Embed Size (px)

Citation preview

1

Earnings Release | Conference Call – 1Q13

May 7th, 2013

2

Agenda

Ricardo Ribeiro

Vice President

Carlos Wollenweber

CFO | IR Officer

1Q13 Highlights

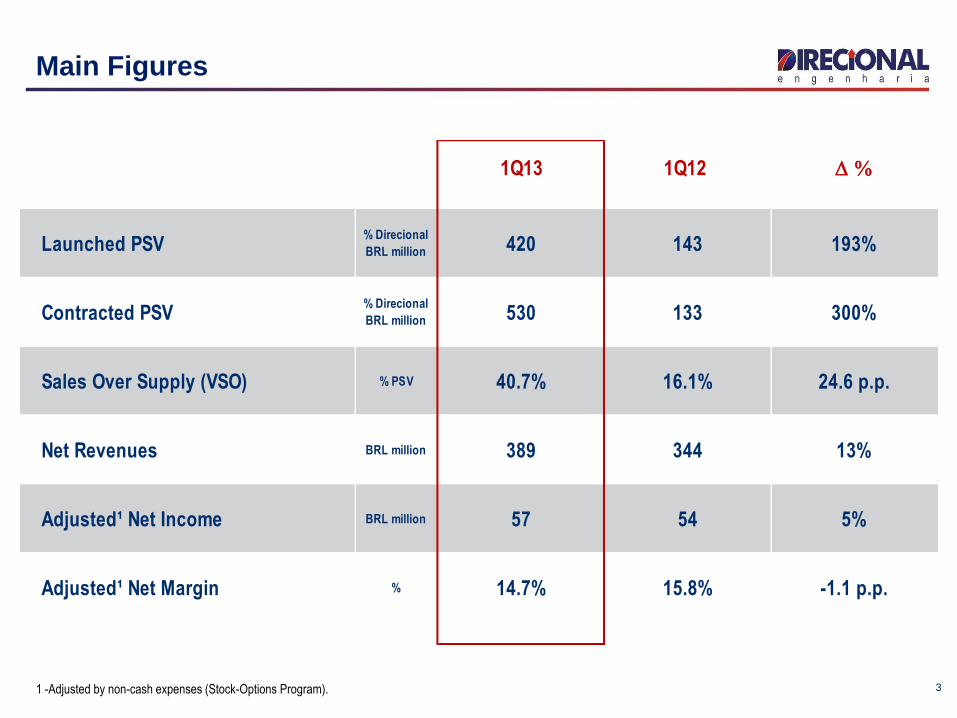

Financial Highlights

1Q13 1Q12 D %

Launched PSV% Direcional

BRL million 420 143 193%

Contracted PSV% Direcional

BRL million 530 133 300%

Sales Over Supply (VSO) % PSV 40.7% 16.1% 24.6 p.p.

Net Revenues BRL million 389 344 13%

Adjusted¹ Net Income BRL million 57 54 5%

Adjusted¹ Net Margin % 14.7% 15.8% -1.1 p.p.

Main Figures

3 1 -Adjusted by non-cash expenses (Stock-Options Program).

4

Launches – 1Q13

143

+193%

1Q13

420

405

15

1Q12

MCMV Level 1

Development

MG5

AP

3

1

PA

4

2

Launched PSV

(R$ million)

Record launches in 1Q13;

Focus on the MCMV Level 1 segment.

Total

(R$'000)

% Direcional

(R$'000)

# of Units

Launched

Total Units

(All Phases)

1 Residencial São José January Macapá - AP 89,280 89,280 1,440 1,440 MCMV Level 1

2 Residencial Orgulho de Minas 2 February Belo Horizonte - MG 14,880 14,880 240 240 MCMV Level 1

3 Viver Melhor Marituba March Marituba - PA 264,000 264,000 4,000 4,000 MCMV Level 1

4 Unique Residence March Belo Horizonte - MG 15,201 15,201 36 36 Upper-Midle

5 Residencial Serras de Minas March Belo Horizonte - MG 36,436 36,436 580 580 MCMV Level 1

Total 1Q13 419,797 419,797 6,296 6,296

Units Launched

Segment1Q13 Projects Date City - State

PSV

5

Sales and VSO – 1Q13

1Q13

40.7%

15.2%

4Q12

55.4%

15.2%

3Q12

41.3%

18.7%

2Q12

36.5%

21.2%

1Q12

16.1% 16.1%

With MCMV Level 1 project

Without MCMV Level 1 project

1Q12 90%

10% 51% 22%

5%

2%

2Q12 94% 88%

3%

2%

1%

3Q12 97% 95% 1% 1%

4Q12 98% 98% 0%

1Q13 100%

3 M 6 M 9 M 12 M 15 M

+300%

1Q13

530

405

125

1Q12

133

133

Sales by Period of Launching - 1Q13

(% PSV – Ex-MCMV Level 1)

8%

2011

19%

<2011 34%

1Q12 3%

2Q12 8%

3Q12

4Q12

25% 1Q13

4%

Contracted PSV

(R$ million)

Sales-over-supply ratio (VSO)

(% Units)

Sales Speed

(% Units)

Record sales in 1Q13;

Sales were 26% higher than launched PSV;

SoS of 40.7%.

MCMV Level 1

Development

6

Inventory

1Q13

1%

2012 40%

2011

29%

2010 12%

<2010

2%

Concluded Units

16%

Midweast 17.8%

Southeast 33.0%

North 49.1%

Inventory Track Record

(R$ million)

Inventory by Launch Period

(% PSV)

Inventory Market Value by Region

(% PSV)

Reduction of 17% in total inventory;

Reduction of 18.6 % in inventory of completed units.

667 -7.5%

-16.7%

1Q13

561

106

2012

800

670

130

2011

721

668

53

Under Construction

Concluded Units

Under Construction 560.870 84,1% 1.848 78,6%

Finished Units 105.714 15,9% 502 21,4%

Total 666.584 100,0% 2.350 100,0%

Inventory % Units in Inventory %PSV in Inventory (BRL'000)

% Direcional

7

Carlos Wollenweber

CFO | IR Officer

Financial Highlights

1Q13 1Q12 D %

Units Under Construction 55,119 35,899 54%

% of Industrialization (# of units) 75% 50% 24 p.p.

Construction Sites 49 37 32.4%

Average # of Units by Construction Sites 1,125 970 16%

# of Cities 13 10 30%

8

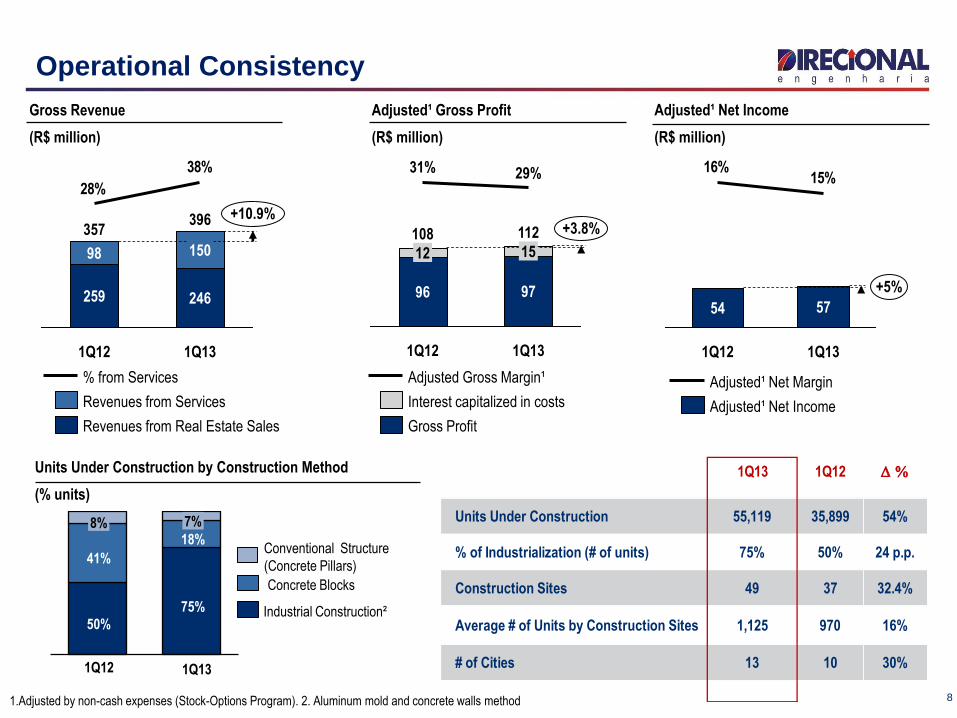

Operational Consistency

8%

75%

1Q13

18%

50%

41%

7%

1Q12

Units Under Construction by Construction Method

(% units)

Industrial Construction²

Concrete Blocks

Conventional Structure

(Concrete Pillars)

Adjusted¹ Gross Profit

(R$ million)

112 +3.8%

1Q13

97

15

29%

1Q12

108

96

12

31%

Gross Profit

Interest capitalized in costs

Adjusted Gross Margin¹

Gross Revenue

(R$ million)

38%

28%

396 +10.9%

1Q13

246

150

1Q12

357

259

98

Revenues from Real Estate Sales

Revenues from Services

% from Services

1.Adjusted by non-cash expenses (Stock-Options Program). 2. Aluminum mold and concrete walls method

Adjusted¹ Net Income

(R$ million)

15%

16%

1Q13

+5%

57

1Q12

54

Adjusted¹ Net Income

Adjusted¹ Net Margin

9

“Repasse” and Cash Burn

1Q13

-30

4Q12

-5

3Q12

-43

2Q12

-50

1Q12

-75

Cash Burn

(R$ Million)

+33% 82.9 52.9

4Q12

136.2

63.4

72.8

1Q12

39.8

43.1

-19%

1Q13

110.3

57.4

Financing Transfer (“Repasses”)

(R$ million)

"Associativo"

SFH

Cash Burn – Adjusted by Accounts Receivable

(R$ milhões)

40.2

Net Cash Burn from

the increase on

Accounts Receivable

of Finished Units

Variation on

Accounts Receivable

of Finished Units

70.5

Cash Burn

-30.3

Seasonal reduction in the number of financing installments passed on to the banks impacted cash flow in 1Q13;

Net of accounts receivable from completed units, it represents cash flow of R$40 mn;

The increase in accounts receivable from completed units is due to the PSV of R$154 million delivered in the quarter.

BRL (Million) 1Q13 4Q12 D %

Accounts Receivable (BRL'000) -Development 1,450 1,375 5%

Concluded Units 577 506 14%

Under Construction 874 869 1%

1Q13 1Q13

Previous Method Current Method

Net Revenue 376.3 12.3 388.5

Gross Income 96.2 1.0 97.2

Net income Before Minority 55.4 1.5 56.9

Minority -0.6 -1.5 -2.1

Adjusted Net Income 57.0 0.0 57.0

Adjusted Net Margin 15.1% -0.5 p.p. 14.7%

Adjustments

1Q13 Results – Change in the Accounting Method¹

10

1 - With the adoption of IFRS 11, expected for the fiscal year ending on December 31, 2013, jointly-owned subsidiaries that are currently booked proportionately in the financial

statements will be booked under the equity income method, in compliance with IAS 28R – Investments in Associates, Subsidiaries and Joint Ventures.

Total issue amount

Term

Grace period

Rate

Coordinators

Early settlement option As of Nov/14, penalty 0.2% p.y.

R$ 200 million

4 years

2 years

CDI + 1% p.y.

Itau BBA, BB, Bradesco

Information on the debenture issue:

11

12

Disclosure

This presentation contains certain forward-looking statements concerning the business prospects,

projections of operating and financial results and growth potential of the Company, which are based on

management’s current expectations and estimates of the future performance of the Company. Although the

Company believes such forward-looking statements are based on reasonable assumptions, it can give no

assurance that its expectations will be achieved. Expectations and estimates that are based on the future

prospects of the Company are highly dependent upon market behavior, Brazil’s political and economic

situation, existing and future regulations of the industry and international markets and, therefore, are

subject to changes outside the Company’s and management’s control. The Company undertakes no

obligation to update any information contained herein or to revise any forward-looking statement as a result

of new information, future events or other information.

13

Contacts

Carlos Wollenweber CFO | IR Officer

Paulo Sousa IR Analyst

Luiz Felipe Almeida IR Analyst

www.direcional.com.b/ir

(55 31) 3214-6200

(55 31) 3214-6450

![RESULTS PRESENTATION - CaixaBank · 2014-02-06 · results presentation january - december [2013] 2 ... 4q13 1q13 2q13 3q13 4q13 63% 77% 66% 65% 61% 45% 48% 49% 49% 54% 4q12 1q13](https://img.pdfslide.us/doc/110x75/5f0a718a7e708231d42ba8e9/results-presentation-caixabank-2014-02-06-results-presentation-january-december.jpg)