Embed Size (px)

Citation preview

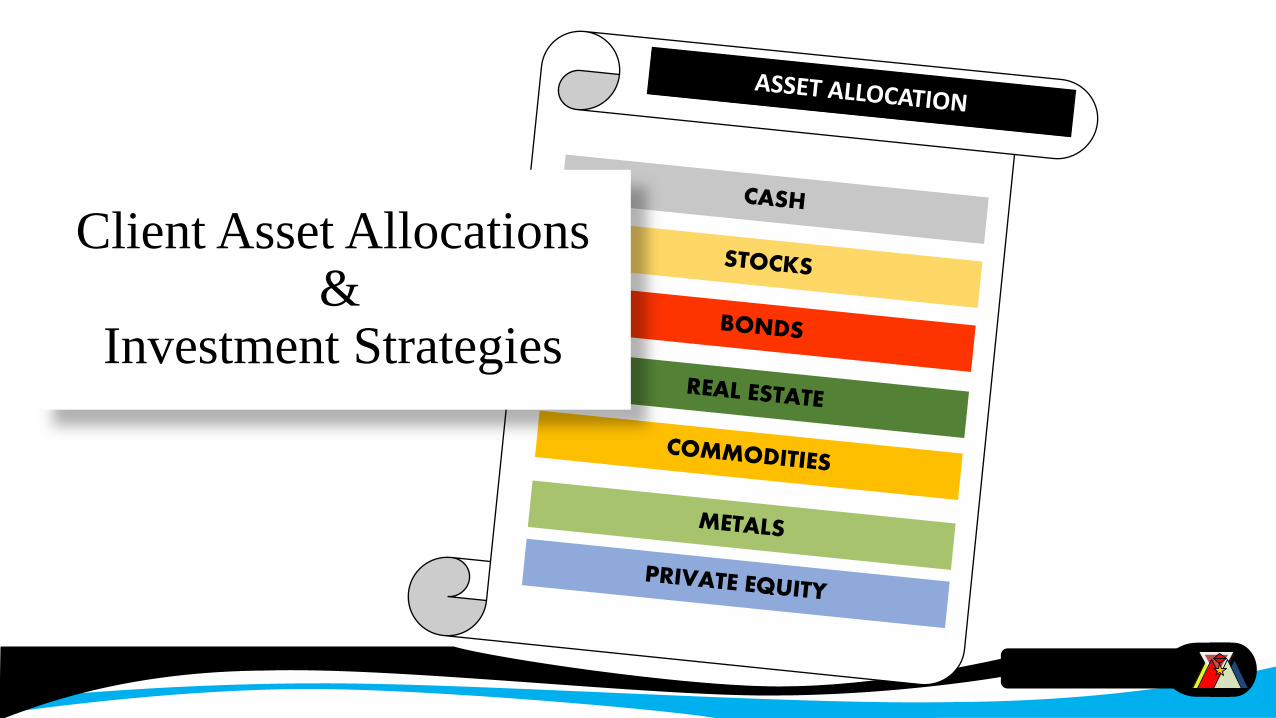

Client Asset Allocations&

Investment Strategies

Asset Allocation

Asset allocation: the process of determining the appropriate mix for different

asset classes in an investor’s portfolio and maintaining those proportions over

time. For individual investors, the process involves three strategies:

Portfolio Rebalancing

Strategic Asset Allocation

Tactical Asset Allocation

Strategic Asset Allocation (SAA)

• Strategic asset allocation (SAA): is the benchmark asset mix designed to

achieve the client’s longer-term objectives while taking into account any

constraints.

• It incorporates the expectations of the investment advisor or the advisory firm

for the return, risk, and correlation among the asset classes.

Once set, the SAA becomes a benchmark for performance of the client’s

portfolio. It is also referred to as policy, passive, or benchmark asset

allocation.

It requires the following steps:

• Establish client objectives and constraints

• Specify asset classes eligible for the portfolio;

• Specify capital market expectations

• Derive the efficient portfolio frontier;

• Find and set the optimal asset mix.

SAA aims to design an optimal, or efficient, portfolio for which the expected

return is maximized for a given level of risk or, equally, the risk is minimized for

a given expected return.

The overall objective is normally based on balancing the need to control

inflation, interest rate, and market risk against the desire for enhanced returns.

Strategic Asset Allocation (SAA)

Steps: Strategic Asset Allocation

• Establish client objectives and constraints: based on factors such as the

client’s return objectives, risk tolerance, time horizon, liquidity needs, legal

constraints, tax considerations, and other special circumstances.

Goals and objectives often conflict with one another, and investors with short

horizons face different risks than do long-term investors. Goals and

objectives should be clearly articulated.

E.g., average portfolio return of 4% above the inflation rate, beating an

inflation index by 2%pa etc.

The aim should be for a single strategic asset allocation for a client’s entire

investment portfolio at any given time, balancing the client’s objectives and

constraints across one relatively long-term time horizon.

Specify asset classes eligible for the portfolio: three broad asset classes; cash,

debt securities (also known as bonds or fixed-income securities), and equities

but this is no longer adequate due to the evolution and proliferation of financial

instruments.

An Asset class is a group of assets available for direct investment that has a set

of return and risk characteristics distinct from those of other groups of assets.

Specifically, the group selected should have a low or negative correlation with

other asset classes.

The IA should combine low- or negative-correlation assets to build the lowest-

variance, highest-return portfolio possible.

Steps: Strategic Asset Allocation

• Specify capital market expectations - developing a set of capital market

expectations for the various asset classes being considered for the portfolio

mix.

These expectations specify returns, variances, and co-variances (correlation

coefficients) among the various asset classes.

Expectations are normally based on historical asset class results, including

average returns, standard deviations, etc for each asset class which is adjusted

for current economic forecasts, based on prevailing economic scenarios and

probability of occurrence.

Steps: Strategic Asset Allocation

Specify capital market expectations (cont’d)

Forecasts are reviewed periodically – quarterly, semi/ annually, typically based

on 5yr periods, recent trends and potential changes in asset class returns.

• Deriving the efficient portfolio frontier; the “portfolio opportunity set” (the

set of all possible asset combinations) is derived from capital market

expectations and their probability distributions.

Then from this set, the efficient frontier – the highest-return portfolio at each

risk level – is identified.

Steps: Strategic Asset Allocation

Find and set the optimal asset mix- The integration of capital market

expectations and risk tolerances to produce the long-term asset mix that reflects

the optimum portfolio at the investor’s risk level.

The optimum portfolio is selected using one of three methods:

• Rules of thumb

• Ad hoc approach

• Mean-variance analysis

Steps: Strategic Asset Allocation

Rule of thumb: Based on simple rules that are quite simple to implement

e.g. time diversification and Age approach..

o Time diversification: over the long term, the return/risk trade-off for

equities improves over that of all other asset classes, and therefore the

longer the time horizon, the lower the risk of holding equities over

longer periods. This leads to a recommendation that younger clients

hold a greater percentage of their portfolios in equities than older

clients would because equities offer the greatest expected return.

Steps: Strategic Asset Allocation

o Age Approach: recommends a specific SAA based solely on the client’s

age. It suggests an allocation to debt securities (including cash and cash

equivalents) equal to the client’s age. With this rule, the allocation to

equities equals 100 minus the client’s age.

Steps: Strategic Asset Allocation

E.g., For a 35 year old client, the age approach to strategic asset allocation

suggests a 65% weight in equities and a 35% weight in debt securities.

As the client approaches retirement, the allocation to debt securities will

increase and the allocation to equities will decline.

By retirement, the suggested allocation will be 35% in equities and 65% in debt

securities.

• Mean-variance Analysis:

1. A “pure” mean-variance analysis requires the investment advisor to

include information on capital market expectations and to estimate a

numerical value for the client’s risk tolerance.

The specific analysis provides guidance on how to estimate the risk

tolerance variable.

Using this information, the “pure” optimizer, a quadratic formula that

maximizes investor utility, recommends a single strategic asset

allocation that is both efficient and acceptable given the client’s risk

tolerance.

Steps: Strategic Asset Allocation

2. Other optimizers require only a set of capital market expectations as input.

Using this information, they produce several recommended asset allocations, all

of which are efficient.

The advisor then simply selects what he feels is the appropriate asset allocation

for the client based on the client’s return objective and risk tolerance.

Complex calculations and computer programs are normally designed to client

responses in a model to determine client risk appetites and appropriate strategic

asset allocation.

Steps: Strategic Asset Allocation

Ad Hoc Approach: least desirable or applied as it concentrates on gut

feeling about the market but yet, clients goals and objective considered. Not

recommended.

Steps: Strategic Asset Allocation

• Also referred to as dynamic asset allocation.

The client’s portfolio must be rebalanced periodically to maintain the desired

asset mix over the long term.

Rebalancing is necessary because the actual asset mix will change as

dividends and interest payments are made and as market prices and economic

conditions change.

Rebalancing may also be required if changes occur in the client’s objectives

or constraints or in the expected risk and return of the asset classes.

Asset Allocation - Portfolio Rebalancing

• This is a decision by the client and investment advisor to change the client’s

original SAA to take advantage of perceived opportunities created by short-

term fluctuations in the relative performance of asset classes.

TAA operates within limits determined by minimum and maximum asset class

weights.

It is also occasionally referred to as active asset allocation.

Together; Strategic asset allocation, portfolio rebalancing and Tactical asset

allocation are referred to as Integrated Asset Allocation.

Asset Allocation – Tactical Asset Allocation

Benefits of Asset Allocation

• Accounts for most of a portfolio’s long-term returns.

• The strategic asset allocation is designed to be an optimal investment portfolio:

Portfolios are subject to two kinds of risk: systematic (related to the market)

and unsystematic (related to the individual security).

The goal of strategic asset allocation is to lower systematic risk and eliminate

unsystematic risk.

• It allows meaningful performance measurement. In the absence of a clear

SAA, goal setting – and measuring progress against those goals – would be

difficult.

• Long-term investment objectives are kept in focus – focusing tool.

• Tactical asset allocation allows for opportunities to realize enhanced returns

through successful portfolio tilting.

Benefits of Asset Allocation

Dynamic asset allocation refers to the systematic rebalancing, either temporally

or based on weights, needed to return the portfolio to the long-term benchmark

asset-class mix. Rebalancing reflects the following basic assumptions:

Capital market expectations remain constant. If capital market expectations

change, all calculations underlying the asset mix are redone.

Risk tolerance remains constant. If risk tolerance changes, the efficient frontier

remains intact but the optimum portfolio changes.

Dynamic Asset Allocation

Investment objectives remain constant.

If objectives change, the efficient frontier

remains intact but the optimum portfolio

changes.

The asset mix may drift from the target

because of structural or procedural

administrative matters, abnormal returns

within asset classes, or changing capital

market conditions.

Dynamic Asset Allocation

CASH

ASSET ALLOCATION

STOCKS

BONDS

REAL ESTATE

COMMODITIES

METALS

PRIVATE EQUITY

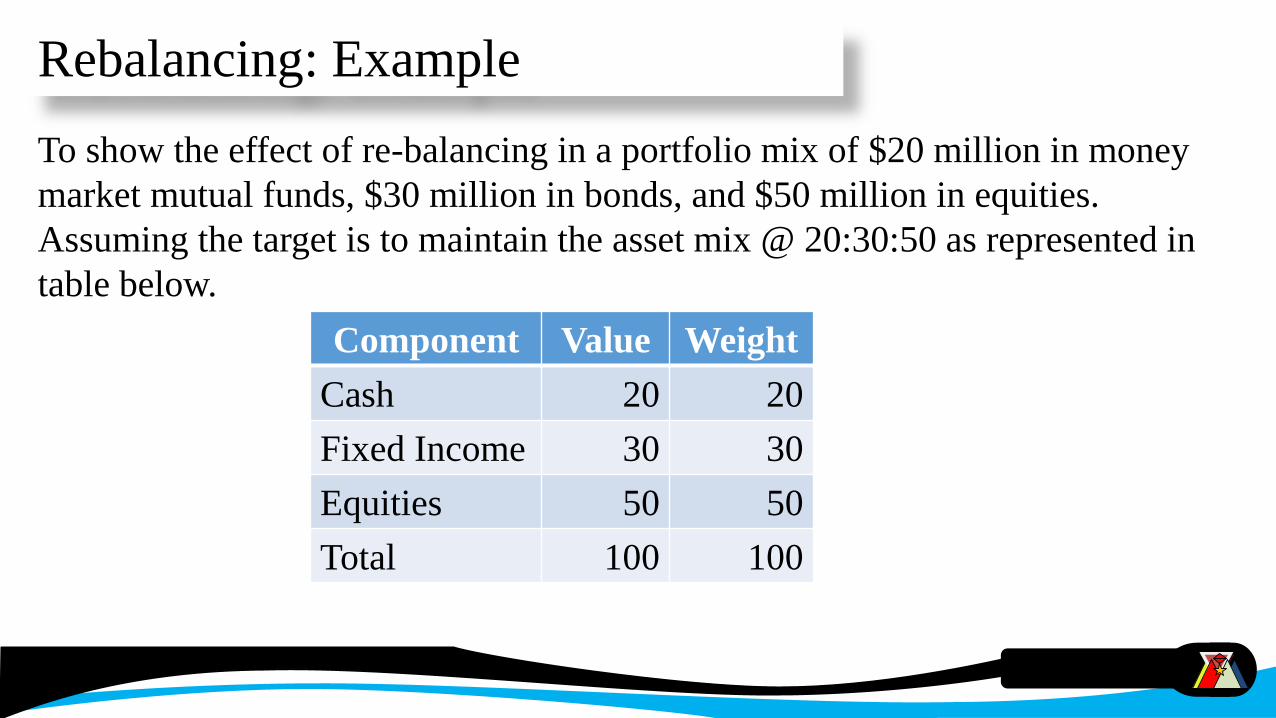

Component Value Weight

Cash 20 20

Fixed Income 30 30

Equities 50 50

Total 100 100

To show the effect of re-balancing in a portfolio mix of $20 million in money

market mutual funds, $30 million in bonds, and $50 million in equities.

Assuming the target is to maintain the asset mix @ 20:30:50 as represented in

table below.

Rebalancing: Example

Rebalancing: Example

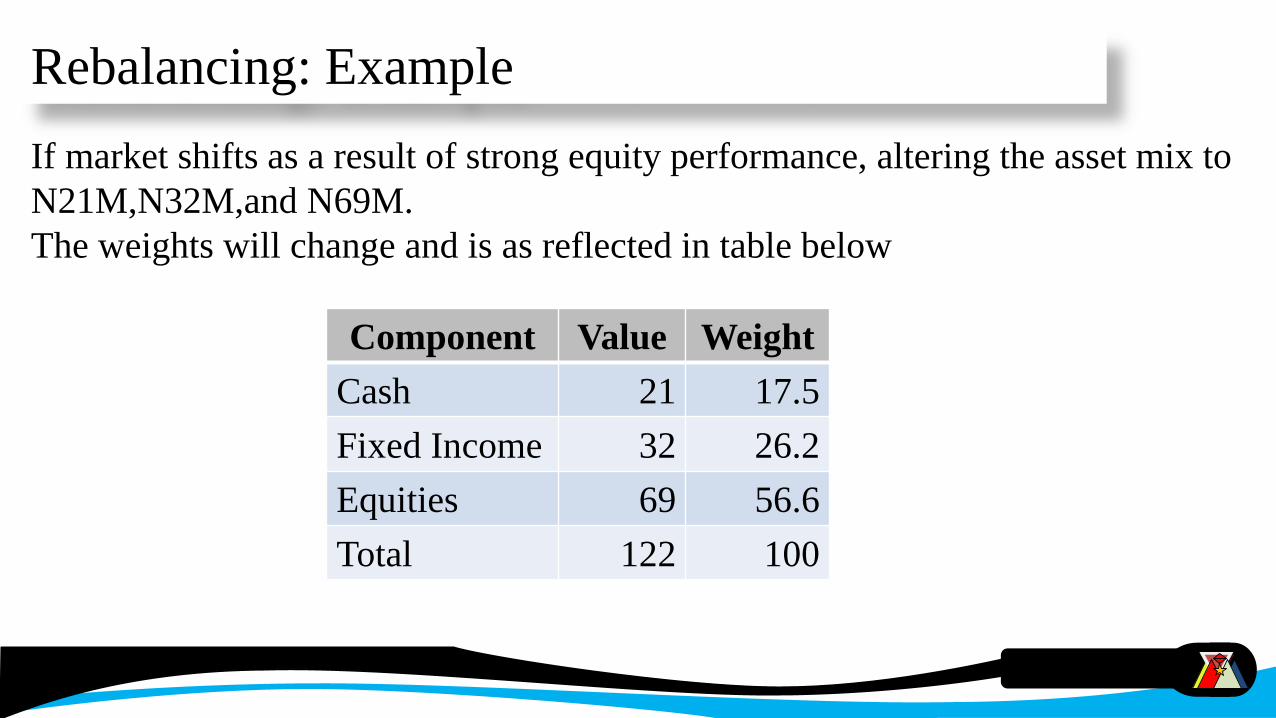

Component Value Weight

Cash 21 17.5

Fixed Income 32 26.2

Equities 69 56.6

Total 122 100

If market shifts as a result of strong equity performance, altering the asset mix to

N21M,N32M,and N69M.

The weights will change and is as reflected in table below

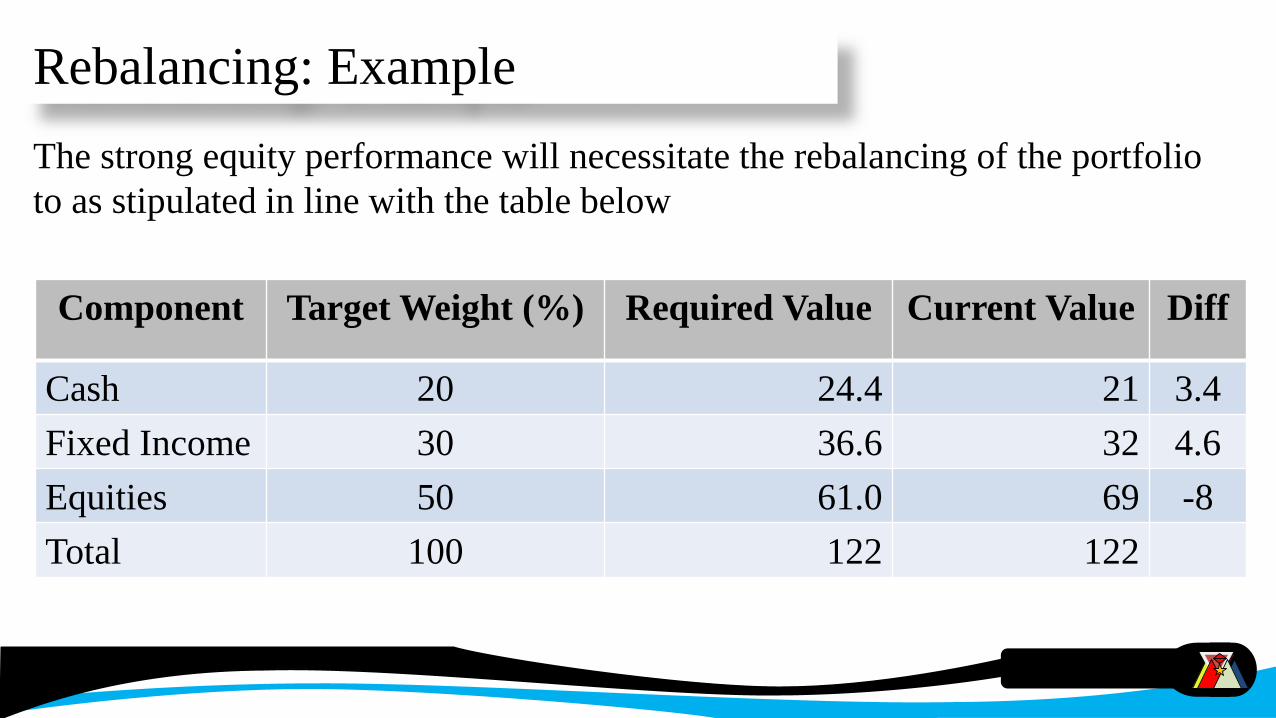

Component Target Weight (%) Required Value Current Value Diff

Cash 20 24.4 21 3.4

Fixed Income 30 36.6 32 4.6

Equities 50 61.0 69 -8

Total 100 122 122

The strong equity performance will necessitate the rebalancing of the portfolio

to as stipulated in line with the table below

Rebalancing: Example

Tactical Asset Allocation

The process of tilting a portfolio to take advantage of perceived inefficiencies in

the prices of securities in different asset classes or in different sectors within a

class.

The portfolio’s policy statement often defines a range for such tactical tilting that

goes beyond the strategic asset weightings. (e.g., overweighting stocks over

bonds).

*moving in and out of assets can incur costs e.g., transaction costs

ASSET ALLOCATION BY ACCUMULATION STAGE

Asset Allocation: Accumulation Statge

There is an approach that bases asset accumulation on the various stages in the

clients life.

There are four accumulation stages:

• Seed-money formation stage

• Mid-life growth stage,

• Pre-retirement consolidation stage

• Retirement stage.

The typical characteristics of clients at each of these stages can be used to

develop a client’s strategic asset allocation.

Seed-money formation stage

-occurs between age 20 and age 45. The objective is to accumulate sufficient seed

money to create a base for future growth.

Client has few assets to invest, a lot of optimism and plenty of future saving

power.

This is the client’s most important, yet most vulnerable, stage.

Consider the seed-money formation stage complete when a client has saved twice

his estimated annual post-retirement withdrawals.

Most asset allocation guidelines point to an aggressive portfolio consisting of

70% to 90% equities for younger investors because this group has a longer

horizon.

Seed-money formation stage

Clients at this stage tend to perceive any loss of seed money as significant.

The most important factor during the seed-money formation stage is maintaining

investment discipline and conservatism, month after month, year after year.

The lower volatility of a conservative portfolio will give the investor much-

needed staying power

During accumulation years, portfolios should be reviewed regularly to make

sure that the client’s retirement objectives can be met and/or his expectations can

be adjusted.

Mid-life growth stage

-generally occurs between ages 35 and 60, clients have general idea of where

they are going in their lives.

Importance of luck should not be ignored in the growth of portfolios during this

stage.

Markets move in different waves - secular trends, megatrends or generational

trends, trends can last as long as 20yrs. Usually, the determining factor is client’s

ability to save money.

The asset allocation should be kept at the optimum mix, and rebalanced annually.

The mid-life growth stage is complete when the portfolio value is 20 times the

estimated annual post-retirement withdrawals from the portfolio.

E.g., if a client needs $20,000 per

year (pre-tax) from the portfolio

during retirement and the portfolio

contains $400,000, the client has

completed the mid-life growth stage.

The emphasis during this stage is on

continued saving and the focus is on

long-term goals.

Mid-life growth stage

Changing Priorities

Ahead

Pre-retirement Consolidation Stage

- usually occurs between age 55 and 65. Most of the capital formation, whether it

is the investment portfolio, real estate or business, is completed during this stage.

During this stage, the primary goal is to preserve funds. Any growth is

secondary.

If a client is still working, or retired from work but not in need of periodic

income from her portfolio, then there is still an opportunity to increase the value

of the portfolio conservatively.

Although there is generally supposed to be sufficient money available to

finance retirement through life annuities at this stage, taking the portfolio value

from 20 times to 30 times the estimated annual retirement withdrawals will

allow the client to finance her retirement totally from the portfolio without

using life annuities.

Doing so will also give the client the opportunity to accumulate a sizeable

estate.

Pre-retirement Consolidation Stage

INVESTMENT STRATEGIES

Investment Strategy

- the investment strategy to be used in the selection of individual securities or

managed products for the portfolio needs to be identified.

It is a function of what the manager or advisor believes about investment

finance.

Strategies can be active or passive, can be bottom-up or top-down, can focus on

value or growth or on small- or large-capitalization stocks, or employ sector

rotation.

Passive and Active Equity Strategies

Passive Investing Active Investing

Investment Philosophy

Guiding` Portfolio

Equity Strategies

Equity investment strategy can be Passive or Active.

• An active investment strategy uses expectations about individual securities

and the overall investment environment to build a portfolio that will take

advantage of those expectations.

If the expectations change, the portfolio will likely change as well.

• A passive investment strategy, on the other hand, does not lead to portfolio

changes when expectations change.

Many investors mix passive and active investment strategies when they construct

their portfolios.

Efficient-market Hypothesis

Choice of investment strategy depends on the investor’s belief in market

efficiency.

Efficient-market hypothesis states that asset prices reflect available

information in efficient markets.

Theory has three forms, that assumes different amounts of information is

reflected in asset prices:

• Weak form: Current prices incorporate all information about past prices,

volumes, and returns. This implies that technical analysis cannot consistently

beat the market.

• Semi-strong form: Current prices reflect all publicly available information.

This implies that neither fundamental nor technical analysis can be used and

will do nothing to help investors beat the market.

• Strong form: Prices reflect all information, including insider information.

This implies that no type of further analysis is helpful in beating the market.

Efficient-market Hypothesis

Passive Equity Strategies

Passive Investing Active Investing

Investment Philosophy

Guiding` Portfolio

Passive Strategies

- two most widely recognized Passive Strategies are: indexing and buy-and-

hold.

With a buy-and-hold strategy, the investment advisor and client select a group

of securities or managed products and the client holds them until he or she needs

to sell them to meet investment goals.

An indexed portfolio is designed to track the performance of a specific market

index. Investors do not necessarily need to believe in the efficient-market theory

to index. Investors may simply not have the time, resources, or inclination to

follow an active strategy.

Advantage of Indexing Strategy:

• A low risk of underperforming the benchmark.

• Fees that are usually lower than those associated with most active strategies.

• The fact that the strategy does not depend on the ability of the client or

investment advisor to select securities or managed products that will

outperform the benchmark.

Passive Strategies

Disadvantages to indexing:

• Potential underperformance relative to active strategies

• Risk Index return does not meet portfolio objectives or constraints

• Lack of assurance that the performance of the index will be matched

• The underweighting of some indexes in well-performing sectors

• Inefficiency from an after-tax perspective

Passive Strategies

Strategies: Active Equity Investment

Passive Investing Active Investing

Investment Philosophy

Guiding` Portfolio

Active Equity Investment Strategies

- can be separated into two groups based on the approach used in selecting stocks

for purchase or sale:

• Bottom-up Approach

• Top-down Approach

Investment advisors and clients who pick individual stocks can use either of these

approaches to guide their selections.

Advisors and clients who use managed products can ask the fund manager which

approach he or she uses.

Bottom-up Analysis

Starts with a focus on individual stocks. Investors or portfolio managers review

the characteristics of individual stocks and build portfolios of the best stocks in

terms of forecast risk-return characteristics.

It can be classified as style-based or non-style-based.

Style-based approaches involve focusing on a particular set of stocks that

have similar fundamental characteristics and performance patterns.

Non-style-based approaches do not focus on a particular group of stocks but

involve a search for stocks with the best chance of meeting particular

objectives.

Some investors use screening procedures to identify stocks that have particular

attributes believed to be associated with superior investment performance.

The choice of screening criteria is often based on historical stock returns.

Other bottom-up approaches use a more technical approach in which stocks are

bought or sold based on patterns on stock charts or based on statistical analysis

of historical trading data.

Bottom-up Analysis

Style-based Approach

A bottom-up approach to active equity investing that focuses on a particular set

of stocks that have similar fundamental characteristics and performance patterns.

It can also be seen as a top-down approach to active equity investing that focuses

on whatever style offers the opportunity to outperform at a particular point in

time

o Style-Based Investing

Value and Growth:. There are different ways to define value and growth stocks,

but the company’s price-to-book (P/B) ratio, which compares the company’s

stock price to the book value per share, is the most commonly used factor.

In addition to P/B ratios, Growth and Value Stocks are sometimes distinguished

by their price-earnings (P/E) ratios and dividend yields.

Value stocks tend to have low P/E and P/B ratios and high dividend yields, while

growth stocks have high P/Es and P/Bs and low dividend yields.

Investors and portfolio managers who buy growth stocks tend to focus on a

company’s earnings.

It is believed that higher earnings growth translates into a higher book value

which, assuming the company’s P/B ratio stays the same, will translate into a

higher stock price.

The risks of owning a growth stock are that earnings, and hence book value,

might not increase as expected or that P/B could decline.

Growth stocks can be further subdivided into those that display consistent

growth in earnings and those that display significant earnings momentum.

o Style-Based Investing

Both of these subgroups generally possess high P/E and P/B multiples

(reflecting potential for future earnings growth) and low dividend yields

(reflecting tendency to re-invest earnings in the business).

Value Stocks: tendency to focus on the company’s share price. Sought, are

stocks trading at prices that reflect a lower-than-justified P/B ratio.

It’s believed, the market will realize this low valuation and, assuming that the

book value remains unchanged, the P/B should rise, which will translate into a

higher stock price.

o Style-Based Investing

Value investors can be grouped into three categories:

• Investors who focus solely on stocks with low P/B ratios – stocks in this

category typically include those of depressed cyclical companies and

companies with low dividend yields and little or no current earnings

• Investors who focus on low P/E ratios, which are typical of stocks in

defensive, cyclical, or out-of-favour industries

• Yield investors who focus on stocks with above-average dividend yields

o Style-Based Investing

Market Capitalization. Another definition of equity style which focuses on

the size of the company as measured by equity market capitalization.

The stocks with the smallest market capitalizations are called small-cap stocks

and those with the largest market capitalizations are called large-cap stocks.

There is no precise definition of what constitutes a small- or large-cap stock; it

depends on the country and the overall market capitalization of the country’s

equity market.

o Style-Based Investing: Market Capitalization

o Non-Style-Based

Focus is not a particular group of stocks but involve a search for stocks with the

best chance of meeting particular objectives. There basically three approaches

are:

• Pure Fundamental

• Pure Quantitative

• Pure Technical

These approaches try to identify the best stocks regardless of style, size, or any

other consideration except, possibly, the stock’s contribution to overall portfolio

risk and diversification

o Non-Style Based Investing - Pure Fundamental

Pure Fundamental. This approach involves analysis of the company’s

historical and projected financial performance and valuation.

Usually involves an in-depth look at the company’s financial statements, with a

focus on earnings growth and cash flow, as well as the quality of the company’s

management and other factors.

The decision to buy or sell a stock is often based on an estimate of the stock’s

true value compared with the stock’s market price.

Approach is related to the value style because stocks are considered for purchase

based on intrinsic value. i.e. inexpensive or true value.

Pure Quantitative. The pure quantitative approach combines historical

fundamental data (earnings, cash flow, book value, etc.) with a statistical

analysis using computer-based models to identify the best stocks according to

specific criteria.

Large investment house employ quantitative analysts who regularly

communicate list of recommended stocks based on their analysis to clients e.g.,

ARM, Stanbic IBTC, Meristem

o Non-Style Based Investing - Pure Quantitative

o Non-Style Based Investing - Pure Technical

This approach assumes that all known market influences are fully reflected in

market prices and that nothing is to be gained by conducting fundamental

analysis.

Technicians analyze historical market action to determine probable future price

trends.

Many large investment dealers employ technical analysts who recommend stocks

based on technical indicators.

• Top-Down Approaches

begins with a focus on the attributes of individual stocks, the top-down approach

begins with an analysis of large scale factors.

A top-down approach may be either :

oMacroeconomic Approach

o Style-based Approach

o Top-Down : Macroeconomic Approach

This traditional top-down approach to selecting stocks begins with macro- and

microeconomic analysis of trends and market forecasts in the global, regional

and national economies.

Then selection of industries or sectors with the potential to outperform other

sectors given the expected economic outlook.

Premise that the fortunes of economic sectors ebb and flow in response to

changes in the economic cycle and that the investor or portfolio manager is able

to pick the sector most likely to experience superior growth.

Such an investor is likely to be characterized a sector rotator or market timer.

o Top-Down : Style-Based Approach

The Style-based Approach selects stocks from whichever style is expected to

perform best given the analysis of the large scale factors and capital market

factors.

At times, this may require a focus on small-cap value stocks, while at other

times it could mean focusing on large-cap growth stocks.

• Passive Equity Portfolio Management

Long-term buy-hold Strategy

Usually tracks an index over time

Designed to match market performance

Manager is judged on how well target index is tracked

• Active Equity Portfolio Management

Attempts at outperforming a passive benchmark portfolio on a risk

adjusted basis

Passive vs. Active Management