Embed Size (px)

Citation preview

1. Official Brazilian government data released on 7 March confirmed Brazil’s longest and

deepest recession in documented history. The 3.6% GDP contraction added to an accumulated

loss of 7.2% in the 2015-2016 period and an almost 9% hit in GDP per capita. Whilst results for

Q4 were slightly worse than expected (0.9% contraction), the full year negative result was

mostly expected and the majority of analysts have not altered their forecasts for this year

(average predictions 0.5% growth in 2017).

2. 2016 sector data portrays widespread recession, as expected. On the supply side, agricultural

sector performance was hit hard by both the domestic crisis and an unprecedented bad crop

season, which culminated in a 6.6% decline. Industry shrank 3.8%, showing a slight

improvement from the 6.6% contraction registered last year. Finally, the service sector

(responsible for more than 60% of the country’s GDP) faced the same fall as 2015, contracting

by 2.7%. On the demand side, private consumption suffered a 4.2% loss in 2016, while

investment fell 10.2%.

3. But we can finally see a light at the end of the tunnel. Despite the important negative

carryover effect (-1.1%), which leads most forecasts for 2017 (including the IMF) to not

overcome the 0.5% barrier, activity is expected to gradually pick up by 1Q201. The first results

for 2017 confirm this cautious recovery. January showed industrial production achieving the

first positive variation in year-over-year terms (+1.4%) after 34 consecutive declines; February

registered a record trade surplus, with increase in both imports and exports (11.4% for the first

and 22.4% for the latter). Finally, after a painful 22 months of continuous job depletion,

February also brought good news on the employment front: a positive result of 35,000 new job

- despite the seasonally adjusted numbers showing a slightly worse picture.

4. Upgrade by Moody’s and success in government’s first concession reflect change in risk

perception. As 2016 GDP results were released last week, the government’s counter-attack

strategy was to announce some good news: a £10bn infrastructure concession plan that would

create 200,000 direct and indirect jobs. Although part of this relates to old projects being “re

launched”, the first bidding for airport was considered a success: no companies involved in Lava

Jato, three foreign firms and a total of £1bn in expected investments. According to Temer, the

successful round showed that Brazil has regained credibility on the international front.

5. Surfing on the same positive wave, international media expresses excitement. An article

published on 9 March by the Economist (read full article here) portrays a generous picture of

President Temer, praising his efforts with the expected economic and fiscal reforms despite

highlights on impeachment and strong unpopularity. A week later, Brazil’s flag featured as one

“balloon countries going up” on the cover of same magazine, while Financial Times1 highlighted

Brazil’s Central Bank’s chief optimism at the G20 meeting, confirming that “this will be the year

of recovery”. Temer again celebrated the resumption of Brazil’s credibility with international

markets.

1 Read full article here.

BRAZIL ECONOMIC FOCUS: March 2017

There’s light at the end of the tunnel – but don’t lose your flashlight just yet

Social Security Reform Proposal:

On 6th

December, President Temer and his economic team

presented Congress the long awaited Social Security Reform

proposal.

Key points proposed:

(i) convergence of rules for retirement and benefits for public, private urban and rural sector workers; - This includes parliamentarians; however,

their transition into the new system is yet to be defined. Congress may change the proposal and try to exclude themselves from the new rules.

(ii) imposition of a minimum age for retirement for both men and women – 65 years;

(iii) preserving the proportionality of the benefit to the period of contribution – minimum of 49 years of contribution required for having the right to receive the full amount;

(iv) stricter rules for the benefits for the surviving partner;

(v) Transition rules valid only for men above 50 and women above 45, which suggests that in a matter of little more than a decade the vast majority of new retirees will abide by the new rules.

Forecasts: (i) Government calculates the change will save £161bn in

public spending between 2018 and 2027 (if proposal is approved in totality).

Reforming Brazil’s social security system is urgent and long overdue. Social security accounts for more than 40% of government’s primary spending and is not included in nominal expenditure cap proposal. Its deficit should reach £28bn by the end of 2016 (4% GDP) and spending could reach 20% of GDP in 2020 if the current system is maintained. Therefore, sending this proposal was an important move by Temer’s government, and its approval will represent the second (and also crucial) step into resuming fiscal sustainability.

6. Nonetheless, relevant risks shouldn’t be underestimated. Gradual recovery of macroeconomic

indicators and positive expectations from international and domestic financial markets highly

contrast with “real life” in Brazil. Lagging indicators such as unemployment (12.6%), real

interest rates (7.15%) and household debt (declining but yet high at 42.2%) still hurt the

majority of the population. Not surprisingly,

ordinary people don’t share the enthusiasm of

financial markets.

7. Surprises are no strangers to Brazil’s

unpredictable political scene, as reflected by

the recent meat scandal. On March 17 Brazilian

Federal Police launched an investigation into the

packaging of rotten meat by food giants such as

JBS and the bribery of Ministry of Agriculture

officials. Brazil’s meat exports have in one week

come to a near halt, falling to US$74,000 from a

daily average of US$63 million as of 21 March.

Agriculture Minister Blairo Maggi says the

scandal could reduce Brazil’s exports by

US$1.5bn this year. Nonetheless, the overall

impact of the scandal on Brazil’s growth should

be limited. Unfortunately, the same can’t be

said to the country’s image.

8. And sustainable growth recovery

remains contingent on the government’s ability

in passing major structure reforms. These

include the tax system and a new fiscal regime

for indebted states. The tax reform aims at

improving the business environment by

untangling the Brazilian tax system, including

implementing proposals such as the VAT (Value-

Added Tax). For the indebted state governments, Temer’s economic team suggests suspending

payments to the federal government for up to three years in exchange for the adoption of strict

fiscal measures such as privatisation of state companies and increasing civil servants’

contributions to the pensions. However, despite long lasting negotiations, no agreement has

yet been reached.

9. Which won’t be an easy task. After easily approving the expenditure ceiling cap, social security

reform will be the first hard test, as flagged by the widespread public demonstrations that

featured the country’s main capitals last week. At the same time, failure in approving the long

overdue restructuring of Brazil’s social security system (or approving it with many alterations)

will harm fiscal consolidation and most likely affect improving leading indicators such as

investor and business confidence, dragging growth expectations for this year (see box on the

left).

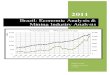

Monthly Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16 Dec-16 Jan-17 Feb-17

Inflation (12 mth.

accum.)10.36 9.39 9.28 9.32 8.84 8.74 8.97 8.48 7.87 6.99 6.29 5.35 4.76

Benchmark Interest

Rate14.25 14.25 14.25 14.25 14.25 14.25 14.25 14.25 14.00 13.75 13.75 13.00 12.25

Unemployment (%) 10.2 10.9 11.2 11.2 11. 3 11.6 11.8 11.8 11.8 11.9 12.0 12.6 n/a

Exchange Rate end of

period (BRL/USD)3.98 3.56 3.45 3.60 3.21 3.24 3.24 3.25 3.18 3.40 3.26 3.12 3.09

Trade Balance (US$

bn.)3 4.4 4.9 6.4 4 4.6 4.1 3.8 2.4 4.7 4.4 2.7 4.6

Exports (US$ bn.) 13.4 16 15.4 17.6 16.7 16.3 17 15.8 13.7 16.2 15.9 14.9 15.5

Imports (US$ bn.) 10.3 11.6 10.5 11.1 13.8 11.8 12.9 12 11.4 11.5 11.5 12.2 10.9

FDI (US$ mi) 5920.4 5557.4 6820.4 6145.5 3917.4 208.3 7207.7 5273.6 8399.6 8592.9 15409.5 11528 n/a

UK exports (US$ mi) 238.8 174.3 248.7 190.3 190.7 169.6 204 225.4 182.5 150.9 175.8 127.7 127.9

UK imports (US$ mi) 254.1 236.3 203.8 256.1 235.3 202.6 278.6 284.6 294 245.3 189.5 223.1 161.5

Quarterly 2016 Q1 Q2 Q3 Q4

GDP (% var. QoQ) -0.3 -0.6 -0.8 -0.9

Key Macroeconomic Indicators