Embed Size (px)

Citation preview

Color

Scheme

234 93 46

109 179 63

235 235 235

0 75 141

253 185 36

Accent

Color

31 179 179

192 0 0

“This presentation contains forward-looking statements. These statements are made under the “safe harbor” provisions established

by the U.S. Private Securities Litigation Reform Act of 1995. Forward-looking statements involve inherent risks and uncertainties.

The forward-looking statements in this presentation reflect the expectations of the Bank’s management and are based on currently

available data; however, actual experience with respect to these factors is subject to future events and uncertainties, which could

materially impact the Bank’s expectations. A number of factors could cause actual performance and results to differ materially from

those contained in any forward-looking statement, including but not limited to the following: the anticipated growth of the Bank’s

credit portfolio, including its trade finance portfolio; the continuation of the Bank’s preferred creditor status; the impact of increasing

interest rates and of the macroeconomic environment in the Region on the Bank’s financial condition; the execution of the Bank’s

strategies and initiatives, including its revenue diversification strategy; the adequacy of the Bank’s allowance for credit losses; the

need for additional provisions for credit losses; the Bank’s ability to achieve future growth, the Bank’s ability to reduce its liquidity

levels and increase its leverage; the Bank’s ability to maintain its investment-grade credit ratings; the availability and mix of future

sources of funding for the Bank’s lending operations; potential trading losses; the possibility of fraud; and the adequacy of the

Bank’s sources of liquidity to replace large deposit withdrawals.”

2

Third Quarter Highlights

3

Core operating trends strengthened in Q3 Business profit up 27% QoQ, EPS up 26%

Total 3Q credit disbursements up 12% to $3.2B

Net interest margin improves to 2.13%

Conservative approach towards credit portfolio with selective growth and strenghtening of

credit provisions

Stable asset quality NPL ratio stable at 1.3% of Loan Portfolio, with reserves coverage at 1.3x

Trade represents 61% of Total Commercial Portfolio

Brazil exposure remains at 18% of Total Commercial Portfolio

Bladex loan syndication and structuring business performing well Three transactions concluded in 3Q, for a total eight deals YTD, despite weak market

Bladex ranked #14 by volume and #6 by number of deals

Outlook improving Brazil and Argentina slated to leave recession in 2017

NIM supported by base rates, mitigating impact of short-term trade oriented origination

Non-core items no longer affecting results

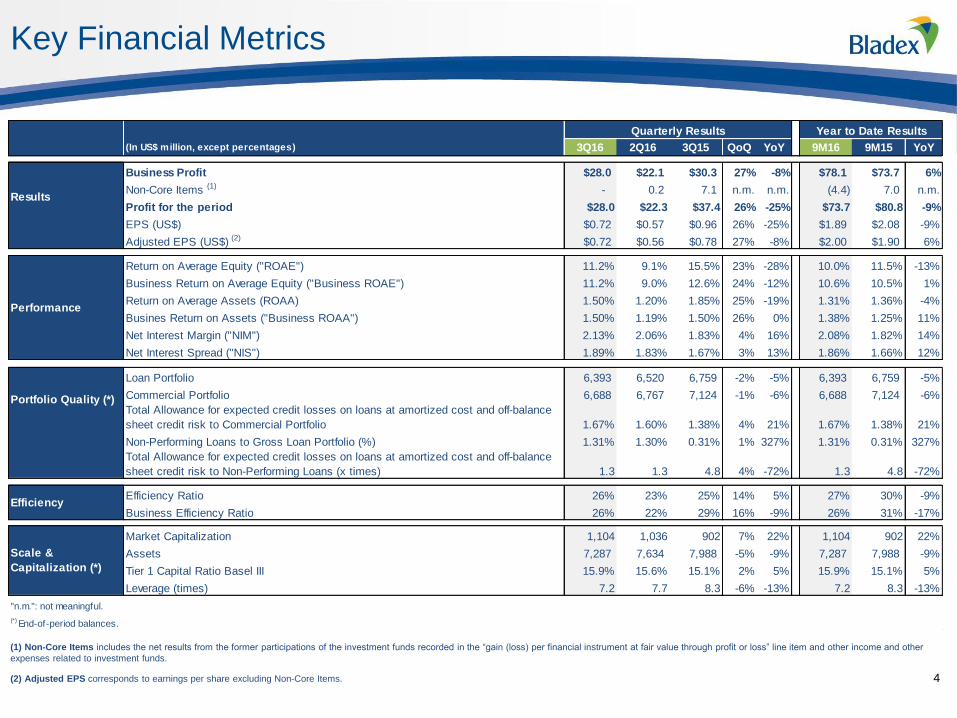

Key Financial Metrics

(1) Non-Core Items includes the net results from the former participations of the investment funds recorded in the “gain (loss) per financial instrument at fair value through profit or loss” line item and other income and other

expenses related to investment funds.

(2) Adjusted EPS corresponds to earnings per share excluding Non-Core Items. 4

Quarterly Results Year to Date Results

(In US$ million, except percentages) 3Q16 2Q16 3Q15 QoQ YoY 9M16 9M15 YoY

Business Profit $28.0 $22.1 $30.3 27% -8% $78.1 $73.7 6%

Non-Core Items (1) - 0.2 7.1 n.m. n.m. (4.4) 7.0 n.m.

Profit for the period $28.0 $22.3 $37.4 26% -25% $73.7 $80.8 -9%

EPS (US$) $0.72 $0.57 $0.96 26% -25% $1.89 $2.08 -9%

Adjusted EPS (US$) (2) $0.72 $0.56 $0.78 27% -8% $2.00 $1.90 6%

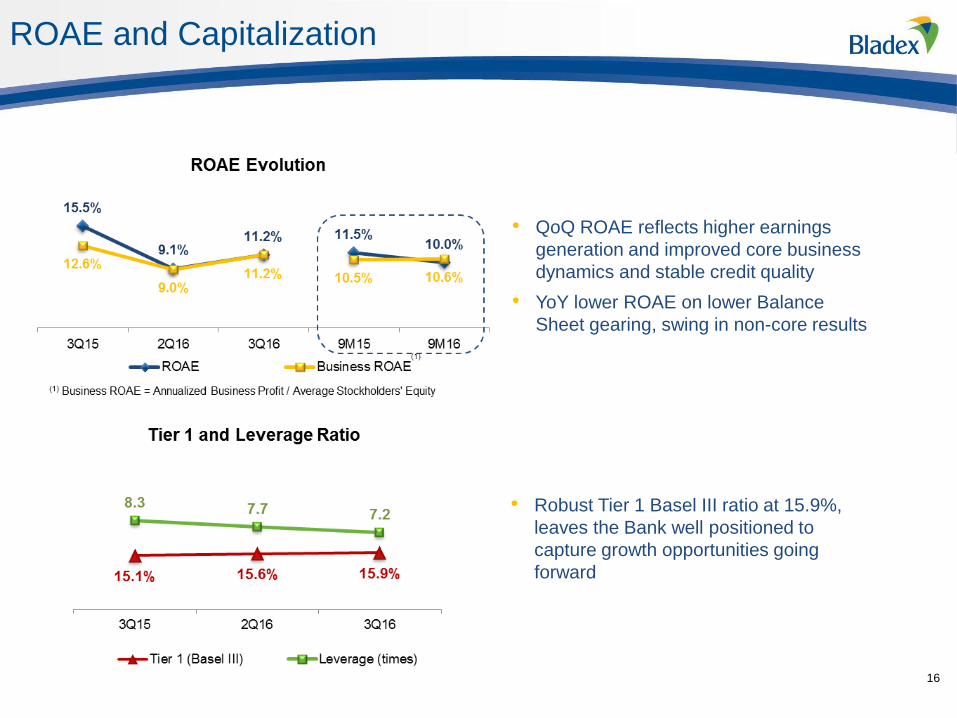

Return on Average Equity ("ROAE") 11.2% 9.1% 15.5% 23% -28% 10.0% 11.5% -13%

Business Return on Average Equity ("Business ROAE") 11.2% 9.0% 12.6% 24% -12% 10.6% 10.5% 1%

Return on Average Assets (ROAA) 1.50% 1.20% 1.85% 25% -19% 1.31% 1.36% -4%

Busines Return on Assets ("Business ROAA") 1.50% 1.19% 1.50% 26% 0% 1.38% 1.25% 11%

Net Interest Margin ("NIM") 2.13% 2.06% 1.83% 4% 16% 2.08% 1.82% 14%

Net Interest Spread ("NIS") 1.89% 1.83% 1.67% 3% 13% 1.86% 1.66% 12%

Loan Portfolio 6,393 6,520 6,759 -2% -5% 6,393 6,759 -5%

Commercial Portfolio 6,688 6,767 7,124 -1% -6% 6,688 7,124 -6%

Total Allowance for expected credit losses on loans at amortized cost and off-balance

sheet credit risk to Commercial Portfolio 1.67% 1.60% 1.38% 4% 21% 1.67% 1.38% 21%

Non-Performing Loans to Gross Loan Portfolio (%) 1.31% 1.30% 0.31% 1% 327% 1.31% 0.31% 327%

Total Allowance for expected credit losses on loans at amortized cost and off-balance

sheet credit risk to Non-Performing Loans (x times) 1.3 1.3 4.8 4% -72% 1.3 4.8 -72%

Efficiency Ratio 26% 23% 25% 14% 5% 27% 30% -9%

Business Efficiency Ratio 26% 22% 29% 16% -9% 26% 31% -17%

Market Capitalization 1,104 1,036 902 7% 22% 1,104 902 22%

Assets 7,287 7,634 7,988 -5% -9% 7,287 7,988 -9%

Tier 1 Capital Ratio Basel III 15.9% 15.6% 15.1% 2% 5% 15.9% 15.1% 5%

Leverage (times) 7.2 7.7 8.3 -6% -13% 7.2 8.3 -13%

"n.m.": not meaningful.

(*) End-of-period balances.

Results

Performance

Portfolio Quality (*)

Efficiency

Scale &

Capitalization (*)

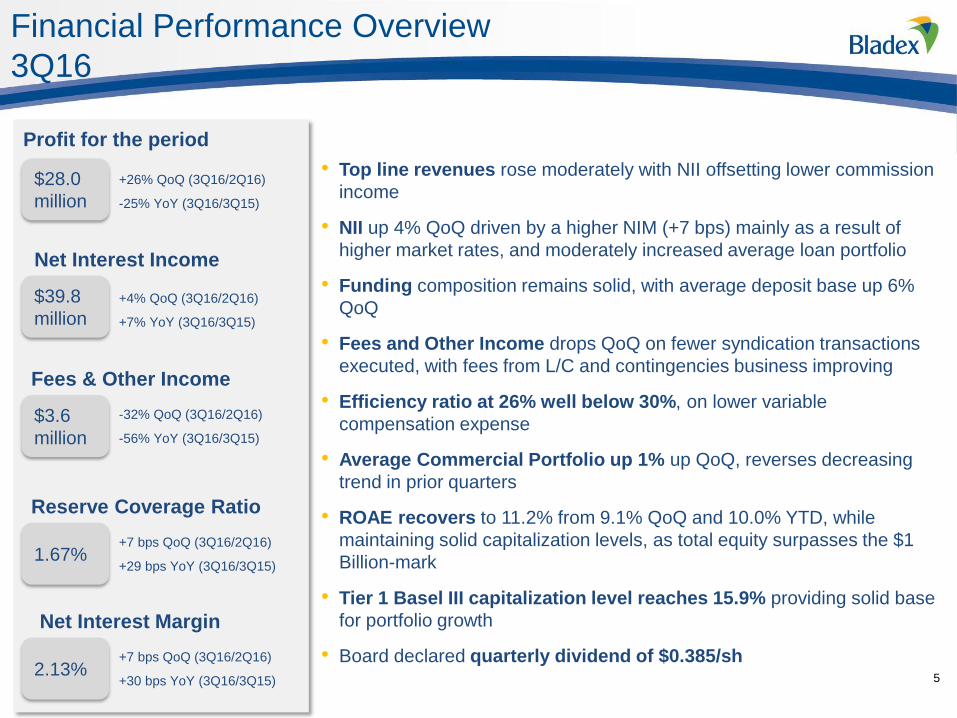

Financial Performance Overview

3Q16

5

• Top line revenues rose moderately with NII offsetting lower commission

income

• NII up 4% QoQ driven by a higher NIM (+7 bps) mainly as a result of

higher market rates, and moderately increased average loan portfolio

• Funding composition remains solid, with average deposit base up 6%

QoQ

• Fees and Other Income drops QoQ on fewer syndication transactions

executed, with fees from L/C and contingencies business improving

• Efficiency ratio at 26% well below 30%, on lower variable

compensation expense

• Average Commercial Portfolio up 1% up QoQ, reverses decreasing

trend in prior quarters

• ROAE recovers to 11.2% from 9.1% QoQ and 10.0% YTD, while

maintaining solid capitalization levels, as total equity surpasses the $1

Billion-mark

• Tier 1 Basel III capitalization level reaches 15.9% providing solid base

for portfolio growth

• Board declared quarterly dividend of $0.385/sh

Profit for the period

$28.0

million

+26% QoQ (3Q16/2Q16)

-25% YoY (3Q16/3Q15)

$39.8

million

Net Interest Income

Fees & Other Income

$3.6

million

Reserve Coverage Ratio

+4% QoQ (3Q16/2Q16)

+7% YoY (3Q16/3Q15)

-32% QoQ (3Q16/2Q16)

-56% YoY (3Q16/3Q15)

1.67% +7 bps QoQ (3Q16/2Q16)

+29 bps YoY (3Q16/3Q15)

Net Interest Margin

2.13% +7 bps QoQ (3Q16/2Q16)

+30 bps YoY (3Q16/3Q15)

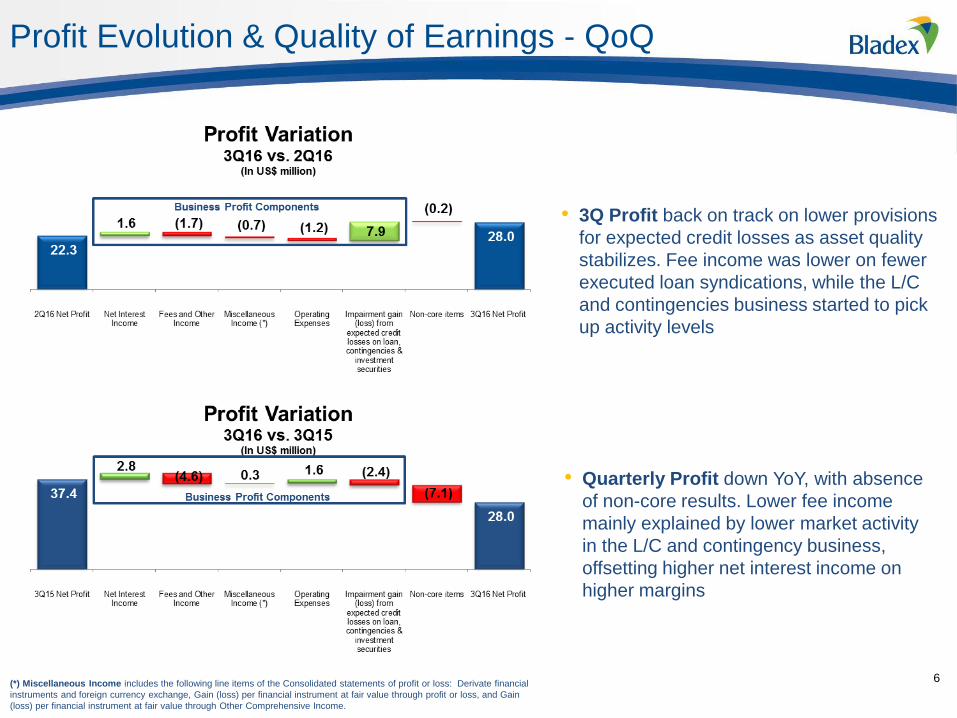

Profit Evolution & Quality of Earnings - QoQ

6 (*) Miscellaneous Income includes the following line items of the Consolidated statements of profit or loss: Derivate financial

instruments and foreign currency exchange, Gain (loss) per financial instrument at fair value through profit or loss, and Gain

(loss) per financial instrument at fair value through Other Comprehensive Income.

• 3Q Profit back on track on lower provisions

for expected credit losses as asset quality

stabilizes. Fee income was lower on fewer

executed loan syndications, while the L/C

and contingencies business started to pick

up activity levels

• Quarterly Profit down YoY, with absence

of non-core results. Lower fee income

mainly explained by lower market activity

in the L/C and contingency business,

offsetting higher net interest income on

higher margins

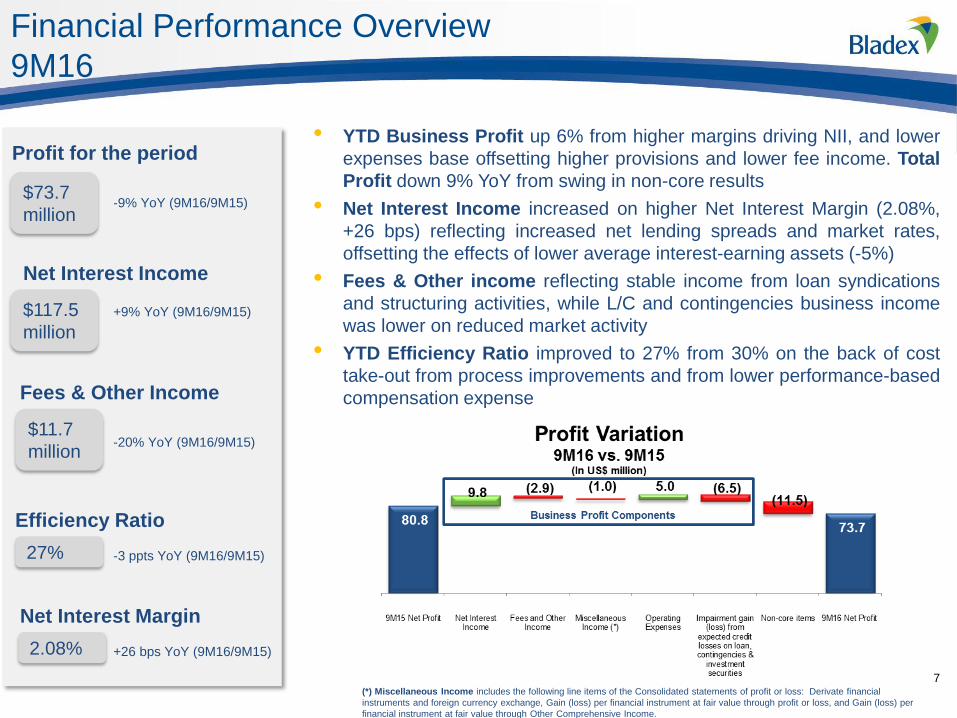

Financial Performance Overview

9M16

7 (*) Miscellaneous Income includes the following line items of the Consolidated statements of profit or loss: Derivate financial

instruments and foreign currency exchange, Gain (loss) per financial instrument at fair value through profit or loss, and Gain (loss) per

financial instrument at fair value through Other Comprehensive Income.

• YTD Business Profit up 6% from higher margins driving NII, and lower

expenses base offsetting higher provisions and lower fee income. Total

Profit down 9% YoY from swing in non-core results

• Net Interest Income increased on higher Net Interest Margin (2.08%,

+26 bps) reflecting increased net lending spreads and market rates,

offsetting the effects of lower average interest-earning assets (-5%)

• Fees & Other income reflecting stable income from loan syndications

and structuring activities, while L/C and contingencies business income

was lower on reduced market activity

• YTD Efficiency Ratio improved to 27% from 30% on the back of cost

take-out from process improvements and from lower performance-based

compensation expense

Profit for the period

$73.7

million -9% YoY (9M16/9M15)

$117.5

million

Net Interest Income

Fees & Other Income

$11.7

million

+9% YoY (9M16/9M15)

-20% YoY (9M16/9M15)

Net Interest Margin

2.08%

Efficiency Ratio

27% -3 ppts YoY (9M16/9M15)

+26 bps YoY (9M16/9M15)

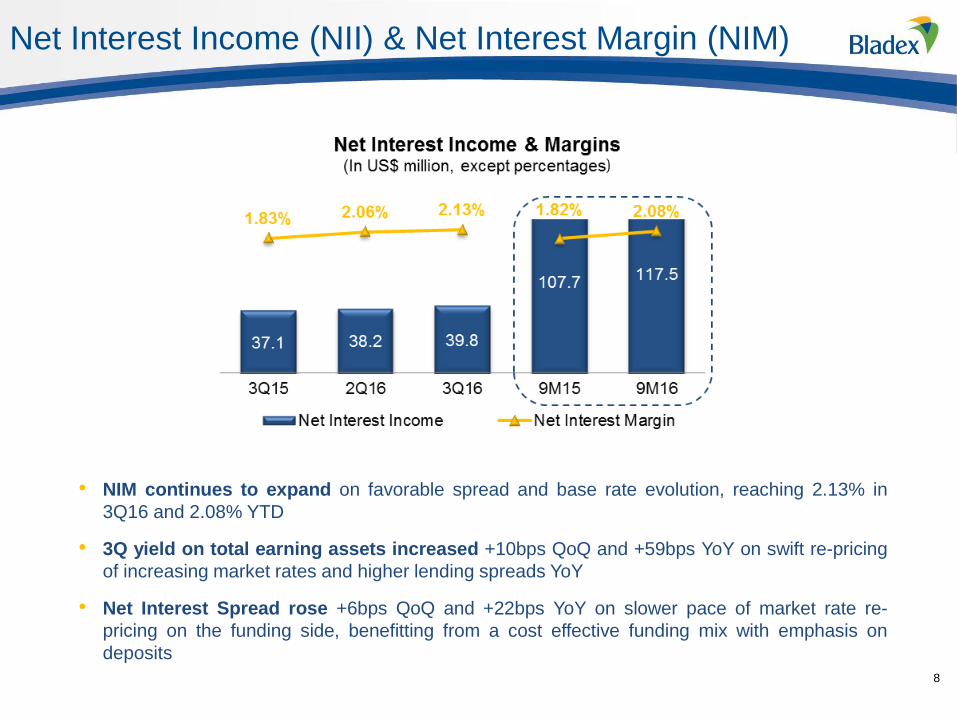

Net Interest Income (NII) & Net Interest Margin (NIM)

8

• NIM continues to expand on favorable spread and base rate evolution, reaching 2.13% in

3Q16 and 2.08% YTD

• 3Q yield on total earning assets increased +10bps QoQ and +59bps YoY on swift re-pricing

of increasing market rates and higher lending spreads YoY

• Net Interest Spread rose +6bps QoQ and +22bps YoY on slower pace of market rate re-

pricing on the funding side, benefitting from a cost effective funding mix with emphasis on

deposits

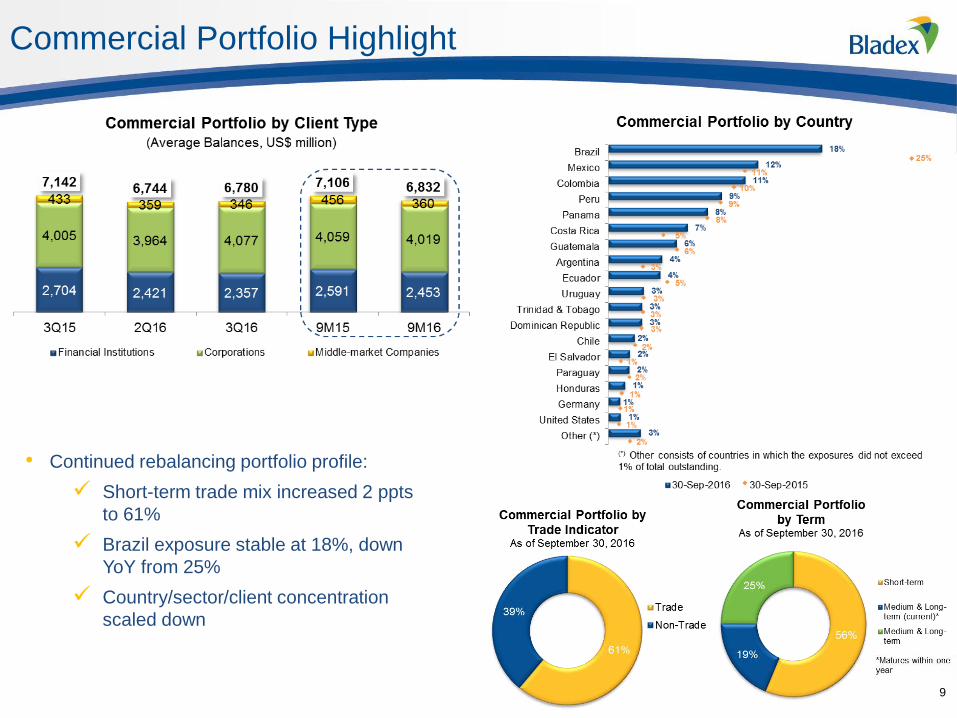

Commercial Portfolio Highlight

9

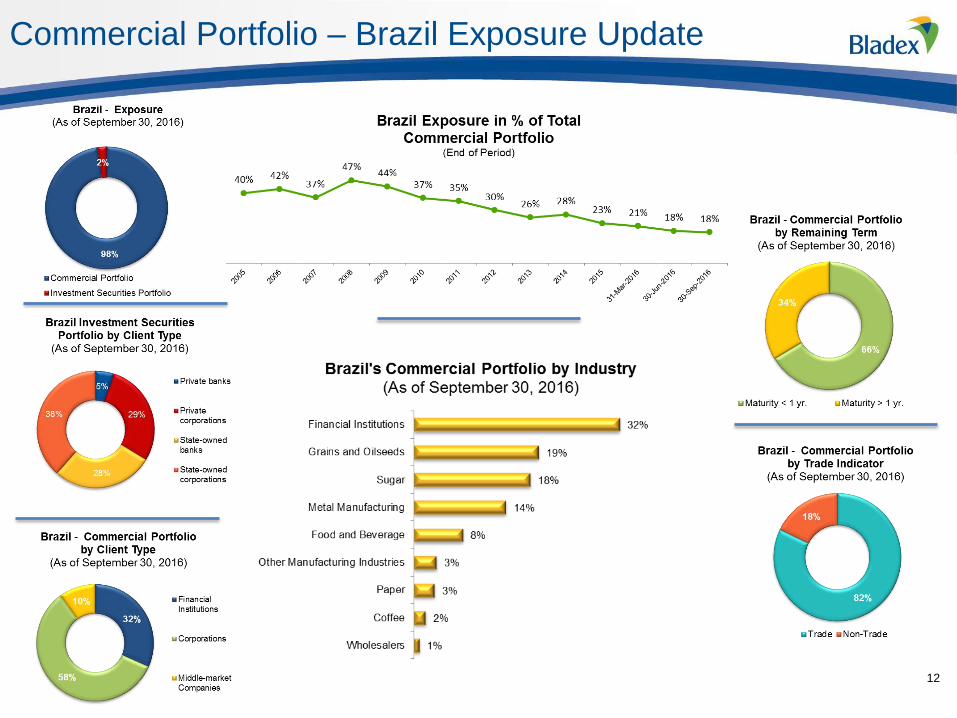

• Continued rebalancing portfolio profile:

Short-term trade mix increased 2 ppts

to 61%

Brazil exposure stable at 18%, down

YoY from 25%

Country/sector/client concentration

scaled down

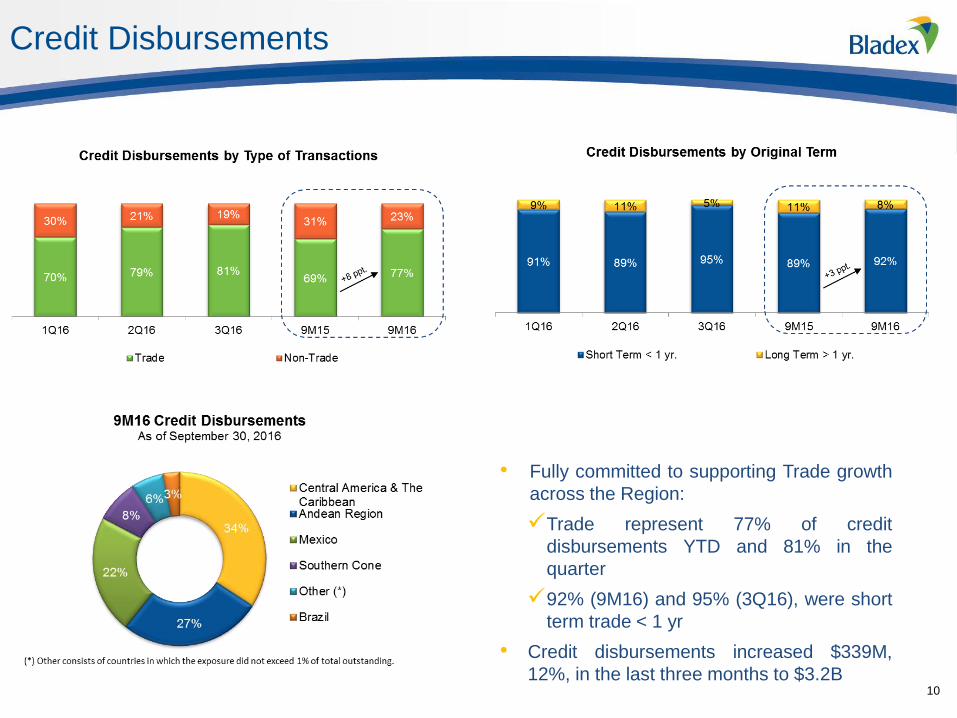

Credit Disbursements

10

• Fully committed to supporting Trade growth

across the Region:

Trade represent 77% of credit

disbursements YTD and 81% in the

quarter

92% (9M16) and 95% (3Q16), were short

term trade < 1 yr

• Credit disbursements increased $339M,

12%, in the last three months to $3.2B

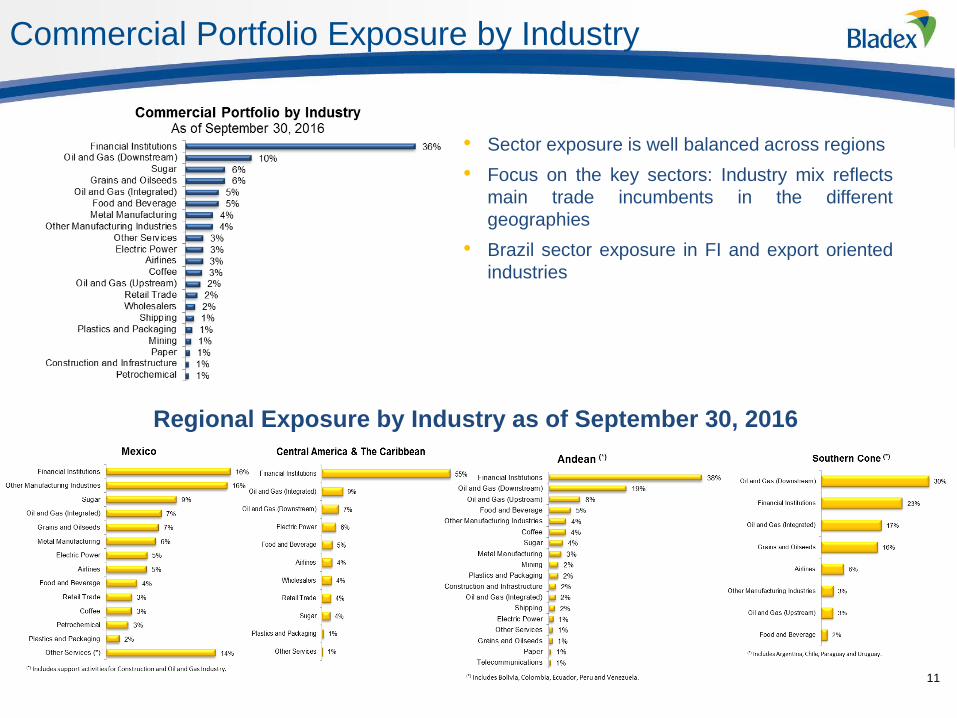

Commercial Portfolio Exposure by Industry

11

• Sector exposure is well balanced across regions

• Focus on the key sectors: Industry mix reflects

main trade incumbents in the different

geographies

• Brazil sector exposure in FI and export oriented

industries

Regional Exposure by Industry as of September 30, 2016

Commercial Portfolio – Brazil Exposure Update

12

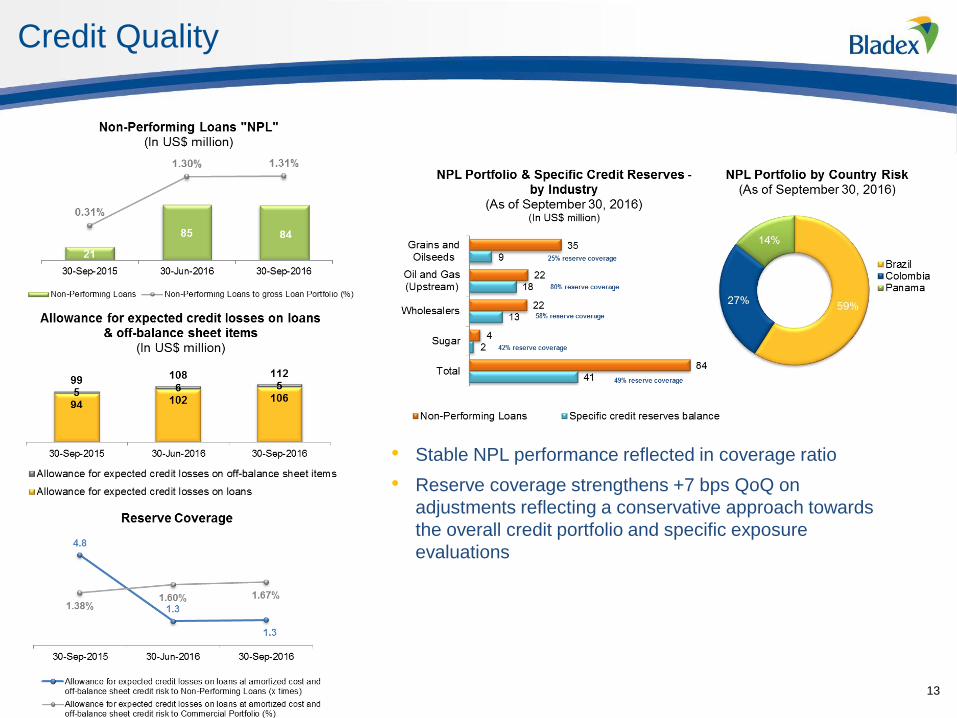

Credit Quality

13

• Stable NPL performance reflected in coverage ratio

• Reserve coverage strengthens +7 bps QoQ on

adjustments reflecting a conservative approach towards

the overall credit portfolio and specific exposure

evaluations

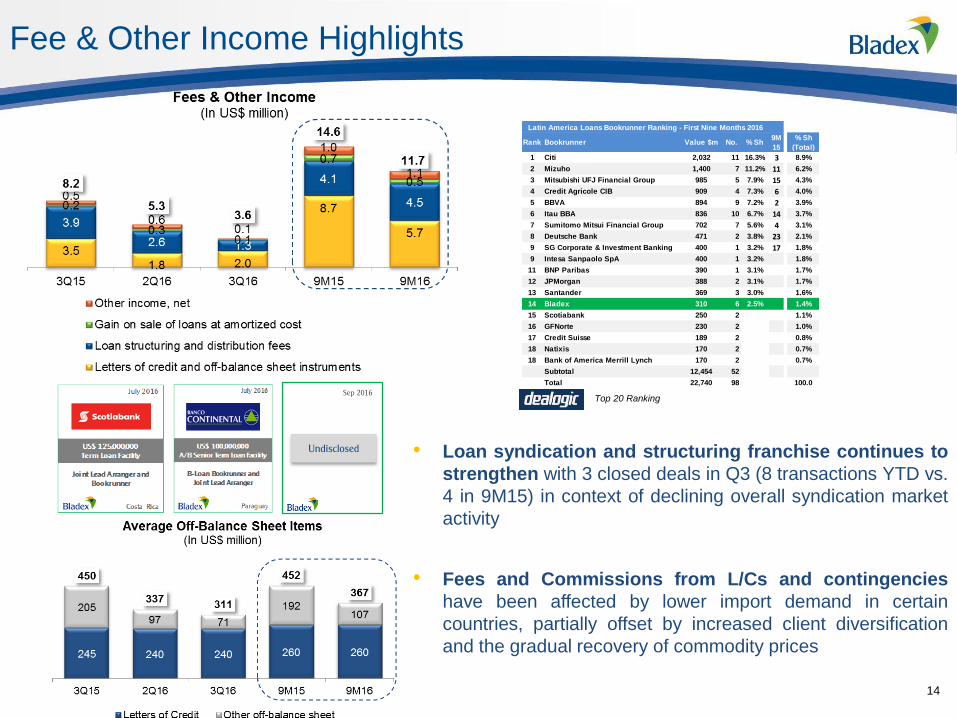

Fee & Other Income Highlights

14

Sep 2016

Undisclosed • Loan syndication and structuring franchise continues to

strengthen with 3 closed deals in Q3 (8 transactions YTD vs.

4 in 9M15) in context of declining overall syndication market

activity

• Fees and Commissions from L/Cs and contingencies

have been affected by lower import demand in certain

countries, partially offset by increased client diversification

and the gradual recovery of commodity prices

Rank Bookrunner Value $m No. % Sh9M

15

% Sh

(Total)

1 Citi 2,032 11 16.3% 3 8.9%

2 Mizuho 1,400 7 11.2% 11 6.2%

3 Mitsubishi UFJ Financial Group 985 5 7.9% 15 4.3%

4 Credit Agricole CIB 909 4 7.3% 6 4.0%

5 BBVA 894 9 7.2% 2 3.9%

6 Itau BBA 836 10 6.7% 14 3.7%

7 Sumitomo Mitsui Financial Group 702 7 5.6% 4 3.1%

8 Deutsche Bank 471 2 3.8% 23 2.1%

9 SG Corporate & Investment Banking 400 1 3.2% 17 1.8%

9 Intesa Sanpaolo SpA 400 1 3.2% 1.8%

11 BNP Paribas 390 1 3.1% 1.7%

12 JPMorgan 388 2 3.1% 1.7%

13 Santander 369 3 3.0% 1.6%

14 Bladex 310 6 2.5% 1.4%

15 Scotiabank 250 2 1.1%

16 GFNorte 230 2 1.0%

17 Credit Suisse 189 2 0.8%

18 Natixis 170 2 0.7%

18 Bank of America Merrill Lynch 170 2 0.7%

Subtotal 12,454 52

Total 22,740 98 100.0

Latin America Loans Bookrunner Ranking - First Nine Months 2016

Top 20 Ranking

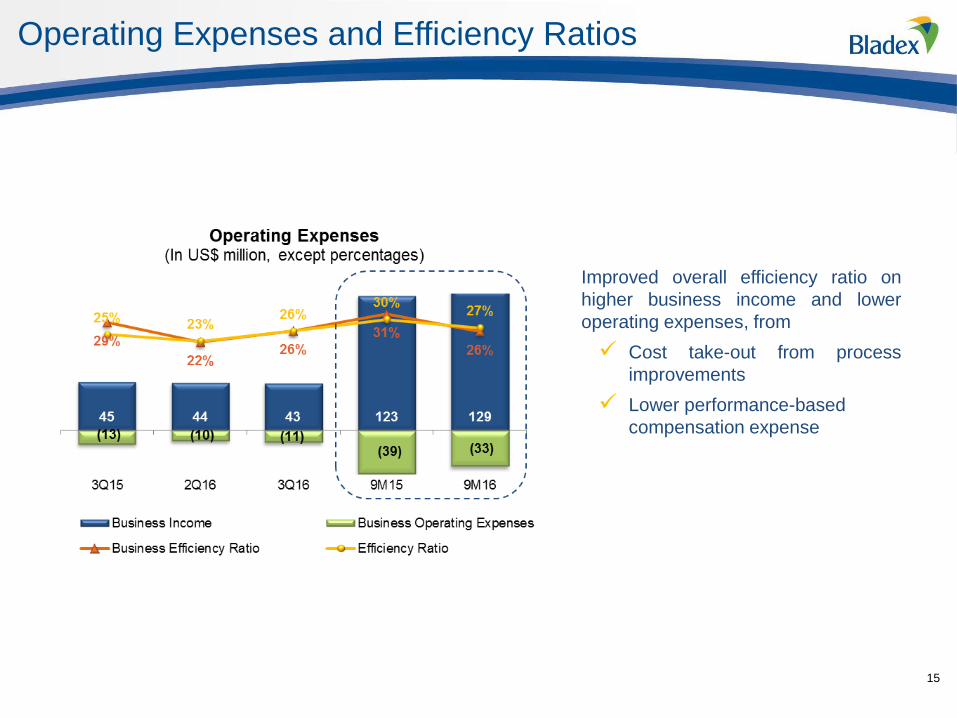

Operating Expenses and Efficiency Ratios

15

• Improved overall efficiency ratio on

higher business income and lower

operating expenses, from

Cost take-out from process

improvements

Lower performance-based

compensation expense

ROAE and Capitalization

• QoQ ROAE reflects higher earnings

generation and improved core business

dynamics and stable credit quality

• YoY lower ROAE on lower Balance

Sheet gearing, swing in non-core results

• Robust Tier 1 Basel III ratio at 15.9%,

leaves the Bank well positioned to

capture growth opportunities going

forward

16

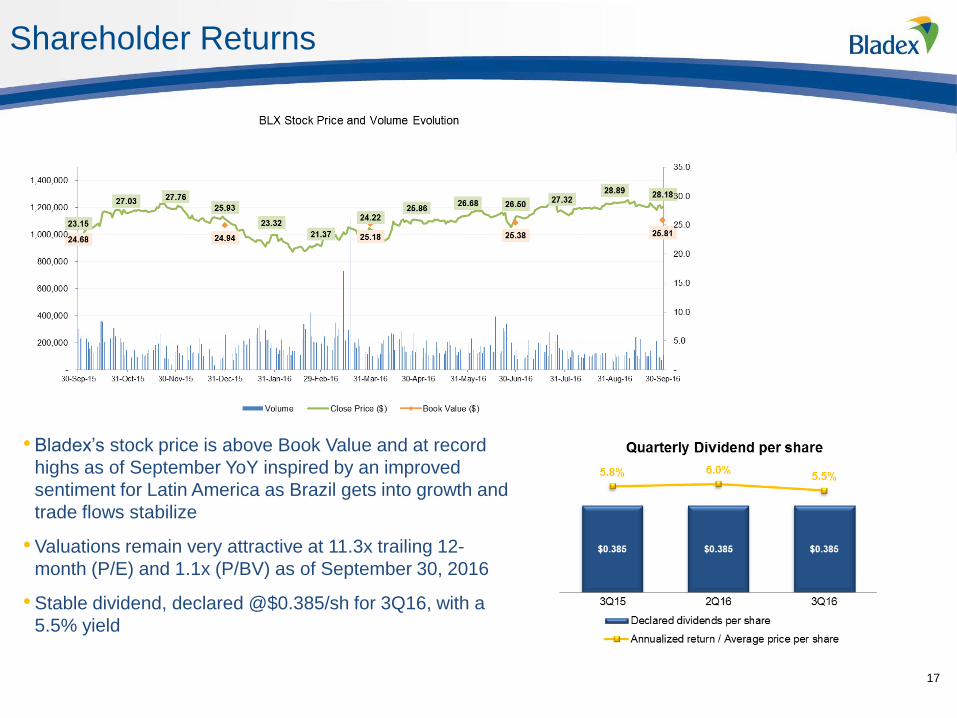

Shareholder Returns

• Bladex’s stock price is above Book Value and at record

highs as of September YoY inspired by an improved

sentiment for Latin America as Brazil gets into growth and

trade flows stabilize

• Valuations remain very attractive at 11.3x trailing 12-

month (P/E) and 1.1x (P/BV) as of September 30, 2016

• Stable dividend, declared @$0.385/sh for 3Q16, with a

5.5% yield

17

Questions & Answers

18

Thank You

19