Embed Size (px)

Citation preview

From (US) financial crisis to eurocrisis: Why are American houses connected to Europe's internal imbalances?

Herman Schwartz University of Virginia 27 September 2013

UNC Chapel Hill / TAM

Everything you need to know…

Euroland: an Op7mal Currency Area?

• Euro only works if Europe is an OCA • OCA needs: – Essen7ally open financial markets (Yes) – Essen7ally open goods markets (Mostly, but…) – High internal labor mobility (No) – High fiscal transfers (No) – And – same ideas about proper policy

• Result: regional instabili7es that are magnified by na7onal poli7cal structures

US Produc7vity growth vs wage growth % change 1948-‐2011

100

150

200

250

300

350

400

1948

1951

1954

1957

1960

1963

1966

1969

1972

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

2005

2008

2011

Wages* ProducWvity

Produc7vity vs average wage and average income of top 1%, in US, 1979+

Rising US household debt compared to incomes

1:1 ra7o

The 1991-‐2007 US growth cycle

Asia Recycles US Dollars as new Treasury / MBS Debt

Disinfla7on Housing Finance System

More Consump7on

US trade deficits à Global Growth

Faster US Economic Growth

↑ Tax revenue Fed ↓ interest rates

Low interest rates No welfare state

China’s growth cycle, 2000s

Central bank Sterilizes $$ Issuing RMB

State Banks & party elites

More investment for exports

Central Bank buys $$

Trade Surplus

↓ domes7c consump7on

The 1995-‐2000s German growth trap

Slower job crea7on

Wage restraint

Low Domes7c Demand

Less Domes7c Consump7on

Less domes7c investment

Slower rela7ve economic growth

↓ Tax revenue Tight money

policy

Net Exports Contribu7on to each countries’ GDP Growth 1995-‐2009

-‐10

-‐5

0

5

10

15

20

25

30

The 1995-‐2000s German growth trap

Slower job crea7on

Wage restraint

Low Domes7c Demand

Less Domes7c Consump7on

Less domes7c investment

Slower rela7ve economic growth

↓ Tax revenue

Tight money policy

Export surplus

German banks buy PIGS debt

German banks buy US

Mortgage bonds

Germany’s trade surpluses (€ bil)

0

20

40

60

80

100

120

140

Germany to EU27

Germanyto ROW

RelaWve Unit Labor Costs (wage in euros * produc7vity) 2000=100

80

90

100

110

120

130

140

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Germany

France

Italy

Spain

Netherlands

Germany produces but does not consume – final consump7on expenditure growth as

% of German growth (Germany = 100)

80%

100%

120%

140%

160%

180%

200%

220%

240%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Ireland Greece Spain Italy Portugal

Cumula7ve growth in GDP pc, PPP 1999-‐2009

EU member interest rates 1995 -‐ 2011

EURO introduced

Lehman crash

EU internal trade balances, € mils More imports = rising “foreign” debt

-‐200,000

-‐150,000

-‐100,000

-‐50,000

0

50,000

100,000

150,000

200,000

250,000

300,000

1999 2000 2001 2002 2003 2004 2005 2006 2007

Netherlands

Germany

France

Greece

United Kingdom Italy

Spain

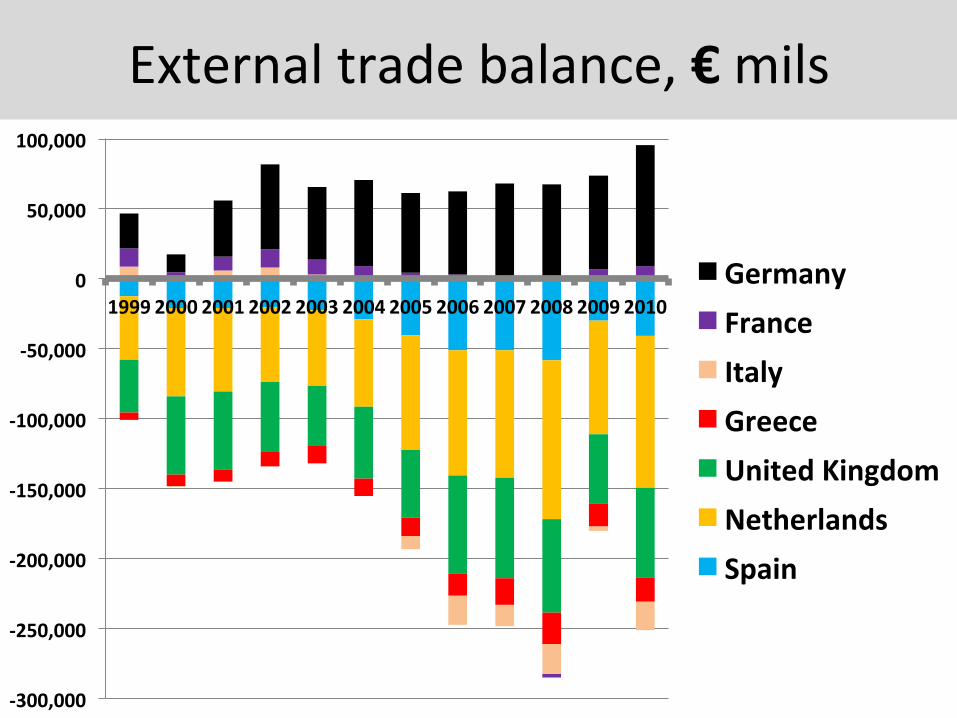

External trade balance, € mils

-‐300,000

-‐250,000

-‐200,000

-‐150,000

-‐100,000

-‐50,000

0

50,000

100,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 Germany France Italy Greece United Kingdom Netherlands Spain

US trade deficit (goods only, disaggregated, $bil.)

-‐700

-‐600

-‐500

-‐400

-‐300

-‐200

-‐100

0

100

200

EU x Germany

Lat. America

Canada

Rest of world

Germany

Japan

Middle East

China

EU member interest rates 1995 -‐ 2011

EURO introduced

Lehman crash

Fiscal (welfare state) excess? (budget balance as % of GDP)

-‐6.0

-‐4.0

-‐2.0

0.0

2.0

4.0

6.0 Denmark Germany Sweden

Fiscal (welfare state) excess? (budget balance % of GDP)

-‐30.0

-‐25.0

-‐20.0

-‐15.0

-‐10.0

-‐5.0

0.0

5.0

Germany Greece Ireland Italy Portugal Spain

It’s financial debt, not sovereign

Topics: US equity markets holding in despite poor economic data; which fiscal cliff is worse; European Credit Divorce; will China respond to economic CPR; After 50

3

July 17, 2012

Sometimes a Great Notion (1971): how did the US dig itself out of wartime debt levels after WWII? I find that there is a lot of misreporting about how US debt levels were halved during the 1950’s. As shown in the table below, government spending was not cut sharply; there was no radical increase in tax collections, either from businesses or from households; and the Fed did not engineer negative long-term real interest rates to jumpstart growth. In addition to the competitive advantage the US had over recovering Axis Powers, the US of the 1950’s benefited from pro-business policies that resulted in over 4% annualized GDP growth throughout the decade. This approach is not in play now, raising questions about how the US will deal with 80% net debt to GDP for only the second time in its 200+ year history.

A brief detour: The 1971 film chosen above is about rugged individualism, the power of small business and the lack of reliance on government or organized labor to solve problems. It’s actually hard to find a pro-business or pro-capitalist film. According to Larry Ribstein at the University of Illinois College of Law (see page 6 for details), US filmmakers have a long history of disliking profit-maximization, and have generated a huge volume of work depicting evil, soulless corporations and heartless capitalists. He quotes Joseph Schumpeter and theorizes that filmmakers are an intelligentsia over-produced by the bounties of capitalism which directs its resentment at a society that refuses to value what they do. Ouch! Scenes from a Marriage (1973): the European Credit Divorce keeps getting more worse A decade of European monetary integration continues to unravel. As shown below, Eurozone banks are cutting their cross-border credit exposure as fast as they can. Unsurprisingly, the rest of the world is not any more anxious to lend to the European Periphery, and is cutting its exposures as well. The ECB is providing the stop-gap to finance all of this capital flight, which helps prevent an outright Depression. But to be more optimistic on Europe, we need to see some improved economic conditions in the Periphery, and evidence that structural reforms are paying off. As things stand now, there are still serious questions about how the ECB and the EU will come up with the money to finance all the maturing Peripheral sovereign and bank debt that investors no longer want to hold. Total Periphery sovereign and bank debt: almost 7 trillion Euros.

Net debt (% of GDP)

Net debt (bn)

Nominal GDP (bn)

Real GDP (bn 1950 USD)

Outlays (% of GDP)

Receipts (% of GDP)

Average real 10-year rate

1950 80% $219 $273 $273 16% 14% 1.3%1951 67% $214 $320 $302 14% 16% -5.3%1952 62% $215 $349 $322 19% 19% 0.5%1953 59% $218 $373 $341 21% 19% 2.0%1954 60% $224 $377 $343 19% 19% 2.1%1955 57% $227 $396 $354 17% 17% 3.1%1956 52% $222 $427 $368 17% 18% 1.7%1957 49% $219 $451 $377 17% 18% 0.3%1958 49% $226 $460 $377 18% 17% 0.6%1959 48% $235 $490 $398 19% 16% 3.3%1960 46% $237 $519 $415 18% 18% 2.7%

Comp. ann'l gr: 0.8% 6.6% 4.3%Source: OMB, BEA, Robert Shiller data set, Bureau of Labor Statistics.

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

2004 2005 2006 2007 2008 2009 2010 20112.5

3

3.5

4

4.5

5

5.5

6

6.5

7

Source: BIS. Data as of Q4 2011.

Flight of the BumblebeeTrillions, USD

Cross-borderlending within the Euro zone

Non-Euro zone lending to the Periphery

0

1

2

3

4

5

6

7

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011Source: J.P. Morgan Securities LLC.

Peripheral sovereign and financial debtTrillions, Euros

Sovereign

Financial

1950’s time capsule: taxes were regarded as a greater cause for small business failures than tight money. Eisenhower championed legislation which eased tax burdens on small business and which culminated in a bill eliminating double-taxation (Subchapter S); he also eliminated wage and price controls. In the 1950’s, the private sector accounted for a post-war peak of 86% of all employment, a level not seen since.

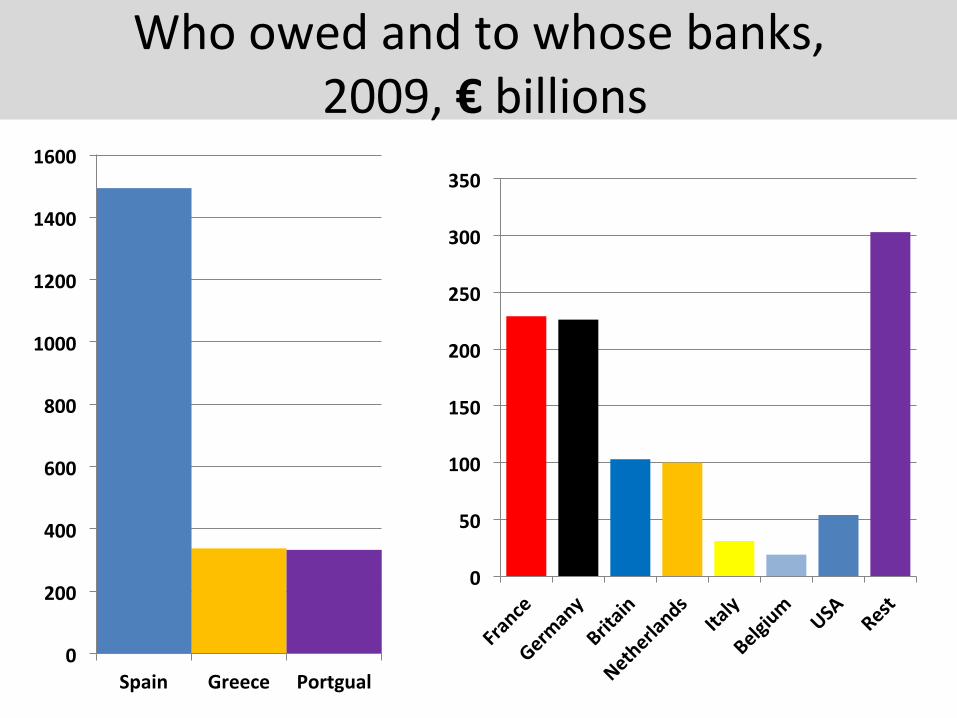

What if Greece (Spain, Italy) defaulted?

Who owed and to whose banks, 2009, € billions

0

200

400

600

800

1000

1200

1400

1600

Spain Greece Portgual

0

50

100

150

200

250

300

350

Private capital ounlows, public inflows…

as % of GDP of Spain, Greece, Italy, Portugal, Ireland

The ECB reacts

C H A P T E R 1 G LO B A L F I N A N C I A L S TA B I L I T Y A S S E S S M E N T

International Monetary Fund | October 2012 5

–12–10

–8–6–4–2

02468

Jan-10 Apr-10 Jul-10 Oct-10 Jan-11 Apr-11 Jul-11 Oct-11 Jan-12

CorePeriphery

Sources: Haver Analytics; and IMF staff estimates.Note: To estimate the autonomous, private-sector-driven component of total flows,

flows are calculated as the sum of net portfolio and other investment flows, excluding changes in TARGET2 balances at the central bank. Core = Belgium, France, Germany, and the Netherlands; periphery = Greece, Ireland, Italy, Portugal, and Spain.

Figure 1.5. Portfolio and Other Investment Capital Flows in the Euro Area, Excluding Central Banks(Cumulative from December 2009, in percent of GDP in preceding year)

Capital "ight from the periphery to the core…

3

4

5

6

7

Spain (foreign share)Italy (foreign share)

Spain yield (right scale)Italy yield (right scale)

0

10

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Jan-

10Ap

r-10

Jul-1

0Oc

t-10

Jan-

11Ap

r-11

Jul-1

1Oc

t-11

Jan-

12Ap

r-12

Jul-1

2

20

30

40

50

60

Introductionof euro

Source: Bloomberg L.P.Note: Share of nonresident investors in total debt stock, and generic yield of 10‐year

government bond. Yields are 3-month moving averages.

Figure 1.6. Spain and Italy: Changes in Foreign Investor Shares and Yields(In percent)

…is widening sovereign spreads as foreign holdings of periphery debt fall…

Bankingsector

Publicsector

0

500

1,000

1,500

2,000

2,500

ECB borrowing

Borrowing from

private banks

EFSF/EFSMSMP

ECB borrowing

Borrowing from

private banks

Sources: Bank for International Settlements (BIS); Bloomberg L.P.; European Financial Stability Fund; Haver Analytics; national central banks; and IMF staff estimates.

Note: Current exposures of the rest of the euro area to the periphery (Greece, Ireland, Italy, Portugal, and Spain) amount to €2.2 trillion; including cross‐border lending by euro area banks reporting to the BIS on an ultimate risk basis (end‐March 2012); periphery banks' borrowing from the Eurosystem, excluding emergency liquidity assistance; ECB purchases of periphery government bonds through its SMP; and EFSF and EFSM contributions to programs with Greece, Ireland, Portugal, and Spain. ECB = European Central Bank; EFSF = European Financial Stability Facility; EFSM = European Financial Stabilisation Mechanism; SMP = Securities Market Programme.

Figure 1.7. Euro Area Exposures to Greece, Ireland, Italy, Portugal, and Spain(In billions of euros)

Dec-09 Current

…and private borrowing is being replaced by public sector "ows…

0

100

200

300

400

500

Jan-11 Apr-11 Jul-11 Oct-11 Jan-12 Apr-12 Jul-12

SovereignsBanksNon!nancial !rms

Growing divergencebetween periphery

and core

Sources: Bloomberg L.P.; Thomson Reuters Datastream; and IMF staff estimates.Note: Data for sovereigns are weighted by GDP; for banks, by assets; and for

nonfinancial firms, by outstanding bonds. Corporate spreads are calculated via option-adjusted bond spreads. Core = Austria, Belgium, Finland, Germany, and the Netherlands; periphery = Greece, Ireland, Italy, Portugal, and Spain.

Figure 1.8. Periphery Minus Core Credit Default Swap Spreads(In basis points)

…resulting in a growing divergence in periphery-core funding costs and spreads…

Wolfgang Schauble (FRG Fin Minister) “Nobody in Europe sees this contradic7on between fiscal policy consolida7on and growth. We have a growth-‐friendly process of consolida7on, and we have sustainable growth, however you want to word it.”

Washington Post 10 April 2013

Eurozone 2012 GDP growth: -‐ 0.6% 2013: -‐ 0.4% Eurozone Q2 unemployment rate: 12.1% Eurozone total employment = level of Q2 2005

The eurozone is a straw house

QUESTIONS?