Embed Size (px)

Citation preview

A REPORT SAMPLE CURIOUS TRENDS: THE FOOD INDUSTRY 2015 The Year of Transition

The past year in the food industry has been a year of

transitions. The consumer is moving from paper to digital

lists. Price has risen as a consideration both at the grocery

and when selecting a restaurant and Millennials are

impacting food consumption behavior.

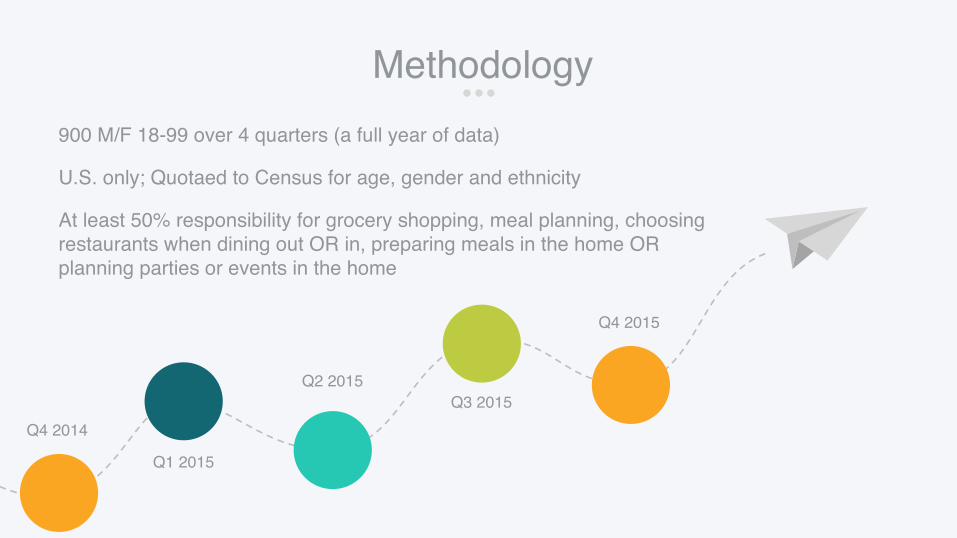

Methodology900 M/F 18-99 over 4 quarters (a full year of data)

U.S. only; Quotaed to Census for age, gender and ethnicity

At least 50% responsibility for grocery shopping, meal planning, choosing restaurants when dining out OR in, preparing meals in the home OR planning parties or events in the home

Q2 2015Q3 2015

Q1 2015

Q4 2015

Q4 2014

TechnoAssistance

The digital revolution continues to

impact how the consumer

communicates food-related

comments and what they may eat.

However, they are also embracing

technologies that affect how they

shop the category.

THREE TRENDS THAT WILL CHANGE THE FOOD INDUSTRY:

SeasonalImpact

Consumers have moved beyond the

expected seasonalities, such as

shopping for Thanksgiving or

Christmas, to the seasons having an

impact on what channels they shop

and even where in the store they

begin their journey.

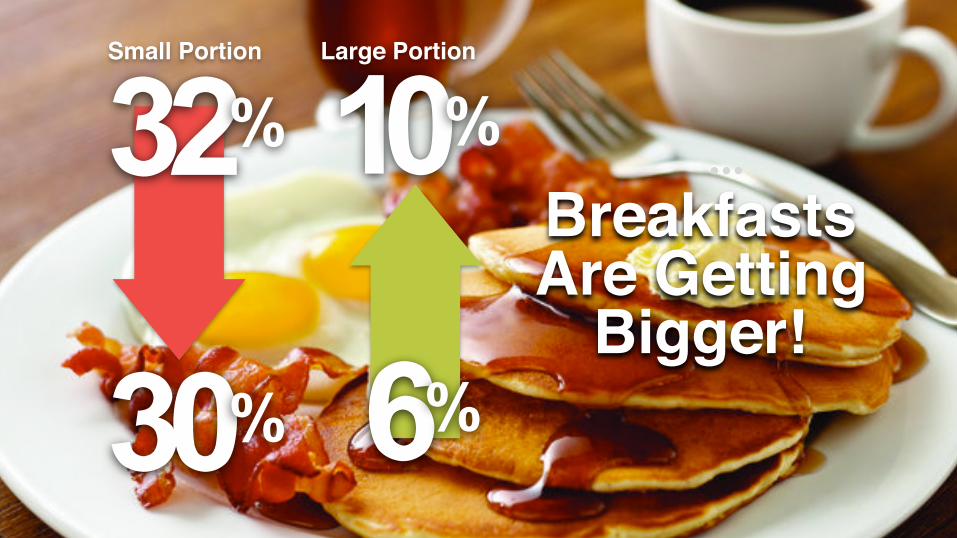

2CautiousGrazing

Grazing, that is eating more small

meals, continues to be a trend;

however, it must be understood that

while portion sizes have increased,

there is rising concern from

consumers over the quality of what

goes into their bodies.

1 3

4

CautiousGrazing

1

Small Portion

BreakfastsAre Getting

Bigger!

30%

10%32%

6%

Large Portion

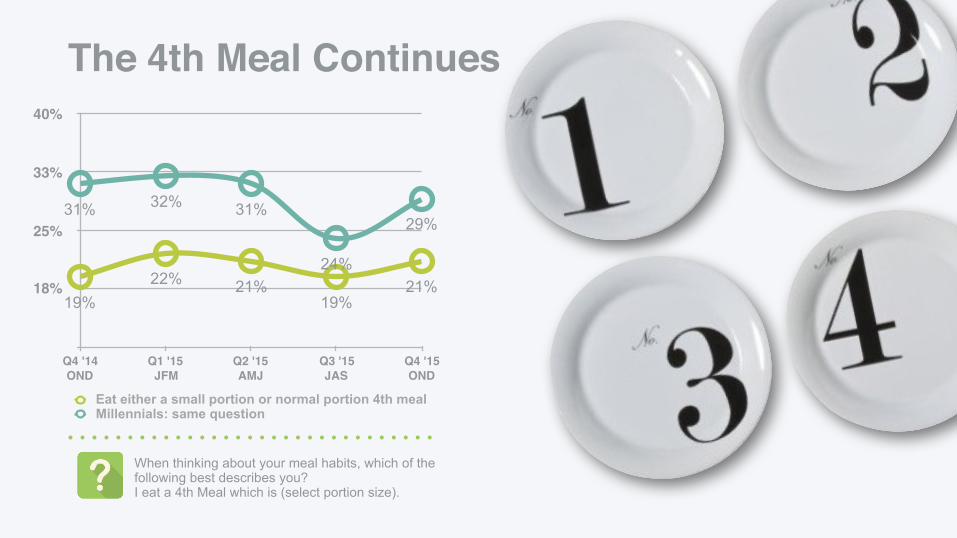

The 4th Meal Continues

18%

25%

33%

40%

Q4 '14OND

Q1 '15JFM

Q2 '15AMJ

Q3 '15JAS

Q4 '15OND

31% 32% 31%

24%

29%

19%22% 21%

19%21%

Eat either a small portion or normal portion 4th mealMillennials: same question

When thinking about your meal habits, which of the following best describes you? I eat a 4th Meal which is (select portion size).

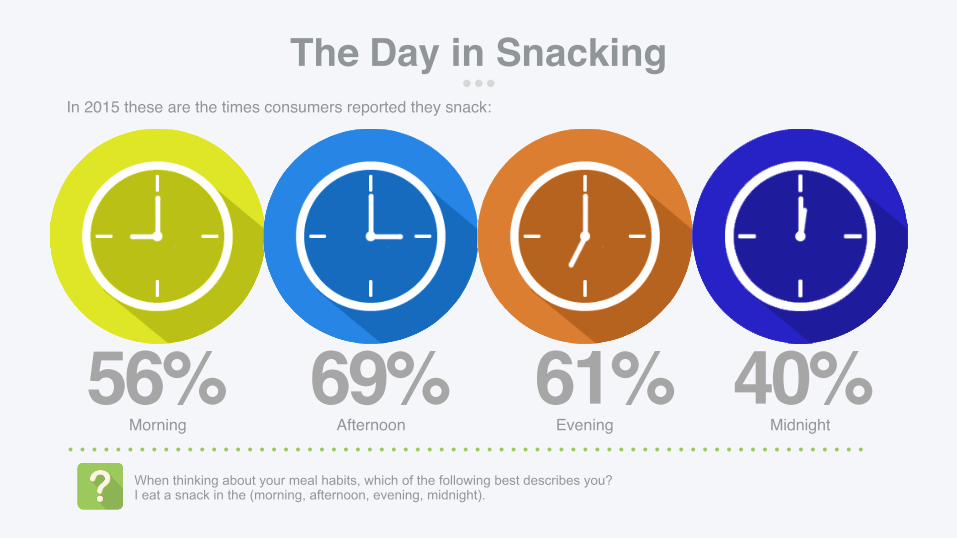

In 2015 these are the times consumers reported they snack:

The Day in Snacking

56% 69% 61% 40%Morning Afternoon Evening Midnight

When thinking about your meal habits, which of the following best describes you? I eat a snack in the (morning, afternoon, evening, midnight).

Variety

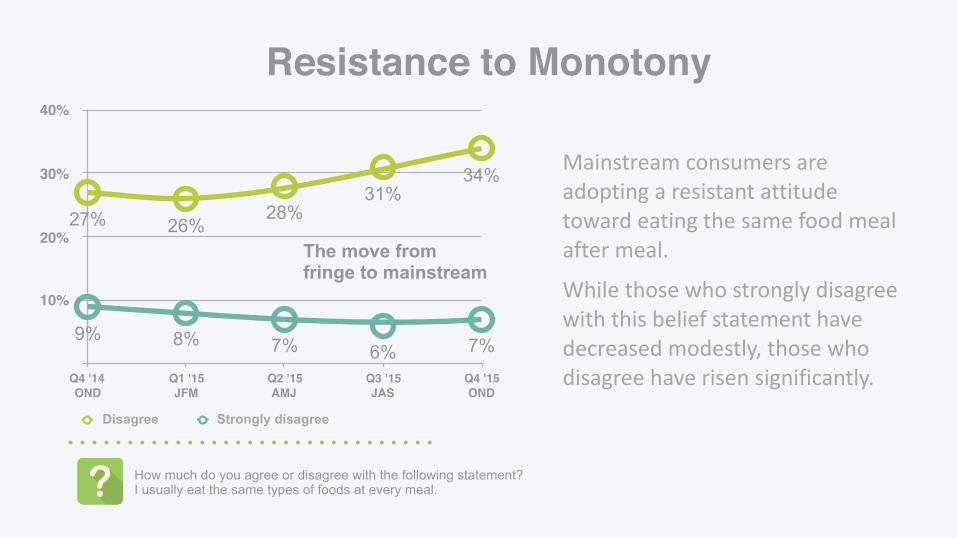

Resistance to Monotony

10%

20%

30%

40%

Q4 '14OND

Q1 '15JFM

Q2 '15AMJ

Q3 '15JAS

Q4 '15OND

9% 8% 7% 6% 7%

27% 26%28%

31%34%

Disagree Strongly disagree

Mainstream consumers are adopting a resistant attitude toward eating the same food meal after meal.

While those who strongly disagree with this belief statement have decreased modestly, those who disagree have risen significantly.

How much do you agree or disagree with the following statement? I usually eat the same types of foods at every meal.

The move from fringe to mainstream

Health

When it comes to the time spent making selections, consumers spend more time making decisions in the meat & seafood sections than in any other sections of the grocery. The produce section comes in second.

The Shopping Journey

20%Produce

30%Meat & Seafood

Thinking about your typical route through the store, in which of the following sections do you spend the most time making your selections?

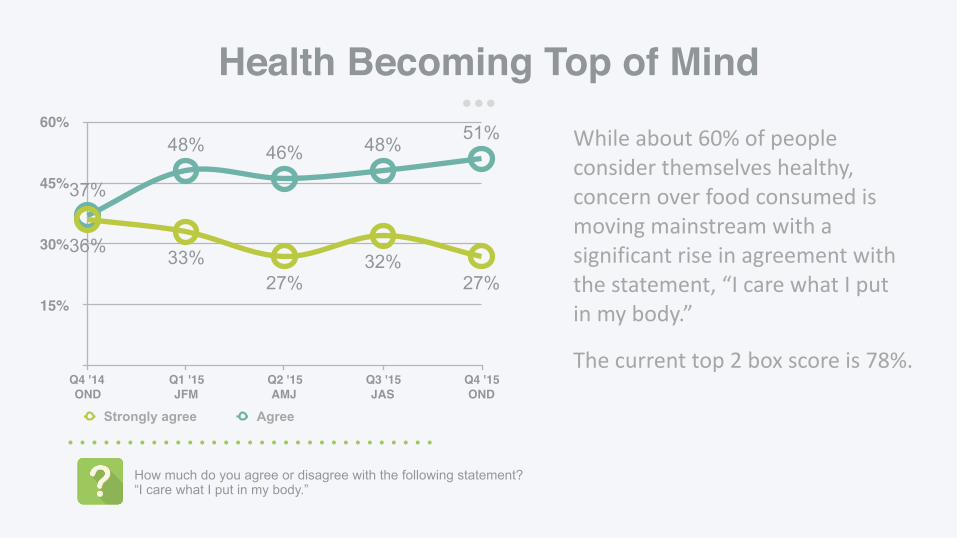

Health Becoming Top of Mind

15%

30%

45%

60%

Q4 '14OND

Q1 '15JFM

Q2 '15AMJ

Q3 '15JAS

Q4 '15OND

37%

48% 46% 48% 51%

36% 33%27%

32%27%

Strongly agree Agree

While about 60% of people consider themselves healthy, concern over food consumed is moving mainstream with a significant rise in agreement with the statement, “I care what I put in my body.”

The current top 2 box score is 78%.

How much do you agree or disagree with the following statement? “I care what I put in my body.”

47%

43%GMO Concern

on the Rise

How much do you agree or disagree with the following statement? “I care what I put in my body.”

TOP 2 BOX

Price

32%

27%

Rising Concern

AboutIncreased

Food PricesThinking about food in general, please rate your level of concern with the following. “Increases in food prices”

VERY CONCERNED

48%

55%

63%

70%

Q4 '14OND

Q1 '15JFM

Q2 '15AMJ

Q3 '15JAS

Q4 '15OND

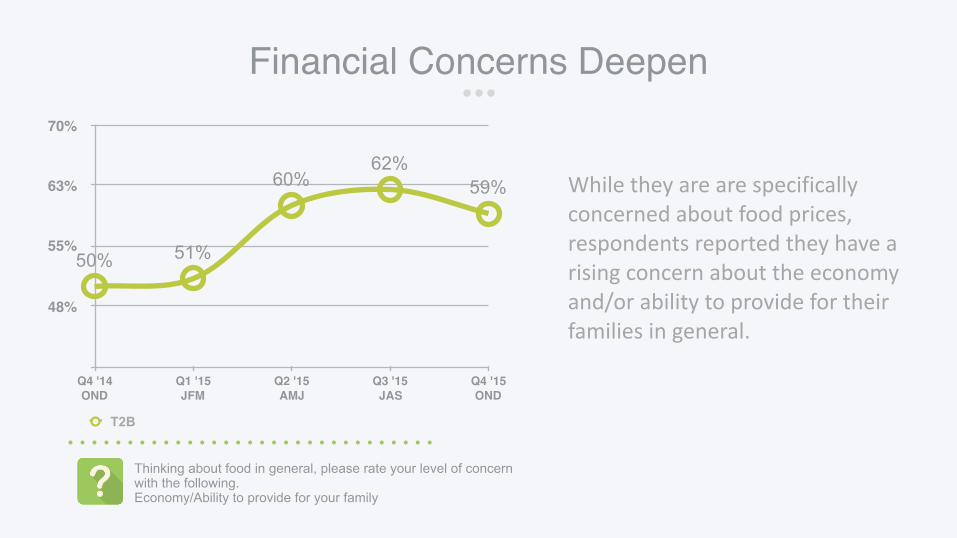

50% 51%

60%62%

59%

T2B

While they are are specifically concerned about food prices, respondents reported they have a rising concern about the economy and/or ability to provide for their families in general.

Thinking about food in general, please rate your level of concern with the following. Economy/Ability to provide for your family

Financial Concerns Deepen

24.5%

29%

33.5%

38%

Q4 '14OND

Q1 '15JFM

Q2 '15AMJ

Q3 '15JAS

Q4 '15OND

32%30%

38% 38%36%

Stongly Agree

Shopping Motivations 17

There was an increase in those who “strongly agree” with a money savings goal statement indicating the year ended with even greater concern about food cost than when it began.

How much do you agree or disagree with the following statement? “My number one goal when shopping is to save as much money as possible.”

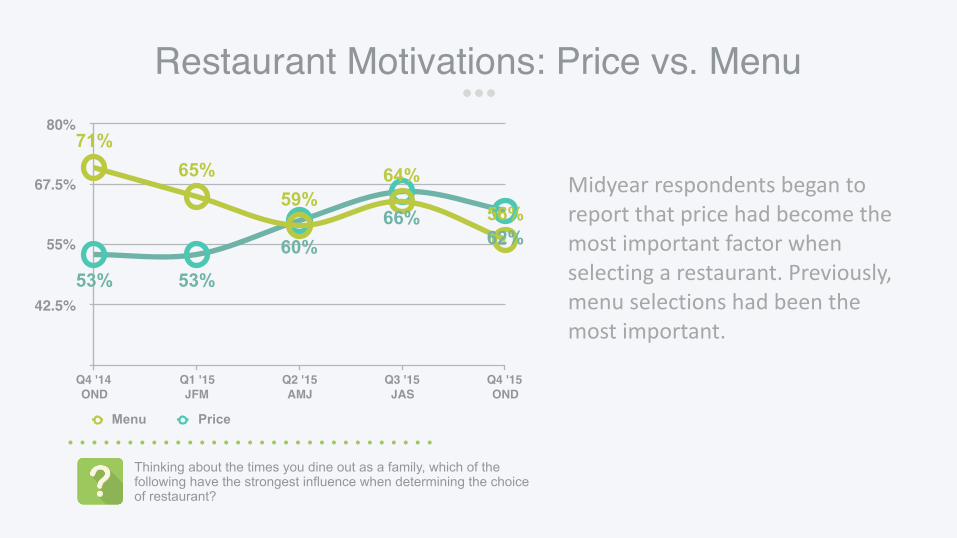

Restaurant Motivations: Price vs. Menu

42.5%

55%

67.5%

80%

Q4 '14OND

Q1 '15JFM

Q2 '15AMJ

Q3 '15JAS

Q4 '15OND

53% 53%

60%66%

62%

71%65%

59%64%

56%

Menu Price

Midyear respondents began to report that price had become the most important factor when selecting a restaurant. Previously, menu selections had been the most important.

Thinking about the times you dine out as a family, which of the following have the strongest influence when determining the choice of restaurant?

SeasonalImpact

2

American Food Seasons

Winter Spring Summer Fall

More ethnically adventurous

How they shop How they prepareHow they eat

Fewer overall shopping trips

More home-prepared mealsShop more at specialty stores Shop more at local markets

More time planning meals

Begin shopping in bakery Sourcing less importantSourcing less important

More shopping for comfort food

Meal replacement more common

More carb watching

There are some surprising trends throughout the year. While we expect holidays to impact shopping behavior, seasonality also affects many other behaviors such as carb watching, beginning a shopping trip in the bakery section, sourcing sensitivity and others.

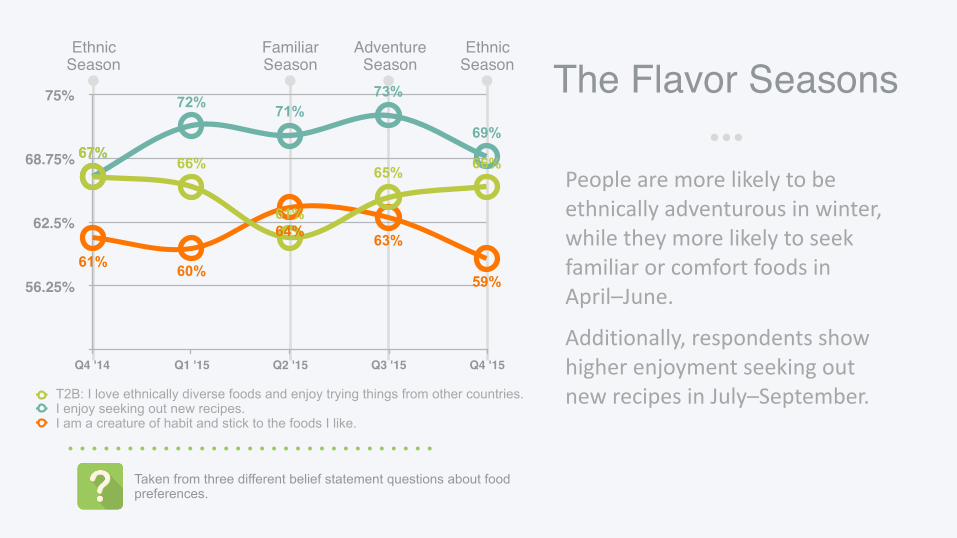

People are more likely to be ethnically adventurous in winter, while they more likely to seek familiar or comfort foods in April–June.

Additionally, respondents show higher enjoyment seeking out new recipes in July–September.

The Flavor Seasons

56.25%

62.5%

68.75%

75%

Q4 '14 Q1 '15 Q2 '15 Q3 '15 Q4 '15

61% 60%

64% 63%

59%

67%

72% 71%73%

69%67%

66%

61%

65% 66%

T2B: I love ethnically diverse foods and enjoy trying things from other countries.I enjoy seeking out new recipes.I am a creature of habit and stick to the foods I like.

EthnicSeason

EthnicSeason

AdventureSeason

FamiliarSeason

Taken from three different belief statement questions about food preferences.

While the grocery store is still king, U.S. consumers are visiting specialty stores more in the winter (7% in Q4 2014 and 6% in Q4 2015 compared to 4% and 5% in other seasons). And, no surprise, consumers visit local markets more in the spring (Q2).

Specialty StoresSeasonality

0.0

0.0

0.1

0.1

Q4 '14OND

Q1 '15JFM

Q2 '15AMJ

Q3 '15JAS

Q4 '15OND

7%

5%

4% 4%

6%

Specialty Store Visits

Now please think about the food you purchase for your household. Please select the one type of store where you shop most often for food.

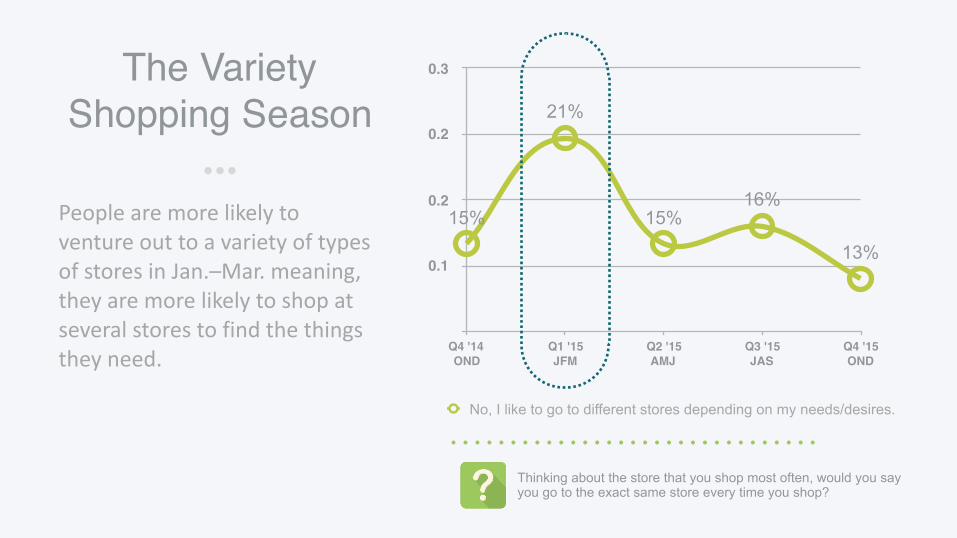

People are more likely to venture out to a variety of types of stores in Jan.–Mar. meaning, they are more likely to shop at several stores to find the things they need.

The Variety Shopping Season

0.1

0.2

0.2

0.3

Q4 '14OND

Q1 '15JFM

Q2 '15AMJ

Q3 '15JAS

Q4 '15OND

15%

21%

15%16%

13%

No, I like to go to different stores depending on my needs/desires.

Thinking about the store that you shop most often, would you say you go to the exact same store every time you shop?

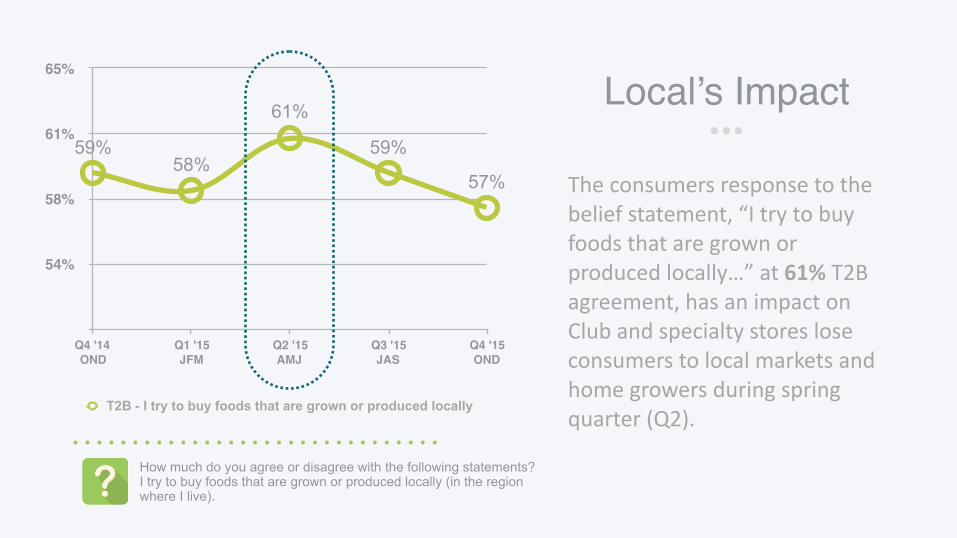

The consumers response to the belief statement, “I try to buy foods that are grown or produced locally…” at 61% T2B agreement, has an impact on Club and specialty stores lose consumers to local markets and home growers during spring quarter (Q2).

Local’s Impact

54%

58%

61%

65%

Q4 '14OND

Q1 '15JFM

Q2 '15AMJ

Q3 '15JAS

Q4 '15OND

59%58%

61%

59%

57%

T2B - I try to buy foods that are grown or produced locally

How much do you agree or disagree with the following statements? I try to buy foods that are grown or produced locally (in the region where I live).

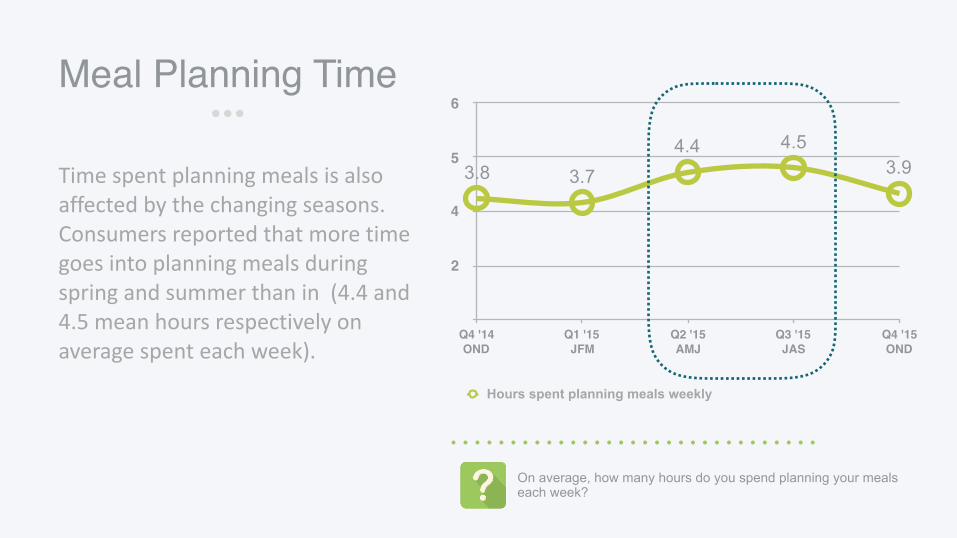

Time spent planning meals is also affected by the changing seasons. Consumers reported that more time goes into planning meals during spring and summer than in (4.4 and 4.5 mean hours respectively on average spent each week).

Meal Planning Time

2

4

5

6

Q4 '14OND

Q1 '15JFM

Q2 '15AMJ

Q3 '15JAS

Q4 '15OND

3.8 3.74.4 4.5

3.9

Hours spent planning meals weekly

On average, how many hours do you spend planning your meals each week?

thank you.Contact: Jeff Dattilo Email: [email protected]