Embed Size (px)

Citation preview

LIVE WEBCASTUPDATE ON BEPS PROJECT

2015 DELIVERABLES AND BEYOND

15 December 20143:00pm – 4:00pm (CET)

Pascal Saint-Amans

Director, Centre for Tax Policy and Administration

Raffaele Russo

Head of BEPS Project

Achim Pross

Head of International Cooperation and Tax Administration Division

Marlies de Ruiter

Head of Tax Treaty, Transfer Pricing and Financial Transactions

2

Speakers

Ask questions and comment throughout the webcast

3

Join the discussion

Directly: Enter your question in the space provided

Via email: [email protected]

Via Twitter: Follow us on @OECDlive using #BEPS

2014 DELIVERABLES

PRESENTED TO THE

G20 FINANCE MINISTERS

AND LEADERS

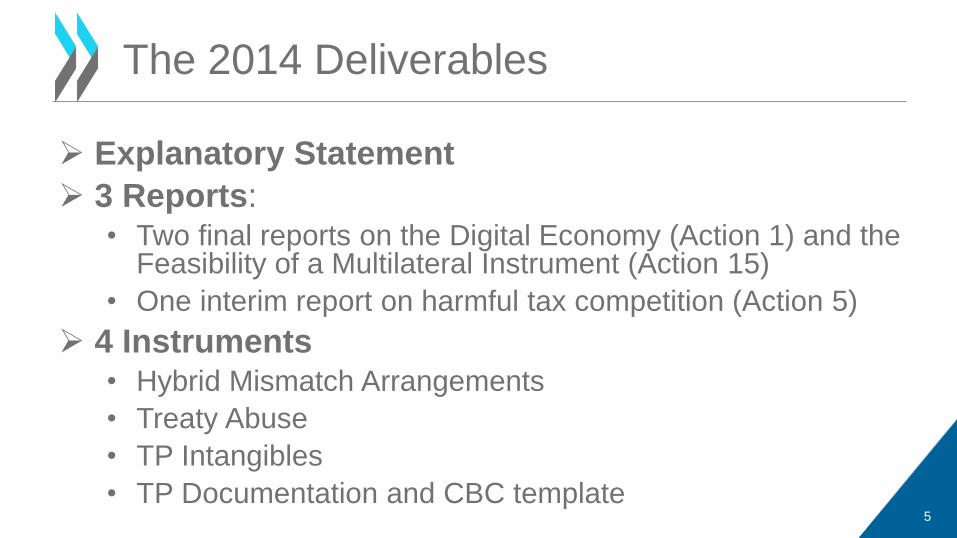

Explanatory Statement

3 Reports:• Two final reports on the Digital Economy (Action 1) and the

Feasibility of a Multilateral Instrument (Action 15)

• One interim report on harmful tax competition (Action 5)

4 Instruments• Hybrid Mismatch Arrangements

• Treaty Abuse

• TP Intangibles

• TP Documentation and CBC template 5

The 2014 Deliverables

Communiqué Meeting of G20 Finance Ministers and Central Bank Governors

Cairns, 20-21 September 2014

[…] Today, we welcome the significant progress achieved towards the completion of our two-year

G20/OECD Base Erosion and Profit Shifting (BEPS) Action Plan and commit to finalising all action

items in 2015. We are deepening developing country engagement in tackling BEPS issues and

ensuring that their concerns are addressed.

G20 Leaders’ Communiqué Brisbane Summit, 15-16 November 2014

[…] We welcome the significant progress on the G20/OECD Base Erosion and Profit Shifting

(BEPS) Action Plan to modernise international tax rules. We are committed to finalising this work

in 2015, including transparency of taxpayer-specific rulings found to constitute harmful tax

practices. We welcome progress being made on taxation of patent boxes. We welcome deeper

engagement of developing countries in the BEPS project to address their concerns.

6

G20 Reactions

STRENGTHENING THE

ENGAGEMENT WITH

DEVELOPING COUNTRIES

New structured

dialogue process

8

Developing countries

participating in the BEPS Project:

Albania, Bangladesh, Jamaica, Kenya,

Morocco, Nigeria, Peru, Philippines,

Senegal, Tunisia, plus CIAT (Inter-

American Center of Tax

Administrations) and ATAF (African

Tax Administration Forum)

• Asia: Seoul, 12-13 February 2015

• Francophone countries: Gabon,

23 February 2015, with CREDAF

• LAC: Lima, 26-27 February 2015,

with CIAT

• Eurasia: March 2015 TBC

• Africa: March 2015 TBC, with

ATAF

To be developed by OECD, IMF, UN, WBG and regional

organisations on:

• Tax incentives

• Comparables

• Indirect transfers of assets

• Transfer Pricing documentation requirement

• Strengthen capacity development on treaty

negotiation

• Base eroding payments between MNEs

affiliates

• Artificial profit shifting through supply chain

restructuring

• Successful implementation of assessment of

BEPS risks

1. Direct participation in the Committee on Fiscal Affairs and its subsidiary

bodies

2. Regional Networks of tax policy and

administration officials

3. Capacity building support

FOLLOW-UP WORK ON

THE 2014 DELIVERABLES

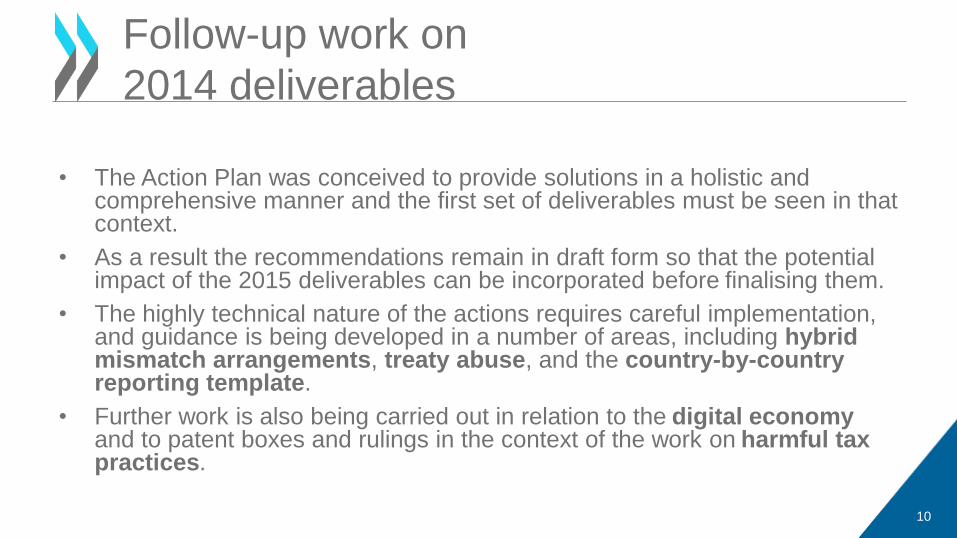

• The Action Plan was conceived to provide solutions in a holistic and comprehensive manner and the first set of deliverables must be seen in that context.

• As a result the recommendations remain in draft form so that the potential impact of the 2015 deliverables can be incorporated before finalising them.

• The highly technical nature of the actions requires careful implementation, and guidance is being developed in a number of areas, including hybrid mismatch arrangements, treaty abuse, and the country-by-country reporting template.

• Further work is also being carried out in relation to the digital economy and to patent boxes and rulings in the context of the work on harmful tax practices.

10

Follow-up work on

2014 deliverables

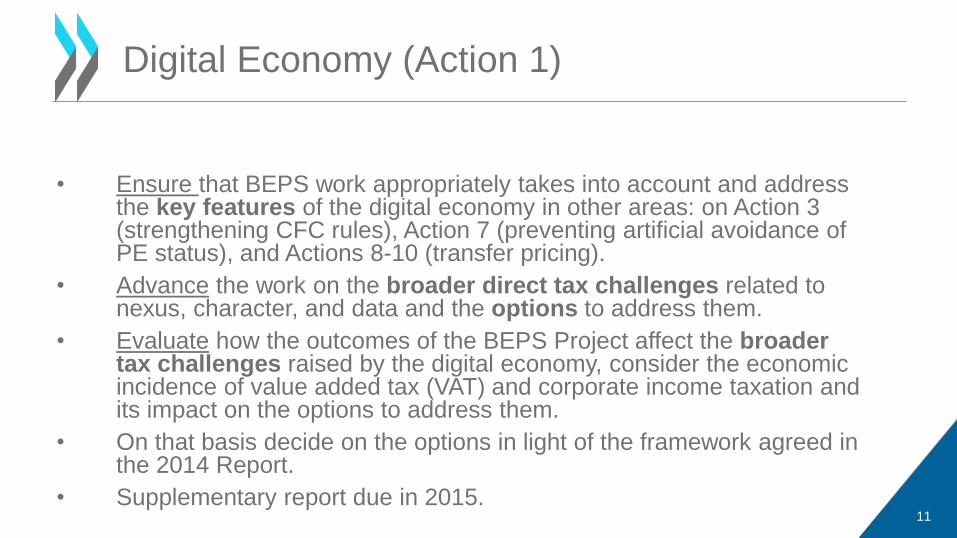

• Ensure that BEPS work appropriately takes into account and address the key features of the digital economy in other areas: on Action 3 (strengthening CFC rules), Action 7 (preventing artificial avoidance of PE status), and Actions 8-10 (transfer pricing).

• Advance the work on the broader direct tax challenges related to nexus, character, and data and the options to address them.

• Evaluate how the outcomes of the BEPS Project affect the broader tax challenges raised by the digital economy, consider the economic incidence of value added tax (VAT) and corporate income taxation and its impact on the options to address them.

• On that basis decide on the options in light of the framework agreed in the 2014 Report.

• Supplementary report due in 2015. 11

Digital Economy (Action 1)

12

Hybrid Mismatch

Arrangements (Action 2)

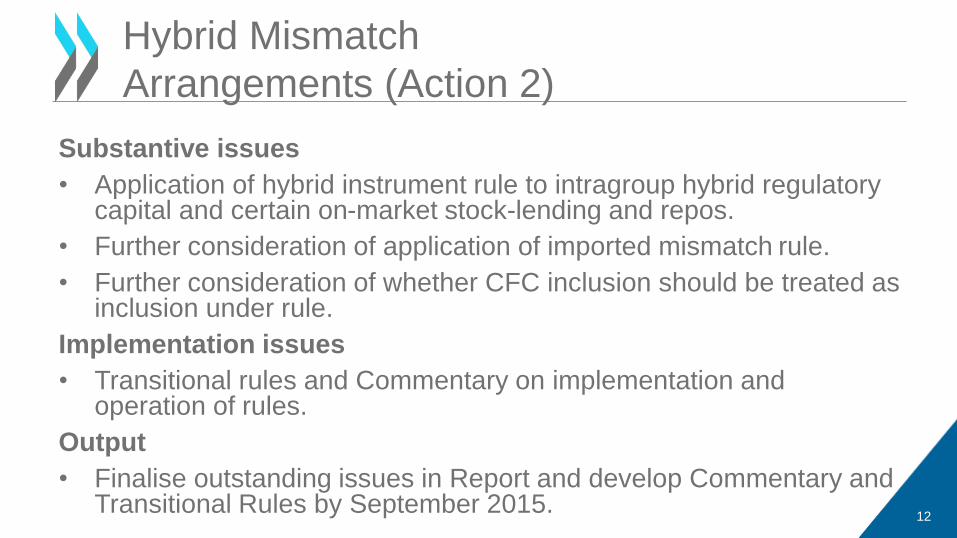

Substantive issues

• Application of hybrid instrument rule to intragroup hybrid regulatory capital and certain on-market stock-lending and repos.

• Further consideration of application of imported mismatch rule.

• Further consideration of whether CFC inclusion should be treated as inclusion under rule.

Implementation issues

• Transitional rules and Commentary on implementation and operation of rules.

Output

• Finalise outstanding issues in Report and develop Commentary and Transitional Rules by September 2015.

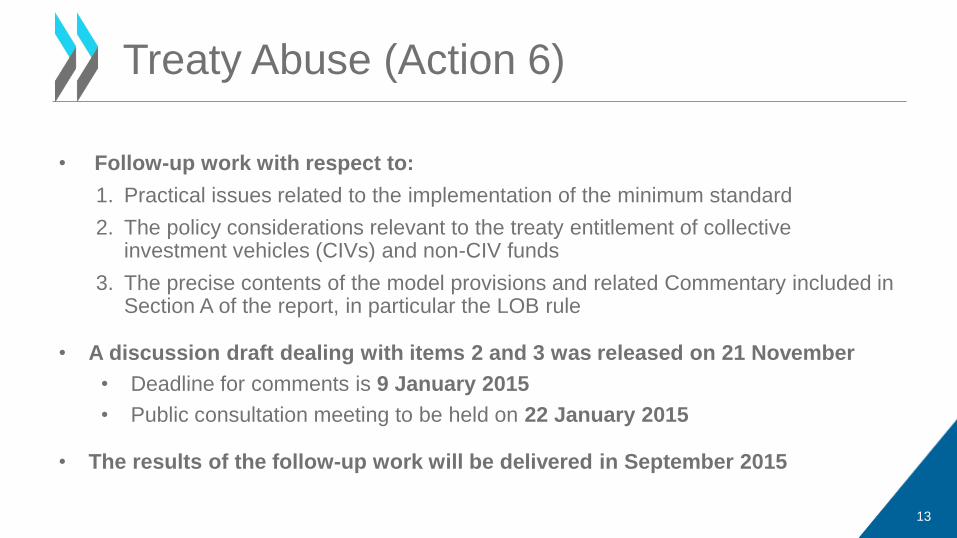

• Follow-up work with respect to:

1. Practical issues related to the implementation of the minimum standard

2. The policy considerations relevant to the treaty entitlement of collective investment vehicles (CIVs) and non-CIV funds

3. The precise contents of the model provisions and related Commentary included in Section A of the report, in particular the LOB rule

• A discussion draft dealing with items 2 and 3 was released on 21 November

• Deadline for comments is 9 January 2015

• Public consultation meeting to be held on 22 January 2015

• The results of the follow-up work will be delivered in September 2015

13

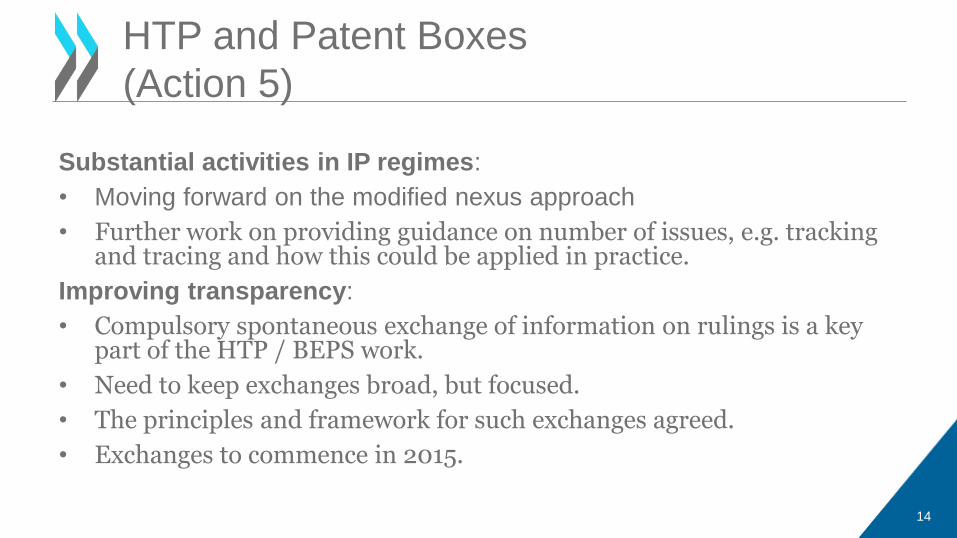

Treaty Abuse (Action 6)

Substantial activities in IP regimes:

• Moving forward on the modified nexus approach

• Further work on providing guidance on number of issues, e.g. tracking and tracing and how this could be applied in practice.

Improving transparency:

• Compulsory spontaneous exchange of information on rulings is a key part of the HTP / BEPS work.

• Need to keep exchanges broad, but focused.

• The principles and framework for such exchanges agreed.

• Exchanges to commence in 2015.

14

HTP and Patent Boxes

(Action 5)

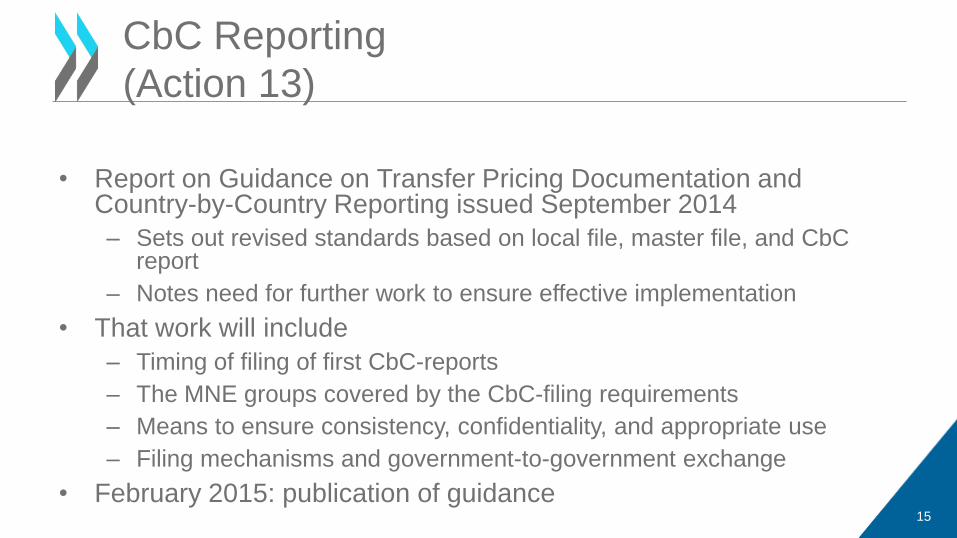

• Report on Guidance on Transfer Pricing Documentation and Country-by-Country Reporting issued September 2014

– Sets out revised standards based on local file, master file, and CbCreport

– Notes need for further work to ensure effective implementation

• That work will include

– Timing of filing of first CbC-reports

– The MNE groups covered by the CbC-filing requirements

– Means to ensure consistency, confidentiality, and appropriate use

– Filing mechanisms and government-to-government exchange

• February 2015: publication of guidance15

CbC Reporting

(Action 13)

2015 DISCUSSION

DRAFTS FOR PUBLIC

COMMENTS

16

ARTIFICIAL AVOIDANCE

OF PE (ACTION 7)

17

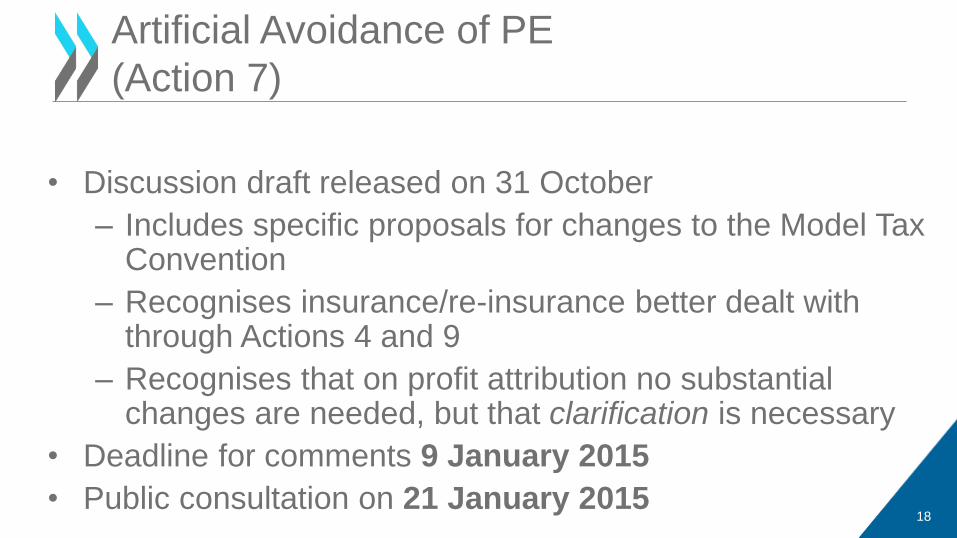

• Discussion draft released on 31 October

– Includes specific proposals for changes to the Model Tax Convention

– Recognises insurance/re-insurance better dealt with through Actions 4 and 9

– Recognises that on profit attribution no substantial changes are needed, but that clarification is necessary

• Deadline for comments 9 January 2015

• Public consultation on 21 January 201518

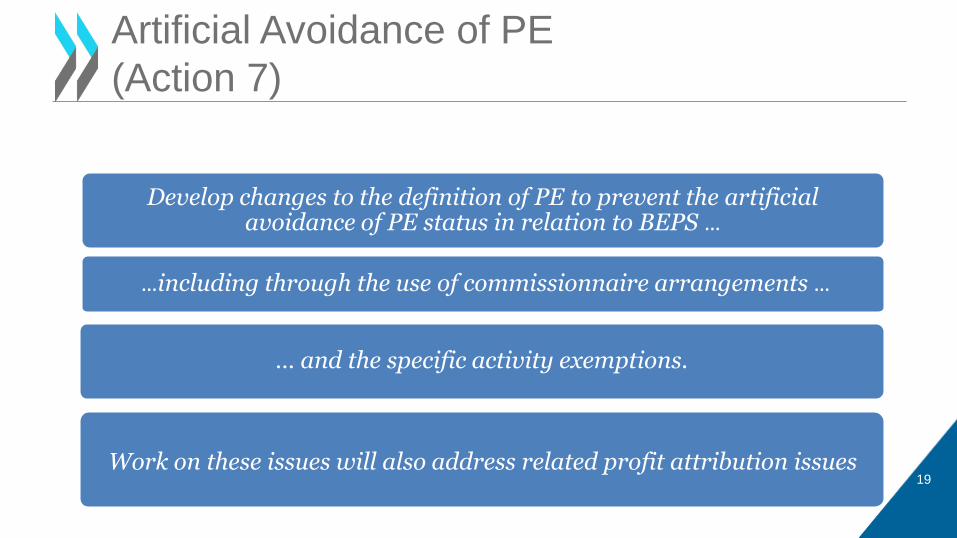

Artificial Avoidance of PE

(Action 7)

19

Develop changes to the definition of PE to prevent the artificial avoidance of PE status in relation to BEPS …

Work on these issues will also address related profit attribution issues

… and the specific activity exemptions.

…including through the use of commissionnaire arrangements …

Artificial Avoidance of PE

(Action 7)

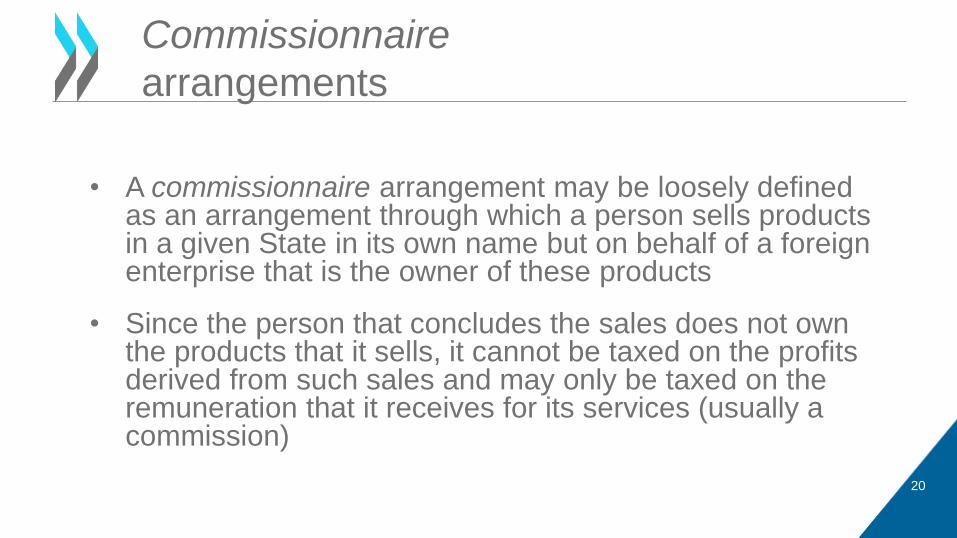

• A commissionnaire arrangement may be loosely defined as an arrangement through which a person sells products in a given State in its own name but on behalf of a foreign enterprise that is the owner of these products

• Since the person that concludes the sales does not own the products that it sells, it cannot be taxed on the profits derived from such sales and may only be taxed on the remuneration that it receives for its services (usually a commission)

Commissionnaire

arrangements

20

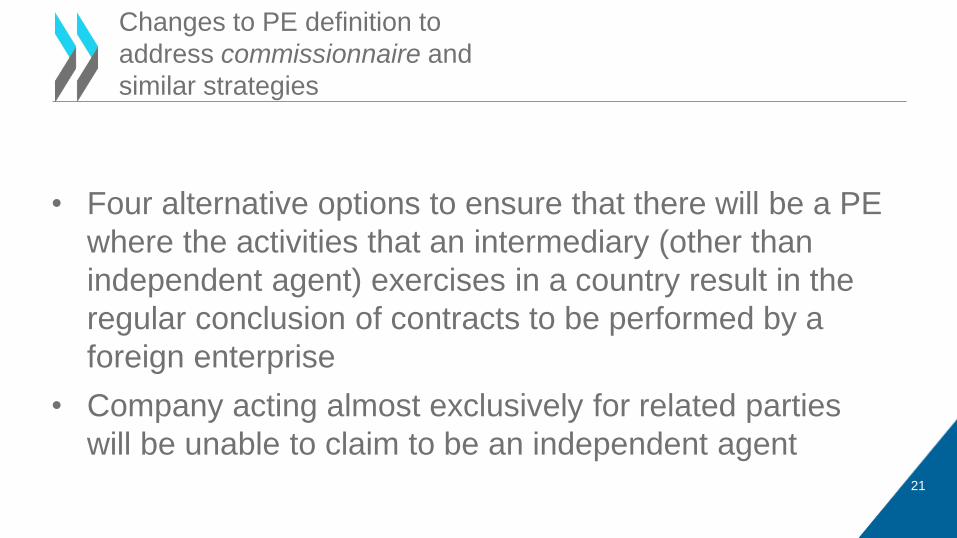

• Four alternative options to ensure that there will be a PE

where the activities that an intermediary (other than

independent agent) exercises in a country result in the

regular conclusion of contracts to be performed by a

foreign enterprise

• Company acting almost exclusively for related parties

will be unable to claim to be an independent agent

Changes to PE definition to

address commissionnaire and

similar strategies

21

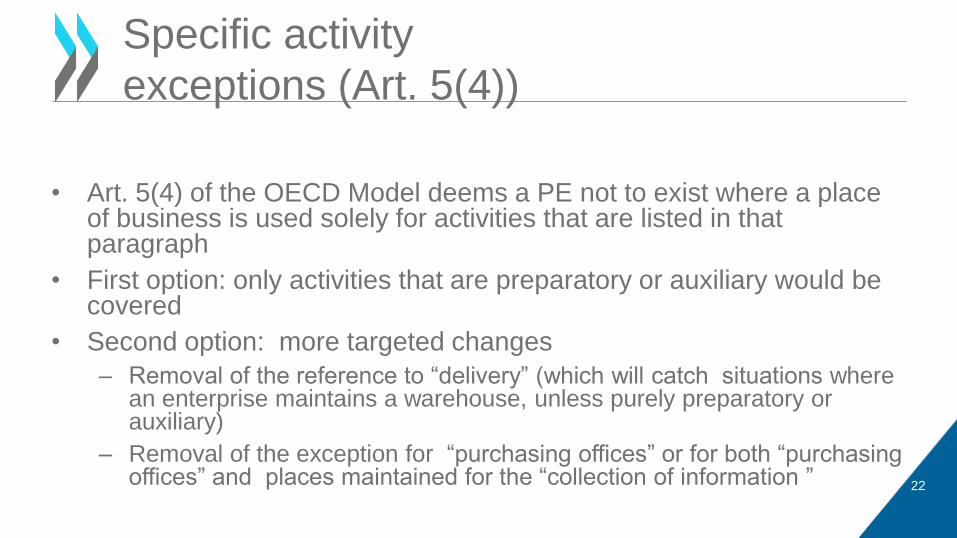

• Art. 5(4) of the OECD Model deems a PE not to exist where a place of business is used solely for activities that are listed in that paragraph

• First option: only activities that are preparatory or auxiliary would be covered

• Second option: more targeted changes

– Removal of the reference to “delivery” (which will catch situations where an enterprise maintains a warehouse, unless purely preparatory or auxiliary)

– Removal of the exception for “purchasing offices” or for both “purchasing offices” and places maintained for the “collection of information ”

Specific activity

exceptions (Art. 5(4))

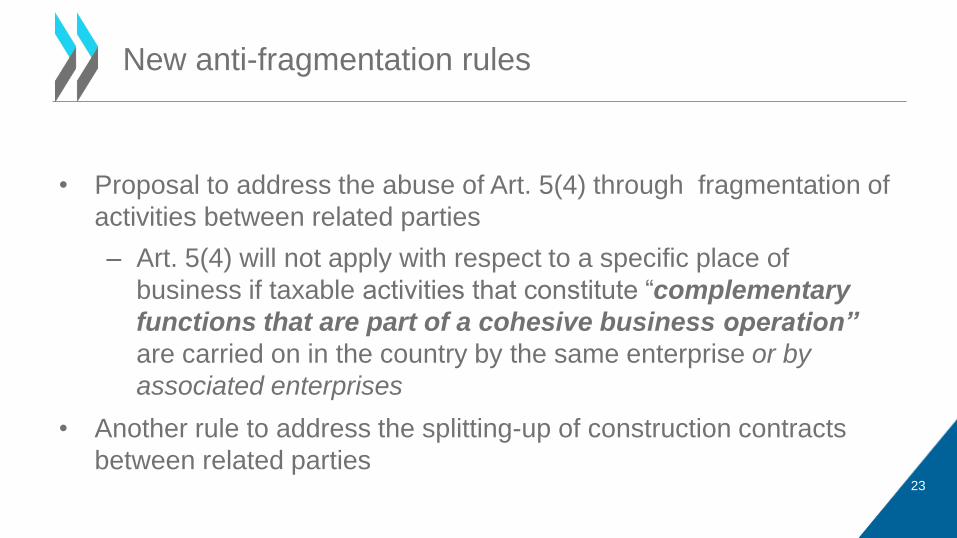

22

• Proposal to address the abuse of Art. 5(4) through fragmentation of

activities between related parties

– Art. 5(4) will not apply with respect to a specific place of

business if taxable activities that constitute “complementary

functions that are part of a cohesive business operation”

are carried on in the country by the same enterprise or by

associated enterprises

• Another rule to address the splitting-up of construction contracts

between related parties

New anti-fragmentation rules

23

INTEREST DEDUCTIBILITY

(ACTION 4)

24

25

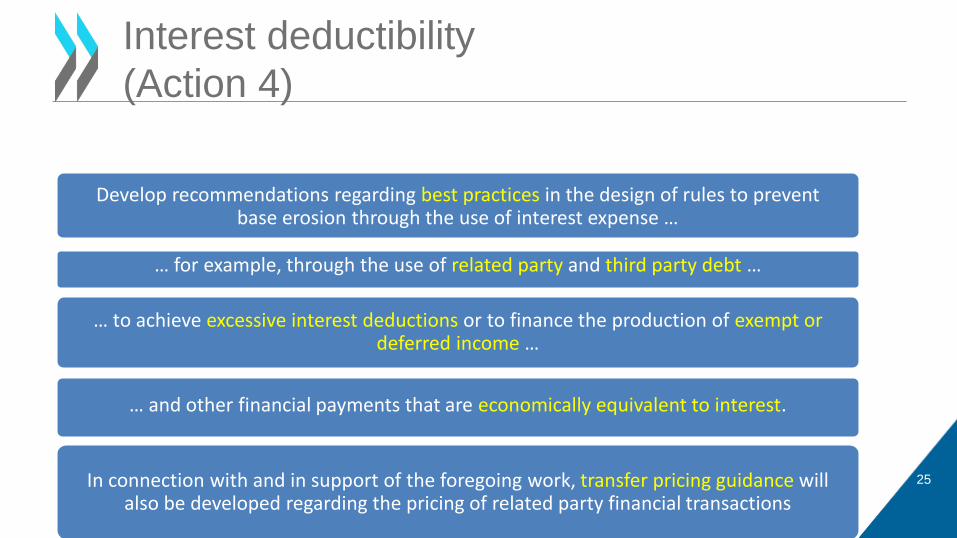

Interest deductibility

(Action 4)

Develop recommendations regarding best practices in the design of rules to prevent base erosion through the use of interest expense …

In connection with and in support of the foregoing work, transfer pricing guidance will also be developed regarding the pricing of related party financial transactions

… to achieve excessive interest deductions or to finance the production of exempt or deferred income …

… for example, through the use of related party and third party debt …

… and other financial payments that are economically equivalent to interest.

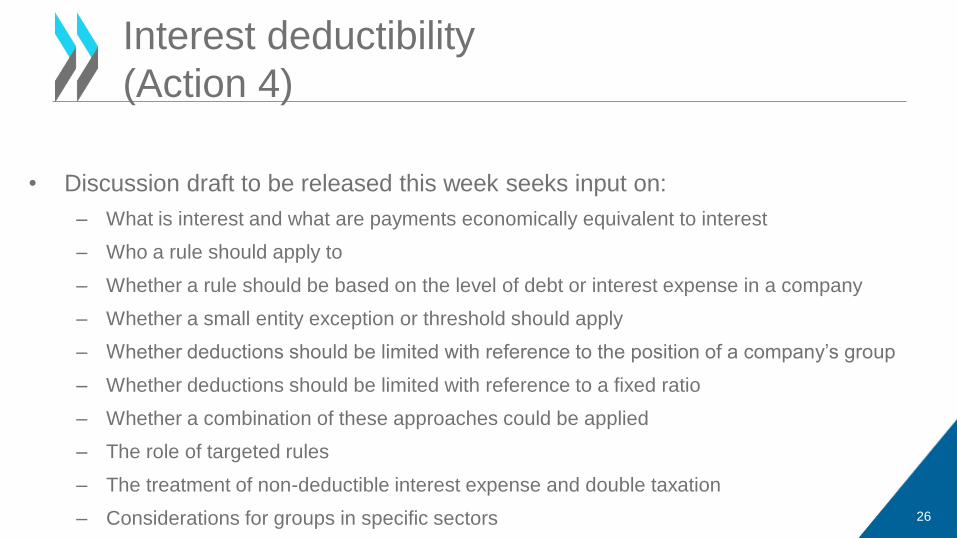

• Discussion draft to be released this week seeks input on:

– What is interest and what are payments economically equivalent to interest

– Who a rule should apply to

– Whether a rule should be based on the level of debt or interest expense in a company

– Whether a small entity exception or threshold should apply

– Whether deductions should be limited with reference to the position of a company’s group

– Whether deductions should be limited with reference to a fixed ratio

– Whether a combination of these approaches could be applied

– The role of targeted rules

– The treatment of non-deductible interest expense and double taxation

– Considerations for groups in specific sectors 26

Interest deductibility

(Action 4)

27

Interest deductibility

(Action 4)

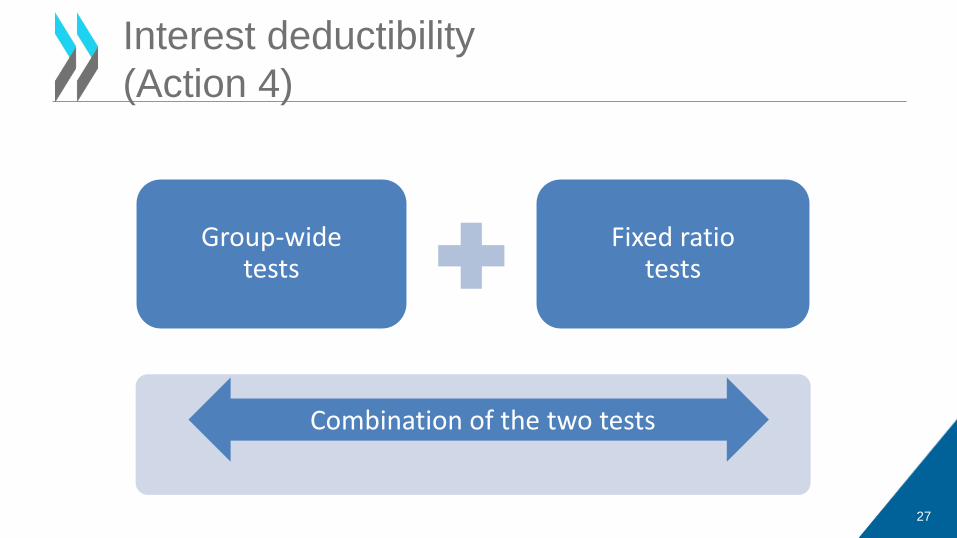

Group-wide tests

Fixed ratio tests

Combination of the two tests

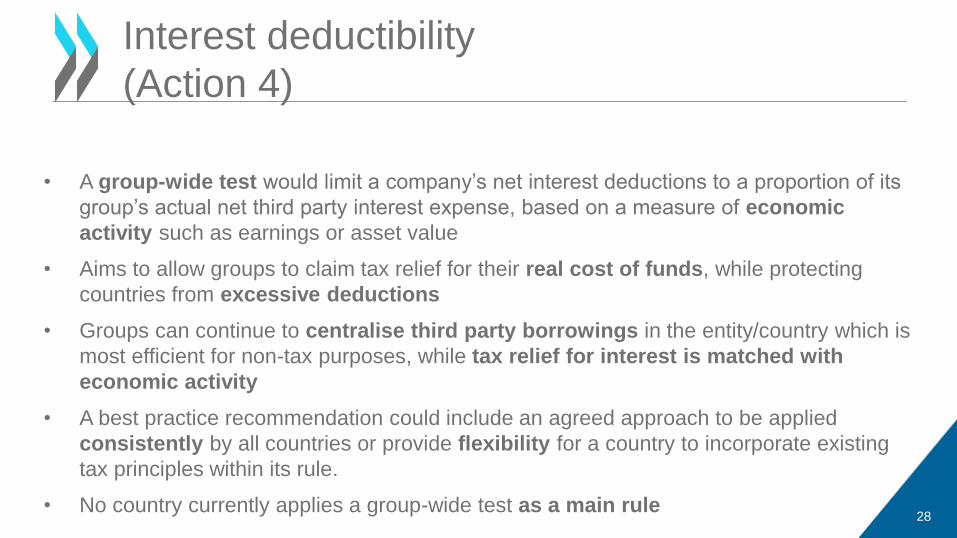

• A group-wide test would limit a company’s net interest deductions to a proportion of its

group’s actual net third party interest expense, based on a measure of economic

activity such as earnings or asset value

• Aims to allow groups to claim tax relief for their real cost of funds, while protecting

countries from excessive deductions

• Groups can continue to centralise third party borrowings in the entity/country which is

most efficient for non-tax purposes, while tax relief for interest is matched with

economic activity

• A best practice recommendation could include an agreed approach to be applied

consistently by all countries or provide flexibility for a country to incorporate existing

tax principles within its rule.

• No country currently applies a group-wide test as a main rule 28

Interest deductibility

(Action 4)

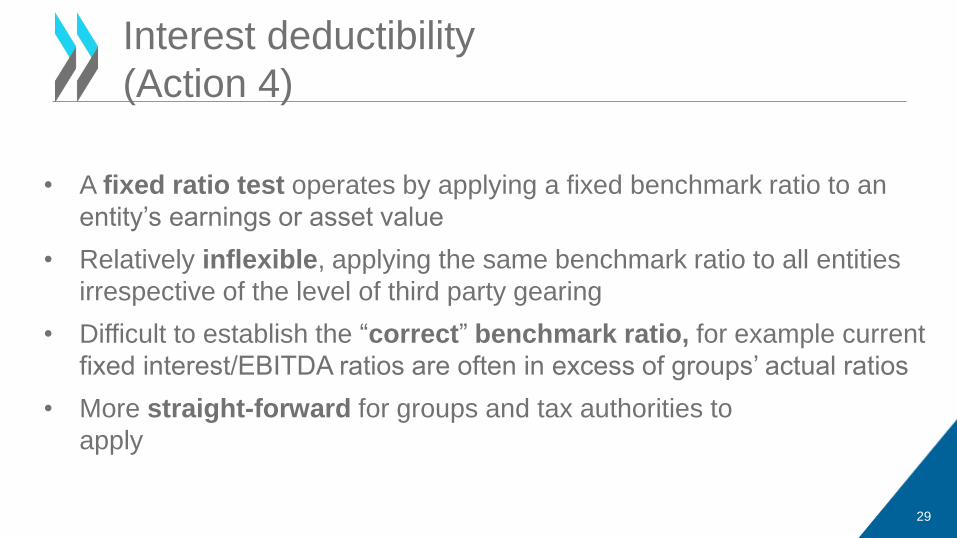

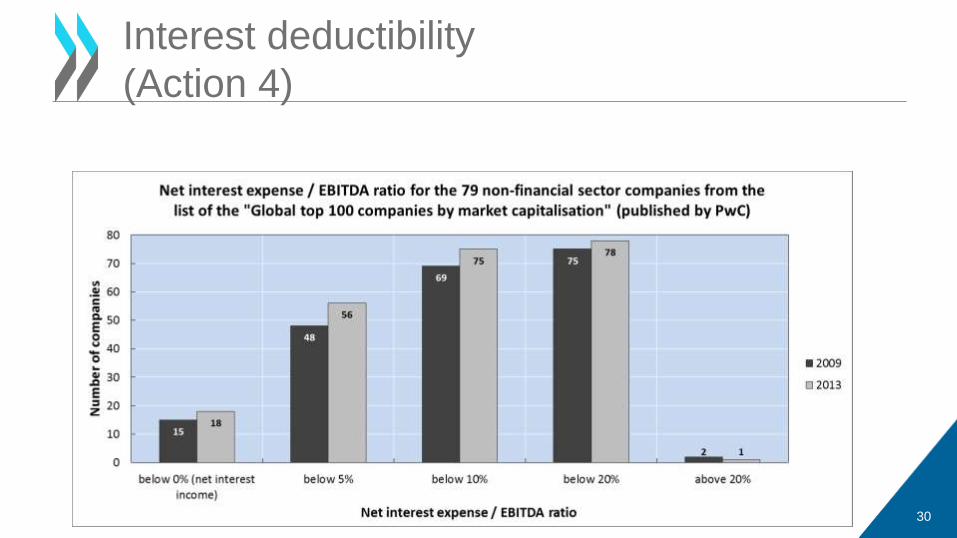

• A fixed ratio test operates by applying a fixed benchmark ratio to an

entity’s earnings or asset value

• Relatively inflexible, applying the same benchmark ratio to all entities

irrespective of the level of third party gearing

• Difficult to establish the “correct” benchmark ratio, for example current

fixed interest/EBITDA ratios are often in excess of groups’ actual ratios

• More straight-forward for groups and tax authorities to

apply

29

Interest deductibility

(Action 4)

30

Interest deductibility

(Action 4)

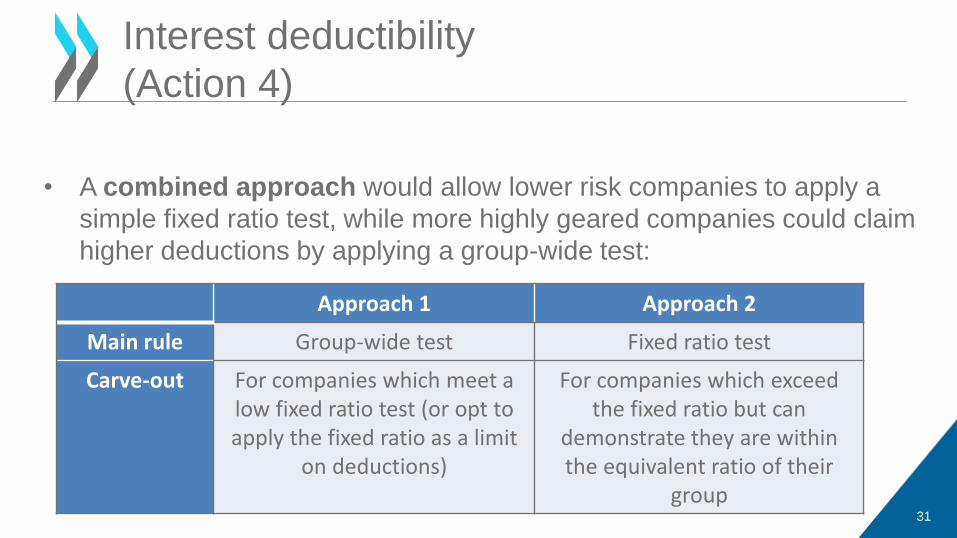

• A combined approach would allow lower risk companies to apply a

simple fixed ratio test, while more highly geared companies could claim

higher deductions by applying a group-wide test:

31

Interest deductibility

(Action 4)

Approach 1 Approach 2

Main rule Group-wide test Fixed ratio test

Carve-out For companies which meet a low fixed ratio test (or opt to apply the fixed ratio as a limit

on deductions)

For companies which exceed the fixed ratio but can

demonstrate they are within the equivalent ratio of their

group

• Discussion draft to be released this week for

comment by 6 February 2015

• Public consultation to be held in Paris on

17 February 2015

32

Interest deductibility

(Action 4)

LOW VALUE-ADDING

SERVICES (ACTION 10)

33

• Discussion Draft released 3 November 2014 for comments by 14 January 2015

• Proposes a simplified approach which reduces the scope for base erosion through excessive management fees and head office expenses.

• The approach

– Identifies a wide category of common intra-group services and determines a very limited profit mark-up

– Applies a consistent allocation key

– Provides greater transparency through specific reporting requirements including documentation showing the determination of the cost pool

34

Low value-adding

services

MULTILATERAL

INSTRUMENT (ACTION 15)

35

• In January 2015, the CFA will consider a draft mandate

for the negotiation of a multilateral instrument.

• The mandate will deal with the scope of the instrument

and the timeline to deliver.

• Once agreed the mandate will be presented to the

OECD Council and the G20 with a view to convene an

ad hoc group of interested parties and start the work.

36

Work on Multilateral

Instrument

UPCOMING

DISCUSSION

DRAFTS

37

38

Upcoming Discussion Drafts

• Interest deductions and other financial payments

• Transfer Pricing, risk and recharacterisation

• Transfer Pricing Aspects of commodity transactions

• The use of profit splits in the context of global value

chains

• More effective dispute resolution

JOIN THE

DISCUSSION

Ask questions and comment

40

Join the discussion

Directly: Enter your question in the space provided

Via email: [email protected]

Via Twitter: Follow us via @OECDlive using #BEPS

Further Information

Website: www.oecd.org/tax/beps.htm

Contact: [email protected]

Tax email alerts: www.oecd.org/oecddirect