Embed Size (px)

Citation preview

1

Earnings Release | Conference Call – 1Q11

2

Agenda

Ricardo Ribeiro Gontijo

COO

Roberto Senna

CEO

Carlos Wollenweber

CFO | IR

1Q11 Highlights

Operating Highlights

Financial Highlights

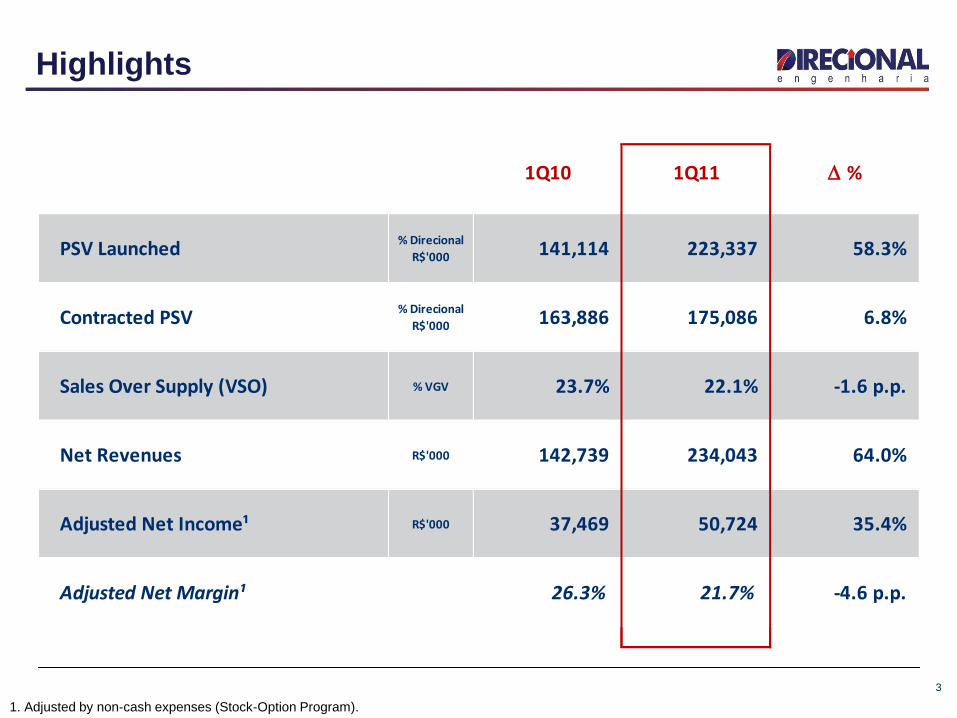

1Q10 1Q11 D %

PSV Launched % Direcional

R$'000 141,114 223,337 58.3%

Contracted PSV% Direcional

R$'000 163,886 175,086 6.8%

Sales Over Supply (VSO) % PSV 23.7% 22.1% -1.6 p.p.

Net Revenues R$'000 142,739 234,043 64.0%

Adjusted Net Income¹ R$'000 37,469 50,724 35.4%

Adjusted Net Margin¹ 26.3% 21.7% -4.6 p.p.

1Q10 1Q11 D %

PSV Launched % Direcional

R$'000 141,114 223,337 58.3%

Contracted PSV% Direcional

R$'000 163,886 175,086 6.8%

Sales Over Supply (VSO) % VGV 23.7% 22.1% -1.6 p.p.

Net Revenues R$'000 142,739 234,043 64.0%

Adjusted Net Income¹ R$'000 37,469 50,724 35.4%

Adjusted Net Margin¹ 26.3% 21.7% -4.6 p.p.

Highlights

3

1. Adjusted by non-cash expenses (Stock-Option Program).

4

March

R$ 59.1 million

R$ 229.2k

R$ 3,653

258

Launch

Total PSV

Price (R$/unit)

Price (R$/sq.m).

# Units

Belo Horizonte - MG Location

February

R$ 49.7 million

R$ 119.6k

R$ 2,416

416

Santa Maria - DF

March

R$ 81.9 million

R$ 256.0k

R$ 3,456

320

Manaus - AM

Brisas do Parque Boulevard Esplanada Setor Total Ville

Highlights: 1Q11 Launches

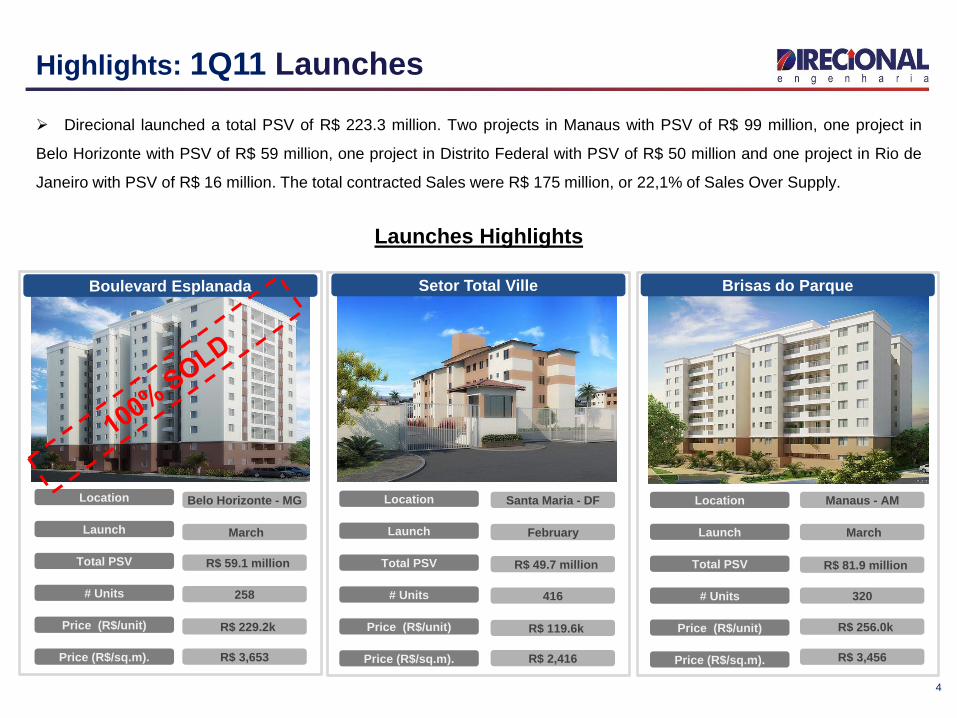

Direcional launched a total PSV of R$ 223.3 million. Two projects in Manaus with PSV of R$ 99 million, one project in

Belo Horizonte with PSV of R$ 59 million, one project in Distrito Federal with PSV of R$ 50 million and one project in Rio de

Janeiro with PSV of R$ 16 million. The total contracted Sales were R$ 175 million, or 22,1% of Sales Over Supply.

Launches Highlights

Launch

Total PSV

Price (R$/unit)

Price (R$/sq.m).

# Units

Location

Launch

Total PSV

Price (R$/unit)

Price (R$/sq.m).

# Units

Location

14.9 20.7 33.0 48.2 56.8

1Q10 2Q10 3Q10 4Q11 1Q11

5

Bairro Carioca construction site

Infrastructure already in place.

281.2%

Revenue of Services Evolution

Date •4Q10

PSV Contracted

•R$ 114.2 million

# de Units •2,240 Units

Construction Start

•May 2011

BAIRRO CARIOCA

DF:

PSV R$

253MN

6

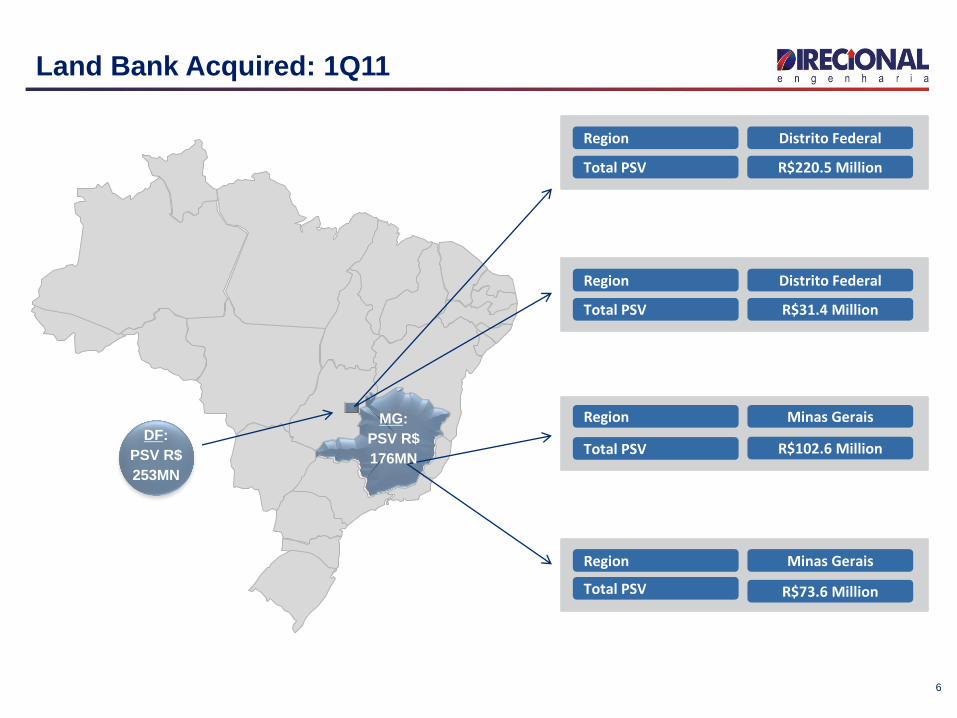

Region Distrito Federal

Total PSV R$220.5 Million

Region Distrito Federal

Total PSV R$31.4 Million

Region Minas Gerais

Total PSV R$73.6 Million

Region Minas Gerais

Total PSV R$102.6 Million

Land Bank Acquired: 1Q11

MG:

PSV R$

176MN

7

Operating Highlights

Ricardo Ribeiro Gontijo

Operating Highlights

Launches

Sales

Land bank

Inventory

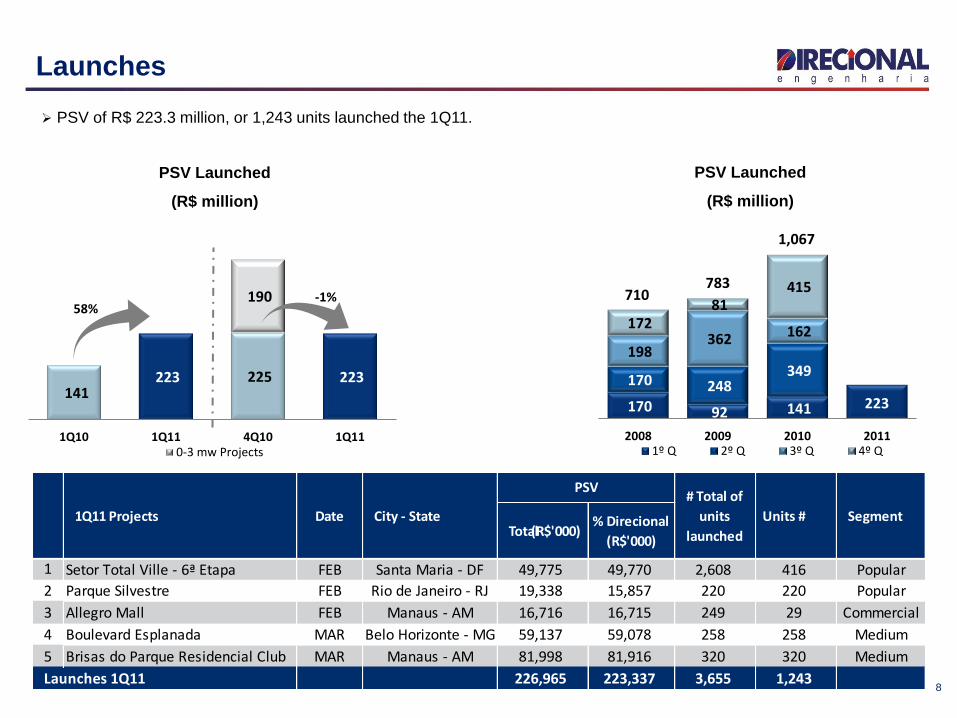

141 223 225 223

190

1Q10 1Q11 4Q10 1Q110-3 mw Projects

Total(R$'000)% Direcional

(R$'000)

1 Setor Total Ville - 6ª Etapa FEB Santa Maria - DF 49,775 49,770 2,608 416 Popular

2 Parque Silvestre FEB Rio de Janeiro - RJ 19,338 15,857 220 220 Popular

3 Allegro Mall FEB Manaus - AM 16,716 16,715 249 29 Commercial

4 Boulevard Esplanada MAR Belo Horizonte - MG 59,137 59,078 258 258 Medium

5 Brisas do Parque Residencial Club MAR Manaus - AM 81,998 81,916 320 320 Medium

Launches 1Q11 226,965 223,337 3,655 1,243

Segment Units #

PSV# Total of

units

launched

1Q11 Projects Date City - State

170 92 141 223

170 248 349

198 362 162

172 81

415

2008 2009 2010 20111º Q 2º Q 3º Q 4º Q

8

Launches

PSV of R$ 223.3 million, or 1,243 units launched the 1Q11.

PSV Launched

(R$ million)

PSV Launched

(R$ million)

710 783

1,067

58% -1%

97.8%

51.2%

46.5%

2.2% 2.3%

1Q10 1Q11

Popular Medium Upper Middle Commercial

73.3%

28.1%

24.5%

33.5%

2.2%

38.5%

1Q10 1Q11

North Midwest Southeast

9

Launches Breakdown

Launches

(Segment Breakdown - Units)

Launches

(Geographic Breakdown - Units)

Boulevard Esplanada Setor Total Ville

Parque Silvestre

Brisas do Parque

Allegro Mall

76,8%54,3%

17,7%39,8%

5,5%3,5%2,4%

1Q10 1Q11

Popular Medium Upper Middle Commercial

164 175 217

175

190

1T10 1T11 4T10 1T110-3 mw Projects

57.7%32.0%

34.6%

25.3%

7.7%

42.7%

1Q10 1Q11

North Midwest Southeast

80 90 164 175 123 190

324 153 243

143

85

137

406

2008 2009 2010 20111º Q 2º Q 3º Q 4º Q

Contracted PSV

(R$ million)

Sales Evolution

(R$ million)

Sales

(Geographic Breakdown)

Sales

(Segment Breakdown)

10

Sales

In the 1Q11 Direcional sold 1,211 units with a total PSV of R$ 174.6 million, and average price of R$ 183.0 thousand.

441

661

1.037

+7% -19%

17%

89%

17%

87%

48%

19%

4%

27%

4%

7%

3%

14%

5%

1%

5%1Q10

2Q10

3Q10

4Q10

1Q11

3M 6M 9M 12M 15M

91%

58%

97%

53%

48%

33.8%38.3%

23.7%19.4% 20.8%

27.6%

22.1%

1Q10 2Q10* 3Q10 4Q10* 1Q11

With 0-3 mw projects Without 0-3 mw projects

11

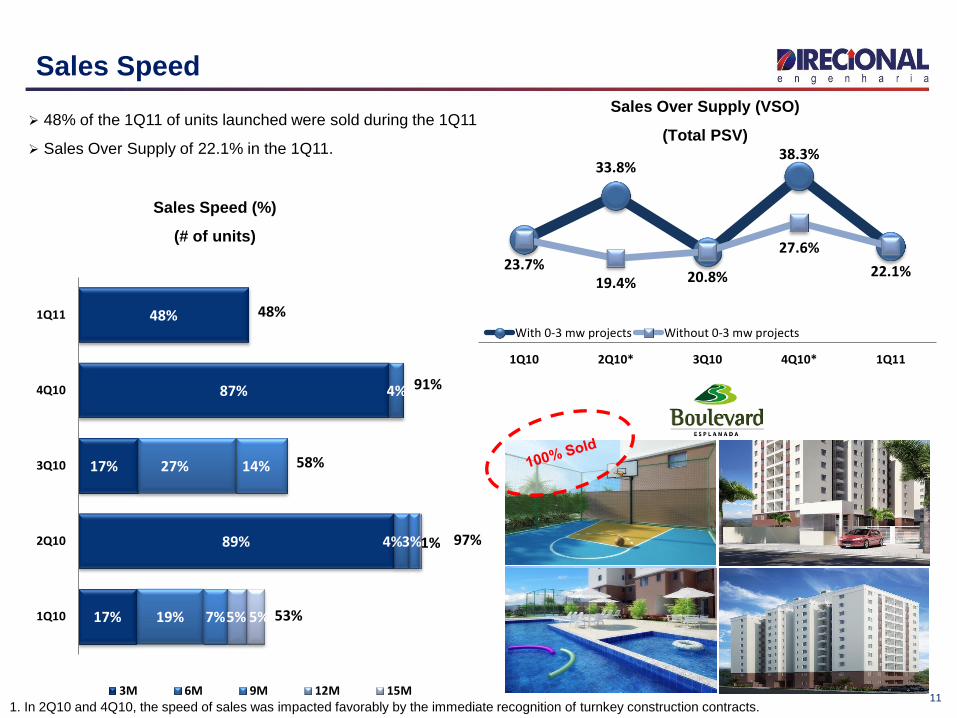

Sales Speed

48% of the 1Q11 of units launched were sold during the 1Q11

Sales Over Supply of 22.1% in the 1Q11.

Sales Over Supply (VSO)

(Total PSV)

Sales Speed (%)

(# of units)

1. In 2Q10 and 4Q10, the speed of sales was impacted favorably by the immediate recognition of turnkey construction contracts.

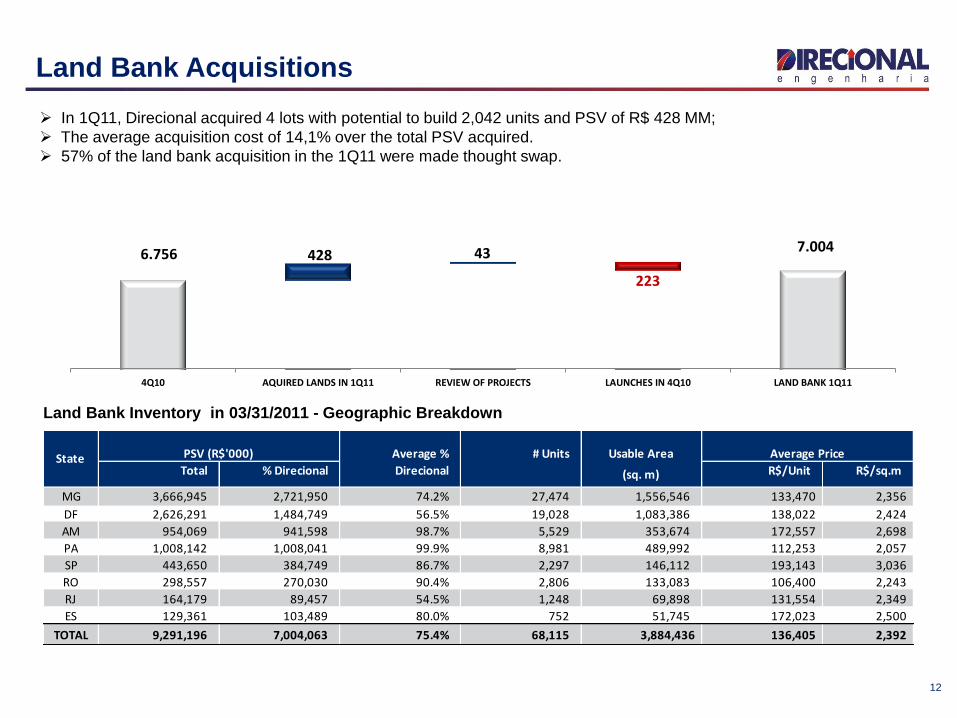

6.756 7.004428 43

223

4Q10 AQUIRED LANDS IN 1Q11 REVIEW OF PROJECTS LAUNCHES IN 4Q10 LAND BANK 1Q11

Average % # Units Usable Area

Total % Direcional Direcional (sq. m) R$/Unit R$/sq.m

MG 3,666,945 2,721,950 74.2% 27,474 1,556,546 133,470 2,356

DF 2,626,291 1,484,749 56.5% 19,028 1,083,386 138,022 2,424

AM 954,069 941,598 98.7% 5,529 353,674 172,557 2,698

PA 1,008,142 1,008,041 99.9% 8,981 489,992 112,253 2,057

SP 443,650 384,749 86.7% 2,297 146,112 193,143 3,036

RO 298,557 270,030 90.4% 2,806 133,083 106,400 2,243

RJ 164,179 89,457 54.5% 1,248 69,898 131,554 2,349

ES 129,361 103,489 80.0% 752 51,745 172,023 2,500

TOTAL 9,291,196 7,004,063 75.4% 68,115 3,884,436 136,405 2,392

PSV (R$'000) Average PriceState

12

Land Bank Acquisitions

In 1Q11, Direcional acquired 4 lots with potential to build 2,042 units and PSV of R$ 428 MM;

The average acquisition cost of 14,1% over the total PSV acquired.

57% of the land bank acquisition in the 1Q11 were made thought swap.

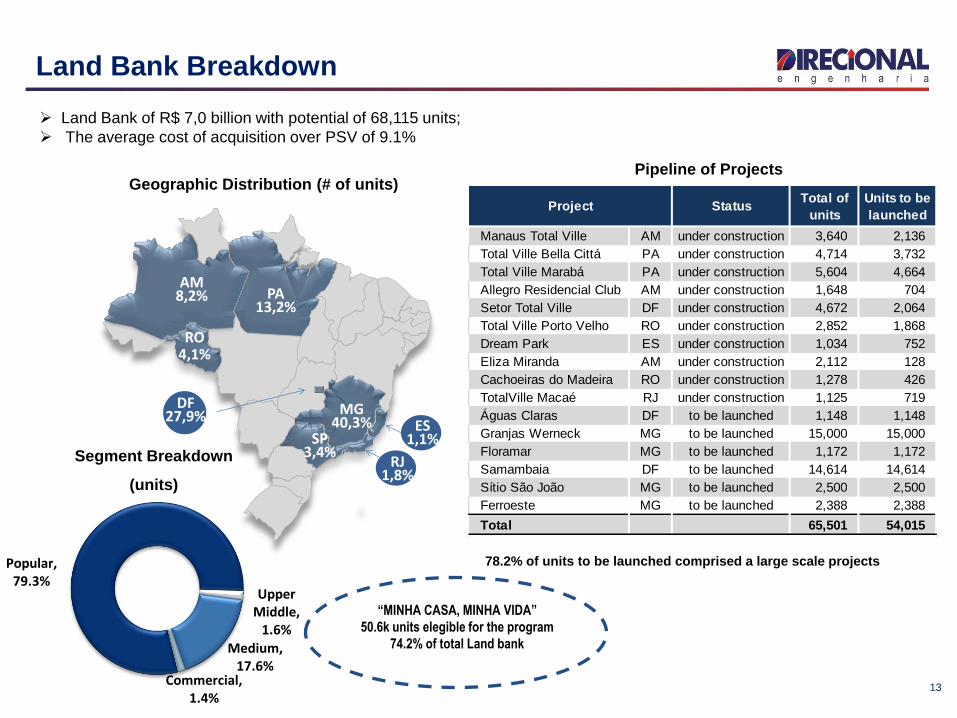

Land Bank Inventory in 03/31/2011 - Geographic Breakdown

Manaus Total Ville AM under construction 3,640 2,136

Total Ville Bella Cittá PA under construction 4,714 3,732

Total Ville Marabá PA under construction 5,604 4,664

Allegro Residencial Club AM under construction 1,648 704

Setor Total Ville DF under construction 4,672 2,064

Total Ville Porto Velho RO under construction 2,852 1,868

Dream Park ES under construction 1,034 752

Eliza Miranda AM under construction 2,112 128

Cachoeiras do Madeira RO under construction 1,278 426

TotalVille Macaé RJ under construction 1,125 719

Águas Claras DF to be launched 1,148 1,148

Granjas Werneck MG to be launched 15,000 15,000

Floramar MG to be launched 1,172 1,172

Samambaia DF to be launched 14,614 14,614

Sítio São João MG to be launched 2,500 2,500

Ferroeste MG to be launched 2,388 2,388

Total 65,501 54,015

Project StatusTotal of

units

Units to be

launched

Popular, 79.3%

Upper Middle,

1.6%

Medium, 17.6%

Commercial, 1.4%

13

1

ES1,1%

AM8,2%

MG40,3%

RO4,1%

SP3,4%

PA13,2%

DF27,9%

RJ1,8%

Land Bank Breakdown

Land Bank of R$ 7,0 billion with potential of 68,115 units;

The average cost of acquisition over PSV of 9.1%

Geographic Distribution (# of units)

Segment Breakdown

(units)

Pipeline of Projects

78.2% of units to be launched comprised a large scale projects

“MINHA CASA, MINHA VIDA”

50.6k units elegible for the program

74.2% of total Land bank

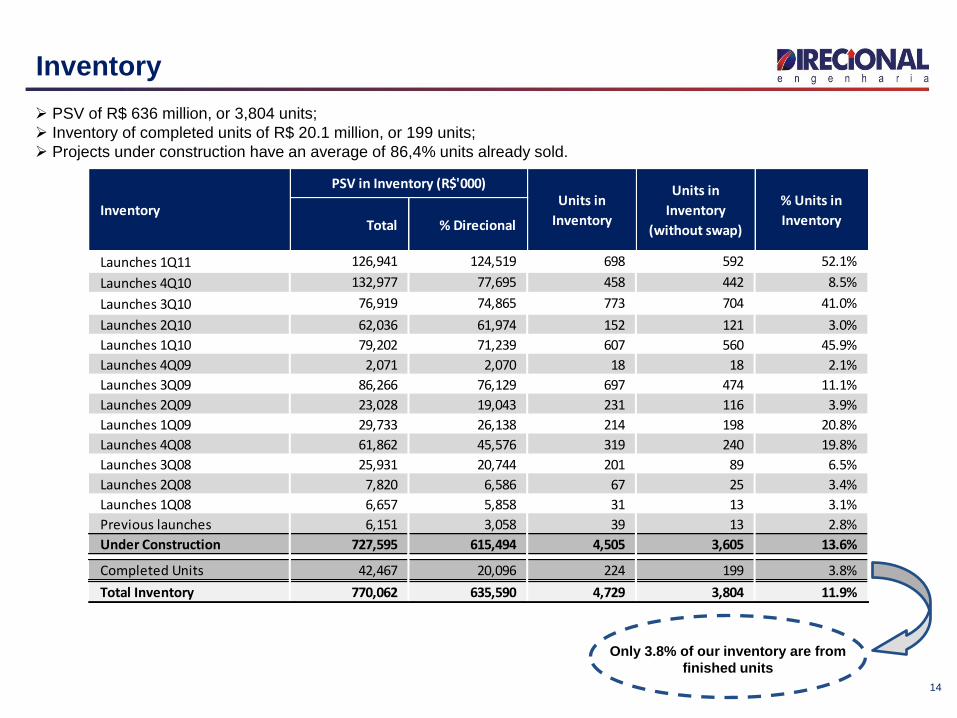

Total % Direcional

Launches 1Q11 126,941 124,519 698 592 52.1%

Launches 4Q10 132,977 77,695 458 442 8.5%

Launches 3Q10 76,919 74,865 773 704 41.0%

Launches 2Q10 62,036 61,974 152 121 3.0%

Launches 1Q10 79,202 71,239 607 560 45.9%

Launches 4Q09 2,071 2,070 18 18 2.1%

Launches 3Q09 86,266 76,129 697 474 11.1%

Launches 2Q09 23,028 19,043 231 116 3.9%

Launches 1Q09 29,733 26,138 214 198 20.8%

Launches 4Q08 61,862 45,576 319 240 19.8%

Launches 3Q08 25,931 20,744 201 89 6.5%

Launches 2Q08 7,820 6,586 67 25 3.4%

Launches 1Q08 6,657 5,858 31 13 3.1%

Previous launches 6,151 3,058 39 13 2.8%

Under Construction 727,595 615,494 4,505 3,605 13.6%

Completed Units 42,467 20,096 224 199 3.8%

Total Inventory 770,062 635,590 4,729 3,804 11.9%

Inventory

PSV in Inventory (R$'000)Units in

Inventory

Units in

Inventory

(without swap)

% Units in

Inventory

14

Inventory

PSV of R$ 636 million, or 3,804 units;

Inventory of completed units of R$ 20.1 million, or 199 units;

Projects under construction have an average of 86,4% units already sold.

Only 3.8% of our inventory are from

finished units

15

Financial Highlights

Financial Performance

Liquidity Indicators

Results to be Recognized

Performance Shares

Carlos Wollenweber

Financial Highlights

Development, 76.2%

Management Fee, 0.8%

0-3 MW Projects, 22.5%

Brokerage, 0.5%

37

51 51 51

26.3% 21.7% 19.3% 21.7%

0.0 %

10. 0%

20. 0%

30. 0%

40. 0%

50. 0%

60. 0%

70. 0%

80. 0%

90. 0%

100 .0%

30

35

40

45

50

55

1Q10 1Q11 4Q10 1Q11

Margem Líquida

143

234 263

234

1Q10 1Q11 4Q10 1Q11

63.4 102.3 263.2 377.6 781.9 234.0

24.0% 21.1%24.5% 22.5% 22.6% 21.7%

2006 2007 2008 2009 2010 2011

Net Revenue Net Margin

+64%

-11%

16

Financial Highlights

Adjusted Net Income and Net Margin1

1. Adjusted by non-cash expenses (Stock-Option Program).

Gross Revenue Breakdown

Net Revenues

+35%

0%

CAGR: 87,4%

Net Revenue and Net Margin Evolution

14,9 20,7 33,0 48,2 56,8 48,2 56,8

10,4% 12,5% 15,7% 18,3%24,3%

18,3%24,3%

1Q10 2Q10 3Q10 4Q10 1Q11 4Q10 1Q11% of Revenues

Revenue of Services Evolution

17

Financial Highlights

Gross Profit and Gross Margin

+31%

-17%

281,2% +18%

50

66

79

66 35.1%

28.0% 29.9% 28.0%

0.0 %

20. 0%

40. 0%

60. 0%

80. 0%

100 .0%

120 .0%

40

45

50

55

60

65

70

75

80

1Q10 1Q11 4Q10 1Q11Gross Margin

3,9 5,0 6,2 5,0

1,9%

2,3%

1,3%

2,3%

2,1%

-3,0%

-2,0%

-1,0%

0,0 %

1,0 %

2,0 %

3,0 %

-

2,0

4,0

6,0

8,0

10,0

12,0

14,0

16,0

18,0

20,0

1Q10 1Q11 4Q10 1Q11% of Sales % of Sales without 0-3 sw projects

8,4

16,2 17,4 16,2

5,9%6,9% 6,6% 6,9%

-4,0%

-2,0%

0,0 %

2,0 %

4,0 %

6,0 %

8,0 %

-

5,0

10,0

15,0

20,0

25,0

30,0

1Q10 1Q11 4Q10 1Q11% of Revenue

42 58 65 58

29.7% 24.7% 24.7% 24.7%

0.0 %

20. 0%

40. 0%

60. 0%

80. 0%

100 .0%

120 .0%

-

10

20

30

40

50

60

70

80

1Q10 1Q11 4Q10 1Q11Ebitda Margin

18

Financial Highlights

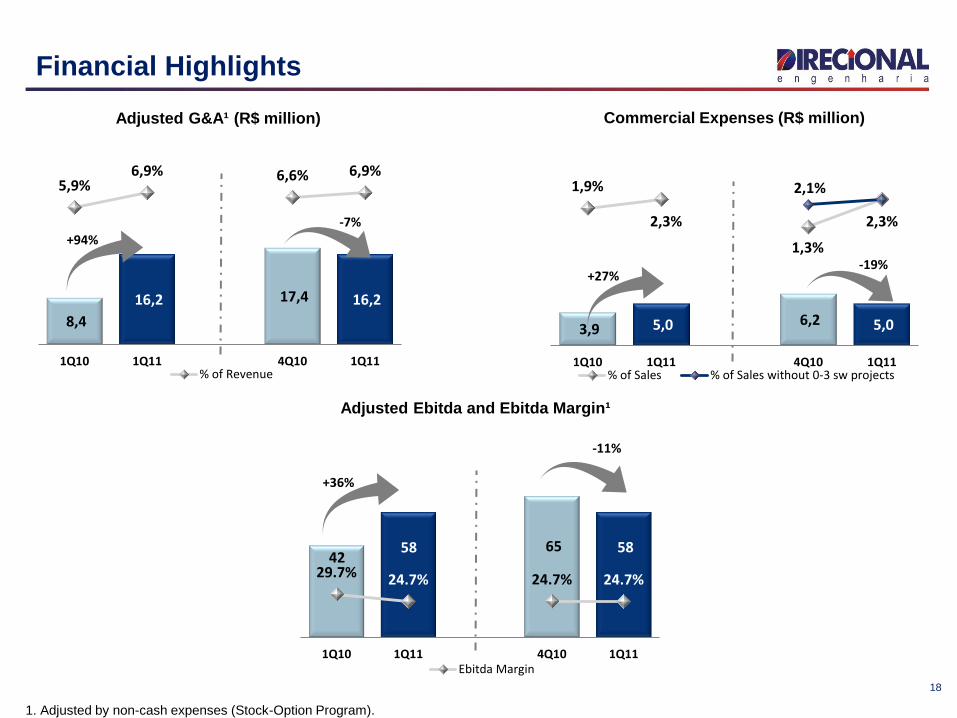

Adjusted Ebitda and Ebitda Margin¹

Adjusted G&A¹ (R$ million) Commercial Expenses (R$ million)

+94%

-7%

+27% -19%

+36%

-11%

1. Adjusted by non-cash expenses (Stock-Option Program).

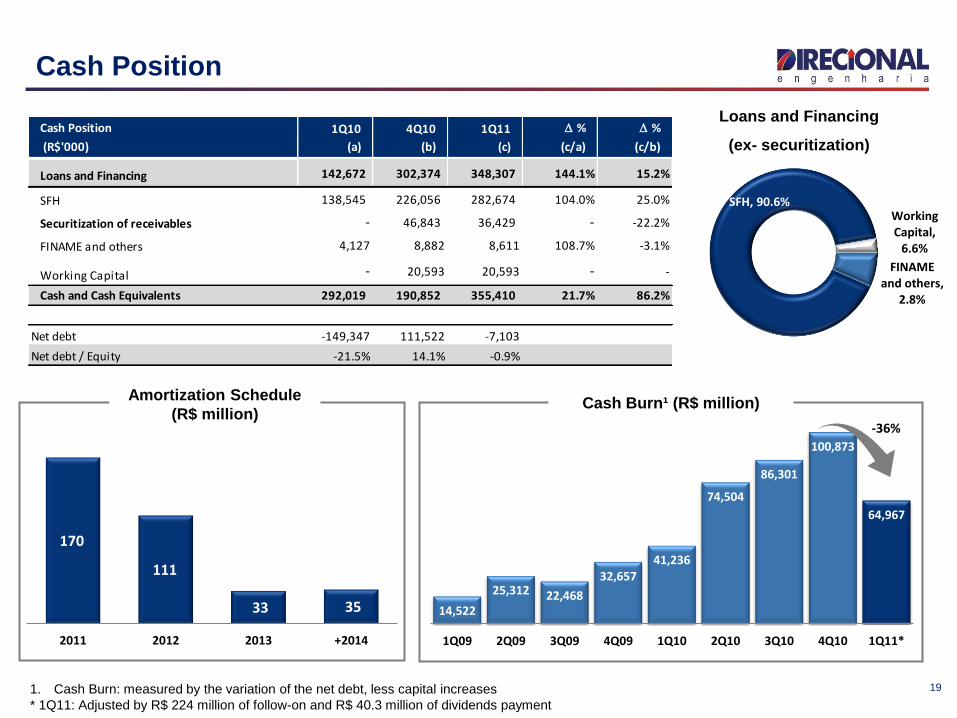

Cash Position 1Q10 4Q10 1Q11 D % D %

(R$'000) (a) (b) (c) (c/a) (c/b)

Loans and Financing 142,672 302,374 348,307 144.1% 15.2%

SFH 138,545 226,056 282,674 104.0% 25.0%

Securitization of receivables - 46,843 36,429 - -22.2%

FINAME and others 4,127 8,882 8,611 108.7% -3.1%

Working Capital - 20,593 20,593 - -

Cash and Cash Equivalents 292,019 190,852 355,410 21.7% 86.2%

Net debt -149,347 111,522 -7,103

Net debt / Equity -21.5% 14.1% -0.9%

SFH, 90.6%

FINAME and others,

2.8%

Working Capital,

6.6%

14,522

25,312 22,468

32,65741,236

74,504

86,301

100,873

64,967

1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11*

170

111

33 35

2011 2012 2013 +2014

1. Cash Burn: measured by the variation of the net debt, less capital increases

* 1Q11: Adjusted by R$ 224 million of follow-on and R$ 40.3 million of dividends payment

19

Cash Position

Amortization Schedule

(R$ million) Cash Burn¹ (R$ million)

Loans and Financing

(ex- securitization)

-36%

49.5%44.7%

5.8%

2011 2012 2013+

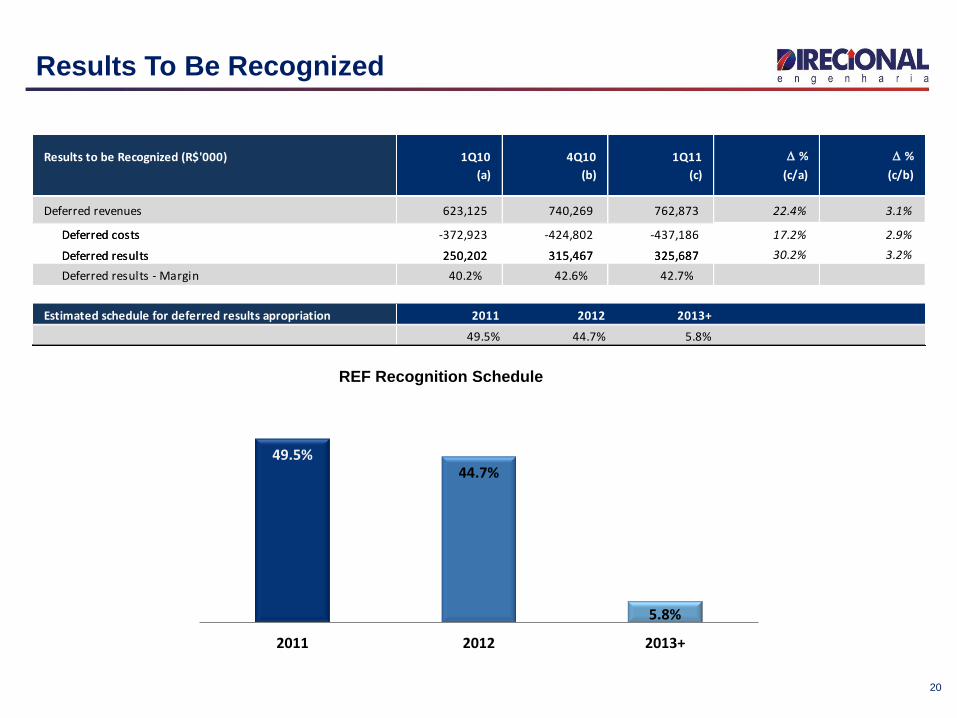

Results to be Recognized (R$'000) 1Q10 4Q10 1Q11 D % D %

(a) (b) (c) (c/a) (c/b)

Deferred revenues 623,125 740,269 762,873 22.4% 3.1%

Deferred costs -372,923 -424,802 -437,186 17.2% 2.9%

Deferred results 250,202 315,467 325,687 30.2% 3.2%

Deferred results - Margin 40.2% 42.6% 42.7%

Estimated schedule for deferred results apropriation 2011 2012 2013+

49.5% 44.7% 5.8%

Results to be Recognized (R$'000) 1Q10 4Q10 1Q11 D % D %

(a) (b) (c) (c/a) (c/b)

Deferred revenues 623,125 740,269 762,873 22.4% 3.1%

Deferred costs -372,923 -424,802 -437,186 17.2% 2.9%

Deferred results 250,202 315,467 325,687 30.2% 3.2%

Deferred results - Margin 40.2% 42.6% 42.7%

Estimated schedule for deferred results apropriation 2011 2012 2013+

49.5% 44.7% 5.8%

20

Results To Be Recognized

REF Recognition Schedule

0

20

40

60

80

100

120

140

160

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

18

-No

v-0

9

1-D

ec-0

9

11

-De

c-0

9

23

-De

c-0

9

8-J

an-1

0

20

-Jan

-10

2-F

eb

-10

12

-Fe

b-1

0

26

-Fe

b-1

0

10

-Mar

-10

22

-Mar

-10

1-A

pr-

10

14

-Ap

r-1

0

27

-Ap

r-1

0

7-M

ay-1

0

19

-May

-10

1-J

un

-10

15

-Ju

n-1

0

25

-Ju

n-1

0

7-J

ul-

10

21

-Ju

l-1

0

3-A

ug-

10

16

-Au

g-1

0

30

-Au

g-1

0

15

-Se

p-1

0

1-O

ct-1

0

14

-Oct

-10

26

-Oct

-10

8-N

ov-

10

23

-No

v-1

0

3-D

ec-1

0

17

-De

c-1

0

30

-De

c-1

0

12

-Jan

-11

24

-Jan

-11

4-F

eb

-11

16

-Fe

b-1

1

28

-Fe

b-1

1

14

-Mar

-11

24

-Mar

-11

5-A

pr-

11

15

-Ap

r-1

1

29

-Ap

r-1

1

Pre

ço d

a A

ção

Vo

lum

e (

R$

mil)

Volume (R$ '000)

0

20

40

60

80

100

120

140

160

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

18

-No

v-0

9

1-D

ec-0

9

11

-De

c-0

9

23

-De

c-0

9

8-J

an-1

0

20

-Jan

-10

2-F

eb

-10

12

-Fe

b-1

0

26

-Fe

b-1

0

10

-Mar

-10

22

-Mar

-10

1-A

pr-

10

14

-Ap

r-1

0

27

-Ap

r-1

0

7-M

ay-1

0

19

-May

-10

1-J

un

-10

15

-Ju

n-1

0

25

-Ju

n-1

0

7-J

ul-

10

21

-Ju

l-1

0

3-A

ug-

10

16

-Au

g-1

0

30

-Au

g-1

0

15

-Se

p-1

0

1-O

ct-1

0

14

-Oct

-10

26

-Oct

-10

8-N

ov-

10

23

-No

v-1

0

3-D

ec-1

0

17

-De

c-1

0

30

-De

c-1

0

12

-Jan

-11

24

-Jan

-11

4-F

eb

-11

16

-Fe

b-1

1

28

-Fe

b-1

1

14

-Mar

-11

24

-Mar

-11

5-A

pr-

11

15

-Ap

r-1

1

29

-Ap

r-1

1

Sto

ck P

rice

Vo

lum

e (

R$

'00

0)

Average Volume (21 days) Direcional Ibovespa IMOB

21

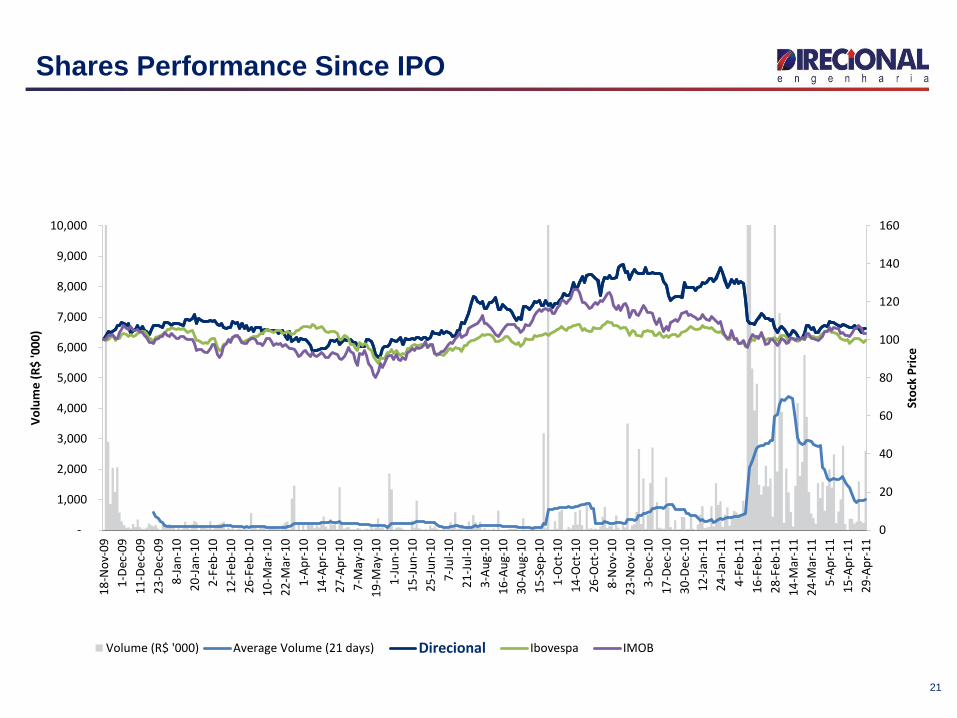

Shares Performance Since IPO

22

Disclosure

This presentation contains certain forward-looking statements concerning the business prospects,

projections of operating and financial results and growth potential of the Company, which are based on

management’s current expectations and estimates of the future performance of the Company. Although the

Company believes such forward-looking statements are based on reasonable assumptions, it can give no

assurance that its expectations will be achieved. Expectations and estimates that are based on the future

prospects of the Company are highly dependent upon market behavior, Brazil’s political and economic

situation, existing and future regulations of the industry and international markets and, therefore, are

subject to changes outside the Company’s and management’s control. The Company undertakes no

obligation to update any information contained herein or to revise any forward-looking statement as a result

of new information, future events or other information.

23

Contacts

Carlos Wollenweber CFO | IR Officer

Lucas Bousas IR Analyst

Paulo Sousa IR Assistant

www.direcional.com.br

(55 31) 3214-6200

(55 31) 3214-6450