Embed Size (px)

Citation preview

1/10

Innovation and cost reduction in offshore wind Kate Freeman

Offshore Wind Journal Conference

February 7 2017

2/10

• Recent trends in offshore wind LCOE

• Time is money – how the speed of installation influences

cost of energy

• Scale versus cost – can we get the balance right?

Contents

Agenda Innovations and cost reduction in offshore wind

Selected clients

BVG Associates

Business advisory

• Analysis and forecasting

• Strategic advice

• Business and supply chain development

Technology

• Engineering services

• Due diligence

• Strategy and R&D support

Economics

• Socioeconomics and local benefits

• Technology and project economic modelling

• Policy and local content assessment

© BVG Associates 2017

3/10 © BVG Associates 2017

4/10

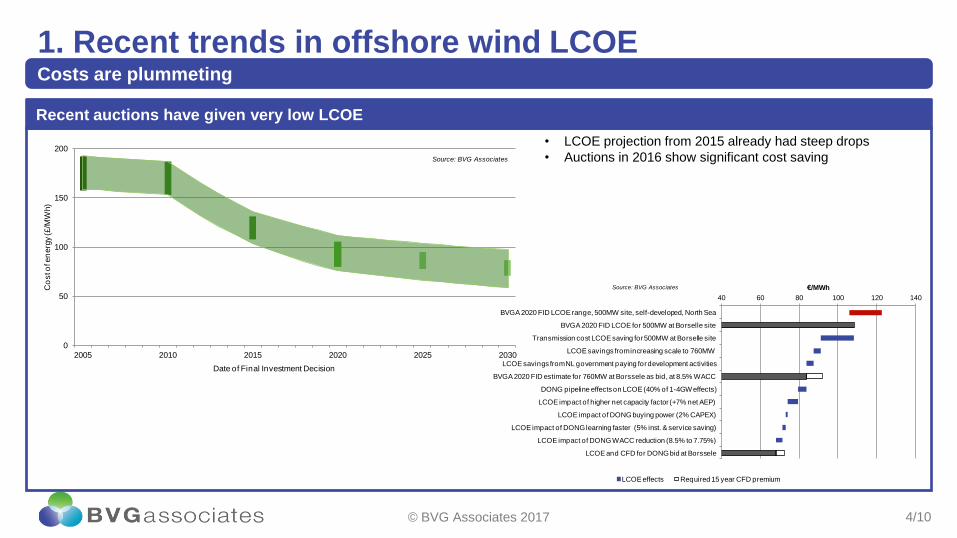

1. Recent trends in offshore wind LCOE Costs are plummeting

• LCOE projection from 2015 already had steep drops

• Auctions in 2016 show significant cost saving

Recent auctions have given very low LCOE

© BVG Associates 2017

0

50

100

150

200

2005 2010 2015 2020 2025 2030

Co

st o

f en

erg

y (£

/MW

h)

Date of Final Investment Decision

Source: BVG Associates

40 60 80 100 120 140

BVGA 2020 FID LCOE range, 500MW site, self-developed, North Sea

BVGA 2020 FID LCOE for 500MW at Borselle site

Transmission cost LCOE saving for 500MW at Borselle site

LCOE savings from increasing scale to 760MW

LCOE savings from NL government paying for development activities

BVGA 2020 FID estimate for 760MW at Borssele as bid, at 8.5% WACC

DONG pipeline effects on LCOE (40% of 1-4GW effects)

LCOE impact of higher net capacity factor (+7% net AEP)

LCOE impact of DONG buying power (2% CAPEX)

LCOE impact of DONG learning faster (5% inst. & service saving)

LCOE impact of DONG WACC reduction (8.5% to 7.75%)

LCOE and CFD for DONG bid at Borssele

€/MWh

LCOE effects Required 15 year CFD premium

Source: BVG Associates

5/10

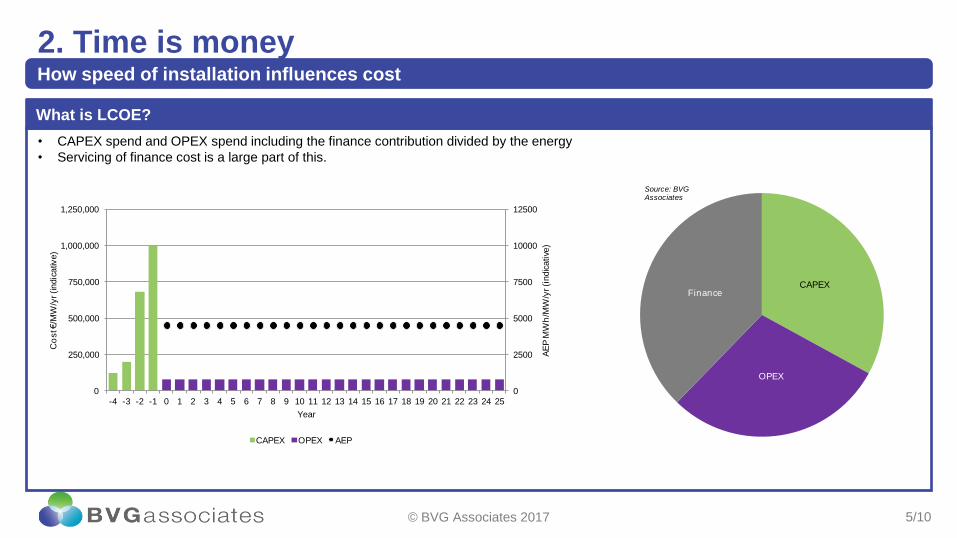

2. Time is money How speed of installation influences cost

• CAPEX spend and OPEX spend including the finance contribution divided by the energy

• Servicing of finance cost is a large part of this.

What is LCOE?

© BVG Associates 2017

0

2500

5000

7500

10000

12500

0

250,000

500,000

750,000

1,000,000

1,250,000

-4 -3 -2 -1 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

AE

P M

Wh

/MW

/yr (i

ndic

ative

)

Co

st €

/MW

/yr (indic

ativ

e)

Year

CAPEX OPEX AEP

CAPEX

OPEX

Finance

Source: BVG Associates

6/10

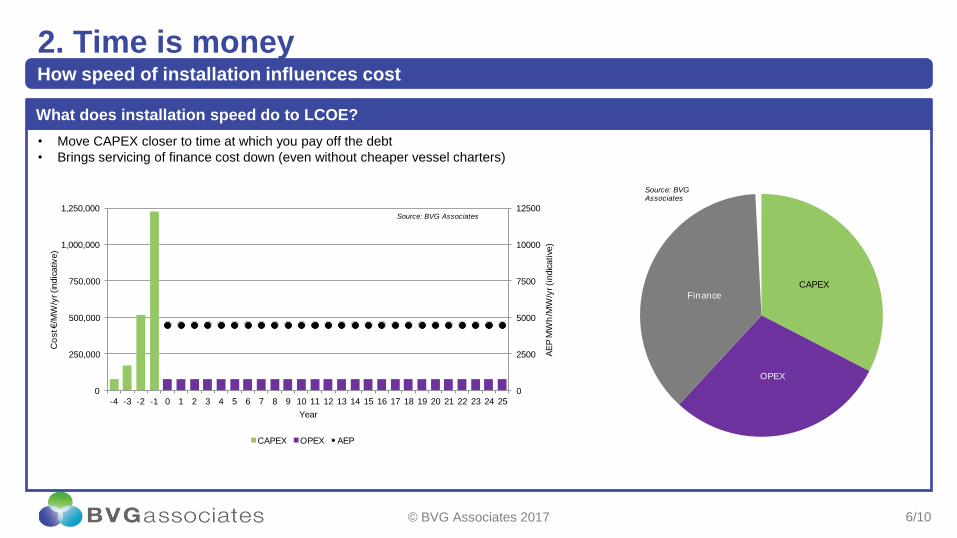

2. Time is money How speed of installation influences cost

• Move CAPEX closer to time at which you pay off the debt

• Brings servicing of finance cost down (even without cheaper vessel charters)

What does installation speed do to LCOE?

© BVG Associates 2017

0

2500

5000

7500

10000

12500

0

250,000

500,000

750,000

1,000,000

1,250,000

-4 -3 -2 -1 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

AE

P M

Wh

/MW

/yr (i

ndic

ative

)

Co

st €

/MW

/yr (indic

ativ

e)

Year

CAPEX OPEX AEP

Source: BVG Associates

CAPEX

OPEX

Finance

Source: BVG Associates

7/10

3. Scale versus cost Can we get the balance right?

• Too many were surprised by the rapid introduction of 8MW turbines

• A lot of investment in turbine installation vessels but the fleet no longer looks fit for purpose

• Upgrades to vessels (legs and cranes) can plug the gap in the short term

• Are there any vessels that can install a 10MW+

• When vessel investments were committed in 2010-12, the forecast market was a lot larger

• Is there a business case for a new vessel?

Collaboration is vital

© BVG Associates 2017

Look at the site-by-site saving of moving

from 8MW to 10MW. If everything else

costs the same, you would have a saving

of 20% in CAPEX and 20% in OPEX.

In AEP, the saving from array interactions

using a similarly MW/km2 density is around

0.2%.

• Fewer sites to build and connect

• Fewer turbines to block the wind flow for the others

• Fewer pieces of equipment to go wrong

BUT

• Need bigger vessels that can handle the large structures

• Move from tried and tested machines to less proven (and first of a kind) technologies

• When a single turbine goes down, a larger fraction of the wind farm energy is being lost

From a simple cost of energy position, bigger is better

8/10

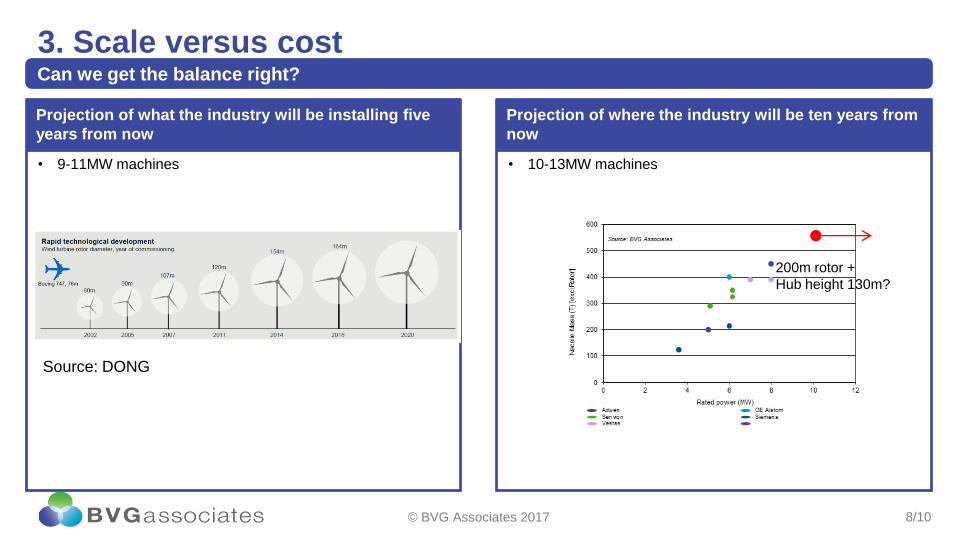

3. Scale versus cost Can we get the balance right?

• 9-11MW machines

Projection of what the industry will be installing five

years from now

© BVG Associates 2017

• 10-13MW machines

Projection of where the industry will be ten years from

now

Source: DONG

200m rotor +

Hub height 130m?

9/10

4. Conclusions So what?

• The recent cost reductions will cause project developers to focus on those areas where they can reduce cost. You are going to see

hard bargaining.

• Speed of installation as well as overall cost of installation can help reduce cost. Anything that you can do to have slicker processes

will help. Anything that you can do to avoid weather downtime will help.

• Turbines are going to get a lot bigger. Project developers are banking on this and are banking on being able to handle them.

Prepare for the future

© BVG Associates 2017

10/10

Thank you BVG Associates Ltd

The Blackthorn Centre

Purton Road

Cricklade, Swindon

SN6 6HY UK

tel +44 (0) 1793 752 308

@bvgassociates

www.bvgassociates.com

BVG Associates Ltd

The Boathouse

Silversands

Aberdour, Fife

KY3 0TZ UK

tel +44 (0) 1383 870 014

BVG Associates LLC

874 Walker Road

Suite C

Dover

Delaware

19904 USA

tel +1 (313) 462 0673

This presentation and its content is copyright of BVG Associates Limited - © BVG Associates 2017. All rights are reserved.

Any redistribution or reproduction of part or all of the contents of this presentation in any form is prohibited other than the following:

• You may print or download to a local hard disk extracts for your personal and non-commercial use only.

• You may copy the content to individual third parties for their personal use, but only if you acknowledge BVG Associates as the source

of the material.

You may not, except with our express written permission, distribute or commercially exploit the content.

© BVG Associates 2017