Embed Size (px)

DESCRIPTION

changing landscape of marketing

Citation preview

Objective

Revolutionary impact of digital technology and how is it adapted by consumers and marketers

How has this changed consumers and marketers

Trends in Media

Impact of Digital technology on Education and

e-learning

Opened‐up learning to multiple delivery methods - in‐campus, distance learning ,e‐Learning and m-

learning

iPhone and iPad stamps their marks on the education sector

e-Books enter mainstream and students start embracing

Impact of Digital technology on Politics and

Finance

Perfected online fundraising by using social media

tools

Changed political fundraising & electioneering forever

Raised $45 million online

U.S. President: Barak Obama

Embedded hardware & service solutions in the

finance sector

Enabled investors an ability to crunch, analysis &

store data

Lifeline for mutual & hedge funds, insurance

brokers, banks & finance institutions

Mayor : Michael Bloomberg

Impact of Digital technology on Music and

Social Engagement

Salvaged the music business from declining CD‟s sales

Introduced iPod music player, iTunes digital music

software, the iTunes Store and iPad

Apple CEO Steve Jobs

Super‐sized dating possibilities at Harvard

University

Transitioned into a global social media

phenomenon

Delivered platform to connect and expand

friend/biz contacts

Facebook: Mark Zuckerberg

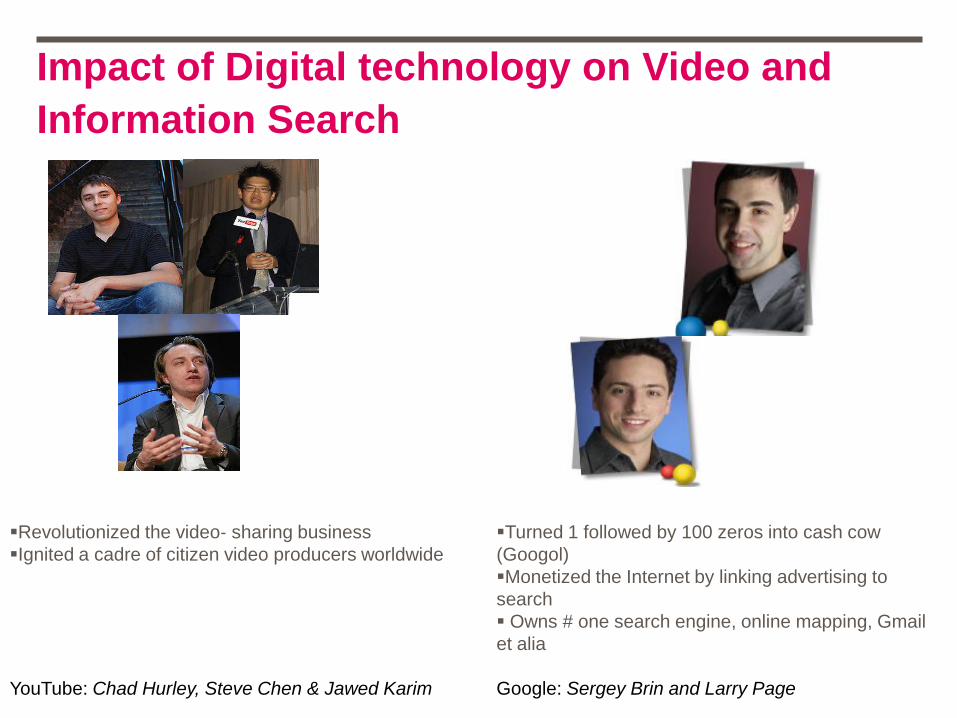

Impact of Digital technology on Video and

Information Search

Revolutionized the video‐ sharing business

Ignited a cadre of citizen video producers worldwide

YouTube: Chad Hurley, Steve Chen & Jawed Karim

Turned 1 followed by 100 zeros into cash cow

(Googol)

Monetized the Internet by linking advertising to

search

Owns # one search engine, online mapping, Gmail

et alia

Google: Sergey Brin and Larry Page

Plus ηa change, plus c'est la mκme chose.

In times of great change it is important to reflect

upon what has changed and what remains

unchanged

The New Age Marketing

“It‟s the economy stupid”

James Carville ,1992

“It‟s a people driven economy stupid”

Erik Qualman, 2009

What has changed ?

Production Consumption

Technology Information search ,compare & select products

Distribution Consume and share experiences

Who has triggered this change ?

Consumers

Four Ps of Marketing

Traditional Media Digital Media ( SN/Search, DTH/Mobile etc)

Product, Price

Place and Promotion

Shift in consumer control

Pre-Digital

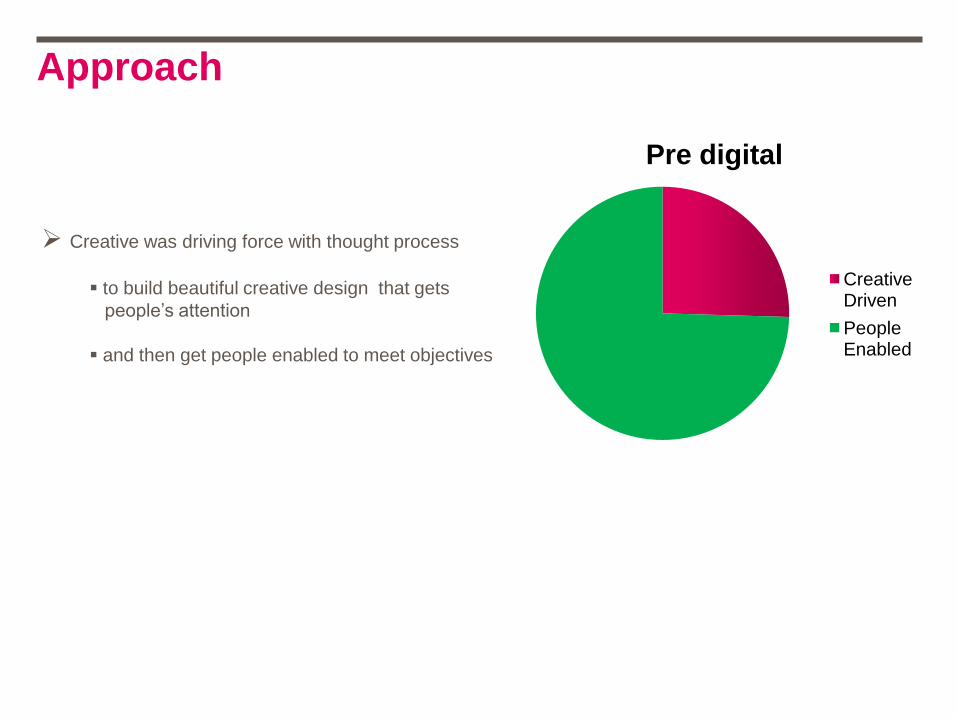

Approach

Pre digital

Creative Driven

People Enabled

Creative was driving force with thought process

to build beautiful creative design that gets

people‟s attention

and then get people enabled to meet objectives

Consumer

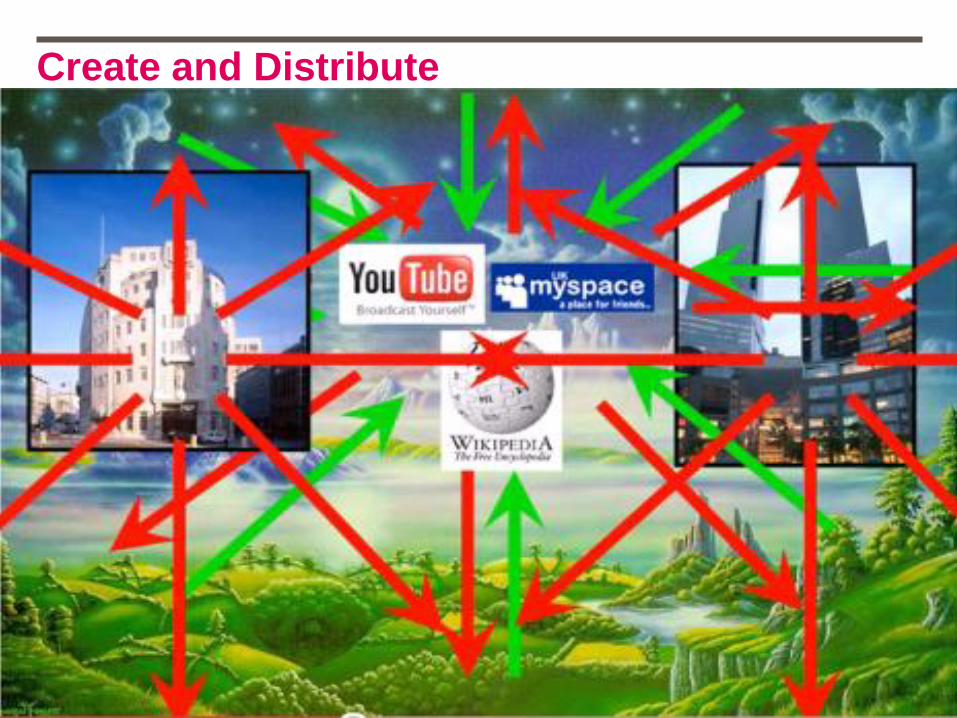

Create and Distribute

Media handed down from on high…

…. along with its general tone and attitude

Consumption

Media was only consumed at set schedule and place

The way we interact with companies

and brands were limited to analog only.

In person, phone and in-bank branch

were primary ways the customer touched the brand

or company‟s service

Consumer checks and references was among peer

group, relatives, sales representatives and catalogues

Marketing Touch Points- Finite

Digital

Marketing is going Digital

Transformative shifts in Marketing

Phase1 – Music goes digital from LP to CD.

World of music doesn‟t change much

same model of conceptualization, creation

and distribution

Phase2 – Challenge for marketer as distribution becomes free

Phase1 – Books goes digital from Britannica to CD. World of

Books doesn‟t change much

Phase2 – Content becomes decentralized that changes

centralized concept of Britannica

Phase1 – From centralized, outbound not differentiated

campaigns using traditional media to centralized, not highly

differentiated outbound campaign using e-mail and landing

pages

Phase2 – Currency of marketers ( Information) goes digital

and is freely available

What is really happening ?

Information becomes free

Prospects access information online

Sales is no longer information conduit

Sales is not able to read body languages

The challenge of reading and understanding digital body

language of buyer falls on marketing

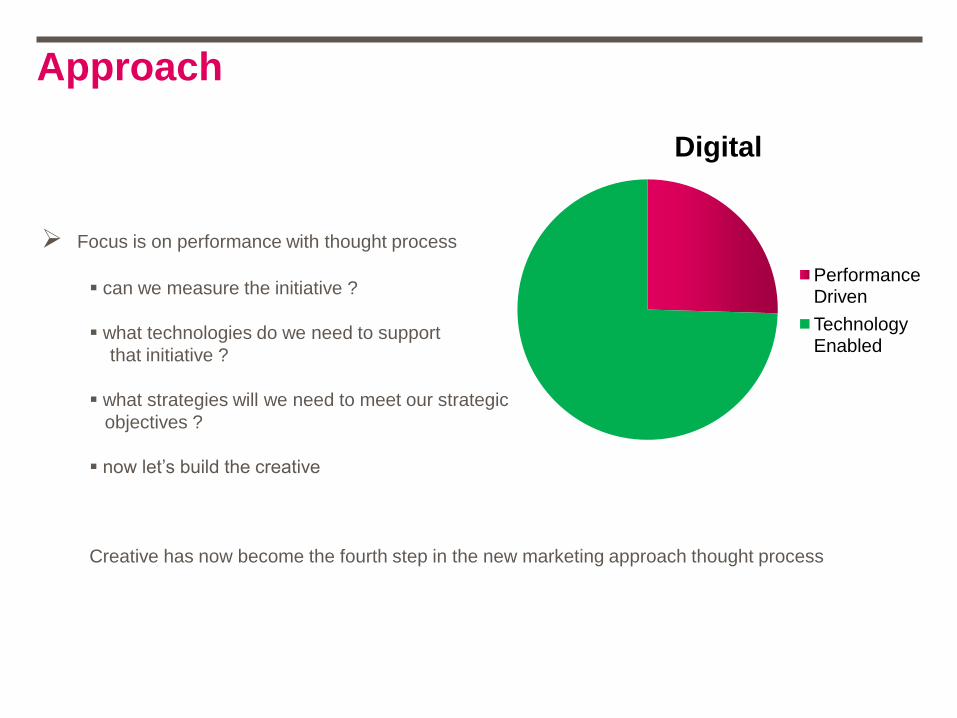

Approach

Digital

Performance Driven

Technology Enabled

Focus is on performance with thought process

can we measure the initiative ?

what technologies do we need to support

that initiative ?

what strategies will we need to meet our strategic

objectives ?

now let‟s build the creative

Creative has now become the fourth step in the new marketing approach thought process

Consumer

Create and Distribute

Single Source and complete consumer control

Blogging

“Since the first computer in 1965, what used to fit in a building now fits in your pocket, what fits in

your pocket now will fit inside a blood cell in 25 years”

Ray Kurzweil

The line between digital and analog encounters blur all

together

The volume of “social touch points” reaches critical

mass. “ been there, done that” experience sharing

common on CGM. Fragmentation becomes the norm

Marketing recognizes and differentiates between “ yet

another talk channel” versus the desire to “enable

social participation”

Blending interactive and social to produce digital

applications that connect people and get them talking

Consumption happens anytime, anywhere

It‟s easier than ever to reach a large audience, but

harder than ever to really connect with it

With infinite customer choice of media, marketers are

competing to make those connections.

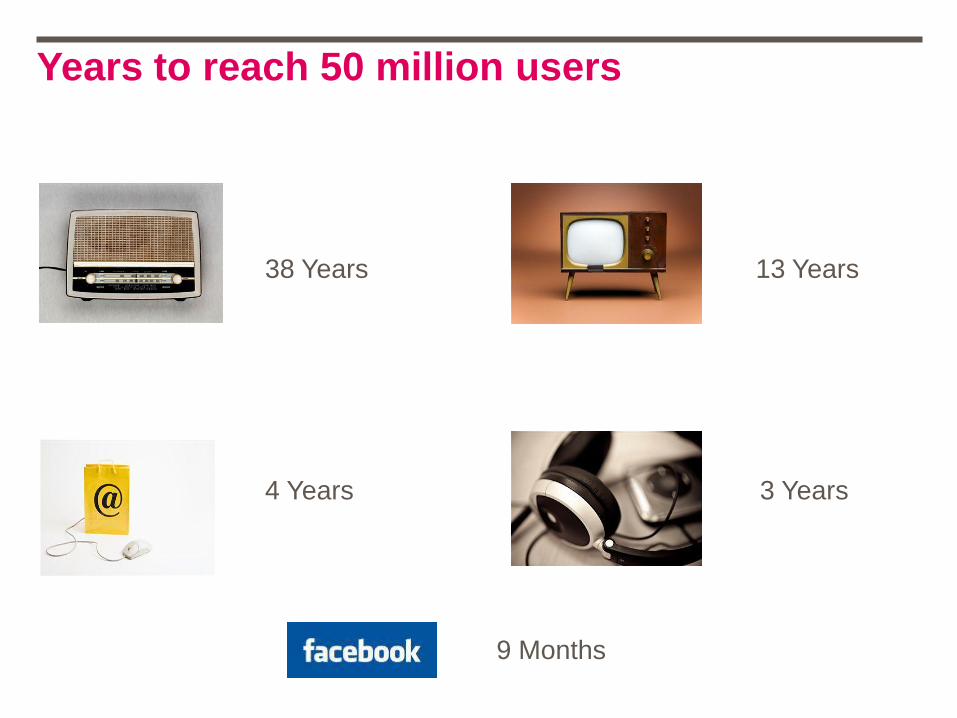

Years to reach 50 million users

38 Years 13 Years

4 Years 3 Years

9 Months

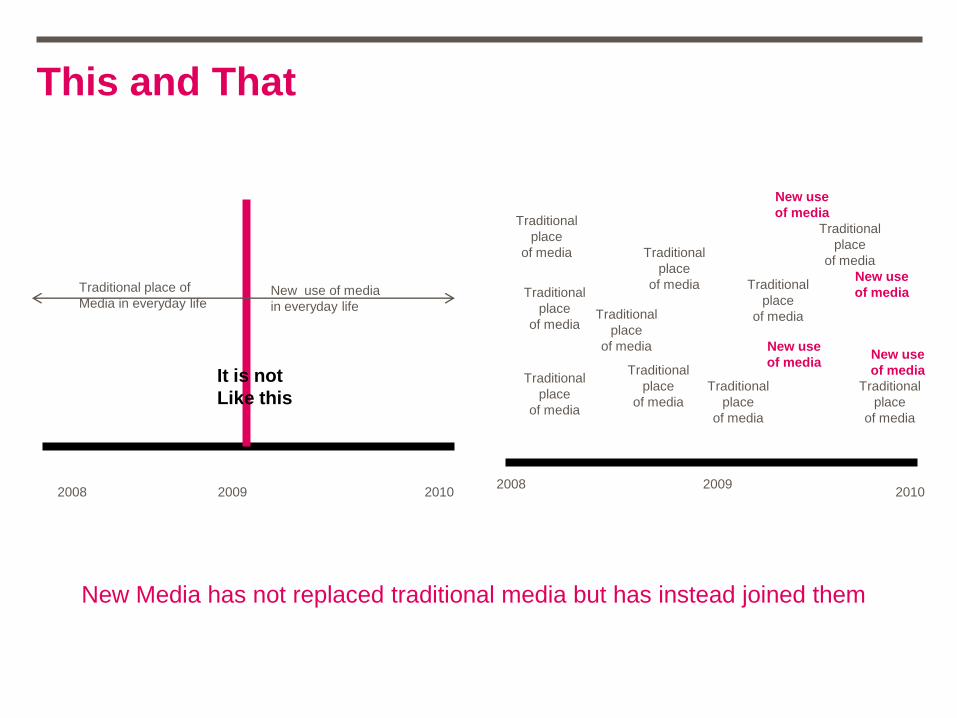

This and That

Traditional place of

Media in everyday lifeNew use of media

in everyday life

It is not

Like this

2008 2009 20102008 2009

2010

Traditional

place

of media

Traditional

place

of mediaTraditional

place

of media

Traditional

place

of media Traditional

place

of media

Traditional

place

of media

Traditional

place

of media

Traditional

place

of media

Traditional

place

of media

Traditional

place

of media

New use

of media

New use

of media

New use

of media

New use

of media

New Media has not replaced traditional media but has instead joined them

Turning the corners

Increased use of existing data and predictive models to make marketing decisions

Increasingly merging of offline and online marketing strategies

Interactive to social applications

Increased collaboration

Listen Participate Collaborate

Focus shifting to Insights :

Enable interested people to find your brand

Better understanding of consumer preferences

Increase consumer engagement

Become an Industry thought leader

The Buyer has changed; Marketers will too

Interactivity and control in hands of consumer

Volvo ran a homepage on Youtube that had a Twitter feed embedded in the ad. Unit

Networked and mobile consumer

Using technology to create, share and distribute information

Conscious consumer

Demands authenticity and transparency

BP oil spill

Ecopolitan houses/office and Green products ( car & appliances)

SBI Green Channel

1

The Buyer has changed; Marketers will too

“ Tell – and- sell marketing” (No linear process of one way communication with consumers)

to “Discuss with” ( Marketers and advertisers need to work with consumers)

Producing communication with a brand message to producing Consumer value

The Buyer has changed; Marketers will too

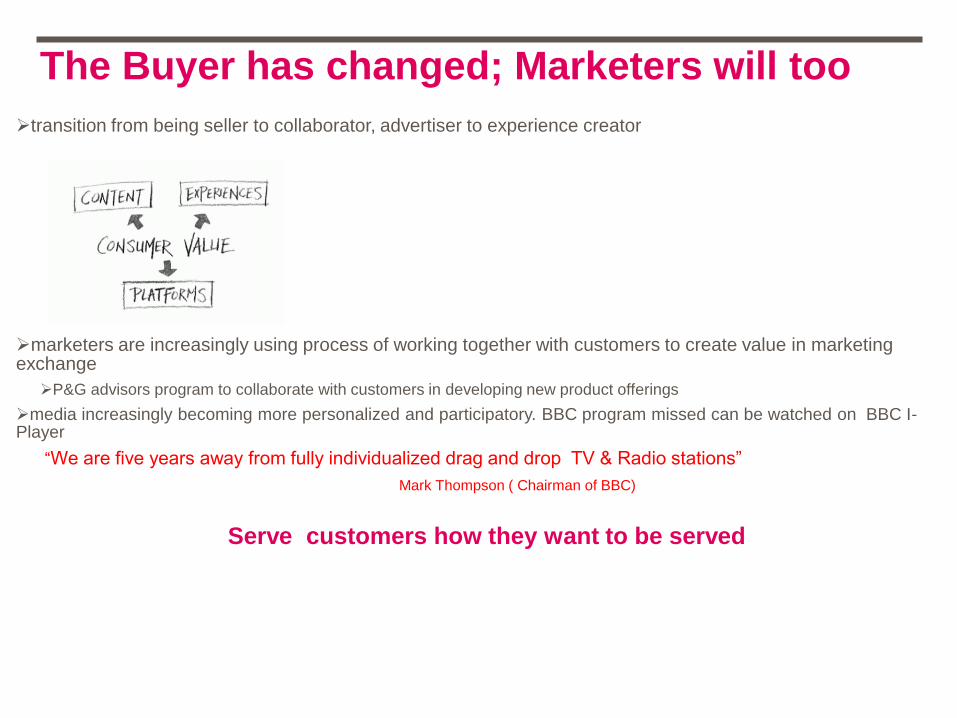

transition from being seller to collaborator, advertiser to experience creator

marketers are increasingly using process of working together with customers to create value in marketing exchange

P&G advisors program to collaborate with customers in developing new product offerings

media increasingly becoming more personalized and participatory. BBC program missed can be watched on BBC I-Player

“We are five years away from fully individualized drag and drop TV & Radio stations”

Mark Thompson ( Chairman of BBC)

Serve customers how they want to be served

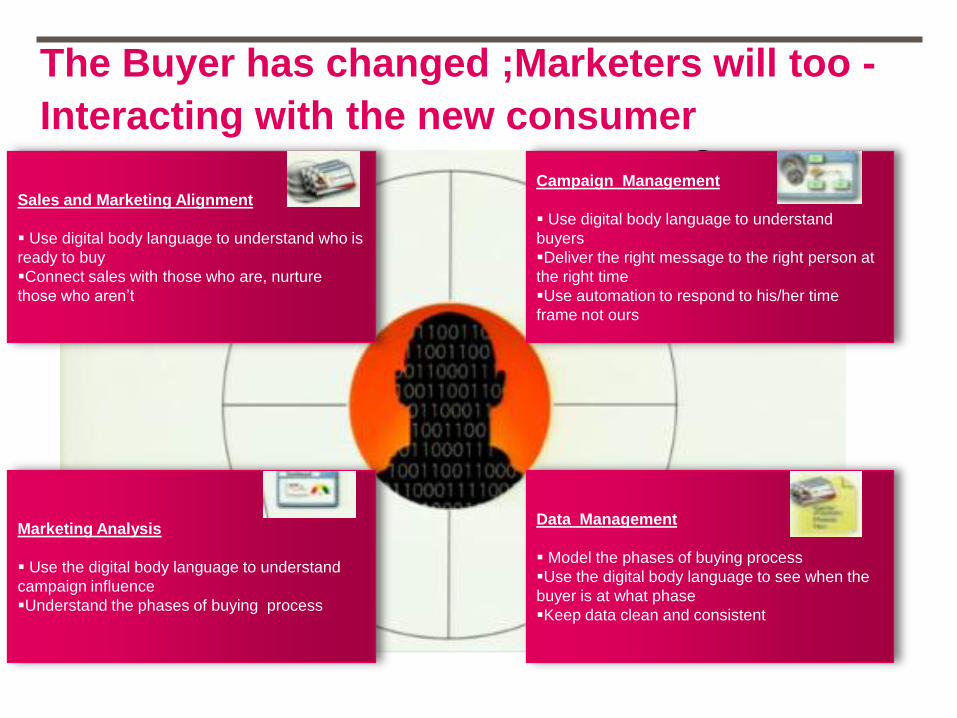

Campaign Management

Use digital body language to understand

buyers

Deliver the right message to the right person at

the right time

Use automation to respond to his/her time

frame not ours

Sales and Marketing Alignment

Use digital body language to understand who is

ready to buy

Connect sales with those who are, nurture

those who aren‟t

Data Management

Model the phases of buying process

Use the digital body language to see when the

buyer is at what phase

Keep data clean and consistent

Marketing Analysis

Use the digital body language to understand

campaign influence

Understand the phases of buying process

The Buyer has changed ;Marketers will too -

Interacting with the new consumer

The Importance of When

the popularity of Twitter has helped marketers to focus on one element of media - the importance of

WHEN

real time communication is beginning to happen on many more platforms than just Twitter through

tools like status updates on Facebook and LinkedIn and mobile messaging

auto companies like GM & Toyota are partnering with Edmunds.com ( online automobile information

provider) to create contextual messages that are triggered by customer activity and facilitate customer

decision making. Replacing „Just-in-case‟ with „Just-in-time‟ communication

reaching audiences anytime, anywhere ,on any device will drive engagement and conversion

many adverts already carry URLs, in the future we will see ads linking to desktop widgets etc.

2D bar codes ( QR codes) –

2

Communicating with multiple stakeholders

Who

Consumer

Reporters

Analysts

Competitors

Regulators

Activists

Why

To Inform, Purchase and spread Loyalty

Accelerate Research, Fact –finding

Offers scoop/Insight‟s

Intelligence gathering

Vocal consumers provide indicators into future

problems

Helps reinforce or solidify a key position

3 Changing notion of one stakeholder- Consumer. Other non-commercial stakeholders have become

important especially with the emergence of social media.

Who are these stakeholders and what are there motivations ?

Increasingly marketing strategies are designed taking cognizance of not just consumers but also these

external stakeholders eg Royal Caribbean Cruz … HaitiPassengers took to an Internet message board to protest the idea of vacationing where "tens of thousands of dead

people are being piled up on the streets

Communicating with multiple stakeholders

Scan current state:

Analyzing the top 10 sites/ forums that discuss brand/ competition

What information is sought

Do customers speak highly about the brand or not

Is sentiments positive or negative

Which discussion board or website are sought out for authority by analyst who cover category

What issues are most likely to prompt consumers to spread information to others

Decide

Which issues deserve the most attention from you

How can CGM be used to promote/ minimize negative message damage in social space

It‟s not the size of brand megaphone that matters any more; it‟s the size of consumer

megaphones that is becoming important

3

Interactive to Social They are talking to each other before they are taking to the brand

Social networking and exchange of information outside the brand space is increasing

More than 1.5 million pieces of content ( weblinks, news stories, blog post, photos etc) are shared on Facebook daily

Twitter averages 50 million tweets per day with 2-3 twitter accounts activated every second

Twitter is a vast –self answering community. Increasingly people go on twitter to ask questions and get

answers

marketers are “growing more ears”

Dell approach to Twitter:

“We don‟t have a choice on whether we do social media, the question is how well we do it”

Erik Qualman

4

RAM - connecting with consumers

Relevance

Automation

Media

5

RelevanceFundamentally altering consumer mindsets, rapidly shifting consumer preferences and transformed consumer

spending habits ,makes it inevitable for us to remain relevant

The right relevance( right message, at the right time to the right person) and the right response factor ( right segmentation,

demographics, psychographics, lifestyle) is gaining importance

3D consumer classification ( Attitude, experience and interest) replaces only demographic /psychographic classifications

Not just showing ads when a consumer is actively searching , but rather using what they are searching for to understand

what is relevant to them, advertising is getting closer to information

Consistent message no matter the medium, should be relevant and resonates with consumers

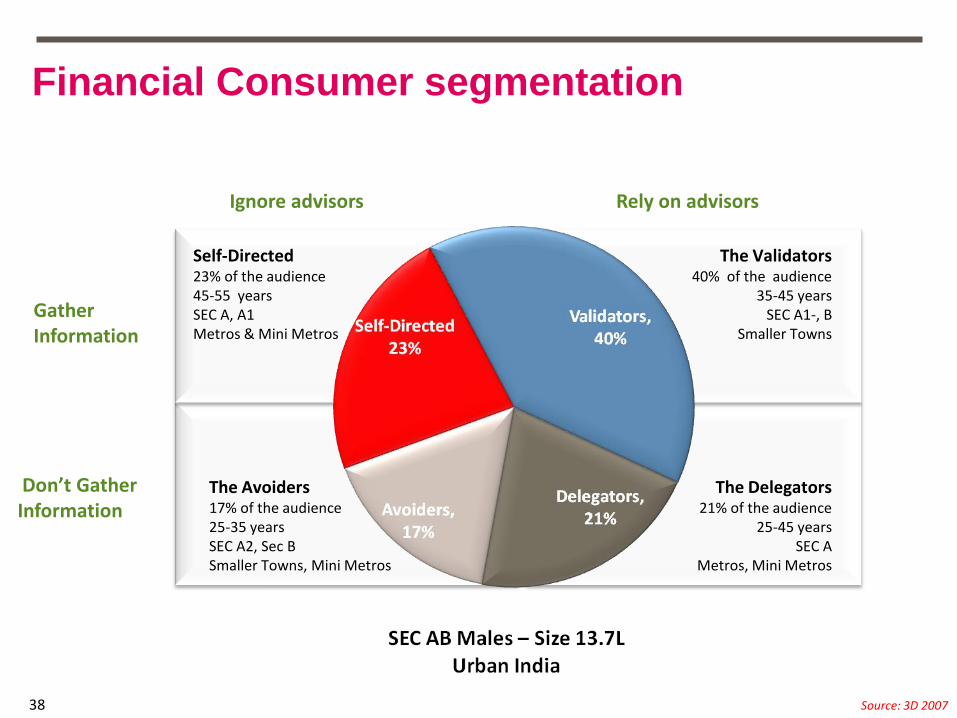

Segmenting financial consumer

The Delegators21% of the audience

25-45 yearsSEC A

Metros, Mini Metros

The Validators40% of the audience

35-45 yearsSEC A1-, B

Smaller Towns

Financial Consumer segmentation

Source: 3D 2007

GatherInformation

Don’t GatherInformation

Ignore advisors Rely on advisors

Self-Directed23% of the audience45-55 yearsSEC A, A1Metros & Mini Metros

The Avoiders17% of the audience25-35 yearsSEC A2, Sec BSmaller Towns, Mini Metros

38

Attitude ,Value and Needs

Source: 3D 2007

Self-Directed“I Have Confidence in Me”

Wants to take control ,

be it in terms of security and

finances.

Value: Information, speed and

control.

Needs : High need of

empowerment. Needs control

The Avoider“Trust no one”

Mistrusts advisors, does not want

in your face service

Value: Safe investments that are

simple and hassle free

Needs: Simplicity

The Validator“Money, money, money”

Wants to stretch the rupee to the

maximum

Value: Information, advice, trusted

relationship.Needs: High need of Information.

Will need personalized service

in all channels

The Delegator“Be there & take care of me”

Looks for someone who‟ll be

available at all times, offers great

service

Value: Advice, good service and a

trusted relationship

Needs :High need for relationship

Financial Behavior

Self-Directed• Takes financial decisions by

himself

Selects best products and price

Thinks he can outsmart the

market and make money when he

wants

Does his research before

investing, gathers information to

aid him

The AvoiderTends to spend money without

thinking

Is risk averse

Distrust financial advisors

Believes it is too early to start

planning for the future

Does not gather information

The ValidatorInterested in finances

Seeks advice on complex

decision

Believes he is good at managing

money

Is happy with his current

standard of living

Invests in stocks, shares and

mutual funds

The DelegatorTends to spend money but does

not like the idea of being in debt •

Prefers to have someone more

knowledgeable help with decision

• Wants to be a saver and a

planner • Does not actively gather

information

The DelegatorTends to spend money but does

not like the idea of being in debt

Prefers to have someone more

knowledgeable help with decision

Does not actively gather

information

Source: 3D 2007

Research Decisions

Self-Directed• Financial company website,

Online reviews, research, price /

product comparison on websites,

Newspapers & Magazines

The AvoiderAdvertising, Newspapers and

Magazines, Friends and family

The Validator•Agents, Sales representatives,

Broker/ financial advisor,

Advertising, Financial company

website, Online Reviews,

Research, Price /Product

comparison on websites,

Newspapers & Magazines

The DelegatorTends to spend money but does

not like the idea of being in debt •

Prefers to have someone more

knowledgeable help with decision

• Wants to be a saver and a

planner • Does not actively gather

information

The Delegator• Agents, Sales representatives,

Broker/ financial advisor,

WOM/Friends/Family, Advertising

Source: 3D 2007

NEED

VA

LIDA

TION

Financial Consumer segmentation

SELF

DIR

ECTE

D

DELEG

ATE FIN

AN

CIA

L P

LAN

NIN

G

GatherInformation

Don’t GatherInformation

Ignore advisors Rely on advisors

LOW

TR

UST

42

New Users ( How we get them to play)

What will make them try RBS?

How can we address this through marketing

New Users ( How we get them to play)

How can we build trust with them ?

How can we address this through marketing?

Brand Switchers

What will make them switch brand ?

How can we address this through

marketing?

Brand Switchers

What will make them switch brand ?

How can we address this through

marketing?

I Have Confidence in Me…

They want to take control of their own , be it in terms of security or finances.

Consumer satisfaction :

Product and operational focus

Marketing Opportunity:

Empower him to participate through feedback and dialogue in the process of product enhancement

and correction. Help them to be in control of their access to products and services

Media Implications

Provide him with information ( Newspapers & Online ) DM/ EDM, will look for online reviews, challenging

and engaging online/ on-air evolved financial games Provide him information /investment alerts on mobile/

mail, DM/EDM, editorial content ( reviews/ratings/analysis) will be critical

Applying Segmentation : Self –directed

consumers

Money, Money, Money…..

They continue to focus on pruning unnecessary expenses and shop with a list. They are spread across

income classes and try to stretch their rupee farther.

Consumer satisfaction

Human and product focus

Marketing Opportunity:

Up-front the value a brand offers to him. Help him feel smart about getting better bargains through

innovative schemes and promotions. Enhance the aspirational value of brands so he feels better about

investing with you

Media Implications

Will look for information – read more of newspapers ads, online, company reports , compare product

features. High standards and high expectations from Advisors. Will source information. Provide him with

account alerts , industry analysis etc

Applying Segmentation: Validator

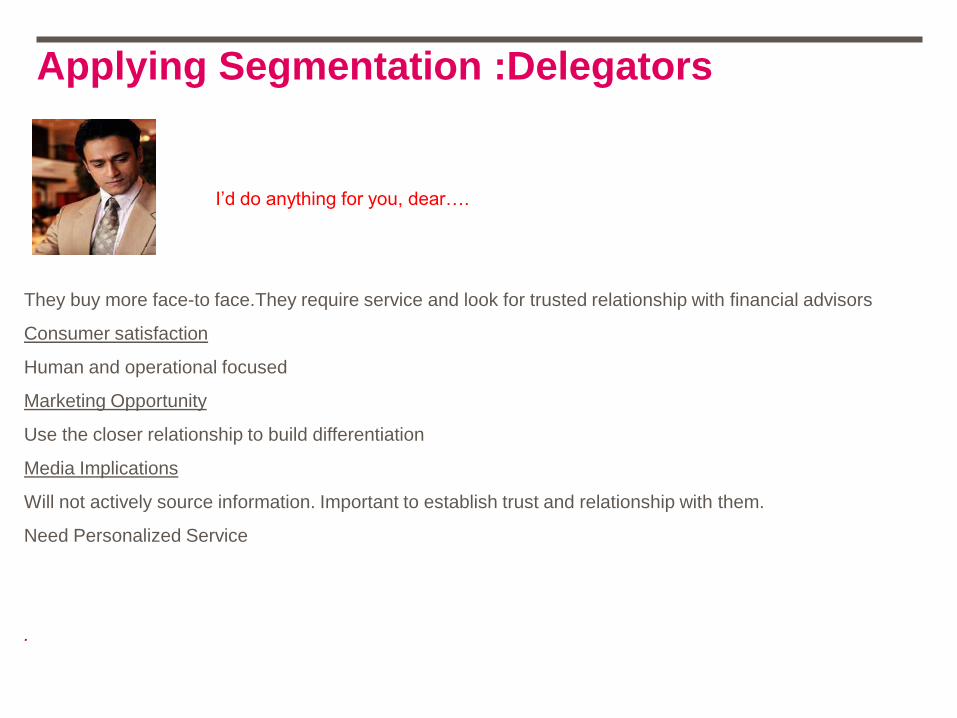

I‟d do anything for you, dear….

They buy more face-to face.They require service and look for trusted relationship with financial advisors

Consumer satisfaction

Human and operational focused

Marketing Opportunity

Use the closer relationship to build differentiation

Media Implications

Will not actively source information. Important to establish trust and relationship with them.

Need Personalized Service

.

Applying Segmentation :Delegators

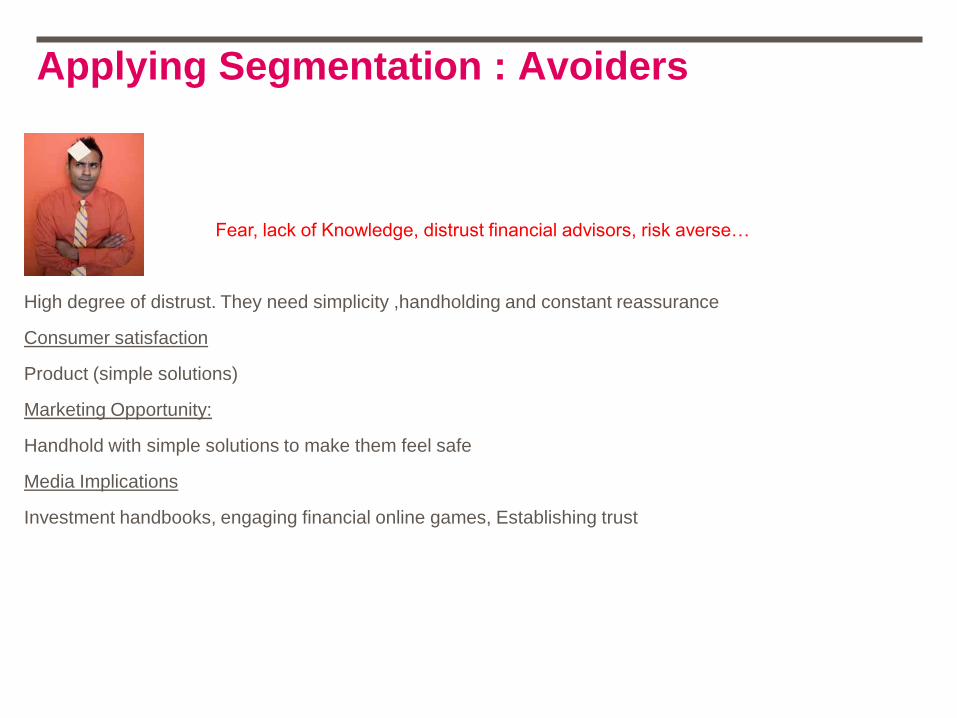

.

Fear, lack of Knowledge, distrust financial advisors, risk averse…

High degree of distrust. They need simplicity ,handholding and constant reassurance

Consumer satisfaction

Product (simple solutions)

Marketing Opportunity:

Handhold with simple solutions to make them feel safe

Media Implications

Investment handbooks, engaging financial online games, Establishing trust

Applying Segmentation : Avoiders

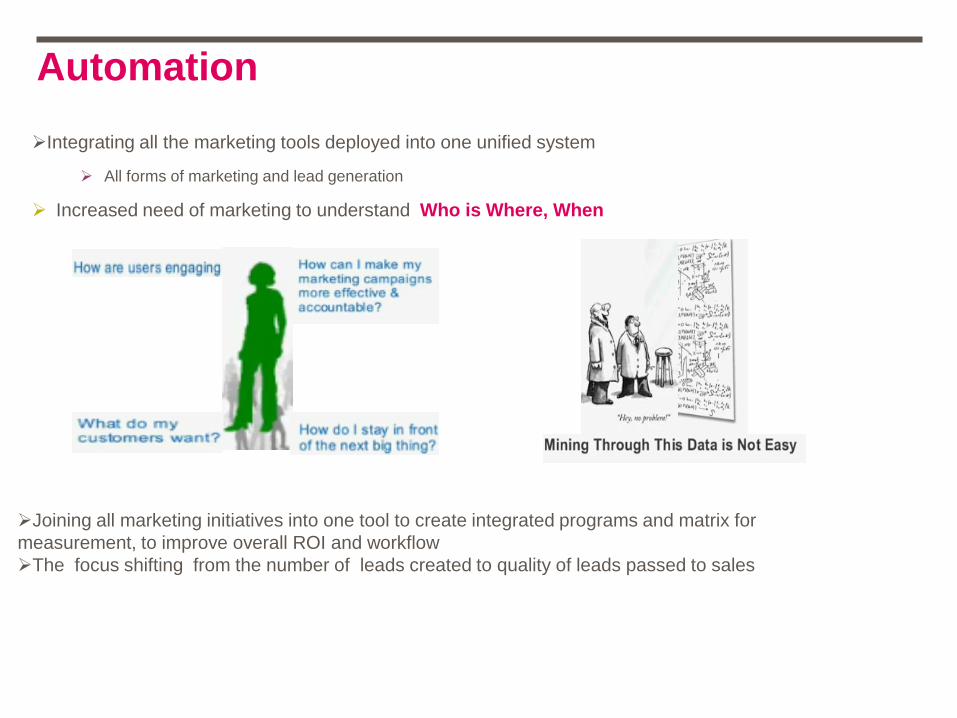

Automation

Integrating all the marketing tools deployed into one unified system

All forms of marketing and lead generation

Increased need of marketing to understand Who is Where, When

Joining all marketing initiatives into one tool to create integrated programs and matrix for

measurement, to improve overall ROI and workflow

The focus shifting from the number of leads created to quality of leads passed to sales

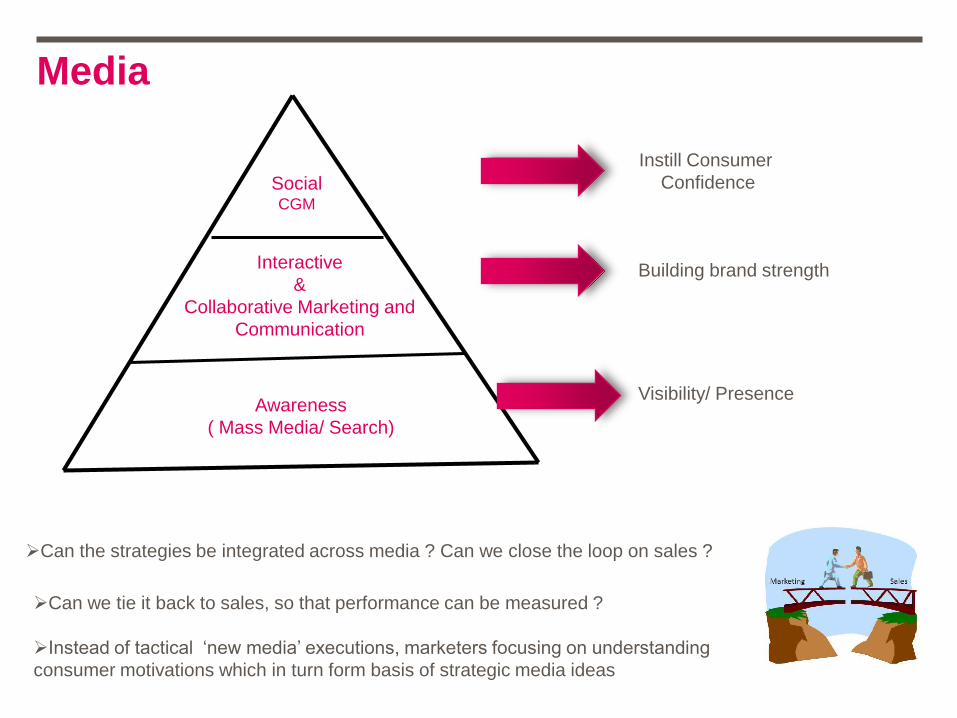

Media

SocialCGM

Interactive

&

Collaborative Marketing and

Communication

Awareness

( Mass Media/ Search)

Visibility/ Presence

Building brand strength

Instill Consumer

Confidence

Can the strategies be integrated across media ? Can we close the loop on sales ?

Can we tie it back to sales, so that performance can be measured ?

Instead of tactical „new media‟ executions, marketers focusing on understanding

consumer motivations which in turn form basis of strategic media ideas

Applying Framework

Entertain ConnectInform Assist Convert

Website/

One to one

Sales visits

Widgets, Call

center, Applications

Advertising, DM,

EDM,PR,

Organic and Paid

Search, Rating

sites, Forums

Interaction and

Engagement

activities, SN,

Blogs

Ads, Banners

Videos, Games

Viral

5

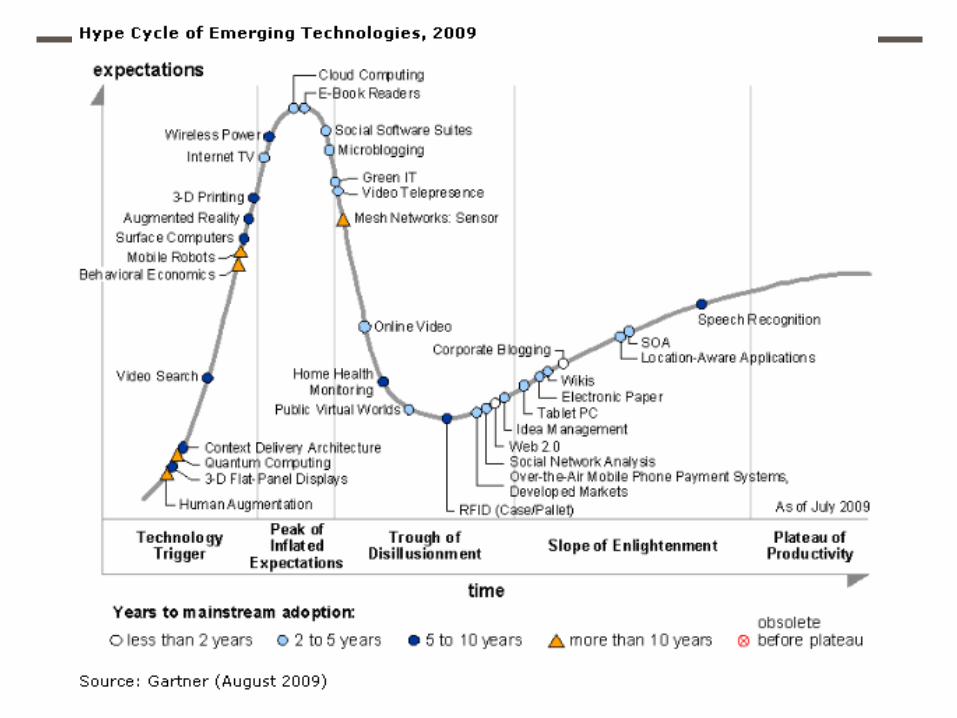

Five Emerging Technologies

Apple’s Tablet

Online TV

Cloud Computing

Augmented RealityMobile Transaction (Mobile Banking)

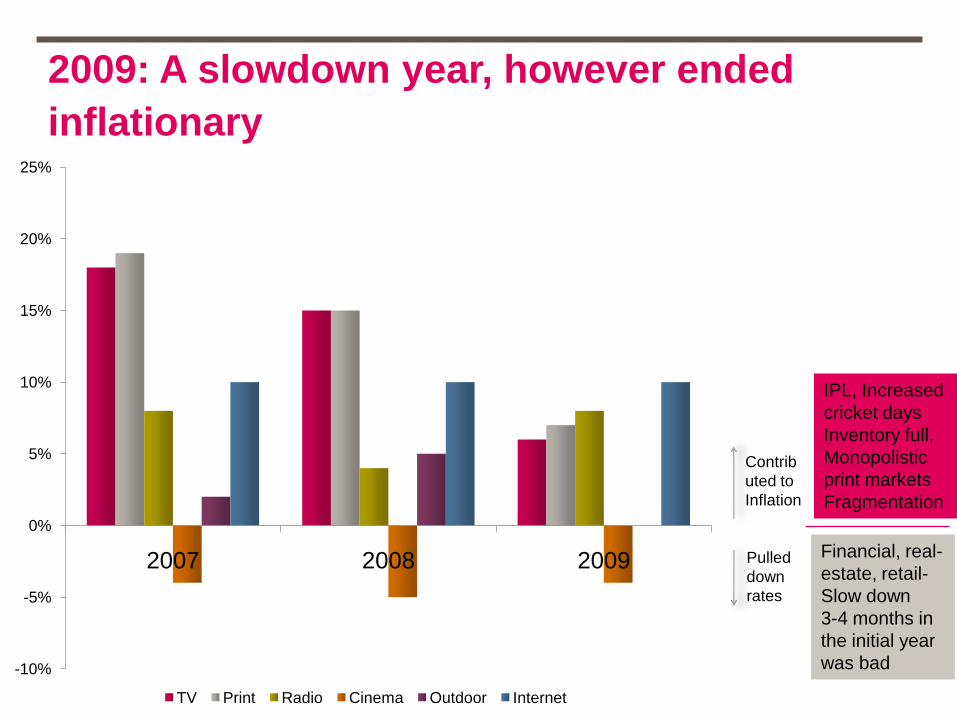

Media Inflation

2009: A slowdown year, however ended

inflationary

-10%

-5%

0%

5%

10%

15%

20%

25%

2007 2008 2009

TV Print Radio Cinema Outdoor Internet

Pulled

down

rates

Contrib

uted to

Inflation

IPL, Increased

cricket days

Inventory full,

Monopolistic

print markets

Fragmentation

Financial, real-

estate, retail-

Slow down

3-4 months in

the initial year

was bad

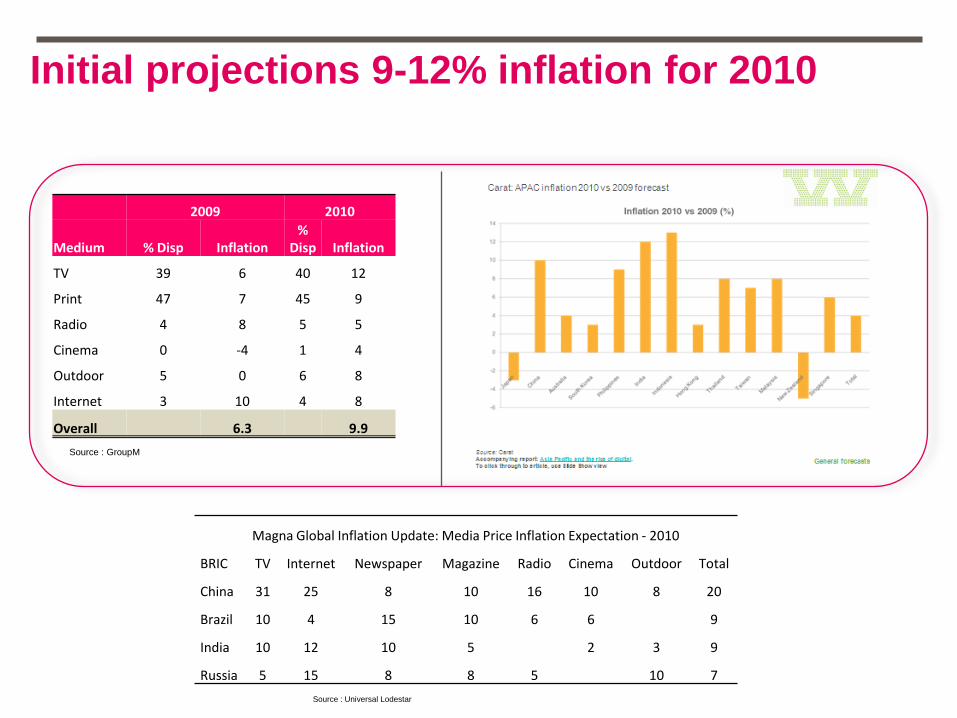

Initial projections 9-12% inflation for 2010

2009 2010

Medium % Disp Inflation%

Disp Inflation

TV 39 6 40 12

Print 47 7 45 9

Radio 4 8 5 5

Cinema 0 -4 1 4

Outdoor 5 0 6 8

Internet 3 10 4 8

Overall 6.3 9.9

Magna Global Inflation Update: Media Price Inflation Expectation - 2010

BRIC TV Internet Newspaper Magazine Radio Cinema Outdoor Total

China 31 25 8 10 16 10 8 20

Brazil 10 4 15 10 6 6 9

India 10 12 10 5 2 3 9

Russia 5 15 8 8 5 10 7

Source : Universal Lodestar

Source : GroupM

Media Trends in 2010

1 5 % g r o w t h

E v o l v i n g B u o y a n t T h r i v i n g

1

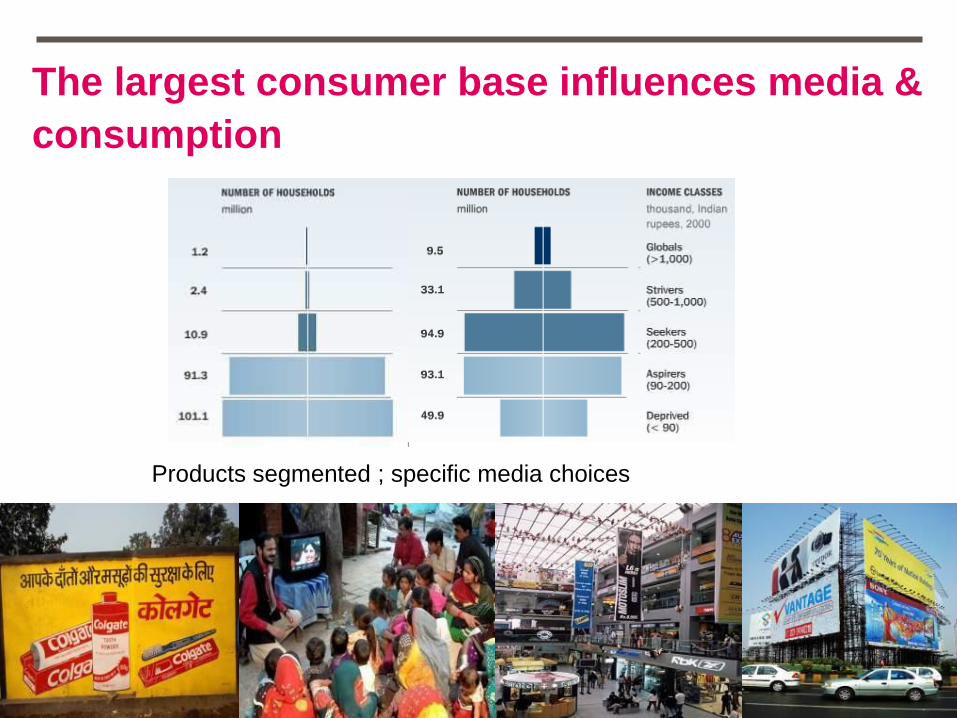

The largest consumer base influences media &

consumption

Products segmented ; specific media choices

D e m a n d > S u p p l y

N e w a d v e r t i s e r s r u l e m e d i a

2

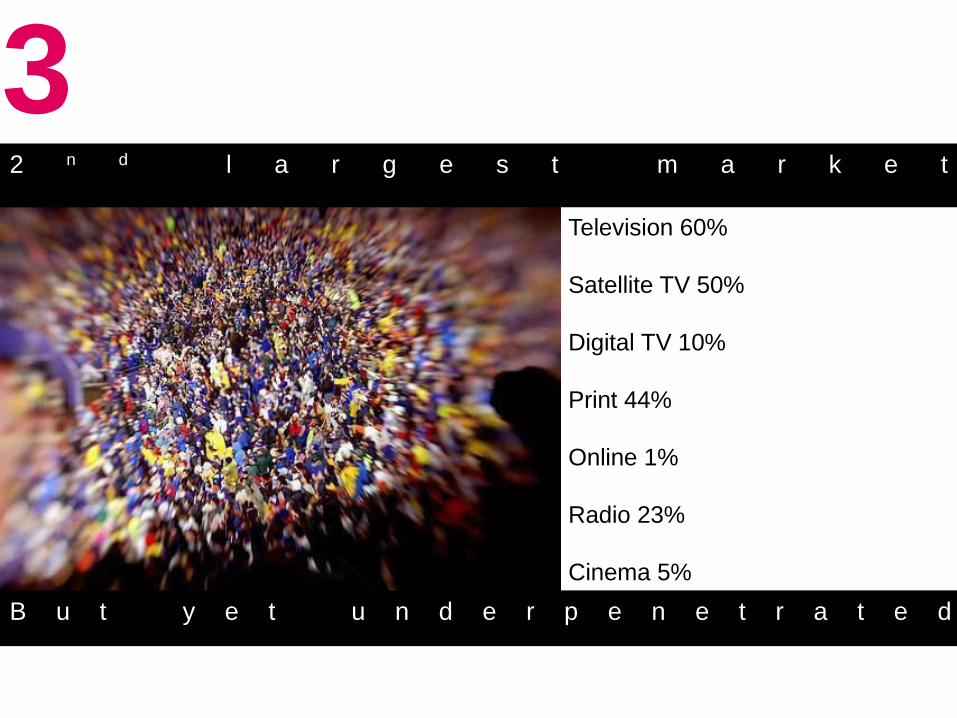

2 n d l a r g e s t m a r k e t

B u t y e t u n d e r p e n e t r a t e d

Television 60%

Satellite TV 50%

Digital TV 10%

Print 44%

Online 1%

Radio 23%

Cinema 5%

3

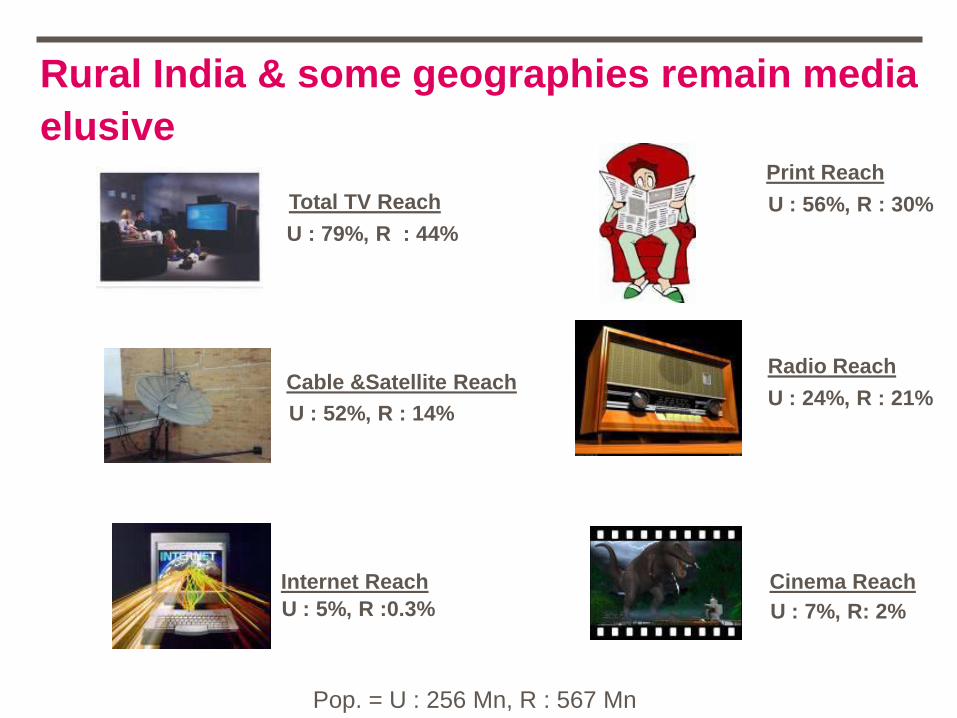

U : 79%, R : 44%

Total TV Reach

U : 52%, R : 14%

Cable &Satellite Reach

U : 56%, R : 30%

Print Reach

U : 24%, R : 21%

Radio Reach

U : 5%, R :0.3%

Internet Reach

U : 7%, R: 2%

Cinema Reach

Pop. = U : 256 Mn, R : 567 Mn

Rural India & some geographies remain media

elusive

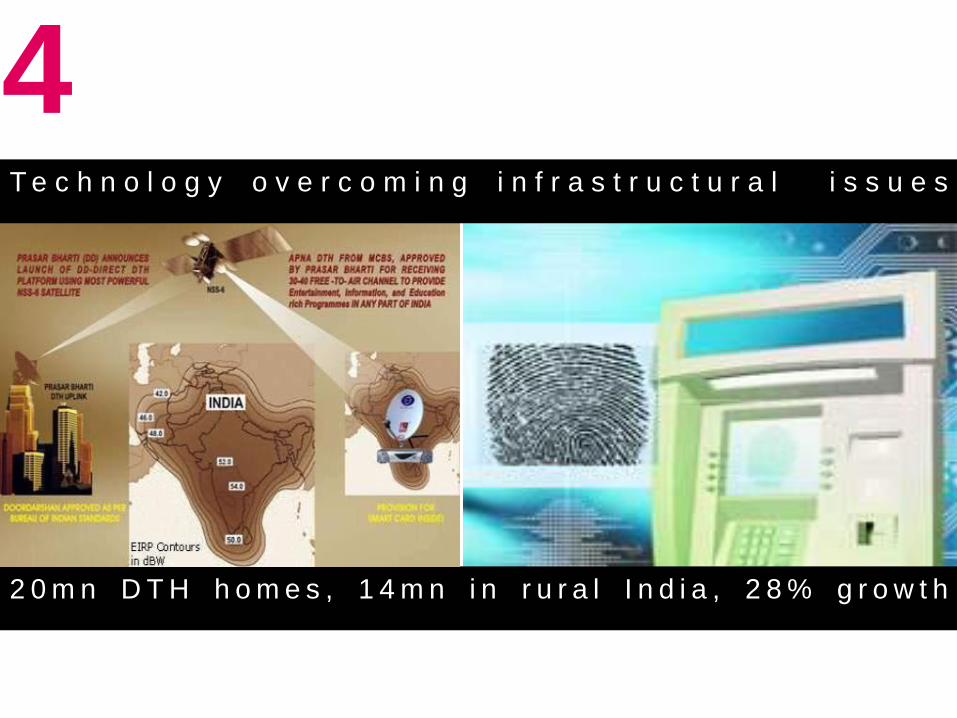

2 0 m n D T H h o m e s , 1 4 m n i n r u r a l I n d i a , 2 8 % g r o w t h

T e c h n o l o g y o v e r c o m i n g i n f r a s t r u c t u r a l i s s u e s

4

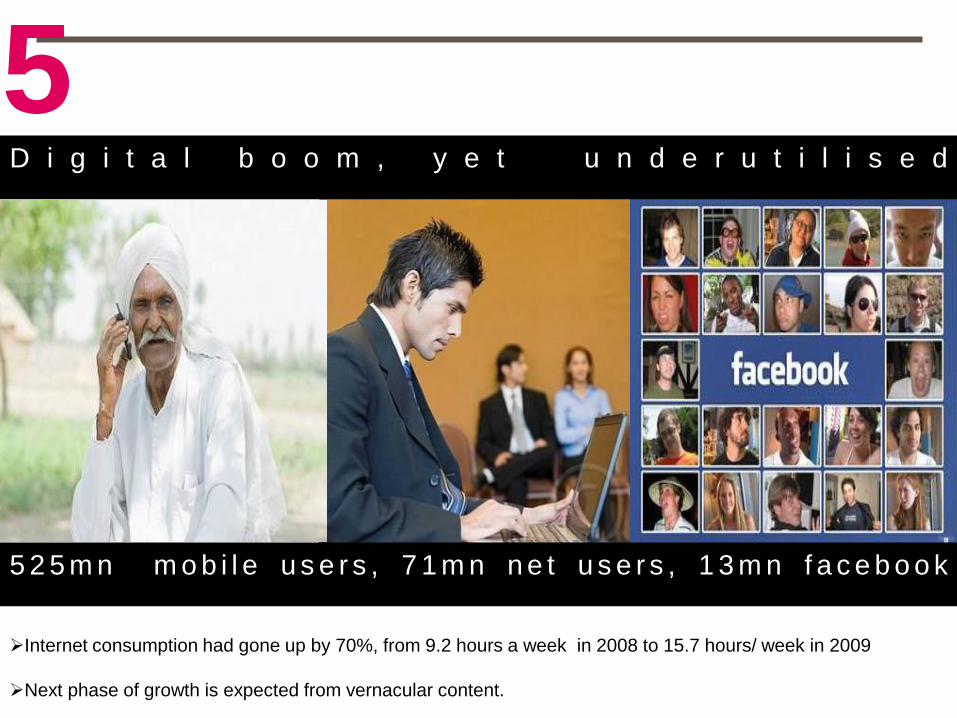

Internet consumption had gone up by 70%, from 9.2 hours a week in 2008 to 15.7 hours/ week in 2009

Next phase of growth is expected from vernacular content.

D i g i t a l b o o m , y e t u n d e r u t i l i s e d

5 2 5 m n m o b i l e u s e r s , 7 1 m n n e t u s e r s , 1 3 m n f a c e b o o k

5

5 4 % o f I n d i a i s u n d e r t h e a g e o f 2 5

N e w f o r m a t s N e w m e d i a M y m e d i a

6

The traditional media reach is stagnating

Youth consume( multi-media taskers), communicate( IM, SMS,Chat) and create media( Blog, Video & Photo

sharing) at the same time Cost of reaching & engaging with youth is higher than women/men by 150%

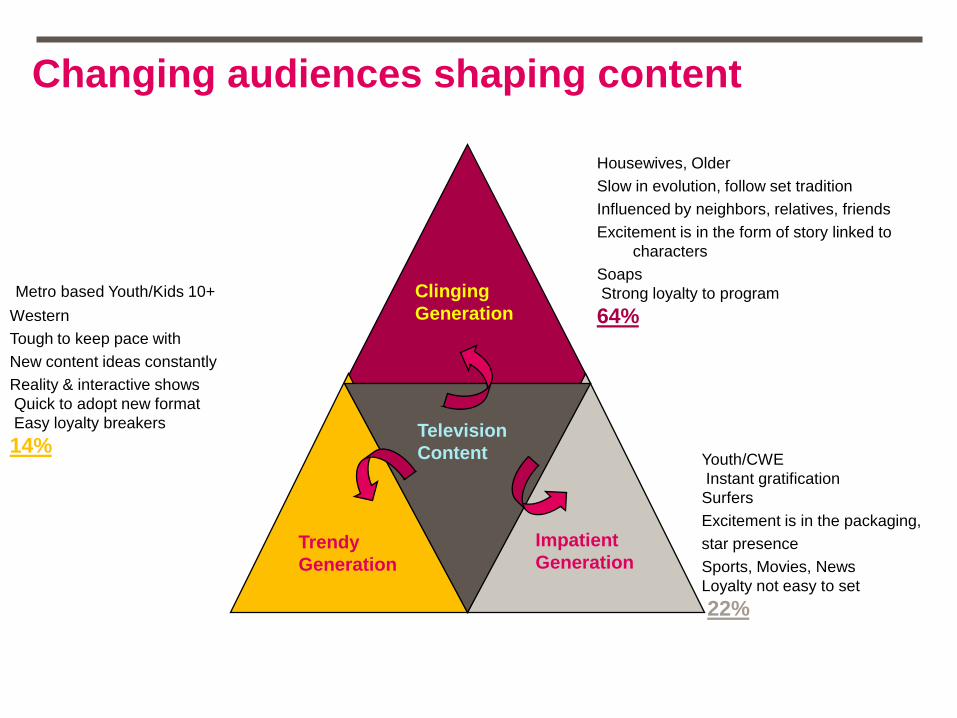

Changing audiences shaping content

Impatient

Generation

Clinging

Generation

Trendy

Generation

Television

Content

Housewives, Older

Slow in evolution, follow set tradition

Influenced by neighbors, relatives, friends

Excitement is in the form of story linked to

characters

Soaps

Strong loyalty to program

64%

Youth/CWE

Instant gratification

Surfers

Excitement is in the packaging,

star presence

Sports, Movies, News

Loyalty not easy to set

22%

Metro based Youth/Kids 10+

Western

Tough to keep pace with

New content ideas constantly

Reality & interactive shows

Quick to adopt new format

Easy loyalty breakers

14%

G r o w i n g h o m o g e n e i t y

G r o w i n g h e t e r o g e n e i t y

7

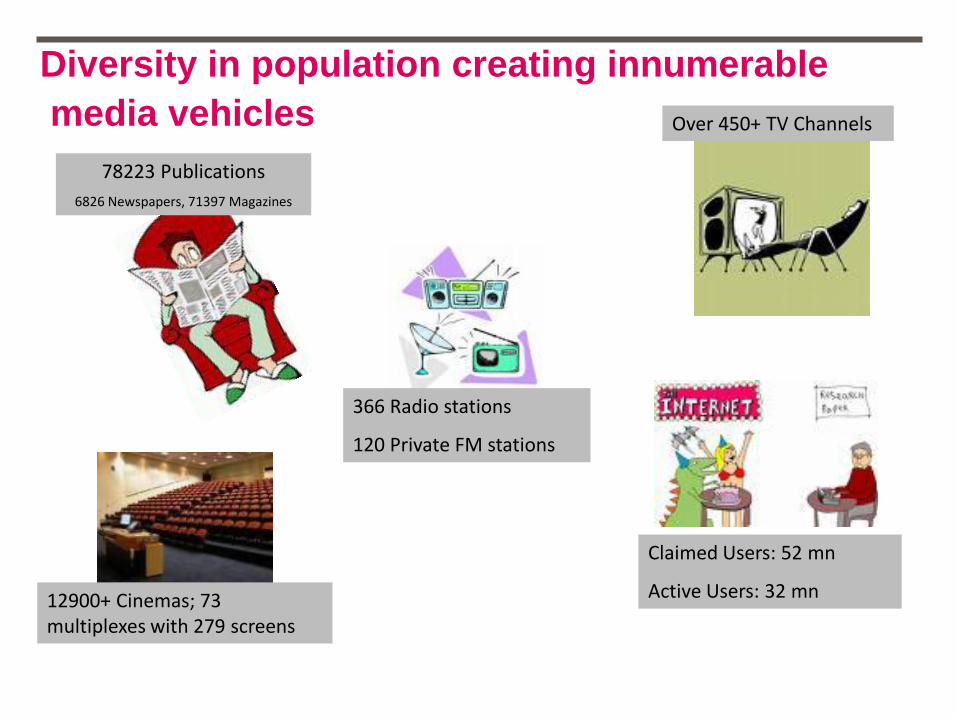

Diversity in population creating innumerable

media vehicles Over 450+ TV Channels

78223 Publications

6826 Newspapers, 71397 Magazines

366 Radio stations

120 Private FM stations

12900+ Cinemas; 73 multiplexes with 279 screens

Claimed Users: 52 mn

Active Users: 32 mn

L i t e r a c y s p u r s p r i n t b o o m

1 0 % g r o w t h , r e v e n u e s $ 2 b n , > 1 2 m a j o r l a u n c h e s p . a

8

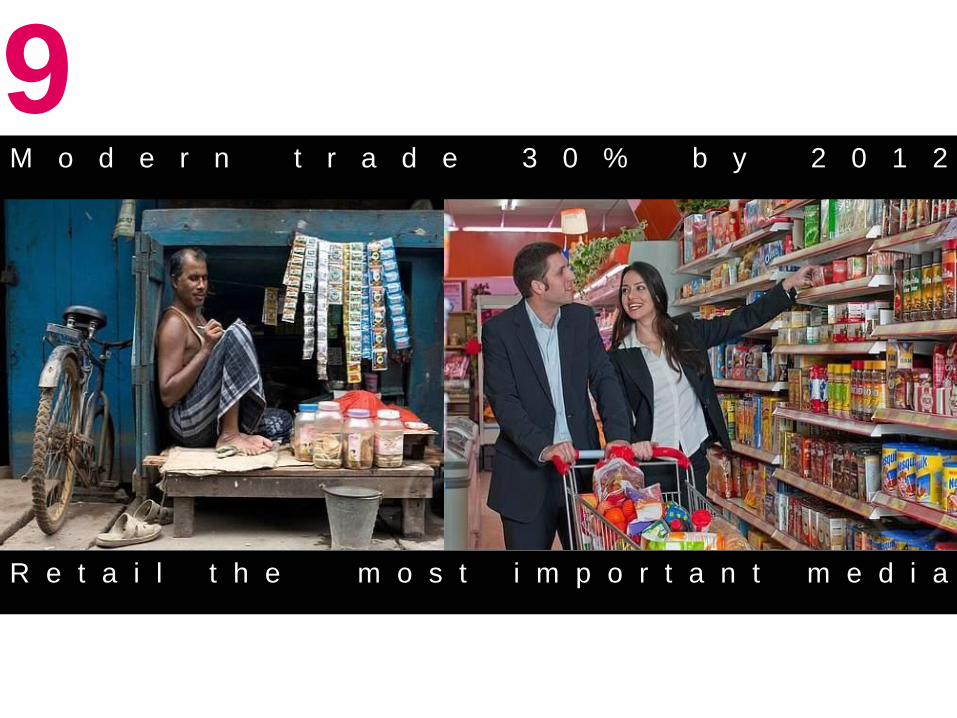

R e t a i l t h e m o s t i m p o r t a n t m e d i a

M o d e r n t r a d e 3 0 % b y 2 0 1 2

9

Exp lod ing TV, Rad io s ta t i ons , pub l i ca t i ons , webs i tes e tc .

F ragmen t ed a t t en t i on f o r a l r eady p r essu r i zed consum er s

10

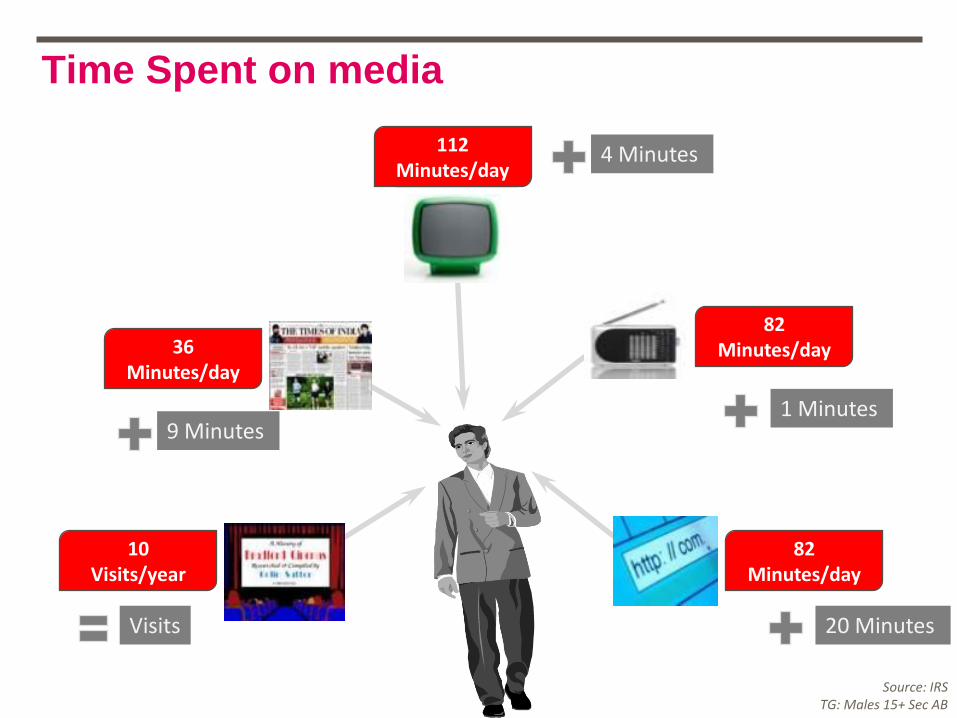

Source: IRS TG: Males 15+ Sec AB

108 Minutes/day

10 Visits/year

27 Minutes/day

81 Minutes/day

63 Minutes/day

112Minutes/day

36Minutes/day

10Visits/year

82Minutes/day

82Minutes/day

4 Minutes

9 Minutes1 Minutes

20 MinutesVisits

Time Spent on media

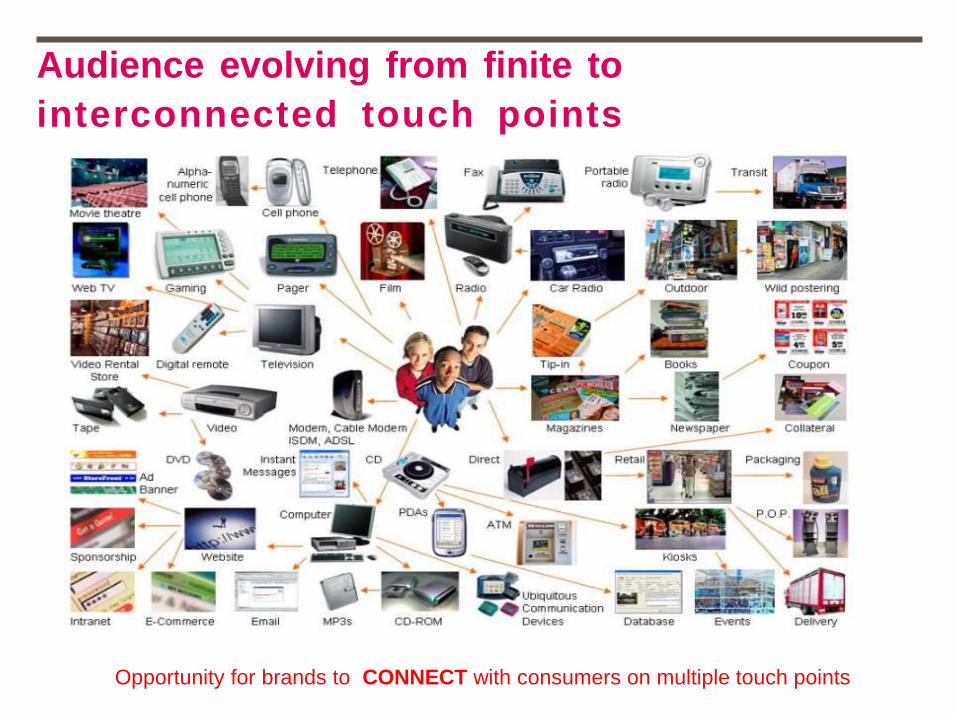

Audience evolving from finite to

interconnected touch points

Opportunity for brands to CONNECT with consumers on multiple touch points