Embed Size (px)

Citation preview

Arezzo&Co Investor Day

2016

AG

EN

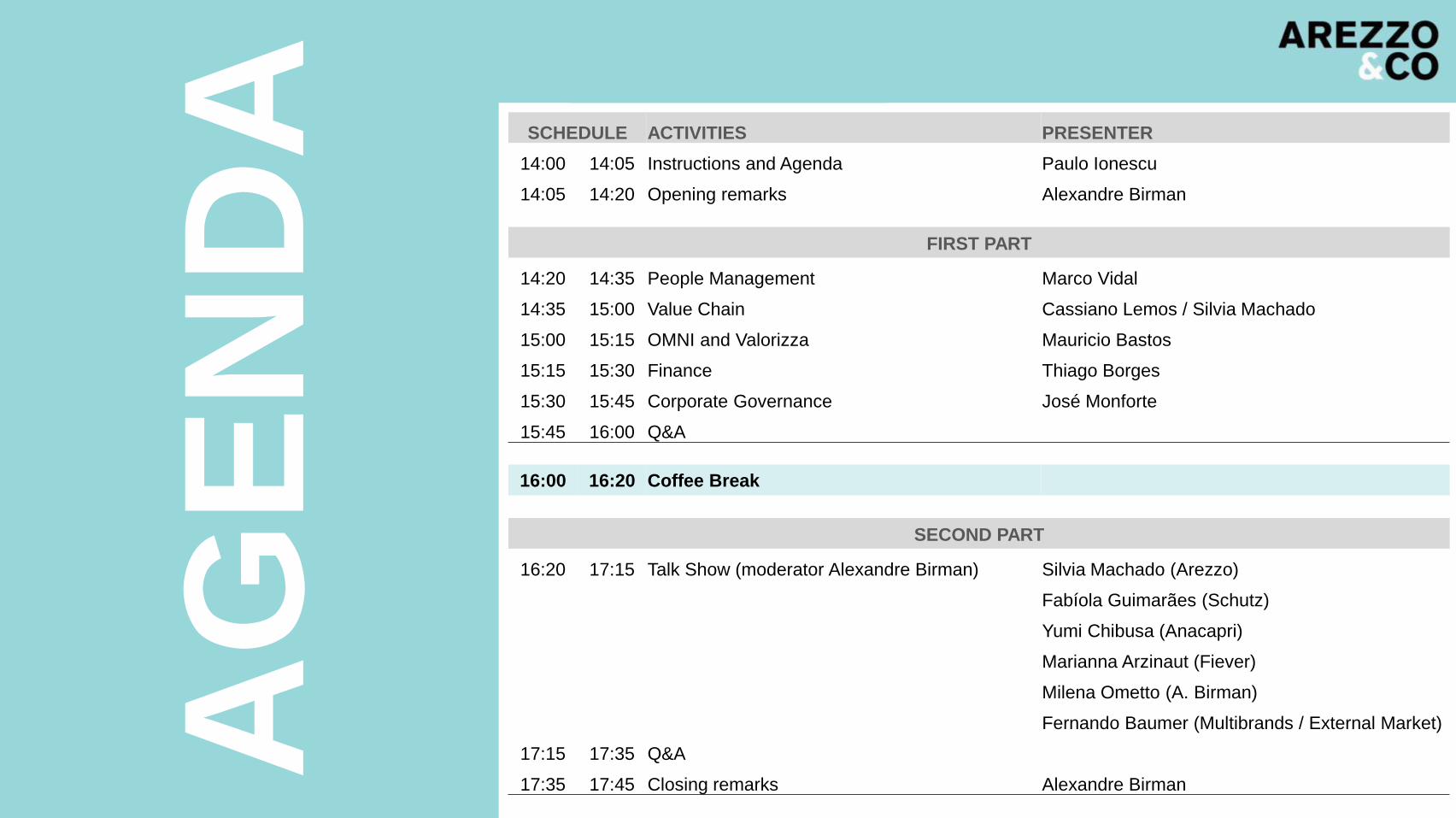

DA SCHEDULE ACTIVITIES PRESENTER

14:00 14:05 Instructions and Agenda Paulo Ionescu

14:05 14:20 Opening remarks Alexandre Birman

FIRST PART

14:20 14:35 People Management Marco Vidal

14:35 15:00 Value Chain Cassiano Lemos / Silvia Machado

15:00 15:15 OMNI and Valorizza Mauricio Bastos

15:15 15:30 Finance Thiago Borges

15:30 15:45 Corporate Governance José Monforte

15:45 16:00 Q&A

16:00 16:20 Coffee Break

SECOND PART

16:20 17:15 Talk Show (moderator Alexandre Birman) Silvia Machado (Arezzo)

Fabíola Guimarães (Schutz)

Yumi Chibusa (Anacapri)

Marianna Arzinaut (Fiever)

Milena Ometto (A. Birman)

Fernando Baumer (Multibrands / External Market)

17:15 17:35 Q&A

17:35 17:45 Closing remarks Alexandre Birman

Arezzo&Co Investor DayOpening remarks

Alexandre BirmanCEO

December 9th, 2016

4

Opening RemarksReference platform of brands

The Company has a strong portfolio of Top of Mind brands within Brazil

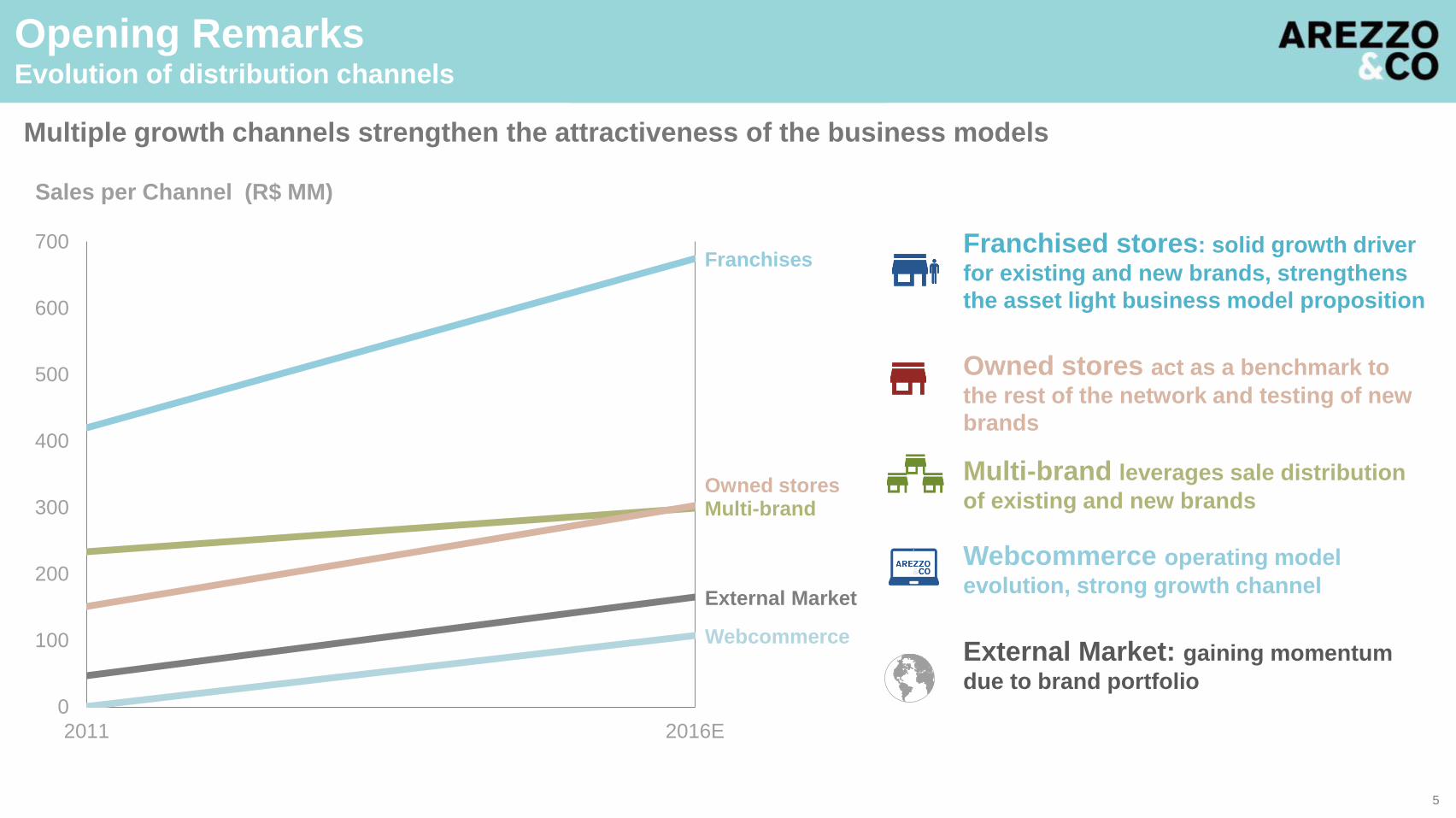

Franchises

Multi-brandOwned stores

External Market

Webcommerce

0

100

200

300

400

500

600

700

2011 2016E

Sales per Channel (R$ MM)

Franchised stores: solid growth driver

for existing and new brands, strengthens

the asset light business model proposition

Owned stores act as a benchmark to

the rest of the network and testing of new

brands

Webcommerce operating model

evolution, strong growth channel

External Market: gaining momentum

due to brand portfolio

Multi-brand leverages sale distribution

of existing and new brands

Multiple growth channels strengthen the attractiveness of the business models

Opening RemarksEvolution of distribution channels

5

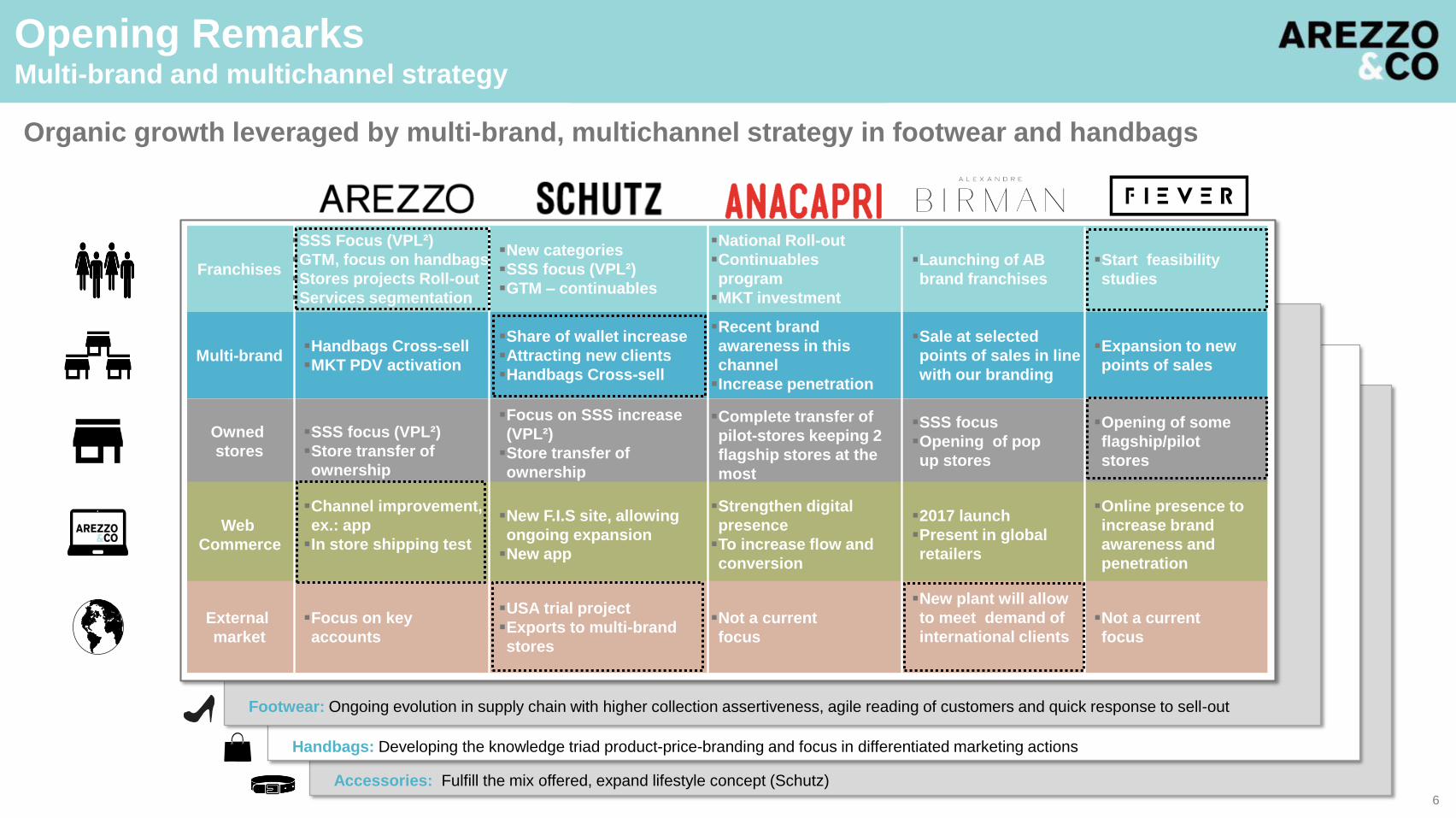

Opening RemarksMulti-brand and multichannel strategy

Footwear: Ongoing evolution in supply chain with higher collection assertiveness, agile reading of customers and quick response to sell-out

Handbags: Developing the knowledge triad product-price-branding and focus in differentiated marketing actions

Accessories: Fulfill the mix offered, expand lifestyle concept (Schutz)

Organic growth leveraged by multi-brand, multichannel strategy in footwear and handbags

Franchises

Multi-brand

Owned

stores

Web

Commerce

External

market

New categories

SSS focus (VPL²)

GTM – continuables

SSS Focus (VPL²)

GTM, focus on handbags

Stores projects Roll-out

Services segmentation

Not a current

focus

Share of wallet increase

Attracting new clients

Handbags Cross-sell

Recent brand

awareness in this

channel

Increase penetration

Handbags Cross-sell

MKT PDV activation

Sale at selected

points of sales in line

with our branding

Expansion to new

points of sales

Focus on SSS increase

(VPL²)

Store transfer of

ownership

Complete transfer of

pilot-stores keeping 2

flagship stores at the

most

SSS focus (VPL²)

Store transfer of

ownership

SSS focus

Opening of pop

up stores

Opening of some

flagship/pilot

stores

New F.I.S site, allowing

ongoing expansion

New app

Strengthen digital

presence

To increase flow and

conversion

Channel improvement,

ex.: app

In store shipping test

2017 launch

Present in global

retailers

Online presence to

increase brand

awareness and

penetration

USA trial project

Exports to multi-brand

stores

Focus on key

accounts

New plant will allow

to meet demand of

international clients

Not a current

focus

National Roll-out

Continuables

program

MKT investment

Start feasibility

studies

Launching of AB

brand franchises

6

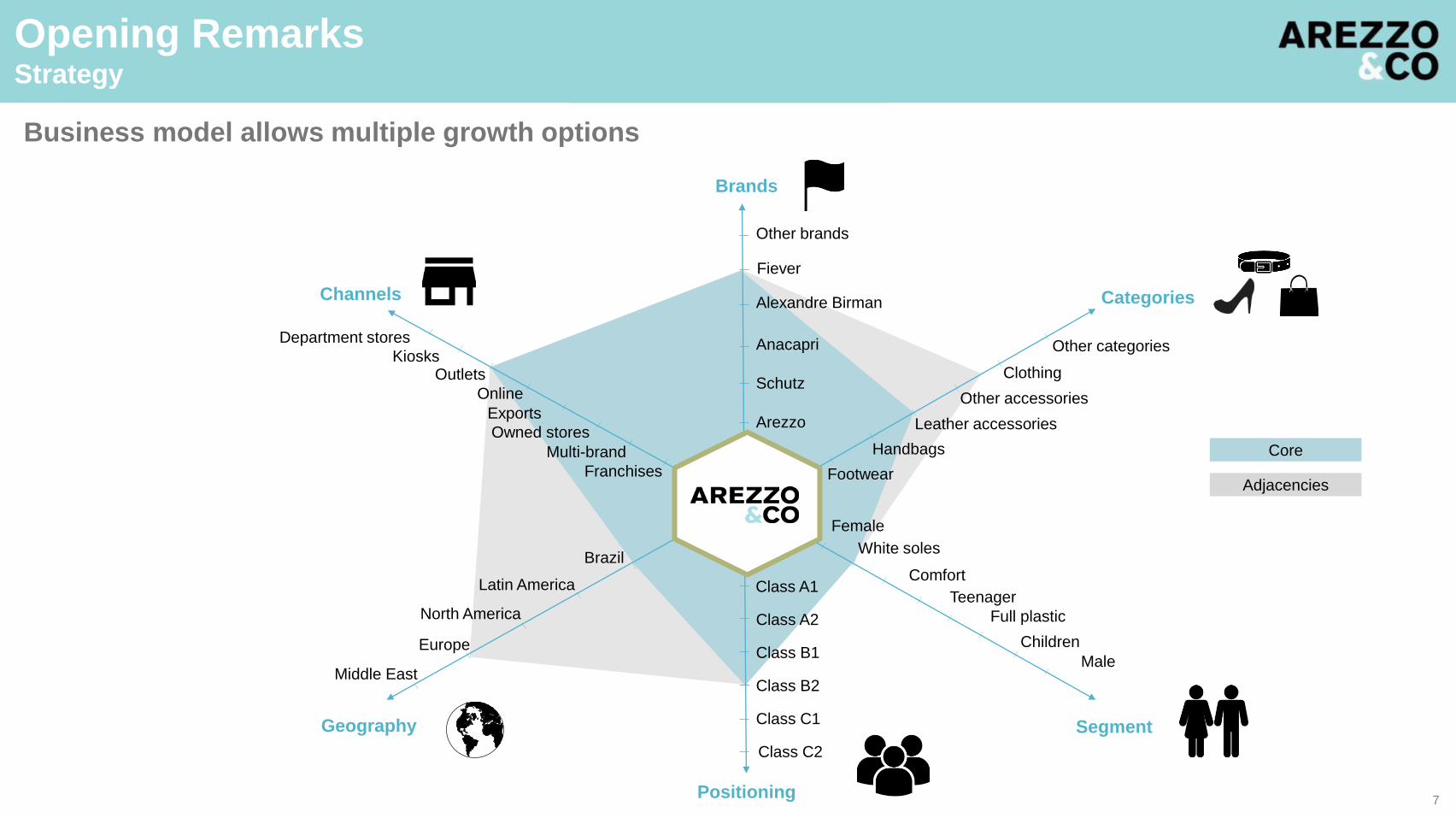

Opening RemarksStrategy

Business model allows multiple growth options

Adjacencies

Core

Brands

Categories

Geography

Female

Children

Teenager

Comfort

Male

White soles

Full plastic

Footwear

Leather accessories

Other accessories

Clothing

Other categories

Brazil

Latin America

North America

Europe

Middle East

Owned stores

Multi-brand

Exports

Online

OutletsKiosks

Department stores

Channels

Franchises

Handbags

Segment

Positioning

Class A1

Class B1

Class C2

Arezzo

Alexandre Birman

Anacapri

Schutz

Class A2

Class B2

Class C1

Other brands

Fiever

7

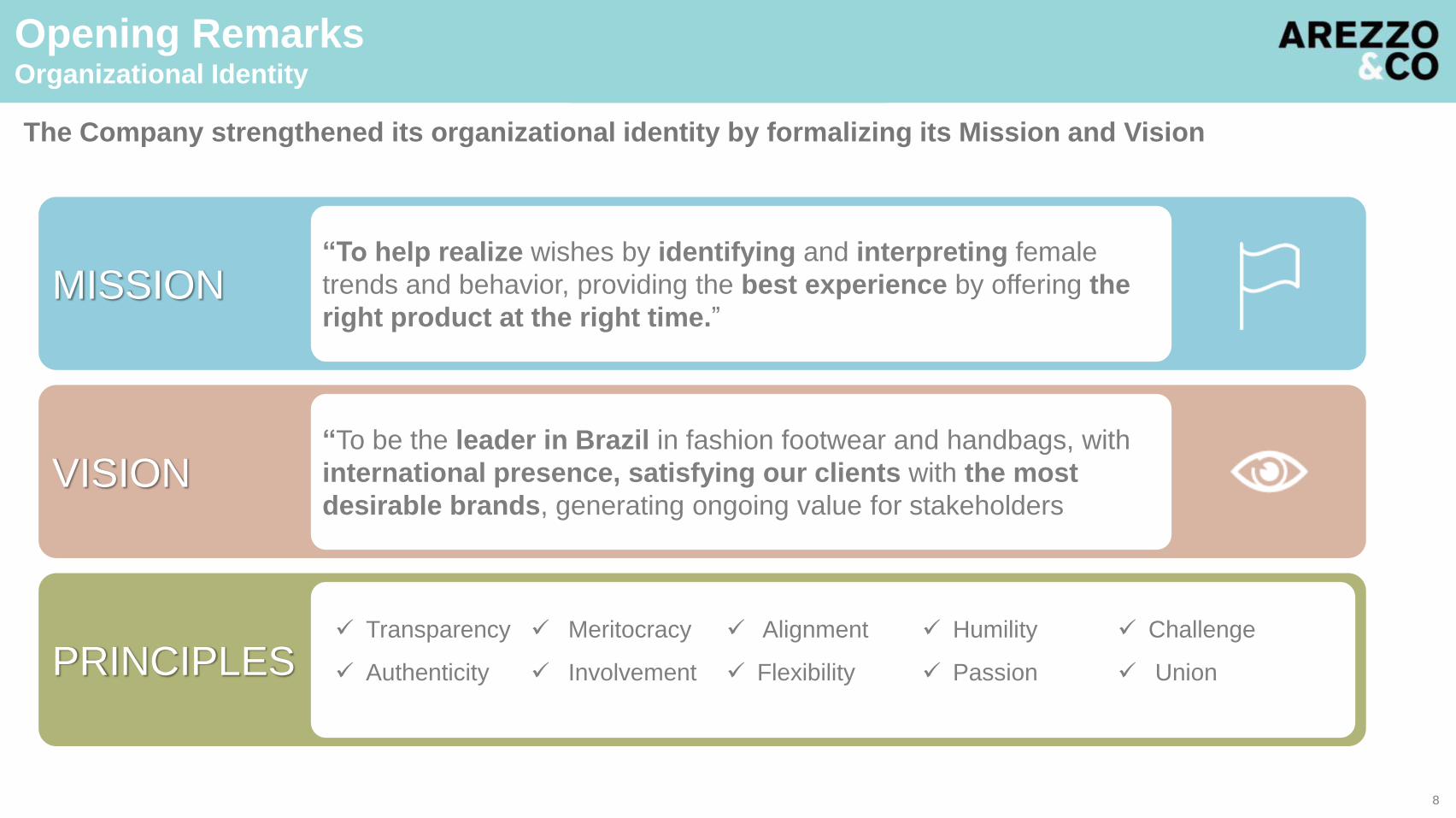

The Company strengthened its organizational identity by formalizing its Mission and Vision

PRINCIPLES Transparency

Authenticity

Meritocracy

Involvement

Alignment

Flexibility

Humility

Passion

Challenge

Union

VISION“To be the leader in Brazil in fashion footwear and handbags, with

international presence, satisfying our clients with the most

desirable brands, generating ongoing value for stakeholders

MISSION“To help realize wishes by identifying and interpreting female

trends and behavior, providing the best experience by offering the

right product at the right time.”

Opening RemarksOrganizational Identity

8

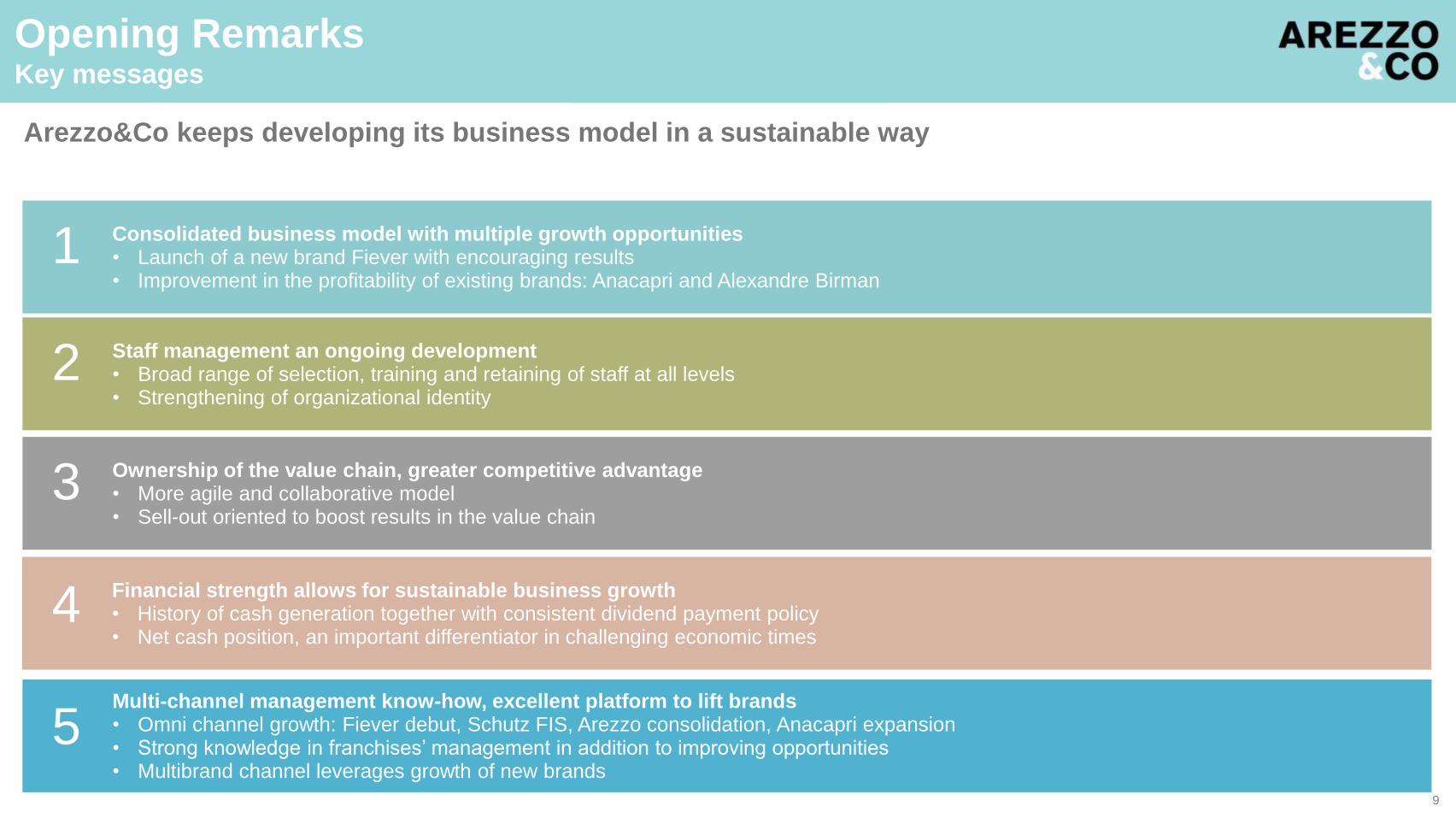

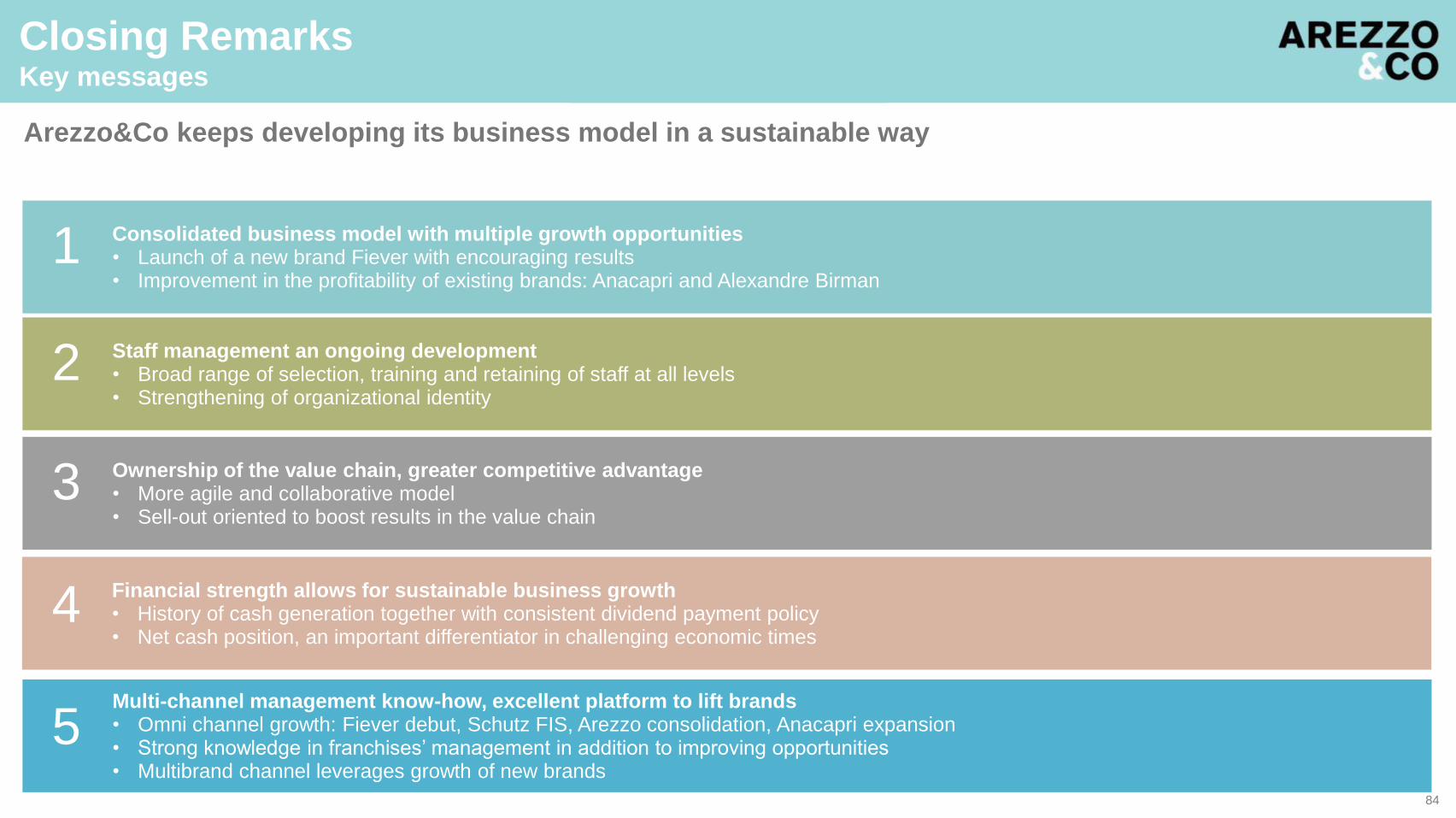

Arezzo&Co keeps developing its business model in a sustainable way

Consolidated business model with multiple growth opportunities• Launch of a new brand Fiever with encouraging results• Improvement in the profitability of existing brands: Anacapri and Alexandre Birman

1

Staff management an ongoing development• Broad range of selection, training and retaining of staff at all levels• Strengthening of organizational identity

2

Ownership of the value chain, greater competitive advantage• More agile and collaborative model• Sell-out oriented to boost results in the value chain

3

Multi-channel management know-how, excellent platform to lift brands• Omni channel growth: Fiever debut, Schutz FIS, Arezzo consolidation, Anacapri expansion• Strong knowledge in franchises’ management in addition to improving opportunities• Multibrand channel leverages growth of new brands

5

Financial strength allows for sustainable business growth• History of cash generation together with consistent dividend payment policy• Net cash position, an important differentiator in challenging economic times

4

Opening RemarksKey messages

9

Arezzo&Co Investor Day

Marco Aurélio VidalPeople Management Director

People Management

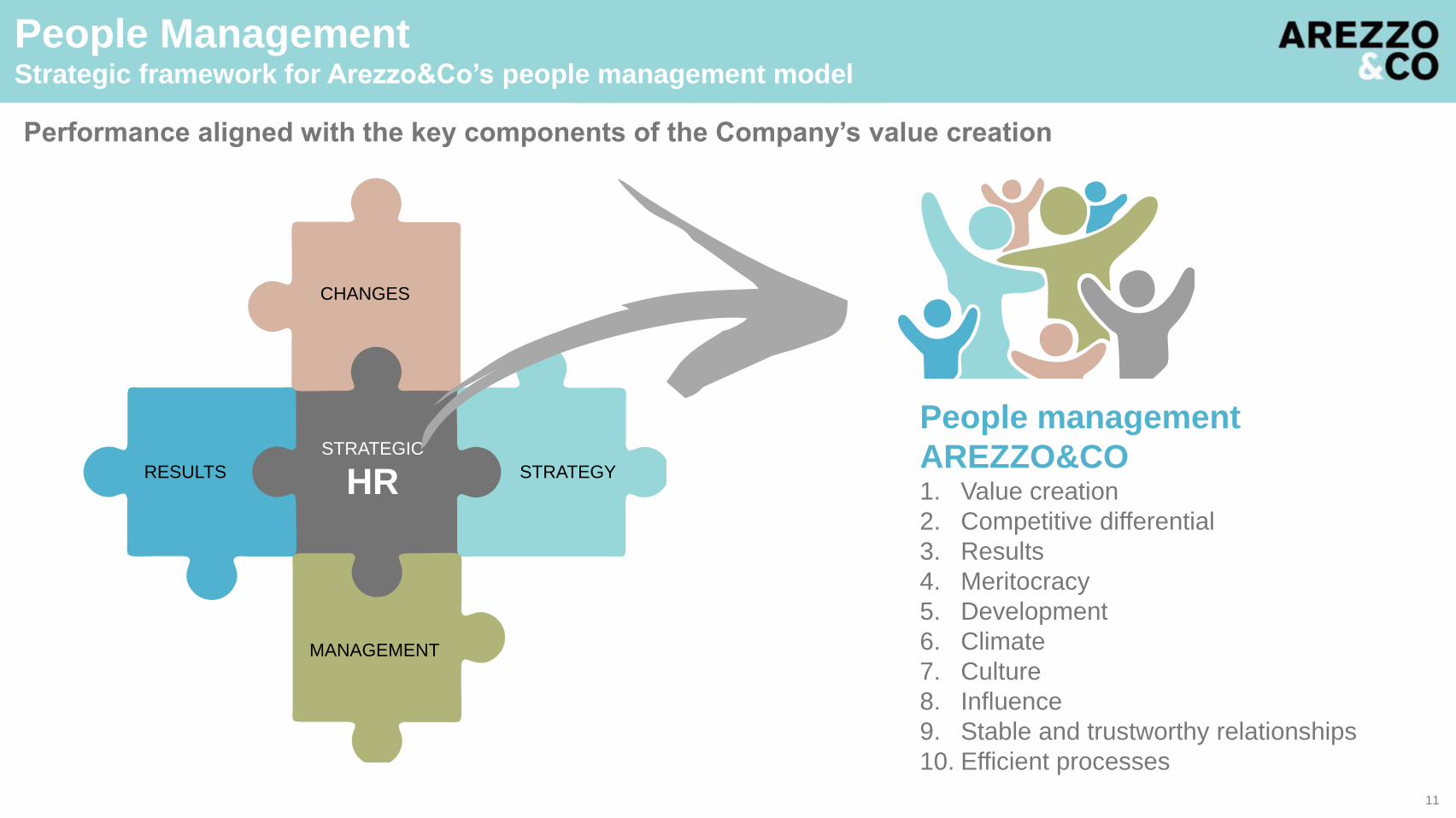

People ManagementStrategic framework for Arezzo&Co’s people management model

Performance aligned with the key components of the Company’s value creation

CHANGES

MANAGEMENT

STRATEGYRESULTS

STRATEGIC

HR

People management

AREZZO&CO1. Value creation

2. Competitive differential

3. Results

4. Meritocracy

5. Development

6. Climate

7. Culture

8. Influence

9. Stable and trustworthy relationships

10. Efficient processes

11

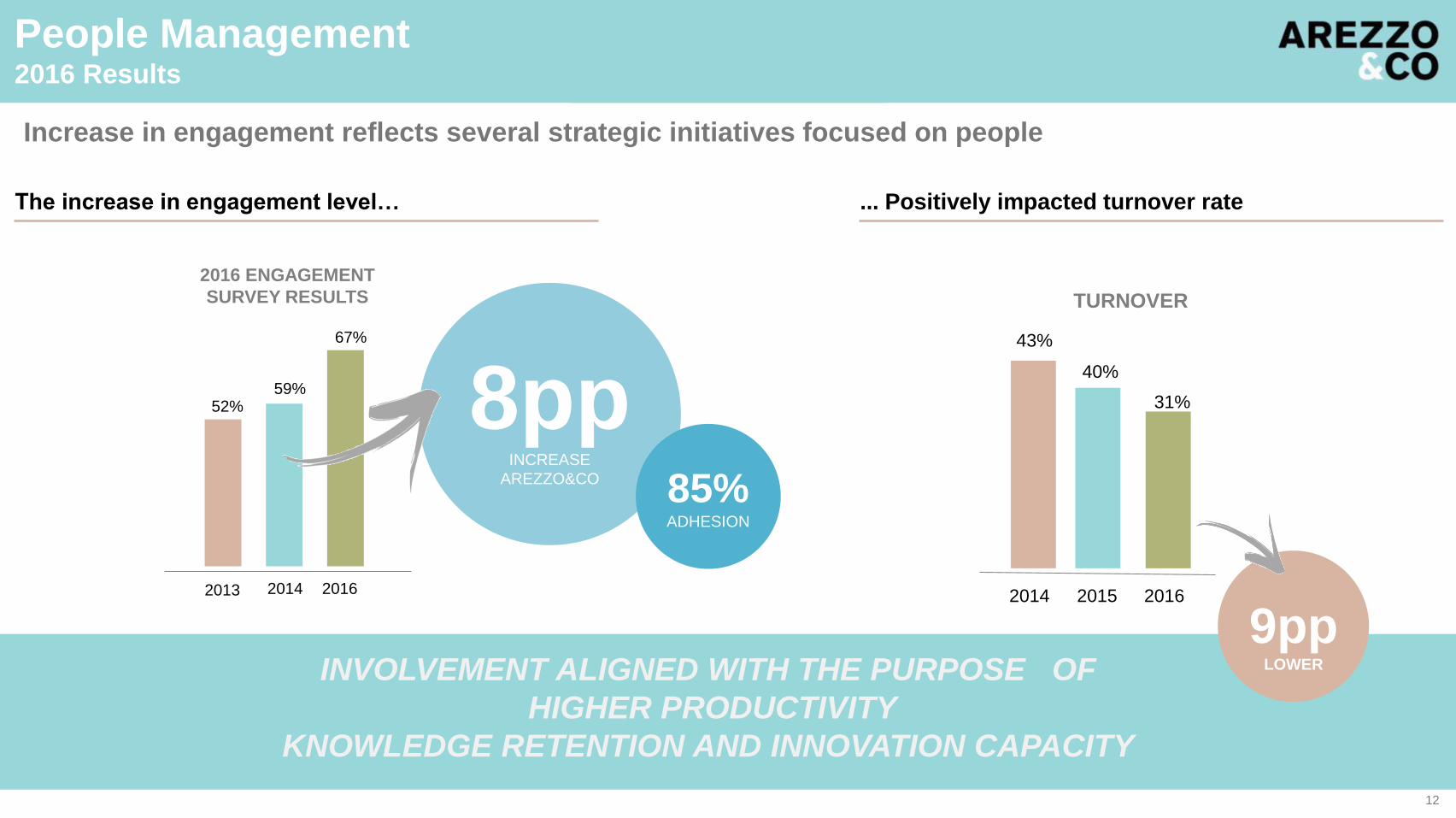

Increase in engagement reflects several strategic initiatives focused on people

... Positively impacted turnover rate

40%

31%

2015 2016

9ppLOWER

TURNOVER

INVOLVEMENT ALIGNED WITH THE PURPOSE OF

HIGHER PRODUCTIVITY

KNOWLEDGE RETENTION AND INNOVATION CAPACITY

The increase in engagement level…

43%

2014

8ppINCREASE

AREZZO&CO

52%59%

67%

2013 2014 2016

2016 ENGAGEMENT

SURVEY RESULTS

85% ADHESION

People Management2016 Results

12

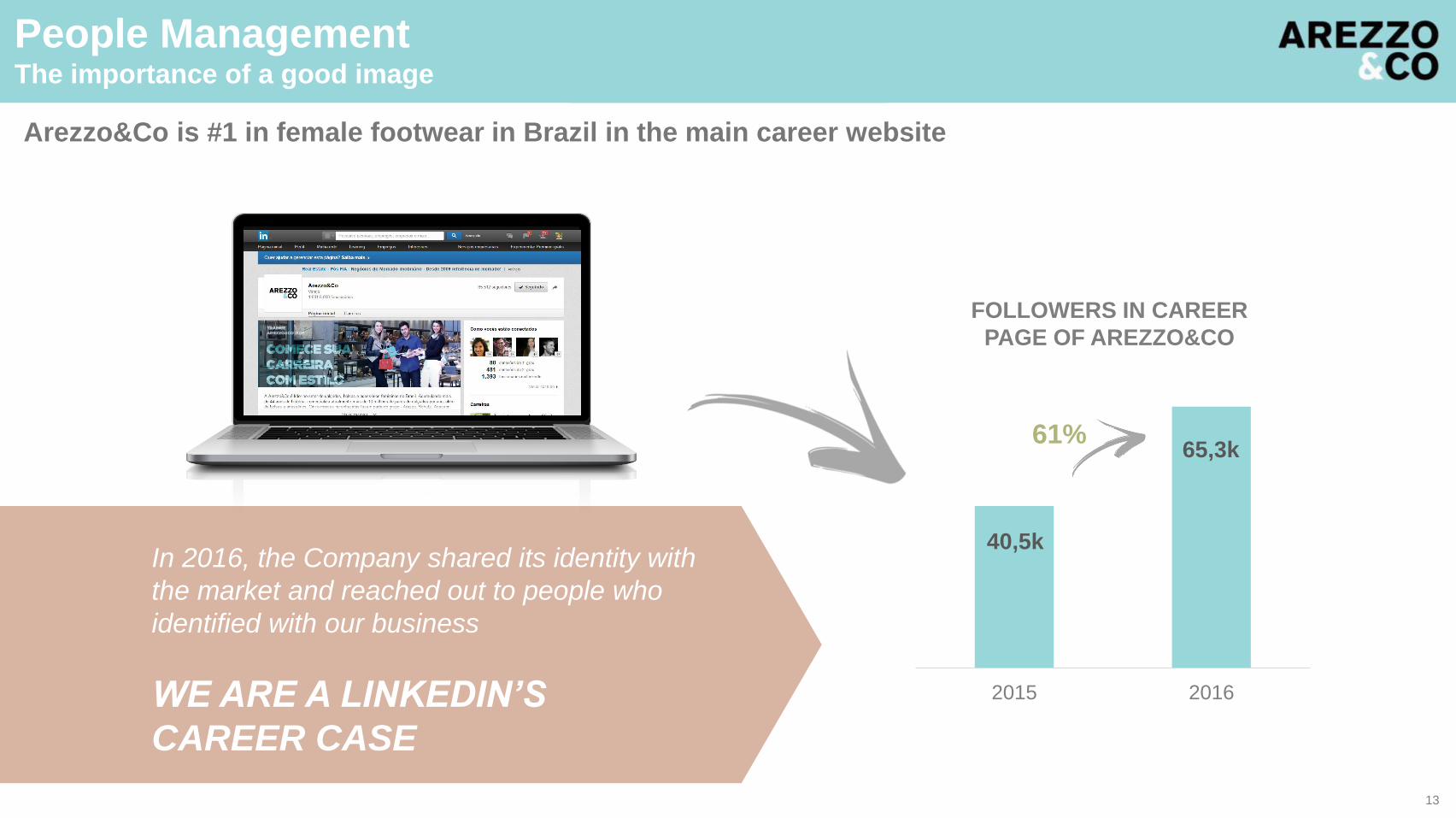

Arezzo&Co is #1 in female footwear in Brazil in the main career website

2015 2016

FOLLOWERS IN CAREER

PAGE OF AREZZO&CO

61%

40,5k

65,3k

In 2016, the Company shared its identity with

the market and reached out to people who

identified with our business

WE ARE A LINKEDIN’S

CAREER CASE

People ManagementThe importance of a good image

13

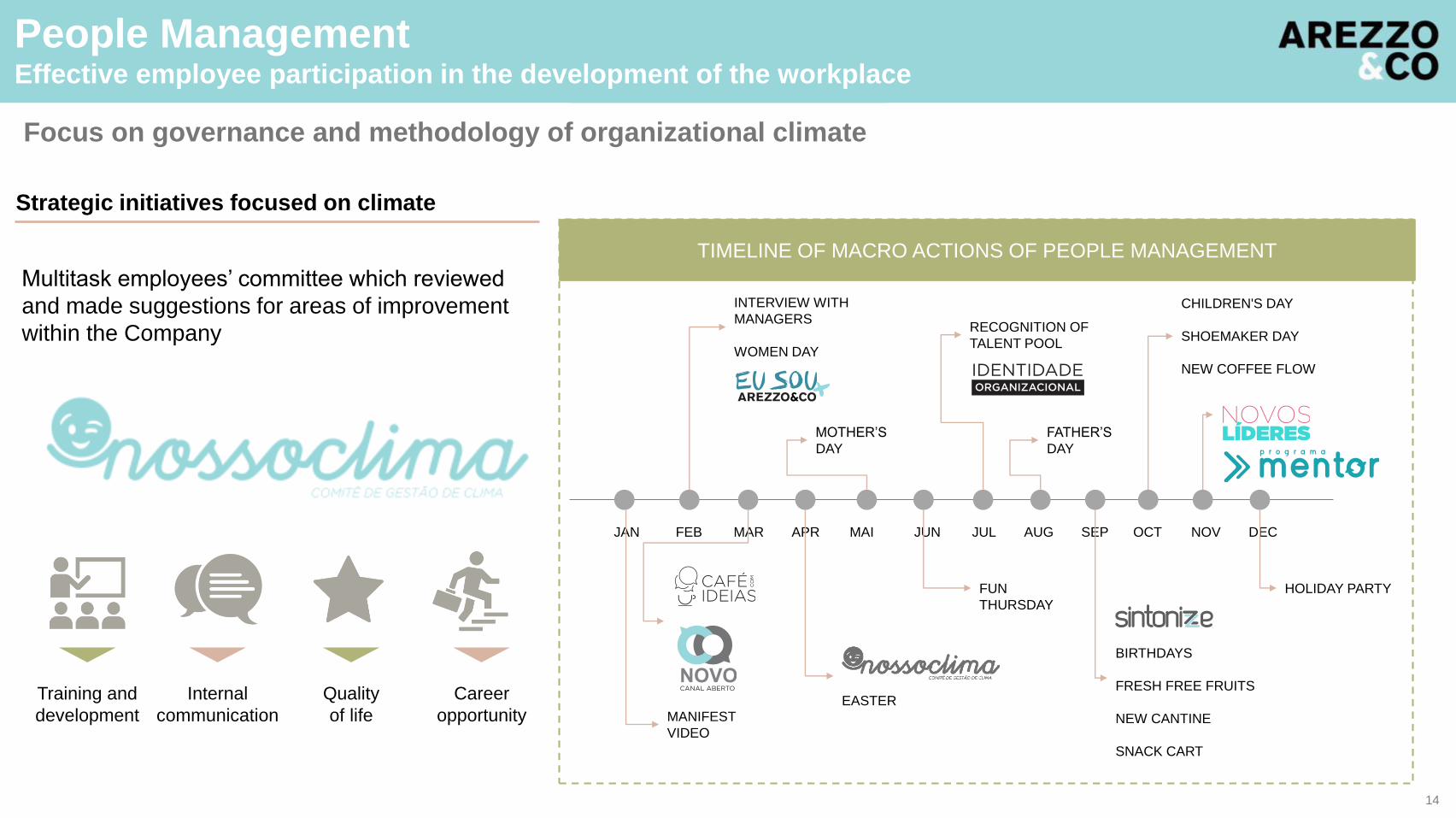

People ManagementEffective employee participation in the development of the workplace

Focus on governance and methodology of organizational climate

Strategic initiatives focused on climate

Training and

development

Internal

communication

Quality

of life

Career

opportunity

TIMELINE OF MACRO ACTIONS OF PEOPLE MANAGEMENT

JAN FEB MAR APR MAI JUN JUL AUG SEP OCT NOV DEC

INTERVIEW WITH

MANAGERS

WOMEN DAY

EASTER

MOTHER’S

DAY

FATHER’S

DAY

BIRTHDAYS

FRESH FREE FRUITS

NEW CANTINE

SNACK CART

CHILDREN'S DAY

SHOEMAKER DAY

NEW COFFEE FLOW

FUN

THURSDAY

Multitask employees’ committee which reviewed

and made suggestions for areas of improvement

within the Company

MANIFEST

VIDEO

HOLIDAY PARTY

RECOGNITION OF

TALENT POOL

14

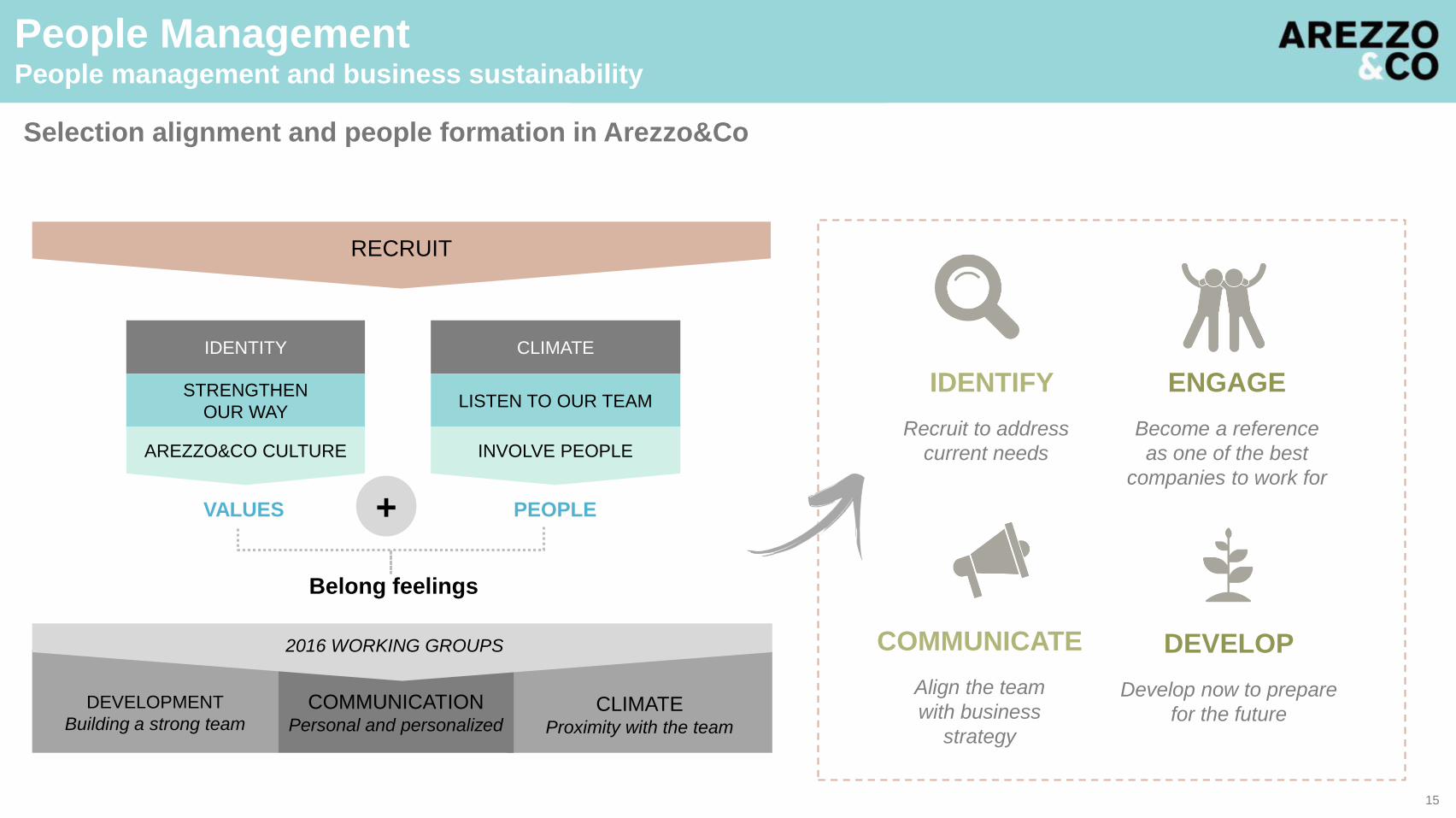

People ManagementPeople management and business sustainability

Selection alignment and people formation in Arezzo&Co

IDENTITY

STRENGTHEN

OUR WAY

CLIMATE

LISTEN TO OUR TEAM

AREZZO&CO CULTURE INVOLVE PEOPLE

VALUES PEOPLE+

Belong feelings

DEVELOPMENT

Building a strong teamCLIMATE

Proximity with the team

RECRUIT

COMMUNICATIONPersonal and personalized

2016 WORKING GROUPS

IDENTIFY

Recruit to address

current needs

ENGAGE

Become a reference

as one of the best

companies to work for

COMMUNICATE

Align the team

with business

strategy

DEVELOP

Develop now to prepare

for the future

15

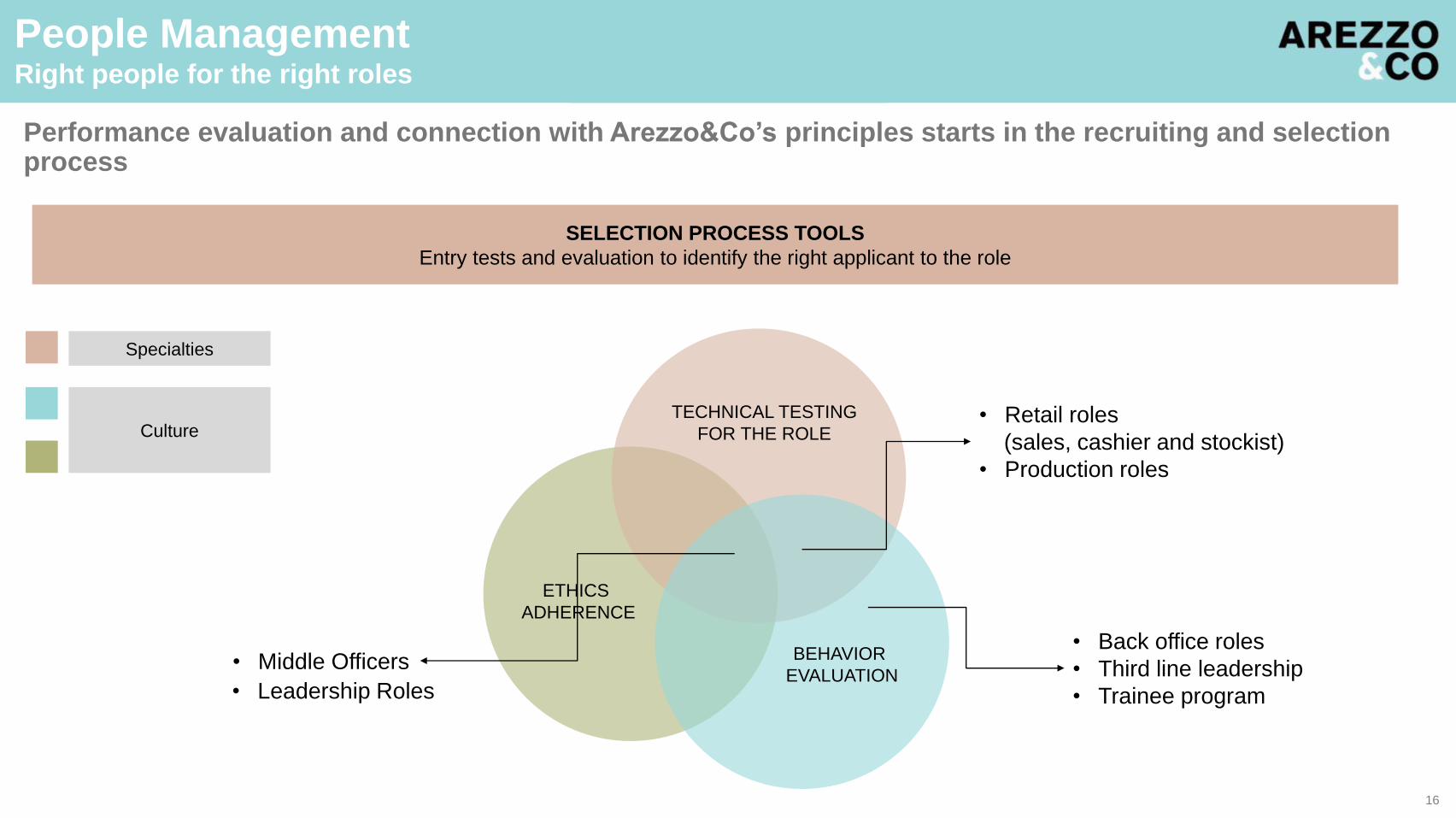

People ManagementRight people for the right roles

Performance evaluation and connection with Arezzo&Co’s principles starts in the recruiting and selection process

TECHNICAL TESTING

FOR THE ROLE

BEHAVIOR

EVALUATION

ETHICS

ADHERENCE

• Retail roles

(sales, cashier and stockist)

• Production roles

• Back office roles

• Third line leadership

• Trainee program• Leadership Roles

Specialties

Culture

SELECTION PROCESS TOOLS

Entry tests and evaluation to identify the right applicant to the role

• Middle Officers

16

23%

54%

23%

MANAGERS

COORDINATORS

SPECIALISTS

ACTIVE DEC/2016

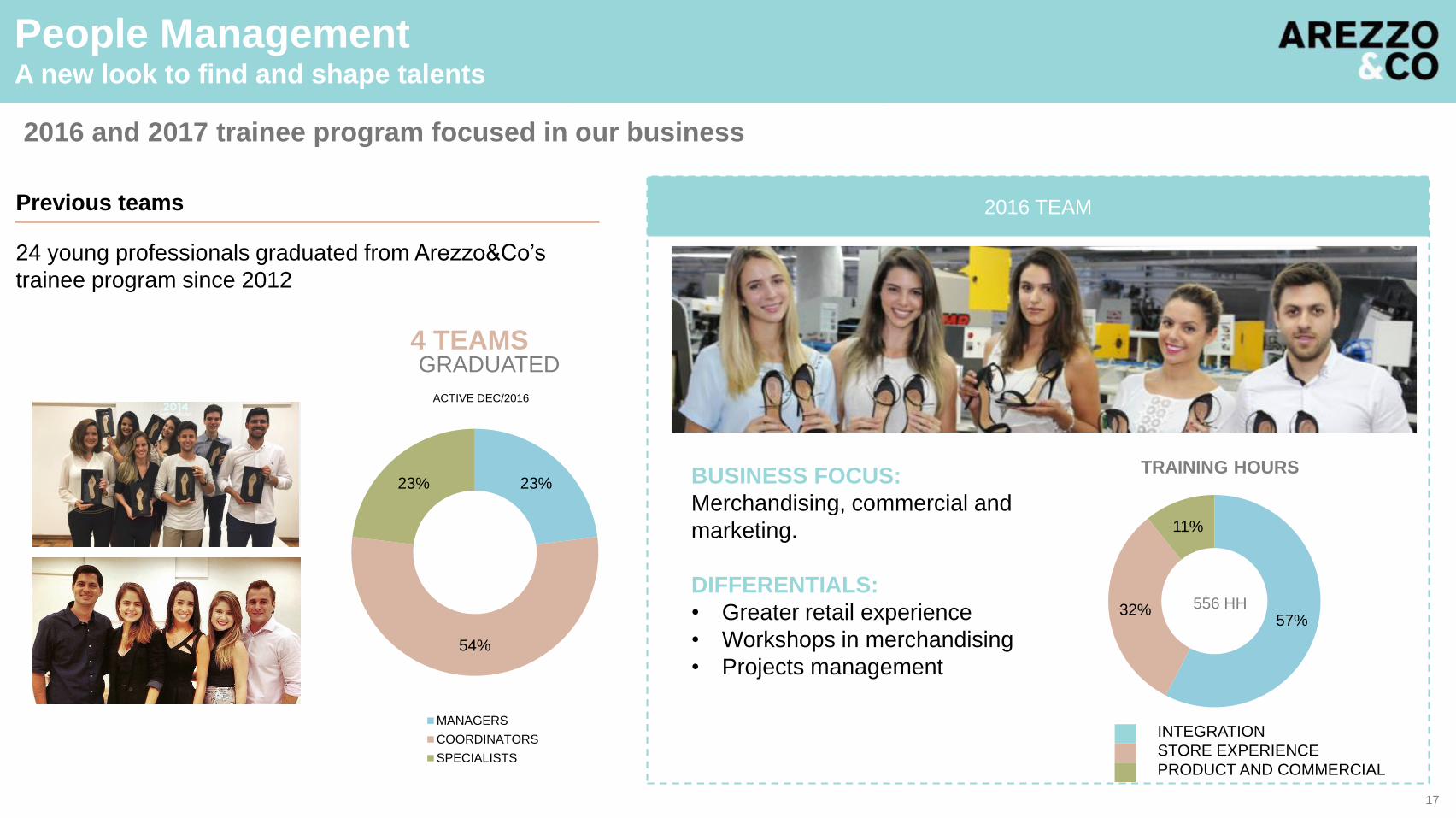

People ManagementA new look to find and shape talents

2016 and 2017 trainee program focused in our business

Previous teams

24 young professionals graduated from Arezzo&Co’s

trainee program since 2012

4 TEAMSGRADUATED

2016 TEAM

BUSINESS FOCUS:

Merchandising, commercial and

marketing.

DIFFERENTIALS:

• Greater retail experience

• Workshops in merchandising

• Projects management

57%32%

11%

TRAINING HOURS

556 HH

INTEGRATION

STORE EXPERIENCE

PRODUCT AND COMMERCIAL

17

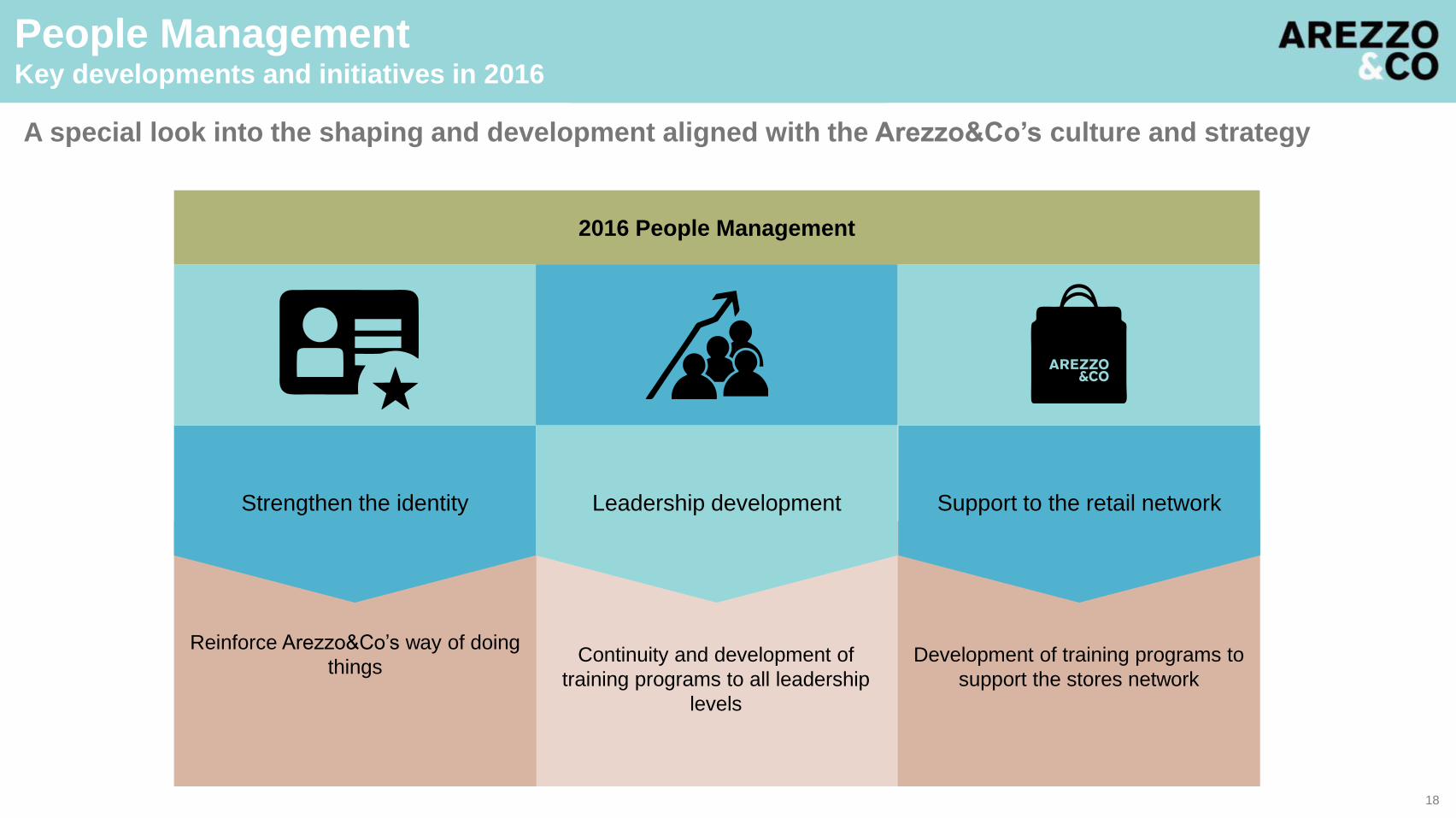

Continuity and development of

training programs to all leadership

levels

Development of training programs to

support the stores network

Reinforce Arezzo&Co’s way of doing

things

Strengthen the identity Leadership development Support to the retail network

2016 People Management

People ManagementKey developments and initiatives in 2016

A special look into the shaping and development aligned with the Arezzo&Co’s culture and strategy

18

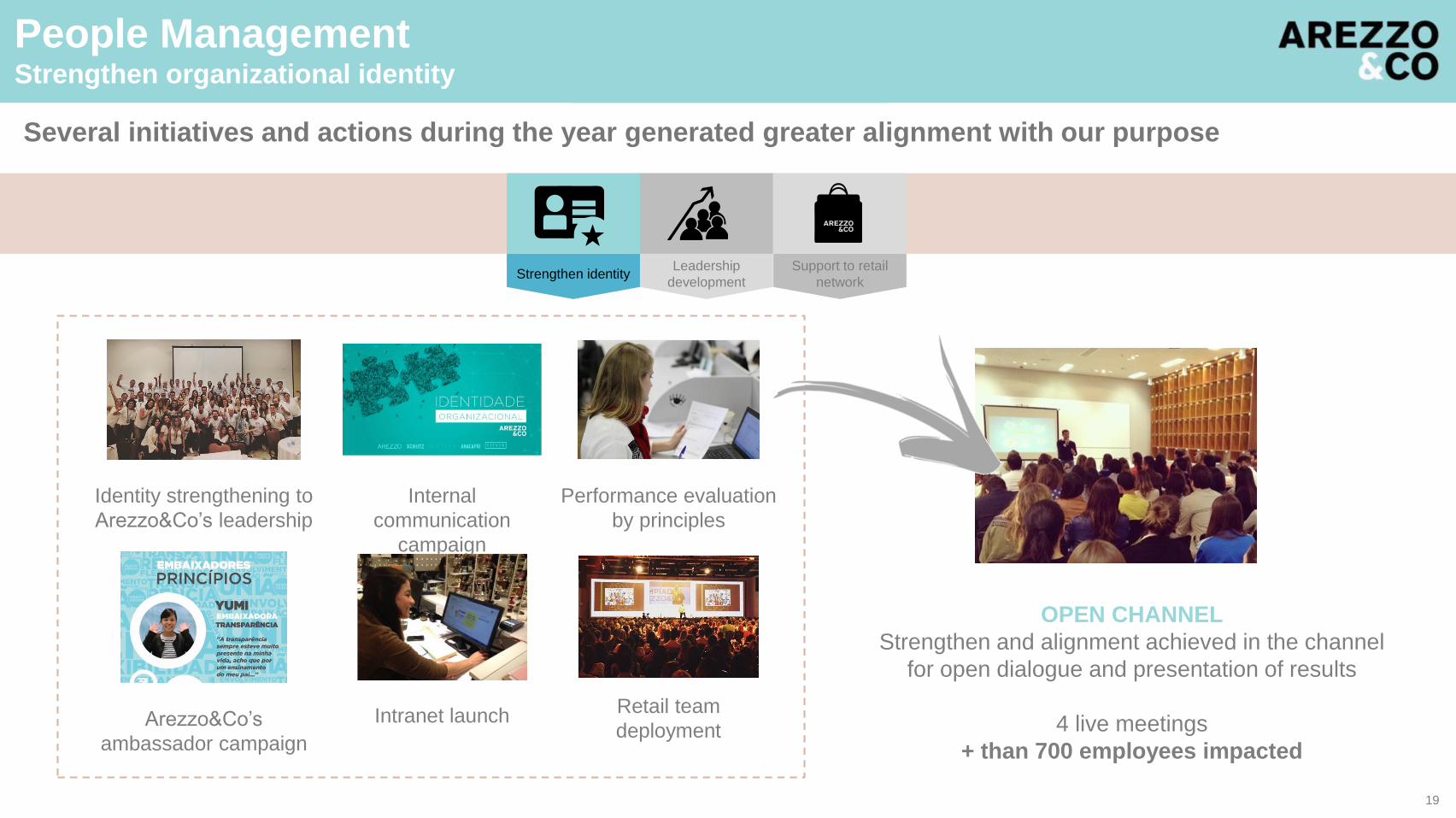

People ManagementStrengthen organizational identity

Several initiatives and actions during the year generated greater alignment with our purpose

Identity strengthening to

Arezzo&Co’s leadership

Performance evaluation

by principles

Internal

communication

campaign

Intranet launchArezzo&Co’s

ambassador campaign

Retail team

deployment

OPEN CHANNEL

Strengthen and alignment achieved in the channel

for open dialogue and presentation of results

4 live meetings

+ than 700 employees impacted

Strengthen identityLeadership

development

Support to retail

network

19

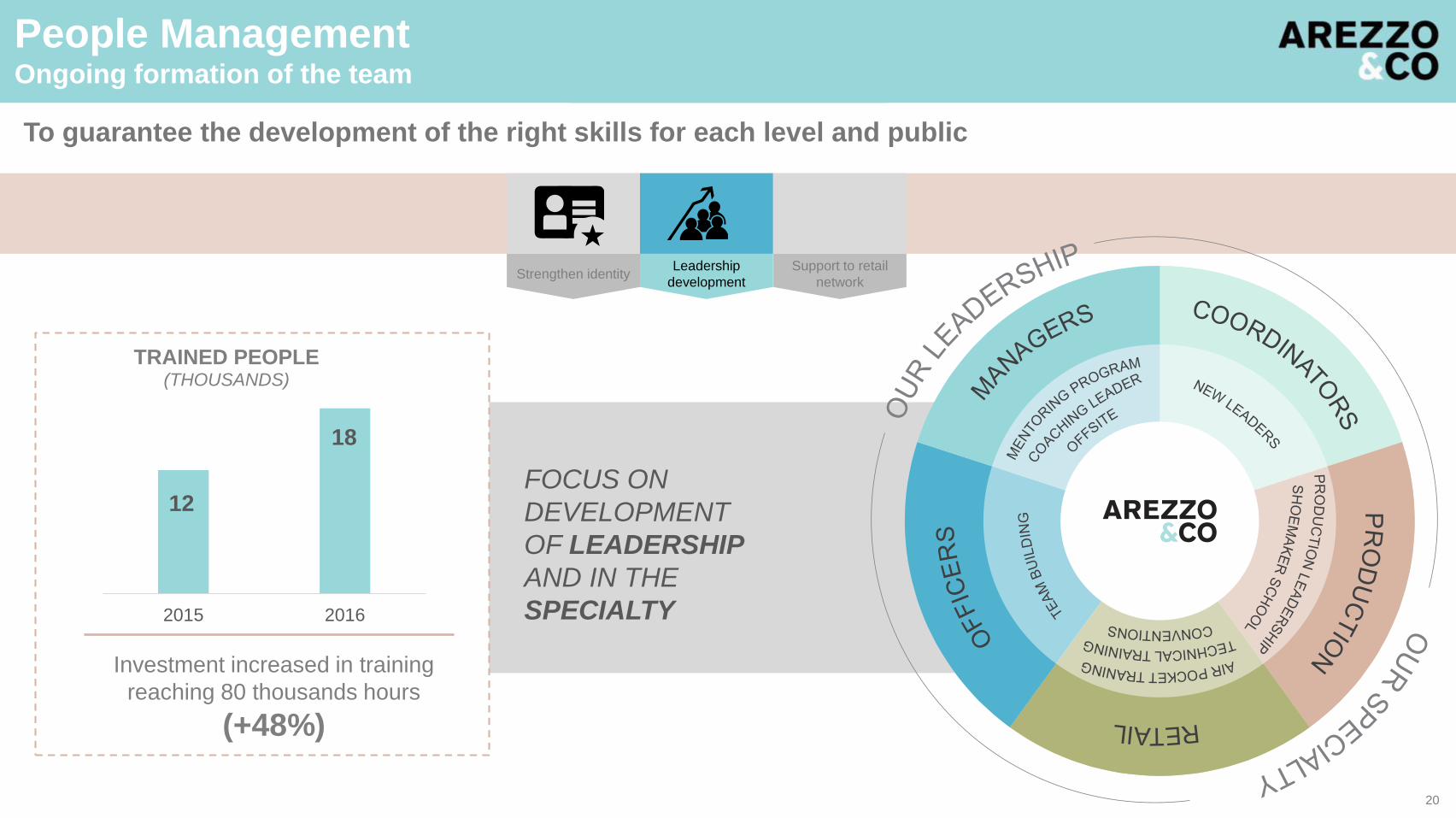

People ManagementOngoing formation of the team

To guarantee the development of the right skills for each level and public

2015 2016

TRAINED PEOPLE(THOUSANDS)

12

18

Investment increased in training

reaching 80 thousands hours

(+48%)

Strengthen identityLeadership

development

Support to retail

network

FOCUS ON

DEVELOPMENT

OF LEADERSHIP

AND IN THE

SPECIALTY

20

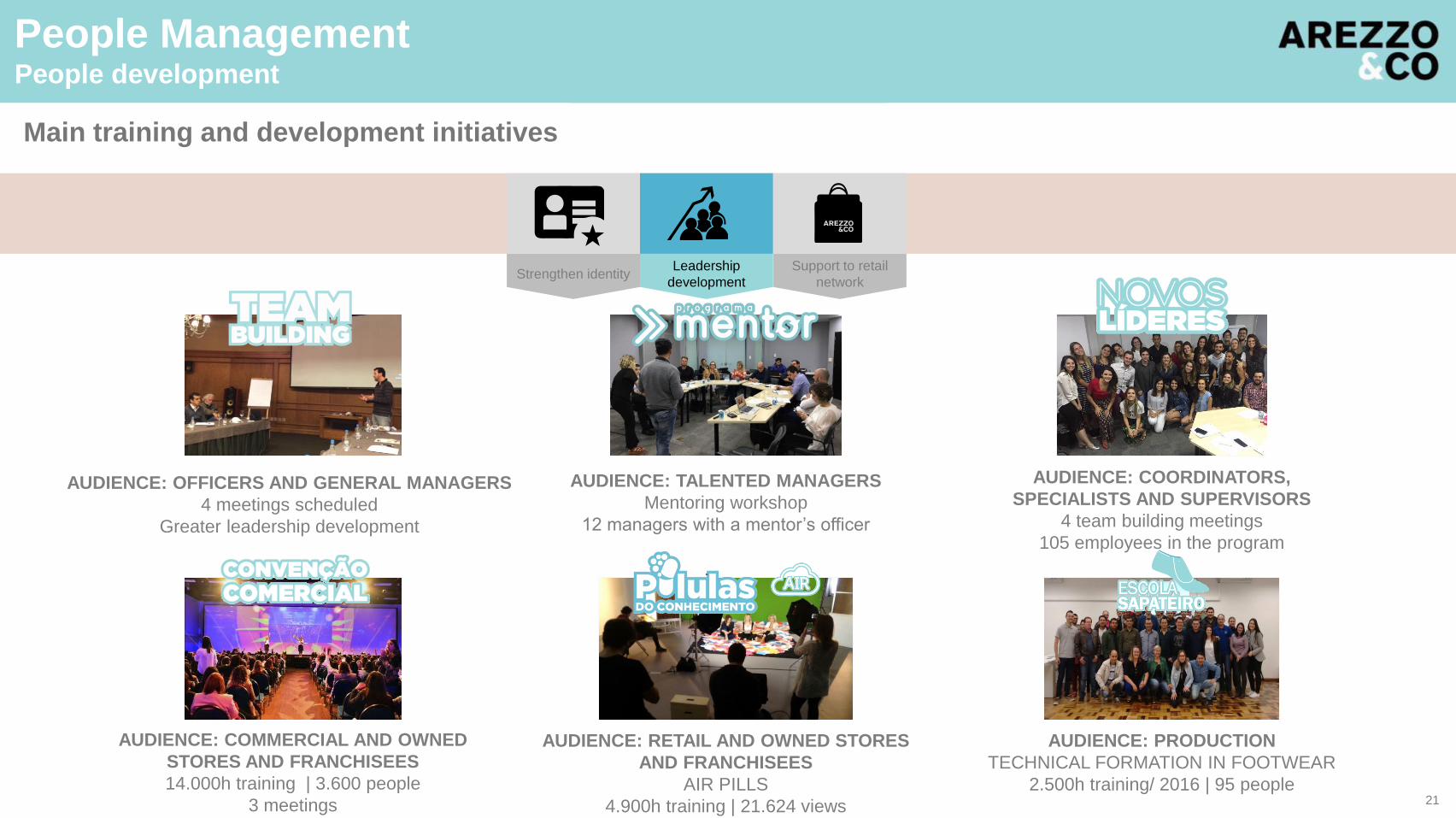

People ManagementPeople development

Main training and development initiatives

AUDIENCE: OFFICERS AND GENERAL MANAGERS

4 meetings scheduled

Greater leadership development

AUDIENCE: TALENTED MANAGERS

Mentoring workshop

12 managers with a mentor’s officer

AUDIENCE: COORDINATORS,

SPECIALISTS AND SUPERVISORS

4 team building meetings

105 employees in the program

AUDIENCE: COMMERCIAL AND OWNED

STORES AND FRANCHISEES

14.000h training | 3.600 people

3 meetings

AUDIENCE: RETAIL AND OWNED STORES

AND FRANCHISEES

AIR PILLS

4.900h training | 21.624 views

AUDIENCE: PRODUCTION

TECHNICAL FORMATION IN FOOTWEAR

2.500h training/ 2016 | 95 people

Strengthen identityLeadership

development

Support to retail

network

21

2

2

People ManagementFranchisee preparation focusing on retail

Standardize processes and attendance to guarantee the best purchasing experience

86%OF STORES USES AIR

35 COURSESFOCUSED IN RETAIL

AVAILABLE IN AIR

18.420HONLINE TRAINING IN 2016

FRANCHISEES INTEGRATION LIVE CONVENTIONS AIR TRAINING

Development focused

in retail

65 trained people

520 hours total

7.900impacted people

Training with consultants

focused in sales processes

and techniques to

strengthen the network

TRAINING HOURS

COMMERCIAL TEAM

2015 2016

3.472H

1.440H

141%

STANDARD TRAINING

Arezzo sales

Schutz sales

Ana Capri sales

Product

Salesperson

Stockist

Cashier

Manager

+20 with specific

focus

Strengthen identityLeadership

development

Support to retail

network

22

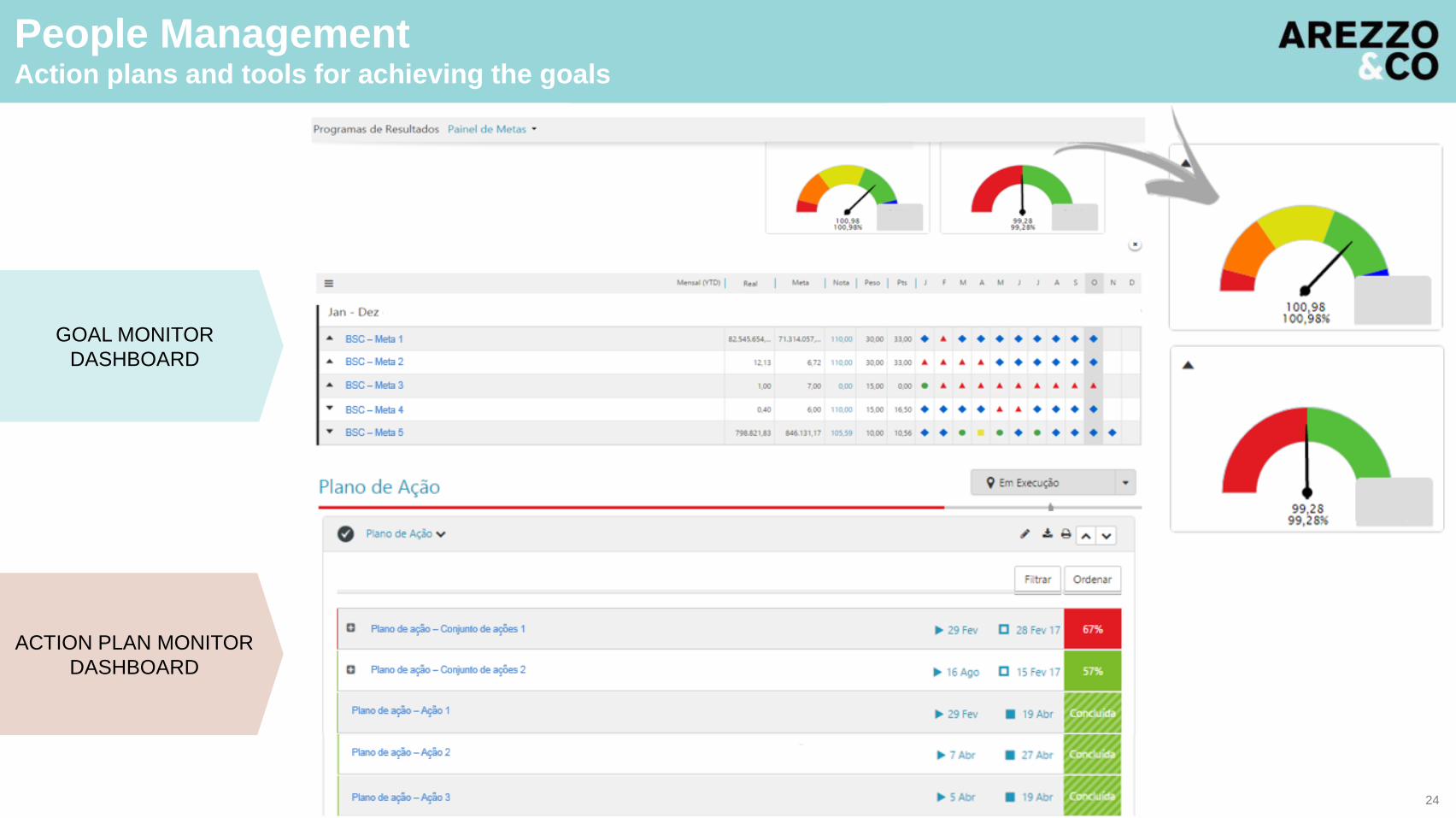

People ManagementPeople management aligned with the strategy

Strategy deployment and annual goals to all managers aligned with the development cycle of HR

BUDGET

GUIDELINES AND

STRATEGIC

PLANNING

BSC

PEOPLE

CYCLE

MANAGEMENT

CYCLE

- 360º EVALUATIONS

- MANAGERS

MEETINGS

- PDI AND FEEDBACK

- ACTION PLAN

- FOLLOW UP MEETINGS

- BSC RESULTS UPDATES

BSC has a system focused in the monitoring of goals

Specialized software in following up goals and action plans to

guarantee synergies

23

People ManagementAction plans and tools for achieving the goals

GOAL MONITOR

DASHBOARD

ACTION PLAN MONITOR

DASHBOARD

24

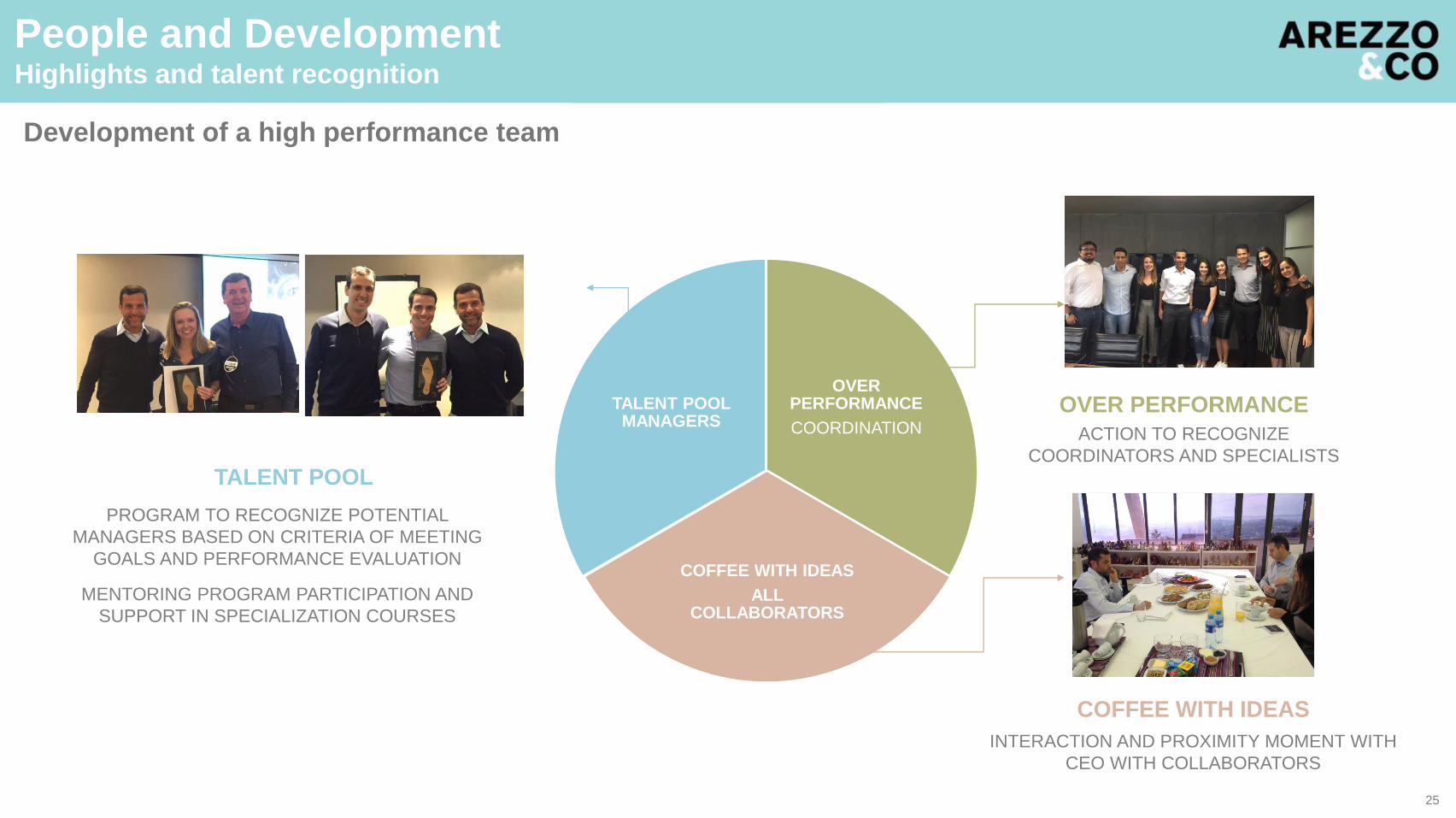

People and DevelopmentHighlights and talent recognition

Development of a high performance team

OVER PERFORMANCE

COORDINATION

COFFEE WITH IDEAS

ALL COLLABORATORS

TALENT POOL MANAGERS

TALENT POOL

OVER PERFORMANCE

COFFEE WITH IDEAS

PROGRAM TO RECOGNIZE POTENTIAL

MANAGERS BASED ON CRITERIA OF MEETING

GOALS AND PERFORMANCE EVALUATION

MENTORING PROGRAM PARTICIPATION AND

SUPPORT IN SPECIALIZATION COURSES

ACTION TO RECOGNIZE

COORDINATORS AND SPECIALISTS

INTERACTION AND PROXIMITY MOMENT WITH

CEO WITH COLLABORATORS

25

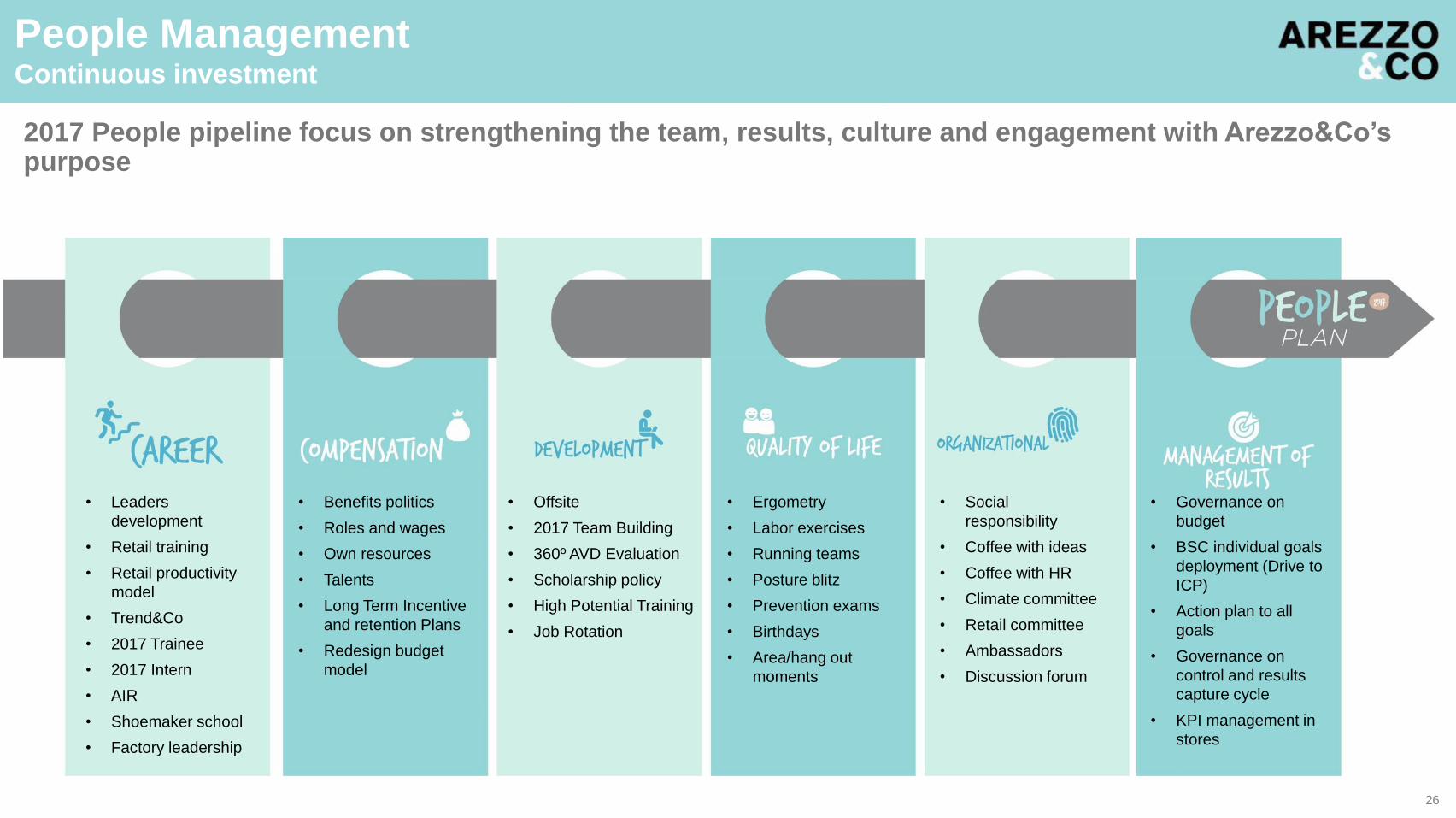

People ManagementContinuous investment

2017 People pipeline focus on strengthening the team, results, culture and engagement with Arezzo&Co’spurpose

• Leaders

development

• Retail training

• Retail productivity

model

• Trend&Co

• 2017 Trainee

• 2017 Intern

• AIR

• Shoemaker school

• Factory leadership

• Benefits politics

• Roles and wages

• Own resources

• Talents

• Long Term Incentive

and retention Plans

• Redesign budget

model

• Offsite

• 2017 Team Building

• 360º AVD Evaluation

• Scholarship policy

• High Potential Training

• Job Rotation

• Ergometry

• Labor exercises

• Running teams

• Posture blitz

• Prevention exams

• Birthdays

• Area/hang out

moments

• Social

responsibility

• Coffee with ideas

• Coffee with HR

• Climate committee

• Retail committee

• Ambassadors

• Discussion forum

• Governance on

budget

• BSC individual goals

deployment (Drive to

ICP)

• Action plan to all

goals

• Governance on

control and results

capture cycle

• KPI management in

stores

26

Promoting people development and strengthening our leaderships

Strategic positioning in People Management- Value creation inside and outside Arezzo&Co- Development of competitive differentials

1

Culture- Organizational identity: Manifest, Mission, Vision, Principles- Alignment of purposes and Arezzo&Co way of being- Recruiting, performance evaluation and development with focus on principles adherence

2

Training and Developing- Customized programs to the development needs of each level- Pipeline strengthening of people through a strong leadership formation and technical capacitation

3

Climate and engagement- Collaborators involvements on setting up the demands and actions to be implemented- Focus on improvement points from the previous climate surveys

5

Management and meritocracy- Strategic and annual goals deployed to all level of the Company, through performance indicators- Stabilization of People management cycles (control and results capture)- Recognition of best performances through criteria

4

27

People ManagementKey messages

Arezzo&Co Investor DayValue Chain

Cassiano Lemos Silvia MachadoLogistics and Planning Director Arezzo BU Director

1

2

3

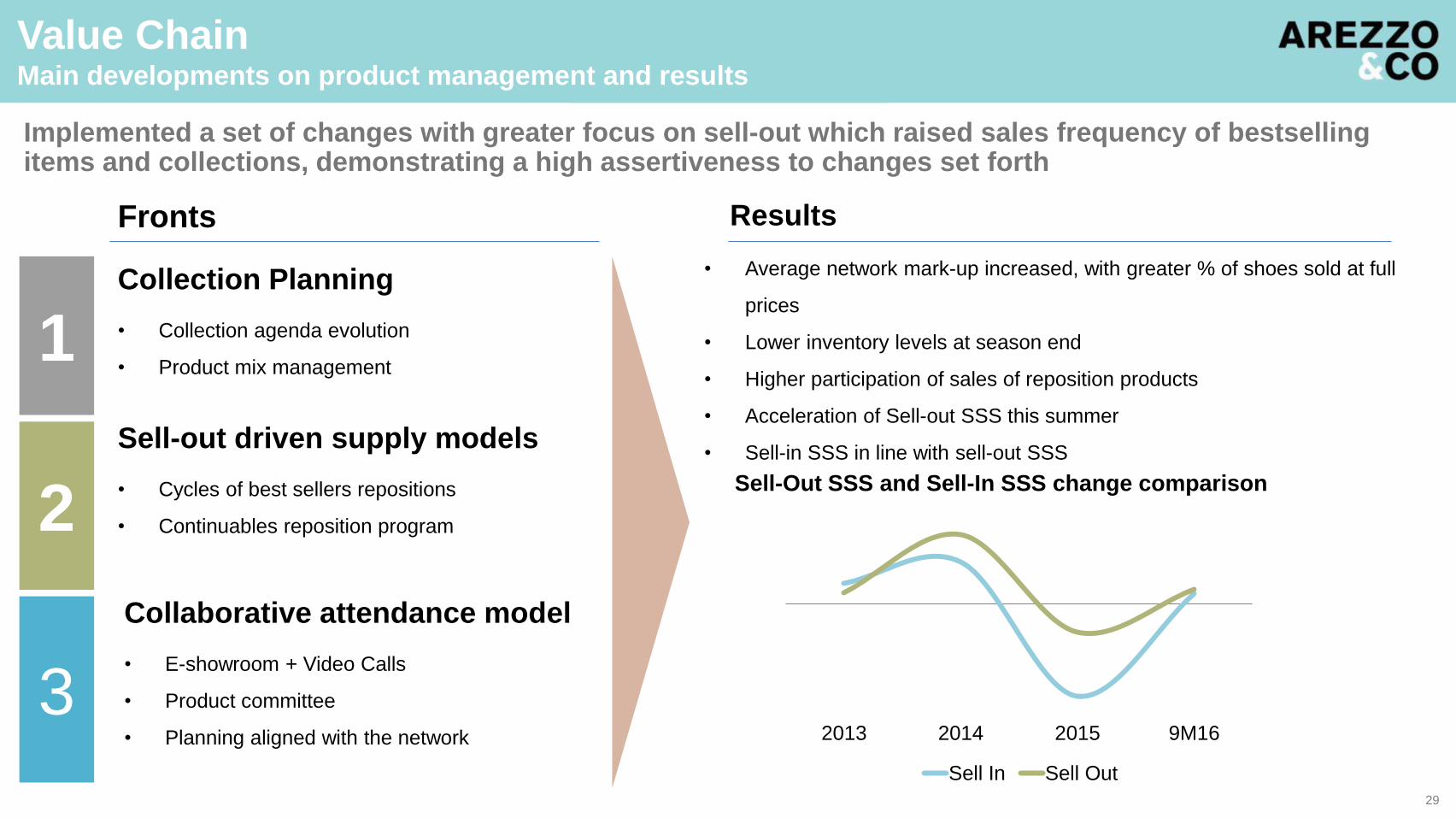

Value ChainMain developments on product management and results

• Average network mark-up increased, with greater % of shoes sold at full

prices

• Lower inventory levels at season end

• Higher participation of sales of reposition products

• Acceleration of Sell-out SSS this summer

• Sell-in SSS in line with sell-out SSS

Collection Planning

• Collection agenda evolution

• Product mix management

Collaborative attendance model

• E-showroom + Video Calls

• Product committee

• Planning aligned with the network

Sell-out driven supply models

• Cycles of best sellers repositions

• Continuables reposition program

Implemented a set of changes with greater focus on sell-out which raised sales frequency of bestselling items and collections, demonstrating a high assertiveness to changes set forth

Sell-Out SSS and Sell-In SSS change comparison

2013 2014 2015 9M16

Sell In Sell Out

Fronts Results

29

Value ChainThe right product at the right time + Client experience with brand

FRANCHISEES MANAGEMENT

PRODUCT MANAGEMENT

30

Value ChainThe right product at the right time + Client experience with brand

FRANCHISEES MANAGEMENT

PRODUCT MANAGEMENT

31

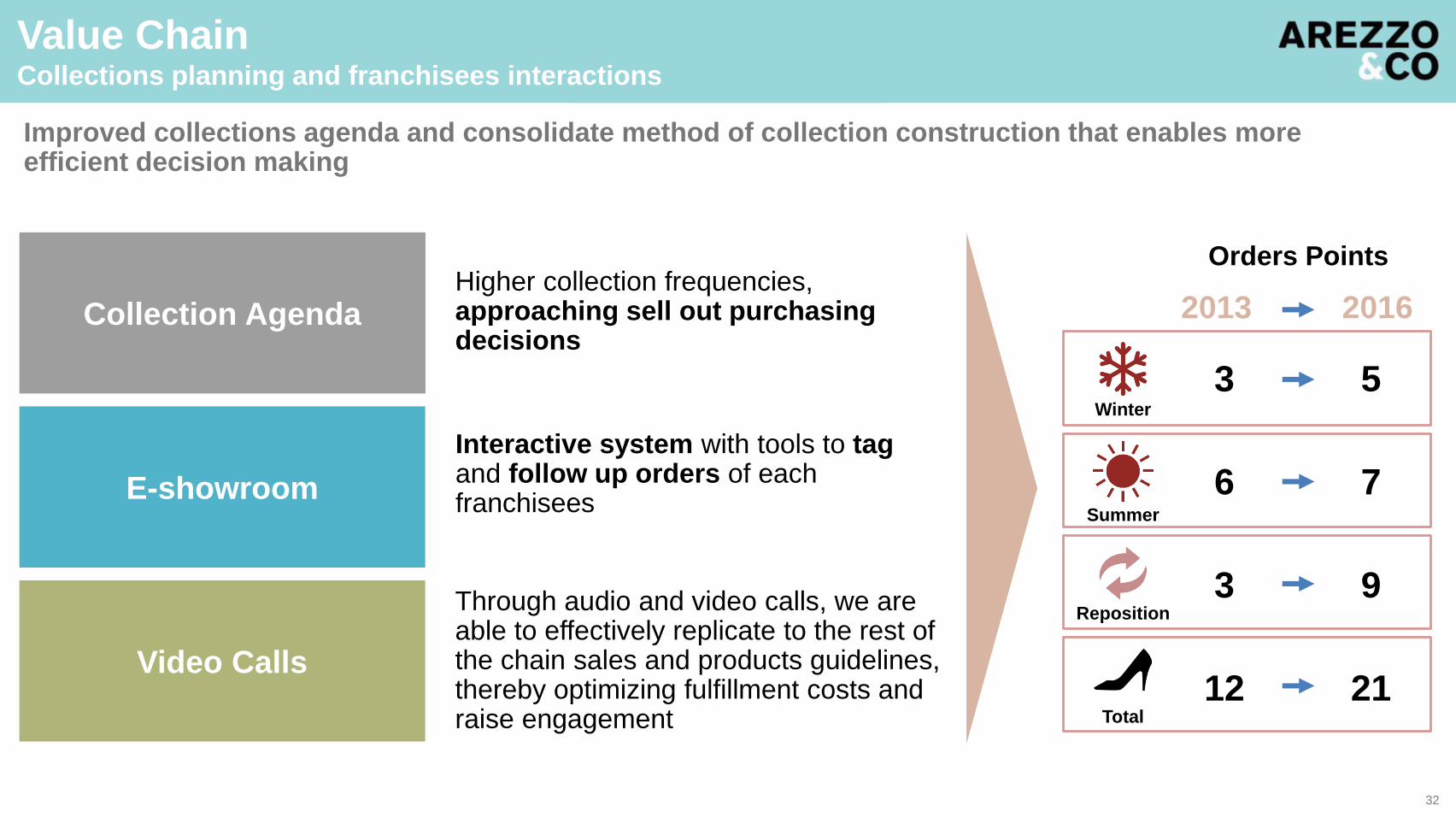

Improved collections agenda and consolidate method of collection construction that enables more efficient decision making

Collection Agenda

E-showroom

Video Calls

Value ChainCollections planning and franchisees interactions

Higher collection frequencies, approaching sell out purchasing decisions

Through audio and video calls, we are able to effectively replicate to the rest of the chain sales and products guidelines, thereby optimizing fulfillment costs and raise engagement

2013 2016

Orders Points

Winter

Summer

Reposition

Total

3

6

3

12

5

7

9

21

32

Interactive system with tools to tag and follow up orders of each franchisees

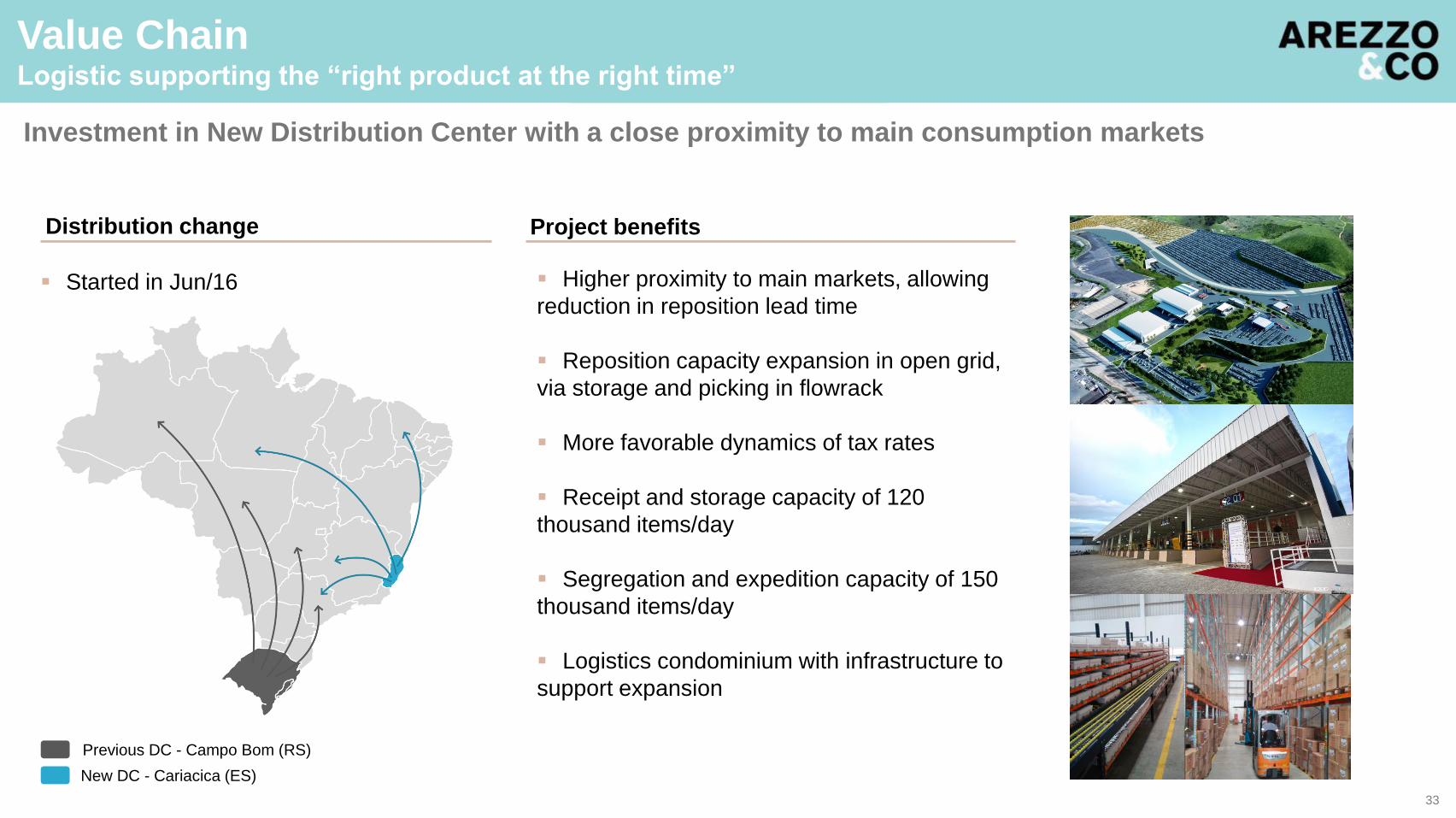

Distribution change Project benefits

Previous DC - Campo Bom (RS)

New DC - Cariacica (ES)

Higher proximity to main markets, allowing

reduction in reposition lead time

Reposition capacity expansion in open grid,

via storage and picking in flowrack

More favorable dynamics of tax rates

Receipt and storage capacity of 120

thousand items/day

Segregation and expedition capacity of 150

thousand items/day

Logistics condominium with infrastructure to

support expansion

Investment in New Distribution Center with a close proximity to main consumption markets

Value ChainLogistic supporting the “right product at the right time”

Started in Jun/16

33

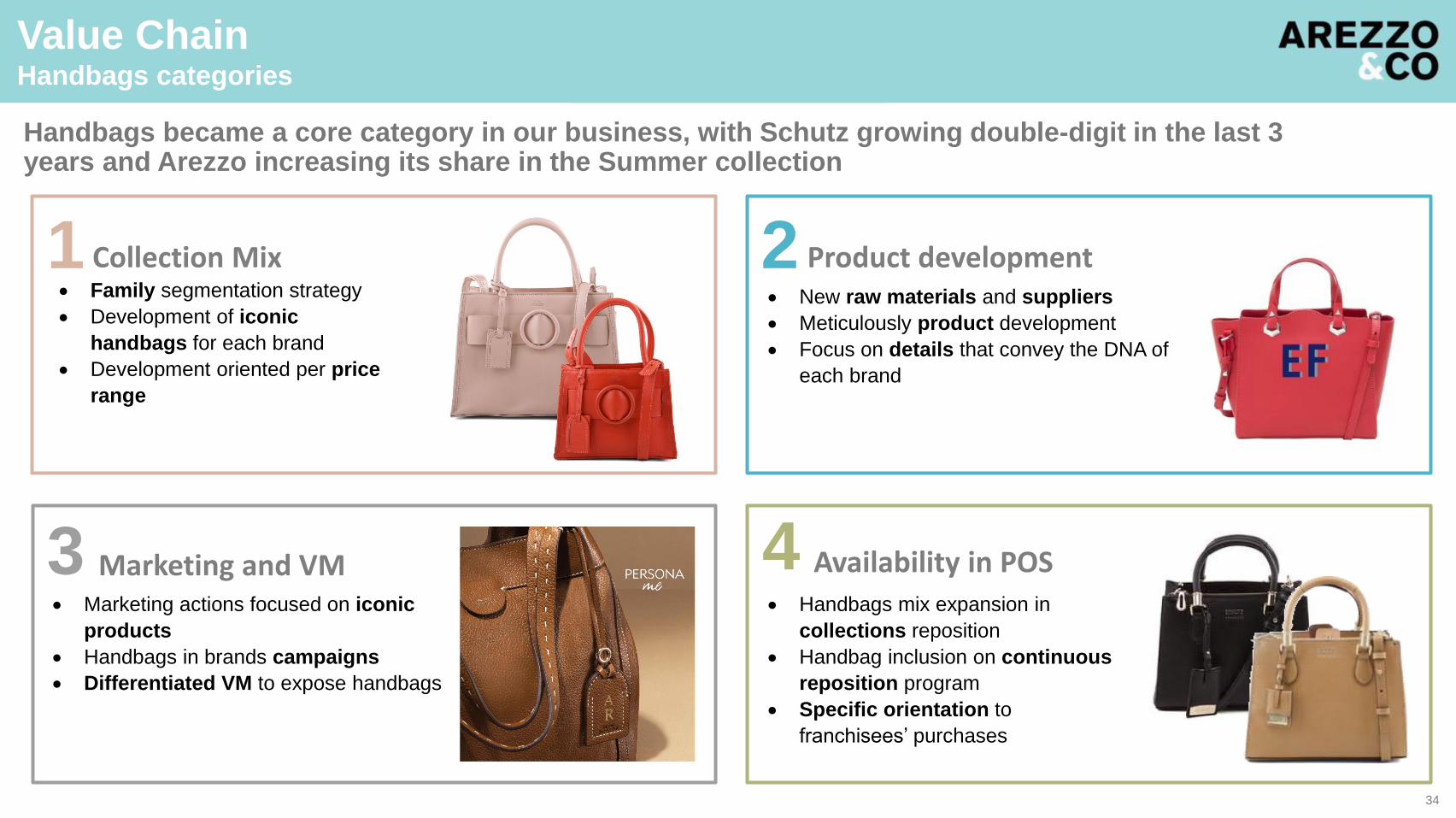

Value ChainHandbags categories

Collection Mix

Availability in POSMarketing and VM

Product development Family segmentation strategy

Development of iconic

handbags for each brand

Development oriented per price

range

New raw materials and suppliers

Meticulously product development

Focus on details that convey the DNA of

each brand

Marketing actions focused on iconic

products

Handbags in brands campaigns

Differentiated VM to expose handbags

Handbags mix expansion in

collections reposition

Handbag inclusion on continuous

reposition program

Specific orientation to

franchisees’ purchases

34

Handbags became a core category in our business, with Schutz growing double-digit in the last 3 years and Arezzo increasing its share in the Summer collection

1

3

2

4

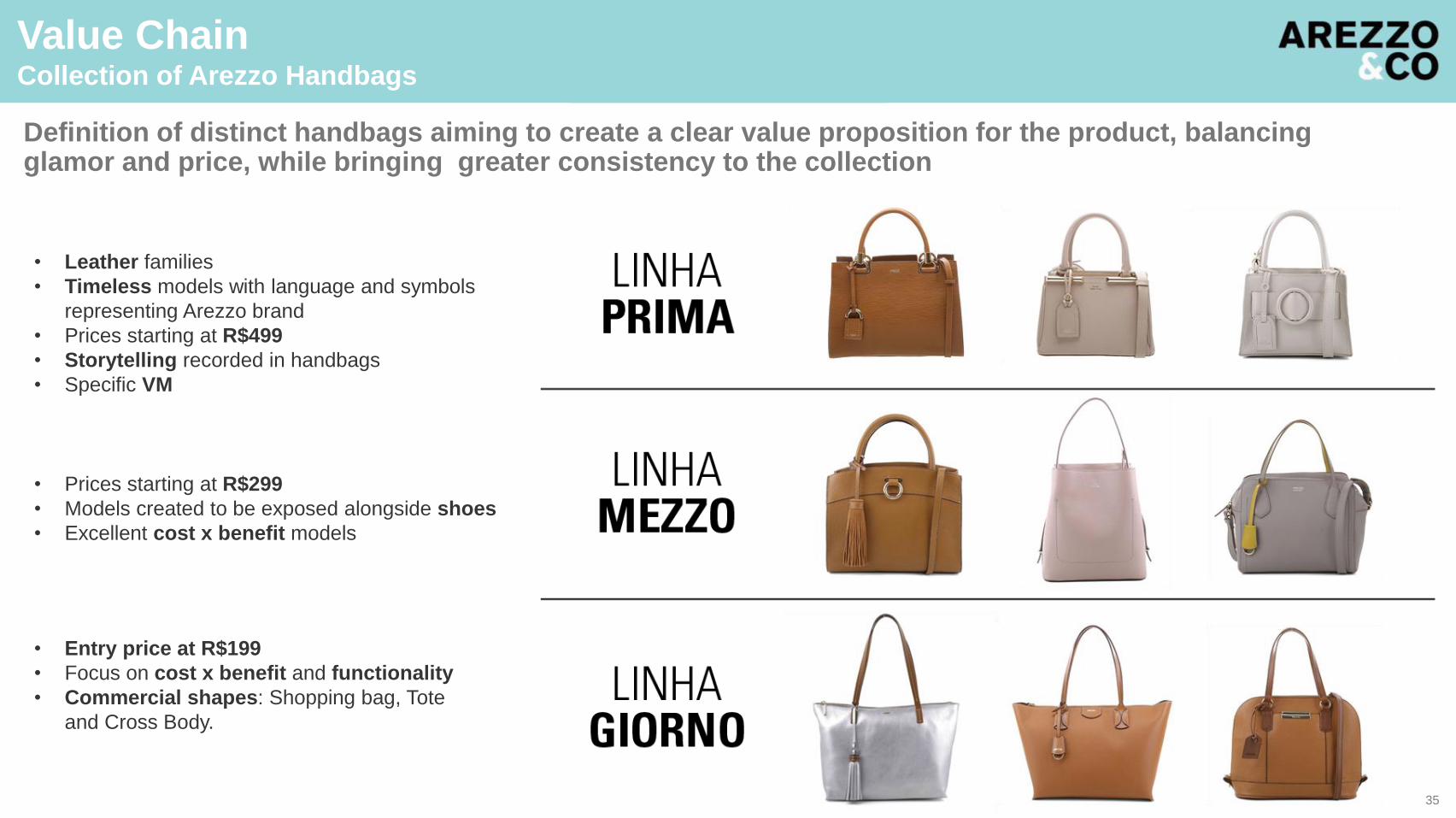

Value ChainCollection of Arezzo Handbags

• Leather families

• Timeless models with language and symbols

representing Arezzo brand

• Prices starting at R$499

• Storytelling recorded in handbags

• Specific VM

• Prices starting at R$299

• Models created to be exposed alongside shoes

• Excellent cost x benefit models

• Entry price at R$199

• Focus on cost x benefit and functionality

• Commercial shapes: Shopping bag, Tote

and Cross Body.

35

Definition of distinct handbags aiming to create a clear value proposition for the product, balancing glamor and price, while bringing greater consistency to the collection

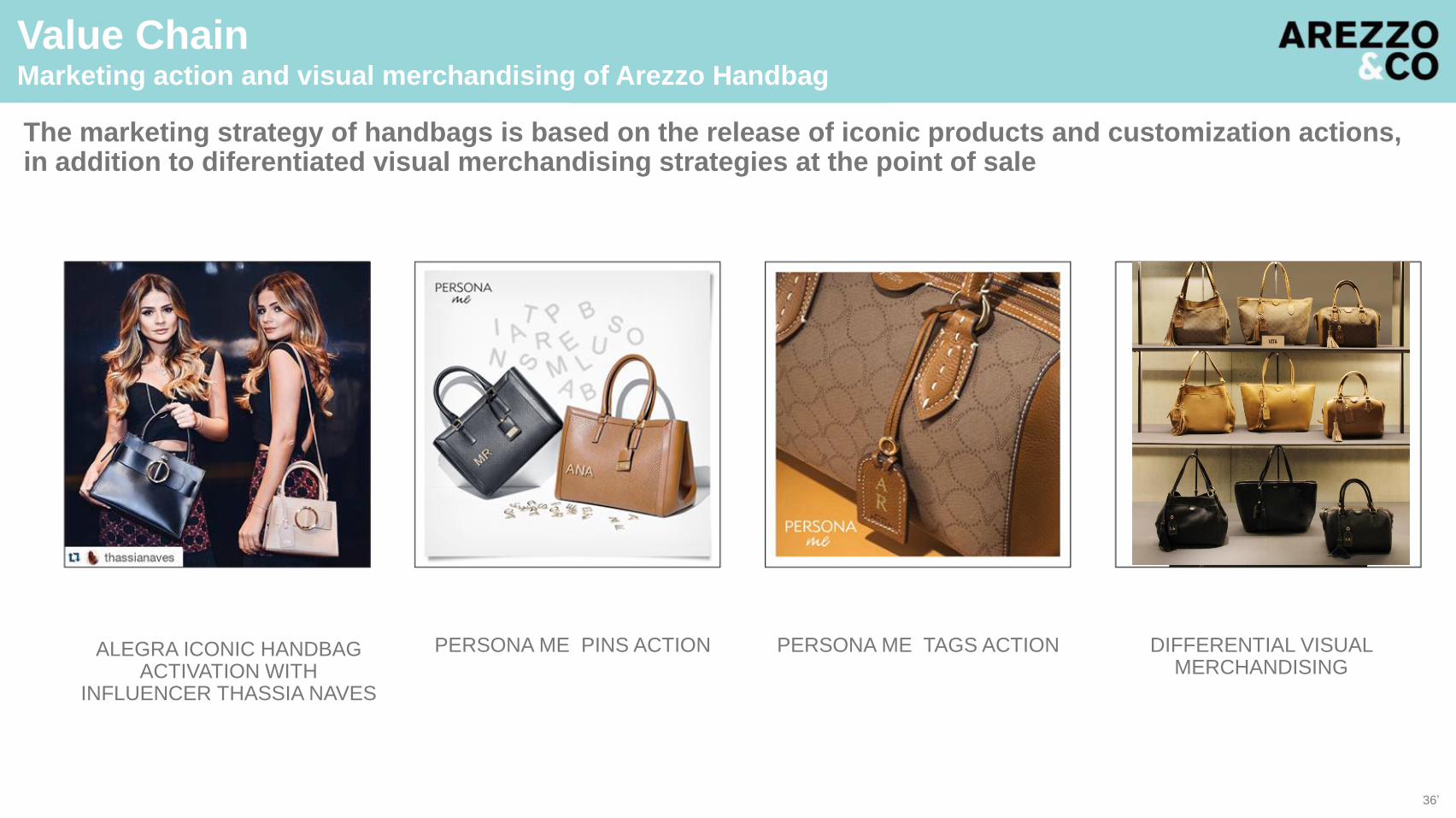

Value ChainMarketing action and visual merchandising of Arezzo Handbag

The marketing strategy of handbags is based on the release of iconic products and customization actions, in addition to diferentiated visual merchandising strategies at the point of sale

ALEGRA ICONIC HANDBAG ACTIVATION WITH

INFLUENCER THASSIA NAVES

PERSONA ME PINS ACTION PERSONA ME TAGS ACTION DIFFERENTIAL VISUAL MERCHANDISING

36’

Value ChainThe right product at the right time + Client experience with brand

FRANCHISEES MANAGEMENT

PRODUCT MANAGEMENT

37

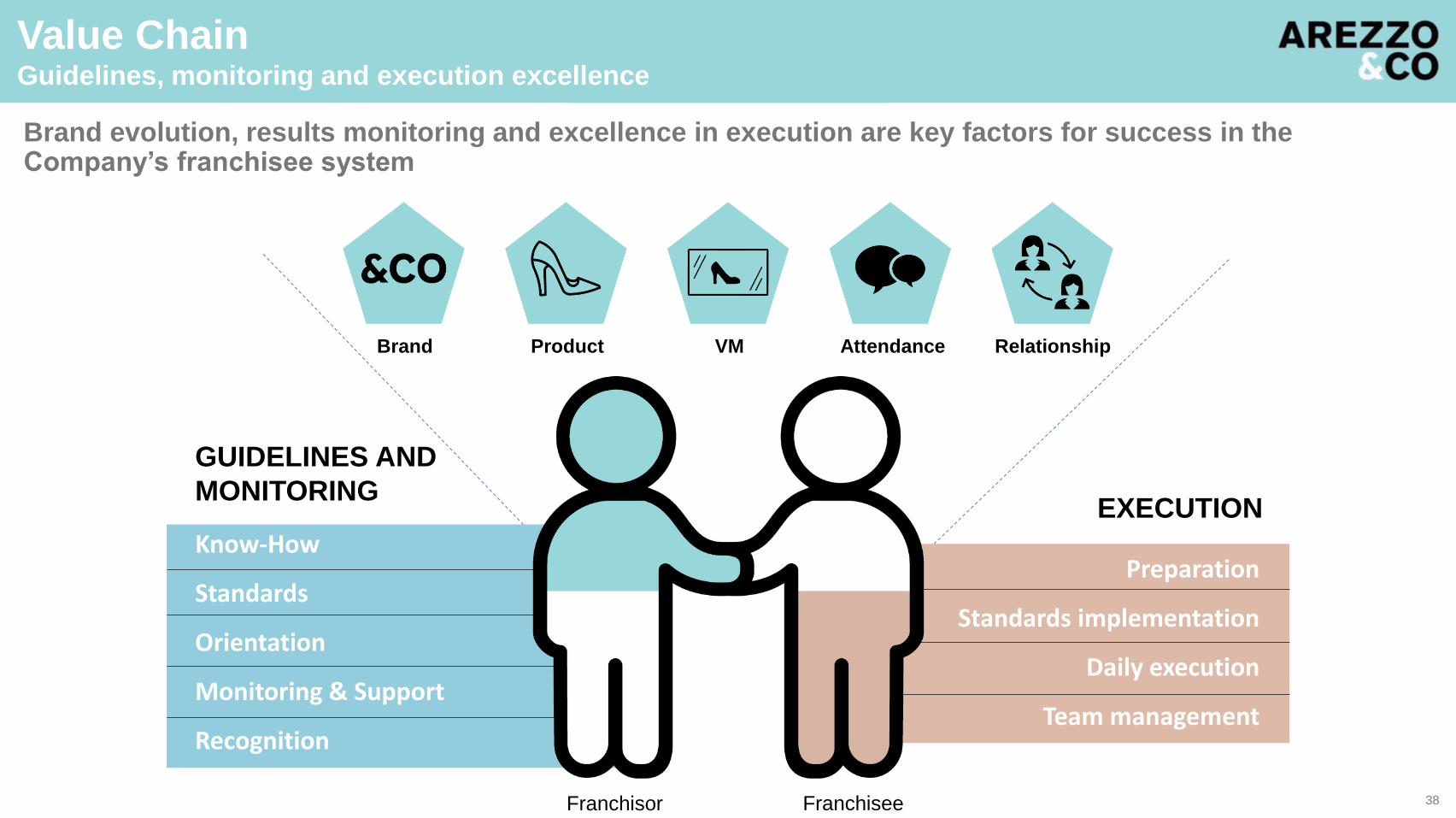

Value ChainGuidelines, monitoring and execution excellence

Brand evolution, results monitoring and excellence in execution are key factors for success in the Company’s franchisee system

GUIDELINES AND

MONITORINGEXECUTION

Know-How

Standards

Orientation

Monitoring & Support

Recognition

Preparation

Standards implementation

Daily execution

Team management

38

Brand Product VM Attendance Relationship

Franchisor Franchisee

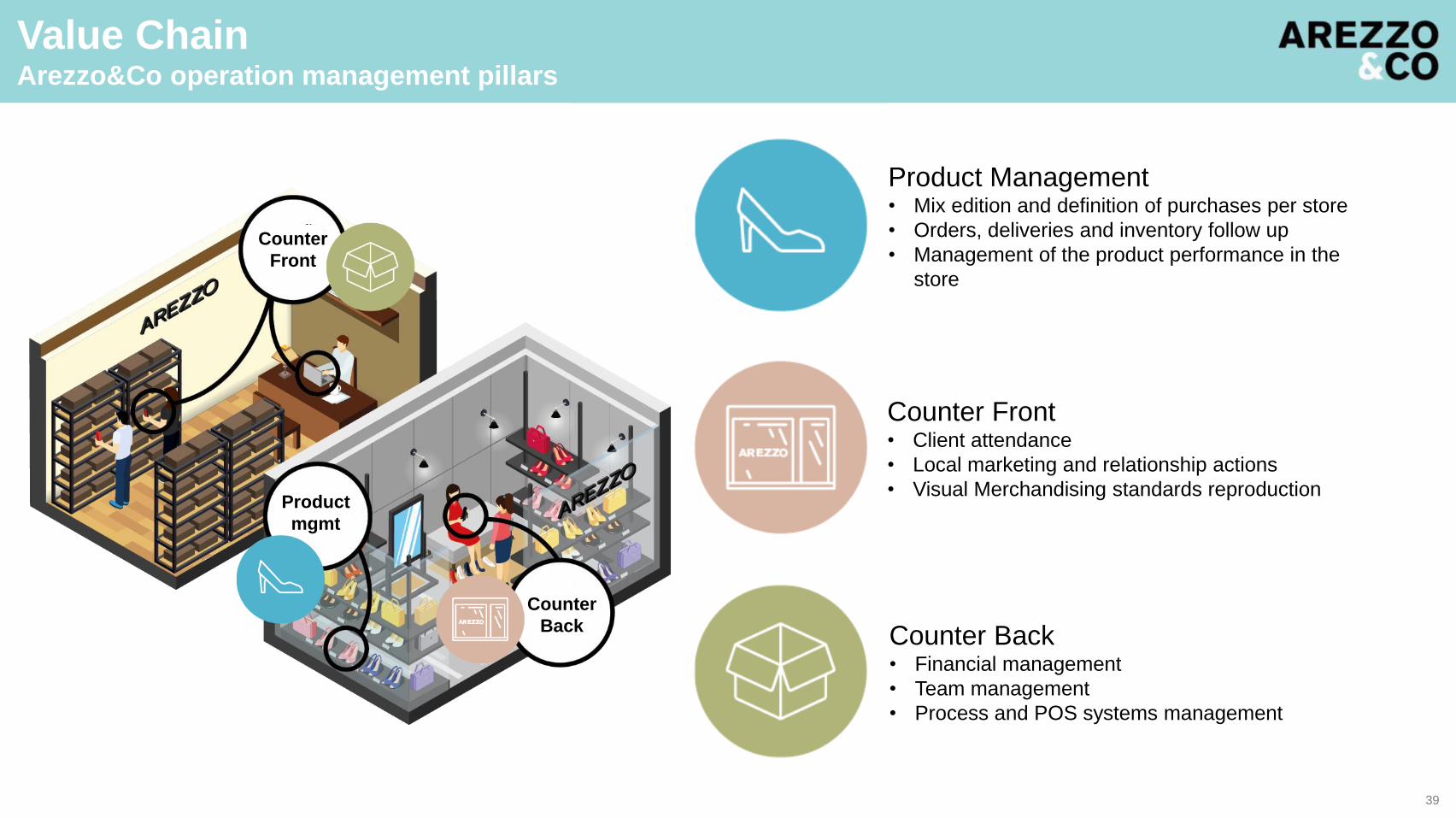

Value ChainArezzo&Co operation management pillars

Product Management• Mix edition and definition of purchases per store

• Orders, deliveries and inventory follow up

• Management of the product performance in the

store

Counter Front• Client attendance

• Local marketing and relationship actions

• Visual Merchandising standards reproduction

Counter Back• Financial management

• Team management

• Process and POS systems management

39

Counter

Front

Counter

Back

Product

mgmt

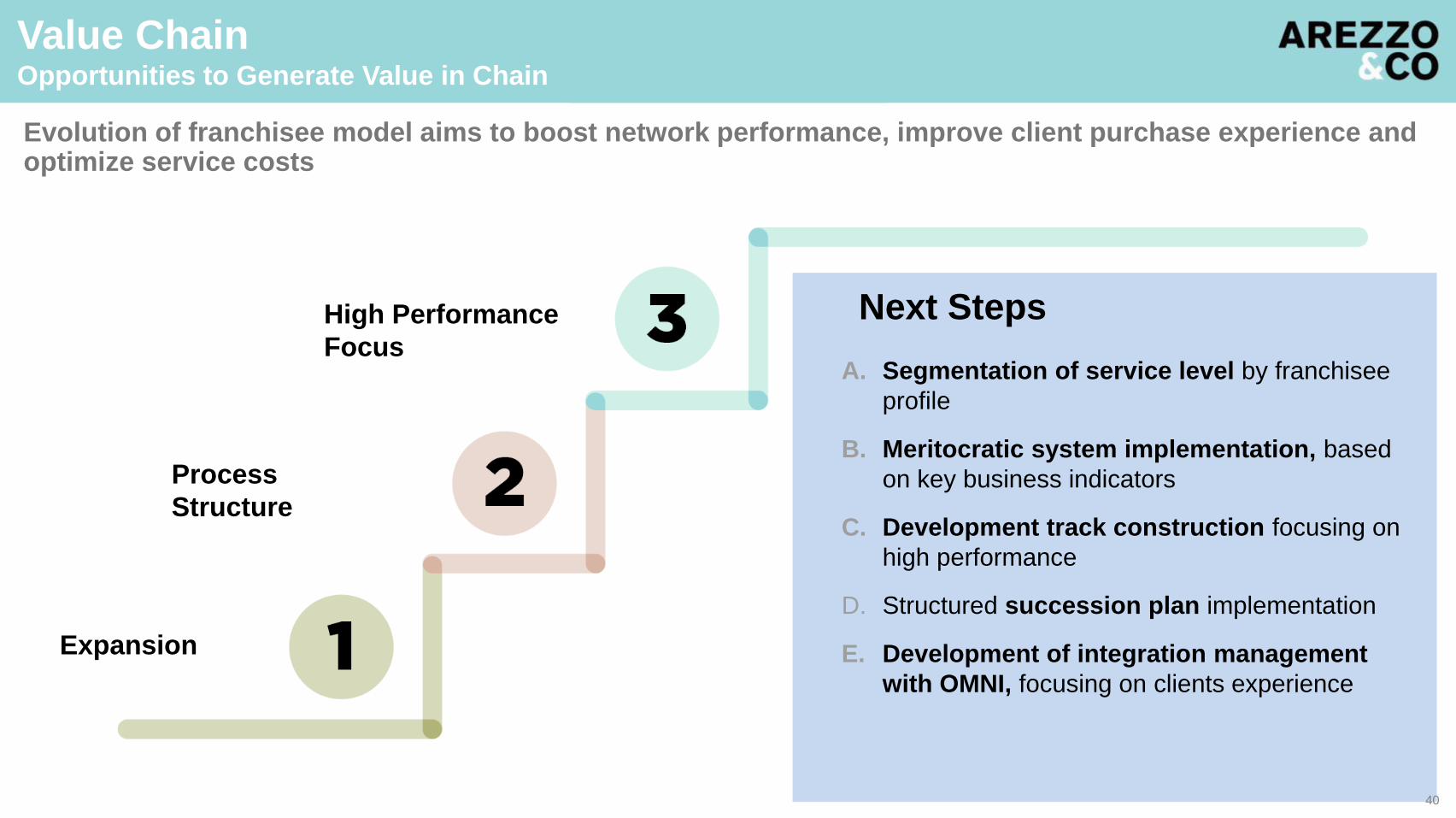

Value ChainOpportunities to Generate Value in Chain

Evolution of franchisee model aims to boost network performance, improve client purchase experience and optimize service costs

A. Segmentation of service level by franchisee

profile

B. Meritocratic system implementation, based

on key business indicators

C. Development track construction focusing on

high performance

D. Structured succession plan implementation

E. Development of integration management

with OMNI, focusing on clients experience

Next Steps

Expansion

Process

Structure

High Performance

Focus

40

Integrated actions in product management and the planning of collections, sell-out supply model and collective attendance, saw better chain-wide results

1

Higher order frequency throughout the year, with input from franchisees via E-show room and Product Comitte allowed for greater assortment decisions

2

Stores supply more agile and collaborative, from initial planning of volumes up to repositions of collection items and continuable, leveraging sales results and margin

3

Better understanding of each operator profile and adequate service will be the base of a clusterized and meritocratic system, promoting high performance across the network, improving shopping experience

5

Endless evolution of brand guidelines, continuous monitoring of results and excellence in execution are key factors for success in a franchised operating model

4

Value ChainKey messages

41

Arezzo&Co Investor DayOMNI and Valorizza

Mauricio BastosOMNI Manager

BEING OMNI MEANS TO BE PRESENT ACROSS ALL RELEVANT CONTACT

POINTS TO OUR CLIENTS, PROMOTING A UNIQUE EXPERIENCE

(UNFORGETTABLE AND INTEGRATED)

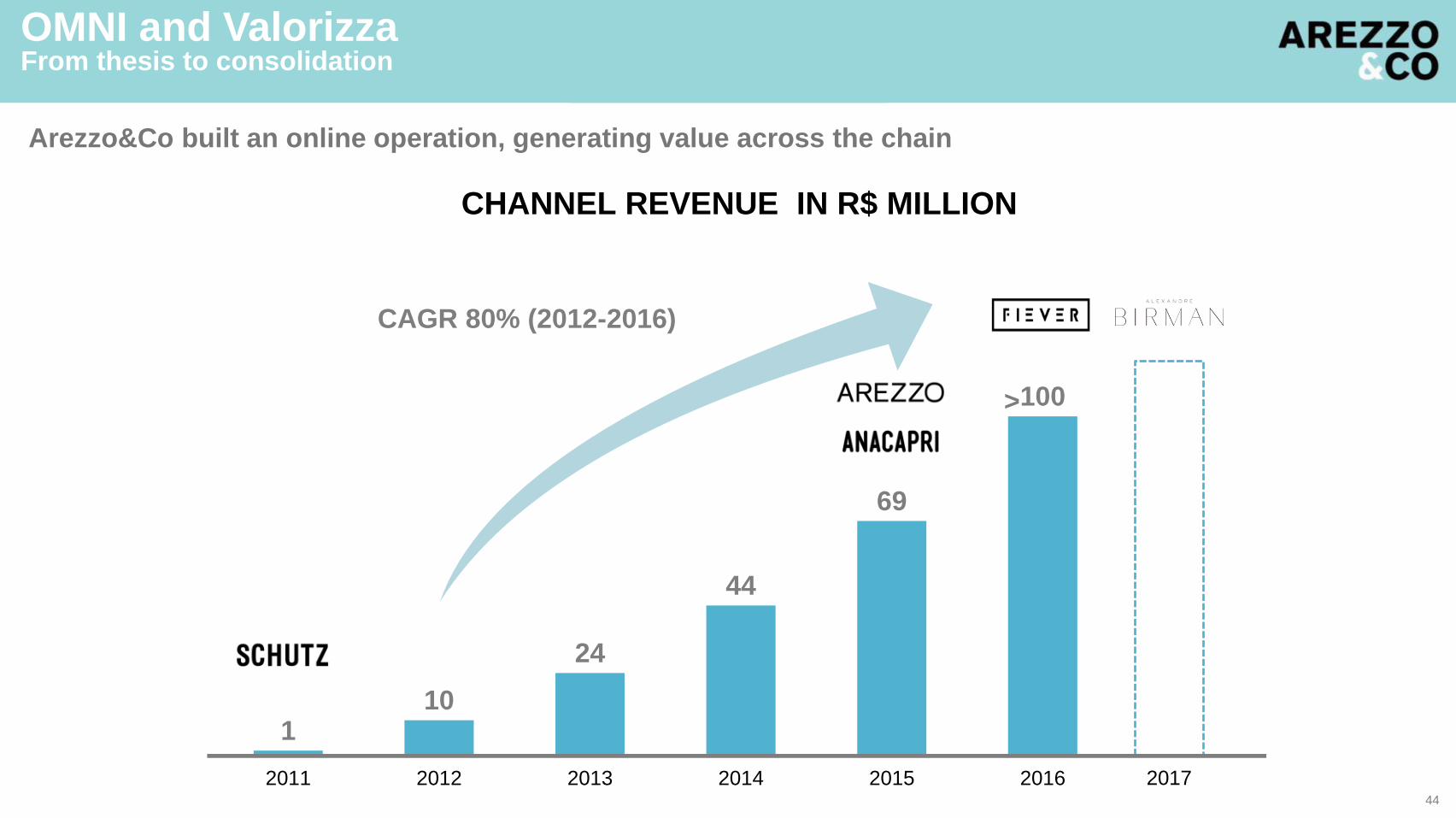

OMNI and ValorizzaFrom thesis to consolidation

43

CAGR 80% (2012-2016)

>

110

24

44

69

100

2011 2012 2013 2014 2015 2016

Arezzo&Co built an online operation, generating value across the chain

CHANNEL REVENUE IN R$ MILLION

OMNI and ValorizzaFrom thesis to consolidation

201744

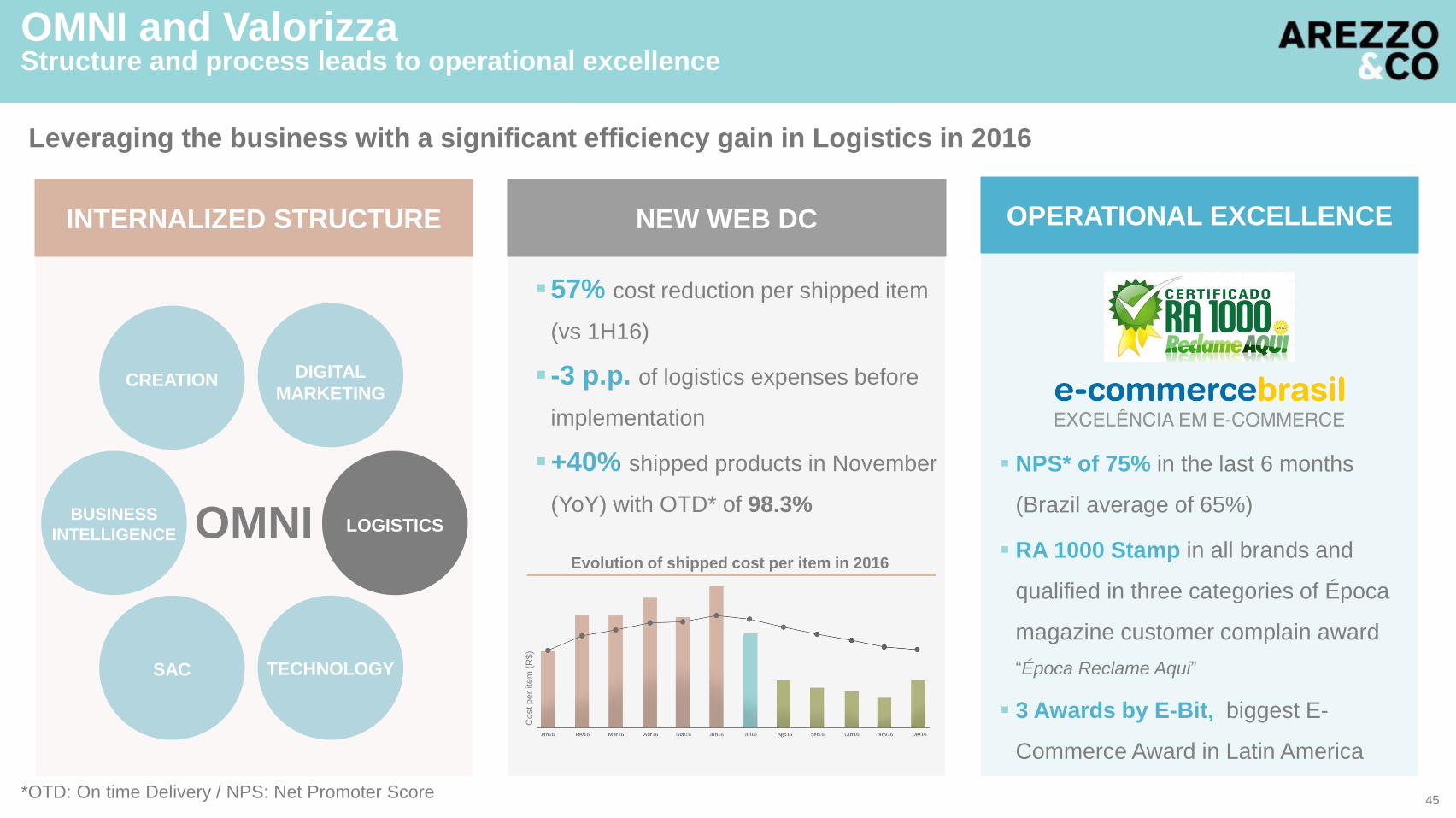

INTERNALIZED STRUCTURE NEW WEB DC OPERATIONAL EXCELLENCE

OMNI

CREATION

LOGISTICS

DIGITAL

MARKETING

BUSINESS

INTELLIGENCE

TECHNOLOGYSAC

Leveraging the business with a significant efficiency gain in Logistics in 2016

57% cost reduction per shipped item

(vs 1H16)

-3 p.p. of logistics expenses before

implementation

+40% shipped products in November

(YoY) with OTD* of 98.3%

NPS* of 75% in the last 6 months

(Brazil average of 65%)

RA 1000 Stamp in all brands and

qualified in three categories of Época

magazine customer complain award

“Época Reclame Aqui”

3 Awards by E-Bit, biggest E-

Commerce Award in Latin America

OMNI and ValorizzaStructure and process leads to operational excellence

Evolution of shipped cost per item in 2016

Cost per

item

(R

$)

*OTD: On time Delivery / NPS: Net Promoter Score45

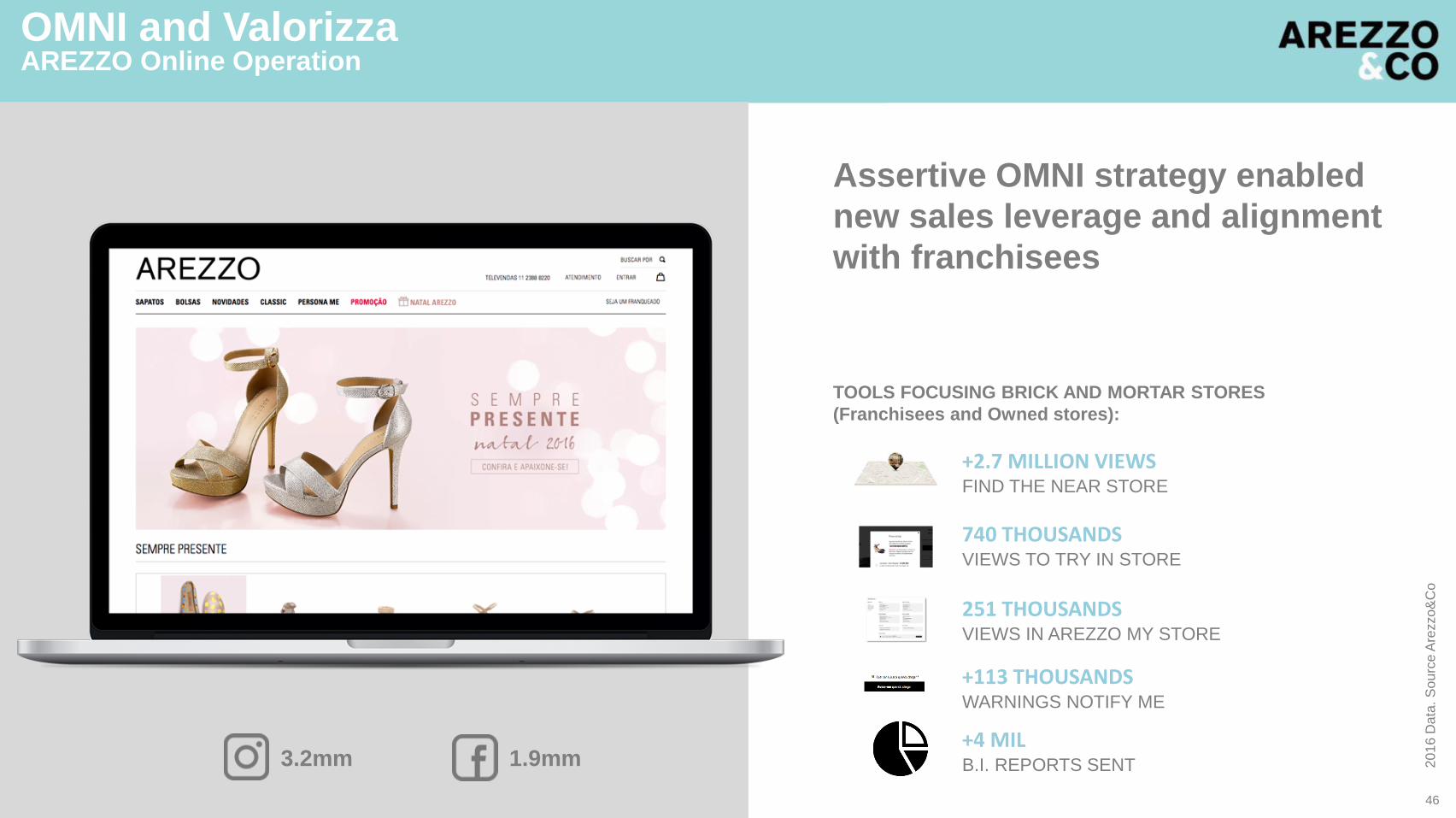

Assertive OMNI strategy enabled

new sales leverage and alignment

with franchisees

20

16

Data

. S

ou

rce A

rezzo

&C

o

OMNI and ValorizzaAREZZO Online Operation

3.2mm 1.9mm

TOOLS FOCUSING BRICK AND MORTAR STORES

(Franchisees and Owned stores):

+2.7 MILLION VIEWSFIND THE NEAR STORE

740 THOUSANDSVIEWS TO TRY IN STORE

251 THOUSANDSVIEWS IN AREZZO MY STORE

+113 THOUSANDSWARNINGS NOTIFY ME

+4 MILB.I. REPORTS SENT

46

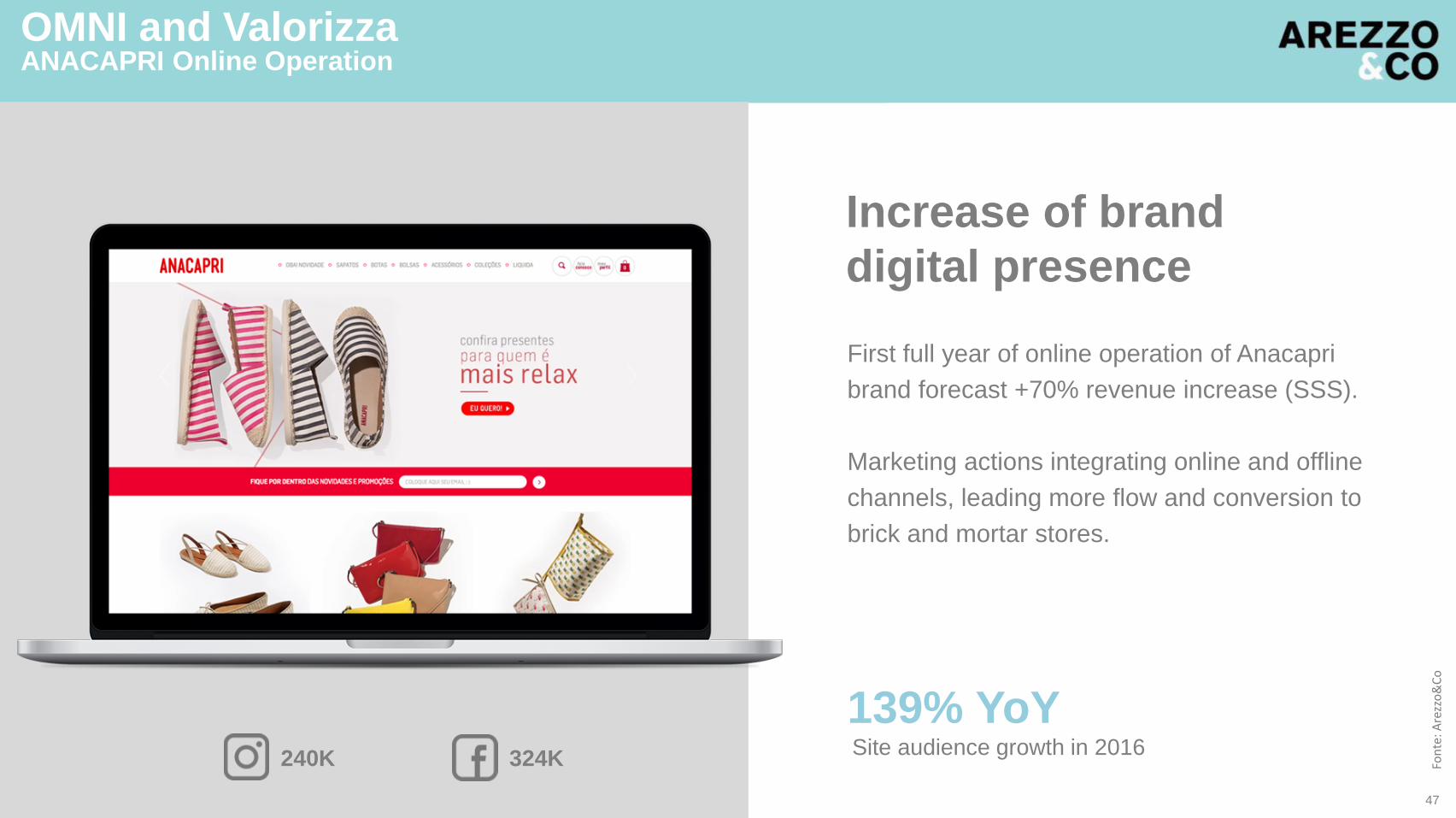

OMNI and ValorizzaANACAPRI Online Operation

240K 324K

First full year of online operation of Anacapri

brand forecast +70% revenue increase (SSS).

Marketing actions integrating online and offline

channels, leading more flow and conversion to

brick and mortar stores.

Increase of brand

digital presence

139% YoYSite audience growth in 2016

Fon

te: A

rezz

o&

Co

47

OMNI and ValorizzaFIEVER Online Operation

39.8k (+148%) 26.1k (+1.353%)

Increase in 5/12 compared to 30/08

Fiever was born digital

• Future projects can be launched faster with lower

investments.

• Lighter platform, with lower customization necessity

• Reduced launch time, 3 months

MAINS PROJECT LESSONS :

Online presence a tool to improve

BRAND AWARENESS.

155% increase in brand search on Google

80 cities already received Fiever products

Sou

rce:

Are

zzo

&C

o

48

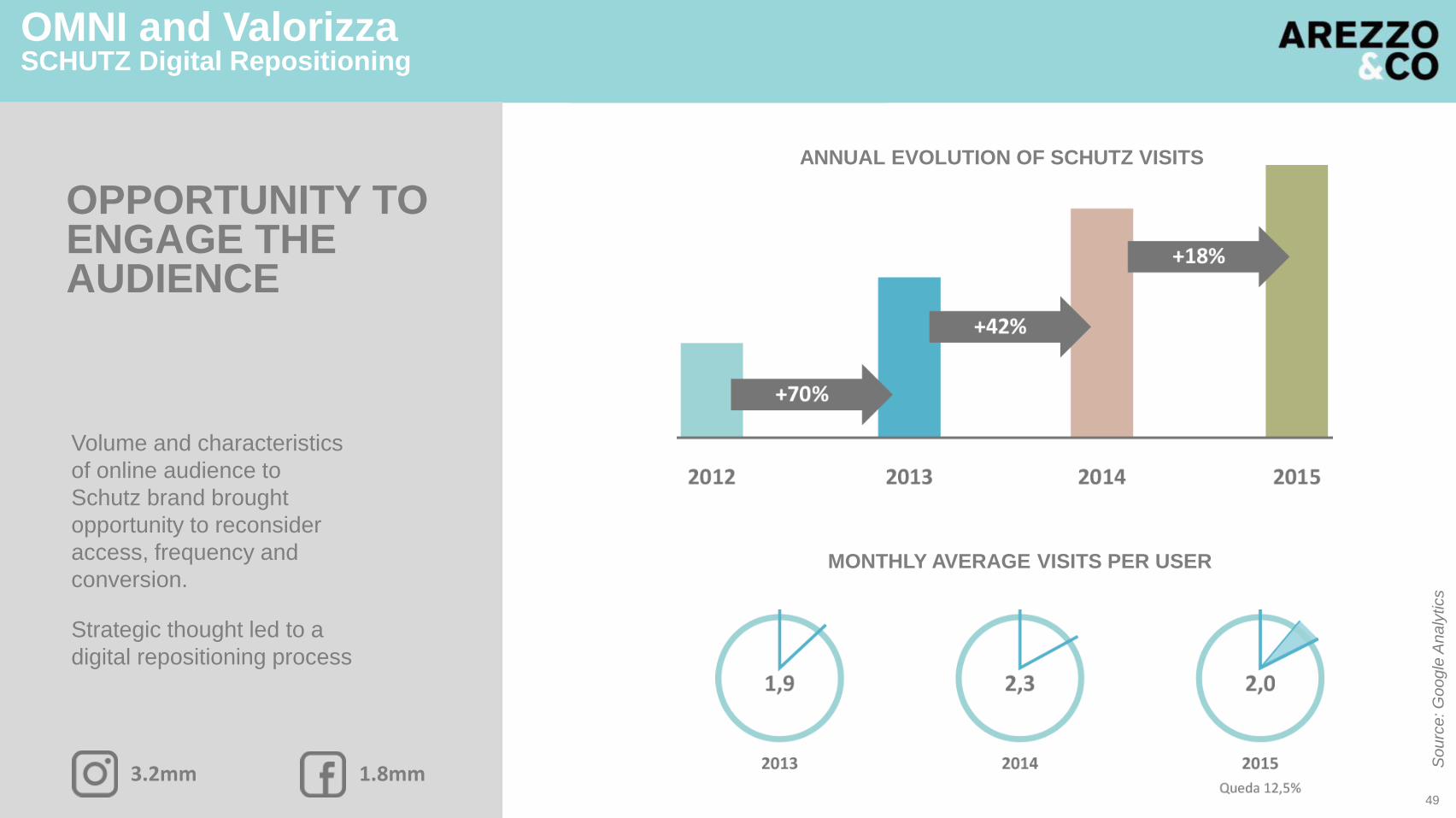

OPPORTUNITY TO ENGAGE THE AUDIENCE

Volume and characteristics

of online audience to

Schutz brand brought

opportunity to reconsider

access, frequency and

conversion.

Strategic thought led to a

digital repositioning process

ANNUAL EVOLUTION OF SCHUTZ VISITS

MONTHLY AVERAGE VISITS PER USER

OMNI and ValorizzaSCHUTZ Digital Repositioning

So

urc

e: G

oo

gle

An

aly

tics

3.2mm 1.8mm49

OMNI and ValorizzaSCHUTZ Digital Repositioning

50

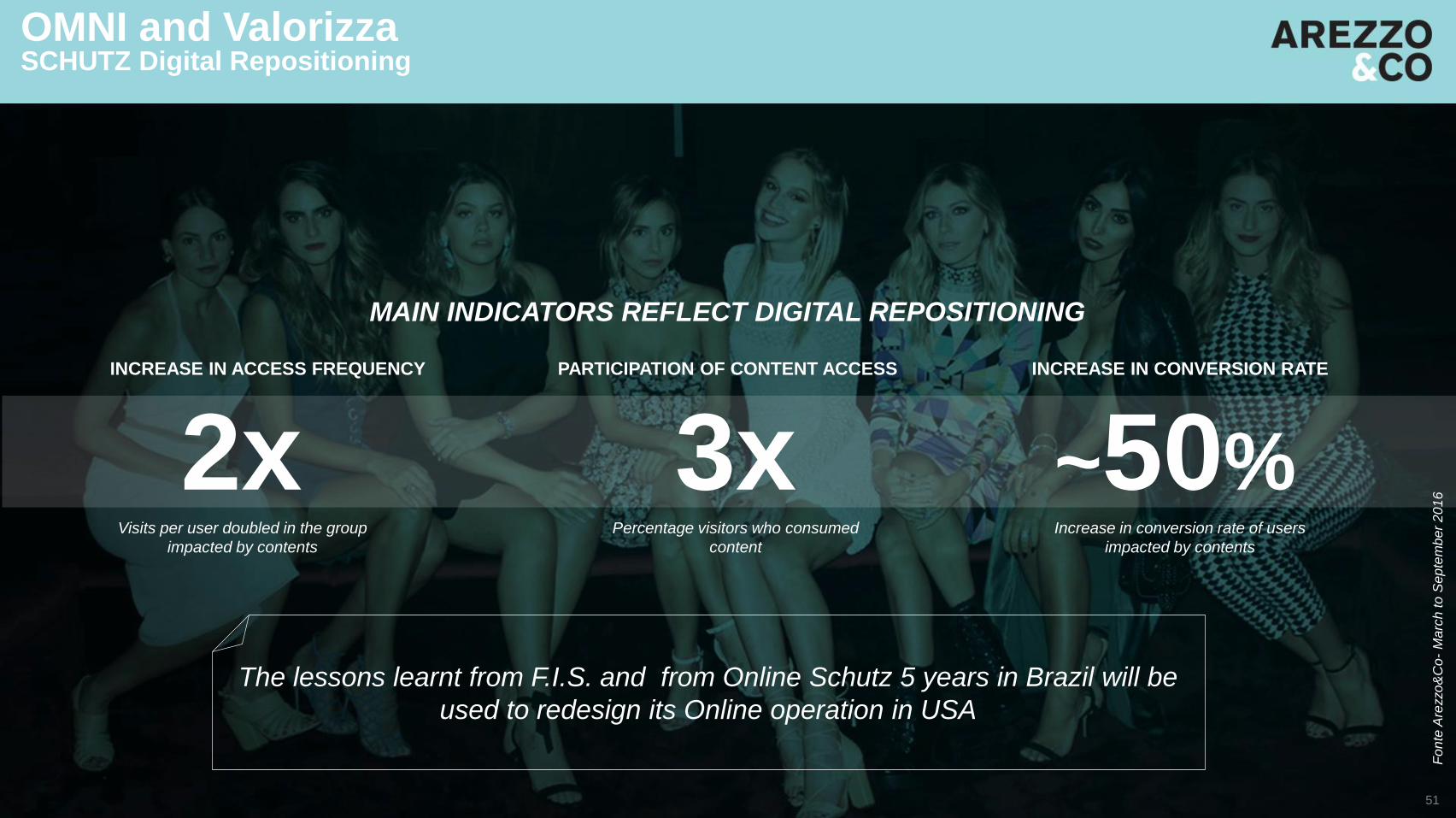

MAIN INDICATORS REFLECT DIGITAL REPOSITIONING

Fo

nte

Are

zzo

&C

o-

Ma

rch to

Se

pte

mb

er

20

16

INCREASE IN ACCESS FREQUENCY PARTICIPATION OF CONTENT ACCESS INCREASE IN CONVERSION RATE

2xVisits per user doubled in the group

impacted by contents

3xPercentage visitors who consumed

content

~50%Increase in conversion rate of users

impacted by contents

The lessons learnt from F.I.S. and from Online Schutz 5 years in Brazil will be

used to redesign its Online operation in USA

OMNI and ValorizzaSCHUTZ Digital Repositioning

51

NEW APP

LAUNCHED

ALIGNED TO F.I.S

CONCEPT

3x moreDepth in navigation (screens

seen per visit)

0.3% 5%increase in revenue share

via app

21%revenue increase before

Android availability

NEW MOBILE SITE

LAUNCHED WITH

SCHUTZ F.I.S. TURN

AROUND

20%conversion increase compared

to September 2015

50% 55%Increase in mobile

audience share

50%mobile revenue + tablet

Sou

rce:

Are

zzo

&C

o

OMNI and ValorizzaSCHUTZ Digital Repositioning

52

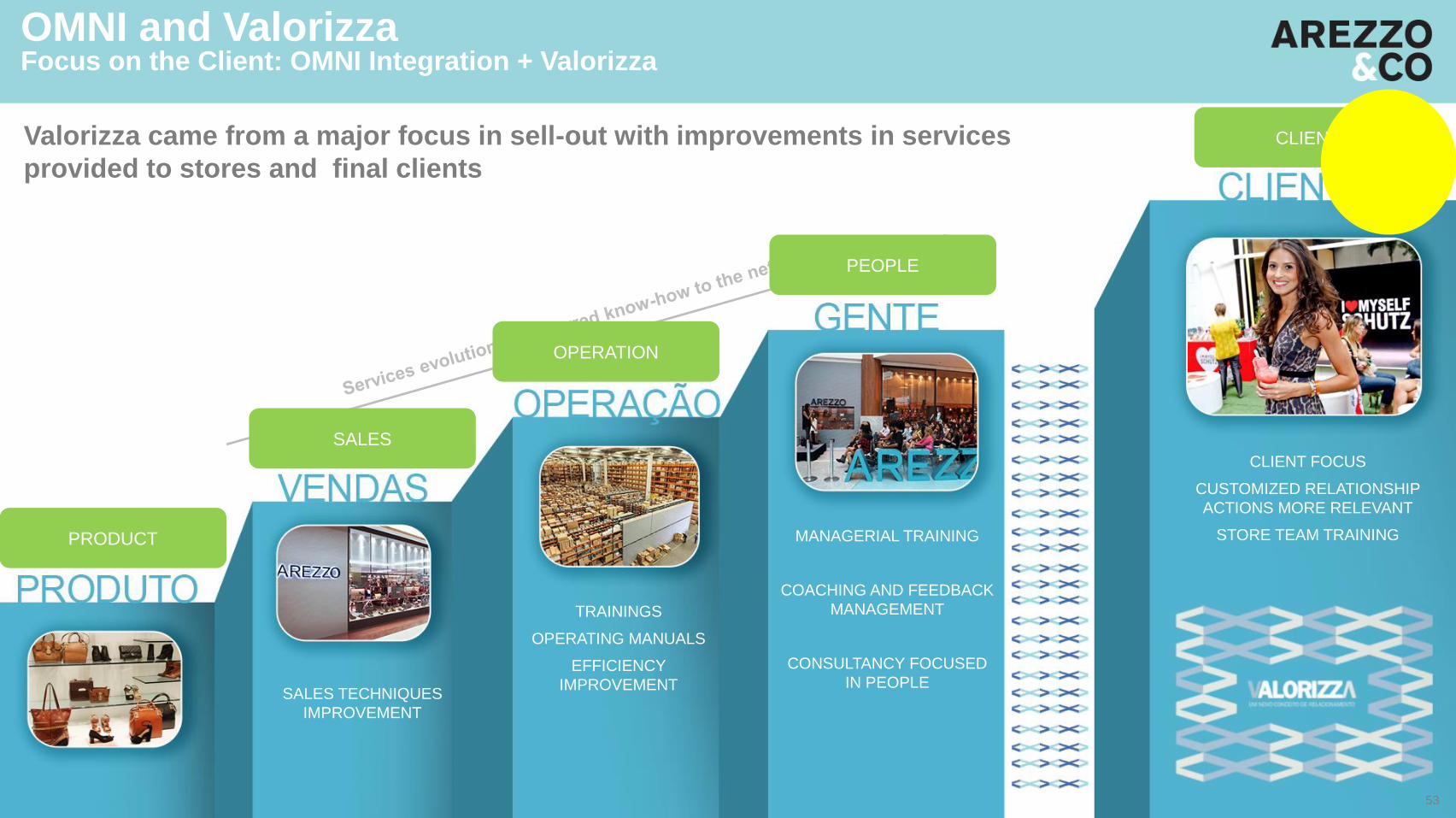

Valorizza came from a major focus in sell-out with improvements in services

provided to stores and final clients

SALES TECHNIQUES

IMPROVEMENT

TRAININGS

OPERATING MANUALS

EFFICIENCY

IMPROVEMENT

MANAGERIAL TRAINING

COACHING AND FEEDBACK

MANAGEMENT

CONSULTANCY FOCUSED

IN PEOPLE

CLIENT FOCUS

CUSTOMIZED RELATIONSHIP

ACTIONS MORE RELEVANT

STORE TEAM TRAINING

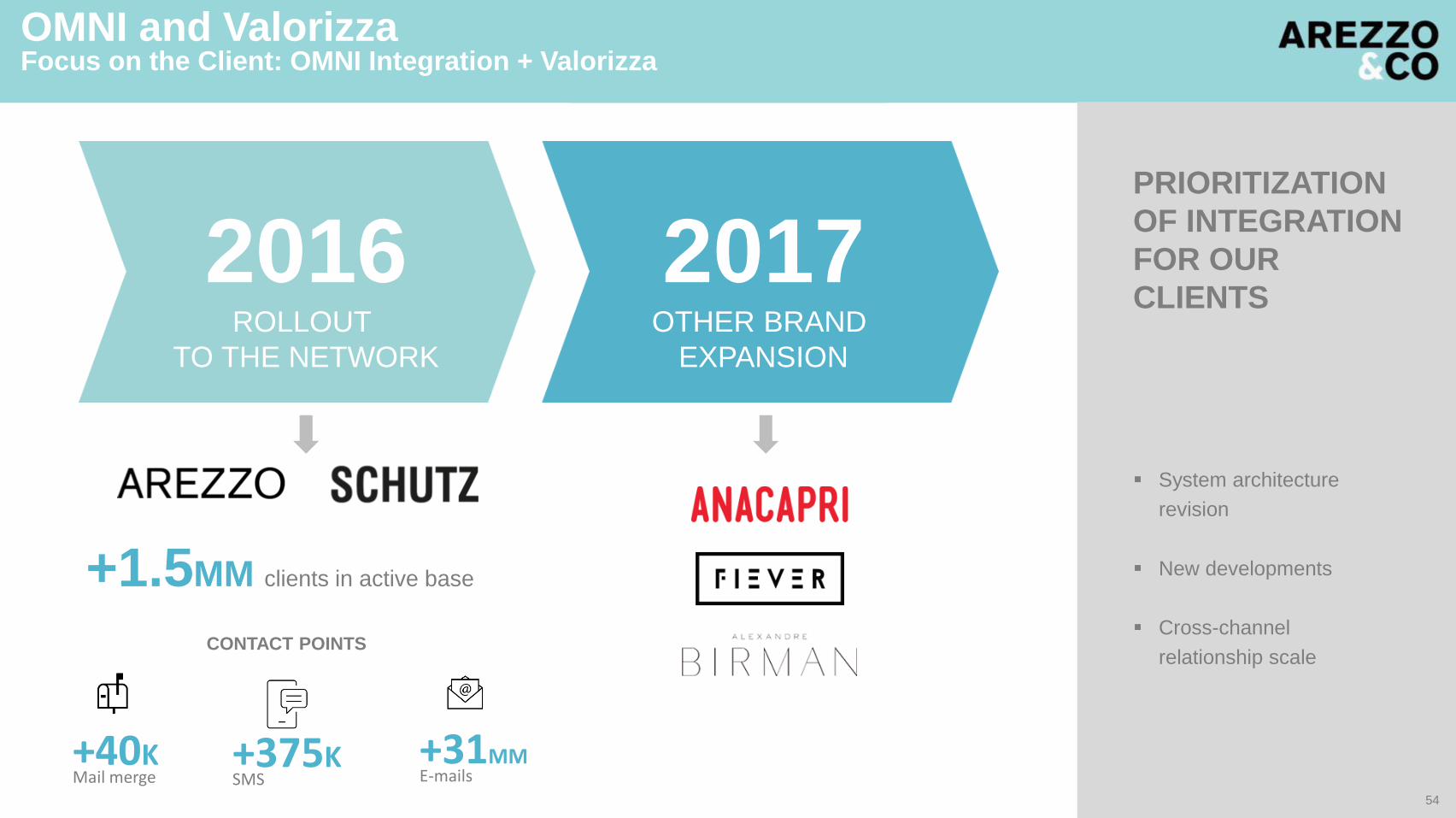

OMNI and ValorizzaFocus on the Client: OMNI Integration + Valorizza

PRODUCT

SALES

OPERATION

PEOPLE

CLIENT

53

2016ROLLOUT

TO THE NETWORK

2017OTHER BRAND

EXPANSION

PRIORITIZATION

OF INTEGRATION

FOR OUR

CLIENTS

System architecture

revision

New developments

Cross-channel

relationship scale

+40KMail merge

+375KSMS

+31MME-mails

+1.5MM clients in active base

CONTACT POINTS

OMNI and ValorizzaFocus on the Client: OMNI Integration + Valorizza

54

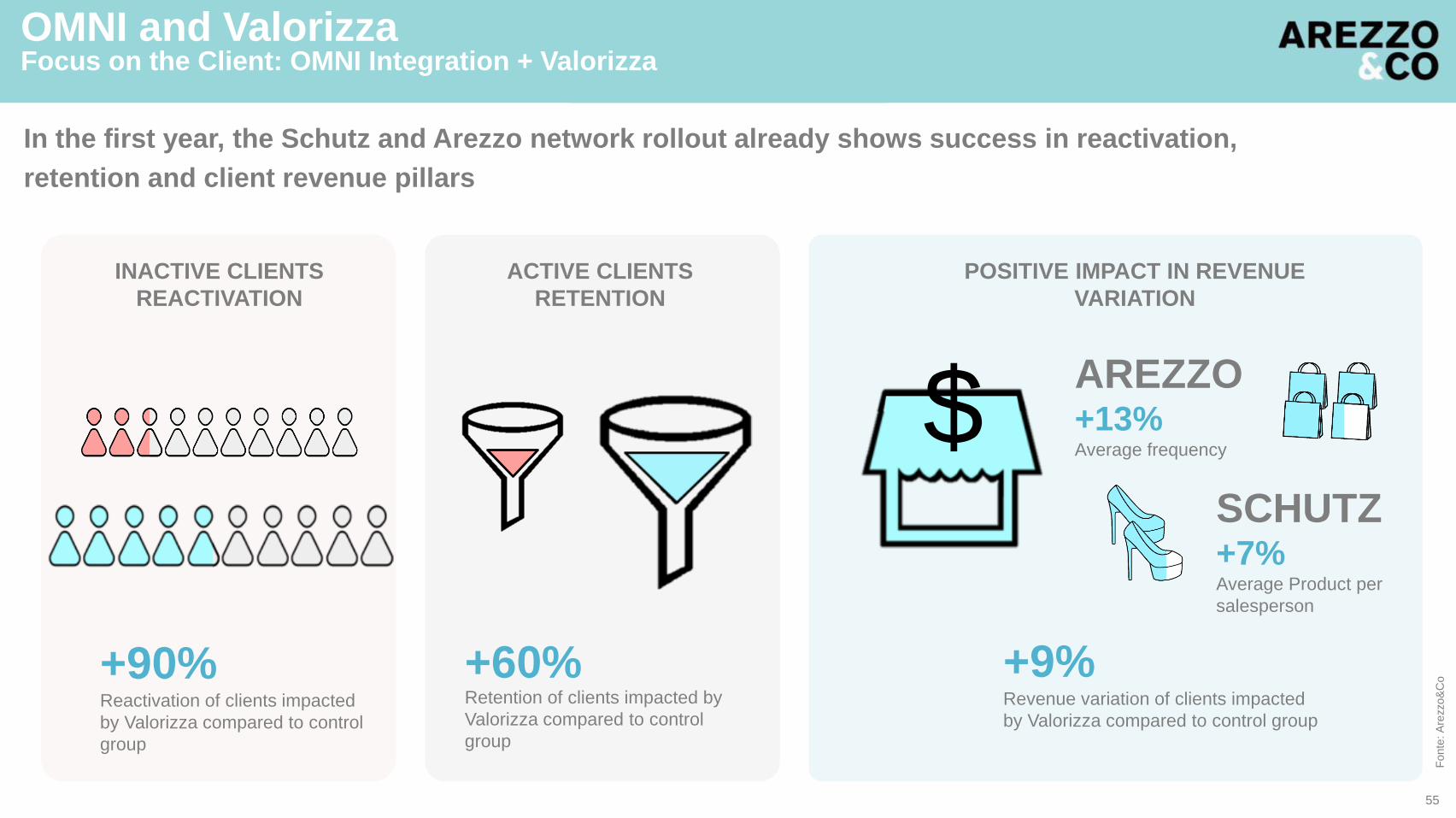

ACTIVE CLIENTS

RETENTION

+60%Retention of clients impacted by

Valorizza compared to control

group

INACTIVE CLIENTS

REACTIVATION

+90%Reactivation of clients impacted

by Valorizza compared to control

group

AREZZO+13%Average frequency

SCHUTZ+7%Average Product per

salesperson

Fonte

: A

rezzo&

Co

POSITIVE IMPACT IN REVENUE

VARIATION

+9%Revenue variation of clients impacted

by Valorizza compared to control group

$

In the first year, the Schutz and Arezzo network rollout already shows success in reactivation,

retention and client revenue pillars

OMNI and ValorizzaFocus on the Client: OMNI Integration + Valorizza

55

Maturation of OMNI client journey

fundamentals

ISOLATED

EXPERIENCES

ONLINE INTEGRATION

OFFLINE INTEGRATION

OMNI INTEGRATION

OMNI INNOVATION

Customization in a single point of contact, using data for a unique channel. Fewer synergy actions. Low integration

Personalization in digital contact points using information from all channels

Personalization in physical contact points using information from all channels

Consistent and integrated experience between channels with journey approaching multiples points of contact

Interactions 1:1 real time

ON and OFF

approach still

with limited

points of contact

Online

experience

personalized

starting from ON

and OFF data

integration

Customized

physical

experiences

starting from ON

and OFF data

integration

Mutual Data

supply from all

channels and

orchestrated

experience

Customized and

individualized

conversations

independent of

the channel or

journey

OMNI and ValorizzaFocus on the Client: OMNI Integration + Valorizza

56

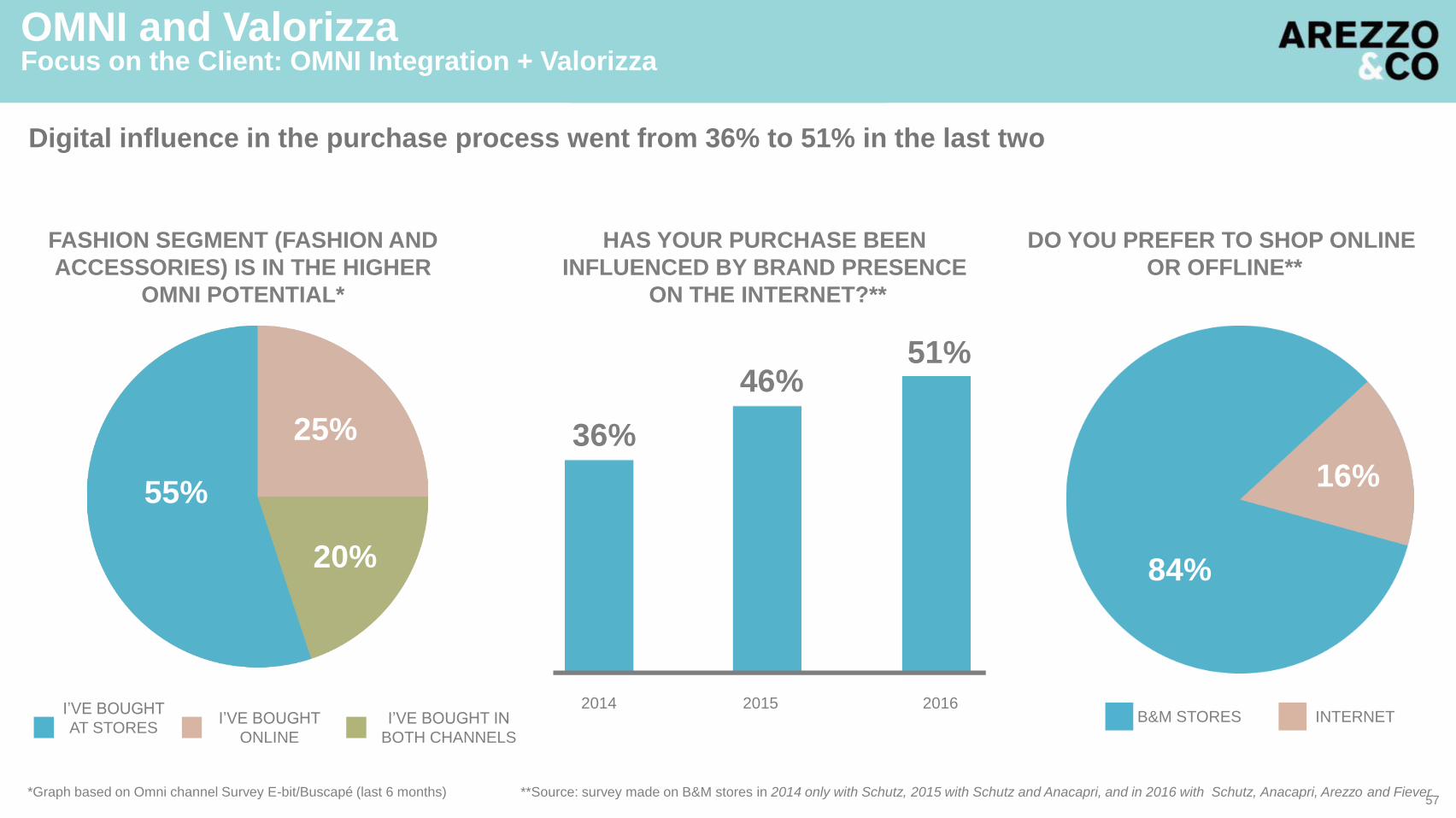

HAS YOUR PURCHASE BEEN

INFLUENCED BY BRAND PRESENCE

ON THE INTERNET?**

2014 2015 2016

DO YOU PREFER TO SHOP ONLINE

OR OFFLINE**

B&M STORES INTERNET

84%

16%

36%

46%51%

Digital influence in the purchase process went from 36% to 51% in the last two

55%

25%

20%

I’VE BOUGHT

ONLINE

I’VE BOUGHT

AT STORESI’VE BOUGHT IN

BOTH CHANNELS

**Source: survey made on B&M stores in 2014 only with Schutz, 2015 with Schutz and Anacapri, and in 2016 with Schutz, Anacapri, Arezzo and Fiever.*Graph based on Omni channel Survey E-bit/Buscapé (last 6 months)

FASHION SEGMENT (FASHION AND

ACCESSORIES) IS IN THE HIGHER

OMNI POTENTIAL*

OMNI and ValorizzaFocus on the Client: OMNI Integration + Valorizza

57

So

urc

e: A

rezzo

&C

o

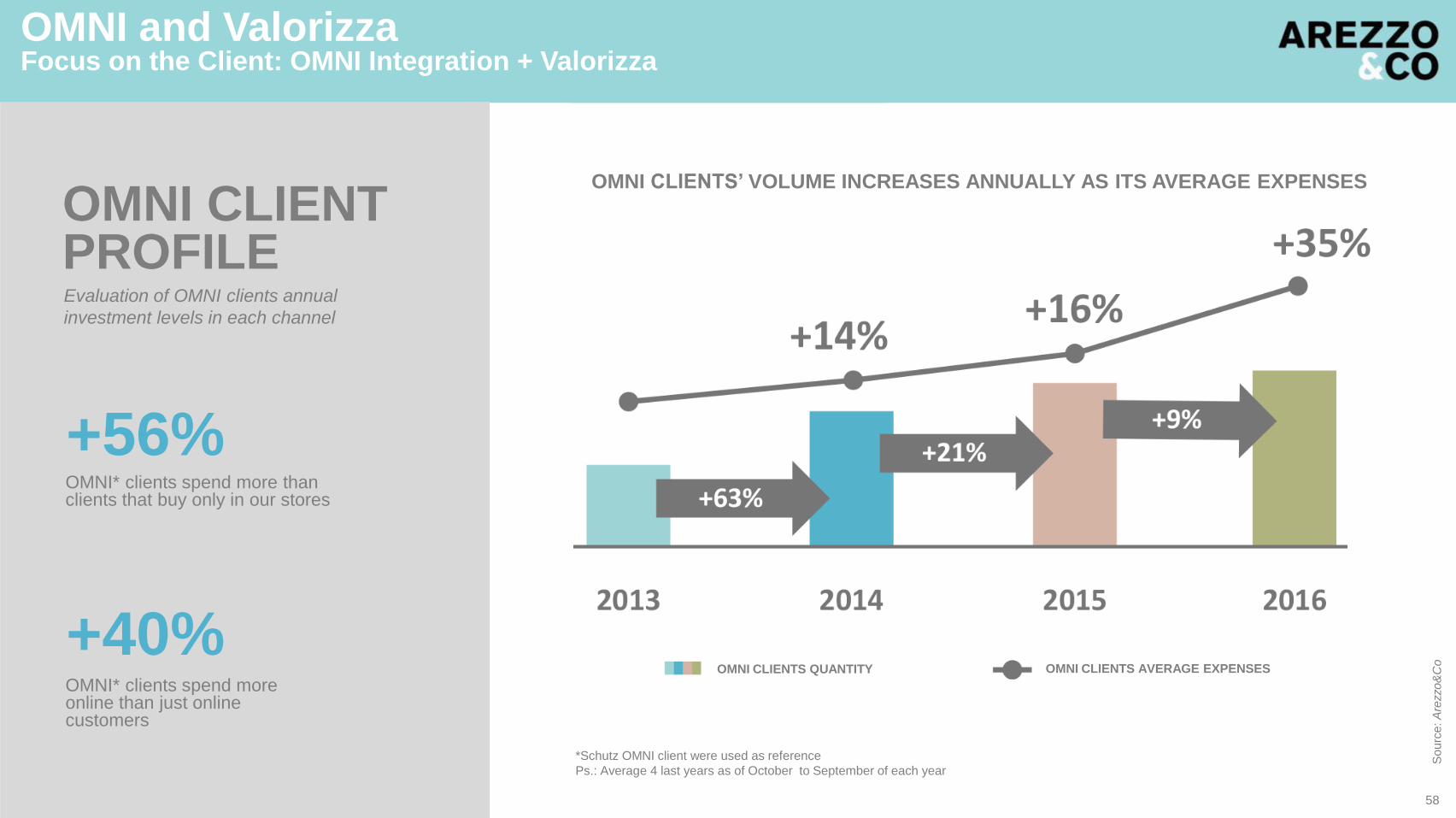

+56%OMNI* clients spend more than clients that buy only in our stores

Evaluation of OMNI clients annual

investment levels in each channel

OMNI CLIENT PROFILE

+40%OMNI* clients spend more online than just online customers

OMNI CLIENTS’ VOLUME INCREASES ANNUALLY AS ITS AVERAGE EXPENSES

*Schutz OMNI client were used as reference

Ps.: Average 4 last years as of October to September of each year

OMNI CLIENTS QUANTITY OMNI CLIENTS AVERAGE EXPENSES

OMNI and ValorizzaFocus on the Client: OMNI Integration + Valorizza

58

STORE SHIPPING

TRIAL (WITH

FRANCHISEES)

2017+

MOBILE EXPERIENCE

DEVELOPMENT

COMPLETE

CLIENT

JOURNEY

SCHUTZ USA

2016TO CAPTURE AREZZO

BRAND POTENTIAL

HIGHER OPERATIONAL

EFFICIENCY

NEW DC

WEB

SCHUTZ FIS

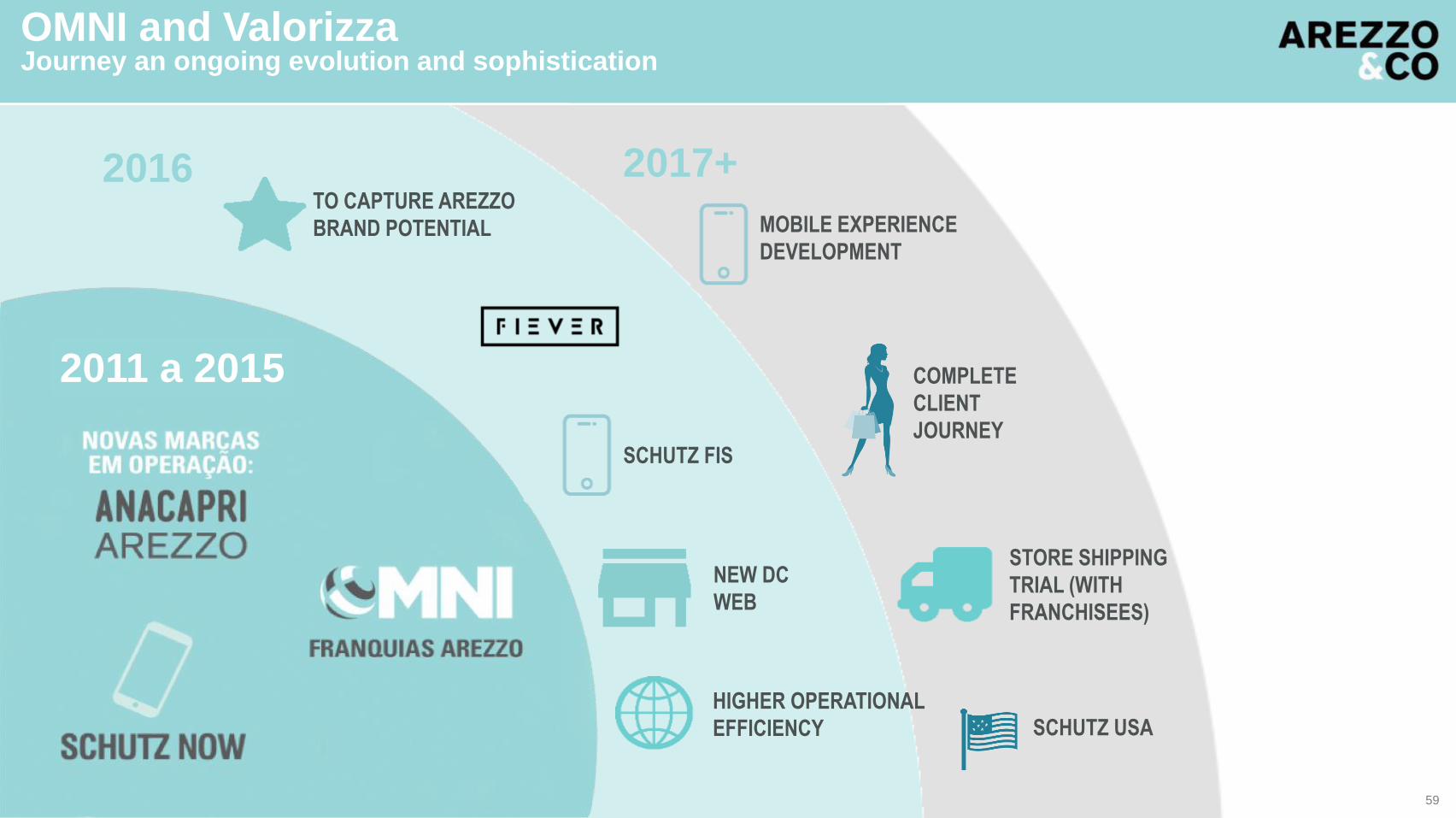

OMNI and ValorizzaJourney an ongoing evolution and sophistication

2011 a 2015

59

Strong structuring of digital operation, leading us to achieve 7% of gross revenues in a 5-year period1

Operational efficiency and synergies is OMNI’s key focus as new Web distribution center positively impacted channel margins2

Maturation of the structure and management of online brands represented by SCHUTZ FIS digital repositioning and faster FIEVER deploy3

Ability to operate new brands and huge opportunity in the internationalization of SCHUTZ brand process5

OMNI and Valorizza integration as a fundamental pillar to capture the potential of the increased digital influence in the purchases process4

Being OMNI means to be present in a consistent way across all relevant contact points, promoting a unique experience (unforgettable and integrated)

60

OMNI and ValorizzaKey messages

Arezzo&Co Investor DayFinance

Thiago Lima BorgesCFO and IRO

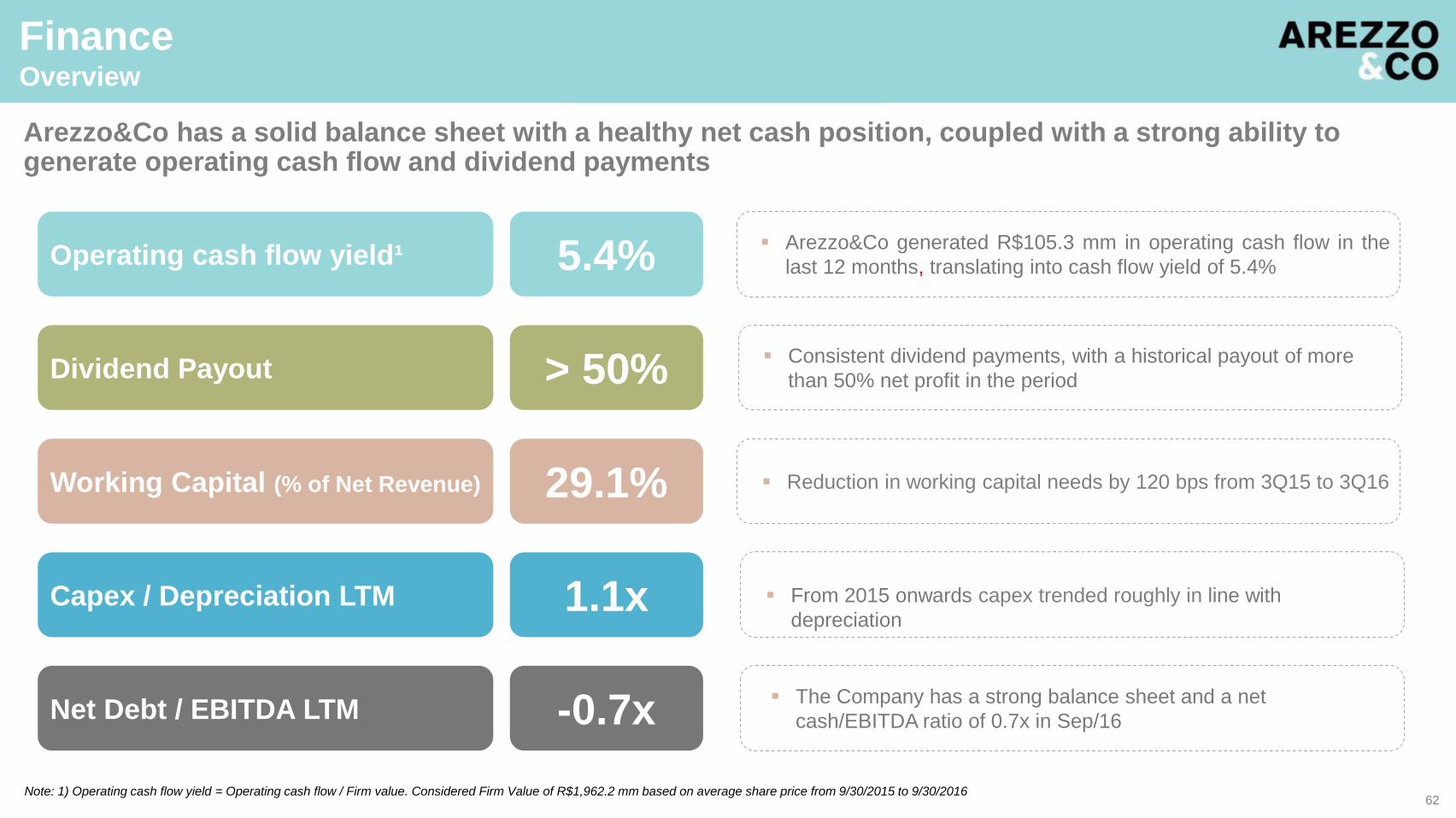

FinanceOverview

Operating cash flow yield¹ 5.4%

Capex / Depreciation LTM 1.1x

The Company has a strong balance sheet and a net

cash/EBITDA ratio of 0.7x in Sep/16

Note: 1) Operating cash flow yield = Operating cash flow / Firm value. Considered Firm Value of R$1,962.2 mm based on average share price from 9/30/2015 to 9/30/2016

Net Debt / EBITDA LTM -0.7x

Arezzo&Co generated R$105.3 mm in operating cash flow in the

last 12 months, translating into cash flow yield of 5.4%

Working Capital (% of Net Revenue) 29.1% Reduction in working capital needs by 120 bps from 3Q15 to 3Q16

Dividend Payout > 50% Consistent dividend payments, with a historical payout of more

than 50% net profit in the period

From 2015 onwards capex trended roughly in line with

depreciation

Arezzo&Co has a solid balance sheet with a healthy net cash position, coupled with a strong ability to generate operating cash flow and dividend payments

62

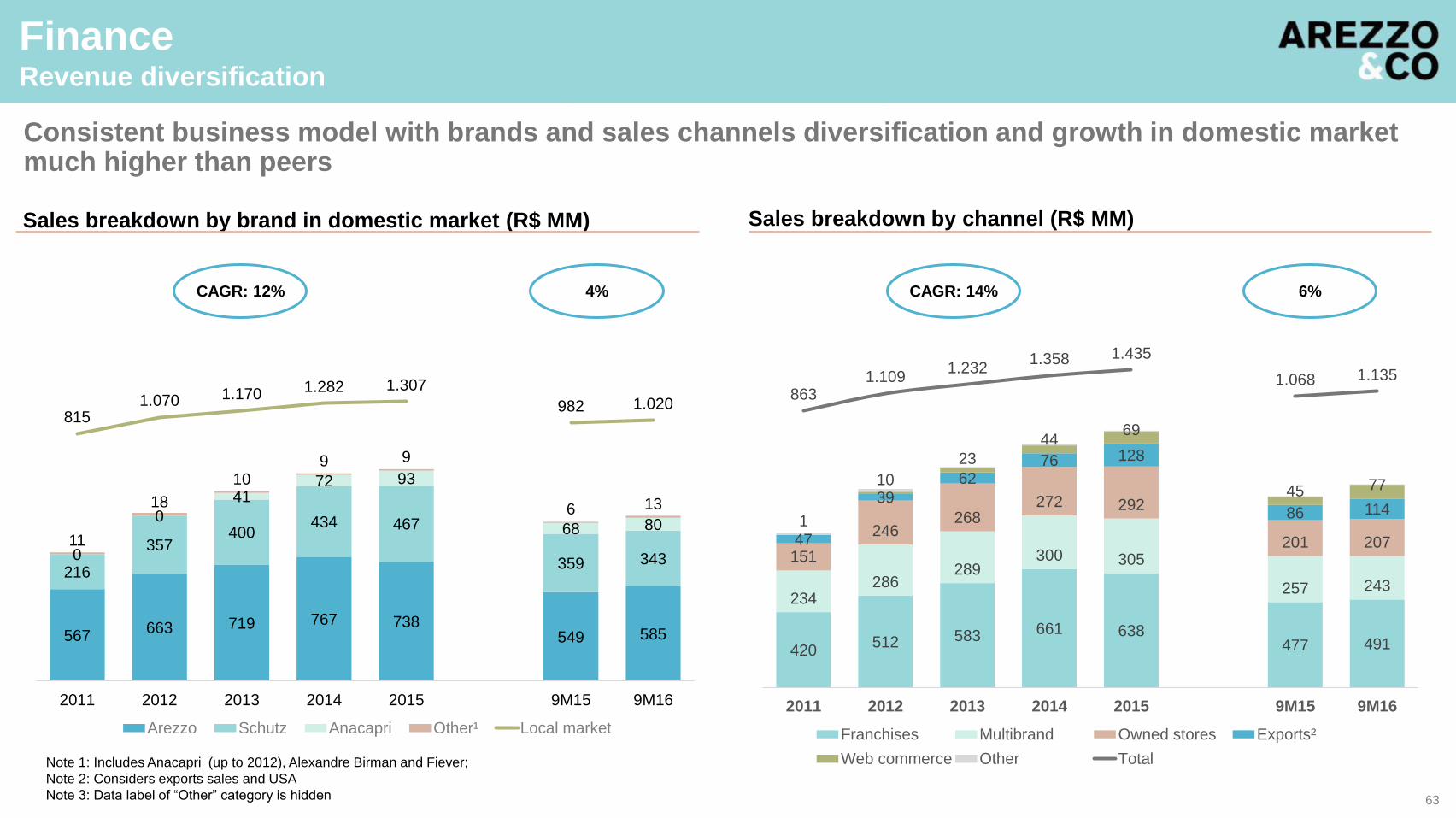

567663 719 767 738

549 585

216

357400

434 467

359 3430

0

4172 93

68 8011

18

109 9

6 13

8151.070 1.170 1.282 1.307

982 1.020

2011 2012 2013 2014 2015 9M15 9M16

Arezzo Schutz Anacapri Other¹ Local market

Sales breakdown by brand in domestic market (R$ MM)

420512 583 661 638

477 491

234286

289300 305

257 243

151

246268

272 292

201 20747

39

6276 128

86 1141

10

23

4469

45 77

8631.109

1.2321.358 1.435

1.068 1.135

(3000,00)

(2500,00)

(2000,00)

(1500,00)

(1000,00)

(500,00)

–

500,00

1000,00

1500,00

2000,00

–

200,00

400,00

600,00

800,00

1000,00

1200,00

1400,00

1600,00

1800,00

2000,00

2011 2012 2013 2014 2015 9M15 9M16

Franchises Multibrand Owned stores Exports²

Web commerce Other TotalNote 1: Includes Anacapri (up to 2012), Alexandre Birman and Fiever;

Note 2: Considers exports sales and USA

Note 3: Data label of “Other” category is hidden

FinanceRevenue diversification

Sales breakdown by channel (R$ MM)

CAGR: 12% 4% CAGR: 14% 6%

Consistent business model with brands and sales channels diversification and growth in domestic market much higher than peers

63

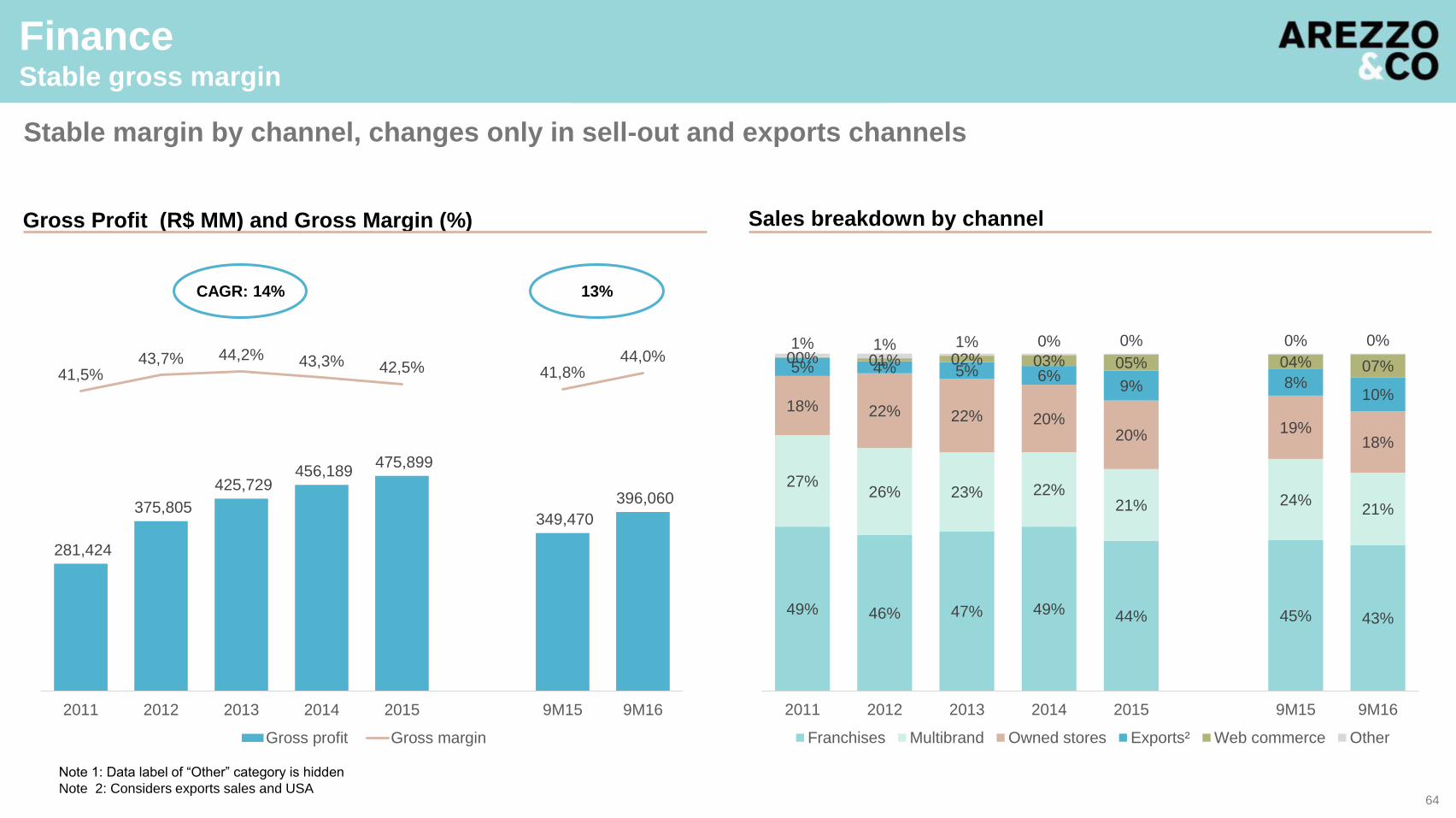

49% 46% 47% 49% 44% 45% 43%

27%26% 23% 22%

21% 24%21%

18% 22% 22% 20%20% 19%

18%

5%4%

5% 6%9% 8%

10%

1% 2% 3% 5% 4% 7%

1% 1% 1%

00%

20%

40%

60%

80%

100%

120%

2011 2012 2013 2014 2015 9M15 9M16

Franchises Multibrand Owned stores Exports² Web commerce Other

49% 46% 47% 49% 44% 45% 43%

27%26% 23% 22%

21% 24%21%

18% 22% 22% 20%20% 19%

18%

5% 4% 5% 6%9% 8%

10%

00% 01% 02% 03% 05% 04% 07%

1% 1% 1% 0% 0% 0% 0%

00%

20%

40%

60%

80%

100%

120%

2011 2012 2013 2014 2015 9M15 9M16

Franchises Multibrand Owned stores Exports² Web commerce Other

281,424

375,805

425,729 456,189

475,899

349,470

396,060

41,5%43,7% 44,2% 43,3% 42,5% 41,8%

44,0%

–

5,00%

10,00%

15,00%

20,00%

25,00%

30,00%

35,00%

40,00%

45,00%

50,00%

–

100,0

200,0

300,0

400,0

500,0

600,0

700,0

800,0

2011 2012 2013 2014 2015 9M15 9M16

Gross profit Gross margin

FinanceStable gross margin

Gross Profit (R$ MM) and Gross Margin (%) Sales breakdown by channel

CAGR: 14% 13%

Note 1: Data label of “Other” category is hidden

Note 2: Considers exports sales and USA

Stable margin by channel, changes only in sell-out and exports channels

64

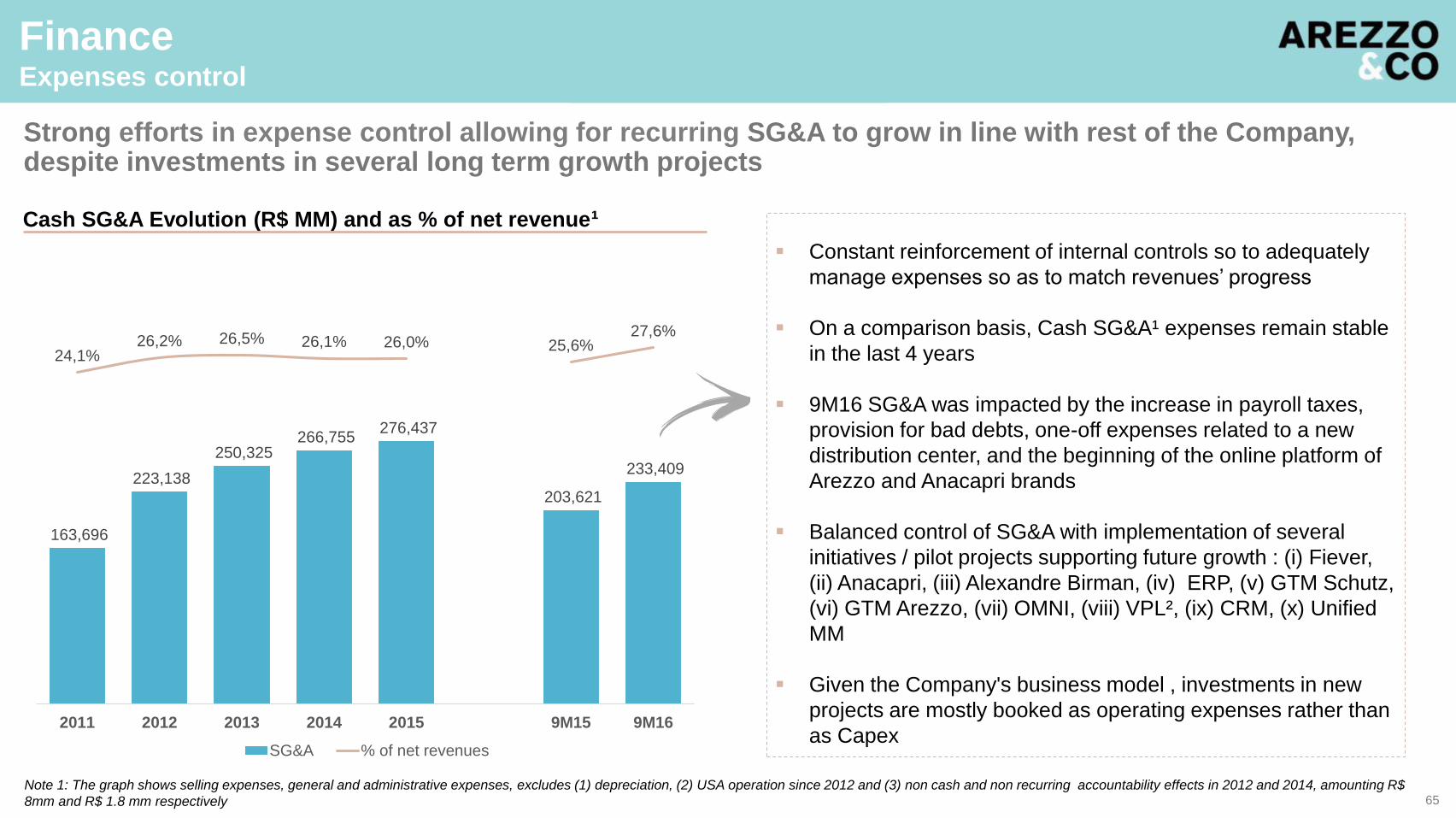

163,696

223,138

250,325 266,755

276,437

203,621

233,409

24,1%26,2% 26,5% 26,1% 26,0% 25,6%

27,6%

-23%

-13%

-03%

08%

18%

28%

38%

-

50,0

100,0

150,0

200,0

250,0

300,0

350,0

400,0

450,0

2011 2012 2013 2014 2015 9M15 9M16

SG&A % of net revenues

Constant reinforcement of internal controls so to adequately

manage expenses so as to match revenues’ progress

On a comparison basis, Cash SG&A¹ expenses remain stable

in the last 4 years

9M16 SG&A was impacted by the increase in payroll taxes,

provision for bad debts, one-off expenses related to a new

distribution center, and the beginning of the online platform of

Arezzo and Anacapri brands

Balanced control of SG&A with implementation of several

initiatives / pilot projects supporting future growth : (i) Fiever,

(ii) Anacapri, (iii) Alexandre Birman, (iv) ERP, (v) GTM Schutz,

(vi) GTM Arezzo, (vii) OMNI, (viii) VPL², (ix) CRM, (x) Unified

MM

Given the Company's business model , investments in new

projects are mostly booked as operating expenses rather than

as Capex

FinanceExpenses control

Cash SG&A Evolution (R$ MM) and as % of net revenue¹

Note 1: The graph shows selling expenses, general and administrative expenses, excludes (1) depreciation, (2) USA operation since 2012 and (3) non cash and non recurring accountability effects in 2012 and 2014, amounting R$

8mm and R$ 1.8 mm respectively

Strong efforts in expense control allowing for recurring SG&A to grow in line with rest of the Company, despite investments in several long term growth projects

65

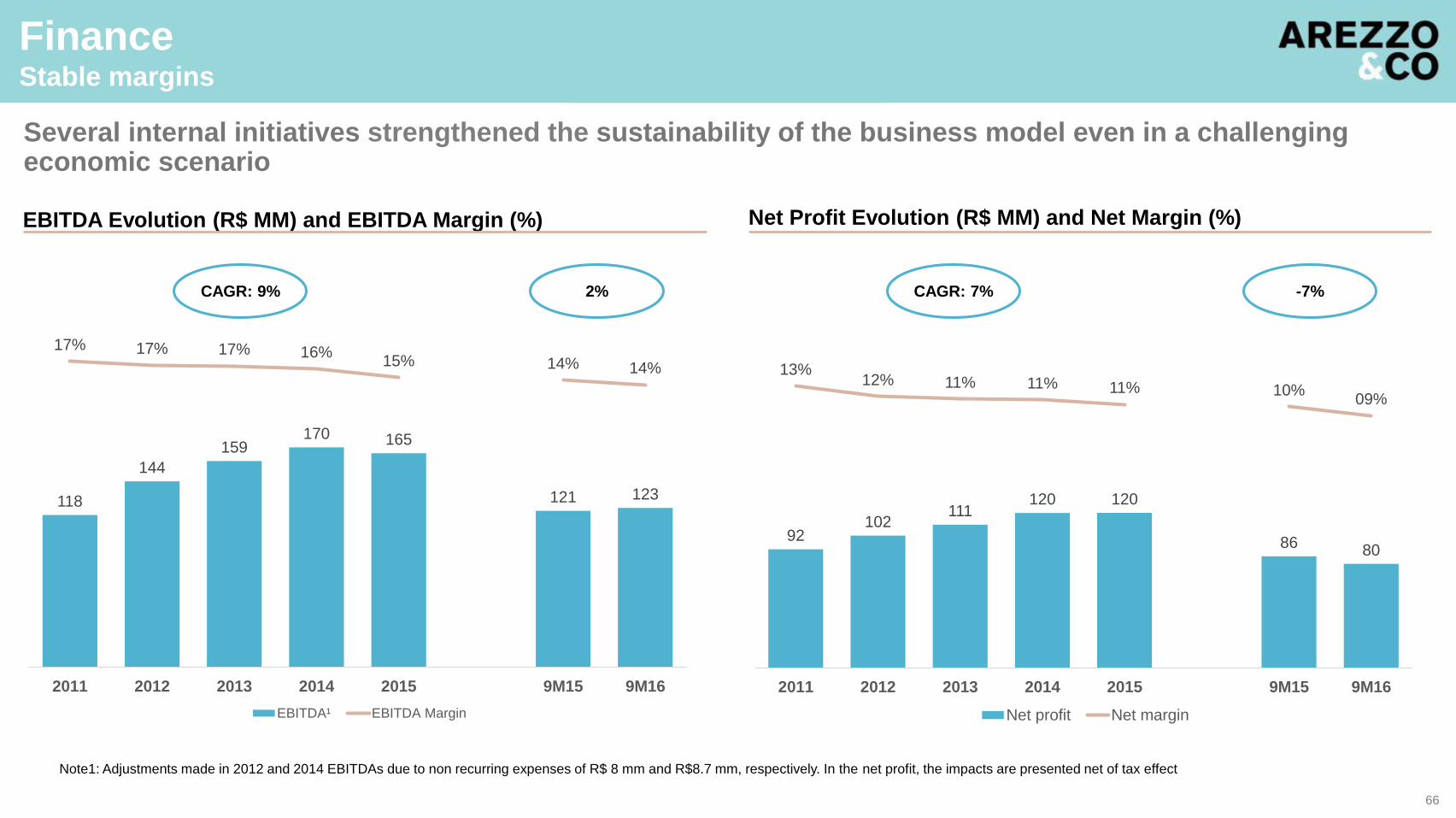

92102

111120 120

8680

13%12% 11% 11% 11% 10%

09%

-30%

-25%

-20%

-15%

-10%

-05%

00%

05%

10%

15%

20%

-

50,00

100,00

150,00

200,00

250,00

2011 2012 2013 2014 2015 9M15 9M16

Net profit Net margin

118

144

159170 165

121 123

17% 17% 17% 16%15% 14% 14%

-30%

-25%

-20%

-15%

-10%

-05%

00%

05%

10%

15%

20%

-

50,00

100,00

150,00

200,00

250,00

2011 2012 2013 2014 2015 9M15 9M16

EBITDA¹ EBITDA Margin

EBITDA Evolution (R$ MM) and EBITDA Margin (%) Net Profit Evolution (R$ MM) and Net Margin (%)

Note1: Adjustments made in 2012 and 2014 EBITDAs due to non recurring expenses of R$ 8 mm and R$8.7 mm, respectively. In the net profit, the impacts are presented net of tax effect

FinanceStable margins

CAGR: 9% 2% CAGR: 7% -7%

Several internal initiatives strengthened the sustainability of the business model even in a challenging economic scenario

66

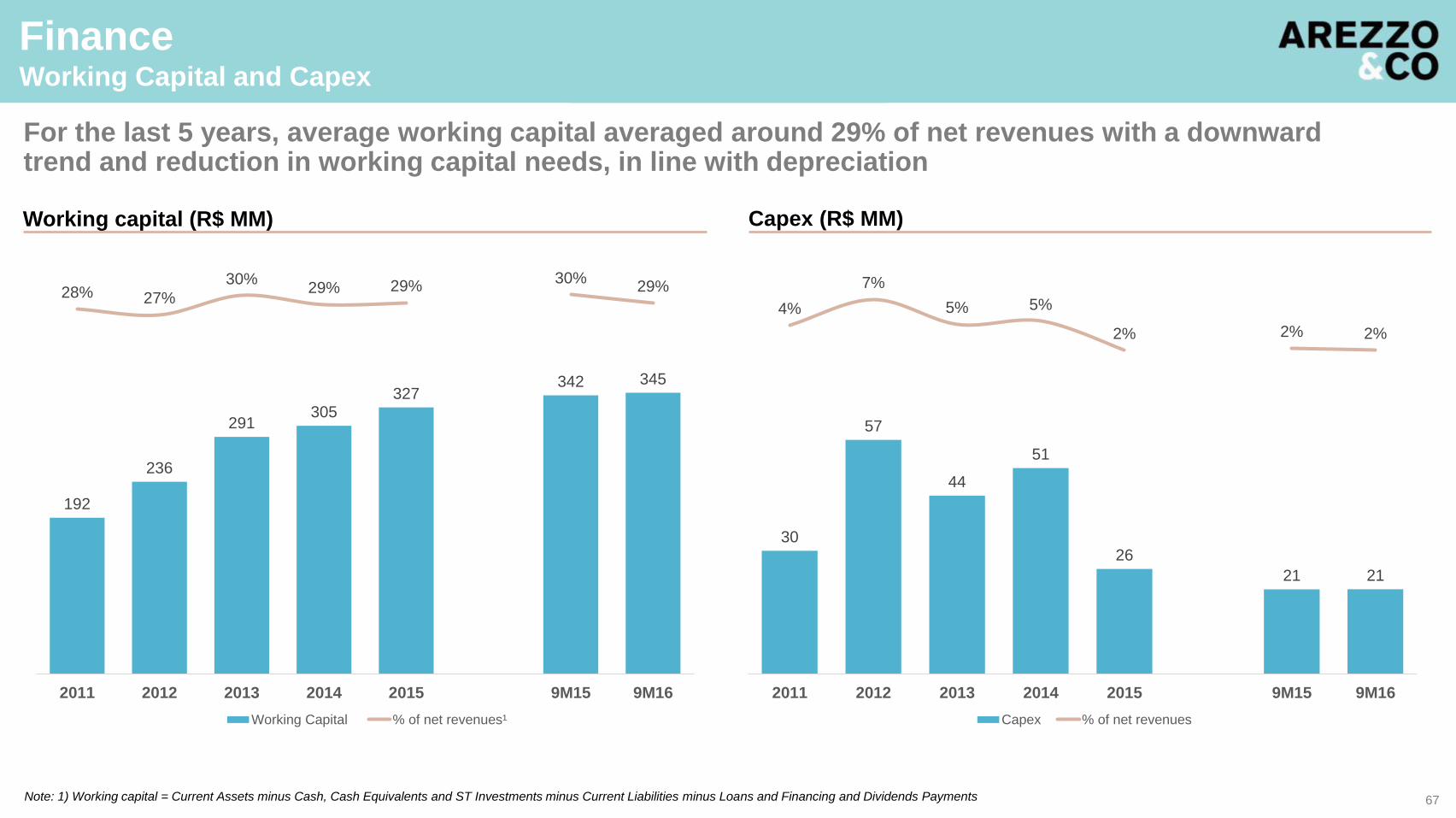

Note: 1) Working capital = Current Assets minus Cash, Cash Equivalents and ST Investments minus Current Liabilities minus Loans and Financing and Dividends Payments

Working capital (R$ MM) Capex (R$ MM)

192

236

291305

327342 345

28% 27%

30%29% 29%

30%29%

-26%

-16%

-06%

05%

15%

25%

35%

-

50,00

100,00

150,00

200,00

250,00

300,00

350,00

400,00

450,00

500,00

2011 2012 2013 2014 2015 9M15 9M16

Working Capital % of net revenues¹

30

57

44

51

26

21 21

4%

7%

5% 5%

2% 2% 2%

-26%

-21%

-16%

-11%

-06%

-01%

05%

10%

-

10,00

20,00

30,00

40,00

50,00

60,00

70,00

80,00

90,00

100,00

2011 2012 2013 2014 2015 9M15 9M16

Capex % of net revenues

FinanceWorking Capital and Capex

For the last 5 years, average working capital averaged around 29% of net revenues with a downward trend and reduction in working capital needs, in line with depreciation

67

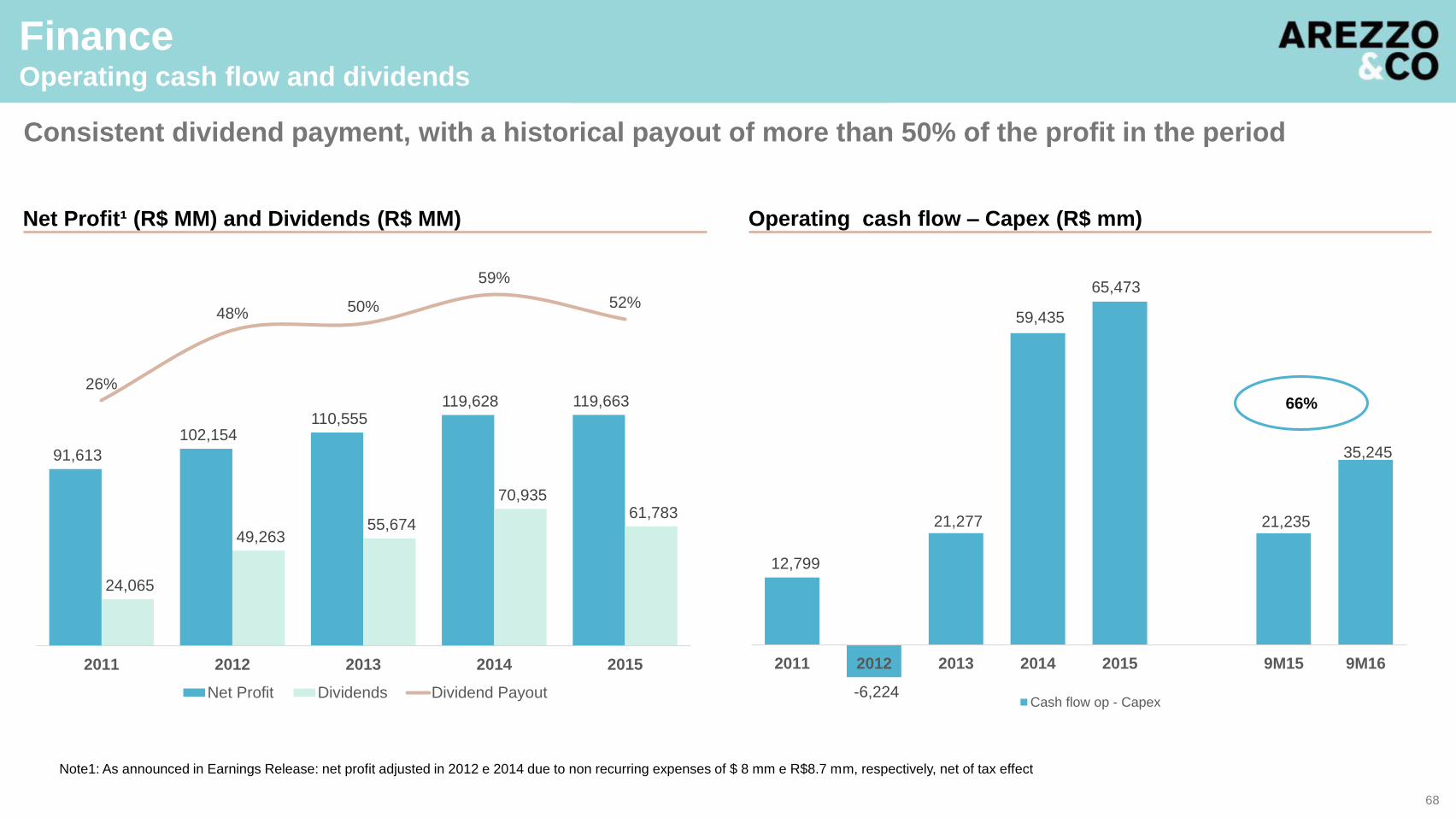

91,613

102,154 110,555

119,628 119,663

24,065

49,263 55,674

70,935 61,783

26%

48% 50%

59%

52%

-50%

-30%

-10%

10%

30%

50%

70%

-

20,0

40,0

60,0

80,0

100,0

120,0

140,0

160,0

180,0

200,0

2011 2012 2013 2014 2015

Net Profit Dividends Dividend Payout

Net Profit¹ (R$ MM) and Dividends (R$ MM) Operating cash flow – Capex (R$ mm)

12,799

-6,224

21,277

59,435

65,473

21,235

35,245

-10,0

-

10,0

20,0

30,0

40,0

50,0

60,0

70,0

2011 2012 2013 2014 2015 9M15 9M16

Cash flow op - Capex

FinanceOperating cash flow and dividends

66%

Consistent dividend payment, with a historical payout of more than 50% of the profit in the period

Note1: As announced in Earnings Release: net profit adjusted in 2012 e 2014 due to non recurring expenses of $ 8 mm e R$8.7 mm, respectively, net of tax effect

68

FinanceKey messages

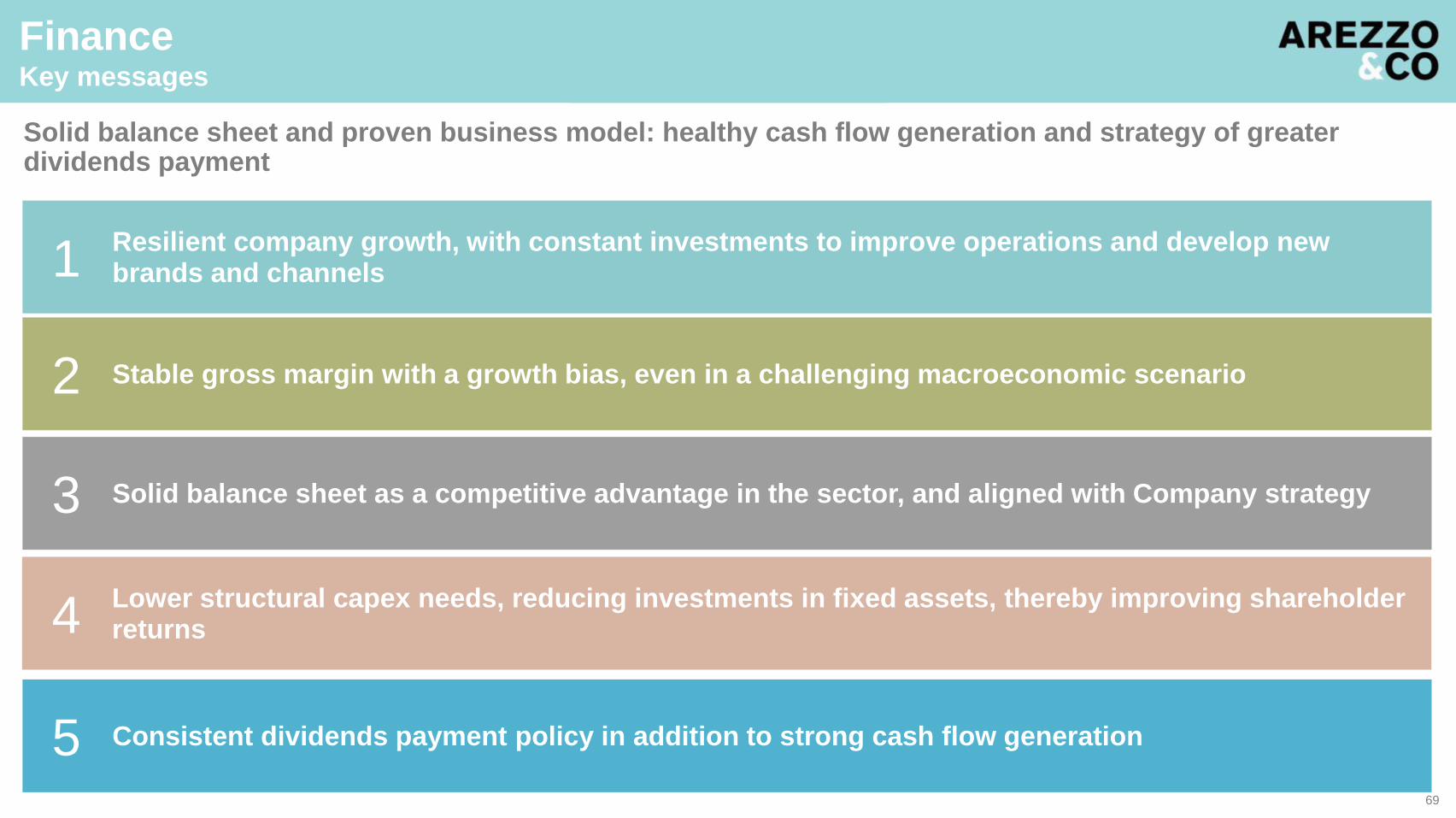

Resilient company growth, with constant investments to improve operations and develop new brands and channels1

Stable gross margin with a growth bias, even in a challenging macroeconomic scenario2

Solid balance sheet as a competitive advantage in the sector, and aligned with Company strategy3

Consistent dividends payment policy in addition to strong cash flow generation5

Lower structural capex needs, reducing investments in fixed assets, thereby improving shareholder returns4

Solid balance sheet and proven business model: healthy cash flow generation and strategy of greater dividends payment

69

Arezzo&Co Investor DayCorporate Governance

José Guimarães Monforte

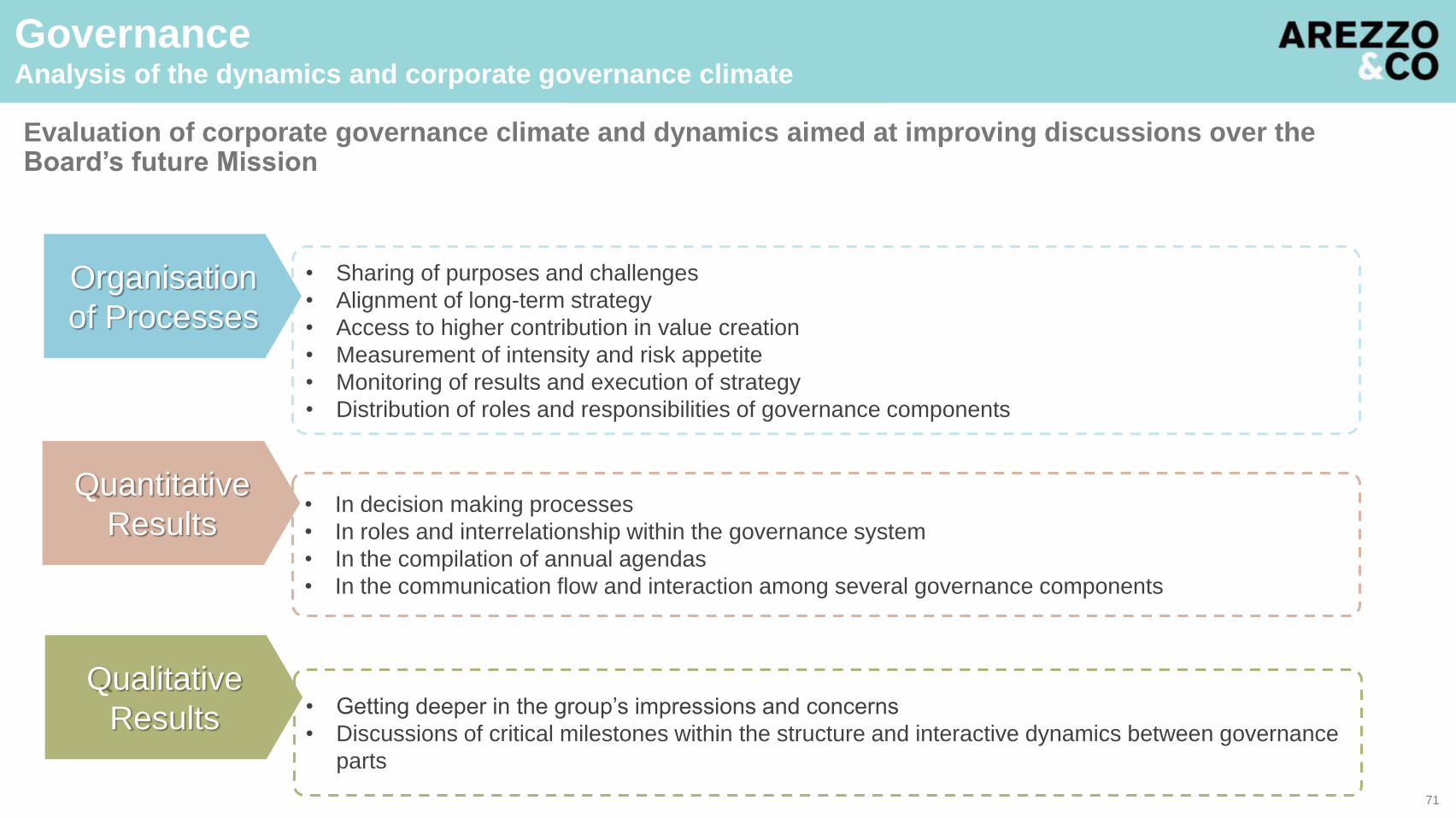

• Sharing of purposes and challenges

• Alignment of long-term strategy

• Access to higher contribution in value creation

• Measurement of intensity and risk appetite

• Monitoring of results and execution of strategy

• Distribution of roles and responsibilities of governance components

Organisation

of Processes

• In decision making processes

• In roles and interrelationship within the governance system

• In the compilation of annual agendas

• In the communication flow and interaction among several governance components

• Getting deeper in the group’s impressions and concerns

• Discussions of critical milestones within the structure and interactive dynamics between governance

parts

Quantitative

Results

Qualitative

Results

GovernanceAnalysis of the dynamics and corporate governance climate

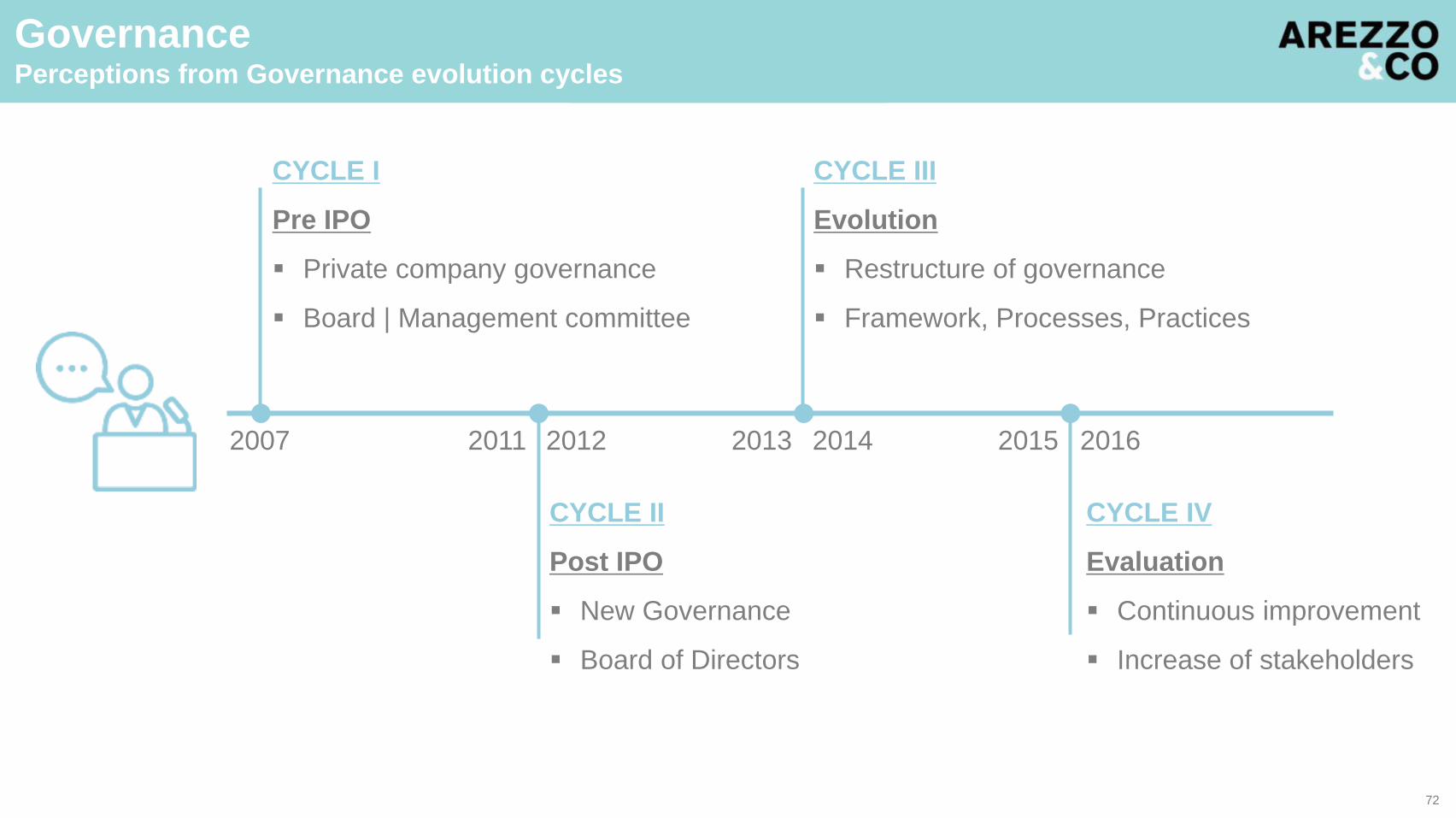

Evaluation of corporate governance climate and dynamics aimed at improving discussions over the Board’s future Mission

71

CYCLE II

Post IPO

New Governance

Board of Directors

CYCLE III

Evolution

Restructure of governance

Framework, Processes, Practices

CYCLE IV

Evaluation

Continuous improvement

Increase of stakeholders

CYCLE I

Pre IPO

Private company governance

Board | Management committee

2007 2011 2012 2013 2014 2015 2016

GovernancePerceptions from Governance evolution cycles

72

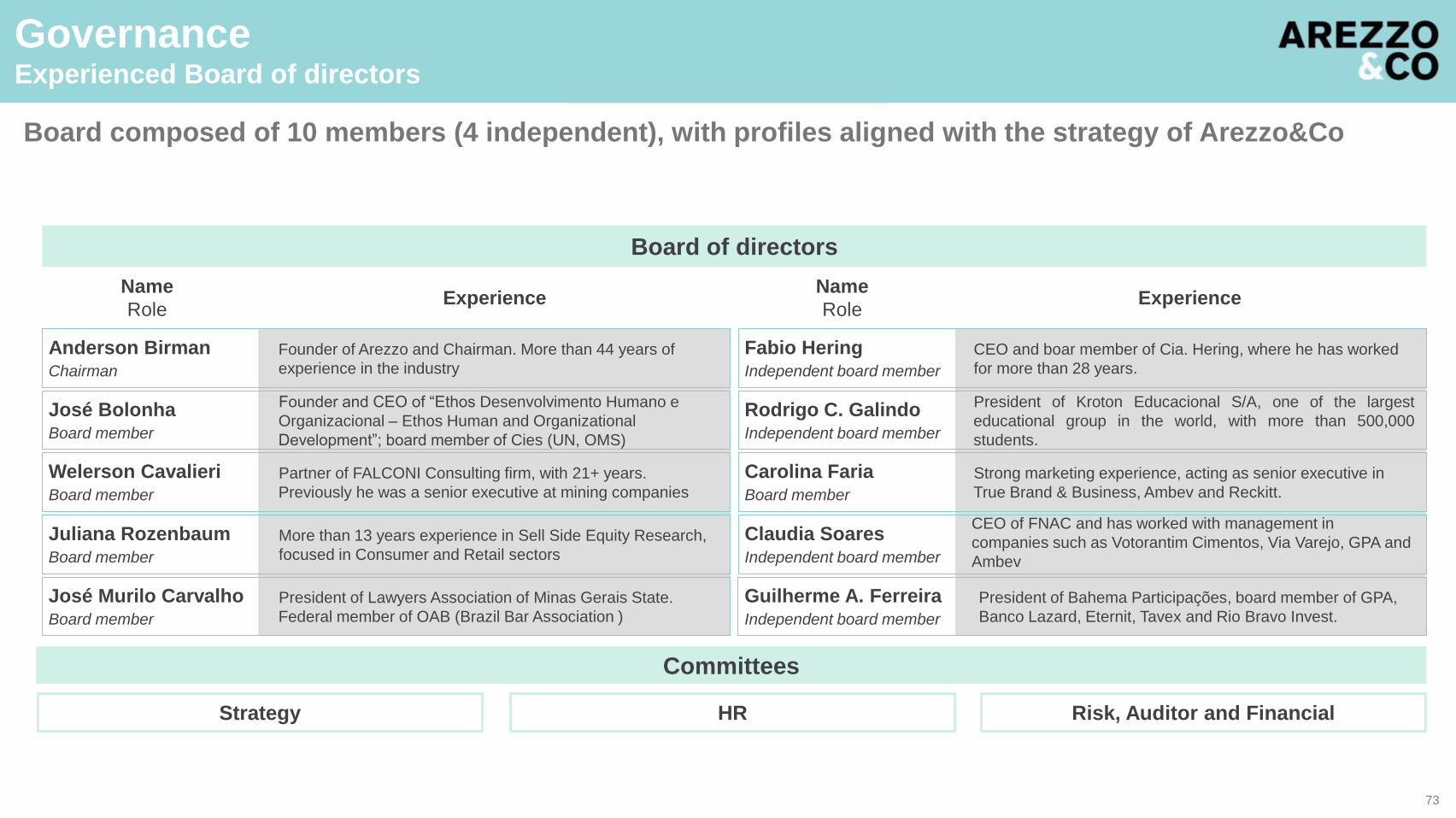

Risk, Auditor and Financial

Committees

Strategy HR

Experience

Board of directors

Anderson BirmanChairman

Founder of Arezzo and Chairman. More than 44 years of

experience in the industry

Fabio HeringIndependent board member

CEO and boar member of Cia. Hering, where he has worked

for more than 28 years.

Carolina FariaBoard member

Strong marketing experience, acting as senior executive in

True Brand & Business, Ambev and Reckitt.

Welerson CavalieriBoard member

Partner of FALCONI Consulting firm, with 21+ years.

Previously he was a senior executive at mining companies

Juliana RozenbaumBoard member

More than 13 years experience in Sell Side Equity Research,

focused in Consumer and Retail sectors

Claudia SoaresIndependent board member

CEO of FNAC and has worked with management in

companies such as Votorantim Cimentos, Via Varejo, GPA and

Ambev

José Murilo CarvalhoBoard member

President of Lawyers Association of Minas Gerais State.

Federal member of OAB (Brazil Bar Association )

Guilherme A. FerreiraIndependent board member

President of Bahema Participações, board member of GPA,

Banco Lazard, Eternit, Tavex and Rio Bravo Invest.

Rodrigo C. GalindoIndependent board member

President of Kroton Educacional S/A, one of the largest

educational group in the world, with more than 500,000

students.

José BolonhaBoard member

Founder and CEO of “Ethos Desenvolvimento Humano e

Organizacional – Ethos Human and Organizational

Development”; board member of Cies (UN, OMS)

Name

RoleExperience

Name

Role

GovernanceExperienced Board of directors

Board composed of 10 members (4 independent), with profiles aligned with the strategy of Arezzo&Co

73

Greater governance practices Higher participations from “players”

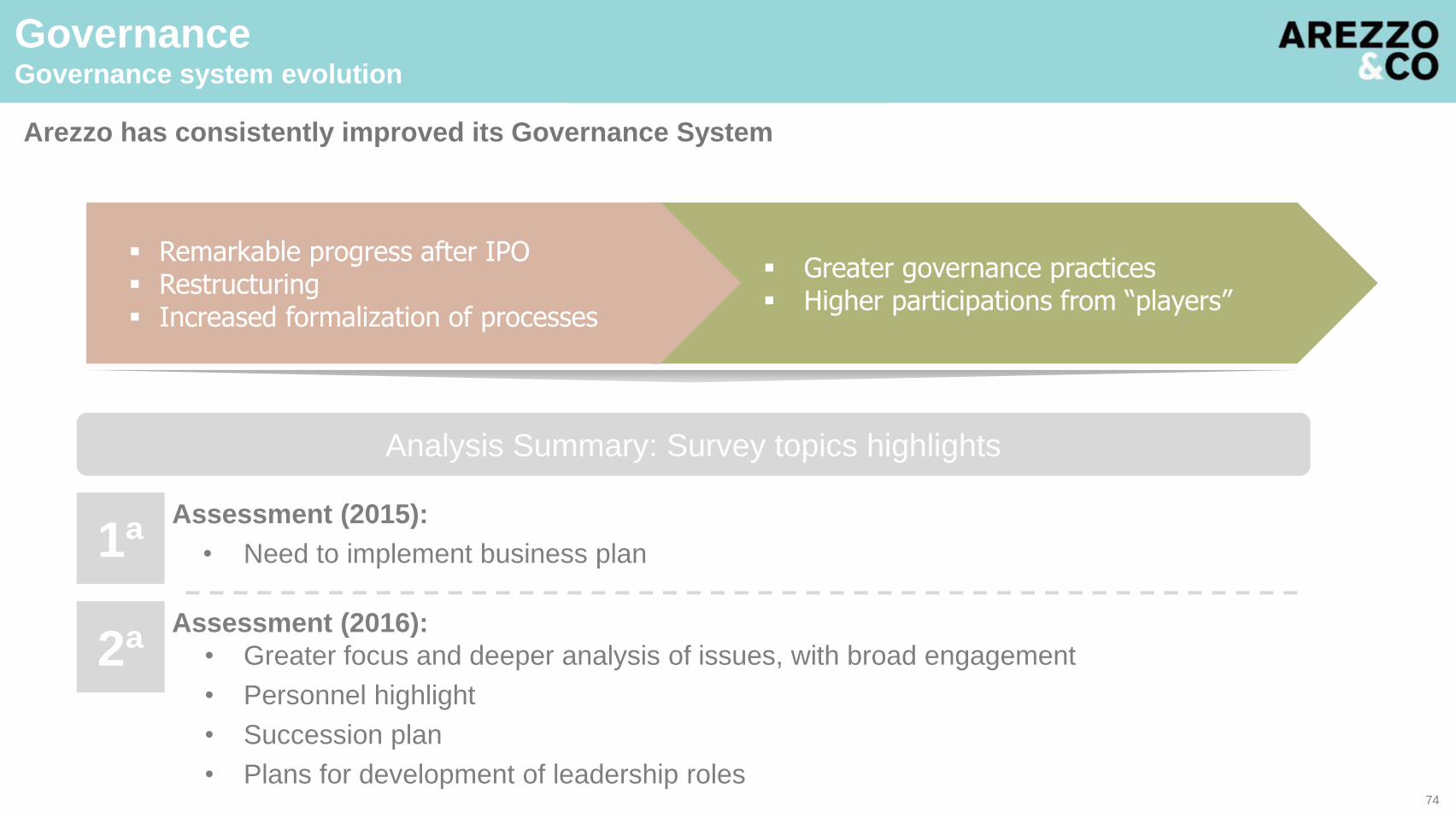

Remarkable progress after IPO Restructuring Increased formalization of processes

Analysis Summary: Survey topics highlights

Assessment (2015):

• Need to implement business plan1ª

Assessment (2016):

• Greater focus and deeper analysis of issues, with broad engagement

• Personnel highlight

• Succession plan

• Plans for development of leadership roles

2ª

Arezzo has consistently improved its Governance System

GovernanceGovernance system evolution

74

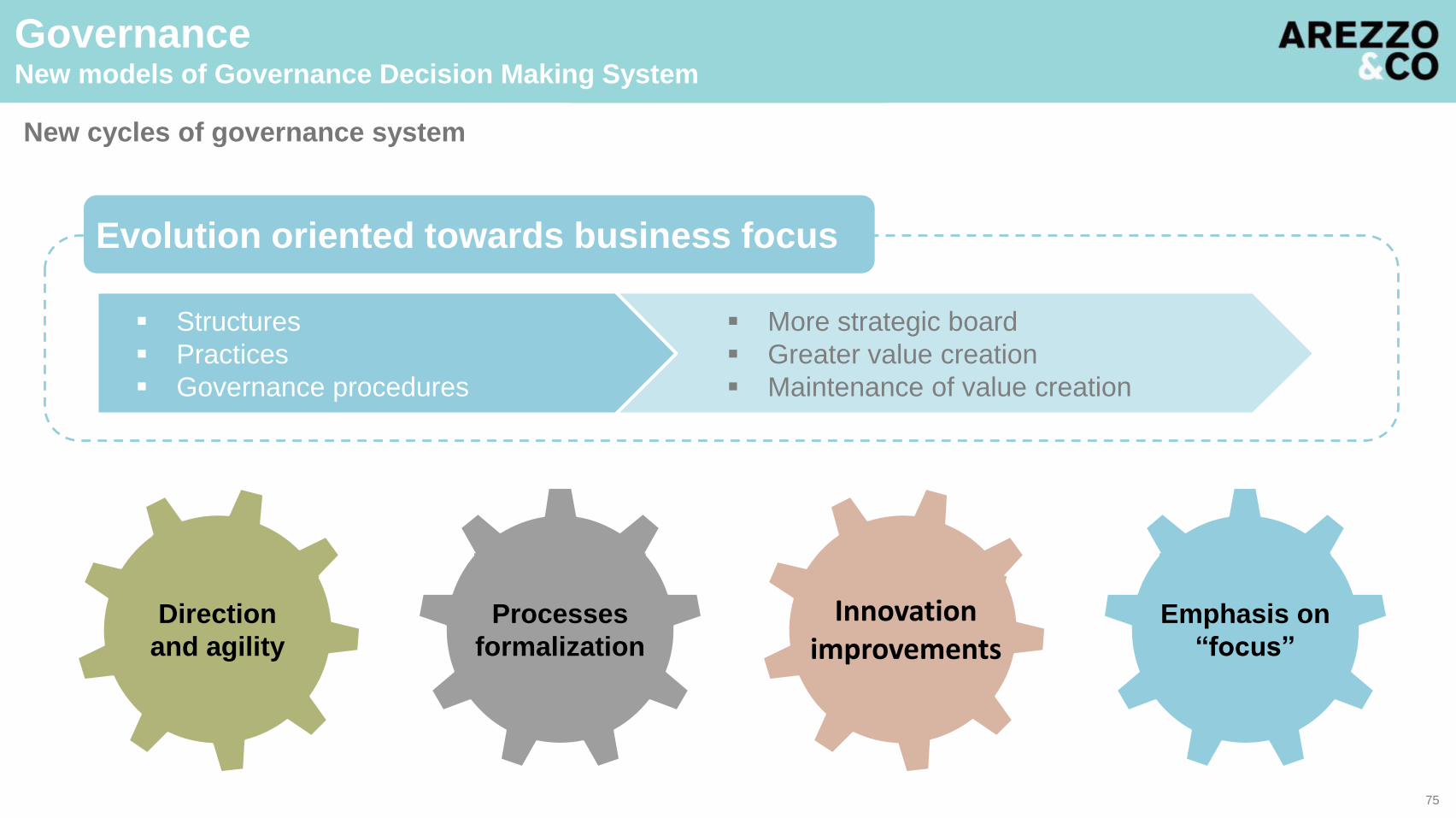

GovernanceNew models of Governance Decision Making System

Direction

and agility

Processes

formalization

Emphasis on

“focus”

Evolution oriented towards business focus

More strategic board

Greater value creation

Maintenance of value creation

Structures

Practices

Governance procedures

New cycles of governance system

Innovation improvements

75

Traditional governance model with basic

engagement, focused in the fiduciary duty,

providing support to CEO’s agenda.

Goes deeper into the understanding of the

business and connects the operating performance to competitive advantages.

The agenda is still the CEO’s agenda.

The working board has only one direction and follows the Company’s

guidelines.

Use the capabilities that were developed and that

combine fiduciary responsibility, operating leadership, contextual intelligence, sistemicthought and strategic

thinking. Its advantage is the combination of three

elements: group’s leadership, expanded

consciousness, fearless engagement.

Has a better understanding of the

company’s reach in a local context, regional, national and international. Expand its vision by using outside

help and foresees interdependency between

the parts. Sees the company in a more ample context. It is limited by its focus in an industry and

segment.

GovernanceNew models in governance decision making process

Consensual

Board

Working

Board

Strategic

Board

Conscious

Board

76

Arezzo&Co Investor Day

AREZZO INDÚSTRIA E COMÉRCIO S.A.

Arezzo&Co Investor Day

Q&AQ&A

AG

EN

DA SCHEDULE ACTIVITIES PRESENTER

14:00 14:05 Instructions and Agenda Paulo Ionescu

14:05 14:20 Opening remarks Alexandre Birman

FIRST PART

14:20 14:35 People Management Marco Vidal

14:35 15:00 Value Chain Cassiano Lemos / Silvia Machado

15:00 15:15 OMNI and Valorizza Mauricio Bastos

15:15 15:30 Finance Thiago Borges

15:30 15:45 Corporate Governance José Monforte

15:45 16:00 Q&A

16:00 16:20 Coffee Break

SECOND PART

16:20 17:15 Talk Show (moderator Alexandre Birman) Silvia Machado (Arezzo)

Fabíola Guimarães (Schutz)

Yumi Chibusa (Anacapri)

Marianna Arzinaut (Fiever)

Milena Ometto (A. Birman)

Fernando Baumer (Multibrands / External Market)

17:15 17:35 Q&A

17:35 17:45 Closing remarks Alexandre Birman

Arezzo&Co Investor DayTalk Show

Arezzo&Co Investor DayClosing remarks

Alexandre BirmanCEO

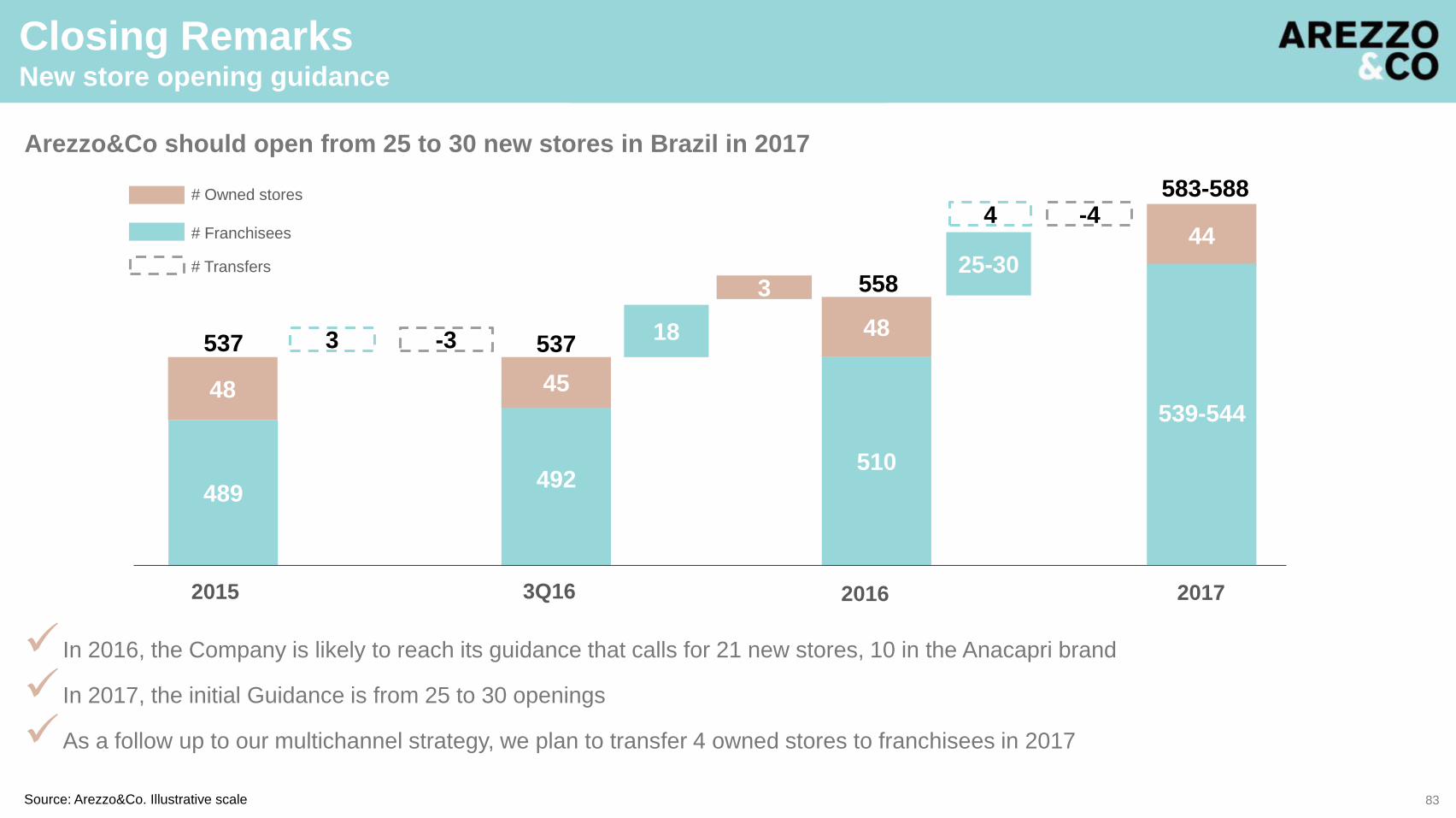

Arezzo&Co should open from 25 to 30 new stores in Brazil in 2017

Closing RemarksNew store opening guidance

5

Source: Arezzo&Co. Illustrative scale

In 2016, the Company is likely to reach its guidance that calls for 21 new stores, 10 in the Anacapri brand

In 2017, the initial Guidance is from 25 to 30 openings

As a follow up to our multichannel strategy, we plan to transfer 4 owned stores to franchisees in 2017

# Owned stores

# Franchisees

492

3Q16 2016

45

537

489

2015

48

53718

510

48

55825-30

2017

44# Transfers

3

3 -3

583-5884 -4

539-544

83

Arezzo&Co keeps developing its business model in a sustainable way

Consolidated business model with multiple growth opportunities• Launch of a new brand Fiever with encouraging results• Improvement in the profitability of existing brands: Anacapri and Alexandre Birman

1

Staff management an ongoing development• Broad range of selection, training and retaining of staff at all levels• Strengthening of organizational identity

2

Ownership of the value chain, greater competitive advantage• More agile and collaborative model• Sell-out oriented to boost results in the value chain

3

Multi-channel management know-how, excellent platform to lift brands• Omni channel growth: Fiever debut, Schutz FIS, Arezzo consolidation, Anacapri expansion• Strong knowledge in franchises’ management in addition to improving opportunities• Multibrand channel leverages growth of new brands

5

Financial strength allows for sustainable business growth• History of cash generation together with consistent dividend payment policy• Net cash position, an important differentiator in challenging economic times

4

84

Closing RemarksKey messages

Arezzo&Co Investor Day

9 de dezembro de 2016