Embed Size (px)

DESCRIPTION

Why we will not experience another Great Depression

Citation preview

1

Why Government interventions will prevent a Depression

Guy LionAs of October 23, 2008

The New Financial Order may have changed by the very next day

2

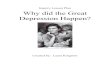

A bit of history…

Why the Great Depression occurred? It was because of very bad Government intervention…

Number of Banks

10000

15000

20000

25000

30000

1926

1927

1928

1929

1930

1931

1932

1933

Almost 50% of banks failed.

3

How to cause a Depression: 1929–1933 Case study

Gold Standard & Fixed

exchange rates

Restrictive monetary policy. Fed Reserve raises interest rates.

Restrictive fiscal policy. Herber Hoover increases taxes and curtails Government spending.

Protectionist trade policy. Congress passes Smoot- Hawley Tariff Act in 1930. Tariffs on U.S. imports double to 50%.

GREAT DEPRESSION. GDP contracts by 33%. Unemployment reaches 25%.

4

How to cause a Depression (in details): 1929–1933 Case study

Gold Standard & Fixed

exchange rates

Restrictive monetary policy. Fed Reserve raises interest rates.

Restrictive fiscal policy. Herber Hoover increases taxes and curtails Government spending.

Lack of Deposit Insurance.

Money supply contracts by -33%.

Public holds on to cash.

Deflation

Banks used to invest in stocks and lend to brokers. 50% of banks fail.

Bank runs

Stock market crash. Dow Jones drops by 89%.

Farmers default

Capital investment drops. Industrial production drops by 54%.

Protectionist trade policy. Congress passes Smoot- Hawley Tariff Act in 1930. Tariffs on U.S. imports double to 50%.

U.S. exports drop 50%.

Consumer Demand drops. Price & income fall 20%-50%.

Business & consumers default

Surviving banks curtail lending

GREAT DEPRESSION. GDP contracts by 33%. Unemployment reaches 25%.

Home prices drop 30%.

5

1929: Really bad policies and vicious feedback loops

• Staying on the Gold Standard constrained policymakers into restrictive policies to prevent inflation and trade deficits to maintain the current US$-Gold conversion rate.

• The restrictive policies triggered negative feedback loops associated with deflation. All GDP components contracted simultaneously.

• Money creation broke down as the public stopped depositing cash (in the absence of deposit insurance combined with nearly 50% of banks failing) and surviving banks stopped lending. Money supply shrank by 33%.

• The ultimate results included a 54% contraction in industrial production, a 33% contraction in GDP coupled with an unemployment rate of 25%.

6

How to spread a Depression globally

After WWI, Germany was burdened with crippling Reparation debt to the Allies. The Allies owed the U.S. for financing their military operations. The Allies relied on Germany’s WWI Reparation debt repayment to repay the U.S. Germany depended on U.S. loans and export earnings to repay WWI Reparation debt.

Under the Gold Standard, the U.S. restrictive policies were transmitted overseas just as if foreign currencies were pegged to the $U.S. The World economy and trade cratered. Germany rescinded on the Reparation debt. The Allies and Germany defaulted on many of their loans to the U.S.

International cash flows resulting from WWI.

$ Debt to U.S. $ U.S. Loan to GermanyAllies

$ WWI Reparation debt

U.S.

Germany Italy

FranceU.K.

7

Financial Pandemics: comparing 1929 vs the current situation

Disease final stage

1929 - 1933

2007 -

VIRUS Contagion Serious symptom Critical disease

Gold StandardRestrictive fiscal, monetary, and trade policies

Deflation Bank failures Depression

Declining U.S. home prices

MBS defaults & write downs

Financial system stressed

Credit default swaps at risk

Wall Street disappears

Credit markets freeze

????????Securitization

During the Great Depression the virus was the Gold Standard framework that turned contagious due to the restrictive fiscal, monetary, and trade policies it triggered pretty much worldwide. This time around, the virus is declining U.S. home price. The associated contagion was triggered by the securitization of MBS and the resulting defaults and write downs of those same MBS.

8

How to prevent a Depression…

Consumer spending Capital investments Government spending

9

Fiscal policy is very expansive

• Congress passed a $168 billion stimulus packaged in February 2008.

• As part of the $700 billion bail out enacted on October 3, 2008, Congress tacked on an additional $150 billion in Government spending.

• Congress is considering another stimulus package in the $150 billion range that could pass by yearend.

• The Budget Deficit rose from $162 billion or 1.2% of GDP in fiscal 2007 to $455 billion (3.2% of GDP) in fiscal 2008. In fiscal 2009, Budget Deficit could easily increase to $700 billion ( 5% of GDP) or much more.

10

Monetary policy is very expansive

• Since June of 2006, the Federal Reserve has lowered the Fed Funds rate from 5.25% to 1.50%.

• Federal Reserve lending has exploded from $189 billion to $937 billion from mid September to mid October. The Fed has expanded its lending way beyond banks to just about all financial intermediaries. See next slide for detail.

11

Federal Reserve lending is skyrocketing

Federal Reserve lending has exploded from $189 billion on 9/10 to $937 billion on 10/08.

Lending to non-banks started in March 08 and now stands at $334 billion. The near $1 trillion Fed lending is also instrumental in fending off a depression.

Federal Reserve lending: 1/01/08 to 10/08/08

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

$ b

illi

on

Source: Federal Reserve. H3.

Total

Banks

Non-banks

12

Scale of Government Intervention is unprecedented

Although some line items are not fully comparable in stimulating effect, the current Government interventions scale is unprecedented.If FDR's New Deal bailed us out of the Great Depression by increasing Government spending from 3% to 9% of GDP, there is little doubt the current much larger coordinated Government interventions should prevent a depression.Also, the FDR New Deal kicked in slowly 4 years after the beginning of the Great Depression. Meanwhile, the current set of Government interventions are pretty much preemptive. Indeed, in the second quarter of 2008, GDP was still growing at 2.7% per annum.

Government interventions % of GDP $ Trillion$250 billion bank capital increases lending capacity by … 16.8% 2.40$ 2009 Budget Deficit fiscal stimulus estimate 4.9% 0.70$ Federal Reserve lending to financial intermediaries 6.6% 0.94$

28.3% 4.04$

The Great Depression and FDR's New Deal in today's dollars Scale of Great Depression GDP contraction in today's terms. -33.0% (4.72)$ FDR's New Deal increase in Federal spending per annum. 6.0% 0.86$

13

Rendering Bank Runs much less likely over the next 3 years

During the Great Depression, they did not have deposit insurance and

nearly 50% of banks disappeared.

Number of Banks

10000

15000

20000

25000

30000

1926

1927

1928

1929

1930

1931

1932

1933

Banks

FDIC guarantees all banks senior

debt for next 3 years

FDIC guarantees all non interest

bearing accounts

FDIC increases deposit insurance

cap to $250K permanently

14

Reducing systemic risk

• On September 7, 2008, the Government nationalized the housing agencies to stabilize the Agency MBS market.

• During 2008, the highly leveraged Wall Street investment banking sector disappeared. Bear Stearns, Lehman, and Merrill Lynch were sold to major commercial banks. Goldman Sachs and Morgan Stanley were converted to regulated commercial banks with higher capital requirements.

• On September 16, the Federal Reserve took control of AIG by lending it $85 billion in exchange for a 79.9% equity stake. This was to stabilize the credit default swap market.

• The $700 billion Emergency Economic Stabilization Act was enacted on October 3, 2008 to shore up the banking sector through $250 billion in equity investment and the remainder to purchase impaired MBS and mortgages (see Appendix A).

• Regulators are considering transferring credit default swaps and derivatives to clearing exchanges just as futures and options. This would eliminate counterparty risk with unregulated hedge funds.

15

A look at the Credit Markets Freeze

16

The Credit Markets Freeze

Because banks’ capital is under stress from mortgage borrowers defaults, money market funds stopped buying banks short-term debt. And, banks have stopped lending to each other (interbank market). Additionally, when Lehman defaulted on its s/t debt it caused one money market fund’s net asset value to fall below $1.00. This caused this same MMF to suffer the equivalent of a run-on-the-bank as it was entirely liquidated by its MMF investors within days. Thus, credit markets have frozen (ice blue, all the dotted blue arrows reflect credit flows that have frozen). As a result, banks have curtailed lending to corporations, small businesses, and households.

CREDITORS

$ $

$ $ $

$ $ $

BORROWERS

Banks

Corporations

Households

Small business

Interbank market

Money market funds

Depositors

Money market funds investors

17

Interest Rates & Spreads. They were cold…

The financial crisis has caused a “flight to quality” as 3-mth T-bills yield have dropped close to 0% while other s/t rates have risen. All spreads have risen dramatically from mid

September till 10/10/08.

3-month Interest Rates thru 10/10/08

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

1/2/2007

3/2/2007

5/2/2007

7/2/2007

9/2/2007

11/2/2007

1/2/2008

3/2/2008

5/2/2008

7/2/2008

9/2/2008

Per

cen

tag

e p

oin

ts3-month Spreads over T-bills thru 10/10/08

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

1/2/2007

3/2/2007

5/2/2007

7/2/2007

9/2/2007

11/2/2007

1/2/2008

3/2/2008

5/2/2008

7/2/2008

9/2/2008

Pe

rce

nta

ge

po

ints

LIBOR

Nonfinancial Commercial Paper

T-bills

LIBOR

Nonfinancial Commercial Paper

Sources: Wells Fargo, Federal Reserve. H.15.

Sources: Wells Fargo, Federal Reserve. H.15.

Interbank markets frozen

CP market under stress

Financial crisis "flight to quality" T-bill rates drop to near 0%.

18

Curing the Credit Markets Freeze

$ $

$

$ $

$ $ $

$ $ $

Banks

Corporations

Households

Small business

Interbank market

Money market funds

Depositors

Money market funds investors

FDIC guarantees all banks senior

debt for next 3 years

U.S. Treasury insures Money Market Funds for next 3 mths

or more...

U.S. Government injects $250

billion in banks to boost

lending

Fed Reserve is buying CP from corporations &

MMFs to revive CP market

Notice that all the former blue dotted arrows denoting frozen credit market flows are now gone indicating those same credit market flows have been revived somewhat.

19

The Cure is working. Spreads not

so wide (cold) anymore

Over the past two weeks, all the curves are going in the right direction. The “flight to quality” has abated as T-Bill yields have risen by almost 100 b.p. The Interbank market has shown signs of life as the LIBOR spread over T-Bill has shrank from 457 b.p. to 253 b.p. And, the Commercial Paper market is also in better shape. Within a few months those spreads should decline to their normal level at less than 50 b.p.

3-month Interest Rates 10/10 - 10/23

0.00

1.00

2.00

3.00

4.00

5.00

6.00

10/10/2008

10/11/2008

10/12/2008

10/13/2008

10/14/2008

10/15/2008

10/16/2008

10/17/2008

10/18/2008

10/19/2008

10/20/2008

10/21/2008

10/22/2008

10/23/2008

Per

cen

tag

e p

oin

ts

3-month Spreads over T-bills thru 10/10/08 - 10/23

0.00

1.00

2.00

3.00

4.00

5.00

6.00

10/10/2008

10/11/2008

10/12/2008

10/13/2008

10/14/2008

10/15/2008

10/16/2008

10/17/2008

10/18/2008

10/19/2008

10/20/2008

10/21/2008

10/22/2008

10/23/2008

Per

cen

tag

e p

oin

ts

Sources: Wells Fargo, Federal Reserve. H.15.

LIBOR

Nonfinancial Commercial Paper

T-bills

LIBOR

Nonfinancial Commercial Paper

Sources: Wells Fargo, Federal Reserve. H.15.

20

Impact of the $250 billion Government equity injection in the banking industry

The Government $250 billion equity injection could support $2.4 trillion in new lending while banks maintain their current Equity/Assets (10.4%) ratio.

This represents a 31% increase in lending capacity or 16.8% of GDP.

In $ billion

As of After $250 b.10/01/08 injection

AssetsOther assets 4,067.2 4,067.2 Loans on books 7,703.6 7,703.6 New loans - 2,413.0

11,770.8 14,183.8

Liabilities & EquityLiabilities 10,551.3 12,714.3 Equity 1,219.5 1,469.5

11,770.8 14,183.8

Equity/Assets ratio 10.4% 10.4%

Source of current data: Federal Reserve H.8. S.A.

21

Just in case Credit Markets and Bank Lending do not fully recover, let’s explore the overall financial health of the borrowers and their

ability to self-finance.

22

Leverage in the Economy is moderate

Source: Federal Reserve/Flow of Funds. B100, B102, B103

Leverage in the Economy. Liabilities/Equity

0%

20%

40%

60%

80%

100%

120%

86Q488Q2

89Q491Q2

92Q494Q2

95Q497Q2

98Q400Q2

01Q403Q2

04Q406Q2

07Q4

Quarterly period

Lia

bil

itie

s/E

qu

ity

Corporations

Small business

Households

Corporations have steadily “deleveraged” since the early 90s.

Small business leverage has risen but is in line with corporations.

Households leverage has risen, but is very low at 0.26.

23

Corporations self–financing capacity is strong

Corporations ability to generate internal cash flow to finance capital expenditures + inventory purchases has remained strong through the first half of 2008.

The measure in blue includes dividends (negative cash flow component). The measure in green excludes dividends.

As shown, corporations now can finance nearly 90% of cap. ex. and inventory internally. And, if they cut dividends this % increases to over 130%.

Source: Federal Reserve/Flow of Funds. F102

Corporations self-financing capability

60%

80%

100%

120%

140%

160%

86Q488Q2

89Q491Q2

92Q494Q2

95Q497Q2

98Q400Q2

01Q403Q2

04Q406Q2

07Q4

Quarterly period

Cash Flow excluding dividend/(Capital expenditures + Inventory purchase)

Cash Flow/(Capital expenditures + Inventory purchase)

This is 4 quarter moving average

24

Small business self financing capability is very strong

As shown, the ratio of internal cash flow to [capital expenditures + inventory] steadily exceeds 200% since end of 1986. In first half of 2008 it stands at over 350%.

Source: Federal Reserve/Flow of Funds. F103

Small Business self-financing capability

200%

250%

300%

350%

400%

450%

500%

550%

600%

Quarterly period

Cash Flow/(Capital expenditures + Inventory purchase)

This is a 4 quarter moving average to smoothen the graph

25

The Myth of the overleveraged U.S. Household (HH)?!

We already observed how HH Liabilities/Equity is very low.

The financial obligation ratio (FOR) is the most inclusive measure of HH debt servicing capacity. In the numerator, it includes all debt (mortgages, consumer loans) plus auto leases, rents, homeowners’ insurance, and property tax. The denominator consists in Disposable Personal Income.

Notice how the renters FOR has steadily declined since 2001. It is now very low at 25.6%. And, the homeowners FOR is even lower at 18.8%.

Source: Federal Reserve Board - Household Debt Service & FOR

Financial Obligation Ratio (FOR) of U.S. Households

10%

15%

20%

25%

30%

35%

Quarterly Period

Homeowners

Renters

26

Foreclosures in perspective…The press focuses on the “explosive growth in foreclosure” mentioning that the foreclosure rate (% of homes entering foreclosures) has nearly doubled between the 2Q of 2008 vs the same quarter last year. That sounds much more catastrophic than stating that the foreclosure rate has increased from 0.30% of homes to 0.56% of homes.

Sources: MBA, U.S. Census, Moody's Economy.com

Foreclosure situation

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

1.60%

1.80%

2.00%

2002

Q1

2002

Q3

2003

Q1

2003

Q3

2004

Q1

2004

Q3

2005

Q1

2005

Q3

2006

Q1

2006

Q3

2007

Q1

2007

Q3

2008

Q1

% o

f H

om

es

% of Homes in foreclosure at quarter end.

% of Homes entering foreclosure during quarter

This foreclosure rate is illustrated by the green line. The black line is a static balance sheet concept that indicates at any one point the % of homes in foreclosure at the time. The value in the current quarter equals the value in the previous quarter plus the homes entering foreclosure during the quarter (green line) minus the homes exiting foreclosure or resold to a new homeowner (not shown on the graph).

27

The Positive side of Foreclosures… Homes are becoming more affordable.

NAR Housing Affordability Index = Median Family Inc./Qualifying Inc. times a 100.

Qualifying income = Yearly Mortgage/0.25 (Debt/Income ratio) assuming a 20% downpayment.

The NAR Housing Affordability Index shows that homes are becoming more affordable as Median Family Income has risen rapidly from 106.1% of Qualifying Income to buy a Median priced home in 2006 to 125.0% in 2008 Q2. This increase in home affordability can be expected to increase over the next few quarters as home prices may remain under some pressure.

NAR Housing Affordability Index

Median Price Monthly Payment Median CompositeExisting Single- Mortgage P & I as a % of Family Qualifying Affordability

Year Family Home Rate Payment* Income Income Income** Index

2006 221,900 6.58 1131 23.6 57,612 54,288 106.12007 217,900 6.52 1104 22.4 59,224 52,992 111.8

2008 Q2 206,500 6.14 1005 20.0 60,294 48,240 125.0

©2008 National Association of REALTORS®* Assumes a 20% downpayment.** Assumes a Debt/Income ratio of 25%.

28

Conclusion: a Depression is very unlikely because…

• Unlike 1929, policymakers are taking most appropriate and immediate preventive policies on an unprecedented scale measured in $trillions that appears to dwarf even FDR’s New Deal.

• The full Government backing of both the banking system and money market funds is already reviving the credit markets.

• Corporations, small business, and households have good self-financing capability that gives the Government policies time to work.

29

Appendix A: Government assisting commercial banks in

resolving their residential real estate risk.

30

Banking exposure to residential real estate

The commercial banking industry total exposure to residential real estate is $2.224 trillion as of June (FDIC data) excluding Agency MBS since the Agencies have been nationalized.

The commercial banking industry capital cushion consists mainly of $1.155 trillion in equity (as of 6/30). After deducting goodwill, this results in a Tier I Capital of $819.9 billion which is equal to 7.2% of assets. This is pretty high since the regulatory requirement is 5%.

In $ billion

Commercial banks residential real estate exposureSingle family mortgages 1,951.4 REO 14.3 Private MBS 19.5 Private CMOs 238.6

2,223.9 Capital cushionEstimated reserves vs mortgages 35.0 Equity 1,155.3 Goodwill 335.4 Tier I Capital estimate 819.9 Leverage ratio est. (Tier I/Assets) 7.2%

Source: FDIC 6/30/2008.

31

Modeling the impact of the remaining $450 billion Government cushion vs real estate risk

Relying on the FDIC data of the previous page, our short model uses one driving assumption: Home Value to Loan (VTL). We assume this value is <100% and we stress it to see how low it could go before the banking industry would not meet its “Well capitalized” Tier I Leverage Ratio. The answer is 65%.

$700 billion bail out less $250 billion equity injection in banks

Model in $ billions

AssumptionHome Value to Loan (VTL) 75%Unsecured exposure 25%

Output.Unsecured exposure 556.0 Prorated reserves 35.0 Exposure after reserves 521.0 Government bail out 450.0 Impact on Tier I Capital 71.0 Impact on Tier I Capital in % 8.7%

ScenariosLeverage

VTL in $ billion in % Ratio80.0% 0.0 0.0% 7.2%77.5% 15.4 1.9% 7.0%75.0% 71.0 8.7% 6.5%72.5% 126.6 15.4% 6.1%70.0% 182.2 22.2% 5.6%67.5% 237.8 29.0% 5.1%65.0% 293.3 35.8% 4.6%

Impact on Tier I Capital

32

Home price decline for banking industry Tier I Leverage < 5%

To answer how much a decrease in home price corresponds to a VTL of 65%, you have to know what was the initial LTV ratio. If you know that, you can calculate the decrease in home price as the VTL ratio is equal to 1/LTV. Given that the majority of the banking residential real estate exposure is associated with on-balance sheet-loans and not securities, the original LTV industry wide may be at the low end of the 80% to 100% range. The resulting calculated decrease in home prices with moderate LTVs are large (greater than 40%).

The remaining $450 billion in Government bail out should provide substantial assistance to the banking industry in dealing with writing down its residential real estate exposure.

Original Original Current Decrease inLTV VTL VTL home price80% 125% 65% -48.0%85% 118% 65% -44.8%90% 111% 65% -41.5%95% 105% 65% -38.3%

100% 100% 65% -35.0%