Embed Size (px)

Citation preview

3RD OECD GREEN INVESTMENT FINANCING FORUM

State and trends of green finance

and green investment needs

Ali Izadi

13 October 2015

1

0

5

10

15

20

25

30

35

40

187

0

187

5

188

0

188

5

189

0

189

5

190

0

190

5

191

0

191

5

192

0

192

5

193

0

193

5

194

0

194

5

195

0

195

5

196

0

196

5

197

0

197

5

198

0

198

5

199

0

199

5

200

0

200

5

201

0

201

5

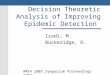

Note: Includes NGL and processing gain, but excludes biofuels

Source: IEA; CDIAC; BP; Bloomberg New

Energy Finance

GLOBAL CARBON EMISSIONS FROM FOSSIL FUELS(GIGATONNES CO2/YEAR)

0.00%2.00%4.00%6.00%8.00%10.00%

30

32

34

36

5.5% 5.7% 3.1% 5.4% 4.2% 3.4% 3.4% 3.4% 3.5%

0%

2%

4%

6%

20

06

20

07

20

08

20

09

20

10

20

11

2012

20

13

20

14

2015

5.5% 5.7% 3.1% 0% 5.4% 4.2% 3.4% 3.4% 3.4% 3.5%

Global GDP growth (real)

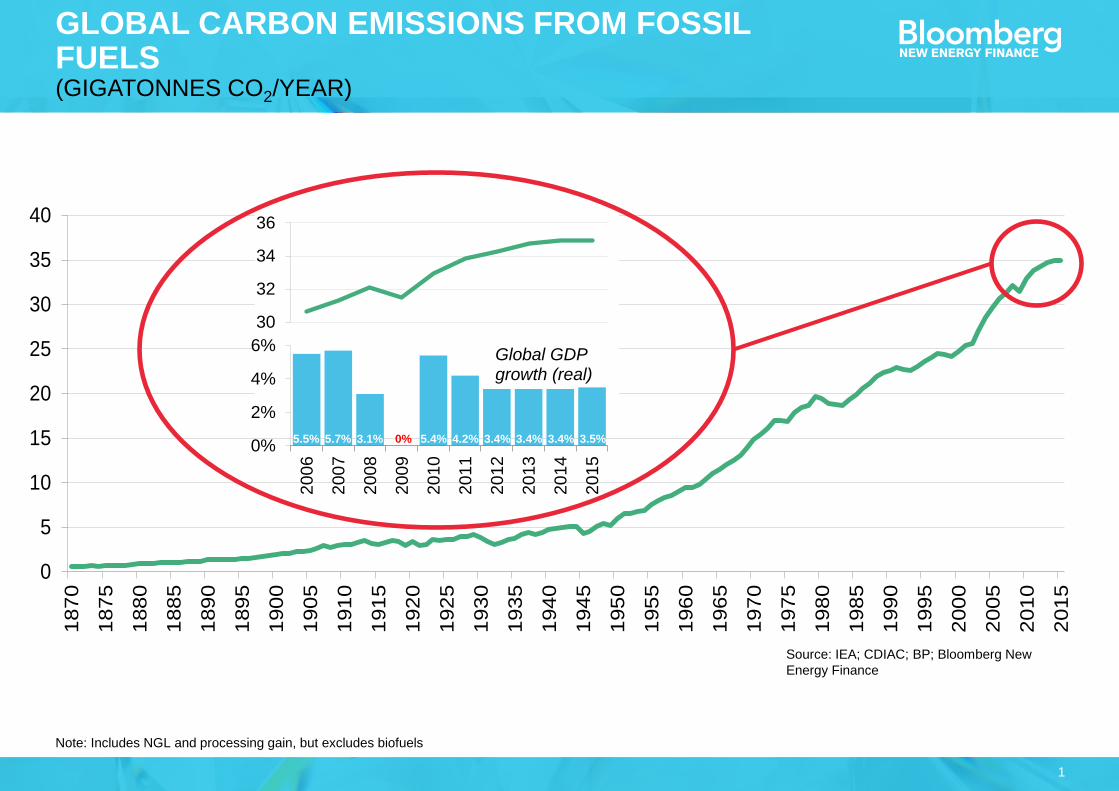

2

$62bn

$88bn

$128bn

$175bn

$206bn $207bn

$274bn

$318bn$297bn

$272bn

$316bn$329bn

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

$146/bbl

Note: Total values include estimates for undisclosed deals. Includes corporate and government R&D, and spending for digital energy and energy

storage projects (not reported in quarterly statistics). Excludes large hydro.

Source: Bloomberg Intelligence, Bloomberg New Energy

Finance

CLEAN ENERGY INVESTMENT ROSE WHILE OIL PLUMMETEDGLOBAL CLEAN ENERGY INVESTMENT VS WTI CRUDE SPOT 2004-15

$48/bbl

Record

investment

3

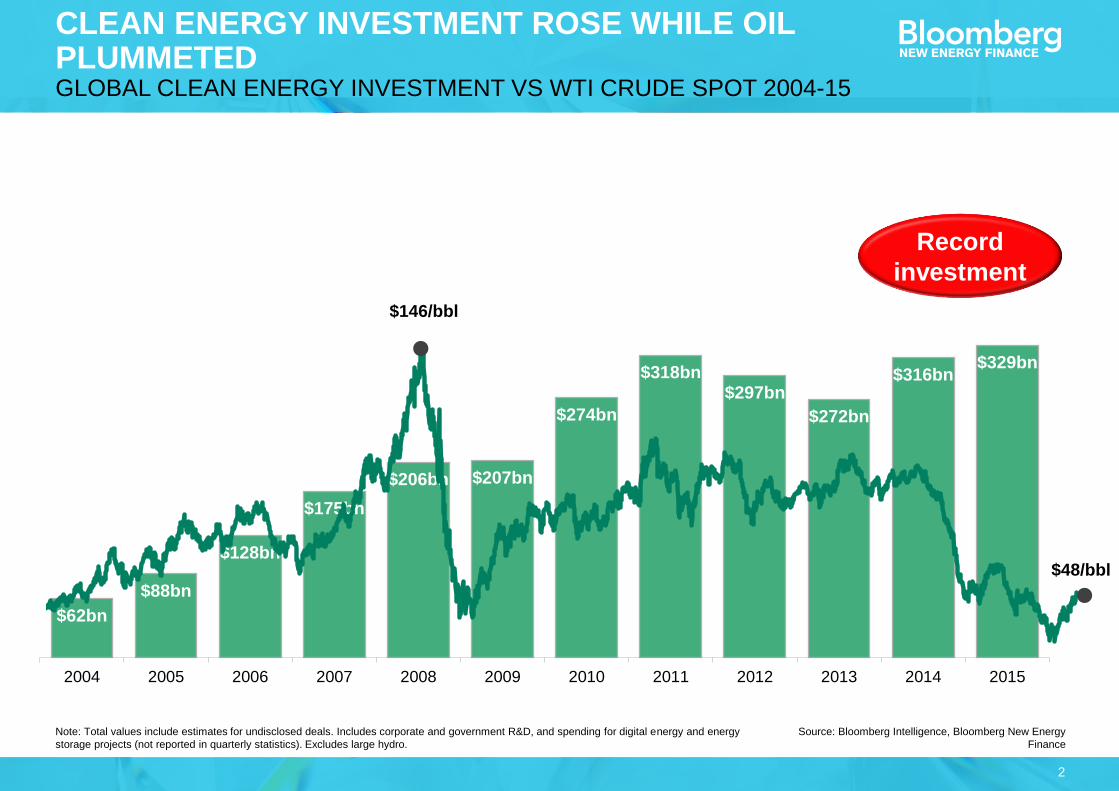

Source: UNEP, Bloomberg New Energy Finance

INVESTMENT IN POWER CAPACITY, 2008–15 ($BN)

Renewables ex large hydro

Fossil fuel

Nuclear

Large hydro

0

50

100

150

200

250

300

2008 2009 2010 2011 2012 2013 2014 2015

4

Note: New investment volume adjusts for re-invested equity. Total values include estimates for undisclosed deals. Source: Bloomberg New Energy FInance

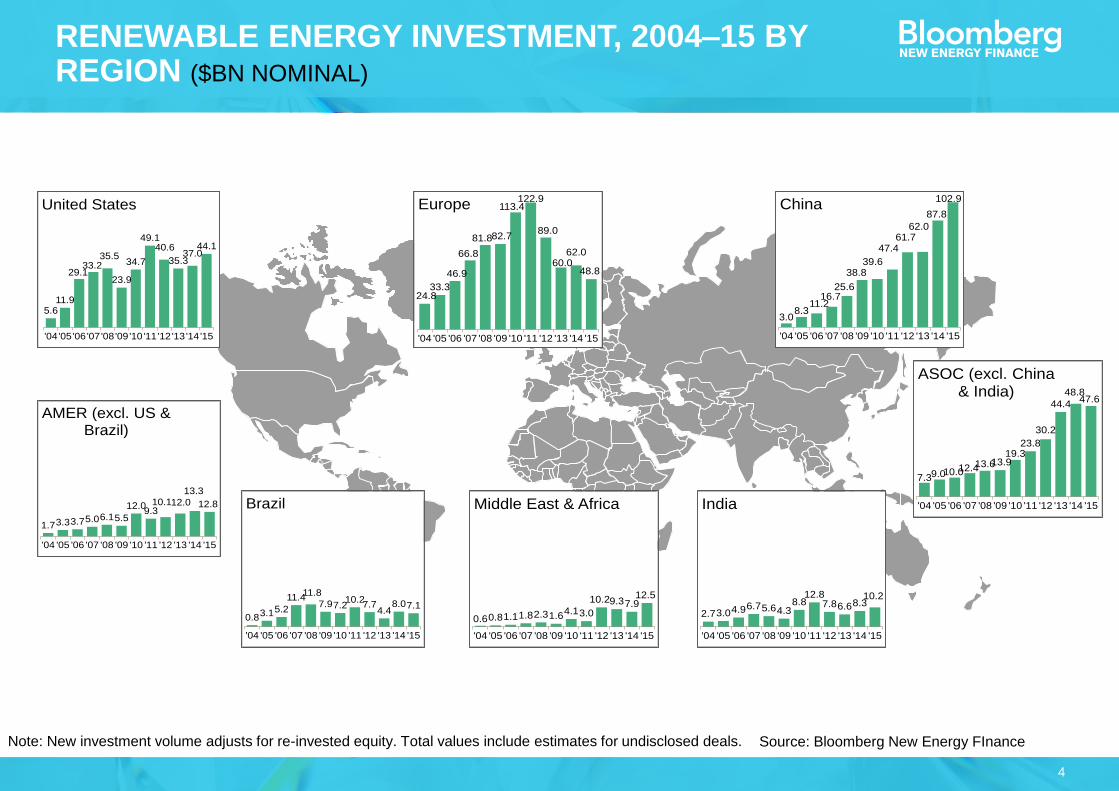

RENEWABLE ENERGY INVESTMENT, 2004–15 BY REGION ($BN NOMINAL)

5.611.9

29.133.2

35.5

23.9

34.7

49.140.6

35.337.0

44.1

'04'05'06'07'08'09'10'11'12'13'14'15

United States

0.83.15.2

11.411.8

7.97.210.2

7.74.4

8.07.1

'04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15

Brazil

1.73.33.75.06.15.5

12.09.3

10.112.0

13.3

12.8

'04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15

AMER (excl. US & Brazil)

24.833.3

46.9

66.8

81.882.7

113.4122.9

89.0

60.062.0

48.8

'04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15

Europe

7.39.010.012.413.613.919.3

23.8

30.2

44.4

48.847.6

'04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15

ASOC (excl. China & India)

3.08.3

11.216.7

25.6

38.839.6

47.461.7

62.0

87.8

102.9

'04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15

China

2.73.04.96.75.64.38.8

12.87.86.68.3

10.2

'04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15

India

0.60.81.11.82.31.64.13.0

10.29.37.912.5

'04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15

Middle East & Africa

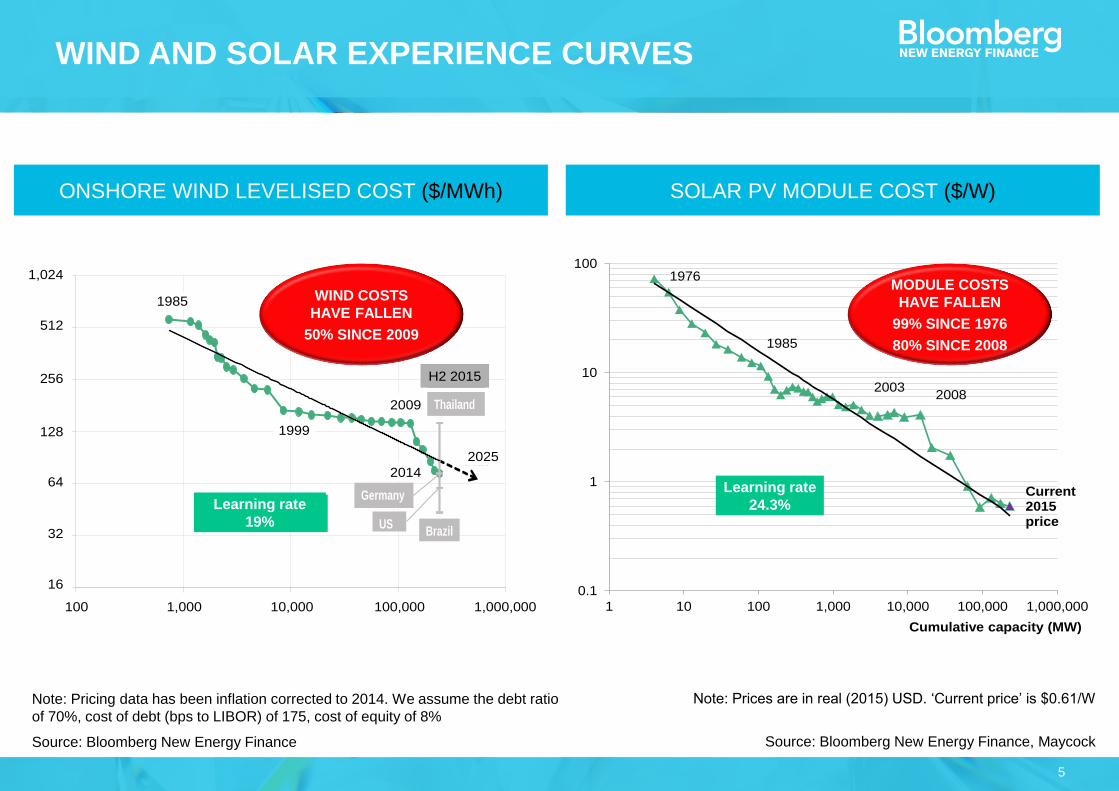

5

0.1

1

10

100

1 10 100 1,000 10,000 100,000 1,000,000

2003

1976

1985

2008

Cumulative capacity (MW)

Current 2015 price

WIND AND SOLAR EXPERIENCE CURVES

Note: Pricing data has been inflation corrected to 2014. We assume the debt ratio

of 70%, cost of debt (bps to LIBOR) of 175, cost of equity of 8%

Source: Bloomberg New Energy Finance

Note: Prices are in real (2015) USD. ‘Current price’ is $0.61/W

Source: Bloomberg New Energy Finance, Maycock

ONSHORE WIND LEVELISED COST ($/MWh) SOLAR PV MODULE COST ($/W)

Learning rate

24.3%

MODULE COSTS

HAVE FALLEN

99% SINCE 1976

80% SINCE 2008

y = 3,582.42x-0.30

R² = 0.91

16

32

64

128

256

512

1,024

100 1,000 10,000 100,000 1,000,000

1985

20252014

Learning rate =19%R² = 0.91

Thailand

Brazil

Germany

US

H1 2015

1999

2009

1,024

512

256

128

64

32

100 1,000 10,000

16

100,000 1,000,000

Learning rate 19%

1985

1999

2009

2014

2025

H2 2015

Learning rate

19%

WIND COSTS

HAVE FALLEN

50% SINCE 2009

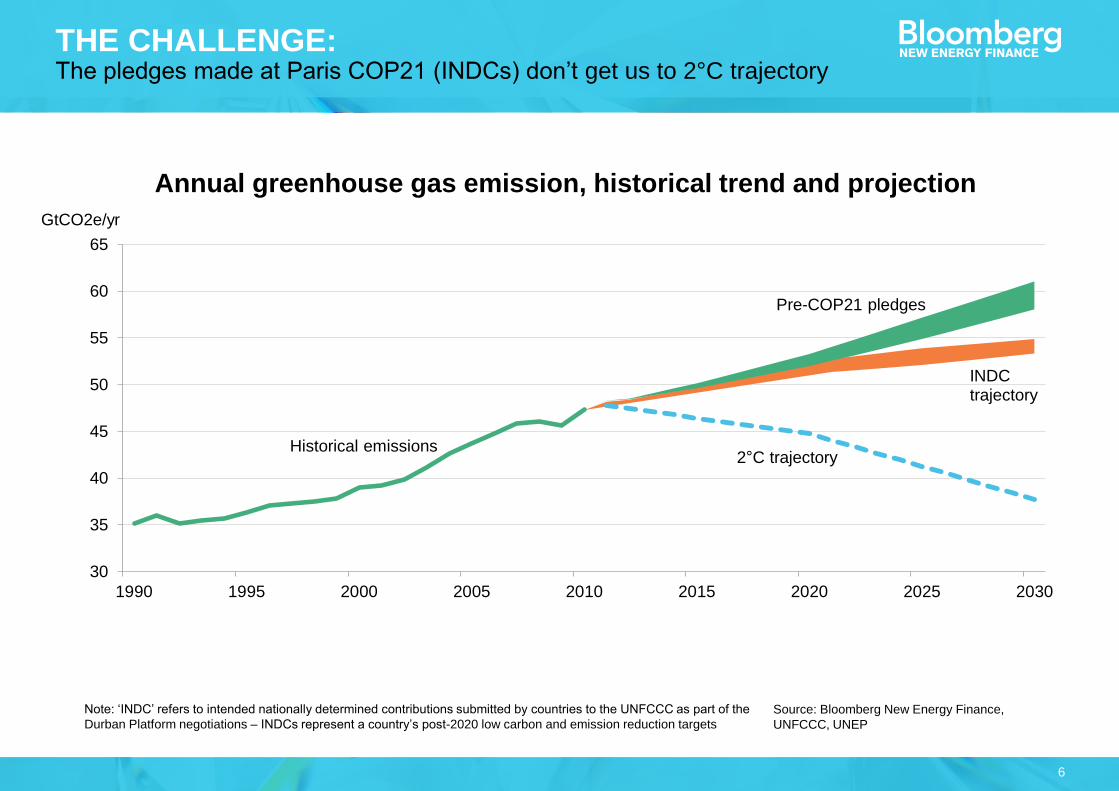

6

30

35

40

45

50

55

60

65

1990 1995 2000 2005 2010 2015 2020 2025 2030

Historical emissions2 C trajectory

INDC trajectory

Pre-COP21 pledges

GtCO2e/yr

THE CHALLENGE: The pledges made at Paris COP21 (INDCs) don’t get us to 2°C trajectory

Source: Bloomberg New Energy Finance,

UNFCCC, UNEP

Note: ‘INDC’ refers to intended nationally determined contributions submitted by countries to the UNFCCC as part of the

Durban Platform negotiations – INDCs represent a country’s post-2020 low carbon and emission reduction targets

Annual greenhouse gas emission, historical trend and projection

7

Source: Bloomberg New Energy Finance

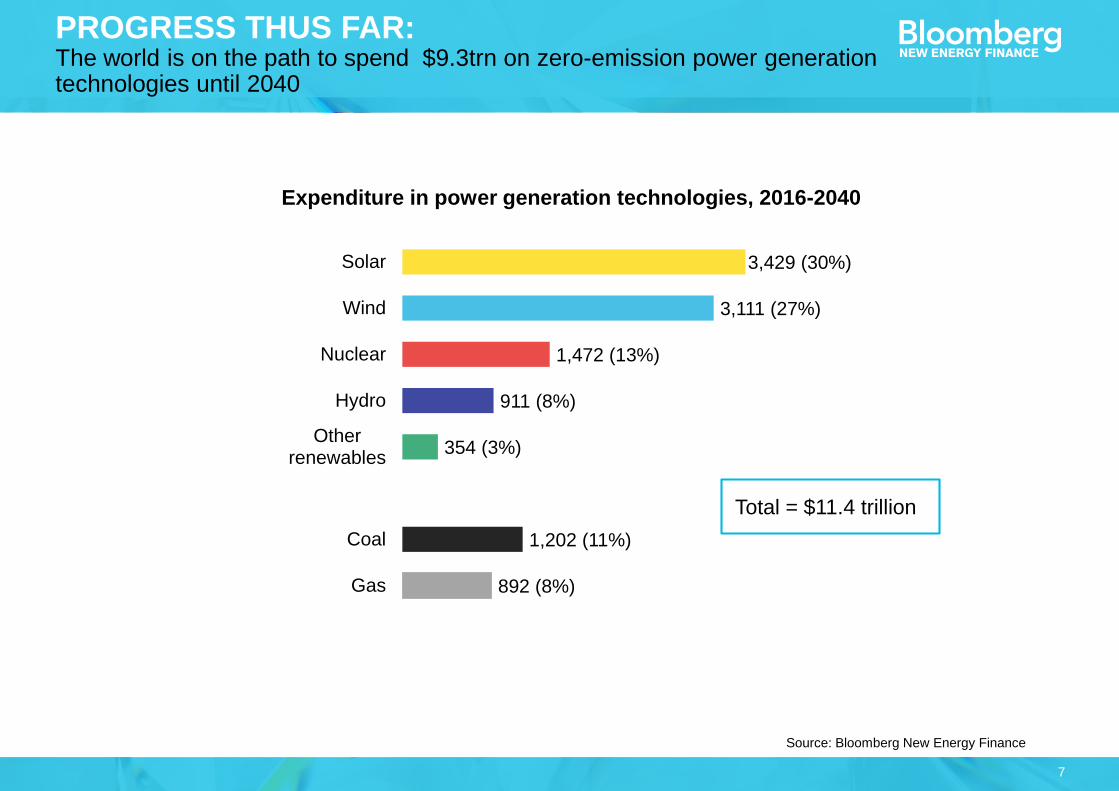

PROGRESS THUS FAR: The world is on the path to spend $9.3trn on zero-emission power generation technologies until 2040

Expenditure in power generation technologies, 2016-2040

3,429 (30%)

3,111 (27%)

1,472 (13%)

911 (8%)

354 (3%)

1,202 (11%)

892 (8%)

Solar

Wind

Nuclear

Hydro

Otherrenewables

Coal

Gas

Total = $11.4 trillion

8

Source: Bloomberg New Energy Finance

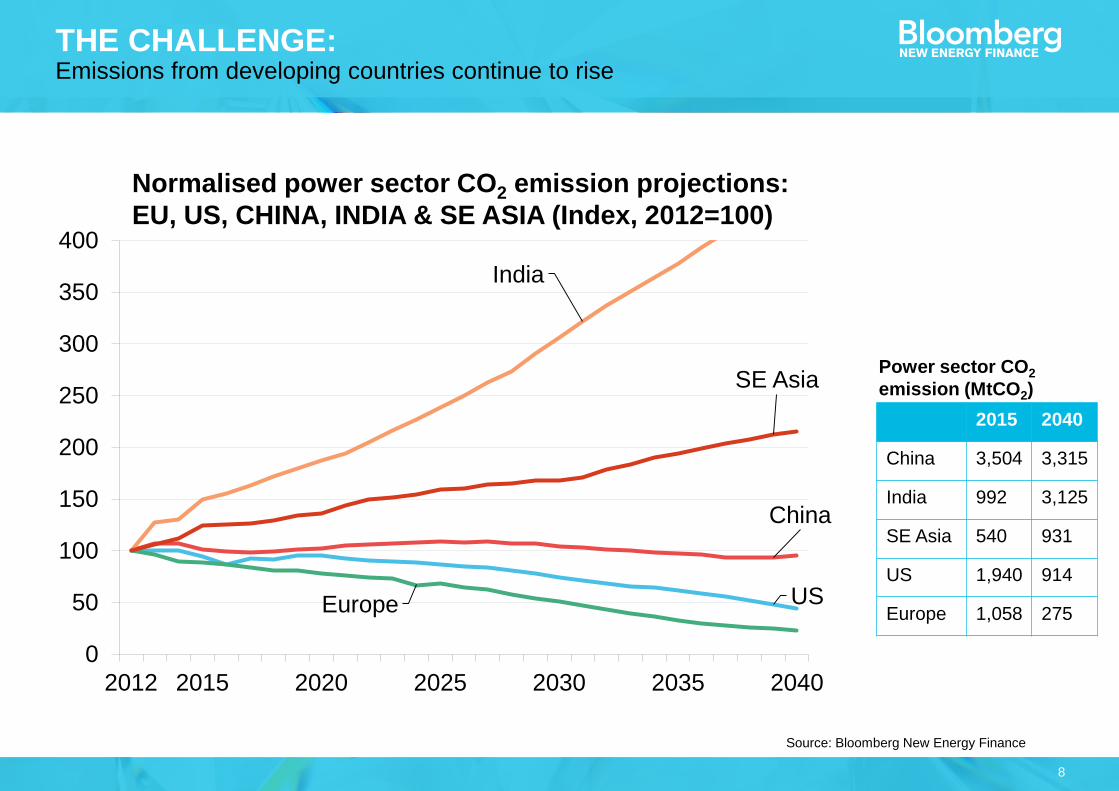

THE CHALLENGE:Emissions from developing countries continue to rise

China

USEurope

India

SE Asia

0

50

100

150

200

250

300

350

400

2012 2015 2020 2025 2030 2035 2040

Normalised power sector CO2 emission projections:

EU, US, CHINA, INDIA & SE ASIA (Index, 2012=100)

2015 2040

China 3,504 3,315

India 992 3,125

SE Asia 540 931

US 1,940 914

Europe 1,058 275

Power sector CO2

emission (MtCO2)

9

Source: Bloomberg New Energy Finance

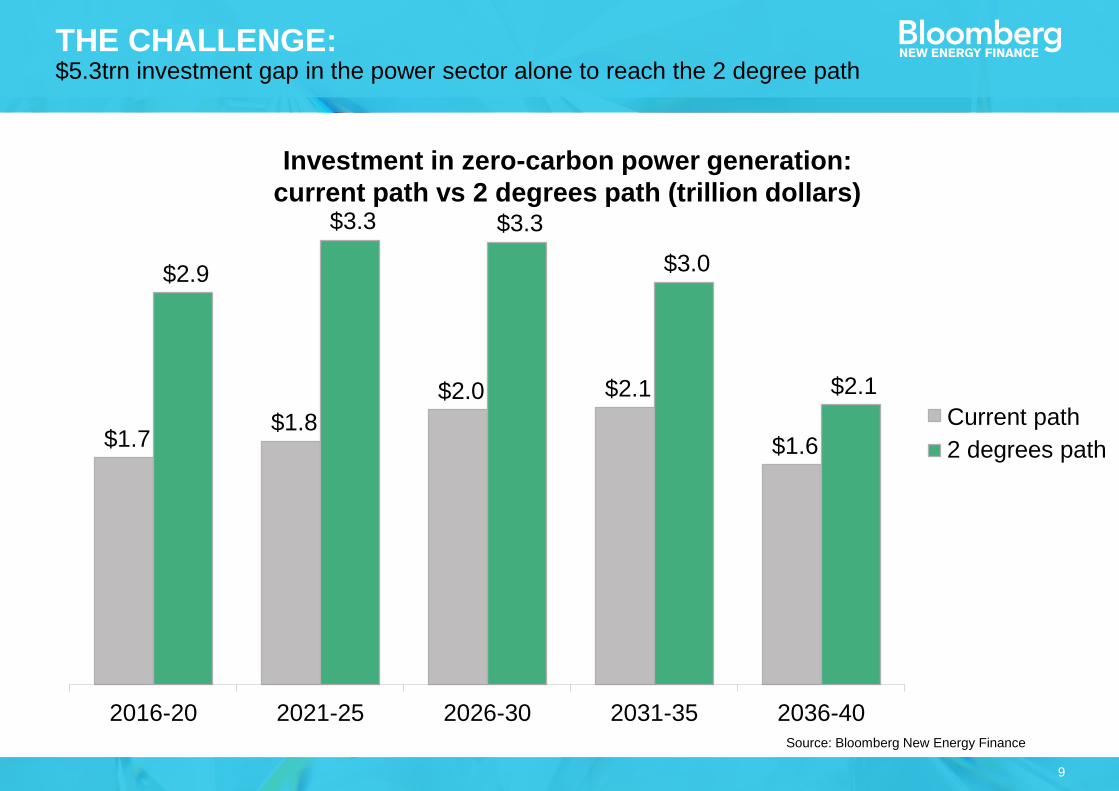

THE CHALLENGE: $5.3trn investment gap in the power sector alone to reach the 2 degree path

$1.7 $1.8

$2.0 $2.1

$1.6

$2.9

$3.3 $3.3

$3.0

$2.1

2016-20 2021-25 2026-30 2031-35 2036-40

NEO2016

2 degrees

Current path

2 degrees path

Investment in zero-carbon power generation:

current path vs 2 degrees path (trillion dollars)

10

This publication is the copyright of Bloomberg New Energy Finance. No portion of this document may be photocopied,

reproduced, scanned into an electronic system or transmitted, forwarded or distributed in any way without prior consent of

Bloomberg New Energy Finance.

The information contained in this publication is derived from carefully selected sources we believe are reasonable. We do

not guarantee its accuracy or completeness and nothing in this document shall be construed to be a representation of such

a guarantee. Any opinions expressed reflect the current judgment of the author of the relevant article or features, and does

not necessarily reflect the opinion of Bloomberg New Energy Finance, Bloomberg Finance L.P., Bloomberg L.P. or any of

their affiliates ("Bloomberg"). The opinions presented are subject to change without notice. Bloomberg accepts no

responsibility for any liability arising from use of this document or its contents. Nothing herein shall constitute or be

construed as an offering of financial instruments, or as investment advice or recommendations by Bloomberg of an

investment strategy or whether or not to "buy," "sell" or "hold" an investment.

COPYRIGHT AND DISCLAIMER

Unique analysis, tools and data for decision-makers

driving change in the energy system

MARKETS Renewable Energy

Energy Smart Technologies

Advanced Transport

Gas

Carbon and RECs

SERVICESAmericas Service

Asia Pacific Service

EMEA Service

Applied Research

Events and Workshops