Embed Size (px)

Citation preview

Asset Allocation Report

Joe and Jane Sample-AffluentRidgefield, Connecticut

PREPARED BY:LINDA HAMILTON - HAMILTON FINANCIAL ADVISORS

MAY 20, 2010

Table of Contents

Asset Allocation Overview.............................................................................................................. 5

Risk Tolerance Analysis.................................................................................................................. 7

Asset Class Details....................................................................................................................... 10

Account Details........................................................................................................................... 11

Current Asset Mix........................................................................................................................ 12

Current Portfolio Breakdown........................................................................................................ 13

Asset Allocation for Entire Portfolio............................................................................................... 15

Efficient Frontier Analysis ............................................................................................................ 16

Asset Allocation Considerations.................................................................................................... 17

Range of Returns........................................................................................................................ 18

Conclusion.................................................................................................................................. 19

Important Terminology................................................................................................................ 20

Disclaimer................................................................................................................................... 23

Client Information

Family InformationClientName Joe Sample-AffluentDate of Birth Oct 1 1960Gender MaleAddress 123 Orchid Drive

Ridgefield, Connecticut 12345United States

Citizenship United States

Name Jane Sample-AffluentDate of Birth Sep 15 1962Gender FemaleAddress 123 Orchid Drive

Ridgefield, Connecticut 12345United States

Citizenship United States

DependentsName Julia Sample-AffluentDate of Birth Jan 4 1995Gender FemaleAddress 123 Orchid Drive

Ridgefield, Connecticut 12345United States

Dependent of Joe and Jane

Name Mark Sample-AffluentDate of Birth Apr 23 1996Gender MaleAddress 123 Orchid Drive

Ridgefield, Connecticut 12345United States

Dependent of Joe and Jane

Professional Advisors

Type NameBusinessPhone # Cell Phone #

Advisor Linda Hamilton (555) 555-1234 (555) 555-4321

Important: The calculations or other information generated by NaviPlan® version 12.0 regarding the likelihood of variousinvestment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees offuture results. These calculations are shown for illustrative purposes only because they utilize return data that may notinclude fees or operating expenses, and are not available for investment. If included, fees and other operating expenseswould materially reduce these calculations. See the Disclaimers section for more information.

Page 4 of 25

Asset Allocation Overview

What is Asset Allocation?Asset allocation is the process of aligning your risk tolerances, financial objectives, and investment timehorizon to your investment portfolio. Selecting different asset types (commonly known as asset classes)may reduce the risk of your overall investment portfolio.

The three most common asset types (classes) are as follows:

• Cash or short-term investments (savings accounts, money market accounts, etc.)

• Fixed Income investments (CDs, bonds, etc.)

• Equities (domestic and foreign stock, etc.)Each of these three asset classes can be further subdivided. For example, equities may be brokendown by size (small, medium or large capitalized companies), different sectors of the economy(technology, financial services, etc.) or be divided geographically (US, Europe, Asia, etc.).

The decision of how to allocate your investments depends on a number of factors including yourinvestment objectives, time horizon, attitudes toward acceptable risk, desired return and tax bracket.

The basic premise of asset allocation is that by diversifying your investments over a number ofdifferent assets and asset classes, you can help reduce the risk of the entire portfolio while maintainingyour desired long-term return rate expectations. Over the long term, an appropriate asset allocation(what to buy) is more important than when to buy. Generally, a decline in one asset class can be offsetby an increase in another. Your choice of individual investments can also help reduce the risk of yourportfolio. For example, if you diversify within each asset class and choose a number of stocks acrossdifferent industries, your technology stock may be declining while your financial services stock may berising. This strategy can also help reduce overall portfolio risk as opposed to investing all of your stocksin a single company or sector of the economy.

Studies have shown selection of a portfolio's asset allocation can be responsible for over 90% of aportfolio's performance with the remaining portion comprised of market timing, security selection, andother factors.

Source: Brinson, Hood and Beebower, "Determinants of Portfolio Performance," Financial Analyst Journal, May-June 1991.

Important: The calculations or other information generated by NaviPlan® version 12.0 regarding the likelihood of variousinvestment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees offuture results. These calculations are shown for illustrative purposes only because they utilize return data that may notinclude fees or operating expenses, and are not available for investment. If included, fees and other operating expenseswould materially reduce these calculations. See the Disclaimers section for more information.

Page 5 of 25

Higher risk and higher potential return?Your overall comfort level with risk should be a major factor in choosing appropriate investments. It isimportant to consider that generally, achieving a higher rate of return requires accepting a higher levelof risk. Higher risk investments are generally appropriate for clients with more aggressive risk profilesand longer investment time horizons. If your financial objective is many years away (retirement, forexample) your investments may withstand the ups and downs of the market. If your goal is only a fewyears away (such as the purchase of a new car), your investment may decline during the period youwish to redeem the investments. Generally, as your financial goal approaches, you should reduce therisk of your investments by reallocating to a less aggressive asset mix.

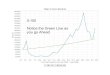

Why should you consider inflation?When planning for an accumulation goal, (retirement, education, or a major purchase) consider theeffect of inflation on the eventual cost of the item. If inflation is not considered, savings may fall shortof your goal. For example, an item that costs $1,000 today will cost $1,344 in 10 years, assuming a3% inflation rate. The graph below shows actual inflation rates for the past 95 years and the averageannual rate of inflation from 1914 to 2008 is 3.28%.

1914 1919 1924 1929 1934 1939 1944 1949 1954 1959 1964 1969 1974 1979 1984 1989 1994 1999 2004-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Inflation Annualized Inflation (to date)

Inflation History data obtained from the U.S. Department of Labor. Inflation rates are based on the Consumer Price Index.

Important: The calculations or other information generated by NaviPlan® version 12.0 regarding the likelihood of variousinvestment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees offuture results. These calculations are shown for illustrative purposes only because they utilize return data that may notinclude fees or operating expenses, and are not available for investment. If included, fees and other operating expenseswould materially reduce these calculations. See the Disclaimers section for more information.

Page 6 of 25

Risk Tolerance Analysis

Risk Tolerance Analysis results:

Portfolio Investment Profile Time Horizon

Entire Portfolio Moderate Very Long

Different investors have different risk tolerances. Much of the difference stems from time horizon. Thatis, someone with a short investment time horizon is less able to withstand losses. The remainder of thedifference is attributable to the individual’s appetite for risk. Volatility can be nerve-wracking for manypeople and they are more comfortable when they can avoid it. However, there is a definite relationshipbetween risk and return. Investors need to recognize this risk/return trade-off. The following risktolerance questionnaire has been designed to measure an individual’s ability (time horizon) andwillingness (risk tolerance) to accept uncertainties in their investment’s performance. The total scorerecommends which of the five risk profiles is most appropriate for the investor.

1. When do you expect to begin withdrawing money from your investment account?

PortfolioLess than 1

year 1 to 2 years 3 to 4 years 5 to 7 years8 to 10years

11 years ormore

Entire Portfolio X

2. Once you begin withdrawing money from your investment account, how long do you expect thewithdrawals to last?

Portfolio

I plan to takea lump sumdistribution 1 to 4 years 5 to 7 years 8 to 10 years

11 years ormore

Entire Portfolio X

3. Inflation, the rise in prices over time, can erode your investment return. Long-term investors shouldbe aware that, if portfolio returns are less than the inflation rate, their ability to purchase goods andservices in the future might actually decline. However, portfolios with long-term returns thatsignificantly exceed inflation are associated with a higher degree of risk.

Which of the following portfolios is most consistent with your investment philosophy?

a) Portfolio 1 will most likely exceed long-term inflation by a significant margin and has a high degreeof risk.

b) Portfolio 2 will most likely exceed long-term inflation by a moderate margin and has a high tomoderate degree of risk.

c) Portfolio 3 will most likely exceed long-term inflation by a small margin and has a moderate degreeof risk.

d) Portfolio 4 will most likely match long-term inflation and has a low degree of risk.

Portfolio Option a Option b Option c Option dEntire Portfolio X

Important: The calculations or other information generated by NaviPlan® version 12.0 regarding the likelihood of variousinvestment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees offuture results. These calculations are shown for illustrative purposes only because they utilize return data that may notinclude fees or operating expenses, and are not available for investment. If included, fees and other operating expenseswould materially reduce these calculations. See the Disclaimers section for more information.

Page 7 of 25

4. Portfolios with the highest average returns also tend to have the highest chance of short-termlosses. The table below provides the average dollar return of four hypothetical investments of $100,000and the possibility of losing money (ending value of less than $100,000) over a one-year holdingperiod. Please select the portfolio with which you are most comfortable.

Probabilities After 1 Year

Possible Average Value at theEnd of One Year

Chance of Losing Money atthe End of One Year

a. Portfolio A $105,000 24%

b. Portfolio B $107,000 27%

c. Portfolio C $108,000 29%

d. Portfolio D $110,000 31%

Portfolio Option a Option b Option c Option dEntire Portfolio X

5. Investing involves a trade-off between risk and return. Historically, investors who have received highlong-term average returns have experienced greater fluctuations in the value of their portfolio andmore frequent short-term losses than investors in more conservative investments have. Considering theabove, which statement best describes your investment goals?

a) Protect the value of my account. In order to minimize the chance for loss, I am willing toaccept the lower long-term returns provided by conservative investments.

b) Keep risk to a minimum while trying to achieve slightly higher returns than the returnsprovided by investments that are more conservative.

c) Balance moderate levels of risk with moderate levels of returns.

d) Maximize long-term investment returns. I am willing to accept large and sometimesdramatic fluctuations in the value of my investments.

Portfolio Statement a Statement b Statement c Statement dEntire Portfolio X

6. Historically, markets have experienced downturns, both short-term and prolonged, followed bymarket recoveries. Suppose you owned a well-diversified portfolio that fell by 20% (i.e. $1,000 initialinvestment would now be worth $800) over a short period, consistent with the overall market.Assuming you still have 10 years until you begin withdrawals, how would you react?

Portfolio

I would notchange myportfolio

I would wait atleast one year

before changing tooptions that are

more conservative

I would wait atleast three monthsbefore changing to

options that aremore conservative

I wouldimmediately

change to optionsthat are moreconservative

Entire Portfolio X

Important: The calculations or other information generated by NaviPlan® version 12.0 regarding the likelihood of variousinvestment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees offuture results. These calculations are shown for illustrative purposes only because they utilize return data that may notinclude fees or operating expenses, and are not available for investment. If included, fees and other operating expenseswould materially reduce these calculations. See the Disclaimers section for more information.

Page 8 of 25

7. The following graph shows the hypothetical results of four sample portfolios over a one-year holdingperiod. The best potential and worst potential gains and losses are presented. Note that the portfoliowith the best potential gain also has the largest potential loss. Which of these portfolios would youprefer to hold?

Portfolio Portfolio A Portfolio B Portfolio C Portfolio DEntire Portfolio X

8. I am comfortable with investments that may frequently experience large declines in value if there isa potential for higher returns.

Portfolio Agree Disagree Strongly disagreeEntire Portfolio X

Important: The calculations or other information generated by NaviPlan® version 12.0 regarding the likelihood of variousinvestment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees offuture results. These calculations are shown for illustrative purposes only because they utilize return data that may notinclude fees or operating expenses, and are not available for investment. If included, fees and other operating expenseswould materially reduce these calculations. See the Disclaimers section for more information.

Page 9 of 25

Asset Class Details

The Asset Class Details table provides a breakdown of the assumptions used to create the total rate ofreturn for each asset class in your analysis. It also provides the standard deviation for each individualasset class as a measure of risk.

Asset Class Details

Asset Class Interest DividendsCapitalGains Tax Free

DeferredGrowth Total

StandardDeviation

Large Cap Growth Equity 0.00% 2.44% 6.47% 0.00% 0.49% 9.40% 23.70%Large Cap Value Equity 0.00% 3.43% 4.37% 0.00% 2.92% 10.72% 18.54%Mid Cap Equity 0.00% 2.79% 7.30% 0.00% 1.00% 11.09% 23.71%Small Cap Equity 0.00% 1.96% 10.54% 0.00% 1.58% 14.08% 28.87%International Equity 0.00% 3.77% 4.69% 0.00% 1.92% 10.38% 24.82%Emerging Markets Equity 0.00% 3.44% 8.41% 0.00% 2.37% 14.22% 34.82%Long Term Bonds 4.58% 0.00% 0.00% 0.00% 0.00% 4.58% 11.87%Intermediate Term Bonds 4.03% 0.00% 0.00% 0.00% 0.00% 4.03% 6.67%Short Term Bonds 3.30% 0.00% 0.00% 0.00% 0.00% 3.30% 3.68%High Yield Bonds 8.17% 0.00% 0.00% 0.00% 0.00% 8.17% 15.23%International Bonds 4.25% 0.00% 0.00% 0.00% 0.00% 4.25% 10.86%Cash 2.81% 0.00% 0.00% 0.00% 0.00% 2.81% 3.09%

Important: The calculations or other information generated by NaviPlan® version 12.0 regarding the likelihood of variousinvestment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees offuture results. These calculations are shown for illustrative purposes only because they utilize return data that may notinclude fees or operating expenses, and are not available for investment. If included, fees and other operating expenseswould materially reduce these calculations. See the Disclaimers section for more information.

Page 10 of 25

Account Details

The table below provides a list of the holdings for each account in the current portfolio.

Description Value % of Account % of PortfolioJoe's 401(k)Columbus Silver $145,000 26.6% 8.4%Vanguard Long-Term Treasury Investor $200,000 36.7% 11.5%American Century Capital Val Inv $200,000 36.7% 11.5%Account Total $545,000 31.5%

Jane's 401(k)Microsoft $75,000 13.0% 4.3%Vanguard Windsor II Investor $250,000 43.5% 14.4%Accessor Income & Growth Allocation C $250,000 43.5% 14.4%Account Total $575,000 33.2%

Ridgefield Bank SavingsNew Holding $50,000 100.0% 2.9%Account Total $50,000 2.9%

Ridgefield Bank CheckingNew Holding $25,000 100.0% 1.4%Account Total $25,000 1.4%

Julia's Education PlanNew Holding $102,000 100.0% 5.9%Account Total $102,000 5.9%

Mark's Education PlanNew Holding $92,000 100.0% 5.3%Account Total $92,000 5.3%

Vacation TimeshareNew Holding $28,000 100.0% 1.6%Account Total $28,000 1.6%

Jane's Brokerage AccountAmerican Funds Bond Fund of Amer A $42,500 42.5% 2.5%DFA US Large Cap Value III $9,500 9.5% 0.5%Pfizer $48,000 48.0% 2.8%Account Total $100,000 5.8%

Joint SavingsNew Holding $215,000 100.0% 12.4%Account Total $215,000 12.4%

Portfolio Total $1,732,000 100.0%

Important: The calculations or other information generated by NaviPlan® version 12.0 regarding the likelihood of variousinvestment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees offuture results. These calculations are shown for illustrative purposes only because they utilize return data that may notinclude fees or operating expenses, and are not available for investment. If included, fees and other operating expenseswould materially reduce these calculations. See the Disclaimers section for more information.

Page 11 of 25

Current Asset Mix

This pie graph illustrates your current asset allocation mix. The table below provides a breakdown ofthe percentages and dollar values for each asset class in the current portfolio.

Current Asset Mix

Rate of Return 7.22%Standard Deviation 10.55%

Current Asset MixAsset Class (%) ($)Large Cap Growth Equity 7.7 134,000Large Cap Value Equity 29.9 518,720Mid Cap Equity 0.9 14,780International Equity 10.2 177,500Emerging Markets Equity 0.3 5,000Long Term Bonds 20.4 353,800Intermediate Term Bonds 2.8 48,000High Yield Bonds 4.6 79,500International Bonds 0.9 14,975Cash 22.3 385,725Total 100.0 1,732,000

Note: The reallocation table above does not reflect the tax effects that may occur when reallocating your assets; these tax effects areaccounted for at the end of the year.

© 2010 Ibbotson Associated, Inc., a wholly owned subsidiary of Morningstar, Inc. All rights reserved. EISI has engaged Ibbotson to developproprietary asset allocation tools for educational purposes. Ibbotson has granted to EISI a license for use thereof. Some assets in this reportmay have been classified based on returns-based style analysis and others may have been manually classified.

Important: The calculations or other information generated by NaviPlan® version 12.0 regarding the likelihood of variousinvestment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees offuture results. These calculations are shown for illustrative purposes only because they utilize return data that may notinclude fees or operating expenses, and are not available for investment. If included, fees and other operating expenseswould materially reduce these calculations. See the Disclaimers section for more information.

Page 12 of 25

Current Portfolio Breakdown

The table below provides a breakdown of the percentages and dollar values for each asset class in thecurrent portfolio.

Asset Class Holding Type

% ofAssetClass

% ofPortfolio Asset Value

Large Cap Growth EquityNew Holding Non-Qualified 4.2% 0.3% $5,600Accessor Income &Growth Allocation C

401(k) 22.4% 1.7% $30,000

American Century CapitalVal Inv

401(k) 3.0% 0.2% $4,000

Microsoft 401(k) 56.0% 4.3% $75,000New Holding 529 Plan 7.6% 0.6% $10,200New Holding 529 Plan 6.9% 0.5% $9,200

Total Large Cap Growth Equity 7.7% $134,000

Large Cap Value EquityDFA US Large Cap ValueIII

Non-Qualified 1.4% 0.4% $7,220

New Holding Non-Qualified 1.1% 0.3% $5,600Pfizer Non-Qualified 9.3% 2.8% $48,000Accessor Income &Growth Allocation C

401(k) 2.9% 0.9% $15,000

American Century CapitalVal Inv

401(k) 35.9% 10.7% $186,000

New Holding 529 Plan 2.0% 0.6% $10,200New Holding 529 Plan 1.8% 0.5% $9,200Vanguard Windsor IIInvestor

401(k) 45.8% 13.7% $237,500

Total Large Cap Value Equity 29.9% $518,720

Mid Cap EquityDFA US Large Cap ValueIII

Non-Qualified 15.4% 0.1% $2,280

Accessor Income &Growth Allocation C

401(k) 84.6% 0.7% $12,500

Total Mid Cap Equity 0.9% $14,780

International EquityAccessor Income &Growth Allocation C

401(k) 18.3% 1.9% $32,500

Columbus Silver 401(k) 81.7% 8.4% $145,000Total International Equity 10.2% $177,500

Emerging Markets EquityAccessor Income &Growth Allocation C

401(k) 100.0% 0.3% $5,000

Long Term BondsAmerican Funds BondFund of Amer A

Non-Qualified 1.4% 0.3% $5,100

New Holding Non-Qualified 30.4% 6.2% $107,500Accessor Income &Growth Allocation C

401(k) 2.8% 0.6% $10,000

American Century CapitalVal Inv

401(k) 1.7% 0.3% $6,000

New Holding 529 Plan 8.6% 1.8% $30,600New Holding 529 Plan 7.8% 1.6% $27,600

Important: The calculations or other information generated by NaviPlan® version 12.0 regarding the likelihood of variousinvestment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees offuture results. These calculations are shown for illustrative purposes only because they utilize return data that may notinclude fees or operating expenses, and are not available for investment. If included, fees and other operating expenseswould materially reduce these calculations. See the Disclaimers section for more information.

Page 13 of 25

Asset Class Holding Type

% ofAssetClass

% ofPortfolio Asset Value

Large Cap Growth EquityVanguard Long-TermTreasury Investor

401(k) 45.8% 9.4% $162,000

Vanguard Windsor IIInvestor

401(k) 1.4% 0.3% $5,000

Total Long Term Bonds 20.4% $353,800

Intermediate Term BondsAmerican Funds BondFund of Amer A

Non-Qualified 14.2% 0.4% $6,800

New Holding Non-Qualified 23.3% 0.6% $11,200Vanguard Long-TermTreasury Investor

401(k) 62.5% 1.7% $30,000

Total Intermediate Term Bonds 2.8% $48,000

High Yield BondsAmerican Funds BondFund of Amer A

Non-Qualified 19.2% 0.9% $15,300

New Holding 529 Plan 38.5% 1.8% $30,600New Holding 529 Plan 34.7% 1.6% $27,600Vanguard Long-TermTreasury Investor

401(k) 7.5% 0.3% $6,000

Total High Yield Bonds 4.6% $79,500

International BondsAmerican Funds BondFund of Amer A

Non-Qualified 19.9% 0.2% $2,975

Accessor Income &Growth Allocation C

401(k) 66.8% 0.6% $10,000

Vanguard Long-TermTreasury Investor

401(k) 13.4% 0.1% $2,000

Total International Bonds 0.9% $14,975

CashAmerican Funds BondFund of Amer A

Non-Qualified 3.2% 0.7% $12,325

New Holding Non-Qualified 13.0% 2.9% $50,000New Holding Non-Qualified 6.5% 1.4% $25,000New Holding Non-Qualified 1.5% 0.3% $5,600New Holding Non-Qualified 27.9% 6.2% $107,500Accessor Income &Growth Allocation C

401(k) 35.0% 7.8% $135,000

American Century CapitalVal Inv

401(k) 1.0% 0.2% $4,000

New Holding 529 Plan 5.3% 1.2% $20,400New Holding 529 Plan 4.8% 1.1% $18,400Vanguard Windsor IIInvestor

401(k) 1.9% 0.4% $7,500

Total Cash 22.3% $385,725Total Portfolio 100.0% $1,732,000

© 2010 Ibbotson Associated, Inc., a wholly owned subsidiary of Morningstar, Inc. All rights reserved. EISI has engaged Ibbotson to developproprietary asset allocation tools for educational purposes. Ibbotson has granted to EISI a license for use thereof. Some assets in this reportmay have been classified based on returns-based style analysis and others may have been manually classified.

Important: The calculations or other information generated by NaviPlan® version 12.0 regarding the likelihood of variousinvestment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees offuture results. These calculations are shown for illustrative purposes only because they utilize return data that may notinclude fees or operating expenses, and are not available for investment. If included, fees and other operating expenseswould materially reduce these calculations. See the Disclaimers section for more information.

Page 14 of 25

Asset Allocation for Entire Portfolio

These pie graphs illustrate your current asset mix and suggested asset mix for your entire portfolio.

Current Asset Mix Suggested Asset MixModerate

Rate of Return 7.22%Standard Deviation 10.55%

Rate of Return 8.21%Standard Deviation 13.30%

The table below provides a breakdown of the percentages and dollar values for each asset class in thecurrent and suggested asset mix. The Change column indicates the rebalancing required to reach thesuggested asset mix.

Current Asset Mix Change Suggested Asset MixAsset Class (%) ($) (%) ($) (%) ($)Large Cap Growth Equity 7.7 134,000 +4.3 +73,840 12.0 207,840Large Cap Value Equity 29.9 518,720 -13.9 -241,600 16.0 277,120Mid Cap Equity 0.9 14,780 +9.1 +158,420 10.0 173,200Small Cap Equity +6.0 +103,920 6.0 103,920International Equity 10.2 177,500 +2.8 +47,660 13.0 225,160Emerging Markets Equity 0.3 5,000 +2.7 +46,960 3.0 51,960Long Term Bonds 20.4 353,800 -14.4 -249,880 6.0 103,920Intermediate Term Bonds 2.8 48,000 +10.2 +177,160 13.0 225,160Short Term Bonds +10.0 +173,200 10.0 173,200High Yield Bonds 4.6 79,500 -1.6 -27,540 3.0 51,960International Bonds 0.9 14,975 +2.1 +36,985 3.0 51,960Cash 22.3 385,725 -17.3 -299,125 5.0 86,600Total 100.0 1,732,000 +0.0 +0 100.0 1,732,000

Note: The reallocation table above does not reflect the tax effects that may occur when reallocating your assets; these tax effects areaccounted for at the end of the year.

© 2010 Ibbotson Associated, Inc., a wholly owned subsidiary of Morningstar, Inc. All rights reserved. EISI has engaged Ibbotson to developproprietary asset allocation tools for educational purposes. Ibbotson has granted to EISI a license for use thereof. Some assets in this reportmay have been classified based on returns-based style analysis and others may have been manually classified.

Consider the following:• Discuss the potential tax consequences of re-allocating your current investment portfolio with your

tax advisor.

• Review your portfolio at least once a year or as your financial circumstances change.

• Make sure your portfolio is properly diversified to help reduce portfolio volatility.

• Determine if your investments within each asset class have been achieving acceptable performancerelative to appropriate benchmarks.

• Income identified as tax-free may still be subject to the Alternative Minimum Tax (AMT).

Important: The calculations or other information generated by NaviPlan® version 12.0 regarding the likelihood of variousinvestment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees offuture results. These calculations are shown for illustrative purposes only because they utilize return data that may notinclude fees or operating expenses, and are not available for investment. If included, fees and other operating expenseswould materially reduce these calculations. See the Disclaimers section for more information.

Page 15 of 25

Efficient Frontier Analysis

The efficient frontier refers to all of the investment portfolios that provide the highest return for a givenamount of risk (measured by standard deviation) and is shown in the graph below by a green line. Alight blue diamond denotes your current portfolio. If the efficient frontier line is above your portfolio,you may be able to obtain a better rate of return for the level of risk you are willing to accept. Theyellow circle denotes our proposed portfolio.

Alternative model portfolios are also plotted on this graph. These additional points on the graphillustrate the risk and return associated with the other portfolios. Remember, only those portfoliosalong the efficient frontier line provide you with the greatest potential return for a given level of risk.

6% 7% 8% 9% 10% 11% 12% 13% 14% 15% 16% 17% 18% 19% 20% 21%Standard Deviation (Risk)

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

Rat

e of

Ret

urn

Efficient Frontier

Current - Rebalanced

Suggested Asset Mix

Conservative

Moderate Conservative

Moderate

Moderate Aggressive

Aggressive

The table below provides the actual values for the points on the graph above.

Return RiskCurrent Asset Mix 7.22% 10.55%Suggested Asset Mix 8.21% 13.30%Conservative 5.27% 6.31%Moderate Conservative 6.70% 9.50%Moderate 8.21% 13.30%Moderate Aggressive 9.64% 17.24%Aggressive 10.82% 20.65%

Important: The calculations or other information generated by NaviPlan® version 12.0 regarding the likelihood of variousinvestment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees offuture results. These calculations are shown for illustrative purposes only because they utilize return data that may notinclude fees or operating expenses, and are not available for investment. If included, fees and other operating expenseswould materially reduce these calculations. See the Disclaimers section for more information.

Page 16 of 25

Asset Allocation Considerations

Asset ReallocationWhile the proposed allocation may be subject to more or less risk, it may also generate a higher orlower rate of return as compared to your current portfolio. The proposed allocation serves as abeginning for your discussions with your advisor.

It is important to note that reallocating non-qualified investments may trigger an additional tax liability.Please review the Income Tax Summary for more information.

Future ContributionsConsider allocating future contributions to those asset classes currently under-weighted. Once yourportfolio reaches your desired allocation, you can align your contributions to match the proposedallocation.

RebalancingMarket activity may cause one asset class to become a greater percentage of the portfolio. Periodicrebalancing helps ensure that your portfolio continues to reflect your desired target asset allocation.Rebalancing ensures that you do not end up overexposed in one type of investment or asset class.

Rebalancing should be done at regular intervals far enough apart to avoid adjustments based onshort-term fluctuations. Reviews should be done frequently enough to keep on track, usually annually.The portfolio should be examined if the allocation deviates over five percent from the original proposedallocation.

Mortality and Expense (M&E) FeesThe rates of return have not been adjusted to included mortality and expense fees attributable tovariable annuities. These fees, and their effects on asset growth, are accounted for as a monthlyexpense of the annuity contract and can be observed in applicable Net Worth reports.

Important: The calculations or other information generated by NaviPlan® version 12.0 regarding the likelihood of variousinvestment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees offuture results. These calculations are shown for illustrative purposes only because they utilize return data that may notinclude fees or operating expenses, and are not available for investment. If included, fees and other operating expenseswould materially reduce these calculations. See the Disclaimers section for more information.

Page 17 of 25

Range of Returns

The following graph illustrates the potential range of returns on investments in your proposedinvestment portfolio. There is a 90% chance your returns over each time period will fall within thegiven range. Assuming the returns are normally distributed, there is a 5% chance you couldoutperform the highest return shown here, as well as a 5% chance you could underperform the lowestreturn shown here. The longer the time period of measurement, the narrower the range of returns.These results assume a buy-and-hold approach to the portfolio over each of the time periodsillustrated.

1 5 10 15 20Year

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

Ret

urn

Perc

enta

ge

Upper Bound Average Return Lower Bound

1 Year 5 Years 10 Years 15 Years 20 Years5th Percentile* 34.81% 20.11% 16.63% 15.08% 14.16%Average Return 8.21% 8.21% 8.21% 8.21% 8.21%95th Percentile** -18.38% -3.68% -0.20% 1.35% 2.27%

* You have a 5% chance of earning a higher return than what is shown over the applicable timeperiod.** You have a 5% chance of earning a lower return than what is shown over the applicable timeperiod.

Important: The calculations or other information generated by NaviPlan® version 12.0 regarding the likelihood of variousinvestment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees offuture results. These calculations are shown for illustrative purposes only because they utilize return data that may notinclude fees or operating expenses, and are not available for investment. If included, fees and other operating expenseswould materially reduce these calculations. See the Disclaimers section for more information.

Page 18 of 25

Conclusion

Now that you have an overview of your current asset allocation, where do you go from here? Ourrecommendations are as follows:

• Review this document – Ensure you understand the information contained in the report. Be sureto ask us questions on areas that need clarification.

• Decide on a course of action – Together, we will evaluate the asset reallocation strategy so thatit is consistent with your objectives and your financial ability.

Just as with any strategy or analysis, you must be diligent about updating the plan. Working with youradvisor, you should review your current asset allocation regularly - annually at a minimum, orwhenever changes in your financial situation warrant a review.

Important: The calculations or other information generated by NaviPlan® version 12.0 regarding the likelihood of variousinvestment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees offuture results. These calculations are shown for illustrative purposes only because they utilize return data that may notinclude fees or operating expenses, and are not available for investment. If included, fees and other operating expenseswould materially reduce these calculations. See the Disclaimers section for more information.

Page 19 of 25

Important Terminology

Rate of return (current asset mix)

The dollar-weighted average rate of return of the assets in the current asset mix.

Rate of return (suggested asset mix)

The rate of return that is calculated based on the investment profile as determined by answers to a risktolerance questionnaire.

Standard deviation

Standard deviation is a statistical measure of the volatility of an asset or account. It measures thedegree to which the rate of return in any one year varies from the historical average rate of return forthat investment; the greater the standard deviation, the riskier the investment.

Investment profile

The investment profile is the result of an analysis of an individual’s investment objectives, time horizon,and risk tolerance in reference to investing.

Portfolio

The combination of assets a client owns.

Time horizon

The length of time desired to achieve a financial goal. A longer time horizon usually allows an individualto withstand more volatility, whereas a shorter time horizon typically requires less volatility and moreliquidity.

Asset mix

The combination of asset classes within an investment portfolio. It can also be a further division withinan asset class of assets such as a mix of small, medium, and large company stock assets.

Current asset mix

The combination of asset classes assigned to the assets included in the current plan.

Suggested asset mix

The asset mix that is derived based on the investment profile as determined by answers to a risktolerance questionnaire.

Entire portfolio

The entire portfolio for the current plan represents the asset mix of all accounts in the plan. The entireportfolio for the proposed plan is the combined suggested and assumed asset mixes.

Uniform Transfer to Minors Act (UTMA) and Uniform Gift to Minors Act (UGMA)

UTMA and UGMA are custodial accounts, owned by a minor with an adult designated as the custodian.The accounts are normally used to save for the child's education. Once the transfer to the accountoccurs, the account is the legal property of the child and can only be used for the child's benefit. Whenthe child reaches the age of majority, control of the account transfers to the child and the child can usethe proceeds as he or she wishes. The UTMA considers the age of majority to be 21 although it is 18 insome states.

Important: The calculations or other information generated by NaviPlan® version 12.0 regarding the likelihood of variousinvestment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees offuture results. These calculations are shown for illustrative purposes only because they utilize return data that may notinclude fees or operating expenses, and are not available for investment. If included, fees and other operating expenseswould materially reduce these calculations. See the Disclaimers section for more information.

Page 20 of 25

Asset class

A category of investments grouped according to common characteristics such as relative liquidity,income characteristics, tax status, and growth characteristics.

Large Cap Growth Equity

Domestic U.S. equity stocks representing securities with a greater-than-average growth orientation,which tend to exhibit higher price-to-book and price-earnings ratios, lower dividend yields, and higherforecasted growth values.

Large Cap Value Equity

Domestic U.S. equity stocks representing securities with a less-than-average growth orientation, whichgenerally have lower price-to-book and price-earnings ratios, higher dividend yields, and lowerforecasted growth values.

Mid Cap Equity

Domestic U.S. equity stocks representing the Russell Mid Cap Index, which consists of the smallest 800companies in the Russell 1000 index as ranked by total market capitalization.

Small Cap Equity

Domestic U.S. equity stocks representing the Russell 2000 Index, which is a small-cap index consistingof the smallest 2,000 companies in the Russell 3000 Index.

International Equity

Stocks representing the MSCI EAFE (Europe, Australasia, Far East) Index, which is a free float-adjustedmarket capitalization index designed to measure developed market equity performance, excluding theU.S. and Canada.

Emerging Markets Equity

Equities representing the MSCI Emerging Markets Index, which is a free float-adjusted marketcapitalization index designed to measure equity market performance in the global emerging markets.

Long-Term Bonds

Bonds where the total returns are calculated for each year on a single bond issued by the U.S.Government with a term of approximately 20 years, and a reasonably current coupon with returns thatdid not reflect potential tax benefits, impaired negotiability, or special redemption or call privileges.

Intermediate-Term Bonds

These bonds represent one-bond portfolios used to construct the intermediate-term index. The bondchosen each year is the shortest non-callable bond with a maturity of not less than five years, and it is“held” for the calendar year.

Short-Term Bonds – U.S. 1-Year Government Bonds

Bonds represent yields on Treasury securities at “constant maturity” and are interpolated by the U.S.Treasury from the daily yield curve. This curve relates the yield on a security to its time to maturity,and is based on the closing market bid yields on actively traded Treasury securities in theover-the-counter market.

High-Yield Bonds

Bonds representing the universe of fixed rate, noninvestment grade debt.

International Bonds

Bonds reflecting the returns provided by investment in international (non-U.S.) fixed income securities.

Important: The calculations or other information generated by NaviPlan® version 12.0 regarding the likelihood of variousinvestment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees offuture results. These calculations are shown for illustrative purposes only because they utilize return data that may notinclude fees or operating expenses, and are not available for investment. If included, fees and other operating expenseswould materially reduce these calculations. See the Disclaimers section for more information.

Page 21 of 25

Cash

Cash reflects the returns provided by short-term fixed income instruments. The index is based on theU.S. 3-month Treasury bills.

Important: The calculations or other information generated by NaviPlan® version 12.0 regarding the likelihood of variousinvestment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees offuture results. These calculations are shown for illustrative purposes only because they utilize return data that may notinclude fees or operating expenses, and are not available for investment. If included, fees and other operating expenseswould materially reduce these calculations. See the Disclaimers section for more information.

Page 22 of 25

Disclaimer

IMPORTANT: Please read this section carefully. It contains an explanation of some of thelimitations of this report.

IMPORTANT: The calculations or other information generated by NaviPlan regarding the likelihood ofvarious investment outcomes are hypothetical in nature, do not reflect actual investment results, andare not guarantees of future results.

Below is an outline of several specific limitations of the calculations of financial models ingeneral and of NaviPlan specifically.

The Calculations Contained in This Report Depend in Part, on Personal Data That You Provide

The assumptions used in this assessment are based on information provided and reviewed by you.These assumptions must be reconsidered on a frequent basis to ensure the results are adjustedaccordingly. The smallest of changes in assumptions can have a dramatic impact on the outcome ofthis assessment. Any inaccurate representation by you of any facts or assumptions used in thisassessment invalidates the results.

This Report is Not a Comprehensive Financial Report and Does Not Include, Among Other Things, aReview of Your Insurance Policies

We have made no attempt to review your property and liability insurance policies (auto andhomeowners, for example). We strongly recommend that in conjunction with this assessment, youconsult with your property and liability agent to review your current coverage to ensure it continues tobe appropriate. In doing so, you may wish to review the dollar amount of your coverage, thedeductibles, the liability coverage (including an umbrella policy), and the premium amounts.

NaviPlan Does Not Constitute Legal, Accounting, or Tax Advice

This assessment does not constitute advice in the areas of legal, accounting or tax. It is yourresponsibility to consult with the appropriate professionals in those areas either independently or inconjunction with this assessment process.

Circular 230: Any income tax, estate tax or gift tax advice contained within this document was notintended or written to be used for, and cannot be used for, the purpose of avoiding penalties that maybe imposed.

Discussion of the Limits of Financial Modeling

Inherent Limitations in Financial Model Results

Investment outcomes in the real world are the result of a near infinite set of variables, few of whichcan be accurately anticipated. Any financial model, such as NaviPlan, can only consider a small subsetof the factors that may affect investment outcomes and the ability to accurately anticipate those fewfactors is limited. For these reasons, investors should understand that the calculations made in thisassessment are hypothetical, do not reflect actual investment results, and are not guarantees of futureresults.

Results May Vary With Each Use and Over Time

The results presented in this assessment are not predictions of actual results. Actual results may varyto a material degree due to external factors beyond the scope and control of this assessment. Historicaldata may have been used to produce future assumptions used in the assessment, such as rates ofreturn. Utilizing historical data has limitations as past performance is not a guarantee or predictor offuture performance.

Important: The calculations or other information generated by NaviPlan® version 12.0 regarding the likelihood of variousinvestment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees offuture results. These calculations are shown for illustrative purposes only because they utilize return data that may notinclude fees or operating expenses, and are not available for investment. If included, fees and other operating expenseswould materially reduce these calculations. See the Disclaimers section for more information.

Page 23 of 25

Outline of the Limitations of NaviPlan and Financial Modeling

Your Future Resources and Needs May Be Different From the Estimates That You Provide

This assessment is intended to help you in making decisions on your financial future based, in part, oninformation that you have provided and reviewed. The proposed asset allocation presented in thisassessment is based, in part, on your answers to a risk tolerance questionnaire and may represent amore aggressive—and therefore more risky—investment strategy than your current asset allocationmix.

The calculations contained in the report utilize the information that you have provided and reviewedincluding, but not limited to, your age, tolerance for investment risk, income, assets, liabilities,anticipated expenses, and likely retirement age. Some of this information may change in unanticipatedways in the future and those changes may make NaviPlan less useful.

NaviPlan Considers Investment in Only a Few Broad Investment Categories

NaviPlan utilizes this information to estimate your future needs and financial resources and to identifyan allocation of your current and future resources, given your tolerance for investment risk, to a fewbroad investment categories: large-cap equity, mid-cap equity, small-cap equity, international equity,emerging equity, bonds, and cash.

In general, NaviPlan favors the investment categories that have higher historical and expected returns.The extent of the recommended allocation to these favored investment categories is limited by theinvestor’s disclosed tolerance for risk. In general, higher returns are associated with higher risk.

These broad investment categories are not specific securities, funds, or investment products andNaviPlan is not an offer or solicitation to purchase any securities or investment products. The assumedrates of return of these broad categories are based on the returns of indices. These indices do notinclude fees or operating expenses and are not available for investment. These indices are unmanagedand the returns are shown for illustrative purposes only.

It is important to note that the broad categories that are used are not comprehensive and otherinvestments that are not considered may have characteristics that are similar or superior to thecategories that are used in NaviPlan.

NaviPlan Calculates Investment Returns Far Into the Future Using Ibbotson Data

For all asset class forecasts, Ibbotson uses the building block approach to generate expected returnestimates. The building block approach uses current market statistics as its foundation and addshistorical performance relationships to build expected return forecasts. This approach separates theexpected return of each asset class into three components: the real risk-free rate, expected inflation,and risk premia. The real risk-free rate is the return that can be earned without incurring any default orinflation risk. Expected inflation is the additional reward demanded to compensate investors for futureprice increases, and risk premia measures the additional reward demanded for accepting uncertaintyassociated with investing in a given asset class. Any calculation of future returns of any asset category,including any calculation using historical returns as a guide, has severe limitations. Changes in marketconditions or economic conditions can cause investment returns in the future to be very different fromreturns in the past. Returns realized in the future can, in fact, be much lower, or even negative, for allor some of these asset categories and, if so, the calculations in NaviPlan will be less useful.

Any assets, including the broad asset categories considered in NaviPlan, that offer potential profits alsoentail the possibility of losses.

Important: The calculations or other information generated by NaviPlan® version 12.0 regarding the likelihood of variousinvestment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees offuture results. These calculations are shown for illustrative purposes only because they utilize return data that may notinclude fees or operating expenses, and are not available for investment. If included, fees and other operating expenseswould materially reduce these calculations. See the Disclaimers section for more information.

Page 24 of 25

Furthermore, it is significant that the historical data for these investment categories does not reflectinvestment fees or expenses that an investor would pay when investing in securities or investmentproducts. The fees and expenses would significantly reduce net investment returns and a calculationtaking account of fees and expenses would result in lower expected asset values in the future.

NaviPlan Calculations Include Limited Accounting for Taxes

The federal and state income tax laws are extremely complex and subject to continuous change.NaviPlan has limited capability to model any individual’s tax liability, and future tax laws may besignificantly different from current tax laws. Any changes in tax law may affect returns for any giveninvestment and make the calculations produced by NaviPlan less useful. The calculations containlimited support for the tax impact on transfers of money or redemptions of funds.

NaviPlan Calculations Do Not Include Fees and Expenses

The calculations utilize return data that do not include fees or operating expenses. If included, fees andother operating expenses would materially reduce these calculations. Recommendations included in thecalculations to redeem funds from certain investments or transfer money to others do not account forfees and charges that may be incurred.

NaviPlan Calculations May Include Variable Products

Variable life insurance policies or deferred variable annuities are inherently risky and may be includedin the calculations. The return rate assumptions used throughout this analysis do not relate to theunderlying product illustrated. These returns should not be used as a proxy for actual performance asthey may exaggerate the performance potential of the underlying investment accounts (subaccounts).Any calculations incorporating variable products are hypothetical and intended to show how theperformance of the underlying subaccounts could affect the value and death benefit of the variableproducts; these calculations are not intended to predict or project investment results.

The rates of return have not been adjusted to include mortality and expense fees attributable tovariable annuities. These fees, and their effects on asset growth, are accounted for as a monthlyexpense of the annuity contract and can be observed in applicable net worth reports.

If a variable annuity included in this analysis contains a guaranteed minimum withdrawal rider, it isimportant to understand that if the contract value is greater than the guaranteed minimum withdrawalbenefit once withdrawals begin, as an investor you will have paid for the rider and not actually used it.

Income taxes during the annuitization phase are accounted for in the calculations. See the sectiontitled NaviPlan Calculations Include Limited Accounting for Taxes in this Disclaimer for furtherinformation on the tax methodology used.

Important: The calculations or other information generated by NaviPlan® version 12.0 regarding the likelihood of variousinvestment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees offuture results. These calculations are shown for illustrative purposes only because they utilize return data that may notinclude fees or operating expenses, and are not available for investment. If included, fees and other operating expenseswould materially reduce these calculations. See the Disclaimers section for more information.

Page 25 of 25