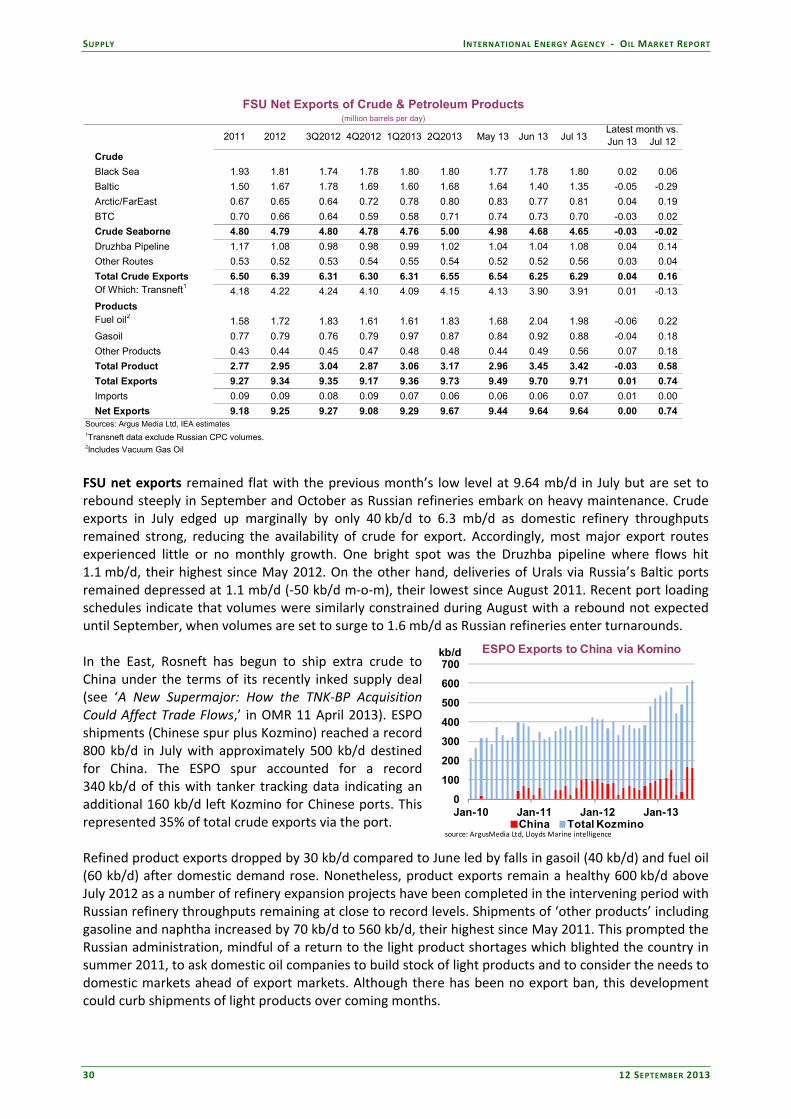

Embed Size (px)

Citation preview

12 September 2013

HIGHLIGHTS Oil futures escalated in August on rising geopolitical tensions over

Syria’s suspected use of chemical weapons and the near total shut‐in of Libyan production. Prices turned lower in early‐September as a Russian proposal for Syria to surrender its chemical weapons gained traction. Brent was last trading at $111.60/bbl, WTI at $107.50/bbl.

The forecast of global demand growth remains flat at 895 kb/d for 2013, as stronger–than‐expected deliveries in July offset concerns about the demand impact of currency fluctuations in emerging market economies. Demand growth is forecast to rise to 1.1 mb/d in 2014, as the underlying macroeconomic backdrop solidifies.

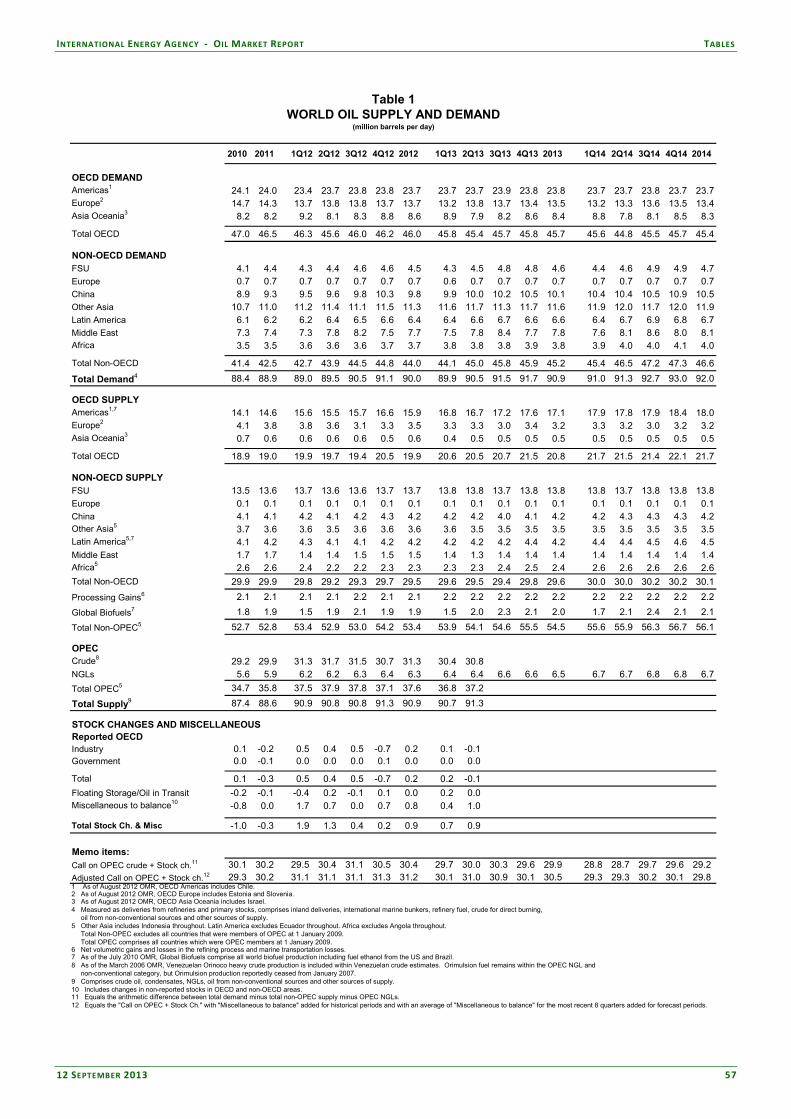

Global supply is estimated to have fallen by 770 kb/d in August to 91.59 mb/d, with both non‐OPEC and OPEC registering monthly declines. In 3Q13 non‐OPEC production is expected to rise by 520 kb/d q‐o‐q as a seasonal decline in the North Sea is more than made up for by North American growth and steady production elsewhere.

OPEC crude supplies fell by 260 kb/d to 30.51 mb/d in August as near‐record Saudi output only partly offset a collapse in Libyan production. The ‘call on OPEC crude and stock change’ was raised by 200 kb/d on higher demand for 3Q13 but lowered by 100 kb/d for 4Q13, to 30.3 mb/d and 29.6 mb/d, respectively.

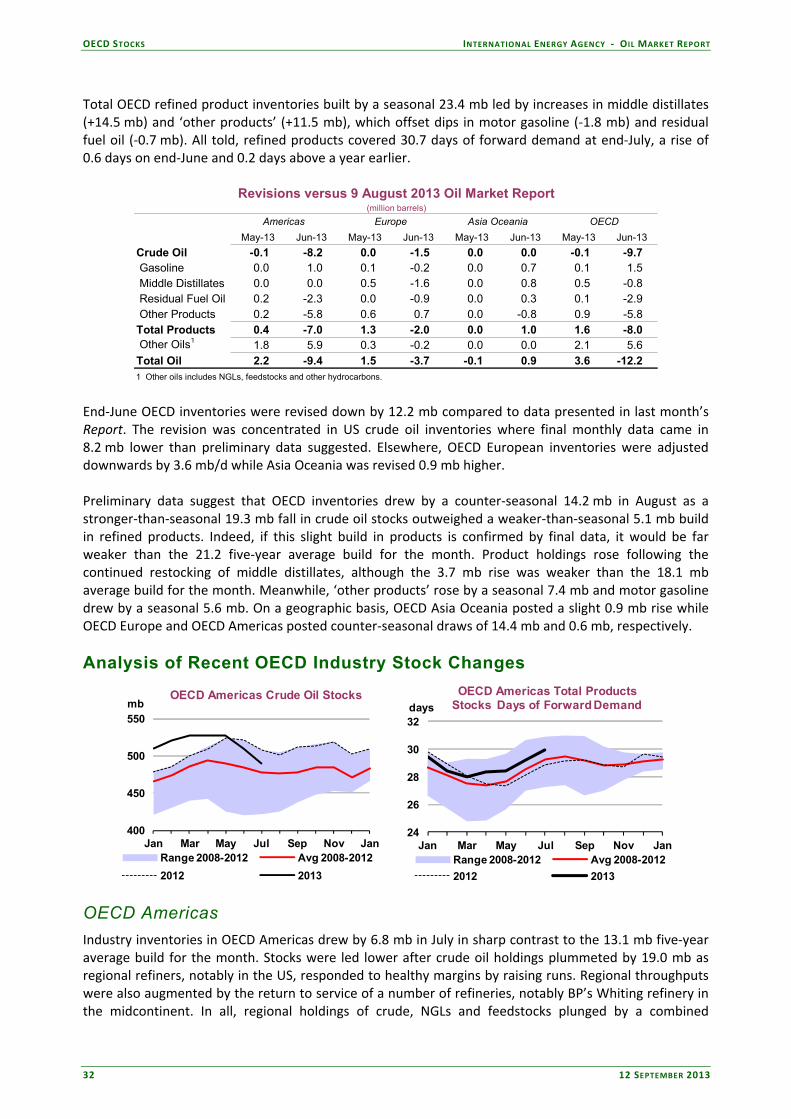

OECD commercial total oil stocks built by a weak 8.0 mb to 2 659 mb in July, bringing their deficit to the five‐year average to 65 mb, its widest in two years. Refined products covered 30.7 days of forward demand, a rise of 0.6 day on end‐June. Preliminary data indicate OECD inventories drew counter‐seasonally by 14.2 mb in August.

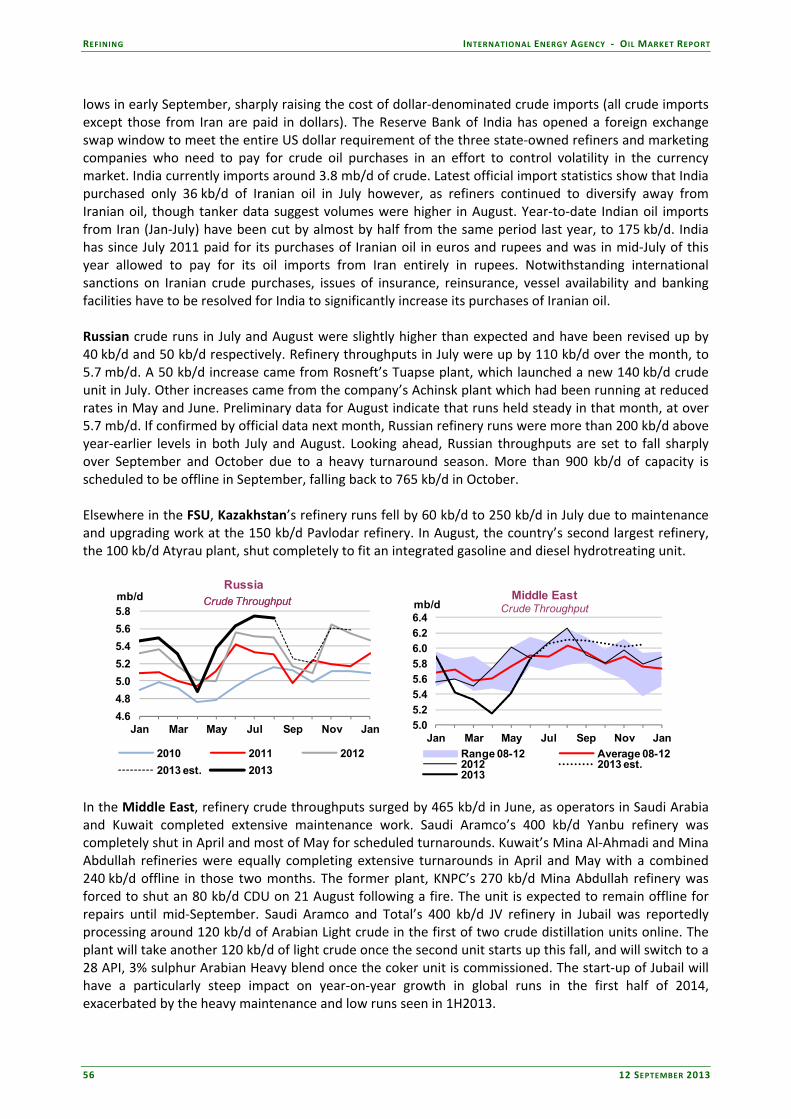

Global refinery crude runs reached a seasonal peak in July, at an estimated 78.2 mb/d, up 1 mb/d from June and 1.8 mb/d above a year earlier. Throughputs are set to fall steeply from August on weaker margins and heavy maintenance. Global runs average 77.2 mb/d in 3Q13, up 1.1 mb/d y‐o‐y, and 76.8 mb/d in 4Q13.

TABLE OF CONTENTS

HIGHLIGHTS ....................................................................................................................................................................................... 1

HEATING UP AND COOLING DOWN ..................................................................................................................................... 3

DEMAND ............................................................................................................................................................................................. 4 Summary ........................................................................................................................................................................................... 4 Global Overview ............................................................................................................................................................................ 4

Emerging Market Currency Depreciation Set to Impact Demand .......................................................................................... 5 Top 10 Consumers ........................................................................................................................................................................ 6 OECD ............................................................................................................................................................................................. 12

Americas ................................................................................................................................................................................... 12 Europe ....................................................................................................................................................................................... 13 Asia Oceania ............................................................................................................................................................................. 14

Non-OECD ................................................................................................................................................................................... 14

SUPPLY ................................................................................................................................................................................................ 16 Summary ......................................................................................................................................................................................... 16 OPEC Crude Oil Supply ............................................................................................................................................................. 17

Libyan Oil Supplies Cascade Lower .......................................................................................................................................... 20 Non-OPEC Overview ................................................................................................................................................................. 22 OECD ............................................................................................................................................................................................. 23

North America ........................................................................................................................................................................ 23 Mexico’s Proposed Energy Sector Reforms – A Watershed for the Energy Industry? ......................................................... 24 North Sea .................................................................................................................................................................................. 27

Non-OECD ................................................................................................................................................................................... 27 Latin America ........................................................................................................................................................................... 27 Asia ............................................................................................................................................................................................. 28 Africa .......................................................................................................................................................................................... 28 Former Soviet Union .............................................................................................................................................................. 29

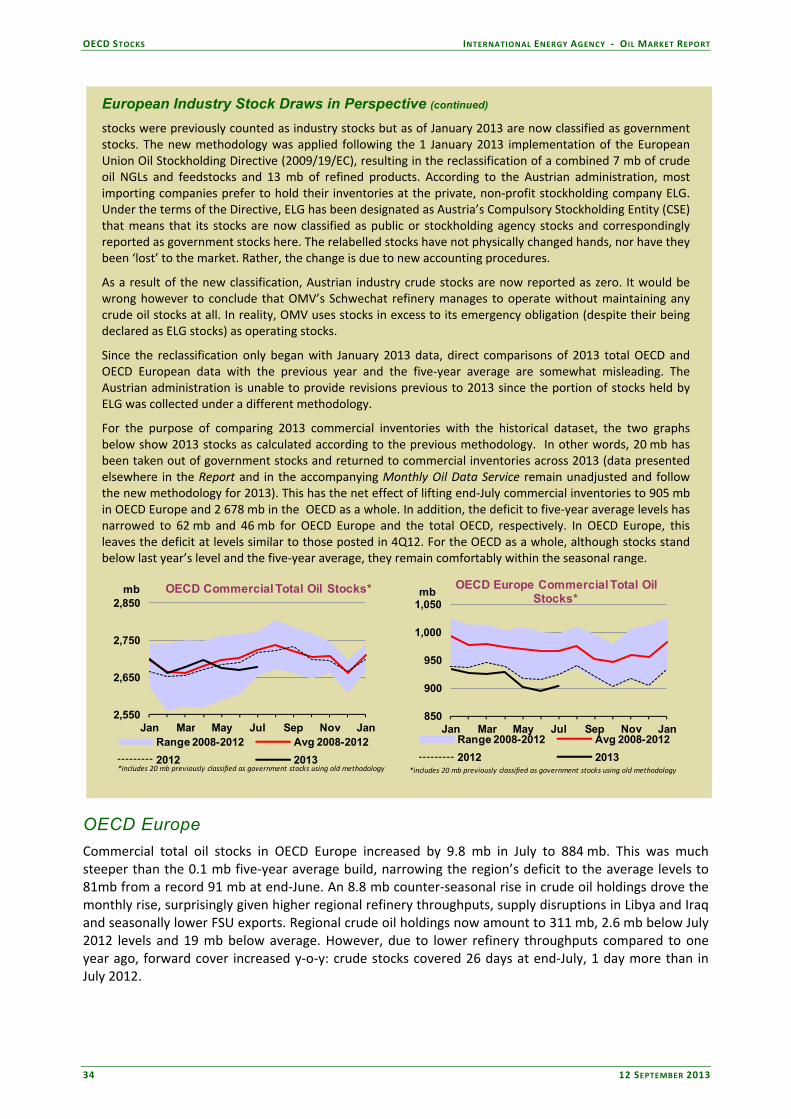

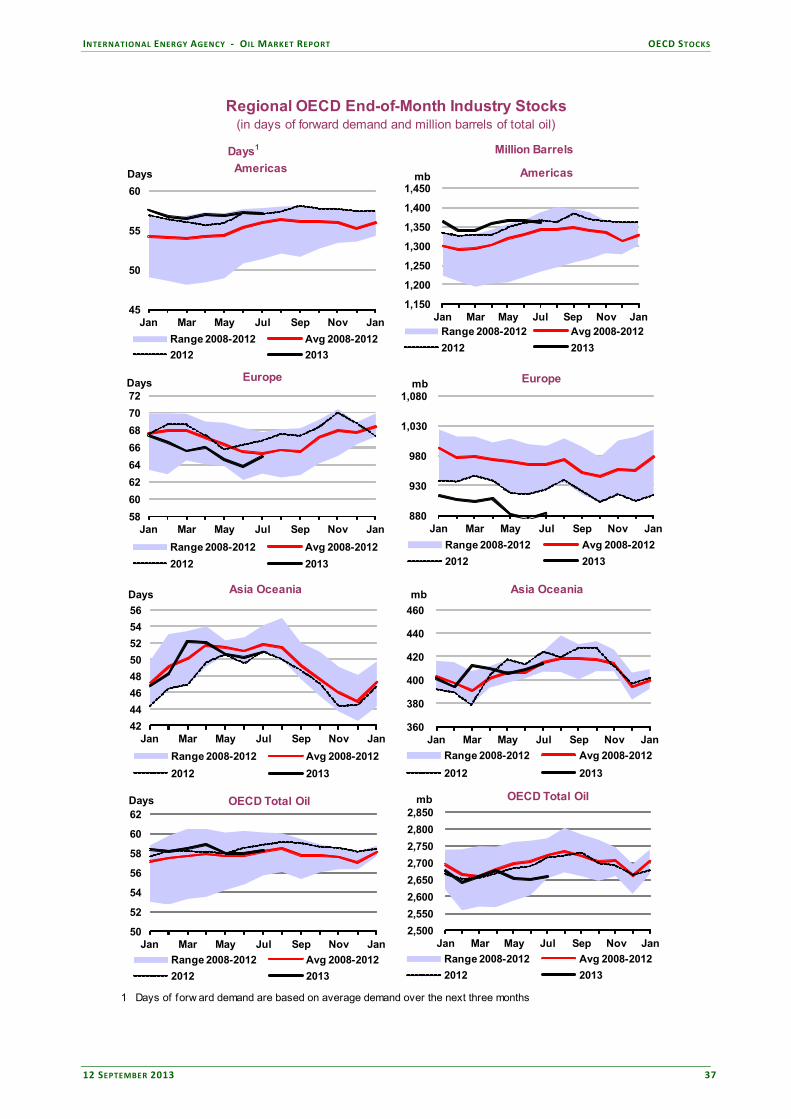

OECD STOCKS ................................................................................................................................................................................ 31 Summary ......................................................................................................................................................................................... 31 OECD Inventory Position at End-July and Revisions to Preliminary Data ....................................................................... 31 Analysis of Recent OECD Industry Stock Changes .............................................................................................................. 32

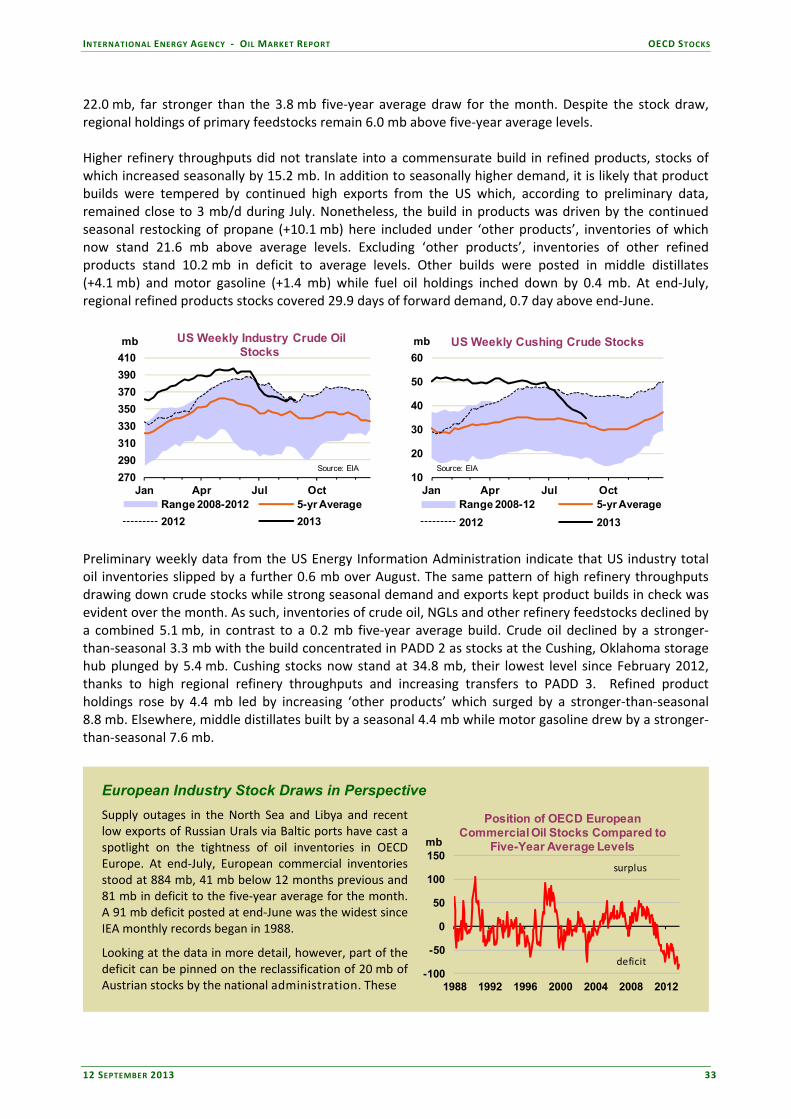

OECD Americas ...................................................................................................................................................................... 32 European Industry Stock Draws in Perspective ....................................................................................................................... 33 OECD Europe .......................................................................................................................................................................... 34 OECD Asia Oceania ............................................................................................................................................................... 35

Recent Developments in Singapore and China Stocks ......................................................................................................... 36

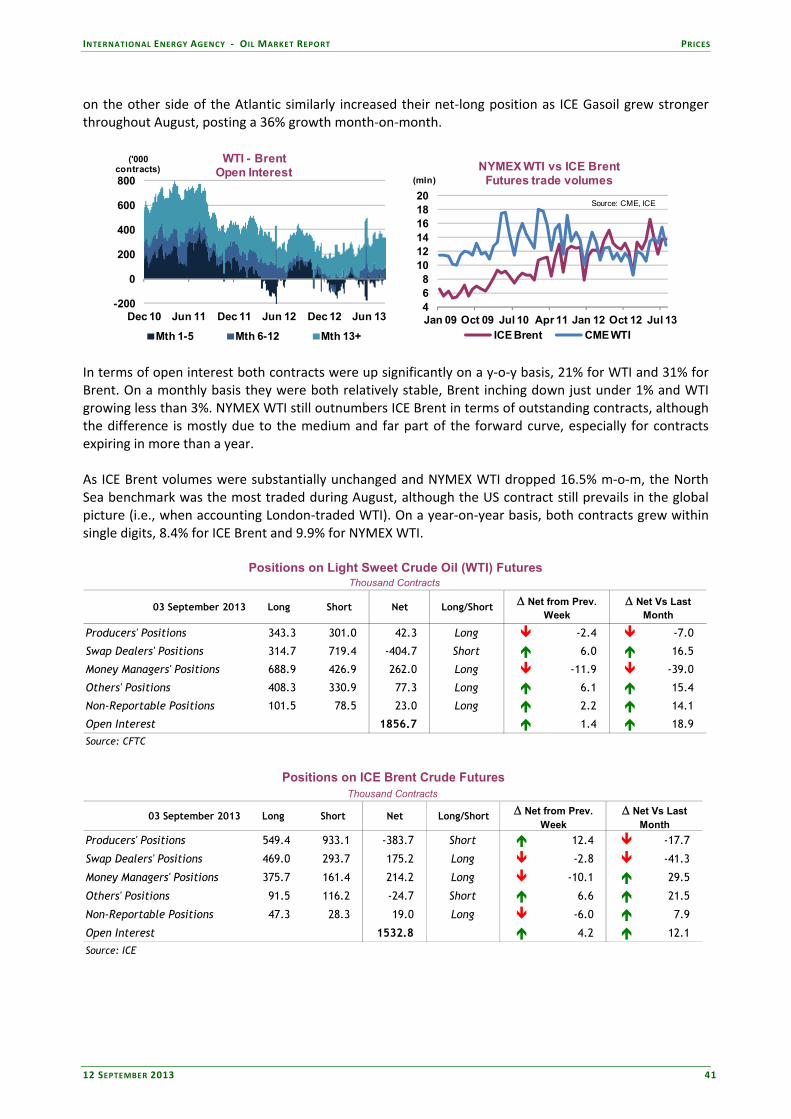

PRICES ................................................................................................................................................................................................. 38 Summary ......................................................................................................................................................................................... 38 Market Overview ......................................................................................................................................................................... 38 Futures Markets ............................................................................................................................................................................ 40

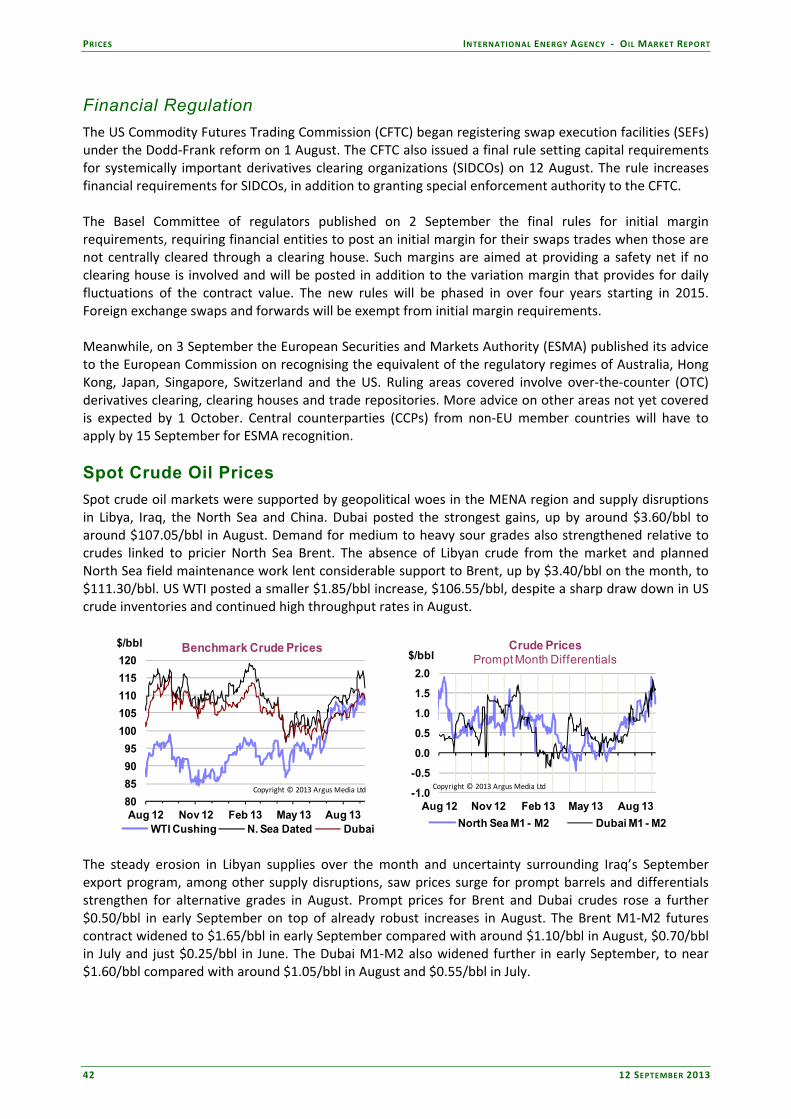

Financial Regulation ................................................................................................................................................................. 42 Spot Crude Oil Prices ................................................................................................................................................................. 42 Spot Product Prices ..................................................................................................................................................................... 44 Freight ............................................................................................................................................................................................. 46

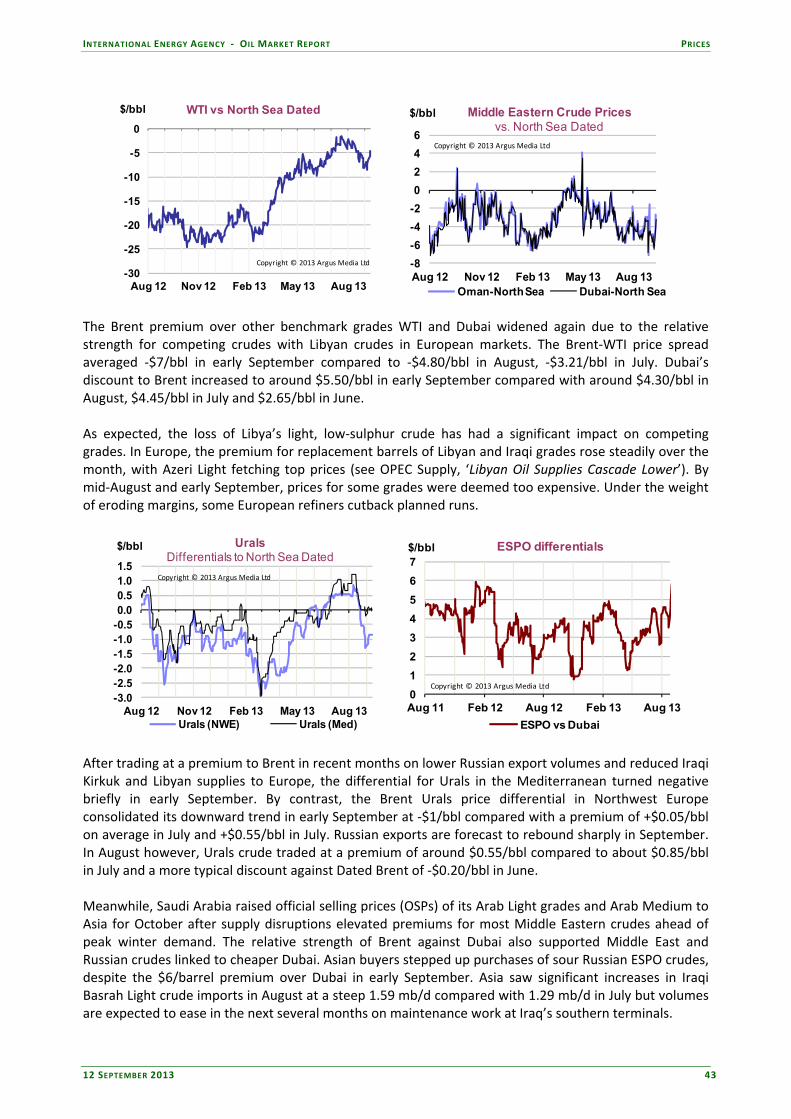

REFINING ........................................................................................................................................................................................... 48 Summary ......................................................................................................................................................................................... 48 Global Refinery Overview .......................................................................................................................................................... 48

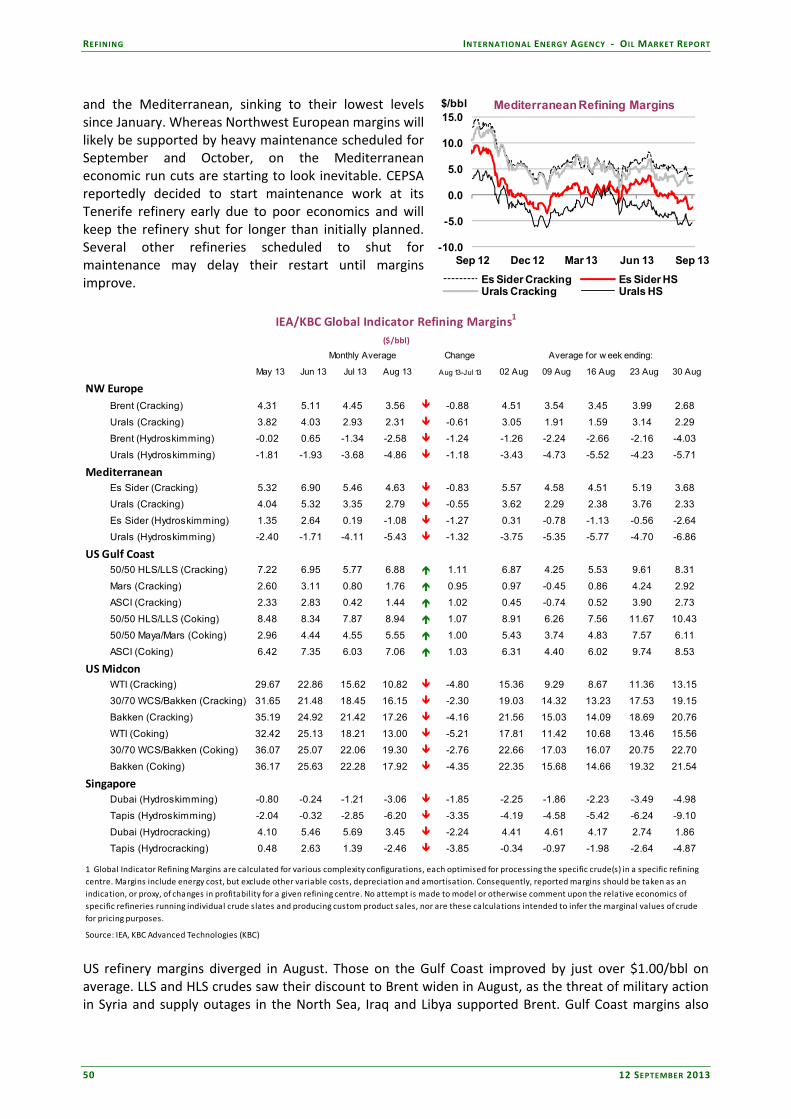

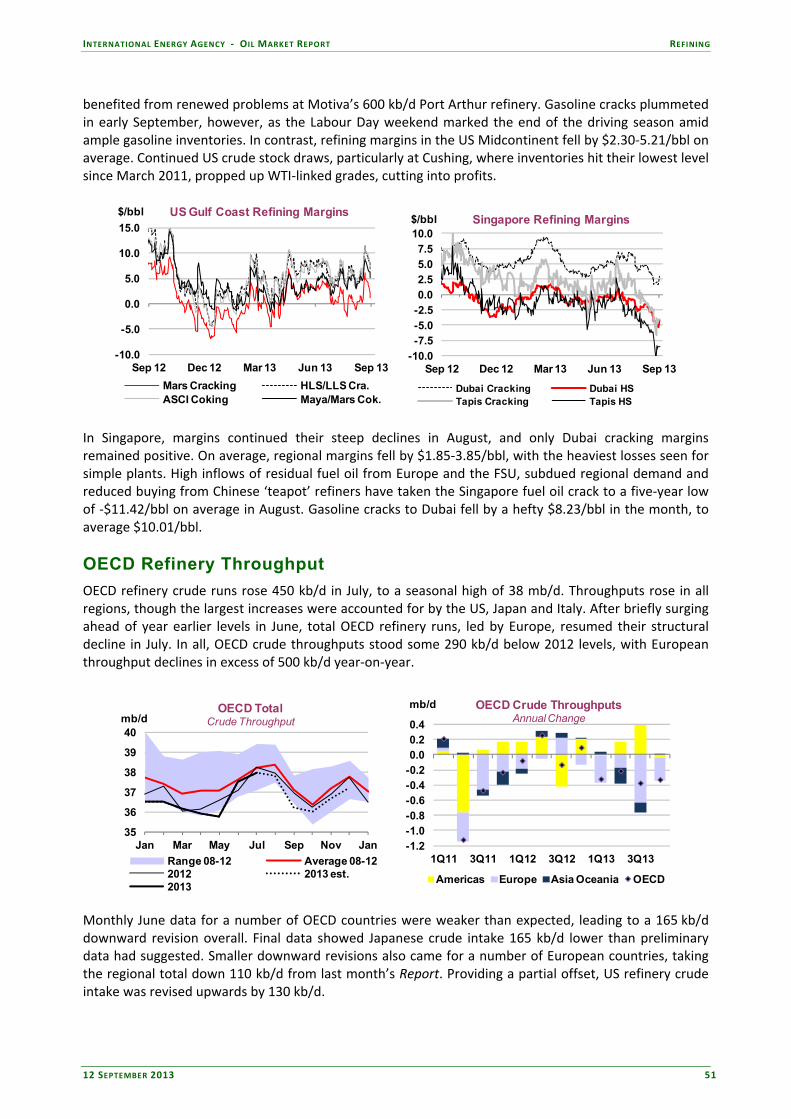

Refining Margins ....................................................................................................................................................................... 49 OECD Refinery Throughput ...................................................................................................................................................... 51 Non-OECD Refinery Throughput ............................................................................................................................................ 54

TABLES ................................................................................................................................................................................................ 57

INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT MARKET OVERVIEW

12 SEPTEMBER 2013 3

HEATING UP AND COOLING DOWN After rallying to six‐month highs amid expectations of western military strikes in Syria, benchmark Brent oil prices ratcheted down again as support seemed to build for an alternative plan to withhold strikes and neutralise Syrian chemical weapon stocks instead. Whether a crisis has been permanently averted or merely postponed remains unclear, however. Oil markets may be taking a breather, but prices remain elevated. The Syrian conflict continues to rage. Across the Mediterranean, a collapse in Libyan exports, which played a large supporting role in the recent run‐up in prices, shows no sign of abating. While there are still plenty of causes for concern, there is some good news, too. Despite continued tensions, the recent tightening of oil market fundamentals – the broad bullish backdrop that has arguably heightened the oil market’s sensitivity to the Syrian threat – looks set to give way to somewhat easier conditions in the fourth quarter. After hitting an all‐time high in July, refinery demand for crude is receding. Nowhere is this truer than in Russia, where a refining boom slashed crude exports in summer, but where heavy seasonal plant maintenance now looks set to reopen the export floodgates. In Europe and Asia, some refiners may decide to extend maintenance shutdowns due to poor margins. Global crude supply – notwithstanding the Libyan problems – looks set for an upward jump in 4Q13, thanks to a heady mix of seasonal, cyclical, political and structural factors. The winding down of seasonal field maintenance in the North Sea and the US Gulf of Mexico will bolster 4Q13 supply – even as a political accord between Sudan and South Sudan sets the stage for a ramp‐up in Sudanese crude exports. New North American production – including US light tight oil and Canadian synthetic crude – continues to surge. Saudi production is hovering near record highs, even as a seasonal dip in domestic air‐conditioning demand looks set to free up more barrels for export. OECD oil inventories have tightened in recent months but may be on the verge of a rebound. The latest data suggest that total industry oil stocks built by just a fraction of the five‐year average in July, bringing the OECD oil stock deficit to the five‐year average to 65 mb, its widest in two years. Our supply/demand forecast suggests however that, even in the absence of an increase in OPEC production (i.e., holding OPEC crude output flat at August levels), rebounding OECD stocks could match or even exceed their five‐year average by December. Assuming zero Libyan production from September through December, stocks could still top their five‐year average by end‐year. Measured in days of forward demand, OECD product stocks under both scenarios would exceed their five‐year range by the end of this month. These projections must be taken with a grain of salt, as reality rarely unfolds according to plan. Our balances also predicted seasonal growth in OECD oil stocks for the last six months, whereas in fact stocks held about flat. That discrepancy shows up as a hefty “Miscellaneous to Balance” time item of 1 mb/d for 2Q13 – reflecting either non‐OECD stock builds, unreported OECD builds, overstated supply, understated demand, or any combination of the above. To correct for such a factor, we have tried carrying forward a large “Miscellaneous to Balance” line item in our 4Q13 balance scenarios. Even so, OECD demand cover is still likely to rise to the top of the range through the remainder of the year if OPEC output is held steady, or hover near average levels in a low OPEC supply scenario. Global balances are of course a rather coarse way of looking at the market, especially in the absence of good non‐OECD stock data. The big picture also masks regional imbalances that can be a challenge for market participants on the ground. Surging US LTO or Canadian synthetic production might be good news for US refiners but not as much of a help to Mediterranean refiners looking for a substitute for disrupted Libyan barrels. Any shift in market conditions will yield winners and losers, until the markets rebalance. But, while the geopolitical storms in the Middle East and North Africa have yet to pass, easing fundamentals look set to lessen the pressure somewhat on market participants – at least for the next few months.

DEMAND INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT

4 12 SEPTEMBER 2013

DEMAND

Summary

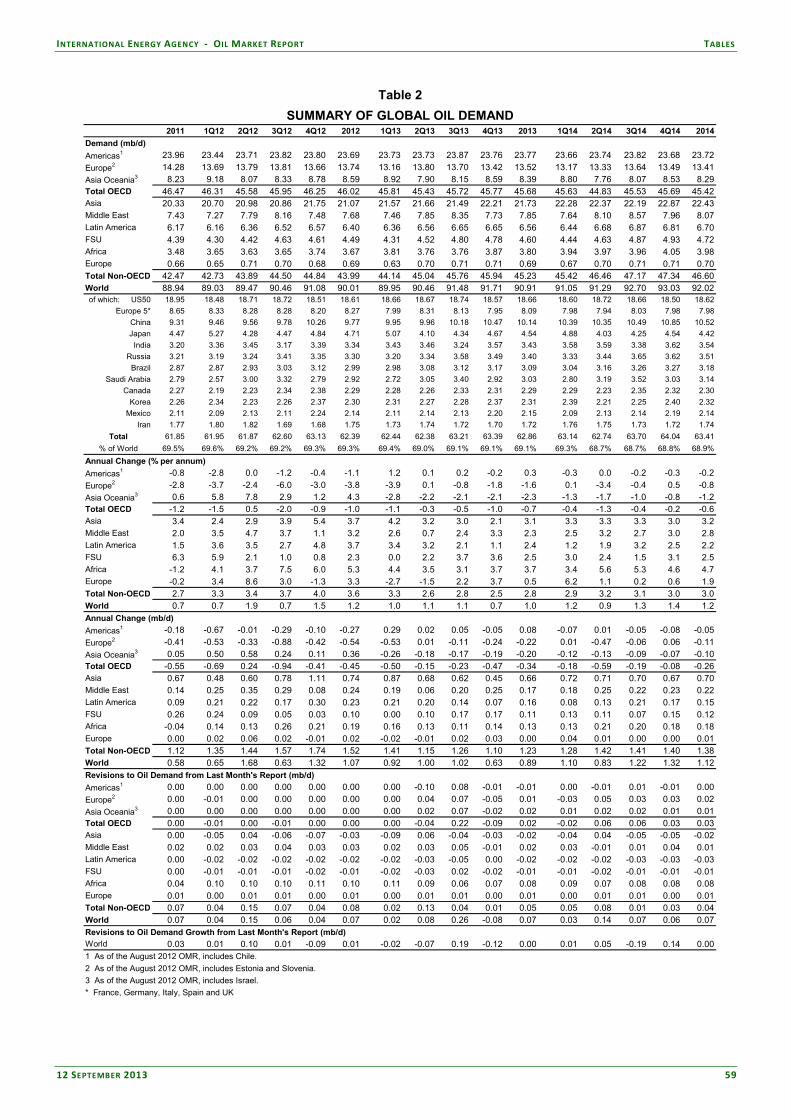

Global oil demand growth is forecast to pick up to 1.1 mb/d in 2014 from 895 kb/d in 2013 as the underlying macroeconomic situation improves. Global oil demand is projected to average 90.9 mb/d in 2013 and 92.0 mb/d in 2014.

High cooling use in July and August raised the estimate of demand for 3Q13, compounding the impact of modest improvements in the economy. Roughly 260 kb/d has been added to the total 3Q13 global consumption estimate, to 91.5 mb/d, since last month’s Report. Upward adjustments to the July demand estimates for the US (+190 kb/d), China (+175 kb/d) and Russia (+90 kb/d) led the revision.

Global Oil Demand (2012-2014)

(million barrels per day)

1Q12 2Q12 3Q12 4Q12 2012 1Q13 2Q13 3Q13 4Q13 2013 1Q14 2Q14 3Q14 4Q14 2014Africa 3.6 3.6 3.6 3.7 3.7 3.8 3.8 3.8 3.9 3.8 3.9 4.0 4.0 4.1 4.0Americas 29.6 30.1 30.3 30.4 30.1 30.1 30.3 30.5 30.4 30.3 30.1 30.4 30.7 30.5 30.4Asia/Pacif ic 29.9 29.1 29.2 30.5 29.7 30.5 29.6 29.6 30.8 30.1 31.1 30.1 30.3 31.4 30.7Europe 14.3 14.5 14.5 14.3 14.4 13.8 14.5 14.4 14.1 14.2 13.8 14.0 14.4 14.2 14.1FSU 4.3 4.4 4.6 4.6 4.5 4.3 4.5 4.8 4.8 4.6 4.4 4.6 4.9 4.9 4.7Middle East 7.3 7.8 8.2 7.5 7.7 7.5 7.8 8.4 7.7 7.8 7.6 8.1 8.6 8.0 8.1World 89.0 89.5 90.5 91.1 90.0 89.9 90.5 91.5 91.7 90.9 91.0 91.3 92.7 93.0 92.0Annual Chg (%) 0.7 1.9 0.7 1.5 1.2 1.0 1.1 1.1 0.7 1.0 1.2 0.9 1.3 1.4 1.2Annual Chg (mb/d) 0.7 1.7 0.6 1.3 1.1 0.9 1.0 1.0 0.6 0.9 1.1 0.8 1.2 1.3 1.1Changes from last OMR (mb/d) 0.04 0.15 0.06 0.04 0.07 0.02 0.08 0.26 -0.08 0.07 0.03 0.13 0.07 0.06 0.07

Currency depreciation in a number of emerging markets, adding to the impact of already high oil prices, has raised the possibility of further associated price effects on demand. Several countries – including India, Indonesia, Malaysia, Peru, the Philippines and Thailand – have faced dramatic currency depreciation versus the US dollar in recent weeks. If sustained, this may ultimately curb their demand trend or, in countries where oil subsidies are in place, raise pressure on their governments to reduce those subsidy programmes.

The divergence in demand trends between emerging markets and developed economies has been easing somewhat lately. Data for 2Q13 show the OECD demand contraction slowing to 0.3% y‐o‐y and non‐OECD demand growth easing to 2.6%, a much narrower gap in the growth pattern than the average of the last five years.

Global Overview

The possibility of slowing oil demand in emerging markets has dominated the headlines recently, with reports of sharp currency depreciation in several non‐OECD countries compounding the effect of already high oil prices in US dollar terms. Higher prices, with all else being held equal, have a negative influence on demand, although in many countries subsidies can cushion their effect for some time. Countering such concerns are the latest demand numbers, which on balance came in stronger than expected for July. Overall, global oil demand is forecast to average roughly 90.9 mb/d in 2013, up by 895 kb/d (or 1.0%) y‐o‐y, essentially unchanged on last month’s growth estimate. Growth is expected to accelerate in 2014 to around 1.1 mb/d (or 1.2%), lifting demand to 92.0 mb/d, as the macroeconomic backdrop continues to improve. The International Monetary Fund’s July World Economic Outlook forecast a rise in global GDP growth to 3.8% in 2014, from 3.1% in 2013; predictions that underpin our oil forecasts. Heightened

INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT DEMAND

12 SEPTEMBER 2013 5

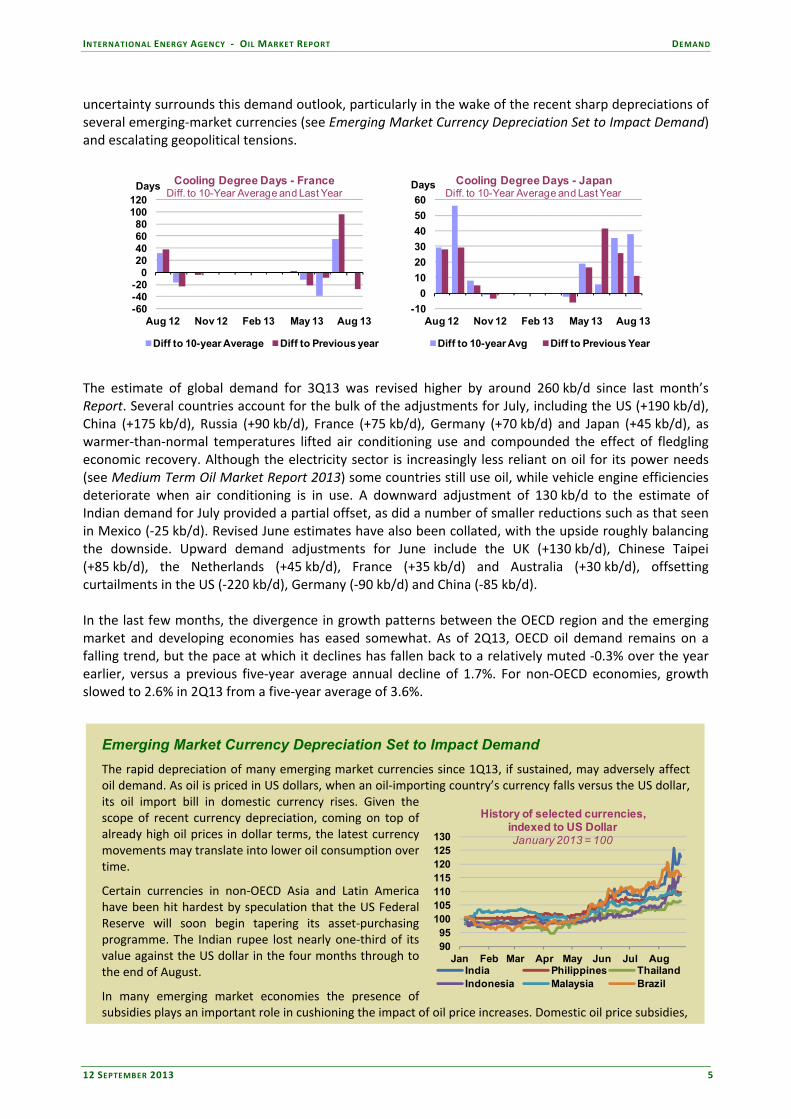

uncertainty surrounds this demand outlook, particularly in the wake of the recent sharp depreciations of several emerging‐market currencies (see Emerging Market Currency Depreciation Set to Impact Demand) and escalating geopolitical tensions.

-60-40-20

020406080

100120

Aug 12 Nov 12 Feb 13 May 13 Aug 13

Days Cooling Degree Days - FranceDiff. to 10-Year Average and Last Year

Diff to 10-year Average Diff to Previous year

-10

0

10

20

30

40

50

60

Aug 12 Nov 12 Feb 13 May 13 Aug 13

Days Cooling Degree Days - JapanDiff. to 10-Year Average and Last Year

Diff to 10-year Avg Diff to Previous Year

The estimate of global demand for 3Q13 was revised higher by around 260 kb/d since last month’s Report. Several countries account for the bulk of the adjustments for July, including the US (+190 kb/d), China (+175 kb/d), Russia (+90 kb/d), France (+75 kb/d), Germany (+70 kb/d) and Japan (+45 kb/d), as warmer‐than‐normal temperatures lifted air conditioning use and compounded the effect of fledgling economic recovery. Although the electricity sector is increasingly less reliant on oil for its power needs (see Medium Term Oil Market Report 2013) some countries still use oil, while vehicle engine efficiencies deteriorate when air conditioning is in use. A downward adjustment of 130 kb/d to the estimate of Indian demand for July provided a partial offset, as did a number of smaller reductions such as that seen in Mexico (‐25 kb/d). Revised June estimates have also been collated, with the upside roughly balancing the downside. Upward demand adjustments for June include the UK (+130 kb/d), Chinese Taipei (+85 kb/d), the Netherlands (+45 kb/d), France (+35 kb/d) and Australia (+30 kb/d), offsetting curtailments in the US (‐220 kb/d), Germany (‐90 kb/d) and China (‐85 kb/d). In the last few months, the divergence in growth patterns between the OECD region and the emerging market and developing economies has eased somewhat. As of 2Q13, OECD oil demand remains on a falling trend, but the pace at which it declines has fallen back to a relatively muted ‐0.3% over the year earlier, versus a previous five‐year average annual decline of 1.7%. For non‐OECD economies, growth slowed to 2.6% in 2Q13 from a five‐year average of 3.6%.

Emerging Market Currency Depreciation Set to Impact Demand

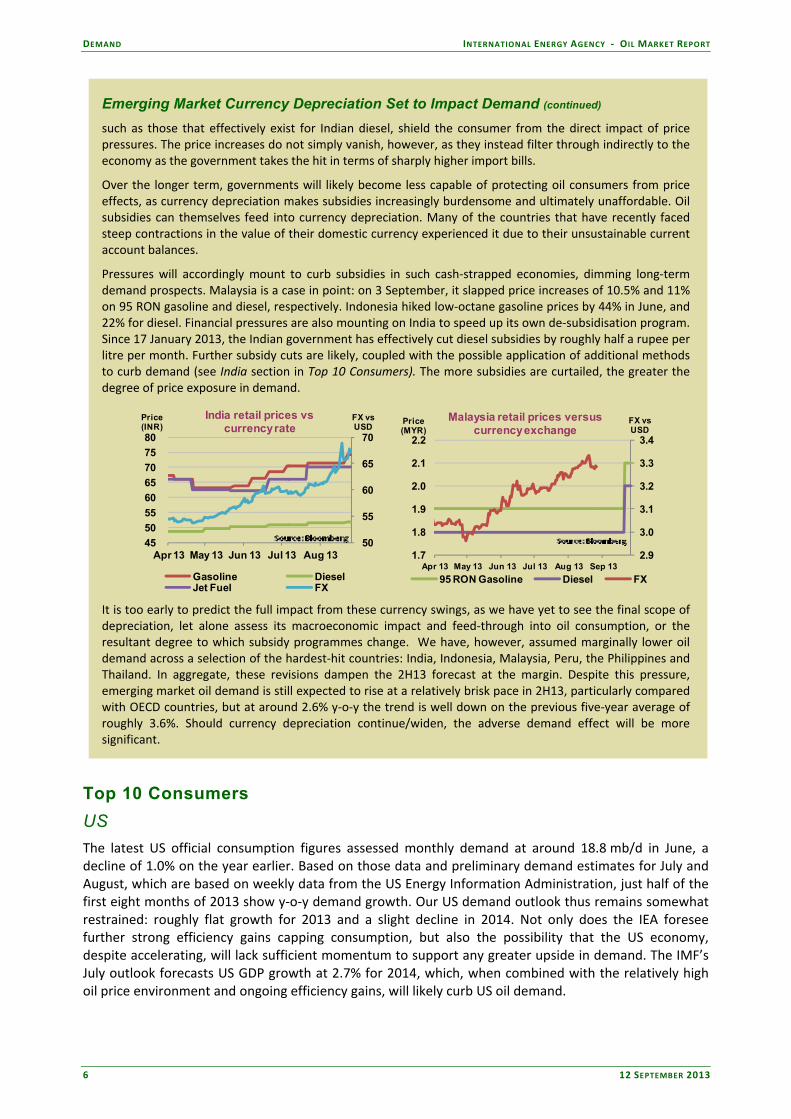

The rapid depreciation of many emerging market currencies since 1Q13, if sustained, may adversely affect oil demand. As oil is priced in US dollars, when an oil‐importing country’s currency falls versus the US dollar, its oil import bill in domestic currency rises. Given the scope of recent currency depreciation, coming on top of already high oil prices in dollar terms, the latest currency movements may translate into lower oil consumption over time.

Certain currencies in non‐OECD Asia and Latin America have been hit hardest by speculation that the US Federal Reserve will soon begin tapering its asset‐purchasing programme. The Indian rupee lost nearly one‐third of its value against the US dollar in the four months through to the end of August.

In many emerging market economies the presence of subsidies plays an important role in cushioning the impact of oil price increases. Domestic oil price subsidies,

9095

100105110115120125130

Jan Feb Mar Apr May Jun Jul Aug

History of selected currencies, indexed to US DollarJanuary 2013 = 100

India Philippines ThailandIndonesia Malaysia Brazil

DEMAND INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT

6 12 SEPTEMBER 2013

Emerging Market Currency Depreciation Set to Impact Demand (continued)

such as those that effectively exist for Indian diesel, shield the consumer from the direct impact of price pressures. The price increases do not simply vanish, however, as they instead filter through indirectly to the economy as the government takes the hit in terms of sharply higher import bills.

Over the longer term, governments will likely become less capable of protecting oil consumers from price effects, as currency depreciation makes subsidies increasingly burdensome and ultimately unaffordable. Oil subsidies can themselves feed into currency depreciation. Many of the countries that have recently faced steep contractions in the value of their domestic currency experienced it due to their unsustainable current account balances.

Pressures will accordingly mount to curb subsidies in such cash‐strapped economies, dimming long‐term demand prospects. Malaysia is a case in point: on 3 September, it slapped price increases of 10.5% and 11% on 95 RON gasoline and diesel, respectively. Indonesia hiked low‐octane gasoline prices by 44% in June, and 22% for diesel. Financial pressures are also mounting on India to speed up its own de‐subsidisation program. Since 17 January 2013, the Indian government has effectively cut diesel subsidies by roughly half a rupee per litre per month. Further subsidy cuts are likely, coupled with the possible application of additional methods to curb demand (see India section in Top 10 Consumers). The more subsidies are curtailed, the greater the degree of price exposure in demand.

50

55

60

65

70

45

50

55

60

65

70

75

80

Apr 13 May 13 Jun 13 Jul 13 Aug 13

FX vs USD

Price (INR)

India retail prices vscurrency rate

Gasoline DieselJet Fuel FX

2.9

3.0

3.1

3.2

3.3

3.4

1.7

1.8

1.9

2.0

2.1

2.2

Apr 13 May 13 Jun 13 Jul 13 Aug 13 Sep 13

FX vs USD

Price (MYR)

Malaysia retail prices versus currency exchange

95 RON Gasoline Diesel FX

It is too early to predict the full impact from these currency swings, as we have yet to see the final scope of depreciation, let alone assess its macroeconomic impact and feed‐through into oil consumption, or the resultant degree to which subsidy programmes change. We have, however, assumed marginally lower oil demand across a selection of the hardest‐hit countries: India, Indonesia, Malaysia, Peru, the Philippines and Thailand. In aggregate, these revisions dampen the 2H13 forecast at the margin. Despite this pressure, emerging market oil demand is still expected to rise at a relatively brisk pace in 2H13, particularly compared with OECD countries, but at around 2.6% y‐o‐y the trend is well down on the previous five‐year average of roughly 3.6%. Should currency depreciation continue/widen, the adverse demand effect will be more significant.

Top 10 Consumers

US

The latest US official consumption figures assessed monthly demand at around 18.8 mb/d in June, a decline of 1.0% on the year earlier. Based on those data and preliminary demand estimates for July and August, which are based on weekly data from the US Energy Information Administration, just half of the first eight months of 2013 show y‐o‐y demand growth. Our US demand outlook thus remains somewhat restrained: roughly flat growth for 2013 and a slight decline in 2014. Not only does the IEA foresee further strong efficiency gains capping consumption, but also the possibility that the US economy, despite accelerating, will lack sufficient momentum to support any greater upside in demand. The IMF’s July outlook forecasts US GDP growth at 2.7% for 2014, which, when combined with the relatively high oil price environment and ongoing efficiency gains, will likely curb US oil demand.

INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT DEMAND

12 SEPTEMBER 2013 7

US50: Total Oil Product Demand

17,500

18,500

19,500

20,500

Jan Apr Jul Oct Jan

kb/d

Range 08-12 5-year avg2012 2013

US50: Motor Gasoline Demand

8,200

8,600

9,000

9,400

Jan Apr Jul Oct Jan

kb/d

Range 08-12 5-year avg2012 2013

Despite reports of recent strength in the US demand, the underlying macroeconomics remain somewhat subdued. Economic growth in 2Q13 amounted to just 0.4% over 1Q13 (but 1.7% when annualised). In essence, the 2Q13 US GDP growth trend was actually below that experienced by the UK, Korea, Germany, France and Japan, and slower than the US pace of growth as recently as 3Q12.

Top-10 Oil Consumers(thousand barrels per day)

Jun-13 2013 2014 Jun-13 2013 2014 Jun-13 2013 2014

US50 18,786 18,661 18,618 -193 55 -43 -1.0 0.3 -0.2

China 10,221 10,140 10,520 526 373 380 5.4 3.8 3.7

Japan 3,877 4,542 4,422 -237 -172 -120 -5.8 -3.7 -2.6

Russia 3,575 3,404 3,512 146 104 108 4.2 3.2 3.2

India 3,415 3,427 3,543 -67 85 116 -1.9 2.6 3.4

Saudi Arabia 3,281 3,026 3,138 53 104 111 1.6 3.6 3.7

Brazil 3,043 3,088 3,185 83 102 97 2.8 3.4 3.1

Germany 2,492 2,382 2,372 -28 -6 -10 -1.1 -0.3 -0.4

Korea 2,301 2,311 2,315 -36 10 4 -1.5 0.4 0.2

Canada 2,233 2,295 2,297 30 8 2 1.3 0.4 0.1

% global demand 59% 59% 59%

Demand Annual Chg (kb/d) Annual Chg (%)

Looming US ‘sequester’ cuts and arguments about the debt ceiling are likely to dampen consumer sentiment in 2H13, with a particular strong impact on gasoline demand as high retail gasoline prices and declining consumer confidence compound the impact of vehicle efficiency gains. The US Energy Information Administration estimates that the efficiency of the US light‐vehicle pool improved by around 1.9% y‐o‐y in 1H13.

China

This has been a mixed month for Chinese demand data, with offsetting adjustments to the June (‐85 kb/d) and July (+175 kb/d) series. This net addition meant that despite the maintenance of our forecast for significantly slower growth in 2H13, the forecast for the year as a whole has been raised modestly, to 3.8% versus last month’s 3.7% projection. Revised estimates of Chinese apparent demand (defined as the sum of refinery output and net product imports, minus product inventory builds) depict roughly 10.2 mb/d of oil products being consumed in June, a gain of 5.4% on the year earlier, supported by particularly sharp gains in transport fuels and naphtha. Preliminary July estimates imply a similar rate of growth, to 10.3 mb/d, despite reports of product destocking which have the effect of inflating apparent demand estimates (see ‘Chinese Demand Forecast Upgraded‘, OMR January 2013). Early indications point towards a significant deceleration in August, in line with the forecast carried in last month’s Report, as refiners reduced runs by 155 kb/d over July.

DEMAND INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT

8 12 SEPTEMBER 2013

China: Total Oil Product Demand

8,500

9,500

10,500

Jan Apr Jul Oct Jan

kb/d

2011 2012 2013 2014

China: Naphtha Demand

600

800

1,000

1,200

Jan Apr Jul Oct Jan

kb/d

Range 2008-2012 5-year avg2012 2013

Supporting the Chinese growth forecast of nearly 4%, in a year of exceptionally choppy demand, is the IMF assumption of 7.8% rise in GDP in 2013 (decelerating to 7.7% in 2014). The latest economic indicators – such as industrial output rising 9.7% y‐o‐y in July and 10.4% in August – add credibility to these forecasts.

China: Demand by Product(thousand barrels per day)

Annual Chg (kb/d) Annual Chg (%)

2012 2013 2014 2013 2014 2013 2014

LPG & Ethane 753 766 788 13 21 1.7 2.8

Naphtha 985 1,079 1,150 94 72 9.5 6.6

Motor Gasoline 1,953 2,100 2,209 147 109 7.6 5.2

Jet Fuel & Kerosene 438 481 510 43 28 9.9 5.9

Gas/Diesel Oil 3,406 3,427 3,525 21 97 0.6 2.8

Residual Fuel Oil 496 519 529 23 10 4.6 1.9

Other Products 1,736 1,768 1,810 31 42 1.8 2.4

Total Products 9,768 10,140 10,520 373 380 3.8 3.7

Demand

Japan

The unusually warm early summer temperatures have raised the estimate of 2013 Japanese oil consumption as power sector needs (driven by air conditioning demand) are likely to exceed earlier expectations. Fuel oil and ‘other product’ demand (which includes crude oil for direct burn) notably support power sector needs. For the year as a whole, an overall decline rate of 3.7% is now assumed (previously the forecast decline rate was 3.8%), taking total Japanese demand to an average of around 4.5 mb/d. Consumption contracted by a steep 4.3% y‐o‐y in 2Q13 but is expected to show slower declines from then on. Having fallen sharply in 1Q13, gasoline demand will lead the reversal in fortunes in 2H13, supported by likely gains in consumer confidence.

Japan: Total Oil Product Demand

3,500

4,000

4,500

5,000

5,500

6,000

Jan Apr Jul Oct Jan

kb/d

Range 08-12 5-year avg2012 2013

Japan: Motor Gasoline Demand

850

900

950

1,000

1,050

1,100

1,150

1,200

Jan Apr Jul Oct Jan

kb/d

Range 08-12 5-year avg2012 2013

INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT DEMAND

12 SEPTEMBER 2013 9

India

In July, for the second consecutive month, Indian demand contracted y‐o‐y as the country’s effective de‐subsidisation programme continues to cut into diesel consumption. Since January, the government has been undergoing a programme of cutting the effective diesel price subsidy by roughly half a rupee per litre per month, whereby half a rupee is equal to roughly one US cent as of 11 September. Reduced agricultural demand and signs of slowing economic growth also contributed. Agricultural consumption has been particularly curbed as of late, with relatively plentiful rains reducing irrigation needs (a big gasoil/diesel user), while the recent economic slowdown has dampened consumption, a pressure compounded as prices have risen. Although consumer purchasing decisions have, to date, largely avoided the most dire consequences from the rupee’s depreciation, with effective subsidies continuing to protect domestic diesel demand, the already cash‐strapped government is under pressure to reduce these subsidies still further, or find alternative methods to curb use. The oil ministry, in an open letter to the Prime Minister, has outlined some potential measures, such as requesting that refiners reduce imports, encouraging people to consume less, or restricting retailers’ opening hours (an option since discarded).

India: Total Oil Product Demand

2,600

3,100

3,600

Jan Apr Jul Oct Jan

kb/d

Range 2008-2012 5-year avg2012 2013

India: Gasoil Demand

800

1,200

1,600

Jan Apr Jul Oct Jan

kb/d

Range 2008-2012 5-year avg2012 2013

Even if governments have many ways to discourage consumption, economists widely believe that the pricing mechanism is the most efficient method of distributing limited supplies. Indeed, the smaller gasoline sector – which accounted for just 11.1% of Indian demand in 2012, versus 41.1% for gasoil – has already experienced some sharp price gains, with six hikes seen since May (gasoline prices having risen by 17.5% between the end of May of the beginning of September, whereas diesel prices have inched up a mere 3.4%). The price effect is far from perfect, however, as demonstrated by the continued strong gains seen in gasoline demand. Also the current programme of curbing the effective diesel subsidy is not simply a commitment to raise the price by the stated amount each month, but instead a pledge to do so until the so‐called under‐recoveries have disappeared. The term under‐recoveries refers to the situation where the actual selling price is lower than the price retailers/distributors pay to refiners. This policy of small but steady steps showed significant progress with the under‐recoveries going down, from about 9 rupees per litre in January to 3.73 rupees per litre for the fortnight of 16 May. Due to a combination of a declining rupee and increases in the Indian crude oil price basket, the under‐recoveries shot up to 12.12 rupees per litre for the fortnight of 1 September. Since January, diesel prices have been raised seven times, for a total of 4.25 rupees per litre. Local media speculation is rife that a one‐off Rupee 5 per litre hike is in the offing. Although this could be a step in the right direction, such a move looks unlikely with elections less than a year away. Whatever method is adopted, we have trimmed our own demand forecast, to 2.6% in 2013, from 2.8% before.

DEMAND INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT

10 12 SEPTEMBER 2013

Russia

The strong recent Russian demand trend continues, with roughly 3.6 mb/d consumed in July, a gain of 5.5% on the year earlier and marking the fifth month in a row that growth has exceeded the previous six‐month average. Once again, manufacturing continues to provide the majority of the demand support, with particularly sharp gains seen in gasoil, fuel oil and ‘other products’. Consumption of jet/kerosene and LPG has lagged as concerns regarding the pace of GDP growth have spread following the somewhat subdued 2Q13 number (+1.2% y‐o‐y).

Russia: Total Oil Product Demand

2,600

2,800

3,000

3,200

3,400

3,600

Jan Apr Jul Oct Jan

kb/d

Range 2008-2012 5-year avg2012 2013

So urce: P etro market R G, IEA

Russia: Residual Fuel Oil Demand

100

200

300

400

Jan Apr Jul Oct Jan

kb/d

Range 2008-2012 5-year avg2012 2013

Source: Petromarket RG, IEA

Regardless of the relatively strong 2Q13 demand showing – with a near 3% gain in Russian oil use seen over the corresponding period for 2012 – the forecast for the year as a whole remains largely unchanged, reflecting nagging concerns about the pace of macroeconomic momentum in the second half of the year. Although the majority of 2013, thus far, saw ‘expansionary’ manufacturing sentiment depicted in its confidence statistics, the perspective clearly darkened in July/August. Filtering from these forces, overall oil consumption growth is forecast to average out at 3.2% in both 2013 and 2014.

Russian Manufacturing PMI

49

50

51

52

53

Aug12 Nov12 Feb13 May13 Aug13

Not e: 50=cont ract ion/ expansion t hreshold. Sources: HSBC, Markit

Brazilian Manufacturing PMI

48

49

50

51

52

53

Aug12 Nov12 Feb13 May13

Not e: 50=cont ract ion/ expansion t hreshold. Sources: HSBC, Markit

Brazil

Brazilian consumption in June averaged 3.0 mb/d, 45 kb/d less than our month earlier prediction. Slowing gasoil demand growth, itself a consequence of the Latin American nation’s recent industrial woes, underpinned the lower number. Industrial sentiment has been on a declining trend since the beginning of the year, although HSBC’s Manufacturing Purchasing Managers’ Index (PMI) remained within ‘expansionary’ territory until July, requiring a less rampant growth in gasoil use, up 2.8% y‐o‐y in June versus previous a 12‐month average gain of 6.5%. This mid‐year weakness, which is likely to continue through 3Q13 if the PMI is any guide, resulted in a modest curtailment in our 2013 growth forecast, to 3.4% – down by two‐tenths of a percentage point on that carried in last month’s Report.

INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT DEMAND

12 SEPTEMBER 2013 11

Saudi Arabia

The consumption data for June came out roughly in‐line with last month’s forecast, up 1.6% on the year earlier to 3.3 mb/d. By far the greatest upside was seen in fuel oil, as demand surged to a near‐five‐year high supported by additional power sector usage. Absolute declines in ‘other products’ and gasoil provided a partial offset, suggesting some switching of direct crude burn and gasoil to fuel oil in power generation. With the underlying macroeconomic environment likely to deteriorate in 2013 – the International Monetary Fund (IMF) forecasting GDP growth of 4.0% in 2013 after a gain of 5.1% in 2012 – then so, too, will oil demand growth, to 3.6% in 2013 from 4.7% in 2012. Similar growth (+3.7%) is foreseen in 2014 as this rough trend continues.

Saudi Arabia: Total Oil Product Demand

1,900

2,300

2,700

3,100

3,500

Jan Apr Jul Oct Jan

kb/d

Range 2008-2012 5-year avg2012 2013

Saudi Arabia: Residual Fuel Oil Demand

200

300

400

500

Jan Apr Jul Oct Jan

kb/d

Range 2008-2012 5-year avg2012 2013

Germany

Despite reports of an uptick in recent German economic activity, the demand forecast for the year as a whole remains essentially flat, as the underlying macroeconomic growth trend remains subdued. The greatest upside, in the forecast, is provided by industrially important gasoil and LPG, while downside momentum is provided by heavier fuel oil and the transportation markets of gasoline and jet/kerosene. Predictions of continued efficiency gains will likely keep the demand forecast restrained in 2014.

Germany: Total Oil Product Demand

2,100

2,300

2,500

2,700

2,900

Jan Apr Jul Oct Jan

kb/d

Range 08-12 5-year avg2012 2013

German: Gasoil Demand

800

1,000

1,200

1,400

Jan Apr Jul Oct Jan

kb/d

Range 08-12 5-year avg2012 2013

Korea

At an average of 2.2 mb/d in July, South Korean demand was in line with the forecast carried in last month’s Report. There has, however been something of a redistribution of product across the barrel, as the previously overestimated ‘other product’ category was seemingly ‘too high’ at the expense of a combination of ‘too little’ fuel oil, LPG, naphtha and gasoil. Particularly strong naphtha demand likely re‐emerged as the earlier spate of heavy cracker maintenance drew to a close. The overall consumption trend, for the year as a whole, is forecast to remain relatively flat, in line with government policy, little changed from last month’s Report.

DEMAND INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT

12 12 SEPTEMBER 2013

Korea: Total Oil Product Demand

1,900

2,100

2,300

2,500

Jan Apr Jul Oct Jan

kb/d

Range 08-12 5-year avg2012 2013

Korea: Naphtha Demand

750

850

950

1,050

1,150

Jan Apr Jul Oct Jan

kb/d

Range 08-12 5-year avg2012 2013

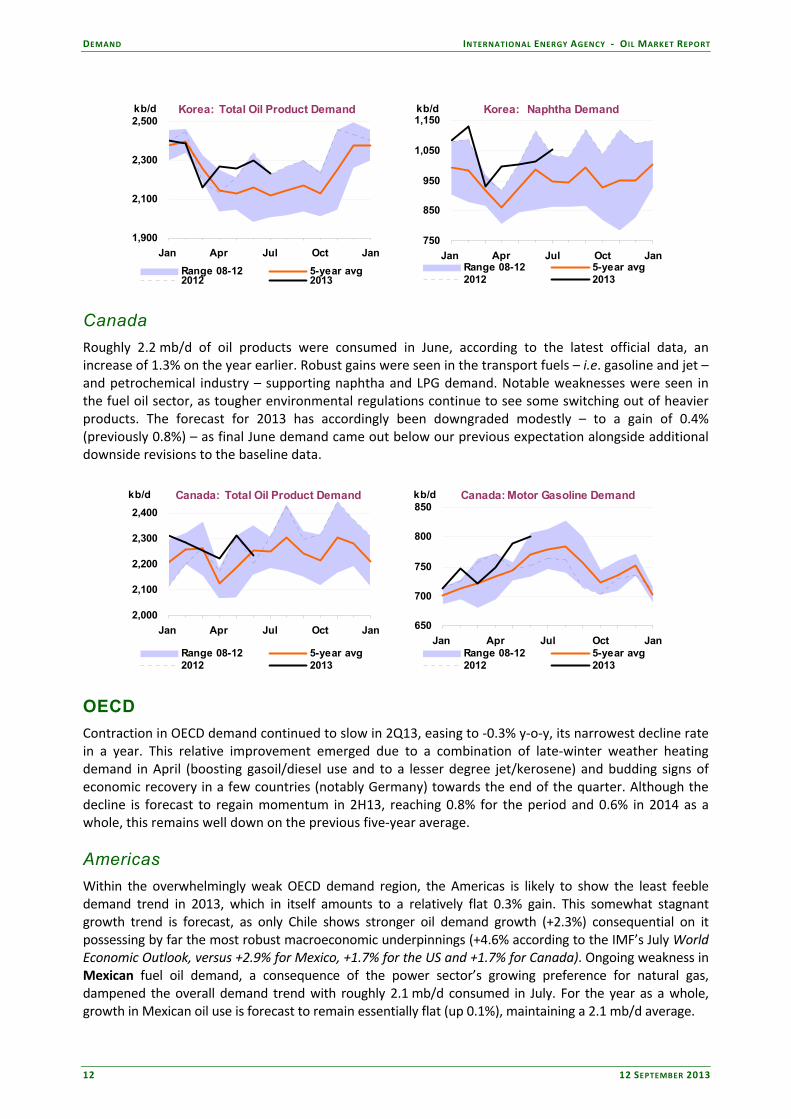

Canada

Roughly 2.2 mb/d of oil products were consumed in June, according to the latest official data, an increase of 1.3% on the year earlier. Robust gains were seen in the transport fuels – i.e. gasoline and jet – and petrochemical industry – supporting naphtha and LPG demand. Notable weaknesses were seen in the fuel oil sector, as tougher environmental regulations continue to see some switching out of heavier products. The forecast for 2013 has accordingly been downgraded modestly – to a gain of 0.4% (previously 0.8%) – as final June demand came out below our previous expectation alongside additional downside revisions to the baseline data.

Canada: Total Oil Product Demand

2,000

2,100

2,200

2,300

2,400

Jan Apr Jul Oct Jan

kb/d

Range 08-12 5-year avg2012 2013

Canada: Motor Gasoline Demand

650

700

750

800

850

Jan Apr Jul Oct Jan

kb/d

Range 08-12 5-year avg2012 2013

OECD

Contraction in OECD demand continued to slow in 2Q13, easing to ‐0.3% y‐o‐y, its narrowest decline rate in a year. This relative improvement emerged due to a combination of late‐winter weather heating demand in April (boosting gasoil/diesel use and to a lesser degree jet/kerosene) and budding signs of economic recovery in a few countries (notably Germany) towards the end of the quarter. Although the decline is forecast to regain momentum in 2H13, reaching 0.8% for the period and 0.6% in 2014 as a whole, this remains well down on the previous five‐year average.

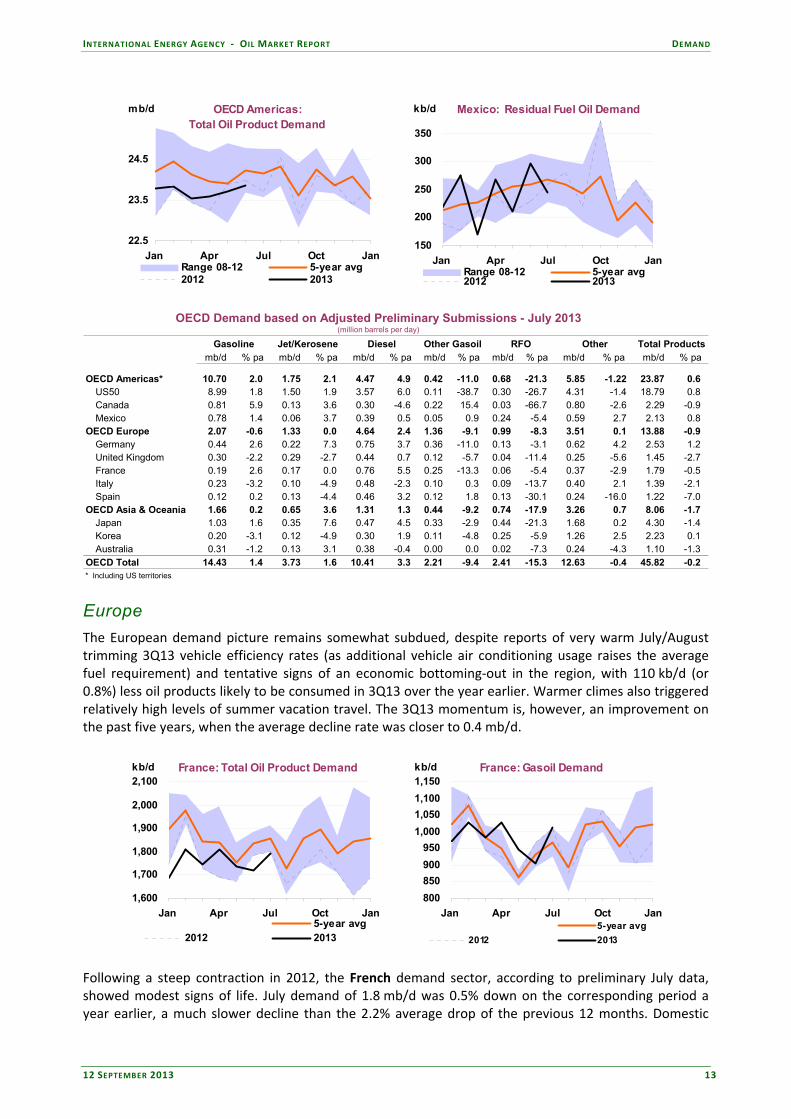

Americas

Within the overwhelmingly weak OECD demand region, the Americas is likely to show the least feeble demand trend in 2013, which in itself amounts to a relatively flat 0.3% gain. This somewhat stagnant growth trend is forecast, as only Chile shows stronger oil demand growth (+2.3%) consequential on it possessing by far the most robust macroeconomic underpinnings (+4.6% according to the IMF’s July World Economic Outlook, versus +2.9% for Mexico, +1.7% for the US and +1.7% for Canada). Ongoing weakness in Mexican fuel oil demand, a consequence of the power sector’s growing preference for natural gas, dampened the overall demand trend with roughly 2.1 mb/d consumed in July. For the year as a whole, growth in Mexican oil use is forecast to remain essentially flat (up 0.1%), maintaining a 2.1 mb/d average.

INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT DEMAND

12 SEPTEMBER 2013 13

OECD Americas:Total Oil Product Demand

22.5

23.5

24.5

Jan Apr Jul Oct Jan

mb/d

Range 08-12 5-year avg2012 2013

Mexico: Residual Fuel Oil Demand

150

200

250

300

350

Jan Apr Jul Oct Jan

kb/d

Range 08-12 5-year avg2012 2013

OECD Demand based on Adjusted Preliminary Submissions - July 2013(million barrels per day)

mb/d % pa mb/d % pa mb/d % pa mb/d % pa mb/d % pa mb/d % pa mb/d % pa

OECD Americas* 10.70 2.0 1.75 2.1 4.47 4.9 0.42 -11.0 0.68 -21.3 5.85 -1.22 23.87 0.6 US50 8.99 1.8 1.50 1.9 3.57 6.0 0.11 -38.7 0.30 -26.7 4.31 -1.4 18.79 0.8 Canada 0.81 5.9 0.13 3.6 0.30 -4.6 0.22 15.4 0.03 -66.7 0.80 -2.6 2.29 -0.9 Mexico 0.78 1.4 0.06 3.7 0.39 0.5 0.05 0.9 0.24 -5.4 0.59 2.7 2.13 0.8

OECD Europe 2.07 -0.6 1.33 0.0 4.64 2.4 1.36 -9.1 0.99 -8.3 3.51 0.1 13.88 -0.9 Germany 0.44 2.6 0.22 7.3 0.75 3.7 0.36 -11.0 0.13 -3.1 0.62 4.2 2.53 1.2 United Kingdom 0.30 -2.2 0.29 -2.7 0.44 0.7 0.12 -5.7 0.04 -11.4 0.25 -5.6 1.45 -2.7 France 0.19 2.6 0.17 0.0 0.76 5.5 0.25 -13.3 0.06 -5.4 0.37 -2.9 1.79 -0.5 Italy 0.23 -3.2 0.10 -4.9 0.48 -2.3 0.10 0.3 0.09 -13.7 0.40 2.1 1.39 -2.1 Spain 0.12 0.2 0.13 -4.4 0.46 3.2 0.12 1.8 0.13 -30.1 0.24 -16.0 1.22 -7.0

OECD Asia & Oceania 1.66 0.2 0.65 3.6 1.31 1.3 0.44 -9.2 0.74 -17.9 3.26 0.7 8.06 -1.7 Japan 1.03 1.6 0.35 7.6 0.47 4.5 0.33 -2.9 0.44 -21.3 1.68 0.2 4.30 -1.4 Korea 0.20 -3.1 0.12 -4.9 0.30 1.9 0.11 -4.8 0.25 -5.9 1.26 2.5 2.23 0.1 Australia 0.31 -1.2 0.13 3.1 0.38 -0.4 0.00 0.0 0.02 -7.3 0.24 -4.3 1.10 -1.3

OECD Total 14.43 1.4 3.73 1.6 10.41 3.3 2.21 -9.4 2.41 -15.3 12.63 -0.4 45.82 -0.2 * Including US territories

RFO Other Total ProductsGasoline Jet/Kerosene Diesel Other Gasoil

Europe

The European demand picture remains somewhat subdued, despite reports of very warm July/August trimming 3Q13 vehicle efficiency rates (as additional vehicle air conditioning usage raises the average fuel requirement) and tentative signs of an economic bottoming‐out in the region, with 110 kb/d (or 0.8%) less oil products likely to be consumed in 3Q13 over the year earlier. Warmer climes also triggered relatively high levels of summer vacation travel. The 3Q13 momentum is, however, an improvement on the past five years, when the average decline rate was closer to 0.4 mb/d.

France: Total Oil Product Demand

1,600

1,700

1,800

1,900

2,000

2,100

Jan Apr Jul Oct Jan

kb/d

5-year avg2012 2013

France: Gasoil Demand

800

850

900

950

1,000

1,050

1,100

1,150

Jan Apr Jul Oct Jan

kb/d

5-year avg

2012 2013

Following a steep contraction in 2012, the French demand sector, according to preliminary July data, showed modest signs of life. July demand of 1.8 mb/d was 0.5% down on the corresponding period a year earlier, a much slower decline than the 2.2% average drop of the previous 12 months. Domestic

DEMAND INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT

14 12 SEPTEMBER 2013

transport fuels led the upside, with total gasoil demand up 0.1% in July, to 1.0 mb/d, and gasoline use up 2.6% to 185 kb/d. The forecast for the year as a whole has been revised, to a decline rate of 1.4% versus the previous ‐2.1% estimate, consequential on roughly 75 kb/d being added to the July estimate and 35 kb/d to June.

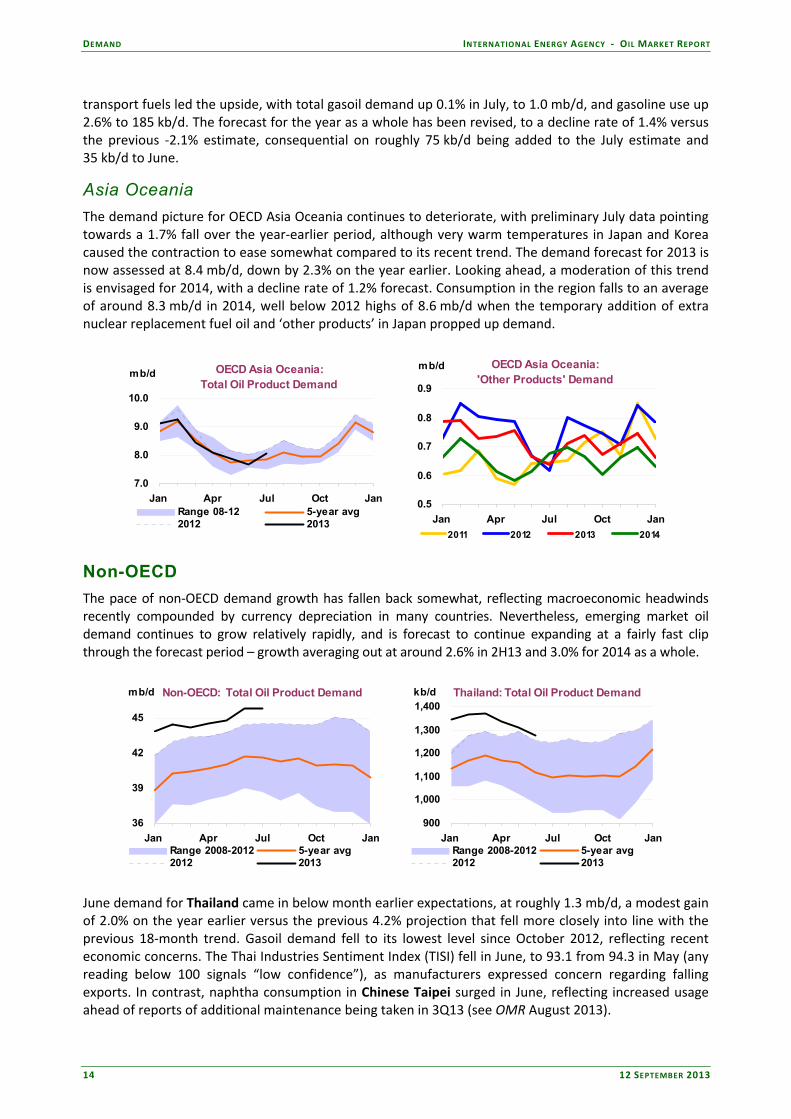

Asia Oceania

The demand picture for OECD Asia Oceania continues to deteriorate, with preliminary July data pointing towards a 1.7% fall over the year‐earlier period, although very warm temperatures in Japan and Korea caused the contraction to ease somewhat compared to its recent trend. The demand forecast for 2013 is now assessed at 8.4 mb/d, down by 2.3% on the year earlier. Looking ahead, a moderation of this trend is envisaged for 2014, with a decline rate of 1.2% forecast. Consumption in the region falls to an average of around 8.3 mb/d in 2014, well below 2012 highs of 8.6 mb/d when the temporary addition of extra nuclear replacement fuel oil and ‘other products’ in Japan propped up demand.

OECD Asia Oceania:Total Oil Product Demand

7.0

8.0

9.0

10.0

Jan Apr Jul Oct Jan

mb/d

Range 08-12 5-year avg2012 2013

OECD Asia Oceania:'Other Products' Demand

0.5

0.6

0.7

0.8

0.9

Jan Apr Jul Oct Jan

mb/d

2011 2012 2013 2014

Non-OECD

The pace of non‐OECD demand growth has fallen back somewhat, reflecting macroeconomic headwinds recently compounded by currency depreciation in many countries. Nevertheless, emerging market oil demand continues to grow relatively rapidly, and is forecast to continue expanding at a fairly fast clip through the forecast period – growth averaging out at around 2.6% in 2H13 and 3.0% for 2014 as a whole.

Non-OECD: Total Oil Product Demand

36

39

42

45

Jan Apr Jul Oct Jan

mb/d

Range 2008-2012 5-year avg2012 2013

Thailand: Total Oil Product Demand

900

1,000

1,100

1,200

1,300

1,400

Jan Apr Jul Oct Jan

kb/d

Range 2008-2012 5-year avg2012 2013

June demand for Thailand came in below month earlier expectations, at roughly 1.3 mb/d, a modest gain of 2.0% on the year earlier versus the previous 4.2% projection that fell more closely into line with the previous 18‐month trend. Gasoil demand fell to its lowest level since October 2012, reflecting recent economic concerns. The Thai Industries Sentiment Index (TISI) fell in June, to 93.1 from 94.3 in May (any reading below 100 signals “low confidence”), as manufacturers expressed concern regarding falling exports. In contrast, naphtha consumption in Chinese Taipei surged in June, reflecting increased usage ahead of reports of additional maintenance being taken in 3Q13 (see OMR August 2013).

INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT DEMAND

12 SEPTEMBER 2013 15

Taiwan: Total Oil Product Demand

700.0

800.0

900.0

1,000.0

1,100.0

1,200.0

Jan Apr Jul Oct Jan

kb/d

Range 2008-2012 5-year avg2012 2013

Taiwan: Naphtha Demand

150

250

350

450

Jan Apr Jul Oct Jan

kb/d

Range 2008-2012 5-year avg2012 2013

Further comprehensive analysis of Yemeni oil demand added roughly 30 kb/d to our 2010 estimate. This additional consumption reflects a reworking of our demand model to incorporate the latest data from the IEA’s Energy Statistics of non‐OECD Countries. Our projection of future trends here has been modestly curtailed since last month’s Report to incorporate the news that a new 400 megawatt gas‐power power plant, in the country’s eastern Marib province, should be open by mid‐2014. Fuel oil dominates the power mix in Yemen, but the opening of the new gas facility in 2014 should bring about a more rapid switch from oil to gas. The new plant should be sufficient to cover the total power sector needs of the capital Sana, which the ministry estimates at 320‐420 megawatts.

Non-OECD: Demand by Region(thousand barrels per day)

Annual Chg (kb/d) Annual Chg (%)

May-13 Jun-13 Jul-13 Jun-13 Jul-13 Jun-13 Jul-13

Africa 3,691 3,815 3,763 238 79 6.7 2.2

Asia 21,487 21,915 21,628 997 573 4.8 2.7

FSU 4,510 4,793 4,791 412 170 9.4 3.7

Latin America 6,537 6,534 6,605 171 175 2.7 2.7

Middle East 7,830 8,061 8,382 253 414 3.2 5.2

Non-OECD Europe 718 686 687 -58 5 -7.8 0.7

Total Products 44,773 45,804 45,856 2,014 1,416 4.6 3.2

Demand

SUPPLY INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT

16 12 SEPTEMBER 2013

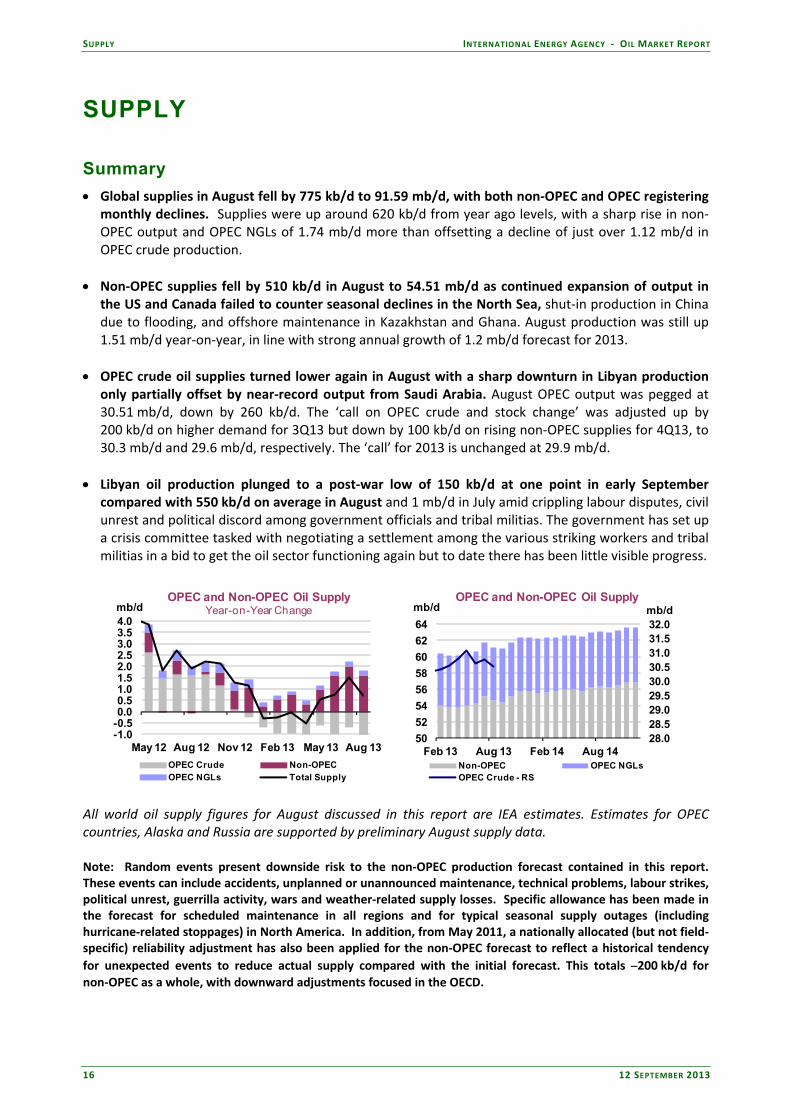

SUPPLY

Summary

Global supplies in August fell by 775 kb/d to 91.59 mb/d, with both non‐OPEC and OPEC registering monthly declines. Supplies were up around 620 kb/d from year ago levels, with a sharp rise in non‐OPEC output and OPEC NGLs of 1.74 mb/d more than offsetting a decline of just over 1.12 mb/d in OPEC crude production.

Non‐OPEC supplies fell by 510 kb/d in August to 54.51 mb/d as continued expansion of output in the US and Canada failed to counter seasonal declines in the North Sea, shut‐in production in China due to flooding, and offshore maintenance in Kazakhstan and Ghana. August production was still up 1.51 mb/d year‐on‐year, in line with strong annual growth of 1.2 mb/d forecast for 2013.

OPEC crude oil supplies turned lower again in August with a sharp downturn in Libyan production only partially offset by near‐record output from Saudi Arabia. August OPEC output was pegged at 30.51 mb/d, down by 260 kb/d. The ‘call on OPEC crude and stock change’ was adjusted up by 200 kb/d on higher demand for 3Q13 but down by 100 kb/d on rising non‐OPEC supplies for 4Q13, to 30.3 mb/d and 29.6 mb/d, respectively. The ‘call’ for 2013 is unchanged at 29.9 mb/d.

Libyan oil production plunged to a post‐war low of 150 kb/d at one point in early September compared with 550 kb/d on average in August and 1 mb/d in July amid crippling labour disputes, civil unrest and political discord among government officials and tribal militias. The government has set up a crisis committee tasked with negotiating a settlement among the various striking workers and tribal militias in a bid to get the oil sector functioning again but to date there has been little visible progress.

-1.0-0.50.00.51.01.52.02.53.03.54.0

May 12 Aug 12 Nov 12 Feb 13 May 13 Aug 13

mb/dOPEC and Non-OPEC Oil Supply

Year-on-Year Change

OPEC Crude Non-OPECOPEC NGLs Total Supply

28.028.529.029.530.030.531.031.532.0

50

52

54

56

58

60

62

64

Feb 13 Aug 13 Feb 14 Aug 14

mb/dmb/dOPEC and Non-OPEC Oil Supply

Non-OPEC OPEC NGLsOPEC Crude - RS

All world oil supply figures for August discussed in this report are IEA estimates. Estimates for OPEC countries, Alaska and Russia are supported by preliminary August supply data. Note: Random events present downside risk to the non‐OPEC production forecast contained in this report. These events can include accidents, unplanned or unannounced maintenance, technical problems, labour strikes, political unrest, guerrilla activity, wars and weather‐related supply losses. Specific allowance has been made in the forecast for scheduled maintenance in all regions and for typical seasonal supply outages (including hurricane‐related stoppages) in North America. In addition, from May 2011, a nationally allocated (but not field‐specific) reliability adjustment has also been applied for the non‐OPEC forecast to reflect a historical tendency

for unexpected events to reduce actual supply compared with the initial forecast. This totals ‒200 kb/d for non‐OPEC as a whole, with downward adjustments focused in the OECD.

INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT SUPPLY

12 SEPTEMBER 2013 17

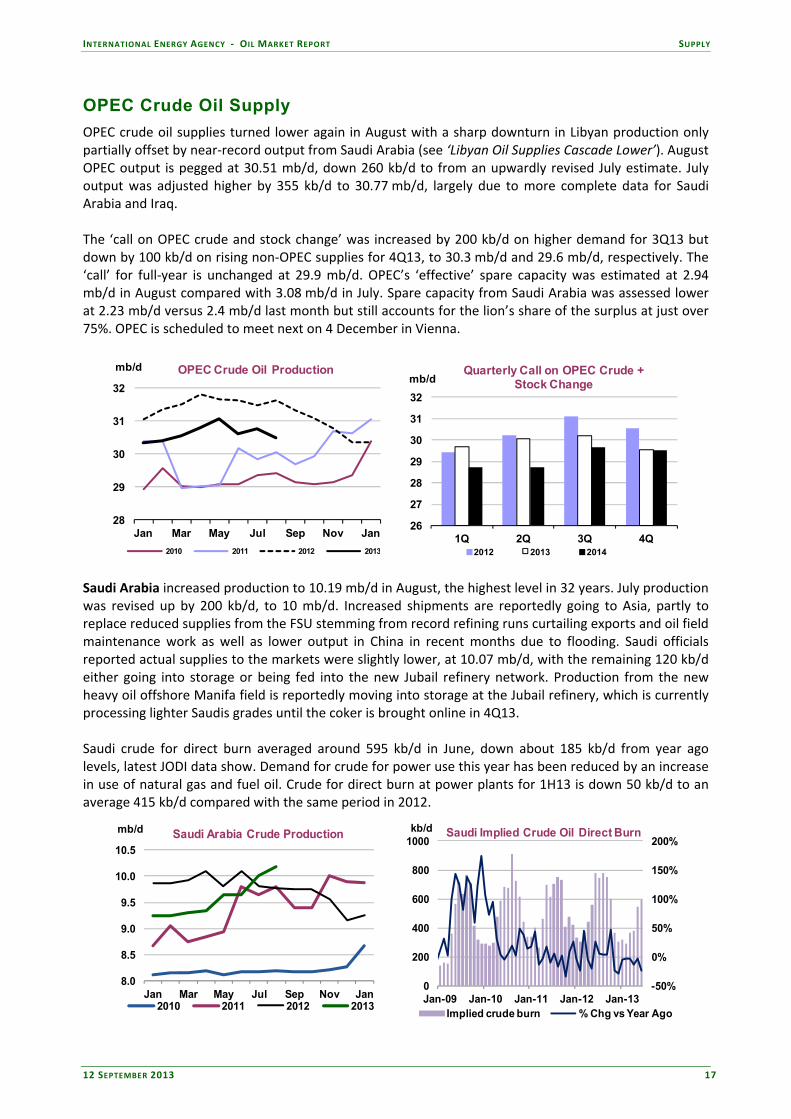

OPEC Crude Oil Supply

OPEC crude oil supplies turned lower again in August with a sharp downturn in Libyan production only partially offset by near‐record output from Saudi Arabia (see ‘Libyan Oil Supplies Cascade Lower’). August OPEC output is pegged at 30.51 mb/d, down 260 kb/d to from an upwardly revised July estimate. July output was adjusted higher by 355 kb/d to 30.77 mb/d, largely due to more complete data for Saudi Arabia and Iraq. The ‘call on OPEC crude and stock change’ was increased by 200 kb/d on higher demand for 3Q13 but down by 100 kb/d on rising non‐OPEC supplies for 4Q13, to 30.3 mb/d and 29.6 mb/d, respectively. The ‘call’ for full‐year is unchanged at 29.9 mb/d. OPEC’s ‘effective’ spare capacity was estimated at 2.94 mb/d in August compared with 3.08 mb/d in July. Spare capacity from Saudi Arabia was assessed lower at 2.23 mb/d versus 2.4 mb/d last month but still accounts for the lion’s share of the surplus at just over 75%. OPEC is scheduled to meet next on 4 December in Vienna.

28

29

30

31

32

Jan Mar May Jul Sep Nov Jan

mb/d OPEC Crude Oil Production

2010 2011 2012 2013

26

27

28

29

30

31

32

1Q 2Q 3Q 4Q

mb/dQuarterly Call on OPEC Crude +

Stock Change

2012 2013 2014

Saudi Arabia increased production to 10.19 mb/d in August, the highest level in 32 years. July production was revised up by 200 kb/d, to 10 mb/d. Increased shipments are reportedly going to Asia, partly to replace reduced supplies from the FSU stemming from record refining runs curtailing exports and oil field maintenance work as well as lower output in China in recent months due to flooding. Saudi officials reported actual supplies to the markets were slightly lower, at 10.07 mb/d, with the remaining 120 kb/d either going into storage or being fed into the new Jubail refinery network. Production from the new heavy oil offshore Manifa field is reportedly moving into storage at the Jubail refinery, which is currently processing lighter Saudis grades until the coker is brought online in 4Q13. Saudi crude for direct burn averaged around 595 kb/d in June, down about 185 kb/d from year ago levels, latest JODI data show. Demand for crude for power use this year has been reduced by an increase in use of natural gas and fuel oil. Crude for direct burn at power plants for 1H13 is down 50 kb/d to an average 415 kb/d compared with the same period in 2012.

8.0

8.5

9.0

9.5

10.0

10.5

Jan Mar May Jul Sep Nov Jan

mb/d Saudi Arabia Crude Production

2010 2011 2012 2013

-50%

0%

50%

100%

150%

200%

0

200

400

600

800

1000

Jan-09 Jan-10 Jan-11 Jan-12 Jan-13

kb/d Saudi Implied Crude Oil Direct Burn

Implied crude burn % Chg vs Year Ago

SUPPLY INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT

18 12 SEPTEMBER 2013

Iraqi crude oil output edged higher in August, up by just over 100 kb/d to 3.17 mb/d. July output was revised up by 70 kb/d to 3.06 mb/d, largely due to higher‐than‐forecast crude burn at power stations. Total exports rose about 165 kb/d to 2.47 mb/d in August, with southern shipments exceptionally robust while northern volumes remained constrained. Exports of Basrah crude rose by 140 kb/d to 2.29 mb/d as State Oil Marketing Co (SOMO) ramped up volumes ahead of planned maintenance work at the southern Basrah and Khor Al‐Amaya shipping terminals in September.

2.2

2.4

2.6

2.8

3.0

3.2

3.4

Jan Mar May Jul Sep Nov Jan

mb/d Iraq Crude Production

2010 2011 2012 2013

0.0

0.5

1.0

1.5

2.0

Jan 12 Apr 12 Jul 12 Oct 12 Jan 13 Apr 13 Jul 13

mb/d Basrah Oil Exports

Far East Europe US Conflicting reports for the outlook for southern exports in September and through the end of the year have forced traders and refiners to seek replacement barrels, especially in Asia where 70% of Basrah crude is normally processed. Officials initially told regular buyers that planned infrastructure work at the Gulf export terminals would cut shipments by as much as 500 kb/d in September but reversed course in mid‐August and said the project would be postponed. However, contractors said in September it was not possible to scale back and alter plans for the terminal work. That said, the 8 September work start date has been delayed 4‐5 days due to unexpected technical issues. SOMO nominations were cut to 1.8 mb/d from 2.3 mb/d, or about 500 kb/d. Amid all the confusion regular buyers of Iraqi crude are lining up alternative supplies, which in turn has elevated price differentials for competing crudes such as Urals, Azeri and other sour grades in Europe as well as Middle East grades such as Abu Dhabi’s Murban. Northern exports of Kirkuk crude were only marginally higher in August, up around 25 kb/d to 180 kb/d. Militant attacks on the key pipeline running to the Mediterranean port of Ceyhan continue to disrupt export flows, with volumes nearly halved from a 2013 peak of 330 kb/d in March. In addition, shipments from the Kurdistan region to the Kirkuk‐Ceyhan crude pipeline remain shut‐off. The ongoing dispute over payment and contract terms between Baghdad and the Kurdistan Regional Government (KRG) has been complicated by the KRG’s decision to go ahead with new pipeline projects to let exports bypass the Kirkuk‐Ceyhan line controlled by the central government. A further 40‐50 kb/d of crude and condensates is moving via trucks through Turkey. Crude production in the KRG area was estimated at 140 kb/d in August. Iran’s crude oil production rose to 2.68 mb/d in August, up 30 kb/d from July levels. Preliminary data show total crude imports from Iran averaged 985 kb/d in August, up just under 100 kb/d from July levels. Data for July imports were revised down to 900 kb/d compared with 1.16 mb/d reported last month. In August China, Japan, South Korea, Turkey, the UAE and Syria imported Iranian crude, tanker data show. Import volumes are based on data submitted by OECD countries, non‐OECD statistics from customs agencies, tanker movements and news reports. After payment problems stalled liftings in July, preliminary data show India posted the largest month‐on‐month increase in August, up 125 kb/d to around 165 kb/d. Japanese imports from Iran rose by about 50 kb/d to 225 kb/d in August while China increased volumes to 440 kb/d from around 400 kb/d in July. Last month, Syria imported crude for the third time this year, at around 30 kb/d.

INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT SUPPLY

12 SEPTEMBER 2013 19

2.5

2.7

2.9

3.1

3.3

3.5

3.7

3.9

Jan Mar May Jul Sep Nov Jan

mb/d Iran Crude Production

2010 2011 2012 2013

0.0

0.5

1.0

1.5

2.0

2.5

3.0

0.0

0.2

0.4

0.6

0.8

1.0

1.2

Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13

mb/d Iranian Crude Imports

Total - RHS OECD EUROECD PAC China / IndiaOther Non-OECD

Washington extended six‐month waivers of US sanctions in early September to Japan and the ten European Union nations also already operating under the EU’s July 2012 embargo. The State Department will review waivers to China, India, South Korea, Turkey, and five other countries in December.

Production from Kuwait and the UAE each declined by 30 kb/d in August, to 2.77 mb/d and 2.72 mb/d, respectively. Qatari output was unchanged at 725 kb/d.

Jun 2013 Jul 2013 Aug 2013

Supply Supply Supply

Algeria 1.12 1.15 1.12 1.18 0.06 1.15

Angola 1.78 1.73 1.70 1.89 0.19 1.76

Ecuador 0.52 0.52 0.52 0.53 0.01 0.51

Iran 2.70 2.65 2.68 2.97 0.29 2.69

Iraq 3.05 3.06 3.17 3.33 0.17 3.10

Kuwait2 2.82 2.80 2.77 2.90 0.13 2.82

Libya 1.15 1.00 0.55 1.40 0.85 1.34

Nigeria3 1.88 1.92 1.90 2.25 0.35 1.97

Qatar 0.73 0.73 0.73 0.75 0.03 0.73

Saudi Arabia2 9.65 10.00 10.19 12.40 2.21 9.41

UAE 2.73 2.75 2.72 2.90 0.18 2.69

Venezuela4 2.50 2.47 2.47 2.60 0.14 2.48

Total OPEC 30.62 30.77 30.51 35.10 4.59 30.63

(excluding Iraq, Nigeria, Libya and Iran) 2.94

1 Capacity levels can be reached within 30 days and sustained for 90 days.2 Includes half of Neutral Zone production.

3 Nigeria's current capacity estimate excludes some 200 kb/d of shut-in capacity.

4 Includes upgraded Orinoco extra-heavy oil assumed at 435 kb/d in August.

Sustainable Production

Capacity1

Spare Capacity vs Aug 2013

Supply

1H13 Average Crude Supply

OPEC Crude Production(million barrels per day)

Ecuador’s production averaged 520 kb/d in August. Increased output is due to reconditioning of wells and increased drilling of horizontal wells, which has led to an upward baseline revision of 20 kb/d from May to July. Venezuelan production in August was unchanged at 2.47 mb/d.

Nigerian output edged lower in August, off 20 kb/d to 1.9 mb/d. Production has stayed below 2 mb/d for the fifth consecutive month due to escalating oil thefts damaging pipeline infrastructure. In early September ENI lifted the force majeure on its Brass River crude oil production that had been in place since last March. Bonny Light exports remain under force majeure since April, affecting about 150 kb/d. Export loading schedules indicate volumes should start to recover in October and November.

Angolan crude output declined by 25 kb/d to 1.7 mb/d in August. The lower output stemmed from outages at the Saturno field, part of the 150 kb/d PSVM project. As a result, BP declared force majeure on its Saturno exports on 21 August due to technical problems.

SUPPLY INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT

20 12 SEPTEMBER 2013

Libyan Oil Supplies Cascade Lower

Oil production in Libya plunged to a post‐war low of 150 kb/d at one point in early September compared with 550 kb/d on average in August and 1 mb/d in July amid crippling labour disputes, civil unrest and political infighting among tribal militias. Exports have tumbled to just 80 kb/d versus 1.2 mb/d previously, with shipments operating only from the country’s two offshore fields, Bouri and al Jurf. The burgeoning crisis, the worst since the onset of the civil war in early 2011, is weakening already‐fragile government institutions and choking off vital revenues. Striking workers have halted exports and forced the closure of the eastern region’s oil‐producing fields off and on since the end of May. Tribal groups are now pushing for federalism whereby regions control export flows and revenues.

In late August, Libya's largest western oilfields were closed after militants shut down the pipeline linking the fields to the ports. The two major fields affected were Elephant and El Sharara, which have a combined capacity of around 500 kb/d. After reaching a 2013 high of 1.42 mb/d in April, production has steadily was averaging 250 kb/d in the first week of September. This compares to an average of 1.4 mb/d in 2012, 460 kb/d in 2011 and 1.55 mb/d in 2010, pre‐civil war.

The government has set up a crisis committee tasked with negotiating a settlement among the various striking workers and tribal militias in a bid to get the oil sector functioning again. The head of the government energy committee, however, said little headway had been made between government and tribal mediators as well as with an array of protest groups. The striking workers and disgruntled civilians are demanding a multitude of changes, ranging from improved pay packages and management changes to a share of the revenues and greater regional autonomy, which have combined to complicate the already challenging negotiations.

2010 2011 2012 Jan‐13 Feb‐13 Mar‐13 Apr‐13 May‐13 Jun‐13 Jul‐13 Aug‐13

Crude Oil 1550 458 1387 1380 1400 1360 1420 1350 1150 1000 550

NGLs 111 27 89 99 99 99 90 90 90 80 80

Total 1661 485 1476 1479 1499 1459 1510 1440 1240 1080 630

Libyan Crude and NGL Production (kb/d)

Aside from the offshore exports, Libyan terminals have been shut by port worker strikes or following occupation by members of the Petroleum Facilities Guard. Newswire reports in late August indicated that the Marsa al Brega and Marsa al Hariga terminals would return to normal by early September proved overly optimistic, and recent tanker tracking data do not support these claims. Indeed, according to tracking data, the last crude cargo to leave Libya was a 700 kb Aframax tanker which left the offshore Bouri terminal on 20 August, bound for Italy. Previous to this, the land‐based Zaiwa terminal was exporting regular cargos until 19 August. The country’s main crude export terminal at Es Sider last exported a cargo on 26 July when an Aframax left for Spain.

The country’s five domestic refineries with a combined capacity of 378 kb/d have only operated sporadically since the civil war, with prolonged shutdowns reported. The largest refinery, the 220 kb/d Ras Lanuf plant, has also been closed due to worker protests and the lack of crude, as did the 120 kb/d Zawiya refinery. Latest estimates of Libyan refinery crude throughputs were around 120 kb/d in July, with the remainder of the crude exported.

Recent import data indicate that the bulk of Libya’s crude exports head to OECD member countries, with OECD Europe taking just under 900 kb/d so far in 2013 (June is the latest month for which OECD import data are available). To date, Italy has been Libya’s largest customer. A large proportion of Libya’s exports are used by refiners in the Mediterranean basin or in other European countries with pipeline access to Mediterranean import terminals. Australia is the only OECD member taking significant long‐haul Libyan volumes, although it has cut imports steadily since February.

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

Jan-11 Oct-11 Jul-12 Apr-13

mb/d Libya Crude Production

INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT SUPPLY

12 SEPTEMBER 2013 21

Libyan Oil Supplies Cascade Lower (continued)

Outside of the OECD, recent tanker tracking data indicate that so far in 2013, sporadic cargoes of Libyan crude have been occasionally heading to Asia, notably China, Indonesia and Thailand.

2009 2010 2011 2012 Jan‐13 Feb‐13 Mar‐13 Apr‐13 May‐13 Jun‐13% of total crude

imports (2012)

France 131 210 64 128 134 147 114 92 127 135 11.2%

Germany 167 147 56 173 170 190 195 197 183 203 9.2%

Italy 413 368 96 288 273 219 218 223 302 216 20.9%

Spain 102 138 23 98 92 109 57 57 96 67 8.3%

United Kingdom 37 55 15 59 0 86 97 96 79 59 5.5%

Other OECD Europe 135 168 38 167 243 206 121 110 144 130 3.7%

Total OECD Europe 986 1086 293 914 912 956 803 775 930 811 8.2%

Total OECD 1049 1140 312 1018 970 1026 929 858 1043 948 3.7%

OECD Crude Imports from Libya (kb/d)

Since Libyan crudes are light and sweet in nature, they have high yields of gasoline, low‐sulphur diesel and jet fuel, which make them highly sought‐after by European refiners. They are also difficult to replace since there are few crudes of similar quality. The closest quality replacement crudes for the lost Libyan streams of Es Sider, Sarir, El Shahara and Bu Attifel are Ekofisk and Brent crudes from the North Sea, BTC Blend from the FSU, Bonny and Qua Iboe from Nigeria and Algerian Saharan Blend. In the last few month, due to seasonal maintenance in the North Sea, the output of Ekofisk and Brent has been constrained, helping to propel North Sea Dated prices to their recent highs. It is also worth noting that during the 2011 Libyan civil war European refiners were forced to turn to incremental sour supplies made available by OPEC members, notably Saudi Arabia, which were not a like‐for‐like replacement for lost Libyan crudes. Additionally, the increasing sweet‐sour differentials over 2011 also drew in limited supplies to Europe of light, sweet Latin American and West African crudes, which would otherwise have been used by US Gulf Coast refiners.

Bu AttifelEl Shahara

Saharan Blend

Qua IboeBonny

SarirCusiana

Es Sider Forties

Arab Extra Light

Brazil Roncador

Arab Light

KirkukArab Medium

Basrah Light

Brent

0.0

0.5

1.0

1.5

2.0

2.5

3.0

% S

ulp

hu

r

API

Selected Crude Oil Export Streams by Quality

BTC

28 32 36 40 44 48

SUPPLY INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT

22 12 SEPTEMBER 2013

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

1Q10 4Q10 3Q11 2Q12 1Q13 4Q13 3Q14

mb/d Total Non-OPEC Supply, y-o-y chg

Other North America Total

Non-OPEC Overview

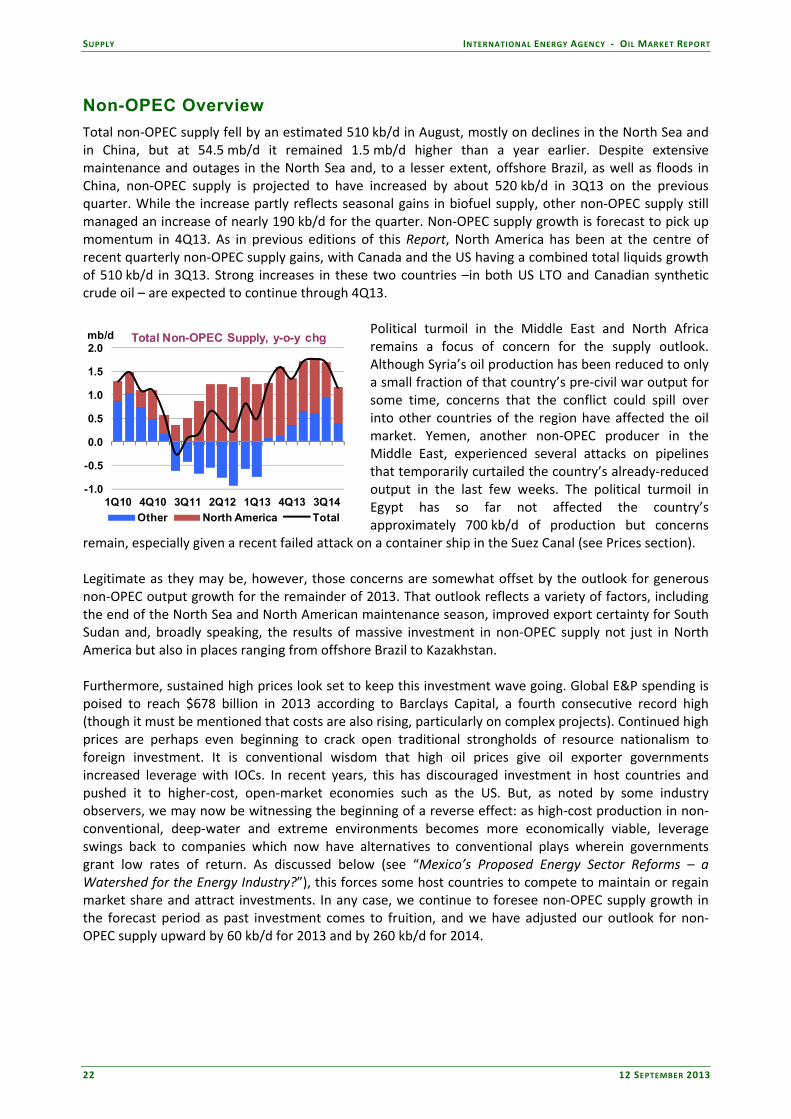

Total non‐OPEC supply fell by an estimated 510 kb/d in August, mostly on declines in the North Sea and in China, but at 54.5 mb/d it remained 1.5 mb/d higher than a year earlier. Despite extensive maintenance and outages in the North Sea and, to a lesser extent, offshore Brazil, as well as floods in China, non‐OPEC supply is projected to have increased by about 520 kb/d in 3Q13 on the previous quarter. While the increase partly reflects seasonal gains in biofuel supply, other non‐OPEC supply still managed an increase of nearly 190 kb/d for the quarter. Non‐OPEC supply growth is forecast to pick up momentum in 4Q13. As in previous editions of this Report, North America has been at the centre of recent quarterly non‐OPEC supply gains, with Canada and the US having a combined total liquids growth of 510 kb/d in 3Q13. Strong increases in these two countries –in both US LTO and Canadian synthetic crude oil – are expected to continue through 4Q13.

Political turmoil in the Middle East and North Africa remains a focus of concern for the supply outlook. Although Syria’s oil production has been reduced to only a small fraction of that country’s pre‐civil war output for some time, concerns that the conflict could spill over into other countries of the region have affected the oil market. Yemen, another non‐OPEC producer in the Middle East, experienced several attacks on pipelines that temporarily curtailed the country’s already‐reduced output in the last few weeks. The political turmoil in Egypt has so far not affected the country’s approximately 700 kb/d of production but concerns

remain, especially given a recent failed attack on a container ship in the Suez Canal (see Prices section). Legitimate as they may be, however, those concerns are somewhat offset by the outlook for generous non‐OPEC output growth for the remainder of 2013. That outlook reflects a variety of factors, including the end of the North Sea and North American maintenance season, improved export certainty for South Sudan and, broadly speaking, the results of massive investment in non‐OPEC supply not just in North America but also in places ranging from offshore Brazil to Kazakhstan. Furthermore, sustained high prices look set to keep this investment wave going. Global E&P spending is poised to reach $678 billion in 2013 according to Barclays Capital, a fourth consecutive record high (though it must be mentioned that costs are also rising, particularly on complex projects). Continued high prices are perhaps even beginning to crack open traditional strongholds of resource nationalism to foreign investment. It is conventional wisdom that high oil prices give oil exporter governments increased leverage with IOCs. In recent years, this has discouraged investment in host countries and pushed it to higher‐cost, open‐market economies such as the US. But, as noted by some industry observers, we may now be witnessing the beginning of a reverse effect: as high‐cost production in non‐conventional, deep‐water and extreme environments becomes more economically viable, leverage swings back to companies which now have alternatives to conventional plays wherein governments grant low rates of return. As discussed below (see “Mexico’s Proposed Energy Sector Reforms – a Watershed for the Energy Industry?”), this forces some host countries to compete to maintain or regain market share and attract investments. In any case, we continue to foresee non‐OPEC supply growth in the forecast period as past investment comes to fruition, and we have adjusted our outlook for non‐OPEC supply upward by 60 kb/d for 2013 and by 260 kb/d for 2014.

INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT SUPPLY

12 SEPTEMBER 2013 23

OECD

North America

US – July preliminary; Alaska actual, other states estimated: US crude oil production averaged 1.1 mb/d higher in July 2013 than in July 2012, at 7.5 mb/d. Preliminary weekly figures for August show production holding steady, with declines in Alaska compensated by continued growth in tight oil at the Eagle Ford (where over 5,700 oil and gas wells have been drilled since 2008) and Permian basins in Texas. Likewise, 3Q13 crude oil production is forecast at 7.5 mb/d. Disruption risks in the US Gulf of Mexico at the peak of the hurricane season make for a forecast of a slight decline in September. On the other hand, the development of new shale plays, such as the Mississippian‐Woodford Trend in Oklahoma and Kansas, augurs continued production growth into the medium term, when some existing shale oil plays may begin to decline.

Pipeline and rail transport capacity continues to expand and thereby accommodate production growth, with about 500 kb/d of crude oil pipeline capacity added in the US in 2013. The 700 kb/d‐capacity Gulf Coast pipeline from the Cushing hub to Houston is targeted for completion by the end of the year. Alaska crude production fell below 500 kb/d in June and is forecast to remain below that level through 2014. Additional US West Coast refineries, such as the Puget Sound plant in Washington state, are exploring the possibility of rail transport of North Dakota crude to make up for declining Alaska tanker shipments. Tesoro already has a