Embed Size (px)

Citation preview

HDFC HUL ITC SBI TCS

1,073.90 0.47 % 741.25 0.91 % 355.15 0.79 % 2460.45 V - 1.70 % 2524.60 + 5.05 + 6.65 + 2.80 -42.55

S&P BSE SENSEX

1

For the premier Bombay Stock Exchange that pioneered the stock broking activity in India, 135 years of experience seems to be a proud milestone. A lot has changed since 1875 when 318 persons became members of what today is called The Stock Exchange, Mumbai by paying a Princely amount of Re. 1.

Since then, the country's capital markets have passed through both good and bad periods. The journey in the 20th century has not been an easy one. Till the decade of eighties, there was no scale to measure the ups and downs in the Indian stock market. The Stock Exchange, Mumbai in 1986 came out with a stock index that subsequently became the barometer of the Indian stock market.

Sensex is not only scientifically designed but also based on globally accepted construction and review methodology. First compiled in 1986, Sensex is a basket of 30 constituent stocks representing a sample of large, liquid and representative companies.

The base year of Sensex is 1978-79 and the base value is 100. The index is widely reported in both domestic and international markets through print as well as electronic media.

The Index was initially calculated based on the "Full Market Capitalization" methodology but was shifted to the free-float methodology with effect from September 1, 2003. The "Free-float Market Capitalization" methodology of index construction is regarded as an industry best practice globally. All major index providers like MSCI, FTSE, STOXX, S&P and Dow Jones use the Free-float methodology.

Due to is wide acceptance amongst the Indian investors; Sensex is regarded to be the pulse of the Indian stock market. As the oldest index in the country, it provides the time series data over a fairly long period of time (From 1979 onwards). Small wonder, the Sensex has over the years become one of the most prominent brands in the country.

The growth of equity markets in India has been phenomenal in the decade gone by. Right from early nineties the stock market witnessed heightened activity in terms of various bull and bear runs. The Sensex captured all these events in the most judicial manner.

S&P BSE Sensex

2

Sensex is calculated using the "Free-float Market Capitalization" methodology. As per this methodology, the level of index at any point of time reflects the Free-float market value of 30 component stocks relative to a base period. The market capitalization of a company is determined by multiplying the price of its stock by the number of shares issued by the company. This market capitalization is further multiplied by the free-float factor to determine the free float market capitalization.

The base period of Sensex is 1978-79 and the base value is 100 index points. This is often indicated by the notation 1978-79=100. The calculation of Sensex involves dividing the Free-float market capitalization of 30 companies in the Index by a number called the Index Divisor.

The Divisor is the only link to the original base period value of the Sensex. It keeps the Index comparable over time and is the adjustment point for all Index adjustments arising out of corporate actions, replacement of scrips etc. During market hours, prices of the index scrips, at which latest trades are executed, are used by the trading system to calculate Sensex every 15 seconds and disseminated in real time.

Understanding Free Float Methodology

Free-float Methodology refers to an index construction methodology that takes into consideration only the free-float market capitalisation of a company for the purpose of index calculation and assigning weight to stocks in Index. Free-float market capitalization is defined as that proportion of total shares issued by the company that are readily available for trading in the market.

It generally excludes promoters' holding, government holding, strategic holding and other locked-in shares that will not come to the market for trading in the normal course. In other words, the market capitalization of each company in a Free-float index is reduced to the extent of its readily available shares in the market.

In India, BSE pioneered the concept of Free-float by launching BSE TECk in July, 2001 and Bank Ex in June, 2003. While BSE TECk Index is a TMT benchmark, BankEx is positioned as a benchmark for the banking sector stocks. Sensex becomes the third index in India to be based on the globally accepted Free-float Methodology.

Calculation of Sensex

03

Suppose the Index consists of only 2 stocks:

Stock A and Stock B.

Suppose company A has 1,000 shares in total, of which 200 are held by the promoters, so that only 800 shares are available for trading to the general public. These 800 shares are the so-called 'free-floating' shares.

Similarly, company B has 2,000 shares in total, of which 1,000 are held by the promoters and the rest 1,000 are free-floating.

Now suppose the current market price of stock A is Rs.120. Thus, the 'total' market capitalisation of company A is Rs.120,000 (1,000 x 120), but its free-float market capitalisation is Rs.96,000 (800 x 120).

Similarly, suppose the current market price of stock B is Rs.200. The total market capitalisation of company B will thus be Rs.400,000 (2,000 x 200), but its free-float market cap is only Rs.200,000 (1,000 x 200).

So as of today the market capitalisation of the index (i.e. stocks A and B) is Rs.520,000 (Rs.120,000 + Rs.400,000); while the free-float market capitalisation of the index is Rs.296,000. (Rs.96,000 + Rs.200,000).

The year 1978-79 is considered the base year of the index with a value set to 100.

What this means is that suppose at that time the market capitalisation of the stocks that comprised the index then was, say, 60,000 (remember at that time there may have been some other stocks in the index, not A and B, but that does not matter), then we assume that an index market cap of 60,000 is equal to an index-value of 100.

Thus the value of the index today is = 296,000 x 100/60,000 = 493.33

This is how the Sensex is calculated.

The factor 100/60000 is called index divisor.

Example

04

The Scrip Selection Criteria for S&P BSE SENSEX

The general guidelines for selection of constituents in S&P BSE SENSEX are as follows:

Equities of companies listed on Bombay Stock Exchange Ltd. (excluding companies classified in Z group, listed mutual funds, scrips suspended on the last day of the month prior to review date, scrips objected by the Surveillance department of the Exchange and those that are traded under permitted category) shall be considered eligible.

Listing History: The scrip should have a listing history of at least three months at BSE. An exception may be granted to one month, if the average free-float market capitalization of a newly listed company ranks in the top 10 of all companies listed at BSE. In the event that a company is listed on account of a merger / demerger / amalgamation, a minimum listing history is not required.

The scrip should have been traded on each and every trading day in the last three months at BSE. Exceptions can be made for extreme reasons like scrip suspension etc.

Companies that have reported revenue in the latest four quarters from its core activity are considered eligible.

From the list of constituents selected through Steps 1-4, the top 75 companies based on free-float market capitalisation (avg. 3 months) are selected as well as any additional companies that are in the top 75 based on full market capitalization (avg. 3 months).

The filtered list of constituents selected through Step 5 (which can be greater than 75 companies) is then ranked on absolute turnover (avg. 3 months).

Any company in the filtered, sorted list created in Step 6 that has Cumulative Turnover of >98%, are excluded, so long as the remaining list has more than 30 scrips.

The filtered list calculated in Step 7 is then sorted by free float market capitalization. Any company having a weight within this filtered constituent list of <0.50% shall be excluded.

All remaining companies will be sorted on sector and sub-sorted in the descending order of rank on free-float market capitalization.

Industry/Sector Representation: Scrip selection will generally attempt to maintain index sectoral weights that are broadly in-line with the overall market.

Track Record: In the opinion of the BSE Index Committee, all companies included within the S&P BSE SENSEX should have an acceptable track record.

05

What causes Stock prices to change?

Stock prices change every day as a result of market forces. This means that share prices change because of supply and demand. If more people want to buy a stock (demand) than sell it (supply), then the price moves up. Conversely, if more people wanted to sell a stock than buy it, there would be greater supply than demand, and the price would fall. Understanding supply and demand is easy. What is difficult to comprehend is what makes people like a particular stock and dislike another stock. This comes down to figuring out what news is positive for a company and what news is negative. There are many answers to this problem and just about any investor you ask has their own ideas and strategies.

The principal theory is that the price movement of a stock indicates what investors feel a company is worth. The price of a stock doesn't only reflect a company's current value, it also reflects the growth that investors expect in the future.

Earnings are what affect investors' valuation of a company, but there are other indicators that investors use to predict stock price. Remember, it is investors' sentiments, attitudes and expectations that ultimately affect stock prices.

The most important factor that affects the value of a company is its earnings. Earnings are the profit a company makes, and in the long run no company can survive without them. If a company never makes money, it isn't going to stay in business. Public companies are required to report their earnings four times a year (once each quarter).

Investors & analyst watch with great attention at these times, which are referred to as earnings seasons. The reason behind this is that analysts base their future value of a company on their earnings projection. If a company's results surprise (are better than expected), the price jumps up. If a company's results disappoint (are worse than expected), then the price will fall.

It's not just earnings that can change the sentiment towards a stock (which, in turn, changes its price). During the dotcom bubble, for example, dozens of internet companies rose to have market capitalizations in the billions of dollars without ever making even the smallest profit. As we all know, these valuations did not hold, and most internet companies saw their values shrink to a fraction of their highs. Still, the fact that prices did move that much demonstrates that there are factors other than current earnings that influence stocks.

Investors have developed literally hundreds of these variables, ratios and indicators. Some you may have already heard of, such as the price earnings ratio, while others are extremely complicated and obscure with names like Chaikin Oscillator or Moving Average Convergence Divergence.

06

The Bombay Stock Exchange developed the BSE SENSEX in 1986, giving the BSE a means to measure overall performance of the exchange. In 2000, the BSE used this index to open its derivatives market, trading SENSEX future contacts. The development of SENSEX option along with equity derivatives followed in 2001 and 2002, expanding the BSE‟s trading platform. Historically an open-cry floor trading exchange, the Bombay Stock Exchange switched to an electronic trading system in 1995.

The growth of the equity market in India has been phenomenal in the present decade. Right from early nineties, the stock market witnessed heightened activity in terms of various bull and bear runs. In the late nineties, the Indian market witnessed a huge frenzy in the 'TMT' sectors. More recently, real estate caught the fancy of the investors. S&P BSE SENSEX has captured all these happenings in the most judicious manner. One can identify the booms and busts of the Indian equity market through S&P BSE SENSEX. As the oldest index in the country, it provides the time series data over a fairly long period of time (from 1979 onwards). Small wonder, the S&P BSE SENSEX has become one of the most prominent brands in the country.

Here is a timeline on the rise of the SENSEX through Indian stock market history.

SENSEX TIMELINE

25/07/1990

SENSEX touched 1000 points for the first time

15/01/1992

SENSEX touched 2000 points

29/02/1992

SENSEX touched 3000 points

30/03/1992

SENSEX touched 4000 points

11/10/1999

SENSEX touched 5000 points

11/02/2000

SENSEX touched 6000 points

21/06/2005

SENSEX touched 7000 points

08/09/2005

SENSEX touched 8000 points

09/12/2005

SENSEX touched 9000 points

07/02/2006

SENSEX touched 10000 points

27/03/2006

SENSEX touched 11000 points

20/04/2006

SENSEX touched 12000 points

30/10/2006

SENSEX touched 13000 points

05/12/2006

SENSEX touched 14000

06/07/2007

SENSEX touched 15000 points

19/09/2007

SENSEX touched 16000 points

26/09/2007

SENSEX touched 17000 points

09/10/2007

SENSEX touched 18000 points

History of S&P BSE Sensex

1

Biggest falls

15/10/2007

SENSEX touched 19000 points

11/12/2007

SENSEX touched 20000 points

05/11/2010

SENSEX touched 21000 points

24/03/2014

SENSEX touched 22000 points

09/05/2014

SENSEX touched 23000 points

13/05/2014

SENSEX touched 24000 points

16/05/2014

SENSEX touched 25000 points

07/07/2014

SENSEX touched 26000 points

02/02/2014

SENSEX touched 27000 points

21/01/2008

SENSEX fall by 1408 points

24/10/2008

SENSEX fall by 1070 points

17/03/2008

SENSEX fall by 951 points

03/03/2008

SENSEX fall by 900 points

21/01/2008

SENSEX fall by 875 points

08

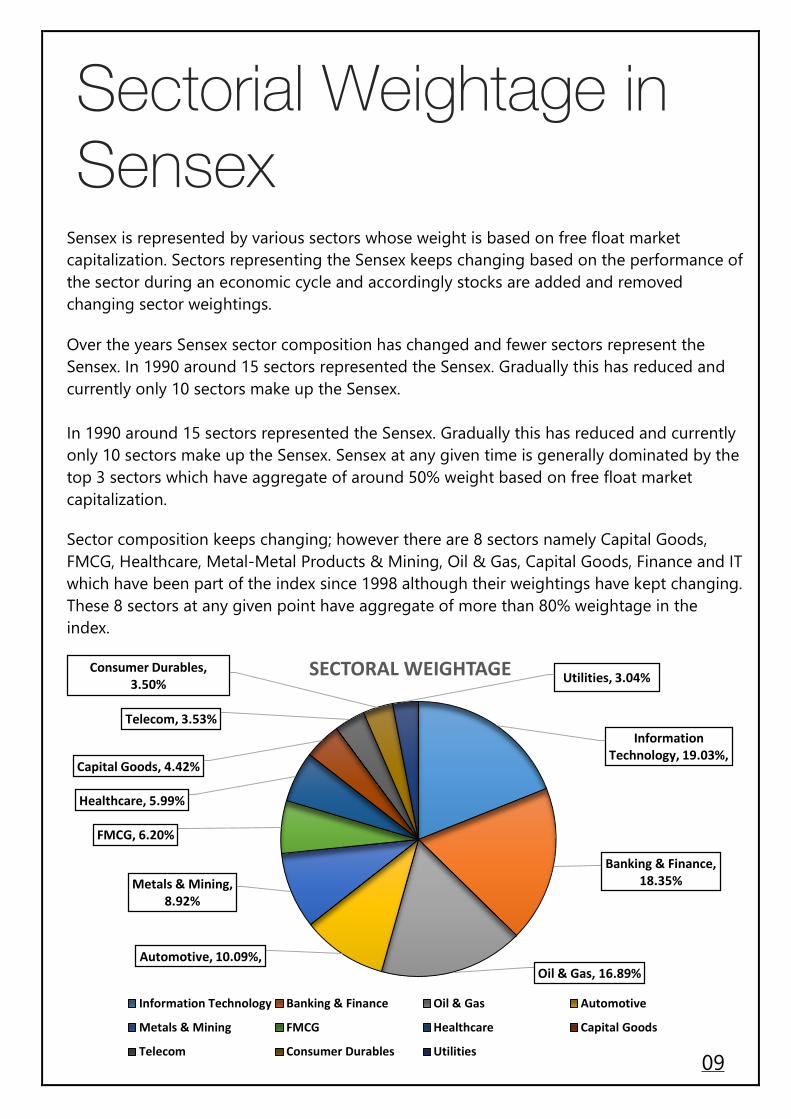

Sensex is represented by various sectors whose weight is based on free float market capitalization. Sectors representing the Sensex keeps changing based on the performance of the sector during an economic cycle and accordingly stocks are added and removed changing sector weightings.

Over the years Sensex sector composition has changed and fewer sectors represent the Sensex. In 1990 around 15 sectors represented the Sensex. Gradually this has reduced and currently only 10 sectors make up the Sensex.

In 1990 around 15 sectors represented the Sensex. Gradually this has reduced and currently only 10 sectors make up the Sensex. Sensex at any given time is generally dominated by the top 3 sectors which have aggregate of around 50% weight based on free float market capitalization.

Sector composition keeps changing; however there are 8 sectors namely Capital Goods, FMCG, Healthcare, Metal-Metal Products & Mining, Oil & Gas, Capital Goods, Finance and IT which have been part of the index since 1998 although their weightings have kept changing. These 8 sectors at any given point have aggregate of more than 80% weightage in the index.

Sectorial Weightage in Sensex

Information Technology, 19.03%,

Banking & Finance, 18.35%

Oil & Gas, 16.89%Automotive, 10.09%,

Metals & Mining, 8.92%

FMCG, 6.20%

Healthcare, 5.99%

Capital Goods, 4.42%

Telecom, 3.53%

Consumer Durables, 3.50% Utilities, 3.04%SECTORAL WEIGHTAGE

Information Technology Banking & Finance Oil & Gas Automotive

Metals & Mining FMCG Healthcare Capital Goods

Telecom Consumer Durables Utilities 09

The weightage of a company in the Sensex or Nifty depends on its free-float m-cap. It is a percentage of the total market capitalisation of the index. So, if the market capitalisation of a company is Rs.1 crore, while that of the index if Rs.200 crore, its stock has a weightage of 0.5%. For this reason, higher the free-float m-cap of a company, greater is its weightage on the index. Also, the more the public-holding, the higher will be the free float market capitalisation.

Suppose, today the value of Sensex is 20,000 and a company like TCS holds a weightage of 10%, this means, TCS’s value as a portion of the Sensex is 2000. So, if TCS’ share price increases by 5%, its value of 2000 will also rise by the same percentage to 2100. As a result, the Sensex will also rise by 100 points.

Many investment firms also follow weightages of stocks and also allocate funds the same way. So, for example, if the weightage of a company drops in the Sensex, the percentage of total funds being allocated will also fall. (The values given in the following pie diagram are rounded off)

The Weightage of 30 SENSEX Constituent Companies

Sensex Composition

Axis Bank1%

Bajaj Auto2%

Bharti Airtel2%

Bhel1%

Cipla1%

Coal India1%

Dr. Reddy's Lab2%

GAIL1%

HDFC7%

HDFC BANK7%

HERO Motocorp1%

HUL3%

Hindalco1%

ICICI Bank7%

Infosys9%ITC

11%

L&T4%

M&M2%

Maruti Suzuki1%

NTPC2%

ONGC4%

RELIANCE IND.9%

SBI3%

SESA STERLITE2%

SUN PHARMA3%

TATA MOTORS4%

TATA POWER1%

TATA STEEL1%

TCS7%

WEIGHT

Axis Bank Bajaj Auto Bharti Airtel Bhel Cipla Coal India

Dr. Reddy's Lab GAIL HDFC HDFC BANK HERO Motocorp HUL

Hindalco ICICI Bank Infosys ITC L&T M&M

Maruti Suzuki NTPC ONGC RELIANCE IND. SBI SESA STERLITE

SUN PHARMA TATA MOTORS TATA POWER TATA STEEL TCS 10

While ITC’s cigarette division continues to clock healthy growth, its improving profitability in the non-cigarette businesses is driving earnings. Despite a hike in excise duty of cigarettes it has witnessed volume growth.

ITC is planning to enter the lucrative dairy market much of which is unorganised. The move is part of ITC’s diversification strategy. Before this, the companies’ last move was to venture into the consumer goods business, which has successfully paved off.

Business Segments

ITC remains one of the high conviction buys, given the strong resilience in its core cigarette business.

ITC is set to foray into the dairy segment with value-added products like ghee and milk powder being the preliminary offerings. The launch of ghee would be pan-India but powdered milk would be initially used in house by the company for its other FMCG products. The company plans to set up six plants across the country for its dairy business. ITC's constant extension into new FMCG segments over the years has been led by the company's intention to reduce its dependence on cigarettes (facing extensive tax and government regulations hampering volume growth in cigarettes).Though profitability from the FMCG

segment would be gradual, the company's strong distribution and sourcing network would aid in building a strong presence across the segments in which it enters.

ITC BUY

₹ 359

Cigarettes & Cigars

Packaging & Printing

Education & Stationary

Hotels

Personal Care

Foods

Broker Reports

BUY 10

HOLD 4

SELL 2

SENSEX WEIGHT

10.75%

The price & data indicated is as on date 19/09/2014

INDIVIDUAL STOCK ANALYSIS OF 30 SENSEX CONSTITUENT COMPANIES

11

After his sensational return to the company he co-founded, N R Narayana Murthy has displayed typical zeal in setting the house in order along with newly appointed CEO Vikas Sikka. To improve employee morale, Infosys has announced salary increments. A return to the company’s earlier PSPD model (predictability, sustainability, profitability & de-risking) is expected as the company strives to improve operational performance.

While the problem of crisis of leadership may have been solved, it will be some time before the management changes are reflected in numbers.

Business Segments

Infosys has been volatile largely because of the changes in management. It has strengthened its relationship with BP by extending its agreement with the global oil major by another five years, in particular application support and development. It has to redevelop a new growth strategy and execute.

One thing that you might want to consider is that the IT sector remains a sector where though the growth is slower than what it used to be in the past but it is still growing. It will still have the tailwinds of the rupee behind it and of course they remained cash surplus. So in a market which may suddenly due to global pressure may turn negative, stocks like Infosys will remain

stable.

Infosys HOLD

₹3,702

Business Services

Technology Services

Outsourcing Services

Broker Reports

BUY 5

HOLD 4

SELL 3

SENSEX WEIGHT

9.16 %

The price & data indicated is as on date 19/09/2014

12

Though there is a risk of timing, Reliance Industries is going to be the biggest beneficiary of the recent natural gas price reform. The Indian rupee’s depreciation & improving refining margins are going to be the other drivers of its earnings.

Analysts have already started upgrading their earnings estimates for the financial year 2015-16. The upgrades are in the range of 15-16%.

Business Segments

Reliance Industries is considering investing about $13 billion to build new projects, including a 400,000 barrels per day refinery at its Jamnagar complex to boost profit by processing cheap, heavy grades.

RIL will save about $450 million annually by importing 1.5 million tonnes of ethane from US for its petrochemical plant, according to a report. Imported ethane will substitute its current propane imports and a portion of naphtha used for ethylene production. It is set to start selling diesel from over 1,400 petrol pumps across India from October this year.

RIL has planned to invest $2 billion (around Rs.12,000 crore) in its three shale assets in the US, betting big on the potential of extracting natural gas and oil from the sedimentary rock formations. RIL has also made an investment of USD 70 million in a wholly owned subsidiary (WOS) in the UAE.

RIL BUY

₹ 995

Oil & Gas Exploration &

Production

Petroleum Refining &

Marketing

Petrochemicals

Textile

Retail

Broker Reports

BUY 20

HOLD 6

SELL 2

SENSEX WEIGHT

9.13%

The price & data indicated is as on date 19/09/2014

13

The June marked the 58th consecutive quarter of over 20% year on year growth in net profit for HDFC Bank. Yet, its stock had been languishing perhaps because of its high valuation and the prolonged economic slowdown until last year. This despite the fact that the bank remains best in class in terms of core parameters like earnings, growth, asset quality, high NIM, high CASA & high return ratios.

However, anlysts are of the view that most of the positives are already factored into the stock’s price, which leaves little room for an upside. The opinion can certainly change if the merger with HDFC comes to picture.

Business Segments

Personal Banking

Private Banking

Corporate Banking

SME Banking

Wholesale Banking

DEMAT Services

HDFC Bank, India's second-largest private sector lender by revenue, is planning a renewed push into the country's vast rural hinterland, and expects its non-urban operations to become profitable by 2016.

The fortunes are closely watched by international fund managers given its reputation for asset quality and technological innovation, and their investments have made the bank India's largest by market capitalisation.

The retail loans accelerated at the fastest pace of 14.5% year on year during the period, while loans to industry expanded 10%. The loans to services increased 12% to during the same period and farm loans expanded 7.6%.

HDFC Bank's deteriorating asset quality continues to pose a major challenge. As the company, aiming at rapid expansion, stretches to meet growth targets and takes on new loans that are better to avoid, it often leads to asset quality deterioration. With the bank further expanding its reach, we believe that this trend will likely persist going forward.

HDFC BANK

₹ 855

Broker Reports

BUY 8

SELL 3

BUY

SENSEX WEIGHT

7.22%

The price & data indicated is as on date 19/09/2014

14

HDFC continues to be the disputed leader among the housing finance companies. The other factors that attract long term investors to this counter include its operational excellence demonstrated over several decades, sustainable revenue & net profit growth & high asset quality. Despite its big size, HDFC’s base is expected to grow by more than 20% in the coming years as well.

Though spreads within the sector may get squeezed in the medium term due to the problems faced by the housing sector, HDFC is well positioned to defend its margins due tto its wider reaach & size. However, there is not much upside in the medium term in this counter as the valuation is high. For long term perspective, it is a definite buy.

Business Segments

The easing of lending & reserve regulations by The Reserve Bank of India has been beneficial for HDFC. Investors are wagering that HDFC Bank Ltd and Housing Development Finance Corp. Ltd (HDFC) will pursue a megamerger that would deliver returns unmatched by any peer. A merger would allow HDFC Bank to offer financial services to 4.8 million home-loan customers gained from the combination, while deposits at its 3,500 branches could help fund rising demand for mortgages. The new entity would boast the largest capital buffer of any major bank. It will be a bank with high capitalization and very high return-on-equity.

HDFC

₹1,066

Property Lending

Mortgages

General Insurance

Life Insurance

Mutual Funds

Broker Reports

BUY 9

SELL 2

SENSEX WEIGHT

7.19%

BUY

The price & data indicated is as on date 19/09/2014

15

Despite the likely impact of the anticipated US Immigration Bill, the Indian IT’s strongest player is expected to continue to do well in the future as well. Since the bill will have significant impact if passed in the current form, TCS has already started concentrating on newer opportunities (under penetrated geographies & new technologies).

Tata Consultancy Services being the biggest Indian IT player, TCS is benefiting from from the ongoing US ecnomic revival. It is also expected to benefit in a big way from the rupees depreciation. With TCS being the market’s favourite, its valuation is a little stretched at the current levels.

Business Segments

Despite rising revenues from India, TCS remains cautious on the domestic segment saying it is waiting for "more broad-based confidence" to come back.

However, in certain states like Telangana, TCS is in an expansion mode and plans to add another 28,000 jobs to the existing 26,000 soon.

Technology budgets of large American corporations are expected to increase in 2015, with the proportion of outsourcing spends set to grow even faster as the world's largest economy stabilises, the US is the largest market for the company, fetching over 50% of its sales.

TCS in an expansion move has opened Saudi Arabia's first all-female BPO centre, which will provide employment to up to 3,000 women in three years.

TCS HOLD

₹ 2,715

Application Development & Maintenance

Asset Leverage Solution

Assurance Services

Business Process Management/Outsourcing

Consulting

IT infrastructure services

Enterprise Data Management & Integration Services

Technological Engineering & Industrial Services

Broker Reports

BUY 6

HOLD 5

SELL 1

SENSEX WEIGHT

6.85%

The price & data indicated is as on date 19/09/2014

16

For the past few quarters, ICICI Bank has been churning out very good numbers despite a slowdown in the economy. It has shown improvement in operating performance & a pick-up in retail business growth.

In the future, net interest margin is expected to further improve by almost 300 bps over financial years 2011-13 & is expected to expand due to the healthy performance by subsidiaries, mainly general insurance. The stock appears attractively price at current levels & should give a reasonable upside given the ongoing expansion.

Business Segments

ICICI Bank will take ahead its financial inclusion strategy, is planning to add another 1.5 million bank accounts in this financial year. In the last financial year, more than 75 percent of ICICI Bank's new branches were added in the rural and semi-urban areas. And as on now, about 52 per cent of the bank's overall branch network is in rural areas.

Apart from expanding the branch network, the bank has also been expanding its ATM network in the hinterland and currently has over 2,200 ATMs in semi urban and rural areas. As a result of these measures, in the last financial year, bank's rural portfolio has grown by 50 per cent.

ICICI Bank, through its Dubai branch, has sold five-and-half year fixed rate notes for an aggregate principal amount of $500 million (Rs.3000 crore).

ICICI BANKBUY

₹1,570

Personal Banking

Wealth Management

Corporate Banking

Privilege Banking

Business Services

Insurance

Broking, etc.

Broker Reports

BUY 14

HOLD 2

SELL 1

SENSEX WEIGHT

6.56%

The price & data indicated is as on date 19/09/2014

17

While it is reasonable for the market to punish weak counters from the infra sector, a strong player like L&T has also taken a beating. Many infrastructure players face a cash crunch. This is likely to help strong players like L&T expand at the cost of weaker competitors. Lower commodity prices will also help L&T improve its margins.

The company is expected to remain stable at current levels & generate positive returns for investors once the revival in capex takes place.

Business Segments

Larsen & Toubro (L&T) has bagged Rs.1885 crore contract from NTPC for setting up steam generators for Tanda Thermal Power Plant in Uttar Pradesh.

The company secured an offshore contract worth Rs.1340 crore from ONGC. In the onshore segment, L&T Hydrocarbon Engineering has secured a contract of Rs.580 crore from a leading company engaged in hydrocarbon downstream processing.

L&T, in a strategic move to strengthen its design base in the Infrastructure space, has acquired 50% of the stake in L&T-Ramboll Consulting Engineers Limited hitherto held by Ramboll Denmark AS. With this acquisition, LTR now becomes a wholly owned subsidiary of L&T. The company will continue to offer single point 'concept to commissioning' consultancy services for infrastructure projects like airports, roads, bridges, ports and maritime structure including environment, transport planning and other related

services.

Larsen & Tubro

₹1,535

Process Technology

Project Management

Construction

Detailed Engineering

Modular Fabrication

Commissioning

Procurement

Broker Reports

BUY 10

HOLD 2

SELL 3

SENSEX WEIGHT

4.34%

BUY

The price & data indicated is as on date 19/09/2014.

18

IN the auto sector, the commercial vehicles segment is the worst affected. Tata motors passenger vehicle segment is also under pressure.

Due to these factors, the company’s consolidated numbers may remain weak for a few more quarters despite Jaguar & Land Rover (JLR) good performance. In addition to the continued traction of the new Range Rover, JLR has a strong range of products for the nexxt two to three years. Among them, the launch of smaller segments, expected by the end of 2014, is going to be the most significant because it is expected to boost the sales.

Business Segments

Tata Motors reported 9.7 per cent decline in global sales at 73,524 units in August, 2014. Sales of luxury brand Jaguar Land Rover rose 2.44 per cent to 31,650 units in August as compared to 30,895 units in the same month last year. Sales of commercial vehicles declined 19.6 per cent in August to 30,536 units from 37,983 units a year ago. Jaguar Land Rover faced probes from China’s antitrust regulator, due to alleged monopolistic practices of inflating vehicle and spare parts prices. China probes possibly hurting profits, coupled with tepid sales outlook in the politically troubled Eastern Europe, weighed on automotive stocks, which performed weaker than broader indices.

Moody's Investors Service has recently upgraded ratings of Tata Motors, on account of Tata Sons' track record in providing timely support to the company. The agency upgraded corporate family ratings of Tata Motors to Ba2/Stable from Ba3/Stable.

TATA MOTORS

₹ 520

Broker Reports

BUY 6

HOLD 6

SELL 2

Car & Utility Vehicles

Trucks & Buses

Defence & Homeland Security Vehicles

Jaguar & Land Rover Luxury Cars

HOLD

SENSEX WEIGHT

4.03%

The price & data indicated is as on date 19/09/2014

19

The recent reforms like reduction in under recoveries due to regular increases in diesel price, and doubling of natural gas sector price from April, 2014 are god for the oil & gas sector as a whole. However, there are reports that ONGC may be asked to bear the same subsidy burden during the April- June period as well. Though, theoretically, ONGC will benefit from the gas price hike, the government will take it back in the form of higher oil subsidy share to bring down the fiscal deficit.

Barring government interference, ONGC is a very good investment for the long term, so existing investors should hold on to it & others should buy it.

Business Segments

ONGC's significant oil discovery in Bay of Bengal will begin production in 2019, with a peak output of 4.5 million tonnes a year, 20 percent more than previous estimates. The oil discovery in Krishna Godavari basin block KG-DWN-98/2 or KG-D5 will be the first large oil production from the east coast. The block also has 10 gas discoveries. Conservative estimates put the production at 75,000-plus bpd. Also, USD 6-6.5 per unit gas price hike for ONGC is expected from the centre. The company has invested Rs 81,890 crore in bringing on stream newer discoveries and arrest natural decline that has set in its ageing fields. However, there is a bit of a concern, since the cabinet has given nod to the sale of government’s stake in PSUs, this might lead to fall in prices in the short term.

ONGCBUY

₹ 405

Crude Oil Exploration

Natural Gas Exploration

& Production

Methane Extraction

LPG & Naptha

C2- C3

Broker Reports

BUY 8

HOLD 1

SENSEX WEIGHT

3.43%

The price & data indicated is as on date 19/09/2014

20

Sun Pharmaceuticals has grown by leaps & bounds from its humble beginning in 1983. Even so, it is expected to grow by around 20% in the next 1 year. To make its earnings stream more predictable, the company recently settled its ongoing litigation with Wyeth & Atland Pharma by making a lump sum payment of $ 550 million. With the litigation out of the way, the earnings growth will take centre stage in this counter. Since most of its earnings are in dollars, any further rupee depreciation will help the company.

However, its valuation has sky rocketed in the recent past. Therefore, in the medium term, the stock doesn’t hold much potential for upside gains from its current levels.

Business Segments

It entered into a licensing agreement with Merck for investigational therapeutic antibody Tildrakizumab to be used for treatment of chronic plaque psoriasis. Under terms of the agreement, Sun Pharma will acquire worldwide rights to Tildrakizumab for use in all human indications from Merck in exchange for an upfront payment of USD 80 million. Merck is eligible to receive undisclosed payments associated with regulatory (including product approval). On the other hand, the USFDA's has started surprise inspections at Sun Pharma's Halol facility in USA.

SUN PHARMA

₹ 359

Capsules

Tablets

Syrups

Ampoules

Vails

Pouch

Inhaler

Tube

Broker Reports

BUY 10

HOLD 4

SELL 2

SENSEX WEIGHT

2.94%

The price & data indicated is as on date 19/09/2014

HOLD

21

HUL’s shares surged to a record high recently after the company’s UK parent completed an open offer, raising its stake in the Indian unit by almost 15%. Given the sharp rally, most analyst fear a decline in its share piece in the near future. Besides, weak consumer sentiment is likely to keep a lid on volume growth. A weakening rupee also makes the imported raw materials costlier, which will put pressure on margins. However, a good monsoon would boost consumption in rural areas, which would improve margins.

In what clearly highlights the hectic pace at which the Indian consumer is evolving and the urgency with which marketers are trying to decipher their needs and cater to them to stay ahead of the curve, Hindustan Unilever has kicked off a new operating framework which deals in distinct consumer clusters that are expected to make the organization future ready.

Business Segments

Food & Drink

Personal Care

Home Care

Water Purifiers

Packaging

Health & Hygiene

Hindustan Unilever, having a diversified portfolio performed better during the last quarter. Their aggregate sales grew 16.5 per cent due to the price hikes to cover the increased cost of raw materials. However, the net profit grew at slower pace at 11.65 per cent, largely due to a 181 basis points increase in the raw material costs over the previous year's level.

HUL intends to build a strong e-commerce platform & use its retail distribution reach across the country to deliver products to consumers at their doorsteps with the kirana stores playing a key role in the project. HUL currently has a distribution reach of 3.2 million outlets across the country.

HUL

₹ 737

Broker Reports

BUY 2

HOLD 2

SELL 3

SELL

SENSEX WEIGHT

2.39%

The price & data indicated is as on date 19/09/2014

22

The State Bank of India is already going through a tough period of margin compression & asset quality concerns. These problems may continue for a few more quarters till the economy recovers. Moreover, the finance minister is now putting pressure on PSU banks to reduce lending rates, & some banks have yielded. Since the competition won’t allow banks to reduce their deposit rates simultaneously, margin pressure is going to increase.

Hence, the SBI’s immediate outlook is weak. Since most of these negatives have not affected the price much. Therefore, the long term investors may hold on to the stock.

Business Segments

State Bank of India has revised interest rates on retail term deposits below Rs.1 crore. The country's largest bank has cut the deposit rates for 1-3 years to 8.75 percent from 9 percent, while for the period of 180-210 days, it has hiked the rates to 7.25 percent from 7 percent. It also raised the deposit rate by 25 bps in the 180-210 days category to 7.25 per cent.

The credit rating agency Moody’s has recently given a downgrade rating to SBI. However, the bank says that the downgrade would not affect their expansion plans worldwide. The bank is set to open a branch in Saudi Arabia and one in Qatar from where opportunity of remittances is high. On an average 40-50 overseas branches shall be opened over next two years. On large scale SBI’s new branches shall be opened in Nepal, besides Australia, New Zealand, for which we have retail banking licenses.

SBI

₹ 2,568

Personal Banking

Agricultural/Rural Banking

Corporate Banking

International Banking

SME Finance

NRI Services

Broker Reports

BUY 3

HOLD 4

SELL 1

SENSEX WEIGHT

2.57%

The price & data indicated is as on date 19/09/2014

HOLD

23

The telecom company’s African operations continue to be a major drag on performance. Two years since it acquired the African business, revenue growth & margins remain weak. In the domestic market the company’s operations are growing, with both voice & data traffics growing at a decent pace.

However, regulatory issues pose a threat. Last quarter, a penalty of Rs.650cr. was slapped on the company for violating the country’s roaming norms. The prospect of more surcharges from the government, along with the upcoming license renewals, make the stock’s prospectus uncertain.

Business Segments

Bharti Airtel and Eaton Towers today announced an agreement for the divestment of over 3500 telecoms towers from Airtel to Eaton Towers.

However, the TRAI has objected to the structure of the Rs.700 crore Bharti Airtel-Loop Mobile deal, throwing continuation of mobile services to more than 3 million of the latter's subscribers into uncertainty with less than two months left before its permit in Mumbai expires. With regards to expansion, the company has launched its 3G service in African country Chad following recent award of license for high speed Internet services by the Chadian government. Also, it may have to spend Rs.436 crore for merging Airtel Broadband Services with itself towards differential spectrum cost and migration fee.

BHARTI AIRTEL HOLD

₹ 415

Mobile Teleservices, Internet, Landline, Digital TV, Airtel Money

Application tools for enterprise

Connectivity Solutions

ERP Solutions

VoIP Solutions

IT Infrastructure Services

Broker Reports

BUY 6

HOLD 3

SELL 1

SENSEX WEIGHT

2.38%

The price & data indicated is as on date 19/09/2014

24

Though the passenger vehicles segment is going through a difficult phase, Mahindra & Mahindra could compensate for it with improved tractor sales. Against a 13 % fall in the passenger vehicle segment in the June Quarter this year, on year on year basis. M&M’s tractor sales in the same month increased by 23 %.

Increased rural income & a good monsoon should help increase the demand for the tractors. M&M has changed the vehicles’ specifications to circumvent the additional tax imposed on SUVs. It is planning to launch four new vehicles in different vehicle segments by the end of this year.

Business Segments

The company will enter into a deal with the European automobile major — PSA Peugeot Citroen, for a tie-up in the scooter space. The deal revolves around sharing technology and a distribution tie-up across geographies, both in Europe and India and other emerging markets.

The company has also tied up with Snapdeal for online pre-bookings of the company's upcoming new version of SUV Scorpio, prior to its launch. The analysts & the broker houses believe that M&M is a good choice considering the estimates that show the automobile sector could likely see a turnaround in FY15.

M&MBUY

₹1,375

Personal Vehicles

Commercial Vehicles

Spares

Customization Services

Vehicular Mobility Services

Design Services

Broker Reports

BUY 10

HOLD 2

SENSEX WEIGHT

2.31%

The price & data indicated is as on date 19/09/2014

25

Though Wipro’s valuation is currently cheap compared with that of its peers, this is reasonable because of its lower growth rate & weaker margins. While Wipro is taking a number of correct steps like revamping sales team to increase the number of deals & moderating attrition by increasing employee satisfaction, the impact of these measures is not yet visible in revenue or net profit growth.

The guidance, given by Wipro’s management for the last quarter is however positive. This means that there may be an immediate trigger seen for this counter. Wipro’s expected recovery may get delayed to 2014-15. Since the stock is quoting at reasonable levels, existing investors should hold on to the stock & new investors should take a buy action.

Business Segments

Wipro Arabia, a subsidiary of IT firm Wipro, has bagged a contract from Saudi-based Saudi Electricity Company for implementing and rolling out plant maintenance and project system functionality of SAP ERP application. Wipro Arabia, a subsidiary of IT firm Wipro, has bagged a contract from Saudi-based Saudi Electricity Company for implementing and rolling out plant maintenance and project system functionality of SAP ERP application.

Wipro is enabling Muji, a leading retailer in Japan, to deliver a superior shopping experience through real-time insights into the buying behavior of its customers.

WIPRO

₹ 586

Analytics & Information Management

Infrastructure Management Services

Application & Cloud Services

Consulting Services

Product Engineering Solutions

Broker Reports

BUY 6

SENSEX WEIGHT

2.11 %

The price & data indicated is as on date

BUY

26

Bajaj Auto reported fair good sales numbers in the last quarter. As the various segments of economy are recovering, the muted demand for two wheelers has also increased. The worker strikes at its chakan plant have also been resolved, which caused the company production losses.

However, tough competitions in the two wheeler segment is expected to keep margins low.

Better volumes numbers are definitely supportive for Bajaj Auto, what is more important is to deliver on the margin front. They have been successful with the scooter segment where the volume has been on an extremely positive side. However, at the margin front they have not been so successful compared to their peers.

Business Segments

Two Wheelers

Three Wheelers

Quadra cycle

Commercial Vehicles

Spares

Bajaj Auto's total sales increased by 8 percent year-on-year (up 5.6 percent month-on-month) to 3.37 lakh units. The company expects to see total sales of 4 lakh units in next few months. New Discover sales will grow to 25,000-30,000 units per month. We expect 3-wheeler sales of 55,000 units per month going forward. The company’s total sales growth was pushed up by a 56% rise in commercial vehicle sales. Total CV sales went up to 52,538 units, which the company said was the highest sales for any month.

Discover brand sales went up by 16% to 93,000 units. The company is betting on new Discover 150 to bring up the volumes and recover lost market share. Exports, too, were highest for any month with 1.75 lakh units, which was a 21% growth.

Bajaj Auto has also recently launched two sport motorcycles from Austrian partner KTM.

BAJAJ AUTO

₹ 2,410

Broker Reports

BUY 6

HOLD 7

SELL 6

SENSEX WEIGHT

1.75%

The price & data indicated is as on date 19/09/2014

HOLD

27

The pharma major’s US operations are showing an improved traction, leading to a rally in stock price over the past few months. A string of new product approvals from the USFDA have led to significant product launches that are expected to boost earnings this fiscal year.

In the last quarter, Dr. Reddy’s launched 28 new generic products & filed 24 new product registrations. A weak rupee also provides a fillip to its dollar revenues. Given the high earnings visibility, most analyst are positive about it.

Business Segments

Dr Reddy's deal with GlaxoSmithKline Plc for generic formulations is under review. However, it'll be a little premature to say that the deal will be terminated. Dr Reddy's deal with GlaxoSmithKline for generic formulations is under review. However, at the moment, it'll be a little premature to say that the deal will be terminated.

Dr. Reddy’s with a robust product portfolio, filings and necessary manufacturing infrastructure are well placed to capitalise on this forthcoming opportunity. Dr Reddy's have been the most prolific filers for Para-IVs. Analysts believe that the company will continue to do extremely well on the back of generics, domestic consumption, new product introductions and consolidation in the industry.

Dr.REDDY LABS BUY

₹3,222

Generic Formulations

Active Ingredients

Pharmaceutical Services

Bio- Similars

Proprietary Products

Broker Reports

BUY 8

HOLD 1

SENSEX WEIGHT

1.75%

The price & data indicated is as on date 19/09/2014 28

NTPC’s problems may be ending. The country’s largest power producer National Thermal Power Corporation will benefit from the ongoing power sector reforms. CCEA’s new coal price mechanism will help it import coal to mitigate the shortfall from Coal India supplies.

The recent allocation of four more captive coal mines with an aggregate reserve of 2 billion tonne will provide fuel security. The company is also maintaining its pace of capacity addition. It commissioned around 4000 megawatts in 2013-14. At current valuations, it is the sector’s safest bet.

Business Segments

State-run NTPC is scouting for coal assets overseas and has invited proposals form coal miners interested in offloading stake. The move is aimed at ensuring a steady supply of imported coal which the power producer needs for its plants.

NTPC, which generates 43,128 MW of power through its 38 power stations, imports coal to meet its fuel requirement. The company plans to use 17 million ton of imported coal this fiscal. NTPC consumed about 148 million tonne of domestic coal and 10.8 million tonne of the imported variety.

The Andhra Pradesh government has allotted 1,200 acres of land on lease basis to National Thermal Power Corporation Ltd for setting up 4,000 mw power project in Visakhapatnam, with an investment outlay of `20,000 crore.

NTPC, is running its plants at over 80% capacity compared to an average of 62% last year, leading to higher demand for coal.

NTPCBUY

₹ 138

Electricity Generation

Power plant Construction

Power Management

Renewable Energy

Production

Broker Reports

BUY 5

HOLD 1

SELL 1

SENSEX WEIGHT

1.71%

The price & data indicated is as on date

29

Besides weak global commodity prices, Sesa Sterlite Industries, India’s largest copper smelter, is currently facing multiple problems. Though the Supreme Court has temporarily allowed the company to operate its smelter, despite its ongoing fight with the Tamil Nadu Pollution control board on this issue continues.

Other concerns pertain to the merger between Sterlite & Sesa Goa, which is a time taking process. Sterlite’s power division also faces problems like transmission bottlenecks, issues regarding coal quality, and so on. However, all these negatives have already been factored into the price. Hence, long term investors may continue to hold the stock till clarity emerges on a few of these issues.

Business Segments

Flat Products

Long Products

Construction Products

Agricultural Implements

Bearings

Design & Automation

The Orissa government has granted Sesa Sterlite a prospecting license for two laterite deposits, which would give the company some respite on the raw material front for its 1 million ton per annum alumina refinery in Lanjigarh.

Sesa Sterlite is currently facing losses on account of the high import and transportation costs of bauxite ore from outside Orissa to feed the plant.

The need is also there for meeting fund requirements to repay existing debt and for proposed capital expenditure of the group including subsidiary, associate firms and its buy out of the balance stake of Hindustan Zinc and Balco and for general corporate purposes.

Shareholders' approval has also been sought for issuing convertible securities of up to Rs.6,000 crore and for private placement of non-convertible debentures (NCDs) of up to Rs.4,000 crore.

SESA STERLITE

₹ 284

Broker Reports

BUY 3

HOLD 2

SELL 3

SELL

SENSEX WEIGHT

1.49%

The price & data indicated is as on date 19/09/2014 30

In addition to the fall in steel prices triggered by global commodity woes, Tata Steel also has to manage its high debt.

However, Tata Steel continues to be the strongest domestic player in metals with access to key raw materials. The ongoing restructuring in his overseas operations has also started yielding fruit. There are also reports that the company is planning to sell its stake in the other group companies to reduce debt & fund its expansion plans. Existing investors may continue to hold on to the stock.

Business Segments

Flat Products

Long Products

Construction Products

Agricultural Implements

Bearings

Design & Automation

The currency depreciation in both euro and GBP is broadly positive for Tata Steel, as European steel prices inch up and, given the high local currency fixed costs, margins would expand in local currency terms

As the festival season starts, local steel demand should improve in India, driving steel prices higher locally. The much-awaited cyclical steel demand recovery should also start over the coming months.

Tata Steel is setting up a 55,000 tonne per annum (TPA) Ferro chrome plant at Gopalpur in Ganjam district of Odisha and its first unit is expected to start operations by March 2015. The steel major has already got in-principle approvals from the designated authorities to set up an industrial park at the same location.

Tata Steel has boosted revenue and profit for its full-year result in Australia. The expansion plans include, two new facilities are being built in Auckland, with new plant and machinery to enhance processing capability and efficiency, and another purpose-built facility in Palmerston North is scheduled to open at the end of the year.

TATA STEEL

₹ 511

Broker Reports

BUY 8

SELL 3

BUY

SENSEX WEIGHT

1.29%

The price & data indicated is as on date 19/09/2014

31

The company has given a lower guidance for revenue & margins over the next two years, citing rebuilding of product pipeline in the United States. However, its outlook remains positive due to the expected ramp up in key markets and ongoing expansion plans.

Cipla is expected to complete its $ 488 million takeover of South African Medpro this month. Its expansion in emerging markets & increased spending on research & development to build product pipeline provide comfort over the medium to long term. However, the stock may remain range bound due to its ongoing investment phase.

Business Segments

Global and Indian drug makers including Cipla have been hit in India by wide-ranging government-imposed price reductions over the last year. Cipla is among the companies that will be affected by the latest decision to cap the prices of 36 drugs, including those used to treat infections and diabetes, in the government’s latest move to make essential medicines more affordable.

Cipla has entered in to a commercial collaboration with UK-based S&D Pharma in the Czech Republic and Slovakia region to focus on its core therapy areas, while S&D Pharma will be the key partner for generics & to

distribute all products, including respiratory products; and this portfolio will increase over the next few years.

CIPLA

₹ 627

Active Pharmaceutical-

Ingredients

Formulations

Veterinary

Therapy Endoscopy

Broker Reports

BUY 3

HOLD 6

SELL 2

SENSEX WEIGHT

1.22%

The price & data indicated is as on date

HOLD

32

Hero Motocorp had been affected by the slowdown in the two wheeler demand last year, but has turned itself towards positive figures in the past two quarters, clocking a rise in volume. However, it lost some market share to its erstwhile partner Honda.

In the domestic market, the company has planned a capex of Rs.25 billion over the next two years. Besides, its operations in Africa & Latin America have also started, displaying strong intent to gain a firm foothold in the other emerging markets. However, weak competition & stagnant demand in the domestic market is likely to keep the margins under pressure.

Business Segments

Hero MotoCorp plans to invest Rs.2,200 crore to set up a manufacturing plant in Andhra Pradesh. The new plant will provide employment to around 9,000 people. The proposed plant will have a capacity of 1.8 million units & will be Hero MotoCorp's sixth facility and will take the company's overall annual capacity to 12 million units. The company has appointed Markus Braunsperger, a top automobile designer from Germany's BMW as the head of R&D division.

Analyst believe that if the real economy picks up then the four wheeler, two wheeler and the commercial vehicle segments are absolutely best suited to participate in the cyclical recovery.

HERO Motocorp

₹2,951

Two Wheelers

-Premium Bikes

-Off Road Bikes

-Scooters

-City Bikes

Broker Reports

BUY 4

SELL 3

SENSEX WEIGHT

1.18%

The price & data indicated is as on date

HOLD

33

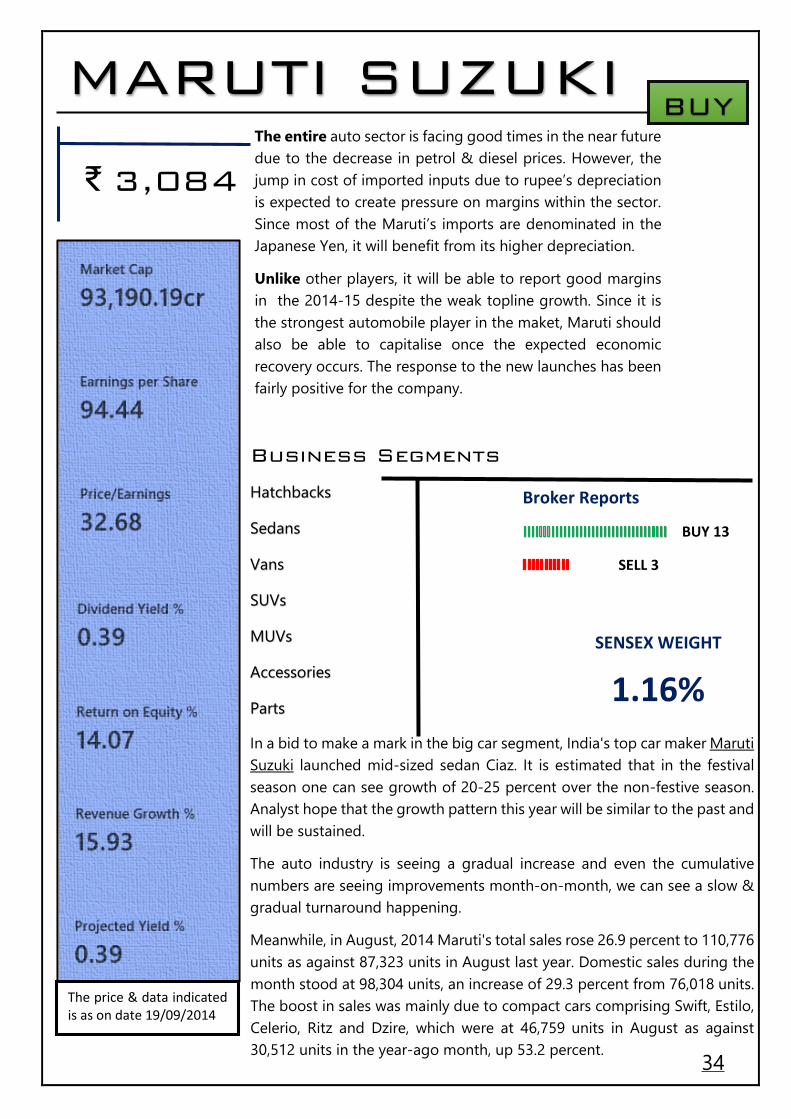

The entire auto sector is facing good times in the near future due to the decrease in petrol & diesel prices. However, the jump in cost of imported inputs due to rupee’s depreciation is expected to create pressure on margins within the sector. Since most of the Maruti’s imports are denominated in the Japanese Yen, it will benefit from its higher depreciation.

Unlike other players, it will be able to report good margins in the 2014-15 despite the weak topline growth. Since it is the strongest automobile player in the maket, Maruti should also be able to capitalise once the expected economic recovery occurs. The response to the new launches has been fairly positive for the company.

Business Segments

Hatchbacks

Sedans

Vans

SUVs

MUVs

Accessories

Parts

In a bid to make a mark in the big car segment, India's top car maker Maruti Suzuki launched mid-sized sedan Ciaz. It is estimated that in the festival season one can see growth of 20-25 percent over the non-festive season. Analyst hope that the growth pattern this year will be similar to the past and will be sustained.

The auto industry is seeing a gradual increase and even the cumulative numbers are seeing improvements month-on-month, we can see a slow & gradual turnaround happening.

Meanwhile, in August, 2014 Maruti's total sales rose 26.9 percent to 110,776 units as against 87,323 units in August last year. Domestic sales during the month stood at 98,304 units, an increase of 29.3 percent from 76,018 units. The boost in sales was mainly due to compact cars comprising Swift, Estilo, Celerio, Ritz and Dzire, which were at 46,759 units in August as against 30,512 units in the year-ago month, up 53.2 percent.

MARUTI SUZUKI

₹ 3,084

Broker Reports

BUY 13

SELL 3

BUY

SENSEX WEIGHT

1.16%

The price & data indicated is as on date 19/09/2014

34

The World’s largest coal producer has underperformed the Sensex this year due to its inability to ramp up its production & due to fall in the coal prices globally. Growth has been a concern given the delays in environmental & production approvals for mining projects.

However, sentiment is slowly turning positive for the stock due to the recent government approval to setup an independent coal regulator. This is expected to speed up clearances, usher in more transparency in pricing, and improve supply. Attractive valuations & receding policy risks may keep the stock buoyant.

Business Segments

Boosted by environmental relaxation in mining, Coal India could meet the production target of 507 MT for the current fiscal by ramping up its production despite falling short till August. The company expects an incremental production of at least 10 million tonnes to a maximum of 20 million tonnes from existing mines. The expansion limit for coal mines has been increased without the mandatory public hearing. Increasing production up to 6 MT for mining in case of mines having generating capacity of more than 20 MT a year, will now not require any consent from locals. It has cut the amount of the fuel it’s selling at competitive auctions to bolster supplies to power stations to meet demand.

COAL INDIABUY

₹ 345

Coking Coal

Semi Coking Coal

NLW Coking Coal

Beneficiated Coal

Middlings

Rejects

LTC Coke

Coal Fines

Tar/Heavy Oil

Light Oil/Soft Pitch

Broker Reports

BUY 8

HOLD 2

SELL 1

SENSEX WEIGHT

1.02%

The price & data indicated is as on date 19/09/2014 35

After the recent gas price hike, gas transmission company Gas Authority of India ltd. Could be adversely affected in the near term. Its gas cost will increase substantially, but it will not be able to pass this on to customers as the pricing of both LPG & petrochemicals is based on import parity.

It expects a hit of $ 218 million annually on pre-tax profits on account of higher costs. This, in addition to its subsidy burden, will dent profitability. Gail, on its part, is trying to free itself from the subsidy burden by changing focus from transportation of gas to trading, thereby reducing its dependence on the regulated business.

Business Segments

State-run gas utility GAIL has made available natural gas from alternate sources to industries in Gujarat whose domestic fuel allocation was snapped to give fuel for the CNG sector.

The Oil Ministry had directed Gail to cut domestic gas supplies - called APM gas - to non-priority sector so that cheaper fuel can be made available for supply as compressed natural gas (CNG) to automobiles and piped cooking gas (PNG) to households in cities.

Considering the requirement of gas to other industries, Gail has offered to supply equivalent amount of alternate gas, possibly imported LNG, so that the production of such industries do not suffer.

The pipeline to be used to supply gas to Pakistan starting from western Indian state of Gujarat would be built by Gail India.

GAIL

₹ 449

Natural Gas Supply

Liquid Hydrocarbon

Petrochemicals

LPG Transmission

City Gas Distribution

Gas Exploration

Broker Reports

SELL 5

HOLD 1

SENSEX WEIGHT

0.94%

The price & data indicated is as on date 19/09/2014

SELL

36

The stock has corrected sharply this year in line with the downturn in the metals sector. A global slowdown in demand for commodities has taken its toll on the sector. These conditions are likely to persist for a while.

For Hindalco, lack of approvals for captive coal mines for its green field smelters & weak aluminium prices remain a concern. While the near term positive triggers are not visible, analysts are of the opinion that the negatives are already priced in. Besides, Hindalco’s US based subsidiary, Novelis, lends comfort with good earnings. Given the stock’s low valuation, investors should hold on to it for the medium term.

Business Segments

Hindalco Industries Ltd., India’s second-largest aluminum maker, postponed a share sale to institutional investors on uncertainty about its access to cheap raw materials, people with knowledge of the matter said. The company was seeking to raise as much as 50 billion rupees ($818 million) from the share sale. Hindalco’s Mahan smelter, tied with another project as the company’s biggest aluminum plant with its 360,000-ton capacity, would be affected by the cancellation of the mine permit. The company claimed it has sufficient inventory of bauxite to run Muri and Renukoot alumina refineries despite the recent closure of its six mines by the Jharkhand state government. However, the fact that lack of bauxite mineral forced the company to drop its alumina production in April-June quarter gives another picture.

HINDALCO

₹ 164

Aluminium

Copper

Cargo Handling

Packaging

Fertilisers

Acids

Broker Reports

BUY 3

HOLD 3

SELL 2

SENSEX WEIGHT

0.89%

The price & data indicated is as on date 19/09/2014

HOLD

37

TATA Power continues to suffer due to issues like losses to at Mundra UMPP and lower profitability at the Indonesian coal mines due to weak coal prices. However, with the government bringing in more reforms in the power sector, Tata Power, the country’s most efficient power producer, is expected to reap good dividends.

Though delayed, electricity tariffs have started going up. The State Electricity Regulator has approved a tariff increase for urban residential consumers. While Tata Power looks forward to increase its capacity at the Mundra UMPP to 5600 megawatts, the stock will trade low till there is clarity about the compensatory tariff.

Business Segments

Tata Power’s subsidiary Tata Solar has been ranked as India's largest integrated solar player. Among the domestic module suppliers category also, it is the leading player. The company has been particularly successful at winning large, public sector projects which could be one of the key growth drivers in the future.

In a bid to meet the ever-increasing demand of power for the Mumbai city, Tata Power wants to convert unit 6 of the Trombay plant to run on coal so it can permanently supply 500 mw. However, it has hurdles in its way ahead.

Tata Power's wholly-owned subsidiary Bhira Investments Ltd has redeemed $450 million (approximately Rs.2,700 crore) worth of loans to replace them with less costlier debt options.

TATA POWER

₹ 87

Electricity Generation

Transmission

Distribution

Trading

Power Services

Strategic Engineering

Solar Energy

Broker Reports

BUY 2

SELL 4

SENSEX WEIGHT

0.75%

The price & data indicated is as on date 19/09/2014

SELL

38

Earnings Visibility remains a big concern for this capital goods manufacturer. The prolonged slowdown & poor investment climate are reflected in a falling order book & slackening pace of order execution.

As the demand environment remains sluggish, fiscal year 2015- 16 is expected to be tough for the company. Its revenue & profit margins are expected to decline. Given these issues, there appears to be little scope for a turnaround in the near term. Despite its attractive valuation, the stock may appear to be an underperformer.

Business Segments

State-owned BHARAT HEAVY ELECTRICALS LTD., saw its net profit nearly half to Rs.3,461 crore in the last fiscal, is also keen to tap opportunities in the nuclear power segment and possible entry into core-nuclear area. BHEL has mentioned that power sector is facing numerous constraints related to fuel supply, financial health of the state distribution companies, land acquisition, and regulatory clearances. These factors have resulted in finalisation of fewer new projects and slowdown in execution of some projects.

BHEL is also targeting countries like Russia, Kazakhstan, Belarus, and Tajikistan that form a part of the Commonwealth of Independent States (CIS) and also hold promising investment avenues.

BHEL has bagged an order worth over Rs.3,500 crore for setting up a thermal power project in Gujarat. The contract has been awarded by the GSECL.

BHEL

₹ 226

Power

Transmission

Transportation

Non- Conventional Energy

Operation & Maintenance Spares

Broker Reports

SELL 10

SENSEX WEIGHT

0.7%

The price & data indicated is as on date 19/09/2014

SELL

39

As the investment cycle and money flow within the economy improves, the bank can see a reasonable amount of deflation in its stressed assets pool.

Axis Bank is among the best capitalised bank and is likely to benefit from a recovery in the economy. An increase in investment activity will boost its fee income and add to its profitability. Considering high visibility of the earnings growth and the healthy asset quality.

Business Segments

Axis Bank has managed to grow much faster than some of the other domestic peers and now it is at a stage where it is almost as big as the biggest of the lot.

Axis bank will be announcing festive season offers on its auto loans and credit card offerings in the next few weeks. It has also announced the launch of e-surveillance facility, a service that allows a 24x7, 365 days centrally monitored automated security of ATMs.

On the other hand, Finance ministry will soon invite bids from merchant bankers to advise the government on new ETF, so that it could reduce its stake in the companies like Axis Bank. Analysts attribute the bank’s growth to the gradual recovery in investor sentiment, amid hopes of a recovery in the macro economy.

AXIS BANK

₹ 407

Personal Banking

Private Banking

Business Banking

NRI Banking

Agriculture Banking

Rural Banking

Broker Reports

BUY 7

SENSEX WEIGHT

0.7 %

BUY

The price & data indicated is as on date 19/09/2014

40

There are no permanent Sensex Stocks There is a constant churn in the composition of Sensex stocks

Jan, 2009

Sun Pharmaceuticals Satyam Computers

Jun, 2009

Ranbaxy Laboratories Hero Honda Motors

May, 2010

Sun Pharmaceuticals Cipla

Jindal Steel & Power Grasim Industries

Dec, 2010

Bajaj Auto ACC

Aug, 2011

Coal India RIL

Sun Pharmaceuticals R.Com

Jan, 2012

GAIL DLF

Dr Reddy’s Laboratories Jaiprakash Ass.

Scrips Included Scrips Excluded

Most wanted by

Mutual funds High MF holding shows the

counter’s attractiveness

L&T | 15.56%

ITC | 13.04%

ICICI | 11.53%

MS | 5.99%

Infosys | 5.76% 42

*Figures are percentage shares held by FIIs in the respective companies.

FII’s Favourites FII holding shows stock’s

attractiveness, but

excessive holding can add

to risk if they start

withdrawing.

HDFC | 77.36 %

Tata Motors | 67.06 %

Axis Bank | 48.38 %

Infosys | 41.56 %

ICICI Bank | 40.03 %

43

#Figures in Rupees. # Data for past four quarters ending June, 2014.

*The above data indicates the Change in price of a stock in the past four quarters ending June.

*Figures in Rupees.

TATA Steel, 10

M&M, 10.4

HDFC, 14

Larsen & Tubro, 14.25

Coal India, 29

0 5 10 15 20 25 30 35

TATA Steel

M&M

HDFC

Larsen & Tubro

Coal India

Highest Dividend Payers

Sensex stocks that paid the highest dividend

10.5 Stocks that moved the Sensex in the past year

Hero Motocorp, 668

Dr. Reddy's Lab, 713

L & T, 762

SBI, 936

Maruti Suzuki, 1610

0 200 400 600 800 1000 1200 1400 1600 1800

Hero Motocorp

Dr. Reddy's Lab

L & T

SBI

Maruti Suzuki

Top Gainers

44

Sensex returns for different tenures

Annualised returns from investment made in Sensex during the past 20 years. The chart shows the gain/loss to any person who bought the Sensex in one year and sold it in 1 year later (holding period 1 year). Performance depends on the entry point. Despite the recent rally, the annualised return average from the Sensex is only 8.1% if you entered at the end of previous rally in August, 2008.

The chart shows the gain/loss to any person who bought the Sector in one year and sold it in 1 year later (holding

period 1 year). Annualised return for the previous 10 years.

-46.72

65.78

-13.71

11.85

-0.17

14.72

-3.92

33.73

-27.93

-3.75-12.12

10.7 8.08 10.68 8.08

10.68

10.9910.08

16.5323.05

41.03

-60

-40

-20

0

20

40

60

80

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Leaders & Laggards keep changing

SUGAR 219

SUGAR237

SUGAR249

REALTY307

POWER116

-12FMCG

METAL207

CD35 FMCG

25

FMCG33

IT45

FMCG42

-7OIL & GAS

OIL & GAS34

-63SUGAR

-24IT

-79REALTY

TELECOM1

-28REALTY

-36SUGAR

-26METAL

-15AUTO-100

-50

0

50

100

150

200

250

300

350

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Best Performing Sector Worst Performing Sector