Embed Size (px)

Citation preview

The Fundamentals of Managed Care

The first module of the Managed Health Care Unit considers those things that define and characterize Managed Health Care. A discussion regarding the various interpretations of the term, managed care is followed by an overview of the distinguishing characteristics of managed care. The first module will focus on the following aspects of managed care:

• The sharing of risk. • Controlling access to providers. • The comprehensive management of cases. • Achieving high quality care. • Preventive care.

Definitions and Characteristics of Managed Care

Generally, managed care can be defined as any medical expense plan that tries to limit costs by modifying the behavior of participants. Included in this definition is the process of monitoring and regulating health care services. Also considered are the institutions that provide such services and the care providers themselves. Finally, the fees paid by both the health care organizations and the consumer are part of this definition. Obviously, many people use the term managed care to mean different things. Indeed, the term managed care is often used to refer to any of the following set of circumstances:

• A traditional indemnity plan that requires second opinions. • A traditional indemnity plan that requires hospital pre-certification • HMOs and PPOs that limit a participant's choice of a medical providers. • HMOs and PPOs that use case management

Generally however, in the evolution of managed care plans over the past few years, the following five characteristics are considered basic to any type of managed care plan. A. Risk Sharing The most successful managed care plans share in the financial consequences of a medical decision. Many managed care plans have clauses in the contract to encourage cost-effective care. A physician who minimizes his/her diagnostic tests might receive some form of bonus. It is to be hoped that this relationship will eliminate unnecessary tests, yet not discourage doctors from ordering tests that should be performed. B. Control of Access to Providers Unrestricted access to physicians and hospitals makes it difficult to control costs. Therefore, most managed care plans try to encourage, or indeed force; their participants to use predetermined care providers. The primary care physician is the gatekeeper who determines when and if the expense of a referral to a specialist is appropriate or necessary. This limitation on the number of providers allows managed care plans to better control costs by allowing them to negotiate fees with their predetermined care providers. C. Comprehensive Case Management

Utilization reviews at all levels are an integral part of all successful managed care plans. These reviews are intended to provide something of a second opinion regarding health care decisions. Any health care action proposed is reviewed by a panel of physicians and other medical professionals in order to determine the most cost-effective and beneficial way to treat the particular patient in question. Done correctly, these reviews should eliminate or at the very least decrease unnecessary medical procedures that are both expensive and tend to clog the medical care process. D. High Quality Care In a successfully managed care plan, providers are carefully selected and monitored in order to provide a consistently high quality of continuing care. Physician specialists must be board certified. They do this by passing standardized examinations in their field of specialization. Often, other physicians in the managed care networks are also board certified. This situation indicates that this particular HMO network is concerned with quality. Support staff are also licensed in some fashion or specially trained in order to maintain a high quality of care. Nurses are usually registered and lab technicians are certified. There is also a peer review process. In this process, physicians evaluate other physicians; nurses evaluate other nurses, etc. This evaluation process is usually done in the form of a case review in which physicians and other care providers go over the procedures involved in a particular case. Other considerations involved in maintaining high quality care include how quickly the patient is seen for routine care, how long a patient spends in a waiting room, the convenience of HMO facility locations, and financial stability. E. Preventive Care

Healthier life styles and preventive care maintenance are both crucial parts of a successful managed care plan. To this end, HMOs often offer elaborate health education programs designed to involve all members in their own health care. These classes are designed to prevent illness, promote good health, change unhealthy habits, and help cope with current health problems or injuries. These classes are usually offered at no cost to the member or for a small co-payment. Registered nurses and professional educators generally conduct classes and have a specialty in the area. Attendance at these classes is not required of the members but they are encouraged to attend. The topics of these classes can be anything from allergy treatment, obesity, how to cope with migraine headaches, to nutrition counseling and fitness. Though the points above are admirable objectives, they must still be contained in an insurance policy that meets all the requirements of a legal contract. The phrasing and wording of health insurance contracts can be widely varied. However, we should be aware of some common features. Indeed, health insurance contracts are generally divided into several broad topics or sections. Together, they form the basis for the rights and obligations of both the insured and the insurance company. The law often requires that these insurance policy contracts contain certain provisions. The two most common, yet essential, components of the contract are the insuring clause and the actual face of the policy. It is within these two components that we find the basics of the policy. The insuring clause will contain the following crucial information:

• The identity of the insurer. • The identity of the insured • A general definition of the coverage to be provided in the policy. • The type of loss that is to be covered. • The extent to which the loss is to be compensated. • The statement of the promise to pay benefits subject to all the provisions, exclusions and

conditions of the policy. • A reference to a definition clause for greater detail regarding coverage.

The policy face is simply a standard printed form that provides the following information:

• The name of the insurance company. • A summary of the type of policy contained in the contract. • A summary of the type of coverage contained in the contract. • The name of the insured. • The time that the policy goes into effect. • The time policy expires. • Policy renewal procedures. • A brief statement of type of benefits.

The renewal procedures can vary and they are explained in the renewal provision component of the contract. The renewal provision contains the terms, provisions for renewal of the policy, and must appear on the front page of the policy. There are numerous types of renewal provisions but one may classify them into five categories, which include the following:

• Term: This is a nonrenewable policy and thus no provision is made for renewal. If continued coverage is desired, a new policy must be written and premiums might change at that time.

• Optionally Renewable: This is, by far, the most common of the renewal provisions. The insured has no renewal rights but the insurer may terminate at the anniversary date or, sometimes, at any premium due date.

• Conditionally Renewable: The insured may renew the contract from period to period or continue the contract to a stated age or date. This of course is subject to the insurer’s right to decline renewal under the conditions specified in the contract. Premiums may be increased at the time of renewal.

• Guaranteed Renewable: The insured usually has the right to continue the policy until a specified time as long as premiums are made promptly. The insurer cannot refuse to renew the policy. Premiums may be increased but only for an entire class of those who are insured and not just for an individual.

• Non-cancelable: The insured has the right to continue the contract by timely payment of premiums until a specified age. The insurer cannot refuse to renew the policy. Obviously, premiums will be higher with this type of renewal provision. The premium cannot be increased but the policy may call for a graduated premium schedule.

The reader should now have a solid grasp of those things that characterize managed care as well as an understanding of the accepted definition of the term, managed care. He or she should also have an understanding of the issues regarding control and risk in providing comprehensive managed care. Finally, the reader should be able to distinguish the components of both preventive care and high quality care.

The second module of the Managed Health Care Unit considers the material costs in providing quality managed care. A discussion of the relationship between cost and quality is followed by a brief inquiry into various rating systems. This module will focus on the following aspects of costs and managed care:

• The relationship between profits and providing managed care. • The relationship between profits and premiums • The relationship among profits, premiums and quality managed care.

Cost and Managed Care

Benefits specialists and employers seem to agree that there is a correlation between the degree of managed care and benefit costs. That is to say, the greater the degree of managed care the lower the cost. From highest to lowest with respect to annual benefit costs, benefit plans are usually ranked in the following order:

• Traditional insurance company and Blue Cross and Blue Shield plans without case management.

• Traditional insurance company and Blue Cross and Blue Shield plans with case management.

• PPOs. • Point of service plans. • Independent practice association HMOs. • Closed panel HMOs.

It should be noted that the degree of managed care increases as one goes down the list. Not surprisingly, there also seems to be a high correlation between the level of annual benefit costs and the rate of cost increases. Recently, the cost of traditional benefit plans has been increasing at an annual rate approximately twice the annual increase in the cost of closed panel HMOs. A. Profits and Managed Care Like hospitals, HMOs were originally nonprofit organizations. However, in order to take advantage of better technology and other benefits deriving from the extensive network of medical research, HMOs became for-profit organizations. Some began to offer public stock options and thus became investor-owned. Obviously, investors like to see some profits so HMOs had to make some money in order to keep investors happy and to continue to grow within the rapidly changing health care industry. Originally, HMOs would often affiliate themselves with institutions like nursing homes to help generate income. Today, HMOs have become a lucrative investment and are being bought,

managed and initiated by large international conglomerates. As in any industry, there has been a trend among managed care organizations like HMOs and PPOs to consolidate and specialize. This consolidation and specialization is usually done in terms of population and geographic areas served. Indeed, in order to compete, venerable facilities like hospitals and Blue Cross- and Blue Shield are being forced to involve themselves in the managed health care industry in order to survive. B. Profits and Premiums

Although HMOs try to be reasonable and affordable when determining payments for their members, they must also be substantial enough to keep the HMO financially stable and generate a profit for investors. In attempting to achieve this delicate balance, the industry has developed three rating systems. These rating systems were developed in an attempt to be fair and effective. They are used to determine monthly premiums for services needed in specific areas or to determine services needed by specific populations. In the experience rating system, the members are broken down into groups by sex, employer, age, etc. Then, based on the HMOs past experience with a particular group and how much it costs to cover that group, the different groups are charged accordingly. The prospective rating system bases premium cost for members on unanticipated costs within a sub-group rather than on past experience with that sub-group. This method of rating premiums is becoming more popular. This is because HMOs are increasingly more concerned with the rapidly rising future costs of health care and the potential impact of those costs on the coverage for their members. The community rating system maintains the same premium for everyone enrolled in the network regardless of age, sex, pre-existing condition, or any other factor. Thus, if premium payments change for one group, then they change for all groups within the system. Federally qualified HMOs are required by law to use the community ratings system except when determining premium payments for high-risk groups and private enrollees. Still, the amount charged must be the same for all members of each high-risk group and for all private enrollees. The reader should now have a solid grasp of the complexities involved in the material costs of managed care. He or she should also have a good understanding of various rating systems as they are applied to managed care. Finally, the reader should understand the relationship among profits, premiums, and quality managed care.

The third module of the Managed Health Care Unit considers the purposes of managed health care and the evolution of those purposes. A discussion regarding the historical evolution of the relationship between costs and needs is followed by an inquiry into how both traditional and managed care plans have responded to this evolution. The module will focus on the following aspects of our evolving health care system:

• The relationship between rising health care costs and the evolution of plans. • Historical milestones in the evolution. • The response of traditional plans to rising costs. • The response of managed plans to rising costs.

The Evolution and Purpose of Managed Care In 1929, the Los Angeles Department of Water and Power arranged for two doctors to provide medical care for two thousand of the department's employees and their families. This care was to be provided for a fixed and prepaid amount of money per month. This humble initial arrangement is often considered to be the first managed care system inaugurating the great age of the HMOs. Incidentally, the monthly premium for prepaid health care for the employees and families of the Los Angeles Department of Water and Power was $2. A. Health Care Costs and Managed Care

Until the 1930's, medical expenses were borne primarily by the ill or injured persons or their families. It was not unusual, however, for hospitals and physicians to provide care on a charity basis if the patient lacked the resources to pay. What has been described as the earliest health-insurance plans were in reality disability income coverage. However, at that time, medical costs were relatively low and the continuation of income was often the difference between a person's ability to pay medical bills and the need to rely on charity. It was during the Great Depression that the first organizations designed to provide health care, later called Blue Cross, would be developed. These organizations were originally controlled by hospitals and were designed to provide first dollar coverage for hospital expenses. Then, in the late 1930's, physicians followed the hospitals lead and established Blue Shield plans. Throughout the 1940's, Blue Cross and Blue shield were the predominant providers of medical expense coverage. Noticing the success of Blue Cross, insurance companies entered the market for hospital insurance in the 1930's and added coverage for surgical expenses and physicians' expenses. However, these insurance companies had little success in competing with Blue Cross and Blue Shield until they developed a new product in 1949 called Major Medical Expense Insurance. Thus, by the middle of the 1950's insurance companies surpassed Blue Cross-and Blue Shield in premium volume and number of persons covered. Thanks to a 1949 Supreme Court ruling stating that employee benefits were subject to collective bargaining, the number of persons covered by medical expense insurance plans grew rapidly during the 1950's and 1960's. In addition, during the 1960's the federal and state governments became a serious providers of medical expense coverage by creating health insurance programs for the elderly and the poor. Medicare provided benefits for people age 65 and older. Medicaid provided medical benefits for

certain classes of low-income individuals and families. It is obvious that these two programs provided benefits to large numbers of people who would otherwise not have been able to receive adequate medical care. However, bringing so many people under coverage at the same time created a dramatic shortage of medical facilities and professionals. Demand for medical care increased and thus health care costs increased. In 1950, expenditures for health care equaled 4.4% of Gross Domestic Product and increased to 5.4% in 1960 and 7.3% in 1970. Faced with these exploding costs, larger employers started turning to self-funding of medical expense benefits. Cash flow was improved and savings were created by avoiding state-mandated benefits and state premium taxes. In 1973, the Health Maintenance Organization Act was passed. This legislation was designed to encourage the growth of HMOs by providing funding for their development costs and mandating that certain employers make these plans available to employees. The subsequent growth of HMOs is, no doubt, a result of this legislation. Nevertheless, the cost of medical care continued to expand at an alarming rate. By 1988, expenditures for health care reached 9.2% of Gross Domestic Product. In the 1990s, expenditures for health care are 12.2% of the Gross Domestic Product. Moreover, it is expected that at the end of the decade health care costs for Americans will be 15% of the Gross Domestic Product. One should also keep in mind that about 15% of the American population, (a percentage that includes many employed people and their families), have no insurance. A dramatic change that has taken place in the 1990's must be noted here. In 1980, approximately 90% of all insured workers were covered under traditional medical expense plans, and 5% were covered under HMOs. Traditional means briefly, that if a worker or family member was sick, he or she had complete freedom in choosing a doctor or a hospital. Medical bills were paid by the plan and no attempts were made to control costs or the utilization of services. By the mid 1990's however, close to 75% of employees were enrolled in managed-care plans. Of the remaining 25%, very few are in traditional plans. Between 1970 and the early 1990's, the average annual increase in the cost of medical care was approximately two times the average annual increase in the Consumer Price Index. There is no single reason for this increase but one might look to a combination of the following for an answer:

• There is no incentive for patients and providers of health care to economize on the use of health care service. This is because private health insurers or the government pays a growing portion of the country’s health care expenditures.

• Because many medical expense plans provide first dollar coverage for many health care costs, there is no incentive for patients to avoid the most expensive forms of treatment.

• Current demographics indicate that the population is aging and the incidence of illness increases obviously with age.

• The continuing increase in the number of AIDS cases over the last decade has resulted in increasing costs. It is not unusual for health care costs for an employee with AIDS to exceed $100,000.

• The exciting and invaluable technological advances that have taken place in the last decade, including such things as CAT scans, organ transplants, and fetal monitoring, are expensive. The miraculous does not come cheap and these technological advances can prolong the life of the terminally ill thus increasing medical expenses. The miraculous result of medical research is only limited by the creative imagination of the researchers.

• There is an under capacity of medical facilities. In other words, in the United States, there is an overabundance of hospital beds that are expensive to maintain. There is also a surplus of physicians and an oversupply of physicians will drive up the average costs of medical procedures in order to prevent the physician’s average income from dropping.

• Malpractice suits are on the rise. Care providers are much more likely to be sued than ever before and malpractice awards are several times greater than the general rate of inflation. Therefore, higher malpractice premiums charged by insurance companies are ultimately passed on to consumers. Not surprisingly, also, malpractice suits have resulted in an increase in defensive medical techniques with routine tests likely to be performed more often.

B. Traditional Plans Versus Managed Care Plan

The major difference between traditional medical expense plans and managed care plans is the limitation on the choice of medical care providers to which one has access. This difference, however, can have a profound impact both on medical care costs and the health of an employee. In a traditional medical expense plan predicated on a fee-for-service arrangement, the physician only has a chance to treat a person when he or she is sick. Thus, only when a person is sick can the doctor or the facilities make any money. Thus, the sicker the patient the more money the physicians and the facilities can make. This is because each service is paid for separately. Also, in a traditional medical expense plan insurance companies make no effort to cover services to prevent an employee from becoming ill. Thus, the doctors rarely see anyone who simply is concerned with staying healthy. In a traditional medical expense plan, the emphasis is on healing the sick, not in preventing people from getting sick or encouraging them to stay healthy. Normally, insurance companies will cover more of the cost of care if the patient is hospitalized rather than just coming into the clinic or going to the doctor's office for some preventive care. Therefore, it is cheaper for the patient and easier for the doctor to put the patient in a hospital bed. Obviously, this is an expensive practice and health-insurance premiums will continue to rise in order to cover this practice.

The fourth module of the Managed Health Care Unit considers the types of delivery systems available to managed health care providers. A discussion regarding the purposes of these delivery systems and their congressional context is followed by a detailed inquiry into the distinguishing characteristics of the various delivery systems. The module will focus on the following aspects of managed health care delivery systems:

• Services and characteristics of Health Maintenance Organizations. • Sponsorship of Health Maintenance Organizations. • The types of Health Maintenance Organizations.

Types of Managed Health Care Delivery Systems Managed health care is designed to provide a structured and disciplined framework that provides health care to the consumer in an efficient and timely fashion. It is this efficiency that enables costs to be controlled by eliminating steps and processes that might increase the spending in the health care delivery system. In 1973, the United States Congress passed the Health Maintenance Organization Act. This was done in order to establish some guidelines concerning the operation and maintenance of HMOs and to try to standardize the development of HMOs. This Act also provided funds to research the growth and progress of HMOs and to design ways to improve the HMO delivery system. In 1979, the Health Maintenance Organization Act was amended to include by IPAs, PPOs and other managed care systems.

A. Health Maintenance Organizations

The term HMO is often incorrectly used to refer to any managed-care system. This is unfortunate because the distinctions are important. A health maintenance organization is the most common type of managed care system but even within the HMOs, there are many variations. Although a precise definition is difficult, HMOs are generally regarded as organized systems of health care that provide a comprehensive array of medical services on a prepaid basis to voluntarily enrolled persons living within a specified geographic region. HMOs behave like insurance companies and the Blue Cross and Blue Shield organizations because they too finance health care. However, unlike insurance companies and the Blue Cross and Blue Shield organizations, they also deliver medical services. The challenge for HMOs is to provide quality care within a set budget and yet not minimize the health care provided. This obvious contradiction of purpose is a primary concern of the critics of managed care. However, HMOs approach this dilemma in many valid ways. HMOs often get a discount by contacting with certain hospitals in exchange for a good estimate of patients who will need hospitalization. The concept of a guaranteed patient base assures the hospital, or any other health care facility for that matter, that there will be people seeking care from their facility. Therefore, the hospital can better afford to contract health maintenance organization for reduced rates on health care for its members. No physical examination is required to join under group plans and, HMOs cannot turn down applicants due to a pre-existing condition. The only requirement across the board is access to previous medical records. Once accepted into the plan, all health care is covered as long as the enrollee remains within that plan and its guidelines. Failing to pay monthly premiums will cause the loss of membership in the HMO. However, HMOs do not have the option to not re-enroll a consumer or discontinue coverage if the member does not comply with the plan's rules such as not receiving care within the network or not seeing the primary care provider or even if a member makes an unnecessary amount of trips for care. The following services are covered in some manner through most managed care systems. Indeed, most of these services only require the payment of a small visit fee since the cost of care has already been covered in the monthly premium payment.

• Laboratory diagnostic testing, including X-rays. • Consultation services. • Doctors' visits and hospital care received within the network. • Necessary emergency rooms services. • Maternity care. • Medically necessary surgery. • Mental health services. • Vision and hearing examinations. • Health education programs. • Inpatient hospital care- semiprivate room. • Prescription drugs. • Extended/continuous care facilities. • Reconstructive surgery. • Home health visits.

The following are generally not covered:

• Dental surgery. • Services not recommended or approved by one's primary care provider. • Any experimental care. • Cosmetic/plastic surgery.

As of 1996, there were more than 600 HMOs in existence. During the last decade, the number of persons enrolled in HMOs has more than doubled, but the number of HMOs is down by about 20% because of plan mergers. Today, the 25 largest plans enroll one-third of HMO participants. In addition to this, almost 85% of HMO subscribers are in plans that belong to one of about 50 chains of HMOs. Obviously, the tendency in the industry has been toward growth and consolidation. B. Distinguishing Characteristics of HMOs There are certain characteristics of HMOs that distinguish them from insurance companies and Blue Cross or Blue Shield organizations. A person enrolled in an HMO is offered a comprehensive package of health care services, which usually include benefits for outpatient services as well as for hospitalization. Enrolled members usually get these services at no cost except the periodically required premium. In some cases, there is a small co-payment such as $10 for a visit to the physician or $5-10 for a drug prescription filled. It is preventive care that is emphasized by HMOs and they provide preventive services like routine physicals and immunizations. Insurance companies and Blue Cross and Blue Shield usually do not cover preventive care even when Major Medical Coverage is provided. Another primary concern of HMOs is the control of medical expenses. HMOs try to detect and treat medical problems at an early stage by encouraging and providing preventive care. It is the belief that such preventive care can help to avoid expensive medical treatment later. It is also the objective of HMOs to provide treatment on an outpatient basis when and if possible. Insurance companies and Blue Cross and Blue Shield provide more comprehensive coverage when a person is hospitalized. Therefore, the less expensive outpatient treatments were often not prescribed or performed. Obviously, the emphasis on outpatient treatment and preventive medicine has resulted in a much lower hospitalization rate for HMO enrollees than for the population as a whole. This could be, however, the result of younger and healthier employees electing HMO coverage more often. HMOs use salaried employees that may also result in lower costs because the physician or care provider has no financial incentive to prescribe additional, and possibly unnecessary, treatment. As mentioned earlier, physicians and other medical professionals in some HMOs may receive bonuses if the HMO operates efficiently and has a surplus. Finally, HMOs provide for the delivery of medical services, which in many cases are performed by salaried physicians and other personnel employed by the HMO. This is in stark contrast to the usual fee-for-service delivery system of medical care. However, some HMOs do contract with providers on a fee-for-service basis. People enrolled in an HMO plan are required to obtain their care from providers of medical services who are affiliated with the HMO. HMOs often operate in a specific geographic region not much larger than a single metropolitan area and this requirement then may result in limited coverage for subscribers if they seek treatment elsewhere. Only in the case of medical emergencies do HMOs allow for out of area coverage. Primary care physicians serve as the first line of treatment. They also serve in a control capacity in terms of access to specialists. Only if the primary care physician recommends a specialist will the HMO cover benefits resulting from the service of that specialist. The specialist may be a physician who has contracted with the HMO or he or she may be an employee in a group practice plan. The HMO subscriber has little or no input regarding which specialist is chosen. This has been one of the more controversial aspects of HMO care. It has also been one that has discouraged an even larger enrollment. Many HMOs, responding to these concerns, now make it easier to see a specialist. Nurses in a physician’s office or staff members of the HMO who may be contacted by telephone can sometimes make specialist referrals. Indeed, some HMOs now have direct access or self-referrals, which allow subscribers to see network specialists without

going through the primary care physician. However, the specialist in this case may have to contact the HMO for authorization before proceeding with any tests or treatment. C. HMOs and Sponsors Recently HMOs have begun to operate as for-profit organizations. Though many subscribers are covered by HMOs that are sponsored by consumer groups, an increasing number of subscribers are covered by plans sponsored by the Blue Cross or Blue Shield organizations or insurance companies. Physicians, labor unions, hospitals, or private investors may also be sponsors of HMOs. Physician hospital organizations have recently established HMOs. A physician hospital organization is a legal entity that is formed by one or more physicians groups and hospitals. It contracts, negotiates, and markets the services of the hospitals and the physicians. Physician and hospital organizations may form their own HMOs or they may contract with existing HMOs or other forms of managed care organizations. Physician and hospital organizations may form their own HMOs or they may contract with existing HMOs or other forms of managed care organizations. Insurance companies have finally come to the realization that HMOs are viable alternatives to financing and delivering health care and could thus be offered as one of their products. Indeed, so enthusiastically have insurance companies embraced the idea of HMOs that, in addition to sponsoring and owning HMOs, they are actively involved with HMOs in many ways that include the following:

• Providing administrative services, such as claims monitoring accounting and computer services and actuarial advice.

• Providing emergency out of area coverage. A National Insurance Co. may be better equipped to administer out of area claims than an HMO.

• Consulting in such areas as administration and plan design • Providing hospitalization coverage. HMOs that do not control their own hospital facilities

may provide this benefit by purchasing coverage for their subscribers. • Designing sales literature and other marketing assistance. Indeed, some agents of

insurance companies have been used to market HMOs. This is usually done in conjunction with the marketing of the insurance company's hospitalization plan when the HMO does not provide hospitalization coverage to its subscribers.

• Providing a variety of financial support systems, such as reinsurance, if an HMO experiences greater than expected demand for services or even agreements to bail out financially troubled HMOs.

D. Types of HMOs There are numerous types of HMOs. The first HMO plans are often described as closed panel plans under which subscribers must use physicians employed by the plan or by organizations with which it contracts. In a closed panel plan, there are several general practitioners. Thus, subscribers can usually select their physician from among those general practitioners still accepting new patients. They can then make medical appointments just as if the physician was in private practice. However, there is frequently little choice among specialists because the plan may have a contract with only one physician or a limited number of physicians in a specific area of specialization. Although the number of closed panel plans is relatively small, they account for about 30 percent of all HMO subscribers. Closed panel plans fall into three categories including:

• Group model HMOs. • Network model HMOs. • Staff model HMOs.

More recently, HMOs have been formed which are described as open panel plans and consist of individual practice associations. This is a more flexible concept and subscribers may choose physicians from a broader base of options thus allowing more physicians to participate in the plan. About 40% of HMO subscribers are in an individual practice association. Most of remaining HMOs are mixed model plans.

1) Staff Model HMOs A staff model HMO directly employs the medical staff of nurses, doctors, technicians, secretaries, and administrators. These people are not involved in any other practice outside the HMO network of which they are a part. Ideally, all functions are maintained in an HMO owned and operated health care center or clinic. The staff model HMO is a complete medical center within itself. This HMO owns its own facilities and hires its own physicians. It may even own its own hospitals, laboratories, and pharmacies or it may contract for these services. If it is not large enough to justify hiring its own specialists in a given field, it may also have contracts with specialists in order to treat subscribers. Employees of the staff model HMO are paid a salary and perhaps an incentive bonus. There is a great deal of control over costs in a staff model HMO. This is because it controls the salaries of its physicians, who might find themselves unemployed if the HMO does not make a profit or if they do not provide care within the utilization and cost parameters of the HMO. High startup costs and high fixed costs once they are operating have discouraged the establishment of staff model HMOs despite their potential for huge cost savings. 2) Group Model HMOs

This is the most common type of closed panel plan. In a group model, HMO physicians and other medical personnel are employees of another legal entity that has a contractual relationship with the HMO to provide medical services for its subscribers. This is usually an exclusive arrangement and the provider's physicians only treat subscribers of the HMO. The physicians in a group model HMO generally operate out of one or more common facilities. Under a group model plan, the HMO may contract with a single provider of medical services or with different providers for different types of services. Usually, the group model HMO pays for services on a capitation basis. This means that the provider of services gets a predetermined fee per year for each subscriber and must provide all coverage services for this capitation fee. Conveniently, this fee is independent of how the provider compensates its own employees. The provider thus shares the risk in that it will lose money if utilization is higher than expected or increase its profit if utilization is lower-than-expected. Obviously, the provider has a very real incentive to control costs. 3) Network Model HMOs A network model HMO differs from a group model HMO in that it contracts with two or more independent groups of physicians in order to provide medical services to its subscribers. Physician groups that enter this type of arrangement often treat non-HMO patients on a fee-for-service basis. Because network HMOs are a conglomerate of groups who contract their services their group practices are coordinated by management HMO to provide some organization to the network. A group model HMO is usually geographically centralized but a network HMO may contract outside of the local area. Indeed, a network HMO usually spans several geographic areas and its size alone allows for reaching into other localities and area hospitals. Individual Practice Associations give the physician the best of both managed-care and fee-for-service worlds. The physicians in an Individual Practice Association can keep their current private practice and established patient clientele and they are now guaranteed patients from the IPA/HMO membership. The IPA agrees to handle the physicians billing and provide a network of other associates and referrals upon which the doctors may rely. Members make prepayment premiums to the IPA who will in turn reimburse the doctors for service according to the specifics

of the plan. IPAs are often referred to as open panel plans because subscribers choose from a list of participating physicians. The number of physicians participating in this type of HMO is frequently larger than the number participating in group practice plans and may include several physicians within a given specialty. Most of the newer HMOs are IPAs and the percentage of HMO subscribers served by these plans is growing. IPAs do not usually own their own hospitals but rather contract with local hospitals to provide the necessary services for their subscribers. The doctors are required pay a membership fee to join the IPA and they must agree to abide by the Associations rules and guidelines. They must also pay their own malpractice insurance and maintain their own medical license. Often the requirements include the following:

• The physicians must already have an established practice. • The physicians must agree to a contract for a minimum of one year with the IPA. • The physicians must agree to provide written reason and intent to withdraw.

Because of the guaranteed and stable patient base, many physicians enthusiastically embrace these types of managed care networks. 5) Mixed Model HMOs An increasing number of HMOs are operating as mixed model plans. This means that the organization of the plan is some combination of two or more of the plans previously described. This combination usually evolves as a plan grows. For example, a plan might have been established as a staff model HMO, and later, in order to extend its capacity or geographic region by adding additional physicians becomes an IPA arrangement. Some mixed models have also evolved from the merger of two plans using different organizational forms. E. Preferred Provider Organizations This is a concept that continues to receive a great deal of attention from both employers and insurance companies. A few PPOs have existed on a small scale for many years. However, since the early 1980's, PPOs have grown in number and are being viewed as the new weapon to control increased medical care costs. By 1995, approximately 2500 PPOs were in existence and an estimated 120 million employees and dependents had the option of using them for medical care. The purpose of the PPO is to include the interests of both the physician and the consumer by making them feel comfortable in the system and what it offers to each of them. PPOs are generally sponsored by an insurance company or a hospital or they may even be put together by an employer. PPOs are different from other HMOs because they are not prepaid health plans. Rather, they offer services for members a reduced rate. Although there are many variations, PPOs can be described as groups of health care providers that contract with union trust funds, insurance companies, employers, or third-party administrators to provide medical care services at a reduced fee. They may provide a broad array of medical services. These services include physician services, hospital care, laboratory costs, and home health care. They may be limited only to hospitalization or physician services. Some PPOs are very specialized and provide specific services such as mental health care benefits, substance abuse services, maternity care, dental care, or prescription drugs. A primary difference between PPOs and HMOs is that employees are not required to use the practitioners or facilities of PPOs that contract with their group insurance company or employer. Instead, they can make a choice every time they need medical care. However, lower or reduced deductibles and co-payments as well as increased benefits, such as preventive health care, are offered as incentives for employees to use the PPO. PPOs are not as restricted in policies when it comes to refusing enrollees. They can impose restrictions concerning pre-existing conditions where other HMO plans cannot do that. They may also regulate new members by subjecting them to a waiting period before coverage begins. Both of these options are important in keeping costs low in a health care system. Pre-existing conditions include terminal diseases, mental disorders, and physical handicaps. Many PPOs will not cover these expenses. In 1985, the Preferred Provider Health Care Act was signed which helped PPOs gain more accessibility in health care. A "freedom of choice" clause protects the patients' rights to seek care

outside the plan, yet still maintain some coverage through the PPO. The "any willing provider" clause protects the right of any physician, hospital or health care facility to become PPO affiliated if it meets the requirements and agrees to the terms of PPO regulations. A variation of the preferred provider organization is the exclusive provider organization. The primary difference is that an exclusive provider organization does not provide coverage outside of the preferred provider network. However, in those infrequent instances where the network does not contain an appropriate specialist that specialist will be provided from outside the network. This fact makes the exclusive provider organization very similar to an HMO. PPOs are subject to much less regulation that HMOs. In fact, until recently, they were largely unregulated. However, the NAIC passed the Preferred Provider Arrangements Model Act, which is brief, but at least establishes a minimal regulatory framework. F. Point of Service Plans A new and rapidly expanding type of managed care arrangement is the point of service plan. Estimates suggest that 25 to 30 percent of managed care subscribers be covered under point of service plans. The point of service plan can be defined as a hybrid arrangement that combines aspects of a traditional medical expense plan with that of an HMO or a PPO. In a point of service plan, participants can elect, at the time medical treatment is needed, whether to receive that treatment within the plan's network or outside of the network. Naturally, expenses received outside the network are reimbursed as if the subscriber was covered under a traditional indemnity plan. However, the deductibles and co-payments will be higher than if treatment were chosen within the network. All preventive care must still be received through the network. Physical examinations, immunizations, and other preventive care procedures will not be covered, to any extent, outside the point of service network. Points of service plans accept enrollees with pre-existing conditions but may impose a waiting period for those members before coverage begins. Point of service plans also may put a ceiling on the costs it will cover for the treatment of such pre-existing conditions. Point of service plans may also have stipulations concerning the amount that will be covered outside the network. This is determined by what they consider to be "reasonable costs" for any particular procedure performed by an outside physician or facility. The reader should now have a good understanding of both the purposes and the recent history of Health Maintenance Organizations. He or she should also have a solid grasp of the general services provided by these organizations. Finally, the reader should be familiar with the distinguishing characteristics of the Health Maintenance Organization.

The fifth module of the Managed Health Care Unit considers the variations among plans regarding enrollment and the crucial topic of coverage. A discussion involving enrollment stipulations and the characteristics of coverage contingencies is followed by an overview of the types of coverage and various coverage options. This module will focus on the following aspects of coverage and enrollment in Managed Health Care Plans:

• Enrollment time-lines. • Pre-enrollment information seminars. • The characteristics of a standard managed health care package. • The scope of supplemental coverage.

Enrollment and Coverage Enrollment and coverage can differ among the various managed health-care plans. Questions such as:

• Who is covered? • When are they covered? • How much is covered?

are pivotal in selecting a managed health-care plan. A. Enrollment Employees are usually accepted immediately and with few questions. Employers are required to conduct an open enrollment every year or every other year, during which employees may explore other health benefits options and switch their coverage without penalty or added costs. The open enrollment generally lasts one month and the employer will provide information about different health care packages that they are offering as benefits. Employees are encouraged to attend seminars and meetings conducted by representatives from each health plan. They are encouraged to read up on all the information presented to them even if they do not feel they want to change their benefit health plan. The level of coverage may also be changed during this period. Indeed, the employees may also switch to a different branch of the HMO in which they are currently enrolled. They may want to do this if they have moved since they originally enrolled, or if they are unhappy with the health facility, they had originally chosen. Primary care providers may be changed at any time and there is no need to wait until open enrollment to do so. No physical examination is required to join an HMO through an employer. The HMO, however, must be informed of pre-existing conditions and treatments through the past medical history that is usually provided upon enrollment. However, the HMO cannot deny coverage because of the pre-existing condition. Many employers will pay part or all of the premium for the health plan as an incentive for employees to join the managed care plan. B. Coverage

A standard managed health care package usually includes the following:

• Surgery: any surgical services deemed medically necessary. This excludes cosmetic surgery unless it is designed to fix birth defects or disfigurement from illness or injury

• Physician services: this includes any medical, surgical, specialty or consultative services including stitches, setting fractures, removing warts, applying dressings and bandages, splints, casts and collars.

• Anesthesia: during surgery is comprehensive. • Hospital services: both outpatient and inpatient. Inpatient includes a semi private room

and board. Outpatient includes physical therapy consultation and recovery checkups. • Emergency services: the emergency room must be part of the network. • Laboratory Services: blood sugar tests, cholesterol tests, urinalysis, blood counts,

cancer screening, breeding tests, X-rays, tuberculosis screenings. • Outpatient chemical dependency services • Maternity care: including prenatal, delivery services, caesarian section if necessary,

hospital stay, post delivery care. The baby is immediately covered under the plan including coverage for birth defects.

• Mental health services: outpatient.

Some plans offer supplemental coverage. They are included in some plans but not others and many of these supplemental services may be provided at extra cost through higher monthly premium payments. These options include but are not limited to the following:

• Eye exams for adults

• Prescription medication • Dental care • Allergy injections • Prescription glasses • Skilled nursing facilities • Extended care facilities • Home health care • Inpatient psychiatric care • Long-term rehabilitation • Inpatient chemical dependency • Ambulance services • Home visit nurse services • Medical equipment coverage

Chiropractor visits are most often not covered. Physicians rarely refer a patient to a chiropractor but instead send a member to someone in orthopedics or a physical therapist to receive care. Some HMOs however are beginning to affiliate a chiropractor in their benefits option but chiropractic medicine is still viewed with skepticism by the conservative medical establishment. Health Insurance contracts vary widely. Most insurance companies write more than a dozen basic policies. Several riders (optional clauses) may enhance these policies. Therefore, the number of possible combinations is formidable. The most commonly used eight contracts, or combinations of contracts, are the following:

• Aleatory Contract: In this contract, one party may give more than another may. There is no mutual exchange of monetary value.

• Participating Contract: a contract on which a portion of the overcharge of premiums is paid back to the policyholder. This is like a dividend but since it is a return of a portion of the premium, it is not subject to taxation.

• Unilateral Contract: as the phrase implies, this is a contract that can only be enforced against one party.

• Valued Contract: this contract specifies the predetermined amount due the beneficiary or insured in case of loss. This contract does not try to indemnify the insured for the actual dollar amount of the incurred loss.

• Indemnity Contract: this contract reimburses the insured for the actual amount of the incurred loss.

• Non-participating Contract: this contract costs less per thousand dollars than a participating contract. No dividends are paid.

The provisions of the Uniform Policy Provisions Law regulate the above insurance contracts. This law was developed by the National Association of Insurance Commissioners. Twelve mandatory provisions are included in this law and they must be a part of individual health insurance policies. There are also eleven optional provisions that are not required to be included in the policies. However, if the subject matter of any of these eleven is contained in the policy, the policy must be phrased in a manner that is in accord with the appropriate optional provision. An insurer may alter or revoke any of the mandatory or optional provisions. However, the alterations or revocations must not be less favorable to the insured or beneficiary than the original policy. Mandatory provisions are usually referred to as “Required Provisions” or “General Provisions.” The twelve mandatory provisions consist of the following:

• Reasonable Notice of Loss Provision: the policyholder or insured must give the insurance company or agent written notice of a claim within twenty days of the loss or as soon as is reasonably possible. Notice to the insurer or its agent with enough information to identify the insured shall be sufficient. In the case of disability benefits payable for at

least two years, notice of the continuation of disability is required at a minimum of six months. This of course is waived in the absence of legal capability.

• The Time Limit in Certain Defenses Provision: is designed to limit the period of time in which an insurer may challenge the contract or deny a claim or grounds of material misrepresentation in the application.

• The Reinstatement Provision: provides for putting a policy back in force that has lapsed for non-payment of premiums. This provision states that if a policy lapses and an application for reinstatement is not required, acceptance of the overdue premium by the insurer will reinstate the policy. If an application is required, and if a conditional receipt is issued, reinstatement is effective as of the date the application is approved, within forty-five days, unless the insurer has previously notified the insured in writing of its disapproval. A reinstatement policy covers only injuries occurring after reinstatement and illness that begins ten days after the date of reinstatement. The reinstatement provision cannot be applied retroactively for more than sixty days before the date of reinstatement. An exception can be made in the case of policies guaranteed renewable to at least the age of fifty or for at least five years after the age of forty-four.

• The Time of Payment Claims Provision: requires that claims will be paid immediately upon receipt of proof of loss. Periodic payments, however, are to be made as specified in the policy or at least monthly. Balances unpaid when the claim terminates shall be paid immediately upon receipt of due proof of loss.

• The Claims Forms Provision: requires the insurer to furnish claim forms within fifteen days of being notified of the claim. If the forms are not furnished, then the insured will be deemed to have complied with the requirements of filing proof of loss upon submitting written proof of the occurrence, character and extent of the loss.

• The Grace Period Provision: allows a policyholder a grace period of seven days for weekly premium policies, ten days for monthly premium policies and thirty days for all other policies. During the grace period, the policyholder may pay the premium and thus keep the policy in force. If the policy contains a cancellation provision, a reference to the cancellation provision may be made in the grace period provision. If a policy provides that the insurer reserves the right to refuse renewal of a policy, then an additional provision allows the insurer to avoid the grace period provision by giving notice of its’ intent not to renew.

• The Proof of Loss Provision: limits the time within which the insured may file a written proof of loss. Proof of loss must be filed within ninety days of loss. In the case of continuing loss, the proof must be filed within ninety days after the end of a period for which the insurer is liable. If the insured cannot comply with these requirements, then proof of loss must be filed within a reasonable time not to exceed one year. In the event of legal incapacity, there is no time limit on filing a proof of loss.

• The Entire Contract Provision: states that the policy, or the policy plus the application shall constitute the entire contract. Neither the insured nor the insurer may add to or subtract from the contract without the approval of both the insured and the insurer.

• The Legal Actions Provision: restricts the time period during which the insured may bring a legal action against his or her own insurance company. This provision requires that no legal action to collect may be started sooner than sixth days after the proof of loss is filed. This is done to allow the insurer to evaluate the claim. The insurer may also not be sued later than three years after the time the proof of loss is required to be filed.

• The Payment of Claims Provision: specifies that death benefits will be paid to any named beneficiary, but if none is named, the benefits will be paid to the estate of the insured. All other benefits are paid to the insured. Insurers may ad either or both of two optional provisions. The first optional provision that may be added provides that if no beneficiary is named or if the named beneficiary is legally incapable of signing a valid release, the insurer may pay an amount specified in the provision not to exceed one thousand dollars to any relative by blood or marriage of the insured or to the beneficiary who is deemed by the insurer to be equitably entitled thereto. This is often called a facility of payment clause. The second optional provision gives the insurer the option of making payments for medical, surgical and nursing expenses directly to the person or institution rendering the care or services.

• The Change of Beneficiary Provision: if an individual health insurance policy provides a death benefit then it must contain this provision. This provision gives the insured the right to change beneficiaries, or make any other change, without the consent of the beneficiaries. This provision is negated if the insured has made an irrevocable designation of a beneficiary. An assignment provision allows the insured to transfer the benefits provided by the policy. For instance, an injured or sick person might assign his or her medical benefits to his or her doctor in order to pay for his or her care.

• The Physical Examination and Autopsy Provision: allows the insurer, at it’s’ own expense, to examine the person of the insured while a claim is pending. In the event of death, the insurer may have an autopsy performed at its’ own expense if that procedure is not prohibited by local law.

The Uniform Policy Provision Law also describes eleven other provisions. These provisions, however, are not required. They are most commonly referred to as optional provisions. They are included in the policy only when the subject of any of them is part of the policy. That part of the policy, then, must be phrased according to the specifications found in the Uniform Policy Provision Law regarding optional provisions. The eleven optional provisions consist of the following:

• The Misstatement of Age Provision: applies when the applicant misstates his or her age. Coverage and benefits may be adjusted to the level of the correct age.

• The Insurance with Others Insurers Provision: states that if the insured has other policies providing coverage on an expense-incurred or service-incurred basis, and if the insurer had no notice of the other policies, the liability under the policy will be limited to a proportion of the total loss suffered by the insured. This proportion is determined by dividing the sum of the amount payable under the policy with this provision and the amount of valid coverage that the insurer had notice of by the total amount payable under all valid coverage.

• The Relations of Earnings to Insurance Provision: concerns itself with over-insurance for disability benefits. This provision attempts to guarantee that an insured will not receive more money from disability insurance than he or she would receive from working. This situation can occur when the insured has more than one disability income policy. This provision may only be used in non-cancelable and guaranteed renewable contracts. The provision states that if at the time the disability begins the insured’s total disability income exceeds his or her income or average earned income for the preceding two years, the disability income benefits will be reduced proportionately. Premiums for the excess coverage are to be returned to the insured.

• The Cancellation Provision: allows the insurer to cancel the policy on five days written notice. Any unearned premiums are refunded on a pro rata basis. After the initial policy term, the insured may cancel at any time by written notice delivered or mailed to the insurer. Cancellation is effective upon receipt of notice or upon such date as specified in the notice. A refund is computed on a short rate basis. Cancellation does not affect claims originating before the effective date of cancellation.

• The Illegal Occupation or Felony Provision: allows the insurer to deny liability if the insured’s loss results from committing or attempting to commit a felony.

• The Occupation of the Insured Provision: This provision is obviously especially important to accident insurance writing. It states that if the insured is injured or contracts an illness after having changed his or her occupation, or while doing for compensation anything pertaining to a more hazardous occupation, benefits will be reduced to an amount that the premium would have purchased for the insured while engaged in the hazardous occupation. If the insured changes jobs and that change results in a less hazardous occupation, then he or she may apply for a rate reduction.

• Over-Insurance Provision: was created to limit the problems of over-insurance by putting a limit on the amount of insurance that an insured can have with one insurance company. This provision is usually found in policies sold without individual underwriting. There are two versions of this provision. The first version provides that any amount of insurance in excess of a stated amount will be void and that all premiums for the excess of insurance will be refunded to the insured or to his or her estate. The second version provides that insurance on the insured under a like policy or policies will be limited to the one such policy the insured (or the insured’s beneficiary or estate) may elect. The premiums for the other policies will be refunded.

• The Direct Pay Provision: this provision regulates all payments not made on an expense incurred or service incurred basis. An example of a direct pay benefit regulated under this provision would be disability income benefits.

• The Deduction of Unpaid Premiums Provision: allows deduction of unpaid premiums from claim payments. Upon the payment of a claim, any premium then due yet unpaid may be deducted from claim payments.

• The State Law Provision: amends the policy to conform to the minimum requirements of all applicable state laws.

• The “Under the Influence” Provision: states that the insurer is not liable for any loss resulting from the insured being intoxicated or under the influence of a narcotic unless that narcotic was prescribed by a physician.

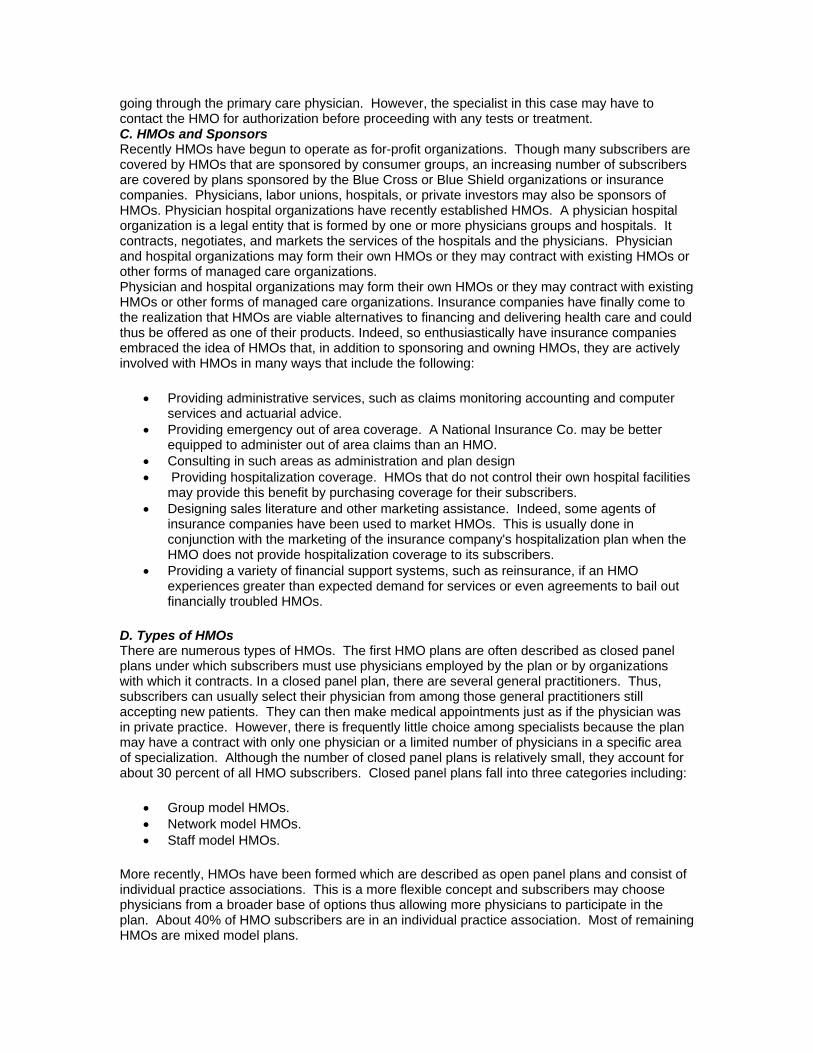

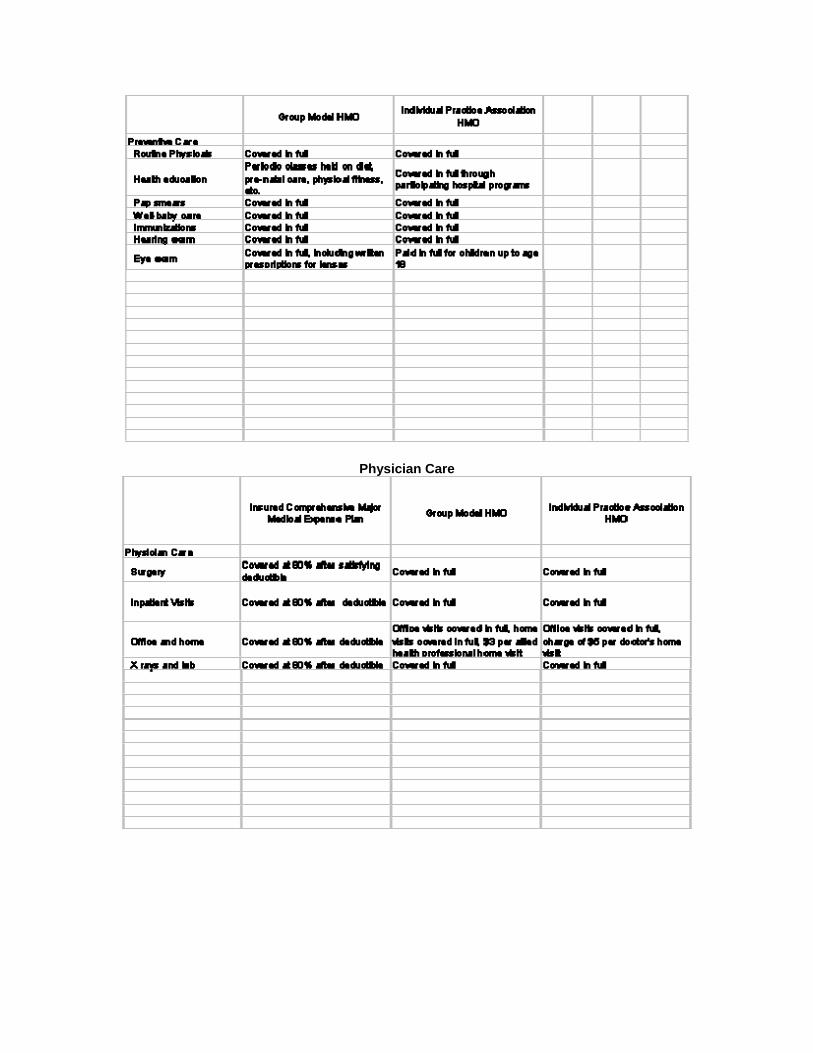

The reader should now have a solid grasp of the mechanics of enrollment. He or she should also understand the characteristics of a standard managed health care package. The following tables describe likenesses and differences in coverage across insured comprehensive medical expense plans, group model HMOs, and individual practice HMOs. By examining these tables, you will find that many of the concepts presented in previous modules become clearer. You will also find that there are serious financial implications for individuals and companies. By having an awareness of these implications, you will be better able to advice your own customers concerning the best choices for their specific circumstances. The tables compare managed health care basics, preventive care, physician care, hospital services, outpatient care and specialized care.

Managed Health Care Basics

Preventive Care

Physician Care

Hospital Services

Outpatient Services

Specialized Care

The sixth module of the Managed Health Care Unit considers the recent shifts and changes in the managed health care industry. A discussion regarding the latest issues surrounding accreditation is followed by a look at some of the ways recent legislation has responded to those issues. This module will focus on the following aspects of managed health care:

• Accreditation standards. • Accreditation organizations. • Federal and state legislation.

Recent development in Managed Health Care The quality of care provided by managed care organizations has recently revolved around two developments. The first is the increased interest in accreditation. The second is the introduction of the passage of laws in many states designed to solve consumer and provider concerns about quality of care, access to care, and choice. A. Accreditation As managed care has evolved, there has been an increasing awareness by some regarding quality. This has led many employers to require that managed care organizations meet some type of accreditation standards. The National Committee for Quality Assurance is the leading organization for accrediting managed care organizations. The NCQA is a non-profit independent organization that was established in 1990. It evaluates six areas of managed care performance, which includes the following:

• Physician's credentials. • Members rights and responsibilities. • Quality improvement. • Utilization management. • Preventive health services. • Medical records.

It has also developed a set a performance measures to serve employers as purchasers of managed care services. These measures are known as the Health Plan Employer Data and Information Set consisting of seventy-five measures that fall into eight categories including the following:

• Effectiveness of care. • Descriptive information. • Member satisfaction. • Access to and availability of care. • Health plan stability. • Cost of care. • Informed health care choice. • Use of services.

Just as there is competition in everything, there is competition among accreditation entities. The Joint Commission on Accreditation of Healthcare Organizations is a competing source of accreditation as is the American Accreditation Health Care Commission, Inc. B. Recent Legislation

The introduction and passage of several types of legislation by state legislatures as well as the federal government has been the result of the following recent issues in managed health care:

• Growth in enrollment in managed care organizations. • Consumer and provider backlash. • Intense competition to control costs within the managed-care industry.

1) Postpartum Stays Half the states have passed legislation providing minimum stays of at least 48 hours for mothers and newborns following delivery. The federal government has passed similar legislation. 2) No Gag Rules Several states have passed legislation preventing managed-care organizations from including provisions in their contracts that prevent doctors from discussing with patients' treatment options that may not be covered under their health plans. Legislation has also been passed that prevents managed care organizations from including provisions in their contracts that prevent doctors from referring very ill patients for specialized care by providers outside the plan. 3) "Any Willing Provider" Laws There has been some concern, particularly by physicians, that managed care organizations exclude or expel doctors for providing care or tests that the doctor, but not the managed-care organization, feels is necessary. In response to this, several states have passed "any willing provider" laws that require HMOs to accept any provider who is willing to accept the plan's basic terms and fees. In effect, this legislation eliminates quality guidelines as the sole source for recruiting providers. Some extreme responses estimate that this type of legislation could result in an increase of 15 to 30 per cent in managed care premiums. 4) Emergency Care Managed care organizations have been criticized for generally refusing to pay for emergency room care, claiming that emergency room treatment was unnecessary. Several states now require a plan to pay emergency room charges whenever a prudent layperson considers a situation to be an emergency. In addition, care cannot be delayed to get plan authorization for treatment. It is obvious that managed care has evolved into an institution of tremendous importance and size. As such, it will continue to generate both controversy and care far into the future. The reader should now have a familiarity with the recent issues in the managed health care field. He or she should also now understand the evolving standards of accreditation and the legislative responses to those evolving standards. Finally, the reader should have a solid grasp of the nature of the organizations involved in the accreditation process.

Fundamentals of Managed Care

Table of Contents

1. Definitions and Characteristics of Managed Care

A. Risk Sharing

B. The Control of Access to Providers

C. Comprehensive Case Management

D. High-Quality Care

E. Preventive Care

2. Costs and Managed Care

A. Profits and Managed Care

B. Profits and Premiums

3. The Evolution and Purpose of Managed Care

A. Health Care Costs and Managed Care

B. Traditional Plans versus Managed Care Plan

4. Types of Managed Health Care Delivery Systems

A. Health Maintenance Organizations

B. Distinguishing Characteristics of HMOs

C. HMOs and Sponsors

D. Types of HMOs

(1.) Staff Model HMOs

(2.) Group Model HMOs

(3.) Network Model HMOs

(4.) Individual Practice Associations

(5.) Mixed Model HMOs

E. Preferred Provider Organizations

F. Point of Service Plans

5. Enrollment and Coverage

A. Enrollment

B. Coverage

6. Recent Developments

A. Accreditation

B. Recent Legislation

(1.) Postpartum Stays

(2.) No Gag Rules

(3.) "Any Willing Provider" Laws

(4.) Emergency Care