Embed Size (px)

Citation preview

#cbizmhmwebinar 1

CBIZ & MHM Executive Education Series™

Recent Tax Developments Impacting the Architecture/Engineering/Construction Industries Cord Armstrong December 1 and 15, 2015

#cbizmhmwebinar 2

About Us

• Together, CBIZ & MHM are a Top Ten accounting provider • Offices in most major markets • Tax, audit and attest* and advisory services • Over 2,900 professionals nationwide

A member of Kreston International A global network of independent accounting firms

#cbizmhmwebinar 3

Before We Get Started…

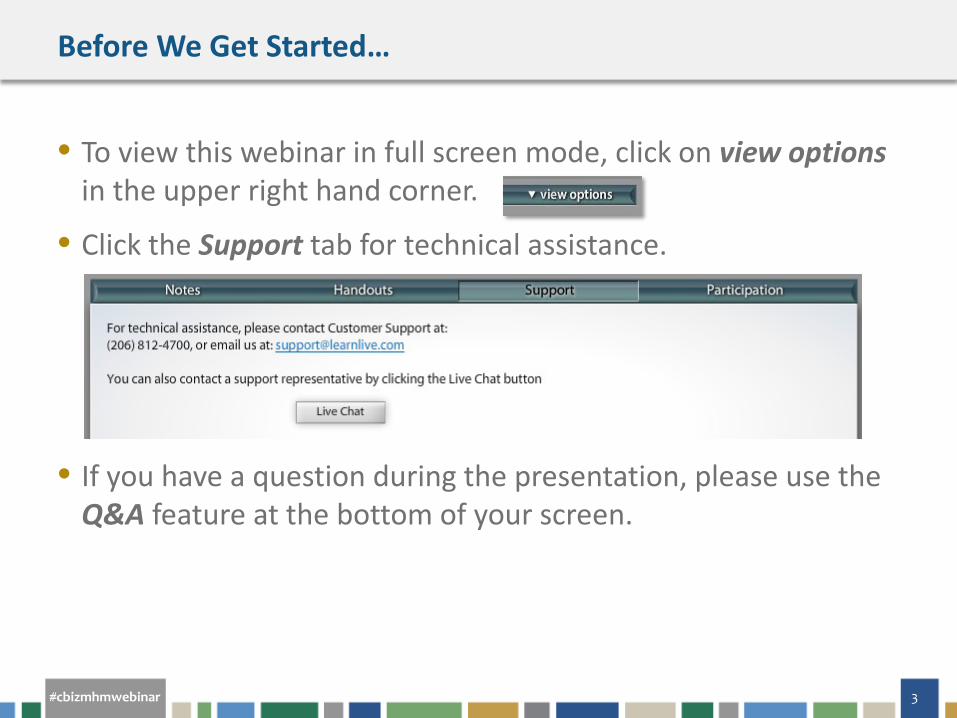

• To view this webinar in full screen mode, click on view options in the upper right hand corner.

• Click the Support tab for technical assistance.

• If you have a question during the presentation, please use the Q&A feature at the bottom of your screen.

#cbizmhmwebinar 4

CPE Credit

This webinar is eligible for CPE credit. To receive credit, you will need to answer periodic participation markers throughout the webinar. External participants will receive their CPE certificate via email immediately following the webinar.

#cbizmhmwebinar 5

Disclaimer

The information in this Executive Education Series course is a brief summary and may not include all

the details relevant to your situation.

Please contact your service provider to further discuss the impact on your business.

CBIZ & MHM 6

Cord Armstrong is a Managing Director in the company’s tax division.

His involvement spans all aspects of Federal and State taxation,

including compliance, planning and research for businesses and high net

worth individuals.

Cord has more than 20 years of experience in public accounting and is

responsible for the supervision of staff in various tax compliance and

research matters for individuals, businesses, trusts and estates. His

duties also include review of federal and state corporate returns for the

company’s audit clients as well as significant year-end tax planning and

consulting. Cord specializes in the construction industry and is a member

of the company's National Construction Industry Practice Group. He also

has a specialty in estate and gift tax matters and has represented

corporate and individual clients before the Internal Revenue Service and

other state and local tax authorities

602.264.6835 • [email protected]

Cord D. Armstrong CPA, MST, CCIFP Managing Director

Presenter

#cbizmhmwebinar 7

Agenda

Status of Tax Extenders

02

01

03

04

Recent Tax Court Cases

IRS Notice 2015-40 – IRS seeks Input on the New Revenue Recognition Standards

Proposed Regulations for IRC Sec. 199 (DPAD) and affect on the construction industry

Other Hot Topics for Contractors

06

05

Questions

#cbizmhmwebinar 8

Status of Tax Extenders

RECENT TAX DEVELOPMENTS IMPACTING THE ARCHITECTURE/ENGINEERING/CONSTRUCTION

INDUSTRIES

#cbizmhmwebinar 9

Status of Tax Extenders

• Many of the popular provisions that expired as the end of last year include • 50% Bonus Depreciation • Increased 179 Depreciation (increased to $500K) • 15 Year straight-line depreciation for qualified leaseholds • Research and Experimentation Credit • 179D Deduction for energy efficient buildings • Work Opportunity Tax Credit • Reduction in Built-in-gain recognition period

#cbizmhmwebinar 10

Status of Tax Extenders

• Recent House Legislation • House has passed a series of bills permanently extending

many of the popular provisions (bonus depreciation, increased 179, etc.)

• New Ways and Means Committee Chairman – Rep. Kevin Brady

• Rep. Brady said he wants to get something done this fall (driving for a permanent extension or at least a two year extension)

#cbizmhmwebinar 11

Status of Tax Extenders

• Recent Senate Legislation • Extender bill passed in July of 2015 (extends 52 provisions for

two years)

• Senate Finance Chairman Orrin Hatch recently met with Rep. Brady to plan a path forward with making at least some of the extenders permanent prior to the end of the year

• Senate version of extender bill included a modification to 179D to allow non-profits and tribal organizations – watch final bill

#cbizmhmwebinar 12

Status of Tax Extenders

• Where are we at now?

• The expired provisions are likely to be in the last two revenue bills to be passed before the end of the year • Highway Bill or • Omnibus Spending package

• Most likely scenario is there will only be a one year extension – retroactive to the beginning of the year

#cbizmhmwebinar 13

Recent Tax Developments Impacting the Architecture/Engineering/Construction

Industries

Recent Tax Court Cases

#cbizmhmwebinar 14

Howard Hughes Company LLC v. Comm., 116 2d 2015-6597

• Appeals Court for the 5th Circuit affirmed the original courts decision on 10/27/15 –Victory for the IRS

• Background • Taxpayer was a residential land developer in the Las Vegas

area who sold land to builders but did not construct any of the homes on the land sold

• Taxpayer accounted for the sale of the lots under the CCM since they were home construction contracts – thus income was deferred until all of the development costs were completed

#cbizmhmwebinar 15

Howard Hughes Company LLC v. Comm., 116 2d 2015-6597

• Reason for the Ruling • The crux of the dispute was the ambiguous language in the

80% test that defines a home construction contract

• The Appellate Court said the Tax Court correctly construed the “plain and ordinary” meaning of the statute and regulations and that home construction exception only applies if the taxpayer constructs the dwelling units

#cbizmhmwebinar 16

IRS Appeals Shea Homes Decision

• Background • Taxpayer developed planned communities however In

contrast to Howard Hughes the taxpayer also built the individual homes in addition to the developments infrastructure and improvement costs

• The entire subdivision development was treated as a single contract - not just the individual homes sold -deferring income for a long time under the CCM

#cbizmhmwebinar 17

IRS Appeals Shea Homes Decision

• Court Decision • Original court decision was a victory for the taxpayer

• The Tax Court determined they were permitted to use the CCM for their sales of homes in their planned development

• Reason for the Ruling • The court ruled that the subject matter of the contract

consisted of the home and the larger development costs - amenities and common improvements

#cbizmhmwebinar 18

Frontier Custom Builders v Comm, 116 AFTR 2d 2015-6146

• Appeals Court for the 5th Circuit affirmed the original courts decision on 9/16/15 – Victory for the IRS

• Background • Taxpayer is a custom home builder who claimed deductions

including employee salaries and year-end bonuses, including $1,318,000 in total compensation paid to the company’s President – did not capitalize any of the compensation in ending inventory

#cbizmhmwebinar 19

Frontier Custom Builders v Comm, 116 AFTR 2d 2015-6146

• Reason for the Ruling • The Tax Court determined that most of the salaries at issue

should have been capitalized as mixed service costs (allocated to incomplete homes), instead of deducted, under IRC Sec. 263A

• Large home builders are exempt from the cost allocation rules of IRC Sec. 460(c) but must follow the UNICAP rules under IRC Sec. 263A (the rules are virtually the same)

• Taxpayer claimed the 263A did not apply because they were a marketing and sales company

#cbizmhmwebinar 20

IRS Seeks Input on New Revenue Recognition Standards

IRS Notice 2015-40

RECENT TAX DEVELOPMENTS IMPACTING THE ARCHITECTURE/ENGINEERING/CONSTRUCTION

INDUSTRIES

#cbizmhmwebinar 21

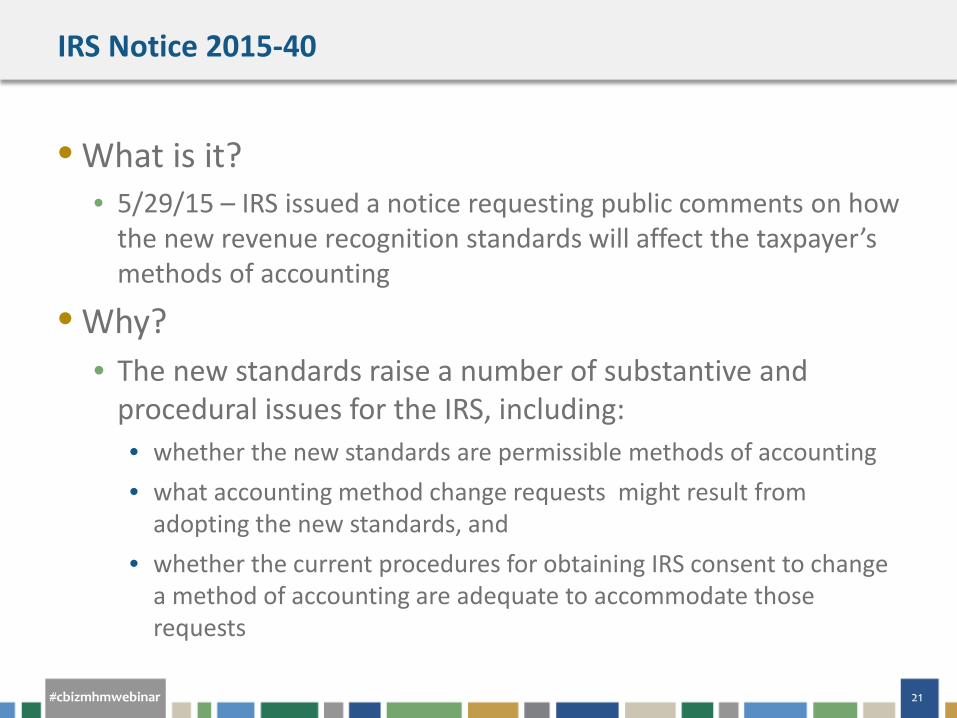

IRS Notice 2015-40

• What is it? • 5/29/15 – IRS issued a notice requesting public comments on how

the new revenue recognition standards will affect the taxpayer’s methods of accounting

• Why? • The new standards raise a number of substantive and

procedural issues for the IRS, including: • whether the new standards are permissible methods of accounting • what accounting method change requests might result from

adopting the new standards, and • whether the current procedures for obtaining IRS consent to change

a method of accounting are adequate to accommodate those requests

#cbizmhmwebinar 22

IRS Notice 2015-40

• Important things to note about the new revenue recognition standards • The percentage of completion method is effectively

eliminated for financial reporting purposes

• The core principal of revenue recognition is that revenue is recognized as goods or services are transferred to customers (similar to PCM)

• Nonpublic entities are required to adopt the new standards for years beginning after December 15, 2018, however they may elect to apply them for years beginning after December 15, 2017

#cbizmhmwebinar 23

IRS Notice 2015-40

• The Association of General Contractors (AGC) responded to the notice and pointed out specific areas that may give rise to book/tax differences as a result of the new standards that might be addressed in future guidance including : • Multiple Performance Obligations within a Construction

Contract

• Uninstalled Materials

• Variable Consideration

• Costs of Obtaining a Construction Contract

#cbizmhmwebinar 24

IRS Notice 2015-40

• Multiple Performance Obligations • May be necessary to sever and account for the contract as

two or more contracts for financial reporting purposes

• However Reg. 1.460(e)(3)(i) prohibits a taxpayer from severing a long-term contract accounted for under PCM without obtaining consent from the commissioner

• AGC asked that the IRS make this an automatic change to be consistent and conform to the accounting for financial statement purposes

#cbizmhmwebinar 25

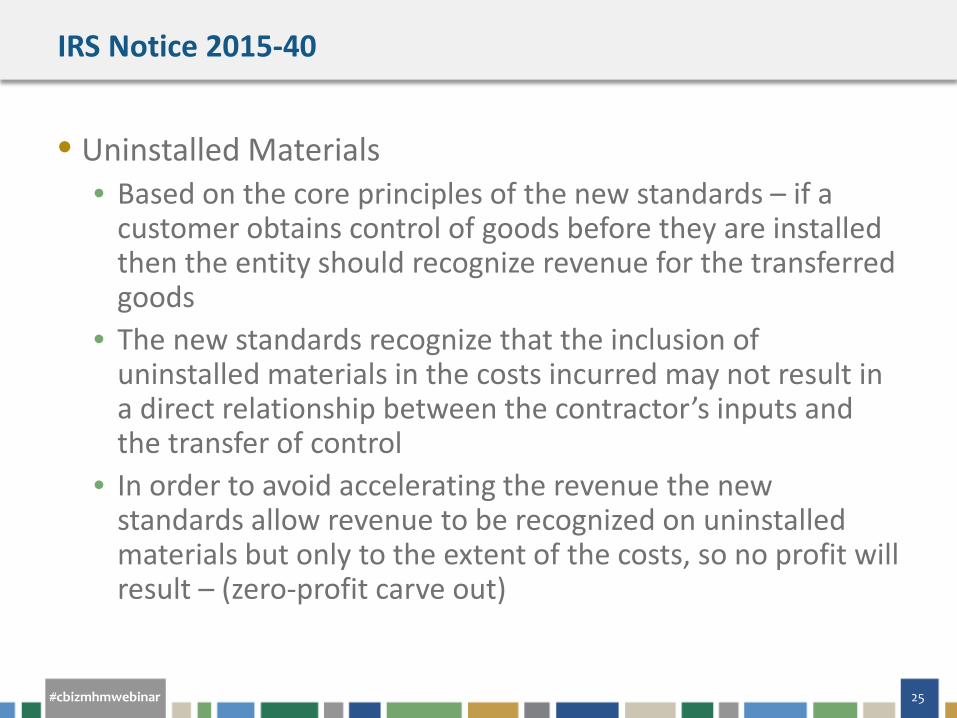

IRS Notice 2015-40

• Uninstalled Materials • Based on the core principles of the new standards – if a

customer obtains control of goods before they are installed then the entity should recognize revenue for the transferred goods

• The new standards recognize that the inclusion of uninstalled materials in the costs incurred may not result in a direct relationship between the contractor’s inputs and the transfer of control

• In order to avoid accelerating the revenue the new standards allow revenue to be recognized on uninstalled materials but only to the extent of the costs, so no profit will result – (zero-profit carve out)

#cbizmhmwebinar 26

IRS Notice 2015-40

• Uninstalled Materials - continued • This zero-profit carve out would cause and even greater

acceleration of profit for tax purposes than we have now under SOP 81-1 since the costs of materials dedicated to the project are included in the cost-to-cost calculation under IRC 460

• AGC also asked that this carve out for the transfer of uninstalled materials be allowed to be severed into a separate contract in order to be consistent and conform to the accounting for financial reporting purposes

• See the book/tax differences in the following example

#cbizmhmwebinar 27

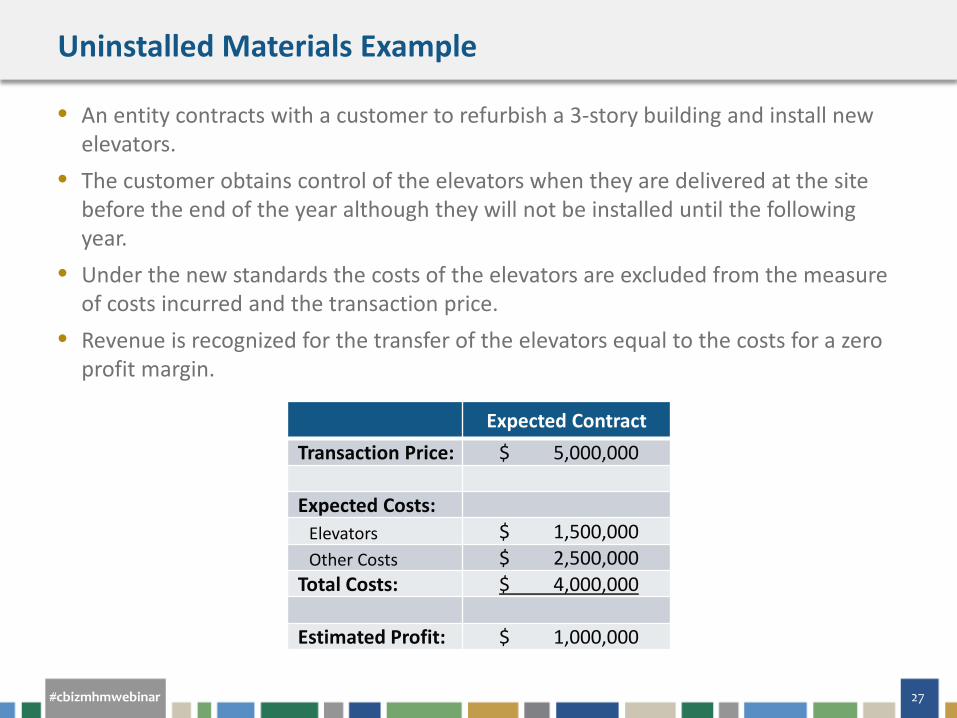

Uninstalled Materials Example

• An entity contracts with a customer to refurbish a 3-story building and install new elevators.

• The customer obtains control of the elevators when they are delivered at the site before the end of the year although they will not be installed until the following year.

• Under the new standards the costs of the elevators are excluded from the measure of costs incurred and the transaction price.

• Revenue is recognized for the transfer of the elevators equal to the costs for a zero profit margin.

Expected Contract Transaction Price: $ 5,000,000

Expected Costs: Elevators $ 1,500,000 Other Costs $ 2,500,000 Total Costs: $ 4,000,000

Estimated Profit: $ 1,000,000

#cbizmhmwebinar 28

Uninstalled Materials Example Continued

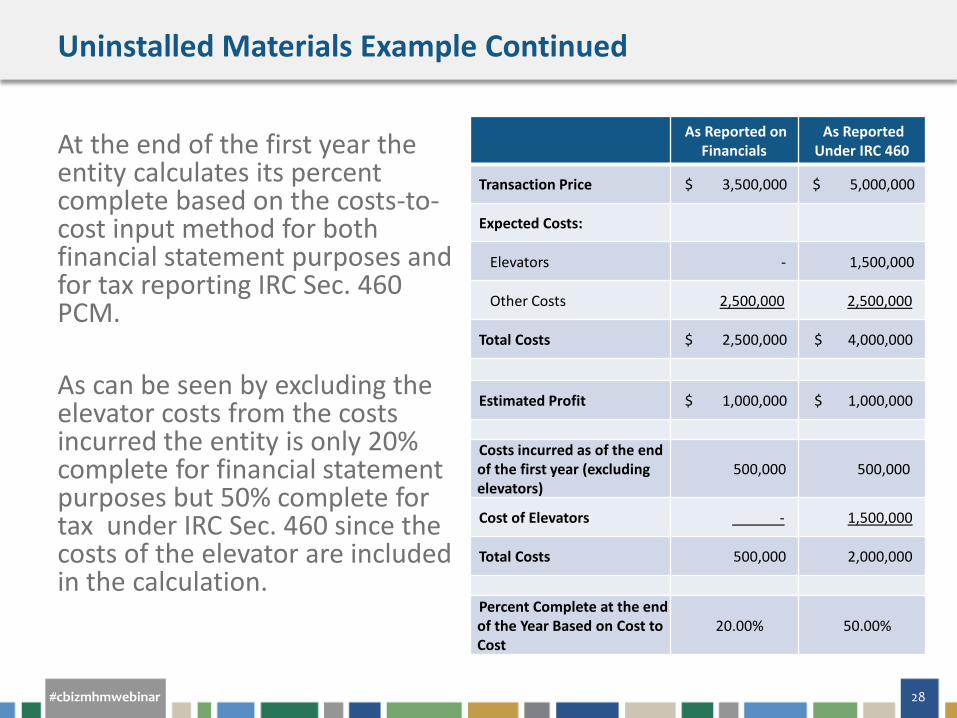

At the end of the first year the entity calculates its percent complete based on the costs-to-cost input method for both financial statement purposes and for tax reporting IRC Sec. 460 PCM. As can be seen by excluding the elevator costs from the costs incurred the entity is only 20% complete for financial statement purposes but 50% complete for tax under IRC Sec. 460 since the costs of the elevator are included in the calculation.

As Reported on Financials

As Reported Under IRC 460

Transaction Price $ 3,500,000 $ 5,000,000

Expected Costs:

Elevators - 1,500,000

Other Costs 2,500,000 2,500,000

Total Costs $ 2,500,000 $ 4,000,000

Estimated Profit $ 1,000,000 $ 1,000,000

Costs incurred as of the end of the first year (excluding elevators)

500,000 500,000

Cost of Elevators - 1,500,000

Total Costs 500,000 2,000,000

Percent Complete at the end of the Year Based on Cost to Cost

20.00% 50.00%

#cbizmhmwebinar 29

Uninstalled Materials Example Continued

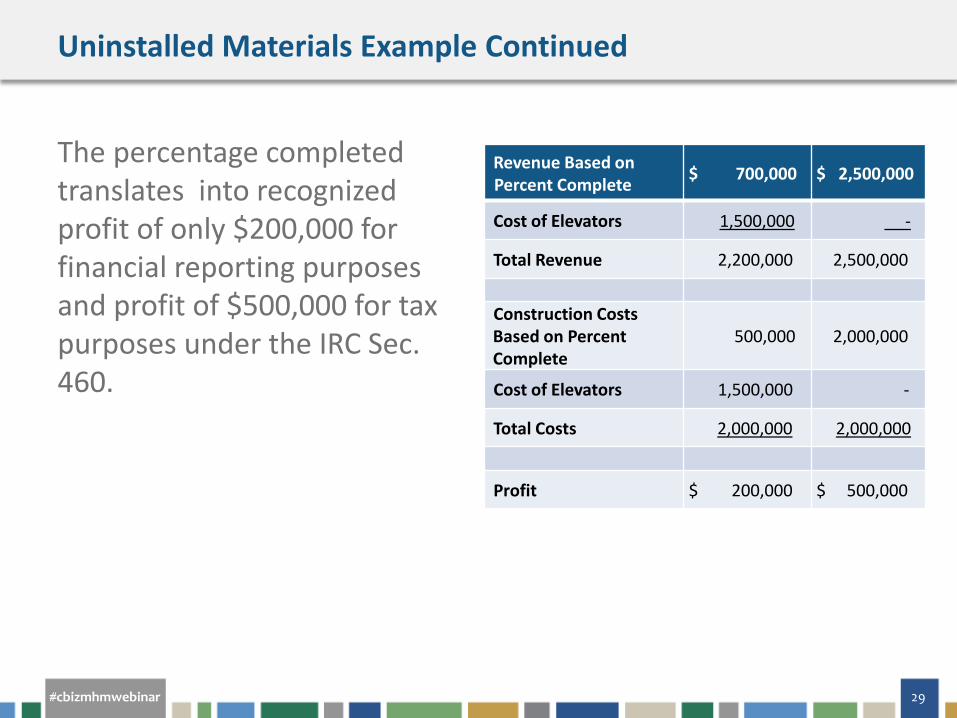

The percentage completed translates into recognized profit of only $200,000 for financial reporting purposes and profit of $500,000 for tax purposes under the IRC Sec. 460.

Revenue Based on Percent Complete $ 700,000 $ 2,500,000

Cost of Elevators 1,500,000 -

Total Revenue 2,200,000 2,500,000

Construction Costs Based on Percent Complete

500,000 2,000,000

Cost of Elevators 1,500,000 -

Total Costs 2,000,000 2,000,000

Profit $ 200,000 $ 500,000

#cbizmhmwebinar 30

Recent Tax Developments Impacting the Architecture/Engineering/Construction

Industries

Proposed Regs on Sec. 199 Domestic Production Activities Deduction

#cbizmhmwebinar 31

Proposed Regs on IRC Sec. 199

• IRS issued proposed regulations on 8/26/15 • would apply to tax years beginning on or after the date the

final regs are published

• covers a wide range of topics including several affecting taxpayers in the construction industry as follows: • new definition of “substantial renovation” • revised definition of general contractor activities • new rule with multiple building projects • allocating contract costs for L-T contracts

#cbizmhmwebinar 32

Proposed Regs on IRC Sec. 199

• Brief Background on the Deduction • Taxpayers may claim a deduction to offset income from

domestic manufacturing and other domestic production activities equal to 9% of the smaller of the taxpayer’s • qualified production activities income (QPAI), or • taxable income (determined without regard to the 199 deduction)

• The deduction can not exceed 50% of the W-2 wages of the employer

#cbizmhmwebinar 33

Proposed Regs on IRC Sec. 199

• New Definition of Substantial Renovation • The existing regs define construction activities as those

performed in connection with a project to erect or substantially renovate real property

• Currently “substantial renovation” is defined to mean renovation of a major component or substantial structural part of real property that • materially increases the value of the property, • substantially prolongs the useful life of the property, or • adapts the property to a new or different use

#cbizmhmwebinar 34

Proposed Regs on IRC Sec. 199

• New Definition of Substantial Renovation - continued

• The proposed regs would revise the definition of to conform to the capitalization requirements under the new tangible property regulations

• The revised 263 regs defines the capitalization rules for improvements for a unit of property: • Betterments • Adaptions to a new of different use • Restorations

• New definition could limit what qualifies for DPAD

#cbizmhmwebinar 35

Proposed Regs on IRC Sec. 199

• Revised Definition of General Contractor Activities • Construction activities as defined by the current regs

include the activities performed by a general contractor or activities typically performed by a general contractor

• Under the proposed regs a taxpayer whose only engagement in the activity is primarily limited to approving or authorizing invoices or payments is not considered engaged in a construction activity as a general contractor

#cbizmhmwebinar 36

Proposed Regs on IRC Sec. 199

• New Rule for Multiple Building Projects • Under the existing regs a taxpayer can use any reasonable

method based on all of the facts and circumstances to determine what construction activities constitute an item of DPGR

• However, the IRS has concluded that treating gross receipts from the sale of a multiple building project as one item is not a reasonable method if the taxpayer did not substantially renovate each building in the project

#cbizmhmwebinar 37

Proposed Regs on IRC Sec. 199

• Allocating Cost of Goods Sold with LT Contracts • Current regs describe how a taxpayer determines its CGS

allocable to DPGR – but doesn't address long-term contracts

• The proposed regulations would add that in the case of transactions accounted for under a long-term contract method of accounting (either PCM or CCM) CGS for this section would include allocable contract costs under IRC Sec. 460

#cbizmhmwebinar 38

Proposed Regs on IRC Sec. 199

• New Rules - Contracted Manufacturing Activities • The existing regs have a “benefits and burdens of

ownership” test to prevent more than one taxpayer from being allowed the deduction

• The proposed regs would replace the benefits and burdens test for a new rule that would only allow the party that performs the qualifying activity under the contract the deduction

• This rule would not apply to construction contracts – both GC and Subs can take the deduction

#cbizmhmwebinar 39

Other Hot Topics for Contractors

RECENT TAX DEVELOPMENTS IMPACTING THE ARCHITECTURE/ENGINEERING/CONSTRUCTION

INDUSTRIES

#cbizmhmwebinar 40

Other Hot Topics for Contractors

• Accounting Methods for Long-Term Contracts • Make sure you are using the correct method • Large contractors vs. small contractors as defined in IRC Sec.

460 • No 3115 required if small contractors average gross receipts

exceed $10M • January 2015 – IRS released advanced consent methods -

now change to PCM from a wrong method is automatic • Cash method taxpayer going over the $10M threshold can

now elect accrual and PCM at same time • PCCCM for residential contracts • 10% Complete Method

#cbizmhmwebinar 41

Other Hot Topics for Contractors

• Retention (Retainage) • Change from overall accrual method to accrual less

retention method - automatic change – benefits: • small subcontractors exempt from PCM, and • large subcontractors with contracts completed during the year (non

long-term contracts)

• Exclusion of retention payables for large general contractors using PCM – non-automatic change • Must be able to prove that the retainage amount is not deductible

until the “all events” test is met – i.e. the contract terms with the subcontractor are clear that retention is not payable until full acceptance and completion of the job has occurred

#cbizmhmwebinar 42

Other Hot Topics for Contractors

• 2008 Proposed Regs on Home Construction Contracts • Would expand the types of contracts that would qualify as

home construction contracts by specifically stating that common improvements qualify even if the contract is not for construction of any dwelling units

• Effective for tax years beginning on or after the regulations are finalized

• The preamble to the prosed regulations indicates that the IRS and Treasury are also expecting to propose specific severing and completion rules for home construction contracts accounted for using the CCM

#cbizmhmwebinar 43

Other Hot Topics for Contractors

• Per Diems • Still subject to 50% limitation even though allocated to job

costs • IRS is still questioning the percentage allocated to meals –

lodging only per diems are not allowed • Must have an accountable plan for lodging expenses

otherwise entire per diem could be attributable to meals and subject to the 50% limitation

• Employers that pay less than applicable federal rate can make an election to allocate 40% to the M&IE portion

• Per IRS regs issued in 2013 contractor can have customer reimburse them for the workers per diem expenses – customer bears the 50% limitation – works great for governmental or not-for-profit customers

#cbizmhmwebinar 44

Other Hot Topics for Contractors

• Other Issues • Taxpayers using incorrect interest rates in Look-Back

calculation – may get proposed regulations eliminating look-back for contracts completed within two years

• R & E Credits – IRS knows this is a huge area right now for the construction industry – all cases are assigned to IRS engineers and evaluated on a case by case basis – IRS has also increased audits

#cbizmhmwebinar 45

? QUESTIONS

#cbizmhmwebinar 46

If You Enjoyed This Webcast…

Upcoming Courses: • 12/8 & 12/11:Lobbying and Political Activity Guidance for 501(c)(3) Organizations

• 12/10: Revenue Recognition Update for the Technology Industry

• 12/17: What's New at the PCAOB and SEC?

• 1/7 & 1/14: Fourth Quarter Accounting and Financial Reporting Issues Update

Recent Thought Leadership: • U.S. Partnerships Owned by Canadians May Have an Unexpected Filing Requirement

• 6 End-of-Year Money Moves to Help Boost Your Net Worth

• Tennessee Enacts Tax Reform Measures

• Substantiation Changes Proposed to Charitable Contribution Returns

• The Implications of Debt-Financed Distributions

#cbizmhmwebinar 47

Connect with Us

linkedin.com/company/ mayer-hoffman-mccann-p.c.

@mhm_pc

youtube.com/ mayerhoffmanmccann

slideshare.net/mhmpc

linkedin.com/company/ cbiz-mhm-llc

@cbizmhm

youtube.com/ BizTipsVideos

slideshare.net/CBIZInc

MHM CBIZ