Embed Size (px)

Citation preview

IS BIGGER BEST?E X A M I N I N G T H E E C O N O M I E S O F S C A L E O F R E N E W A B L E E N E R G Y

John Farrell Director of Energy Democracy

December 5, 2016

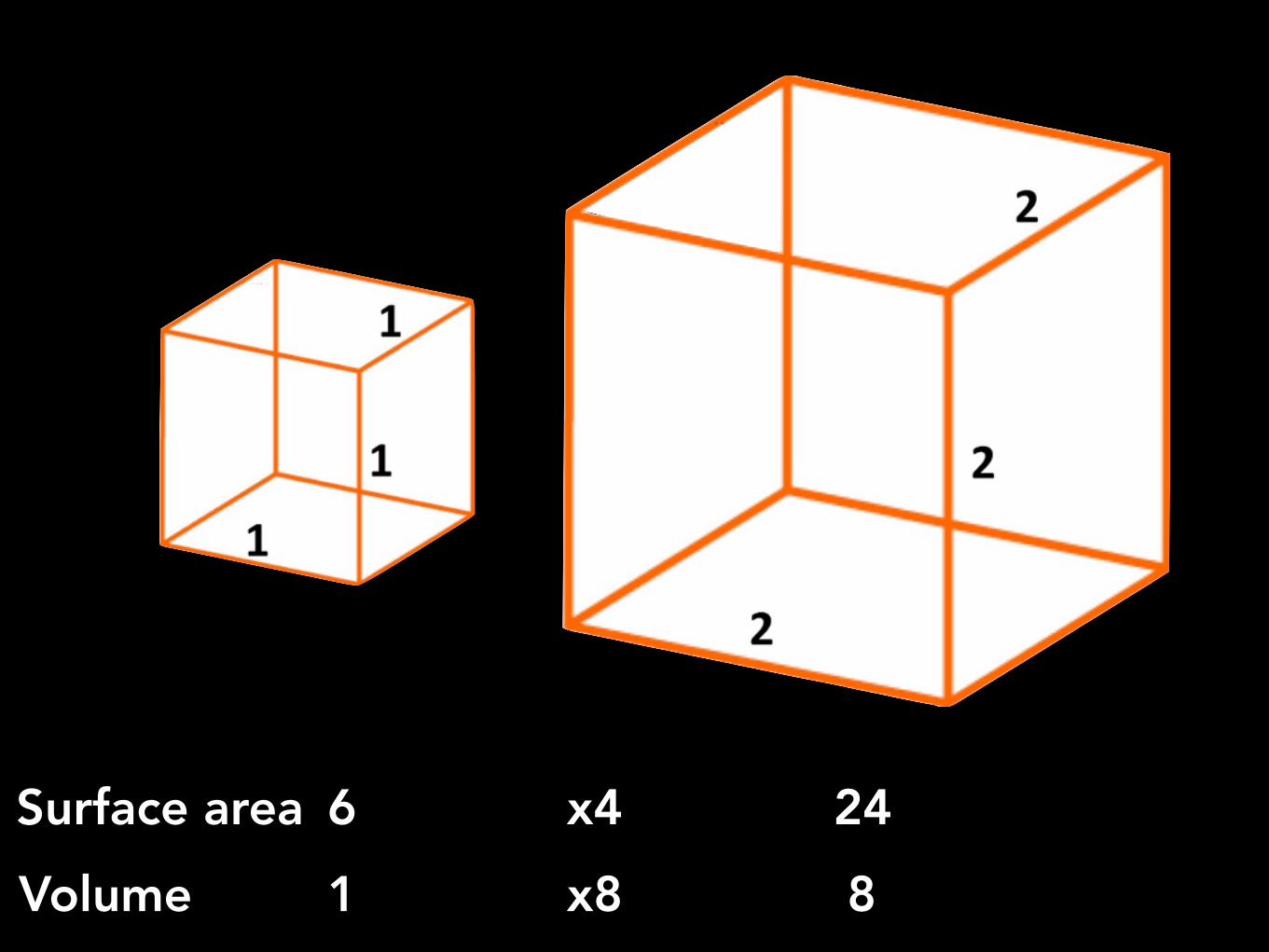

A H I S T O R Y O F B I G T H I N G S

Volume 1 8Surface area 6 24x4

x8

Ther

mal

Effi

cien

cy

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Maximum efficiency

Average efficiency

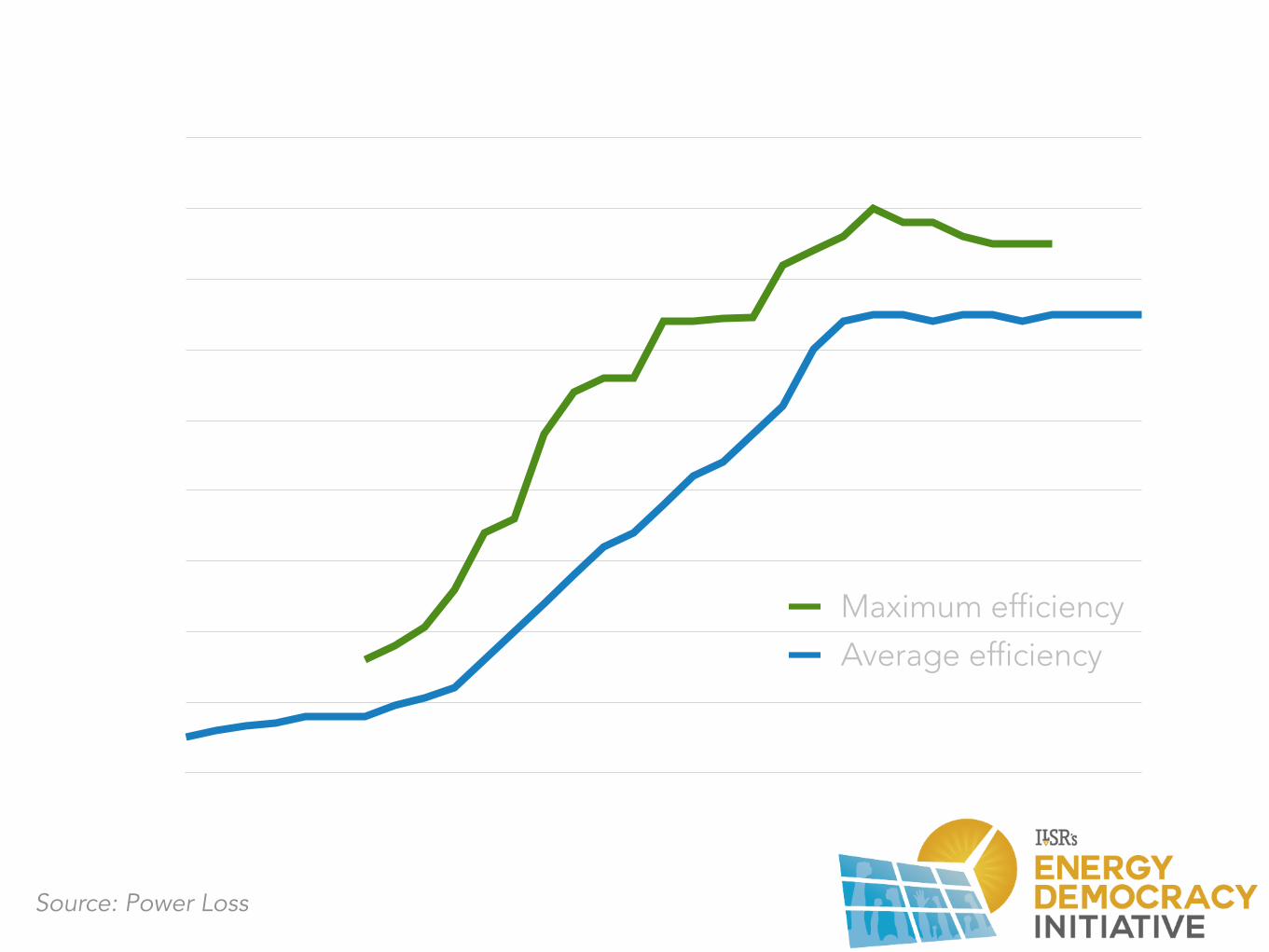

P O W E R P L A N T E F F I C I E N C Y

Source: Power Loss

1882 19941900 1925 1950 1975

W H I C H S TAT E T O P O W E R T H E M A L L ?

W H I C H S TAT E T O P O W E R T H E M A L L ?

W I N D P O W E R

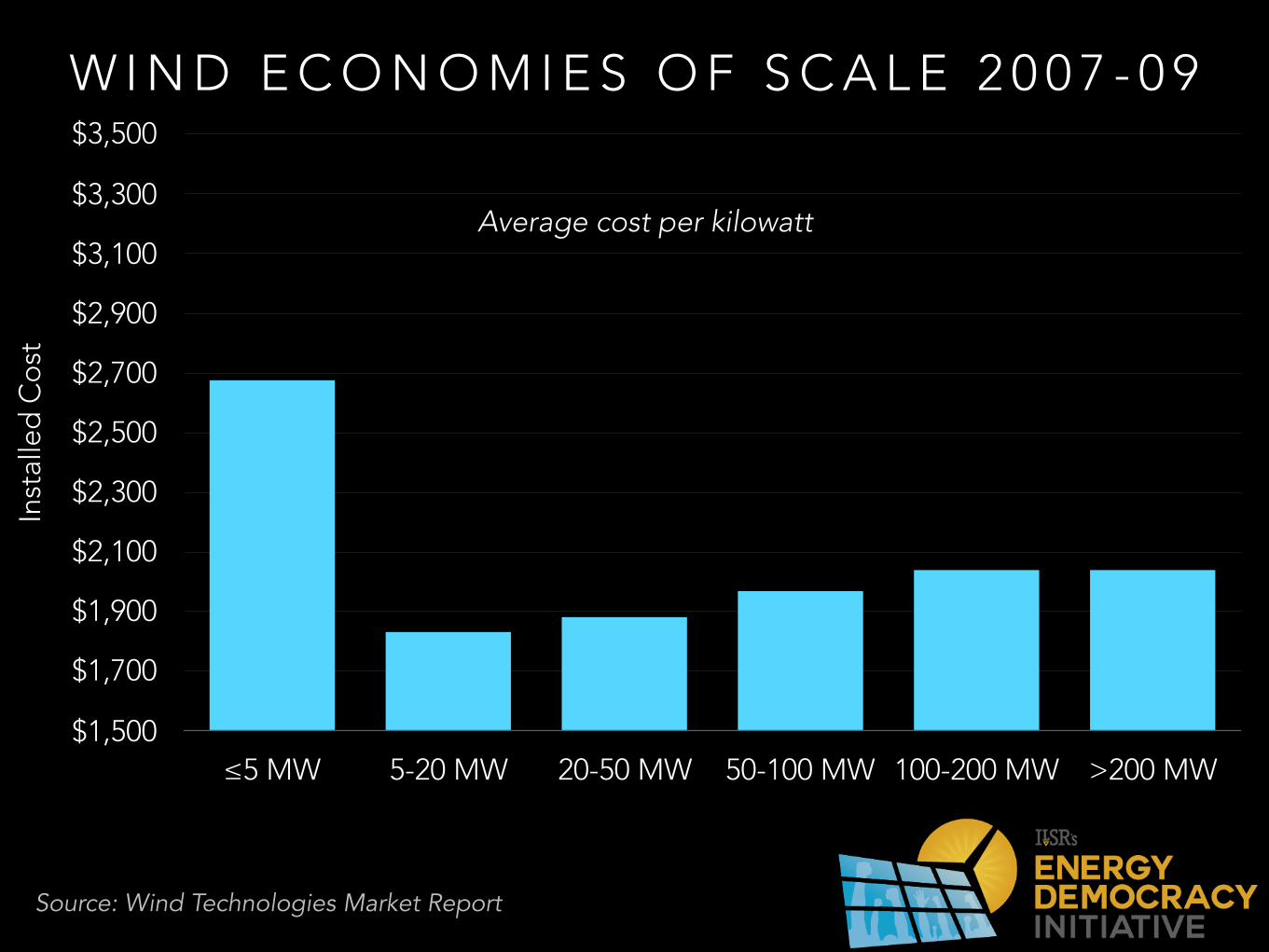

S U R P R I S I N G S AV I N G S I N S M A L L N E S S

Inst

alle

d C

ost

$1,500

$1,700

$1,900

$2,100

$2,300

$2,500

$2,700

$2,900

$3,100

$3,300

$3,500

≤5 MW 5-20 MW 20-50 MW 50-100 MW 100-200 MW >200 MW

W I N D E C O N O M I E S O F S C A L E 2 0 0 7 - 0 9

Source: Wind Technologies Market Report

Average cost per kilowatt

Inst

alle

d C

ost

$1,500

$1,700

$1,900

$2,100

$2,300

$2,500

$2,700

$2,900

$3,100

$3,300

$3,500

≤5 MW 5-20 MW 20-50 MW 50-100 MW 100-200 MW >200 MW

W I N D E C O N O M I E S O F S C A L E 2 0 0 7 - 0 9

Source: Wind Technologies Market Report

Average cost per kilowatt

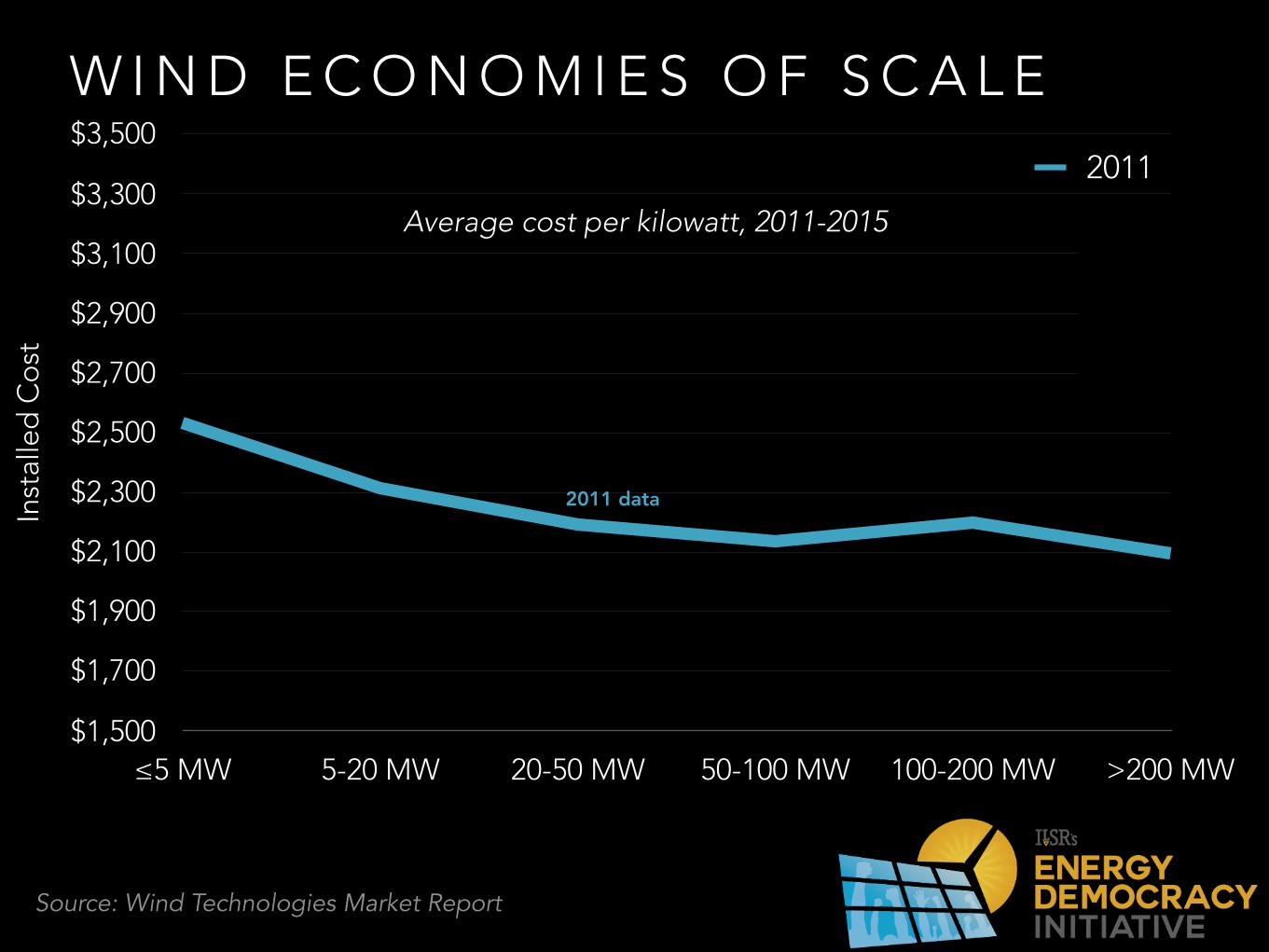

W I N D E C O N O M I E S O F S C A L EIn

stal

led

Co

st

$1,500

$1,700

$1,900

$2,100

$2,300

$2,500

$2,700

$2,900

$3,100

$3,300

$3,500

≤5 MW 5-20 MW 20-50 MW 50-100 MW 100-200 MW >200 MW

2011

2012

2013

2014

2015

Source: Wind Technologies Market Report

Average cost per kilowatt, 2011-2015

2011 data

W I N D E C O N O M I E S O F S C A L EIn

stal

led

Co

st

$1,500

$1,700

$1,900

$2,100

$2,300

$2,500

$2,700

$2,900

$3,100

$3,300

$3,500

≤5 MW 5-20 MW 20-50 MW 50-100 MW 100-200 MW >200 MW

2011

2012

2013

2014

2015

Source: Wind Technologies Market Report

Average cost per kilowatt, 2011-2015

2011 data

2015 data

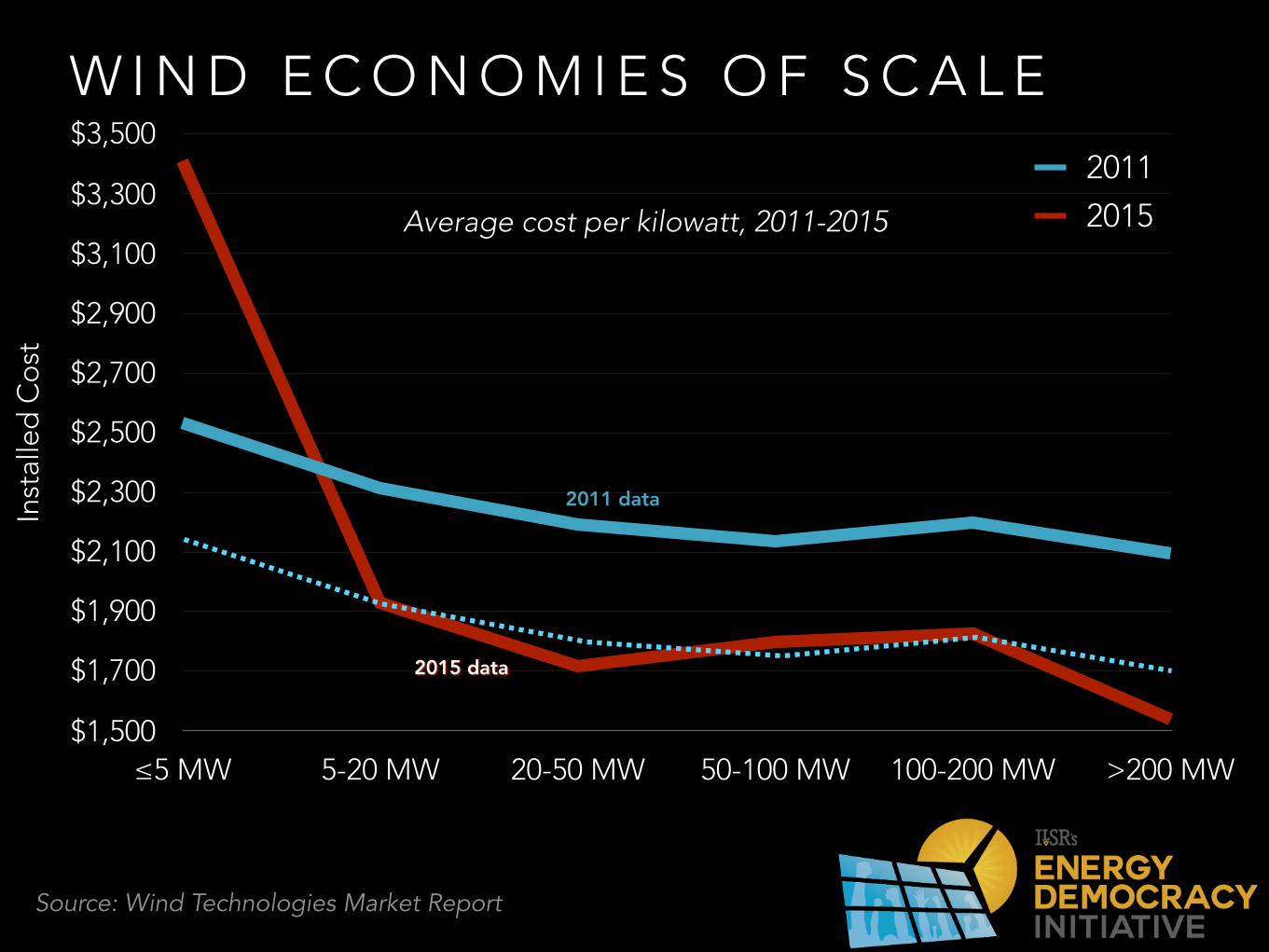

W I N D E C O N O M I E S O F S C A L EIn

stal

led

Co

st

$1,500

$1,700

$1,900

$2,100

$2,300

$2,500

$2,700

$2,900

$3,100

$3,300

$3,500

≤5 MW 5-20 MW 20-50 MW 50-100 MW 100-200 MW >200 MW

2011

2015

Source: Wind Technologies Market Report

Average cost per kilowatt, 2011-2015

2011 data

2015 data

W I N D E C O N O M I E S O F S C A L EIn

stal

led

Co

st

0%

20%

40%

60%

80%

100%

120%

140%

≤5 MW 5-20 MW 20-50 MW 50-100 MW 100-200 MW >200 MW

84%87%88%92%100%

131%Average cost per kilowatt as a percentage of 5-20 MW wind projects,

2011-2015 average data

Source: Wind Technologies Market Report

$2,191/kW

B E N E F I T S O F L O C A L

W I N D V. W I R E S : R E L AT I V E C O S T O F G E T T I N G W I N D P O W E R F R O M FA R A W AY

Source: ILSR

250 500 750 1000

10% 108% 131% 154% 176%

20% 93% 116% 139% 162%

30% 78% 101% 124% 147%

40% 64% 86% 109% 132%

50% 49% 72% 94% 117%

60% 34% 57% 80% 102%

Distance from electric customers (miles)

Baseline cost of 3.6¢ per kilowatt-hour

Incr

ease

in w

ind

sp

eed

W I N D V. W I R E S : R E L AT I V E C O S T O F G E T T I N G W I N D P O W E R F R O M FA R A W AY

Source: ILSR

250 500 750 1000

10% 108% 131% 154% 176%

20% 93% 116% 139% 162%

30% 78% 101% 124% 147%

40% 64% 86% 109% 132%

50% 49% 72% 94% 117%

60% 34% 57% 80% 102%

Distance from electric customers (miles)

Transmission cost outweighs wind speed benefit

Baseline cost of 3.6¢ per kilowatt-hour

Incr

ease

in w

ind

sp

eed

Transmission lowers cost

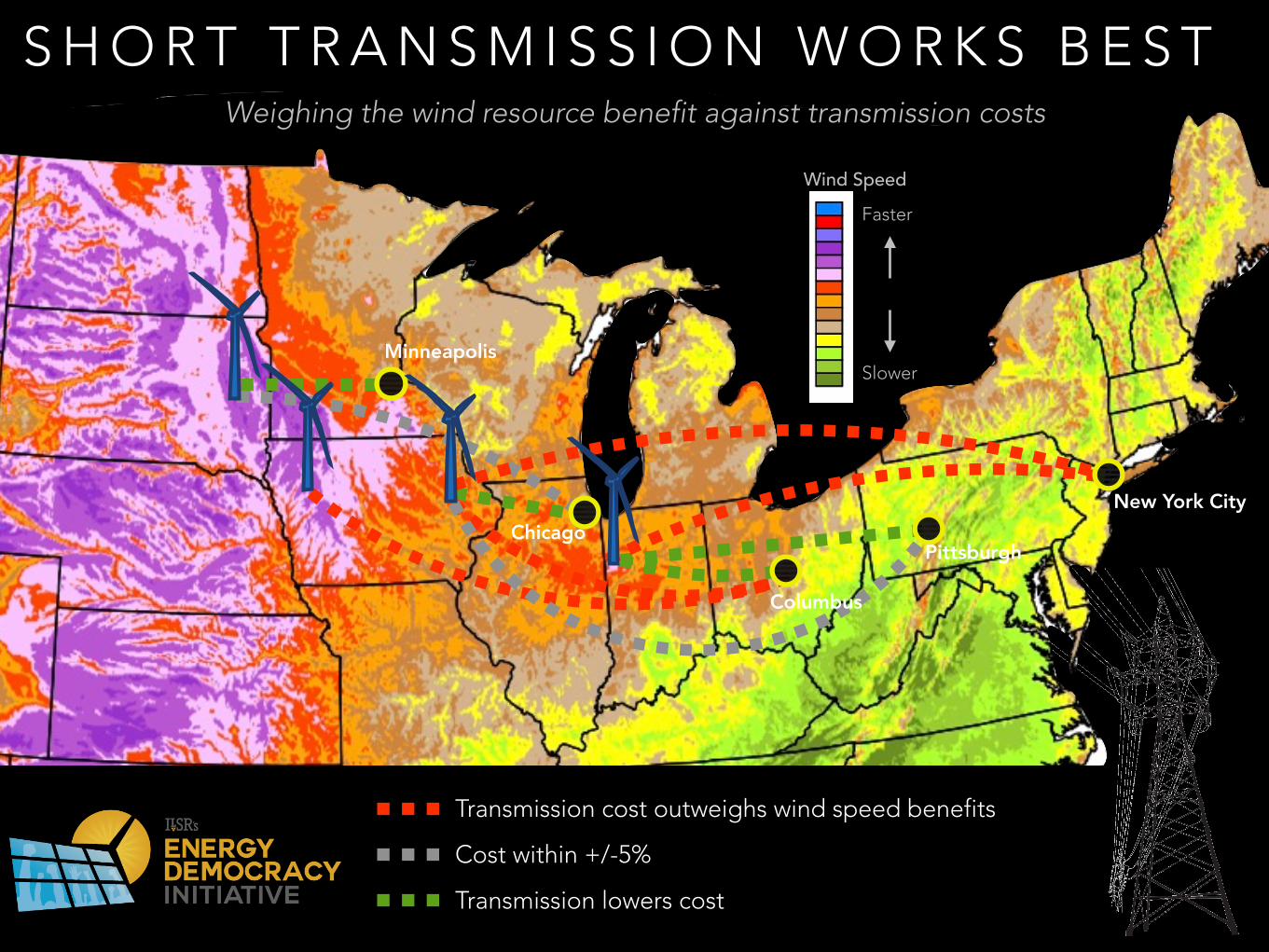

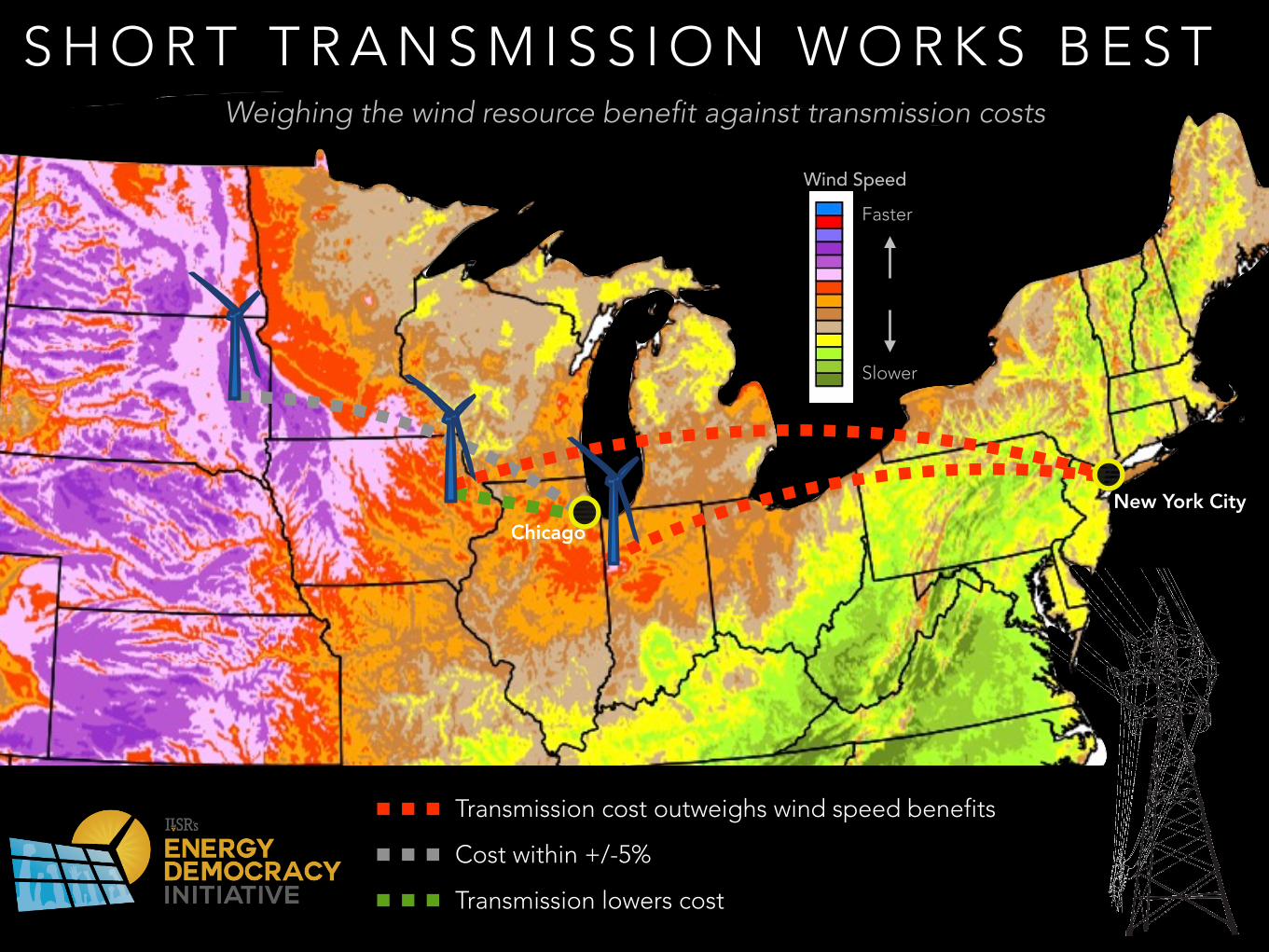

S H O R T T R A N S M I S S I O N W O R K S B E S TWeighing the wind resource benefit against transmission costs

Transmission cost outweighs wind speed benefits

Minneapolis

Chicago

Columbus

Pittsburgh

New York City

Transmission lowers cost

Cost within +/-5%

Wind SpeedFaster

Slower

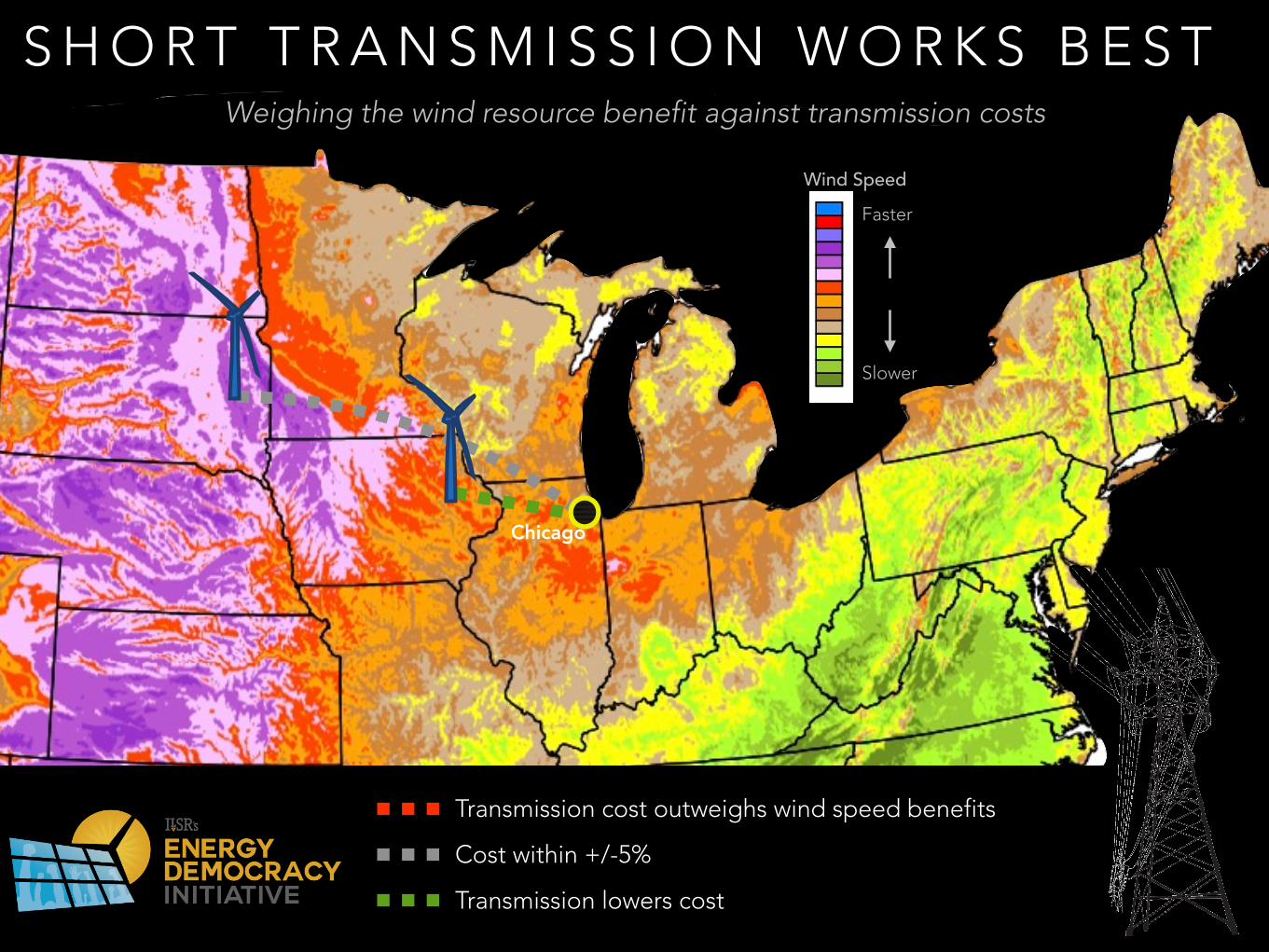

S H O R T T R A N S M I S S I O N W O R K S B E S TWeighing the wind resource benefit against transmission costs

Transmission cost outweighs wind speed benefits

Chicago

Transmission lowers cost

Cost within +/-5%

Wind SpeedFaster

Slower

S H O R T T R A N S M I S S I O N W O R K S B E S TWeighing the wind resource benefit against transmission costs

Transmission cost outweighs wind speed benefits

ChicagoNew York City

Transmission lowers cost

Cost within +/-5%

Wind SpeedFaster

Slower

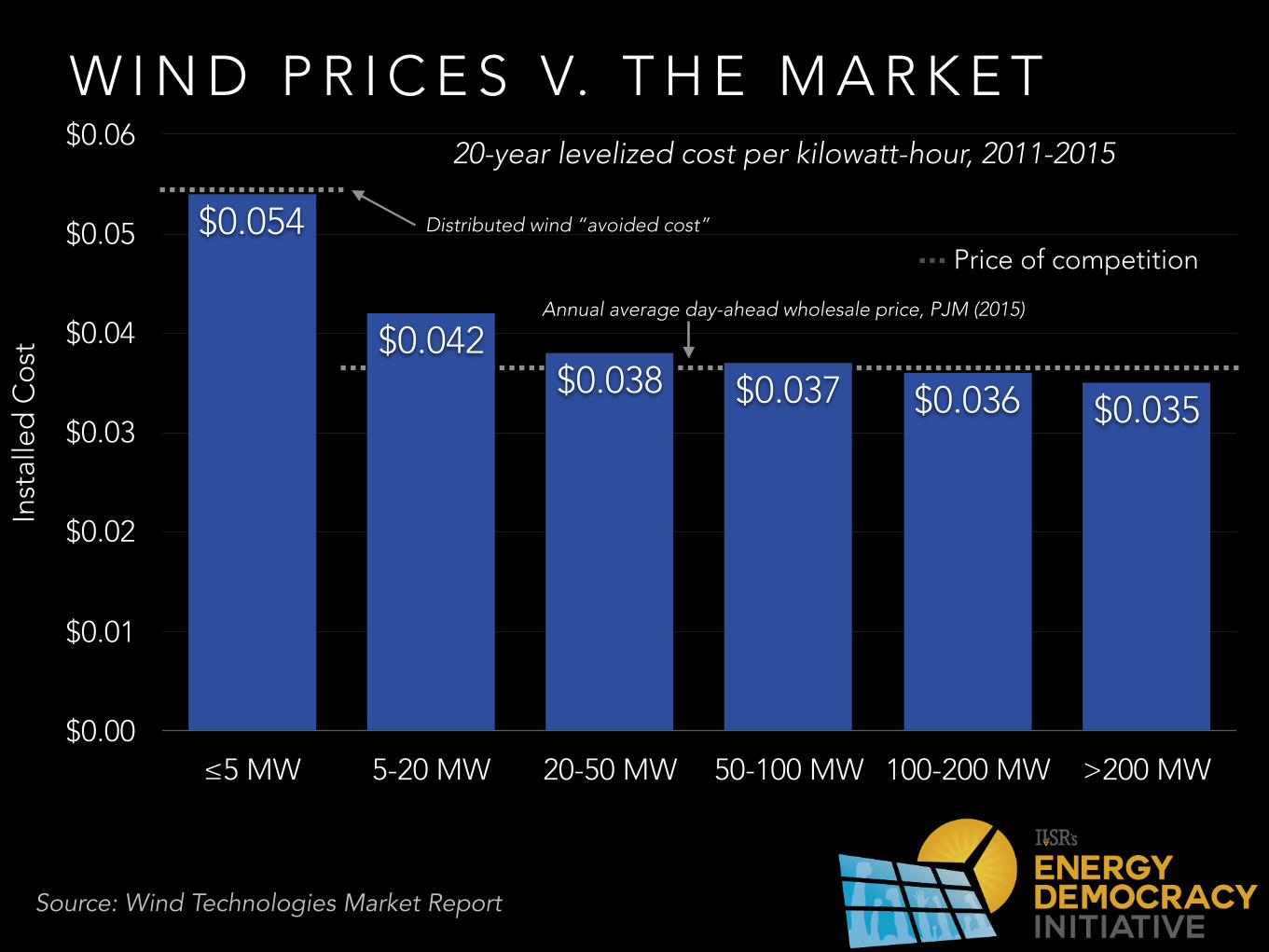

T H E P R I C E T H AT M AT T E R S

W I N D P R I C E S V. T H E M A R K E T20-year levelized cost per kilowatt-hour, 2011-2015

Source: Wind Technologies Market Report

Price of competition

Annual average day-ahead wholesale price, PJM (2015)

Distributed wind “avoided cost”

Inst

alle

d C

ost

$0.00

$0.01

$0.02

$0.03

$0.04

$0.05

$0.06

≤5 MW 5-20 MW 20-50 MW 50-100 MW 100-200 MW >200 MW

$0.035$0.036$0.037$0.038$0.042

$0.054

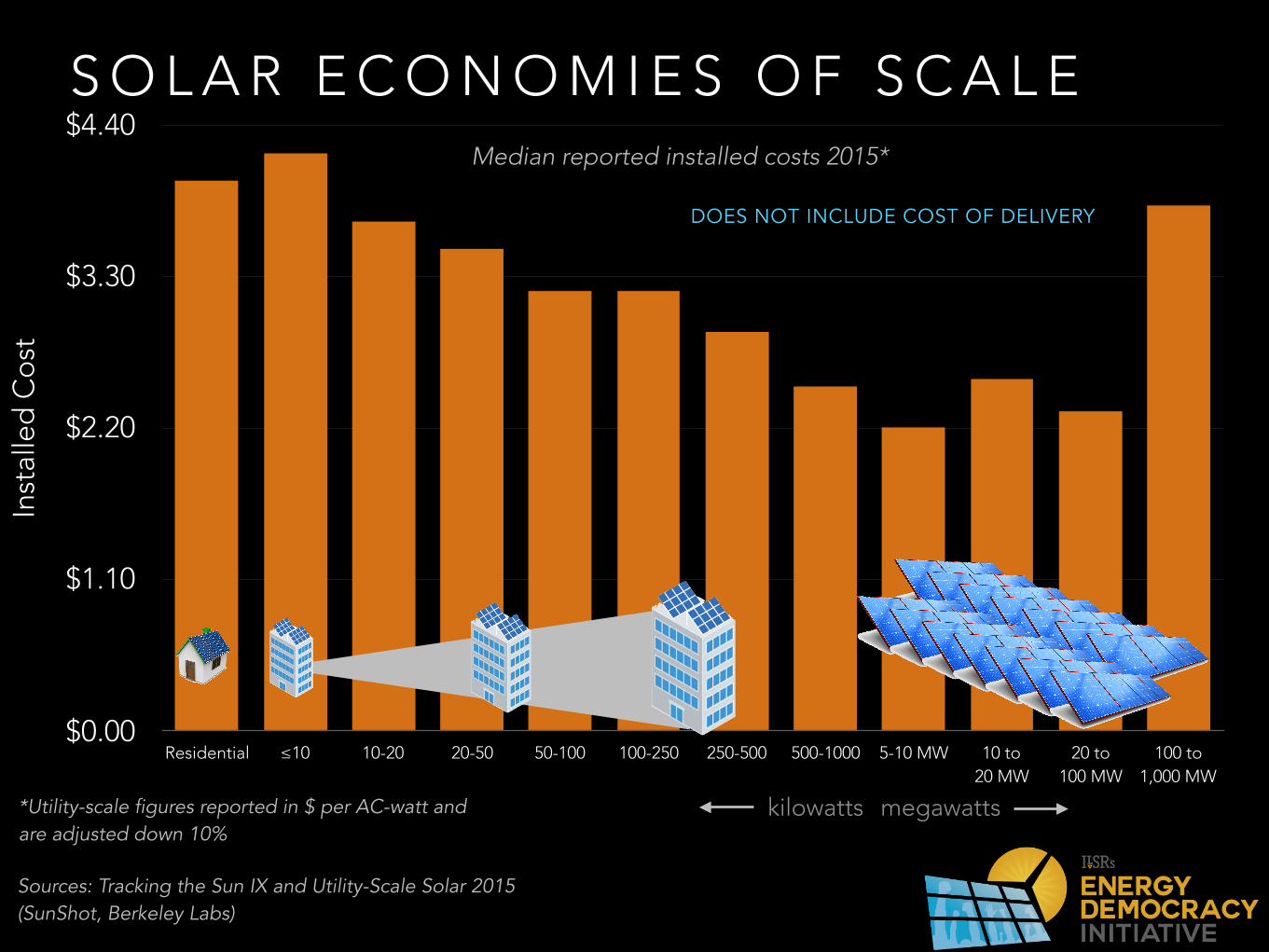

S O L A R P O W E R

S O L A R E C O N O M I E S O F S C A L EIn

stal

led

Co

st

$0.00

$1.10

$2.20

$3.30

$4.40

Residential ≤10 10-20 20-50 50-100 100-250 250-500 500-1000 5-10 MW 10 to 20 MW

20 to 100 MW

100 to 1,000 MW

Median reported installed costs 2015*

kilowatts megawatts

Sources: Tracking the Sun IX and Utility-Scale Solar 2015 (SunShot, Berkeley Labs)

DOES NOT INCLUDE COST OF DELIVERY

*Utility-scale figures reported in $ per AC-watt and are adjusted down 10%

S O L A R E C O N O M I E S O F S C A L EC

ost

of e

lect

ricity

0.0¢

2.0¢

4.0¢

6.0¢

8.0¢

10.0¢

12.0¢

14.0¢

Residential ≤10 10-20 20-50 50-100 100-250 250-500 500-1000 5-10 MW 10 to 20 MW

20 to 100 MW

100 to 1,000 MW

Estimated levelized cost of electricity based on reported 2015 costs*

kilowatts megawatts

Sources: Tracking the Sun IX and Utility-Scale Solar 2015 (SunShot, Berkeley Labs); SAM (NREL); ILSR

DOES NOT INCLUDE COST OF DELIVERY

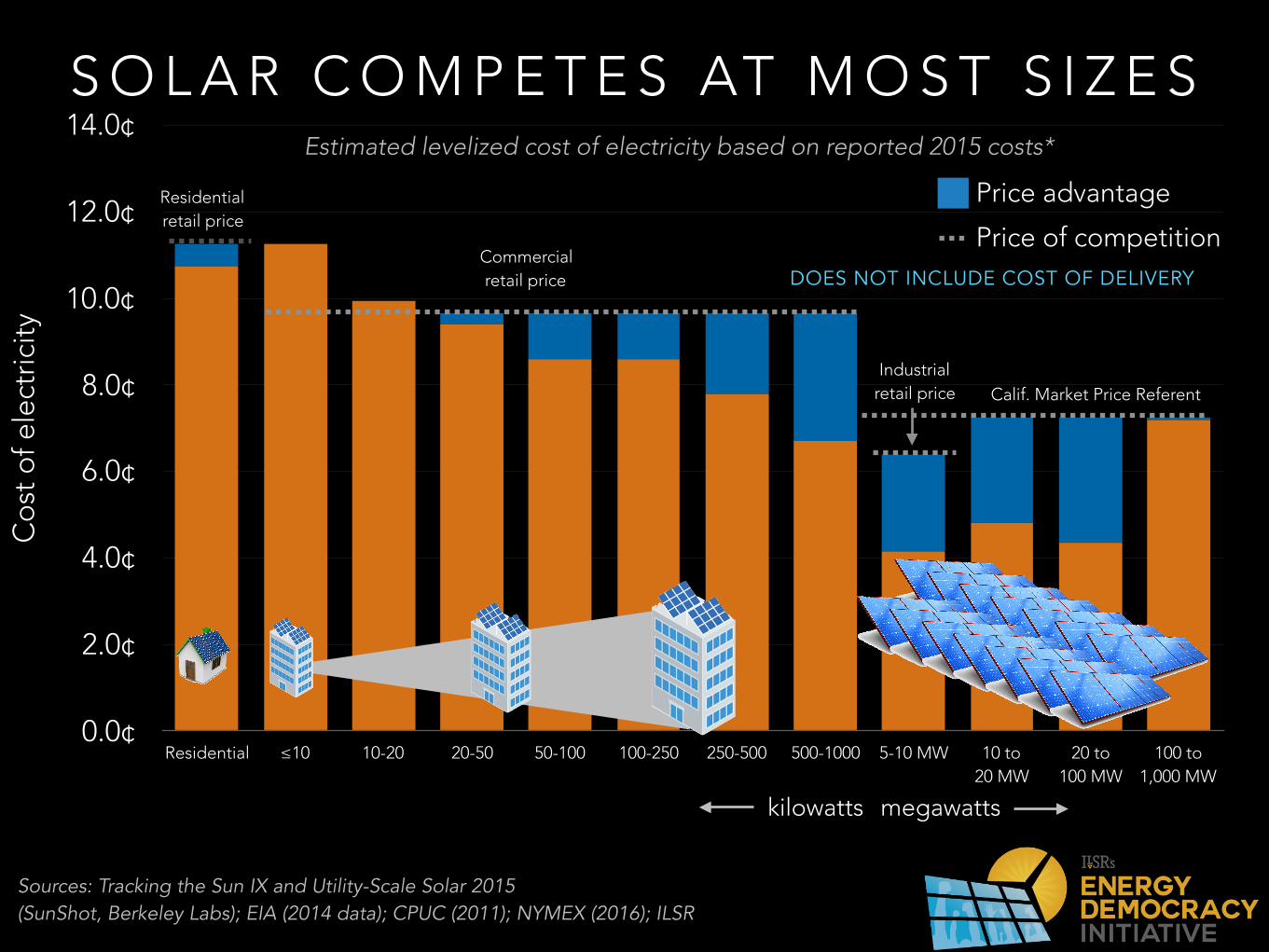

T H E P R I C E T H AT M AT T E R S

Co

st o

f ele

ctric

ity

0.0¢

2.0¢

4.0¢

6.0¢

8.0¢

10.0¢

12.0¢

14.0¢

Residential ≤10 10-20 20-50 50-100 100-250 250-500 500-1000 5-10 MW 10 to 20 MW

20 to 100 MW

100 to 1,000 MW

S O L A R C O M P E T E S AT M O S T S I Z E S

kilowatts megawatts

Sources: Tracking the Sun IX and Utility-Scale Solar 2015 (SunShot, Berkeley Labs); EIA (2014 data); CPUC (2011); NYMEX (2016); ILSR

DOES NOT INCLUDE COST OF DELIVERY

Residential retail price

Commercial retail price

Industrial retail price Calif. Market Price Referent

Price of competition

Price advantage

Estimated levelized cost of electricity based on reported 2015 costs*

S I Z A B L E D E P L O Y M E N T S

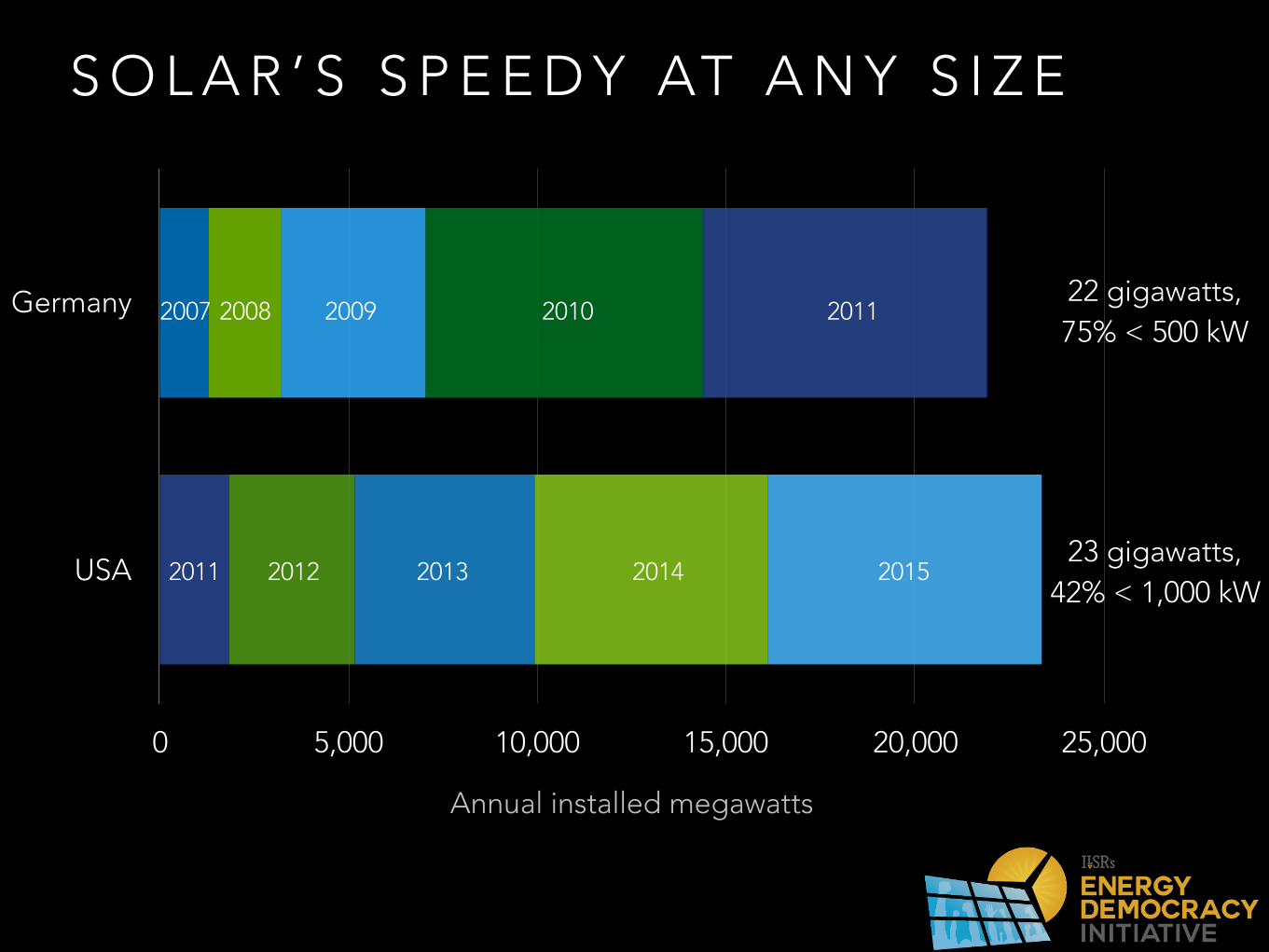

S O L A R ’ S S P E E D Y AT A N Y S I Z E

Germany

USA

Annual installed megawatts

0 5,000 10,000 15,000 20,000 25,000

22 gigawatts, 75% < 500 kW

23 gigawatts, 42% < 1,000 kW

2007 2008 2009 2010 2011

2011 2012 2013 2014 2015

Inst

alle

d C

ost

($/W

att)

Germany Japan USA Australia France

$2.10

$1.60

$3.50

$2.10

$1.20

$2.60

$1.80

$4.00

$2.90

$1.70

Residential

Small Non-residential

$0.0 $1.3 $2.5 $3.8 $5.0

33 GW 32 GW

12 GW

5 GW 4 GW

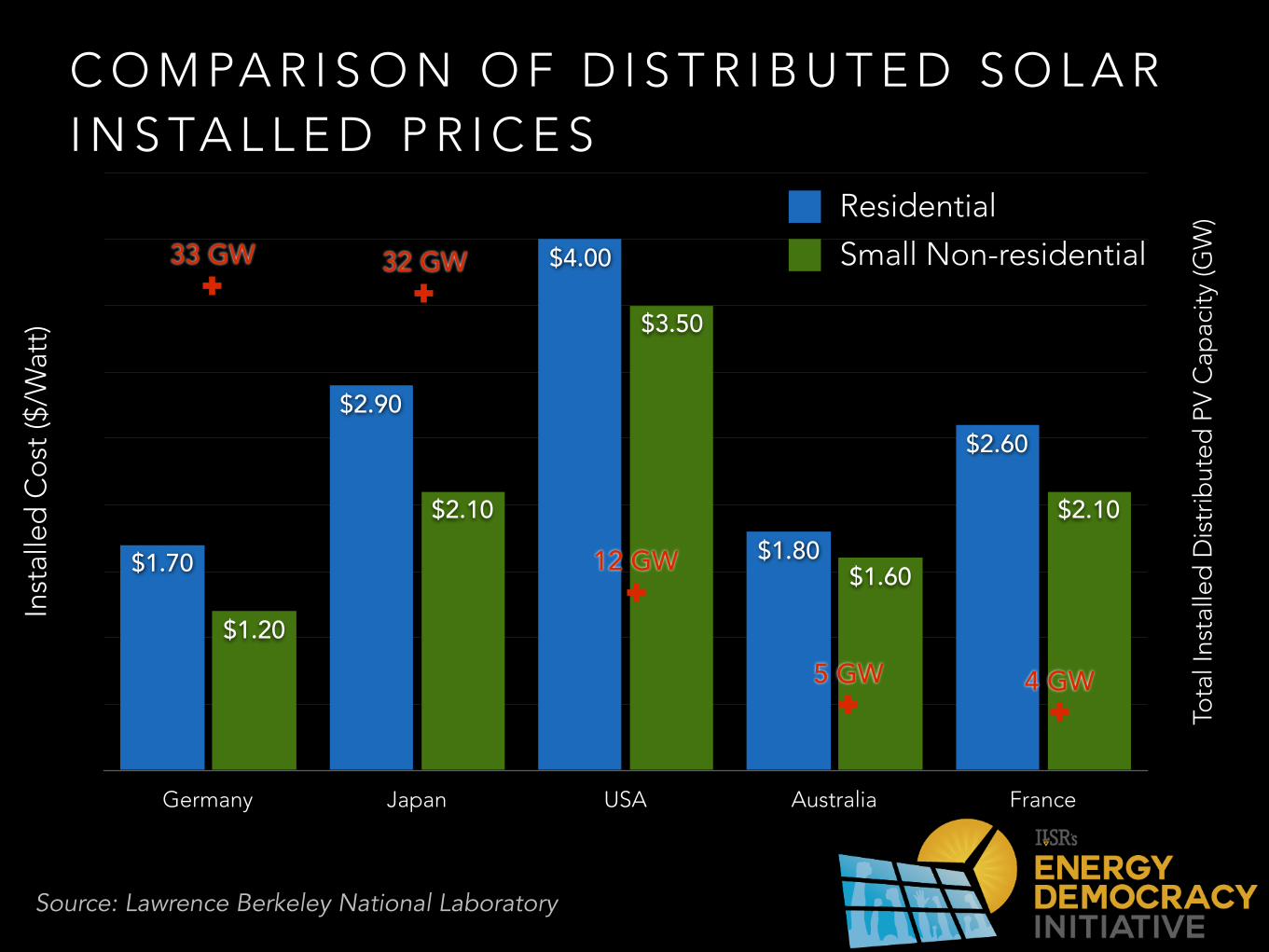

C O M PA R I S O N O F D I S T R I B U T E D S O L A R I N S TA L L E D P R I C E S

Tota

l Ins

talle

d D

istr

ibut

ed P

V C

apac

ity (G

W)

Source: Lawrence Berkeley National Laboratory

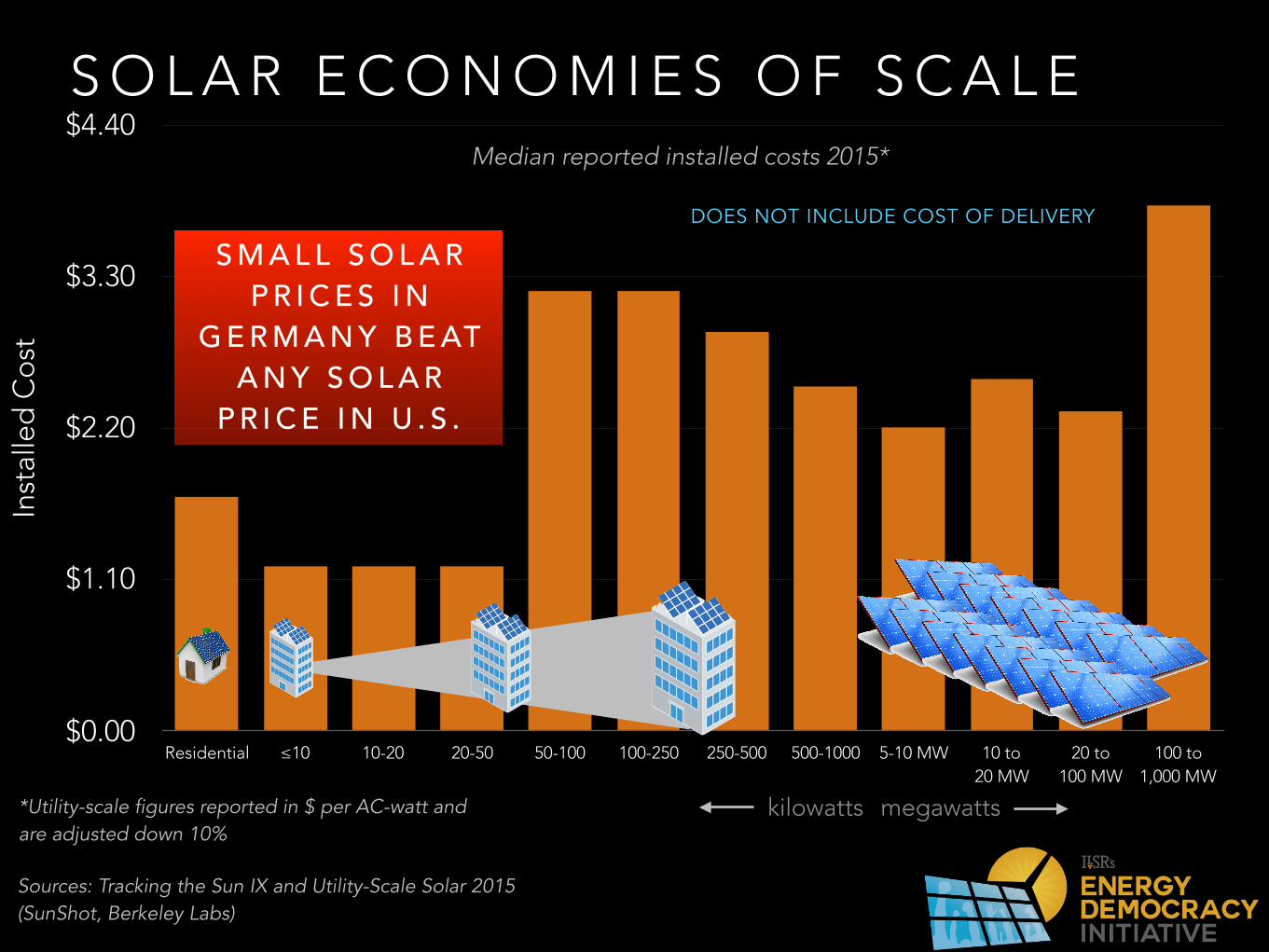

S O L A R E C O N O M I E S O F S C A L EIn

stal

led

Co

st

$0.00

$1.10

$2.20

$3.30

$4.40

Residential ≤10 10-20 20-50 50-100 100-250 250-500 500-1000 5-10 MW 10 to 20 MW

20 to 100 MW

100 to 1,000 MW

Median reported installed costs 2015*

kilowatts megawatts

Sources: Tracking the Sun IX and Utility-Scale Solar 2015 (SunShot, Berkeley Labs)

DOES NOT INCLUDE COST OF DELIVERY

*Utility-scale figures reported in $ per AC-watt and are adjusted down 10%

S M A L L S O L A R P R I C E S I N

G E R M A N Y B E AT A N Y S O L A R

P R I C E I N U . S .

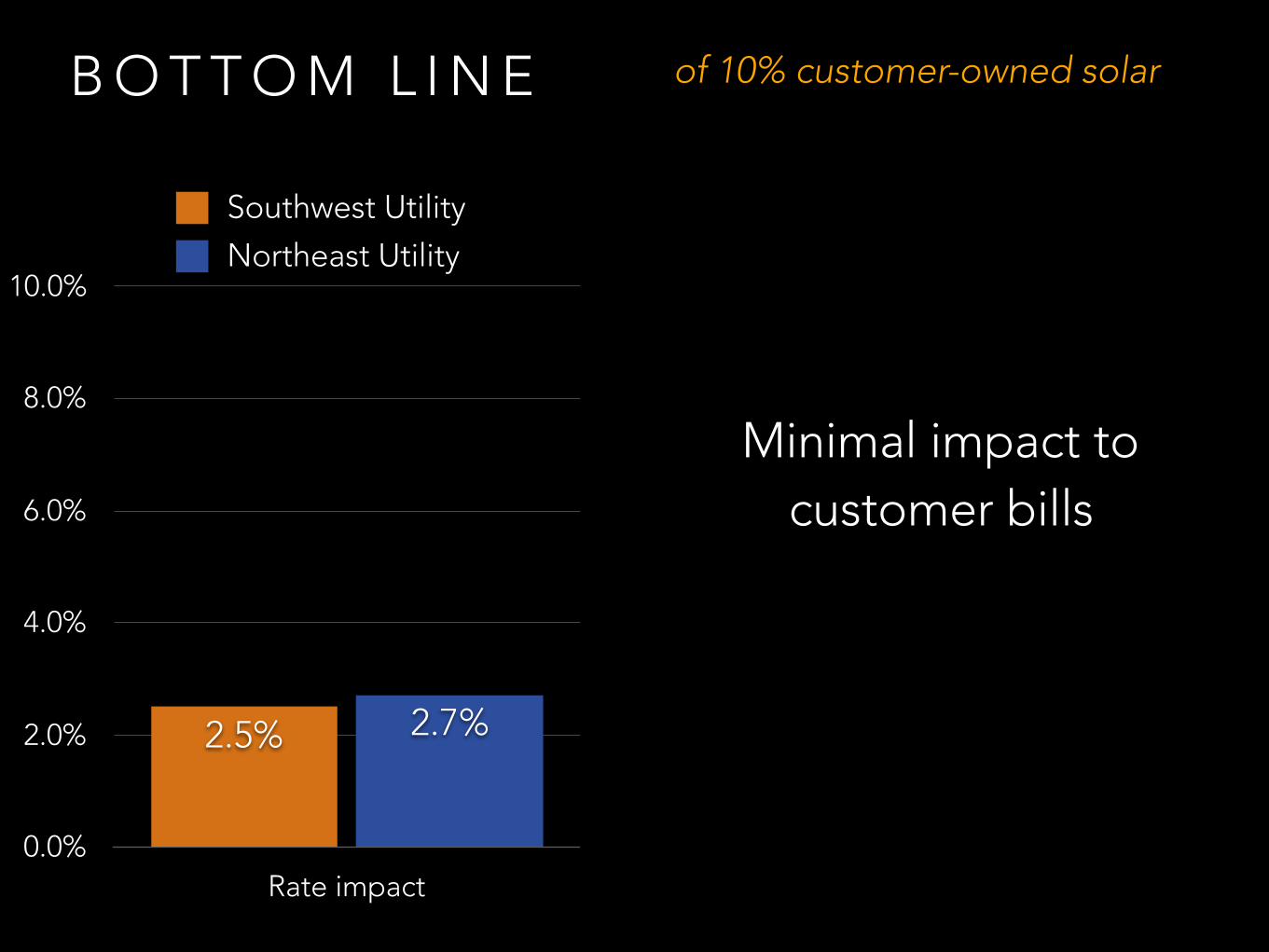

B O T T O M L I N E ?

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

Rate impact

2.7%2.5%

Southwest Utility

Northeast Utility

B O T T O M L I N E of 10% customer-owned solar

Minimal impact to customer bills

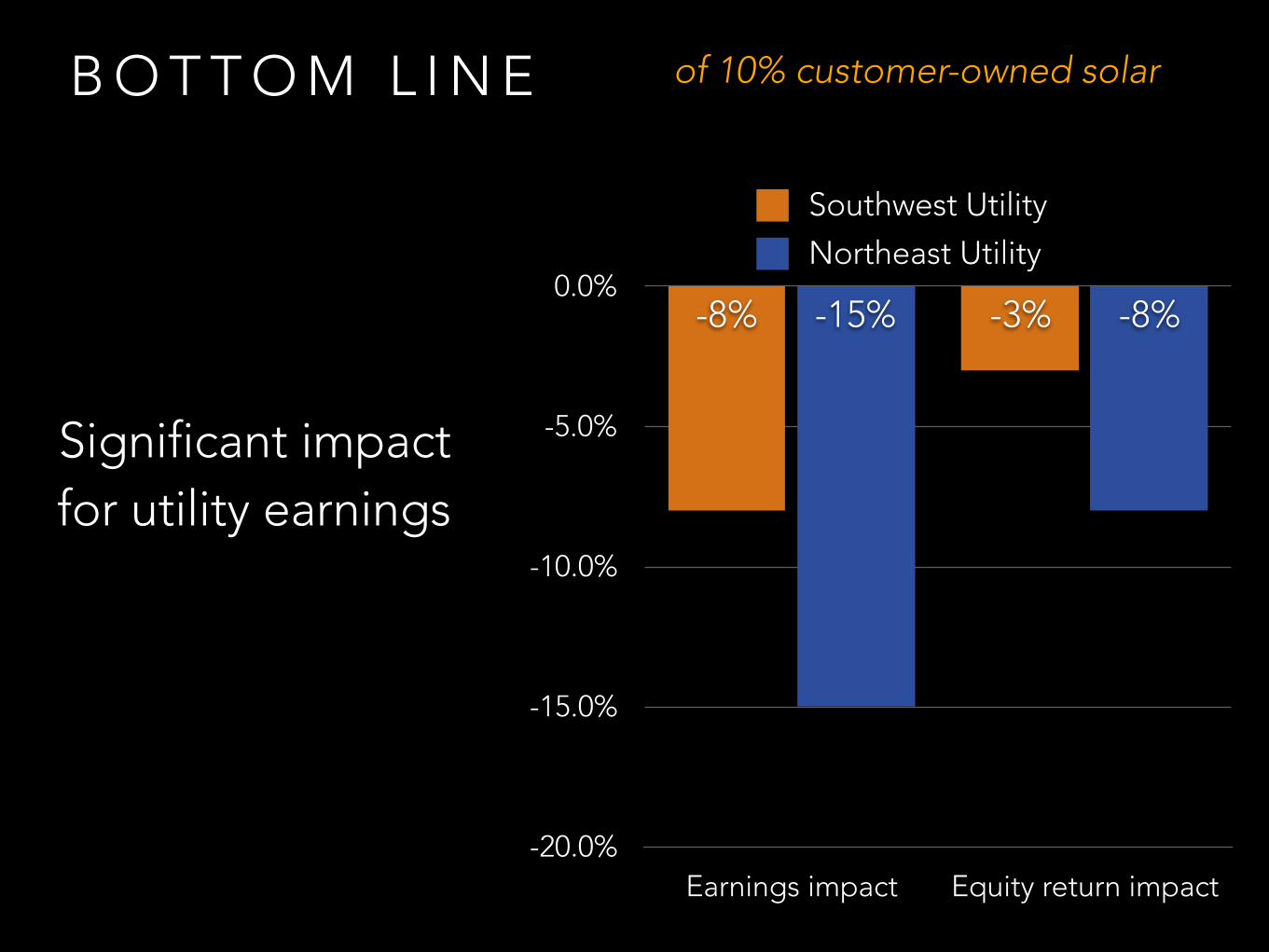

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

Earnings impact Equity return impact

-8%-15% -3%-8%

Southwest Utility

Northeast Utility

B O T T O M L I N E of 10% customer-owned solar

Significant impact for utility earnings

W H O C A R E S ?

“There is one great advantage that must follow regulation, and

that advantage is protection"

“We come to work each day to do what we did the day before”

3.2

3.3

3.4

3.5

3.6

3.7

3.8

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

I N W H AT Y E A R S D I D E L E C T R I C I T Y S A L E S P E A K ?

trillion kilowatt-hours

3.2

3.3

3.4

3.5

3.6

3.7

3.8

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

P E A K

S TA G N A N T R E TA I L S A L E S

trillion kilowatt-hours

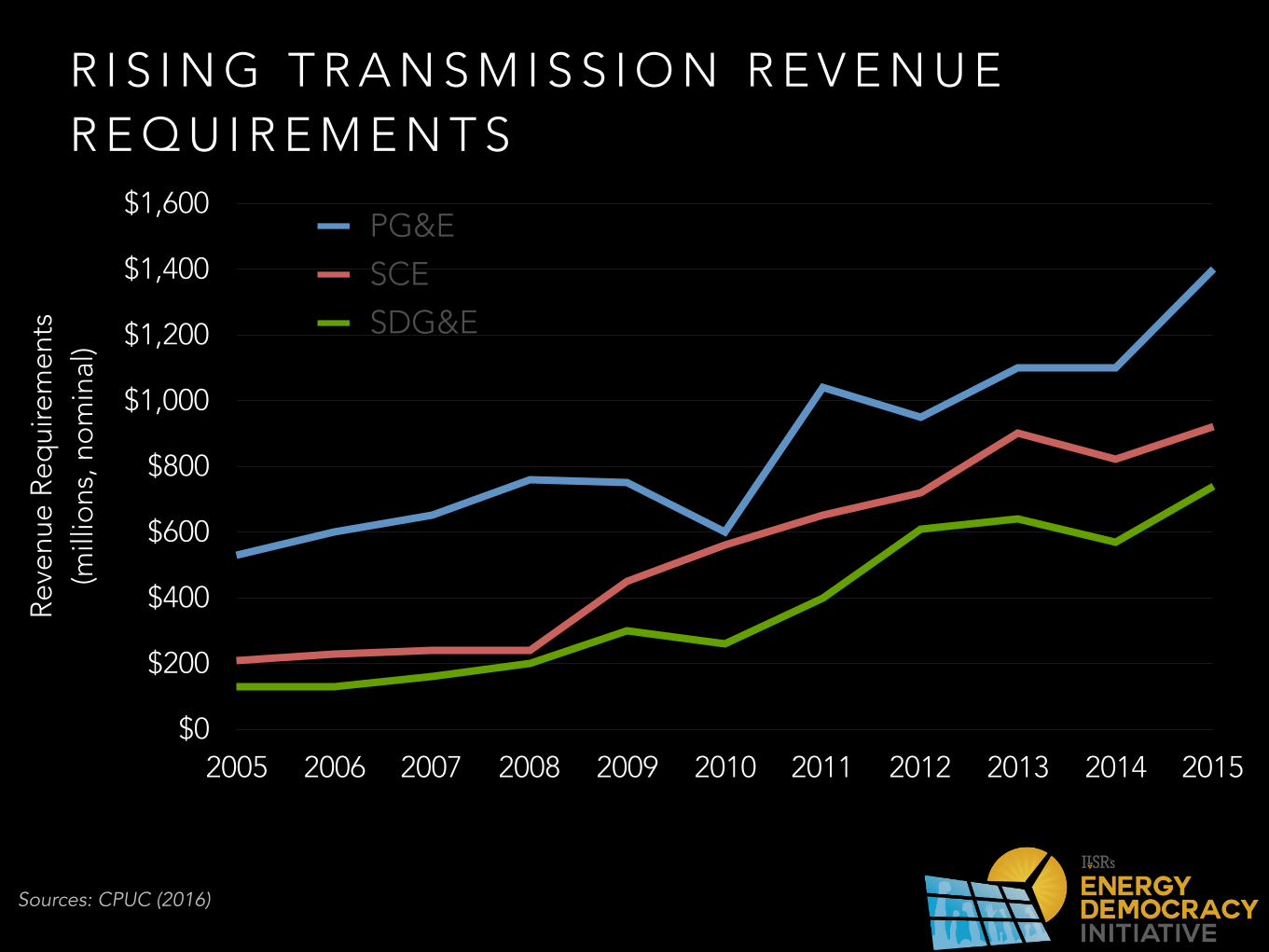

Reve

nue

Req

uire

men

ts

(mill

ions

, no

min

al)

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

PG&E

SCE

SDG&E

R I S I N G T R A N S M I S S I O N R E V E N U E R E Q U I R E M E N T S

Sources: CPUC (2016)

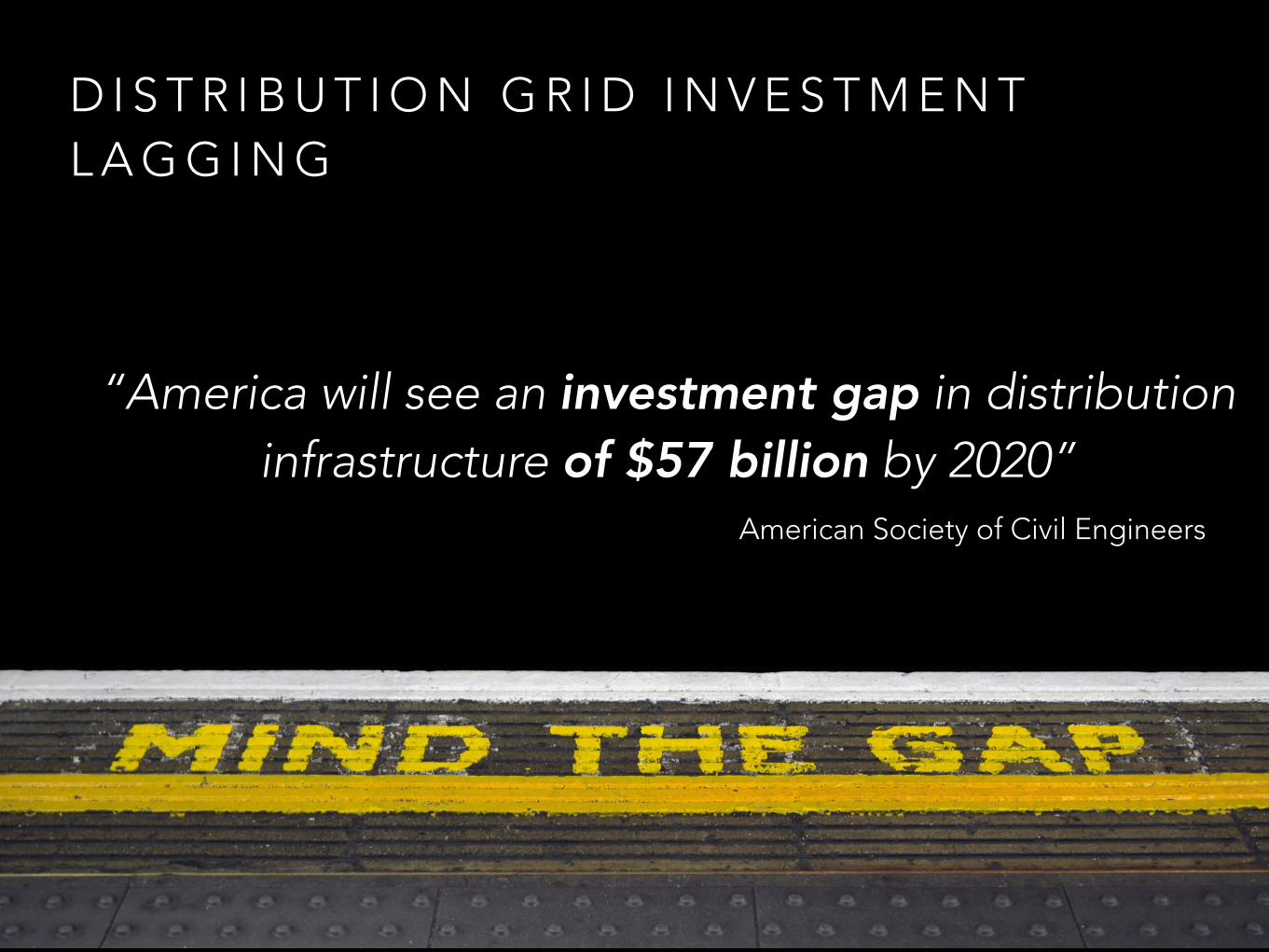

D I S T R I B U T I O N G R I D I N V E S T M E N T L A G G I N G

American Society of Civil Engineers

“America will see an investment gap in distribution infrastructure of $57 billion by 2020”

F R E E D O M T O G E N E R AT E U N D E R F I R ESTATES FACING CHALLENGES TO DISTRIBUTED POWER

May 2016- Q1 2016 action- No recent action

Source: The 50 States of Solar: Q1 2016, NC Clean Energy Technology

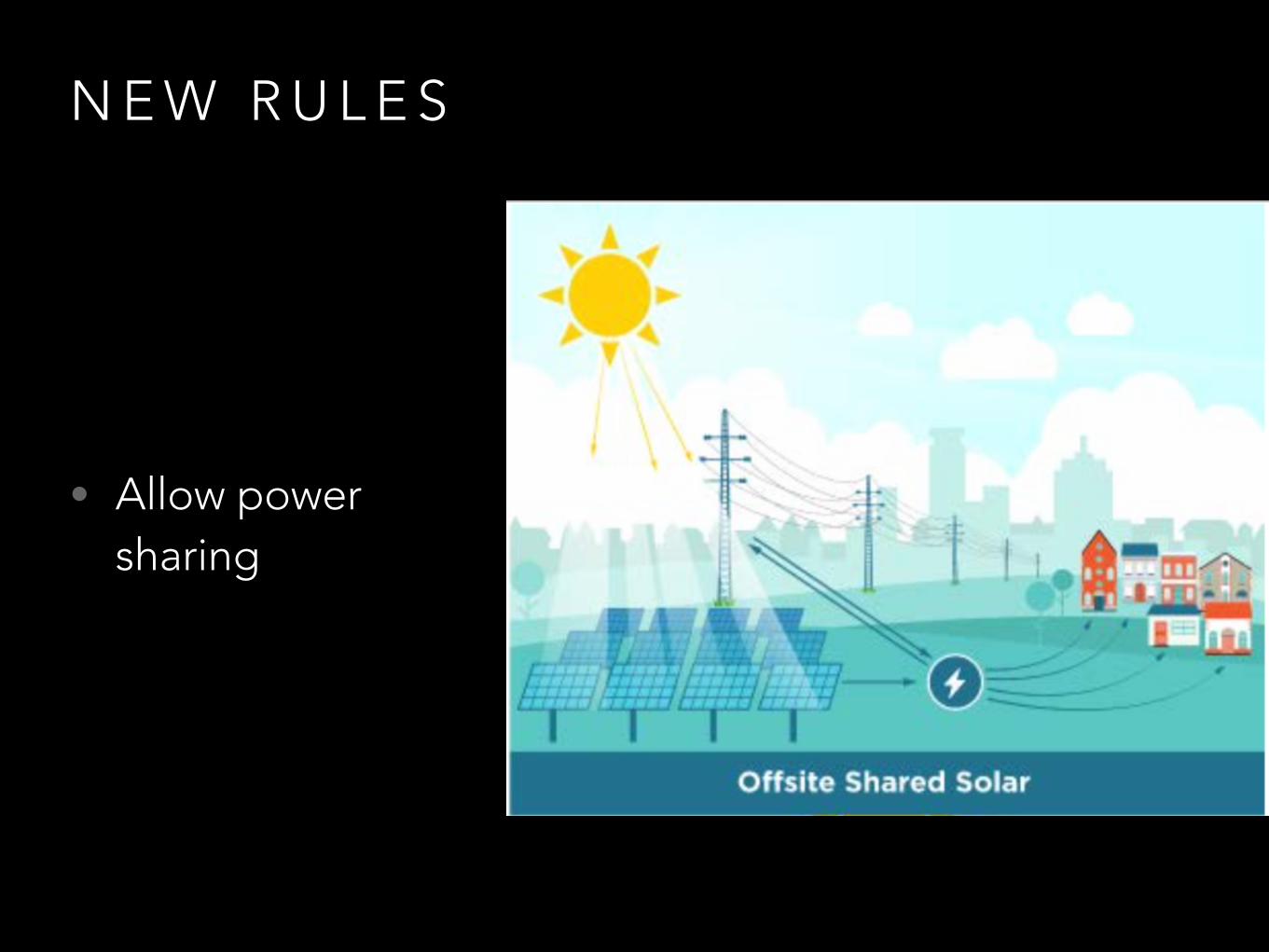

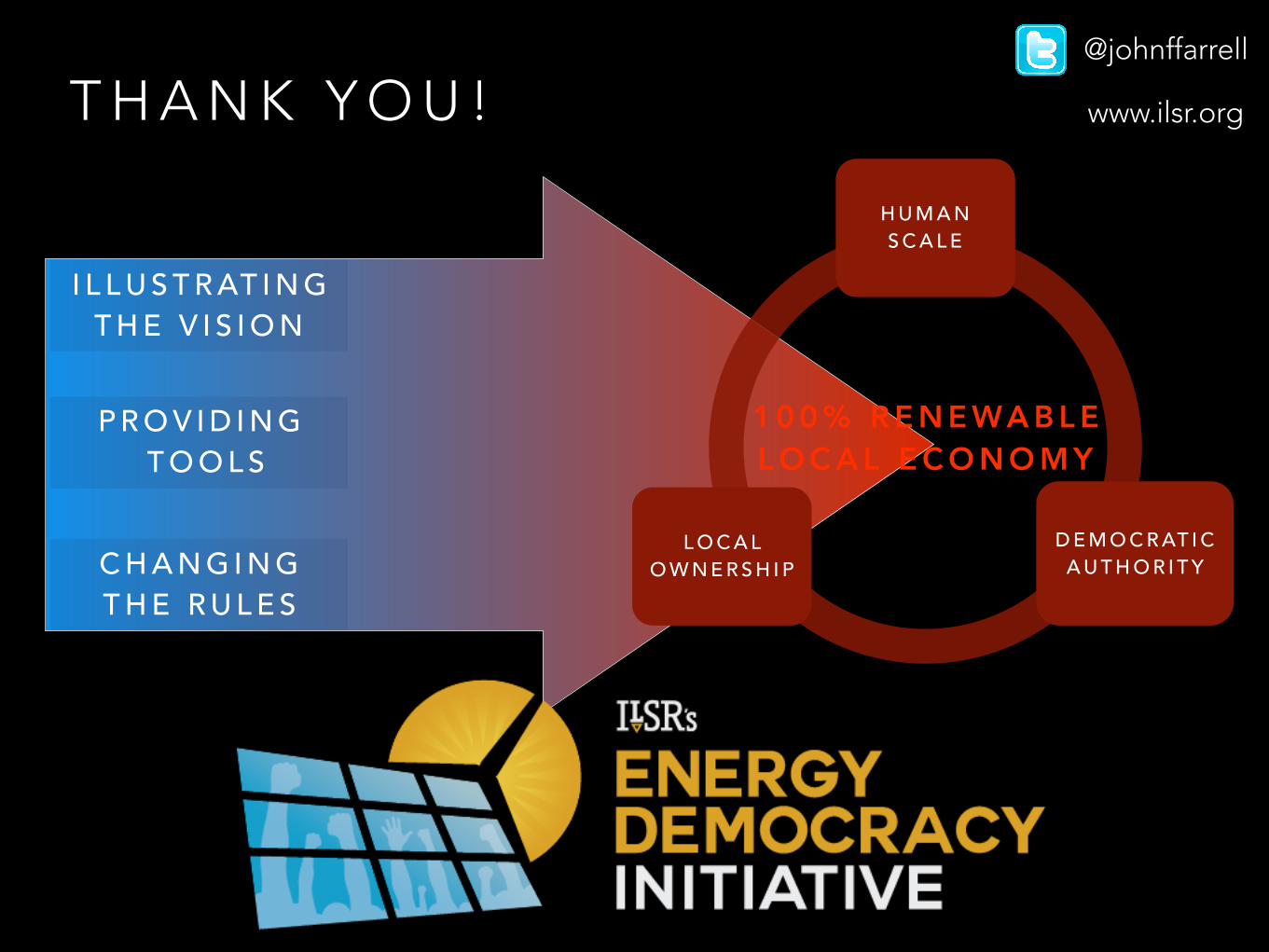

N E W R U L E S

• Enable alternatives

N E W R U L E S

• Set up markets

N E W R U L E S

• Allow power sharing

Report: Is Bigger Best in Renewable Energy?

Download the report

Introduction: the Savings of Size? —————————————————

Renewable Energy Economies of Scale ————————————————— Evidence to the Contrary —————————————————

Limits to Scale in Wind —————————————————

Limits to Scale in Solar —————————————————

Does Big or Small Grow Fastest? ————————————————— Evidence to the Contrary————————————————— Summary

John Farrell

T H A N K Y O U !@johnffarrell

www.ilsr.org

C H A N G I N G T H E R U L E S

P R O V I D I N G T O O L S

1 0 0 % R E N E WA B L E L O C A L E C O N O M Y

H U M A N S C A L E

L O C A L O W N E R S H I P

D E M O C R AT I C A U T H O R I T Y

I L L U S T R AT I N G T H E V I S I O N