Embed Size (px)

DESCRIPTION

Metso's Interim Review January 1 - March 31, 2014. Presentation. Read more: www.metso.com/investors

Citation preview

Matti Kähkönen, President and CEO Harri Nikunen, CFO

April 24, 2014

© Metso © Metso

Forward looking statements

It should be noted that certain statements herein which are not historical facts, including, without limitation, those regarding expectations for general economic development and the market situation, expectations for customer industry profitability and investment willingness, expectations for company growth, development and profitability and the realization of synergy benefits and cost savings, and statements preceded by ”expects”, ”estimates”, ”forecasts” or similar expressions, are forward-looking statements. These statements are based on current decisions and plans and currently known factors. They involve risks and uncertainties which may cause the actual results to materially differ from the results currently expected by the company.

Such factors include, but are not limited to:

1) general economic conditions, including fluctuations in exchange rates and interest levels which influence the operating environment and profitability of customers and thereby the orders received by the company and their margins

2) the competitive situation, especially significant technological solutions developed by competitors

3) the company’s own operating conditions, such as the success of production, product development and project management and their continuous development and improvement

4) the success of pending and future acquisitions and restructuring.

2

© Metso © Metso

1. Quarterly highlights

2. Metso value creation

3. Financial performance

4. Outlook and guidance

Content

3

© Metso © Metso

• We are committed to taking personal responsibility for our own safety and for the safety of others

• All incidents can be prevented • Our LTIF has been trending down

Safety is our top priority

4 LTIF = Lost time incident frequency (per million working hours) NMF= Near miss and risk observation frequency (per million working hours)

Target: LTIF less than 1 Long term occupational safety target: LTIF 0 Our lost time incident frequency in 2013 was 4.2

0

50

100

150

200

250

300

350

400

0

2

4

6

8

10

12

14

16

Lost time incident frequency (LTIF)

Nearmiss and risk observation frequency (NMF)

Q1/2014 highlights Matti Kähkönen

President and CEO

© Metso © Metso

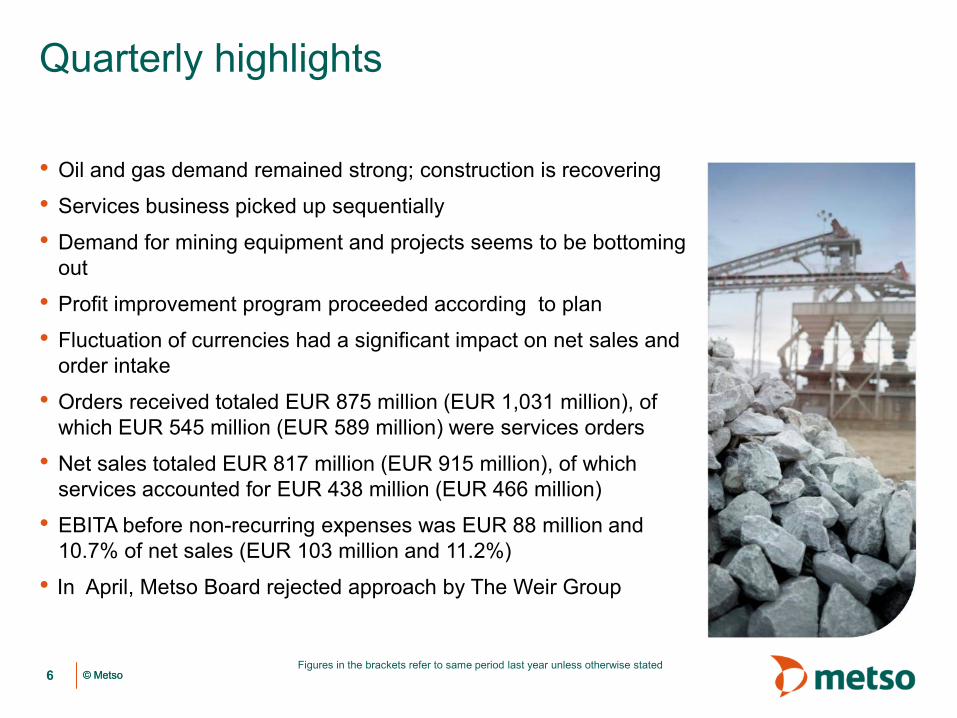

• Oil and gas demand remained strong; construction is recovering

• Services business picked up sequentially

• Demand for mining equipment and projects seems to be bottoming out

• Profit improvement program proceeded according to plan

• Fluctuation of currencies had a significant impact on net sales and order intake

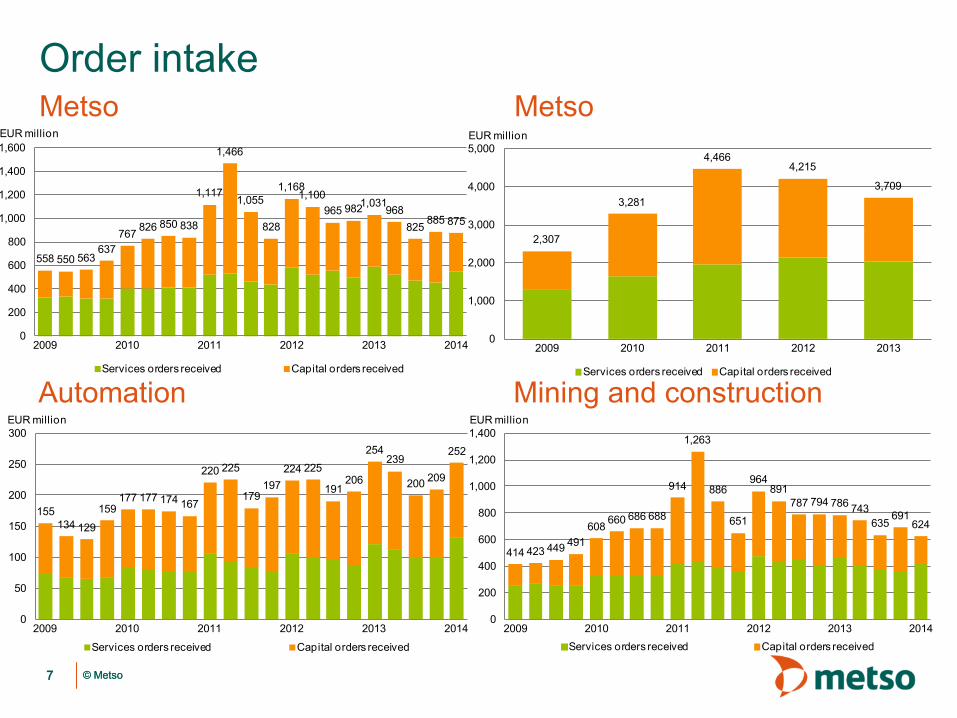

• Orders received totaled EUR 875 million (EUR 1,031 million), of which EUR 545 million (EUR 589 million) were services orders

• Net sales totaled EUR 817 million (EUR 915 million), of which services accounted for EUR 438 million (EUR 466 million)

• EBITA before non-recurring expenses was EUR 88 million and 10.7% of net sales (EUR 103 million and 11.2%)

• In April, Metso Board rejected approach by The Weir Group

Quarterly highlights

6 Figures in the brackets refer to same period last year unless otherwise stated

© Metso © Metso

Order intake Metso

7

Automation Mining and construction

Metso

558 550 563637

767 826 850 838

1,117

1,466

1,055

828

1,1681,100

965 9821,031968

825 885 875

0

200

400

600

800

1,000

1,200

1,400

1,600

2009 2010 2011 2012 2013 2014

EUR million

Services orders received Capital orders received

2,307

3,281

4,4664,215

3,709

0

1,000

2,000

3,000

4,000

5,000

2009 2010 2011 2012 2013

EUR million

Services orders received Capital orders received

155134 129

159177 177 174 167

220 225

179197

224 225

191206

254239

200 209

252

0

50

100

150

200

250

300

2009 2010 2011 2012 2013 2014

EUR million

Services orders received Capital orders received

414 423 449 491608 660 686 688

914

1,263

886

651

964891

787 794 786 743635

691624

0

200

400

600

800

1,000

1,200

1,400

2009 2010 2011 2012 2013 2014

EUR million

Services orders received Capital orders received

© Metso © Metso

Order intake by country

8

• Orders from the US and Canada were significantly higher

• Orders from China grew in Mining and Construction

• No big project orders from South America

EUR million Q1/2014 Q4/2013 Change %% of all orders

USA 135 114 19 15China 75 51 47 9Brazil 70 94 -24 8Canada 54 27 100 6Australia 48 45 7 5Finland 38 42 -11 4Chile 37 135 -72 4India 35 25 40 4Russia 30 27 11 3Sweden 27 23 17 3

© Metso © Metso

2,902 3,018

3,672

4,2823,858

0

1,000

2,000

3,000

4,000

5,000

2009 2010 2011 2012 2013

EUR million

Services net sales Capital net sales

735 746 685 736647

726 748898

744871 901

1,156

959

1,1161,0751,132

915988 937

1,018

817

0

200

400

600

800

1,000

1,200

1,400

1,600

2009 2010 2011 2012 2013 2014

EUR million

Services net sales Capital net sales

Net sales Metso

9

Automation Mining and construction

Metso

177 180152

166146 156 151

198

165 176 185

244

182

232211

233

184207 214

249

186

0

50

100

150

200

250

300

2009 2010 2011 2012 2013 2014

EUR million

Services net sales Capital net sales

568 581540 579

509584 609

717

592

711 736

928

787

899 882924

744800

742784

631

0

200

400

600

800

1,000

2009 2010 2011 2012 2013 2014

EUR million

Services net sales Capital net sales

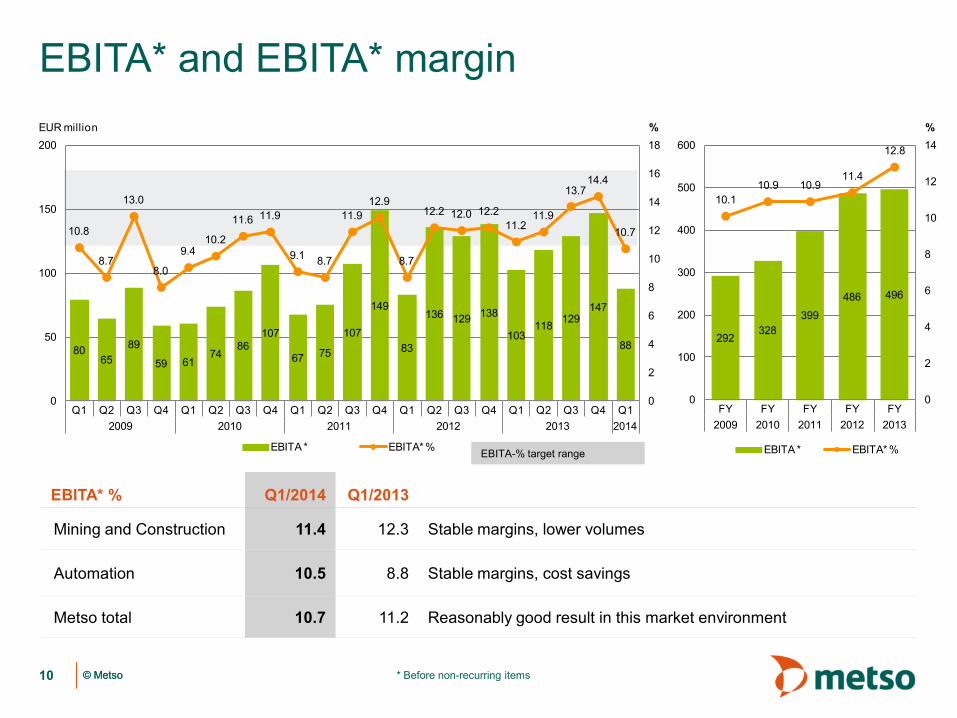

© Metso © Metso * Before non-recurring items

EBITA* and EBITA* margin

10

EBITA-% target range

EBITA* % Q1/2014 Q1/2013

Mining and Construction 11.4 12.3 Stable margins, lower volumes

Automation 10.5 8.8 Stable margins, cost savings

Metso total 10.7 11.2 Reasonably good result in this market environment

292328

399

486 496

10.110.9 10.9

11.4

12.8

0

2

4

6

8

10

12

14

0

100

200

300

400

500

600

FY FY FY FY FY2009 2010 2011 2012 2013

%

EBITA * EBITA* %

8065

89

59 6174

86107

67 75

107

149

83

136 129 138

103118 129

147

88

10.8

8.7

13.0

8.0

9.410.2

11.6 11.9

9.1 8.7

11.912.9

8.7

12.2 12.0 12.211.2

11.9

13.714.4

10.7

0

2

4

6

8

10

12

14

16

18

0

50

100

150

200

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q12009 2010 2011 2012 2013 2014

%EUR million

EBITA * EBITA* %

© Metso © Metso

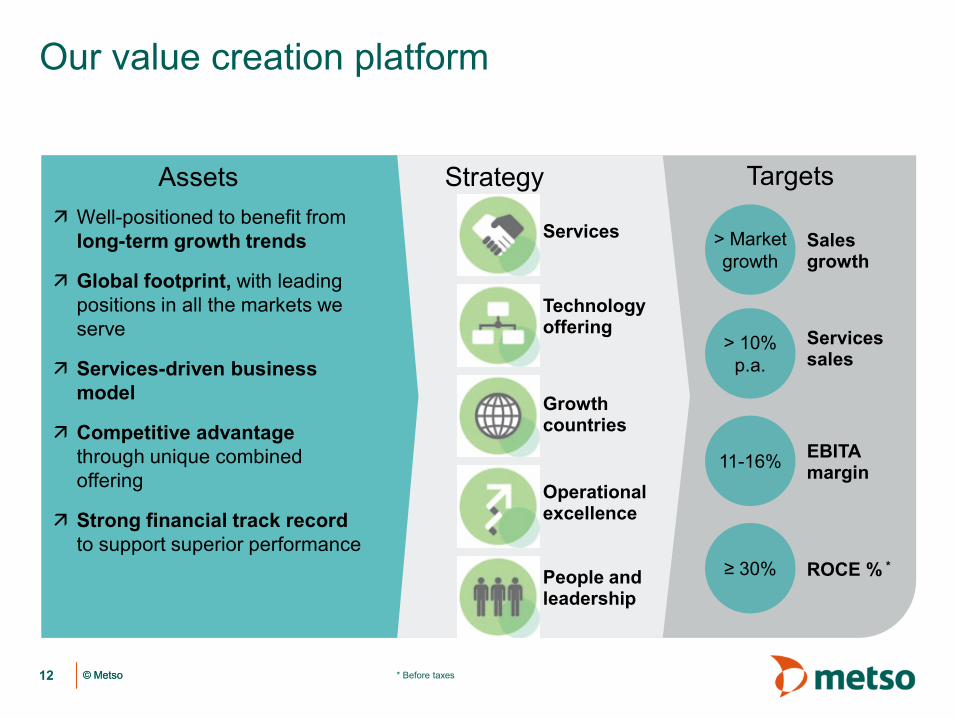

• Significant shareholder value has been created through the demerger

• Both Metso and Valmet share prices have shown positive development

• We will continue leveraging our • unrivaled services presence and capabilities • strong global market positions to capitalize on growth

opportunities • competitive advantage through a unique combined offering • ongoing profit improvement and capital efficiency programs • strong financial track record

Metso value creation

11

© Metso © Metso

Our value creation platform

12 * Before taxes

Well-positioned to benefit from long-term growth trends

Global footprint, with leading positions in all the markets we serve

Services-driven business model

Competitive advantage through unique combined offering

Strong financial track record to support superior performance

Assets Strategy Targets

≥ 30% ROCE % *

11-16% EBITA margin

> 10% p.a.

Services sales

> Market growth

Sales growth

Services

Technology offering

Growth countries

Operational excellence

People and leadership

Financial performance Harri Nikunen, CFO

© Metso © Metso

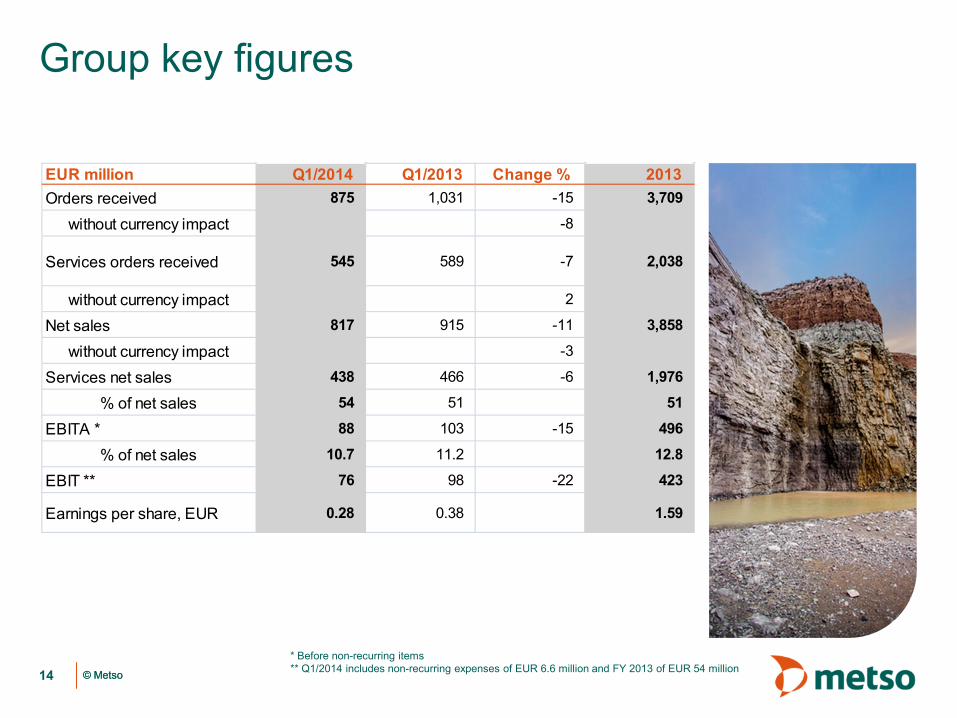

Group key figures

14 * Before non-recurring items ** Q1/2014 includes non-recurring expenses of EUR 6.6 million and FY 2013 of EUR 54 million

EUR million Q1/2014 Q1/2013 Change % 2013Orders received 875 1,031 -15 3,709

without currency impact -8

Services orders received 545 589 -7 2,038

without currency impact 2

Net sales 817 915 -11 3,858

without currency impact -3

Services net sales 438 466 -6 1,976

% of net sales 54 51 51

EBITA * 88 103 -15 496

% of net sales 10.7 11.2 12.8

EBIT ** 76 98 -22 423

Earnings per share, EUR 0.28 0.38 1.59

© Metso © Metso

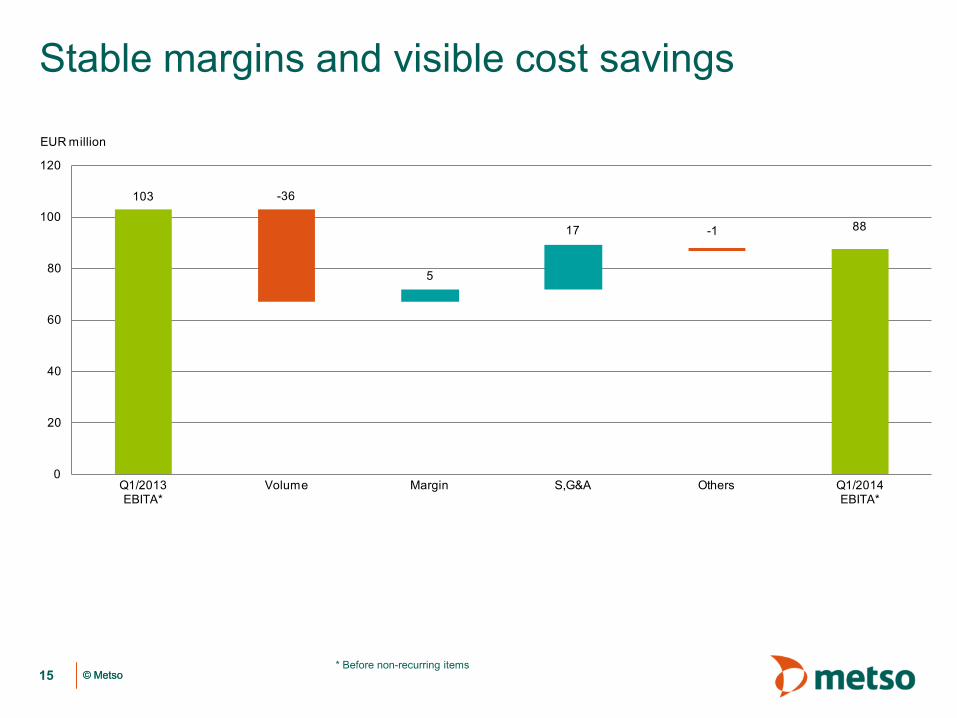

103

88

-36

5

17 -1

0

20

40

60

80

100

120

Q1/2013 EBITA*

Volume Margin S,G&A Others Q1/2014 EBITA*

EUR million

Stable margins and visible cost savings

15 * Before non-recurring items

© Metso © Metso

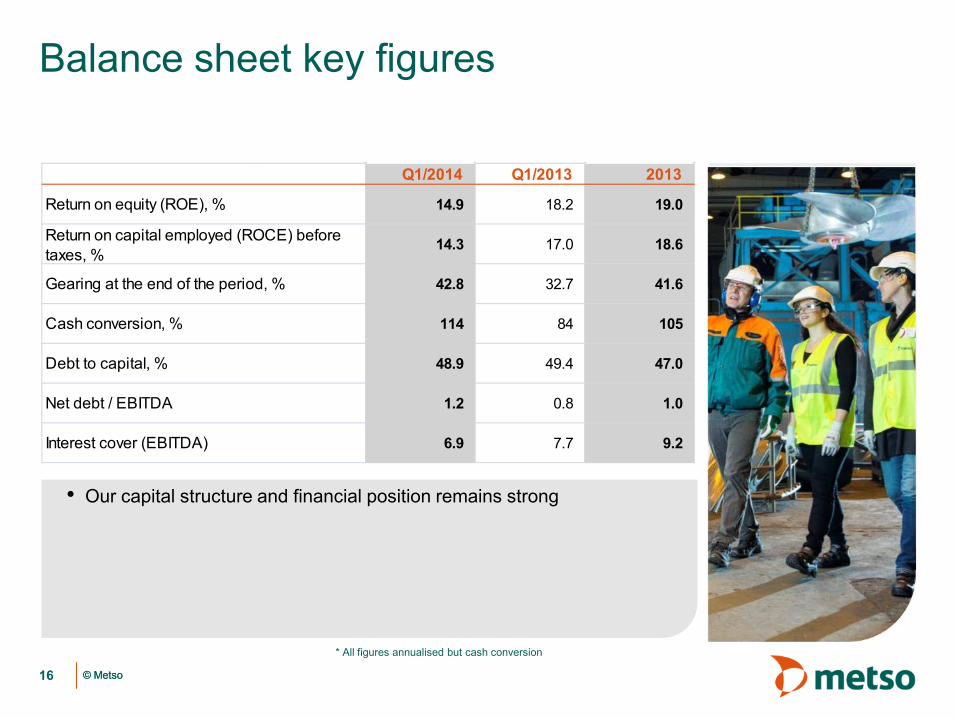

Balance sheet key figures

16

• Our capital structure and financial position remains strong

Q1/2014 Q1/2013 2013

14.9 18.2 19.0

14.3 17.0 18.6

42.8 32.7 41.6

114 84 105

48.9 49.4 47.0

1.2 0.8 1.0

6.9 7.7 9.2Interest cover (EBITDA)

Return on equity (ROE), %

Return on capital employed (ROCE) before taxes, %

Gearing at the end of the period, %

Cash conversion, %

Debt to capital, %

Net debt / EBITDA

* All figures annualised but cash conversion

© Metso © Metso

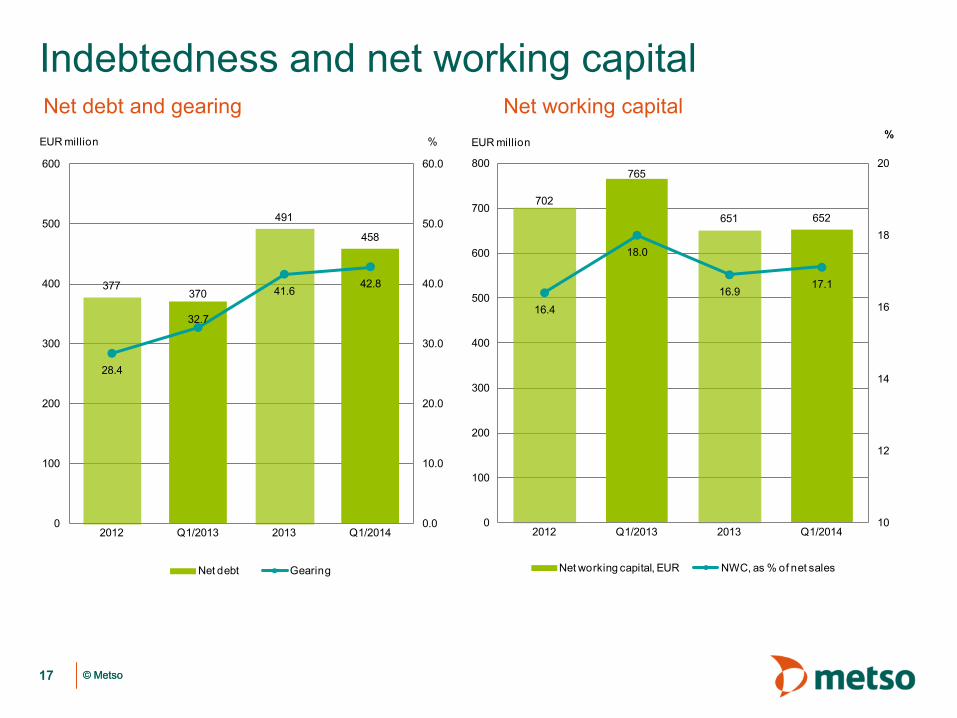

Indebtedness and net working capital

17

Net working capital Net debt and gearing

377370

491

458

28.4

32.7

41.642.8

0.0

10.0

20.0

30.0

40.0

50.0

60.0

0

100

200

300

400

500

600

2012 Q1/2013 2013 Q1/2014

%EUR million

Net debt Gearing

702

765

651 652

16.4

18.0

16.917.1

10

12

14

16

18

20

0

100

200

300

400

500

600

700

800

2012 Q1/2013 2013 Q1/2014

%EUR million

Net working capital, EUR NWC, as % of net sales

© Metso © Metso 18

* Before non-recurring items ** Excluding cash and other non-operative balance sheet items, annualized

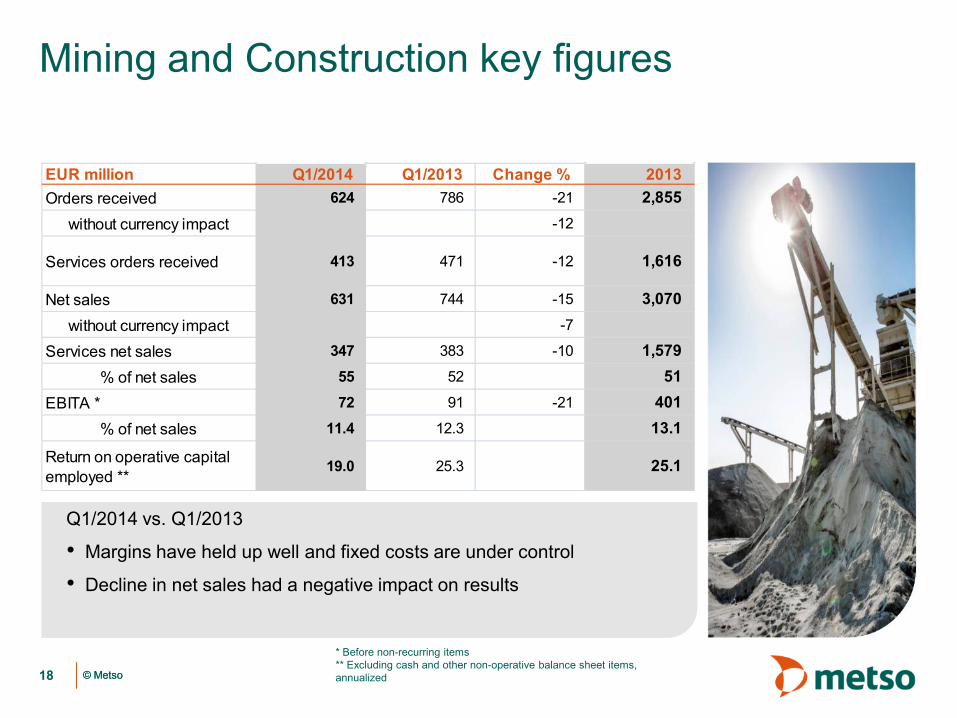

Mining and Construction key figures

Q1/2014 vs. Q1/2013

• Margins have held up well and fixed costs are under control

• Decline in net sales had a negative impact on results

EUR million Q1/2014 Q1/2013 Change % 2013Orders received 624 786 -21 2,855

without currency impact -12

Services orders received 413 471 -12 1,616

Net sales 631 744 -15 3,070without currency impact -7

Services net sales 347 383 -10 1,579% of net sales 55 52 51

EBITA * 72 91 -21 401% of net sales 11.4 12.3 13.1

Return on operative capital employed **

19.0 25.3 25.1

© Metso © Metso

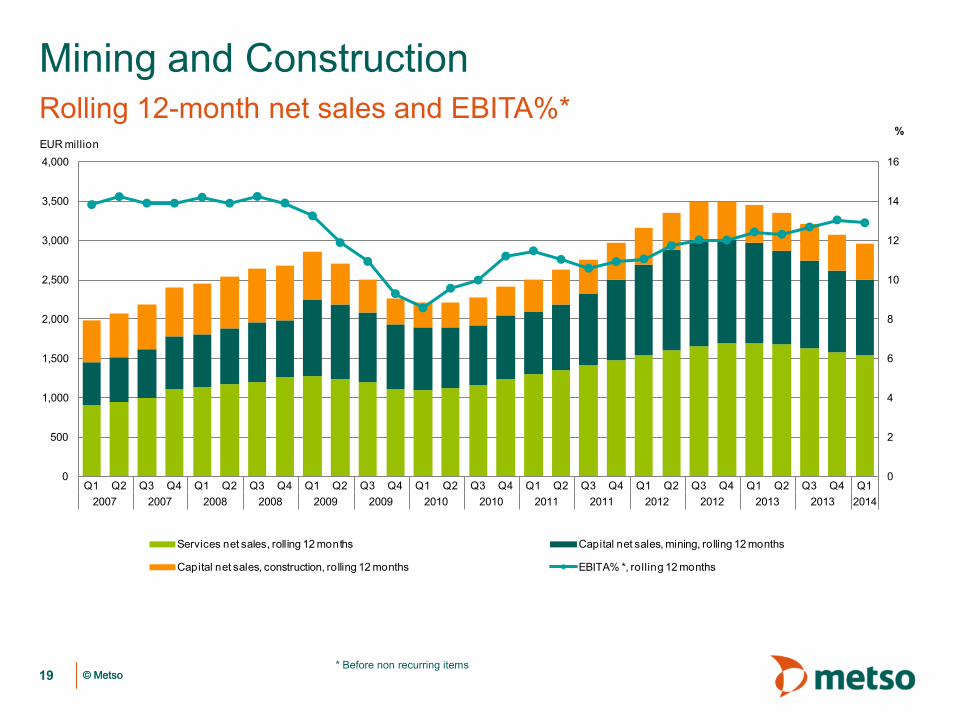

Mining and Construction Rolling 12-month net sales and EBITA%*

19 * Before non recurring items

0

2

4

6

8

10

12

14

16

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q12007 2007 2008 2008 2009 2009 2010 2010 2011 2011 2012 2012 2013 2013 2014

%EUR million

Services net sales, rolling 12 months Capital net sales, mining, rolling 12 months

Capital net sales, construction, rolling 12 months EBITA% *, rolling 12 months

© Metso © Metso

* Before non-recurring items ** Excluding cash and other non-operative balance sheet items, annualized

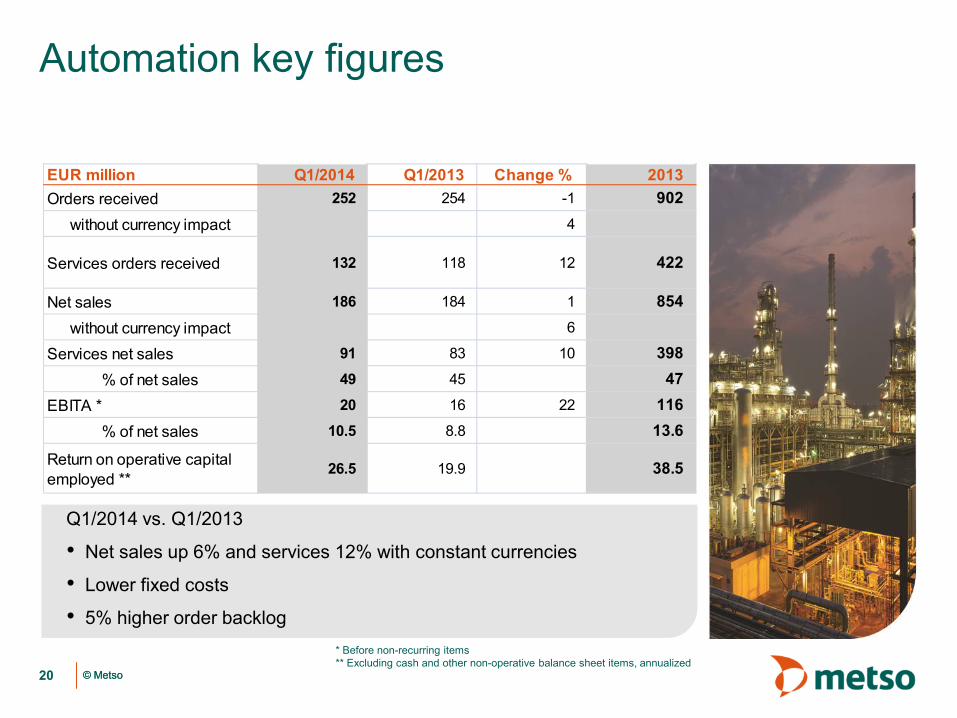

Automation key figures

20

Q1/2014 vs. Q1/2013

• Net sales up 6% and services 12% with constant currencies

• Lower fixed costs

• 5% higher order backlog

EUR million Q1/2014 Q1/2013 Change % 2013Orders received 252 254 -1 902

without currency impact 4

Services orders received 132 118 12 422

Net sales 186 184 1 854without currency impact 6

Services net sales 91 83 10 398% of net sales 49 45 47

EBITA * 20 16 22 116% of net sales 10.5 8.8 13.6

Return on operative capital employed **

26.5 19.9 38.5

© Metso © Metso

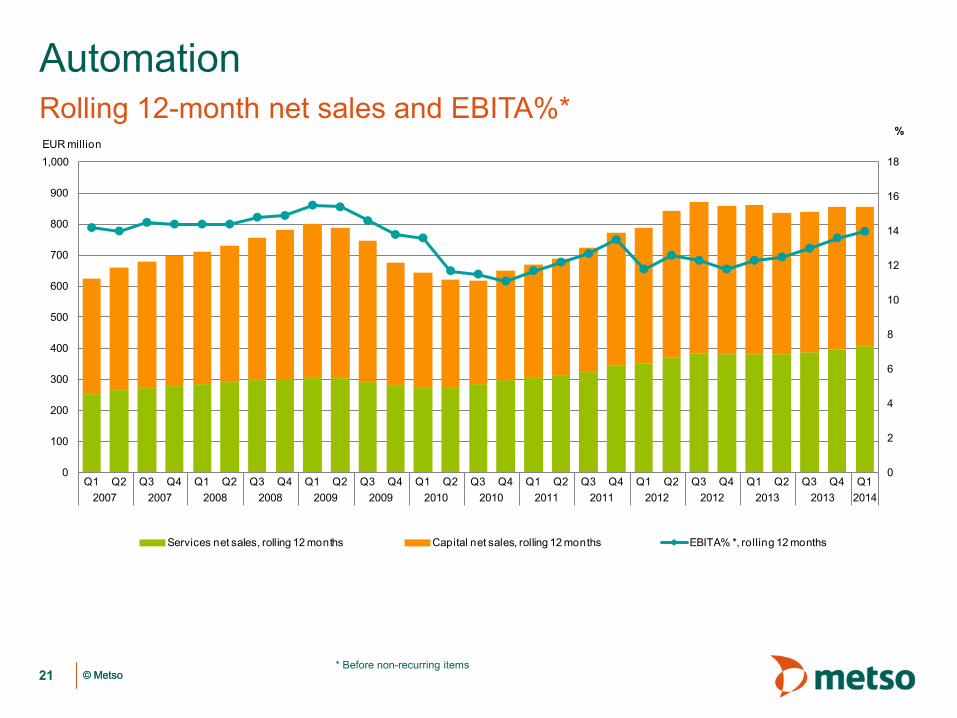

Automation Rolling 12-month net sales and EBITA%*

21 * Before non-recurring items

0

2

4

6

8

10

12

14

16

18

0

100

200

300

400

500

600

700

800

900

1,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q12007 2007 2008 2008 2009 2009 2010 2010 2011 2011 2012 2012 2013 2013 2014

%EUR million

Services net sales, rolling 12 months Capital net sales, rolling 12 months EBITA% *, rolling 12 months

© Metso © Metso

• Program was announced in autumn 2013 • We are responding to the soft market environment in

mining and adjusting to the new Group structure • The current scope encompasses headcount

reduction of 1,300-1,400 • Targeted gross savings total EUR 120-130 million • Completion rate is 60%, targeting full completion by

the end of 2014 • Savings to be fully achieved in H1/2015

Profit improvement program proceeding according to plan

22

© Metso © Metso

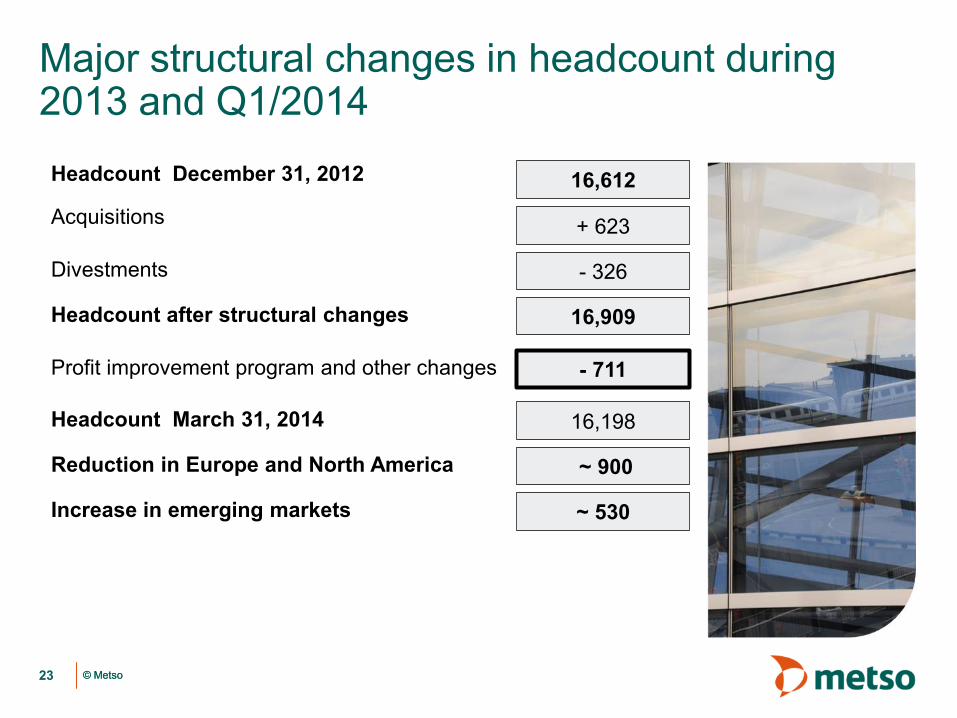

Major structural changes in headcount during 2013 and Q1/2014

23

Headcount December 31, 2012 16,612 Acquisitions + 623

Divestments - 326

Headcount after structural changes 16,909

Profit improvement program and other changes - 711

Headcount March 31, 2014 16,198

Reduction in Europe and North America ~ 900

Increase in emerging markets ~ 530

Outlook and guidance Matti Kähkönen

President and CEO

© Metso © Metso

Market outlook

55% of net sales 55% service intensity Current demand: • Weak for the equipment and project business • Services good

20% of net sales 40% service intensity Current demand: • Satisfactory for the equipment and

services

22% of net sales 45% service intensity Current demand: • Good in oil and gas; satisfactory in

pulp and paper • Services good

3-6 months market outlook

Equipment Services

Equipment Services

25

Equipment Services

Mining Construction Automation

© Metso © Metso

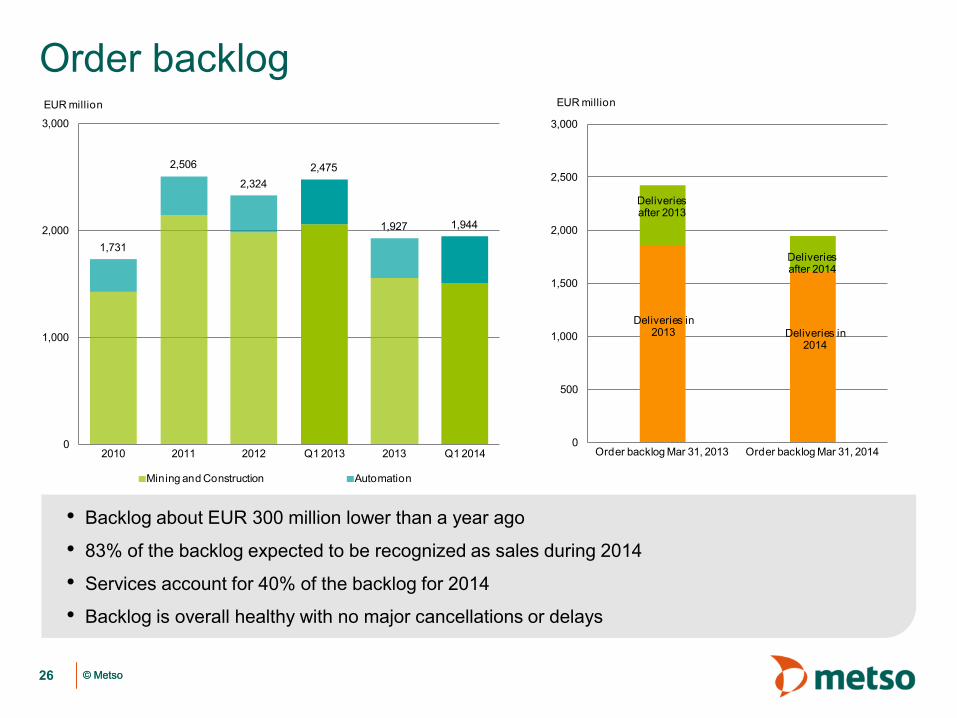

Order backlog

26

• Backlog about EUR 300 million lower than a year ago

• 83% of the backlog expected to be recognized as sales during 2014

• Services account for 40% of the backlog for 2014

• Backlog is overall healthy with no major cancellations or delays

1,731

2,506

2,3242,475

1,927 1,944

0

1,000

2,000

3,000

2010 2011 2012 Q1 2013 2013 Q1 2014

EUR million

Mining and Construction Automation

Deliveries in 2014

Deliveries after 2014

Deliveries in 2013

Deliveries after 2013

0

500

1,000

1,500

2,000

2,500

3,000

Order backlog Mar 31, 2013 Order backlog Mar 31, 2014

EUR million

© Metso © Metso 27

Based on our market outlook, backlog for 2014, current exchange rates and ongoing cost-efficiency actions, we estimate that

• our net sales in 2014 will be somewhat below 2013

• and EBITA margin before non recurring items for 2014 will be at around 12%

Guidance for 2014

company/metso metsogroup metsoworld metsoworld metsogroup

www.metso.com