Embed Size (px)

DESCRIPTION

Citation preview

Third quarter 2013 results

14 November 2013

Data in EUR million, unless otherwise stated 3Q 2013 Results Report

DISCLAIMER: Please see important disclaimer in section 8 of this document

ONO – Third quarter 2013 results (unaudited) - 2

Content

1. REPORTING STRUCTURE ............................................................................................ 3

2. OVERVIEW OF GRUPO CORPORATIVO ONO ................................................................ 4

2.1. Key operating and financial events .......................................................................... 5

2.2. Financial highlights ................................................................................................ 7

2.3. Operating highlights............................................................................................... 7

3. GRUPO CORPORATIVO ONO ..................................................................................... 10

3.1. Condensed Consolidated Financial Statements ....................................................... 10

3.2. Notes to the condensed Consolidated Balance Sheet .............................................. 21

3.3. Notes to the Condensed Consolidated Cash Flow ................................................... 23

4. ONO MIDCO ............................................................................................................... 25

5. CABLEUROPA ............................................................................................................ 27

5.1. Condensed Consolidated Financial Statements ....................................................... 27

5.2. Debt and liquidity ................................................................................................ 29

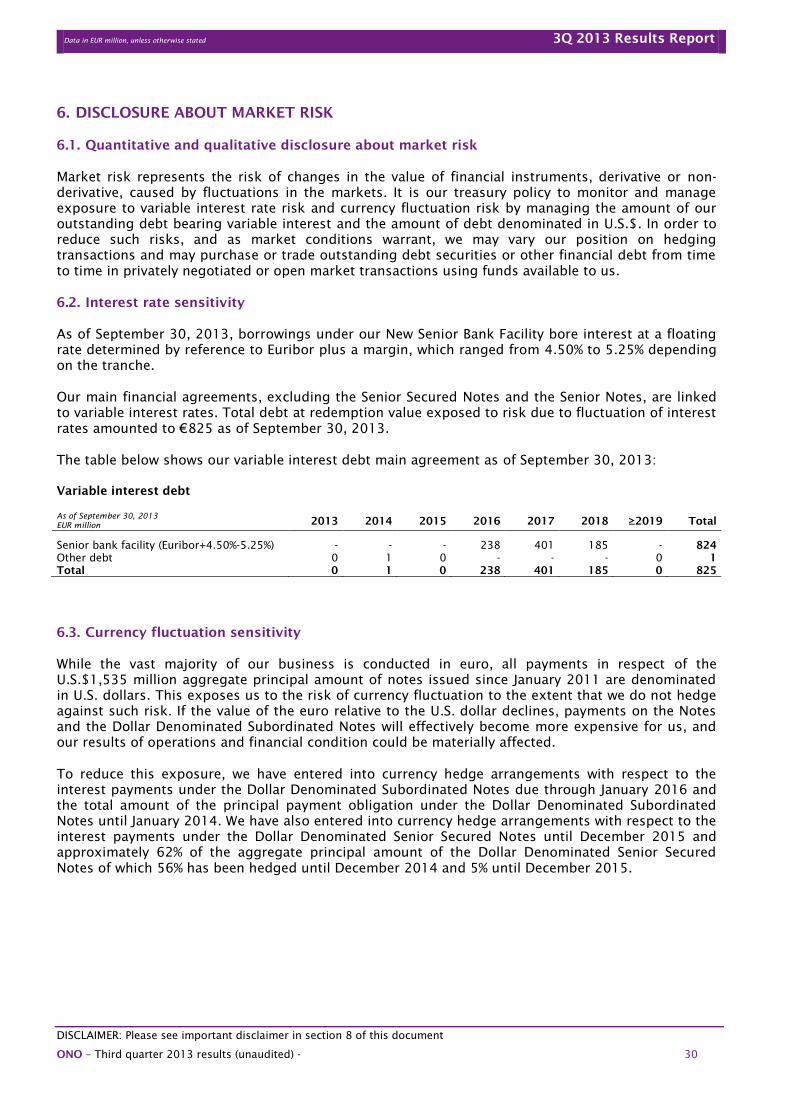

6. DISCLOSURE ABOUT MARKET RISK ........................................................................... 30

6.1. Quantitative and qualitative disclosure about market risk .......................................... 30

6.2. Interest rate sensitivity ......................................................................................... 30

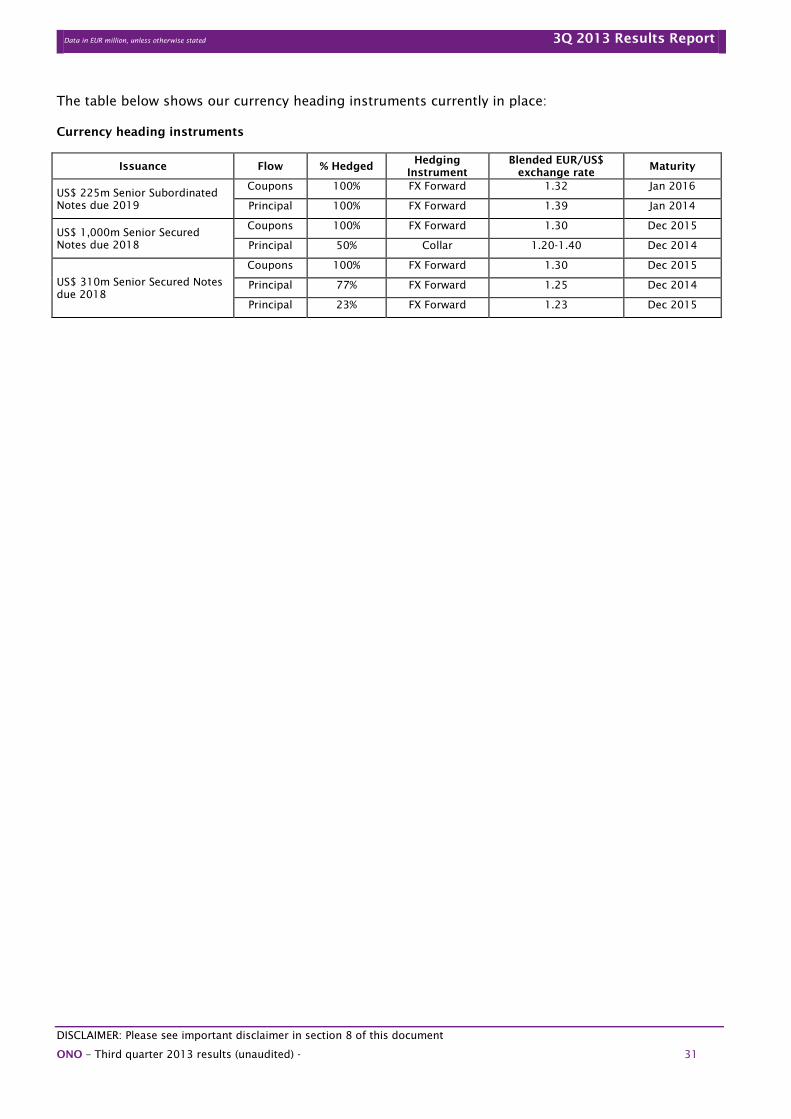

6.3. Currency fluctuation sensitivity .............................................................................. 30

7. GLOSSARY ................................................................................................................ 32

7.1. Operational Definitions ......................................................................................... 32

7.2. Financial Definitions ............................................................................................ 32

7.3. Total Homes and Businesses Data ........................................................................ 33

8. DISCLAIMER .............................................................................................................. 34

Data in EUR million, unless otherwise stated 3Q 2013 Results Report

DISCLAIMER: Please see important disclaimer in section 8 of this document

ONO – Third quarter 2013 results (unaudited) - 3

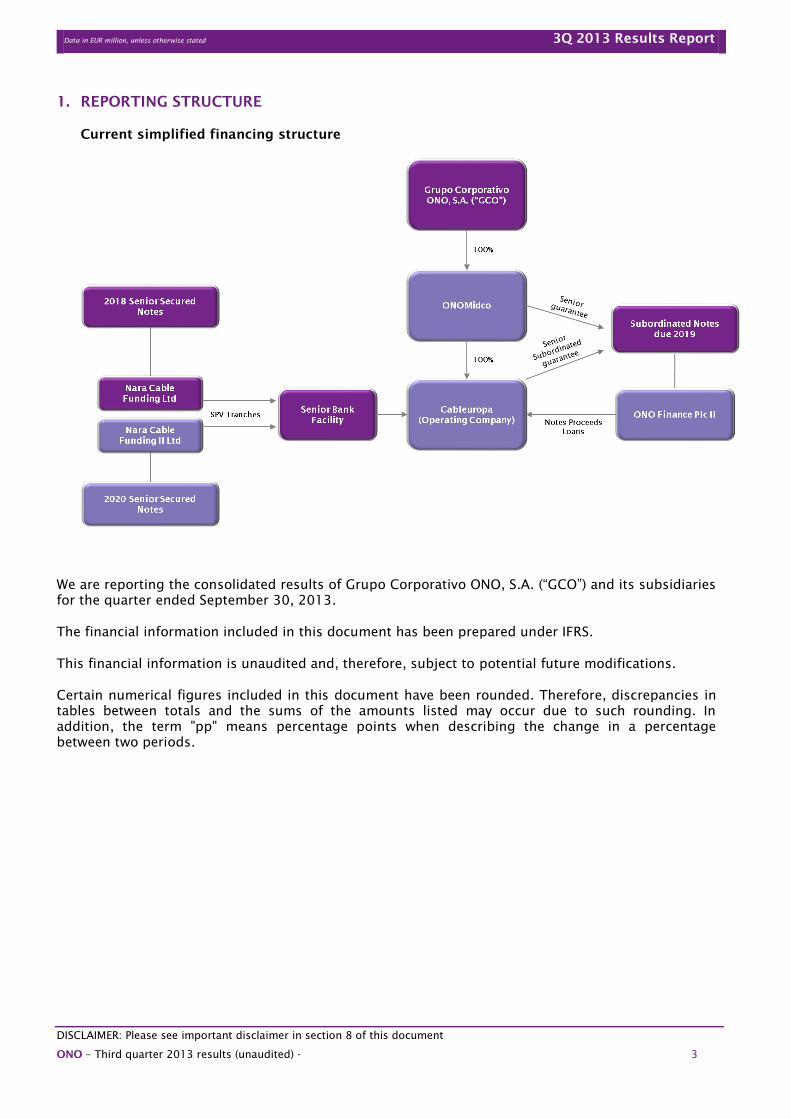

1. REPORTING STRUCTURE

Current simplified financing structure

We are reporting the consolidated results of Grupo Corporativo ONO, S.A. (“GCO”) and its subsidiaries

for the quarter ended September 30, 2013.

The financial information included in this document has been prepared under IFRS.

This financial information is unaudited and, therefore, subject to potential future modifications.

Certain numerical figures included in this document have been rounded. Therefore, discrepancies in

tables between totals and the sums of the amounts listed may occur due to such rounding. In

addition, the term "pp" means percentage points when describing the change in a percentage

between two periods.

Data in EUR million, unless otherwise stated 3Q 2013 Results Report

DISCLAIMER: Please see important disclaimer in section 8 of this document

ONO – Third quarter 2013 results (unaudited) - 4

2. OVERVIEW OF GRUPO CORPORATIVO ONO

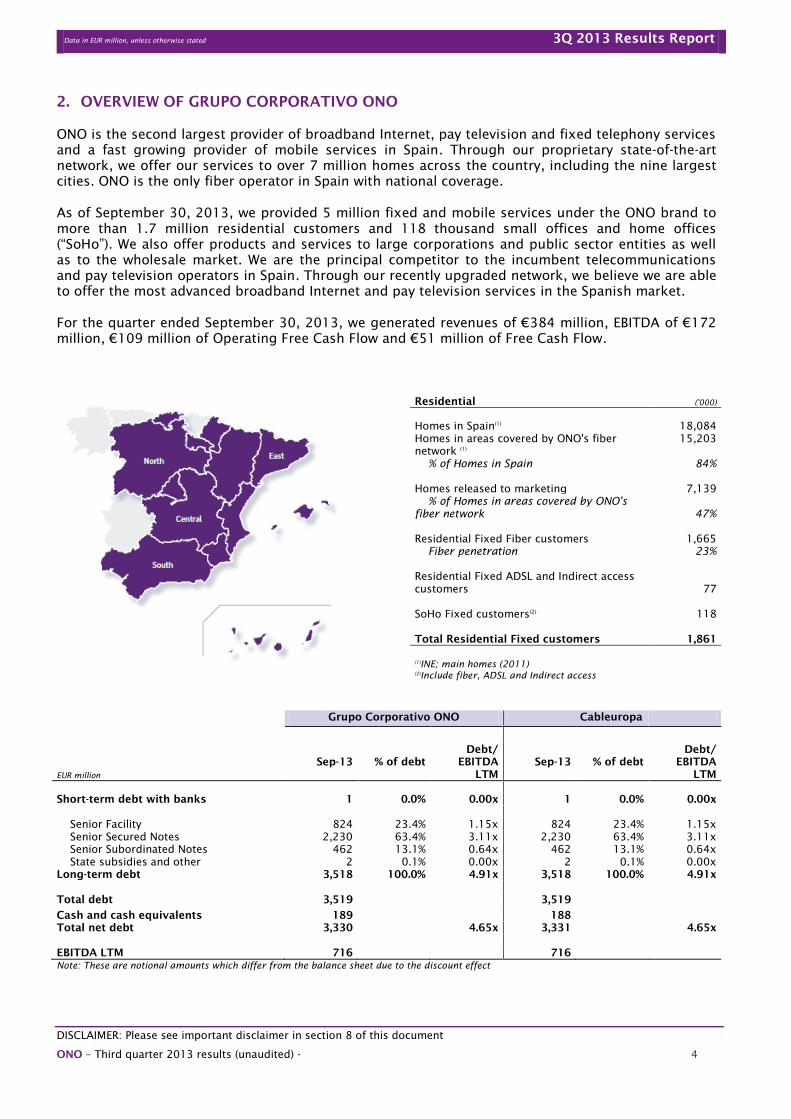

ONO is the second largest provider of broadband Internet, pay television and fixed telephony services

and a fast growing provider of mobile services in Spain. Through our proprietary state-of-the-art

network, we offer our services to over 7 million homes across the country, including the nine largest

cities. ONO is the only fiber operator in Spain with national coverage.

As of September 30, 2013, we provided 5 million fixed and mobile services under the ONO brand to

more than 1.7 million residential customers and 118 thousand small offices and home offices

(“SoHo”). We also offer products and services to large corporations and public sector entities as well

as to the wholesale market. We are the principal competitor to the incumbent telecommunications

and pay television operators in Spain. Through our recently upgraded network, we believe we are able

to offer the most advanced broadband Internet and pay television services in the Spanish market.

For the quarter ended September 30, 2013, we generated revenues of €384 million, EBITDA of €172

million, €109 million of Operating Free Cash Flow and €51 million of Free Cash Flow.

Residential ('000)

Homes in Spain(1)

18,084

Homes in areas covered by ONO's fiber

network (1)

15,203

% of Homes in Spain 84%

Homes released to marketing 7,139

% of Homes in areas covered by ONO's

fiber network 47%

Residential Fixed Fiber customers 1,665

Fiber penetration 23%

Residential Fixed ADSL and Indirect access

customers 77

SoHo Fixed customers(2)

118

Total Residential Fixed customers

1,861

(1)

INE; main homes (2011)

(2)

Include fiber, ADSL and Indirect access

Grupo Corporativo ONO Cableuropa

EUR million

Sep-13 % of debt

Debt/

EBITDA

LTM

Sep-13 % of debt

Debt/

EBITDA

LTM

Short-term debt with banks 1 0.0% 0.00x 1 0.0% 0.00x

Senior Facility 824 23.4% 1.15x 824 23.4% 1.15x

Senior Secured Notes 2,230 63.4% 3.11x 2,230 63.4% 3.11x

Senior Subordinated Notes 462 13.1% 0.64x 462 13.1% 0.64x

State subsidies and other 2 0.1% 0.00x 2 0.1% 0.00x

Long-term debt 3,518 100.0% 4.91x 3,518 100.0% 4.91x

Total debt 3,519 3,519

Cash and cash equivalents 189 188

Total net debt 3,330 4.65x 3,331 4.65x

EBITDA LTM 716 716

Note: These are notional amounts which differ from the balance sheet due to the discount effect

Data in EUR million, unless otherwise stated 3Q 2013 Results Report

DISCLAIMER: Please see important disclaimer in section 8 of this document

ONO – Third quarter 2013 results (unaudited) - 5

2.1. Key operating and financial events

ONO renews its strategy to better compete in current macro and industry environments

In October 2013, during our First Capital Markets Day, we announced the launching of our

renewed strategy to better compete in current macro and industry environments with the ambition

of becoming the preferred option for households and SoHos as provider of communication and

entertainment services in Spain.

Our renewed strategy will focus in three strategic drivers: (i) reach more customers to accelerate

sustainable growth; (ii) increase customer loyalty to reduce churn and create more value; and (iii)

improve our profitability while increasing targeted investments to continue generating cash.

In order to achieve these strategic goals, we have identified five pillars on which to build our

renewed strategy:

1) Development of a differentiated commercial offering with special focus in super high

broadband speeds (>50Mbps) and mobile (Multi-Sims) in order to increase the share of

wallet of our customers while we improve our go-to-market effectiveness and we selectively

increase our marketing investments.

2) Increase customer satisfaction and loyalty to reduce churn through the commercialization

of bundled products (3P/4P), providing free speed upgrades and other product upgrades to

customers as well as providing a superior customer experience.

3) Continuous product innovation in order to reach more customers and provide a superior

customer experience (i.e. TiVo, TV online, WiFi public network, other entertainment

services).

4) Fully digitalize customer life cycle to improve customer experience and reduce costs

through the development of a full eServices functionality and the improvement of our

eCare and eSales platforms.

5) Maximize process efficiency in order to improve our cost structure from good to best in

class through business optimization initiatives (building optimizations, contract

renegotiations, improving call center metrics, reducing field repairs and increasing self-

installation amongst other initiatives) and organizational optimizations.

We believe that ONO is the telecom company best positioned to fully take advantage of a

stabilization of the Spanish macroeconomic environment and that through the implementation of

our renewed strategy we will be able to achieve (i) faster growth; (ii) strong cash generation and

(iii) sustained deleveraging which we believe will provide a compelling return proposition for

investors.

Further advances in high-speed Internet

We continue to lead the market in super-fast broadband. At present we have the capability to

deliver broadband speeds of up to 200Mbps to over 7 million homes in Spain which makes us the

only telecom operator able to market these products on a broad scale.

On the back of our state-of-the-art infrastructure we have developed a superior offering with real

broadband speeds of up to 100 Mbps for residential customers and up to 200Mbps for SoHos (we

expect to launch 500 Mbps broadband speeds in the near future) that compares favorably to the

high-end packages with up to 30 Mbps speeds offered by the DSL players on a non-homogenous

basis.

Data in EUR million, unless otherwise stated 3Q 2013 Results Report

DISCLAIMER: Please see important disclaimer in section 8 of this document

ONO – Third quarter 2013 results (unaudited) - 6

In August 2013 we took a step forward in our strong commitment towards super high speeds. On

the one hand we fully redefined our retail offering to include exclusively super high broadband

speeds packages of 50,100 & 200 Mbps (we continue to marginally sell 20Mbps broadband

packages through the on-line channel for most price sensitive customers). On the other hand, we

launched a loyalty campaign by which we are seeking to migrate existing customers to our new

super high speeds product offering either for free or for a small incremental price.

As of September 2013, 818 thousand residential customers subscribed to our high and super-high

speed Internet packages, representing 60% of our residential broadband customer base and

almost 600 thousand broadband customers had already been migrated to our new product

offerings. We believe that these commercial results position ONO as the market leader in high-

speed Internet in Spain.

Further advances in mobile

We have increased our total mobile services by 587 thousand in the last twelve months to reach

902 thousand as of September 2013 on the back of our competitive price plans. We believe this to

be an excellent commercial result.

During 2012, we redefined our mobile proposition with the aim of adapting our tariffs to new

customers’ needs and markets dynamics. This included the development of more compelling

fixed-mobile convergent and bundled offers and the introduction of selective handset financing.

In August 2013 we further improved our mobile proposition and we launched a renewed multi-SIM

mobile package by which customers can subscribe to a 200min/200Mbps product for €5 per

month. We expect this service to continue delivering positive results in the future on the back of

our competitive price plans.

Further advances in pay TV

In October 2011, we officially launched our next generation TV service (TiVo) to customers in

Madrid and Barcelona and since then we have made this service available in our entire network.

This innovative product, which we believe is unmatched in Spain, provides our customers with a

high quality interactive experience and a wide variety of content combining 37 HD channels (HD

leadership in Spain), 3D functionalities and broadband connectivity with a powerful and

personalized search engine and a PVR (Personal Video Recorder).

As of September 2013, we had over 259 thousand TiVo services which represent 31% of our TV

customer base. We believe that the TiVo results so far suggest positive market acceptance as

showcased by the positive momentum in customer acquisitions, low churn levels and high

satisfaction metrics.

With the aim of continuing to improve our pay TV offering, in October 2013 we upgraded our TiVo

service with new functionalities that include an improved user interface, an improved search

engine, the ability to share content between different TiVo boxes within a household and a new

energy saving mode amongst other.

We intent to continue improving our pay TV offering in the near future with the development of

new products and services such as TV online. We believe this will help us to increase the number

of our TV customers and revenues going forward.

Data in EUR million, unless otherwise stated 3Q 2013 Results Report

DISCLAIMER: Please see important disclaimer in section 8 of this document

ONO – Third quarter 2013 results (unaudited) - 7

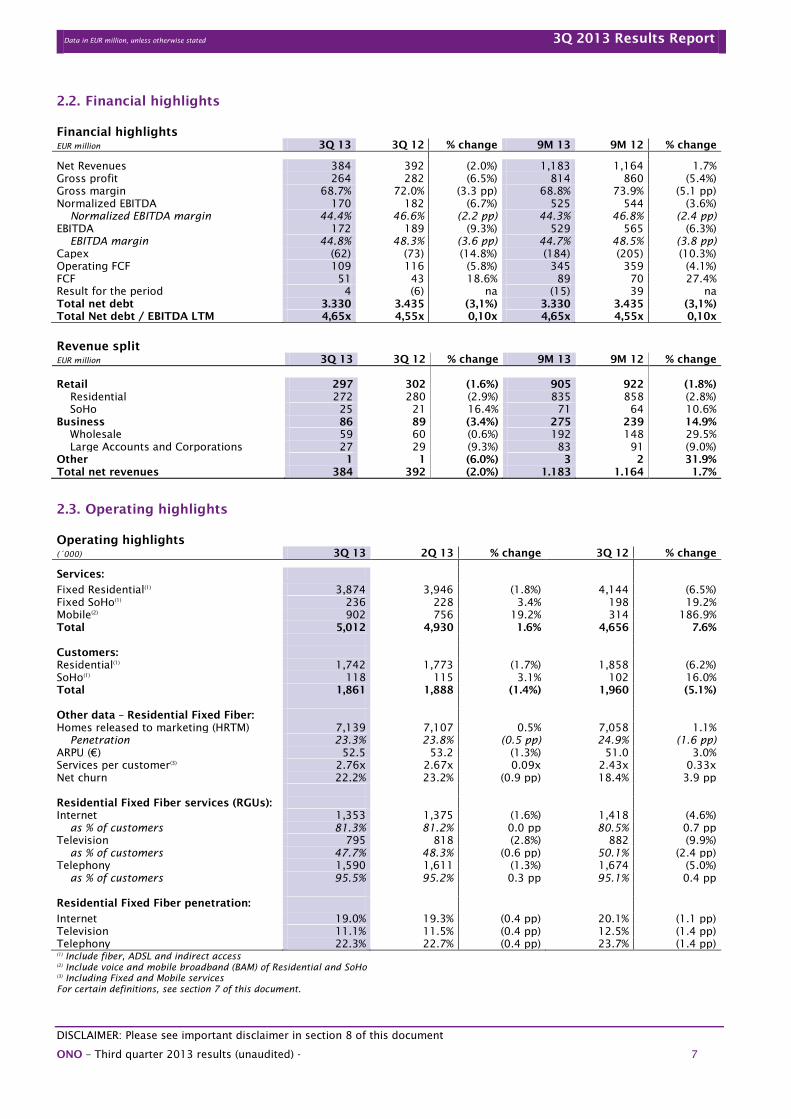

2.2. Financial highlights

Financial highlights

EUR million 3Q 13 3Q 12 % change 9M 13 9M 12 % change

Net Revenues 384 392 (2.0%) 1,183 1,164 1.7%

Gross profit 264 282 (6.5%) 814 860 (5.4%)

Gross margin 68.7% 72.0% (3.3 pp) 68.8% 73.9% (5.1 pp)

Normalized EBITDA 170 182 (6.7%) 525 544 (3.6%)

Normalized EBITDA margin 44.4% 46.6% (2.2 pp) 44.3% 46.8% (2.4 pp)

EBITDA 172 189 (9.3%) 529 565 (6.3%)

EBITDA margin 44.8% 48.3% (3.6 pp) 44.7% 48.5% (3.8 pp)

Capex (62) (73) (14.8%) (184) (205) (10.3%)

Operating FCF 109 116 (5.8%) 345 359 (4.1%)

FCF 51 43 18.6% 89 70 27.4%

Result for the period 4 (6) na (15) 39 na

Total net debt 3.330 3.435 (3,1%) 3.330 3.435 (3,1%)

Total Net debt / EBITDA LTM 4,65x 4,55x 0,10x 4,65x 4,55x 0,10x

Revenue split

EUR million 3Q 13 3Q 12 % change 9M 13 9M 12 % change

Retail 297 302 (1.6%) 905 922 (1.8%)

Residential 272 280 (2.9%) 835 858 (2.8%)

SoHo 25 21 16.4% 71 64 10.6%

Business 86 89 (3.4%) 275 239 14.9%

Wholesale 59 60 (0.6%) 192 148 29.5%

Large Accounts and Corporations 27 29 (9.3%) 83 91 (9.0%)

Other 1 1 (6.0%) 3 2 31.9%

Total net revenues 384 392 (2.0%) 1.183 1.164 1.7%

2.3. Operating highlights

Operating highlights

(´000) 3Q 13 2Q 13 % change 3Q 12 % change

Services:

Fixed Residential(1)

3,874 3,946 (1.8%) 4,144 (6.5%)

Fixed SoHo(1)

236 228 3.4% 198 19.2%

Mobile(2)

902 756 19.2% 314 186.9%

Total 5,012 4,930 1.6% 4,656 7.6%

Customers:

Residential(1)

1,742 1,773 (1.7%) 1,858 (6.2%)

SoHo(1)

118 115 3.1% 102 16.0%

Total 1,861 1,888 (1.4%) 1,960 (5.1%)

Other data – Residential Fixed Fiber:

Homes released to marketing (HRTM) 7,139 7,107 0.5% 7,058 1.1%

Penetration 23.3% 23.8% (0.5 pp) 24.9% (1.6 pp)

ARPU (€) 52.5 53.2 (1.3%) 51.0 3.0%

Services per customer(3)

2.76x 2.67x 0.09x 2.43x 0.33x

Net churn 22.2% 23.2% (0.9 pp) 18.4% 3.9 pp

Residential Fixed Fiber services (RGUs):

Internet 1,353 1,375 (1.6%) 1,418 (4.6%)

as % of customers 81.3% 81.2% 0.0 pp 80.5% 0.7 pp

Television 795 818 (2.8%) 882 (9.9%)

as % of customers 47.7% 48.3% (0.6 pp) 50.1% (2.4 pp)

Telephony 1,590 1,611 (1.3%) 1,674 (5.0%)

as % of customers 95.5% 95.2% 0.3 pp 95.1% 0.4 pp

Residential Fixed Fiber penetration:

Internet 19.0% 19.3% (0.4 pp) 20.1% (1.1 pp)

Television 11.1% 11.5% (0.4 pp) 12.5% (1.4 pp)

Telephony 22.3% 22.7% (0.4 pp) 23.7% (1.4 pp)

(1)

Include fiber, ADSL and indirect access

(2)

Include voice and mobile broadband (BAM) of Residential and SoHo

(3)

Including Fixed and Mobile services

For certain definitions, see section 7 of this document.

Data in EUR million, unless otherwise stated 3Q 2013 Results Report

DISCLAIMER: Please see important disclaimer in section 8 of this document

ONO – Third quarter 2013 results (unaudited) - 8

We ended September with over 5 million services taken by 1.9 million retail customers. Our push into

mobile has allowed us to grow the services we provide to our retail customers by 1.6% in the quarter

or 81 thousand services.

The third quarter of 2013 was marked by the continuation of the challenging macroeconomic

environment (although slightly improving) but more importantly, by the tough market competition.

From a macroeconomic perspective during the quarter consumers continued to lose spending power

on the back of reinforced fiscal pressures and real and nominal wage reductions; this, combined with

an absence of visibility on the future, has continued to negatively impact consumption.

From a competitive landscape the quarter confirmed the market trend towards convergent offers and

price based competition. On convergence, we have been an early promoter of this concept. Early

success is proving stable and we now have over 902 thousand mobile customers with a very

considerable impact on revenues and churn. We fully expect convergence to be a dominant force

going forward as more and more households see this as a positive product solution for their entire

telecommunication needs based on simplicity and significant savings. But convergence puts a lot of

pressure on telecommunication companies as all operators are trying to defend their customer base

even at high price discounts.

In this environment, we increasingly see a polarization between those customers willing to pay more

for better products and services and those who are more price sensitive and ready to give away

quality in exchange for price.

We have seen this trend taking a toll on our pay television services that decreased by almost 23

thousand in the quarter. The polarization of the market is also impacting our fixed telephony service

where the most price sensitive customers within our customer base, mainly single play, are dropping

the service and going “mobile” only which has resulted in 20 thousand fixed telephony loses in the

quarter. Also although we have seen a strong performance of high and super-high speed internet

customers (95% of our new customers acquisition during the quarter were in high speeds), the

aggressive pricing movements from our competitors have negatively impacted our low speeds

broadband customers leading to a loss of almost 22 thousand services in the quarter.

In order to better compete in current macro and market environments in October 2013 we announced

the launch of a renewed strategy with a focus in three strategic drivers: (i) reach more customers to

accelerate sustainable growth; (ii) increase customer loyalty to reduce churn and create more value;

and (iii) improve our profitability while increasing targeted investments to continue generating cash.

In order to achieve these strategic goals, we have identified five pillars on which to build our renewed

strategy: (i) Development of a differentiated commercial offering with special focus in super high

broadband speeds (>50Mbps) and mobile (Multi-Sims); (ii) Increase customer satisfaction and loyalty

to reduce churn; (iii) Continuous product innovation in order reach more customers and provide a

superior customer experience (i.e. TiVo, TV online, WiFi public network, other entertainment

services); (iv) Fully digitalize customer life cycle to improve customer experience and reduce costs;

and (v) Maximize process efficiency in order to improve our cost structure from good to best in class.

We expect that as results of the implementation of our renewed strategy we will be able to reverse

the negative trends experienced in our operating metrics in the past quarters and to achieve future

customer and services growth.

Residential fiber ARPU increased by €1.5 as compared with the same quarter of the previous year to

reach €52.5. ARPU has continued to be negatively impacted by the challenging macro environment

and the increased price pressures described above. Nevertheless, this decrease has been fully offset

by the good performance of TiVo and mobile. We believe the high quality of our customer base and

our superior product offering (including high-speed Internet, mobile and TiVo) have proven to be

extremely useful tools to increase ARPU in the current environment in which consumption based

products are heavily affected.

Data in EUR million, unless otherwise stated 3Q 2013 Results Report

DISCLAIMER: Please see important disclaimer in section 8 of this document

ONO – Third quarter 2013 results (unaudited) - 9

Our focus on providing bundled services, the continuous up-sale and cross-sale campaigns to our

customer base as well as our push into mobile have enabled us to increase our residential fiber

services per customer by 0.3x in the last twelve months to reach 2.76x as of September. In addition,

in the third quarter of 2013, 86% of our residential fiber customers subscribed to a bundled package

(47% Double, 39% Triple) and 13% subscribed to a quadruple play package which makes us the

leading provider of bundled services in Spain.

Residential fiber net churn decreased by 1% in the quarter to reach 22.2% as of September 2013. The

negative macro and industry environments have continued to negatively impact our most price

sensitive customers, typically those that subscribe to a single service or to a low tier double or triple

play packages. Nevertheless we believe that the new initiatives we have developed on the back of our

renewed strategy that include: (i) free speeds upgrades and product repositioning (over 600 thousand

customers migrated as of September 2013); (ii) high quality customers acquisition; and (iii) improved

prevention and retention processes are already delivering positive results and will continue to help us

reduce churn going forward.

Our SoHo segment continued to perform well and we managed to add over 8 thousand services and 4

thousand customers in the last quarter to reach 236 thousand and 118 thousand, respectively. These

good results were mainly driven by: (i) our strong product offerings and competitive price plans that

include broadband speeds of up to 200 Mbps (500 Mbps in the near future), mobile, multi-site

services as well as other value added services (including domain registration, housing, hosting and

cloud computing; (ii) our successful channel mix strategy; (iii) the improvement of our brand

awareness (through brand recognition activities and direct marketing efforts amongst other

initiatives); and (iv) the improvement of customer experience and churn levels as result of our

improved multi-skill platforms.

Data in EUR million, unless otherwise stated 3Q 2013 Results Report

DISCLAIMER: Please see important disclaimer in section 8 of this document

ONO – Third quarter 2013 results (unaudited) - 10

3. GRUPO CORPORATIVO ONO

3.1. Condensed Consolidated Financial Statements

Condensed Consolidated Statements of Operations

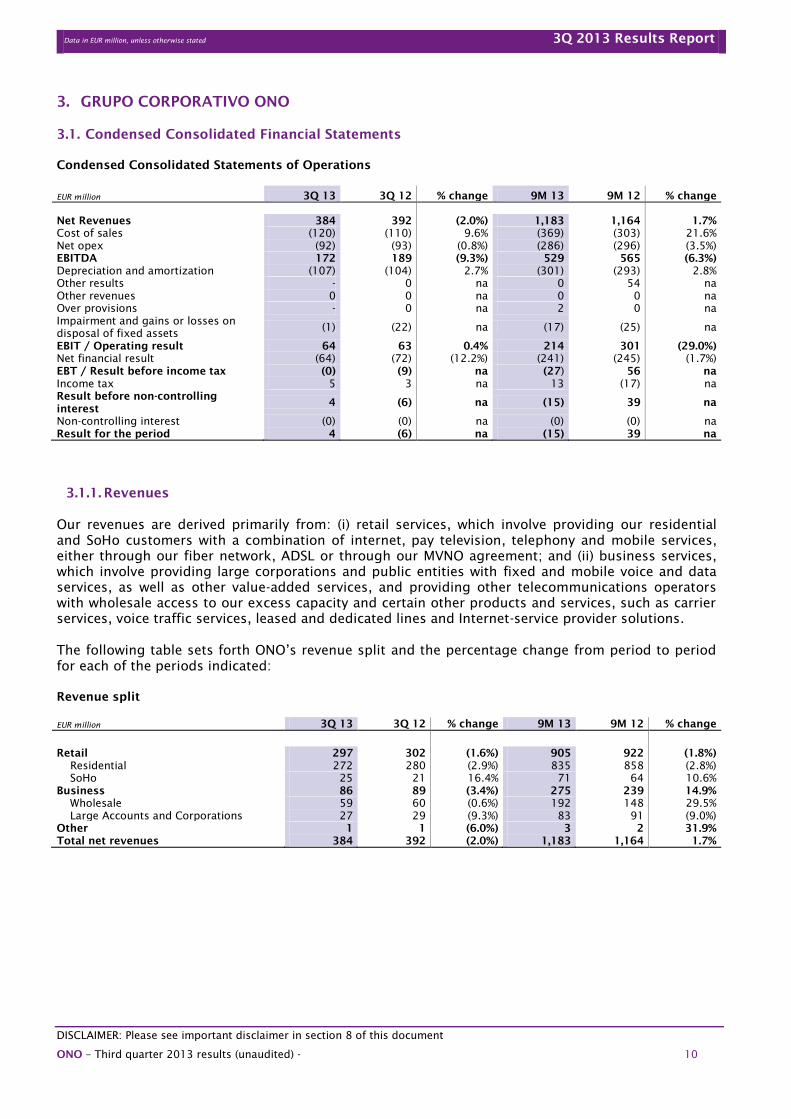

EUR million 3Q 13 3Q 12 % change 9M 13 9M 12 % change

Net Revenues 384 392 (2.0%) 1,183 1,164 1.7%

Cost of sales (120) (110) 9.6% (369) (303) 21.6%

Net opex (92) (93) (0.8%) (286) (296) (3.5%)

EBITDA 172 189 (9.3%) 529 565 (6.3%)

Depreciation and amortization (107) (104) 2.7% (301) (293) 2.8%

Other results - 0 na 0 54 na

Other revenues 0 0 na 0 0 na

Over provisions - 0 na 2 0 na

Impairment and gains or losses on

disposal of fixed assets (1) (22) na (17) (25) na

EBIT / Operating result 64 63 0.4% 214 301 (29.0%)

Net financial result (64) (72) (12.2%) (241) (245) (1.7%)

EBT / Result before income tax (0) (9) na (27) 56 na

Income tax 5 3 na 13 (17) na

Result before non-controlling

interest 4 (6) na (15) 39 na

Non-controlling interest (0) (0) na (0) (0) na

Result for the period 4 (6) na (15) 39 na

3.1.1. Revenues

Our revenues are derived primarily from: (i) retail services, which involve providing our residential

and SoHo customers with a combination of internet, pay television, telephony and mobile services,

either through our fiber network, ADSL or through our MVNO agreement; and (ii) business services,

which involve providing large corporations and public entities with fixed and mobile voice and data

services, as well as other value-added services, and providing other telecommunications operators

with wholesale access to our excess capacity and certain other products and services, such as carrier

services, voice traffic services, leased and dedicated lines and Internet-service provider solutions.

The following table sets forth ONO’s revenue split and the percentage change from period to period

for each of the periods indicated:

Revenue split

EUR million 3Q 13 3Q 12 % change 9M 13 9M 12 % change

Retail 297 302 (1.6%) 905 922 (1.8%)

Residential 272 280 (2.9%) 835 858 (2.8%)

SoHo 25 21 16.4% 71 64 10.6%

Business 86 89 (3.4%) 275 239 14.9%

Wholesale 59 60 (0.6%) 192 148 29.5%

Large Accounts and Corporations 27 29 (9.3%) 83 91 (9.0%)

Other 1 1 (6.0%) 3 2 31.9%

Total net revenues 384 392 (2.0%) 1,183 1,164 1.7%

Data in EUR million, unless otherwise stated 3Q 2013 Results Report

DISCLAIMER: Please see important disclaimer in section 8 of this document

ONO – Third quarter 2013 results (unaudited) - 11

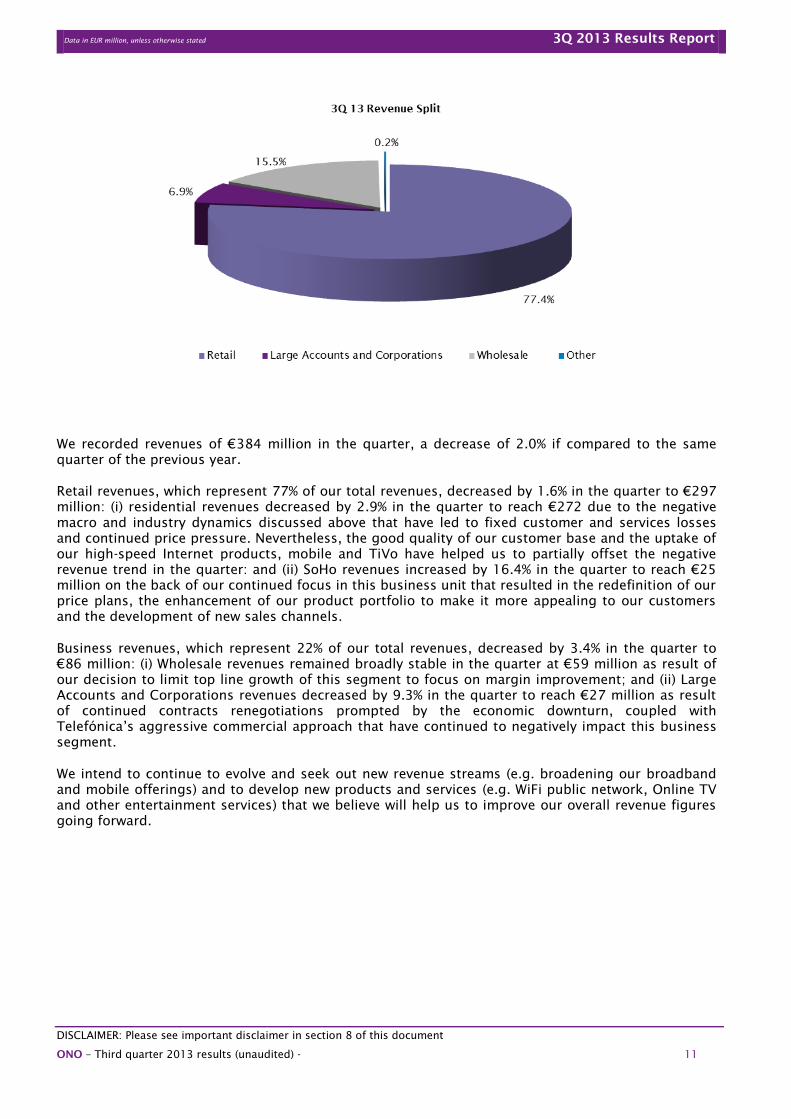

We recorded revenues of €384 million in the quarter, a decrease of 2.0% if compared to the same

quarter of the previous year.

Retail revenues, which represent 77% of our total revenues, decreased by 1.6% in the quarter to €297

million: (i) residential revenues decreased by 2.9% in the quarter to reach €272 due to the negative

macro and industry dynamics discussed above that have led to fixed customer and services losses

and continued price pressure. Nevertheless, the good quality of our customer base and the uptake of

our high-speed Internet products, mobile and TiVo have helped us to partially offset the negative

revenue trend in the quarter: and (ii) SoHo revenues increased by 16.4% in the quarter to reach €25

million on the back of our continued focus in this business unit that resulted in the redefinition of our

price plans, the enhancement of our product portfolio to make it more appealing to our customers

and the development of new sales channels.

Business revenues, which represent 22% of our total revenues, decreased by 3.4% in the quarter to

€86 million: (i) Wholesale revenues remained broadly stable in the quarter at €59 million as result of

our decision to limit top line growth of this segment to focus on margin improvement; and (ii) Large

Accounts and Corporations revenues decreased by 9.3% in the quarter to reach €27 million as result

of continued contracts renegotiations prompted by the economic downturn, coupled with

Telefónica’s aggressive commercial approach that have continued to negatively impact this business

segment.

We intend to continue to evolve and seek out new revenue streams (e.g. broadening our broadband

and mobile offerings) and to develop new products and services (e.g. WiFi public network, Online TV

and other entertainment services) that we believe will help us to improve our overall revenue figures

going forward.

Data in EUR million, unless otherwise stated 3Q 2013 Results Report

DISCLAIMER: Please see important disclaimer in section 8 of this document

ONO – Third quarter 2013 results (unaudited) - 12

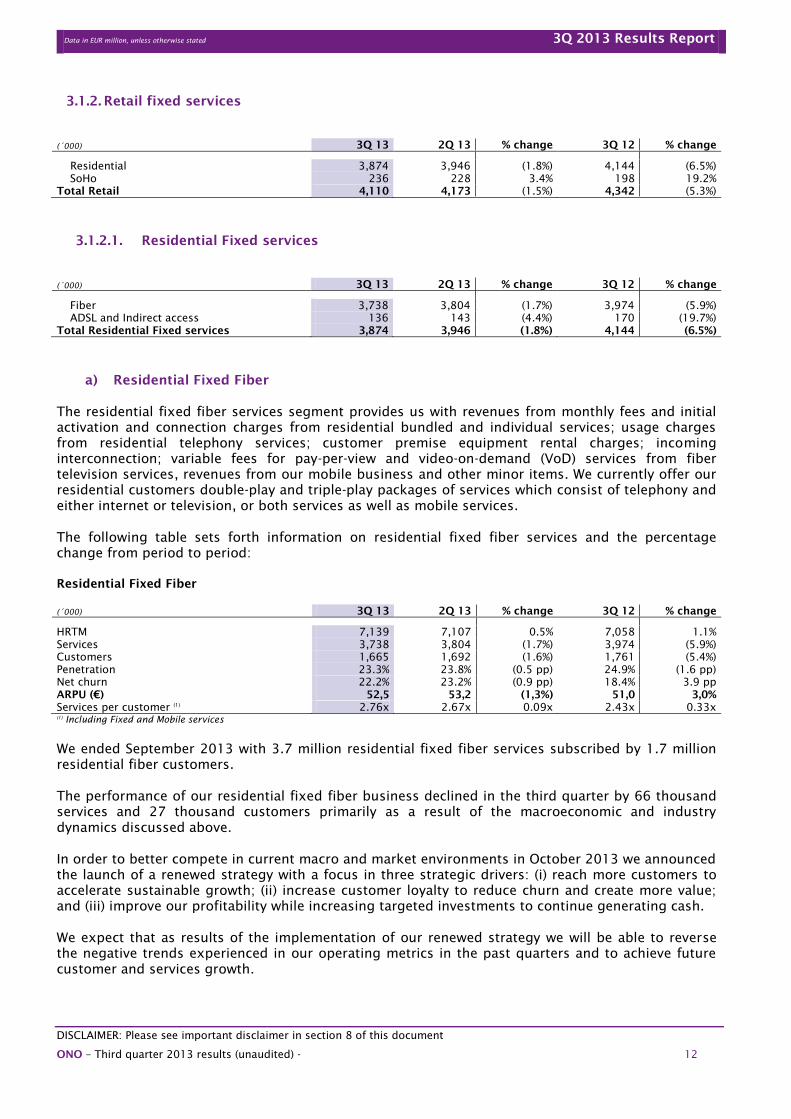

3.1.2. Retail fixed services

(´000) 3Q 13 2Q 13 % change 3Q 12 % change

Residential 3,874 3,946 (1.8%) 4,144 (6.5%)

SoHo 236 228 3.4% 198 19.2%

Total Retail 4,110 4,173 (1.5%) 4,342 (5.3%)

3.1.2.1. Residential Fixed services

(´000) 3Q 13 2Q 13 % change 3Q 12 % change

Fiber 3,738 3,804 (1.7%) 3,974 (5.9%)

ADSL and Indirect access 136 143 (4.4%) 170 (19.7%)

Total Residential Fixed services 3,874 3,946 (1.8%) 4,144 (6.5%)

a) Residential Fixed Fiber

The residential fixed fiber services segment provides us with revenues from monthly fees and initial

activation and connection charges from residential bundled and individual services; usage charges

from residential telephony services; customer premise equipment rental charges; incoming

interconnection; variable fees for pay-per-view and video-on-demand (VoD) services from fiber

television services, revenues from our mobile business and other minor items. We currently offer our

residential customers double-play and triple-play packages of services which consist of telephony and

either internet or television, or both services as well as mobile services.

The following table sets forth information on residential fixed fiber services and the percentage

change from period to period:

Residential Fixed Fiber

(´000) 3Q 13 2Q 13 % change 3Q 12 % change

HRTM 7,139 7,107 0.5% 7,058 1.1%

Services 3,738 3,804 (1.7%) 3,974 (5.9%)

Customers 1,665 1,692 (1.6%) 1,761 (5.4%)

Penetration 23.3% 23.8% (0.5 pp) 24.9% (1.6 pp)

Net churn 22.2% 23.2% (0.9 pp) 18.4% 3.9 pp

ARPU (€) 52,5 53,2 (1,3%) 51,0 3,0%

Services per customer (1)

2.76x 2.67x 0.09x 2.43x 0.33x

(1)

Including Fixed and Mobile services

We ended September 2013 with 3.7 million residential fixed fiber services subscribed by 1.7 million

residential fiber customers.

The performance of our residential fixed fiber business declined in the third quarter by 66 thousand

services and 27 thousand customers primarily as a result of the macroeconomic and industry

dynamics discussed above.

In order to better compete in current macro and market environments in October 2013 we announced

the launch of a renewed strategy with a focus in three strategic drivers: (i) reach more customers to

accelerate sustainable growth; (ii) increase customer loyalty to reduce churn and create more value;

and (iii) improve our profitability while increasing targeted investments to continue generating cash.

We expect that as results of the implementation of our renewed strategy we will be able to reverse

the negative trends experienced in our operating metrics in the past quarters and to achieve future

customer and services growth.

Data in EUR million, unless otherwise stated 3Q 2013 Results Report

DISCLAIMER: Please see important disclaimer in section 8 of this document

ONO – Third quarter 2013 results (unaudited) - 13

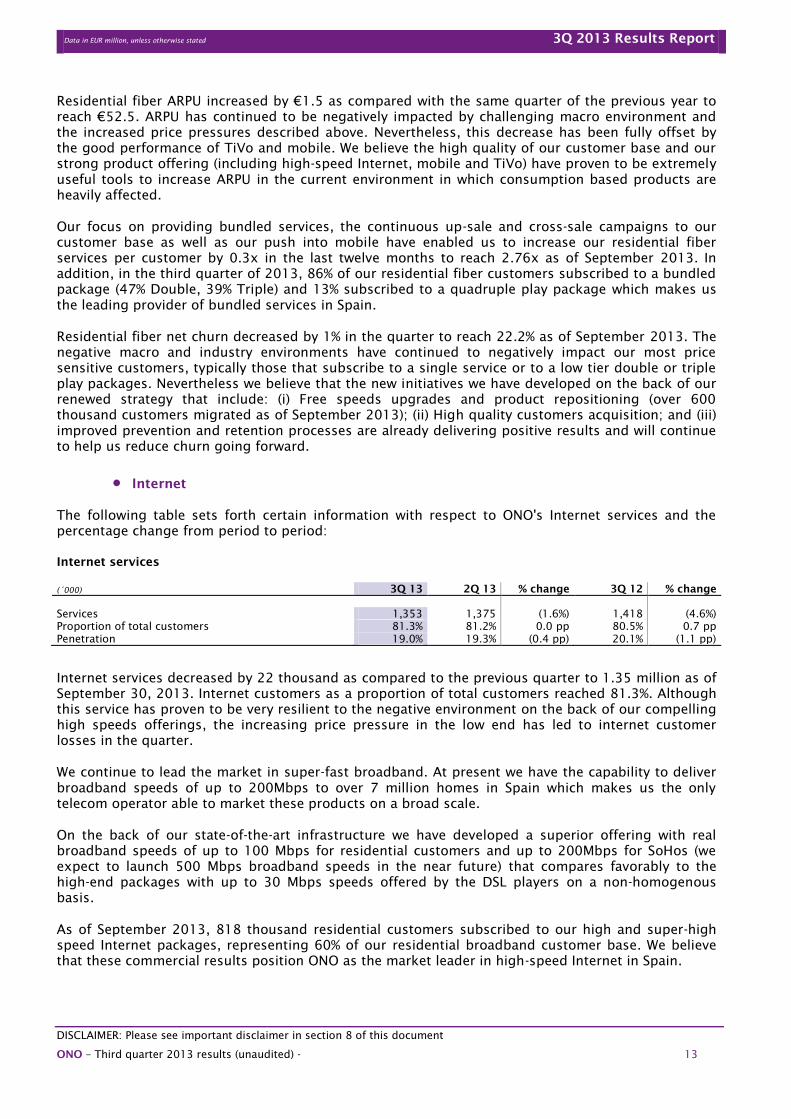

Residential fiber ARPU increased by €1.5 as compared with the same quarter of the previous year to

reach €52.5. ARPU has continued to be negatively impacted by challenging macro environment and

the increased price pressures described above. Nevertheless, this decrease has been fully offset by

the good performance of TiVo and mobile. We believe the high quality of our customer base and our

strong product offering (including high-speed Internet, mobile and TiVo) have proven to be extremely

useful tools to increase ARPU in the current environment in which consumption based products are

heavily affected.

Our focus on providing bundled services, the continuous up-sale and cross-sale campaigns to our

customer base as well as our push into mobile have enabled us to increase our residential fiber

services per customer by 0.3x in the last twelve months to reach 2.76x as of September 2013. In

addition, in the third quarter of 2013, 86% of our residential fiber customers subscribed to a bundled

package (47% Double, 39% Triple) and 13% subscribed to a quadruple play package which makes us

the leading provider of bundled services in Spain.

Residential fiber net churn decreased by 1% in the quarter to reach 22.2% as of September 2013. The

negative macro and industry environments have continued to negatively impact our most price

sensitive customers, typically those that subscribe to a single service or to a low tier double or triple

play packages. Nevertheless we believe that the new initiatives we have developed on the back of our

renewed strategy that include: (i) Free speeds upgrades and product repositioning (over 600

thousand customers migrated as of September 2013); (ii) High quality customers acquisition; and (iii)

improved prevention and retention processes are already delivering positive results and will continue

to help us reduce churn going forward.

Internet

The following table sets forth certain information with respect to ONO's Internet services and the

percentage change from period to period:

Internet services

(´000) 3Q 13 2Q 13 % change 3Q 12 % change

Services 1,353 1,375 (1.6%) 1,418 (4.6%)

Proportion of total customers 81.3% 81.2% 0.0 pp 80.5% 0.7 pp

Penetration 19.0% 19.3% (0.4 pp) 20.1% (1.1 pp)

Internet services decreased by 22 thousand as compared to the previous quarter to 1.35 million as of

September 30, 2013. Internet customers as a proportion of total customers reached 81.3%. Although

this service has proven to be very resilient to the negative environment on the back of our compelling

high speeds offerings, the increasing price pressure in the low end has led to internet customer

losses in the quarter.

We continue to lead the market in super-fast broadband. At present we have the capability to deliver

broadband speeds of up to 200Mbps to over 7 million homes in Spain which makes us the only

telecom operator able to market these products on a broad scale.

On the back of our state-of-the-art infrastructure we have developed a superior offering with real

broadband speeds of up to 100 Mbps for residential customers and up to 200Mbps for SoHos (we

expect to launch 500 Mbps broadband speeds in the near future) that compares favorably to the

high-end packages with up to 30 Mbps speeds offered by the DSL players on a non-homogenous

basis.

As of September 2013, 818 thousand residential customers subscribed to our high and super-high

speed Internet packages, representing 60% of our residential broadband customer base. We believe

that these commercial results position ONO as the market leader in high-speed Internet in Spain.

Data in EUR million, unless otherwise stated 3Q 2013 Results Report

DISCLAIMER: Please see important disclaimer in section 8 of this document

ONO – Third quarter 2013 results (unaudited) - 14

In August 2013 we took a step forward in our strong commitment towards super high speeds. On the

one hand we fully redefined our retail offering to include exclusively super high broadband speeds

packages of 50,100 & 200 Mbps (we continue to marginally sell 20Mbps broadband packages

through the on-line channel for most price sensitive customers). On the other hand, we launched a

loyalty campaign by which we are seeking to migrate existing customers to our new super high speed

product offering either for free or fore a small incremental price.

We expect that as results of the implementation of our renewed strategy we will be able to reverse

the negative trend experienced in our broadband customer numbers in the past quarters and to

achieve future broadband customer growth.

Television

The following table sets forth certain information with respect to ONO’s television services and the

percentage change from period to period:

Television services

(´000) 3Q 13 2Q 13 % change 3Q 12 % change

Services 795 818 (2.8%) 882 (9.9%)

Proportion of total customers 47.7% 48.3% (0.6 pp) 50.1% (2.4 pp)

Penetration 11.1% 11.5% (0.4 pp) 12.5% (1.4 pp)

Fiber television services decreased by 23 thousand as compared to the previous quarter to 795

thousand as of September 30, 2013. We believe this service continues to be impacted by the negative

macroeconomic environment, the significant price increase experienced in football and the VAT

increase which we believe is motivating our most price sensitive customers to drop the service and

switch to “free to air” services in order to preserve their disposable income.

To proactively address the weakness on this service, we are promoting TiVo, a unique product that

has positioned ONO at the forefront of the TV market in Spain. This innovative product, which we

believe is unmatched in Spain, provides our customers with a high quality interactive experience and

a wide variety of content combining 37 HD channels (HD leadership in Spain), 3D functionalities and

broadband connectivity with a powerful and personalized search engine and a PVR (Personal Video

Recorder). We believe these unique functionalities will help us to increase the number of our TV

customers and revenues going forward.

As of September 2013, we had over 259 thousand TiVo services which represent 31% of our TV

customer base. We believe that the TiVo results so far suggest positive market acceptance showcased

by the positive momentum in customer acquisitions, low churn levels and high customer satisfaction

metrics.

With the aim of continuing to improve our pay TV offering, in October 2013 we upgraded our TiVo

product with new functionalities that include an improved user interface, an improved search engine,

the ability to share content between different TiVo boxes within a household and a new energy saving

mode amongst other.

We intend to continue improving our pay TV offering in the near future with the development of new

products and services such as online TV services what we believe will help us to increase the number

of our TV customers and revenues going forward.

Data in EUR million, unless otherwise stated 3Q 2013 Results Report

DISCLAIMER: Please see important disclaimer in section 8 of this document

ONO – Third quarter 2013 results (unaudited) - 15

Telephony

The following table sets forth certain information with respect to ONO’s telephony services and the

percentage change from period to period:

Telephony services

(´000) 3Q 13 2Q 13 % change 3Q 12 % change

Services 1,590 1,611 (1.3%) 1,674 (5.0%)

Proportion of total customers 95.5% 95.2% 0.3 pp 95.1% 0.4 pp

Penetration 22.3% 22.7% (0.4 pp) 23.7% (1.4 pp)

Telephony services decreased by 20 thousand as compared to the previous quarter to 1.6 million as

of September 30, 2013. This service has been impacted by the negative macro and market

environments discussed above that have taken a toll in a portion of our most price sensitive

customers within our base, mainly single play telephony customers that are going “mobile only” to

preserve their disposable incomes.

b) Residential Fixed ADSL and Indirect access

Residential Fixed ADSL includes services offered through full unbundling of the local loop (ULL).

These services provide us with revenues from monthly fees from telephony and broadband Internet

services and usage charges from telephony services.

The following table sets forth information on residential ADSL and Indirect access services and the

percentage change from period to period:

Residential Fixed ADSL and Indirect access

(´000) 3Q 13 2Q 13 % change 3Q 12 % change

Customers 77 81 (4.4%) 97 (20.3%)

Services 136 143 (4.4%) 170 (19.7%)

Services per customer 1.76x 1.76x 0.00x 1.75x 0.01x

Residential Fixed ADSL and Indirect access services decreased by 6 thousand as compared to

previous quarter to reach 136 thousand services as of September 30, 2013. Residential Fixed ADSL

and Indirect access customers also decreased by 4 thousand as compared to previous quarter to

reach 77 thousand customers as of September 30, 2013 mainly due to the industry dynamics and

negative macroeconomic environment discussed above.

3.1.2.2. SoHo fixed services

Revenues from SoHo services are derived from fees paid by small and medium sized enterprises for

fixed and mobile voice and data services, offered individually or as a bundle and from incoming

interconnection revenues within this segment.

SoHo

(´000) 3Q 13 2Q 13 % change 3Q 12 % change

Customers 118 115 3.1% 102 16.0%

Services 236 228 3.4% 198 19.2%

Services per customer 1.99x 1.98x 0.01x 1.93x 0.05x

Revenues (€m) 25 24 5.5% 21 16.4%

SoHo services increased by more than 8 thousand as compared to previous quarter to 236 thousand

services as of September 30, 2013. Our SoHo customer base also performed well and increased by

almost 4 thousand in the quarter to reach 118 thousand customers.

Data in EUR million, unless otherwise stated 3Q 2013 Results Report

DISCLAIMER: Please see important disclaimer in section 8 of this document

ONO – Third quarter 2013 results (unaudited) - 16

These good results were mainly driven by: (i) our strong product offering and competitive price plans

that include broadband speeds of up to 200 Mbps (500 Mbps in the near future), mobile, multi-site

services as well as other value added services (including domain registration, housing, hosting and

cloud computing; (ii) our successful channel mix strategy; (iii) the improvement of our brand

awareness (through brand recognition activities and direct marketing efforts amongst other

initiatives); and (iv) the improvement customer experience and churn levels as result of our improved

multi-skill platforms.

3.1.2.3. Retail mobile services

The following table sets forth certain information with respect to ONO’s retail mobile services and the

percentage change from period to period:

Mobile

(´000) 3Q 13 2Q 13 % change 3Q 12 % change

Mobile services 902 756 19.2% 314 186.9%

Revenues (€m) 35 32 10.1% 13 170.5%

Includes voice and mobile broadband (BAM) of Residential and SoHo

We have managed to increase our mobile services by 145 thousand as compared to previous quarter

and by 587 thousand in the last twelve months to reach 902 thousand services as of September 30,

2013. Revenues increased by 10% compared to the previous quarter and by 2.7x in the first nine

months of 2013 compared to first nine months of last year.

Since mobile is fundamental element in the Spanish telecom market we believe we are extremely well

positioned to take advantage of this market trend. Mobile broadens our ability to deliver superior

value to our customers which in turn leads to incremental revenues. Also mobile is not only a growth

driver, but also a very powerful loyalty and customer satisfaction tool as showcased by the extremely

low churn levels we experience on convergent offers.

In May 2012, we substantially improved our mobile offerings in order to make our mobile products

more appealing to our customers. In September 2012, we began financing handsets as a complement

to our SIM card. In addition, in October 2012, we further redefined our mobile offerings and began

bundling our fixed and mobile products in a single package in order to improve our offerings and

adapt to current market trends and customers' needs. We believe this will help us to further grow our

mobile business over the medium term.

In April 2013, we renewed our MVNO agreement with Telefonica for 2.5 additional years on

satisfactory terms. We believe this agreement enables us to provide a compelling mobile proposition

to our current customers and provides the foundation on which we can continue to grow and improve

our convergent offerings while we work in future solutions to support our growth in mobile.

In August 2013 we further improved our mobile proposition and launched a renewed multi-SIM

mobile package by which customers can subscribe to a 200min/200Mbps product for €5 per month.

We expect this service to continue delivering positive results in the future on the back of our renewed

product offering and to maintain the low churn levels achieved.

Data in EUR million, unless otherwise stated 3Q 2013 Results Report

DISCLAIMER: Please see important disclaimer in section 8 of this document

ONO – Third quarter 2013 results (unaudited) - 17

3.1.3. Business services

3.1.3.1. Wholesale

Revenues from the wholesale business unit are derived from carrier services, voice traffic services,

leased and dedicated lines and ISP solutions, provided to other telecommunications operators and

from the provision of intelligent network services.

Wholesale

EUR million 3Q 13 3Q 12 % change 9M 13 9M 12 % change

Revenues 59 60 (0.6%) 192 148 29.5%

Wholesale revenues remained broadly stable as compared to the previous quarter reaching €59

million as a result of our decision to limit top line growth of this segment to focus in margin

improvement

The strong performance experienced in this segment in the past quarters is the result of a carefully

planned set of initiatives launched in the last two years to boost voice services revenues. In 2010, we

laid the foundations for growth by setting up a VoIP platform to help us manage prepaid services,

implementing a LCR tool (Least-Cost Routing) and reengineering the whole delivery process to make

it more efficient and faster. Since 2011, we added new IP traffic termination providers to improve our

commercial offer and we strengthened the team by hiring an experienced sales representative and a

routing manager.

Going forward we expect to continue growing our wholesale business albeit at a slower pace while we

seek to increase the margin contribution of this business segment.

3.1.3.2. Large Accounts and Corporations

Revenues within the Large Accounts and Corporations business segment are derived from

customized solutions designed to satisfy the communication needs (voice, Internet, data solutions

and equipment) of large corporate groups, institutions and central and autonomous government

agencies, through an integrated range of tailored services.

The following table sets forth revenues from the Large Accounts and Corporations segment and the

percentage change from period to period:

Large Accounts and Corporations

EUR million 3Q 13 3Q 12 % change 9M 13 9M 12 % change

Revenues 27 29 (9.3%) 83 91 (9.0%)

Large Accounts and Corporations revenues decreased by 9.3% as compared to previous quarters to

€27 million as a result of continued contracts renegotiations prompted by the economic downturn,

coupled with Telefónica’s aggressive commercial approach have continued to negatively impact this

business segment.

Data in EUR million, unless otherwise stated 3Q 2013 Results Report

DISCLAIMER: Please see important disclaimer in section 8 of this document

ONO – Third quarter 2013 results (unaudited) - 18

3.1.4. Cost of sales and Gross profit

The following table sets forth ONO's gross profit and the percentage change for the periods

indicated:

Cost of sales and Gross Profit

EUR million 3Q 13 3Q 12 % change 9M 13 9M 12 % change

Total net revenues 384 392 (2.0%) 1,183 1,164 1.7%

Cost of sales (120) (110) 9.6% (369) (303) 21.6%

PPA (1) (2) (69.5%) (2) (7) (69.5%)

Gross profit (1)

263 280 (6.0%) 812 854 (4.8%)

Gross margin 68.5% 71.4% (2.9 pp) 68.6% 73.3% (4.7 pp)

(1)

Adjusted for the PPA provision

Cost of sales principally consists of interconnection and backbone network costs for

telecommunications services, Internet connectivity costs, circuit rental expenses and programming

costs for fiber television services.

Interconnection costs for telephony services are generated by calls made by our customers that

terminate outside our network. Internet connectivity costs mainly consist of fees for the bandwidth

used for our Internet transit outside of Spain. Fiber television programming fees consist primarily of

fees paid to television content owners to distribute their fiber television content and fees paid to

distribute movies and football on a pay-per-view basis.

Our cost of sales increased by 9.6% as compared to the same quarter of 2012 to €120 million as a

consequence of increased interconnection costs related with our wholesale activity as well as costs

related with our growing mobile business.

3.1.5. Operating expenses (“Opex”)

The following table sets forth ONO's Opex and the percentage change from period to period for each

of the periods indicated:

Operating expenses

EUR million 3Q 13 3Q 12 % change 9M 13 9M 12 % change

Gross opex (105) (107) (2.3%) (326) (340) (4.1%)

PPA (1) (5) (84.7%) (2) (14) (84.7%)

Capitalised costs 13 14 (11.9%) 40 44 (8.4%)

Net opex (1)

(93) (97) (4.7%) (288) (309) (7.1%)

% of revenues 24.1% 24.8% (0.7 pp) 24.3% 26.6% (2.3 pp)

(1)

Adjusted for the PPA provision

Gross opex consists principally of expenses related to wages and salaries and other operating

expenses, including professional services, marketing and selling expenses, network operation and

maintenance, information systems, administrative overhead and billing costs. Capitalized costs relate

to, inter alia, direct labour costs associated with the development and upgrade of our network and

the installations carried out at customer premises.

Our net operating expenses decreased by 4.7% as compared to the same quarter of 2012 to €93

million.

Improving our cost structure and our efficiency is a key priority for the company. We believe this is

helping us to support our profitability and adapt to the challenging economic environment. This crisis

is creating opportunities to introduce greater flexibility in our cost structures and we are taking

advantage of these opportunities by being more selective both internally and externally to adjust to

the downward pressures on our margins.

Data in EUR million, unless otherwise stated 3Q 2013 Results Report

DISCLAIMER: Please see important disclaimer in section 8 of this document

ONO – Third quarter 2013 results (unaudited) - 19

During the year, our strict cost control policies coupled with continuous optimization and

transformation initiatives have led to sustained Opex savings across the entire organization despite

the increased price pressures resulting from higher CPI levels.

Examples of the initiatives that we have implemented so far include: (i) renegotiation of our collective

bargaining agreement in order to link salaries evolution to the profitability of the business; (ii)

increase the number of sales through our most cost efficient channels (on-line); (iii) improving

network maintenance and fault resolution to reduce costs; and (iv) building optimization.

Although we have made noticeable the progress made so far we believe that there is a lot more to do

in the next quarters to make our business more efficient, resilient and capable of withstanding the

hostile environment in which we operate. We have identified two levers to continue improving our

cost structure and that we believe will help us to take it from good to best in class: (i) Fully digitalize

customer life cycle through the development of a full eServices functionality and the improvement of

our eCare and eSales platforms; and (ii) maximize process efficiency through optimization initiatives

(building optimizations, contract renegotiations, improving call center business metrics, reducing

field repairs and increasing self-installation amongst other initiatives) and organizational

optimizations.

3.1.6. EBITDA

The following table sets forth ONO's EBITDA and the percentage change from period to period for

each of the periods indicated:

EBITDA and EBITDA Normalized

EUR million 3Q 13 3Q 12 % change 9M 13 9M 12 % change

Net Revenues 384 392 (2.0%) 1,183 1,164 1.7%

Cost of sales (121) (112) 7.9% (371) (310) 19.6%

Net opex (93) (97) (4.7%) (288) (309) (7.1%)

Normalized EBITDA 170 182 (6.7%) 525 544 (3.6%)

Normalized EBITDA margin 44.4% 46.6% (2.2 pp) 44.3% 46.8% (2.4 pp)

PPA Adjustment 1.39 6.82 (79.6%) 4.18 20.46 (79.6%)

EBITDA 172 189 (9.3%) 529 565 (6.3%)

EBITDA margin 44.8% 48.3% (3.6 pp) 44.7% 48.5% (3.8 pp)

Normalized EBITDA (EBITDA adjusted for the PPA provision) decreased by 6.7% as in the quarter to

reach €170 million and reported EBITDA decreased 9.3% this quarter to reach €172 million as results

of the challenging macro and industry environments described before.

The PPA provision is a non-cash adjustment that relates to the release of onerous contract provisions

which arose on the acquisition of Auna. In 2005, the realizable value of the Auna net assets acquired

exceeded the acquisition price. In writing down the value of book assets acquired in line with the

acquisition price, a provision was recorded on the balance sheet. This amount was assigned to the

network maintenance and rental contracts acquired with Auna as these contracts were deemed to be

stuck at a higher value than market.

In the period 2006-2012, we took the following accounting approach attending to the relevant

accounting rules in place:

– Profit & Loss Statement: PPA provision was applied from 2006 to 2012 as a contra expense

within Cost of sales and Opex thereby benefiting reporting EBITDA.

– Cash Flow Statement: Payments of the onerous contracts were recorded under the “other” line

of the cash flow in order to arrive to FCF.

Although we utilized the majority of the PPA provision in the period 2006-2012, approximately €1.4

million has yet to be used in 2013 (the PPA impact was €27 million in 2012).

Data in EUR million, unless otherwise stated 3Q 2013 Results Report

DISCLAIMER: Please see important disclaimer in section 8 of this document

ONO – Third quarter 2013 results (unaudited) - 20

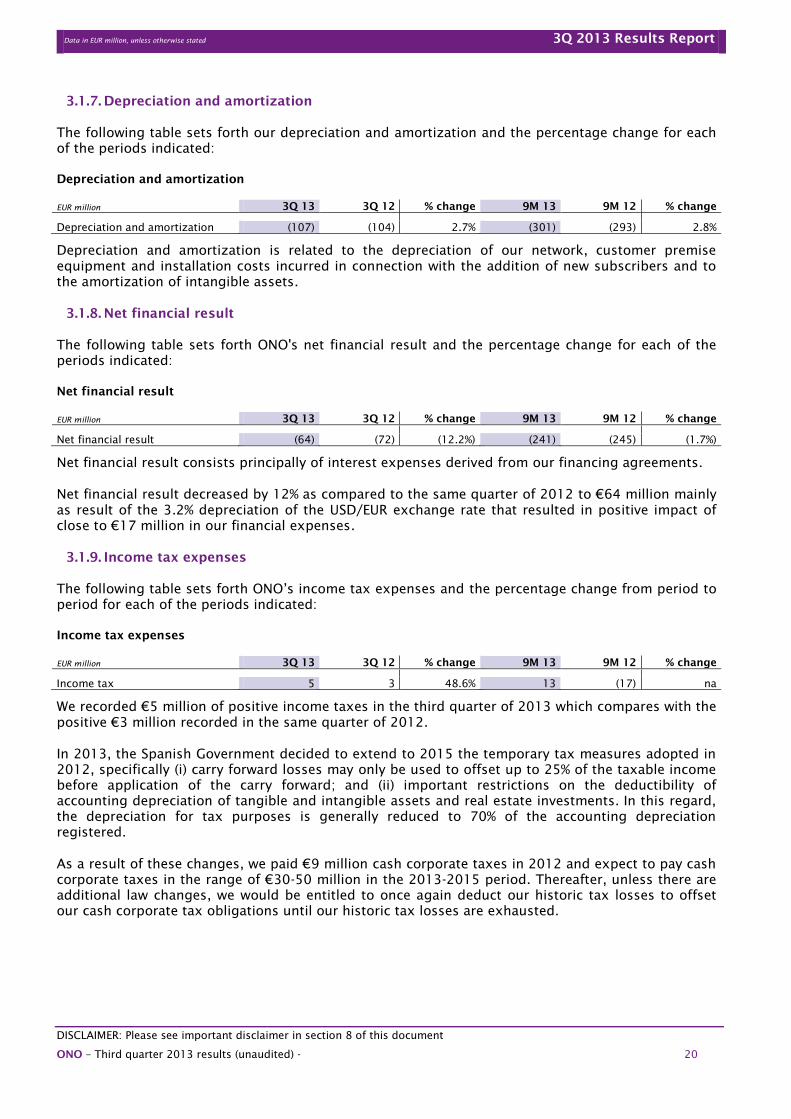

3.1.7. Depreciation and amortization

The following table sets forth our depreciation and amortization and the percentage change for each

of the periods indicated:

Depreciation and amortization

EUR million 3Q 13 3Q 12 % change 9M 13 9M 12 % change

Depreciation and amortization (107) (104) 2.7% (301) (293) 2.8%

Depreciation and amortization is related to the depreciation of our network, customer premise

equipment and installation costs incurred in connection with the addition of new subscribers and to

the amortization of intangible assets.

3.1.8. Net financial result

The following table sets forth ONO's net financial result and the percentage change for each of the

periods indicated:

Net financial result

EUR million 3Q 13 3Q 12 % change 9M 13 9M 12 % change

Net financial result (64) (72) (12.2%) (241) (245) (1.7%)

Net financial result consists principally of interest expenses derived from our financing agreements.

Net financial result decreased by 12% as compared to the same quarter of 2012 to €64 million mainly

as result of the 3.2% depreciation of the USD/EUR exchange rate that resulted in positive impact of

close to €17 million in our financial expenses.

3.1.9. Income tax expenses

The following table sets forth ONO’s income tax expenses and the percentage change from period to

period for each of the periods indicated:

Income tax expenses

EUR million 3Q 13 3Q 12 % change 9M 13 9M 12 % change

Income tax 5 3 48.6% 13 (17) na

We recorded €5 million of positive income taxes in the third quarter of 2013 which compares with the

positive €3 million recorded in the same quarter of 2012.

In 2013, the Spanish Government decided to extend to 2015 the temporary tax measures adopted in

2012, specifically (i) carry forward losses may only be used to offset up to 25% of the taxable income

before application of the carry forward; and (ii) important restrictions on the deductibility of

accounting depreciation of tangible and intangible assets and real estate investments. In this regard,

the depreciation for tax purposes is generally reduced to 70% of the accounting depreciation

registered.

As a result of these changes, we paid €9 million cash corporate taxes in 2012 and expect to pay cash

corporate taxes in the range of €30-50 million in the 2013-2015 period. Thereafter, unless there are

additional law changes, we would be entitled to once again deduct our historic tax losses to offset

our cash corporate tax obligations until our historic tax losses are exhausted.

Data in EUR million, unless otherwise stated 3Q 2013 Results Report

DISCLAIMER: Please see important disclaimer in section 8 of this document

ONO – Third quarter 2013 results (unaudited) - 21

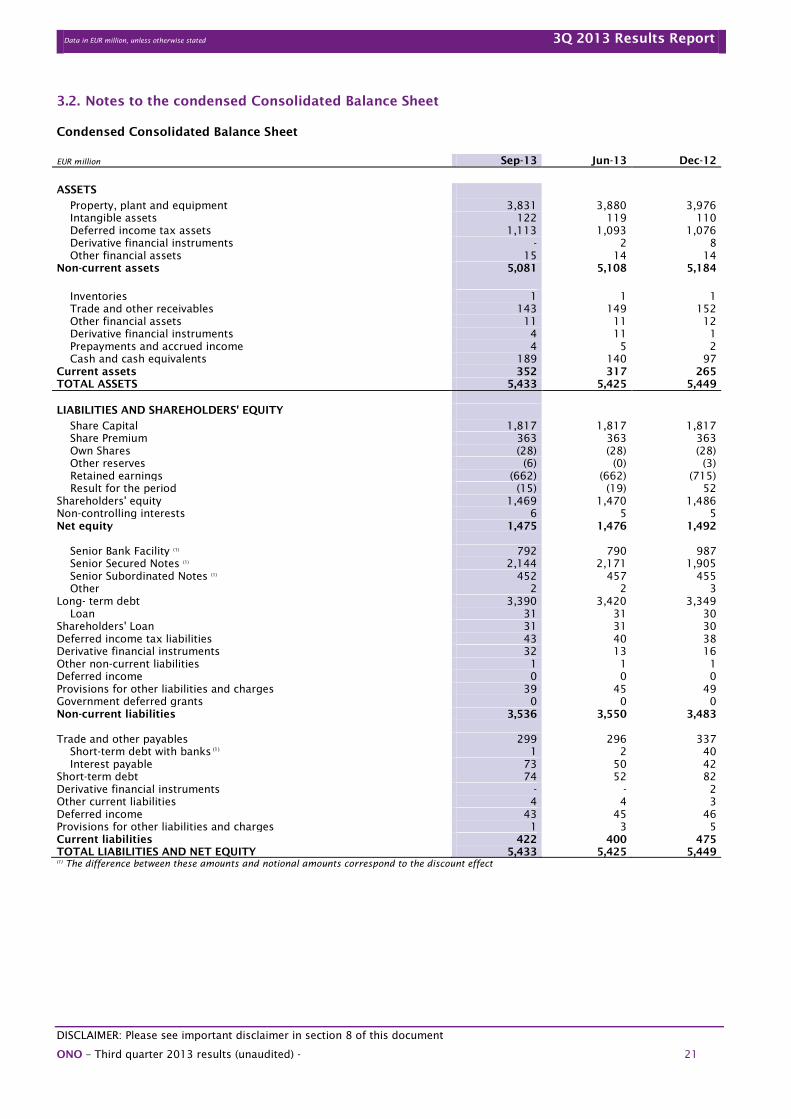

3.2. Notes to the condensed Consolidated Balance Sheet

Condensed Consolidated Balance Sheet

EUR million Sep-13 Jun-13 Dec-12

ASSETS

Property, plant and equipment 3,831 3,880 3,976

Intangible assets 122 119 110

Deferred income tax assets 1,113 1,093 1,076

Derivative financial instruments - 2 8

Other financial assets 15 14 14

Non-current assets 5,081 5,108 5,184

Inventories 1 1 1

Trade and other receivables 143 149 152

Other financial assets 11 11 12

Derivative financial instruments 4 11 1

Prepayments and accrued income 4 5 2

Cash and cash equivalents 189 140 97

Current assets 352 317 265

TOTAL ASSETS 5,433 5,425 5,449

LIABILITIES AND SHAREHOLDERS' EQUITY

Share Capital 1,817 1,817 1,817

Share Premium 363 363 363

Own Shares (28) (28) (28)

Other reserves (6) (0) (3)

Retained earnings (662) (662) (715)

Result for the period (15) (19) 52

Shareholders' equity 1,469 1,470 1,486

Non-controlling interests 6 5 5

Net equity 1,475 1,476 1,492

Senior Bank Facility (1)

792 790 987

Senior Secured Notes (1)

2,144 2,171 1,905

Senior Subordinated Notes (1)

452 457 455

Other

2 2 3

Long- term debt 3,390 3,420 3,349

Loan 31 31 30

Shareholders' Loan 31 31 30

Deferred income tax liabilities 43 40 38

Derivative financial instruments 32 13 16

Other non-current liabilities 1 1 1

Deferred income 0 0 0

Provisions for other liabilities and charges 39 45 49

Government deferred grants 0 0 0

Non-current liabilities 3,536 3,550 3,483

Trade and other payables 299 296 337

Short-term debt with banks (1)

1 2 40

Interest payable

73 50 42

Short-term debt 74 52 82

Derivative financial instruments - - 2

Other current liabilities 4 4 3

Deferred income 43 45 46

Provisions for other liabilities and charges 1 3 5

Current liabilities 422 400 475

TOTAL LIABILITIES AND NET EQUITY 5,433 5,425 5,449

(1)

The difference between these amounts and notional amounts correspond to the discount effect

Data in EUR million, unless otherwise stated 3Q 2013 Results Report

DISCLAIMER: Please see important disclaimer in section 8 of this document

ONO – Third quarter 2013 results (unaudited) - 22

Shareholders’ equity

EUR million

Share

Capital

Share

premium

Own

shares

Other

reserves

Retained

earnings

Result

for the

period

Non-

controlling

interests

Total

Balance Dec 31, 2012 1,817 363 (28) (3) (715) 52 5 1,492

Previous year result

distribution - - - - 52 (52) - -

Net loss for the period - - - - - (15) - (15)

Change in fair value (2) (2)

Transfer to income

statements 0 0

Balance Sep 30, 2013 1,817 363 (28) (6) (662) (15) 6 1,475

Debt and liquidity

As of 30 sep 2013. EUR million

Maximum

available

Short term

debt

Long term

debt Total debt Availability

Debt with credit entities:

Senior Facility 924 - 824 824 100

Senior Secured Notes 2,230 - 2,230 2,230 -

Other credit facilities 3 1 0 1 3

Total debt with credit entities 3,157 1 3,054 3,055 103

Other debt:

Senior subordinated notes 462 - 462 462 -

State subsidies 3 0 2 3 -

Total other debt 464 0 464 464 -

Total debt 3,622 1 3,518 3,519 103

Cash and cash equivalents 189 189

Total net debt 3,330 291

EBITDA LTM 716

Total net debt/EBITDA LTM 4.65x

Debt by maturity (amounts drawn)

EUR million

2013 2014 2015 2016 2017 2018 2019 ≥2020 Total

Debt with credit entities:

Term Loan A (“TLA”) - - - 238 401 - - - 639

Term Loan B (“TLB”) - - - - - 185 - - 185

Revolving Credit Facility (“RCF”)(1)

- - - - - - - - -

Tranche SPV 1 - - - - - 700 - - 700

Tranche SPV 2 - - - - - 300 - - 300

Tranche SPV 3 - - - - - 741 - - 741

Tranche SPV 4 - - - - - 230 - - 230

Tranche SPV 5 - - - - - - - 260 260

Total Senior Facility - - - 238 401 2,155 - 260 3,054

Senior Subordinated Notes - - - - - - 462 - 462

Other credit facilities 0 1 0 0 0 0 0 1 3

Total gross debt 0 1 0 239 401 2,155 462 261 3,519

(1)

€100 million of RCF available but not drawn.

Note: (1) The difference between these amounts and notional amounts correspond to the discount effect

Our liquidity requirements arise primarily to meet our on-going debt service obligations and to fund

working capital and capital expenditure requirements. Our principal sources of funds have been cash

flow from operations, cash and cash equivalents on our balance sheet, borrowings under our credit

facilities and borrowings under other financing agreements.

As of September 30, 2013 we had €189 million of cash and cash equivalents and €103 million

available lines under undrawn credit facilities (including the €100 million Revolving Facility under the

New Senior Bank Facility Agreement), for a total liquidity of €292 million.

Data in EUR million, unless otherwise stated 3Q 2013 Results Report

DISCLAIMER: Please see important disclaimer in section 8 of this document

ONO – Third quarter 2013 results (unaudited) - 23

As a result of our refinancing process completed in June 2012 and the issuance of the €260 million

Senior Secured Notes in February 2013, the maturity profile of our debt has been significantly

improved and currently we have no relevant debt maturities before 2017.

We expect the maturities of the Bank Tranches of our Senior Facility (Term Loan A, Term Loan B and

RCF (if drawn)) to be met through available cash and cash equivalents and operating cash flow.

However, we expect that we will be required to refinance a substantial portion of the indebtedness

under the Notes Tranches of the New Senior Facility on or before their maturity in 2018.

We may incur additional indebtedness in the future principally to fund our interest expenses, working

capital needs and, to the extent not covered by operating cash flows, capital expenditures. Any

drawings under the New Senior Bank Facility Agreement are subject to the satisfaction of certain

conditions precedent and compliance with covenants, including the maintenance of certain ratios.

In order to reduce interest expense in the future, we may elect to use available cash to repay debt or

purchase our bonds in the market from time to time.

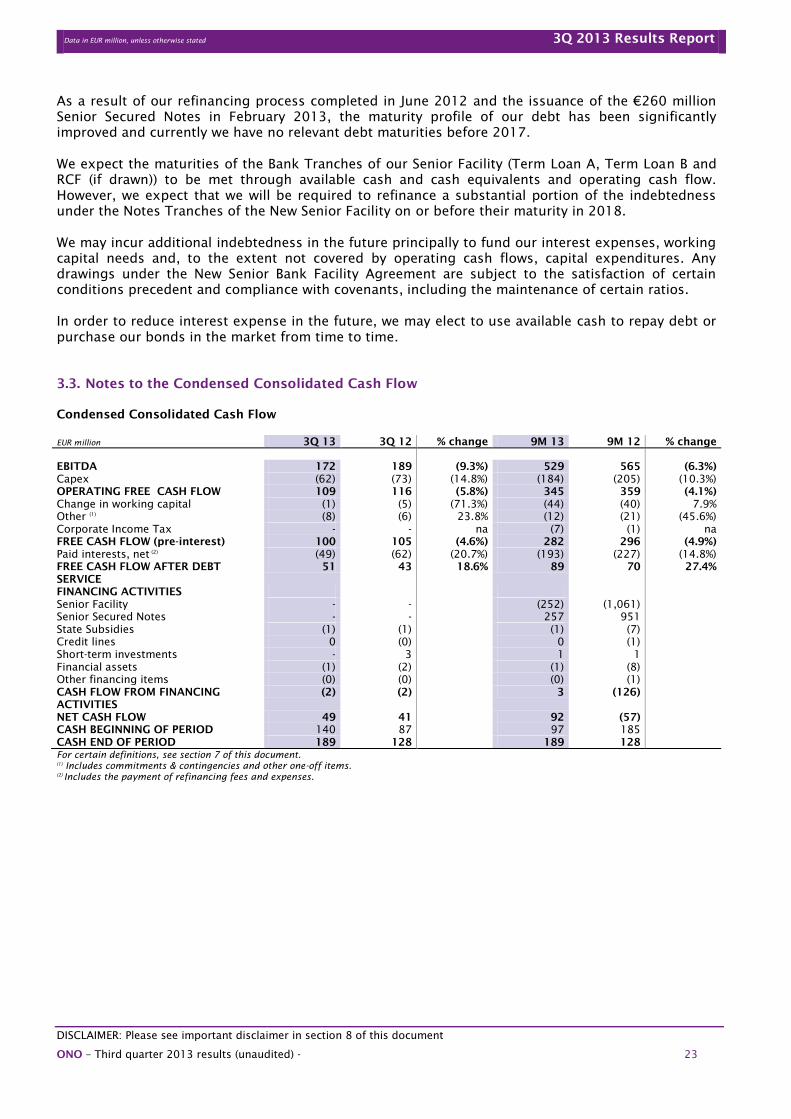

3.3. Notes to the Condensed Consolidated Cash Flow

Condensed Consolidated Cash Flow

EUR million 3Q 13 3Q 12 % change 9M 13 9M 12 % change

EBITDA 172 189 (9.3%) 529 565 (6.3%)

Capex (62) (73) (14.8%) (184) (205) (10.3%)

OPERATING FREE CASH FLOW 109 116 (5.8%) 345 359 (4.1%)

Change in working capital (1) (5) (71.3%) (44) (40) 7.9%

Other (1)

(8) (6) 23.8% (12) (21) (45.6%)

Corporate Income Tax - - na (7) (1) na

FREE CASH FLOW (pre-interest) 100 105 (4.6%) 282 296 (4.9%)

Paid interests, net (2)

(49) (62) (20.7%) (193) (227) (14.8%)

FREE CASH FLOW AFTER DEBT

SERVICE

51 43 18.6% 89 70 27.4%

FINANCING ACTIVITIES

Senior Facility - - (252) (1,061)

Senior Secured Notes - - 257 951

State Subsidies (1) (1) (1) (7)

Credit lines 0 (0) 0 (1)

Short-term investments - 3 1 1

Financial assets (1) (2) (1) (8)

Other financing items (0) (0) (0) (1)

CASH FLOW FROM FINANCING

ACTIVITIES

(2) (2) 3 (126)

NET CASH FLOW 49 41 92 (57)

CASH BEGINNING OF PERIOD 140 87 97 185

CASH END OF PERIOD 189 128 189 128

For certain definitions, see section 7 of this document.

(1)

Includes commitments & contingencies and other one-off items.

(2)

Includes the payment of refinancing fees and expenses.

Data in EUR million, unless otherwise stated 3Q 2013 Results Report

DISCLAIMER: Please see important disclaimer in section 8 of this document

ONO – Third quarter 2013 results (unaudited) - 24

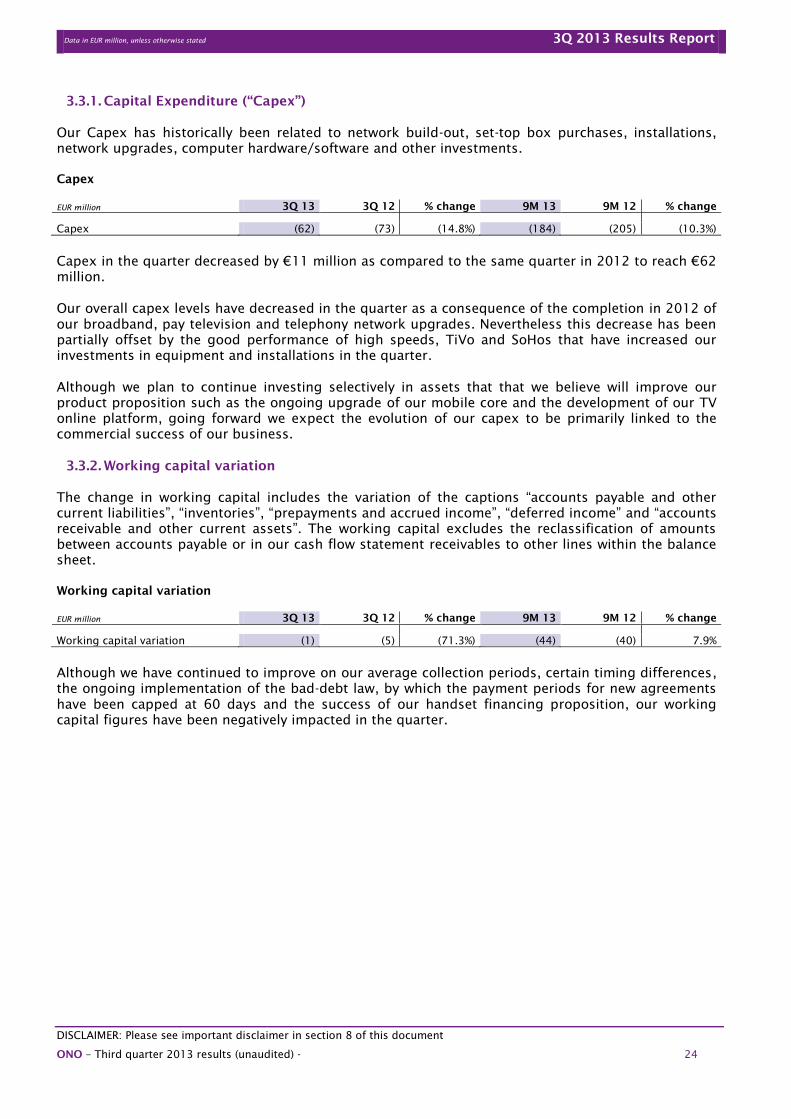

3.3.1. Capital Expenditure (“Capex”)

Our Capex has historically been related to network build-out, set-top box purchases, installations,

network upgrades, computer hardware/software and other investments.

Capex

EUR million 3Q 13 3Q 12 % change 9M 13 9M 12 % change

Capex (62) (73) (14.8%) (184) (205) (10.3%)

Capex in the quarter decreased by €11 million as compared to the same quarter in 2012 to reach €62

million.

Our overall capex levels have decreased in the quarter as a consequence of the completion in 2012 of

our broadband, pay television and telephony network upgrades. Nevertheless this decrease has been

partially offset by the good performance of high speeds, TiVo and SoHos that have increased our

investments in equipment and installations in the quarter.

Although we plan to continue investing selectively in assets that that we believe will improve our

product proposition such as the ongoing upgrade of our mobile core and the development of our TV

online platform, going forward we expect the evolution of our capex to be primarily linked to the

commercial success of our business.

3.3.2. Working capital variation

The change in working capital includes the variation of the captions “accounts payable and other

current liabilities”, “inventories”, “prepayments and accrued income”, “deferred income” and “accounts

receivable and other current assets”. The working capital excludes the reclassification of amounts

between accounts payable or in our cash flow statement receivables to other lines within the balance

sheet.

Working capital variation

EUR million 3Q 13 3Q 12 % change 9M 13 9M 12 % change

Working capital variation (1) (5) (71.3%) (44) (40) 7.9%

Although we have continued to improve on our average collection periods, certain timing differences,

the ongoing implementation of the bad-debt law, by which the payment periods for new agreements

have been capped at 60 days and the success of our handset financing proposition, our working

capital figures have been negatively impacted in the quarter.

Data in EUR million, unless otherwise stated 3Q 2013 Results Report

DISCLAIMER: Please see important disclaimer in section 8 of this document

ONO – Third quarter 2013 results (unaudited) - 25

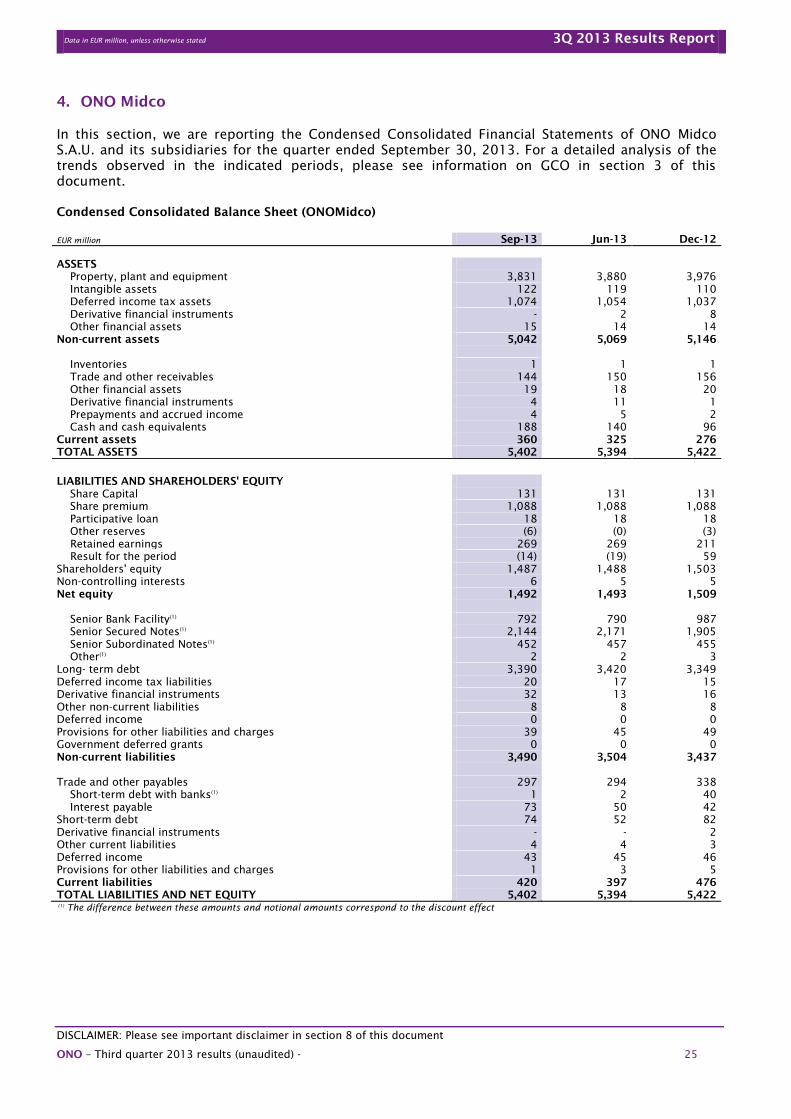

4. ONO Midco

In this section, we are reporting the Condensed Consolidated Financial Statements of ONO Midco

S.A.U. and its subsidiaries for the quarter ended September 30, 2013. For a detailed analysis of the

trends observed in the indicated periods, please see information on GCO in section 3 of this

document.

Condensed Consolidated Balance Sheet (ONOMidco)

EUR million Sep-13 Jun-13 Dec-12

ASSETS

Property, plant and equipment 3,831 3,880 3,976

Intangible assets 122 119 110

Deferred income tax assets 1,074 1,054 1,037

Derivative financial instruments - 2 8

Other financial assets 15 14 14

Non-current assets 5,042 5,069 5,146

Inventories 1 1 1

Trade and other receivables 144 150 156

Other financial assets 19 18 20

Derivative financial instruments 4 11 1

Prepayments and accrued income 4 5 2

Cash and cash equivalents 188 140 96

Current assets 360 325 276

TOTAL ASSETS 5,402 5,394 5,422

LIABILITIES AND SHAREHOLDERS' EQUITY

Share Capital 131 131 131

Share premium 1,088 1,088 1,088

Participative loan 18 18 18

Other reserves (6) (0) (3)

Retained earnings 269 269 211

Result for the period (14) (19) 59

Shareholders' equity 1,487 1,488 1,503

Non-controlling interests 6 5 5

Net equity 1,492 1,493 1,509

Senior Bank Facility(1)

792 790 987

Senior Secured Notes(1)

2,144 2,171 1,905

Senior Subordinated Notes(1)

452 457 455

Other(1)

2 2 3

Long- term debt 3,390 3,420 3,349

Deferred income tax liabilities 20 17 15

Derivative financial instruments 32 13 16

Other non-current liabilities 8 8 8

Deferred income 0 0 0

Provisions for other liabilities and charges 39 45 49

Government deferred grants 0 0 0

Non-current liabilities 3,490 3,504 3,437

Trade and other payables 297 294 338

Short-term debt with banks(1)

1 2 40

Interest payable 73 50 42

Short-term debt 74 52 82

Derivative financial instruments - - 2

Other current liabilities 4 4 3

Deferred income 43 45 46

Provisions for other liabilities and charges 1 3 5

Current liabilities 420 397 476

TOTAL LIABILITIES AND NET EQUITY 5,402 5,394 5,422

(1)

The difference between these amounts and notional amounts correspond to the discount effect

Data in EUR million, unless otherwise stated 3Q 2013 Results Report

DISCLAIMER: Please see important disclaimer in section 8 of this document

ONO – Third quarter 2013 results (unaudited) - 26

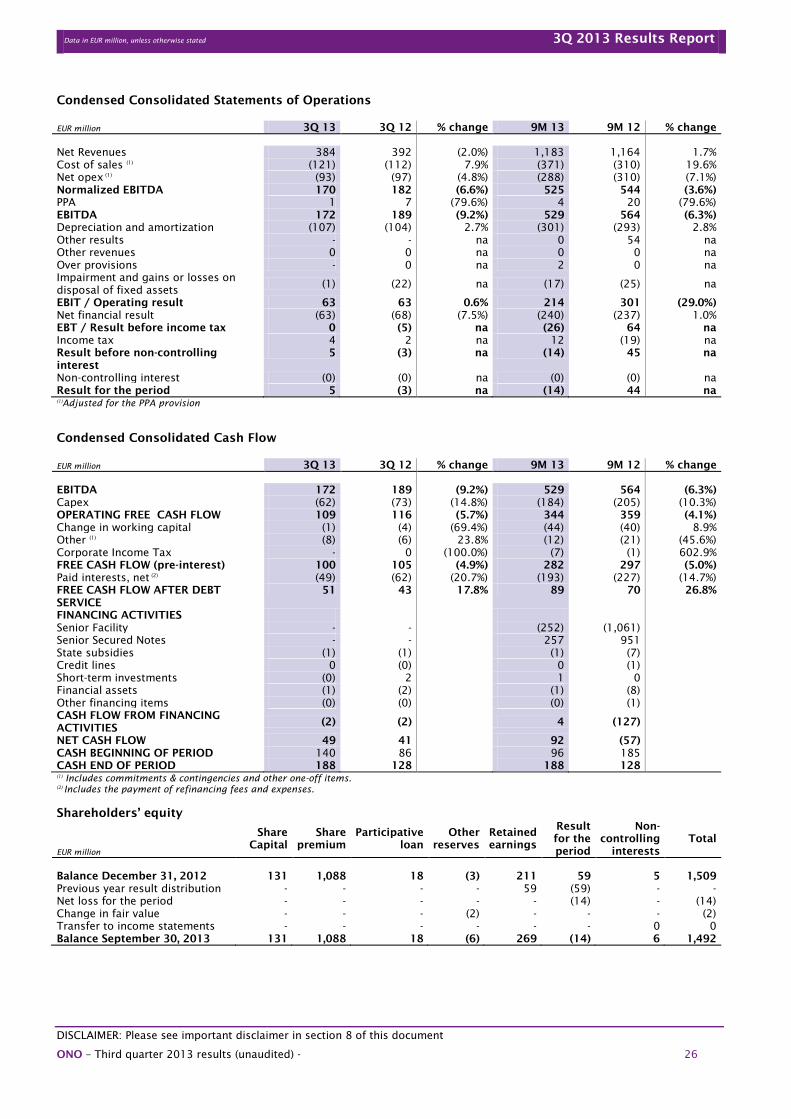

Condensed Consolidated Statements of Operations

EUR million 3Q 13 3Q 12 % change 9M 13 9M 12 % change

Net Revenues 384 392 (2.0%) 1,183 1,164 1.7%

Cost of sales (1)

(121) (112) 7.9% (371) (310) 19.6%

Net opex (1)

(93) (97) (4.8%) (288) (310) (7.1%)

Normalized EBITDA 170 182 (6.6%) 525 544 (3.6%)

PPA 1 7 (79.6%) 4 20 (79.6%)

EBITDA 172 189 (9.2%) 529 564 (6.3%)

Depreciation and amortization (107) (104) 2.7% (301) (293) 2.8%

Other results - - na 0 54 na

Other revenues 0 0 na 0 0 na

Over provisions - 0 na 2 0 na

Impairment and gains or losses on

disposal of fixed assets (1) (22) na (17) (25) na

EBIT / Operating result 63 63 0.6% 214 301 (29.0%)

Net financial result (63) (68) (7.5%) (240) (237) 1.0%

EBT / Result before income tax 0 (5) na (26) 64 na

Income tax 4 2 na 12 (19) na

Result before non-controlling

interest

5 (3) na (14) 45 na

Non-controlling interest (0) (0) na (0) (0) na

Result for the period 5 (3) na (14) 44 na

(1)

Adjusted for the PPA provision

Condensed Consolidated Cash Flow

EUR million 3Q 13 3Q 12 % change 9M 13 9M 12 % change

EBITDA 172 189 (9.2%) 529 564 (6.3%)

Capex (62) (73) (14.8%) (184) (205) (10.3%)

OPERATING FREE CASH FLOW 109 116 (5.7%) 344 359 (4.1%)

Change in working capital (1) (4) (69.4%) (44) (40) 8.9%

Other (1)

(8) (6) 23.8% (12) (21) (45.6%)

Corporate Income Tax - 0 (100.0%) (7) (1) 602.9%

FREE CASH FLOW (pre-interest) 100 105 (4.9%) 282 297 (5.0%)

Paid interests, net (2)

(49) (62) (20.7%) (193) (227) (14.7%)

FREE CASH FLOW AFTER DEBT

SERVICE

51 43 17.8% 89 70 26.8%

FINANCING ACTIVITIES

Senior Facility - - (252) (1,061)

Senior Secured Notes - - 257 951

State subsidies (1) (1) (1) (7)

Credit lines 0 (0) 0 (1)

Short-term investments (0) 2 1 0

Financial assets (1) (2) (1) (8)

Other financing items (0) (0) (0) (1)

CASH FLOW FROM FINANCING

ACTIVITIES (2) (2) 4 (127)

NET CASH FLOW 49 41 92 (57)

CASH BEGINNING OF PERIOD 140 86 96 185

CASH END OF PERIOD 188 128 188 128

(1)

Includes commitments & contingencies and other one-off items.

(2)

Includes the payment of refinancing fees and expenses.

Shareholders’ equity

EUR million

Share

Capital

Share

premium

Participative

loan

Other

reserves

Retained

earnings

Result

for the

period

Non-

controlling

interests

Total

Balance December 31, 2012 131 1,088 18 (3) 211 59 5 1,509

Previous year result distribution - - - - 59 (59) - -

Net loss for the period - - - - - (14) - (14)

Change in fair value - - - (2) - - - (2)

Transfer to income statements - - - - - - 0 0

Balance September 30, 2013 131 1,088 18 (6) 269 (14) 6 1,492

Data in EUR million, unless otherwise stated 3Q 2013 Results Report

DISCLAIMER: Please see important disclaimer in section 8 of this document

ONO – Third quarter 2013 results (unaudited) - 27

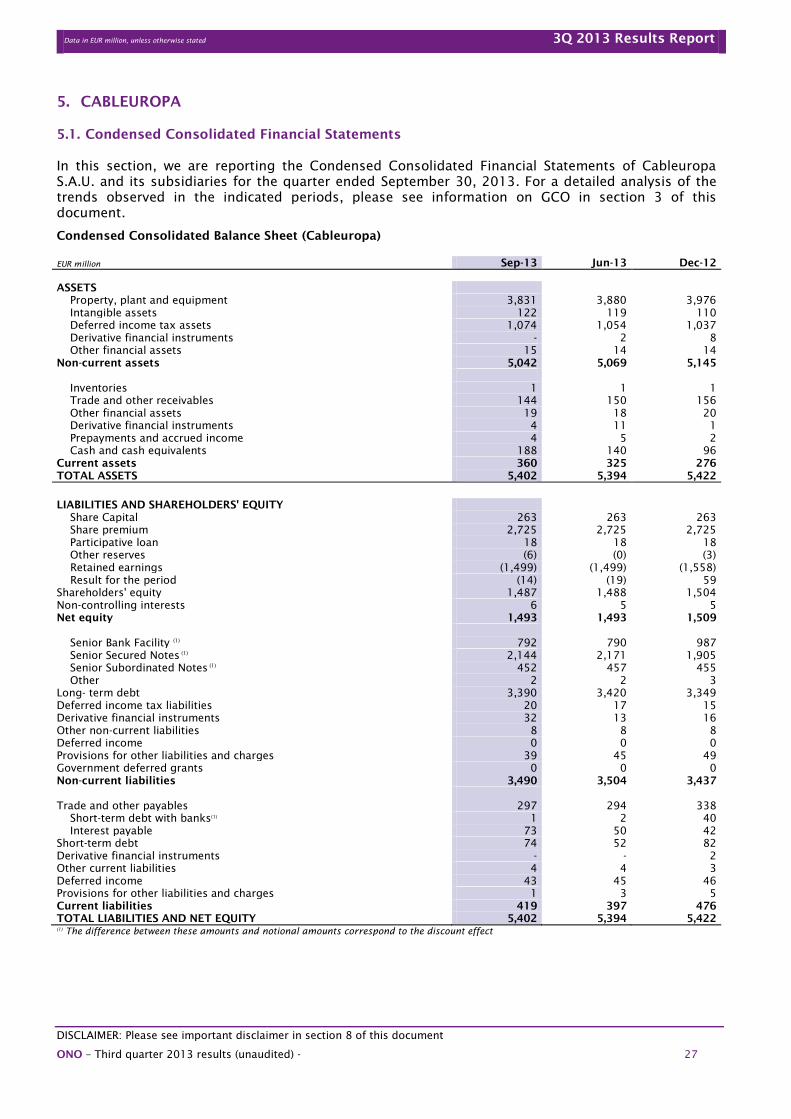

5. CABLEUROPA

5.1. Condensed Consolidated Financial Statements

In this section, we are reporting the Condensed Consolidated Financial Statements of Cableuropa

S.A.U. and its subsidiaries for the quarter ended September 30, 2013. For a detailed analysis of the

trends observed in the indicated periods, please see information on GCO in section 3 of this

document.

Condensed Consolidated Balance Sheet (Cableuropa)

EUR million Sep-13 Jun-13 Dec-12

ASSETS

Property, plant and equipment 3,831 3,880 3,976

Intangible assets 122 119 110

Deferred income tax assets 1,074 1,054 1,037

Derivative financial instruments - 2 8

Other financial assets 15 14 14

Non-current assets 5,042 5,069 5,145

Inventories 1 1 1

Trade and other receivables 144 150 156

Other financial assets 19 18 20

Derivative financial instruments 4 11 1

Prepayments and accrued income 4 5 2

Cash and cash equivalents 188 140 96

Current assets 360 325 276

TOTAL ASSETS 5,402 5,394 5,422

LIABILITIES AND SHAREHOLDERS' EQUITY

Share Capital 263 263 263

Share premium 2,725 2,725 2,725

Participative loan 18 18 18

Other reserves (6) (0) (3)

Retained earnings (1,499) (1,499) (1,558)

Result for the period (14) (19) 59

Shareholders' equity 1,487 1,488 1,504

Non-controlling interests 6 5 5

Net equity 1,493 1,493 1,509

Senior Bank Facility (1)

792 790 987

Senior Secured Notes (1)

2,144 2,171 1,905

Senior Subordinated Notes (1)

452 457 455

Other 2 2 3

Long- term debt 3,390 3,420 3,349

Deferred income tax liabilities 20 17 15

Derivative financial instruments 32 13 16

Other non-current liabilities 8 8 8

Deferred income 0 0 0

Provisions for other liabilities and charges 39 45 49

Government deferred grants 0 0 0

Non-current liabilities 3,490 3,504 3,437

Trade and other payables 297 294 338

Short-term debt with banks(1)

1 2 40

Interest payable 73 50 42

Short-term debt 74 52 82

Derivative financial instruments - - 2

Other current liabilities 4 4 3

Deferred income 43 45 46

Provisions for other liabilities and charges 1 3 5

Current liabilities 419 397 476

TOTAL LIABILITIES AND NET EQUITY 5,402 5,394 5,422

(1)

The difference between these amounts and notional amounts correspond to the discount effect

Data in EUR million, unless otherwise stated 3Q 2013 Results Report

DISCLAIMER: Please see important disclaimer in section 8 of this document

ONO – Third quarter 2013 results (unaudited) - 28

Condensed Consolidated Statements of Operations

EUR million 3Q 13 3Q 12 % change 9M 13 9M 12 % change

Net Revenues 384 392 (2.0%) 1,183 1,164 1.7%

Cost of sales (1)

(121) (112) 7.9% (371) (310) 19.6%

Net opex (1)

(93) (97) (4.8%) (288) (310) (7.1%)

Normalized EBITDA 170 182 (6.6%) 525 544 (3.6%)

PPA 1 7 (79.6%) 4 20 (79.6%)

EBITDA 172 189 (9.2%) 529 564 (6.3%)

Depreciation and amortization (107) (104) 2.7% (301) (293) 2.8%

Other results - - na 0 54 na

Other revenues 0 0 na 0 0 na