Embed Size (px)

Citation preview

Session ID: ECT-100

Structuring Indirect Rates

Insight 2011

Presented byPhilip Steigner

04/18/20232 ©2011 Deltek, Inc. All Rights Reserved

Project Manufacturing

Human Resources

Project Management

Financial Management

Enabling Success

Winning More Business

Reducing the Cost of Compliance

Increasing Project Visibility

Improving Cash Flow

CRM and Capture Management

Teaming Solutions

Market Intelligence

Business Performance Management

Know More

Win More

Do More

04/18/20233 ©2011 Deltek, Inc. All Rights Reserved

Project Manufacturing

Human Resources

Financial Management

Project Management

Do More

CRM and Capture Management

Teaming Solutions

Market IntelligenceWin More

Do More

Project Execution & Management

Reporting, GRC & Compliance

Project & Corp Accounting

Time, Expense, Labor, Payroll

Business Performance Management

Know More

04/18/20234 ©2011 Deltek, Inc. All Rights Reserved

Agenda Definitions

Composition of indirect pools and bases

Workshop

Strategic plan and design of indirect rates

Common errors

Q & A

04/18/20235 ©2011 Deltek, Inc. All Rights Reserved

Key Takeaways To provide direction to enable you to strategically design an indirect

rate structure that has the following attributes:

Complies with Federal Regulations

Maximizes cost recovery

Aligns with the vision of your organization

Incorporates best practices and industry standards

04/18/20236 ©2011 Deltek, Inc. All Rights Reserved

Definitions

04/18/20237 ©2011 Deltek, Inc. All Rights Reserved

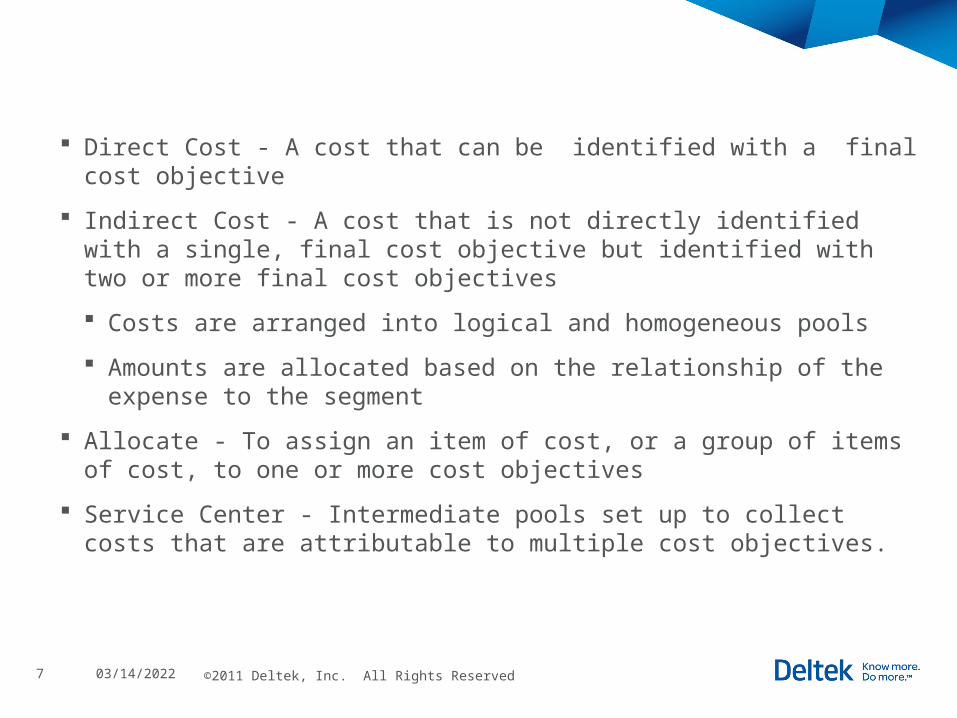

Direct Cost - A cost that can be identified with a final cost objective

Indirect Cost - A cost that is not directly identified with a single, final cost objective but identified with two or more final cost objectives

Costs are arranged into logical and homogeneous pools

Amounts are allocated based on the relationship of the expense to the segment

Allocate - To assign an item of cost, or a group of items of cost, to one or more cost objectives

Service Center - Intermediate pools set up to collect costs that are attributable to multiple cost objectives.

04/18/20238 ©2011 Deltek, Inc. All Rights Reserved

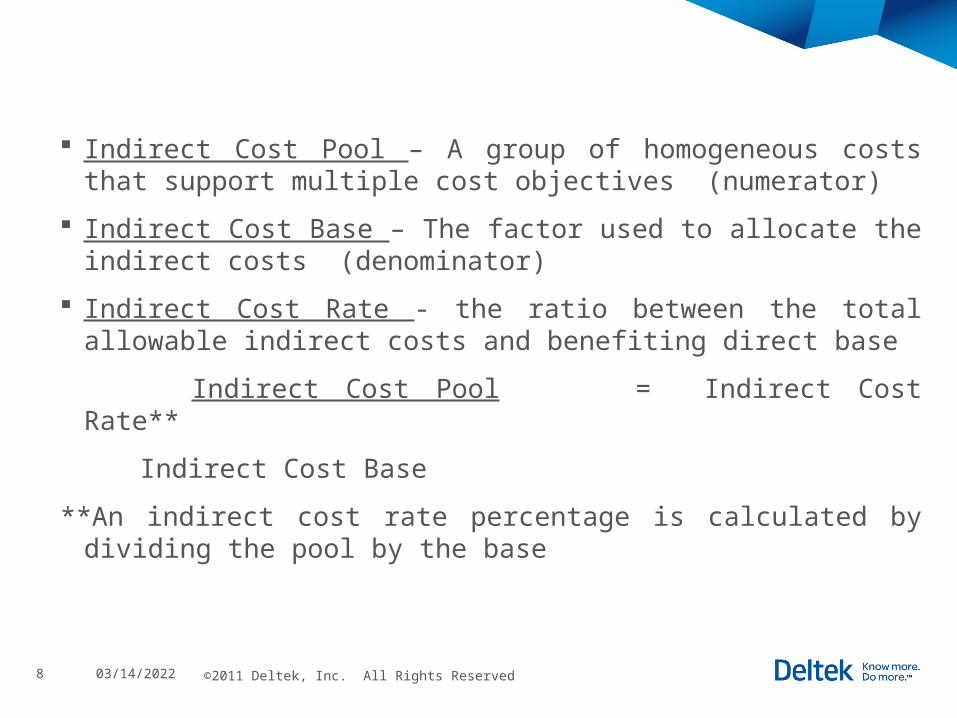

Indirect Cost Pool – A group of homogeneous costs that support multiple cost objectives (numerator)

Indirect Cost Base – The factor used to allocate the indirect costs (denominator)

Indirect Cost Rate - the ratio between the total allowable indirect costs and benefiting direct base

Indirect Cost Pool = Indirect Cost Rate**

Indirect Cost Base

**An indirect cost rate percentage is calculated by dividing the pool by the base

04/18/20239 ©2011 Deltek, Inc. All Rights Reserved

Composition of indirect pools and bases

04/18/202310 ©2011 Deltek, Inc. All Rights Reserved

The allocation of costs should be accomplished on a cost benefit basis

Pools – composed of indirect costs accumulated with other like costs (homogeneous pools)

Base – allocation method

04/18/202311 ©2011 Deltek, Inc. All Rights Reserved

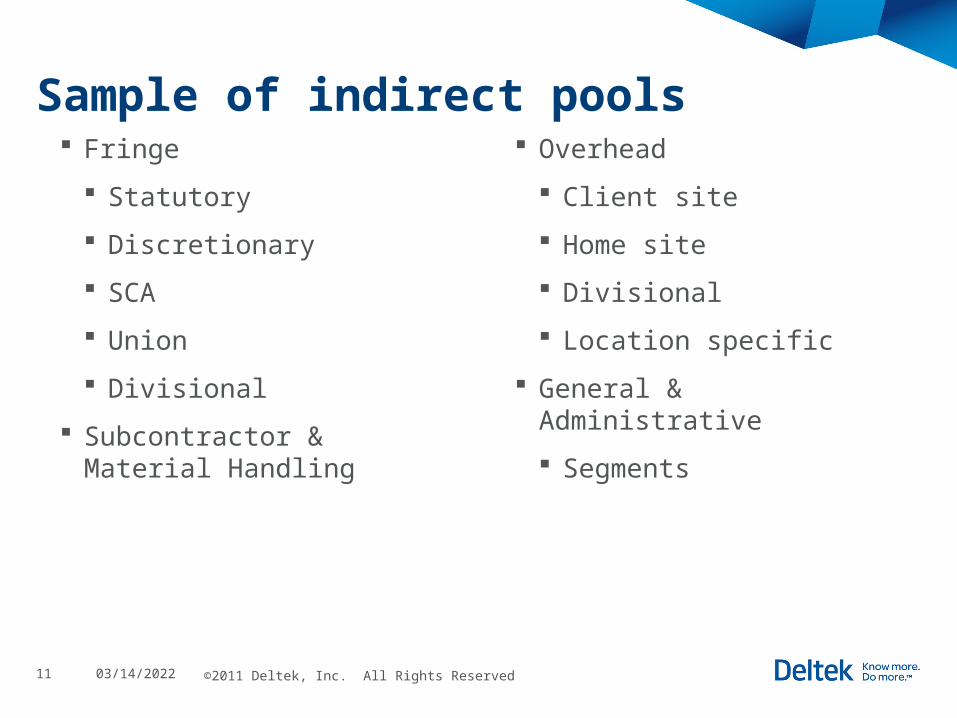

Sample of indirect pools Fringe

Statutory

Discretionary

SCA

Union

Divisional

Subcontractor & Material Handling

Overhead

Client site

Home site

Divisional

Location specific

General & Administrative

Segments

04/18/202312 ©2011 Deltek, Inc. All Rights Reserved

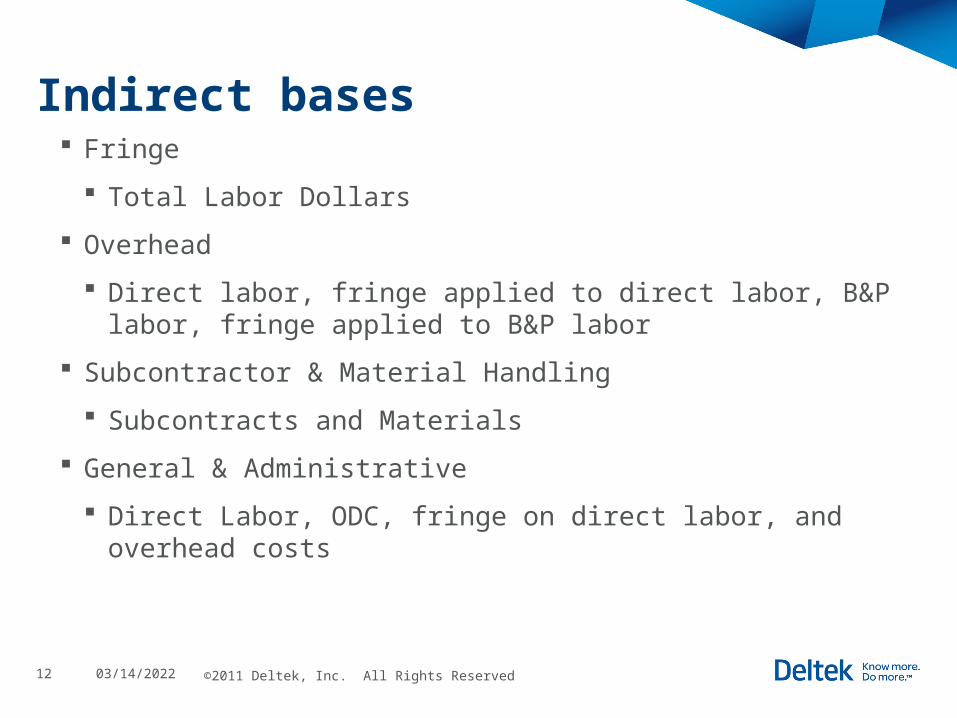

Indirect bases Fringe

Total Labor Dollars

Overhead

Direct labor, fringe applied to direct labor, B&P labor, fringe applied to B&P labor

Subcontractor & Material Handling

Subcontracts and Materials

General & Administrative

Direct Labor, ODC, fringe on direct labor, and overhead costs

04/18/202313 ©2011 Deltek, Inc. All Rights Reserved

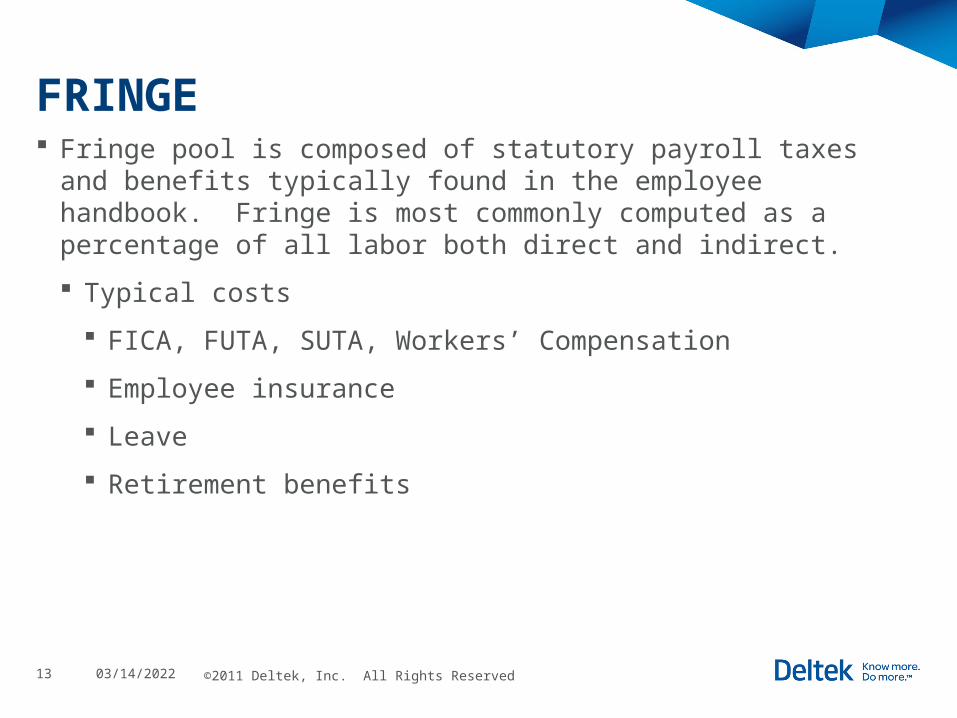

FRINGE Fringe pool is composed of statutory payroll taxes and benefits typically

found in the employee handbook. Fringe is most commonly computed as a percentage of all labor both direct and indirect.

Typical costs

FICA, FUTA, SUTA, Workers’ Compensation

Employee insurance

Leave

Retirement benefits

04/18/202314 ©2011 Deltek, Inc. All Rights Reserved

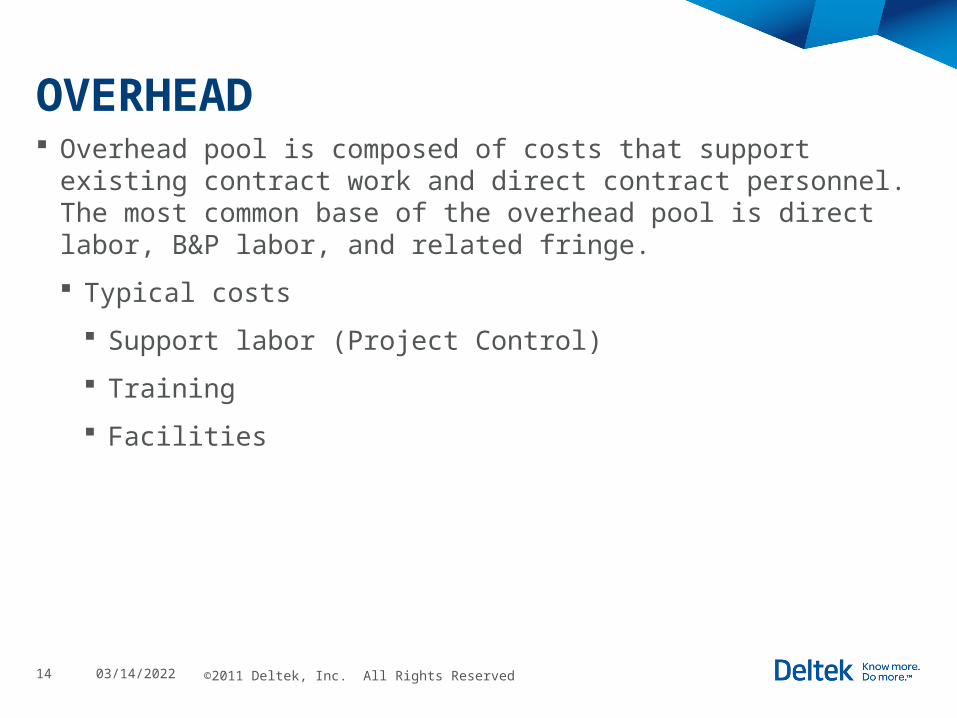

OVERHEAD Overhead pool is composed of costs that support existing contract work

and direct contract personnel. The most common base of the overhead pool is direct labor, B&P labor, and related fringe.

Typical costs

Support labor (Project Control)

Training

Facilities

04/18/202315 ©2011 Deltek, Inc. All Rights Reserved

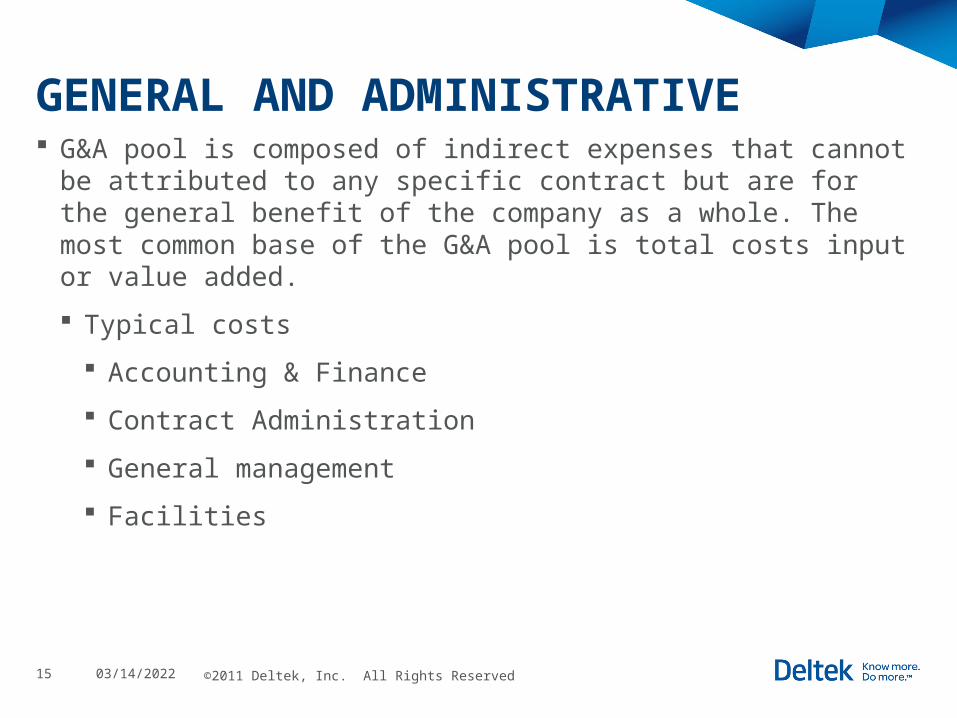

GENERAL AND ADMINISTRATIVE G&A pool is composed of indirect expenses that cannot be attributed to

any specific contract but are for the general benefit of the company as a whole. The most common base of the G&A pool is total costs input or value added.

Typical costs

Accounting & Finance

Contract Administration

General management

Facilities

04/18/202316 ©2011 Deltek, Inc. All Rights Reserved

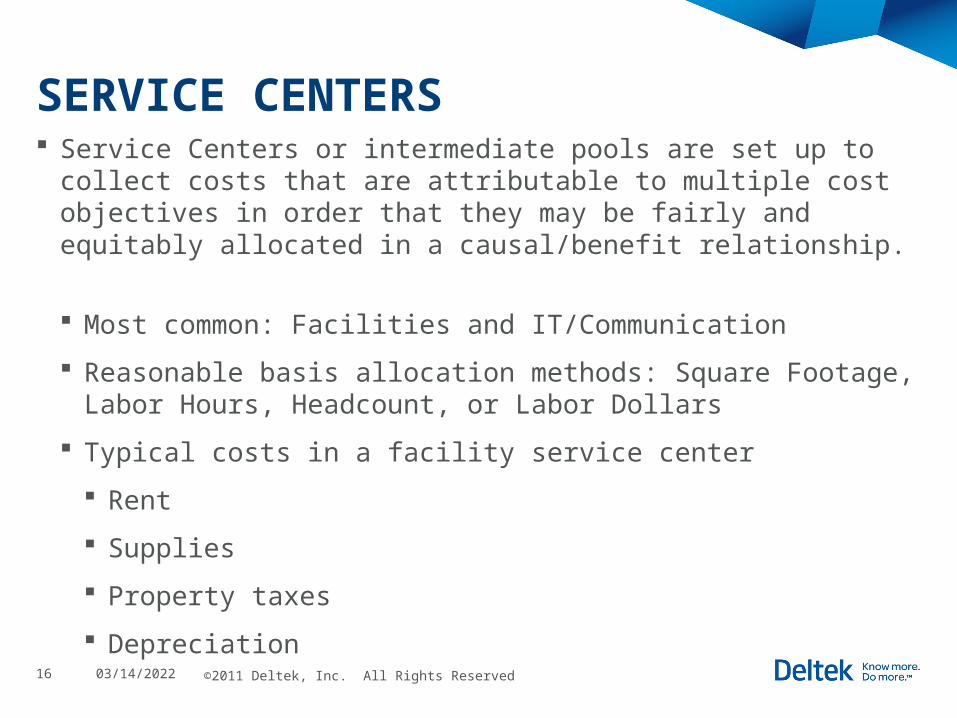

SERVICE CENTERS Service Centers or intermediate pools are set up to collect costs that are

attributable to multiple cost objectives in order that they may be fairly and equitably allocated in a causal/benefit relationship.

Most common: Facilities and IT/Communication

Reasonable basis allocation methods: Square Footage, Labor Hours, Headcount, or Labor Dollars

Typical costs in a facility service center

Rent

Supplies

Property taxes

Depreciation

04/18/202317 ©2011 Deltek, Inc. All Rights Reserved

Workshop

04/18/202318 ©2011 Deltek, Inc. All Rights Reserved

Strategic plan and design of indirect rates

04/18/202319 ©2011 Deltek, Inc. All Rights Reserved

Placement of costs Bonuses

Should only be in fringe if a universal plan exists

Review plan documents

Treatment of deferred plans

04/18/202320 ©2011 Deltek, Inc. All Rights Reserved

Placement of costs Bonuses

Direct vs. Indirect

Labor

Depreciation

Leases (office, equipment, vehicles)

04/18/202321 ©2011 Deltek, Inc. All Rights Reserved

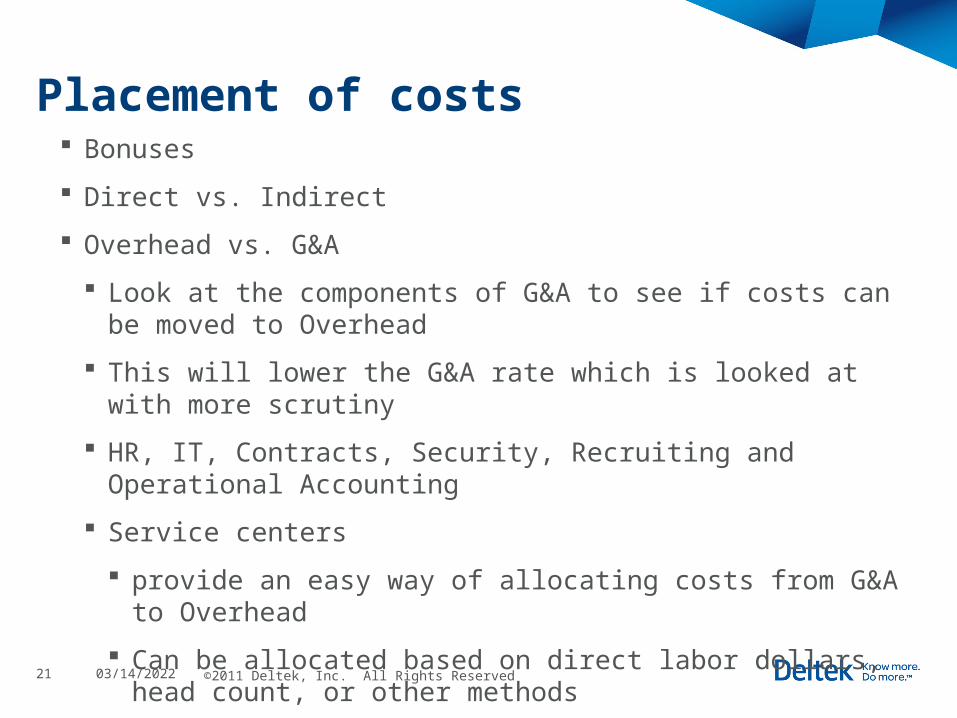

Placement of costs Bonuses

Direct vs. Indirect

Overhead vs. G&A

Look at the components of G&A to see if costs can be moved to Overhead

This will lower the G&A rate which is looked at with more scrutiny

HR, IT, Contracts, Security, Recruiting and Operational Accounting

Service centers

provide an easy way of allocating costs from G&A to Overhead

Can be allocated based on direct labor dollars, head count, or other methods

04/18/202322 ©2011 Deltek, Inc. All Rights Reserved

Placement of costs Bonuses

Direct vs. Indirect

Overhead vs. G&A

Sound financial data

Helps understand the cost of getting new business

If you have the infrastructure in place you will know the risks you are taking

DCAA or other agency reps do not approve job cost accounting software packages; they approve job cost accounting practices

04/18/202323 ©2011 Deltek, Inc. All Rights Reserved

Architecture Appearance

Not changing total costs

Understand your business and your options

Understand your customers and how they evaluate costs and the role costs play in a contract award

04/18/202324 ©2011 Deltek, Inc. All Rights Reserved

Architecture Appearance

Fringe rate

Reduced scrutiny

Without a fringe rate overhead is inflated

Placing fringe on direct labor in the base of the overhead pool

04/18/202325 ©2011 Deltek, Inc. All Rights Reserved

Architecture Appearance

Fringe rate

Overhead rate

Client site vs. Home site

If principal effort is to chase client site work limit overhead

Look at options of classifying client site overhead as a direct costs

Setting up divisions

Treat consultants like employees and put the consultant labor in the base of overhead

Single overhead pool with a facility adder for employees working at different offices

04/18/202326 ©2011 Deltek, Inc. All Rights Reserved

Architecture Appearance

Fringe rate

Overhead rate

Other rates

Consider setting up a Subcontractor Material & Handling rate

This will take the subs out of the base of G&A

Does not include travel or ODC’s

Consultants can be contested if included in this pool

04/18/202327 ©2011 Deltek, Inc. All Rights Reserved

Architecture Appearance

Fringe rate

Overhead rate

Other rates

Cost vs. benefit

Should be considered with all decisions

When allocating service centers if you use a manual base instead of direct labor the allocation can not be run automatically

04/18/202328 ©2011 Deltek, Inc. All Rights Reserved

Hedging your bets Impact of new business

Adjust rates in bids for impact of new business

Understand the relationship between indirect costs and business volume

How will additional workforce and costs effects rates

Will you need to open a new office in a new location

04/18/202329 ©2011 Deltek, Inc. All Rights Reserved

Hedging your bets Impact of new business

Knowing how an indirect cost will react to a change in volume is important for such pricing actions as equitable adjustments and terminations and for the projection of indirect costs

04/18/202330 ©2011 Deltek, Inc. All Rights Reserved

Total value proposition Wrap rate

Calculation

Knowing your market space

04/18/202331 ©2011 Deltek, Inc. All Rights Reserved

Total value proposition Wrap rate

Subcontract material & handling

When should you have one

Effect on other rates

04/18/202332 ©2011 Deltek, Inc. All Rights Reserved

Common errors

04/18/202333 ©2011 Deltek, Inc. All Rights Reserved

Noncompliance with FAR 31.203(c)

Indirect costs should be accumulated by logical cost groupings so as to permit use of an allocation base that is common to all cost objectives to which the groupings is to be allocated.

Unallowable costs are to remain in the base from which they originate.

Noncompliance with CAS 402

Requires consistency in accumulating costs incurred for the same purpose

04/18/202334 ©2011 Deltek, Inc. All Rights Reserved

Inaccurate rate calculations

Proof of indirect rates

Exclusion of B&P labor from the base of overhead

Exclusion of SM&H costs from the base of G&A

Submitting actual rates inconsistent with provisional rates

Noncompliance with FAR 52.232-20 and 21

Indirect rate limitations (ceilings)

Limitation on costs

04/18/202335

Questions

©2011 Deltek, Inc. All Rights Reserved

www.twitter.com/deltek

www.facebook.com/deltekinc

www.linkedin.com/company/163414

www.youtube.com/user/deltekinc

04/18/202336 ©2011 Deltek, Inc. All Rights Reserved

Call to Action Philip Steigner – Senior Manager Audit & Assurance

805 King Farm Blvd, Suite 300, Rockville, MD 20850 301-222-8280 [email protected]

Philip Steigner joined Aronson LLC in September 1997 and is a Senior Manager in the firm’s Government Contracting Services Group. He has 13 years of public accounting experience with a concentration over the past ten years in government contracting.

His focus is on complex financial reporting including mergers & acquisitions, consolidations, foreign entity transactions, joint ventures, income taxes, and ESOP’s. Over the course of his career, Phil has managed client accounts from various areas including government contractors, construction contractors, and real estate partnerships. Philip is a featured speaker on financial and operational accounting topics. He is a graduate of Washington & Jefferson College and currently holds an active CPA license in the state of Maryland.