.6% 19.8%

HAWTHORNE ~ 23 $965,000 -20.2% $1,100,000 11.1% 29.4%

HEATHWOOD 6 N/A N/A $550,000 3.9% 0.1%

HEMMANT 7 N/A N/A $425,000 2.8% -1.2%

HENDRA ~ 15 $811,000 -22.8% $850,000 4.7% 5.0%

HIGHGATE HILL ~ 4 N/A N/A $1,052,500 23.8% 31.2%

HOLLAND PARK 30 $675,000 10.1% $645,000 9.3% 18.3%

HOLLAND PARK WEST 25 $710,000 6.3% $625,000 8.7% 12.2%

INALA 44 $330,000 3.1% $316,000 8.1% 6.4%

INDOOROOPILLY ~ 26 $755,000 -14.0% $799,000 8.0% 19.4%

JAMBOREE HEIGHTS 11 $449,000 3.5% $426,250 -3.1% -1.3%

JINDALEE ~ 24 $556,500 22.3% $510,000 5.3% 2.1%

KANGAROO POINT ~ f 11 $951,000 N/A $951,000 25.4% 42.6%

KARANA DOWNS 7 N/A N/A $399,000 6.1% 1.0%

KARANA DOWNS ^ 7 N/A N/A $524,500 14.0% 1.4%

KEDRON 29 $595,000 -2.1% $605,000 -3.2% 12.2%

KELVIN GROVE 10 $700,694 -8.7% $730,000 6.6% 15.0%

KENMORE 38 $610,000 -0.2% $597,500 4.2% 6.7%

KENMORE HILLS 6 N/A N/A $743,500 14.4% 8.4%

KEPERRA 13 $460,000 5.1% $462,750 4.9% 5.9%

KURABY ~ 24 $479,500 -24.2% $603,000 4.6% 9.6%

LOTA ~ 12 $500,000 -14.5% $555,000 7.1% 19.1%

LUTWYCHE 6 N/A N/A $746,666 3.7% 27.6%

MACGREGOR ~ 12 $755,250 2.1% $695,000 12.6% 31.1%

MACKENZIE 6 N/A N/A $730,000 9.4% 17.7%

MANLY 17 $765,000 3.4% $748,000 10.2% 5.6%

MANLY WEST 44 $537,500 -4.9% $538,500 10.1% 8.6%

MANSFIELD 26 $590,000 0.0% $560,000 2.8% 10.2%

MCDOWALL 22 $586,250 -3.1% $600,000 3.3% 8.1%

MIDDLE PARK 8 N/A N/A $568,000 8.2% 6.3%

MITCHELTON 20 $618,000 4.3% $586,250 7.6% 14.6%

MOGGILL 20 $544,000 0.3% $508,000 -0.1% 4.7%

MOOROOKA 39 $580,000 -3.3% $560,000 5.2% 14.3%

MORNINGSIDE 32 $758,000 14.0% $699,500 9.5% 18.0%

MOUNT GRAVATT 8 N/A N/A $630,750 13.1% 28.7%

MOUNT GRAVATT EAST 55 $565,000 0.9% $560,000 0.9% 17.6%

MURARRIE 18 $620,000 4.2% $600,000 9.8% 11.1%

NEW FARM 11 $1,363,000 6.5% $1,328,750 6.3% 20.8%

NEWMARKET 12 $700,000 -12.2% $756,000 3.4% 4.4%

NORMAN PARK 21 $765,000 7.7% $785,000 -0.6% 18.0%

NORTHGATE ~ 15 $560,000 -16.4% $625,000 9.2% 32.7%

NUDGEE 12 $601,000 8.3% $557,750 0.2% 17.4%

NUNDAH 21 $675,000 13.6% $720,000 10.8% 24.6%

OXLEY 29 $472,000 -9.0% $500,500 6.8% 10.2%

PADDINGTON 23 $845,000 -12.4% $880,000 -5.4% 8.6%

PARKINSON 33 $600,000 0.4% $585,000 3.1% 11.4%

PULLENVALE ^ ~ 4 N/A N/A $932,500 0.9% -12.9%

RED HILL 21 $817,500 1.6% $802,500 7.7% 16.3%

RICHLANDS 5 N/A N/A $415,000 N/A N/A

RIVERHILLS 16 $425,000 -8.8% $449,500 3.7% 3.3%

ROBERTSON ~ 11 $1,088,000 44.3% $803,500 8.3% 12.8%

ROCHEDALE 4 N/A N/A $918,000 N/A N/A

ROCKLEA 6 N/A N/A $380,000 6.4% 5.9%

RUNCORN 35 $515,000 -7.5% $505,000 7.7% 18.0%

SALISBURY 26 $521,500 0.4% $513,000 5.2% 14.0%

SANDGATE ~ 15 $660,000 19.5% $535,000 -6.6% -2.9%

SEVEN HILLS 10 $735,500 N/A $740,000 17.3% 26.5%

SEVENTEEN MILE ROCKS 9 N/A N/A $619,000 -5.5% 13.6%

SHERWOOD 9 N/A N/A $805,000 13.5% 17.8%

SHORNCLIFFE 5 N/A N/A $675,000 N/A 2.9%

SINNAMON PARK 26 $587,750 -9.2% $630,000 7.6% -1.3%

SPRING HILL 6 N/A N/A $893,000 -3.2% 17.7%

ST LUCIA 10 $1,150,000 4.5% $1,100,000 10.0% 11.1%

STAFFORD 26 $565,000 2.7% $551,000 4.0% 16.0%

STAFFORD HEIGHTS 24 $510,000 -3.3% $529,000 3.7% 11.4%

STRETTON ~ 17 $860,000 -4.7% $843,400 17.2% 36.3%

SUNNYBANK 27 $680,000 -6.3% $680,000 13.3% 26.2%

SUNNYBANK HILLS 42 $650,000 -2.2% $610,000 5.2% 19.6%

TAIGUM 11 $469,500 N/A $484,500 6.5% 7.4%

TARINGA 13 $890,000 0.6% $830,000 1.2% 9.2%

TARRAGINDI 37 $709,500 9.2% $680,000 13.3% 15.3%

TENERIFFE 8 N/A N/A $1,475,000 N/A N/A

THE GAP 60 $628,500 5.3% $611,750 7.3% 9.0%

TINGALPA 29 $449,500 -2.3% $462,000 0.4% 5.0%

TOOWONG 16 $900,000 9.1% $755,000 2.4% 7.1%

UPPER KEDRON 10 $611,750 N/A $600,750 11.3% 11.3%

UPPER MOUNT GRAVATT 36 $575,000 -5.7% $580,800 8.6% 22.9%

VIRGINIA 12 $550,000 7.3% $528,000 6.7% 22.8%

WAKERLEY 37 $713,500 3.0% $710,000 8.4% 17.4%

WAVELL HEIGHTS 44 $638,000 2.2% $628,750 9.8% 21.7%

8 QUEENSLAND MARKET MONITOR

BRISBANE MARKET UPDATES

SALES MARKET - UNITS & TOWNHOUSES

SALES MARKET - UNITS & TOWNHOUSES (CONT’D)

SUBURB NUMBER OF SALES

MEDIAN SALE

QTRLY CHANGE

ANNUAL MEDIAN

SALE

1YR CHANGE

5YR CHANGE

SALES MARKET - HOUSES (CONT’D)

SUBURB NUMBER OF SALES

MEDIAN SALE

QTRLY CHANGE

ANNUAL MEDIAN

SALE

1YR CHANGE

5YR CHANGE

BRISBANE (LGA) 2,172 $430,000 1.2% $430,000 2.4% 4.1%

ACACIA RIDGE 16 $348,000 N/A $348,000 0.0% N/A

ALBION ~ * 10 $410,000 -13.7% $419,000 -5.8% -4.6%

ALDERLEY 8 N/A N/A $435,000 -0.6% 10.1%

ANNERLEY ~ 34 $380,000 4.3% $389,000 -9.5% 3.2%

ASCOT ~ 14 $476,000 25.3% $428,000 -0.5% 5.5%

ASHGROVE 9 N/A N/A $440,000 -4.3% 7.3%

ASPLEY 12 $369,000 N/A $366,000 -5.7% -3.4%

AUCHENFLOWER ~ 26 $429,000 -13.3% $439,000 -7.0% 0.9%

BALMORAL 9 N/A N/A $526,000 13.7% 4.8%

BOWEN HILLS ~ * 17 $365,000 -24.0% $419,250 -7.1% -0.2%

BRACKEN RIDGE 4 N/A N/A $322,000 N/A -9.3%

BRIDGEMAN DOWNS 3 N/A N/A $345,000 N/A -6.6%

BRISBANE CITY 119 $481,250 -5.2% $497,500 -0.5% 8.2%

BULIMBA * 32 $625,000 11.1% $589,288 4.1% 14.9%

CALAMVALE 26 $397,888 10.5% $380,000 4.1% 5.8%

CAMP HILL 4 N/A N/A $407,000 N/A -5.3%

CARINA 21 $450,000 4.7% $450,000 4.8% 3.7%

CARINA HEIGHTS 12 $460,000 -6.1% $477,500 4.3% 3.8%

CARINDALE ~ t 7 N/A N/A $520,000 23.8% 2.5%

CARSELDINE 9 N/A N/A $380,000 -3.1% 2.4%

CHERMSIDE 33 $427,500 7.7% $405,000 1.3% -5.6%

CLAYFIELD 52 $367,500 -7.0% $375,100 -3.8% 3.0%

COOPERS PLAINS 2 N/A N/A $377,953 -1.6% N/A

COORPAROO ~ 41 $369,000 -11.1% $400,000 3.4% 4.4%

DARRA 8 N/A N/A $325,500 N/A N/A

DOOLANDELLA 1 N/A N/A $339,000 -2.7% 0.4%

EAST BRISBANE 18 $402,500 -10.6% $420,000 3.1% -5.8%

EIGHT MILE PLAINS 18 $400,000 -1.2% $405,000 5.2% 8.0%

ENOGGERA 5 N/A N/A $410,000 2.5% N/A

EVERTON PARK 19 $350,000 -8.4% $412,000 -0.1% 3.8%

FITZGIBBON 8 N/A N/A $358,000 N/A N/A

FORTITUDE VALLEY 52 $460,000 3.4% $450,500 1.2% 7.3%

GAYTHORNE 10 $424,500 4.4% $432,500 5.5% 1.8%

GORDON PARK 8 N/A N/A $400,250 10.0% 12.7%

GREENSLOPES 24 $381,000 -6.5% $376,500 0.7% -0.3%

HAMILTON ~ 43 $566,250 19.0% $567,500 11.1% 22.7%

HAWTHORNE ~ 14 $526,900 N/A $550,000 8.9% 31.0%

HIGHGATE HILL ~ 15 $520,000 -20.9% $534,000 4.7% 17.1%

WEST END 20 $977,500 -9.7% $990,000 1.0% 26.1%

WESTLAKE 11 $616,000 6.2% $610,000 -3.9% -1.2%

WILSTON 12 $877,500 7.6% $871,000 5.6% 2.3%

WINDSOR 21 $850,000 14.5% $767,500 12.0% 14.6%

WISHART 18 $659,250 -3.8% $630,000 12.1% 12.6%

WOOLLOONGABBA 7 N/A N/A $747,000 12.3% 10.2%

WOOLOOWIN 28 $835,000 10.5% $803,000 3.5% 16.4%

WYNNUM 50 $605,000 0.7% $616,000 16.8% 15.0%

WYNNUM WEST 50 $487,500 5.4% $465,000 -1.1% 4.5%

YERONGA ~ 15 $755,000 -15.2% $757,500 12.1% 12.2%

ZILLMERE 28 $443,250 0.2% $439,000 8.4% 10.0%

HOLLAND PARK WEST * 10 $413,201 -3.7% $431,250 14.2% 20.0%

INDOOROOPILLY 36 $464,750 -0.1% $462,500 -1.6% 0.0%

KANGAROO POINT 40 $526,250 3.2% $502,500 2.6% -3.4%

KEDRON ~ 12 $458,750 5.5% $432,500 21.8% 26.7%

KELVIN GROVE 24 $492,000 2.4% $452,450 -4.3% 8.5%

LUTWYCHE 14 $442,750 -3.8% $459,158 12.0% 17.7%

MANLY 8 N/A N/A $420,000 N/A N/A

MANLY WEST 8 N/A N/A $368,000 3.7% -3.8%

MCDOWALL 3 N/A N/A $468,750 15.7% N/A

MILTON * 3 N/A N/A $544,350 22.9% N/A

MITCHELTON 6 N/A N/A $420,000 N/A 6.5%

MOOROOKA 23 $400,000 -7.4% $407,500 10.1% -3.0%

MORNINGSIDE * 47 $485,000 -3.0% $480,000 1.9% 9.1%

MOUNT GRAVATT 2 N/A N/A $453,000 N/A N/A

MOUNT GRAVATT EAST * t 29 $430,000 -6.3% $447,000 13.2% 17.6%

MURARRIE 1 N/A N/A $440,000 -3.2% -4.3%

NEW FARM 46 $552,500 -7.9% $570,000 1.8% 7.5%

NEWMARKET 5 N/A N/A $430,000 -5.2% -8.5%

NEWSTEAD ~ 17 $723,500 -6.6% $715,000 -6.8% 4.9%

NORMAN PARK 13 $430,000 N/A $487,000 -4.0% 1.5%

NORTHGATE 11 $365,000 N/A $399,900 6.6% 14.3%

NUDGEE - N/A N/A $448,000 N/A N/A

NUNDAH ~ 67 $445,000 15.6% $413,500 -3.6% 3.9%

OXLEY 9 N/A N/A $363,000 N/A 0.8%

PADDINGTON 7 N/A N/A $515,000 6.1% 15.6%

RED HILL 14 $420,000 1.2% $445,000 9.3% N/A

RICHLANDS 8 N/A N/A $346,900 2.8% 2.6%

RUNCORN 21 $340,000 1.0% $332,000 -1.5% -2.1%

SHERWOOD * 21 $440,000 18.6% $445,000 0.0% 7.2%

SOUTH BRISBANE ~ 29 $494,500 1.0% $472,750 -8.2% -0.1%

SPRING HILL 38 $436,500 3.9% $435,400 12.4% 14.6%

ST LUCIA 35 $455,000 -10.3% $496,500 5.6% 12.3%

STAFFORD * 21 $407,500 -7.9% $440,500 11.5% 14.4%

SUNNYBANK HILLS 18 $360,000 N/A $350,000 1.4% -4.4%

TAIGUM ~ 17 $323,250 2.6% $346,000 -10.1% -3.9%

TARINGA 27 $395,000 -9.7% $435,000 4.3% 2.4%

TENERIFFE ~ 37 $590,000 18.5% $559,000 -9.8% 1.6%

THE GAP ~ t 13 $565,000 22.2% $465,000 3.4% 12.0%

TINGALPA 8 N/A N/A $365,000 10.8% 2.4%

TOOWONG ~ 44 $419,000 -8.3% $423,750 -7.4% -3.7%

UPPER MOUNT GRAVATT ~ t 21 $325,000 -14.9% $384,750 -14.7% -7.3%

WAKERLEY 4 N/A N/A $400,000 -3.1% -5.7%

WEST END ~ * 27 $565,000 -16.4% $585,000 13.8% 4.9%

WINDSOR ~ 10 $475,000 15.9% $460,000 16.5% 24.3%

WISHART 8 N/A N/A $385,000 2.4% 6.4%

WOOLLOONGABBA 16 $439,000 4.5% $418,000 4.8% -1.6%

WYNNUM * 20 $390,000 -4.8% $435,000 17.6% 13.0%

WYNNUM WEST ~ t 13 $360,000 15.8% $345,000 -3.9% 2.1%

YERONGA 11 $493,000 8.4% $466,250 7.1% 12.3%

ZILLMERE ~ 10 $312,250 -12.9% $353,750 4.0% -3.1%

Direct Connect makes moving easy for your customers by arranging their utility connections and other moving solutions. We invite you to experience the difference with us today.

CALL US ON 1300 664 715or visit agents.directconnect.com.au

9 SEPTEMBER QUARTER 2015

BRISBANE MARKET UPDATES

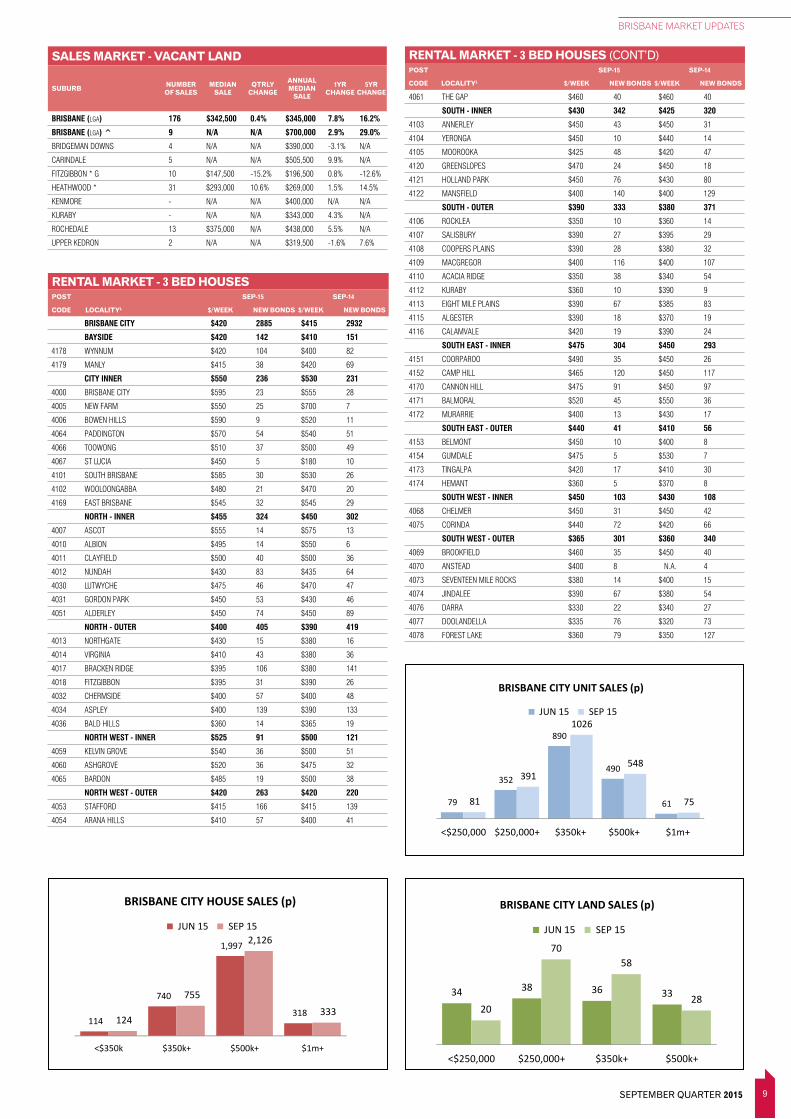

RENTAL MARKET - 3 BED HOUSES (CONT’D)POST SEP-15 SEP-14

CODE LOCALITYL $/WEEK NEW BONDS $/WEEK NEW BONDS

RENTAL MARKET - 3 BED HOUSESPOST SEP-15 SEP-14

CODE LOCALITYL $/WEEK NEW BONDS $/WEEK NEW BONDS

SALES MARKET - VACANT LAND

SUBURB NUMBER OF SALES

MEDIAN SALE

QTRLY CHANGE

ANNUAL MEDIAN

SALE

1YR CHANGE

5YR CHANGE

BRISBANE (LGA) 176 $342,500 0.4% $345,000 7.8% 16.2%

BRISBANE (LGA) ^ 9 N/A N/A $700,000 2.9% 29.0%

BRIDGEMAN DOWNS 4 N/A N/A $390,000 -3.1% N/A

CARINDALE 5 N/A N/A $505,500 9.9% N/A

FITZGIBBON * G 10 $147,500 -15.2% $196,500 0.8% -12.6%

HEATHWOOD * 31 $293,000 10.6% $269,000 1.5% 14.5%

KENMORE - N/A N/A $400,000 N/A N/A

KURABY - N/A N/A $343,000 4.3% N/A

ROCHEDALE 13 $375,000 N/A $438,000 5.5% N/A

UPPER KEDRON 2 N/A N/A $319,500 -1.6% 7.6%

BRISBANE CITY $420 2885 $415 2932

BAYSIDE $420 142 $410 151

4178 WYNNUM $420 104 $400 82

4179 MANLY $415 38 $420 69

CITY INNER $550 236 $530 231

4000 BRISBANE CITY $595 23 $555 28

4005 NEW FARM $550 25 $700 7

4006 BOWEN HILLS $590 9 $520 11

4064 PADDINGTON $570 54 $540 51

4066 TOOWONG $510 37 $500 49

4067 ST LUCIA $450 5 $180 10

4101 SOUTH BRISBANE $585 30 $530 26

4102 WOOLOONGABBA $480 21 $470 20

4169 EAST BRISBANE $545 32 $545 29

NORTH - INNER $455 324 $450 302

4007 ASCOT $555 14 $575 13

4010 ALBION $495 14 $550 6

4011 CLAYFIELD $500 40 $500 36

4012 NUNDAH $430 83 $435 64

4030 LUTWYCHE $475 46 $470 47

4031 GORDON PARK $450 53 $430 46

4051 ALDERLEY $450 74 $450 89

NORTH - OUTER $400 405 $390 419

4013 NORTHGATE $430 15 $380 16

4014 VIRGINIA $410 43 $380 36

4017 BRACKEN RIDGE $395 106 $380 141

4018 FITZGIBBON $395 31 $390 26

4032 CHERMSIDE $400 57 $400 48

4034 ASPLEY $400 139 $390 133

4036 BALD HILLS $360 14 $365 19

NORTH WEST - INNER $525 91 $500 121

4059 KELVIN GROVE $540 36 $500 51

4060 ASHGROVE $520 36 $475 32

4065 BARDON $485 19 $500 38

NORTH WEST - OUTER $420 263 $420 220

4053 STAFFORD $415 166 $415 139

4054 ARANA HILLS $410 57 $400 41

4061 THE GAP $460 40 $460 40

SOUTH - INNER $430 342 $425 320

4103 ANNERLEY $450 43 $450 31

4104 YERONGA $450 10 $440 14

4105 MOOROOKA $425 48 $420 47

4120 GREENSLOPES $470 24 $450 18

4121 HOLLAND PARK $450 76 $430 80

4122 MANSFIELD $400 140 $400 129

SOUTH - OUTER $390 333 $380 371

4106 ROCKLEA $350 10 $360 14

4107 SALISBURY $390 27 $395 29

4108 COOPERS PLAINS $390 28 $380 32

4109 MACGREGOR $400 116 $400 107

4110 ACACIA RIDGE $350 38 $340 54

4112 KURABY $360 10 $390 9

4113 EIGHT MILE PLAINS $390 67 $385 83

4115 ALGESTER $390 18 $370 19

4116 CALAMVALE $420 19 $390 24

SOUTH EAST - INNER $475 304 $450 293

4151 COORPAROO $490 35 $450 26

4152 CAMP HILL $465 120 $450 117

4170 CANNON HILL $475 91 $450 97

4171 BALMORAL $520 45 $550 36

4172 MURARRIE $400 13 $430 17

SOUTH EAST - OUTER $440 41 $410 56

4153 BELMONT $450 10 $400 8

4154 GUMDALE $475 5 $530 7

4173 TINGALPA $420 17 $410 30

4174 HEMANT $360 5 $370 8

SOUTH WEST - INNER $450 103 $430 108

4068 CHELMER $450 31 $450 42

4075 CORINDA $440 72 $420 66

SOUTH WEST - OUTER $365 301 $360 340

4069 BROOKFIELD $460 35 $450 40

4070 ANSTEAD $400 8 N.A. 4

4073 SEVENTEEN MILE ROCKS $380 14 $400 15

4074 JINDALEE $390 67 $380 54

4076 DARRA $330 22 $340 27

4077 DOOLANDELLA $335 76 $320 73

4078 FOREST LAKE $360 79 $350 127

LAND PRICEPOINTS

(p) Preliminary. See explanatory notes for further information. Source: REIQ, data provided by CoreLogic RP Data.

34 38 36 33

20

7058

28

<$250,000 $250,000+ $350k+ $500k+

BRISBANE CITY LAND SALES (p)

JUN 15 SEP 15

449

10044

8

464

10029 3

<$250,000 $250,000+ $350k+ $500k+

BRISBANE SURROUNDS LAND SALES (p)

JUN 15 SEP 15Includes IPSWICH, LOGAN, MORETON BAY & REDLAND

98

38

617

111

36

13 14

<$250,000 $250,000+ $350k+ $500k+

GOLD COAST LAND SALES (p)

JUN 15 SEP 15

70

36

21

7

6155

149

<$250,000 $250,000+ $350k+ $500k+

SUNSHINE COAST & NOOSA LAND SALES (p)

JUN 15 SEP 1581

124

56

115

<$250,000 $250,000+ $350k+

CAIRNS & DOUGLAS LAND SALES (p)

JUN 15 SEP 15

53

5 1

78

1 1

<$250,000 $250,000+ $350k+

FRASER COAST LAND SALES (p)

JUN 15 SEP 15

22

2 1

10

31

<$250,000 $250,000+ $350k+

GLADSTONE LAND SALES (p)

JUN 15 SEP 15

53

1 0

43

3 0

<$250,000 $250,000+ $350k+

ROCKHAMPTON & LIVINGSTONE LAND SALES (p)

JUN 15 SEP 15

46

2 0

54

4 1

<$250,000 $250,000+ $350k+

TOOWOOMBA LAND SALES (p)

JUN 15 SEP 15

46

2 3

72

71

<$250,000 $250,000+ $350k+

TOWNSVILLE LAND SALES (p)

JUN 15 SEP 15

15

4 4

22

30

<$250,000 $250,000+ $350k+

MACKAY LAND SALES (p)

JUN 15 SEP 15

36

1 1

41

0 0

<$250,000 $250,000+ $350k+

BUNDABERG LAND SALES (p)

JUN 15 SEP 15

UNIT PRICEPOINTS

79

352

890

490

6181

391

1026

548

75

<$250,000 $250,000+ $350k+ $500k+ $1m+

BRISBANE CITY UNIT SALES (p)

JUN 15 SEP 15

269 286

173

70

7

235 246203

65 4

<$250,000 $250,000+ $350k+ $500k+ $1m+

BRISBANE SURROUNDS UNIT SALES (p)

JUN 15 SEP 15

INCLUDES IPSWICH, LOGAN, MORETON BAY & REDLAND

195

542471

234

33

265

678

555

337

55

<$250,000 $250,000+ $350k+ $500k+ $1m+

GOLD COAST UNIT SALES (p)

JUN 15 SEP 15

74

209 221

127

28

76

220 217

137

22

<$250,000 $250,000+ $350k+ $500k+ $1m+

SUNSHINE COAST & NOOSA UNIT SALES (p)

JUN 15 SEP 15

27

12

62

1315

2 1

<$250,000 $250,000+ $350k+ $500k+

BUNDABERG UNIT SALES (p)

JUN 15 SEP 15

206

5930 27

3

219

6343 34

6

<$250,000 $250,000+ $350k+ $500k+ $1m+

CAIRNS & DOUGLAS UNIT SALES (p)

JUN 15 SEP 15

3228

93

43

15

3 3

<$250,000 $250,000+ $350k+ $500k+

FRASER COAST UNIT SALES (p)

JUN 15 SEP 15

89

3

1

34

3

0

<$250,000 $250,000+ $350k+ $500k+

GLADSTONE UNIT SALES (p)

JUN 15 SEP 15

34

24 21 18

1

48

24

149

2

<$250,000 $250,000+ $350k+ $500k+ $1m+

TOWNSVILLE UNIT SALES (p)

JUN 15 SEP 15

13

7 64

12

7

3

0

<$250,000 $250,000+ $350k+ $500k+

MACKAY UNIT SALES (p)

JUN 15 SEP 15

12

68

3

7 78

5

<$250,000 $250,000+ $350k+ $500k+

ROCKHAMPTON & LIVINGSTONE UNIT SALES (p)

JUN 15 SEP 15

31

44

144

31

60

187

<$250,000 $250,000+ $350k+ $500k+

TOOWOOMBA UNIT SALES (p)

JUN 15 SEP 15

HOUSE PRICEPOINTS

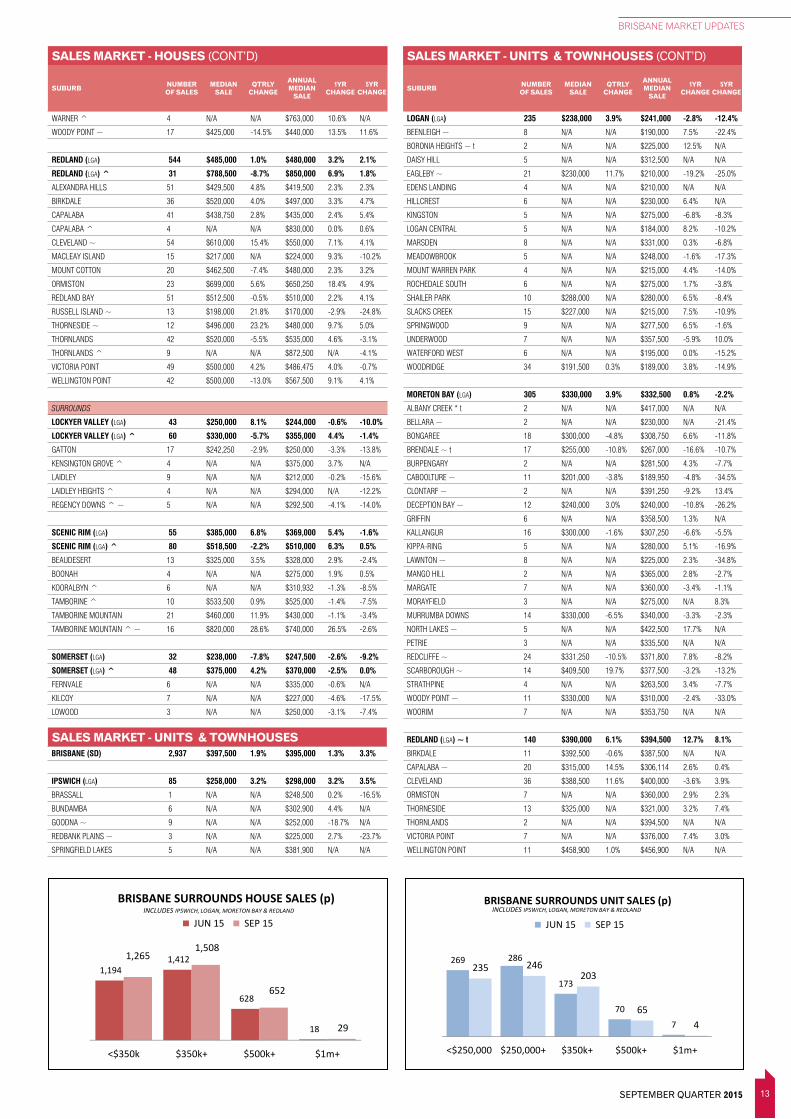

1,194 1,412

628

18

1,265 1,508

652

29

<$350k $350k+ $500k+ $1m+

BRISBANE SURROUNDS HOUSE SALES (p)

JUN 15 SEP 15INCLUDES IPSWICH, LOGAN, MORETON BAY & REDLAND

55

557 698

119 44

567

776

139

<$350k $350k+ $500k+ $1m+

GOLD COAST HOUSE SALES (p)

JUN 15 SEP 15

163

43

8

166

42

7

<$350k $350k+ $500k+

BUNDABERG HOUSE SALES (p)

JUN 15 SEP 15

153

213

90

3

160

247

114

4

<$350k $350k+ $500k+ $1m+

CAIRNS & DOUGLAS HOUSE SALES (p)

JUN 15 SEP 15

211

71

14

203

78

13

<$350k $350k+ $500k+

FRASER COAST HOUSE SALES (p)

JUN 15 SEP 15

48 52

14

57

45

8

<$350k $350k+ $500k+

GLADSTONE HOUSE SALES (p)

JUN 15 SEP 15

227

156

46

222

149

50

<$350k $350k+ $500k+

TOWNSVILLE HOUSE SALES (p)

JUN 15 SEP 15

75 63

21

89

69

16

<$350k $350k+ $500k+

MACKAY HOUSE SALES (p)

JUN 15 SEP 15

133

72

22

146

57

26

<$350k $350k+ $500k+

ROCKHAMPTON & LIVINGSTONE HOUSE SALES (p)

MAR 15 JUN 15

114

740

1,997

318 124

755

2,126

333

<$350k $350k+ $500k+ $1m+

BRISBANE CITY HOUSE SALES (p)

JUN 15 SEP 15215

163

56

233 200

59

<$350k $350k+ $500k+

TOOWOOMBA HOUSE SALES (p)

JUN 15 SEP 15

70

431 427

58 92

437 477

42

<$350k $350k+ $500k+ $1m+

SUNSHINE COAST & NOOSA HOUSE SALES (p)

JUN 15 SEP 15

10 QUEENSLAND MARKET MONITOR

BRISBANE MARKET UPDATES

RENTAL MARKET - 2 BED UNITSPOST SEP-15 SEP-14

CODE LOCALITYL $/WEEK NEW BONDS $/WEEK NEW BONDS

RENTAL MARKET - 3 BED TOWNHOUSESPOST SEP-15 SEP-14

CODE LOCALITYL $/WEEK NEW BONDS $/WEEK NEW BONDS

DID YOU KNOW?YOU CAN GET MEDIAN WEEKLY RENTS FOR OTHER PROPERTY TYPES ONLINE ATWWW.RTA.QLD.GOV.AU

BRISBANE CITY $415 1715 $405 1653

BAYSIDE $400 144 $400 91

4178 WYNNUM $410 103 $400 53

4179 MANLY $395 41 $390 38

CITY INNER $610 65 $600 66

4000 BRISBANE CITY $600 7 N.A. 2

4005 NEW FARM $690 9 N.A. 2

4006 BOWEN HILLS $490 11 $625 13

4064 PADDINGTON $595 7 $600 14

4066 TOOWONG $640 5 $550 11

4067 ST LUCIA $610 10 $575 9

4169 EAST BRISBANE $620 9 $550 8

NORTH - INNER $490 114 $470 96

4007 ASCOT $550 13 $550 9

4011 CLAYFIELD $520 13 $500 12

4012 NUNDAH $470 20 $450 18

4030 LUTWYCHE $490 13 $495 8

4031 GORDON PARK $460 27 $450 19

4051 ALDERLEY $490 24 $450 28

NORTH - OUTER $390 196 $380 236

4013 NORTHGATE $430 11 $410 12

4014 VIRGINIA $450 7 $0 0

4017 BRACKEN RIDGE $370 42 $365 34

4018 FITZGIBBON $370 32 $296 66

4032 CHERMSIDE $425 28 $430 22

4034 ASPLEY $400 67 $395 93

4036 BALD HILLS $365 9 $294 9

NORTH WEST - INNER $510 16 $500 20

4059 KELVIN GROVE $570 7 $500 13

4060 ASHGROVE $450 6 N.A. 4

NORTH WEST - OUTER $420 46 $425 51

4053 STAFFORD $420 37 $425 41

4054 ARANA HILLS $400 7 $400 7

SOUTH - INNER $450 155 $440 155

4103 ANNERLEY $480 29 $490 27

4104 YERONGA $500 11 $480 17

4105 MOOROOKA $420 12 $450 23

4120 GREENSLOPES $465 18 $495 15

4121 HOLLAND PARK $430 9 $460 7

4122 MANSFIELD $430 75 $420 66

SOUTH - OUTER $400 395 $390 396

4107 SALISBURY $505 6 $495 7

4109 MACGREGOR $415 75 $405 63

4110 ACACIA RIDGE $350 8 $340 41

4112 KURABY $385 18 $380 18

4113 EIGHT MILE PLAINS $410 145 $400 149

4115 ALGESTER $375 27 $380 31

4116 CALAMVALE $385 112 $385 85

SOUTH EAST - INNER $480 241 $485 209

4151 COORPAROO $500 21 $495 8

4152 CAMP HILL $450 114 $450 96

4170 CANNON HILL $500 61 $500 69

4171 BALMORAL $595 38 $540 30

4172 MURARRIE $530 7 $475 6

SOUTH EAST - OUTER $415 59 $410 55

4153 BELMONT $430 10 $420 7

4154 GUMDALE $410 33 $410 30

4173 TINGALPA $399 16 $385 17

SOUTH WEST - INNER $400 62 $420 76

4068 CHELMER $510 11 $485 25

4075 CORINDA $400 51 $400 51

SOUTH WEST - OUTER $360 222 $360 202

4073 SEVENTEEN MILE ROCKS $400 14 $400 11

4074 JINDALEE $480 19 $435 19

4076 DARRA $375 15 $375 28

4077 DOOLANDELLA $355 130 $355 103

4078 FOREST LAKE $365 39 $355 38

BRISBANE CITY $400 4716 $400 4474

BAYSIDE $320 51 $340 37

4178 WYNNUM $310 36 $330 26

4179 MANLY $370 15 $430 11

CITY INNER $495 1924 $495 1925

4000 BRISBANE CITY $580 365 $590 358

4005 NEW FARM $500 359 $495 300

4006 BOWEN HILLS $495 254 $495 279

4064 PADDINGTON $410 64 $405 64

4066 TOOWONG $390 183 $415 248

4067 ST LUCIA $430 125 $430 110

4101 SOUTH BRISBANE $500 284 $500 289

4102 WOOLOONGABBA $450 84 $460 101

4169 EAST BRISBANE $490 206 $465 176

NORTH - INNER $360 924 $360 855

4007 ASCOT $420 172 $395 136

4010 ALBION $375 28 $390 29

4011 CLAYFIELD $345 128 $355 131

4012 NUNDAH $390 237 $375 220

4030 LUTWYCHE $340 140 $340 125

4031 GORDON PARK $325 77 $330 74

4051 ALDERLEY $350 142 $340 140

NORTH - OUTER $350 263 $350 241

4013 NORTHGATE $310 25 $300 27

4017 BRACKEN RIDGE $305 25 $300 22

4018 FITZGIBBON $350 13 $330 5

4032 CHERMSIDE $350 103 $375 102

4034 ASPLEY $350 92 $350 77

NORTH WEST - INNER $435 187 $400 156

4059 KELVIN GROVE $485 134 $430 106

4060 ASHGROVE $360 40 $380 40

4065 BARDON $300 13 $300 10

NORTH WEST - OUTER $375 110 $370 95

4053 STAFFORD $375 107 $370 91

SOUTH - INNER $365 403 $365 444

4103 ANNERLEY $350 105 $350 113

4104 YERONGA $370 26 $370 37

4105 MOOROOKA $350 67 $350 69

4120 GREENSLOPES $360 86 $370 104

4121 HOLLAND PARK $350 42 $340 35

4122 MANSFIELD $410 73 $390 84

SOUTH - OUTER $335 60 $320 58

4106 ROCKLEA $300 5 $250 6

4107 SALISBURY $306 7 N.A. 4

4108 COOPERS PLAINS $400 20 $250 6

4109 MACGREGOR $390 14 $390 24

4113 EIGHT MILE PLAINS $375 5 $340 5

4115 ALGESTER $290 8 $300 6

SOUTH EAST - INNER $390 490 $380 387

4151 COORPAROO $360 177 $360 152

4152 CAMP HILL $360 43 $360 30

4170 CANNON HILL $390 105 $395 88

4171 BALMORAL $450 149 $435 114

4172 MURARRIE $410 16 N.A. 3

SOUTH EAST - OUTER N/A 6 N/A 2

SOUTH WEST - INNER $385 270 $370 251

4068 CHELMER $390 214 $375 212

4075 CORINDA $364 56 $335 39

SOUTH WEST - OUTER $320 28 $325 23

4076 DARRA $240 6 $250 6

4077 DOOLANDELLA $290 8 N.A. 1

4078 FOREST LAKE $330 10 $335 10

11 SEPTEMBER QUARTER 2015

BRISBANE MARKET UPDATES

GREATER BRISBANE

FALLING

STABILISINGRECOVERING

RISING

BRISBANE HOUSE MARKETSSeptember Quarter 2015

Source: REIQ

Brisbane↑ Moreton Bay

↑ LoganRedlandIpswich

FALLING

STABILISINGRECOVERING

RISING

QUEENSLAND HOUSE MARKETSSeptember Quarter 2015

Source: REIQ

Brisbane SDCairns

Gold CoastSunsine Coast

Fraser Coast

MackayBundaberg Gladstone

Rockhampton Townsville

↑ Toowoomba

The Brisbane Statistical Division, also known as Greater Brisbane, improved considerably with preliminary sales activity and listings up significantly.

Average days on market and average vendor discounting have continued to improve, despite increased supply coming onto the market which would normally soften those statistics. Data reveals that the outer suburbs are in demand from owner occupiers and investors.

The strengthening local economy and positive population growth are key drivers for continued property demand.

Rental markets throughout Greater Brisbane are tight and demand from tenants is spread throughout the inner, middle and outer suburbs as many move further out seeking more affordable options. Investors are offloading properties and in many cases selling to owner occupiers.

HOUSE MARKET

For the September quarter, the Brisbane Statistical Division (SD) recorded little change in its median house price, up 0.2 per cent. However, sales activity was up five per cent compared with the previous quarter.

Moreton Bay has taken the lead as the strongest performing house market in Greater Brisbane with the shortest days on market and lowest average vendor discounting.

Logan City has recorded the largest increase in preliminary sales activity over the year to September, up 17 per cent.

Logan has also overtaken Redland City in average vendor discounting.

Ipswich may be trailing the other regions in terms of time on market and vendor discounting, but it was the standout performer for sales activity.

According to local agents, this comes as no surprise given the relative affordability of the region and the strong rental yields being achieved.

Owner occupiers are starting to see good value for money in suburbs outside of metropolitan Brisbane. Over the year to September, the suburbs of Yamanto (Ipswich), Deception Bay (Moreton Bay), Rochedale South (Logan) and Mango Hill (Moreton Bay) recorded the highest increase in preliminary sales compared to the previous year including suburbs within metropolitan Brisbane.

Median prices across the Greater Brisbane council areas are likely to continue to attract buyer interest given their relative affordability and accessibility to major business and retail districts.

UNIT MARKET

Over the September quarter, Brisbane Statistical Division median sale price increased 1.9 per cent off the back of a seven per cent increase in preliminary sales numbers.

While median sale price growth was consistent across the council areas, sales activity was mixed.

Ipswich once again recorded the strongest increase in sales activity while buyer activity in Logan, Moreton Bay and Redland City eased or stabilised.

Interest in the Ipswich unit and townhouse market is strong with average days on market and average vendor discounting remaining relatively unchanged, despite an increase of 12 per cent in listings over the year to August.

RENTAL MARKET

Vacancy rates in the outer suburbs of Greater Brisbane were mixed, with Ipswich City tightening to 1.3 per cent, a new lowest record for the region.

Local agents say rental stock is low as a result of continued tenant demand and many tenants are staying put partly because their options are so limited. The sale of investment properties to owner-occupiers is contributing to the short supply rental stock.

Logan City vacancy rate dropped, while Moreton Bay has remained below two per cent despite a slight lift this quarter.

The Pine Rivers region in the Moreton Bay council area remains one of the tightest rental markets with a vacancy rate of 1.3 per cent.

Local agents in the Redland City Council area say new residential developments are adding to supply and are competitively priced, which means established rentals are experiencing tougher conditions. Over the three months to September, the region’s vacancy rate was up 0.2 percentage points to 2.5 per cent.

12 QUEENSLAND MARKET MONITOR

BRISBANE MARKET UPDATES

MUNRUBEN ^ 7 N/A N/A $516,000 0.2% 1.2%

NEW BEITH ^ 10 $562,750 N/A $550,000 -0.9% 4.0%

REGENTS PARK 53 $360,000 -4.5% $355,278 0.4% -2.7%

ROCHEDALE SOUTH 59 $464,000 3.1% $453,000 6.6% 8.1%

SHAILER PARK 42 $527,250 1.4% $510,000 6.6% 8.5%

SLACKS CREEK 29 $320,000 4.6% $315,000 6.8% 5.0%

SPRINGWOOD 23 $435,000 -3.9% $443,500 1.3% 5.5%

TANAH MERAH 19 $410,000 -1.9% $410,000 3.8% 4.6%

UNDERWOOD 24 $500,000 0.9% $500,000 4.5% 11.7%

WATERFORD 15 $358,000 -5.8% $380,000 7.0% -6.2%

WATERFORD WEST 15 $314,000 -6.3% $311,000 -1.0% -2.8%

WINDAROO 16 $397,000 -8.3% $420,000 0.7% -1.2%

WOODRIDGE 27 $298,000 3.7% $280,000 7.7% 3.3%

YARRABILBA 14 $395,000 5.9% $381,950 -3.7% N/A

MORETON BAY (LGA) 1,349 $406,000 1.2% $401,000 2.8% 0.3%

MORETON BAY (LGA) ^ 219 $582,000 0.8% $590,000 5.4% -1.6%

ALBANY CREEK 38 $571,500 -1.1% $540,000 8.0% 2.5%

ARANA HILLS 22 $482,500 2.5% $487,330 6.9% 7.1%

BANKSIA BEACH ~ f 30 $580,000 28.9% $490,000 5.2% 1.0%

BEACHMERE 7 N/A N/A $320,000 0.8% -11.1%

BELLARA 12 $352,500 12.4% $325,000 -0.9% -4.4%

BELLMERE 21 $350,000 7.7% $335,000 3.1% -7.7%

BONGAREE 21 $367,500 -11.4% $389,000 -2.1% -7.4%

BRAY PARK 37 $387,000 -0.8% $385,000 5.5% 4.6%

BUNYA ^ 7 N/A N/A $802,500 10.5% N/A

BURPENGARY 24 $406,000 5.5% $382,000 7.0% 1.9%

BURPENGARY ^ 9 N/A N/A $543,750 2.6% 2.3%

BURPENGARY EAST 4 N/A N/A $410,500 3.4% N/A

BURPENGARY EAST ^ 6 N/A N/A $525,000 -0.9% -6.3%

CABOOLTURE 57 $290,250 3.8% $295,000 2.8% -7.8%

CABOOLTURE ^ 21 $517,500 5.6% $500,000 10.9% 6.4%

CABOOLTURE SOUTH 23 $279,000 5.9% $266,000 -3.3% -9.2%

CASHMERE ~ 13 $684,500 16.8% $653,750 5.9% 21.1%

CLONTARF 40 $415,000 0.0% $395,000 5.3% 9.1%

DAKABIN 7 N/A N/A $450,000 5.9% 4.7%

DECEPTION BAY 80 $330,000 4.6% $320,000 6.7% 0.0%

EATONS HILL 16 $546,000 3.9% $540,000 1.1% 5.2%

ELIMBAH ^ 12 $505,000 -1.9% $510,000 6.3% -1.1%

EVERTON HILLS 10 $527,000 5.0% $512,000 5.6% 10.7%

FERNY HILLS 23 $512,500 2.5% $486,250 4.9% 5.7%

GRIFFIN 29 $455,000 8.1% $438,250 1.3% 5.6%

JOYNER 6 N/A N/A $533,000 N/A 14.6%

KALLANGUR 57 $370,000 4.8% $355,000 4.1% -0.6%

KIPPA-RING 25 $385,000 0.0% $375,000 0.0% 1.4%

LAWNTON 13 $365,000 3.9% $362,500 7.1% 3.9%

MANGO HILL ~ 24 $515,000 17.6% $455,000 4.5% 0.7%

MARGATE 24 $410,000 -8.9% $417,000 11.2% 8.3%

MORAYFIELD 57 $335,000 4.7% $325,000 4.8% -3.0%

MORAYFIELD ^ 12 $558,000 4.3% $550,000 5.8% 0.0%

MURRUMBA DOWNS 24 $463,000 -7.4% $481,500 7.0% 9.4%

NARANGBA 61 $447,500 2.9% $440,000 4.8% 1.4%

NARANGBA ^ 5 N/A N/A $650,000 N/A N/A

NEWPORT 13 $799,000 N/A $799,000 -1.4% -6.0%

NINGI 7 N/A N/A $360,000 2.3% N/A

NINGI ^ 14 $442,250 N/A $508,750 6.0% -1.2%

NORTH LAKES 81 $445,000 -1.1% $449,750 0.1% -1.2%

PETRIE 33 $372,000 -3.1% $392,000 5.9% 1.1%

REDCLIFFE 33 $397,500 -0.4% $390,000 3.4% 2.6%

ROTHWELL 18 $404,250 2.9% $397,000 3.1% 3.7%

SAMFORD VALLEY ^ 16 $880,000 N/A $875,000 1.6% 5.7%

SANDSTONE POINT 14 $379,500 -3.9% $380,000 2.7% -5.0%

SCARBOROUGH ~ f 33 $415,000 -22.3% $465,000 -3.0% -3.1%

STRATHPINE 40 $350,500 -1.3% $355,000 0.0% 1.4%

TOORBUL 6 N/A N/A $275,000 N/A N/A

UPPER CABOOLTURE 7 N/A N/A $335,000 6.3% -3.1%

UPPER CABOOLTURE ^ 6 N/A N/A $530,000 4.4% -3.2%

WAMURAN ^ 12 $522,500 N/A $532,500 9.0% N/A

WARNER 44 $485,000 4.3% $482,500 2.7% 0.7%

SALES MARKET - HOUSES (CONT’D)

SUBURB NUMBER OF SALES

MEDIAN SALE

QTRLY CHANGE

ANNUAL MEDIAN

SALE

1YR CHANGE

5YR CHANGE

SALES MARKET - HOUSES

SUBURB NUMBER OF SALES

MEDIAN SALE

QTRLY CHANGE

ANNUAL MEDIAN

SALE

1YR CHANGE

5YR CHANGE

BRISBANE (SD) 7,002 $480,000 0.2% $480,000 2.1% 5.5%

BRISBANE (SD) ^ 582 $585,000 1.7% $580,000 3.6% -0.6%

IPSWICH (LGA) 718 $320,000 1.6% $320,000 4.6% 0.0%

IPSWICH (LGA) ^ 58 $500,000 2.8% $480,000 5.5% -2.0%

AUGUSTINE HEIGHTS 19 $445,000 -3.1% $499,500 2.7% -11.6%

BELLBIRD PARK 16 $315,000 3.9% $325,000 4.4% 1.9%

BOOVAL 11 $289,500 8.2% $279,500 7.5% -2.6%

BRASSALL 36 $335,000 6.3% $322,000 2.2% -3.9%

BROOKWATER ~ * 13 $730,000 N/A $700,000 -2.8% N/A

BUNDAMBA 24 $271,000 0.7% $280,000 1.8% 2.4%

CAMIRA 20 $355,500 0.1% $349,500 5.2% -0.4%

COALFALLS 10 $290,000 N/A $290,000 N/A N/A

COLLINGWOOD PARK 34 $329,500 6.3% $313,000 2.6% -2.0%

DEEBING HEIGHTS 14 $369,000 N/A $380,000 N/A N/A

EAST IPSWICH ~ 10 $250,000 -29.8% $270,000 12.5% -1.8%

EASTERN HEIGHTS 12 $256,000 -1.5% $265,000 -2.8% -5.9%

FLINDERS VIEW ~ 16 $305,500 -16.8% $337,000 -5.7% -15.2%

GAILES 7 N/A N/A $235,250 N/A N/A

GOODNA 27 $285,000 0.9% $285,000 1.8% -3.4%

IPSWICH ~ 14 $315,000 -4.5% $343,500 30.6% 3.5%

KARALEE ^ 11 $560,000 8.7% $515,000 1.0% -2.4%

LEICHHARDT 8 N/A N/A $222,000 3.3% -11.2%

NEWTOWN 6 N/A N/A $325,000 3.7% -5.8%

NORTH BOOVAL 9 N/A N/A $275,000 19.6% -3.1%

NORTH IPSWICH 17 $265,000 -1.9% $264,000 4.3% -10.1%

ONE MILE 9 N/A N/A $245,000 6.5% -4.3%

RACEVIEW 37 $306,000 1.2% $307,000 1.3% -5.5%

REDBANK 8 N/A N/A $292,500 N/A N/A

REDBANK PLAINS 69 $310,000 1.5% $310,000 5.1% 2.3%

RIVERVIEW 9 N/A N/A $223,750 -4.8% -11.6%

ROSEWOOD 5 N/A N/A $274,750 5.7% 3.3%

SADLIERS CROSSING 9 N/A N/A $321,000 N/A 1.6%

SILKSTONE 13 $287,000 7.1% $262,500 -0.9% -7.0%

SPRINGFIELD 32 $405,000 5.2% $390,000 3.2% 4.3%

SPRINGFIELD LAKES 54 $410,000 -1.3% $414,936 5.0% 2.3%

YAMANTO 32 $420,000 2.4% $415,000 18.6% 18.6%

LOGAN (LGA) 910 $359,000 0.4% $358,000 3.8% -0.6%

LOGAN (LGA) ^ 180 $537,500 1.4% $526,750 3.3% 2.3%

BEENLEIGH 34 $300,000 -4.3% $305,500 5.3% -7.4%

BETHANIA 9 N/A N/A $302,000 7.0% -4.1%

BORONIA HEIGHTS 24 $318,000 3.2% $315,000 0.0% -0.3%

BROWNS PLAINS 21 $320,000 1.6% $315,000 3.4% -3.7%

CEDAR GROVE ^ 7 N/A N/A $419,000 -1.4% -0.2%

CEDAR VALE ^ 9 N/A N/A $460,000 7.0% 5.1%

CHAMBERS FLAT ^ 5 N/A N/A $508,000 N/A N/A

CORNUBIA ^ 6 N/A N/A $745,000 N/A N/A

CORNUBIA ~ 20 $505,000 26.3% $495,000 5.3% 5.4%

CRESTMEAD 51 $302,000 -2.6% $302,000 4.1% -3.2%

DAISY HILL 32 $430,000 2.4% $450,000 4.3% 7.1%

EAGLEBY 43 $281,000 3.3% $271,500 6.5% -6.4%

EDENS LANDING 16 $344,000 10.3% $339,000 -0.3% -6.1%

FORESTDALE ^ 5 N/A N/A $720,000 11.6% 7.1%

GREENBANK ^ 25 $560,000 7.7% $526,500 1.7% 0.3%

HERITAGE PARK 16 $436,000 -2.4% $417,500 2.7% -0.6%

HILLCREST 14 $336,000 0.0% $335,000 4.7% -1.5%

HOLMVIEW 11 $353,500 -1.3% $358,000 N/A N/A

JIMBOOMBA 13 $385,250 -1.2% $377,750 4.6% 0.7%

JIMBOOMBA ^ 22 $472,000 2.6% $465,000 1.1% -5.0%

KINGSTON 39 $300,000 5.8% $285,000 7.5% -0.8%

LOGAN CENTRAL 14 $295,000 0.0% $289,145 9.5% 4.0%

LOGAN RESERVE 14 $360,000 -12.6% $374,806 10.6% N/A

LOGAN VILLAGE ^ 5 N/A N/A $492,000 -0.6% -8.3%

LOGANHOLME 20 $385,000 8.1% $380,000 6.1% 1.3%

LOGANLEA 24 $325,000 -8.1% $331,250 7.4% 1.9%

MARSDEN 43 $326,000 0.3% $334,500 7.2% 3.6%

MEADOWBROOK 8 N/A N/A $389,500 5.3% -2.4%

MOUNT WARREN PARK 28 $329,000 -7.5% $335,500 -1.3% -11.2%

13 SEPTEMBER QUARTER 2015

BRISBANE MARKET UPDATES

WARNER ^ 4 N/A N/A $763,000 10.6% N/A

WOODY POINT ~ 17 $425,000 -14.5% $440,000 13.5% 11.6%

REDLAND (LGA) 544 $485,000 1.0% $480,000 3.2% 2.1%

REDLAND (LGA) ^ 31 $788,500 -8.7% $850,000 6.9% 1.8%

ALEXANDRA HILLS 51 $429,500 4.8% $419,500 2.3% 2.3%

BIRKDALE 36 $520,000 4.0% $497,000 3.3% 4.7%

CAPALABA 41 $438,750 2.8% $435,000 2.4% 5.4%

CAPALABA ^ 4 N/A N/A $830,000 0.0% 0.6%

CLEVELAND ~ 54 $610,000 15.4% $550,000 7.1% 4.1%

MACLEAY ISLAND 15 $217,000 N/A $224,000 9.3% -10.2%

MOUNT COTTON 20 $462,500 -7.4% $480,000 2.3% 3.2%

ORMISTON 23 $699,000 5.6% $650,250 18.4% 4.9%

REDLAND BAY 51 $512,500 -0.5% $510,000 2.2% 4.1%

RUSSELL ISLAND ~ 13 $198,000 21.8% $170,000 -2.9% -24.8%

THORNESIDE ~ 12 $496,000 23.2% $480,000 9.7% 5.0%

THORNLANDS 42 $520,000 -5.5% $535,000 4.6% -3.1%

THORNLANDS ^ 9 N/A N/A $872,500 N/A -4.1%

VICTORIA POINT 49 $500,000 4.2% $486,475 4.0% -0.7%

WELLINGTON POINT 42 $500,000 -13.0% $567,500 9.1% 4.1%

SURROUNDS

LOCKYER VALLEY (LGA) 43 $250,000 8.1% $244,000 -0.6% -10.0%

LOCKYER VALLEY (LGA) ^ 60 $330,000 -5.7% $355,000 4.4% -1.4%

GATTON 17 $242,250 -2.9% $250,000 -3.3% -13.8%

KENSINGTON GROVE ^ 4 N/A N/A $375,000 3.7% N/A

LAIDLEY 9 N/A N/A $212,000 -0.2% -15.6%

LAIDLEY HEIGHTS ^ 4 N/A N/A $294,000 N/A -12.2%

REGENCY DOWNS ^ ~ 5 N/A N/A $292,500 -4.1% -14.0%

SCENIC RIM (LGA) 55 $385,000 6.8% $369,000 5.4% -1.6%

SCENIC RIM (LGA) ^ 80 $518,500 -2.2% $510,000 6.3% 0.5%

BEAUDESERT 13 $325,000 3.5% $328,000 2.9% -2.4%

BOONAH 4 N/A N/A $275,000 1.9% 0.5%

KOORALBYN ^ 6 N/A N/A $310,932 -1.3% -8.5%

TAMBORINE ^ 10 $533,500 0.9% $525,000 -1.4% -7.5%

TAMBORINE MOUNTAIN 21 $460,000 11.9% $430,000 -1.1% -3.4%

TAMBORINE MOUNTAIN ^ ~ 16 $820,000 28.6% $740,000 26.5% -2.6%

SOMERSET (LGA) 32 $238,000 -7.8% $247,500 -2.6% -9.2%

SOMERSET (LGA) ^ 48 $375,000 4.2% $370,000 -2.5% 0.0%

FERNVALE 6 N/A N/A $335,000 -0.6% N/A

KILCOY 7 N/A N/A $227,000 -4.6% -17.5%

LOWOOD 3 N/A N/A $250,000 -3.1% -7.4%

SALES MARKET - HOUSES (CONT’D)

SUBURB NUMBER OF SALES

MEDIAN SALE

QTRLY CHANGE

ANNUAL MEDIAN

SALE

1YR CHANGE

5YR CHANGE

UNIT PRICEPOINTS

79

352

890

490

6181

391

1026

548

75

<$250,000 $250,000+ $350k+ $500k+ $1m+

BRISBANE CITY UNIT SALES (p)

JUN 15 SEP 15

269 286

173

70

7

235 246203

65 4

<$250,000 $250,000+ $350k+ $500k+ $1m+

BRISBANE SURROUNDS UNIT SALES (p)

JUN 15 SEP 15

INCLUDES IPSWICH, LOGAN, MORETON BAY & REDLAND

195

542471

234

33

265

678

555

337

55

<$250,000 $250,000+ $350k+ $500k+ $1m+

GOLD COAST UNIT SALES (p)

JUN 15 SEP 15

74

209 221

127

28

76

220 217

137

22

<$250,000 $250,000+ $350k+ $500k+ $1m+

SUNSHINE COAST & NOOSA UNIT SALES (p)

JUN 15 SEP 15

27

12

62

1315

2 1

<$250,000 $250,000+ $350k+ $500k+

BUNDABERG UNIT SALES (p)

JUN 15 SEP 15

206

5930 27

3

219

6343 34

6

<$250,000 $250,000+ $350k+ $500k+ $1m+

CAIRNS & DOUGLAS UNIT SALES (p)

JUN 15 SEP 15

3228

93

43

15

3 3

<$250,000 $250,000+ $350k+ $500k+

FRASER COAST UNIT SALES (p)

JUN 15 SEP 15

89

3

1

34

3

0

<$250,000 $250,000+ $350k+ $500k+

GLADSTONE UNIT SALES (p)

JUN 15 SEP 15

34

24 21 18

1

48

24

149

2

<$250,000 $250,000+ $350k+ $500k+ $1m+

TOWNSVILLE UNIT SALES (p)

JUN 15 SEP 15

13

7 64

12

7

3

0

<$250,000 $250,000+ $350k+ $500k+

MACKAY UNIT SALES (p)

JUN 15 SEP 15

12

68

3

7 78

5

<$250,000 $250,000+ $350k+ $500k+

ROCKHAMPTON & LIVINGSTONE UNIT SALES (p)

JUN 15 SEP 15

31

44

144

31

60

187

<$250,000 $250,000+ $350k+ $500k+

TOOWOOMBA UNIT SALES (p)

JUN 15 SEP 15

SALES MARKET - UNITS & TOWNHOUSES (CONT’D)

SUBURB NUMBER OF SALES

MEDIAN SALE

QTRLY CHANGE

ANNUAL MEDIAN

SALE

1YR CHANGE

5YR CHANGE

BRISBANE (SD) 2,937 $397,500 1.9% $395,000 1.3% 3.3%

IPSWICH (LGA) 85 $258,000 3.2% $298,000 3.2% 3.5%

BRASSALL 1 N/A N/A $248,500 0.2% -16.5%

BUNDAMBA 6 N/A N/A $302,900 4.4% N/A

GOODNA ~ 9 N/A N/A $252,000 -18.7% N/A

REDBANK PLAINS ~ 3 N/A N/A $225,000 2.7% -23.7%

SPRINGFIELD LAKES 5 N/A N/A $381,900 N/A N/A

SALES MARKET - UNITS & TOWNHOUSES

LOGAN (LGA) 235 $238,000 3.9% $241,000 -2.8% -12.4%

BEENLEIGH ~ 8 N/A N/A $190,000 7.5% -22.4%

BORONIA HEIGHTS ~ t 2 N/A N/A $225,000 12.5% N/A

DAISY HILL 5 N/A N/A $312,500 N/A N/A

EAGLEBY ~ 21 $230,000 11.7% $210,000 -19.2% -25.0%

EDENS LANDING 4 N/A N/A $210,000 N/A N/A

HILLCREST 6 N/A N/A $230,000 6.4% N/A

KINGSTON 5 N/A N/A $275,000 -6.8% -8.3%

LOGAN CENTRAL 5 N/A N/A $184,000 8.2% -10.2%

MARSDEN 8 N/A N/A $331,000 0.3% -6.8%

MEADOWBROOK 5 N/A N/A $248,000 -1.6% -17.3%

MOUNT WARREN PARK 4 N/A N/A $215,000 4.4% -14.0%

ROCHEDALE SOUTH 6 N/A N/A $275,000 1.7% -3.8%

SHAILER PARK 10 $288,000 N/A $280,000 6.5% -8.4%

SLACKS CREEK 15 $227,000 N/A $215,000 7.5% -10.9%

SPRINGWOOD 9 N/A N/A $277,500 6.5% -1.6%

UNDERWOOD 7 N/A N/A $357,500 -5.9% 10.0%

WATERFORD WEST 6 N/A N/A $195,000 0.0% -15.2%

WOODRIDGE 34 $191,500 0.3% $189,000 3.8% -14.9%

MORETON BAY (LGA) 305 $330,000 3.9% $332,500 0.8% -2.2%

ALBANY CREEK * t 2 N/A N/A $417,000 N/A N/A

BELLARA ~ 2 N/A N/A $230,000 N/A -21.4%

BONGAREE 18 $300,000 -4.8% $308,750 6.6% -11.8%

BRENDALE ~ t 17 $255,000 -10.8% $267,000 -16.6% -10.7%

BURPENGARY 2 N/A N/A $281,500 4.3% -7.7%

CABOOLTURE ~ 11 $201,000 -3.8% $189,950 -4.8% -34.5%

CLONTARF ~ 2 N/A N/A $391,250 -9.2% 13.4%

DECEPTION BAY ~ 12 $240,000 3.0% $240,000 -10.8% -26.2%

GRIFFIN 6 N/A N/A $358,500 1.3% N/A

KALLANGUR 16 $300,000 -1.6% $307,250 -6.6% -5.5%

KIPPA-RING 5 N/A N/A $280,000 5.1% -16.9%

LAWNTON ~ 8 N/A N/A $225,000 2.3% -34.8%

MANGO HILL 2 N/A N/A $365,000 2.8% -2.7%

MARGATE 7 N/A N/A $360,000 -3.4% -1.1%

MORAYFIELD 3 N/A N/A $275,000 N/A 8.3%

MURRUMBA DOWNS 14 $330,000 -6.5% $340,000 -3.3% -2.3%

NORTH LAKES ~ 5 N/A N/A $422,500 17.7% N/A

PETRIE 3 N/A N/A $335,500 N/A N/A

REDCLIFFE ~ 24 $331,250 -10.5% $371,800 7.8% -8.2%

SCARBOROUGH ~ 14 $409,500 19.7% $377,500 -3.2% -13.2%

STRATHPINE 4 N/A N/A $263,500 3.4% -7.7%

WOODY POINT ~ 11 $330,000 N/A $310,000 -2.4% -33.0%

WOORIM 7 N/A N/A $353,750 N/A N/A

REDLAND (LGA) ~ t 140 $390,000 6.1% $394,500 12.7% 8.1%

BIRKDALE 11 $392,500 -0.6% $387,500 N/A N/A

CAPALABA ~ 20 $315,000 14.5% $306,114 2.6% 0.4%

CLEVELAND 36 $388,500 11.6% $400,000 -3.6% 3.9%

ORMISTON 7 N/A N/A $360,000 2.9% 2.3%

THORNESIDE 13 $325,000 N/A $321,000 3.2% 7.4%

THORNLANDS 2 N/A N/A $394,500 N/A N/A

VICTORIA POINT 7 N/A N/A $376,000 7.4% 3.0%

WELLINGTON POINT 11 $458,900 1.0% $456,900 N/A N/A

HOUSE PRICEPOINTS

1,194 1,412

628

18

1,265 1,508

652

29

<$350k $350k+ $500k+ $1m+

BRISBANE SURROUNDS HOUSE SALES (p)

JUN 15 SEP 15INCLUDES IPSWICH, LOGAN, MORETON BAY & REDLAND

55

557 698

119 44

567

776

139

<$350k $350k+ $500k+ $1m+

GOLD COAST HOUSE SALES (p)

JUN 15 SEP 15

163

43

8

166

42

7

<$350k $350k+ $500k+

BUNDABERG HOUSE SALES (p)

JUN 15 SEP 15

153

213

90

3

160

247

114

4

<$350k $350k+ $500k+ $1m+

CAIRNS & DOUGLAS HOUSE SALES (p)

JUN 15 SEP 15

211

71

14

203

78

13

<$350k $350k+ $500k+

FRASER COAST HOUSE SALES (p)

JUN 15 SEP 15

48 52

14

57

45

8

<$350k $350k+ $500k+

GLADSTONE HOUSE SALES (p)

JUN 15 SEP 15

227

156

46

222

149

50

<$350k $350k+ $500k+

TOWNSVILLE HOUSE SALES (p)

JUN 15 SEP 15

75 63

21

89

69

16

<$350k $350k+ $500k+

MACKAY HOUSE SALES (p)

JUN 15 SEP 15

133

72

22

146

57

26

<$350k $350k+ $500k+

ROCKHAMPTON & LIVINGSTONE HOUSE SALES (p)

MAR 15 JUN 15

114

740

1,997

318 124

755

2,126

333

<$350k $350k+ $500k+ $1m+

BRISBANE CITY HOUSE SALES (p)

JUN 15 SEP 15215

163

56

233 200

59

<$350k $350k+ $500k+

TOOWOOMBA HOUSE SALES (p)

JUN 15 SEP 15

70

431 427

58 92

437 477

42

<$350k $350k+ $500k+ $1m+

SUNSHINE COAST & NOOSA HOUSE SALES (p)

JUN 15 SEP 15

14 QUEENSLAND MARKET MONITOR

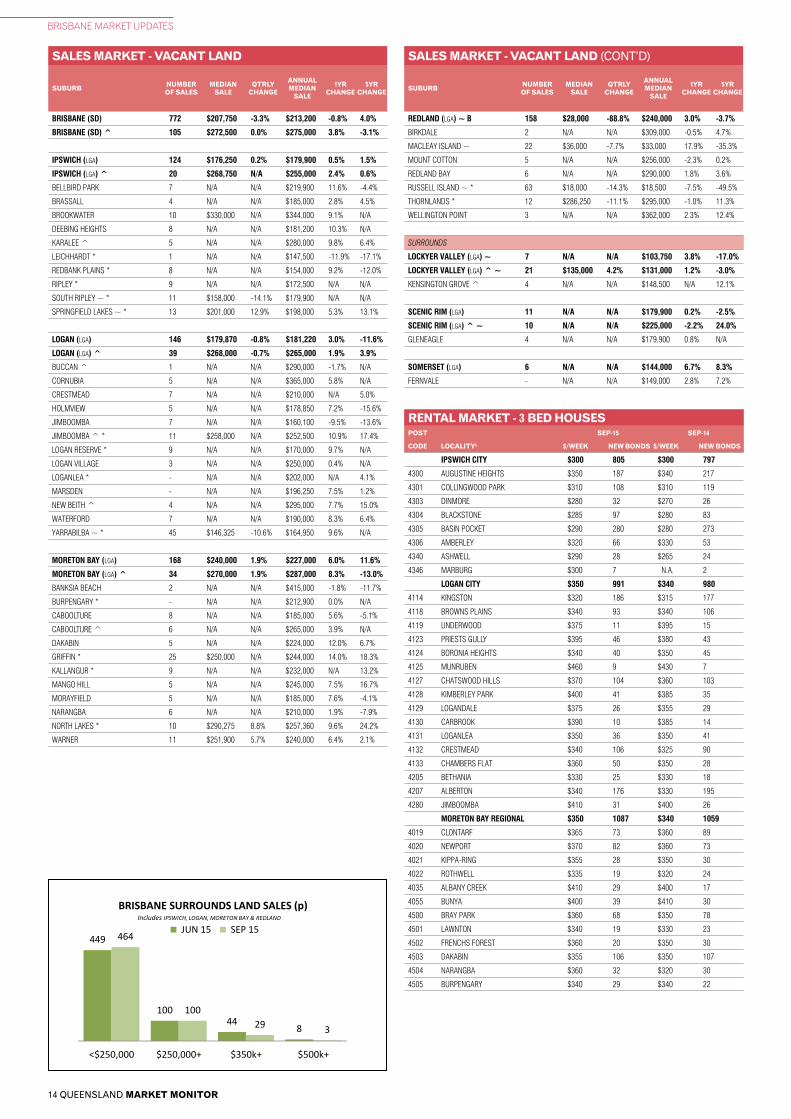

BRISBANE MARKET UPDATES

REDLAND (LGA) ~ B 158 $28,000 -88.8% $240,000 3.0% -3.7%

BIRKDALE 2 N/A N/A $309,000 -0.5% 4.7%

MACLEAY ISLAND ~ 22 $36,000 -7.7% $33,000 17.9% -35.3%

MOUNT COTTON 5 N/A N/A $256,000 -2.3% 0.2%

REDLAND BAY 6 N/A N/A $290,000 1.8% 3.6%

RUSSELL ISLAND ~ * 63 $18,000 -14.3% $18,500 -7.5% -49.5%

THORNLANDS * 12 $286,250 -11.1% $295,000 -1.0% 11.3%

WELLINGTON POINT 3 N/A N/A $362,000 2.3% 12.4%

SURROUNDS

LOCKYER VALLEY (LGA) ~ 7 N/A N/A $103,750 3.8% -17.0%

LOCKYER VALLEY (LGA) ^ ~ 21 $135,000 4.2% $131,000 1.2% -3.0%

KENSINGTON GROVE ^ 4 N/A N/A $148,500 N/A 12.1%

SCENIC RIM (LGA) 11 N/A N/A $179,900 0.2% -2.5%

SCENIC RIM (LGA) ^ ~ 10 N/A N/A $225,000 -2.2% 24.0%

GLENEAGLE 4 N/A N/A $179,900 0.8% N/A

SOMERSET (LGA) 6 N/A N/A $144,000 6.7% 8.3%

FERNVALE - N/A N/A $149,000 2.8% 7.2%

SALES MARKET - VACANT LAND (CONT’D)

SUBURB NUMBER OF SALES

MEDIAN SALE

QTRLY CHANGE

ANNUAL MEDIAN

SALE

1YR CHANGE

5YR CHANGE

RENTAL MARKET - 3 BED HOUSESPOST SEP-15 SEP-14

CODE LOCALITYL $/WEEK NEW BONDS $/WEEK NEW BONDS

BRISBANE (SD) 772 $207,750 -3.3% $213,200 -0.8% 4.0%

BRISBANE (SD) ^ 105 $272,500 0.0% $275,000 3.8% -3.1%

IPSWICH (LGA) 124 $176,250 0.2% $179,900 0.5% 1.5%

IPSWICH (LGA) ^ 20 $268,750 N/A $255,000 2.4% 0.6%

BELLBIRD PARK 7 N/A N/A $219,900 11.6% -4.4%

BRASSALL 4 N/A N/A $185,000 2.8% 4.5%

BROOKWATER 10 $330,000 N/A $344,000 9.1% N/A

DEEBING HEIGHTS 8 N/A N/A $181,200 10.3% N/A

KARALEE ^ 5 N/A N/A $280,000 9.8% 6.4%

LEICHHARDT * 1 N/A N/A $147,500 -11.9% -17.1%

REDBANK PLAINS * 8 N/A N/A $154,000 9.2% -12.0%

RIPLEY * 9 N/A N/A $172,500 N/A N/A

SOUTH RIPLEY ~ * 11 $158,000 -14.1% $179,900 N/A N/A

SPRINGFIELD LAKES ~ * 13 $201,000 12.9% $198,000 5.3% 13.1%

LOGAN (LGA) 146 $179,870 -0.8% $181,220 3.0% -11.6%

LOGAN (LGA) ^ 39 $268,000 -0.7% $265,000 1.9% 3.9%

BUCCAN ^ 1 N/A N/A $290,000 -1.7% N/A

CORNUBIA 5 N/A N/A $365,000 5.8% N/A

CRESTMEAD 7 N/A N/A $210,000 N/A 5.0%

HOLMVIEW 5 N/A N/A $178,850 7.2% -15.6%

JIMBOOMBA 7 N/A N/A $160,100 -9.5% -13.6%

JIMBOOMBA ^ * 11 $258,000 N/A $252,500 10.9% 17.4%

LOGAN RESERVE * 9 N/A N/A $170,000 9.7% N/A

LOGAN VILLAGE 3 N/A N/A $250,000 0.4% N/A

LOGANLEA * - N/A N/A $202,000 N/A 4.1%

MARSDEN - N/A N/A $196,250 7.5% 1.2%

NEW BEITH ^ 4 N/A N/A $295,000 7.7% 15.0%

WATERFORD 7 N/A N/A $190,000 8.3% 6.4%

YARRABILBA ~ * 45 $146,325 -10.6% $164,950 9.6% N/A

MORETON BAY (LGA) 168 $240,000 1.9% $227,000 6.0% 11.6%

MORETON BAY (LGA) ^ 34 $270,000 1.9% $287,000 8.3% -13.0%

BANKSIA BEACH 2 N/A N/A $415,000 -1.8% -11.7%

BURPENGARY * - N/A N/A $212,900 0.0% N/A

CABOOLTURE 8 N/A N/A $185,000 5.6% -5.1%

CABOOLTURE ^ 6 N/A N/A $265,000 3.9% N/A

DAKABIN 5 N/A N/A $224,000 12.0% 6.7%

GRIFFIN * 25 $250,000 N/A $244,000 14.0% 18.3%

KALLANGUR * 9 N/A N/A $232,000 N/A 13.2%

MANGO HILL 5 N/A N/A $245,000 7.5% 16.7%

MORAYFIELD 5 N/A N/A $185,000 7.6% -4.1%

NARANGBA 6 N/A N/A $210,000 1.9% -7.9%

NORTH LAKES * 10 $290,275 8.8% $257,360 9.6% 24.2%

WARNER 11 $251,900 5.7% $240,000 6.4% 2.1%

IPSWICH CITY $300 805 $300 797

4300 AUGUSTINE HEIGHTS $350 187 $340 217

4301 COLLINGWOOD PARK $310 108 $310 119

4303 DINMORE $280 32 $270 26

4304 BLACKSTONE $285 97 $280 83

4305 BASIN POCKET $290 280 $280 273

4306 AMBERLEY $320 66 $330 53

4340 ASHWELL $290 28 $265 24

4346 MARBURG $300 7 N.A. 2

LOGAN CITY $350 991 $340 980

4114 KINGSTON $320 186 $315 177

4118 BROWNS PLAINS $340 93 $340 106

4119 UNDERWOOD $375 11 $395 15

4123 PRIESTS GULLY $395 46 $380 43

4124 BORONIA HEIGHTS $340 40 $350 45

4125 MUNRUBEN $460 9 $430 7

4127 CHATSWOOD HILLS $370 104 $360 103

4128 KIMBERLEY PARK $400 41 $385 35

4129 LOGANDALE $375 26 $355 29

4130 CARBROOK $390 10 $385 14

4131 LOGANLEA $350 36 $350 41

4132 CRESTMEAD $340 106 $325 90

4133 CHAMBERS FLAT $360 50 $350 28

4205 BETHANIA $330 25 $330 18

4207 ALBERTON $340 176 $330 195

4280 JIMBOOMBA $410 31 $400 26

MORETON BAY REGIONAL $350 1087 $340 1059

4019 CLONTARF $365 73 $360 89

4020 NEWPORT $370 82 $360 73

4021 KIPPA-RING $355 28 $350 30

4022 ROTHWELL $335 19 $320 24

4035 ALBANY CREEK $410 29 $400 17

4055 BUNYA $400 39 $410 30

4500 BRAY PARK $360 68 $350 78

4501 LAWNTON $340 19 $330 23

4502 FRENCHS FOREST $360 20 $350 30

4503 DAKABIN $355 106 $350 107

4504 NARANGBA $360 32 $320 30

4505 BURPENGARY $340 29 $340 22

SALES MARKET - VACANT LAND

SUBURB NUMBER OF SALES

MEDIAN SALE

QTRLY CHANGE

ANNUAL MEDIAN

SALE

1YR CHANGE

5YR CHANGE

LAND PRICEPOINTS

(p) Preliminary. See explanatory notes for further information. Source: REIQ, data provided by CoreLogic RP Data.

34 38 36 33

20

7058

28

<$250,000 $250,000+ $350k+ $500k+

BRISBANE CITY LAND SALES (p)

JUN 15 SEP 15

449

10044

8

464

10029 3

<$250,000 $250,000+ $350k+ $500k+

BRISBANE SURROUNDS LAND SALES (p)

JUN 15 SEP 15Includes IPSWICH, LOGAN, MORETON BAY & REDLAND

98

38

617

111

36

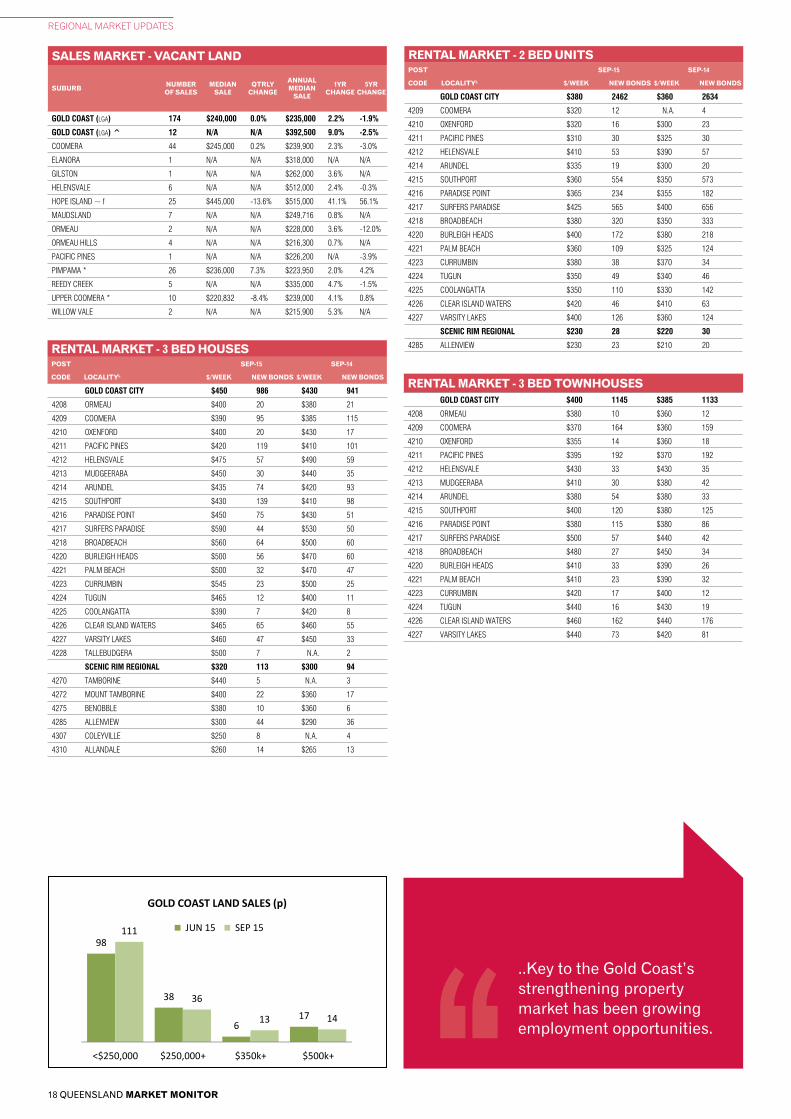

13 14

<$250,000 $250,000+ $350k+ $500k+

GOLD COAST LAND SALES (p)

JUN 15 SEP 15

70

36

21

7

6155

149

<$250,000 $250,000+ $350k+ $500k+

SUNSHINE COAST & NOOSA LAND SALES (p)

JUN 15 SEP 1581

124

56

115

<$250,000 $250,000+ $350k+

CAIRNS & DOUGLAS LAND SALES (p)

JUN 15 SEP 15

53

5 1

78

1 1

<$250,000 $250,000+ $350k+

FRASER COAST LAND SALES (p)

JUN 15 SEP 15

22

2 1

10

31

<$250,000 $250,000+ $350k+

GLADSTONE LAND SALES (p)

JUN 15 SEP 15

53

1 0

43

3 0

<$250,000 $250,000+ $350k+

ROCKHAMPTON & LIVINGSTONE LAND SALES (p)

JUN 15 SEP 15

46

2 0

54

4 1

<$250,000 $250,000+ $350k+

TOOWOOMBA LAND SALES (p)

JUN 15 SEP 15

46

2 3

72

71

<$250,000 $250,000+ $350k+

TOWNSVILLE LAND SALES (p)

JUN 15 SEP 15

15

4 4

22

30

<$250,000 $250,000+ $350k+

MACKAY LAND SALES (p)

JUN 15 SEP 15

36

1 1

41

0 0

<$250,000 $250,000+ $350k+

BUNDABERG LAND SALES (p)

JUN 15 SEP 15

15 SEPTEMBER QUARTER 2015

BRISBANE MARKET UPDATES

4506 MOORINA $305 66 $295 54

4507 BANKSIA BEACH $350 41 $335 44

4508 DECEPTION BAY $320 92 $305 106

4509 MANGO HILL $380 102 $380 78

4510 BALINGOOL $300 173 $285 162

4511 GODWIN BEACH $345 23 $335 28

4514 BELLTHORPE $330 9 $300 12

4520 ARMSTRONG CREEK $435 14 $450 8

4521 CAMPBELLS POCKET $370 14 $410 7

REDLAND CITY $390 343 $380 361

4157 CAPALABA $395 22 $400 30

4158 THORNESIDE $385 14 $360 9